ifroutlook for indian borrowers 2016

TRANSCRIPT

FEBRUARY 2016

www.ifre.com

I N T E R N A T I O N A L F I N A N C I N G R E V I E W R O U N D T A B L E

OUTLOOK FOR INDIAN BORROWERS

Sponsored by

01 Outlook for Indian Borrowers RT cover.indd 1 02/02/2016 17:24:25

IFR: ESSENTIAL COVERAGE OF THE GLOBAL CAPITAL MARKETS

Thomson Reuters’ International Financing Review is the leading source of fixed income, capital markets and investment banking news and commentary. IFR’s team of market specialists report on capital raising across asset classes, from rumour through to market reception – in real-time, online, on mobile, in print – and now in Thomson Reuters Eikon.

IFR’s special reports, roundtables and conferences provide expert thought leadership to a senior financial markets audience; IFR Awards are the industry’s most prestigious. Markets professionals worldwide rely on IFR’s combination of commentary, analysis, data and forecasting for intelligence they can act on.

Visit financial.thomsonreuters.com/IFR to find out more about IFR and request a free trial.

MX11338 - IFR Generic Advert Nov 15 v4.indd 1 04/12/2015 12:12

International Financing Review Outlook for Indian Borrowers Roundtable February 2016 1

FOREWORD

IFR’s Outlook for Indian Borrowers Roundtable took place in Singapore in December 2015. As with the Indian

Credit Conference in Mumbai that had preceded it by a couple of weeks, the backdrop was IFR’s inaugural Indian Borrowers Survey, results of which are published in this supplement following the edited transcript.

Using Thomson Reuters proprietary data, we looked at all borrowing in the database by entities whose ultimate parent company was Indian and which had raised finance between January 2014 and June 2015 in the domestic and offshore bond and syndicated loan markets. The results, which were gathered during the third and early fourth quarters of 2015, were illuminating.

Broadly speaking around 200 borrowers tapped the loan market and slightly more (225) accessed the bond market, with some (relatively limited) crossover. Total borrowing in dollar-equivalent terms across all markets was close to US$180bn. Not surprisingly, the bond market saw a lot more serial issuance than the loan market, particularly in the rupee sector. The local market offered good funding to India’s Triple A statist corporates as well as to borrowers in the housing finance, real estate, power and infrastructure sectors.

India’s large industrial groups borrowed through a veritable forest of group subsidiaries and offshoots, while there was also a number of one-off special purpose entities (some regional state-linked) tapping the market for specific purposes, mainly for project and infrastructure finance. All-in-all, we estimated the true universe of entities to be around (but probably fewer than) 200 companies, with many of those with modest funding requirements coming to the market just one or two times in our sample period.

With a healthy 20% response rate to the confidential survey, questions focused on borrowers’ intentions in terms of transferring between loan and bond markets and between offshore and onshore markets & on willingness to diversify sources of funding, and on key areas of concern.

The Singapore roundtable event presented a summary of the survey findings followed by a spirited discussion with a panel of experts from the sell-side, buy-side, and issuer and ratings sectors. With the US Federal Reserve having tightened in December and the Reserve Bank of India having loosened monetary policy with a 50bp rate cut in September, the scene was set for some interesting dynamics in the capital and bank markets.

The broad consensus from the conversation was that the domestic market would need to do a lot of the heavy lifting. But even when the domestic growth and capex cycle kicks in and sluggish credit demand picks up, there will be sufficient rupee liquidity in the local market (given growth in deposits above advances) to take up the slack. This is particularly true, given the preparedness of some borrowers to refinance bank facilities or raise capital for new projects in the bond market, and the parallel preparedness of the banks to extend credit in a rate down cycle that will hold out the prospects of better spread levels.

At the time of the discussion, Masala bonds had been front-of-mind globally as a potentially exciting theme for 2016. But IFR’s Singapore panel very expertly threw out a lot of caution around this market and espoused a broadly unenthusiastic view, which turned out to be spot on.

Moderator: Manju Dalal Editor-at-Large: Keith Mullin Participants: Philippe Ahoua, Anjan Ghosh, Sanjay Guglani, Vikas Halan, David Rasquinha, Nipa Seth,

Event producer: Paul Nicholson Head of production: Clive George IFR production manager: Carole Styles Senior production executive: Gavin White

Global advertising production manager: Gloria Balbastro +44 (0)20 7542 4348 Global Head – Advertising & Sponsorship Sales: Shahid Hamid

Advertising & Sponsorship Sales Directors: Leonie Welss, Marianna Masters, Francesca Colombo

Manager of Sponsorship Sales, LPC: Natalie Bonelli Client Services: [email protected]

ISSN 0953 0223 Printed by Wyndeham Grange Ltd © Thomson Reuters 2016 www.ifre.com

UNAUTHORISED PHOTOCOPYING IS ILLEGAL

cover

A yellow leaf drifts in a pond

REUTERS/Alexander

Demianchuk

02 Outlook for India Borrowers [email protected] 1 02/02/2016 17:24:40

2

Roundtable participants

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

International Financing Review Outlook for Indian Borrowers Roundtable February 2016

PHILIPPE AHOUAIFCPhilippe Ahoua is head of treasury client solutions for the Asia Pacific region at the International Finance Corporation, the private-sector lending arm of the World Bank. He joined the IFC in 1995 in the treasury department, and earlier worked at Bank of America in Washington DC and ED&F Mann Group in London. He is based in Singapore.

VIKAS HALANMoody’s Investors ServiceVikas Halan is senior credit officer for the corporate finance group of Moody’s Investors Service in Asia. Based in Singapore, he specialises in analyzing South and Southeast Asian corporates in the oil & gas, resources and transportation industries. Before joining Moody’s, he worked for JP Morgan in Hong Kong as a capital markets and ratings advisor for APAC clients.

ANJAN GHOSHICRAAnjan Ghosh is chief ratings officer at ICRA Ltd. He is responsible for ratings in the corporate and infrastructure sector, covering both bank loan ratings as well as debt ratings. He has also served on deputation at the London office of Moody’s Investors Service. Before joining ICRA, he worked at Tata Steel.

DAVID RASQUINHAExport-Import Bank of IndiaDavid Rasquinha is deputy managing director at Export-Import Bank of India responsible for project exports, trade finance, lines of credit, treasury and risk management. He has held a range of positions since joining the bank in 1985, serving as the bank’s resident representative in Washington, DC from 1999 to 2004. Rasquinha has also served on several working groups set up by the Reserve Bank of India.

03 Outlook for India Borrowers Bios and copy.indd 2 03/02/2016 09:20:41

3

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

International Financing Review Outlook for Indian Borrowers Roundtable February 2016

SANJAY GUGLANISilverdale CapitalSanjay Guglani is CEO of fund management company Silverdale Capital. In a varied career, he has been instrumental in creating offshore equity and credit derivatives markets for mid-cap Indian corporates, and started his entrepreneurial career as the founder of Saksham Group in India, one of the country’s largest proprietary/managed accounts fund managers. Earlier, Guglani helped set up capital market ventures for GE Capital and managed one of the largest cash-futures arbitrage books in India.

NIPA SHETHTrust GroupNipa Sheth is the founding director of Trust Group. Under her leadership, Trust Group has grown from being a distribution house of debt products in 2001 to a fully fledged investment bank providing services across origination, intermediation, advisory and fund management and distribution.

MANJU DALALIFR, Moderator

KEITH MULLINEditor-at-Large, IFRRoundtable Editor

03 Outlook for India Borrowers Bios and copy.indd 3 03/02/2016 09:20:45

4

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

International Financing Review Outlook for Indian Borrowers Roundtable February 2016

IFR: WHAT DOES THE BORROWING LANDSCAPE LOOK LIKE FOR INDIAN ISSUERS IN 2016?

VIKAS HALAN, MOODY’S: The demand and supply of credit in 2016 will be lower than 2015 and the Fed rate hike will likely alter the funding mix from more offshore to less offshore. As we saw in the last policy statement, higher Fed rates at a time when the global economy is not doing that well plus the need to protect the Indian economy led to that 50bp rate cut by the Reserve Bank of India in September 2015.

If we extrapolate that, the Fed rate hike will probably see looser Indian monetary policy so a greater supply of credit will be available for Indian borrowers onshore.

PHILIPPE AHOUA, IFC: Higher US interest rates obviously are going to discourage borrowers all over the region from borrowing in international currencies, which from the IFC perspective, is a good thing. On the basis of the corporates we interact with, Indian banks have taken a fairly aggressive stance in terms of lending to corporates domestically.

