ieej outlook 2018 - international energy forum - ief · ieej outlook 2018 – prospects and...

TRANSCRIPT

IEEJ

Out

look

201

8

IEEJ

© 2

017

The 427th Forum on Research Work

IEEJ Outlook 2018 – Prospects and challenges until 2050 – Tokyo, 12 October 2017 The Institute of Energy Economics, Japan

Energy, Environment and Economy

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Overview of the current global energy market

2

• Although the trend of Asia as leading the global energy market remains unchanged, developments in the US and China, which accounts for 40% of the energy market, must be carefully monitored.

• World coal demand dropped for two years in a row (US and China largely) while oil and gas grew. China’s coal consumption declined for the third consecutive year (2016, BP).

• Discussions on Peak Oil (supply) of the 2000s are now changing to Peak Demand. Note the recent movements that aim to ban the sale of internal combustion engine vehicles.

• CO2 emissions dropped in 2015 but increased again in 2016. India and ASEAN showed big increases despite the declined observed in the US and China.

• Paris Agreement calls for “Long-term low greenhouse gas emission development strategies” by 2020. This Outlook expands its estimation period to 2050.

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Scenarios in this Outlook

3

<Energy Model Analysis> #Reference Scenario Reflects past trends with current energy and environment policies. Does not reflect any aggressive policies for low-carbon measures. #Advanced Technologies Scenario Assumes the introduction of powerful policies to enhance energy security and address climate change issues. It promotes utmost penetration of low-carbon technologies. #Oil Demand Peak Case Assumes a more rapid introduction of electric drive vehicles than in the reference scenario, to analyze the possibilities of oil demand peak. *1 ZEV: battery electric vehicles, plug-in hybrid electric vehicles and fuel cell battery vehicles

*2 CCT: ultra super critical, advanced-USC and integrated coal gasification combined cycle

❖Examples for Technology

<Climate Model Analysis> #Reference: Emissions path with continuing past trends #Minimizing Cost: Emissions path with minimizing total cost #Halving Emissions by 2050: Emissions path reflected RCP2.6 in AR5 by IPCC

Reference Advanced Technologies

Peak Oil Demand

Ener

gy e

ffic

ienc

y Vehicle technology (ZEV*1 sales share)

9% in 2030 20% in 2050

21% 43%

30% 100%

Coal-fired power generation (CCT*2 share in newly installed capacity)

30% in 2030 90% in 2050

70% 100%

Same as Reference

Carb

on fr

ee

tech

nolo

gy Installed capacity

Solar PV Wind Nuclear

(2015 to 2050) 0.2 to 1.5 TW 0.4 to 1.9 TW 0.4 to 0.6 TW

(2050) 2.5 TW 3.0 TW 1.0 TW

Thermal power generation with CCS (Only countries and regions with CO2 storage potential excluding aquifers)

none Newly installed after 2030

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Energy Outlook up to 2050

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

0

50

100

150

200

250

1990 2000 2010 2020 2030 2040 2050

Y2015=100-250 250 750

China

India

ASEAN

Other Asia

*MENA

**SS Africa

Latin America

Europe

Intl. bunkers

OECDN

on-O

ECD

2015-20302030-2050

Mtoe

Energy market shifting to southern Asia

Despite large improvements in energy efficiency/intensity, global energy demand continues to increase. Two thirds of the energy growth comes from non-OECD Asia. As China peaks during the 2040s, the center of gravity of the market shifts within Asia towards the south.

5

❖ Global Population, GDP and Energy ❖ Growth in Primary Energy

255

145

132

GDP

Energy

Population

<Reference>

* Middle East and North Africa, **Sub-Saharan Africa

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Demand led by fuels for Generation & Transport

Three quarters of the growth until 2050 are for fuels for power generation and transportation. The economic development and improvements in living standards of the relatively poor and populous areas – non-OECD Asia – contribute to the global energy expansion.

6

❖ Electricity ❖ Oil fuels for vehicles

<Reference>

7.0

2.83.8

1.62.2

8.6

-10

-8

-6

-4

-2

0

2

4

6

8

10

0

2

4

6

8

10

12

Chin

a

Indi

a

ASEA

N

Oth

er A

sia

Oth

erN

on-O

ECD

OEC

D

PWh

MWh/p

Growth in 2015-2050

Electricity demand per capita

0.320.19

0.26

0.070.15

0.70

-1.2

-0.8

-0.4

0.0

0.4

0.8

-8

-4

0

4

8

12

16

20

Chin

a

Indi

a

ASEA

N

Oth

er A

sia

Oth

erN

on-O

ECD

OEC

D

Mb/d

unit/p

Growth in 2015-2050

Vehicle ownership per capita

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

21.2

32.9

44.1

0

10

20

30

40

50

1990 2010 2030 2050

GtCO2

13.6

19.8

0

5

10

15

20

2015 2050

Gtoe

-0.5 0.5 1.5 2.5

Coal

Oil

Natural Gas

Nuclear

Renewables Asia*

RoW**

Gtoe

High dependence on fossil fuels continues

Sixty percent of the growth in electricity demand will be met by thermal power generation, especially natural gas. Asia leads the large global increase in fossil fuels required for power generation as well as for transportation. The high dependence on fossil fuels remains unchanged and energy related CO2 emissions increase by 34% by 2050.

7

❖ Growth in Primary Energy ❖ Energy-related CO2

<Reference>

❖ Energy Mix

* Non-OECD Asia, **Rest of the world

81%

79%

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

19.8

17.2

0

5

10

15

20

25

1990 2000 2010 2020 2030 2040 2050

Reference

Advanced Technology

Gtoe

elec.elec.

elec.

other fuels

other fuels

other fuels

genera-tion loss

transmission

losses*

-0.8 -0.6 -0.4 -0.2 0.0

Industry

Transport

Building

PowerGeneration

Gtoe

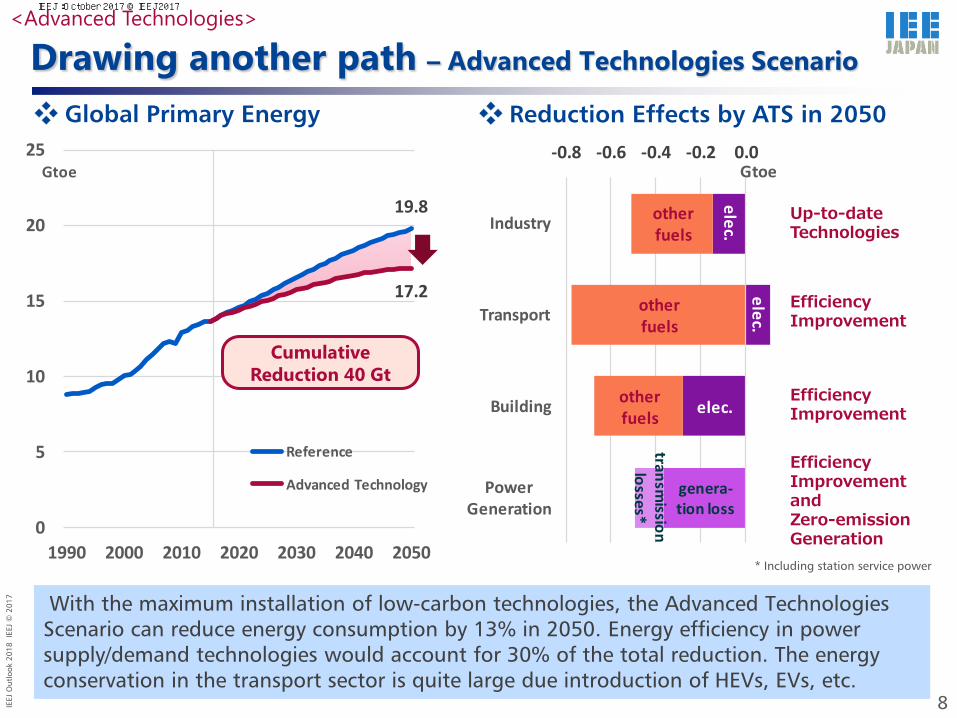

Drawing another path – Advanced Technologies Scenario

With the maximum installation of low-carbon technologies, the Advanced Technologies Scenario can reduce energy consumption by 13% in 2050. Energy efficiency in power supply/demand technologies would account for 30% of the total reduction. The energy conservation in the transport sector is quite large due introduction of HEVs, EVs, etc.

