icici pru report prabhakarc

DESCRIPTION

ffsfsd d d c c df dc d sdvs azd z sd f dv d dTRANSCRIPT

Summer Internship Report

On

For

ICICI PRUDENTIAL LIFE INSURANCE CO LTD

Submitted By:

ACKNOWLEDGEMENT

We are thankful to management of ICICI Prudential Life Insurance

Company Ltd for granting the opportunity, corporation and valuable

information for completion of this project.

No words are enough to thank Mr.Vipin Anand (Channel Development

Manager), who not only inspired us to work on this project but also accepted

to guide us a lot. In spite of heavy responsibilities and busy schedules, they

always managed time to provide proper guidance.

We are also thankful to our college professors for their constant suggestion

which resulted in successful completion of the project. Last but not the least;

we would like to thank our parents and friends for giving us their constant

support and encouragement in completion of our project.

Prabhakar Joshi

3

PREFACE

The competition in the insurance sector is highly volatile in nature. Over the

decade only government undertaking company was operating in India but

with the opening up of the economy several new players like private sector

& multinational insurance entered in Indian horizon.

In the given project we made a comparative analysis of mutual fund & life

insurance among MNC. Comparing their features & services one hand &

also done a research on the interest of investor regarding mutual fund & life

insurance in ICICI prudential company limited.

Research design method used was descriptive research. The

sampling method used was simple random sampling. We have taken a size

of 60 respondents. I first formed a structure questionnaire to collect data &

the questionnaire is filled by the person, who have one charted insurance

company & or more with any other MNC insurance company.

On the basis of filled questionnaire, coding sheet is formulated & the

conclusions are drawn with the help of graphs pie charts.

4

TABLE OF CONTENTS

AKNOWLEGEMENT

PREFACE

CONTENTS OF TABLE

EXECUTITIVE SUMMARY OF THE PROJECT

COMPANY PROFILE

PRODUCT POLICIES

PRODUCT PORTFOLIO

INTRODUCTION TO CHANNEL DEVELOPMENT

AND RECRUITMENT

METHODOLOGY USED TO RECRUIT ADVISOR

SWOT ANALYSIS

FUTURE GROWTH PROSPECTS OF COMPANY

COMPETITIVE ANALYSIS WITH HDFC

STANDARD LIFE

RECOMMENDATONS

LEARNINGS

BIBLIOGRAPHY

5

EXECUTIVE SUMMARY

Identifying different profiles of the people and giving them Career &

Business Opportunity to join ICICI Prudential as an advisor.

A market survey was done on life insurance companies. Different questions

regarding the companies training programs for advisor, top 5 usp's, training

centers etc were asked. The areas covered up in this survey were Noida and

Ghaziabad. The report contains details of different life insurance companies,

which are in healthy competition with ICICI Prudential life insurance.

Insurance industry is growing rapidly day-by-day. India itself has a

population of 1.12billion out of which roughly 33.2% people are insured.

This clearly shows that most of the people are not insured just because they

don’t know much about insurance. Most people have some common queries

about life insurance:

What is Life Insurance ?

A policy that will pay a specified sum to beneficiaries upon happening of an

unexpected event to the insured.

An agreement that guarantees the payment of a stated amount of

Monetary benefits upon death of the insured.

6

Why Insurance ?

Insurance is the protection of life and assets against unpredictable

circumstance. Whether it is a general accident policy, a Mediclaim policy or

a pension policy, an insurance policy helps you to scope with uncertainty

and insecurity.

Ever thought about why you should take an insurance policy. For one, it

helps you to hedge risks against unforeseen circumstances and save more. If

that's not all, it is:

Superior to an ordinary savings plan as it provides full protection

against risk of death.

Encourages and forces compulsory savings unlike other saving

instruments, wherein the saved money can be easily withdrawn.

Provides loan to tie over a temporary difficult phase and is also

acceptable as security for a commercial loan.

Offers tax relief to policyholders.

Hedges risk against uncertainty.

For a policy taken under the MWP Act 1874, (Married Women's

Property Act), a trust is created for wife and children as beneficiaries.

Based on the concept of sharing of losses, the society will benefit as

catastrophic losses are spread globally.

7

Who can buy a life insurance policy ?

Any person above 18 years of age, who is eligible to enter into a valid

contract, can go for an insurance policy. Subject to certain conditions, a

policy can be taken on the life of a spouse or children.

How is a life insurance policy useful ?

Planning for the financial consequences of a premature death is an essential

part of every financial plan. Generally, the consequences are simply too

large to ignore and cannot be totally covered with your own resources. Life

insurance is nothing but a contract with an insurance company under which

the insured (purchaser) pays a premium in exchange for coverage of

specified losses. Life insurance protects your family against the risk of the

premature death of you (or your spouse). Life insurance planning should

consider your family's short-term needs (for example, medical expenses) and

long-term needs (for example, replacing your income).

In the course of our life we are accosted by risk-that of failing health,

financial losses, accidents and so on. Insurance is a means by which life's

uncertainties are addressed in financial terms. It offers a monetary

compensation against those losses. Insurance is considered more as a

hedging mechanism rather than a true investment avenue. Life insurance, in

particular is essentially acknowledged as a mechanism that eliminates risk-

substituting certainty for uncertainty primarily by transferring risk from the

insured to the insurer.

8

Is life insurance a saving instrument ?

Life insurance is mainly considered as a saving instrument rather than an

investment avenue as it promotes compulsory savings besides reducing tax

burden on the policyholder and protects the family of the policyholder in the

event of unforeseen happening. It is the only saving instrument, which

covers the life risk besides giving tax concession both at entry (premium

paid) and at exit points. The section 10 (D) of the income tax act totally

exempts payment of tax on any amount received as bonus against life

insurance policies

9

COMPANY PROFILE

ICICI Prudential Life Insurance Company is joint venture between two heavy weights, ICICI Bank, India and Prudential Plc., UK. The name, ICICI Bank is not a new name in the Indian finance sector. It is India’s second largest bank and largest private sector bank with over 50 years of financial experience. It offers a wide range of banking products and financial services to corporate and retail customers in the areas of investment banking, life and non-life insurance, venture capital and asset management. It is a leading player in the retail banking market and has over 13 million retail customer accounts. The Bank has a network of over 570 branches and extension counters, and 2,000 ATMs.

Prudential Plc. is a London based finance company. It was established in the year 1848. The name Prudential might not be familiar among us but we have an emotional attachment with this name and specially our previous generation. The reason Many of us were infants when Kapil Dev Nikhanj lifted the Cricket World Cup at Lords in the year 1983. That World Cup was sponsored by none other than Prudential Plc.

Another famous example. In the year 1998, a movie named Titanic took away almost all the Academy Awards of that year. The incident of Titanic was a true one. The accident took place in the year 1913. It was Prudential Plc., which provided the ship the insurance coverage. The business of Prudential Plc. spans across the globe. By its products and services, it has brought a revolution of sort in the finance sector. It provides retail financial services products and services to more than 16 million customers, policyholder and unit holders worldwide. The credit goes to the company to bring to the market an integrated range of financial services and products that now includes life assurance, pensions, mutual funds, banking, investment management and general insurance. Since its inception, it has been doing its business with its flag always flying high.

10

ICICI Prudential began its operations in India in December 2000. It is

among the first private sector insurance companies to get the approval from

Insurance Regulatory Development Authority (IRDA). ICICI Prudential’s

equity base stands at Rs. 1185 crore with ICICI Bank and Prudential plc

holding 74% and 26% stake respectively. Until Sep 30, 2005, the company

wrote 283,818 policies. Inn the process, it has garnered Rs 820 crore of new

Business premiums for a total sum assured of Rs 7,131 crore. For the past

four years, ICICI Prudential has been donning the No. 1 position in the

private life insurance sector in the country. It has a wide range of flexible

products that meet the needs of the Indian customer at every step.

Although for the last 50 years LIC has been the only company to cater the

consumer needs in the insurance sector but in the past 5 years 21 insurance

companies have emerged in this scenario

ICICI Prudential Life

Birla Sun Life

Bajaj Allianz

Max New York Life

Met Life

ING Vysa

Om Kotak Mahindra

Tata AIG

Aviva

HDFC Standard Life

11

SBI Life

IFFCO-TOKIO

Reliance life

Bharti

PNB Life

New players need to recognize the limitations of their rival and decide upon

the right mix of distribution channels in their business.

12

PRODUCTS PORTFOLIO

ICICI Prudential has a wide array of insurance plans that have been designed with the philosophy that different individuals are bound to have differing insurance needs.

The ideal insurance plan is one that addresses the exact insurance needs of the individual that will depend on the age and life stage of the individual apart from a host of other factors.

Life Insurance Plans:

Under Life insurance plans, ICICI Prudential offers plans under the

following major

categories:

Education Insurance Plans

Wealth Creation Plans

Premium Guarantee plans

Protection Plans

Retirement Solutions:

The primary objective of a retirement plan is to help you provide for your

financial needs in your post retirement years.

ForeverLife

Lifetime Super Pension

Life Link Super Pension

13

Health Product Suite:

Under Health Product Suite, ICICI Prudential offers plans under the

following major categories:

Health Assure

Health Assure Plus

Hospital Care

Cancer Care

Cancer Care Plus

Diabetes Care

Diabetes Care Plus

14

PRODUCT PORTFOLIO

PREMIER LIFE

How do I start?

Open an account with a minimum contribution of:

Rs. 60,000/ annum for annual premium payment

Rs. 30,000/ half year for half-yearly payment

Rs. 5,000/month for monthly premium

BENEFITS

a. Death benefits

The death benefit will be higher of the Sum Assured (decreased by the amount of withdrawals mode) or value of units.

b. Liquidity

Partial withdrawals would be allowed after 3rd year policy year & after payment of 3 year premium. Partial withdrawals would be subject to surrender value. Each partial withdrawal during the 4 th and 5th year would

15

be limited to 20% of the value of the investment at the time of withdrawal. The minimum partial withdrawals amount as to be Rs . 10,000.