We’ve also seen a lot of interest in the domestic corporate bond market, and from second-tier credits that we talk to in some other markets such as the Masala bond market. In terms of borrowings, it should

be a fairly active year for Indian corporates on the back of that rate cut.

DAVID RASQUINHA, EXPORT-IMPORT BANK OF INDIA: I’d always felt that when the Fed rate hike came, it would be a non-event that had already been pretty much priced it into the market’s reckoning. I agree with Vikas: it’s going to be onshore. An important point here is that Indian bank deposits are growing faster than the rate of growth of advances, and this has been the case for close to two years now so there is plenty of liquidity.

But demand has not really been there. Maybe one of the reasons is over-leveraging, and also because rates have been high. As the Reserve Bank reduces rates, you will probably see some of that slack being picked up.

NIPA SHETH, TRUST GROUP: We were hoping that December 2015 would see be a Fed hike, an event that had been talked about for more than 18 months so there was already a lot of discounting. Even though India has cut 125bp since the beginning of 2015, in terms of government securities we are at almost the same levels as we were before the cuts.

The thing is: India is seeing among the highest real interest rates we’ve seen in the last decade. By changing to CPI from WPI, the effective rate

03 Outlook for India Borrowers Bios and copy.indd 4 03/02/2016 09:20:46

5

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

International Financing Review Outlook for Indian Borrowers Roundtable February 2016

of interest has changed significantly. In terms of borrowing, we feel the government investment cycle is due to start. In fact, they’ve already started in the railways and roads in the first cycle of borrowing.

Privately-owned promoters will probably also prepare for the investment cycle two years down the line so a lot of mature projects should come into the bond market from the bank market. Eventually, our sense is that you will see a lot of bank funding moving to lower interest-rate bond funding.

SANJAY GUGLANI, SILVERDALE CAPITAL: I agree with Nipa. The key thing to observe is in terms of real interest rates, which are among the highest India has seen in the last few decades. Having said that, I would put forward two points.

Number one is if you look historically, whenever India’s financial condition has been positive, increases in the Fed rate haven’t impacted much whether that was 1999 or 2004. So purely from a global perspective, we do not see a Fed rate hike having a major impact on Indian corporates.

Having said that, intent and requirement are two different things altogether. Does India need to go offshore to borrow? Maybe not since, as correctly pointed out by my colleagues here, there is ample liquidity to take care of the first tier of growth, which is just kicking in.

But the key problem I have is the issue of intent. It is the right time for the government to explore active shifts in terms of the internationalisation of the market. Masala bonds are a good start. But they should work more in terms of creating a sovereign yield curve, even if it’s using quasi-sovereigns such as ExIm, or SBI. The point is you cannot dig the well when you’re thirsty. 2016 is a fantastic time for India to come to the global markets and establish a benchmark that will help when it requires funds in late 2017, early 2018.

ANJAN GHOSH, ICRA: India’s credit growth right now is quite sluggish and deposit growth is at least a couple of percentage points higher than trade growth. So combined with the fact that the investment cycle continues to be very sluggish, there is not really much of a requirement in terms of tapping the offshore market.

Looking at some statistics, the overall FII flow in the equity and debt market in 2014 was something like US$45bn. In 2015 to-date, it’s hardly anything. There are probably reasons both on the equity side as well as the debt side but there has been hardly any inflow on a net basis. So to that extent, I don’t think the additional Fed rate hike will really have so much of an impact. In fact, I would worry more about the impact it has on the exchange rate and the unhedged foreign currency exposures of Indian corporates.

IFR: ARE THERE ANY SECTORS IN PARTICULAR IN INDIA WHICH ARE MORE PRONE TO INTEREST RATE RISK?

ANJAN GHOSH, ICRA: We are at the high end of the rate cycle. Interest rates have started coming down and

the general consensus it that they are going to trend down further. So we are going to see some benefits for highly leveraged corporates. My personal feeling is that leverage levels are so high and Ebitda so low that a few basis points here and there won’t really make a difference.

The rate move in India will possibly make more difference in terms of giving an uplift to consumer sentiment. Some of the consumption-oriented sectors like automobiles or real estate might get a bit of uplift from interest rates in India coming down.

More importantly and more germane to the topic we are discussing today, because of a reduction in interest rates, we would possibly see more refinancing activities in the bond market i.e. more bank loans being replaced by bond market issuance especially for projects which have completed and which have a one or two-year track record of operations. That is a trend which we’re already seeing in the last one or two years. And that is a trend, which is likely to get a fillip going forward.

IFR: I WANTED TO TAKE A STEP BACK AND LOOK AT THE REGULATORY ENVIRONMENT IN INDIA. WHAT ARE THE KEY ELEMENTS THAT YOU WOULD POINT TO?

VIKAS HALAN, MOODY’S: Borrowers are still constrained, especially when it comes to foreign currency issuance under the Reserve Bank’s ECB guidelines. Just look at the restrictions that are placed on borrowers. There are end-use restrictions; there is an all-in cost ceiling; and you have very steep hedging costs. All of these combined make very little sense for someone to borrow in foreign currency and hedge versus borrowing in domestic currency. Only companies that have natural hedges can actually borrow in foreign currencies so that would mean commodity companies.

Now so far as reforms are concerned, what we have clearly seen is the government moving on some of the immediate issues it faced. One was, of course, the Coal Block Auction and the metals and mining bill [Mines and Minerals Development and Regulation Bill]. What it hasn’t yet been able to do, of course, is the Goods and Services Tax (GST), the land acquisition and other Big Bang reforms that it promised.

PHILIPPE AHOUA, IFC: As a multilateral development bank, we’re in a different position to fellow panellists. And also as a development bank where the Indian government sits on our board, I’d be very remiss to say that the experience and what it has done has been anything other than positive.

What has changed is the regulatory framework, the environment and the mentality, both at the Reserve Bank and the Ministry of Finance, as far as development of capital markets. When we started our Masala bond programme in 2013, we saw a shift in the regulatory mindset, and in terms of non-residents looking to develop the offshore bond market. So that’s been very helpful.

In November 2015, the RBI relaxed some of the regulations around multilaterals providing hedging products to certain projects in India. I think that’s a

03 Outlook for India Borrowers Bios and copy.indd 5 03/02/2016 09:20:49

International Financing Review Outlook for Indian Borrowers Roundtable February 20166

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

One of the

biggest

achievements

of this

government

has been the

single-minded

focus on

inflation

really big development for us, because it allows us to mobilise funds for projects in places like Japan with non-development bank and non-traditional borrower/lenders in India.

Loosening the former FII license, which is now the FPI, has also been very helpful. It’s helped us play a bit more in the corporate bond space and support certain bond issuance by domestic corporates. So in general for us, it’s only been a positive as far as the mindset of the regulatory environment in India.

DAVID RASQUINHA, EXPORT-IMPORT BANK OF INDIA: I’m pretty much with Philippe on this. We’re a different kind of animal from a typical Indian borrowe, in that the business driver for us is exogenous. It is project exports internationally. And where the government comes in is in terms of policy, in terms of its overseas development assistance, lines of credit to African countries; the strategic initiatives on project exports in the SAARC (South Asian Association for Regional Cooperation) region. So it’s not really a function of the regulatory environment as much as the government’s policy direction.

And there we are seeing a lot of movement. We had the India-Africa Forum Summit recently, where the prime minister announced Rs10bn. We’ve launched a new scheme for the SAARC countries to build up project exports. For me, that’s extremely positive but it has nothing to do with the regulatory environment.

NIPA SHETH, TRUST GROUP: I’ll restrict my comments to changes that have impacted the bond market. Masala Bond developments are one area; partial credit enhancements will go a long way in terms of infrastructure projects, while allowing foreign investors to buy distressed or defaulted bonds is another. Also, I think the repo guidelines which are expected to come soon will change a lot in terms of the bond market.

SANJAY GUGLANI, SILVERDALE CAPITAL: We’ve seen a lot of positive developments and hopefully more will come through. For us as foreign investors, the biggest concern in India has always been in terms of policy flip-flops. My biggest worry in India is not what the government will do in terms of the future. My biggest problem in India is what the government will do regarding the past. We have seen it in a small way in GAAR (general anti-avoidance rule), which gets postponed every few months. And then of course we had the great Minimum Alternate Tax (MAT) saga.

I’m often asked: “Since you run such a large US oil book and being of Indian origin, why don’t you launch an India fund?” My answer is this, “I cannot run a fund with a one-year duration. How can I open a new fund let alone a long-term fund if the policies are for less than one year?” We talk about withholding tax at 5%, and then put a caveat of trickle-down in 2014/15/16 but we don’t know what it is. My biggest worry is whether, talking about 2016, I have a guarantee that it will be 2016. The answer is no. So the problem we face as investors is more to do with administration rather than purely in terms of policy.

