ibisworld industry report 71391 golf courses & country ...course... · ibisworld industry...

TRANSCRIPT

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 1

IBISWorld Industry Report 71391Golf Courses & Country Clubs in the USAugust�2011� Taylor�Hamilton

Stable course: Retiring baby boomers and rising participation will support industry demand

2� About�this�Industry2 Industry Definition

2 Main Activities

2 Similar Industries

3 Additional Resources

4� Industry�at�a�Glance

5� Industry�Performance5 Executive Summary

5 Key External Drivers

6 Current Performance

9 Industry Outlook

11 Industry Life Cycle

13� Products�&�Markets13 Supply Chain

13 Products & Services

14 Demand Determinants

15 Major Markets

17 International Trade

18 Business Locations

20� Competitive�Landscape20 Market Share Concentration

20 Key Success Factors

21 Cost Structure Benchmarks

22 Basis of Competition

23 Barriers to Entry

23 Industry Globalization

24� Major�Companies

27� Operating�Conditions27 Capital Intensity

28 Technology & Systems

28 Revenue Volatility

29 Regulation & Policy

30 Industry Assistance

31� Key�Statistics31 Industry Data

31 Annual Change

31 Key Ratios

32� Jargon�&�Glossary

www.ibisworld.com��|��1-800-330-3772��| ��[email protected]

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 2

This industry includes firms that operate golf courses as their primary activity and may include country clubs that have dining and other recreational facilities. These establishments often provide food and beverage services,

equipment rental services and golf instruction. Golf courses can be public, private, semiprivate or part of a country club. This industry excludes golf driving ranges, miniature golf facilities and golf course resorts and hotels.

The�primary�activities�of�this�industry�are

Operation of golf courses and country clubs

Operation of associated golf course services – food and beverage

Operation of associated golf course services – golf equipment rental services

Operation of associated golf course services – golf instruction services

Operation of country clubs

71399 Golf�Driving�Ranges�&�Family�Fun�Centers�in�the�USOperating driving ranges and miniature golf courses is classified in Industry 71399 – All Other Amusement and Recreation Industry in the US.

72111 Hotels�&�Motels�in�the�USOperating resorts where golf facilities are combined with accommodations is classified in Industry 72111 – Hotels (except Casino Hotels) and Motels in the US.

72112 Casino�Hotels�in�the�USOperating resorts where golf facilities are combined with accommodations is classified in Industry 72112 – Casino Hotels in the US.

72119 Bed�&�Breakfast�&�Hostel�Accommodations�in�the�USOperating resorts where golf facilities are combined with accommodations is classified in Industry 72119 – Other Traveler Accommodation in the US.

Industry�Definition

Main�Activities�

Similar�Industries

About�this�Industry

The�major�products�and�services�in�this�industry�are

Equipment rentals and sales

Food and beverage sales

Golf course green fees

Membership fees

Other sales and service fees

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 3

About�this�Industry

Additional�Resources For�additional�information�on�this�industry

www.ihrsa.org�International Health, Racquet & Sportsclub Association

www.ngf.org�National Golf Foundation

www.usga.org�United States Golf Association

�IBISWorld writes over 700 US industry reports that are updated up to four times a year. To see all reports, go to www.ibisworld.com

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 4

Hou

rs p

er d

ay

5.30

5.05

5.10

5.15

5.20

5.25

1501 03 05 07 09 11 13Year

Time spent on leisure and sports

SOURCE: WWW.IBISWORLD.COM

% c

hang

e

6

−4

−2

0

2

4

1703 05 07 09 11 13 15Year

Revenue Employment

Revenue vs. employment growth

Products and services segmentation (2011)

39%Membership fees

25%Golf course green fees

21%Food and

beverage sales

8%Other sales and

service fees

7%Equipment rentals

and sales

SOURCE: WWW.IBISWORLD.COM

Key�Statistics�Snapshot

Industry�at�a�GlanceGolf�Courses�&�Country�Clubs�in�2011

Industry�Structure Life Cycle Stage Mature

Revenue Volatility Low

Capital Intensity Medium

Industry Assistance None

Concentration Level Low

Regulation Level Medium

Technology Change Low

Barriers to Entry High

Industry Globalization Low

Competition Level High

Revenue

$22.3bnProfit

$445.3mWages

$8.8bnBusinesses

10,885

Annual�Growth�11-16

1.5%Annual�Growth�06-11

0.6%

Key�External�DriversTime�spent�on�leisure�and�sportsPer�capita�disposable�incomeCompetition�from�hospitality�clubsHouseholds�earning�over�$100,000Median�age�of�population

Market�ShareThere are no Major Players in this industry

p. 24

p. 5

FOR ADDITIONAL STATISTICS AND TIME SERIES SEE THE APPENDIX ON PAGE 31

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 5

Key�External�Drivers Time spent on leisure and sportsAn increase in available leisure time for golfers and country club patrons will encourage higher participation and demand for services. This factor will contribute to growth in industry revenue. However, this driver is expected to decrease slowly over 2011, representing a potential threat to the industry.

Per capita disposable incomeIncreased household disposable income leads to greater expenditure on leisure activities. In particular, an increase in per capita disposable income benefits demand for expensive golf and country club memberships. This driver is expected to increase slowly over 2011.

Competition from hospitality clubs Increased competition from other industries that supply substitute products and services can reduce industry revenue. This competition may come from other recreational sports, other hospitality establishments or rival country clubs. This driver is expected to remain flat over 2011.

Households earning over $100,000Country club memberships are often very expensive; therefore, only wealthier individuals can afford these luxuries. Wealthy households are most likely to spend significant money each year on green fees and country club memberships. This driver is expected to increase over 2011, resulting in a potential opportunity for the industry.

Executive�Summary

Over five years to 2011, the Golf Courses and Country Clubs industry has experienced declines due to lower spending and high unemployment. These recessionary conditions eroded revenue growth that was achieved in 2006 and 2007. During the five years since 2006, IBISWorld expects revenue increased 0.6% on average per year to about $22.3 billion in 2011.

The recession caused individuals to cut discretionary spending on recreational activities like golf. Because the cost of maintaining a golf course or country club remains fairly constant regardless of customer participation, a decline in the number of individuals attending golf courses or paying club fees caused most establishments to

suffer losses. As a result of these conditions, enterprises declined at an average annual rate of 0.4% to total 10,885 in the five years to 2011. Slow increases in golfing participation and the emergence of alternative recreational activities have also hindered industry growth.

While adverse conditions have plagued the industry as of late, golf courses and country clubs provide a very popular activity for customers; outside of financial barriers, demand for and interest in golf continue to grow. IBISWorld anticipates the industry to regain revenue in 2011 by 1.6%, thanks to a stabilizing economy and increasing discretionary spending. The industry is projected to benefit from sustained demand in the future and post average revenue growth of 1.4% per year to $23.9 billion by 2016. The industry is also expected to break the drought in profit, with increased participation in 2011 anticipated to yield positive margins.

Industry�PerformanceExecutive�Summary�� |�� Key�External�Drivers�� |�� Current�PerformanceIndustry�Outlook�� |�� Life�Cycle�Stage

� Growing demand for and interest in golf will slowly revive the industry, boosting revenue

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 6

Industry�Performance

Increased�participation

Recently, increases in participation have coincided with falling revenue. The difference indicates growing numbers of occasional golfers. These golfers only play up to seven times a year and do not significantly influence revenue levels. Regular or avid golfers, who play at least 25 rounds annually, may constitute a small segment of participants; however,

avid golfers account for most golf-related spending (about 65.0% of revenue). The number of core golfers (those who play eight weeks or more per year) has declined as a proportion of total participants. This trend does not bode well for the industry, which generates significantly more of its revenue from regular golfers than occasional golfers.

Current�Performance

Since 2006, the Golf Courses and Country Clubs industry has been hit hard by a drop in consumer and business spending. Because the industry relies solely on its customer base, declining participation has limited growth to 0.6% annually on average. Consumer sentiment and household wealth have taken a plunge since the recession began in 2008, causing many

to cut back on expensive leisure activities. Golfing is considered a leisure activity, but it is also a luxury. The sport remains popular in the United States, so it is poised to benefit from sustained demand in the future. In 2011, rebounding disposable incomes are expected to lead to increased spending on golfing, pulling revenue up 1.6% to $22.3 billion.

