ifc 25/2014progressing opportunity cost pricing in the …/media/economics advisory/i… · web...

TRANSCRIPT

Progressing opportunity cost pricing in the 400 MHz bandDiscussion paperJUNE 2014

CanberraRed Building Benjamin OfficesChan Street Belconnen ACT

PO Box 78Belconnen ACT 2616

T +61 2 6219 5555F +61 2 6219 5353

MelbourneLevel 32 Melbourne Central Tower360 Elizabeth Street Melbourne VIC

PO Box 13112Law Courts Melbourne VIC 8010

T +61 3 9963 6800F +61 3 9963 6899

SydneyLevel 5 The Bay Centre65 Pirrama Road Pyrmont NSW

PO Box Q500Queen Victoria Building NSW 1230

T +61 2 9334 7700 1800 226 667F +61 2 9334 7799

Copyright notice

http://creativecommons.org/licenses/by/3.0/au/

With the exception of coats of arms, logos, emblems, images, other third-party material or devices protected by a trademark, this content is licensed under the Creative Commons Australia Attribution 3.0 Licence.

We request attribution as: © Commonwealth of Australia (Australian Communications and Media Authority) 2014.

All other rights are reserved.

The Australian Communications and Media Authority has undertaken reasonable enquiries to identify material owned by third parties and secure permission for its reproduction. Permission may need to be obtained from third parties to re-use their material.

Written enquiries may be sent to:

Manager, Editorial and DesignPO Box 13112Law CourtsMelbourne VIC 8010Tel: 03 9963 6968Email: [email protected]

acma | iii

1 Introduction and objectives1.1 OC in high density areas 11.2 Introducing OC in remote density areas 21.3 Structure of this paper 2

2 Background2.1 Introduction of OC principles 32.2 Responsibilities and spectrum management principles 32.3 Demand and congestion risk 4

3 Licensee behaviour in the high density areas

4 Monitoring the impact of OC pricing in the high density areas4.1 Summary of monitoring 84.2 Insights from ACMA frequency assigners 104.3 Consultation on the monitoring metrics 114.4 Preliminary view in high density areas 11

5 Introducing OC in the remote density areas5.1 Setting the licence tax rate in the remote density areas 135.2 A closer look at the Pilbara 135.3 Preliminary view in remote density areas 15

6 Revising apparatus licence taxes

7 Invitation to commentMaking a submission 18

Appendix A—Findings of the monitoring

Appendix B—Long-term tax signals

Appendix C—Summary of proposed changes to Licence Tax Determinations

acma | iv

1 Introduction and objectives1.1 OC in high density areasIn August 2012, the ACMA introduced opportunity cost (OC) pricing in the high density areas of the 400 MHz band as a complementary component to the 400 MHz band review. The 400 MHz band has experienced significant congestion in the high density areas of Sydney/Wollongong, Melbourne/Geelong and Brisbane/Gold Coast.1 The congestion has made it difficult for new licences to be issued and therefore new services to be provided.

The increase in the licence tax rate is designed to encourage licensees with low-value uses to exit, enabling entry of currently excluded high-value uses. The move to OC pricing is being staged through a series of 15 per cent increments in the licence tax rate. This staged implementation reflects uncertainty about the ‘true’ market clearing price and provides flexibility to the ACMA to discontinue tax increases if congestion is eventually removed—and considered unlikely to return in the foreseeable future—prior to all the intended tax increases being implemented.

The ACMA implemented the first of five intended increments towards a new OC-based licence tax rate of $199/kHz (plus annual CPI escalation) for these high density areas of the 400 MHz band on 15 August 2012. The remaining increments towards the full OC-based tax rate are yet to be made, and will only be implemented after monitoring the impact on demand and congestion of the tax increase and other regulatory changes.

In their responses to an earlier ACMA discussion paper seeking feedback on the introduction of OC pricing in the 400 MHz band, stakeholders generally considered that the ACMA should conduct appropriate reviews of the impact of prior tax increases before implementing further increases.2 Stakeholders also sought guidance and detail on how the ACMA intended to monitor, review and measure the impacts of OC pricing on demand.

This discussion paper delivers on this undertaking to consult with stakeholders about the appropriate indicators of demand and congestion; the impacts to date of the tax increase, and the need for further tax increases. It also develops a framework for analysing these issues that may be useful in future consideration of the planned subsequent licence tax increases.

The monitoring analysis indicates that the combination of regulatory changes and the licence tax increase is working to relieve congestion and to assist in the rotation from low to high-value uses. However, given the acute congestion experienced prior to these policy changes, it is unlikely that the impacts to date are consistent with the long-term removal of congestion. Further, demand for spectrum is likely to continue to grow, which suggests continuing rationalisation of spectrum demand is likely to be required to ensure that congestion does not re-emerge. Given this, the ACMA is proposing to implement the second increment to the licence tax rate towards full OC.

1 These high density areas are depicted as maps along with their geo-spatial coordinates in the a pparatus licence fee schedule. 2 ACMA, Adoption of opportunity cost pricing for apparatus licences in the 400 MHz band, April 2012.

acma | 1

1.2 Introducing OC in remote density areasIn April 2012, the ACMA also sought views on the possibility of applying OC pricing in remote density areas and associated implications of setting apparatus licence taxes at or close to the minimum tax amount (currently $37.48). It also sought views on the possibility of class licensing and the extent to which certain services may deny spectrum to others.

The ACMA stated in its response to the 400 MHz OC pricing paper that it also intended to introduce OC pricing in remote density areas of the 400 MHz band and would consult further about the appropriate level.3 Nevertheless, the ACMA signalled that, given the lower demand and lack of congestion in remote density areas, it anticipates that implementing OC-based apparatus licence taxes in remote density areas would be likely to imply reductions from current levels.

The ACMA currently considers there is scope to increase the public benefit from encouraging use of spectrum across the remote density areas of the 400 MHz band by reducing the licence tax rate to $0.00 per kHz (subject to the minimum tax rule). Moreover, such a reduction in the licence tax rate is unlikely to generate a significant increase in spectrum use such that excess supply would be removed and scarcity would emerge. The ACMA considers that lowering the licence tax to $0.00 per kHz is consistent with OC principles; would encourage increased use with resultant benefit, and not constrain any viable use. Given this, the ACMA is proposing to reduce the licence tax rate applicable for the remote density areas of the 400 MHz band to $0.00 per kHz.

1.3 Structure of this paper> Chapter 1 provides a brief introduction to the ACMA’s adoption of OC pricing in the

400 MHz band. > Chapter 2 positions the issues within the ACMA’s spectrum management

responsibilities and provides critical background to pricing spectrum consistent with OC principles. This reflects the ACMA’s strong view that any change to the licence tax rate that is implemented must be consistent with and effective within the environment they are introduced into.

> Chapter 3 outlines the likely intended responses from current and potential licensees and the complexities involved in monitoring impacts in such a context.

> Chapter 4 provides an overview of the monitoring undertaken by the ACMA to assess the impact of introducing an OC-based licence tax rate in the high density areas of the 400 MHz band in August 2012, and to inform a decision around the need for further tax increases

> Chapter 5 details the ACMA’s consideration of introducing licence tax rates based on OC in the remote density areas of the 400 MHz band. It also details whether the relevant apparatus licence taxes should be set to zero, given current excess supply at the current tax rate across most of the remote density areas.

> Chapter 6 outlines how the proposed changes to licence taxes for both high density and remote density areas would be implemented in the relevant legislation.

> Chapter 7 invites interested stakeholders to comment on the issues set out in this paper or any other issues relevant to setting appropriate apparatus licence taxes in both contexts.

3 ACMA, The ACMA response to public submissions—adoption of opportunity cost pricing for apparatus licences in the 400 MHz band, August 2012.

2 | acma

2 BackgroundThis chapter positions the issues within the ACMA’s spectrum management responsibilities. It also provides a snapshot of current demand in the 400 MHz remote density areas as critical background to pricing spectrum consistent with OC principles. This reflects the ACMA’s strong view that any change to the tax rate that is implemented must be consistent with and effective within the environment they are introduced into.