Taking a step further, I fail to understand how anyone can be blind to the fact that overseas venues, whether it’s the Singapore exchange or the Dubai exchange, end up having more trading than India on, for example, Nifty. Or in USD/INR. Why should it be exported to Singapore? I’m proud of Singapore. I live in Singapore. But can’t we have regulatory frameworks to enable us to hedge onshore?

And then we have a crazy thing called the ‘FI restricted list’. So every morning I have to look at my FI restricted list to know if I’m restricted from buying or not. India is a very interesting country to work in and it offers us huge opportunities. But when I work in Cayman, I get 35 years’ definitive tax rates; in India, I don’t have 35 weeks’ definitive tax rates.

Is the government doing well? Yes. It has done fantastically well. The biggest thing they’ve done is in terms of the monetary policy framework around RBI. But let me remind you, this framework was mooted way back in 1963, so it’s taken us quite a few years to get this finally signed. But I’m glad we’ve got there. RBI knows what they’re supposed to do; that’s a very positive step. And like any growth, there are two steps forward, one step back. Which is perfectly fine, as long as you’re going forward.

What is required in India is not in terms of politicians. Politicians are supposed to provide strategy. What India requires is administrators. Here’s a pointer for you: we had exactly 4,802 officers in the Indian Administrative Service as of January 2015 to run a country of 1.26 billion people.

ANJAN GHOSH, ICRA: Just to add to what Sanjay said, regarding the monetary policy framework. I think one of the biggest achievements of this government has been the single-minded focus – and I mean government as well as RBI – on inflation. Even though people generally attribute progress to tailwinds in the form of lower oil and commodity prices, I would like to believe that there have been a lot of other steps taken by the government in terms of restricting minimum support prices.

India will shift from consumption-led growth to investment-led growth; hopefully that growth will come soon. That has really played a huge role in terms of bringing down inflation significantly and it has an impact, not only on the economy but also on the investment cycle as well as the interest-rate cycle. That is one of the most important achievements of the government, which is often passed off as a collateral benefit of lower oil prices.

I’d like to elaborate on another element, which Nipa has already mentioned. The government and RBI have taken a lot of steps in terms of kick-starting the bond market. Nipa already mentioned the partial credit enhancement schemes. Then you have increased limits for FIIs. Of course, there are caveats, which Sanjay has mentioned.

Then there was the recent RBI discussion paper encouraging corporates to look at borrowing part of their working capital requirements from the bond market, while SEBI has recently framed the guidelines for the municipal bond market. And we’ve Infrastructure Investment Trust (InvIT) developments.

03 Outlook for India Borrowers Bios and copy.indd 6 03/02/2016 09:20:51

International Financing Review Outlook for Indian Borrowers Roundtable February 2016 7

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

A lot of incremental steps are being taken to relieve the stress on the banking system and to ensure that the bond market develops.

IFR: TOTAL G3 BOND ISSUANCE BY INDIAN BORROWERS WAS US$17.5BN IN 2014. IN 2015 YEAR-TO-DATE, THE NUMBER IS US$8.3BN, ACCORDING TO THOMSON REUTERS. IF YOU LOOK AT THE QUANTUM OF US DOLLAR BONDS MATURING IN THE NEXT TWO YEARS, US$7.2BN FALLS DUE IN 2016 AND ANOTHER US$3.4BN IN 2017. WHAT CAN WE EXPECT TO SEE IN TERM OF ISSUANCE IN 2016? COULD INDIAN BORROWERS BREACH THE OFFSHORE ISSUANCE PEAK WE SAW IN 2014?

SANJAY GUGLANI, SILVERDALE CAPITAL: There are a couple of factors. First is the issue of supply. We don’t see any major activity in terms of the M&A sector that will require a huge amount of funding for offshore acquisitions by Indian firms. Having said that, we will see certain companies looking to internationalise their books. Bharti is a classic example; the company has done a fantastic in creating a yield curve for itself and that will pay dividends in the long term.

The next dimension to look at is asset-backed borrowing. This is an area where India has lagged

other economies and where I see maximum scope for improvement, notwithstanding my previous caveat in terms of policy flip-flops.

So we saw an SLBC-backed deal for AE Rotor but the RBI banned it; we saw a deal for DLF and RBI banned it; we also saw that IFFCO deal with Credit Suisse, but the RBI banned it. We’ve had around 15 examples but one solitary deal done. This doesn’t look good because the idea is to develop the market.

It’s important to have the framework laid out. As you’re aware, unlike in the US where just 25% of the US debt requirement is met by the banks, in India 75% and above comes from the banks. If we have strong enforcement in India, if bond covenants are tightened, we will see the market deepening and things will take off.

Our biggest problem is that we require a premium because of enforcement costs. There are something like 30 million cases pending in various courts in India and some take years to resolve so we require a certain risk premium to be motivated to go onshore.

The only jack in the pack could be what Nipa presented earlier, in terms of real interest rates. If real interest rates in India go high, it could change the picture when the corporates start looking in terms of the offshore market.

03 Outlook for India Borrowers Bios and copy.indd 7 03/02/2016 09:20:52

International Financing Review Outlook for Indian Borrowers Roundtable February 20168

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

You will see

refinancing but

beyond that,

it doesn’t look

like there’s

much M&A

activity in

the pipeline,

nor major

investment

projects

IFR: HOW DO YOU SEE THE SCENARIO IN 2016, DAVID?

DAVID RASQUINHA, EXPORT-IMPORT BANK OF INDIA: As a borrower, as I said before, our mission is exogenous so I’m probably not a good benchmark. But if you ask me in general and referring to the numbers you quoted, I suspect 2014 was a bit of an outlier. Two possibilities – and sticking my neck out a little here. At the end of 2013, the rupee had plunged to all-time lows so a lot of the slack in terms of the anticipated depreciation had worked its way through the system. There was a little more appetite for taking on exchange risk.

Secondly, the new government generated a lot of euphoria in 2014, some of it a little irrational. I think the two contributed to a rise in foreign currency issuance in 2014. So it’s probably not the best benchmark to evaluate against.

For 2016, there are a few factors. Capacity utilisation is still extremely low. The RBI governor recently said that it’s around 70% although it differs from industry to industry. Business isn’t doing too well and investment is not happening much, either. Projects are stuck and new projects are not coming up. So no operational demand, no investment demand. I would suspect you’re really going to see refinancing demand. That’s really going to be the driver in 2016.

VIKAS HALAN, MOODY’S: Demand on the investment side looks quite weak. If you look at the sector composition of foreign currency issuance out of India, nearly 60% comes from commodities. A lot of it has been acquisition-related issuance by oil and gas companies such as Reliance, ONGC and Oil India. We’ve also had the likes of Vedanta and Tata Steel. So nearly 60% of issuance from India came from the oil and gas or commodity sectors. And then you have the banks.

You will see refinancing but beyond that, it doesn’t look like there’s much M&A activity in the pipeline, as Sanjay mentioned, nor major investment projects. So 2016 will not see a topping of 2014, and maybe not even 2015.

IFR: WHAT ABOUT APPETITE FOR HIGH-YIELD FROM INDIA?

VIKAS HALAN, MOODY’S: One of the issues for high-yield issuers is the all-in cost ceiling, meaning they have to borrow within the 500bp limit set by RBI. That limits the overall universe to very few issuers in our high ‘Ba’ category, or you have issuers like Indiabulls and Lodha that used structures that are not captured by ECB guidelines.

Those kinds of activities are also tied to investments overseas that don’t seem to be happening at the moment, which, in my view, is a little bit puzzling, because if you look at global asset valuations, especially on the commodity side, it’s getting very attractive. We might end up seeing more M&A as we get closer to the end of 2016, which would increase the demand for credit.

NIPA SHETH, TRUST GROUP: When investors talk about the high-yield space, I don’t really understand

what range they’re looking at. If you look at bond funding relative to bank lending rates, most Triple A companies can borrow at around 100bp lower in the bond market than they can get from the banks.

If you look at the universe of rated companies, only 10% would be Double A and above. Bank lending rates for companies rated Double A and below are not as high as levels in the bond market, which prices spreads at much higher levels. So none of those companies actually access the bond market because bank funding lines are anywhere close to 10%, 11%, at the most 12% whereas the bond market probably does not have appetite at Double A minus and below.