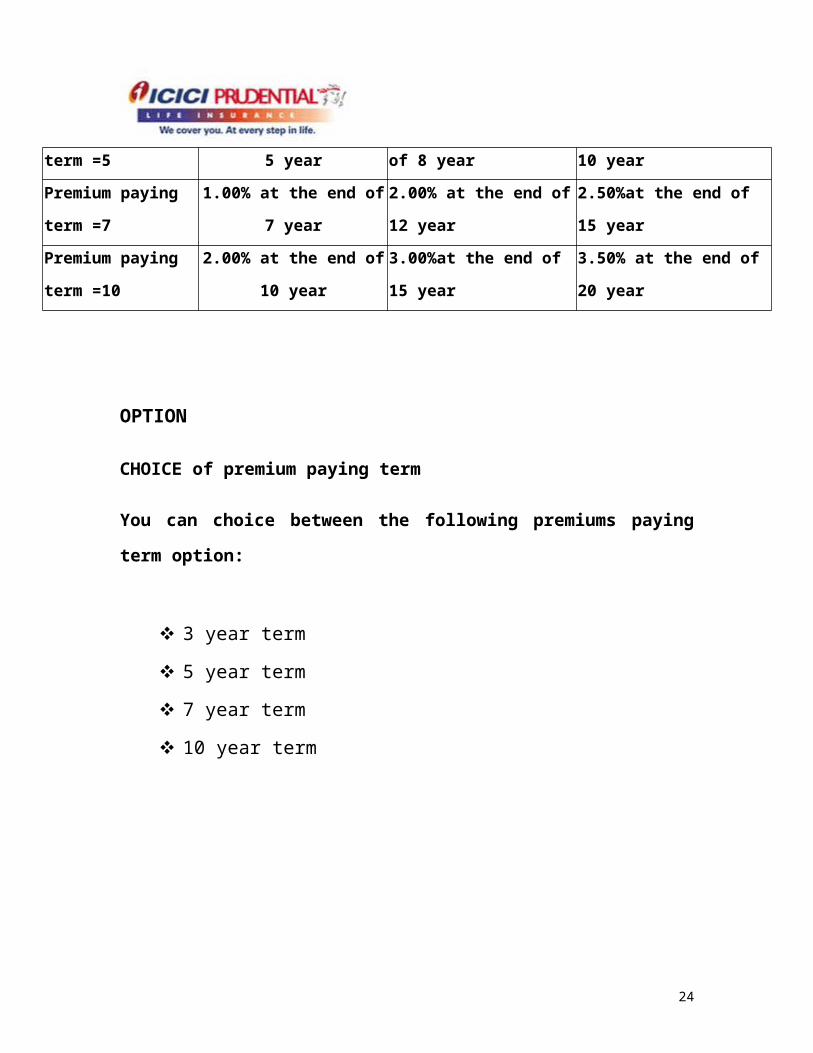

c. Additional allocation of units

There would be additional survival units payable to the

policy holder at various point of time during the coverage

term.

Premium paying

term Bonus Units Received

Premium paying

term =3 Nil Nil 0.50% at the end of 6th year

Premium paying

term =5 0.25% at the end of 5 year 0.50 % at the end of 8 year 1.00% at the end of 10 year

Premium paying

term =7 1.00% at the end of 7 year 2.00% at the end of 12 year 2.50%at the end of 15 year

Premium paying

term =10 2.00% at the end of 10 year 3.00%at the end of 15 year 3.50% at the end of 20 year

16

OPTION

CHOICE of premium paying term

You can choice between the following premiums paying term option:

3 year term

5 year term

7 year term

10 year term

17

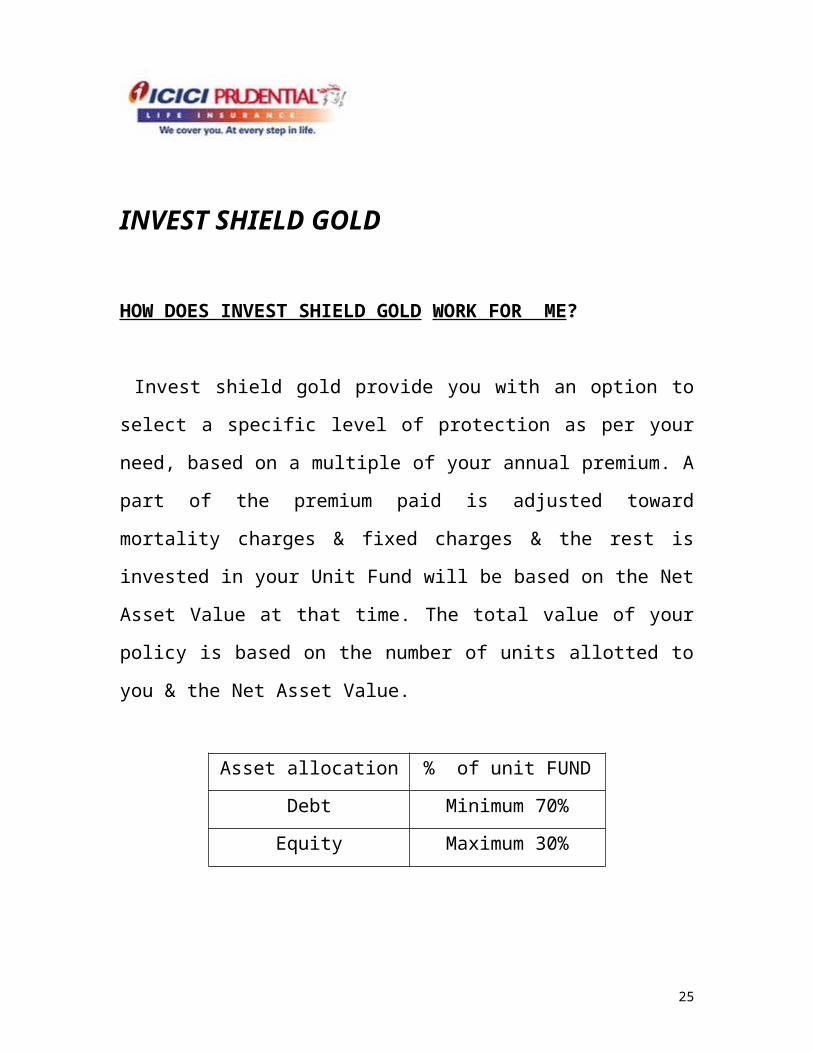

INVEST SHIELD GOLD

HOW DOES INVEST SHIELD GOLD WORK FOR ME?

Invest shield gold provide you with an option to select a specific level of

protection as per your need, based on a multiple of your annual premium. A

part of the premium paid is adjusted toward mortality charges & fixed

charges & the rest is invested in your Unit Fund will be based on the Net

Asset Value at that time. The total value of your policy is based on the

number of units allotted to you & the Net Asset Value.

Asset allocation % of unit FUND

Debt Minimum 70%

Equity Maximum 30%

18

What are the limits or conditions?

Minimum age at entry: 0 year

Maximum age at entry: 60 year

Maximum age at maturity: 75 year

Minimum sum assured: Rs.1, 00,000

How do I start?

You can start with a minimum premium of:

Rs. 25,000per annum premium payment

Rs. 12500 per half-year for half- yearly premium payment

Rs. 2084 per month for monthly premium

BENEFITS

In unfortunate event of the death of the life assured the nominee

received the Sum Assured along with the higher of the value of your

Unit Fund

Or the guaranteed value of your Unit Fund, provided due till date is

paid in full.

At the end of the police term, either the value of your Unit Fund or the

guaranteed value of your Unit FUND, whichever is higher will be paid as

maturity benefits.

19

Choice of Premium payment term

Premium Payment term Maturity Term

5 Year 10 Year

7 Year 15 Year

10 Year 20 Year

SOME CHARGES:

Fixed charges

Fund-related charges

Mortality charges

Top-up charges

EDUCATION GURANTEED

Smart Kid Education plan have 4 products offer:

Unit-linked Regular premium

Unit-linked Regular Premium II

Unit-linked Single Premium II

Regular Premium

The uniqueness of this plan is that even if anything happens to the parent,

the benefits to the child are not compromised. The benefits under this police:

Death benefits The death benefit is equal to the Sum Assured chosen at the

Time parent applies & will be payable immediately on the police holder.

20

In case of unfortunate death, here is how the police work:

Sum Assured chosen is paid immediately

The police benefits continue so that the unit can be withdrawn for

your child as & when required for education or developmental needs.

21

INVEST SHIELD LIFE

How does Invest Shield Life work for me?

You can choose a specific level of protection as per your needs, based on a

multiple of your annual premium. Part of the premium paid by you is

adjusted towards mortality charges, allocation charges & fixed charges &

the rest is invested in your Unit Fund. Entry into the Unit Fund will be

based on the NAV at that time. The total value of your police is based on

the number of unit allocated to you & the NAV.

HOW DO I START?

Choose your term from 10 to 30 years & a minimum premium of:

Rs. 8000 per annum for annual premium payment

Rs. 4000 per half-year for half-yearly premium payment

Rs. 667 per month for monthly premium payment

22

What are the limits or conditions applicable?

Minimum age at entry: 0 year

Maximum age at entry: 55 year

Maximum age at maturity: 65 year

Maximum cover ceasing age: 75 year

Minimum term: 10 year

Maximum term: 30 year

Minimum Sum Assured: Rs. 1, 00,000

Now, ICICI prudential Life Insurance presents a comprehensive range of

unit-linked product that take care of your wealth creation by providing you

flexibilities in saving & investment & option for your production needs. We

present life time II comprehensive portfolio of products that provide you

complete flexibility to choose a solution, based on your specific needs.

23

LIFE TIMEHow do I start?

Open an account with a minimum premium of …

Rs. 18000/-p.a. for annual mode

Rs. 9000/-per half year for half-yearly mode

Rs. 1500/- per month for monthly mode

Benefits

Death benefit: In unfortunate event of death, your closes once are spared an

uncertain future. Our guaranteed death benefit ensures that the nominee will

receive the higher of either the death benefit chosen or the value of units.

Liquidity option: There is no maturity date. Anytime after 3year of

commencement you can make partial or complete withdrawals, at no

penalty, to meet your immediate requirements.

Option

a. Choice of Investment Plan

You have the option to choose how you want your investments to

grow based on the objectives of each of the plan.

24

Maximiser:

If high growth in your priority, this is the plan for you. You can enjoy long

term appreciation from a portfolio that is invested primarily in equity &

equity-related securities.

Protector:

If on the other hand your priority is steady return, you can opt for the

protector plan. Here you can accumulated a steady income, at low risk

across a medium to long term period from a portfolio, which is primarily

invested in fixed income securities.

Balancer:

If you prefer a balance of growth & steady returns, choose our balancer plan.

This would ensure that your portfolio is invested in equity & equity-link

securities as well as in fixed income securities.

b. Choice of Switch between Investment options

If at later stage your financial priorities change, you can switch

between the various investment options at any time . there is provision

of 4 free switch every policy year , subject to the condition that the

minimum switch amount is Rs. 10000. Any switch beyond this limit

will be charged at Rs.100/switch.

c. Choice of Top-up

Top-up your investment any time you have surplus funds. The Top-

ups will not have any effect on the Sum Assured of the product. The

minimum amount of top-up is Rs.5000.

25

INTODUCTION TO CHANNEL DEVELOPMENT AND RECRUITMENT

Who is an insurance advisor?

An agent is the representative of an insurance company who sells different

policies or product to its clients.

Another term used for insurance agents is advisors; ICICI Prudential life

insurance company Ltd introduced this term.

Today in life insurance companies’ advisors are known to be the backbone

of the whole system. Advisors/agents do not work on monthly payroll basis;

they receive a certain commission on the policies they sell to the clients.

The eligibility required to become an advisor/agent is that he/she should be

12th pass to operate in urban area and 10th pass for rural areas. Before a

person becomes an advisor/agent he/she has to undergo 100hrs training

according to IRDA norms, which is compulsory.

