iea medium-term market reportseneken.ieej.or.jp/data/4569.pdfchina, brazil, india lead; others grow...

TRANSCRIPT

© OECD/IEA 2011

IEA Medium-Term Market Reports

IEEJ Seminar Tokyo, 20 September 2012

Didier Houssin Director, Energy Markets and Security International Energy Agency

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Introduction to medium term reports

Based on the most recent data available

5 years outlook is important for policy making

Natural gas and renewables are growing fastest

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Gas: global developments

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Key messages – natural gas

Natural gas demand is expected to increase by 576 bcm to reach 3937 bcm by 2017 (2.7%/y) 69% of demand will come from non-OECD countries

With 37% originating from Asian countries

No Golden Age of Gas in Europe

FSU and North America are the largest contributors to global supply

Global gas trade expands by one-third over 2011-17 Trade is shifting to Asia

LNG markets will be tightening over 2012-14

The next wave of LNG exports starts only at end 2014

China becomes the third largest importer after Europe and Asia Oceania

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Gas demand is projected to grow by 2.7%/y over 2011-17

Gas demand is projected to reach around 3940 bcm from 3361 bcm in 2011 (+576 bcm)

69% of the growth will come from non-OECD regions (+400 bcm)

OECD demand only increases by 180 bcm

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

FSU and North America are set to be the largest contributors to additional supply

FSU is growing fast driven by incremental exports, notably to China

North America’s gas production meets booming demand and some LNG exports

China and Australia become significant gas producers

European domestic production continues to decline

Incremental gas production, 2011-17

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Unconventional gas Already 16% of global gas supply

Half of the world’s unconventional gas production comes from tight gas; shale gas is a North American story

Environmental aspects as well as infrastructure, pricing, policy issues need to be tackled

North America Tight ~ 221 bcm Shale ~ 197 bcm CBM ~ 59 bcm

Latin America Tight ~ 2 bcm

Europe CBM < 1 bcm

FSU Tight ~ 20 bcm CBM < 1 bcm

Middle East & Africa Tight gas > 3 bcm

Asia Tight ~ 35 bcm CBM ~ 2 bcm

Australia CBM ~ 6 bcm

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Russia and the Caspian The interest is shifting to Asia

Yamal expected to start producing in 2012 with a potential to produce 115bcm/y by 2017

Far East/East Siberian projects for China/Korea/LNG export await FID

Turkmenistan is increasing exports to China (possibly to 65 bcm by 2020)

FEED on Shah Deniz-II started in 2012, production might begin 2018

2017+ 2017+

2017+

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Asia’s gas production growth supported by China

China production rises strongly but is insufficient to meet demand

India’s gas production struggles to grow

New gas production in Papua New Guinea to support LNG exports

Relatively flat production in Malaysia

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Regional gas prices are drifting further apart

Source: ICE, EIA, IEA, German Customs, Japanese Customs, McCloskey

Avg. gap in 2011:

USD 5.8/MBtu

Avg. gap in 2011

USD 5.0 /MBtu

There are widening disparities between regional gas prices, which are increasingly determined by their respective regional dynamics Asian price development closely connected to oil price