2.1 Introduction of OC principlesIn January 2010, the ACMA announced an in-principle decision to use OC pricing as one of its suite of tools to manage spectrum.4 Setting prices for administratively allocated spectrum, with reference to its OC, is intended to improve the efficiency of spectrum allocation and use. The application of OC pricing to administratively allocated spectrum will require a band-by-band assessment and be influenced by factors such as the levels of congestion and the expected benefits of implementing OC pricing.

In December 2010, the ACMA released the final in a series of four papers titled The way ahead: Timeframes and implementation plans for the 400 MHz band (the Way ahead paper). In this paper, the ACMA confirmed that the 400 MHz band would be the first band where OC pricing would be introduced. This focus on the 400 MHz band predominantly reflected the acute congestion apparent in the high density areas.

2.2 Responsibilities and spectrum management principlesThe ACMA’s responsibilities in managing access to the radiofrequency spectrum are principally discharged under the Radiocommunications Act 1992 (the Act). Paragraph 3(a) states that the object of the Act is:

… to provide for management of the radiofrequency spectrum in order to maximise, by ensuring the efficient allocation and use of the spectrum, the overall public benefit derived from using the radiofrequency spectrum.

The ACMA has developed and widely disseminated a set of principles that guide its decision-making around spectrum management issues and ensure it discharges its responsibilities consistent with the Act. The principles are:> allocate spectrum to the highest value use or uses> enable and encourage spectrum to move to its highest value use or uses> use the least cost and least restrictive approach to achieving policy objectives> to the extent possible, promote both certainty and flexibility> balance the cost of interference and the benefits of greater spectrum utilisation.

The rationale for introducing OC pricing in the high density areas of the 400 MHz band is specifically targeted at addressing particularly acute congestion. This congestion reflects strong growth in demand for spectrum and is partly the result of spectrum being charged significantly less than its estimated OC. Where taxes are below the OC price, some spectrum users (with values in use below the OC-based licence tax rate) will continue to use spectrum, creating productive inefficiencies and therefore inefficient use of spectrum. This is inconsistent with both the principles and objectives of the Act. The introduction of OC principles will improve efficiency by providing

4 ACMA, The ACMA response to public submissions: Opportunity cost pricing of spectrum. January 2010.

acma | 3

incentives for users with lower value uses to discontinue their spectrum use, thus freeing up spectrum to be reallocated to high-value uses.

More efficient use of currently underutilised spectrum is the intended objective and rationale for OC pricing in the remote density areas of the 400 MHz band. Reducing taxes towards OC may facilitate entry of licensees who value this spectrum above the OC tax but below the current tax level. This would have the effect of encouraging greater use of this spectrum. Consistent with the principles of OC pricing, in cases where supply exceeds demand into the foreseeable future, there is unlikely to be alternative productive alternative uses of spectrum, and thus opportunity cost is expected to be zero or negligible.

2.3 Demand and congestion riskThe ACMA considers that the tax rates to be implemented should be consistent with, and effective within, the environment to which they apply. A critical aspect of aligning licence tax rates with OC principles is to examine the demand-supply characteristics of the particular segment, and to consider the risk of congestion and, by extension, spectrum denial. Heat maps analyse the geographical distribution of assignments and can identify areas where the number of existing assignments is approaching its maximum. Consequently, heat maps can provide insights into the current level of demand and the proximity of congestion. In this context, the maximum number of assignments that can operate effectively within a given geographic area depends on a range of factors including:> the size of the relevant area> the location of actual or proposed base stations> the power of the intended transmission> the local terrain (for example, mountains may increase the potential for re-use

within a defined geographic area).

The heat map below is for land mobiles in the X segment of the 400 MHz band as at October 2013. The X segment is allocated to land mobiles services (two frequency, base transmit) and occupies spectrum from 462.5000 MHz to 467.50625 MHz. The X segment is base transmit and is paired with the S segment (452.5 MHz to 457.50625 MHz) for base receive. The heat map is based on 25 kHz channelisation, suggesting an indicative maximum number of assignments of 200.5 Hence, as the actual number of assignments in any geographic area approaches 200, the heat map assigns a colour closer to red. The colour-based (logarithmic) scale is shown at the right of the heat map.

5 The X segment comprises around 5 MHz of spectrum (from 462.5 MHz to 467.50625 MHz) implying around 200 available channels at 25 kHz (5,000 kHz divided by 25 kHz).

4 | acma

Figure 1 Heat map for land mobiles in the X segment of the 400 MHz band at 25 kHz (October 2013)

Source: ACMA internal analysis

The heat map shows continuing high levels of spectrum utilisation in the high density areas of the 400 MHz band. Addressing this ongoing congestion is the rationale for introducing OC pricing in the high density areas of the band.

The heat map also shows significantly lower utilisation of spectrum across most of the remote density areas of Australia relative to that of the medium density and higher density areas. Viewed overall, demand for spectrum in the remote density areas of the

400 MHz band is generally low and there is no evidence of widespread congestion currently. There is also no evidence that congestion equivalent to that experienced in Sydney (as representative of high density areas) will emerge in the foreseeable future.

However, the heat map also shows an area of apparent congestion around the Pilbara region in north-west Western Australia. The Pilbara is colour-coded red indicating that current spectrum is close to the 200 assignment maximum that is consistent with congestion. In fact, spectrum congestion in the Pilbara appears similar to that in Sydney and (assuming 25 kHz channelisation) consistent with imminent exhaust. This may suggest that spectrum demand in the Pilbara—for this segment at least—is already problematic. This has implications for setting the licence tax at an appropriate level.

acma | 5

3 Licensee behaviour in the high density areasThe rationale for introducing OC pricing in the 400 MHz band areas was specifically targeted at addressing particularly acute congestion across the high density areas. This congestion was largely the result of spectrum being charged at a rate that was significantly less than its estimated opportunity cost. This meant that it was viable for licensees with low-value uses to continue to use spectrum. Ongoing use by low-value services has made it difficult for high potential value uses to access spectrum, even though the expected value from using the spectrum is positive at both the old licence tax rate and potentially positive at the newly introduced tax rate based on OC. This was inconsistent with the first two spectrum management principles as spectrum was not currently used for its highest value use and there was limited scope to encourage spectrum to move from low to higher value uses.

The signalled increases in the apparatus licence tax rate in high density areas of the 400 MHz band are intended to encourage certain licensee behaviours. Over time, this is expected to reduce demand for spectrum and thus alleviate the current congestion. It is expected that the licence tax increase in the high density areas of the 400 MHz band would provide an incentive for rational current users of spectrum to:> Discontinue their apparatus licences where the net benefit they gain from using the

spectrum for a particular purpose is negative or other spectrum substitutes are more cost-effective at the now increased licence tax rate or based on the expected implementation of each of the increments.

> Consider the viability of continuing to hold licences where spectrum usage is low.6

> Consider using more spectrally efficient equipment, which would enable narrower transmission bandwidths to be used. This would reduce their need for spectrum and their resultant tax burden relative to a situation where they had continued to use less spectrally efficient equipment.7

Although the ACMA expects these behaviours to emerge as a result of the licence tax rate increase, it has no precise view on which licensees will be impacted. However, it may be that licensees, who perceive their use of the spectrum relative to the apparatus licence tax to be low value, may exit and licensees with higher value potential uses may enter. The ACMA is neither attempting to accurately predict licensee reaction to the higher licence tax at an individual increment nor is it intending to act as a substitute for the market. Instead, the ACMA intends that licensee decisions about spectrum use are informed by efficient price signals based on OC.

The ACMA’s analysis in this context is complicated by licensees responding in large part to their view of the expected long-term licence tax rate, rather than to a particular increment at any point in time. Therefore, even if congestion was fully removed after the first increase, it would not be possible to conclude that congestion had been removed because of the first increase and that further increases were unnecessary. Clearly, this affects the way the monitoring analysis is interpreted and the conclusions that can be made. The ACMA also recognises that mature responses to any tax increase may take several years, or longer, to become apparent, given the typically long, useful lives of assets that complement spectrum. More information on these interrelated issues is provided at Appendix B.

6 Recognising that low use is not necessarily indicative of low value.7 This economic incentive reinforces a regulatory requirement to re-channelise.