A person who wants to be an advisor has first to fill a recruitment form and

has to pay a fee of Rs. 1500/- in favor of ICICI Prudential. Then, he has to

pass a test, which is compiled by IRDA. After he gets through that test he is

awarded a license and then his training starts in the company regarding the

insurance business. ICICI Pru provides this training in 3 modes as per the

suitability of the advisors viz: -

1) Classroom training: - it is a Full Time Training with a period of 17

days regular between 9 am to 5pm at the training centers allotted to

the advisor.

26

2) Online training: - it is another mode of training where the company

provides CD’S and books to the advisor for his own study.

3) Classroom training: - it is a Part Time Training with a period of 36

days.

Advisor Role :

To provide ongoing financial advice for his/her clients:

Identify future clients

Making appointments

Conduct financial review meetings with prospects/clients.

Close sales

Get referrals

Provide service to clients.

Follows internal sales and reporting system.

Working Environment of an advisor/agent.

To be a part of world-class sales team.

Work from your own office or residence.

Work full time or part time (an advisor can work part time by

undergoing only 50hrs of training and 100hrs training is for full

time advisors.)

Earn Commission, Bonus & Incentives.

No upper limits on earnings.

Flexible career.

27

Opportunities for an Advisor/agent.

No startup capital required.

Flexible working environment.

Be your own boss.

Unlimited earning potential.

To be a part of a world-class team.

Commission Structure.

Different products will have different commission structures.

For example: Single Premium products will have a commission of 2%.

Renewal Commission is paid at the following rates:

2nd yr: 7.5% 3rd yr: 7.5% 4th yr: 5% 5th yr: 5% onwards

28

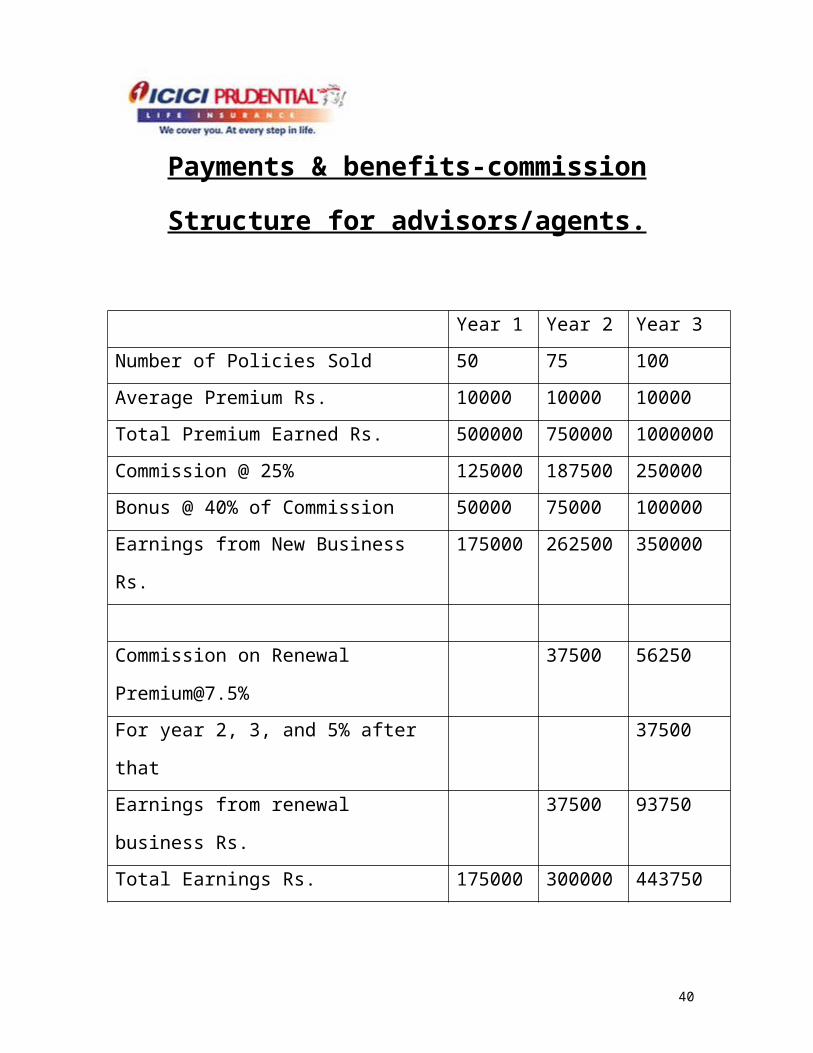

Payments & benefits-commission Structure for

advisors/agents.

Year 1 Year 2 Year 3

Number of Policies Sold 50 75 100

Average Premium Rs. 10000 10000 10000

Total Premium Earned Rs. 500000 750000 1000000

Commission @ 25% 125000 187500 250000

Bonus @ 40% of Commission 50000 75000 100000

Earnings from New Business Rs. 175000 262500 350000

Commission on Renewal [email protected]% 37500 56250

For year 2, 3, and 5% after that 37500

Earnings from renewal business Rs. 37500 93750

Total Earnings Rs. 175000 300000 443750

29

Most preferred profiles to recruit as Advisors/agents.

Housewives

Income Tax Consultant

Chartered Accountant

Sales Personnel’s working in

Automobile Dealership

Credit Card Co.

Telecom

Mutual Fund

DSA’s

M R’s

Doctors

Teachers

VRS Holders

Advisors of other insurance companies

Post Office Agents

Business Men

Accountants OI in an organization

30

How does an advisor/agent work.

Firstly an advisor/agent has to make a list of 100 people that he/she

knows.

Then the Advisor/agent makes a call to these clients and tries to fix an

appointment.

When an appointment is fixed the advisor/agent meets the customer &

tries to sell the product.

After that the advisor/agent asks for the reference of maximum

number of people from the client.

The reference is asked in context to make future calls and the whole

procedure is repeated again.

31

INSURANCE ADVISOR SURVEY

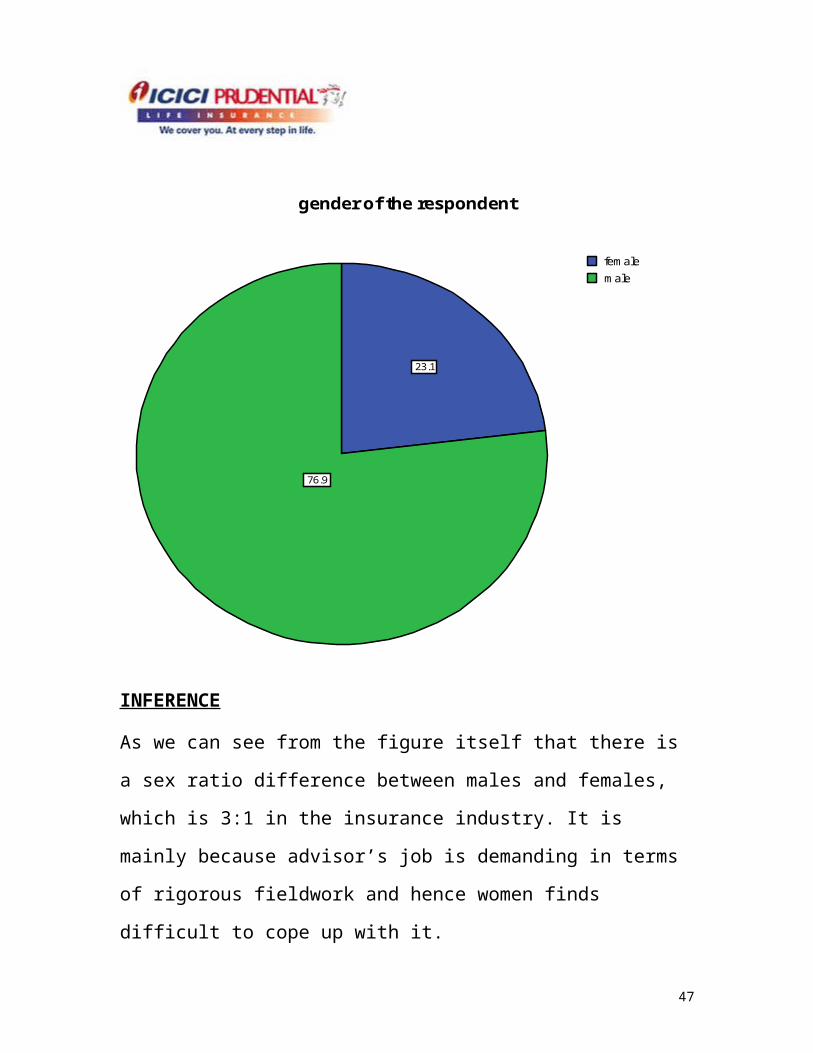

GENDER OF THE RESPONDENTTable 1

Frequency PercentValid

PercentCumulative

PercentValid Female 15 23.1 23.1 23.1 Male 50 76.9 76.9 100.0 Total 65 100.0 100.0

23.1

76.9

female

male

gender of the respondent

32

INFERENCE

As we can see from the figure itself that there is a sex ratio difference

between males and females, which is 3:1 in the insurance industry. It is

mainly because advisor’s job is demanding in terms of rigorous fieldwork

and hence women finds difficult to cope up with it.

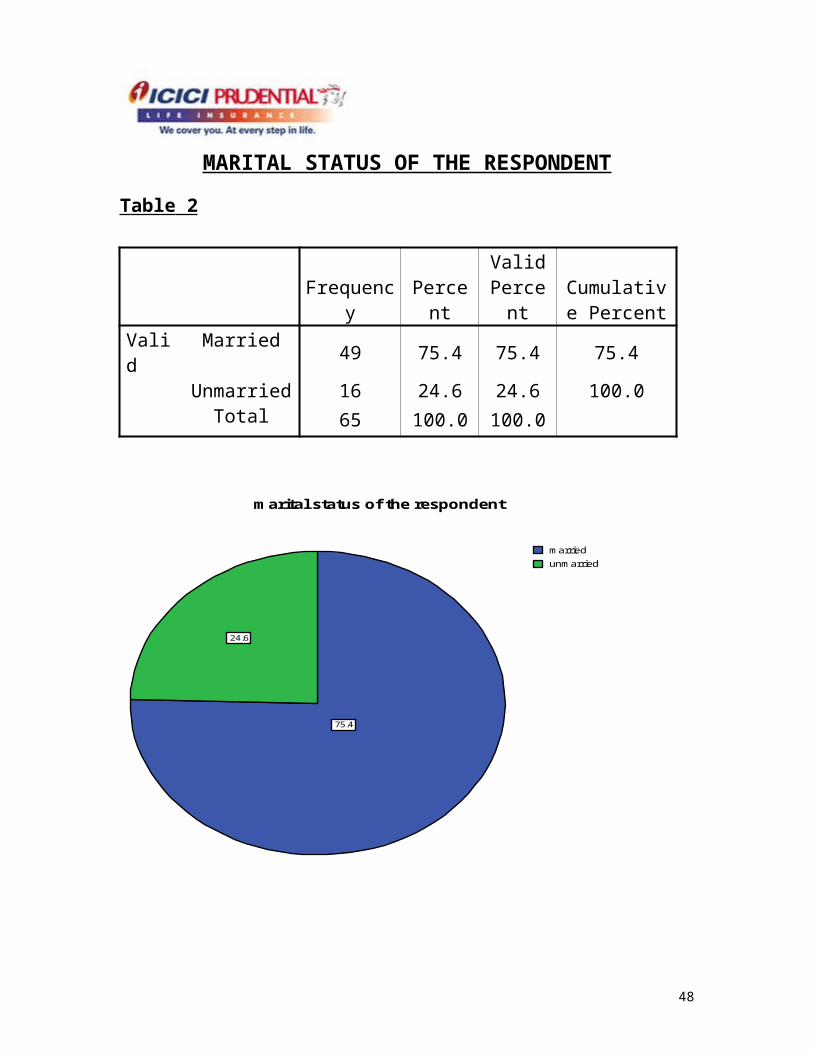

MARITAL STATUS OF THE RESPONDENT

T able 2

Frequency PercentValid

PercentCumulative

PercentValid Married 49 75.4 75.4 75.4 Unmarried 16 24.6 24.6 100.0 Total 65 100.0 100.0

75.4

24.6

married

unmarried

marital status of the respondent

33

INFERENCEMore married people work, as advisors and company prefer to employ them in comparison to unmarried ones because being family people they tend to take their work more seriously. Because generally a laid back attitude has been observed in the unmarried people.

