icca masterclass 2014

TRANSCRIPT

ICCA Masterclass 2014 VAT for International Events in UK

and Ireland

September 2014

2

Why is VAT important?

Three aspects to consider:

Worldwide VAT/GST rates broadly 15-25%, some reduced rates, UK and Ireland standard rates 20% and 23%

It impacts on the profitability of an event

the organiser

the host

the attendee

It can erode margins and impact budgets if not factored in

The Organiser (1)

Location – ensure VAT is on your list of considerations

EU VAT rules enable the VAT impact to be neutralised to an

extent, some more than others, need to consider the whole

chain

UK and Ireland regarded as pragmatic, Ireland slightly more

restrictive on VAT recovery for delegates than UK (on car hire,

food and drinks)

3

4

The Organiser (2) - VAT efficient

structuring for EU events

Acting as agent (disclosed) is most cost effective from VAT perspective due to Tour Operator’s Margin Scheme in EU (TOMS) – host contracts in its own name with venue etc

NB reveals organiser’s margin/fee

• TOMS is a VAT simplification used within the EU where overnight accommodation and/or passenger transport is provided to attendees alongside entrance to event

• Relevant to host’s charges to delegates or on organisers charge to host in some situations

• Inherent VAT cost so recommended contractual position is agency throughout chain

• Organiser can still handle all documentation/tax invoices from hotels etc and make payment

5

The Organiser (2) - VAT Rules

Your Revenue

• Event organising/management fee and related – B2B revenue – subject to VAT where host is located. If both you and host in the same country, you should charge VAT, regardless of where event takes place. If you are in UK or Ireland and host is in a different location, you do not charge VAT, show their VAT # on invoice and

they will self assess local VAT in their country if required – this is VAT neutral

Your Costs

• VAT incurred should be fully recoverable provided it is your VAT (ie invoices correctly addressed to you per the contracts

• VAT incurred overseas only recoverable if an overseas refund mechanism exists (mainly just EU countries, ad hoc others)

• UK and Irish VAT costs should be recoverable • If contracts structured efficiently, venue costs should not be incurred by organiser

6

The Host (1) – VAT Rules

Your Revenue

• Delegate entrance fees – subject to VAT where event takes place,

overseas VAT registration required (EU and most other locations), need to consider impact on pricing early for promotional material

• Sponsorship and advertising – B2B subject to VAT where sponsor is located. If both you and host in same country you should charge VAT, regardless of where the event takes place. If the sponsor is in a different country to you, you do not charge VAT, show their VAT # on invoice and they will self assess local VAT in their country if

required . • Delegate goody bags – subject to VAT where event takes place as

supply of tangible goods - VAT registration required

Your Costs

• Venue hire, accommodation, catering etc – local VAT incurred at reduced or standard rate, should be fully recoverable through local VAT registration. Tax Invoices in host name required to support this

(not organiser name) along with supporting contracts/Agreements • Other conference related costs – many eg design, comms, should

be without local VAT • VAT on costs you incur in your home country in relation to the event

should be fully recoverable on your local VAT return

7

The Host (2) – VAT Rules

• Where there is no charge for entrance to the event

there will be no local VAT registration obligation

• Local VAT incurred on costs can be recovered

provided the event is not regarded as a business

entertainment event (product launch events etc

complex)

• The overseas VAT refund mechanism would be used

to claim the VAT

• The UK and Ireland have generous rules on VAT

recovery compared to other EU locations (although

Ireland blocks some recovery on food, car hire)

8

The Delegates (1) – VAT Rules

• VAT is a consumption tax:

• forms a cost for private individuals (eg most attendees at consumer events)

• generally should not form a cost for businesses except those in certain sectors (eg finance, insurance, health, education). Domestic VAT recovered through their VAT return

• Need to consider impact of VAT on delegate fees when setting pricing as can

have material impact if delegate cannot get a credit

9

The Delegates (2) – VAT Rules

EU Member States plus small number of non EU locations (inc Switzerland) refund VAT to non established businesses

Rules on what is recoverable vary from country to country

Most refund VAT on typical conference costs but none refund VAT on ‘business entertainment’ costs

Some countries (not UK or Ireland) do not refund VAT to US businesses – lack of

reciprocity

Refund claims can be filed quarterly or annually, refund received 9-12 months later

