icici group: strategy & performance spends strong fundamentals driven by domestic demand ......

TRANSCRIPT

ICICI Group: Strategy & Performance

November 2009

2

Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to uncertainty and changes in circumstances. Actual results may differ materially from those included in these statements due to a variety of factors. More information about these factors is contained in ICICI Bank's filings with the Securities and Exchange Commission.

All financial and other information in these slides, other than financial and other information for specific subsidiaries where specifically mentioned, is on an unconsolidated basis for ICICI Bank Limited only unless specifically stated to be on a consolidated basis for ICICI Bank Limited and its subsidiaries. Please also refer to the statement of unconsolidated, consolidated and segmental results required by Indian regulations that has been filed with the stock exchanges in India where ICICI Bank’s equity shares are listed and with the New York Stock Exchange and the US Securities Exchange Commission, and is available on our website www.icicibank.com.

3

Agenda

Market developments

Financial performance

Strategy & execution

4

Key economic indicators

Industrial production grew 9.1% in September 2009, on the back of 10.4% growth in August 2009

Strong capacity utilization in key sectors like steel, aluminium and cement

Increased momentum in home and car sales and debit card spends

Strong fundamentals driven by domestic demand

Q1-2010 GDP growth at 6.1% compared to 5.8% in Q4-2009

5

Key banking sector indicatorsComfortable systemic liquidity: About Rs. 1 trillion lent to RBI on a daily basis

10 year G–sec yields remain volatileBorrowing programme for first half of FY2010 completed successfully Borrowing programme for second half of FY2010 substantially lower

Non-food credit growth muted at 10% at end-October 2009

Growth expected to pick up in second half of FY2010 RBI’s projection for credit and deposit growth for FY2010 at 18%

6

Agenda

Market developments

Financial performance

Strategy & execution

7

Strategy for FY2010

Position balance sheet for next phase of growth

Cost• Keep stringent control on

operating expenses

Credit• Focus on selected credit

opportunities and reduce unsecured retail portfolio

CASA• Increase the proportion of low

cost CASA deposits• Reduce the proportion of

wholesale deposits

Capital• Maintain high capital adequacy

8

Progress in execution of strategy

Robust growth in CASA deposits

Reduction in operating expenses

Reduction in absolute level of net NPAs

Deceleration in retail NPA growth

Substantial progress in

achievement of near term

targets

Well capitalized for a period of sustained growth

9

-50

100150200250300350400450500550

Mar-03

Mar-04

Mar-05

Mar-06

Mar-07

Mar-08

Mar-09

Sep-09

Focus on CASA deposits

1,419

28.7%

Mar 2009

1,5201,262755614562469446Branches

36.9%26.1%21.8%22.7%24.3%23.0%15.5%CASA ratio

Sep 2009

Mar 2008

Mar 2007

Mar 2006

Mar 2005

Mar 2004

Mar 2003

CAGR 48%

Implementation underway for 580 new branches; target to open by March 2010

Sav

ings

dep

osi

ts (R

s. b

n)

10

High capitalisation levelsC

apita

l ad

equa

cy r

atio

ICICI Bank

Other top 9 Indian banks

As per the latest available financials(September 30, 2009)

11.9%

14.1% 13.8%13.5%

14.5%14.7%14.7%

16.5%17.7%

15.7%

0%

5%

10%

15%

20%

Tier-1 Tier-2

11

Stringent cost control

68.35

FY2009

28.72

H1-2010

79.7265.0247.2533.7125.98Operating expenses1

FY2008FY2007FY2006FY2005FY2004Rs. bn

Co

st/a

vera

ge a

sset

s

1. Including DMA

2.2%

1.8%

1.6%

2.3%

2.5%

2.4%

2.3%

1.0%1.2%

1.4%

1.6%

1.8%2.0%

2.2%

2.4%

2.6%

FY2004 FY2005 FY2006 FY2007 FY2008 FY2009 H1-2010

12

Domestic credit strategyICICI Bank moderated credit growth from end of FY2008 anticipating risks in the environment

Moderation in system non-food credit growth from 22.3% in FY2008 to 17.5% in FY2009 and 10.3% at end-October 2009

ICICI Bank using the opportunity to rebalance its funding profile

Areas of growth: mortgages, vehicle loans, project finance and commercial banking

Personal loan disbursements and new credit card issuances reduced substantially from FY2008 levels