34

EDUCATIONAL QUALIFICATION OF THE RESPONDENT

Table 3

Frequency PercentValid

PercentCumulative

PercentValid Inter 5 7.7 7.7 7.7 Graduate 40 61.5 61.5 69.2 Professional 20 30.8 30.8 100.0 Total 65 100.0 100.0

7.7

61.5

30.8

inter

graduate

professional

educational qualification of the respondent

INFERENCEAmong insurance advisors, it has been observed that 61.5% of them are graduates in comparison to professionals like CA’s or MBA’s who are just 30.8%. While intermediate pass people just make 7.7% of the whole lot.

35

CLUB MEMBERSHIP OF THE RESPONDENT

Table 4

Frequency PercentValid

PercentCumulative

PercentValid Yes 17 26.2 26.2 26.2 No 48 73.8 73.8 100.0 Total 65 100.0 100.0

26.2

73.8

yes

no

club membership of the respondent

INFERENCEThe insurance advisors who do remarkable work in terms of fetching business for the company are given club memberships like DM club, MDRT club, Zonal Club etc.

36

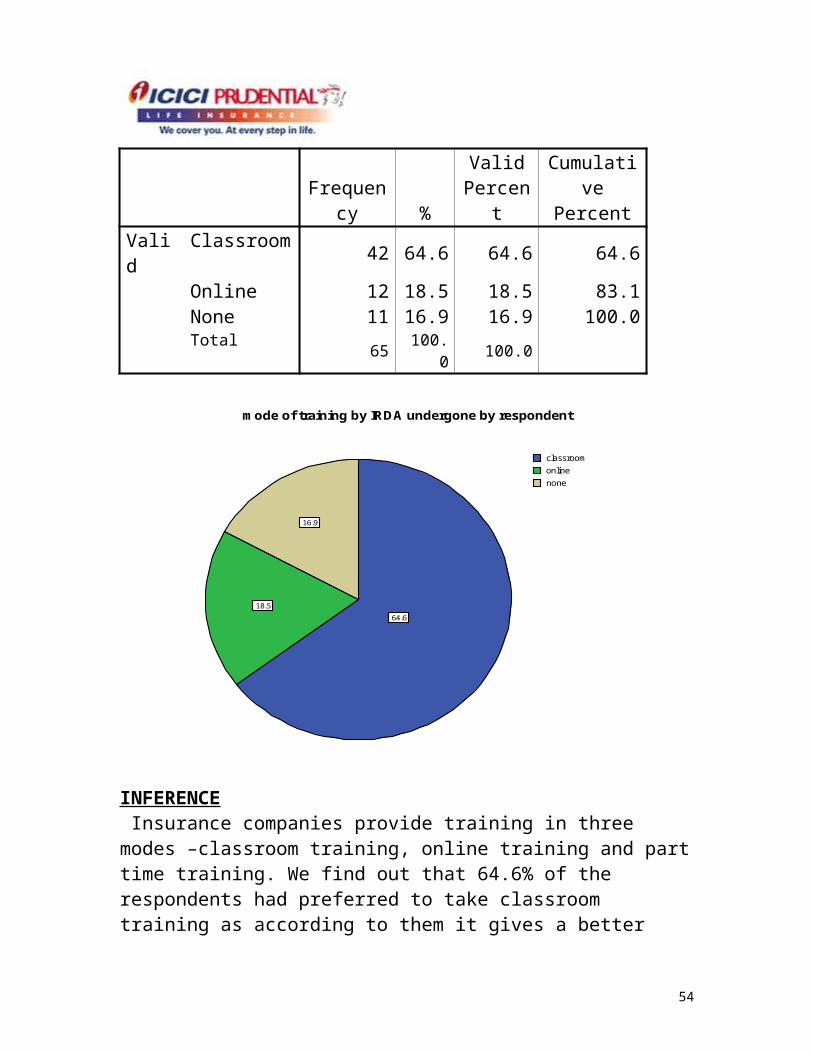

MODE OF TRAINING BY IRDA UNDERGONE BY RESPONDENT

Table 6

64.6

18.5

16.9

classroom

online

none

mode of training by IRDA undergone by respondent

INFERENCE Insurance companies provide training in three modes –classroom training, online training and part time training. We find out that 64.6% of the respondents had preferred to take classroom training as according to them it gives a better hang of the insurance business operations since you are one on

Frequency %Valid

PercentCumulative

PercentValid Classroom 42 64.6 64.6 64.6 Online 12 18.5 18.5 83.1 None 11 16.9 16.9 100.0 Total 65 100.0 100.0

37

one with the training manager and hence you can ask any queries then and there only.

EXPERIENCE IN THE FIELD OF THE RESPONDENT

Table 7

Frequency PercentValid

PercentCumulative

PercentValid 0 to 6

months2 3.1 3.1 3.1

6 to 12 months

7 10.8 10.8 13.8

More than 1 year

56 86.2 86.2 100.0

Total 65 100.0 100.0

0 to 6 months 6 to 12 months more than 1 year

0

20

40

60

80

100

Y A

xis

experience in the field of the respondent

INFERENCE86.2% of the total respondents were found to be well established in this field since they have been working for over one year and majority for the last 10 –15 yrs.

38

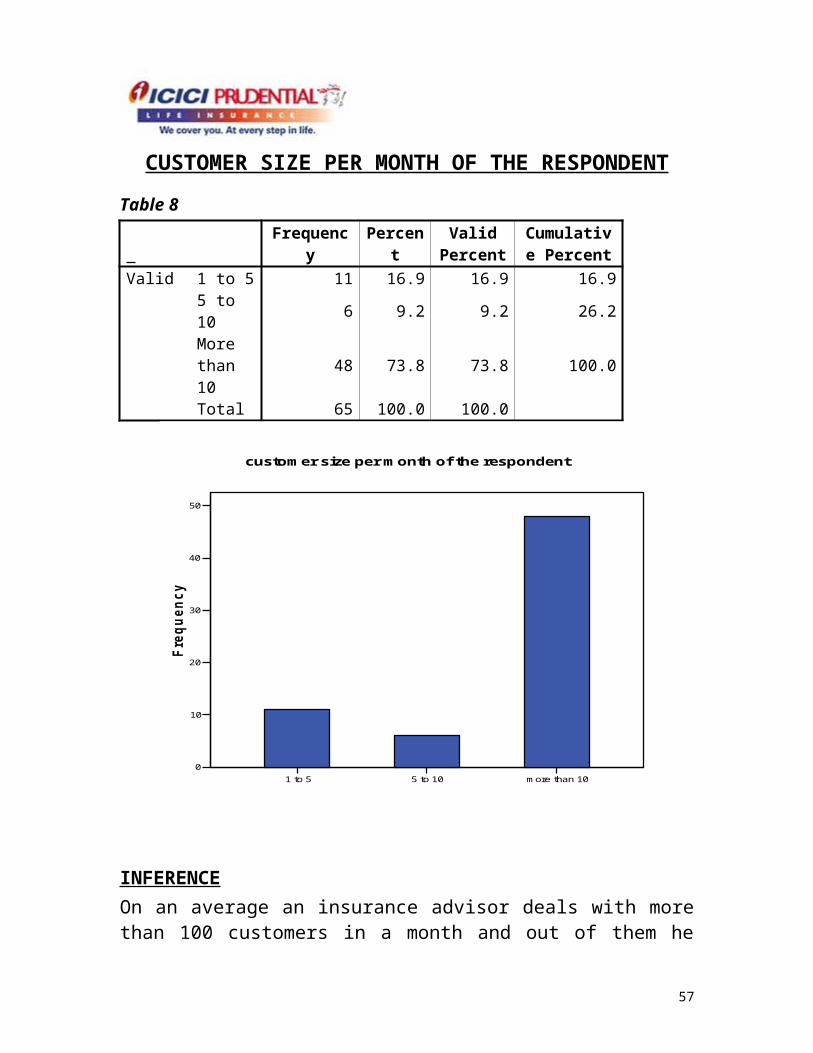

CUSTOMER SIZE PER MONTH OF THE RESPONDENT

Table 8

Frequenc

yPerce

ntValid

PercentCumulative Percent

Valid 1 to 5 11 16.9 16.9 16.9 5 to 10 6 9.2 9.2 26.2 More

than 10

48 73.8 73.8 100.0

Total 65 100.0 100.0

1 to 5 5 to 10 more than 10

0

10

20

30

40

50

Fre

qu

en

cy

customer size per month of the respondent

INFERENCEOn an average an insurance advisor deals with more than 100 customers in a month and out of them he converts 80% of the calls i.e. he sells policies to them. 73.8% of the respondents had a customer base of more than 10 which was the minimum figured option included in our questionnaire. And these were the advisors who had been in this field for the last 5 to 8 years or more than that.

39

CONTACTING THE CUSTOMER BY THE RESPONDENT

Table 9

Frequency PercentValid

PercentCumulative

PercentValid Personal

meeting & telephone

11 13.8 13.8 13.8

Telephone & references

10 15.4 15.4 29.2

All 46 70.8 70.8 100.0 Total 65 100.0 100.0

9

10

46

personal meeting & telephone

telephone & references

all

contacting the customer by the respondent

INFERENCE

When respondents were asked that what are the ways they use for contacting the clientele base they are having then 70.8% of them named telephone calls, personal meetings and references as the major means of keeping in touch with their customers while only 15.4% named telephone calls and references as their sources.