North America is totally disconnected from other regions

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

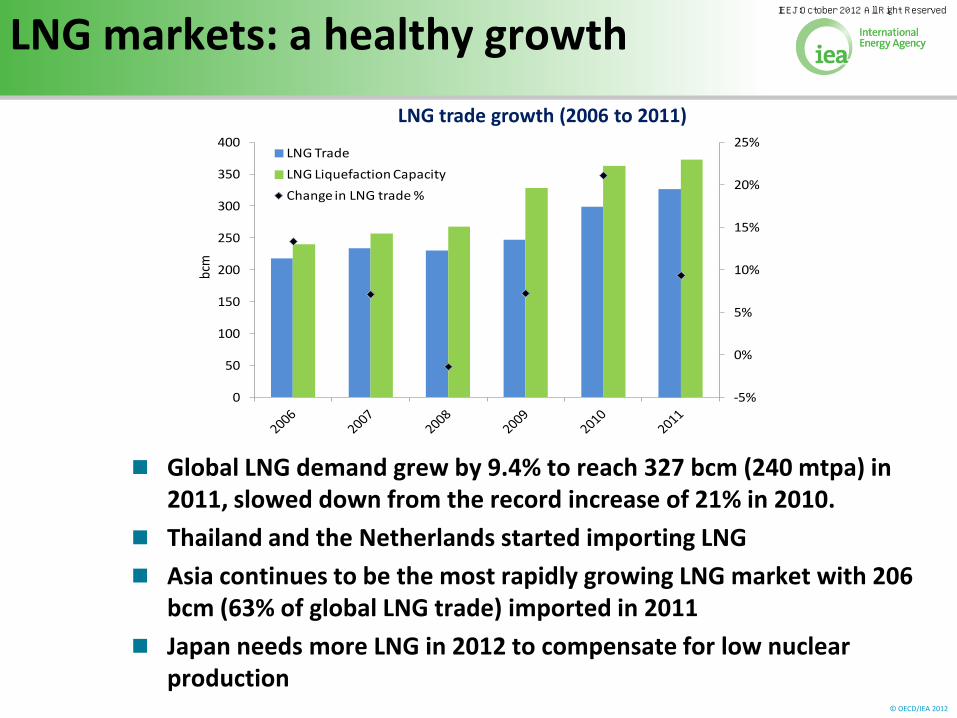

LNG markets: a healthy growth

Global LNG demand grew by 9.4% to reach 327 bcm (240 mtpa) in 2011, slowed down from the record increase of 21% in 2010.

Thailand and the Netherlands started importing LNG

Asia continues to be the most rapidly growing LNG market with 206 bcm (63% of global LNG trade) imported in 2011

Japan needs more LNG in 2012 to compensate for low nuclear production

LNG trade growth (2006 to 2011)

-5%

0%

5%

10%

15%

20%

25%

0

50

100

150

200

250

300

350

400

bcm

LNG Trade

LNG Liquefaction Capacity

Change in LNG trade %

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Global gas trade in 2017

OECD Europe, OECD Asia Oceania and China are all net importers, both OECD regions also export LNG

The trade balance is shifting to Asia, notably China, OECD Asia Oceania and other Asian countries

North America is a net exporter

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Renewables

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Key messages – renewable energy

As a portfolio of renewable technologies matures, global renewable power generation is forecast to rise 40% Supported by policy/market frameworks and economic

attractiveness in increasing range of countries and circumstances

Technology cost developments, grid/system integration, cost/availability of financing also weigh as key variables

High level of economic/policy uncertainty in some countries

This projected growth is an acceleration vs previous period Growth is 60% higher over 2011-17 versus 2005-11

Renewable deployment is projected to spread out geographically, with increased activity in emerging markets Deployment spurring economies of scale in some technologies -

virtuous cycle of improved competition and cost reductions

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Growth in renewable power is forecast to accelerate

Hydropower remains the main renewable power source (+3.1% p.a.)

Non-hydro renewable sources grow at double-digit annual percentage rates (+14.3% p.a.)

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Global renewable electricity production and forecast

Hydropower Wind onshore Bioenergy Solar PV

Geothermal Wind offshore CSP Ocean

TWh

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

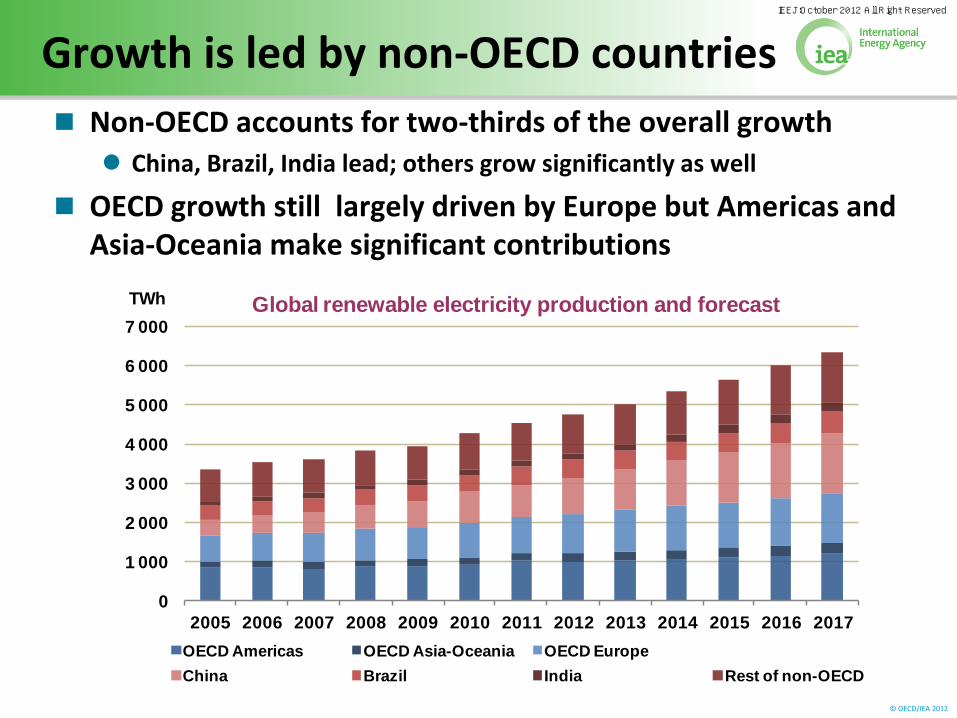

Growth is led by non-OECD countries

Non-OECD accounts for two-thirds of the overall growth China, Brazil, India lead; others grow significantly as well