6 | acma

The ACMA’s objective is to provide signals about the long-term costs of spectrum to enable informed decisions by spectrum users around their use of spectrum and inter-related network assets, typically with long, useful lives. Altering the strongly signalled glide path by not implementing all five ‘planned’ increases introduces uncertainty and distorts the long-term signal component in the licence tax rate. This suggests that the implementation of each of the increments should only be truncated in exceptional circumstances, and after clear evidence that congestion has been removed and rotation to higher value uses significantly progressed.

The ACMA’s monitoring exercise has focused on developing metrics that assist in identifying whether these intended behaviours are occurring and, where possible, quantifying the extent of the response to date.

acma | 7

4 Monitoring the impact of OC pricing in the high density areasThe ACMA’s monitoring exercise has focused on quantitative and qualitative metrics that assist in identifying whether these intended behaviours are occurring and, where possible, quantifying the extent of the response to date. As a result, the ACMA developed metrics which inform on the aggregate level of demand for spectrum in the high density areas of the 400 MHz band. Monitoring these demand-related metrics over time will identify the impacts of the tax increase on demand (combined with the other regulatory changes). It will also assist in considering whether demand has tended sufficiently below supply to alleviate congestion and in turn reduce the need for further tax increases.

As has been noted by stakeholders in previous consultations, the ACMA has also introduced a number of regulatory changes associated with the review of the 400 MHZ band at the same time as introducing the tax increments. The ACMA recognises that this makes it more difficult to identify the unique contribution of tax increments towards the desired licensee behaviours. Recognising this, the ACMA is not intending to disaggregate the behavioural responses of licensees into components attributable separately to the tax increase and separately to the regulatory changes. The focus of the monitoring analysis is on identifying whether congestion in the high density areas of the 400 MHz band has been removed (whether due to regulatory changes or tax changes) such that further tax increases are not required.

4.1 Summary of monitoring The monitoring undertaken to date indicates that the combination of regulatory changes following the 400 MHz review, and the increase in the licence tax rate, is beginning to have some intended outcomes including:> The number of licences and assignments have started to reduce across each of

the high density areas. Since the introduction of the higher licence tax rate, the number of assignments has fallen by 3.9 per cent in Sydney/Wollongong; by 3.5 per cent in Melbourne/Geelong; and risen by 17.8 per cent in Brisbane/Gold Coast.8

> Licensees who ascribe a low value to these licences have surrendered their licences or allowed them to lapse, freeing up spectrum for potential reallocation. Since the introduction of the higher licence tax rate, the aggregate number of lapsed and surrendered licences has totalled 2,999 in Sydney/Wollongong; 1,722 in Melbourne/Geelong; and 1,615 in Brisbane/Gold Coast.

> Previously excluded potential licensees with prospective high-value uses have gained access to freed-up spectrum by taking out licences. Since the introduction of the higher licence tax rate, the aggregate number of new licences has totalled 2,762 in Sydney/Wollongong; 1,396 in Melbourne/Geelong; and 1,872 in Brisbane/Gold Coast.9

> A significant number of licensees have moved to narrower bandwidth channels, where possible, as mandated by new regulatory requirements and reinforced by the tax increase.

8 The increase in Brisbane/Gold Coast reflects operations of the Wireless Government Network Directorate (GWND) and does not reflect the impact of the higher licence tax rate. Prior to the commencement of operations by the GWND, the number of licences was also falling in the Brisbane/Gold Coast high density area.9 Again reflects the impact of the GWND.

8 | acma

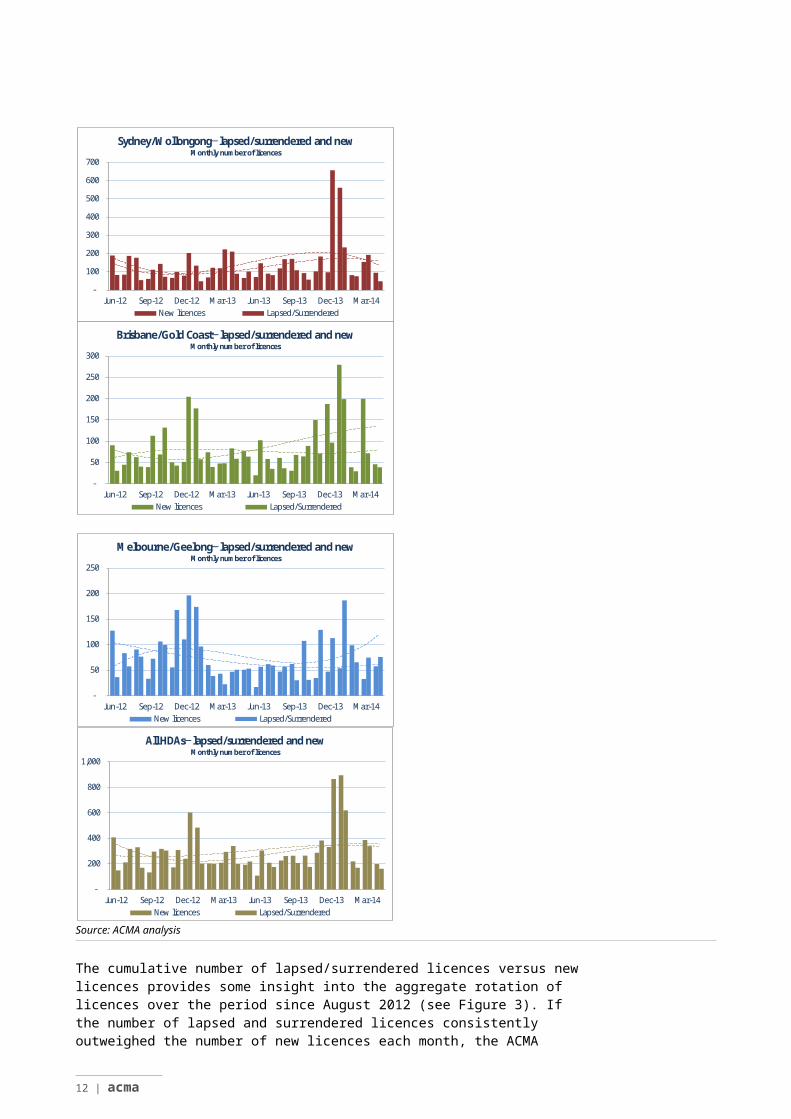

The foregoing analysis (detailed in Appendix A) indicates that the licence tax rate increase (along with the regulatory changes) appears to be encouraging the intended behaviours from existing and potential licensees. Critically, this includes effecting a rotation of spectrum use from low-value to higher value uses. There has been some acceleration of licensees exiting spectrum (lapsed and surrendered licences), which shows that their value in use is negative at the new OC-based licence tax rate or that other spectrum substitutes have become more cost-effective.10 This freeing up of spectrum has facilitated entry by new licensees. Presumably, these new entrants have prospective positive values in use at the new OC-based licence tax rate—otherwise they would not seek access to this spectrum at the higher OC-based tax rate. The monitoring undertaken by the ACMA specifically captures data on both of these intended behaviours. Monthly movements in these metrics are depicted together in the charts below.

Figure 2 Monthly evolution of lapsed/surrendered licences relative to new licences

-

100

200

300

400

500

600

700

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Sydney/Wollongong─lapsed/surrendered and new Monthly number of licences

New licences Lapsed/Surrendered

-

50

100

150

200

250

300

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Brisbane/Gold Coast─lapsed/surrendered and newMonthly number of licences

New licences Lapsed/Surrendered

-

50

100

150

200

250

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Melbourne/Geelong─lapsed/surrendered and newMonthly number of licences

New licences Lapsed/Surrendered

-

200

400

600

800

1,000

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

All HDAs─lapsed/surrendered and newMonthly number of licences

New licences Lapsed/Surrendered

Source: ACMA analysis

The cumulative number of lapsed/surrendered licences versus new licences provides some insight into the aggregate rotation of licences over the period since August 2012 (see Figure 3). If the number of lapsed and surrendered licences consistently outweighed the number of new licences each month, the ACMA would expect to see a wide gap between the aggregate number of lapsed/surrendered licences compared with new licences, since the licence tax rate was increased. However, while the aggregate number of lapsed/surrendered licences has exceeded new licences in both Sydney/Wollongong and Melbourne/Geelong, it is not clear that the gap is significant. In Brisbane/Gold Coast the number of new licences has exceeded the number of lapsed/surrendered licences. The experience in Brisbane/Gold Coast in large part reflects the recent activity of the Government Wireless Network Directorate (GWND) in rolling out a new government wireless network, rather than any response to the 10 Or that substitute inputs are preferable to spectrum as they become relatively cheaper if spectrum is priced at its opportunity cost.

acma | 9

regulatory and/or licence tax rate changes. The GWND is part of the Queensland Department of Science, Information Technology, Innovation and the Arts.