40

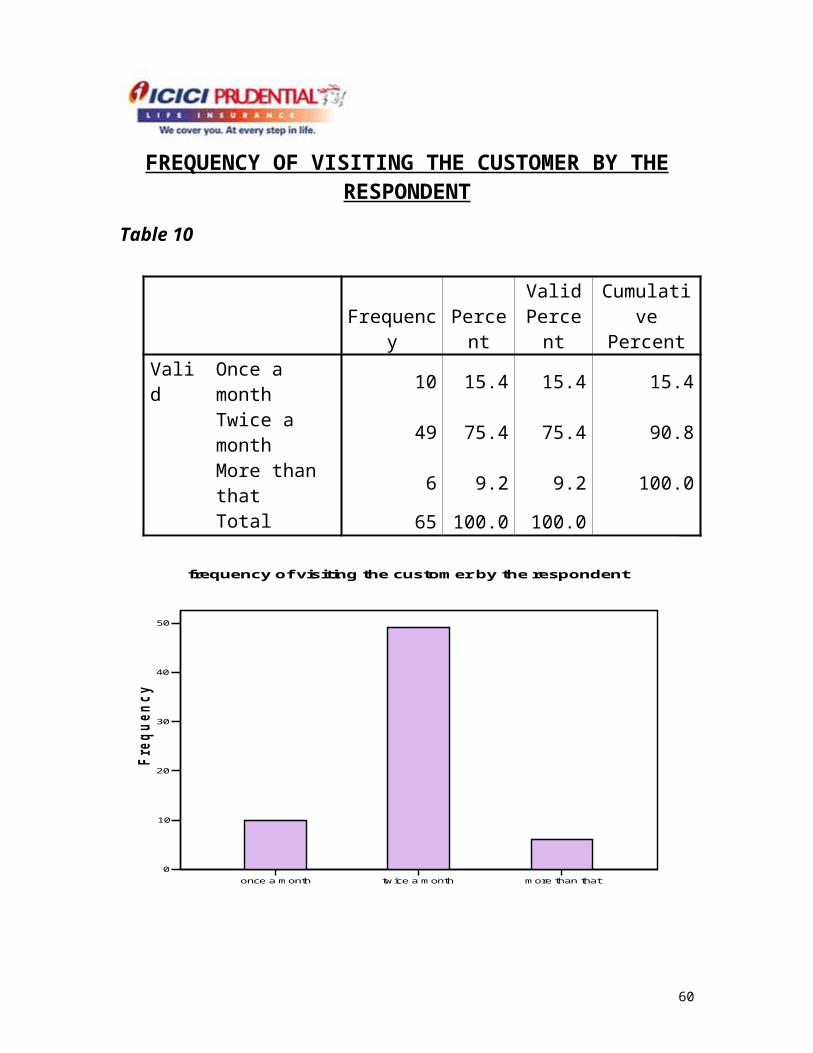

FREQUENCY OF VISITING THE CUSTOMER BY THE RESPONDENT

Table 10

Frequency PercentValid

PercentCumulative

PercentValid Once a month 10 15.4 15.4 15.4 Twice a month 49 75.4 75.4 90.8 More than that 6 9.2 9.2 100.0 Total 65 100.0 100.0

once a month twice a month more than that

0

10

20

30

40

50

Fre

qu

en

cy

frequency of visiting the customer by the respondent

INFERENCE

75.4% of the advisors were find to visit their customers almost twice a month for various purposes like updating the customers for new policies and products company is introducing etc. and only 15.4% visited their clients once a month.

42

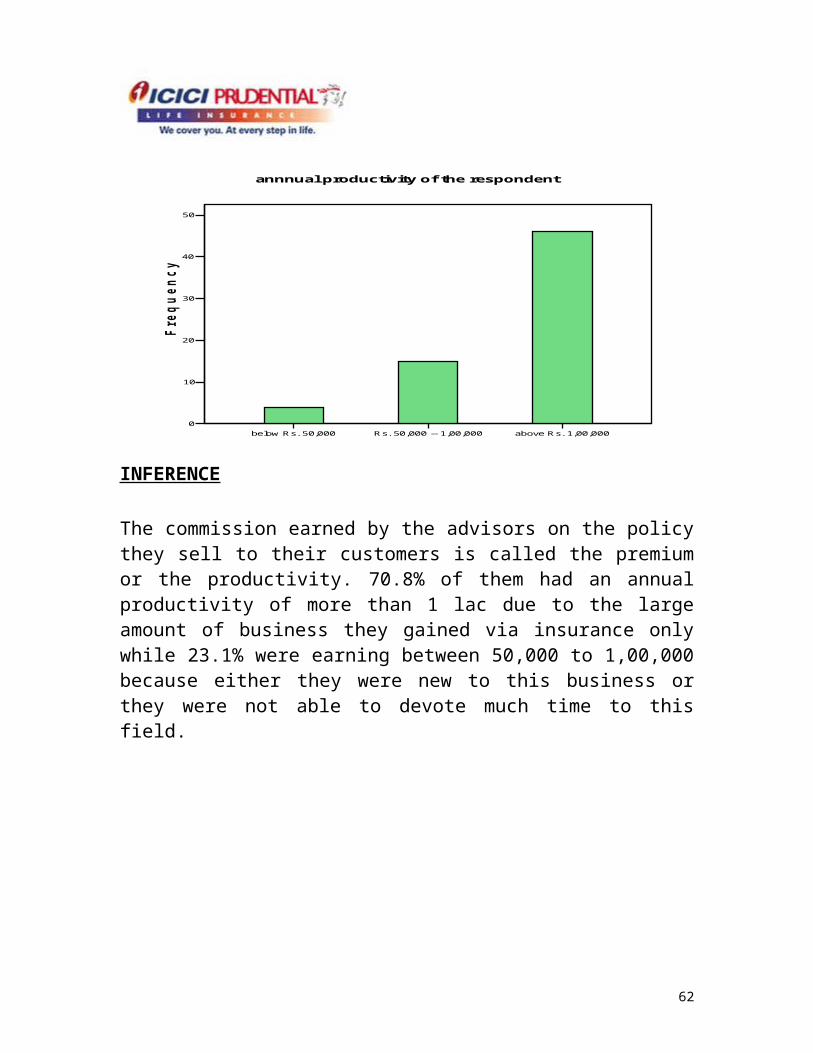

ANNNUAL PRODUCTIVITY OF THE RESPONDENT

Table 11

Frequency PercentValid

PercentCumulative

PercentValid Below Rs.

50,0004 6.2 6.2 6.2

Rs. 50,000 -- 1,00,000

15 23.1 23.1 29.2

Above Rs. 1,00,000

46 70.8 70.8 100.0

Total 65 100.0 100.0

below Rs. 50,000 Rs. 50,000 -- 1,00,000 above Rs. 1,00,000

0

10

20

30

40

50

Fre

qu

en

cy

annnual productivity of the respondent

INFERENCE

The commission earned by the advisors on the policy they sell to their customers is called the premium or the productivity. 70.8% of them had an annual productivity of more than 1 lac due to the large amount of business they gained via insurance only while 23.1% were earning between 50,000 to 1,00,000 because either they were new to this business or they were not able to devote much time to this field.

43

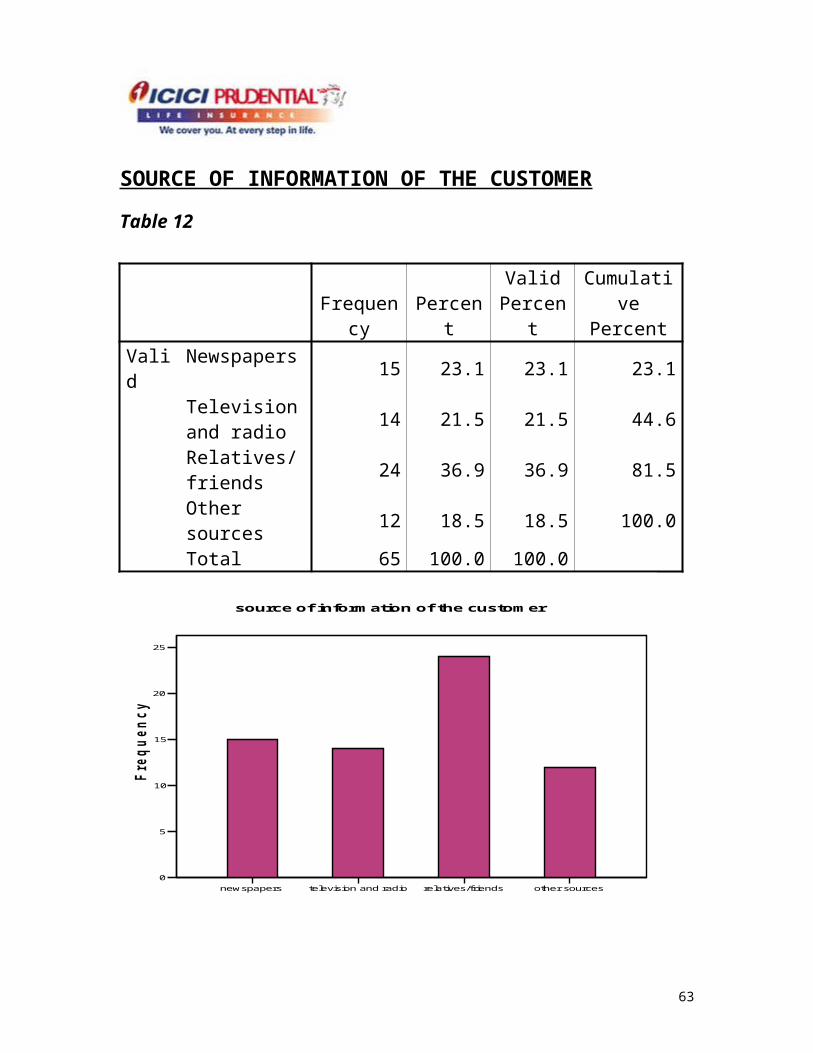

SOURCE OF INFORMATION OF THE CUSTOMER

Table 12

Frequency PercentValid

PercentCumulative

PercentValid Newspapers 15 23.1 23.1 23.1 Television and

radio14 21.5 21.5 44.6

Relatives/friends

24 36.9 36.9 81.5

Other sources 12 18.5 18.5 100.0 Total 65 100.0 100.0

newspapers television and radio relatives/friends other sources

0

5

10

15

20

25

Fre

qu

en

cy

source of information of the customer

INFERENCEAs per the point of view of the 36.9%advisors, the customers usually get to know about the policies and products of any insurance company via their relatives or friends while 23.1% advisors gave the credit to the advertising in the newspapers as the source of information to the people. TV and Radio had 21.5% of the advisors favoring them.

44

PARAMETERS DEMANDED IN INSURANCE POLICIES

Table 13

Frequency PercentValid

PercentCumulative

PercentValid Service 14 21.5 21.5 21.5 Quality 18 27.7 27.7 49.2 Product

features11 16.9 16.9 66.2

Brand 22 33.8 33.8 100.0 Total 65 100.0 100.0

21.54

27.69

16.92

33.85

service

quality

product features

brand

parameters demanded in insurance policies

INFERENCE

33.8% advisors feel that while buying a policy what customer looks is the brand name associated with it. Like for selling a LIC, which is a generic brand you don’t need to do that much hard work because customer knows it.