OECD growth still largely driven by Europe but Americas and Asia-Oceania make significant contributions

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

TWh Global renewable electricity production and forecast

OECD Americas OECD Asia-Oceania OECD Europe

China Brazil India Rest of non-OECD

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Regional analysis

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Gas drives coal down in Americas

Very low gas prices enable gas-fired plants to win market shares at the expense of coal

Renewables generation (excl. hydro) increases strongly but still represents a small share of total generation (8%)

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

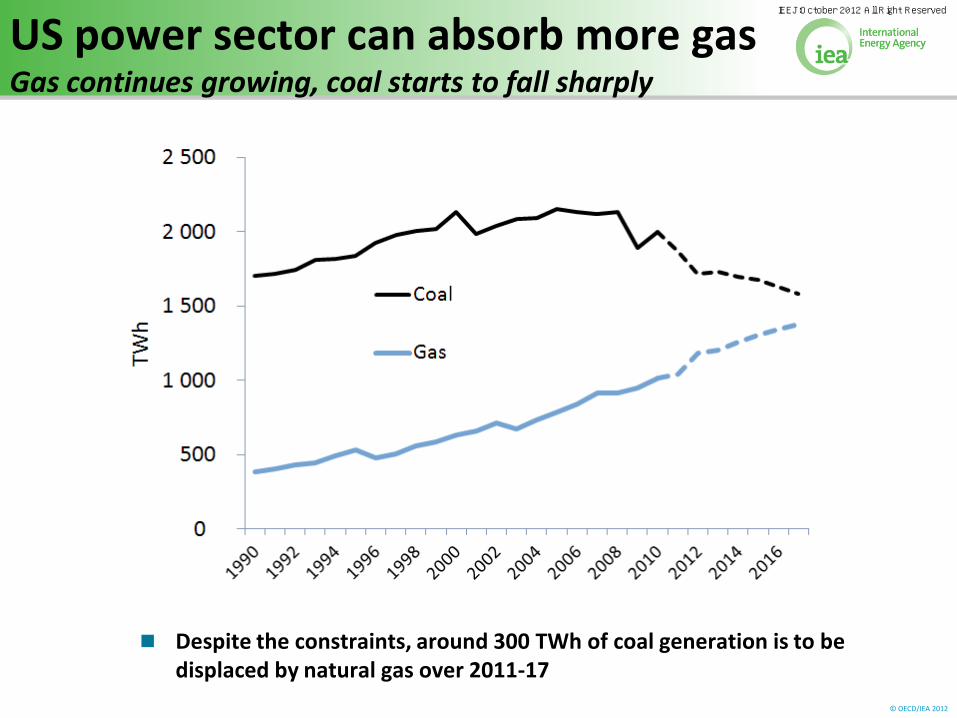

US power sector can absorb more gas Gas continues growing, coal starts to fall sharply

Despite the constraints, around 300 TWh of coal generation is to be displaced by natural gas over 2011-17

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

US renewable generation expected to continue to grow steadily

Average renewable growth of 2.4% annually over 2011-17

Non-hydropower growth at stronger rate, + 8.4% annually Onshore wind, solar PV and bioenergy grow strongest

CSP and geothermal growth are large in global terms

% of total power gen: 9% (2005), 13% (2011), 14-15% (2017)

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

United States renewable generation and forecast

Hydropower Wind onshore Bioenergy Solar PV Geothermal CSP Wind offshore

TWh

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Europe: power demand increases slower due to low GDP growth

There is less room for fossil fuels Gas has to compete against coal-fired plants

Gas is disadvantaged in the early period due to high gas prices

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Golden age of coal in Europe?

