identifying accounting quality - washington university in...

TRANSCRIPT

1

Identifying Accounting Quality

Valeri V. Nikolaev1 The University of Chicago Booth School of Business

Abstract

I develop a new approach to understanding accounting accruals. Unlike prior studies, I explicitly address the economic role of accruals in performance measurement. I characterize accounting quality in terms of a new construct, namely, the degree to which accruals facilitate performance measurement. Further, I develop a flexible strategy for identifying accounting quality. The core identifying assumptions derive from institutional properties of both earnings and cash flows: that both are noisy measures of the same economic performance and they converge as the time horizon extends. These assumptions characterize moments of earnings, cash flows, and accruals solved to recover the variance of performance and accounting error in accruals. I implement several model specifications and consider a number of generalizations. My analysis suggests that the variance of the performance component exceeds accounting error and explains a high fraction of accruals’ variance. I conclude that accruals meet their objective.

First draft: June 10, 2014 Current draft: October 19, 2016

1 I thank Rachel Hayes (the editor), two anonymous referees, Sudipta Basu, Jung Ho Choi, Ilia Dichev, Ray Ball, Philip Berger, Patricia Dechow, Ronald Dye, Paul Hribar, Oleg Kiryukhin, S.P. Kothari, Andrei Kovrijnykh, Christian Leuz, Laurence van Lent, Mark Maffett, Douglas Skinner, Charles Wasley, Joanna Wu, Anastasia Zakolyukina, Stephen Zeff, and workshop participants at Rice University, Temple University, the University of North Carolina at Chapel Hill, the University of Rochester, and conference participants at Carnegie Mellon University for providing helpful comments. Financial support from the University of Chicago Booth School of Business is gratefully acknowledged.

1

1. Introduction.

The primary objective of financial reporting is to provide information about enterprise

performance. This objective is met via the use of accruals. Specifically, accrual accounting provides more

useful measures of economic performance than cash flow-based measures (Trueblood Report 1973,

SFAC 1 and 8, Dechow 1994). Many economic decisions rely directly or indirectly on performance

measurement. Most notably, the greater the error in measuring an agent’s performance, the harder it

becomes to provide incentives (e.g., Prendergast 1999). Economic theory suggests that information about

an agent’s performance should be aggregated in a way that minimizes measurement error (Holmstrom

1979). Broadly, this is what accruals aims to do. Nevertheless, to date, the literature has not offered a

model of accruals that captures their economic role in measuring performance. Without such a model, it is

difficult, if not impossible, to evaluate how well accruals meet this primary objective.

In this paper, I develop a new approach towards understanding accruals and identifying their

quality. This approach builds on the perspective in SFAC 1 (see also SFAC 8) that the role of accruals is

to facilitate performance measurement. I offer a novel model of accruals that explicitly captures this role.

Based on this model, I introduce a concept of accounting quality that is different from those in prior

studies. Accounting quality is characterized by the extent to which accruals fulfill their objective of

producing an accurate performance measure. Further, I develop an econometric framework that permits

the identification of accounting quality (and its components) under a flexible set of assumptions.

Conceptually, I characterize accounting accruals in terms of two different components. The

purpose of the first component is to offset the measurement (timing) errors present in operating cash

flows. To this end, the performance component of accruals includes performance that is not reflected in

the current operating cash flows and excludes current cash flows unrelated to performance in this period.

This occurs, for example, by accruing the expected cash flow earned in the present period (but realized in

the future) and deferring the present period cash flow earned in the future. This component captures the

benefit of accrual accounting. Its variability reflects the true operating volatility or the degree of liquidity

shocks.

2

The second component of accruals represents the “accounting error” or the noise introduced into

earnings (and accruals) when measuring the underlying performance. It captures the cost of using

accruals. The accounting error can arise because of the need to use accounting estimates, assumptions,

and judgments (Dechow and Dichev 2002). However, it can also be due to the non-discretionary

constraints that GAAP places on managerial reporting choices (Beyer et al. 2014). The magnitude of the

second is the primary determinant of how well accruals fulfil their role.

Given the characterization of accruals, it is natural to think of accounting quality as the extent to

which accruals facilitate periodic performance measurement. To measure accounting quality in this way,

it is necessary to identify and separate the variance of the economic performance component in accruals

from the variance of accounting error. The identification strategy I propose takes advantage of the

accounting institutional properties and structure, which serves as a “hook” that is instrumental to

disentangling the performance and error components. In particular, the core identifying assumptions are

that (1) both operating cash flow and earnings, measured on a periodic basis, represent noisy measures of

the same unobservable underlying economic performance and (2) that both the performance component in

accruals and accounting error reverse over time. These institutional properties of accruals impose a

particular structure onto moment conditions based on the auto-covariances and cross-covariances of the

time series of accruals, earnings, and cash flows, which allows the identification of the variance of

economic performance, the variance of the performance component in accruals, and the variance of

accounting error in an unbiased manner. This can be done via the General Method of Moments (Hansen

1982), which does not require distributional assumptions such as normality.

I implement several basic model specifications both at the firm and industry levels and show that

they generate intuitive results. First, I show that the variance of the performance component in accruals on

average exceeds the variance of accounting error. This result is fundamental to understanding the value of

accruals and implies that accounting earnings is a better performance measure than cash flows. I show

that the fraction of accruals’ variance explained by the performance component is on average (median)

71% (78%). Further, I explore whether the accounting error and performance components of accruals are,

3

to a large extent, driven by few common factors and find that this is not the case. The variance of

accounting error varies intuitively with a number of firm-level determinants, such as size, book-to-market,

operating cycle, etc. Finally, I document that both the performance component and accounting error are

priced by the auditor, as reflected in audit fees. However, the accounting error is priced at a much higher

rate. In sum, the approach I offer generates new insights regarding accruals that could not be obtained

previously.

The model of accruals can be generalized and extended in a number of directions, which would

allow a number of important questions about accruals to be addressed. A “frictionless” measurement

system would generate accounting error resembling “white noise” (reversing over time because of the

self-correcting nature of accrual accounting). This error should not exhibit inertia or be systematically

correlated with economic performance or timing error. Deviations from such properties generally must be

informative about different angles of accruals quality. Specifically, these properties may not hold in the

presence of accounting conservatism or systematic earnings management, such as income smoothing

(Gerakos and Kovrijnykh 2013). The framework developed in this paper naturally allows modelling and

understanding these (as well as other) properties of accounting error and the performance component of

accruals. I consider model extensions that incorporate and test for the presence of these frictions.

It is important to explicitly recognize that the current approach relies on identifying assumptions.

As in any empirical application, assumptions are necessary for a researcher to learn something from the

data. One advantage of the current approach is that it requires explicit consideration of the assumptions or

their violations before formulating the moment’s conditions. Another advantage is that accounting quality

can be identified under different sets of assumptions, as discussed above. Therefore, unlike more

conventional ways of measuring accounting quality, the current framework offers opportunities to select

models better suited to a particular application or industry (or even firm).

The quality of accounting information (earnings and accruals) is one of the most important and

widely researched areas in accounting literature (Dechow, Ge, and Schrand 2010). However, recent

decades have seen the accounting literature make relatively little progress in advancing models of

4

accruals. The existing accounting quality measures rely on the decomposition of accruals into

discretionary vs. non-discretionary (Healy 1985) and use the variance of a residual from the regression

models in Jones (1991), and Dechow and Dichev (2002). The main concern with the measures discussed

in the literature is that they do not offer a construct that can separate the error introduced in measuring

economic performance (accounting error) from the portion of accruals that reflects the underlying

economics, i.e., the performance component (Kaplan 1985, Dechow and Skinner 2000, McNichols and

Wilson 1988, McNichols 2002, Kothari, Leone, and Wasley 2005, Hribar and Nichols 2007, Dechow, Ge,

and Schrand 2010, Ball 2013). As a result, these measures in part capture true performance and its

economic variability. The approach offered in this paper is designed to overcome this issue.