45

27.7% favored quality of the product they are selling as the top priority of the customer.16.9% advisors gave their consent to the product features as one of the enticing factor for the customers in buying into a policy.

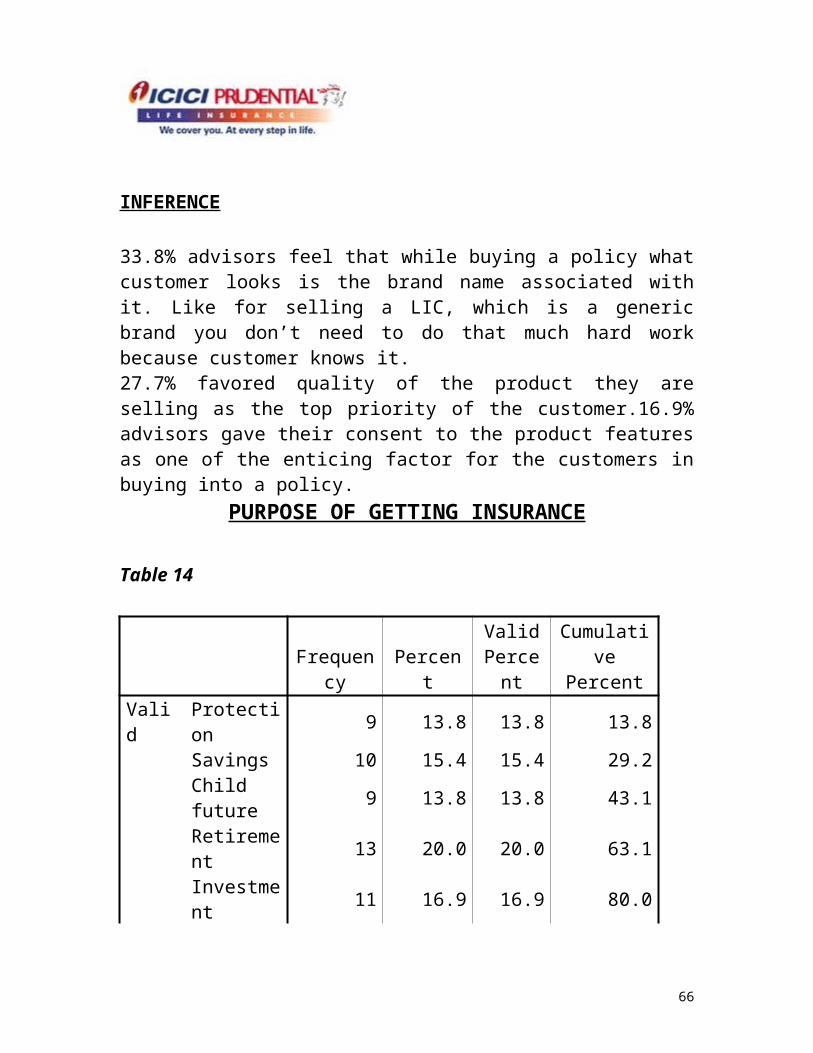

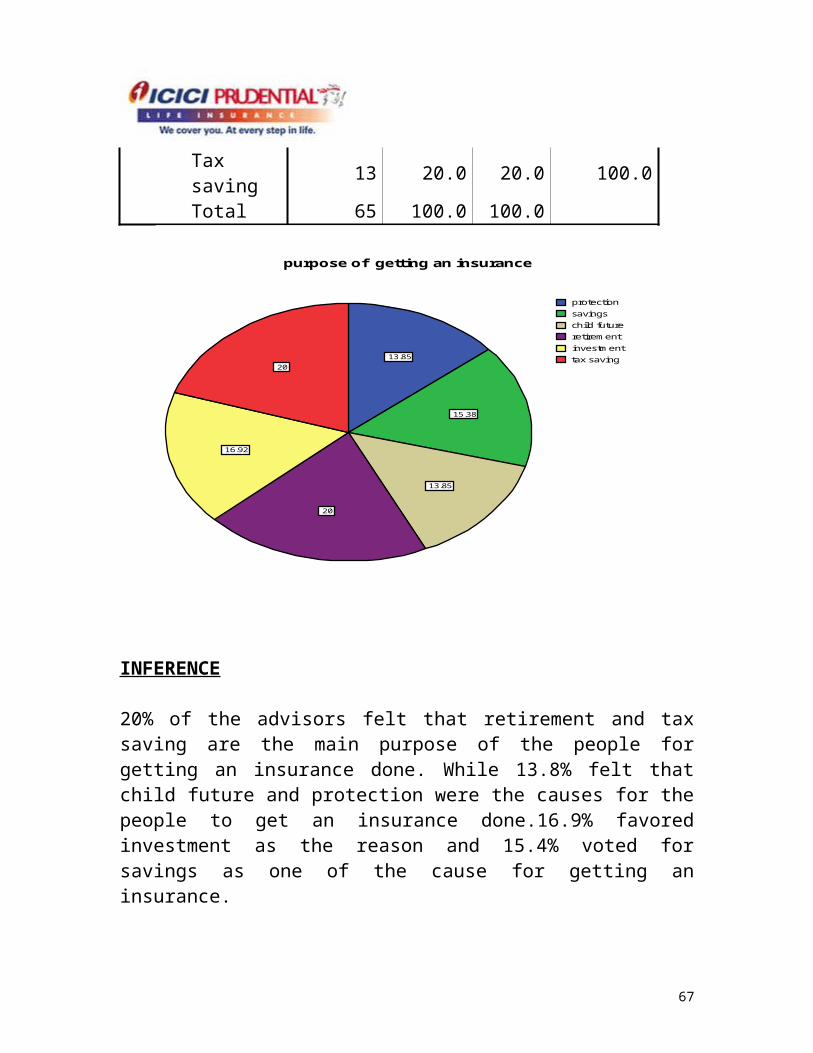

PURPOSE OF GETTING INSURANCE

Table 14

Frequency PercentValid

PercentCumulative

PercentValid Protection 9 13.8 13.8 13.8 Savings 10 15.4 15.4 29.2 Child

future9 13.8 13.8 43.1

Retirement 13 20.0 20.0 63.1 Investment 11 16.9 16.9 80.0 Tax saving 13 20.0 20.0 100.0 Total 65 100.0 100.0

13.85

15.38

13.85

20

16.92

20

protection

savings

child future

retirement

investment

tax saving

purpose of getting an insurance

46

INFERENCE

20% of the advisors felt that retirement and tax saving are the main purpose of the people for getting an insurance done. While 13.8% felt that child future and protection were the causes for the people to get an insurance done.16.9% favored investment as the reason and 15.4% voted for savings as one of the cause for getting an insurance.

47

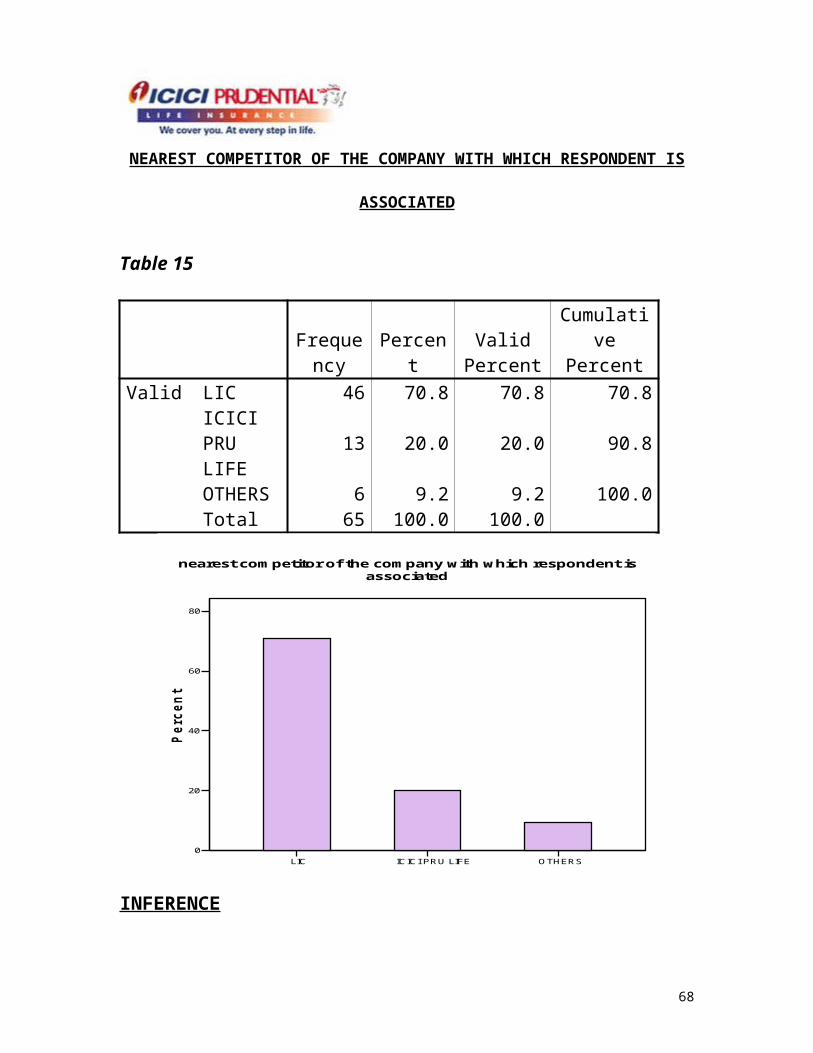

NEAREST COMPETITOR OF THE COMPANY WITH WHICH RESPONDENT

IS ASSOCIATED

Table 15

Frequenc

y PercentValid

PercentCumulative

PercentValid LIC 46 70.8 70.8 70.8 ICICI

PRU LIFE

13 20.0 20.0 90.8

OTHERS 6 9.2 9.2 100.0 Total 65 100.0 100.0

LIC ICICI PRU LIFE OTHERS

0

20

40

60

80

Pe

rc

en

t

nearest competitor of the company with which respondent is associated

INFERENCE

LIC is one generic brand, which no one can beat, and hence the biggest competitor of any insurance company.70.8% of the respondents had this viewpoint while only 20% felt that ICICI Prudential is the next big emerging competitor after LIC of course.