In 2011, demand in the power generation sector dropped by 3 bcm

Low (or negative) power demand growth

Strong growth of renewables

High gas prices with low CO2 prices make gas-fired plants uncompetitive

Gas loses competitiveness in the short term, but will recover (at lower levels than 2011)

0

200

400

600

800

1 000

1 200

TWh

Coal

Gas

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Natural gas prices in Europe

European spot market prices continued to dwell below oil indexed import prices in 2011

Spot market prices stayed low due to overall sluggish demand for natural gas in Europe

0

5

10

15

20

25U

SD/M

Btu

NBP GBP Brent NW European coal marker UK LNG

NBP Avg. -15% of

GBP in 2011

Source: EIA, IEA, German Customs, UK Customs, McCloskey

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

European hubs: strong growth in trade

Physical and traded volume in Europe has continued to increase throughout 2006 -11

Increase shows a decreasing trend in continental Europe

+27% Traded volume versus 2010

+8% Physical volume versus 2010

Continental hubs have overtaken NBP in physically delivered volumes since 2008

NBP continues to dominate trade with 68% of total traded volume in Europe

0

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011 2006 2007 2008 2009 2010 2011

Traded Volume Physical volume

Bcm

TTF NCG GASPOOL Zeebrugge PSV CEGH PEG's

+55%

+46%

+56%

+46%

+27%

+8%

0

200

400

600

800

1000

1200

1400

1600

1800

2006 2007 2008 2009 2010 2011 2006 2007 2008 2009 2010 2011

Traded Volume Physical volume

Bcm

NBP Continental

58%61%

22%

28%

32%

67%

16%

13%

12%

32% 38% 50%

Source: TSO’s and regulators

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Europe continues strong renewable growth, but economic/policy uncertainties weigh

Germany, UK and Turkey are largest growers

Nordic countries grow steadily

Economic conditions and overcapacity challenge Italy, Spain

Eastern Europe growing despite crisis and has a long way to go to fulfill EU 2020 goals

0

200

400

600

800

1 000

1 200

1 400

2011 2012 2013 2014 2015 2016 2017

OECD Europe forecast renewable generation

Hydropower Wind onshore Bioenergy Solar PV

Geothermal Wind offshore CSP Ocean

TWh

0

20

40

60

80

100

120

140

160

180

200

2011 2012 2013 2014 2015 2016 2017

Germany forecast renewable generation

Hydropower Solar PV Wind onshore Bioenergy

Geothermal CSP Wind offshore

TWh

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

In Asia Oceania, the key question mark is Japan’s future energy policy

Assumes some nuclear comes back in Japan (less than half 2010)

Gas-fired generation set to grow, notable to replace missing nuclear

But coal increases as well (Australia, Japan, Korea)

Renewables generation doubles but represents only 6% of total generation

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Japan renewable energy grows strongly with uncertain nuclear and new feed-in tariffs

0

20

40

60

80

100

120

140

160

180

2011 2012 2013 2014 2015 2016 2017

Japan forecast renewable generation

Hydropower Bioenergy Solar PV

Wind onshore Geothermal Wind offshore

TWh

Drivers: Uncertain nuclear restart

New feed-in tariffs

Good match of solar PV for shaving peak load

Challenges: Power system fragmentation

Relatively high capital costs of renewable energy

Location of wind and geothermal resources far from demand centres

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

But replacing nuclear is almost guaranteed to boost LNG demand

0

50

100

150

200

250

300

Nuclear pre Fukushima

Global geothermal

EU solar

German wind

TWh

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

China power demand can accommodate both fast REN and gas growth

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

2 000

4 000

6 000

8 000

2005 2008 2011 2014 2017

Y-o-YChg

TWh China power demand vs GDP growth

Demand Demand, Y-o-Y (RHS) GDP, Y-o-Y (RHS)

Source:

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

China is the fastest growing region of gas demand

Gas demand grows in all sectors, except fertiliser producers

New sectors emerge such as transport

But there remains supply constraints limiting demand

China needs to solve issues such as pricing and regulation

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

China accounts for 40% of global growth in renewable generation

0

300

600

900

1 200

1 500

1 800

2011 2012 2013 2014 2015 2016 2017

China forecast renewable generation

Hydropower Wind onshore Bioenergy Solar PV Wind offshore CSP

TWh

Drivers: Growing energy needs

Diversification

Government targets

Ample low-cost finance

Robust manufacturing

Challenges: Pricing framework

Priority dispatch

Grid upgrades

Prohibitive licensing for small-scale systems

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Want to know more?

The Medium-Term Gas Market Report and Medium-Term Renewable Energy Market Report 2012 can be purchased online at:

www.iea.org

IEEJ:October 2012 All Right Reserved

© OECD/IEA 2012

Thank you!

IEEJ:October 2012 All Right Reserved

Contact: [email protected] The back issues are available at the following URL http://eneken.ieej.or.jp/en/whatsnew/JPOIEL.html