I contribute to the literature in the following ways. First, I develop a new approach to modelling

accruals and understanding their quality. Specifically, I offer a novel model of accruals that explicitly

captures their performance measurement function (SFAC 1, Dechow 1994). Despite the centrality of

accruals in financial accounting, prior literature does not offer such a model. Second, I develop an

econometric strategy to identify and estimate the accounting quality parameters under different sets of

assumptions. In particular, the model allows identification of the variance of the performance component

in accruals, which is essential for understanding the demand for accruals. To my knowledge, I am the first

to exploit the notion that cash flow from operations and earnings reflects the same economic performance

and converge over extended horizons as identifying assumptions.2 Third, I implement several basic model

specifications empirically and show that they generate a number of new insights. To my knowledge, this

is also the first paper to quantify the performance component of accruals and to show that it considerably

exceeds the accounting error in accruals. Fourth, I consider several directions in which to generalize and

extend the model. I offer a way to incorporate the asymmetric timeliness of gains versus losses. I also

consider ways of decomposing the variance of “accounting error” into its “managed” and “unmanaged”

components and offer a novel way of testing for earnings management.

2 I also discuss why conventional proxies for accounting quality based on variations of the models in Jones (1991) and Dechow and Dichev (2002) do not separate economic performance from accounting error (irrespective of the assumptions) but instead measure a different construct.

5

My study complements prior models of accruals (e.g., Dechow, Kothari, and Watts 1998,

Dechow and Dichev 2002) and is related to several recent studies aiming to understand accounting

misreporting. Gerakos and Kovrijnykh (2013) use the idea that earnings management reverses over time

to predict second-order auto-correlation in the error term in an earnings auto-regression. Zakolyukina

(2014) also uses a structural approach to model and quantify intentional GAAP violations. Beyer,

Guttman, and Marinovic (2014) formulate a structural model of earnings manipulations under asymmetric

information. Based on a steady-state equilibrium that characterizes the dynamics of market vs. book

values of equity, they estimate the amount of reporting noise defined as measurement error in the reported

values of a firm’s (book) equity. These studies do not make the distinction between accruals vs. cash

flows and do not model accruals.

The paper’s objective is conceptual in nature. It intends to develop a new approach to modelling

accruals and to consider the identification of accrual accounting quality under several sets of assumptions.

Because the framework allows for estimating many different models that can be used to estimate a

number of different parameters, the issues of empirical implementation and the selection of the best fitting

model, which is also parsimonious and may vary by industry, is a task that lies outside its scope (see Leuz

and Nikolaev 2015). This study proceeds as follows. The next section develops the model and discusses

accounting quality. Section 3 lays out the identification strategy. Section 4 implements several model

specifications provides the empirical analysis. Section 5 considers further extensions of the model.

Section 6 discusses earnings management, and Section 7 concludes.

2. A New Representation of Accruals.

How well did a company perform over a period of time? There is no perfect way to answer this

question. The need to measure economic performance over relatively short time periods, such as quarters

or years, lies at the root of the problem. Different performance measures, such as accounting earnings,

operating cash flow, or stock returns, generally agree about a firm’s performance in the longer run (e.g.,

6

the Trueblood report, 1973, Easton, Harris, and Ohlson 1992).3 In the short run, however, these measures

can give very different answers. The measurement error present in different performance measures thus

has a key property: it arises from the difficulties in attributing (allocating) the underlying economic

performance to a particular time period, i.e., it is a timing error.

To make things more concrete, suppose is the true underlying economic performance over

period (to be defined later). One way to measure this unobservable economic performance is to rely on

cash flow from operations, , which is well known to be subject to the timing error. For example,

purchase of inventory occurs in period , while its sale occurs at 1 at which time it becomes a part of

performance. I model this as follows:

. (1)

This captures the textbook intuition that cash flow is a noisy measure of a firm’s performance. As

the performance measurement error reverses over time, the long run cash flow approximates the long run

economic performance, . In the case of deferred revenues or accrued expenses, is positive (cash

flow exceeds the underlying performance), whereas a case of accrued revenue or deferred expense

implies that is negative. For example, if a company made $100 in credit sales in period (all of which

will be collected), the timing error $100 and understates the true performance accordingly. In

period 1, the collection of $100 is not a part of the period 1 performance and hence 1 cash

flow overstates by $100.

The purpose of accruals is to eliminate the timing error in cash flows. To measure performance

“perfectly”, accountants need to book an accrual . However, the need to rely on

accounting measurement to determine this component introduces accounting error into earnings, , and

accruals. While the error is expected to be smaller, it shares a similar property:

. (2)

3 For example, a simple aggregation of cash inflows less cash outflows over a number of periods (excluding capital transactions with owners) will also succeed in reflecting a firm’s underlying economic performance. At one extreme, the total net cash inflow equals the true economic performance over the life of the firm.

7

As previously, earnings measure the economic performance with a high degree of accuracy over

longer horizons as the timing errors cancel out. A number of factors give rise to accounting error. First,

performance measurement requires making assumptions, estimates, and judgments, which gives rise to

estimation error. Second, error may occur because GAAP imposes constraints on what accountants may

report (e.g., Beyer et al. 2014). Even if a firm’s management observed the true performance, they must

follow GAAP measurement rules rather than just tell investors what the performance is. Third, error can

arise due to intentional earnings manipulations (which I consider in Section 6).

2.1 The implied characterization of accruals.

The above representation of earnings and cash flows implies a simple and intuitive

characterization of accounting accruals:

” ”

.” ”

(3)

The first component of accruals, ≡ , is the “performance measurement

component” of accruals or simply the “performance component”. Its role is to facilitate the measurement

of underlying economic performance relative to cash flow from operations (note that ).

When a firm’s business model leads to large timing errors in cash flow, the performance component is

particularly important. The second component of accruals, ≡ , arises because of

imperfections in accrual accounting. I refer to this component as “accounting error.” If a firm’s

management has incentives to report performance accurately (i.e., the incentives for earnings

management is small) the management will choose accounting methods or techniques that minimize the

variance of accounting error.

2.2 The economic performance.

What is the economic performance from an accounting standpoint? How does it differ from the

economic performance as measured by the change in stock prices? While performance measurement is at

the center of FASB’s (IASB’s) conceptual framework, the framework neither defines performance nor

provides clear answers to these important questions.

8

I define economic performance as the expected cash consequences of transactions or events

that took place in period (including the realized portion), provided that such transactions are subject to

accounting measurement. Analytically, performance is defined as follows:

| , (4)

where ∑ , is the sum of cash flows from all anticipated individual cash-generating

transactions taking place at time 1. Operator excludes future cash flows not subject to accounting

measurement at time . Specifically, ∑ , , is the sum of cash flows over all possible cash-

generating transactions taking place at time 1 multiplied by , 0,1 , which takes the value of

one when transaction is subject to measurement (recognition) under GAAP at time (typically as a

result of another transaction or event, e.g., delivery). Thus, unrealized performance in equation (4)

represents expected future cash flows subject to accounting measurement as of the end of period (e.g.,

net receivables). In contrast, the realized portion consists of (i) unexpected shocks to cash flows

anticipated and included in the prior period’s performance, | and (ii) cash

flows realized at time that were not subject to recognition at 1, 1 . Substituting

these terms into equation (4), we can express performance as:

| | . (5)

Performance thus can be expressed as cash flow less its expected portion included in ,

plus the expected cash flows from transactions in period 1. When | is positive (negative),

it represents the accrued (deferred) portion of performance, i.e., an asset (liability) on the balance sheet.