Key�External�Driverscontinued

Median age of populationGolf is a sport of precision in a calming setting, rather than a fast-paced game of athleticism. An aging population means there will be more

retirees with more leisure time. This trend creates additional demand for golf and country club activities. This driver is expected to increase slowly over 2011.

% c

hang

e

4

−1

0

1

2

3

1705 07 09 11 13 15Year

Per capita disposable income

SOURCE: WWW.IBISWORLD.COM

Hou

rs p

er d

ay

5.30

5.05

5.10

5.15

5.20

5.25

1501 03 05 07 09 11 13Year

Time spent on leisure and sports

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 7

Industry�Performance

Increased�participationcontinued

The recession also adversely affected the industry. With sharp declines in spending and sentiment, many Americans had to cut down on their golfing and or even give up their country club memberships. The industry took its largest full-year revenue hit in 2009, with overall numbers dropping 2.0% that year. Though consumer sentiment improved in 2010, golfing is not anticipated to be high on the priority list for those strongly affected by the recession, even as sentiment continues to revive in 2011.

Golf�courses�in�the�rough

A major consequence of the decline in golfing and country club participation since the recession has been the industry’s lack of profitability. Due to strenuous conditions, IBISWorld estimates that industry profit (earnings before interest and taxes) will only make up 2.0% of revenue in 2011, totaling $442.0 million.

Golf courses and country clubs have experienced tough operating conditions in recent years. High competition, reduced demand and negative earnings have forced many clubs to close, and this trend has accelerated from 2008 onward by tight access to credit and a deteriorating economy. The situation provided an opportunity for well-

funded companies to expand their golf course portfolio as courses were put up for sale. For instance, ClubCorp purchased Seville Golf & Country Club in Gilbert, AZ, in 2008.

With increased competition among participants for fewer golfers, establishments invested more resources into retaining existing members and attracting new ones. Operators discounted memberships, provided reciprocal membership rights to other clubs and improved golf course and country club facilities. Country clubs increased the number of rounds played, particularly during off-peak seasons, by lowering green fees or increasing services.

Necessary�restructuring

In order to reduce operational costs, operators have increased the outsourcing of course maintenance to third parties. Golf course maintenance companies are often able to lower expenditures on material, such as fertilizers and turf, due to bulk purchases from wholesalers. While outsourcing course maintenance has lowered expenses for some golf courses, it can also result in a loss of control and quality of work over time.

Insurance costs have increased for golf courses and country clubs in recent years. Premiums have increased due to heightened legal action taken by individuals hit by golf balls within country club facilities. This trend has pushed green fees higher and is likely to increase in the future.

Reduced golfing participation, combined with a growing number of golf courses and country clubs, forced

Golfi�ng�participation�in�the�United�States

YearParticipants�

(Millions) (% change)

2006 30.0 0.72007 30.1 0.32008 29.8 -1.02009 29.4 -1.32010 29.6 0.72011* 30.0 1.4

*EstimateSOURCE: IBISWORLD

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 8

Industry�Performance

Necessary�restructuringcontinued

industry participants to look for alternative methods of boosting revenue in recent years. This factor has been achieved in several ways, including

improved food and drink services, greater retail sales of golf equipment, promotion of lessons and golfing clinics and better practice facilities.

Fairways�to�bunkers Throughout the 1990s and early 2000s, the development of public golf facilities in the United States increased. Competition in this market has intensified since, with increased availability of daily fee courses adversely affecting demand for some of the country club markets. According to the National Golf Foundation, the growth in supply of available golf courses, fueled by the daily fee market, has outpaced growth in the number of golfers. New golf course construction has experienced slower growth since 2002 due to the acknowledgment of overbuilding in certain markets and fewer residential developers building golf courses to aid housing sales.

In addition to shrinking growth for new course construction, more golf course closings have occurred in the past few years than ever before. In the five years to 2011, the number of golf

courses and country club locations declined at an annualized rate of 0.3% to 11,686. In accordance with the reduction in establishment numbers, employment numbers also declined in 2008 and 2009. Net losses have encouraged golf course operators to examine ways to cut costs, including wage expenses, with the larger firms cutting back on staffing levels in 2008 and 2009. Despite those declines, industry employment has increased at an annualized rate of 0.7% over five years to 320,416 in 2011. A quick rebound in employment over the past year has been driven by consumer demand for high-quality services.

� The growth in golf courses has outpaced growth in the number of golfers

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 9

Industry�Performance

Teeing�off�once�again By the end of 2016, more than 31 million Americans aged 12 and older will play golf at least once during the year. This rising golf participation will be a key driver of revenue growth. Industry profit margins are also forecast to recover

because higher demand will enable higher pricing for services.

The total number of golfing participants is forecast to expand 1.0% over 2012, and discretionary spending activities will help raise revenue an

Demand�drives�profitability

As demand for golf and country club services increases, establishments will be poised to make a positive return after years of net losses. Also, when US wages and incomes rise over several years of improved economic prosperity, golf courses and country clubs will likely increase green and membership fees. This trend will further boost industry profit; however, a greater number of public golf courses in future years will put financial pressures on private courses and clubs. Earnings before interest and taxes are expected to increase to 2.1% of revenue by 2016.

Future industry profitability may be harmed by the presence of many small operators. Small operators are often drawn to the industry by an interest in golf, which overrides concerns of profitability. These establishments

cannot achieve the economies of scale of the larger players, which lowers profit margins. However, earlier consolidation experienced from 2006 to 2011 will ease the effects of the influx of small operators. The oversupply of golf courses has shrunk, and renewed demand will translate into rising course revenue and facility improvements.

Resurgence in the development of new courses or additional decreases in the average number of golfers per course will likely affect the results of operations for industry firms. As noted above, golf course overbuilding in certain markets will benefit some firms, because owners with fewer financial resources and management experience may be forced to liquidate their properties at discounted prices.

Industry�Outlook

After a tough couple of years, the Golf Courses and Country Clubs industry will likely experience improved performance because of a stronger business environment, rising incomes, consumer sentiment and leisure time. These factors will stimulate expansion in the recession’s aftermath as people return to golfing. IBISWorld forecasts that industry revenue will increase at an average annual rate of 1.4% to $23.9 billion over the five years to 2016. During this time, the number of golfing participants is anticipated to grow steadily, supported by the gradual retirement of baby boomers, who will have more time on their hands.