When foreign investors are asking for higher yields, the expectations are high teens. The only space that has been able to offer that kind of yield is the real estate market because the banking sector doesn’t have capital to give to the real estate sector. Therefore we do see very attractive deals coming from a real estate side that get into the high teens.

But anything between 12% and 16%-17% is missing from the Indian market because bank funding lines are available at lower rates. So unless there is an active repo market below Double A, you will never see these companies tapping the Indian bond market. Bank credit will always be a very big part of it – unless the partial guarantee scheme changes things.

ANJAN GHOSH, ICRA: I agree that 2014 issuance seems to have been an aberration. But since interest rates are coming down, local issuance will become more attractive. But even if the investment cycle revives, the market will continue to be dominated by bank loans for quite some time. I don’t really see bond issuance supporting investment activity.

PHILIPPE AHOUA, IFC: A lot of people have been talking about the Fed increasing rates. But what’s interesting is what the Fed does going forward, and what the American economy looks like. There will clearly be a refinancing need. The challenge is going to be whether that refinancing need is going to happen offshore or onshore. And is it going to happen in the form of domestic bond markets or in the form of bank loans?

From a development institution, we’d like to see more of it happening in the bond market, rather than more bank financing. That’s been a challenge in this whole region. This region is dominated by bank financing, and we want to see more of that being refinanced in the bond market. But just to confirm what the panellist have said, that is a challenge in India, because like in other countries in Asia, it’s all locked in to bank financing for various reasons.

IFR: IF YOU LOOK AT THE ONSHORE NUMBERS FOR 2014 AND 2015, RUPEE BOND OFFERINGS AMOUNTED TO RS2TRN IN 2014, AROUND US$30BN EQUIVALENT. IN 2015, SO FAR, WE HAVE ISSUANCE OF RS2.3TRN. AND WE HAVE RS1.4TRN AND RS1.3TRN OF RUPEE BONDS FALLING DUE IN 2016 AND 2017 RESPECTIVELY. IF YOU LOOK AT THE LOAN MARKETS, WE SAW US$50BN EQUIVALENT VOLUMES IN 2014 AGAINST US$30BN 2015 YEAR-TO-DATE. WE HAVE

03 Outlook for India Borrowers Bios and copy.indd 8 03/02/2016 09:20:53

International Financing Review Outlook for Indian Borrowers Roundtable February 2016 9

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

RUPEE LOANS OF US$9BN AND US$10BN MATURING IN THE NEXT TWO YEARS.

GIVEN THIS BACKDROP AND INDIA’S GROWTH PROSPECTS, ARE LOCAL BOND AND LOAN MARKETS DEEP ENOUGH TO MEET POTENTIAL DEMAND UNLEASHED BY GROWTH?

ANJAN GHOSH, ICRA: Credit growth of around 8%-9% is at least a couple of percentage points lower than deposit growth. There are two reasons why credit growth remains sluggish. One of course is the investment cycle not picking up. Second is the steep decline in commodity prices. Working capital requirements have come down substantially so as of now there is enough liquidity and headroom available in the domestic banking system itself to fund growth even if it revives in the next one or two years.

Also, as we have been mentioning, RBI and SEBI have been taking a lot of steps to provide a fillip to the bond market, such as partial credit enhancements under the IIFCL guarantee structure, infrastructure debt funds and REITs. That is essentially designed to ensure that there is quite a bit of refinancing activities that moves to the bond market from the loan market. And it’s something we are already seeing.

So once the investment cycle revives, and with interest rates going down, there will be additional bond issuance to take care of corporate refinancing

needs and the space freed up can be used by the banks to extend more loans.

If the investment cycle were to revive in a big way, given the asset-quality pressures in the banking system and the Basel requirements of maintaining adequate liquidity coverage etc and the huge capital requirement the banks have, there could be a crunch maybe a couple of years down the line. But as of now, we are not experiencing anything because the credit growth is so sluggish.

The other point that needs to be raised once credit growth picks up is the type of capital requirement the banks themselves will have and whether the domestic market is in a position to absorb issuance of AT1 bonds, where investor interest is not very high at the moment.

SANJAY GUGLANI, SILVERDALE CAPITAL: The key point the government has to look at from the policy point of view is in terms of the direction they’re going in. As Anjan just alluded to, the capitalisation of the banks is a huge issue and there is practically no way the local market will be able to finance the capital requirements of the banks.

Beyond the issue of bank capital, it’s worth pointing out that the current five-year capex programme for the railways in India is more than the entire capex outlay for the railways since India’s independence. Demand will be sufficiently large to

03 Outlook for India Borrowers Bios and copy.indd 9 03/02/2016 09:20:55

International Financing Review Outlook for Indian Borrowers Roundtable February 201610

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

If you look at

cumulative

demand for

bank loans

plus bonds, I

don’t think it

will increase

significantly

as there isn’t

much capital

investment

happening

absorb a huge amount of foreign capital. The good news is, of course, that they are inviting foreign capital to come into India and participate.

If you look in terms of defence, we’re years behind schedule. Just to give you a flavour, it takes between three to seven years before a major artillery component is approved. The cycle for testing is three years. If you’re talking big strategic items, of course there is a funding requirement.

NIPA SHETH, TRUST GROUP: There are some interesting dynamics in play. If you look at cumulative demand for bank loans plus bonds, I don’t think it will increase significantly as there isn’t much capital investment happening. You may see some issuers refinance but banks are sitting on a lot of liquidity. If you look at the supply side and real interest rates, we’re looking at channelling funds from real estate and gold into financial savings, which will probably add to more deposits.

We are also seeing that the Indian pension industry is growing at almost 20%-25% and because of some of the steps the government has taken, I wouldn’t even be surprised at 30% growth. So domestic demand and supply should match and then it’s a question of the government’s fiscal deficit.

Until now, Indian bond markets have been dominated by government borrowing and the investment patterns of insurance companies and pension funds are geared to funding the fiscal deficit. In five years, if the government deficit does develop along projected lines, demand will be just enough for the pension funds so the supply or the absorption of the corporate bond market can go much higher.

The second point is some of the NBFC’s balance sheets are growing fast and the understanding and acceptance among international investors of cashflow-based products like CMBS, or annuity based funding, is much higher. So you could see offshore issuers tapping those segments where one is looking at alternative investors and because balance sheets are out-growing what the domestic market can take. It’s a different kind of instruments, the understanding of which is not there with Indian investors at this point in time.

DAVID RASQUINHA, EXPORT-IMPORT BANK OF INDIA: I just wanted to draw your attention to a couple of points. One is a peculiarity of the Indian market. Sanjay referred to it obliquely, which is that the banks are chasing high-yield credits. Those credits don’t go to the bond market; they tap the bank market. That stunts the growth of the bond market because you can’t expect it to grow on high-grade only.

Linked with that is a peculiar Indian institution of the cash credit account. I don’t know if any other country has this kind of a concept. It basically shifts your working capital management to the banks from the corporates. Internationally you have working capital demand loans, and the corporate manages its cashflow based on that. Here, using the cash credit account, the fluctuations are smoothed out. It may not be directly relevant but I think that needs to be done away with, if the bond market is to really develop.

Lastly, I wanted to make reference to the fact that corporate Ebitda is rising steadily but interest cover is dropping. That is an indication of over-leverage in the economy. The number of companies that are frankly leveraged to the point of no return is rising steadily. And even those who are not that badly leveraged are still so heavily borrowed that you have a dichotomy. They want to borrow. And the banks, despite having the money, are not that keen on lending to them, unless it’s rescue financing. Then it’s a different ball game altogether.

PHILIPPE AHOUA, IFC: We are seeing a lot of diversification in products, in terms of financing needs from clients. We’ve been working with renewable energy companies which are looking to securitise some of their assets and sell to investors who may have FPI licenses. So that’s one example.

One of our competitor multilateral development banks is doing a lot of partial credit enhancements with some of the local enhancers. That’s a good thing. That leads us to believe that there is refinancing need out there, and that people are thinking outside of bank loans.

VIKAS HALAN, MOODY’S: The total amount of credit in India deployed by the banks is about INR62trn. If you just take the 8% growth rate that they have been increasing the deployment by, you’re talking close to Rs5trn in additional bank credit each year. If you compare that with Rs2trn that the bond market is doing, it’s still relatively small.

SANJAY GUGLANI, SILVERDALE CAPITAL: Let’s take a step back. We all know the dominance of the banks in India. But if the bond market is developed, what is the fundamental thing you require?

Regulation. The SARFAESI Act (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act) was initially limited to banks and it has now been extended to NBFCs. Can anyone give me any reason as to why it’s not for individuals? The problem is enforcement.