This clarifies that conceptually the timing error is an inverse of future expected cash flows:

| . Timing error, in a classic sense, is a shock to cash flow, , unrelated to current

performance: 1 and 0, e.g., as a result of investment (purchases of assets that will be

used in future periods) or taking credit (liability). For example, a purchase of inventory reduces and

increases | by the same amount. Postponing a payment to suppliers or employees increases

9

but reduces | . Timing errors thus introduce a strong correlation between and and not

between and . This implies that cash flows are more volatile than performance (if the opposite was

true, the variance of would exceed the variance of ). On the surface, it seems that economic

performance is subject to the timing error in the same way cash flow is. However, this is not the case, as

can be seen from the equation (4) given that cash flow shocks and are orthogonal (the implication

is that the true performance is sustainable).

An analogy can be made between accounting performance and market performance, which can be

defined as (inclusive of any dividends):

… | … | , (6)

where cash flows are discounted and information set is all information reflected in stock prices as of

time . This is analogous to a more general definition of accounting performance:

| | , (7)

where ∑ , , ∑ , , , and , 0,1 depending on whether an anticipated

future transaction, , is measured under GAAP at time .4 Future cash flows may or may not be

discounted under GAAP, depending on the accounting treatment (the accounting performance is defined

accordingly).

Thus, conceptual similarities exist between market performance and accounting performance.

However, there are also two key distinctions. First, accountants do not measure all cash flow

consequences of current economic transactions or events. For example, given that the distant cash flows

associated with delivering goods and services, , are uncertain, 0. If this happens for cash

flows with 1, equation (7) reduces to equation (5). For the case of working capital accruals that

estimate to cash flows within one year, 1.

Second, the information set that accountants have, , is different from the information set, ,

reflected by the stock price. Accountants do not observe all information that is impounded in stock prices.

4 Performance thus is a part of Hicksian income (Hicks 1946), i.e., excluding a portion of such income that is not subject to accounting measurement (e.g., changes in future prospects or growth opportunities).

10

At the same time, they have performance relevant information that market obtains from (the release of)

financial statements. The latter is something that makes accrual accounting valuable to investors. It is

important to note that accounting performance, , is defined with respect to the information set available

to accountants, , as opposed to being defined in some absolute sense or with respect to an arbitrary

information set. To the extent that accountants do not observe some information (which is always the case

in real life), the measurement and recognition of its cash consequences are deferred until this information

comes out (e.g., realization happens). In other words, hidden information is viewed as performance only

when it is discovered and becomes available to accountants.

2.3 Accounting error.

Accounting error arises from the difficulties associated with measuring (estimating) the expected

future cash flows, , given the information set available to accountants. Specifically, if ∗ as an

estimate of | , accounting error is defined as the difference between estimated and expected

cash flows:

∗ | | . (8)

This definition of accounting error is in line with SFAC 7, which discusses the distinction

between estimated and expected cash flows (expected cash flow is the sum of probability weighted

amounts in a range of possible estimates).

The estimation is unbiased when we have the following property:

| ∗ | | 0. (9)

2.4 Extended numerical example.

The model given by equations (1)-(4) captures the salient properties of accrual accounting. Let

me illustrate this with an intuitive example. Suppose a company generates $1,000 worth of sales in period

and collects $900 cash. Suppose the true probability of collection equal 95% while an accountant

estimates the probability to be 96%. What are the economic performance, timing, and accounting errors in

this case? The economic performance is: 900 100 ∗ 0.95 $995. The timing error is

11

accordingly: E collections 0.95 ∗ 100 $95, and the corresponding “perfect

accrual” is $95. Finally, the accounting error is E collections E collections

96 95 $1.

This has two implications for what happens in period 1. First, the reversal of the $1

accounting error will take place in period 1, when collections occur. If the actual amount collected in

period 1 is in fact $95, a $1 write-off corrects the $1 overstatement. The actual collection of

receivables, however, does not have to equal $95, which is the expected value. If the actual collections

were $92 ($98) instead, the unexpected cash flow shock is $3 ( $3 . This wedge between realized

and expected cash flows is not a part of accounting error but a consequence of new information unknown

at time . Since it was impossible to anticipate at time , and since it is both earned and realized at time

1, it is a part of . What matters most here is that the higher the overstatement of performance at

time , the lower the earnings at time 1. In contrast, true performance does not feature such reversal

patterns.

2.5 Understanding accounting quality.

Consistent with the Statement of Financial Accounting Concepts No. 8 (see also SFAC 1), I

define the quality of accounting earnings (accruals) in the following way: accounting quality is the extent

to which accrual accounting reflects the unobservable economic performance. The three components

responsible for the quality of accounting earnings and accruals are: the variability of economic

performance, ; the variability of the performance component, ; and the

magnitude of accounting error, . The first component, , the variance of the economic

performance, reflects uncertainty about the future or the riskiness of the business a company. Variance of

the performance component , the signal in accruals, reflects operating volatility, i.e., liquidity shocks to

which a firm’s business model is subject. The value added by accrual accounting increases in and this

component can hence be thought of as the benefit of using accruals. The performance component is of

particular importance to understanding the demand for accrual accounting. Finally, reflects the

12

noisiness of accruals and earnings and thus represents a cost of accrual accounting.

While these three variance components are interesting in their own right, one can also evaluate

accruals quality in terms of their signal-to-noise ratio, / , or its bounded counterpart:

AccountingQualityRatio ≡ ,

which is analogous to R2, showing the fraction of accruals’ variance explained by the performance

component. The numerator captures the signal contained in accruals (i.e., the benefit side), which is

scaled by the magnitude of the noise in accruals (the cost side). It is important to note that this ratio does

not capture all the aspects that characterize accounting quality. Depending on the research objective, the

variance of the accounting error or the variance of the performance component (or their correlation) may

be of interest. Additionally, one can quantify the quality of earnings and cash flows in terms of the

following signal-to-noise ratios:

r / E ≡ EarningsQuality, and r / C ≡ .

2.6 Distinctions from prior models of accruals.

The proposed model of accruals differs from those used in prior studies (e.g., Healy 1985, Jones

1991, Dechow, Kothari, and Watts 1998, Dechow and Dichev 2002). The most notable distinction is that

the model does not decompose accruals into discretionary and non-discretionary components (Healy 1985

and DeAngelo 1986). Conceptually, discretionary accruals aim to measure economic performance (but

may also contain manipulations) given that accounting discretion is granted to a firm’s management to

allow those with a better understanding of the firm’s economics to measure performance more accurately

(e.g., Watts and Zimmerman 1990). At the same time, both and components have discretionary and

non-discretionary parts. For example, may arise because management uses accounting discretion to

achieve a performance target or it makes a discretionary error when estimating, e.g., a bad debt expense.

At the same time, may also arise because a manager does not have full discretion over the reported

numbers under GAAP.