% c

hang

e

4

−4

−2

0

2

1703 05 07 09 11 13 15Year

Industry revenue

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 10

Industry�Performance

Teeing�off�once�againcontinued

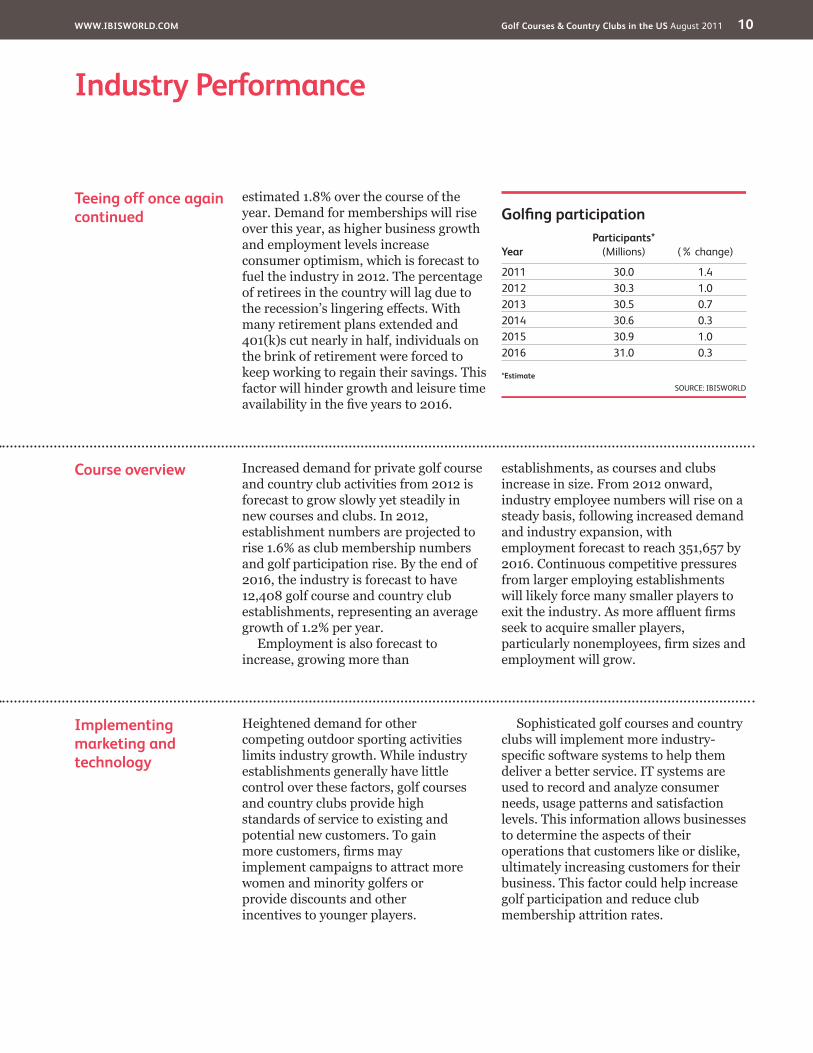

estimated 1.8% over the course of the year. Demand for memberships will rise over this year, as higher business growth and employment levels increase consumer optimism, which is forecast to fuel the industry in 2012. The percentage of retirees in the country will lag due to the recession’s lingering effects. With many retirement plans extended and 401(k)s cut nearly in half, individuals on the brink of retirement were forced to keep working to regain their savings. This factor will hinder growth and leisure time availability in the five years to 2016.

Implementing�marketing�and�technology

Heightened demand for other competing outdoor sporting activities limits industry growth. While industry establishments generally have little control over these factors, golf courses and country clubs provide high standards of service to existing and potential new customers. To gain more customers, firms may implement campaigns to attract more women and minority golfers or provide discounts and other incentives to younger players.

Sophisticated golf courses and country clubs will implement more industry-specific software systems to help them deliver a better service. IT systems are used to record and analyze consumer needs, usage patterns and satisfaction levels. This information allows businesses to determine the aspects of their operations that customers like or dislike, ultimately increasing customers for their business. This factor could help increase golf participation and reduce club membership attrition rates.

Course�overview Increased demand for private golf course and country club activities from 2012 is forecast to grow slowly yet steadily in new courses and clubs. In 2012, establishment numbers are projected to rise 1.6% as club membership numbers and golf participation rise. By the end of 2016, the industry is forecast to have 12,408 golf course and country club establishments, representing an average growth of 1.2% per year.

Employment is also forecast to increase, growing more than

establishments, as courses and clubs increase in size. From 2012 onward, industry employee numbers will rise on a steady basis, following increased demand and industry expansion, with employment forecast to reach 351,657 by 2016. Continuous competitive pressures from larger employing establishments will likely force many smaller players to exit the industry. As more affluent firms seek to acquire smaller players, particularly nonemployees, firm sizes and employment will grow.

Golfi�ng�participation

YearParticipants*�

(Millions) (% change)

2011 30.0 1.42012 30.3 1.02013 30.5 0.72014 30.6 0.32015 30.9 1.02016 31.0 0.3

*EstimateSOURCE: IBISWORLD

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 11

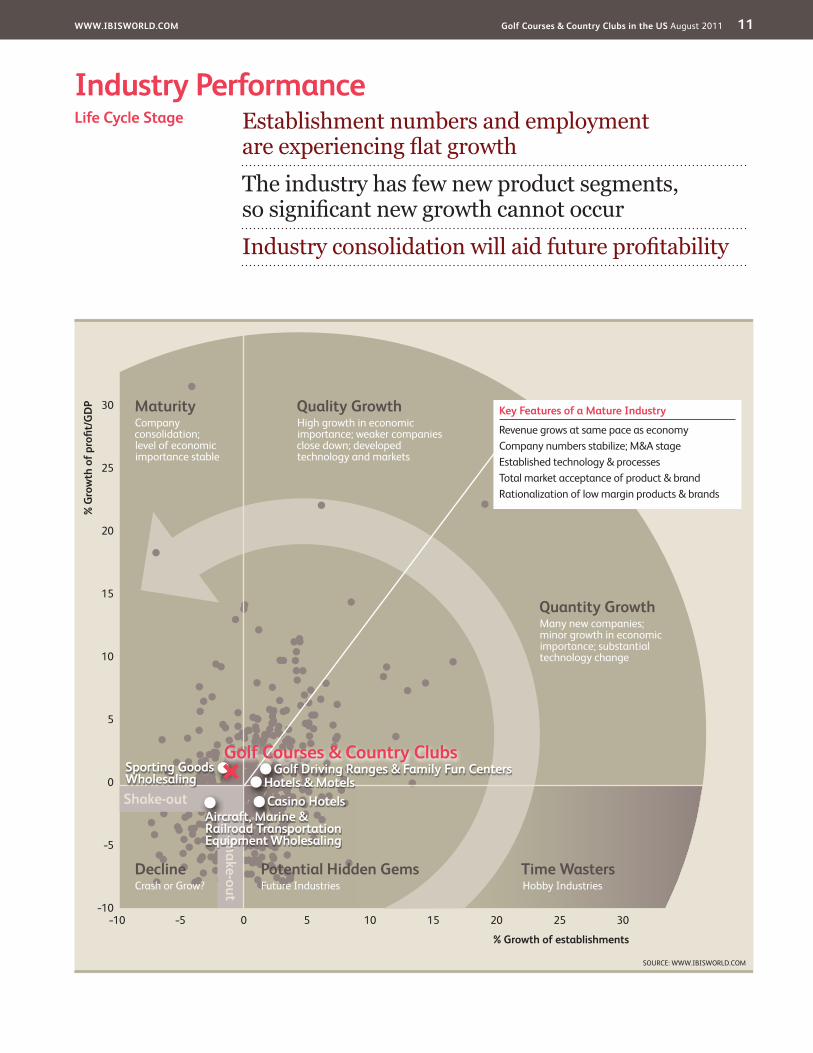

Industry�PerformanceEstablishment numbers and employment are experiencing flat growth

The industry has few new product segments, so significant new growth cannot occur

Industry consolidation will aid future profitability

Life�Cycle�Stage

SOURCE: WWW.IBISWORLD.COM

30

25

20

15

10

5

0

–5

–10–10 100 20–5 155 25 30

%�G

row

th�o

f�pro

fi�t/G

DP

%�Growth�of�establishments

DeclineCrash or Grow?

Potential�Hidden�GemsFuture Industries

Quality�GrowthHigh growth in economic importance; weaker companies close down; developed technology and markets

Time�WastersHobby Industries

MaturityCompany consolidation;level of economic importance stable

Shake-out

Shake-out

Quantity�GrowthMany new companies; minor growth in economic importance; substantial technology change

Key�Features�of�a�Mature�Industry

Revenue grows at same pace as economyCompany numbers stabilize; M&A stageEstablished technology & processesTotal market acceptance of product & brandRationalization of low margin products & brands

Golf�Driving�Ranges�&�Family�Fun�Centers

Aircraft,�Marine�&�Railroad�Transportation�Equipment�Wholesaling

Hotels�&�MotelsSporting�Goods�Wholesaling

Casino�Hotels

Golf�Courses�&�Country�Clubs

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 12

Industry�Performance

Industry�Life�Cycle The Golf Courses and Country Clubs industry in the United States is in a late maturity phase of its life cycle. Growth within the industry has been minimal, but sustained demand for the industry’s services has kept the sector in a mature stage. For instance, industry establishments are anticipated to grow at an annualized rate of 0.4% in the ten years through 2016. Golf courses and country clubs have developed few new services and generally differentiate themselves by the quality and prices that they offer for the use of facilities and for equipment rentals.