I love liquidity, I’m predominantly in the liquid space but I can compromise as long as I know that enforcement is possible. That’s the key problem and the root of the issuance issue: we need to have the governance and enforceability. And we need justice given on time. Justice delayed is justice denied.

IFR: LET’S ADD SOME SPICE TO THE CONVERSATION. I’M REFERRING, OF COURSE, TO MASALA BONDS, A NEW FUNDING TOOL AVAILABLE TO INDIAN BORROWERS. PHILIPPE, HOW READY ARE INDIAN BORROWERS AND FOREIGN INVESTORS FOR THIS MARKET?

PHILIPPE AHOUA, IFC: If you take a step back and look at the Dim Sum bond market, the Chinese government came in and basically said it was going to help support the market’s growth. So you had the top SOEs and it trickled down the credit curve. What you have in the Masala bond market is a sort of ‘first come, first served’ approach but not a credit by credit approach.

03 Outlook for India Borrowers Bios and copy.indd 10 03/02/2016 09:20:56

International Financing Review Outlook for Indian Borrowers Roundtable February 2016 11

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

So you’ve got the IFC; you’ve got some of our sister supranationals and now you have the Triple A names coming out of India. But it’s too premature really to say how readily investors will take to it.

If you ask me this question six months from now when the Triple A names out of India may have issued, then I’ll be able to tell you whether the floodgates are open or not. I really want to be careful in answering that question. I think it’s just a little bit too early to tell.

VIKAS HALAN, MOODY’S: The economics for Indian borrowers don’t make any sense; somebody borrowing in India at local rates and then going overseas and paying 5% additional withholding tax. The reason you go overseas and access international markets is because you want a broader funding pool but it certainly doesn’t seem like that’s the case here. Also you want extension of tenor. That also doesn’t seem likely.

The objective is clearly to internationalise the rupee, but I think it’s too premature. Also from an investor perspective, I just don’t see how they can make money out of something that is paying the same return as a rupee bond. If you take out the hedging costs, the returns are much lower than you would get on the international bond of that company. So clearly, it doesn’t seem to make sense at the moment.

IFR: DAVID, ARE YOU CONSIDERING ONE? HAVE YOU LOOKED AT THE MARKET?

DAVID RASQUINHA, EXPORT-IMPORT BANK OF INDIA: Never say never. But not right now. As Philippe said, I think it’s premature. We have a saying in India: ‘If a boy and a girl are ready to get married, the role of the priest is a formality’. But here, the Reserve Bank of India is the priest and is set to go but the boy and girl are still pretty far apart. The expectations of prospective Indian borrowers don’t quite correspond to the motivations or the features that overseas investors want. There is still a big gap.

In fact, if I can go out a bit on a limb, I think we’re looking at the wrong party. Everybody is looking at the top-rated Indian names to start the Masala bond market, which I think is a mistake. I can get excellent rates for rupees in India. I don’t need to go to the Masala bond market. The incremental benefit to me is little or nothing.

But the second tier, or maybe the third tier of issuers that are still investment grade or just sub-investment grade would probably be willing to pay a premium or it would perhaps be nearer to their local market rates, as compared to the Triple A names. That might work.

NIPA SHETH, TRUST GROUP: It’s a very interesting market. As regards the Triple A issuers, I don’t really

03 Outlook for India Borrowers Bios and copy.indd 11 03/02/2016 09:20:57

International Financing Review Outlook for Indian Borrowers Roundtable February 201612

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

If I were to buy

NTPC bonds

at 8%-8.5%

and hedge I

would make

about 2%-ish.

As of yesterday

evening,

NTPC’s July

21 bond was

giving me

3.61%

think it will make a lot of sense for them to access this market on a long-term basis. You may see one, two, three issuers get pricing established. But it’s so easy for them to access the domestic market at a fantastic rate. They may not need to go to the international market to capture those kinds of rates. Nor do they have an issue of capital, which they can raise from the domestic market.

But it’s setting the tone for times to come. As Sanjay mentioned, the kind of railway spending which we’re talking about in the next five years is huge. If you’re talking about renewable energy, the government is talking about US$10bn of projects per annum. I don’t think India has the capital to fund those kinds of projects over a period of five years. And you cannot be going to the market at the end of five years to double up that market.

At the same time, I’m not too sure about how many Singapore investors would be willing to come to the onshore market. But you have a lot of investors sitting in Europe and the US who may not want to register as FPIs to do a trade. But there are special funds, which could be for renewable energy, for infrastructure, or the social sector. So I think it’s a stage which is being set for that kind of growth for our country.

For someone like an ExIm Bank, which probably gets a better rate than most AAAs, there is no need to come to the international market. But I think it’s setting a tone for infrastructure. Of course, right now the guidelines are restrictive; only companies which can access ECB markets are permitted, but I imagine we will see some issues from the PSU side to set the

tone. And it’ll be up to the other Indian corporates to take it forward.

We do see a lot of NBFCs very keen to access this market for the diversity of investors rather than the cost of funds. I think the immediate banking capital requirements will be big. And at this point of time, the rates are not matching because of the forward curves India has. But probably, at some point in time when the rupee stabilises, a lot of capital can come from this market.

IFR: INTERESTING POINT. RBI HAS NOT ALLOWED INDIAN BANKS TO TAP THE MASALA BOND MARKET, FOR AT1S. BUT THEY SHOULD PROBABLY DO THAT.

SANJAY GUGLANI, SILVERDALE CAPITAL: Masala bonds are too hot for us. My investors are US dollar-denominated investors. If I were to buy NTPC bonds at 8%-8.5% and hedge I would make about 2%-ish. As of yesterday evening, NTPC’s July 21 bond was giving me 3.61%. I dare not go there.

As Nipa said, there is appetite for long duration local currency bonds. And as correctly pointed out, the right people to do a Masala bond are those who can diversify their investor base rather than benefit on rates. That’s a key thing.

On the Dim Sum points that Philippe touched on earlier, let me remind you of two very important things that allowed the market to grow something like 100-fold in three years: intent and vision. When China stared talking about the internationalisation

03 Outlook for India Borrowers Bios and copy.indd 12 03/02/2016 09:21:00

International Financing Review Outlook for Indian Borrowers Roundtable February 2016 13

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

of the yuan they went to a lot of countries and signed dual-currency pacts. That’s the intent part.

They came to Singapore and they offered us a post-hedging uplift of about 20bp-25bp. People like me flocked to it. They did billions in two and a half months. That’s the vision. Until recently, we’ve had a liquid Dim Sum market. We don’t see anything like this happening in India. Rather, the guidelines which came out were: “OK you have to run. I’ll hold both your hands and both of your legs. Now run”. There were so many restrictions out there.

PHILIPPE AHOUA, IFC: Just to add to that, you saw the announcement regarding the Special Drawing Rights and the renminbi. The Chinese government, for all intents and purposes, had made a decision to internationalise the currency. Vikas mentioned that that is too premature in India.

So until the government of India decides that the rupee needs to be internationalised and supports that mechanism, the Masala bond market is not going to grow off of the back of the IFC, the World Bank, ADB, Triple A and other Indian corporates. You have to have the sovereign supporting the market, providing liquidity and providing a sovereign yield curve off of which pricing is going to happen, similar to what’s happening domestically in India.

SANJAY GUGLANI, SILVERDALE CAPITAL: Beyond the requirement of formal regulation and support, which is absolutely critical, I would say the basic thing they need to do is in terms of free rupee hedging. You cannot stop me from hedging. Why pretend?

PHILIPPE AHOUA, IFC: It’s worth mentioning that the Philippines had large funding requirements a few years ago and issued in that format in the offshore market. So you may not want to internationalise your currency but some of your domestic funding requirements could also justify some sort of internationalisation of the currency. So there are a lot of different factors that can play into that process.

IFR: SANJAY, WHAT IS YOUR OUTLOOK ON INDIAN CREDIT?

SANJAY GUGLANI, SILVERDALE CAPITAL: I am bullish by default and by design. The reason I’m bullish by default is because when I run such a big bond fund, I need diversification so whether I love it or hate it, I need to have India paper on my books. I’m bullish by design because we see fantastic credit quality from India, and that’s partly because the sovereign is rated investment grade, at Triple B minus.

03 Outlook for India Borrowers Bios and copy.indd 13 03/02/2016 09:21:02

International Financing Review Outlook for Indian Borrowers Roundtable February 201614

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

There is money

available

whether it is

in the bank

market,

whether it’s in

the wholesale

market, the

high net worth

market, or

retail

Many Indian corporates could technically be better than Triple B so when they go and try to price their securities in the international market, they’re able to get close to Triple B but not close to what would be effectively that real cost.