8

❖ Global Primary Energy ❖ Reduction Effects by ATS in 2050

Up-to-date Technologies

Efficiency Improvement

Efficiency Improvement and Zero-emission Generation

* Including station service power

Cumulative Reduction 40 Gt

<Advanced Technologies>

Efficiency Improvement

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

0

10

20

30

40

50

Reference ATS

2015 2050

PWh

10%

28%47%

0

2

4

6

8

10

12

14

Reference ATS

2015 2050

VRE*

Other RE

Hydro

Nuclear

Gas

Oil

Coal

TW

Zero-emission Generation occupies two thirds

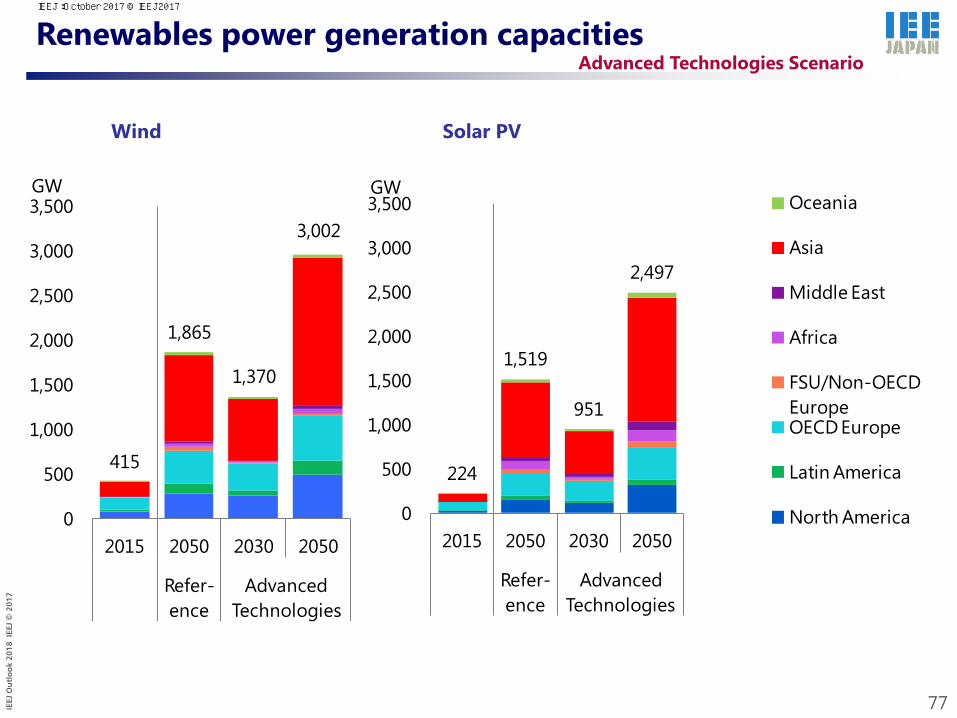

ATS slows the growth in electricity demand from 1.8 times in the reference, down to 1.6 times. In ATS, non-fossil power generation accounts for 60% and zero-emission generation, including thermal generation with CCS represents two thirds (that’s half today’s CO2 emissions per unit of generation). Half of the total power capacity will be comprised of intermittent renewable energy, which needs to further reduce costs and enhance grid stability.

9

❖ Global Power Generation ❖ Global Power Capacity

* Variable Renewable Energy includes solar PV, CSP, wind and marine.

66% 62%

38%

34%

60%

6%

Non-fossil

Fossil with CCS

Fossil

34%

<Advanced Technologies> IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

0

1

2

3

4

5

6

1990 2000 2010 2020 2030 2040 2050

Gtoe

Oil

Coal

Nuclear

Renewables

Gas

Genera-tion

Genera-tion

Genera-tion

Genera-tion

Trans-port

-2 -1 0 1

Coal

Oil

Gas

Nuclear

Renewables

Gtoe

Coal falls significantly and below renewables

In ATS, coal starts to decline from now and is surpassed by renewables around 2040, due mainly to energy efficiency and the elimination of emissions in the power supply/demand sectors. Despite large decline in transportation fuels, oil does not reach a peak. Fossil fuels share of the total in 2050 is reduced to 68%, from 79% in the reference case. It is still a high level of dependence. 10

❖ Primary Energy ❖ Effects by ATS in 2050

(solid line: ATS, dotted line: Reference)

<Advanced Technologies> IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

11

CO2 emissions peak in the middle of 2020s

Energy-related CO2 emissions in ATS decline after 2020s but are still very far from reaching half of current levels by 2050. Efficiency is the most contributor for CO2 reductions from the reference. Two thirds of the total reductions are electricity-related technologies, including non-fossil power, thermal power with CCS and energy efficiency in power supply/demand.

❖ Energy-related CO2 Emissions ❖ Reductions by technology

…… -6.2 Gt

…… -0.4 Gt

…… -2.2 Gt

-14.4 Gt

…… -3.6 Gt

…… -0.5 Gt

…… -1.5 Gt

<Advanced Technologies>

44

30

33

10

20

30

40

50

1990 2000 2010 2020 2030 2040 2050

GtCO2Energy Efficiency

Biofuels

Wind, Solar, etc.

Nuclear

Fuel Switching

CCS

Reference

ATS

Halve

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Ultra-long-term Climate Analysis

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

13

Rule for ultra long-term: Reduce the total cost

Without measures against climate change, the mitigation cost is small, while the adaptation and damage costs become substantial. Aggressive mitigation measures on the other hand, would reduce the adaptation and damage costs but the mitigation costs would be notably colossal.

The climate change issue is a long-term challenge influencing vast areas over many generations. As such, and from a sustainability point of view, the combination (or the mix) of different approaches to reduce the total cost of mitigation, adaptation and damage is important.

❖ Mitigation+Adaptation+Damage=Total Cost ❖ Illustration of Total Cost for Each Path

Mitig

ation

•Typical measures are GHG emissions reduction via energy efficiency and non-fossil energy use. • Includes reduction of GHG release to the atmosphere via CCS • These measures mitigate climate change.

Ad

aptatio

n

•Temperature rise may cause sea-level rise, agricultural crop drought, disease pandemic, etc. • Adaptation includes counter measures such as building banks/reservoir, agricultural research and disease preventive actions.

Dam

age

If mitigation and adaptation cannot reduce the climate change effects enough to stop sea-level rise, draught and pandemics, damage will take place.

パス①

緩和過小

適応大

被害大

パス②

緩和中庸

適応中

被害中

パス③

緩和過大

適応小

被害小

緩和費用

適応費用

被害額

総合コストMitigation Cost Adaptation Cost Damage Value

Total Cost

Mitigation Adaptation Damage

Too Small

Big

Big

Reasonable

Medium

Medium

Too Big

Small

Small

Path 1 Path 2 Path 3

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Minimizing Total Cost in IAM* *Integrated Assessment Model

Total cost of “Minimizing Cost” is half of the reference. In 2150, GHG emissions decrease by 80% from now and temperature rises by 2.6 °centigrade from the late 19th century. In “Halving Emissions by 2050“, temperature peaks at 2100, resulting in 1.7°C in 2150. However, total cost is 20% higher than the reference and double of the “Minimizing Cost“ path.

14

❖ GHG Emissions ❖ GHG Concentrations (incl. aerosol etc.)

❖ Temperature Rise (vs. 1850-1900)

❖ Total Cost (cumulative present value*)

*cumulating 2015 to 2500

*Emissions path reflected “RCP 2.6” in the 5th Assessment Report (AR5) by the Intergovernmental Panel on Climate Change (IPCC).

0

20

40

60

80

2000 2050 2100 2150

GtCO2eq

Reference Minimizing Cost Halving Emissions by 2050*

0

200

400

600

800

1,000

2000 2050 2100 2150

ppm CO2eq

0.0

1.0

2.0

3.0

4.0

2000 2050 2100 2150

°C

0

20

40

60

80

100

Mitigation Adaptation&Damage

Tril. $

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

-10

0

10

20

30

40

50

60

2000 2050 2100 2150 2200

reference high ECS low ECS

GtCO2-eq

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2000 2050 2100 2150 2200

reference high ECS low ECS

°C

-10

0

10

20

30

40

50

60

2000 2050 2100 2150 2200

reference high discount low discount

GtCO2-eq

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2000 2050 2100 2150 2200

reference high discount low discount

°C

Still large uncertainties in the climate analysis

15

❖ GHG emissions and temperature rise using different discount rates (minimizing cost)

Discount rate This model uses 2.5%. There are a range of 1.1 to 4.1% summarized by AR5.

Equilibrium Climate Sensitivity (ECS) This model uses 3 degree. According to AR5, high possibility that ECS is between 1.9 and 4.5 degree.

1.4 °C difference

Note: A parameter indicating how many degrees centigrade the temperature will rise when the atmospheric greenhouse gas concentration (CO2 equivalent concentration) doubles.

Note: The value used when converting future value (income and expenditure) into current value. The lower discount rate tends to raise emphasis of adaptation and damage, and strengthen the latest GHG reduction. The higher discount rate raises emphasis of mitigation costs and delays GHG reduction efforts. Although it changes every year in the model analysis, it is represented by the average value in 2015 to 2300 here.

❖ GHG emissions and temperature rise using different ECS (minimizing cost)

1.3 °C difference

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Another path to “2°C target”

“2°C Minimizing Cost”, for example, is a path that minimize total cost under the condition of 2°C temperature rise in 2150. Its total cost is 20% higher than “Minimizing Cost” without the temperature limit. GHG emissions decrease by 30% in 2050 and needs almost zero-emissions after 2100. Temperature rises to just over 2°C in 2100 and then declines to 2°C.

16

❖ GHG Emissions ❖ GHG Concentrations (incl. aerosol etc.)

❖ Temperature Rise (vs. 1850-1900)

❖ Total Cost (cumulative present value*)

*cumulating 2015 to 2500

*Emissions path reflected “RCP 2.6” in the 5th Assessment Report (AR5) by the Intergovernmental Panel on Climate Change (IPCC).

0

20

40

60

80

2000 2050 2100 2150

GtCO2eq

Reference Minimizing Cost 2°C Minimizing Cost Halving Emissions by 2050*

0

200

400

600

800

1,000

2000 2050 2100 2150

ppm CO2eq

0.0

1.0

2.0

3.0

4.0

2000 2050 2100 2150

°C

0

20

40

60

80

100

Mitigation Adaptation&Damage

Tril. $

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Technology development for ultra long-term

17

Technologies Description Challenges Technologies to reduce CO2 emissions

Next Generation Nuclear Reactors

Fourth-generation nuclear reactors such as ultra-high-temperature gas-cooled reactors(HTGR) and fast reactors, and small- and medium-sized reactors are now being developed internationally.

Expansion of R&D support for next generation reactors

Nuclear fusion reactor

Technology to extract energy just like the sun by nuclear fusion of small mass number such as hydrogen. Deuterium as fuel exists abundantly and universally. Spent nuclear fuel as high-level radioactive waste is not produced.