Over the ten years to 2016, revenue is expected to increase at an annualized

rate of 1.0% and industry value added will increase at about 1.6% on average per year. These growth rates are slightly below annualized increases in GDP of 2.0% during this time and could indicate a declining industry, however the rates reflect particularly bad years in 2008 and 2009 when spending dropped off due to the Great Recession. Revenue, establishments and employment all fell significantly in those years as consumers and businesses cut back on discretionary spending. This has negatively impacted the industry over the past five years because it primarily offers nonessential golf and entertainment services.

�This industry is Mature

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 13

Products�&�Services

The largest product segment within the industry is golf course membership fees. These account for nearly 40% of industry revenue and generally entitle the member to unlimited golf games throughout the year and, if included, access to the associated country club

facilities and events. There has been a steady increase in new golf course numbers since 1990, which has contributed to segment growth of about 3%. However, numbers have begun to decline beginning in late 2008 due to effects of the recession. The upward

�Products�&�MarketsSupply�Chain�� |�� Products�&�Services�� |�� Demand�DeterminantsMajor�Markets�� |�� International�Trade�� |�� Business�Locations

KEY�BUYING�INDUSTRIES

99� Consumers�in�the�US�Individuals use gold courses and country clubs for leisure and special functions.

KEY�SELLING�INDUSTRIES

42386� Aircraft,�Marine�&�Railroad�Transportation�Equipment�Wholesaling�in�the�US�This industry supplies motorized golf carts for use on golf courses.

42391� Sporting�Goods�Wholesaling�in�the�US�This industry supplies golf equipment and other products for sale and use at golf courses.

42434� Footwear�Wholesaling�in�the�US�This industry supplies golf shoes for sale at golf courses.

42441� Grocery�Wholesaling�in�the�US�This industry supplies food and beverage products for sale at golf courses.

42481� Beer�Wholesaling�in�the�US�This industry supplies alcoholic beverages for sale at golf courses.

42482� Wine�&�Spirits�Wholesaling�in�the�US�This industry supplies alcoholic beverages for sale at golf courses.

42491� Farm�Supplies�Wholesaling�in�the�US�This industry supplies fertilizer, plant seed, pesticide and other related products for use in golf course development and maintenance.

Supply�Chain

Products and services segmentation (2011)

Total $22.3bn

39%Membership fees

25%Golf course green fees

21%Food and

beverage sales

8%Other sales and

service fees

7%Equipment rentals

and sales

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 14

Products�&�Markets

DemandDeterminants

Demand for services offered by the Golf Courses and Country Clubs Industry is influenced by many factors. A key factor is the golf participation rate in the United States. As more people take up golf, demand for golf course services increase. In 1950 there were about 3.5 million adult golfers in the US (players over 12 years of age and play at least once per year). By 2011, this number will have increased to about 30.0 million, which represents no change from 2006, with a dip in the meantime. There are also a number of junior golfers that play, which affects the overall demand for the industry.

Demand is also influenced by the number of golf courses and country clubs available for participants. As a greater number of facilities are established,

people are encouraged to join and participate in the industry’s activities. As of 2011, there are about 11,686 golfing establishments. The condition of golf courses also affects how regularly people play. A higher number of golf courses, and the resulting increase in competition among courses, has led to an overall improvement in golf course conditions. Improvements in golf course maintenance technology have also improved course design and conditions. These factors have contributed to demand for the industry’s products over the past few decades.

The status associated with being a member of a country club will influence demand for membership, and although membership of a country club can have negative and positive connotations,

Products�&�Servicescontinued

trend is likely to resume in the long-term future as more new private courses and clubs are forecast to be developed when the economy stabilizes.

Golf course green fees comprise the second largest product segment for the industry with about 25% of industry revenue. These are fees that are paid by golfers, who are not members of a country club, for an individual round of golf. Increased golf participation levels for casual and weekend golfers have increased this segment from about 21% in 2000. This trend is likely to continue as the number of daily fee golf courses within the United States continues to rise at a fast rate. In 1990, there were about 6,000 daily fee golf courses, whereas in 2010, there will be over 9,000. Despite this, the increasing segmentation trend may be softened, as an increasing number of golf courses that are owned and operated by municipalities are being sold to private golf course management companies. Whereas municipality-owned golf courses would often charge

customers a daily green fee to play, private (club) courses charge yearly membership fees.

Food and beverage sales are the third largest product segment, accounting for 21.0% of industry revenue. As private golf course and country clubs generally tend to include lunch and other food services to members, the majority of this revenue was contributed from public courses. Of segment revenue, close to 74.0% is generated from the sale of food and non-alcoholic beverages, while the remaining 26.0% is from the sale of alcoholic beverages alone.

Golf club and other equipment rental, such as golf carts, make up 7.0% of industry sales. Also included in this segment is the sale of golf equipment and accessories, contributing about 3.0% of industry revenue. Other sales and service fees amount to 8.0% of industry revenue. Merchandise sales account for the bulk of these sales, while other revenue comes from miscellaneous items, such as room hire fees, golf lessons, and other sales.

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 15

Products�&�Markets

Major�Markets The average age for golfing participants is about 37 years. Participation among males and females also differs – about 75.0% of participants are male and 25.0% are female. It can also be noted that the participation rates are directly related to income levels. For example, participation rates for incomes between $25,000 and $60,000 are about 8.0% to 20.0%; however, when income levels rise to $150,000, the participation rate increases to about 30.0%. The industry

DemandDeterminantscontinued

demand for these services has increased strongly over the past decade. The price to participate in a round of golf will affect demand. Increases in golfing fees can cause people to seek alternative recreational activities. According to the National Golf Foundation (NGF), in 2007 the median peak season weekend rack rate green fee with cart at 18-hole public (daily fee and municipal) non-resort regulation golf courses in the US was $40.00. States with the highest rates were Hawaii (median $95.00) and Nevada ($89.00). States with the lowest rates were Oklahoma ($30.50) and Alabama ($31.00). Furthermore, NGF states that in 2007, the median peak season weekend rack rate green fee with cart at “non-traditional” public non-resort facilities in the US was $22.00. Non-traditional means either stand-alone 9-hole regulation or short courses (executive and par-3).

Other determinants of demand include the popularity of other sports; the average level of leisure time available to people who play golf; weather patterns; the desire to increase sport participation and fitness levels; and the success of US golfers on the professional golf circuit.

Generally, usage of country club and golf facilities declines during the first and fourth quarters of the year, when colder

temperatures and shorter days reduce the demand for golf and golf-related activities. Typically, clubs generate a greater share of their yearly revenues in the fourth quarter, which includes the holiday and year-end party season. As a result, firms usually generate a disproportionate share of revenues and cash flows in the second, third and fourth quarters of each year and have lower revenues and profits in the first quarter. Firms can also be affected by non-seasonal and severe weather patterns. Periods of extremely hot, cold or rainy weather in a given region can be expected to reduce golf-related revenue for the regions that experience undue weather patterns. Similarly, extended periods of low rainfall can affect the cost and availability of water needed to irrigate golf courses and can adversely affect results for facilities in those specific regions.

Keeping turf grass conditions at a satisfactory level to attract play on golf courses requires significant amounts of water. An establishment’s ability to irrigate a course could be adversely impacted by a drought or other water shortage. A severe drought could adversely affect business and demand for golf courses and country clubs. Conversely, floods caused by extreme rains may interrupt golf play.