13

International business strategyStrong term deposit mobilisation capability in UK and Canada subsidiaries

To be selectively deployed primarily in India-linked assets

Asset repayments in international branches being used to repay maturing liabilities

Limited growth in overall international balance sheet

14

Non-banking subsidiaries strategyICICI Life: Focus on consolidating position as largest private sector life insurer, while maintaining new business profit margins

ICICI General: Focus on maintaining leadership, while improving underwriting profitability

ICICI AMC: Maintain market position among the top three mutual funds

ICICI Securities: Capitalize on retail broking platform and market opportunities to increase revenues and profitability

15

Agenda

Market developments

Financial performance

Strategy & execution

16

Overview: Q2-2010

Standalone profit after tax of Rs. 10.40 billion in Q2-2010

18% sequential increase in standalone profit after tax from Rs. 8.78 billion in Q1-2010Profit after tax in Q2-2009 was Rs. 10.14 billion

Consolidated profit after tax1 of Rs. 11.45 billion in Q2-2010

11% sequential increase in consolidated profit after tax1 from Rs. 10.35 billion in Q1-201076% increase over consolidated profit after tax1 of Rs. 6.51 billion in Q2-2009

1. Unaudited

17

Overview: Q2-2010

Net interest income for Q2-2010 at Rs. 20.36 billion compared to Rs. 19.85 billion for Q1-2010

Net interest margin increased from 2.4% in Q1-2010 to 2.5% in Q2-2010Net interest income in Q2-2009 was Rs. 21.48 billion

Fee income of Rs. 13.87 billion in Q2-2010 compared to Rs. 13.19 billion in Q1-2010

Fee income in line with the reduced investment and mergers & acquisition activity in the corporate sector, reflecting the change in market conditions in the second half of fiscal 2009

Sequential improvement in operating trends

18

Overview: Q2-2010

Continued reduction in operating expenses8% sequential decrease in operating & DMA expensesCost/average asset ratio for Q2-2010 at 1.5% compared to 1.6% for Q1-2010 and 1.7% for Q2-2009

19% sequential decline in total provisions to Rs. 10.71 billion in Q2-2010 from Rs. 13.24 billion in Q1-2010

Sequential improvement in operating trends

19

Balance sheet highlightsCASA ratio of 36.9% at September 30, 2009 compared to 30.0% at September 30, 2008 and 30.4% at June 30, 2009

Increase of Rs. 48.59 bn in savings deposits and Rs. 40.94 bn in current deposits during the quarter

Total capital adequacy of 17.7% and Tier-1 capital adequacy of 13.3% as per RBI’s Basel II framework

Net NPA ratio of 2.19% at September 30, 2009; at the same level as June 30, 2009

20

Performance of subsidiariesICICI Life: Increased market share from 5.5% in April 2009 to 9.3% in September 2009

New business margin maintained at about 19%

ICICI General: Maintained profitability and market share despite continued impact of de-tariffing

ICICI AMC: Maintained market position among the top three mutual funds

ICICI Securities: Increase in revenues and profitability in line with market volume growth, driven by retail broking platform

21

Thank you

22

Annexure

23

Unconsolidated financials

24

Profit & loss statement(Rs. in billion)

148.8%1.551.020.531.690.413.35- Dividend income

(65.5)%0.420.380.041.591.133.01- Other income

24.35

0.46

0.21

13.58

38.60

2.97

13.87

18.24

20.36

Q2-2010

22.85

0.52

1.45

15.43

40.25

(1.53)

18.76

18.77

21.48

Q2-2009

39.99

1.04

3.73

31.77

76.53

(7.47)

38.34

34.15

42.38

H1-2009

25.29

0.52

0.27

14.67

40.75

7.14

13.19

20.90

19.85

Q1-2010

49.64

0.98

0.48

28.25

79.35

10.11

27.06

39.14

40.21

H1-2010

-4.43- Treasury income

(4.1)%159.70Total income

6.6%

(13.2)%

(85.6)%

(12.0)%

(26.1)%

(2.8)%

(5.2)%

Q2-o-Q2growth

5.29DMA expenses

89.25

2.10

63.06

65.24

76.03

83.67

FY2009

Operating profit

Lease depreciation

Operating expenses

- Fee income

Non-interest income

NII

25

Profit & loss statement(Rs. in billion)