Technologies for continuously nuclear fusion and confining them in a certain space, energy balance, cost reduction, financing for large-scale development and establishment of international cooperation system, etc.

Space Photovoltaic Satellite (SPS)

Technologies for solar PV power generation in space where sunlight rings abundantly above than on the ground and transmitting generated electricity to the earth wirelessly via microwave, etc.

Establishment of wireless energy transfer technology, reduction of cost of carrying construction materials to space, etc.

Technologies to sequestrate CO2 or to remove CO2 from the atmosphere

Hydrogen production and usage

Production of carbon-free hydrogen by steam reforming of fossil fuels and by CCS implementation of CO2 generated.

Cost reduction of hydrogen production, efficiency improvement, infrastructure development, etc.

CO2 sequestration and usage (CCU)

Produce carbon compounds to be chemical raw materials, etc. using CO2 as feedstocks by electrochemical method, photochemical method, biochemical method, or thermochemical method. CO2 can be removed from the atmosphere.

Dramatic improvement in quantity and efficiency, etc.

Bio-energy with carbon capture and storage (BECCS)

Absorption of carbon from the atmosphere by photosynthesis with biological process and CCS.

It requires large-scale land and may affect land area available for the production of food etc.

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

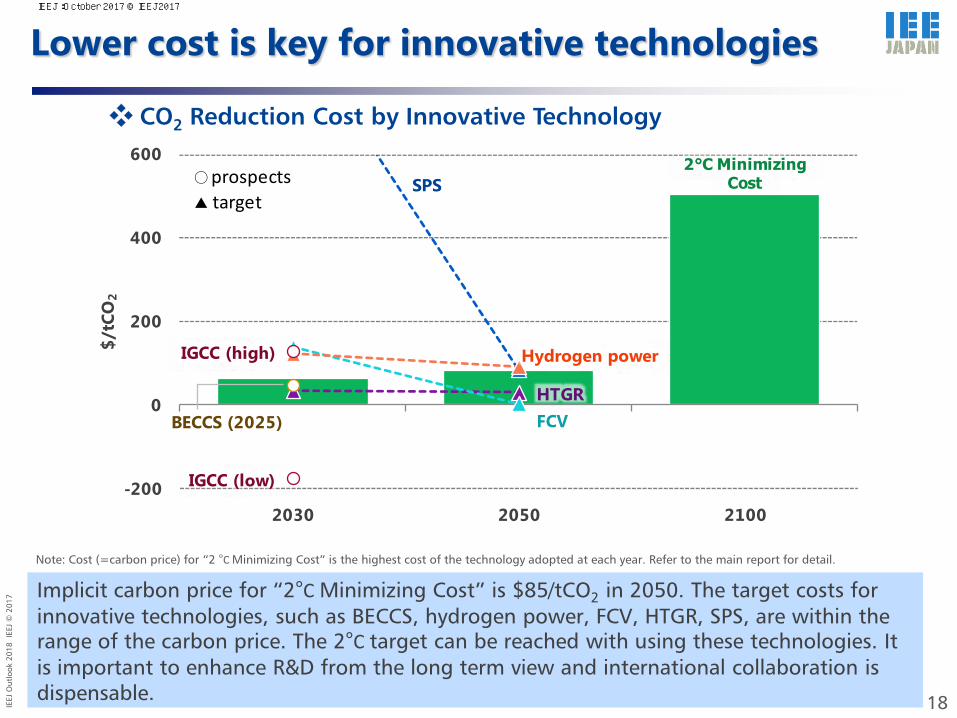

Lower cost is key for innovative technologies

Implicit carbon price for “2°C Minimizing Cost” is $85/tCO2 in 2050. The target costs for innovative technologies, such as BECCS, hydrogen power, FCV, HTGR, SPS, are within the range of the carbon price. The 2°C target can be reached with using these technologies. It is important to enhance R&D from the long term view and international collaboration is dispensable. 18

Note: Cost (=carbon price) for “2 °C Minimizing Cost” is the highest cost of the technology adopted at each year. Refer to the main report for detail.

❖ CO2 Reduction Cost by Innovative Technology

2°C Minimizing Cost

HTGRFCV

Hydrogen power

BECCS (2025)

IGCC (high)

IGCC (low)-200

0

200

400

600

2030 2050 2100

$/tC

O2

SPS○prospects▲ target

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Further CO2 reductions from ATS

19

❖ Energy-related CO2 Emissions

1) CO2 Free Hydrogen (refer to previous Outlook) • Hydrogen power 1 GW x 3000 units • Fuel cell vehicles 1 billion units (H2 demand of 800 Mt/yr corresponds 3 times of today’s LNG) 2) Negative-emission Technology • BECCS: Biomass power 0.5 GW x 2800 units (Fuel supply of 2000 Mtoe/yr needs land of 2.85 million km2) 3) Zero-emission Power and Factories with CCS -10 GtCO2 (Maximum reduction volume by substituting thermal power generation without CCS) • SPS: 1.3 GW x 2300 units or • HTGR: 0.275 GW x 8700 units or • Fusion reactor: 0.5 GW x 4500 units or • Thermal power with CCS: 2800 GW (Estimated CO2 storage potential is over 7000Gt) + -1 GtCO2 • CCS: Installed in 20% of factories and plants (iron & steel, cement, chemicals, pulp & paper, refinery and GTL/CTL)

❖ Examples of technologies needing further reductions

*Emissions path reflected “RCP 2.6” in the 5th Assessment Report (AR5) by the Intergovernmental Panel on Climate Change (IPCC).

44

30

19

10

20

30

40

1990 2010 2030 2050

Reference

ATSGtCO2

<Climate Analysis>●Minimizing Cost

● 2°C Minimizing Cost◆ Halving Emissions by 2050*

▲11Gt

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Peak Oil “Demand” Case

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Transport, especially cars, drives oil demand

About 70% of the increases in oil consumption until 2050 is for transport or petrochemical feedstocks. Road transport, in particular, may decide where the consumption will go.

21

⛽ Oil consumption [Reference Scenario] ⛽ Oil for Road [Reference Scenario]

Oil consumption by cars in OECD countries is decreasing and will be surpassed by non-OECD around 2020. Non-OECD accounts for all future consumption increases.

Others

Non-energy

use

Other transport30

40

4547

Road48

76

90

105114

122

0

20

40

60

80

100

120

2000 2015 2030 2040 2050

Mb

/d

21

19OECD

15

18

26Non-OECD

33

0

10

20

30

40

2000 2010 2020 2030 2040 2050M

b/d

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

The time for car electrification has come?

22

⛽ Selected recent movements by governments/assemblies and car makers A resolution to ban conventional car sales in the European Union by 2030 was passed by the Bundesrat of Germany (2016) Germany

The ruling and opposition parties proposed the abolition of conventional vehicles by 2025 (2016) Norway

The Government announced that it would ban conventional car sales by 2040 (2017)

France

The Government announced that it would ban conventional car sales by 2040 (2017)

United Kingdom

Minister said that all new car sales after 2030 would be electric vehicles (2017)

India

Deputy Minister mentioned that the ban on the sale of conventional vehicles was under investigation (2017) China

The target for FCV sales is more than 30,000/year in 2020 (2015). Reported of full-scale entry into EVs in 2020 (2016)

Announced the strategy to increase EV share in its total sales to 25% with more than 30 models of EVs by 2025 (2017)

Introducing 12 models of EVs by 2022. The target of 30% of its total sales as EVs (2017)

The plan to prepare EVs at all line up by 2020 (2015)

Announced that eco-cars combined with EVs and HEVs will be raised to 70% by 2025 (2017).

In 2030, two-thirds of automobile sales will be electrified. EVs will be released in China in 2018 (2017).

Toyota

Volkswagen

Renault-Nissan

Hyundai

Ford

Honda

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Oil peaks around 2030 with a rapid penetration of ZEVs

Oil consumption by cars in Non-OECD, which continues to increase rapidly in the Reference Scenario, also declines from around 2030. It is as much as one third of the Reference Scenario in 2050.

23

⛽ Oil consumption ⛽ Oil for Road [Peak Oil Demand Case]

In the Peak Oil Demand Case, oil consumption hits a peak of 98 Mb/d around 2030 before declining. The reduction from the Reference Scenario is 7 Mb/d and 33 Mb/d in 2030 and in 2050, respectively.

Note: Dotted lines are the Reference Scenario

8690

105

122

Advanced Technologies

9798

Peak Oil Demand

89

60

80

100

120

2010 2020 2030 2040 2050

Mb

/d

Reference

15

33

21

16

OECD5

18

22

Non-OECD

11

0

10

20

30

40

2000 2010 2020 2030 2040 2050M

b/d

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

While natural gas and coal increase, the petroleum product composition changes

As ZEVs demand for oil declines and electricity increases, the fuel required for power generation also increases. Both natural gas and coal exceeds oil by the late 2030s. Natural gas becomes the largest energy source thereafter.

24

⛽ Changes in consumption (from the Reference Scenario)

⛽ Composition of petroleum products consumption

Note: Excluding own use

Gasoline reduces its share from 27% to 10% in 2050. The share of diesel oil is not reduced as much because diesel oil has other uses. Diesel share in 2050 is 8 points lower than today.

-1,846

-1,596

432

572

-1,567

-83

409

-2,000 -1,000 0

(Mt)

Oil

Coal

Natural gas

Oil

Biomass

Electricity

CO

2Pr

imar

y co

nsu

mp

tio

nRo

ad

Mtoe

2030

2050

Dieseloil

35%34% 33%

Gasoline27%

25% 23%

34%27%

23% 10%

0%

20%

40%

60%

80%

100%

20152030205020302050

Reference Peak Oil Demand

LPG

Naphtha

Jet fuel

Kerosene

Heavyfuel oil

Others

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Crude oil production shifts towards low-cost regions...