Golf�participants�by�working�categoryCategory� Golfi�ng�participants�(%)Professional and management 38Clerical and sales 16Blue collar 25Other 6Retired 15Total 100

SOURCE: NATIONAL GOLF FOUNDATION

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 16

Products�&�Markets

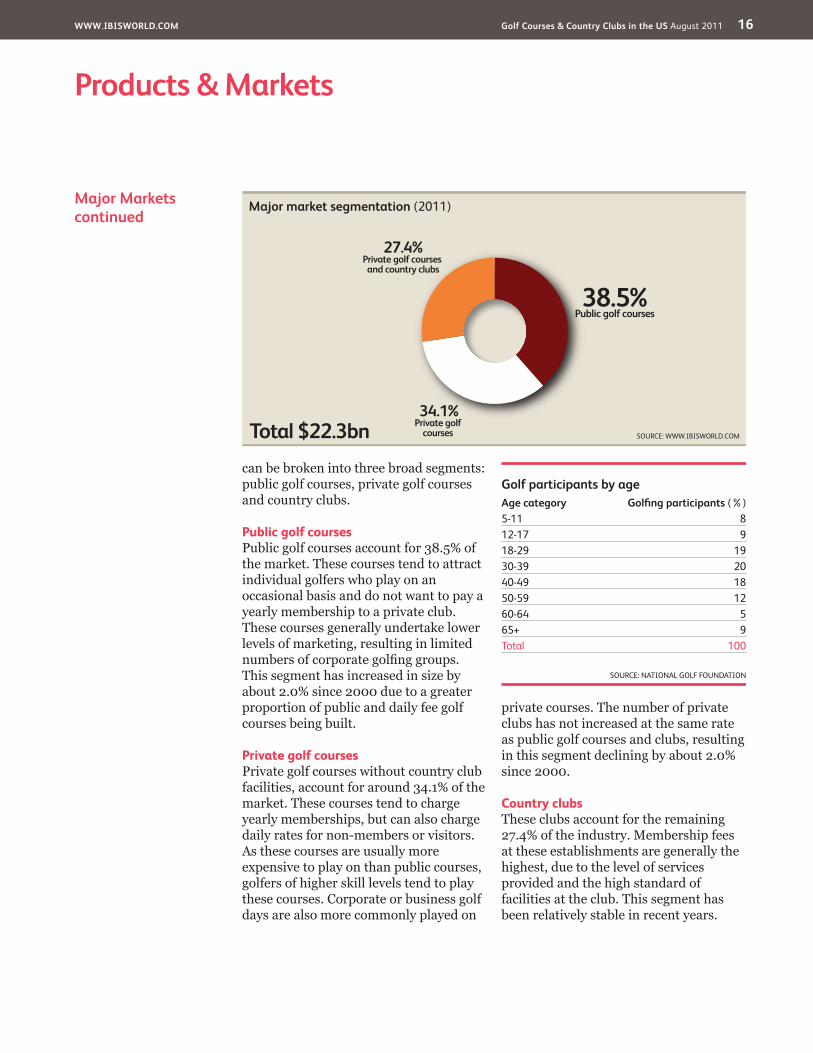

Major�Marketscontinued

can be broken into three broad segments: public golf courses, private golf courses and country clubs.

Public golf coursesPublic golf courses account for 38.5% of the market. These courses tend to attract individual golfers who play on an occasional basis and do not want to pay a yearly membership to a private club. These courses generally undertake lower levels of marketing, resulting in limited numbers of corporate golfing groups. This segment has increased in size by about 2.0% since 2000 due to a greater proportion of public and daily fee golf courses being built.

Private golf coursesPrivate golf courses without country club facilities, account for around 34.1% of the market. These courses tend to charge yearly memberships, but can also charge daily rates for non-members or visitors. As these courses are usually more expensive to play on than public courses, golfers of higher skill levels tend to play these courses. Corporate or business golf days are also more commonly played on

private courses. The number of private clubs has not increased at the same rate as public golf courses and clubs, resulting in this segment declining by about 2.0% since 2000.

Country clubs These clubs account for the remaining 27.4% of the industry. Membership fees at these establishments are generally the highest, due to the level of services provided and the high standard of facilities at the club. This segment has been relatively stable in recent years.

Major market segmentation (2011)

Total $22.3bn

38.5%Public golf courses

34.1%Private golf

courses

27.4%Private golf courses and country clubs

SOURCE: WWW.IBISWORLD.COM

Golf�participants�by�ageAge�category� Golfi�ng�participants�(%)5-11 812-17 918-29 1930-39 2040-49 1850-59 1260-64 565+ 9Total 100

SOURCE: NATIONAL GOLF FOUNDATION

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 17

Products�&�Markets

International�Trade The Golf Courses and Country Clubs Industry is not subject to international trade. Although golf equipment and accessories are imported to and exported

from the United States, these transactions are included at the manufacturing level for sport and recreational goods.

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 18

�Products�&�Markets

Business�Locations�2011

MO2.1

West

West

West

Rocky Mountains Plains

Southwest

Southeast

New England

Great Lakes

VT0.4

MA2.6

RI0.5

NJ2.0

DE0.3

NH0.7

CT1.3

MD1.2

DC0.0

1

5

3

7

2

6

4

8 9

Additional�States�(as marked on map)