Be proactive - raise awareness with attendees that VAT can be recovered (VAT refund businesses) as this reduces the cost of the event

Customs Duty

Incurred on the movement of

hardware/goods into UK/Ireland from

non EU location, or from UK/Ireland into a

non EU location

Customs duty forms a cost

Reliefs for exhibitions/events where

stands and comms equipment shipped

cross border

conditions attached, focused on the

kit leaving the country again

Freight forwarders/shipping agents need

to be briefed to ensure they use the

correct codes on import so that no

customs duty or import VAT is payable

10

11

10 Tips for a more profitable event

1. Factor VAT into your cost projections – for hosts VAT on costs (including any import VAT) will generally only be recoverable if you register for VAT in the country in question

2. Map out different revenue streams and determine VAT treatment in advance

3. If an overseas registration is required, ensure this infrastructure is in place before revenues start being received and promotional material/website finalised

12

10 Tips for a more profitable event

4. Generally more cost effective to act as disclosed agent where possible (invoices and contracts in client’s name) 5. Raise awareness of attendee’s ability to recover overseas VAT

6. Factor overseas VAT into entrance fee for events – anticipate VAT rate changes

13

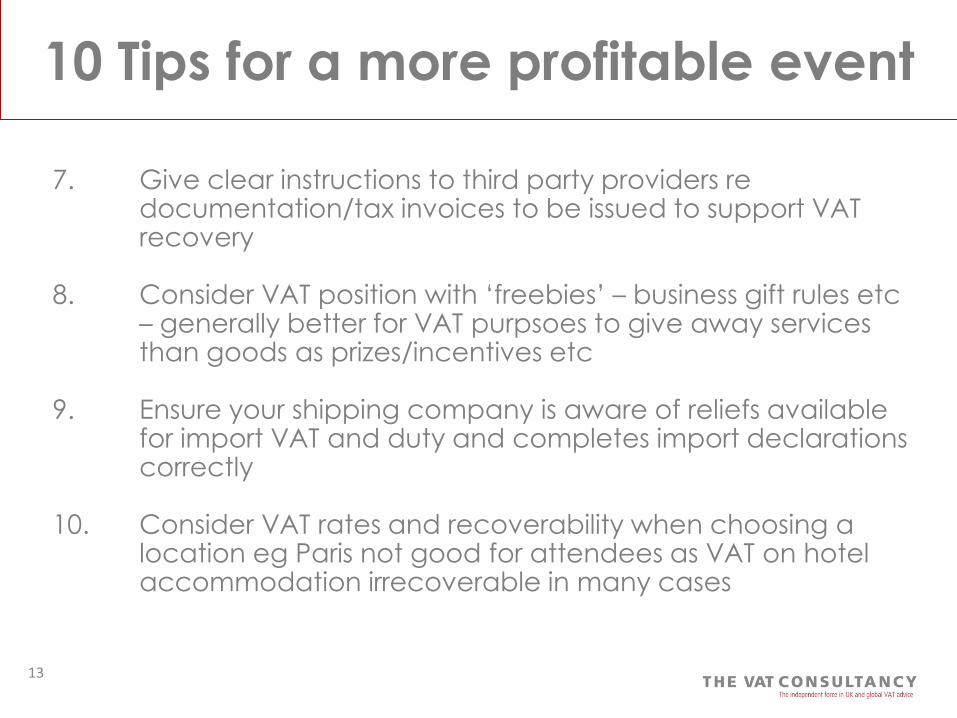

10 Tips for a more profitable event

7. Give clear instructions to third party providers re documentation/tax invoices to be issued to support VAT recovery

8. Consider VAT position with ‘freebies’ – business gift rules etc – generally better for VAT purpsoes to give away services than goods as prizes/incentives etc

9. Ensure your shipping company is aware of reliefs available for import VAT and duty and completes import declarations correctly

10. Consider VAT rates and recoverability when choosing a location eg Paris not good for attendees as VAT on hotel accommodation irrecoverable in many cases

Julie Park

Managing Director

Email: [email protected]

London Office: 020 8941 9200

Sean McGinness

Senior VAT Manager

Email: [email protected]

Head Office: 01962 735350

www.thevatconsultancy.com