Figure 3 Aggregate discontinued and new licences since August 2012

-

500

1,000

1,500

2,000

2,500

3,000

Sydney/Wollongong Brisbane/Gold Coast Melbourne/Geelong

Aggregate entry and exitNumber of licences

Lapsed/surrendered New licences

Source: ACMA analysis

More detail on the monitoring analysis undertaken by the ACMA is in Appendix A. The analysis indicates that the combination of regulatory changes and the licence tax increase is working to relieve congestion and to assist in the rotation from low- to high-value uses. However, given the acute congestion experienced prior to these policy changes, it is unlikely that the impacts to date are consistent with the long-term removal of congestion. Further, demand for spectrum is likely to continue to grow, suggesting continuing rationalisation of spectrum demand is likely to be required to ensure that acute congestion does not re-emerge.

4.2 Insights from ACMA frequency assignersComplementing the detailed quantitative analysis above is anecdotal information from ACMA’s frequency assigners. Their role is to assign frequencies to licensees seeking access to spectrum. A critical aspect of assignment is their assessment of whether there is an appropriate frequency available to assign to a new user (licensee). This takes into account all existing licences and all relevant engineering requirements, mainly around interference mitigation, including distance rules and power requirements. As noted above, they undertake the analysis around the availability of spectrum on a case-by-case basis.

The ACMA’s frequency assigners have been indicating for some time that congestion in the high density areas of the 400 MHz band was making it extremely difficult to readily assign frequencies when requested. Consequently, their role is likely to enable them to have useful insights regarding perceived impacts on their ability to assign frequencies since the tax increase. Given that congestion has been a limiting factor for the ACMA assigners for some time—mainly in the high density areas of the 400 MHz band—it is timely to draw on their experience since the licence tax increase and to understand whether there have been any noticeable impacts from their perspective.

10 | acma

The views of the internal spectrum assigners are summarised below:> There has been some noticeable, but not significant, reduction in their difficulty in

assigning frequency to licensees seeking spectrum in the high density areas of the 400 MHz band.

> Spectrum is still more difficult to allocate in the high density areas of the 400 MHz band than in other bands, for example, VHF.

> Their perception is that the reduction in assignment difficulty to date results from the regulatory requirement around re-channelisation, which frees up spectrum for reassignment rather than a direct consequence of the tax increase.

> They anticipate further improvement in the ease of frequency assignment over the medium term, although again this expectation relates more to continuing re-channelisation rather than a direct effect of the tax increase.

Overall, the feedback from the ACMA assigners suggests that there has been some modest improvement in their ability to assign frequency in the high density areas of the 400 MHz band, although spectrum is still relatively difficult to allocate. They were uncertain about the direct impact of the tax increase relative to that from the regulatory changes; both since August 2012 to date and into the future.

4.3 Consultation on the monitoring metricsThe ACMA has identified a range of metrics that it has monitored; however, it is seeking the views of directly impacted stakeholders as to whether these metrics provide sufficient information on which to form robust views about the need for further licence tax increases. In particular, are there other metrics which could potentially provide useful information in these deliberations?

The ACMA is also interested in stakeholder views about the analysis undertaken to inform a decision about the need for a second tax increase. Particularly, the ACMA is interested in the views of stakeholders about whether the metrics are consistent with the objectives of the monitoring and, by extension, the objectives of introducing OC pricing into the high density areas of the 400 MHz band. Equally as important, the ACMA is interested in stakeholder views on whether the ACMA has interpreted the data and analysis correctly and arrived at valid conclusions.

Question 1> Are the proposed monitoring metrics appropriate for this context?

Question 2> Are there other metrics that offer meaningful insights into the demand

response which should be monitored?Question 3> Has the ACMA interpreted the data and analysis correctly?

4.4 Preliminary view in high density areasBased on the above analysis, the first licence tax increase (combined with the other regulatory changes) has had some intended impacts:> The number of licences and assignments have started to reduce across the high

density areas of Sydney/Wollongong and Melbourne/Geelong. While there has been an increase in the Brisbane/Gold Coast high density area, this can be explained by the commencement of the GWND.

> Some licensees who ascribe a low value to these licences, or have more cost-effective spectrum substitutes at the higher licence tax rate, have surrendered their licences or allowed them to lapse freeing up spectrum for potential reallocation.

acma | 11

> Some previously excluded potential licensees with prospective high value uses have gained access to freed-up spectrum by taking out licences.

> A significant number of licensees have moved to narrower bandwidth channels, where possible, as mandated by new regulatory requirements and reinforced by the tax increase.

However, the minimal shifts in licence numbers, and significant remaining scope for re-channelisation, suggest that the responses to the regulatory and licence tax increase are not yet mature. The monitoring metrics suggest that the market is still responding to the signalled licence tax rate increase and demand is unlikely to have fully moved into equilibrium with supply. Therefore, the ACMA is of the opinion that there is merit in implementing the second of the five potential increases to an OC–based licence tax towards $199/kHz plus CPI.

Question 4> Is the recommendation to implement the second tax increase appropriate

given the information and analysis detailed above?

12 | acma

5 Introducing OC in the remote density areasAs discussed above, the ACMA has applied OC principles to increase the licence tax for the high density areas of the 400 MHz band and intends to apply similar principles in the remote density areas. The ACMA signalled that application of OC principles in the remote density areas was likely to result in a reduction in the licence tax. This chapter outlines the ACMA’s intended application of OC principles to the remote density areas of the 400 MHz band.

5.1 Setting the licence tax rate in the remote density areasExcess supply and a general lack of congestion at the current licence tax rate across most of the remote density areas of the 400 MHz band imply a tax reduction could be appropriate and consistent with the objectives of the Act. However, in the absence of a well-specified demand curve, the appropriate tax rate or extent of tax reduction are difficult to determine.

A test for the scarcity of spectrum is whether at a licence tax rate of $0 all reasonable demand could be accommodated and there would still be excess supply. In this situation, there would be no scarcity of spectrum and no opportunity cost associated with spectrum use. This test for scarcity needs to be forward-looking and anticipate demand over some forward period. This would ideally be linked to the capital expenditure (capex) cycle of spectrum complementary assets (that is, assets used in conjunction with spectrum to derive value and/or provide end-services). As indicated above, it appears unlikely that demand growth in the remote density areas will be such that demand will exceed potential supply. Potential spectrum users will therefore practically always be able to access spectrum. Further, use of spectrum by a particular licensee does not and will not prevent other appropriate potential spectrum users from also accessing spectrum. This strongly implies that the OC of this spectrum in remote density areas could be quite low; potentially $0.

Reflecting this, the ACMA considers that taxing spectrum at a rate of $0 per kHz, subject to the minimum tax rule in the remote density areas of the 400 MHz band, is appropriate.11 It is possible that further use of spectrum could be encouraged by the lower effective licence tax rate. The resulting gain in benefit from increased spectrum use would be a positive outcome of the tax reduction. Given the current extent of unutilised spectrum, heightened demand is unlikely to result in excess demand, congestion or any negative consequences to efficiency; at least for the foreseeable future.

5.2 A closer look at the PilbaraSeveral of the segment-specific heat maps show congestion in and around the Pilbara region. This raises concern about the appropriateness of reducing the licence tax to the minimum tax level. Such a reduction could aggravate the risk of, and potential for, congestion and could therefore be inappropriate and arguably poor regulatory practice.