The other thing I am bullish about is the economy. I am passionate about India. That’s why I talk about what can be done. There is no denying that we’ve seen a huge amount of changes taking place. I firmly believe India is turning around in 2016 and 2017. The future looks bright.

IFR: HOW CAN WE COMPARE THE RELATIVE COSTS OF FUNDING OFFSHORE VERSUS ONSHORE FOR INDIAN BORROWERS?

DAVID RASQUINHA, EXPORT-IMPORT BANK OF INDIA:

I’ve been a bit of a sceptic on this whole issue of the natural hedge, which somebody mentioned earlier. I’ve always been a little sceptical as to whether you can use revenue flow to hedge a capital liability. And particularly in a situation like India, where your exchange rate changes are discontinuous. It’s not a smooth flow. You have sudden ups and downs.

I think the Reserve Bank is on the same page because they’ve been particularly after the banks to ensure that their clients hedge and if they don’t hedge, there is an additional provisioning requirement.

The domestic market offers enough finance. Just to give you an example: tax-free bonds. The issues that have come out so far in 2015 have been tiny but in 2014 you had bigger issues. And you have bigger issues coming up. They’ve been oversubscribed like they’re equity offerings. So there is money available

whether it is in the bank market, whether it is in the wholesale market, the high net worth market, or retail, money is there for investment.

The cost of that money is one point. And equally important – and Sanjay referred to this in passing – is credibility. A typical investor wants not just a good rating but a promoter he can trust. And that is something which is very difficult to price.

NIPA SHETH, TRUST GROUP: As I mentioned earlier, it’s not necessarily always from a cost of funding perspective. It will be a phase for some Triple A companies to access the market but capital-hungry sectors will be the ones that discover the ways and means and the right price point.

Where long-term funding is available, the internal guidelines of pension funds mean they’re restricted to funding only Double A. But for infrastructure or any long-term projects it’s almost impossible to have a Double A rating unless there is some sort of credit enhancement, which has a cost attached.

I think it will be essentially open only for where you look at a piece of capital which is not easily available. And there’s the asset liability mismatch: you may be able to get short-term funding but to get long-term funding if you’re not Double A and above is not easy.

IFR: MY NEXT QUESTION IS ABOUT THE HIGH DEBT LEVELS OF INDIAN CORPORATES. IN A SCENARIO OF STRESSED BALANCE SHEETS, VOLATILE MARKETS, AND A TIGHTENING DOLLAR RATE ENVIRONMENT, DO YOU THINK INDIAN ISSUERS WILL BE ABLE TO COPE WITH THE GROWTH EXPECTATIONS WE HAVE IN TERMS OF RAISING DEBT? YOU ALREADY ARE

03 Outlook for India Borrowers Bios and copy.indd 14 03/02/2016 09:21:05

International Financing Review Outlook for Indian Borrowers Roundtable February 2016 15

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

SITTING ON A LOT OF DEBT. THERE IS NO GROWTH HAPPENING. WHY WOULD YOU NEED TO BORROW?

VIKAS HALAN, MOODY’S: The background that you’ve laid out is one of high leverage: earnings that aren’t growing and high domestic interest rates resulting in lower interest coverage. And you have very little investment need.

Now, let’s the roll the clock 12 months forward. Growth is still there in India. Interest rates are down domestically. Foreign interest rates are up. You have not invested in any projects so your capex is down so whatever free cashflow you had, you’re going to use to repay the debt. The debt level goes down. Earnings go up. Your leverage should be more manageable, provided you don’t invest further.

What we have seen in the past is as soon as you have green shoots in India, you see a lot of risk-taking. People start to build capacity in anticipation so euphoria takes over, and then you have over-supply coming in. And that’s a risk that, if avoided, will see balance sheets improving and credit quality getting better.

ANJAN GHOSH, ICRA: Leverage has to be broken into two parts. Overall, corporate leverage is not a concern. In fact if you look at our domestic ratings business, we have seen a fair share of upgrades in the last couple of years.

The sector that is under stress is the infrastructure sector and the large infrastructure groups. And if

you look at some 13/14 of the very large and very stressed infrastructure groups, their overall debt levels have been growing at around 30%-35% over the last four/five years. Adding to the problem is the fact that of overall debt levels, more than 50% is accounted for by the power and metals sectors, the two sectors where the maximum number of stresses exist.

These are also the sectors that are totally out of favour with equity investors. Even when the equity market boomed a year or so back, we didn’t really see the stock prices in these companies going up. And this is the sector which requires the maximum amount of deleveraging and the maximum amount of equity-raising. I do not see too much equity raising happening, because investors are simply not comfortable with these areas. There would be huge issues on valuation.

Plus, the fact is a lot of structural issues have not been solved, whether it is in the power sector, whether it is in the metals sector. Of course it’s a cyclical issue, so no government can do anything about it. Equity markets may help on the margin. But it will not really take care of the problem.

IFR: INDIAN EQUITY VOLUMES IN 2014 WERE RS11BN. SO FAR IN 2015, WE HAVE SEEN MORE THAN RS19.5BN ISSUED. DOES ANYBODY ON PANEL THINK EQUITY OFFERINGS CAN STRENGTHEN THE INDIAN CREDIT PROFILE?

03 Outlook for India Borrowers Bios and copy.indd 15 03/02/2016 09:21:07

International Financing Review Outlook for Indian Borrowers Roundtable February 201616

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

We’d like to

see more

[Green Bonds]

happening.

This is

something

that a lot of

corporate

clients that we

talk to have

approached us

about

SANJAY GUGLANI, SILVERDALE CAPITAL: On equity financing we will see more issuance coming from India. But a lot of the issuance we’ve seen hasn’t been going towards refinancing debt. Many of the companies we’ve seen in the market have been funded by private equity looking for an exit. I’d be surprised if even half the money raised in the equity market has gone to refinancing. Most of it is a case of Investor A replacing Investor B.

AUDIENCE QUESTION: ONE TOPIC WE HAVEN’T TOUCHED TOO MUCH UPON YET IS GREEN BONDS. IT’S AN AREA THAT HAS BEEN VERY LARGE IN EUROPE, AND INDIA HAS HAD A GREAT START. I’M KEEN TO HEAR THE PANEL’S THOUGHTS ON HOW YOU SEE THIS SECTOR GROWING, AND HOW IMPORTANT IT IS FOR INDIAN BORROWERS?

DAVID RASQUINHA, EXPORT-IMPORT BANK OF INDIA: We had one of our big successes with the green bond we did in the first quarter of 2015. Frankly, we were surprised. We went into that deal expecting to do somewhere around US$250m-$300m. Our objective was to gain entry into the green market to diversify our investor base. Deep down, we would probably have been prepared to even look at paying a small premium. Not necessarily, but it was somewhere there in the back of our minds. To our pleasant surprise, the book started building very quickly. It included green and non-green investors.

The price intentions built to a point where we upsized to US$500m, which was not something we had in mind when we started. And we were able to get a price that was better than we had got just a month and a half previously. We were frankly surprised, because we didn’t think that such a second venture into the market in such a small space of time would have been welcomed.

It was a learning curve for us and maybe we were a bit naïve to begin with. But we were pleasantly surprised at every step of the process. What were our takeaways? We needed to do a lot more information sharing, which we were not used to. We’re used to the standard due diligence on accounting, and macroeconomics and microeconomics but for the green investor market, we had to go into depths of detail, which surprised us. We weren’t expecting those kinds of questions.

So to some extent, we probably lost a couple of green investors, because we were not fully prepared for the kind of rigour they expected. Not that we hadn’t done it but we didn’t have the data available to give them the answers.

To cut a long story short, the experience was phenomenally positive. It outpaced all of our expectations. I’m surprised that other issuers have not followed suit. IDBI did recently but I thought many others would. In fact we were rather pleased with ourselves that we’d opened the market for others. Certainly if the conditions look right, we’d be happy to go back again.

PHILIPPE AHOUA, IFC: IFC is one of the biggest green bond issuers and we were part of the original green bond principles. In India, we supported the Yes Bank rupee green bond by funding it through the Masala green bond we did ourselves. But we’d like to see more of that happening. This is something that a lot of corporate clients that we talk to have approached us about.

With the Yes Bank transaction, we also helped establish some of the green principles and the use of funds. We’d like to partner with anybody; it’s part of our development mandate. We’re looking at it across

03 Outlook for India Borrowers Bios and copy.indd 16 03/02/2016 09:21:11

International Financing Review Outlook for Indian Borrowers Roundtable February 2016 17

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

Asia. But in India particularly, we’ve got a really big team looking at renewable energy and those types of things. That’s a target audience of funding that we’re looking at. Green bond development, both onshore and offshore, is a big deal for us.