13

My model is also conceptually different from that in Dechow and Dichev (2002) (I provide a

detailed discussion in Appendix A). The central distinction is in the accounting error construct, namely,

whether it is an ex post vs. ex ante construct. In the Dechow and Dichev (2002) model, the accounting

error arises from the need to estimate cash flows unknown at time . This is done by accruing an

amount E . They define accounting (estimation) error as follows (see Dechow and Dichev [2002,

38]):

E E E :

E

:

. (10)

As the equation indicates, this error can be decomposed into two mutually uncorrelated

components. The first component is the difference between estimated and expected cash flow, which

reflects accounting. The second, , is driven by the arrival of new information or due to the occurrence

of economic events during the period 1. It is not a result of accounting error and in fact is outside the

accountants’ control. It represents a shock to future cash flows that could not be expected at time and

one should think of as a portion of 1 performance, rather than an error accountants make. Thus,

conceptually, the error in the Dechow-Dichev model does not separate the (ex ante) accounting error from

the ex post performance.5

2.7 Reconciling different views on accounting quality.

Dechow et al. (2010), among others, argue that accounting quality is viewed differently by

different users of accounting information (e.g., debtholders vs. shareholders). This view does not

contradict the view in this paper. Irrespective of who uses the accounting information, the decision maker

is ultimately interested in understanding the economic performance, , and separating it from accounting

noise. However, different users of accounting information may disagree about the measurement and, as a

5 To appreciate this distinction more fully, consider mark-to-market accounting for marketable securities. At any point in time t, liquid markets guarantee prices that measure future expected cash flows from the sale of these securities with a very high degree of accuracy. Thus, ex ante, we know that accounting quality is very high. However, the actual future cash flows realized at time t+1 from the sale of these securities can be very different given that prices can move considerably in response to new information. Such ex post movement is not a part of accounting error in my model.

14

result, the properties of accounting error. In particular, different users place different weights on

information qualities, such as neutrality, conservatism, relevance, reliability, and consistency, all of which

can have an effect on . The question thus becomes: what are the desirable properties of accounting error

? This question is of primary importance in the accounting literature. In a statistical sense, we would

like to resemble white noise that has low variance and is self-corrected (i.e., reverses) over time. In a

world with frictions, e.g., earnings management, such an outcome may or may not be attainable and hence

the properties of accounting error are shaped by the demands from different parties and involve tradeoffs

(e.g., relevance vs. reliability).6 As I discuss further, the approach I offer can be used to study the

properties of accounting error (e.g., conservatism, or correlation with performance), and thus can prove

instrumental to understanding the economic tradeoffs related to accounting measurement.

3. Identification of Accounting Quality.

The key question in the accounting literature on earnings quality is how to separate the

underlying economics, i.e., the portion of accruals that captures economic performance from that which

reflects the error in measuring such performance. This challenging task requires explicit consideration of

the identifying assumptions. The central idea of this paper is that the institutional properties of accounting

processes, namely that (1) cash flows and earnings share the same performance components and (2) the

accounting error in accruals and the performance component reverse over time, serve as a “hook” to tease

out the economic performance in accruals and separate it from accounting error. These properties are

embedded into the model given by equations (1)-(3) above and shape the moment conditions among

accounting time series. It is necessary to make additional statistical assumptions that capture the statistical

properties of both accounting error and performance. The identification of accounting quality is feasible

under different sets of assumptions, as I will discuss throughout the paper.

3.1. Regression-based approach.

6 While some users would prefer a measurement system that is immune to manipulations (e.g., when writing accounting covenants) and hence emphasize reliability, others may look past earnings management when discovering a stock price and could thus emphasize the relevance dimension of accounting information (e.g., fair value measurement).

15

To begin the discussion of identification issues, it is useful to consider a regression-based

approach to earnings quality. If one had a set of determinants that fully explained the performance portion

of accruals, , the identification of accounting error in accruals would be

straightforward. One could effectively control for by using these determinants in a linear regression

and take the variance of the residual from this regression as a measure of accounting error. This is the lens

through which prior measures can be viewed. The two primary methodologies for measuring the quality

of accruals (the seminal contributions of Jones (1991) and Dechow and Dichev (2002) as well as a

number of their variations), use linear regressions to control for the “normal” or non-discretionary portion

of accruals. The variance of the residuals from these models (i.e., abnormal or discretionary accruals) are

used as measures of accruals (earnings) quality (e.g., Francis et al. 2004).

The first thing to note about the regression approach is that it requires identifying assumptions.

Even if one could effectively control for the performance portion of , running an OLS regression

implicitly assumes that that all the determinants of and are uncorrelated. A more fundamental issue,

however, is that this approach, in principle, cannot fully control for using observable variables. If one

could control for with a high degree of accuracy, one would be able to provide a better solution to the

problem (performance measurement) that GAAP is trying to solve using accruals. This contradicts the

logic of having GAAP in the first place. As a result, the regression approach cannot fully isolate the

performance component of accruals to obtain an estimate of accounting error irrespective of the

identifying assumptions one is willing to make. Consistent with this argument, a number of studies

express a concern that measures of accounting quality do not isolate the economic performance present in

accruals (e.g., Dechow, Ge, and Schrand 2010, Wysocki 2009). See Appendix A for additional

discussion.

3.2. Identification strategy and assumptions

My identification strategy relies on the model given by equations (1)–(3) to tease out the

parameters of interest. I propose using moment conditions of the accounting time series: earnings, cash

16

flows, and/or accruals, in combination with the model given by equations (1)–(3) as a basis for

identification of the accounting quality parameters. For example, if accountants make a measurement

error (random or intentional) by overstating receivables in the current period, all else equal, the future

earnings are expected to be lower by the same amount. At the same time, true performance should not

exhibit reversal. These properties allow for statistical discrimination between performance and accounting

error.

It is also necessary, however, to make additional statistical assumptions about the unobservables,

, , and , in order to estimate their variances. While the model can be estimated under different sets

of statistical assumptions, I begin by discussing a benchmark case that serves as a basis for more

complicated models. Subsequently, I discuss how some assumptions can be relaxed or avoided to

improve model specification.

The benchmark case is motivated by what may be thought of as a “frictionless” measurement

system. In such a system, accounting error should resemble white noise, uncorrelated with the economic

performance or the timing error in cash flows. Accordingly, I make the following baseline assumptions:

Assumption A. The process has a finite variance and is uncorrelated with errors and .

Assumption B. The vector of errors , is a white noise vector (independent and serially

uncorrelated variables with finite variance).

Zero correlation between and (and and ) follows from the assumption of unbiased

estimation, E | 0. The idea is that if accountants systematically over- or under-accrued when

accounting for performance fluctuations (i.e., a positive (negative) correlation between economic

performance and accounting error), then it would be possible to adjust the estimation technique in a way

that reduces accounting error. Recall that | and

| , i.e., they only depend on information known by the end of time . This

implies that the unconditional moments 0. This follows from the law of

17

iterated expectations: | | 0.7

The assumption that and are uncorrelated captures the classic notion of timing errors in

cash flows. Is it possible to tell whether it is likely to coincide with a positive timing error or the negative

one? For a mature company (one that is close to a steady state) it is generally not possible to tell. An

unexpected positive shock to economic performance is not more likely to create the need for accrued

performance (negative than deferred performance (positive ).8

Turning to serial correlation in accounting error , the persistence or inertia of this error presents

opportunities to learn from prior errors and hence improves an estimate’s quality. As a benchmark case,

the errors should be serially uncorrelated. Similarly, as a benchmark case I make the same assumption

about to capture the notion of random shocks to cash flows.

An important advantage of using assumptions A and B is the model’s parsimony. However, it is

possible to change or relax these assumptions in a number of ways. I consider such generalizations in

subsequent sections of the paper.

3.3. Moment conditions.

Recall that the processes for earnings, accruals, and cash flows are as follows:

. (1)

. (2)

. (3)

In conjunction with assumptions A and B, this structure allows for the identification of the

variance of the performance component of accruals, ; the variance of the accounting estimation error,

; and the variance of the shocks to economic performance, . This requires selecting moment

conditions that are informative about the parameters of interest and that are based on assumptions that are

7 For example, suppose E collections | , i.e., the probability of collection times credit sales, while accountants estimate collections to be ̂ . In this case, ̂ ̂| 0.