A critical driver of congestion in some segments is alignment of the Australian band plan with the US and European band plans. This means the approved use for that spectrum segment in Australia matches the approved use in the US and Europe. Such alignment provides significant scale for equipment and handset/device manufacturers,

11 This would effectively result in taxing at the minimum tax rate for all relevant licensees.

acma | 13

reducing the cost of non-spectrum inputs to spectrum licensees, including licensees operating (or intending to operate) in Australia. A consequence of this is that there is a significant cost advantage for licensees to congregate in these aligned segments where equipment and handset/device costs are lower. This in turn boosts demand for aligned segments in Australia, contributing to apparent congestion in those segments. Simultaneously, this leaves demand in non-aligned segments significantly lower and unlikely to experience congestion in the foreseeable future. The consequent differential current congestion levels and forward risk across the segments may have implications for setting efficient licence tax rates.

From the perspective of setting an economically efficient licence tax, the critical question is whether viable spectrum demand would be denied if demand for land mobile spectrum continues to rise commensurate with recent trends. Such denial would indicate scarcity and that there was a non-zero opportunity cost associated with this spectrum. However, it appears likely that prospective licensees encountering aligned bands where spectrum is no longer available could move relatively easily to non-aligned bands, albeit incurring some higher costs for equipment and handsets/devices.

There is a range of substitution possibilities for most licensees seeking access to the 400 MHz band. There is ready substitutability of spectrum across the lower end of the band (403 MHz to 470 MHz) and across the upper end of the band (450 MHz to 520 MHz) but not across much of the lower band to much of the upper band. Spectrum within the overlapping zone (450 MHz to 470 MHz) can be both a substitute for spectrum lower in the band and for spectrum higher in the range. This makes spectrum in the overlapping zone particularly attractive and partly explains its apparent congestion.

The heat maps below summarise spectrum demand in two alternate segments (the I and DD segments) which are broadly substitutable for the spectrum in the X segment depicted in the heat map at page 5. The I segment (412.4625 MHz to 413.4375 MHz) is from the lower end of the 400 MHz band while the DD segment (475.19375 MHz to 476.4125 MHz) is from the upper end. The heat maps for both segments indicate that demand in these substitutable segments is quite low and imminent congestion unlikely.

Figure 4 Heat map for land mobiles in the I and DD segments of the 400 MHz band at 25 kHz (October 2013)

I segment DD segment

Source: ACMA internal analysis

It is clear that spectrum in other segments is a substitute for spectrum in the congested segments; albeit with associated higher equipment and handset/devices costs. Reflecting this, viable demand is not denied by spectrum exhaust in the highly congested segments, although there will be a cost disadvantage for equipment and

14 | acma

handsets/devices to move to other non-congested segments. The fact that viable spectrum is not denied suggests that the opportunity cost is low (possibly zero) and that the licence tax should be similarly low.

Reflecting this non-denial of spectrum use, the ACMA is proposing to apply the minimum tax in the Pilbara. This is consistent with the proposed arrangements for the remote density areas of the 400 MHz band. The reduction in licence tax in segments not currently congested, but substitutable for congested spectrum, reduces the aggregate inputs costs (that is, total spectrum and equipment costs) for prospective licensees. This, in part, offsets the equipment cost differential associated with non-alignment and boosts the viability of non-aligned spectrum segments.

5.3 Preliminary view in remote density areasReflecting the above analysis, the ACMA currently considers there is scope to increase the public benefit from encouraging use of spectrum across the remote density areas of the 400 MHz band by reducing the licence tax to $0.00 per kHz (subject to the minimum tax rule). Moreover, such a reduction in the licence tax is unlikely to generate a significant increase in spectrum use, such that excess supply would be removed and scarcity would emerge. Given this, the ACMA considers that lowering the licence tax to $0.00 per kHz is consistent with OC principles; would encourage increased use with resultant benefit; and would not constrain any viable use.

A number of respondents to the consultation on implementing OC pricing in high density areas of the 400 MHz band argued that the introduction of OC-based licence taxes in the remote density area of the 400 MHz band should not retain the minimum tax constraint. Under this constraint, the aggregate licence tax is the maximum of a tax calculated applying the licence tax formula in the Apparatus Licence Fee Schedule12 and a minimum tax amount currently set at $37.48 (and annually escalated by the CPI).

The application of the minimum tax constraint is designed to send efficient price signals to licensees about spectrum use, and to effect adequate recovery of the indirect costs associated with spectrum management from a wide base of licensees. Apparatus licence taxes based only on OC (and not constrained by the minimum tax rule) would only include signals about efficient spectrum use. In addition, the burden of recovery of indirect costs would be partly shifted away from licensees in remote density areas of the 400 MHz band to all other licensees. It is equitable that the burden of indirect cost recovery generally falls on all who benefit from the ACMA’s spectrum management, including all licensees operating in remote density areas of the 400 MHz band. By implication, equity is optimised when the burden of cost recovery is spread across the widest range of taxpayers (that is, that the tax base is as broad as possible) suggesting all licensees across all spectrum bands should make contributions towards covering these indirect costs. Reflecting this, the ACMA is not proposing removal of the minimum tax rule generally or in the context of pricing spectrum in the remote density areas of the 400 MHz band.

12 See the Apparatus Licence Fee Schedule, 5 April 2013, Appendix D, page 38.

acma | 15

Question 5> Do stakeholders agree that setting the licence tax at the minimum tax rate

is appropriate for the remote density area of the 400 MHz band? If not, please provide reasons?

Question 6> Do stakeholders agree that the minimum tax rule should continue to apply

to licensees in the remote density areas of the 400 MHz band? If not, please provide reasons?

Question 7> Do stakeholders agree that available spectrum in other segments means

that viable demand for spectrum will not be denied access? If not, please provide reasons?

Question 8> Do stakeholders agree that the proposed licence tax reduction should

apply to the Pilbara? If not, please provide reasons?

16 | acma

6 Revising apparatus licence taxesIt is proposed that new OC-based taxes will apply to all licences in both the high density and remote density areas of the 400 MHz band, including licences for general use, point-to-point services, point-to-multipoint services and land mobile services. The main exception is for amateur licences. The ACMA proposes to amend the following determinations to reflect the proposals described above:> Radiocommunications (Transmitter Licence Tax) Determination 2003 (No. 2)

(Transmitter Licence Tax Determination).> Radiocommunications (Receiver Licence Tax) Determination 2003 (No. 2)

(Receiver Licence Tax Determination).

Taxes per kHz for both the high density and remote density areas of the 400 MHz band in tables 202, 302, 402 and 502 of the Transmitter Licence Tax Determination and tables 202 and 302 of the Receiver Licence Tax Determination will change. The proposed changes are itemised in Appendix C.

The relevant parts of these proposed changes in the Transmitter Licence Tax Determination and the Receiver Licence Tax Determination will be replicated in the Apparatus Licence Fee Schedule.

acma | 17

7 Invitation to commentMaking a submissionThe ACMA invites comments on the issues set out in this discussion paper or any other issues relevant to setting appropriate apparatus licence taxes. Submissions should be made:By email: [email protected] mail: The Manager

Spectrum Pricing SectionRadiocommunications Policy BranchAustralian Communications and Media AuthorityPO Box 78Belconnen ACT 2616

The closing date for submissions is 14 August 2014.

Electronic submissions in Microsoft Word or Rich Text Format are preferred.

Media enquiries should be directed to Emma Rossi on 02 9334 7719 or by email to [email protected]. Any other enquiries may be directed by email to [email protected].

Effective consultation The ACMA is working to enhance the effectiveness of its stakeholder consultation processes, which are an important source of evidence for its regulatory development activities. To assist stakeholders in formulating submissions to its formal, written consultation processes, it has developed Effective consultation—a guide to making a submission. This guide provides information about the ACMA’s formal written public consultation processes and practical guidance on how to make a submission.

Publication of submissionsIn general, the ACMA publishes all submissions it receives. The ACMA prefers to receive submissions that are not claimed to be confidential. However, the ACMA accepts that a submitter may sometimes wish to provide information in confidence. In these circumstances, submitters are asked to identify the material over which confidentiality is claimed and provide a written explanation for the claim.

The ACMA will consider each confidentiality claim on a case-by-case basis. If the ACMA accepts a claim, it will not publish the confidential information unless authorised or required by law to do so.