Oil price falls due to the change in supply and demand pressure and market perception. Relative to the Reference Scenario (in $2016), prices drop from $95/bbl to $65/bbl in 2030 and from $125/bbl to $50/bbl in 2050. Given such drastic price decreases, regions with low production costs would be the only ones with potential for increases. Only the Middle East is expected to produce more in 2050 than today. North America production decreases by 40% from the Reference Scenario to 13 Mb/d.

25

⛽ Crude oil production [Peak Oil Demand Case]

28.8

9.9

17.113.8

7.2 8.4

33.7

10.7

18.4

13.8

6.9 6.9

37.3

9.213.0 11.5

6.2 5.3

32.4

42.0

11.313.6

21.6 21.9

14.5 15.0

8.812.4

7.4 7.2

0

10

20

30

40

Middle East Others North America Former Soviet Union

Latin America Asia

OPEC Non-OPEC

Mb

/d

2015 2030 2050 Reference

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

...but the economic downturn will affect the Middle East

Although the Middle East achieves a relative gain, the decrease in net oil export revenues is $1.6 trillion; a significant drop of 13% of nominal GDP. At the other end of the spectrum, India which is the second largest oil consumer, benefits the most with a decrease in net oil import costs. It is followed by China, in which more cars are on road than in any other countries. Despite its consumption scale, the United States faces little impact since it is almost oil self-sufficient.

26

⛽ Changes in net oil exports/imports and ratios to nominal GDP [2050]

Note: Europe excludes the former Soviet Union

0.0 0.5 1.0 1.5 2.0 2.5

United States

Japan

OECD Europe

China

India

Latin America

Former USSR

Middle East

Net

imp

ort

sN

et e

xpo

rts

$ trillion

ReferencePeak Oil Demand

Quantity effect

Price effectASEAN

India

Other Asia

Japan

Europe

ChinaOceania

United States

Africa

Latin America

Former USSR

Canada

Middle East

-15%

-10%

-5%

0%

5%

0 50 100 150C

han

ges

in n

et o

il ex

po

rt r

atio

to

n

om

inal

GD

PGD

PReal GDP ($2010 trillion)

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

Impact of less oil consumption diverges

Emission reductions in NOx and PM2.5, the major drivers behind car electrification, are 27% and 3%, respectively, compared to total emissions in 2010. Contribution to air quality in urban areas are expected.

27

⛽ Changes in emissions (from the Reference Scenario)

⛽ Excise taxes on gasoline and diesel oil for automobiles in OECD

Note: Automobile origin. Does not include effect on improvement of conventional automobile emission control performance

Revenues from excise taxes on automotive gasoline and diesel oil will be reduced significantly, unless tax regime changes. They may become financial issues similar to the subsidies for ZEVs at their promotion stage.

-5.4

-30.5

-40 -30 -20 -10 0

2030

2050

NO

x (M

t)

-0.2

-1.2

-1.5 -1.0 -0.5 0.0

2030

2050

PM2

.5 (M

t)

370

313

238270

79

0

100

200

300

400

2030 2050 2030 2050

2015 Reference Peak Oil Demand

$ b

illio

n

IEEJ:October 2017 © IEEJ2017

IEEJ

Out

look

201

8 IE

EJ ©

201

7

How do we recognise the rapid de-oiling?

28

The rising dependence on the Middle East crude oil will increase geopolitical risk for stable supply.

Although it is reasonable to expect that Governments in the Middle East would cut public investment and subsidies to reduce budget deficits while coping with low oil prices, it is difficult to deny the possibility of increasing social anxiety and of a worsening situation in the region.

The role of consuming countries as well as producing countries’ own efforts continue to be important. Support to the efforts represented by Saudi Arabia “Saudi Vision 2030“ is needed.

...and then

It should not be overlooked that in the Peak Oil Demand Case, oil remains required in 2050 on a scale that does not differ from today.

If the supply investment becomes insufficient due to excessive pessimism in the future , it can trigger the switching from oil to other energies threatening energy security.

The Peak Oil Demand Case shows that, under some circumstances, oil consumption can turn into a decline in the not too distant future,.

However, the feasibility of this Case can be said to be extremely challenging because the penetration of ZEVs is far greater than that in the “Advanced Technologies Scenario,” in which a bottom-up approach to the maximum implementation of advanced technologies is adopted. It can be said that oil consumption may not be so easily reduced, so quickly.

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Reference materials

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Geological coverage

• The world is geographically aggregated into 42 regions. • Especially the Asian energy supply/demand structure is considered in detail, aggregating the area into 15 regions.

- United States - Canada

North America

- Australia - New Zealand

Oceania - South Africa (Rep. of) - North Africa - Other Africa

Africa

-Saudi Arabia - Iran - Iraq - UAE - Kuwait - Qatar - Oman - Other Middle East

Middle East - Japan - China - India - Chinese Taipei - Korea - Hong Kong - Indonesia - Malaysia - Philippines - Thailand - Viet Nam - Singapore - Myanmar - Brunei Darussalam - Other Asia

- United Kingdom - Germany - France - Italy - Other OECD Europe

OECD Europe - Russia - Other FSU - Other Non-OECD Europe

Non-OECD Europe

- Mexico - Brazil - Chile - Other Latin America

Latin America

Asia

30

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Energy supply-demand model

World trade model

Computable general equilibrium model

Climate change model

Use the linear programming (LP) method to calculate the future international trade flows of crude oil, petroleum products, etc.

Estimate the economic impacts induced by the changes in energy supply and demand, based on input-output data.

Calculate future GHG concentration in the atmosphere, temperature rise, damage caused by climate change, etc.

Major assumptions

GDP, population, energy prices, exchange rates, international trade, etc.

Technology assessment model

Optimal power generation planning model

Calculate GDP-related indices, price indices, activity indices including material production, etc. consistently.

Use a bottom-up approach to calculate future efficiencies of appliances, vehicles, etc.

Calculate the cost-optimal power generation mix to meet the projected future electricity demand.

Econometric model to project future energy supply and demand by regression analysis of historical trends based on the energy balance tables data of the International Energy Agency (IEA). This model calculates energy demand, supply and transformation as well as related indices including CO2 emissions, CO2 intensities and energy self sufficiency ratios.