AZ2.0

CA6.1

NV0.6

OR1.3

WA1.8

MT0.7

NE1.2

MN3.0

IA2.7

OH5.2 VA

2.2

FL5.4

KS1.5

CO1.1

UT0.4

ID0.7

TX4.9

OK0.9

NC4.0

AK0.1

WY0.3

TN1.8

KY1.8

GA2.5

IL4.0

ME0.9

ND0.6

WI3.4 MI

5.3 PA4.8

WV0.7

SD0.6

NM0.4

AR1.1

MS1.1

AL1.4

SC2.3

LA1.0

HI0.4

IN2.7

NY6.0 5

67

8

321

4

9

SOURCE: WWW.IBISWORLD.COM

Mid- Atlantic

establishments�(%)�

� Less�than�3%� 3%�to�less�than�10%� 10%�to�less�than�20%� 20%�or�more

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 19

�Products�&�Markets

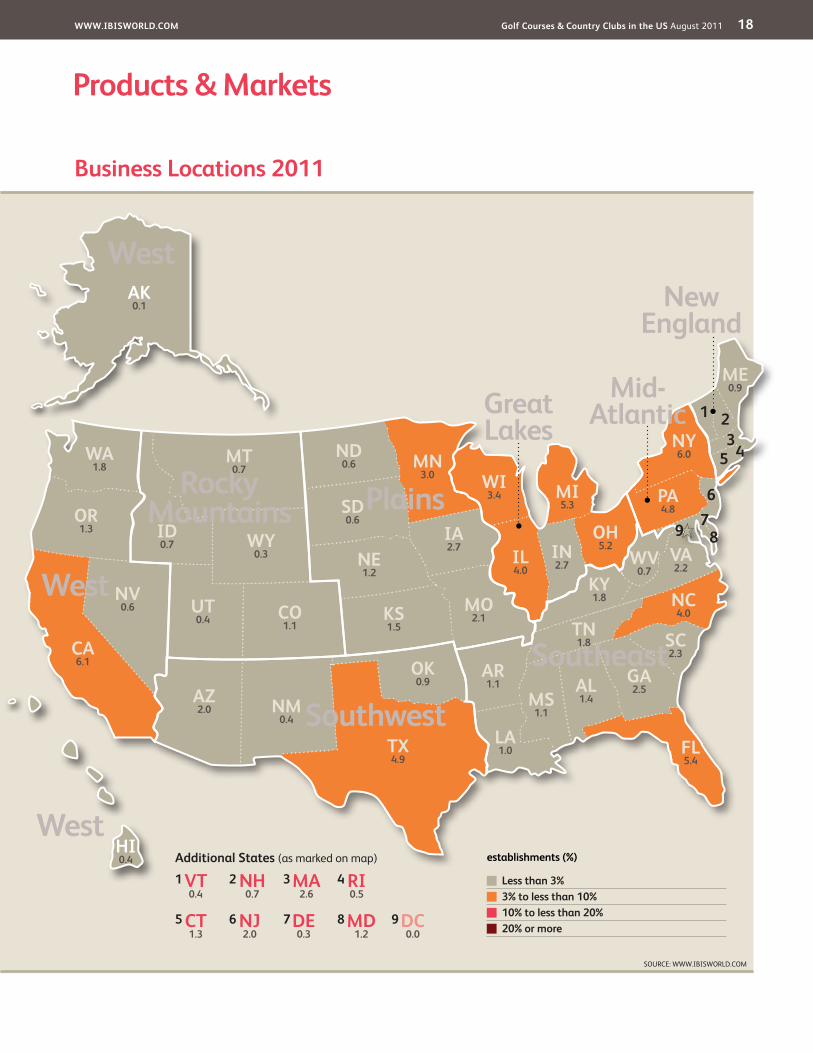

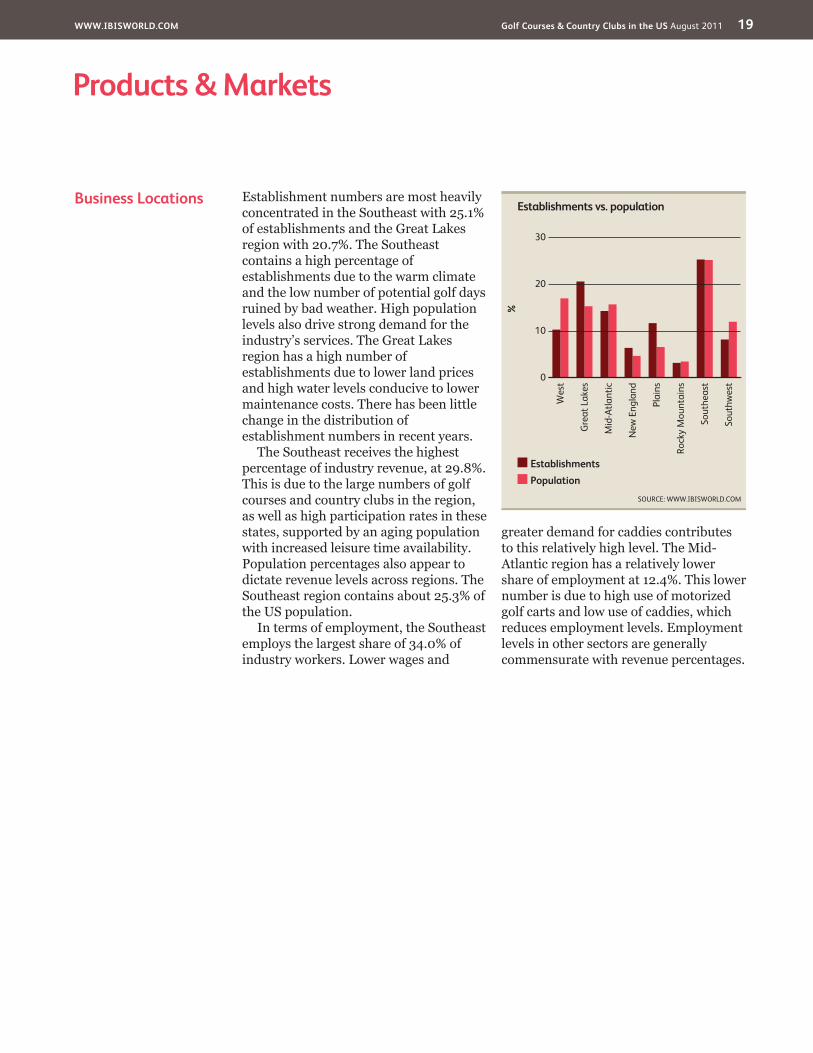

Business�Locations Establishment numbers are most heavily concentrated in the Southeast with 25.1% of establishments and the Great Lakes region with 20.7%. The Southeast contains a high percentage of establishments due to the warm climate and the low number of potential golf days ruined by bad weather. High population levels also drive strong demand for the industry’s services. The Great Lakes region has a high number of establishments due to lower land prices and high water levels conducive to lower maintenance costs. There has been little change in the distribution of establishment numbers in recent years.

The Southeast receives the highest percentage of industry revenue, at 29.8%. This is due to the large numbers of golf courses and country clubs in the region, as well as high participation rates in these states, supported by an aging population with increased leisure time availability. Population percentages also appear to dictate revenue levels across regions. The Southeast region contains about 25.3% of the US population.

In terms of employment, the Southeast employs the largest share of 34.0% of industry workers. Lower wages and

greater demand for caddies contributes to this relatively high level. The Mid-Atlantic region has a relatively lower share of employment at 12.4%. This lower number is due to high use of motorized golf carts and low use of caddies, which reduces employment levels. Employment levels in other sectors are generally commensurate with revenue percentages.

%

30

0

10

20

Sout

hwes

t

Wes

t

Gre

at L

akes

Mid

-Atla

ntic

New

Eng

land

Plai

ns

Rock

y M

ount

ains

Sout

heas

t

EstablishmentsPopulation

Establishments vs. population

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 20

Key�Success�Factors Easy access to further appropriate land for developmentA golf course or country club that intends to expand its operations will require additional land for development.

Economies of scaleCompanies that operate many golf courses and country clubs can reduce average administrative and maintenance costs, which can help to lower fees and increase profits.

Membership of an industry organizationEstablishing strong relationships with numerous professional organizations helps to attract members.

Access to highly skilled workforceFirms in this industry need a highly competent workforce, including green keepers, restaurant staff and golf professionals and instructors.

Ability to pass on cost increasesGolf and country club operators who are able to pass on cost increases are in a better position to boost profits.

Optimum capacity utilizationGolf course and country club operations need to maximize patronage in order to optimize facility usage.

Level of competition existing in the marketOperations that are geographically isolated from competitors but close to consumers and businesses can enjoy reduced competition.

Ability to attract local support/patronageThe success of a golf course or country club is dependent on its ability to attract new members, retain existing members and maintain or increase levels of club usage by members and guests.

Market�Share�Concentration

The Golf Courses and Country Clubs Industry is highly fragmented. The industry is made up of a couple of large firms that operate hundreds of courses, several medium-sized companies that own and operate between five and 20 courses, dozens of companies that operate two to four courses, and thousands of firms that operate a single course.

The four largest golf course and country club operators account for less than 6.5% of industry revenue. This has declined since 2002, when Census data indicated that the top four firms occupied an 8% market share. According to the data, the 8 largest golf course and country club operators earned around 10% of total industry revenue in 2002.

In order for golf course and country club operators to differentiate themselves from their competitors within the industry, these businesses need to focus

on providing customer service, producing high quality courses and facilities, maintaining competitive prices, and controlling operating expenses.

The level of industry concentration within the industry is not expected to change significantly in the future. This is due to the highly fragmented nature of the industry, geographic difficulties in achieving economies of scale via mergers and acquisitions, and high costs to acquire existing golf courses and country clubs. However, there are opportunities for consolidation, as small establishments particularly will be under financial pressure through the recession. The larger operating firms are purchasing golf courses in order to increase their portfolio and stature. In the acquisition of golf courses, companies compete primarily on the basis of price and their reputation for operating golf courses.

Competitive�LandscapeMarket�Share�Concentration�� |�� Key�Success�Factors�� |�� Cost�Structure�BenchmarksBasis�of�Competition�� |�� Barriers�to�Entry�� |�� Industry�Globalization

Level��Concentration in this industry is Low

�IBISWorld identifies 250 Key Success Factors for a business. The most important for this industry are:

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 21

Competitive�Landscape

Cost�Structure�Benchmarks

The cost structure of individual firms within the industry varies depending on the type of golf course and country club facilities being offered, and the structure and size of the company. Overall, this industry has a poor level of profitability. Because costs are relatively unchanged from year to year, profit is largely based on achieving membership and attendance benchmarks. In 2006 and 2007, the industry averaged a pretax and interest profit margin of about 2.3%. Since the recession hit, household wealth and spending has taken a plunge, sending industry profitability down to a low of 1.7%. In 2011, IBISWorld expects earnings to improve to about 2.0% of total revenue, amounting to $442.0 million.

The major component of a company’s expenses is made up of purchases, which includes fertilizers, plants, food, beverages, golf equipment for rent and resale, and other miscellaneous materials. This accounts for 40% of industry revenues. This proportion is variable based on the size and structure of an individual

establishment, but remains relatively consistent from year to year.