Release of submissions where authorised or required by lawAny submissions provided to the ACMA may be released under the Freedom of Information Act 1982 (unless an exemption applies) or shared with other Commonwealth Government agencies under Part 7A of the Australian Communications and Media Authority Act 2005. The ACMA may also be required to release submissions for other reasons including for the purpose of parliamentary processes or where otherwise required by law (for example, under a court subpoena). While the ACMA seeks to consult submitters of confidential information before that information is provided to another party, the ACMA cannot guarantee that confidential information will not be released through these or other legal means.

18 | acma

PrivacyThe Privacy Act 1988 imposes obligations on the ACMA in relation to the collection, security, quality, access, use and disclosure of personal information. These obligations are detailed in the Australian Privacy Principles that apply to organisations and Australian Government agencies from 12 March 2014.

The ACMA may only collect personal information if it is reasonably necessary for, or directly related to, one or more of its functions or activities.

The purposes for which personal information is being collected (such as the names and contact details of submitters) are to:> contribute to the transparency of the consultation process by clarifying, where

appropriate, whose views are represented by a submission > enable the ACMA to contact submitters where follow-up is required or to notify

them of related matters (except where submitters indicate they do not wish to be notified of such matters).

The ACMA will not use the personal information collected for any other purpose, unless the submitter has provided their consent or the ACMA is otherwise permitted to do so under the Privacy Act.

Submissions in response to this paper are voluntary. As mentioned above, the ACMA generally publishes all submissions it receives, including any personal information in the submissions. If a submitter has made a confidentiality claim over personal information which the ACMA has accepted, the submission will be published without that information. The ACMA will not release the personal information unless authorised or required by law to do so.

If a submitter wishes to make a submission anonymously or through use a pseudonym, they are asked to contact the ACMA to see whether it is practicable to do so in light of the subject matter of the consultation. If it is practicable, the ACMA will notify the submitter of any procedures that need to be followed and whether there are any other consequences of making a submission in that way.

Further information on the Privacy Act and the ACMA’s privacy policy is available at www.acma.gov.au/privacypolicy. The privacy policy contains details about how an individual may access personal information about them that is held by the ACMA, and seek the correction of such information. It also explains how an individual may complain about a breach of the Privacy Act and how the ACMA will deal with such a complaint.

acma | 19

Appendix A—Findings of the monitoring As indicated above, the ACMA has developed a suite of metrics that monitor different but inter-related aspects of the intended licensee response to the introduction of higher licence taxes based on OC. The various metrics are outlined below, including their rationale and the aspect of intended licensee response which they inform. The findings of the monitoring analysis undertaken to date are also detailed. The focus is on interpreting the data to determine impacts on licence demand and congestion since the introduction of a licence tax based on OC principles in August 2012. The results of the monitoring provide critical input to a broader consideration of the ‘need’ for a second increase in the licence tax, applicable to the high density areas of the 400 MHz band.

The number of licences and assignmentsThe ACMA had compiled two stock-based metrics in the high density areas of the 400 MHz band—the number of licences at each month end and the number of assignments at each month end. Monitoring these related metrics over time informs the aggregate level of demand for spectrum (represented by the number of licences or assignments). As such, these metrics capture the net effect of various demand-related responses to the higher licence tax rate.

The earliest monthly data available for the licence metric relates to June 2012 (just preceding the licence tax increase) and for assignments relates to August 2012 (coinciding with the licence tax increase). Licensees are only exposed to the higher licence tax as their current licence expires and they are issued with an invoice for a new licence. Therefore, the impact on assignments from the licence tax increase is unlikely to have been front-loaded into August 2012, especially given that the main impetus for consideration of continuing the licence relates to receipt of a licence renewal notice which, for individual licensees, happens across the year.

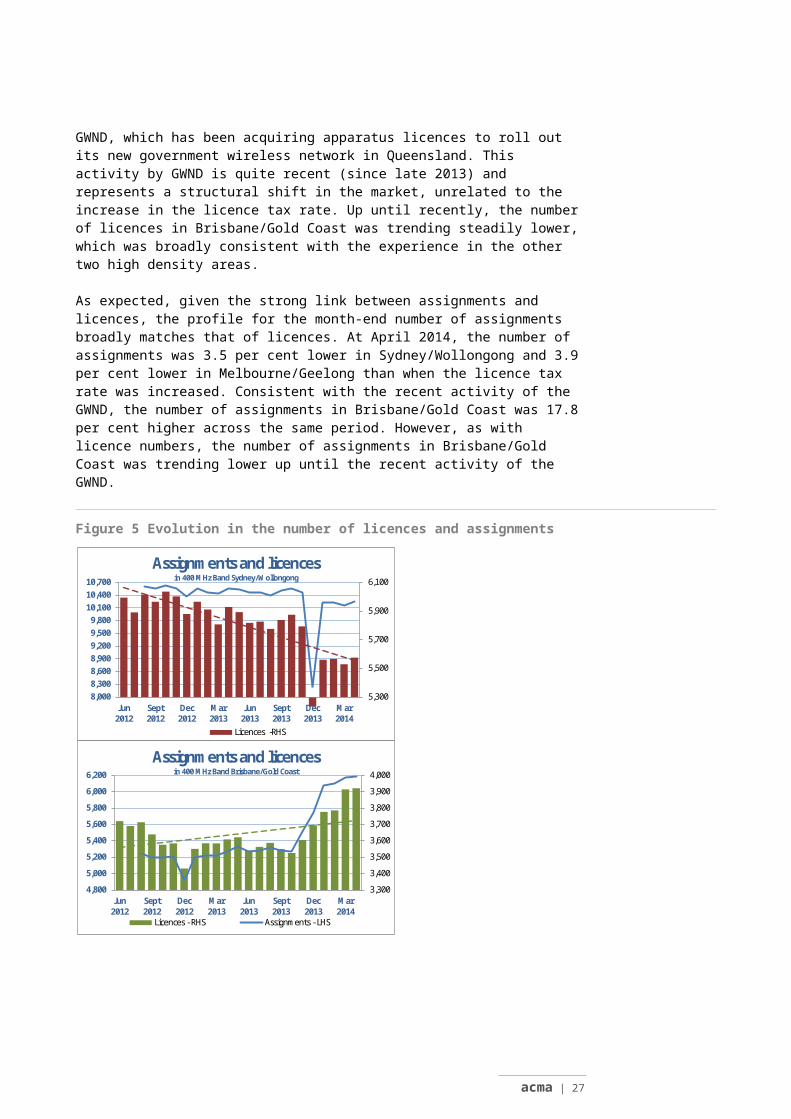

The number of licences at month-end has generally declined steadily since the introduction of the higher OC-based licence tax. This is quite clear in both Sydney/Wollongong and Melbourne/Geelong where the number of licences is now 6.0 per cent and 7.3 per cent lower respectively than when the licence tax rate was increased. In Brisbane/Gold Coast the response to the higher licence tax rate is masked by the emergence of the GWND, which has been acquiring apparatus licences to roll out its new government wireless network in Queensland. This activity by GWND is quite recent (since late 2013) and represents a structural shift in the market, unrelated to the increase in the licence tax rate. Up until recently, the number of licences in Brisbane/Gold Coast was trending steadily lower, which was broadly consistent with the experience in the other two high density areas.

As expected, given the strong link between assignments and licences, the profile for the month-end number of assignments broadly matches that of licences. At April 2014, the number of assignments was 3.5 per cent lower in Sydney/Wollongong and 3.9 per cent lower in Melbourne/Geelong than when the licence tax rate was increased. Consistent with the recent activity of the GWND, the number of assignments in Brisbane/Gold Coast was 17.8 per cent higher across the same period. However, as with licence numbers, the number of assignments in Brisbane/Gold Coast was trending lower up until the recent activity of the GWND.