Experts’ opinions

Macroeconomic model

Modelling framework

31

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

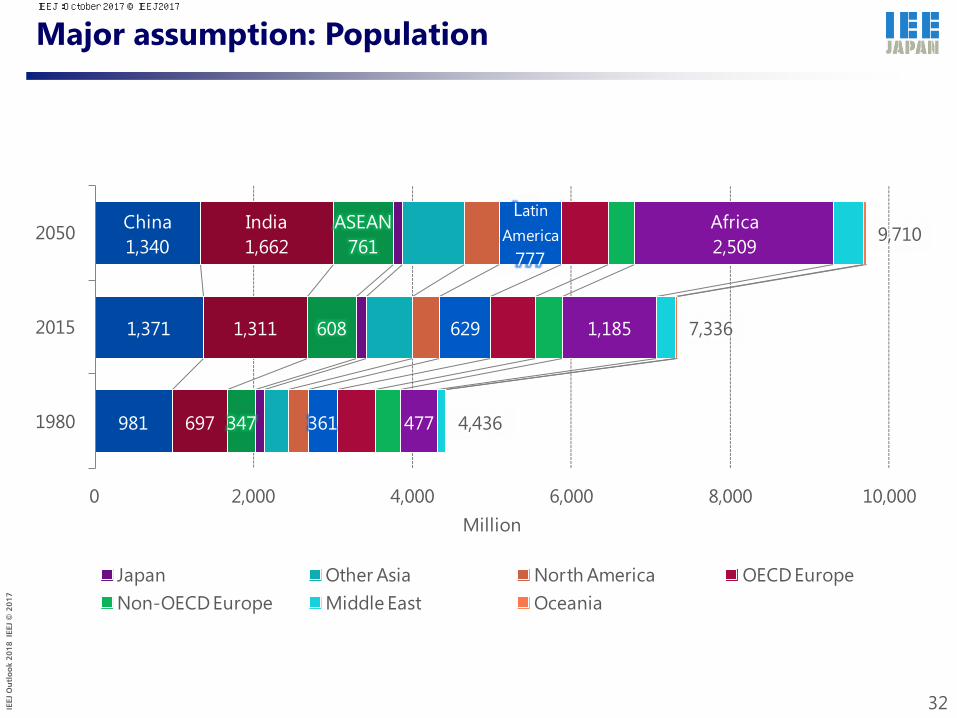

Major assumption: Population

32

981

1,371

China1,340

697

1,311

India1,662

347

608

ASEAN761

361

629

Latin America

777

477

1,185

Africa2,509

4,436

7,336

9,710

0 2,000 4,000 6,000 8,000 10,000

1980

2015

2050

Million

Japan Other Asia North America OECD EuropeNon-OECD Europe Middle East Oceania

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

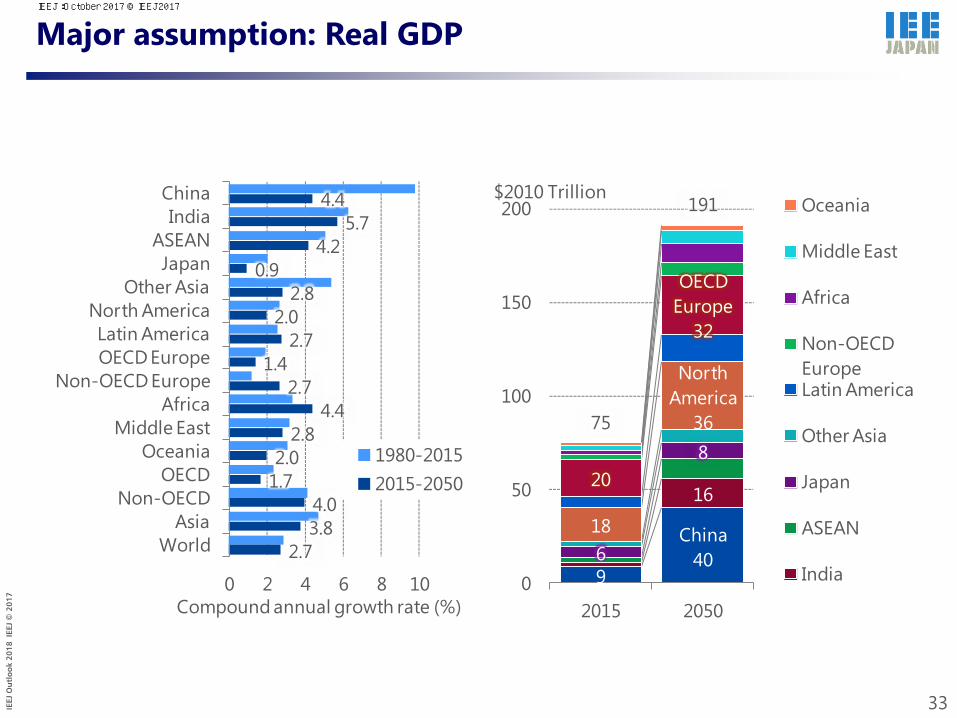

Major assumption: Real GDP

33

4.4 5.7

4.2 0.9

2.8 2.0

2.7 1.4

2.7 4.4

2.8 2.0

1.7 4.0 3.8

2.7

0 2 4 6 8 10

ChinaIndia

ASEANJapan

Other AsiaNorth AmericaLatin AmericaOECD Europe

Non-OECD EuropeAfrica

Middle EastOceania

OECDNon-OECD

AsiaWorld

Compound annual growth rate (%)

1980-20152015-2050

9

China40

16

6

8

18

North America

36

20

OECD Europe

32

75

191

0

50

100

150

200

2015 2050

Oceania

Middle East

Africa

Non-OECD EuropeLatin America

Other Asia

Japan

ASEAN

India

$2010 Trillion

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Major assumption: International energy prices

* Historical prices are nominal price. Assumed future prices are real price in $2016.

CIF import prices for Japan

Crude oil Natural gas

Steam coal

34

0

50

100

150

1980 1990 2000 2010 2020 2030 2040 2050

$/bbl

0

5

10

15

20

1980 1990 2000 2010 2020 2030 2040 2050

JapanEurope (UK)United States

$/MBtu

0

50

100

150

1980 1990 2000 2010 2020 2030 2040 2050

$/t

0

200

400

600

800

1,000

19801990200020102020203020402050

Crude oilNatural gasSteam coal

$/toe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Energy outlook in the world and Asia 2015-2050

Reference Scenario

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

World population, GDP, primary energy consumption and CO2 emissions

36

Reference Scenario

132

255

145 134

0

50

100

150

200

250

300

1980 1990 2000 2010 2015 2020 2030 2040 2050

Primary energyconsumption

Population

2015=100

Real GDP

CO2 emissions100

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

2,000

4,000

6,000

8,000

10,000

1980 1990 2000 2015 2030 2040 2050

North AmericaLatin AmericaAsiaMiddle EastOECD EuropeNon-OECD EuropeAfricaOceania

Mtoe

-146

-145

4

345

526

539

847

3,893

-0.2%

-0.3%

0.1%

0.8%

1.4%

1.6%

2.1%

1.5%

North America

OECD Europe

Oceania

Non-OECD Europe

Latin America

Middle East

Africa

Asia

Mtoe CAGR(2015-2050)

2015 13,700 Mtoe

2050

19,800 Mtoe (×1.5)

Primary energy consumption by region

Changes (2015-2050) World

37

Reference Scenario

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1980 1990 2000 2015 2030 2040 2050

China

India

ASEAN

Japan

Korea

Others

Mtoe

-39

-10

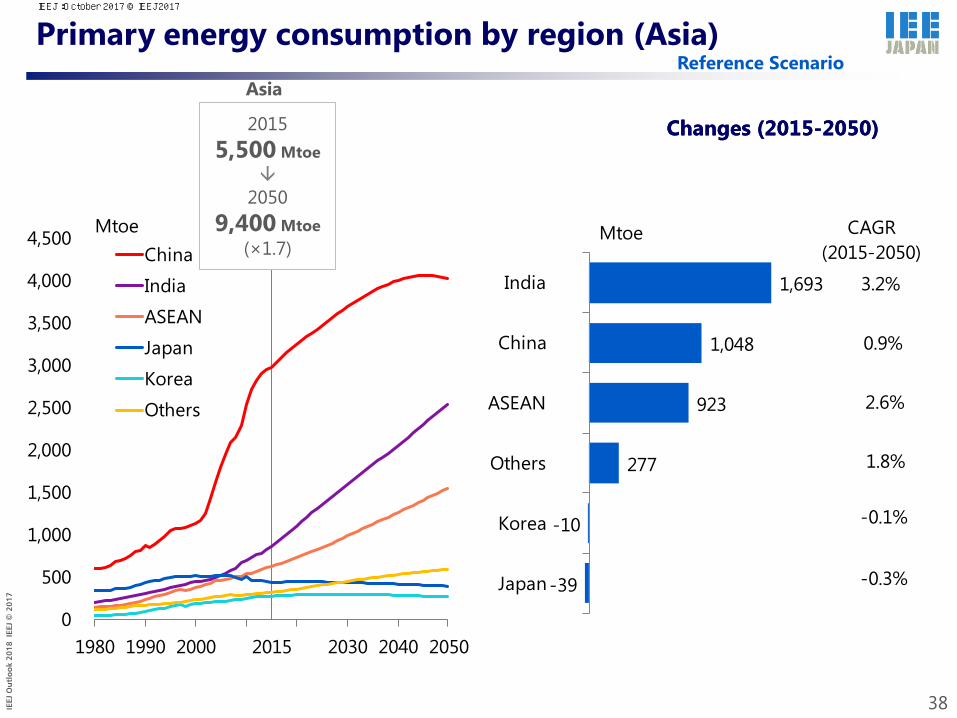

277

923

1,048

1,693

-0.3%

-0.1%

1.8%

2.6%

0.9%

3.2%

Japan

Korea

Others

ASEAN

China

India

Mtoe CAGR(2015-2050)

Primary energy consumption by region (Asia)

38

Reference Scenario

Changes (2015-2050)

Asia

Changes (2015-2050) 2015 5,500 Mtoe

2050

9,400 Mtoe (×1.7)

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1980 1990 2000 2015 2030 2040 2050

CoalOilNatural gasNuclearHydroOther renewables

Mtoe

166

384

695

1,132

1,515

2,250

1.2%

1.3%

0.5%

1.6%

0.9%

1.6%

Hydro

Nuclear

Coal

Other renewables

Oil

Natural gas

MtoeCAGR

(2015-2050)

39

Reference Scenario

Changes (2015-2050) 2015 13,700 Mtoe

2050

19,800 Mtoe (×1.5)

World

Primary energy consumption by source IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1980 1990 2000 2015 2030 2040 2050

CoalOilNatural gasNuclearHydroOther renewables

Mtoe

90

330

443

993

1,015

1,020

1.5%

4.0%

1.6%

1.6%

0.9%

3.1%

Hydro

Nuclear

Other renewables

Oil

Coal

Natural gas

MtoeCAGR

(2015-2050)

Primary energy consumption by source (Asia)

40

Reference Scenario

Changes (2015-2050)

Asia

2015 5,500 Mtoe

2050

9,400 Mtoe (×1.7)

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

1,000

2,000

3,000

4,000

5,000

6,000

1980 1990 2000 2015 2030 2040 2050

Industry

Transport

Buildings, etc.

Non-energy use

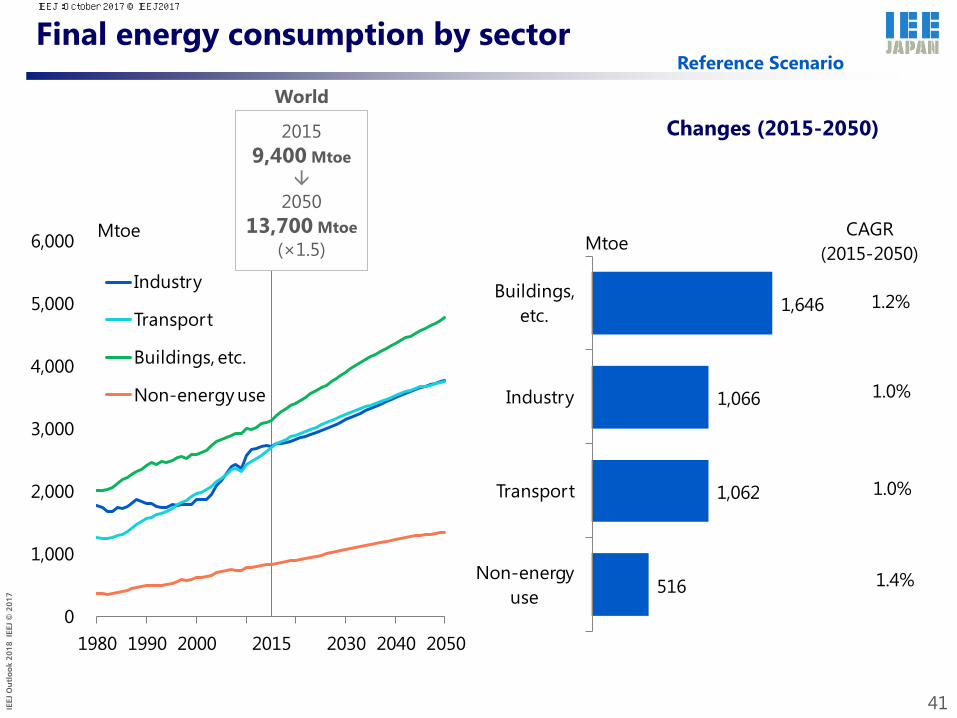

Mtoe

516

1,062

1,066

1,646

1.4%

1.0%

1.0%

1.2%

Non-energy use

Transport

Industry

Buildings, etc.