8 Even growth does not imply a correlation with timing errors as, on one hand, a company will build up inventory or accounts receivables but, at the same time, it will increase payables and accrued expenses. At least a priori, it is not clear that a systematic correlation exists and what its sign should be.

18

likely to be descriptive (Andrews and Lu 2001). The choice of moments is not guided by econometric

theory and is more an art than a science. In general, moments should be chosen to provide substantial

information about the parameters of interest, i.e., changing a parameter should have a first-order effect on

the moment (thus, for example, moments based on distant lags, , are unlikely to be useful as they

are close to zero). Additionally, moments that rely on assumptions that are unlikely to be met should be

avoided. Finally, moments that are linearly dependent will not add information (e.g., moment E

does not add information if moments E and E are used).

The following set of moment conditions suffices to identify the parameters of interest under the

baseline assumptions, although other moments can be used as well (for example, the moment E

can also be useful). Note that all variables are measured as deviations from their means.

1 : E 2 ,

2 : E 2 ,

3 : E 2 2 ,

4 : E ,

5 : E ,

6 : E ,

where is the first-order auto-correlation of economic performance , i.e., the persistence of the

underlying economic performance.9 These moment conditions present six equations with four unknowns.

The first three equations facilitate identification by exploiting the information in two different

performance measures, whereas the last three moments also exploit the reversal in the error components.

GMM estimation can be used to identify and consistently estimate the parameters , , , and at

the firm or industry level.10

As an alternative set of moments, one can use changes in the time series of earnings, cash flows,

and accruals. In this case, it is important to account for differences in the dynamics of the three time

9 Note that the moment conditions are still meaningful even if the parameters change over time. Suppose ,

| , which is a conditional expectation based on information, e.g., some type of economic shock, at time . In this case, ≡ | , , where the first equality follows from the law of iterated expectations. In other words, moments should be interpreted in terms of the unconditional (average) variance of, for example, accounting error and other variables. One could also consider modelling , as a function of time and firm characteristics. 10 Maximum likelihood can also be used to estimate these parameters. Doing so generally increases the efficiency of the estimates but requires distributional assumptions such as normality.

19

series. For example, the differenced version of the accrual process given by equation (3) is as follows:

2 2 . (11)

The differenced formulation implies the following set of moment conditions:

1’ : E ∆ ∆ ∆ 6 ,

2’ : E ∆ ∆ ∆ 6 ,

3’ : E ∆ ∆ 6 6 ,

4’ : E ∆ ∆ ∆ ∆ 4 ,

5’ : E ∆ ∆ ∆ ∆ 4 ,

6’ : E ∆ ∆ 4 4 ,

where ∆ is the first-order auto-correlation of changes in the economic performance, ∆ .

This set of moments is more robust to certain types of misspecification. First, the process may be non-

stationary (e.g., a random walk), in which case the variance of increases without a bound (i.e.,

assumption A is violated, which means that the parameters cannot be estimated consistently). However,

process ∆ is more likely to be stationary. Second, differencing effectively eliminates a persistent

component of accruals due to, for example, growth or the presence of long-term accruals, such as

depreciation, amortization, and deferred taxes, which is a potential source of misspecification in an

empirical implementation.

3.4 Generalized versions of the model.

In the remainder of this section, I discuss how the baseline assumptions can relaxed or avoided.

For example, the timing error, , may be auto-correlated and/or exhibit some correlation with

performance due to growth. Accounting error may be correlated with timing error (this may be a

consequence of accounting conservatism, as discussed in Section 6). Finally, the underlying economic

performance may be correlated with accounting error due to earnings management (Healy 1985,

McNichols and Wilson 1988, Gerakos and Kovrijnykh 2013). In this and subsequent sections of the

paper, I consider scenarios that allow for these possibilities.

Several directions to generalize the model deserve consideration and involve different tradeoffs.

For example, relaxing assumptions by increasing the number of parameters can improve the fit but also

lower the loss of reliability in the estimates (particularly when the time series are short). With this in

20

mind, several directions deserve consideration.

Approach 1. The first direction to modifying the baseline set of assumptions at the firm level is to

assume a pre-specified non-zero correlation structure among the unobservable components. This is an

easy way to capture the correlations discussed above without changing the number of parameters to be

estimated. For example, instead of assuming zero correlation between and , growth firms may

exhibit to a negative correlation, e.g., 0.33. It is straightforward to allow for such a correlation. Ideally,

this number would come from a theoretical model. As an alternative, certain parameters in the pre-

specified correlation structure can be estimated separately, e.g., at the industry-level. Finally, this

approach can be very helpful in checking the sensitivity of the results to model misspecification.

Approach 2. Another direction to relaxing the baseline assumptions is to increase the number of

additional parameters in the model. To do this, it is either necessary or convenient to assume a certain

process for , , and . This is reflected in the following modified set of assumptions.

Assumption A1. Process follows auto-regression, , and (i) corr ,

for 0 and zero otherwise; (ii) corr , for 0 and zero otherwise.

Assumption B1. (i) corr , for 1 and zero for | | 1; (ii) corr ,

for 1 and zero for | | 1; (iii) corr , for 0 and zero otherwise.

Under this set of assumptions, we have nine parameters of interest ( , , , , , , ,

, ), and thus require at least nine linearly independent moment conditions. One could use an

analogous set of equations, E , E , and E , with taking a value from 0 to 4,

which amounts to 16 moments. A potentially more compelling specification is to effectively “difference

out” the auto-correlated performance by substituting into the earnings equation

(proposed by Gerakos and Kovrijnykh 2013) and similarly into the cash flow

equation:

1 ,

1 , (12)

21

.

There are a number of ways that these equations can be used to formulate moments (note that the

last equation is no longer a linear combination of the other two equations). One convenient possibility is

to use moments of the form:

E )( 2 2 1 2 1 .

I provide the complete set of moments, up to three lags, in Appendix C.1. Another possibility is

to multiply both sides of the first equation by (second equation by ), which is analogous to the

Yule-Walker equations. An obvious limitation of this brute force approach is that it adds considerably

more parameters (and algebraic complexity), which is problematic when the time series are short.

Approach 3. The third direction involves altering the baseline assumptions to specify a

parsimonious alternative. For example, one can allow for auto-correlation in the timing errors as well

as for their correlation with performance by assuming that the timing error in cash flow has the form

, such that:

. (13)

This structure of accruals may be descriptive for some business models and preserves the number

of parameters to be estimated.

Approach 4. Finally, a promising way to preserve model parsimony is to incorporate possible

growth via firm characteristics. In particular, to accommodate a possible persistence in the timing error

and simultaneously allow for its correlation with performance, the timing error can be modeled as a

function of firm characteristics correlated with performance (but uncorrelated with accounting error, i.e.,

instruments), such as firm size, market capitalization, growth in fixed asset base, and stock performance.

Specifically, let’s define cash flow ∗ ∗ and ∗ . The systematic

component, , is correlated with performance and autocorrelated over time, whereas is an

orthogonal non-systematic component. In this case, the model can be written as:

.

22

∗ Δ . (14)

∗ Δ .

Knowledge of allows adjusting accruals and cash flows in a way that accommodates the

presence of the systematic performance component (which may be correlated with performance or over

time in any arbitrary manner) effectively eliminating its effect. In such a case, the baseline assumptions A

and B, with respect to , , and , are less likely to be violated. Note that can be identified

separately (or simultaneously) based on the following moment conditions:

∆ ∆ ∆ 0. (15)

Given that ∆ 0 by assumption.

In sum, there are a number of directions for relaxing the baseline assumptions and addressing

potential misspecifications. These offer a number of opportunities for future research.