20 | acma

Figure 5 Evolution in the number of licences and assignments

5,300

5,500

5,700

5,900

6,100

8,0008,3008,6008,9009,2009,5009,800

10,10010,40010,700

Jun2012

Sept2012

Dec2012

Mar2013

Jun2013

Sept2013

Dec2013

Mar2014

Assignments and licencesin 400 MHz Band Sydney/Wollongong

Licences -RHS

3,300

3,400

3,500

3,600

3,700

3,800

3,900

4,000

4,800

5,000

5,200

5,400

5,600

5,800

6,000

6,200

Jun2012

Sept2012

Dec2012

Mar2013

Jun2013

Sept2013

Dec2013

Mar2014

Assignments and licencesin 400 MHz Band Brisbane/Gold Coast

Licences - RHS Assignments - LHS

4,300

4,400

4,500

4,600

4,700

7,000

7,250

7,500

7,750

8,000

8,250

8,500

Jun2012

Sept2012

Dec2012

Mar2013

Jun2013

Sept2013

Dec2013

Mar2014

Assignments and licencesin 400 MHz Band Melbourne/Geelong

Licences-RHS Assignments-LHS

13,500

13,700

13,900

14,100

14,300

14,500

22,000

22,500

23,000

23,500

24,000

Jun2012

Sept2012

Dec2012

Mar2013

Jun2013

Sept2013

Dec2013

Mar2014

Assignments and licencesin 400 MHz Band all High Density Areas

Licences - RHS Assignments-LHS

Source: ACMA analysis

It is apparent from the charts above that there are seasonal impacts on the stock of licences and assignments around calendar year-end. These impacts result in a sharper than trend decline in the number of licences/assignments in December, followed by a rebound in January and continued increases over immediate months. This seasonal impact is mirrored in the monthly profiles around lapsed/surrendered licences and new licences (see sections below).

The declines experienced to date for both licences and assignments appear minor relative to both the stock of licences and assignments in each high density area, the extent of apparent congestion, and as a response to the signalled higher licence tax rate. This suggests that further increases in the licence tax rate are likely to be required before congestion is adequately relieved.

Move from 25 kHz to 12.5 kHz equipmentAs indicated above, another critical aspect of intended congestion alleviation is for licensees to re-channel their spectrum use from 25 kHz to 12.5 kHz, thus reducing their aggregate demand for spectrum. This metric indicates whether licensees have moved from less spectrally efficient equipment that enables channelisation at 25 kHz to more spectrally efficient equipment that enables channelisation at 12.5 kHz. Such re-channelisation is now a regulatory requirement for licensees in the high density areas of the 400 MHz band. It is actively being monitored by the ACMA as part of its broader regulatory focus on the 400 MHz band. In this monitoring context, this metric captures re-channelisation as a reduction in demand for spectrum. In effect, it complements the licence/assignment data which does not recognise a move to narrower channel bandwidth as a reduction in demand. In other words, the number of licences does not reduce if a licensee replaces 25 kHz channelisation with 12.5 kHz, even though the aggregate spectrum demanded (in this example) is halved.

acma | 21

Monthly data has been compiled since October 2012, soon after the licence tax was increased. This data has been compiled on an aggregated basis for all high density areas combined, rather than separately for each high density area.

The charts show that re-channelling has experienced a step-increase after the combination of regulatory change and licence tax increase. The number of licensees implementing finer channels has risen from 8,709 licensees at October 2012 to 11,650 licensees at March 2014. At October 2012, 57.5 per cent of licensees had implemented channels finer than 25 kHz. By March 2014, this had risen to around four-fifths (80.1 per cent).

Figure 6 Transition to narrowband

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Oct-2012 Feb-2013 Jun-2013 Oct-2013 Feb-2014

Evolution of re-channelling

Below 25 kHz At 25 kHz 40%

50%

60%

70%

80%

Oct-2012 Feb-2013 Jun-2013 Oct-2013 Feb-2014

Transition to narrowbandBelow 25 kHz

Source: ACMA analysis

The analysis shows that re-channelisation is well underway and has accelerated since the combination of regulatory requirement and the licence tax increase. Around one-quarter (23.7 per cent) of licences are yet to re-channel, which suggests significant scope for further re-channelisation. This also suggests that implementing a second licence tax rate increase is justified.

Aggregate spectrum demandThis metric essentially monitors the amount of bandwidth actually used by licensees each month. As such, this metric captures, in a single demand proxy, two desirable demand-related responses: first, a reduction in the number of licences held and secondly, a reduction in the amount of spectrum authorised under each licence, which declines with re-channelisation. Monthly data has been captured since October 2012.

This monitoring exercise is focused on the trend movement in this metric rather than implementing a precise estimate of spectrum use (demand), contrasted with a precise estimate of spectrum supply. Again, over time, this metric may initially decline, as re-channelling impacts and as some licensees exit. However, as new licensees enter and re-use freed-up spectrum, this metric may commence rising. Such a rebound in use is consistent with a rotation from low to high-value uses. Moreover, it is a positive outcome as the ACMA does not want to relieve congestion by stifling spectrum use to such an extent that oversupply emerges. This would not be consistent with the Act or the principles.

This metric indicates that overall demand for spectrum has declined steadily across the period since the tax increase (that is, since October 2012), reflecting reductions in the aggregate number of licences and re-channelling. Overall, spectrum demand has fallen by 20.9 per cent since October 2012.

22 | acma

Figure 7 Aggregate spectrum demand (kHz)

0

50,000

100,000

150,000

200,000

250,000

Oct-2012 Feb-2013 Jun-2013 Oct-2013 Feb-2014

Indicative aggregate demand (kHz)

RIOs Government Non-governmentSource: ACMA analysisNote: Data for rail industry organisations (RIO’s) were only separately compiled from August 2013.

The aggregate demand analysis essentially reconfirms the findings around the stock of licences/assignments and re-channelisation. Overall, this suggests that reductions in demand are underway but further increases in the licence tax rate are likely to be required before congestion is adequately relieved. On this basis, implementing the second tax increase is justified.

Lapsed and surrendered licencesAs the signalled higher licence tax rate is implemented, users with low-value uses will find it increasingly unviable to persist in using spectrum, as their net value from spectrum use becomes negative or as substitute inputs to spectrum become more cost-effective. The consequent effective reduction in spectrum demand is an important aspect of the desired rotation from low-value to high-value uses of spectrum. Without this intended exit of low-value uses, there would be no scope to transfer this spectrum to higher value uses. Although surrendering a licence and allowing it to lapse are different mechanisms for discontinuing licences13, they both implicitly relate to a considered view by licensees that the higher OC-based licence tax makes their continuing spectrum use less cost-effective or potentially unviable. Those licensees that surrender licences, or allow them to lapse, reveal that the use of the spectrum is low value relative to the new OC-based licence tax being progressively implemented. As such, this is a critical precondition (by freeing up spectrum) of the intended rotation from low-value uses to high-value uses. Given the similarity of economic response implied in both surrendering and lapsing licences, they have been aggregated into a single metric for this monitoring. The exit of current low-value spectrum licensees is captured in monthly data on the number of surrendered licences and lapsed licences.

Putting aside the year-end spikes in both December 2012 and December 2013, there is no obvious trend in the monthly number of lapsed/surrendered licences. The

13 Surrendering a licence means the licensee notifies the ACMA that it does not intend to use the relevant spectrum for the remainder of the effective licence period. This attracts a refund from the ACMA for the balance. Allowing a licence to lapse means that the licensee does not seek renewal of the licence after a licence period expires.

acma | 23

evolution of lapsed/surrendered licence numbers is partly driven by the timing of renewal and by the proximity of the replacement of new equipment.

Figure 8 Monthly lapsed/surrendered licences by high density area

-

100

200

300

400

500

600

700

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Sydney/Wollongong─lapsed/surrenderedMonthly number of licences

-

50

100

150

200

250

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Brisbane/Gold Coast─lapsed/surrenderedMonthly number of licences

-

50

100

150

200

250

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Melbourne/Geelong─lapsed/surrenderedMonthly number of licences

-

100 200 300 400 500 600 700 800 900

1,000

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

All HDAs─lapsed/surrenderedMonthly number of licences

Source: ACMA analysis

It appears that the combination of regulatory change (because of the implementation of the 400 MHZ review) and the licence tax increase is providing an incentive for licensees to relinquish some licences. At this stage, there is no clear evidence that the rotation out of low-value uses is complete or that congestion has been removed. This implies further increases in the licence tax may be the appropriate incentive for licensees move out of low-value uses.

New licencesThe exit licensees from low-value uses creates the scope for those with higher value uses to enter and encounter the new OC-based licence tax rate. These new entrants are reveal themselves as having positive (expected) values from use at or above the new OC-based licence tax rate, otherwise they would not enter. This represents the second stage of the desired rotation of spectrum from low-value uses to high-value uses. The entry of expected high-value spectrum licensees is captured in data on the number of new licences issued each month.