10.14

3.47

13.61

9.24

22.85

Q2-2009

17.42

5.41

22.83

17.16

39.99

H1-2009

8.78

3.27

12.05

13.24

25.29

Q1-2010

10.40

3.24

13.64

10.71

24.35

Q2-2010

19.18

6.51

25.69

23.95

49.64

H1-2010

6.6%89.25Operating profit

16.0%38.08Provisions

37.58

13.59

51.17

FY2009

2.6%

(6.7)%

0.2%

Q2-o-Q2growth

Profit before tax

Profit after tax

Tax

26

Balance sheet: Assets(Rs. in billion)

1. Investment in security receipts of asset reconstruction companies at September 30, 2009 was Rs. 37.26 bn.

Credit derivative exposure (including off balance sheet exposure) of Rs. 54.08 bn at September 30, 2009 (underlying comprises Indian corporate credits).

Including impact of exchange rate movement

23.4%778.34704.86633.87630.73- SLR investments

21.1%121.00120.97120.9799.93- Equity investment in

subsidiaries

3,849.71

302.25

2,219.85

971.48

356.13

Sep 30, 2008

3,674.19

245.42

1,981.02

1,142.47

305.28

Jun 30, 2009

23.5%1,199.651,030.58Investments

3,663.74

262.82

1,908.60

292.67

Sep 30, 2009

(4.8)%

(13.0)%

(14.0)%

(17.8)%

Y-o-Y growth

3,793.01

279.66

2,183.11

299.66

Mar 31, 2009

Total assets

Fixed & other assets

Advances

Cash & bank balances

27

Credit cards6.8%

Other secured

2%

STPL0.2%

Personal loans

7%

Home57%

Vehicle loans26%

Composition of loan book: September 30, 2009

1. STPL: Small ticket personal loans2. Vehicle loans includes auto loans 11%, commercial

business 14% and two wheelers 1%3. Retail business group includes builder loans and dealer

funding of Rs. 27.41 bn

Total loan book: Rs. 1,909 bn Total retail loan book: Rs. 864 bn

1

SME4%

Rural6%

Retail business

group45%

Overseas branches

27%

Domestic corporate

18%

3

2

28

Equity investment in subsidiaries(Rs. in billion)

99.93

0.14

0.05

0.61

0.87

1.58

3.00

10.96

10.47

23.24

14.59

34.42

Sep 30, 2008

120.97

0.14

0.05

0.61

0.87

1.58

3.00

10.96

11.12

23.25

33.50

35.90

Mar 31, 2009

11.12ICICI Home Finance

23.25ICICI Bank UK

0.61ICICI AMC

33.50ICICI Bank Canada

3.00ICICI Bank Eurasia LLC

10.96ICICI Lombard General Insurance

1.58ICICI Securities Primary Dealership

0.14Others

121.00

0.05

0.87

35.93

Sep 30, 2009

Total

ICICI Venture Funds Mgmt Co.

ICICI Securities Limited

ICICI Prudential Life Insurance

29

Balance sheet: Liabilities(Rs. in billion)

Credit/deposit ratio of 75% on the domestic balance sheet at September 30, 2009

Figures include impact of exchange rate movement

5.2%997.73908.81928.05948.49Borrowings

14.2%493.18444.59410.36431.74- Savings

0.9%236.12195.18216.32237.40- Current

3,849.71

177.25

2,234.02

3.50

475.32

11.13

486.45

Sep 30, 2008

3,663.74

171.61

1,978.32

3.50

501.44

11.14

512.58

Sep 30, 2009

(4.8)%

(3.2)%

(11.4)%

-

5.5%

0.1%

5.4%

Y-o-Y growth

3,793.01

182.65

2,183.48

3.50

484.20

11.13

495.33

Mar 31, 2009

3,674.19

157.59

2,102.36

3.50

490.80

11.13

501.93

Jun 30, 2009

Total liabilities

Other liabilities

Deposits

Preference capital

- Reserves

- Equity capital

Net worth

30

Composition of borrowings

908.81

505.71

16.21

521.92

137.54

249.35

386.89

Jun 30, 2009

504.10 578.53 Overseas

234.42 159.14 - Other borrowings1

259.21 210.82 - Capital instruments

997.73

487.82

16.28

493.63

Sep 30, 2009

948.49

562.65

15.88

369.96

Sep 30, 2008

Total borrowings

- Other borrowings

- Capital instruments

Domestic

(Rs. in billion)

Capital instruments contribute 53% of domestic borrowings

Figures include impact of exchange rate movement1. Includes short term borrowings