MtoeCAGR

(2015-2050)

Final energy consumption by sector

2015 9,400 Mtoe

2050

13,700 Mtoe (×1.5)

World

41

Reference Scenario

Changes (2015-2050)

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

500

1,000

1,500

2,000

2,500

1980 1990 2000 2015 2030 2040 2050

Industry

Transport

Buildings, etc.

Non-energy use

Mtoe

278

616

626

1,003

1.6%

1.0%

2.0%

1.8%

Non-energy use

Industry

Transport

Buildings, etc.

MtoeCAGR

(2015-2050)

Final energy consumption by sector (Asia)

42

Reference Scenario

Changes (2015-2050) Asia

2015 3,600 Mtoe

2050

6,100 Mtoe (×1.7)

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

1,000

2,000

3,000

4,000

5,000

6,000

1980 1990 2000 2015 2030 2040 2050

CoalOilNatural gasElectricityOthers

Mtoe

64

329

829

1,483

1,586

0.2%

0.6%

1.3%

0.9%

1.9%

Coal

Others

Natural gas

Oil

Electricity

MtoeCAGR

(2015-2050)

Final energy consumption by source

43

Reference Scenario

Changes (2015-2050) 2015 9,400 Mtoe

2050

13,700 Mtoe (×1.5)

World

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

500

1,000

1,500

2,000

2,500

1980 1990 2000 2015 2030 2040 2050

CoalOilNatural gasElectricityOthers

Mtoe

60

92

436

965

971

0.2%

0.4%

2.9%

2.4%

1.7%

Coal

Others

Natural gas

Electricity

Oil

MtoeCAGR

(2015-2050)

Final energy consumption by source (Asia)

44

Reference Scenario

Changes (2015-2050) Asia

2015 3,600 Mtoe

2050

6,100 Mtoe (×1.7)

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Oil consumption

By region By sector

Reference Scenario

45

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1980 1990 2000 2015 2030 2040 2050

International bunkersOceaniaAfricaNon-OECD Europe/Central AsiaOECD EuropeMiddle EastAsiaLatin AmericaNorth America

Mtoe

3,102 3,2353,660

4,334

5,0245,471

5,849

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1980 1990 2000 2015 2030 2040 2050

Transformation

Non-energy use

Buildings, etc.

Transport

Industry

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Oil consumption (Asia)

By region

Reference Scenario

46

By sector

0

500

1,000

1,500

2,000

2,500

1980 1990 2000 2015 2030 2040 2050

Others

Korea

Japan

ASEAN

India

China

Mtoe

477618

916

1,330

1,820

2,089

2,323

0

500

1,000

1,500

2,000

2,500

1980 1990 2000 2015 2030 2040 2050

Transformation

Non-energy use

Buildings, etc.

Transport

Industry

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Oil production Reference Scenario

47

92102

11111843% 44%

47%48%

0%

10%

20%

30%

40%

50%

0

20

40

60

80

100

120

140

2015 2030 2040 2050

OPEC share

Asia/Oceania

Non-OECD Europe/Central Asia

Other Latin America

North America

Other Africa

Other Middle East

OPEC non-Middle East

OPEC Middle East

Mb/d

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Oil net imports Reference Scenario

48

-23

-9

1

-2 -5

1 1

7 82

73

-25

-9-5 -3 -4

0 16 7

4

127

-33

-9 -7 -7-2

0 25 6

813 14

-40

-30

-20

-10

0

10

20

Middle East

Non-OECD

Europe/Central

Asia

North America

Latin America

Africa Oceania Other Asia

Japan/ Korea/

Chinese Taipei

OECD Europe

ASEAN China India

Mb/d

2015

2030

2050

Net exporters in 2050 Net importers in 2050

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Major crude oil trade flows (2016)

Japan/Korea/ Chinese Taipei

Non-OECD Europe/ Central Asia

North America

Middle East

Latin America

Africa

OECD Europe

China

ASEAN

Oceania

South Asia 2.2

4.6

1.9

1.1

1.4

3.7

6.0

1.8

2.7

0.6

0.6

Unit: Mb/d

1.0

2.0 1.9

0.5 0.7

49

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Major crude oil trade flows (2030) Reference Scenario

50

1.5

3.3

1.4

1.7

1.5

7.4

4.9

3.6

6.7

0.8

0.6

0.8

0.5 1.0

Unit: Mb/d

0.7

0.6

0.8 0.6

Non-OECD Europe/ Central Asia OECD Europe

Middle East

Africa

Oceania

South Asia

ASEAN

China Japan/Korea/ Chinese Taipei

North America

Latin America

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Natural gas consumption

By region By sector

Reference Scenario

51

0

1,000

2,000

3,000

4,000

5,000

6,000

1980 1990 2000 2015 2030 2040 2050

International bunkersOceaniaAfricaNon-OECD Europe/Central AsiaOECD EuropeMiddle EastAsiaLatin AmericaNorth America

Mtoe

1,2321,663

2,071

2,944

3,845

4,550

5,194

0

1,000

2,000

3,000

4,000

5,000

6,000

1980 1990 2000 2015 2030 2040 2050

Transformation

Non-energy use

Buildings, etc.

Transport

Industry

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

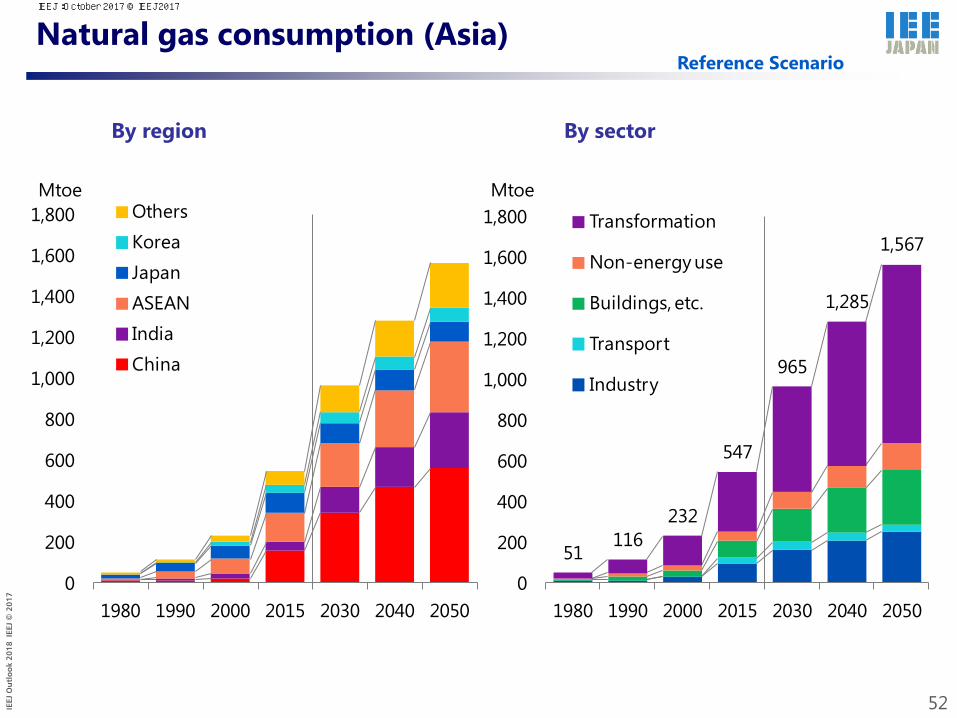

Natural gas consumption (Asia)

By region By sector

Reference Scenario

52

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1980 1990 2000 2015 2030 2040 2050

OthersKoreaJapanASEANIndiaChina

Mtoe

51116

232

547

965

1,285

1,567

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1980 1990 2000 2015 2030 2040 2050

Transformation

Non-energy use

Buildings, etc.

Transport

Industry

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Natural gas production Reference Scenario

53

3,493

4,668

5,521

6,300

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2015 2030 2040 2050

Asia/Oceania

Non-OECD Europe/Central Asia

Latin America

North America

Africa

Middle East

Bcm

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Natural gas net imports Reference Scenario

54

-17

-105-77

-14-50

32

-30 -17

14

125

42

152

-164 -180

-125-96

-54

5417 26

62

143106

203

-269 -260 -246

-134

-36

4873

101138 157

186222

-300

-200

-100

0

100

200

300

North America

Non-OECD

Europe/Central

Asia

Middle East

Oceania Africa Latin America

ASEAN Other Asia

India Japan/Korea/Chinese Taipei

China OECD Europe

Bcm

2015

2030

2050

Net exporters in 2050 Net importers in 2050

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

LNG imports Reference Scenario

55

191

3910 13 8 3

349

96

20 245 3

0

100

200

300

400

500

0

100

200

300

400

Asia Europe Middle East Latin America Africa North America

2016

2030

Mt Bcm

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

56

Unit: Bcm

36

37

166

24

14 24

61

38

55

15

34

10

Pipeline Gas LNG

16

7

Japan/Korea/ Chinese Taipei

Non-OECD Europe/ Central Asia

North America

Middle East

Latin America

Africa

OECD Europe

China

ASEAN

Oceania

South Asia

Major natural gas trade flows (2016) IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Reference Scenario

57

Unit: Bcm

25 35

49 30

26

103 148

45

27

23

23

25

68 22

42

22 13

22

Pipeline Gas LNG

16

Japan/Korea/ Chinese Taipei

Non-OECD Europe/ Central Asia

North America

Middle East

Latin America

Africa

OECD Europe

ASEAN

Oceania

South Asia

China

Major natural gas trade flows (2030) IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Coal consumption

By region

Reference Scenario

58

By sector

0

1,000

2,000

3,000

4,000

5,000

1980 1990 2000 2015 2030 2040 2050

OceaniaAfricaNon-OECD Europe/Central AsiaOECD EuropeMiddle EastAsiaLatin AmericaNorth America

Mtoe

1,783

2,220 2,311

3,8364,254

4,486 4,531

0

1,000

2,000

3,000

4,000

5,000

1980 1990 2000 2015 2030 2040 2050

Transformation

Non-energy use

Buildings, etc.