The second stage of the desired rotation of licensees is for new licensees to take out licences in the spectrum freed up by licence surrenders/lapses. Licensees entering at this stage reveal that their expectations around their value of spectrum use is clearly positive at the higher licence tax and presumably at the expected end-point licence tax rate based on their expectations around the tax glide path.

The number of new licences has been gradually trending down since the higher licence tax was implemented. A seasonal spike in new licences in both January 2013 and January 2014 is quite evident. This is consistent with the spike in exits

24 | acma

(lapsed/surrendered) each December, freeing up spectrum which is quickly taken up by licensees with high-value uses who have been previously denied spectrum.14

Figure 9 Monthly new licences by high density area

-

100

200

300

400

500

600

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Sydney/Wollongong─new licencesMonthly number of licences

-

50

100

150

200

250

300

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Brisbane/Gold Coast─new licencesMonthly number of licences

- 20 40 60 80

100 120 140 160 180 200

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Melbourne/Gold Coast─new licencesMonthly number of licences

-

100 200 300 400 500 600 700 800 900

1,000

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

All HDAs─new licencesMonthly number of licences

Source: ACMA analysis

At this stage, there is no clear evidence that the rotation into high-value uses represented by new licences is complete. This may suggest that ongoing congestion is limiting entry of high-value uses. It may also imply that further increases in the licence tax may be appropriate to encourage the exit of low-value uses, which frees up spectrum to accommodate the entry of high-value uses.

14 An alternate explanation may reflect seasonal factors related to calendar year end.

acma | 25

Appendix B—Long-term tax signalsSpectrum is typically blended with long-life network assets and other non-spectrum inputs to provide services.15 As a result, the efficient price of spectrum must incorporate signals to encourage long-term efficient use of both spectrum and complementary network assets and other non-spectrum inputs. This also means that licensees will react to the long-term price of spectrum rather than just focussing on the current price. Licensees will then assimilate information about the long-term OC-based price of spectrum and market-based prices of network assets and other non-spectrum inputs. They will also use the most efficient long-term combination of spectrum, network assets and other non-spectrum inputs.

This long-term price of spectrum is not normally known with certainty, so licensees typically must factor in their best expectations when considering their spectrum access and inter-related network capital expenditure (capex) decisions. In this context, however, the ACMA has provided strong guidance about the forward profile of the licence tax over at least a five-year horizon. Decisions by spectrum users to continue or commence spectrum licences will nevertheless remain inextricably linked with investment decisions around complementary assets. As a result, a mature response to higher licence taxes may take some time to become apparent.

Depending in part on the capex cycle duration and their stage within that, licensees will progressively begin reacting to the long-term signals implied by the glide path of intended OC-based tax rates. Altering the strongly signalled glide path by not implementing all five ‘planned’ tax increases introduces uncertainty and distorts the long-term signal component in the licence tax rate.16

Further, there may licensees that have vacated spectrum anticipating the licence tax to increase to its expected year-five rate (where the full OC-based tax rate plus cumulative CPI would be effective) making their use of the spectrum unviable. These licensees could be concerned if (for instance) the third, fourth and/or fifth increases were not actually implemented for some reason.

This suggests that considerable care needs to be taken if the potential increments for the licence tax, signalled to current and potential licensees, are not to be fully implemented. This recognises there is a trade-off between providing robust forward signals about long-term spectrum licence tax rates and ensuring that the licence tax rate is not increased beyond that necessary to relieve congestion and achieve equilibrium. The ACMA is well aware of this trade-off.

In this particular context, the forward signal that the ACMA has sent to licensees is that the licence tax rate will be increased progressively towards the estimated OC rate (plus cumulative CPI). However, if the desired objectives (removal of congestion and rotation of use to higher value uses) are achieved and appear durable, prior to reaching the estimated OC rate, further increases will not be necessary.17 As such, commercial views about the long-term evolution of the licence tax rate need to

15 These network assets and other non-spectrum inputs are complementary to spectrum in the sense that provision of the final service could not be facilitated with spectrum (input) alone.16 That is, the forward signal about the likely evolution of spectrum licence tax rates and thus the long-term price of spectrum.17 This reflects the view that introducing licence tax rates based on OC principles is not an end in itself but merely a means of achieving more efficient use of spectrum. If this can be achieved without calibrating the licence tax rate to an estimated OC level, there is no need to further adjust the licence tax rate.

26 | acma

incorporate potential for the licence tax rate to stabilise at a point below the ACMA’s current best view about OC.

However, the monitoring analysis is complicated by the fact that licensees (whether exiting or entering the spectrum market) will be responding in large part to their view of the expected long-term licence tax rate, rather than the licence tax rate effective at any point in time (the short-term licence tax rate).

Reflecting this, the response achieved at any point in time (for example, after the first increase but before any subsequent signalled increases) is driven by the long-term licence tax rate rather than the short-term licence tax rate effective at that time. Therefore, even if congestion was fully removed after the first licence tax rate increase, it would not be possible to analytically conclude that congestion had been removed because of the second increase (that is, the short-term licence tax rate) and that further increases were unnecessary.

On this basis, it will be difficult to determine categorically that the long-term licence tax rate is inappropriate until after licensees have fully adjusted to the long-term licence tax rate. As indicated above, the response time for licensees is inextricably linked to their capex cycle, which is inevitably long-term given the long expected useful lives of spectrum-complementary assets.

After the mature response to the long-term licence tax rate has emerged, it will be possible to confirm whether congestion has been removed and whether further adjustment (to the long-term licence tax rate) is required. Effectively, this means continuing with the signalled licence tax rate increases and reviewing their efficiency in addressing congestion, after all licensees have had sufficient time to adjust.

The focus of annual monitoring is to proactively monitor responses to the increased long-term licence tax rate to ensure that adjustments are more evolutionary than sharp. A situation where lapsed/surrendered licensees largely matched new licences (both month-to-month and on an aggregate period-to-date basis) would indicate an orderly response to the long-term licence tax rate was occurring.

In this situation, the response was consistent with expectations and all signalled increases to the licence tax rate should occur. If, however, lapsed/surrendered sharply accelerated and significantly outnumbered new licences on a sustained basis, it may be possible to discern that the signalled long-term licence tax rate was too high. On that basis, discontinuing (or pausing) the signalled licence tax rate increases may be appropriate, on the basis that the long-term licence tax rate was too high.

acma | 27

Appendix C—Summary of proposed changes to Licence Tax DeterminationsThe tables below summarise the proposed changes to the taxes per kHz for the high and remote density areas of the 400 MHz band in Tables 202, 302, 402 and 502 of the Transmitter Licence Tax Determination and tables 202 and 302 of the Receiver Licence Tax Determination.

High density areas

Table 1 Summary of proposed changes to Licence Tax Determinations

Radiocommunications (Transmitter Licence Tax) Determination 2003 (No. 2)High density area annual licence tax rate ($ per kHz)

>403–520 MHz Currently effective as from 5 April 2014 After implementation of opportunity costTable 202 1.6468 1.8938Table 302 121.7524 140.0153Table 402 30.4381 35.0038Table 502 121.7524 140.0153Radiocommunications (Receiver Licence Tax) Determination 2003 (No. 2)

High density area annual licence tax rate ($ per kHz)>403–520 MHz Currently effective as from 5 April 2014 After implementation of opportunity costTable 202 1.6468 1.8938Table 302 30.4381 35.0038

Remote density areas

Table 2 Summary of proposed changes to Licence Tax Determinations

Radiocommunications (Transmitter Licence Tax) Determination 2003 (No. 2)Remote density area annual licence tax rate ($ per kHz)

>403–520 MHz Currently effective as from 5 April 2014 After implementation of opportunity costTable 202 0.0558 0.0000Table 302 4.1189 0.0000Table 402 0.7183 0.0000Table 502 2.8367 0.0000Radiocommunications (Receiver Licence Tax) Determination 2003 (No. 2)

Remote density area annual licence tax rate ($ per kHz)>403–520 MHz Currently effective as from 5 April 2014 After implementation of opportunity costTable 202 0.0558 0.0000Table 302 0.7183 0.0000

28 | acma