48

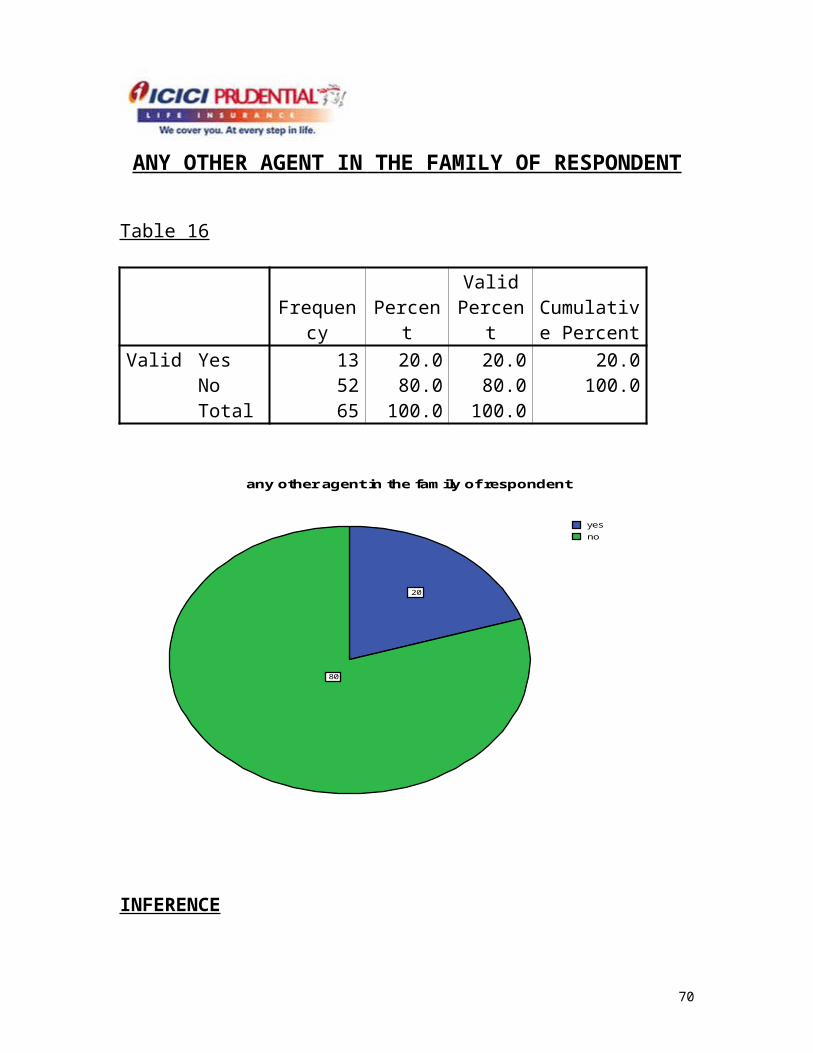

ANY OTHER AGENT IN THE FAMILY OF RESPONDENT

Table 16

Frequency PercentValid

PercentCumulative

PercentValid Yes 13 20.0 20.0 20.0 No 52 80.0 80.0 100.0 Total 65 100.0 100.0

20

80

yes

no

any other agent in the family of respondent

INFERENCE

Only 20% of the total advisors surveyed had some other family member also as an agent along with them and 80% of the advisors were the only one in their family who were into the insurance business.

49

GENERAL MASS SURVEY

GENDER OF THE RESPONDENT

Table 1

Frequency PercentValid

PercentCumulative

PercentValid

Male42 62.7 62.7 62.7

Female 25 37.3 37.3 100.0 Total 67 100.0 100.0

62.7

37.3

male

female

Gender Of The Respondent

INFERENCE

As the figures speak for themselves, total respondents whom we surveyed 62.7% were males while rest were females (37.3%).

50

MARITAL STATUS OF THE RESPONDENT

Table 2

Frequency PercentValid

PercentCumulative

PercentValid Married 32 47.8 47.8 47.8 Unmarried 35 52.2 52.2 100.0 Total 67 100.0 100.0

47.7652.24

married

unmarried

Marital Status Of The Respondent

INFERENCE

As the figure shows that 52.24% were married while 47.76% were unmarried. In a way, it helped us because while prospecting the people for making them the advisors we prefer those who are married.

52

EDUCATIONAL QUALIFICATION OF THE RESPONDENT

Table 3

Frequency PercentValid

PercentCumulative Percent

Valid Any Professional Degree

7 10.4 10.4 10.4

Post Graduate 42 62.7 62.7 73.1 Graduate 9 13.4 13.4 86.6 Undergraduate/ XII

Pass9 13.4 13.4 100.0

Total 67 100.0 100.0

10.4

62.7

13.4

13.4

any peofessional degree

post graduate

graduate

undergraduate/ XII pass

Educational Qualification Of The Respondent

53

INFERENCE

62.7% of the respondents were found to be post graduates and next came under graduates and graduates with 13.4%. Only 10.4% were found to be professionals like CA’s or MBA’s.

54

OCCUPATIONAL BACKGROUND OF THE RESPONDENT

Table 4

Frequency PercentValid

PercentCumulative Percent

Valid Govt/ State Services

21 31.3 31.3 31.3

Private Job 33 49.3 49.3 80.6 Professional 8 11.9 11.9 92.5 Others 5 7.5 7.5 100.0 Total 67 100.0 100.0

31.3

49.3

11.9

7.5

Govt/ State Services

Private Job

Professional

others

Occupatonal Background Of The Respondent

INFERENCE

Most of the respondents belonged to the private sector like they were working in some bank or in any private enterprise so they were easily convertible into agents because they can take agencies on their name while

55

government people can’t do that. Only 31.3% belonged to the government sector.

ANNUAL HOUSEHOLD INCOME

Table 5

Frequency PercentValid

PercentCumulative

PercentValid 5 to 8 lacs 34 50.7 50.7 50.7 3 to 5 lacs 19 28.4 28.4 79.1 1 to 3 lacs 14 20.9 20.9 100.0 Total 67 100.0 100.0

50.7

28.4

20.9

5 to 8 lacs

3 to 5 lacs

1 to 3 lacs

Annual Household Income

INFERENCE

Almost 50.7% were found to earn between 5 to 8 lacs. Those people who are earning up to one lac are avoidable profile for tapping the insurance advisors. We were supposed to look for people who fell in an average income group of earnings between3 to 5 lacs. Even people who had income

56

of 8 lacs were to be ignored because it was difficult to entice them into the insurance business.

57

INTEREST OF THE RESPONDENT IN MAKING EXTRA INCOME

Table 6

76.1

23.9

yes

no

Interest Of The Respondent In Making Extra Income

INFERENCE

When the respondents were asked the question that whether they will be interested in earning a surplus income then 76.1% of them were enthusiastic about it especially when they were told that this business well cost NIL investment from their side. Only 23.9% said they were not inclined to earn extra since they were satisfied with their present business.

Frequency PercentValid

PercentCumulative

PercentValid Yes 51 76.1 76.1 76.1

No 16 23.9 23.9 100.0Total 67 100.0 100.0

58

OPTION CHOSEN BY THE RESPONDENT TO MAKE EXTRA INCOME

Table 7

Frequency PercentValid

PercentCumulative

PercentValid MLM 8 11.9 11.9 11.9 MUTUAL FUND

AGENT/ INSURANCE AGENT

23 34.3 34.3 46.3

TRADING OF STOCK

23 34.3 34.3 80.6

INVESTMENT IN PROPERTY

13 19.4 19.4 100.0

Total 67 100.0 100.0

11.9

34.3

34.3

19.4

MLM

MUTUAL FUND AGENT/ INSURANCE AGENT

TRADING OF STOCK

INVESTMENT IN PROPERTY

Option Chosen By The Respondent To Make Extra Income

INFERENCE34.3% of the respondents wanted to earn that extra income by means of the trading of the stock or being an insurance advisor while 19.4% preferred investing in the property.

59

BEST INSURANCE COMPANY AS RATED BY THE RESPONDENT

Table 8

Frequency PercentValid

PercentCumulative

PercentValid LIC 46 68.7 68.7 68.7 ICICI 15 22.4 22.4 91.0 OTHER 6 9.0 9.0 100.0 Total 67 100.0 100.0

68.7

22.4

9

LIC

ICICI

OTHER

Best Insurance Company As Rated By The Respondent

INFERENCE

When the respondents were asked to give a name of insurance company, which they found best then one could easily see the impact of the LIC in life

60

of a common man since 68.7% instantly took the name of LIC only. ICICI Pru stood second with 22.4% people recalling its brand name.

INTEREST OF THE RESPONDENT IN JOINING ICICI PRU

Table 9

Frequency PercentValid

PercentCumulative Percent

Valid CERTAINLY 29 43.3 43.3 43.3 PROBABLY 26 38.8 38.8 82.1 DEFINITEL

Y NOT12 17.9 17.9 100.0

Total 67 100.0 100.0

43.3

38.8

17.9

CERTAINLY

PROBABLY

DEFINITELY NOT

Interest Of The Respondent In Joining ICICI PRU

INFERENCE

If given a choice to join ICICI Prudential as its advisor, almost 43.3% of the respondents said that they would certainly be interested while only 38.8%

61

said that they would think over it because as per them their decision depended on the money they will be getting from prudential in comparison to other insurance companies.

Interest Of The Respondent In Getting High Returns

Table 10

Frequency PercentValid

PercentCumulative

PercentValid Yes 58 86.6 86.6 86.6 No 9 13.4 13.4 100.0 Total 67 100.0 100.0

86.6

13.4

yes

no

Interest Of The Respondent In Getting High Returns

INFERENCE

86.6% of the total respondents said that they would definitely like to join a business where they will be rewarded with high returns without actually

62

spending a single penny from their pocket. While 13.4% said they are not interested since as per them there is no such business where you don’t have to invest any thing.

63

METHODOLOGY USED TO

RECRUIT ADVISOR The basic aim of the company in providing us with this assignment was to

find out the people’s perception of their brand in the market and via this

increasing their advisor base by encashing on their brand name.

1) Hence, our sales pitch in recruiting the good profile advisor was based

on:

Money:

For those who are needy, greedy and speedy

Excellent back end support, attractive payments and benefits and

Extensive training for that edge over competition

Reward and Recognition

For those who want to be recognized and honored

Several programs including foreign trips, seminars etc.

Selected club memberships like president’s club, ICICI Pru Star

Club, MDRT club etc.

Achievements rewarded with trophies and certificates as well

with Point rewards to give you a flying start.

Career Prospects

For people who want to climb the success ladder fast.

A program like PINNACLE, AGENCY

CHAMPION and TIGER TEAM has been devised.

64

This whole strategy was based on the MASLOW‘s THEORY OF NEEDS.

2) Then, instead of going personally and meeting these already well-

established

Advisors, we tried the concept of holding BOP (Business Opportunity

Presentation).

For this we drafted an invitation, which was a gimmick so as to entice

these advisors into coming to our own office, and it was based on the

pretext of ONE MILION POLICY CELEBRATIONS, the target that

ICICI PRU has just achieved.

And result was good in the sense that we were able to convert 5 to 10

advisors for our company then and there only.

3) Then, we targeted high profile people like CA’s or MBA’s or govt.

people.

For that, we drafted a letter in which we just gave them a hang of what our

proposal was for them (for recruiting them as our advisors) and asked them

to contact us themselves if they are interested.

We got at least 10-15 calls of people who were interested and wanted to

become our advisors. Meetings were held with them and they were

converted.

The BOP letter and then invitation for the BOP i.e. Business Opportunity

Presentation has been attached at the end in the annexure.