Transport

Industry

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Coal consumption (Asia)

By region By sector

Reference Scenario

59

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1980 1990 2000 2015 2030 2040 2050

OthersKoreaJapanASEANIndiaChina

Mtoe

466785

1,037

2,739

3,3203,632 3,754

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1980 1990 2000 2015 2030 2040 2050

Transformation

Non-energy use

Buildings, etc.

Transport

Industry

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Coal production

60

Reference Scenario

3,866 4,246

4,479 4,526

0

1,000

2,000

3,000

4,000

5,000

2015 2030 2040 2050

Oceania

Asia

Non-OECD Europe/Central Asia

Latin America

North America

Africa

Middle East

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Coal net imports Reference Scenario

61

-254

-85-47 -51 -24

9

-14

-161

132 105 117

244

-307

-96-61 -49 -29

12 6

-128

112 131 157

252

-429

-117-59 -56 -53

15 1750 70

116

221 225

-500

-400

-300

-200

-100

0

100

200

300

Oceania Non-OECD

Europe/Central

Asia

Africa North America

Latin America

Middle East

Other Asia

ASEAN OECD Europe

China India Japan/Korea/ChineseTaipei

Mtoe

2015

2030

2050

Net exporters in 2050 Net importers in 2050

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Major steam coal trade flows (2016)

62

Unit: Mt

Non-OECD Europe /Central Asia

North America

Middle East

Latin America

Africa

OECD Europe

China

India

92

5 16

103

44 154 62

43

60

5

20

4

22

9 9

15

58 8 5

21 21 6

Russia

Colombia

South Africa

58

13

4

5

3

6 3

5

2

3 3

3

9

60

6

2 3

7

South-East Asia

Mongolia

Indonesia

Australia

Japan/Korea/ Chinese Taipei

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Reference Scenario

63

Major steam coal trade flows (2030)

90

5 19

96

41 142 80

47

57

9

57

4

9

7 9

15

53 5 4

19 19 6 53

72

5

4

4

6 5

39

3

3 4

12

17

93

5

2 3

2 2

5

9

3

Unit: Mt

Non-OECD Europe /Central Asia

North America

Middle East

Latin America

Africa

OECD Europe

China

India

Russia

Colombia

South-East Asia

Australia

Japan/Korea/ Chinese Taipei

South Africa

Indonesia

Mongolia

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

64

Major coking coal trade flows (2016)

3

27 63

7

4

7

2

13

13 19

40

5

8

7

5

4 4

15

24

1

1

Unit: Mt

Non-OECD Europe /Central Asia

North America

Middle East

Latin America

Africa

OECD Europe

China

India

Russia

Colombia

Mozambique

South-East Asia Indonesia

Mongolia

Australia

Japan/Korea/ Chinese Taipei

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Reference Scenario

65

2

30 66

7

4

3 18

18 19

60

4

6

7

6

2 2

16

2

3

3

10

4

3

2

1

1 1

1

Unit: Mt

Major coking coal trade flows (2030)

Non-OECD Europe /Central Asia

North America

Middle East

Latin America

Africa

OECD Europe

China

India Colombia

South-East Asia

Japan/Korea/ Chinese Taipei

Australia

Russia

Mozambique

Indonesia

Mongolia

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Fossil fuel supply/demand balances (Asia)

Oil

Reference Scenario

66

9411,489

2,006

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

2015 2030 2050

Production

Demand

Net imports

Mtoe

164 425780

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

2015 2030 2050

Mtoe

296 416 626

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

2015 2030 2050

Mtoe

Natural gas Coal

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Electricity final consumption

By region By sector

Reference Scenario

67

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1980 1990 2000 2015 2030 2040 2050

OceaniaAfricaNon-OECD Europe/Central AsiaOECD EuropeMiddle EastAsiaLatin AmericaNorth America

Mtoe

586835

1,092

1,737

2,373

2,852

3,324

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1980 1990 2000 2015 2030 2040 2050

Buildings, etc.

Transport

Industry

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Electricity final consumption (Asia)

By region By sector

Reference Scenario

68

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1980 1990 2000 2015 2030 2040 2050

OthersKoreaJapanASEANIndiaChina

Mtoe

88158

280

740

1,152

1,441

1,705

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1980 1990 2000 2015 2030 2040 2050

Buildings, etc.

Transport

Industry

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Power generation mix Reference Scenario

Electricity generated Share

69

8,28311,864

15,471

24,255

32,965

39,101

44,838

0

10,000

20,000

30,000

40,000

50,000

1980 1990 2000 2015 2030 2040 2050

Other renewables

Hydro

Nuclear

Natural gas

Oil

Coal

TWh

0%

20%

40%

60%

80%

100%

1980 1990 2000 2015 2030 2040 2050

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Power generation mix (Asia) Reference Scenario

Electricity generated Share

70

1,1962,252

4,013

10,204

15,895

19,641

22,874

0

5,000

10,000

15,000

20,000

25,000

1980 1990 2000 2015 2030 2040 2050

Other renewables

Hydro

Nuclear

Natural gas

Oil

Coal

TWh

0%

20%

40%

60%

80%

100%

1980 1990 2000 2015 2030 2040 2050

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

5

10

15

20

25

1980 1990 2000 2015 2030 2040 2050

North America

Latin America

Asia

Middle East

Non-OECD Europe

OECD Europe

Africa

Oceania

GtCO2

-1.1

-1.0

0.0

0.4

0.9

1.1

1.5

8.6

-0.6%

-0.9%

-0.4%

0.4%

1.2%

1.3%

2.4%

1.3%

North America

OECD Europe

Oceania

Non-OECD Europe

Latin America

Middle East

Africa

Asia

CAGR(2015-2050)

GtCO2

CO2 emissions

Changes (2015-2050) 2015 32.9 Gt

2050 44.1 Gt (×1.3)

World

Reference Scenario

71

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

0

2

4

6

8

10

12

1980 1990 2000 2015 2030 2040 2050

China

India

ASEAN

Japan

Korea

Others

GtCO2

-0.3

0.0

0.6

1.2

2.3

4.7

-0.7%

0.1%

2.0%

0.3%

3.0%

3.4%

Japan

Korea

Others

China

ASEAN

India

CAGR(2015-2050)

GtCO2

CO2 emissions (Asia) Reference Scenario

2015 15.1 Gt

2050 23.7 Gt (×1.6)

Asia

72

Changes (2015-2050)

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Advanced Technologies Scenario

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Advanced Technologies Scenario assumptions

In this Scenario, each country further enhances policies on energy security and address climate change. Technology developments and international technology transfers are promoted to further expand the penetration of innovative technologies.

Demand side technologies

■ IndustryUnder sectoral and other approaches, best available technologies on industrial processes (for steelmaking, cement, paper-pulp and oil refining) will be deployed globally

■ TransportClean energy vehicles (highly fuel efficient vehicles, hybrid vehicles, plug-in hybrid vehicles, electric vehicles, fuel cell vehicles) will diffuse further.

■ BuildingsEfficient electric appliances (refrigerators, TVs, etc.), highly efficient water-heating systems (heat pumps, etc.), efficient air conditioning systems and efficient lighting will diffuse further, with heat insulation enhanced.

Supply side technologies

■ Renewable energiesWind power generation, photovoltaic power generation, CSP (concentrated solar power) generation, biomass-fired power generation and biofuel will penetrate further.

■NuclearNuclear power plant construction will be accelerated with capacity factor improved.

■ Highly efficient fossil fuel-fired power generation technologiesCoal-fired power plants (SC,USC, A-USC, IGCC) and natural gas–fired more advanced combined cycle (MACC) plants will penetrate further.

■ Technologies for next-generation transmission and distribution networksLower loss type of transformation and voltage regulator will penerate further

■ Carbon capture and storage

Introducing and enhancing environmental regulations and national targetsEnvironment tax, emissions trading, RPS, subsidy, FIT, efficiency standards, automobile fuel efficiency standard, low carbon fuel standard, energy efficiency labeling, national targets, etc.

R&D investment expansion, international cooperation on energy efficient technology (steelmaking, cement and other areas), support for establishing energy efficiency standards, etc.