4. Empirical Implementation

The primary objective of this paper is conceptual: it offers a new approach to modelling accruals

and measuring accounting quality. Uncovering model specifications that have the best fit with the data,

which can vary by industry or even firm, is a non-trivial task that lies outside the scope of this study. To

demonstrate that the proposed approach has a straightforward implementation and that it generates

plausible results, I estimate three parsimonious model specifications. First, I estimate a “levels”

specification based on moments (1-6), described in Section 3.2. Second, I estimate a “changes”

specification based on moments (1'-6'), described in the same subsection. This specification addresses

possible non-stationarities in performance via differencing. Third, I use generalized specification based on

Approach 4, outlined in Section 3.3. This specification relaxes baseline assumptions by allowing for a

systematic component of the timing error, potentially correlated with performance. The set of

instrumental variables ∆ consists of changes in the log of market capitalization (∆log ), changes in

the log of non-current assets (∆log ), and changes in the ratio of market value of assets to book value

23

of assets (∆ / ). These variables are assumed not to exhibit correlations with accounting error. Both the

second and third specifications aim to accommodate variations of firm growth in the time series.

The primary empirical questions of interest are: Does the performance component in accruals

exceed the amount of accounting noise? What fraction of variance in accruals is explained by the

performance component? The answers to these questions are fundamental to the economic justification

for the use of accruals. I also explore whether the variance components , , and are economically

different or whether they vary in the same way with a set of common determinants. Finally, I explore

whether these parameters are differentially priced by the auditors.

I use data from Compustat for the period from 1987 to 2015 to address this question and also to

conduct several other types of analysis. I conduct the analysis at the industry level and then at the firm

level. To estimate the firm-level parameters, I require 15 or more observations per firm with non-missing

values for accounting variables. I defer details on sample construction and variable measurement to

Appendix B. The resulting sample consists of approximately 2,200 firms, spanning 39 industries. Table 1

provides the summary statistics for the variables used in the estimation and subsequent analysis.

4.1 Does the performance component of accruals dominate accounting noise?

Table 2 presents parameters of interest estimated by industry using GMM. Panels A-C present the

estimates based on the “levels”, “changes”, and “generalized” model specifications, respectively. Panel A

indicates that the average (median) standard deviation of economic performance, , is 0.055 (0.053).

This is the largest parameter in terms of economic magnitude. It is followed by the average (median)

standard deviation of the performance component of accruals, , which is equal to 0.026 (0.025). The

average (median) standard deviation of the accounting error, , is 0.018 (0.017). Panels B and C show

similar and even somewhat more pronounced results. For the “changes” specification, the parameters

and are 0.024 and 0.013, respectively, whereas for the generalized model they are 0.026 and 0.015,

respectively. In all three cases, the differences are positive and highly statistically significant.

The results in this panel contrast substantially with the explanatory power based on traditional

24

regression models. The performance component of accruals explains a much greater fraction of accruals

variance as compared to the variance explained by the regression models. In particular, the average

(median) accounting quality ratio, / , ranges between 0.68 (0.67) and 0.75 (0.76). In contrast,

Panel D indicates that the R2 based on the Jones (1991) or Dechow and Dichev (2002) models are on

average (median) 0.07 (0.07) and 0.35 (0.35). These results confirm that the residual variation in these

models measure (conceptually) different constructs. My findings in Table 2 are more in line with Beyer et

al. (2014), who use equilibrium conditions to derive industry-level estimates of accounting noise present

in the book values of equity. They find that the ratio of the variance of accounting noise to that of

economic performance is roughly 50%. While the parameters are not directly comparable (due to scaling

and given that they do not use accruals or cash flows), this is broadly consistent with my findings that

accounting error is under 50% of the variance of economic performance.

Table 3 presents the analogous set of results estimated by firm. As previously, the “levels”,

“changes,” and the generalized specifications are reported in Panels A-C, respectively. The results at the

firm level are similar to the industry-level findings. Panel A indicates that the average (median) standard

deviation of economic performance, , is 0.051 (0.044). It is followed by the average (median) standard

deviation of performance component, = 0.022 (0.020), and subsequently by the accounting error

component, = 0.015 (0.012). The magnitudes of the average (median) performance and accounting

error components in Panel B are = 0.021 (0.018) and = 0.011 (0.009), respectively. Panel C indicates

that = 0.020 (0.018) vs. = 0.011 (0.009). All these differences are highly significant. The mean

(median) accounting quality ratio, / , ranges between 0.65 (0.71) to 0.71 (0.79), which

continues to contrast markedly with the average explanatory power of the regression-based models in

Panel D.

The evidence in Tables 2 and 3 confirms that, across three model specifications estimated both at

the industry and firm levels, the magnitude of the performance component in accruals dominates the

accounting error component. This constitutes evidence that accrual accounting improves performance

25

measurement compared to cash flow-based measures, in line with SFAS 1 and 8. My results support the

notion that for users of financial statements, the benefits of accrual accounting outweigh the costs.

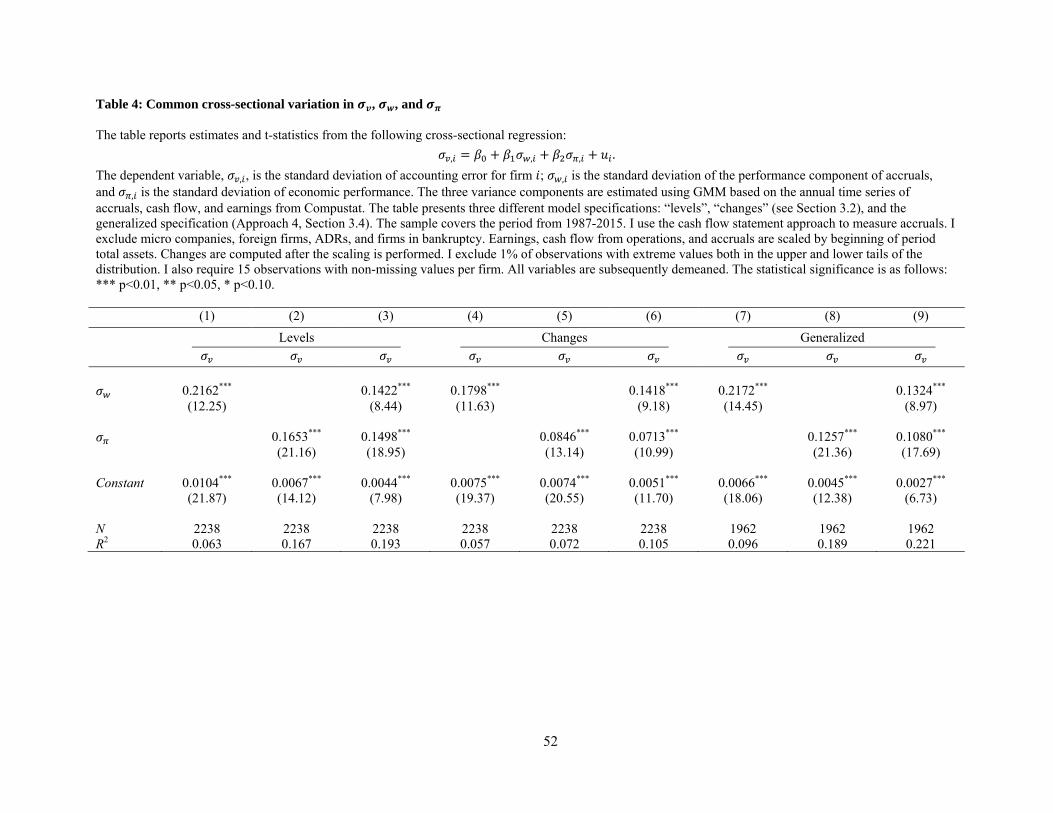

4.2 Does accounting error share much common variation with performance?

The question that arises next is whether the variance components, , , and , share much

common variation cross-sectionally, i.e., are they driven by the same set of the factors? I investigate this

question in Tables 4 and 5 by examining their cross-sectional determinants. Table 4 presents the results

from the following cross-sectional regression based on parameters from the three previously identified

model specifications:

, , , , (16)

where is a firm subscript.