Labor costs make up a large proportion of a firm’s expenses at about 39.6%. This shows that the industry is highly labor intensive. This is indicative of the high levels of golf course maintenance and development required, as well as of the low concentration of firms participating within the industry.

Capital costs are relatively high in this industry, as depreciation amounts to about 6.8% of 2011 revenue. Irrigation maintenance makes up the bulk of this segment. These expenses also include vehicles, golf carts, lawnmowers and other maintenance machinery, as well as kitchen and computer equipment.

There are various other expenses within this industry. In addition to maintaining golf courses and country clubs, firms also tend to spend discretionary capital to expand existing properties and to enter into new business opportunities. Capital expansion funding can be large; however, it does fluctuate from year to year. Other costs include advertising,

Key�Success�Factorscontinued

Economies of scopeGolf course and country clubs that offer a wide variety of services can benefit from additional patronage.

Having a high profile in the marketHosting professional golf tournaments enhances name recognition and provides additional revenue.

Industry�Costs�and�Average�Sector�Costs■�Profi�t■�Rent■�Utilities■�Depreciation■�Other■�Wages■�Purchases

Industry�Costs�(2011)�

Average�Costs�of�all�Industries�in�sector�(2011)�

2.0Profit

40.039.67.66.84.0

7.0Profit

23.233.621.95.73.6

5.2

SOURCE: WWW.IBISWORLD.COM

0 100%

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 22

Competitive�Landscape

Basis�of�Competition The success of businesses in this industry is dependent on their ability to attract new members, retain existing members and maintain or increase levels of club usage by members and guests. While most golf clubs and country clubs devote significant resources to promote their facilities and services, many of the factors affecting club membership and usage are beyond the establishment’s control. Local and federal government laws, including income tax regulations applicable to club members and guests, can adversely influence membership activity. Furthermore, changes in consumer tastes and preferences, local, regional and national economic conditions, including levels of disposable income, weather and demographic trends can also affect demand on club membership and usage.

Firms operating in the Golf Club and Country Clubs industry experience strong competition from rivals. Establishments compete primarily on the basis of management expertise, reputation, featured facilities, quality and breadth of services and price.

For private consumers and business usage, geographic location will be a major influence when choosing a golf course to play on. This factor can be particularly influential when a customer is deciding to join a club, as membership can involve a substantial monetary outlay. The level of competition varies from region to region and is subject to change as existing facilities are renovated or new facilities are developed. An increase in the number or quality of clubs and other facilities in a particular region could significantly increase competition for operators in that region.

For business and corporate usage, facilities such as conference rooms, business facilities, reciprocal rights, restaurants, bars, cafes, other sports facilities, and other features can influence the choice of venue. The status and cost associated with being a member of a country club can also influence the decision of which one to join.

Competition can also be based on the skill level of particular players. A golf player of a low standard is less likely to regularly play on a very expensive golf course. Similarly, a golf course that is particularly challenging to play, due to difficult playing hazards, is less likely to attract low-skilled players. This links in with the quality of the course, where there tends to be higher demand for good quality courses that are reasonably priced for a round of golf. People are reluctant to play on a high priced golf course that is not maintained to a high standard. Although this may be the case, players of a high standard are more likely to pay to play on a high quality golf course. Courses that offer mid-week pricing discounts can attract additional patronage during quiet periods. Average prices for a round of golf at the lower end of the market are between $20 and $25. For top of the range course, fees are upwards of $80.

Finally, there are opportunities for consolidation in the highly fragmented golf course ownership industry and there has been a modest level of consolidation in recent years. In the acquisition of golf courses, companies compete primarily on the basis of price and their reputation for operating golf courses. The marketing and

Cost�Structure�Benchmarkscontinued

administration and insurance. Overall, these expenses total about 7.6% of industry revenue. As firms

attempt to gain an advantage in the market, advertising and promotion costs tend to increase.

Level�&�Trend��Competition in this industry is High and the trend is Increasing

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 23

Competitive�Landscape

Industry�Globalization

Golf courses and country clubs are not engaged in international trade, however the industry is subject to increasing globalization. Major US golf course management companies have increased their ownership of foreign courses and clubs in recent years. These include ClubCorp Inc., American Golf Corporation and Troon Golf LLC. These companies operate in Australia, New Zealand, Fiji, China, Japan, the United Kingdom, Italy, Kuwait, the United Arab Emirates, Mexico, the Caribbean and countries of South America. Furthermore, ownership and management of US golf courses and country clubs is not restricted to domestic firms. Globalization is likely to continue as firms seek to increase their market share

and achieve economies of scale by minimizing average administration and maintenance costs per golf course.

The design of golf courses by well-known past and present golfing professionals also contributes to the level of globalization within the industry. It is common for international golfers, such as Greg Norman (Australia) and Bernhard Langer (Germany), to design and influence US golf courses, facilities and land estates. Many US players also work on golf course designs in foreign countries. As promotion of golf courses becomes more common, the trend of using golf professionals in course design is likely to increase as this can add to the prestige and reputation of a golf course.

Barriers�to�Entry The Golf Courses and Country Clubs industry’s barriers to entry are high. There are various costs for new entrants associated with the purchase of land and the development of a golf course and country club. It is very costly to build, develop and maintain a golf course and associated country club facilities, and the industry observes high machinery and equipment costs. With the industry exhibiting very low profit margins, it is hard for players to ultimately survive.

New firms also have difficulty establishing their golf course and country club services in the market place because of the high number of competitors promoting their existing facilities. The industry is somewhat saturated at the moment, so it is difficult for a new player to gain a market share. Additionally, the industry already has high promotion and

advertising costs, which makes it difficult to break through the clutter. Customer loyalty to existing golf courses and country clubs also tends to be strong, making it difficult to attract new clients. Finally, the industry must abide by planning restrictions, government requirements, and time delays, which can be costly when establishing a new golf course or country club.

Basis�of�Competitioncontinued

management of golf courses and country clubs can have a great influence the choice of sporting and recreational

activities people choose, and by being a larger player it is easier to break through this clutter and gain a competitive edge.

Barriers�to�Entry�checklist� LevelCompetition HighConcentration LowLife Cycle Stage MatureCapital Intensity MediumTechnology Change LowRegulation & Policy MediumIndustry Assistance None

SOURCE: WWW.IBISWORLD.COM

Level�&�Trend��Barriers to Entry in this industry are High and Increasing

Level�&�Trend��Globalization in this industry is Low and the trend is Increasing

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 24

Other�Companies ClubCorp Inc.Estimated market share: 2.5%Headquartered in Dallas, TX, ClubCorp Inc. is one of the largest operators of golf courses, country clubs, health clubs and resorts in the world. Established by Robert Dedman in 1957, the company now owns or manages about 150 golf clubs, country clubs and other facilities across the country and the rest of the world. Following expansion into Australia, China and Mexico, ClubCorp bought several European courses in 1998. The company’s Pinehurst Resort and Country Club in North Carolina held the 2005 US Golf Open, which contributed more than $50 million to operating revenue and $9.3 million to operating profit for that year.

ClubCorp’s resorts and golf courses include such well-known venues as Pinehurst Resort and Country Club in Pinehurst, North Carolina; The Homestead Resort in Hot Springs, Virginia; Barton Creek Resort and Country Club in Austin, TX; Firestone Country Club in Akron, OH; Mission Hills Country Club near Palm Springs, CA; and The City Club on Bunker Hill in Los Angeles. ClubCorp also operates a number of business and sports clubs. Robert Dedman started the company in 1957, and it is owned by private equity firm KSL Capital Partners.

ClubCorp has about 200,000 memberships and receives more than one million guests at its properties annually. The company has partnerships with Acura, E-Z-Go/Textron, Titleist and ESPN. E-Z-Go/Textron supplies golf carts to ClubCorp in exchange for testing of E-Z-Go/Textron product development ideas for new and existing equipment.

The company’s operations are organized into three principal business segments: Country Club and Golf Facilities, Resorts, and Business and Sports Clubs. Other operations that are not assigned to a principal business

segment include the company’s real estate operations and corporate services. This information has been gathered through the latest available company SEC filing, issued in March of 2006. Due to the fact that ClubCorp was acquired by KSL Capital, there have been no subsequent SEC filings. KSL Capital is also a private company, and therefore financial information on its operations is unavailable.