Promoting technology development and international technology cooperation

*SC: Super Critical, USC: Ultra Super Critical, A-USC: Advanced Ultra Super Critical

74

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Major assumption: Energy and environmental technologies

2015 2050 (Reference, 2050)

OECD Non-OECDThermal power plant

[Thermal efficiency (stock basis)] Natural gas: 48.5% 55.7% (56.9%) Natural gas: 36.7% 47.3% (44.9%)Coal: 37.3% 44.4% (45.0%) Coal: 36.5% 40.2% (41.4%)

Nuclear Maintenance of appropriate price in wholesale electricity market

Maintenance of framework for financing initial investment

[Capacity] 2015: 309 GW 327 (241) 2015: 90 GW 629 (337)

Renewables System cost reduction System cost reductionCost reduction of power system Low cost investmentEfficient operation of power system Improvement of power system

[Capacity] Wind: 237 GW 1,091 (718) Wind: 178 GW 1,912 (1,152)Solar: 165 GW 909 (573) Solar: 60 GW 1,588 (946)

Biofuels Development of next generation biofuel Cost reduction of biofuelHigher diffusion of FFV Relating to agricultural policy

[Consumption] 50 Mtoe 107 (68) 26 Mtoe 94 (56)

IndustryTransportation[Average fuel efficiency of new vehicle sales] 14.5 km/L 41.1 (27.8) 12.9 km/L 28.6 (20.2)[Share in annual vehicle sales of ZEV] 0.8% 66% (35%) 0.5% 41% (17%)

Buildingsand insulation is twice. 20% improvement in 2050 in ratio of the Reference ScenarioElectrification and clean cooking in space heating, water heater and cooking

Maintenance of financial scheme for initial investment.

Installing CCS after 2030 (Countries which have storage potential except for aquifer)

Best available technology diffuses 100% in 2050Cost reduction of high fuel efficiency of vehicles. Twice of travel distance of ZEV

The pace of improvement of efficiency of newly installed appliance, equipment

Share of IGCC in install 0% 60% (20%)

Advanced Technologies Scenario

75

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Nuclear power generation capacities Advanced Technologies Scenario

76

385 399492

577638

784

956

0

200

400

600

800

1,000

1,200

2030 2050 2030 2040 2050

2005 2015 Reference Advanced Technologies

Middle East/Africa

Latin America

FSU/Non-OECD Europe

OECD Europe

North America

Asia

GW

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Renewables power generation capacities

Wind Solar PV

77

Advanced Technologies Scenario

415

1,865

1,370

3,002

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 2050 2030 2050

Refer-ence

AdvancedTechnologies

GW

224

1,519

951

2,497

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 2050 2030 2050

Refer-ence

AdvancedTechnologies

GWOceania

Asia

Middle East

Africa

FSU/Non-OECD EuropeOECD Europe

Latin America

North America

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

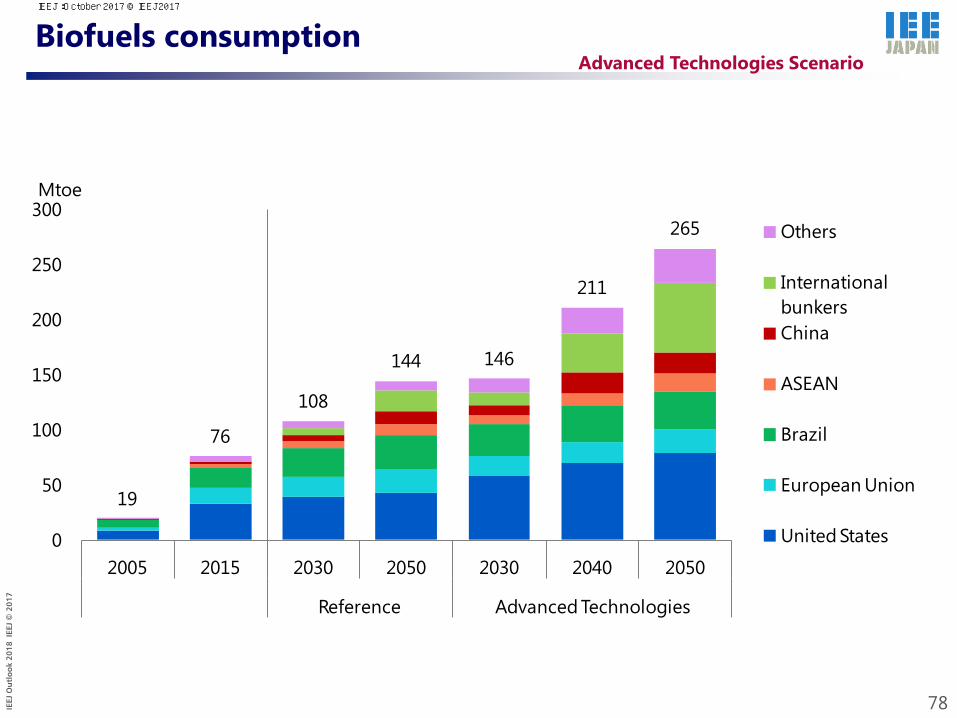

Biofuels consumption

78

Advanced Technologies Scenario

19

76

108

144 146

211

265

0

50

100

150

200

250

300

2005 2015 2030 2050 2030 2040 2050

Reference Advanced Technologies

Others

International bunkersChina

ASEAN

Brazil

European Union

United States

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Vehicle stock and sales by type

Share of new passenger light-duty vehicle sales

Share of passenger light-duty vehicle stocks

79

Advanced Technologies Scenario

97%

56%

23%

2%

1%

1%

1%

25%

37%

9%

18%

8%21%

0% 0%

0%

20%

40%

60%

80%

100%

Reference Advanced Technologies

2015 2050

Plug-in hybrid vehicleElectric vehicleFuel cell vehicle

95%

50%

17%

2%

1%

0%

2%

25%

33%

11%

21%

12%28%

0% 1%

0%

20%

40%

60%

80%

100%

Reference Advanced Technologies

2015 2050

ICE (gasoline, diesel)Compressed natural gasHybrid vehicle

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Fuel efficiency (New sales basis)

Fuel efficiency (Stock basis)

Fuel efficiency of passenger cars

80

Advanced Technologies Scenario

13.6

22.3

32.0

0

5

10

15

20

25

30

35

Reference Advanced Technologies

2015 2050

km/L43% up

12.5

20.4

27.8

0

5

10

15

20

25

30

35

Reference Advanced Technologies

2015 2050

km/L

36% up

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Energy consumption per unit of output in industry

81

Advanced Technologies Scenario

73.2 64.3

80.6 71.2 75.6

66.5 80.1

70.9 68.7 60.6

0

20

40

60

80

100Re

fere

nce

Adva

nced

Tech

nolo

gies

Refe

renc

e

Adva

nced

Tech

nolo

gies

Refe

renc

e

Adva

nced

Tech

nolo

gies

Refe

renc

e

Adva

nced

Tech

nolo

gies

Refe

renc

e

Adva

nced

Tech

nolo

gies

2015 2050Iron and steel

2050Non-metallic

minerals

2050Chemical

2050Paper and pulp

2050Other industries

12% down 12% down 12% down 11% down 11% down2015=100

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Total efficiency in buildings

82

Advanced Technologies Scenario

100

77.0

61.1

50.2 40.0

0

20

40

60

80

100

Reference AdvancedTechnologies

Reference AdvancedTechnologies

2015 2050, Household 2050, Commercial

21% down

20% down

2015=100

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Power generation mix

Electricity generated Capacity

83

Advanced Technologies Scenario

24,255

44,838

31,482

39,733

0

10,000

20,000

30,000

40,000

50,000

2015 2050 2030 2050

Reference Advanced Technologies

Coal Natural gas Oil

TWh

6,169

12,547

8,567

12,488

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2015 2050 2030 2050

Reference Advanced Technologies

Nuclear Hydro Other renewables

GW

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Power generation mix (Asia)

84

Advanced Technologies Scenario

Electricity generated Capacity

10,204

22,874

15,136

20,032

0

5,000

10,000

15,000

20,000

25,000

2015 2050 2030 2050

Reference Advanced Technologies

Coal Natural gas Oil

TWh

2,530

6,178

4,094

6,421

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2015 2050 2030 2050

Reference Advanced Technologies

Nuclear Hydro Other renewables

GW

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Carbon intensity of electricity

*CO2 emissions per kWh at generation end

World Asia

85

Reference & Advanced Technologies Scenarios

374

251

641

566 541

507

445

389

200

300

400

500

600

700

1980 1990 2000 2010 2020 2030 2040 2050

Reference

gCO2/kWh

AdvancedTechnologies

464

322

638 613

646 622

555

487

200

300

400

500

600

700

1980 1990 2000 2010 2020 2030 2040 2050

Reference

gCO2/kWh

AdvancedTechnologies

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Energy savings by region and by sector

Final energy consumption Energy savings by region and by sector

86

Advanced Technologies Scenario

Industry

Transport

Buildings, etc.

Non-energy use

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2015 2050Reference

2050Advanced

Technologies

Mtoe

9,384

13,675

13,675Mtoe

11,831Mtoe

2050Reference

2050Advanced Technologies

United States

OECD EuropeJapan

Other OECDChina

India

Other Asia

OtherNon-OECD

Buildings, etc.

Transport

Industry

Intl. bunkers

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Primary energy consumption reduction

87

Advanced Technologies Scenario

8,774

10,028

12,873 13,647

16,562

18,374

19,789

15,71716,693

17,219

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1990 2000 2010 2015 2020 2030 2040 2050

International bunkersNon-OECDOECDReferenceAdvanced Technologies

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Primary energy consumption reduction (Asia)

88

Advanced Technologies Scenario

2,108

2,887

4,818 5,459

7,434

8,548

9,351

7,078

7,794 8,156

2,000

4,000

6,000

8,000

10,000

1990 2000 2010 2015 2020 2030 2040 2050

Other AsiaASEANIndiaChinaReferenceAdvanced Technologies

Mtoe

IEEJ:October 2017 © IEEJ2017

IEEJ

Ou

tlo

ok

2018

IEE

J ©

201

7

Primary energy consumption by source

World Asia

89