The results indicate that both , and , exhibit positive and highly significant associations

with , across the “levels”, “changes”, and generalized specifications. Such results are intuitive, as

greater uncertainty about economic performance or timing error is likely to be associated with the

presence of errors when measuring performance. However, when included individually, , explains

only 6-10% of the variation in , , depending on model specification. Jointly, , and , explain up to

22% of the cross-sectional variation in , . Overall, it does not appear that the three parameters are driven

by the set of a few common factors.

4.3 Determinants of variance components σ , σ , and σ .

Table 5 explores economic determinants of the three variance components: , , and , based

on the following cross-sectional regression:

, (17)

where is one of the three variance components and is a vector of firm-

characteristics. The firm characteristics I examine include size (Size); number of employees (Employees);

uncertainty (Uncertainty); book-to-market ratio (B/M); leverage (Leverage); profitability (ROA); liquidity

(Liquidity); operating cycle proxies, namely, days in accounts receivable (Days receivables) and

26

inventory (Days inventory); as well as the length of the fixed assets life cycle (Asset life). These variables

are averaged over the same period over which the parameters of interest are estimated.

The table indicates a number of significant associations between each variance component and its

determinants. The coefficient estimates are overall consistent across the three model specifications. In

many instances the results are intuitive. Size is negatively associated with both accounting error and the

timing error (and with performance when Employees is omitted). As one would expect, higher

Uncertainty is associated with greater values for all three parameters, , , and . In contrast, higher

Leverage or longer Asset life are associated with lower values for the parameters. Interestingly, the

remaining explanatory variables do not exhibit associations of the same sign across , , and . As

one would expect, the operating cycle (Days receivables and Days inventory) exhibits a positive link with

accounting error. At the same time, it is negatively associated with the variance of economic performance.

Employees is associated with a lower variance of economic performance but not accounting or timing

errors. B/M, and Profitability exhibit a negative association with accounting error but are positively

related to the timing error. While understanding the explanations behind these associations more fully is

outside the scope of this paper, the main takeaway from this analysis is that the three variance

components appear to be explained by different economic factors.

4.4 Is the accounting error vs. performance component priced differently by the auditor?

The last question I explore empirically is whether there are different pricing implications to

accounting error vs. timing error as far as auditors are concerned. While the auditors will generally not be

able to identify accounting (estimation) error and separate it from timing error, they should be able to tell

when such errors are more likely to be present. I hypothesize that auditors will price both accounting error

and timing error in accruals as both of these create the demand for accrual accounting and hence for an

audit. However, I further hypothesize that the accounting error will be priced at a higher rate because it

imposes additional risk on the auditor (e.g., Hribar, Karvet, and Wilson 2014). To test this hypothesis, I

run the following regression:

log ∑ , (18)

27

where the control variables include a broad set of firm characteristics known to be associated with audit

fees in prior studies (e.g., Simunic 1980, Hribar, Karvet, and Wilson 2014). Because it is not always clear

that it is necessary to control for certain firm characteristics, as they may be correlated with accounting

quality, I estimate the model with and without controls (except for Size, given the nature of the dependent

variable).

The results for this analysis are presented in Table 6. The analysis suggests that all three

components explaining the variance of cash flows and accruals are priced by the auditor. The component

with the lowest pricing multiple is the volatility of economic performance. It is followed by the volatility

of the performance component of accruals. In other words, the variance of high quality accruals is priced.

These results are consistent with the notion that unexpected changes in firm performance as well as the

presence of timing errors increase the demand for an audit. However, the evidence indicates that

accounting error has the highest audit pricing implications. A unit of variance of accounting error is

priced at approximately double what a unit of timing error is priced at and is over five times the pricing of

the variance of economic performance.

As a robustness check, I repeat this analysis using the ratio of audit fees to total assets as the

dependent variable. This analysis is reported in Table 7. While the magnitudes of the coefficients are

different, the inferences are largely unchanged. In fact, the results are even more pronounced, particularly

when the control variables are added (in which case the performance component becomes insignificant).

Overall, the results from this analysis are in line with the prediction that the variance of accruals

explained by accounting error vs. performance is priced differently. More generally, the analysis in this

section suggests that my approach to modelling accruals is straightforward to implement and that it

generates a number of new insights about accruals undocumented elsewhere.

5. Model Extensions

The model can be generalized in several ways to more explicitly capture certain properties of

accruals, such as conditional conservatism in earnings and one-time non-reversing items (disruptions to

28

accounting time series caused by significant events such as acquisitions or divestures (Hribar and Collins

2002)) or slow reversal patterns.

5.1 Incorporating accounting conservatism.

In this section, I discuss how the model can explicitly accommodate accounting conservatism – a

property of accrual accounting that has received much attention in the literature (e.g., Basu 1997, Chen,

Hemmer, and Zhang 2007, Ball and Shivakumar 2006, Nikolaev 2010, Gao 2013, Collins, Hribar, and

Tian 2014, among others).11 Ball and Shivakumar (2006) argue that accruals also accelerate recognition

of the unrealized economic losses and not gains that arise due to changes in expectations of future cash

flows. They argue that the inability to take this effect into account constitutes an important criticism of

discretionary accruals models. This view is consistent with accruals generating a better measure of

economic performance and unrealized gains and losses also being viewed as timing errors in cash flows.

The key issue here, however, is that the unrealized losses and gains follow an asymmetric treatment.

The approach offered in this paper can directly accommodate the asymmetric treatment of shocks

to economic performance. Given that the focus here is on the working capital accruals, let me start by

illustrating the intuition with an inventory impairment example, which follows the lower cost or market

rule. All else equal, consider a loss in inventory value of $100 that occurs in the present period

but is not realized until the next one, when the inventory is sold at a residual value. This loss implies a

timing error in cash flows $100 and requires a negative accrual of $100 to offset the

timing error. By analogy, an unrealized gain in the value of inventory $100 implies an equivalent

timing error in cash flows $100. Without a conservative treatment of gains, an accrual

$100 should be recorded. Because a conservative treatment of gains does not consider the $100 as current

income until the time of sale, it introduces a “conservative error” $100 into earnings (and

accruals). Not that such treatment can be an efficient way of offsetting managerial incentives to overstate

11 It is important to note that the presence of conservative accounting measurement need not lead to “conservative error.” Ideally, the effect of conservatism on earnings will precisely offset any positive bias a firm’s management may introduce, such that the resulting accounting error resembles white noise (and its reversal). See, e.g., Gao (2013). In practice, however, conservatism is likely to affect the properties of accruals and accounting error and in such cases, it should be possible to statistically detect it.

29

reported earnings and thus differs from estimation error more generally. One implication of the

asymmetric treatment of gains and losses is a non-linear correlation between and .

To allow for such properties in the accrual process, one can generalize the model in the following

way:

,

, (19)

c ,

where and represent the timing error in the absence of unrealized gains and losses, which follow an

asymmetric treatment (i.e., in the previously discussed sense). The component represents unrealized

gains (losses) that occur in the present period and is thus subject to asymmetric treatment. This

component is a part of economic performance but it falls out from the current cash flow due to its

timing error, . Because the conservative accounting treatment defers gains but recognizes losses, c

is expected to be zero for negative news, which is recognized in a timely manner, whereas it is expected

to be equal to in the case of unrealized gains that are deferred until realization.