AUDIENCE QUESTION: I JUST WANTED TO REWIND BACK TO OUR DISCUSSION ON MASALA BONDS, WHERE WE TALKED ABOUT INVESTORS NATURALLY BEING EXCITED BY IT BECAUSE IT GIVES THEM A ROUTE TO INVEST INTO INDIA IF THEY DON’T HAVE A FPI VEHICLE. SIMILARLY FROM AN ISSUER’S PERSPECTIVE, ALSO IT WORKS BECAUSE THEY UNEARTH ADDITIONAL LIQUIDITY TO TAP INTO.

NOW WE’RE CLOSE TO NEARLY 9,000 FPIS BEING ESTABLISHED FOR INVESTMENTS INTO INDIA. WHO ARE THESE INVESTORS THAT HAVE SO FAR HAVE NOT HAD REALLY AN ESTABLISHED VEHICLE TO INVEST INTO INDIA, BUT ARE EXPECTED TO BE SPICED UP BY THIS MASALA BOND OPPORTUNITY? WHO ARE WE REALLY CHASING? WHAT ARE THE KINDS OF INVESTOR CLASS THAT WILL REALLY COME IN AND BRING THEIR DELTA?

PHILIPPE AHOUA, IFC: There are around 9,000 investors who have got FPI licenses. Among those investors who are not part of that investor pool is, to give one example, the Teachers’ Retirement Fund of the State

of Washington, which has bought into every maturity we’ve issued in Masala bonds.

Many Uridashi investors in Japan don’t have FPI licenses. I don’t know why. But huge demand is coming out of Japan for Masala bonds because traditionally Japanese investors are used to taking foreign exchange risk. They’re looking for yield and some level of currency stability. That’s exactly the story that the Masala bond offers.

So just to answer that, I wouldn’t underestimate the demand by offering something that is Euroclearable, that you can buy in Luxembourg and which is listed in London or Singapore. You’d be surprised how many people you can unearth in any currency in any format.

If you offer something in a format that people are comfortable with in terms of settlement, eventually the investor is going to take local currency exposure. But it’s settled in dollars. You can buy it on an exchange. You’ll see how many investors you unearth. And what could happen after that, is the investors will then most likely be interested in looking at getting FPI licenses so you increase your pool of potential FPI investors going forward.

IFR: LET’S WRAP UP THE SESSION THERE. A BIG THANK YOU TO OUR PANELLISTS FOR SHARING YOUR INSIGHTS.

03 Outlook for India Borrowers Bios and copy.indd 17 03/02/2016 09:21:12

International Financing Review Outlook for Indian Borrowers Roundtable February 201618

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

Source: IFR

Domestic Offshore Domestic Offshore Loan Loan Bond Bond Market Market Market Market

100%

80%

60%

40%

20%

0

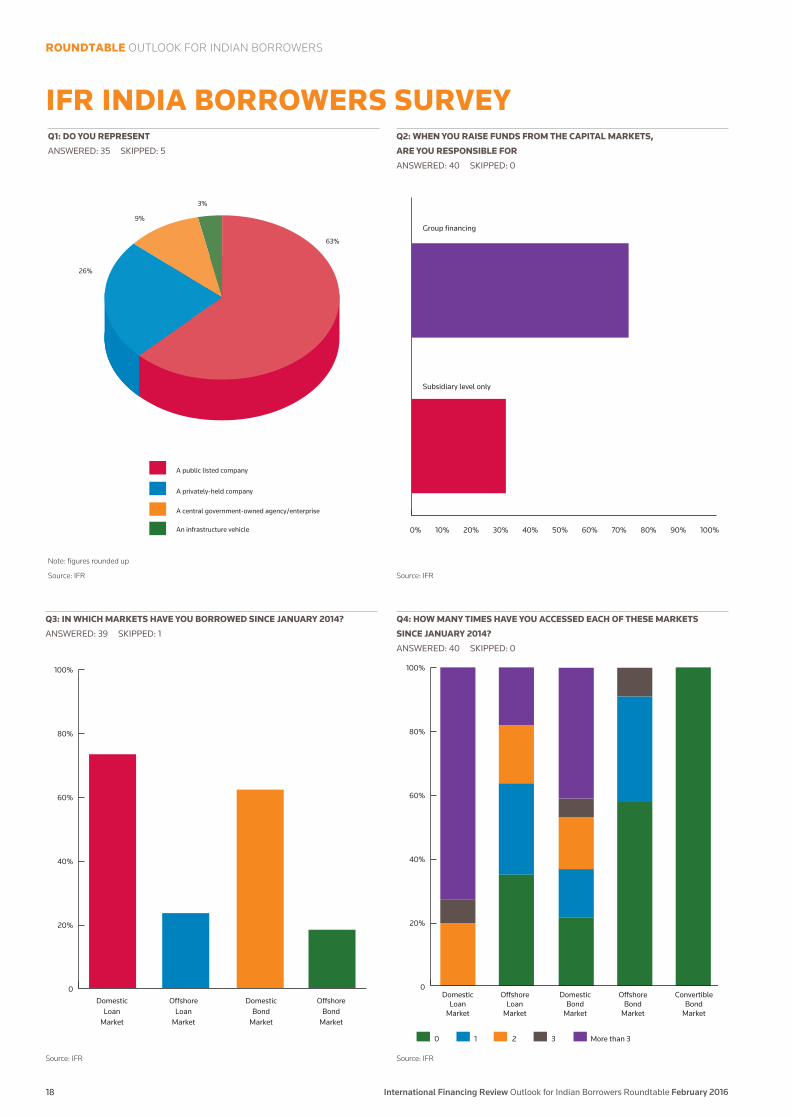

Q3: IN WHICH MARKETS HAVE YOU BORROWED SINCE JANUARY 2014?

ANSWERED: 39 SKIPPED: 1

Note: figures rounded up

Source: IFR

An infrastructure vehicle

A central government-owned agency/enterprise

A privately-held company

A public listed company

63%

3%

9%

26%

Q1: DO YOU REPRESENT

ANSWERED: 35 SKIPPED: 5

Source: IFR

Q2: WHEN YOU RAISE FUNDS FROM THE CAPITAL MARKETS,

ARE YOU RESPONSIBLE FOR

ANSWERED: 40 SKIPPED: 0

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Group financing

Subsidiary level only

Source: IFR

Domestic Offshore Domestic Offshore Convertible Loan Loan Bond Bond Bond Market Market Market Market Market

100%

80%

60%

40%

20%

0

0 1 2 3 More than 3

Q4: HOW MANY TIMES HAVE YOU ACCESSED EACH OF THESE MARKETS

SINCE JANUARY 2014?

ANSWERED: 40 SKIPPED: 0

IFR INDIA BORROWERS SURVEY

03 Outlook for India Borrowers Bios and copy.indd 18 03/02/2016 09:21:13

International Financing Review Outlook for Indian Borrowers Roundtable February 2016 19