31

Capital adequacy (Basel II)

718.32

2,556.08

3,274.40

140.77

428.42

569.19

Jun 30, 2009

4.3%

13.1%

17.4%

3,240.323,564.63Total RWA

2,501.212,758.15- On balance sheet

739.11806.48- Off balance sheet

141.67

431.42

573.09

131.59

421.97

553.55

3.7%

11.8%

15.5%

Mar 31, 2009

4.4%

13.3%

17.7%

Sep 30, 2009

- Tier II

- Tier I

Total Capital

Rs. billion except %

32

Key ratios(Percent)

1. Based on quarterly average net worth2. Annualised for all interim periods

1.51.61.71.8Cost/average assets (incl. DMA)2

36.9%30.4%30.0%28.7%CASA ratio

42.5

47.2

2.4

437

36.1

8.4

Q2-2009

37.1

32.8

2.4

451

31.6

7.0

Q1-2010

36.441.4Fee/income

43.4

2.4

445

33.8

7.7

FY2009

460Book value (Rs.)

36.1

2.5

37.1

8.1

Q2-2010

Cost/income (incl. DMA)

Net interest margin2

Weighted avg EPS (Rs.)2

Return on average net worth1, 2

33

Asset quality and provisioning(Rs. in billion)

Gross retail NPLs at Rs. 64.22 bn and net retail NPLs at Rs. 30.12 bn at September 30, 200958% of net retail NPLs are from unsecured productsNet restructured loans of Rs. 48.57 bn at September 30, 2009

1. Gross NPAs and cumulative provisions include technical write-offs of Rs. 1.26 bn at September 30, 2009

14.36Outstanding general provision on standard assets

2.19%2.19%1.96%Net NPA ratio

46.67

50.28

96.95

Jun 30, 2009

46.19

53.10

99.29

Mar 31, 2009

45.58

49.13

94.71

Sep 30, 2009

Net NPAs

Less: Cumulative provisions

Gross NPAs

34

Overseas subsidiaries

35

ICICI Bank UK asset profile1

1. Includes cash & advances to banks and certificates of deposit

2. Includes US$ 165 mn of India-linked credit derivatives3. Includes securities reclassified to loans & advances in

FY20094. Does not include US$ 157.4 mn of ABS reclassified as

loans & receivable in FY2009

Total assets:USD 8.0 billion

2

4

Net profit of USD 12.6 million in Q2-2010

Capital adequacy ratio at 16.3%

Net MTM write-back of USD 61.0 million (post-tax) in reserves in Q2-2010

Loans & advances

50%

Asset backed securi ties

2%

Other assets & investments

4%

Ind ia l inked investments

5%

Cash & l iquid securi ties

12%

Bonds/notes o f financ ial insti tutions

27% `3

36

ICICI Bank UK liability profile

Total liabilities:USD 8.0 billion

Proportion of retail term deposits in total deposits increased from 35% at September 30, 2008 to 65% at September 30, 2009