65

SWOT ANALYSISStrengths:

Vast untapped market

In a country of 1 billion people there is a huge potential market for life insurance products. In India the penetration of the insurance sector in the rural and semi-urban areas is low. There is a market of 900 million for life insurance and 200 million for householder’s insurance policy. In addition to this the affluent section can be tapped for Overseas Mediclaim and Travel Insurance policies.

Huge pool of skilled professionals

Whether it is banks or insurance companies there is no dearth of skilled professionals in India to carry out a successful bancassurance venture.

Weakness:

Lack of networking among bank branches

In spite of growing emphasis on total branch mechanization (TBM) and full computerization of bank branches, the rural and semi-urban banks have still to see information technology as an enabler. Complete integration of branch network involves huge investments for creating IT and communication infrastructure.

Low savings rate

Though we have a huge market for insurance policies, the middle class who constitutes the bulk of this market is today burdened under inflationary pressures. The secret lies in inculcating savings habit but considering the amount of surplus funds available with the middle class for investing in future security, the ability to save is very nominal

66

Opportunities:

Data mining

Banks have a huge customer database which has to be properly leveraged. Target segments should be identified and tapped.

Wide distribution networks of banks provides a great opportunity to sell insurance products through banks

Another potential area of growth of bancassurance is exploiting the corporate customers and tying up for insurance of the employees of corporate clients

Threats:

Human Resource Challenges

Success in banc assurance venture requires a change in mindset. Though we have a large talent pool, the inability to sell complex insurance products on the part of bank professionals and their reluctance to learn can be severe setback. There has to be a change in the thinking, approach and work culture.

Non-response from the target groups can also pose a challenge as it happened in the USA in 1980s

67

FUTURE GROWTH PROSPECTS OFCOMPANY :

IN the total market share, LIC has reduced its share from 91% to 70%. This

means that private insurance players have got more margins in their hands

which have increased from 9% to 30% in last 2years only.

In the private market share, ICICI PRU leads with 39% of the market share

in its hand followed by Bajaj Allianz with 18% shares and then comes Birla

Sun Life with 15% market shares.

ICICI PRU has been maintaining its NO 1 position since last 5 years

because of its prolific product range and commanding brand equity. It has a

highest capital base of Rs. 925 crores and a team of more than 56,300 well-

trained advisors. It enjoys a brand recall rate of 92% and gives credit of its

success to the 5 core values-

Integrity

Customer

Boundary Less

Ownership

Passion

68

MARKET SHARE IN PRIVATE

SECTOR

69

Total Market SharePrivate

Players

30%

LI C

70%

LIC

Private Players

LATEST UNIT VALUES OF SCHEME

Unit Values of different Plan options as on 08-06-2007

PlanUnit Value (Rs./unit)

Protector (Income) Plan* 15.2064

Balancer (Balanced) Plan* 24.14

Maximiser (Growth) Plan* 47.04

Pension Maximiser (Growth) Plan # 47.35

Pension Balancer (Balanced) Plan # 22.8

Pension Protector (Income) Plan # 13.654

Group Balanced Fund 15.86

Group Debt Fund 12.5022

Group Short Term debt fund 12.4647

Group Growth Fund 20.54

Group Capital Guarantee Short Term Debt Fund 11.8656

Maximiser (Growth) Fund II ^ 25.41

Preserver (Short Term) Fund * ^ 12.0221

Balancer (Balanced) Fund II ^ 15.6

Protector (Income) Fund II ^ 11.3331

Pension Preserver (Short Term) Fund # ~ 11.9604

Pension Maximiser (Growth) Fund II ~ 26.59

Pension Protector (Income) Fund II ~ 11.3368

Pension Balancer (Balanced) Fund II ~ 16.09

Invest Shield Cash *** 11.3759

70

Invest Shield Life ** 13.67

Invest Shield Pension 13.74

ICICI Prudential Life Maximiser III ^^ 11.92

ICICI Prudential Life Balancer III ^^ 11.21

ICICI Prudential Life Protector III ^^ 10.7264

ICICI Prudential Life Preserver III ^^ 10.8909

*Group Capital Guarantee Debt Fund 11.0156

*Group Capital Guarantee Balanced Fund 11.72

InvestShield Life New Fund ## 11.39

Group Capital Guarantee Growth Fund 10.69

Cash Plus Fund 11.9019

Secure Plus Fund 11.8

Secure Plus Pension Fund 11.5337

Flexi Growth * 10.86

Flexi Growth II ^ 10.9

Flexi Growth III ^^ 10.84

Pension Flexi Growth # 10.96

Pension Flexi Growth II ~ 10.88

Flexi Balanced * 10.55

Flexi Balanced II ^ 10.61

Flexi Balanced III ^^ 10.5

Pension Flexi Balanced # 10.73

Pension Flexi Balanced II ~ 10.62

Group Capital Guarantee Short Term Debt Fund II 10.2319

71

Group Capital Guarantee Debt Fund II 10.2166

Group Capital Guarantee Balanced Fund II 10.4

UNIT VALUE CONDITION BEFORE 30-04-07

SchemePerformanc

e(1 year)

Annualized

Returns (Since

Inception)

InceptionDate

Preserver * 7.59% 6.11% 17-May-04

Protector @ 5.42% 7.78% 16-Nov-01

Balancer # 6.18% 17.09% 16-Nov-01

Maximiser $ 6.69% 32.27% 16-Nov-01

Pension Preserver * 7.44% 5.91% 17-May-04

Pension Protector @ 5.47% 6.31% 31-May-02

Pension Balancer # 7.31% 17.81% 31-May-02

Pension Maximiser $ 7.38% 36.40% 31-May-02

InvestShield Cash @ 6.42% 5.30% 04-Jan-05

InvestShield Life ^ 10.63% 13.42% 04-Jan-05

InvestShield Pension ^ 9.96% 13.60% 04-Jan-05

So, in future it might be possible that the unit value of scheme and market

share of ICICI prudential life insurance will be increase.

72

COPETITIVE ANALYSIS WITH HDFC - STANDARD LIFE:

HDFC Standard Life Insurance Company is a joint venture

between India's largest housing finance provider, HDFC and

Europe's largest mutual life assurance company The Standard Life

Assurance Company (U. K).

Standard Life, UK , founded in 1825, has been at the forefront of

the UK insurance industry for 175 years by combining sound

financial judgment with integrity and reliability.

It is the Largest Mutual Life company in Europe and has total

assets of Rs. 5, 50,000 crore.

Training activities for agents/advisors.

As per IRDA guidelines, 100hrs training is compulsory.

Both online & classroom training are available.

Training is compulsory with both part-time & full time

Options.

An objective based exam is conducted by IRDA, the

minimum qualification required is-

12th pass for urban areas

10th pass for rural areas.

73

Commission Structure.

Depends on the product, like on savings

20-40% Ist year premium.

On investment 2%

On pension 7.5%

Modes & ways through which the company recruits agents. Direct contacts.

Newspaper adds.

Consultants.

Member of the company can introduce a new member.

Current agent force500-600 in NOIDA.

Top 5 USP’s (Unique Selling Proposition) Of HDFC Std.Life

Best insurer according to Outlook.

Well supported by foreign Ist private sector life insurance

Company to be granted a license.

Declared bonus every year from the day of incorporation

(only company.)

Provides fast service to the customers in terms of claim

74

During the exposure of 2 months I had in the insurance industry via

ICICI Prudential, it helped me to develop the basic understanding of how

this industry works and the work experience & knowledge gained has

also helped me to give the recommendations as stated below:

An insurance policy is a product, which needs a lot of convincing

before it can be sold because what I analyzed in this internship that

there are very few people who have a basic knowledge about life

insurance especially the lower middle class society. So, it is essential

for the advisor to know what the customer actually needs and then

letting the customer know what benefits he will get out of it.

The limitation here is how to win the trust of people when so many

companies are offering the same product range. Here, icici pru needs

to encash its brand name because after the survey I conducted what I

concluded is that after LIC if people know any other insurance

company is then it is ICICI Prudential.

During the calls where I went along with the Unit manager, I observed

that people in general have the perception that insurance is all about

getting discount in tax. People should be made realize that it is a great

way of saving for the future too.

Besides doing market research, my other job was also to increase the

advisor base of the company. And company preferred the profiles of

76

the already established insurance advisors of the other company

especially the LIC ones. What I suggest is that before approaching

these prominent agents we need to do a SWOT analysis of the co. they

are into. Like LIC Agents usually complain of LOW returns and

hence icici pru can tap them on this loophole of LIC.

Instead of approaching these good profile agents personally, the

company can hold Seminars Or Club Meetings because every one

comes for free lunches. Once they come, they can be given Business

Opportunity presentations about the incentives, commission structure

etc ICICI Pru is offering to its advisors.

Since the commission structure has been fixed by the IRDA only so

no insurance company can give more commission on products but

every company has a different mode of distributing commission, since

ICICI pru has all kind of products and policies with it (including the

products which LIC have and even those which LIC do not have) thus

every agent can earn as much (NO UPPER LIMIT ON EARNINGS)

as he wants because he has more choice to offer to the customer. This

can be one of the sales pitch for the ICICI Pru.

77

LEARNINGS The basic aim of the company in providing us with this assignment was to

find out the people’s perception of their brand in the market and via this

increasing their advisor base by encasing on their brand name.

I learned how to recruit insurance advisor and convinced

them for job profile.

When I was doing this project I met several people & collected their

responses, some of them give positive response, some gave negative

response & some can’t say any thing, they don’t believe in private sector. I

also personally met 20 to 25 people in a day. I also did Tele-calling & had

appointment. It is very helpful in the collection of the customer databases.

Under this project:

No. of customer met; more than 250

No. of customer called (phone); 300

No. of forms filled; more than 100

No. of customer converted; 25

ICICI Prudential Life Insurance Company is the number one private life

insurance company in India with a market share of 42.2%. Birla sun life

stands second in private life insurance companies with a market share of

18.5%. Looking in private sector ICICI Prudential has been the dominant

player because the amount of gap between the market shares is huge.

78

But if we analyze in all sectors of life insurance then LIC has been the

most dominant player since 1956. The impact of LIC has been so

much in both rural and urban areas that people use the term LIC

instead of life insurance.

ICICI prudential faces a big challenge in front of them to stay in the

race with Life insurance Corporation (LIC) because with the entrance

of other companies like Max New York, HDFC Standard Life & Birla

Sun Life the competition has become tougher.

But insurance is also growing day by day, India has a population of

1.2 billion and only 33.3% population is insured. This means

insurance is an upcoming industry but ICICI prudential has to work a

lot on their strategies to overcome LIC.

79

BIBLOGRAPHY

Monthly Fact Sheet MAY 2006

Mutual fund Review MAY 2006

Study Material for AMFI exam

Investment update report of other AMC’S

Various Business Newspaper

Magazines

WWW. AMFINDIA. COM

WWW. ICICIPRULIFE.COM

WWW.INVESTMSRTINDIA.COM

WWW.PERSONALFN.COM

WWW.ECONOMICTIMES.COM

WWW.STOCKINDIA.COM

80