Given the argument above, a natural candidate for the function c(.) is c max 0, .

Intuitively, when is negative, such as in the case of a decline in the value of inventory, the loss is

accrued in the same period, i.e., , whereas the corresponding part of accounting error, max 0, ,

is zero. In contrast, when is positive (as in the case of unrealized gain), conservative accounting

precludes recognition of , so that 0, whereas max 0, . The proposed way of

modelling asymmetric timeliness is equivalent to that in Ball, Kothari, and Nikolaev (2013).

Let’s assume that in the absence of unrealized gains and losses accompanied by conservative

accounting treatment, i.e., when the variance of is zero, the baseline assumptions A and B apply to the

components , , and , as previously. It is necessary to add statistical assumptions about to

formulate moment conditions:

30

Assumption C. The unrealized gain (loss) is uncorrelated with , , and and follows a

distribution symmetric around 0.

Under these assumptions, the following expectations will be satisfied:

E ,

E E max 0, g 0.5 ,

E E max 0, 0.5 ,

E E ,

E E max 0, 0.5 .

This structure relaxes the baseline assumptions we made earlier in a particular way allowing for

the asymmetric timeliness of unrealized gains and losses. The assumption of symmetry appears to be, at

least roughly, descriptive for many gains and losses (e.g., increases in cost of inventory seem to be as

likely, on average, as decreases).12 These expectations include an additional parameter, , and can be

straightforwardly integrated with the moment conditions discussed earlier. Doing so allows the estimation

and isolation of the portion of accruals explained by accounting conservatism, as well as the variances of

the remaining components of accruals.

5.2 Disruptions in accounting time series due to significant changes in the firm.

Hribar and Collins (2002) show that significant changes to a firm’s business, namely mergers and

acquisitions or divestures, introduce disruptions to the time series of accruals. While accruals from the

statement of cash flows can alleviate this issue, Owens, Wu and Zimmerman (2015) still find that

significant economic events such as mergers and discontinued operations inflate the proxies for

discretionary accruals. While issue applies to a lesser extent to working capital accruals, which are

typically used to measure accounting quality, it is useful to consider a way of addressing the presence of

disruptions in the accruals within the current framework.

12 One can also consider dropping the symmetry assumption by adding an extra parameter, . In this case, the following modifications occur: E E max 0, , E E max 0, , and E E max 0, .

31

The presence of a significant event does not always lead to a problem. For example, accruing a

large loss, e.g., due to litigation settlement, is a part of (an adverse shock to) current economic

performance. To the extent that we consider how to separate the current performance from accounting

error, this does not create a problem. This is different when an event introduces a one-time shock to

accruals or cash flows that is neither informative about the core operating performance nor should be

viewed as a part of accounting error, as would be the case for acquisitions or divestitures. Such

“disruptions” in the accruals time series can be modelled as a random variable whose sign and magnitude

depend on the nature of events as well as on other circumstances. Accordingly, let’s assume shock

affects accruals only in time periods when certain events take place. A possible disruption to cash flows

can be viewed in terms of a similar, possibly correlated, shock .

To accommodate such a scenario, the model can be modified in the following way:

,

, (20)

,

where ∈ 0,1 indicates whether an event takes place. The variables can be a result of mergers and

acquisitions, write-offs of non-current assets, discontinued operations, or special items and the associated

cash outlays. For simplicity, let’s assume that and are uncorrelated with other variables, such as

the core economic performance, and that the baseline assumptions apply. The variables and can

be correlated and can have non-zero means. In this case, the first three moment conditions (m(1)-m(3))

from Section 3.4 are modified as follows:

2 2 ,

2 ,

2 ,

where 1 . While these moments include more parameters, we now also can exploit an

additional set of moments:

32

E | 1 E | 0 ≡ ∆ ,

E | 1 E | 0 ≡ ∆ ,

E | 1 E | 0 ≡ ∆ ,

.

The quantities ∆ , ∆ , ∆ and can be computed separately and substituted back into the three

preceding moments for second stage.13 The GMM solution to these moments is a way to address the

presence of disruptions introduced into accruals by a significant event, such as mergers within the

proposed framework. What’s more, the number of parameters to be estimated remains effectively the

same as it was previously.

6. Modelling Earnings Management.

Up to this point, I have not considered how to discriminate between a “managed” (intentional)

component in accruals and a random error. In this section, I discuss several directions for accommodating

earnings management and how one can test for earnings management within the proposed framework.14

To allow for earnings management, one can break down accounting error as follows:

, (21)

where is a managed component of accounting error and is the portion of accounting error defined

as being orthogonal to the managed component. To separate the managed from the unmanaged

components, it is either necessary to exploit the incentives for earnings manipulations. These incentives

may arise from income smoothing considerations, as in Gerakos and Kovrijnykh (2013), or can be

captured by some external “partitioning” variables (e.g., Dechow, Sloan, and Sweeney 1995, Dechow and

Skinner 2000). I discuss these alternatives in the remainder of this section.

13 If one assumes that significant events affect accruals (cash flows) for two consecutive periods, one may further adjust the moments for quantities, E | 1 E | 0 ≡ ∆ ′, etc. 14 Dechow, Hutton, Kim, and Sloan (2012) and Gerakos and Kovrijnykh (2013) also exploit the reversal to estimate earnings management. Dechow et al. (2012) primarily use reversal as a way of gaining statistical power to detect earnings management rather than as an identification tool (identification comes from the specification of the exogenous partitioning variable); although they also argue that reversal improves the model specification. Gerakos and Kovrijnykh (2013) focus on the reversal of earnings management and do not model accruals or earnings quality more generally. These studies do not take advantage of the reversal of the performance component of accruals.

33

6.1 Modelling earnings management: Income smoothing.

Gerakos and Kovrijnykh (2013) argue that earnings management is manifested in earnings via

income smoothing (they do not model accruals and cash flows). They show that incentives to smooth out

shocks to economic performance arise under a fairly general set of managerial preferences.15 In line with

this intuition, they model earnings using the following dynamic structure:

, (22)

where true (unmanaged) economic performance, , follows an AR(1) process, . Based

on this assumption, earnings follow an ARMA process with a negative second-order auto-correlation of

the error term (see equation 12). They test for this auto-correlation of the error term and confirm their

predictions.16 Note that this model effectively assumes that the entire accounting error in accruals is due

to earnings management, i.e., 0 and . Otherwise, the model is not identified.

The approach offered in this study allows this assumption to be relaxed, such that the accounting error

includes both an unmanaged error and the income smoothing component:

. (23)

Assuming that baseline assumptions A and B are applicable under the null hypothesis of no

earnings management, i.e., when var 0 and , the following moments will be satisfied:

E , and E .

These expectations imply a straightforward modification to the moment conditions formulated

under baseline assumptions A and B and can be used to identify the parameters of interest. I defer the

details to Appendix C.2. The advantage of a moments-based estimation is that parameter can be

estimated directly as opposed to using the second-order auto-correlation of earnings residual suggested by

Gerakos and Kovrijnykh (2013). Additionally, this does not require the normality assumption necessary

for estimating the ARMA process.

15 Income smoothing is sometimes viewed as a way of eliminating noise in cash flows. The meaning I use is different: here, income smoothing results in earnings time series that exhibit a lower volatility compared to the volatility of the true underlying performance. 16 Estimation of the ARMA model requires distributional assumptions, namely, normality.

34

6.2 Directional tests of earnings management.

Another way to introduce earnings management is to rely on external information about