Long term Debt14%

Net worth7%

Term deposi ts43%

Other l iab i l i ties

5%

Syndicated loans &

interbank borrowings

9%

Demand deposi ts

22%`

37

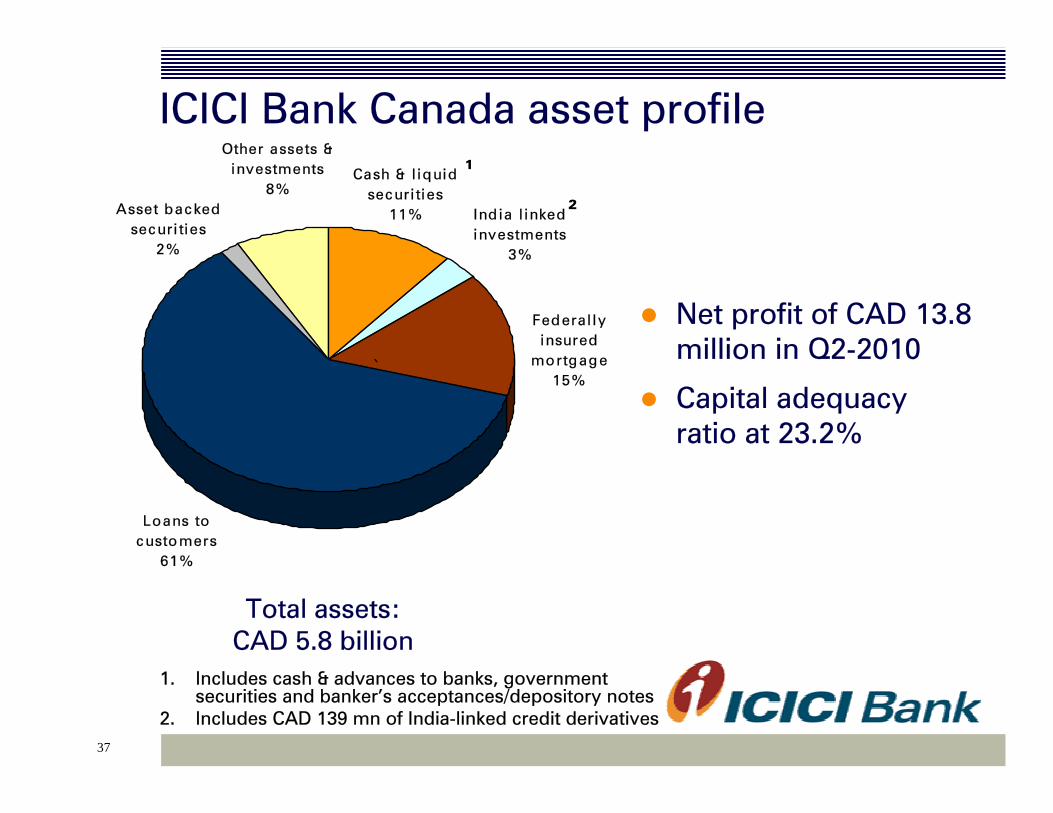

ICICI Bank Canada asset profile

1. Includes cash & advances to banks, government securities and banker’s acceptances/depository notes

2. Includes CAD 139 mn of India-linked credit derivatives

Total assets:CAD 5.8 billion

1

2

Net profit of CAD 13.8 million in Q2-2010

Capital adequacy ratio at 23.2%

Loans to customers

61%

Ind ia l inked investments

3%

Asset backed securi ties

2%

Other assets & investments

8%

Federal ly insured

mortg age15%

Cash & l iquid securi ties

11%

`

38

ICICI Bank Canada liability profile

Total liabilities:CAD 5.8 billion

ICICI Bank Canada balance sheet funded largely out of retail term deposits

Term deposi ts69%

Other l iab i l i ties

2%

Demand deposi ts

11%

Net worth17%

Borrowings1%

`

39

ICICI Bank Eurasia

• Total borrowings of USD 370 million at September 30, 2009

• Capital adequacy of 21.4% at September 30, 2009

• Financial breakeven in H1-2010

1. Includes cash, balances with central bank, nostrobalances, govt bonds & placements with banks

Total assets:USD 453 million

1

Corporate bonds

7%

Retail loans16%

Other assets1%

Cash & liquid securit ies

37%

Loans to corporates &

banks39%

40

Key non-banking subsidiaries

41

ICICI Life

14.8%

301.07

(3.08)

18.7%

2.81

36.56

18.73

15.06

Q2-2009

10.8%

500.93

(0.69)

19.2%

2.33

36.34

23.97

12.12

Q2-2010

Expense ratio

Assets Under Management

NBP margin

New Business Profit (NBP)

Renewal premium

APE

Statutory Loss

Total premium

(Rs. in billion)

Continued market leadership in private sector1

1. During the half year ended September 30, 2009 on new business retail weighted received premium basis.

42

ICICI General

Continued market leadership in private sector2

1. Excluding remittances from third party motor pool

2. During the half year ended September 30, 2009

0.590.04PBT

0.510.01PAT

8.018.48Gross premium1

Q2-2010Q2-2009

(Rs. in billion)

43

Other subsidiaries(Rs. billion)

0.280.18ICICI Home Finance Company1

0.16

0.10

0.09

0.10

Q2-2009

0.48ICICI Prudential Asset Management Company

0.38ICICI Securities Ltd.

0.14

-

Q2-2010Profit after tax

ICICI Venture

ICICI Securities PD

Consolidated profit after tax increased by 76% from Rs. 6.51 billion in Q2-2009 to Rs. 11.45 billion in Q2-2010

1. Loan book of ICICI HFC was Rs. 120.04 bn at September 30, 2009 (June 30, 2009: Rs. 109.34 bn; September 30, 2008: Rs. 115.90 bn)