OUTLOOK FOR INDIAN BORROWERS ROUNDTABLE

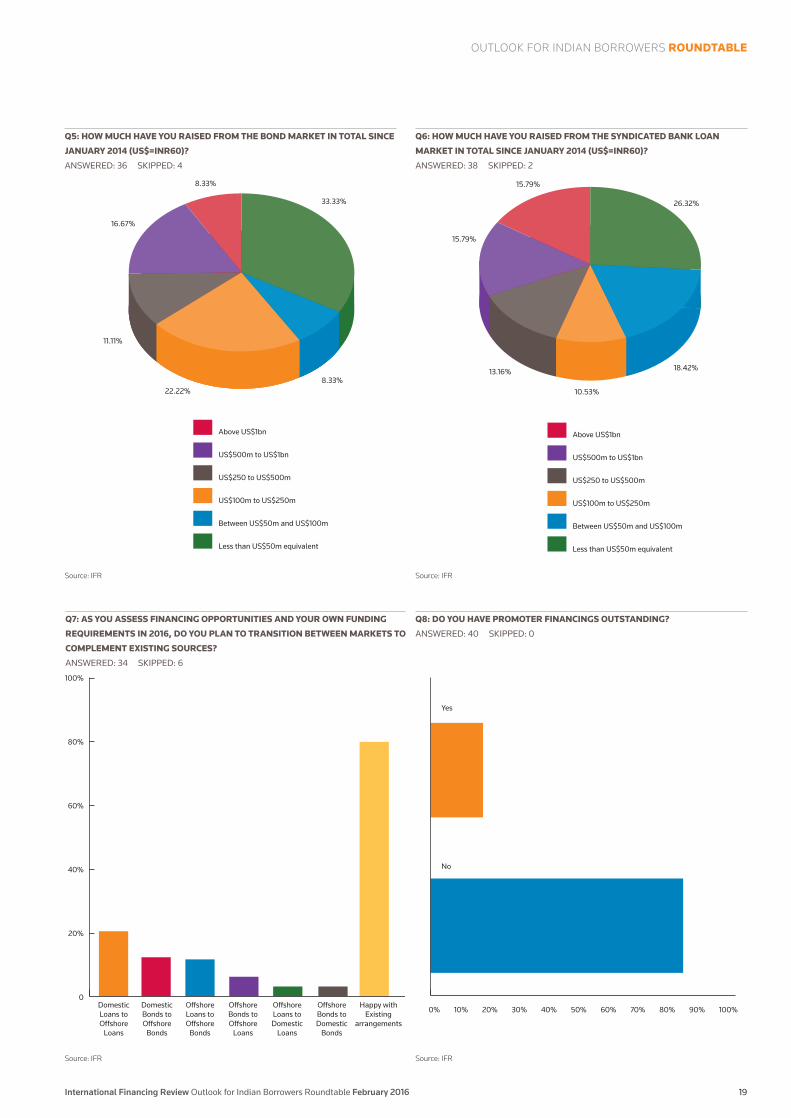

Source: IFR

33.33%

Above US$1bn

US$500m to US$1bn

US$250 to US$500m

US$100m to US$250m

Between US$50m and US$100m

Less than US$50m equivalent

8.33%22.22%

11.11%

8.33%

16.67%

Q5: HOW MUCH HAVE YOU RAISED FROM THE BOND MARKET IN TOTAL SINCE

JANUARY 2014 (US$=INR60)?

ANSWERED: 36 SKIPPED: 4

Source: IFR

Domestic Domestic Offshore Offshore Offshore Offshore Happy with Loans to Bonds to Loans to Bonds to Loans to Bonds to Existing Offshore Offshore Offshore Offshore Domestic Domestic arrangements Loans Bonds Bonds Loans Loans Bonds

100%

80%

60%

40%

20%

0

Q7: AS YOU ASSESS FINANCING OPPORTUNITIES AND YOUR OWN FUNDING

REQUIREMENTS IN 2016, DO YOU PLAN TO TRANSITION BETWEEN MARKETS TO

COMPLEMENT EXISTING SOURCES?

ANSWERED: 34 SKIPPED: 6

Source: IFR

26.32%

Above US$1bn

US$500m to US$1bn

US$250 to US$500m

US$100m to US$250m

Between US$50m and US$100m

Less than US$50m equivalent

18.42%

10.53%

15.79%

15.79%

13.16%

Q6: HOW MUCH HAVE YOU RAISED FROM THE SYNDICATED BANK LOAN

MARKET IN TOTAL SINCE JANUARY 2014 (US$=INR60)?

ANSWERED: 38 SKIPPED: 2

Source: IFR

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Yes

No

Q8: DO YOU HAVE PROMOTER FINANCINGS OUTSTANDING?

ANSWERED: 40 SKIPPED: 0

03 Outlook for India Borrowers Bios and copy.indd 19 03/02/2016 09:21:14

International Financing Review Outlook for Indian Borrowers Roundtable February 201620

ROUNDTABLE OUTLOOK FOR INDIAN BORROWERS

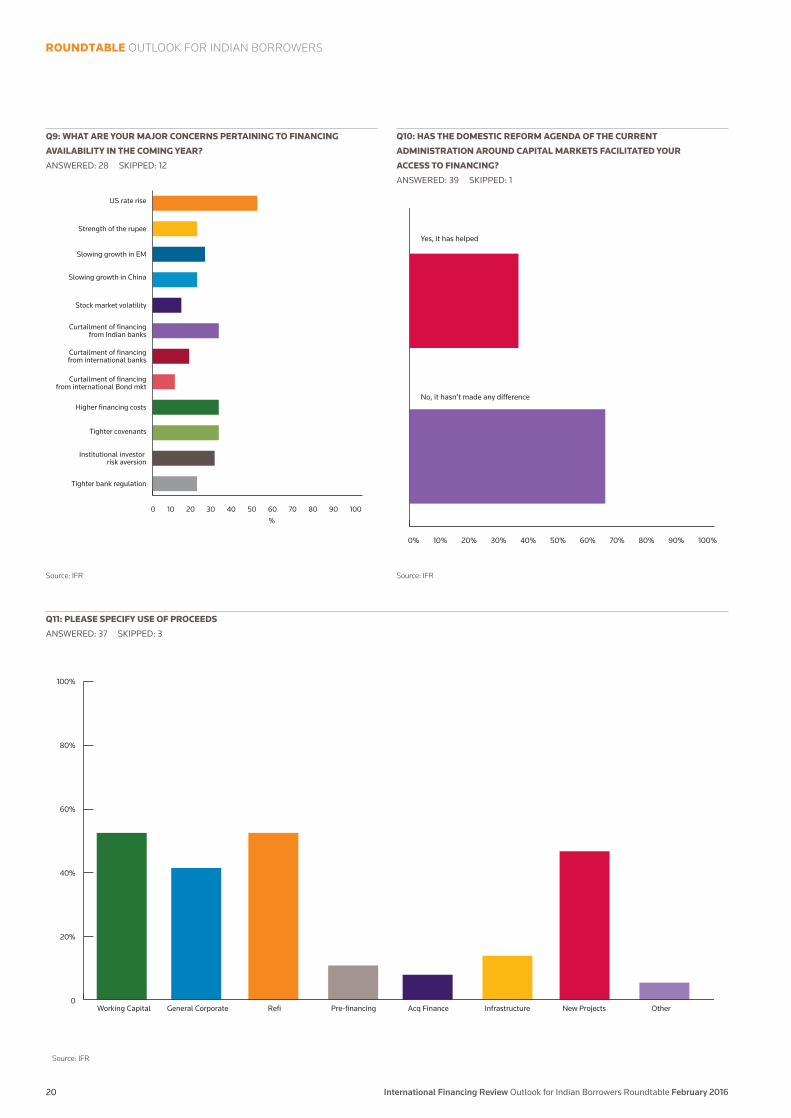

Source: IFR

0 10 20 30 40 50 60 70 80 90 100 %

US rate rise

Strength of the rupee

Slowing growth in EM

Slowing growth in China

Stock market volatility

Curtailment of financingfrom Indian banks

Curtailment of financingfrom international banks

Curtailment of financingfrom international Bond mkt

Higher financing costs

Tighter covenants

Institutional investor risk aversion

Tighter bank regulation

Q9: WHAT ARE YOUR MAJOR CONCERNS PERTAINING TO FINANCING

AVAILABILITY IN THE COMING YEAR?

ANSWERED: 28 SKIPPED: 12

Source: IFR

Working Capital General Corporate Refi Pre-financing Acq Finance Infrastructure New Projects Other

100%

80%

60%

40%

20%

0

Q11: PLEASE SPECIFY USE OF PROCEEDS

ANSWERED: 37 SKIPPED: 3

Source: IFR

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Yes, it has helped

No, it hasn’t made any difference

Q10: HAS THE DOMESTIC REFORM AGENDA OF THE CURRENT

ADMINISTRATION AROUND CAPITAL MARKETS FACILITATED YOUR

ACCESS TO FINANCING?

ANSWERED: 39 SKIPPED: 1

03 Outlook for India Borrowers Bios and copy.indd 20 03/02/2016 09:21:15

A THOMSON REUTERS SERVICE

IFR ASIA: AT THE HEART OF ASIA’S CAPITAL MARKETS

IFR Asia is the world’s most authoritative source of Asian capital markets intelligence, providing in-depth coverage on significant issues across asset classes.Established in 1997, it draws on IFR’s global editorial team – the largest of any capital markets publication, with bureaux throughout the region – to provide deep insight into international and domestic issuance.

IFRAsia.com takes this unrivalled content and adds intra-day updates, plus a searchable archive of IFR Asia stories, to create the perfect business development tool for the region’s investment banking professionals.

To learn more about how you will benefit from IFR Asia’s market-leading intelligence, visit www.IFRAsia.com today.

NOW AVAILABLE INTHOMSON REUTERS EIKON

MX11334 - IFR Asia A4 Advert Nov 15 v2.indd 1 26/11/2015 11:22