In 2008, ClubCorp purchased Seville Golf & Country Club in Gilbert, AZ, and opened a new water park at its Clubs of Kingwood in Texas. In May 2009, the company announced that it would sell Atascocita Country Club in Humble, TX, to Pinehurst Trail Holdings.

Country club and golf facilitiesClubCorp’s portfolio of 99 country club and golf facilities is comprised of 89 private and semiprivate country and golf clubs with nearly 82,000 memberships (as of December 2005), and 10 public golf facilities. The company’s country club and golf facilities are located in 19 states and two foreign countries, providing them with a geographically diverse revenue base. ClubCorp has focused their operations in this segment on private and semiprivate clubs because of their expertise in managing membership-based facilities, the relative competitive position of such clubs as compared to public courses and the stability of recurring membership dues as a primary revenue source.

Operating revenues for the country club and golf facilities segment consist primarily of membership revenues (comprised primarily of membership dues, and to a lesser extent, recognition of deferred membership fees and deposits), golf revenues and food and beverage sales. In 2005, the country club and golf facilities segment generated operating revenue of $525.4 million, or 51.1% of total revenue.

�Major�CompaniesThere�are�no�Major�Players�in�this�industry�� |�� Other�Companies

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 25

Major�Companies

Other�Companiescontinued

American Golf CorporationEstimated market share: 1.2%Headquartered in Santa Monica, CA, American Golf Corporation operates more than 110 golf courses across the United States. The company, which leases about half of these properties from National Golf Properties, employs about 10,000 people directly and indirectly. American Golf Corporation reported strong revenue growth in the 1998 to 2001 period. This was mainly through acquisition and sales growth; however, the company was unable to achieve strong profit figures. Financial problems during 2001, which saw the company report a loss of about $60 million, resulted in the company being bought by a private consortium in 2003, and is now owned by investment firms Goldman Sachs and Starwood Capital. Since 2003, several golf courses have been sold off in an attempt to reduce debts and increase cash flows. American Golf Corporation also runs the American Golf Foundation, which helps promote the game through charity and education.

In 2007, the company agreed to sell more than 20 golf properties to CNL Income Properties for about $245 million. The company is also selling another dozen properties to the private equity group. Dallas-based Evergreen Alliance Golf Limited plans to acquire 15 other courses from American Golf Corporation. IBISWorld estimates American Golf Corporation receives yearly revenue within the Golf Courses and Country Clubs industry of about $250.0 million.

Century Golf PartnersEstimated market share: 1.0%Century Golf Partners is a Dallas-based golf investment company that was formed in early 2005 for the purpose of acquiring and managing country clubs, daily fee golf courses and golf resorts

throughout the country. Century Golf Partners and its financial partners, Walton Street Capital and Lehman Brothers have been among the most active buyers of golf properties in the industry in recent years. The company has pursued revenue growth and increased market share aggressively, however this expansion was likely slowed by the dramatic collapse of partner Lehman Brothers. In 2008, the Century Golf’s portfolio included 55 courses, 40 of which were company owned and another 15 golf courses managed on behalf of third parties. The company achieved revenue of $150 million in 2006, and aimed to generate $200 million in 2008.

Century Golf Partners owns the exclusive worldwide rights to the Arnold Palmer Golf Management brand and operates its courses under the Arnold Palmer name. The following outlines the Arnold Palmer Golf Management group, which itself, has a market share of about 0.5%. Arnold Palmer Golf Management owns or manages around 43 courses in more than a dozen states and offers services in acquisitions, franchising, joint ventures, leasing, and new course development. Golfing legend Arnold Palmer formed the company to manage golf courses in 1984. In 2005, Jim Hinckley acquired the Arnold Palmer Golf Management brand through Century Golf Partners, an operating partner of Chicago-based real estate investment firm Walton Street Capital. Arnold Palmer Golf Management has a team of around 3,700 associates, with revenue of about $70 million.

Troon Golf LLCEstimated market share: Less than 1.0%Headquartered in Scottsdale, AZ, Troon Golf LLC is one of the largest golf course owners and management companies in the United States. The company owns or manages about 200

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 26

Major�Companies

Other�Companiescontinued

golf courses in 31 states and 31 countries, making it among the world’s largest upscale operators. Troon Golf has a significant presence in Arizona and California. Many of Troon Golf courses are located in Europe, the Middle East, the Asia-Pacific, South America and the Caribbean. The company offers loyalty reward points

for golfers that spend a certain value at applicable courses.

Electing to focus solely on high-end luxury golf properties and developments, Troon Golf successfully captures a dominant niche in the golf and hospitality industries. A privately owned company, Troon Golf reports revenue of about $50.0 million.

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 27

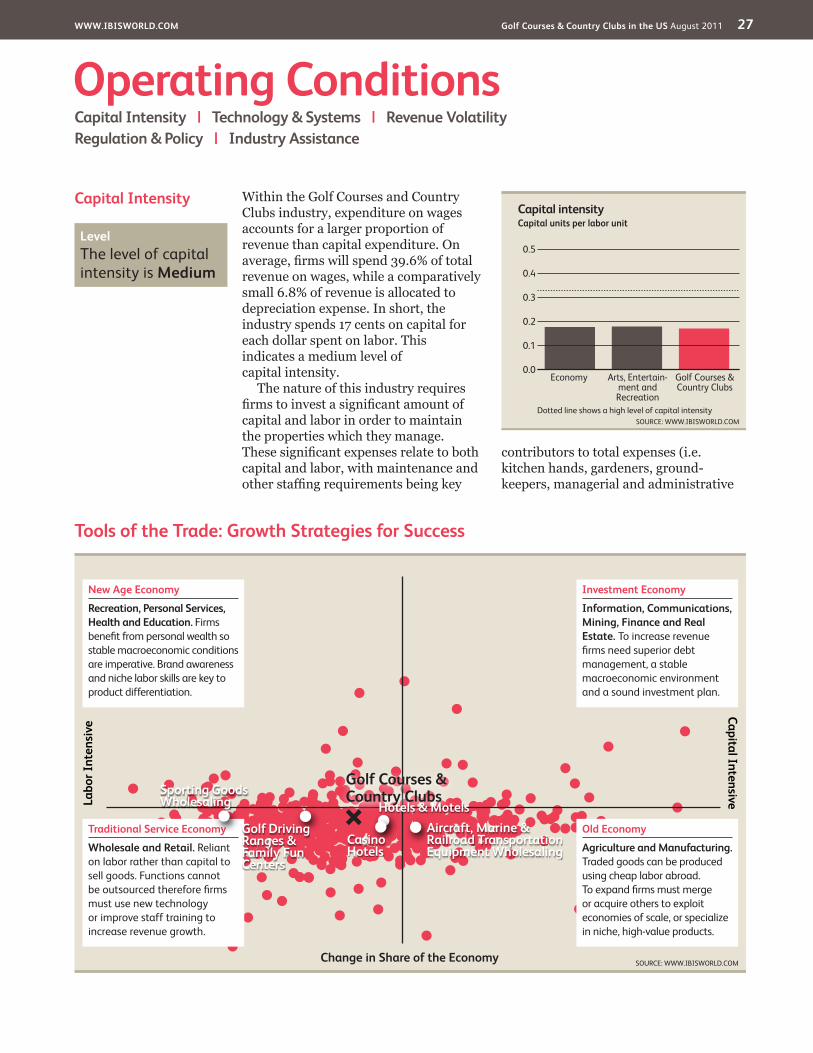

Capital�Intensity Within the Golf Courses and Country Clubs industry, expenditure on wages accounts for a larger proportion of revenue than capital expenditure. On average, firms will spend 39.6% of total revenue on wages, while a comparatively small 6.8% of revenue is allocated to depreciation expense. In short, the industry spends 17 cents on capital for each dollar spent on labor. This indicates a medium level of capital intensity.

The nature of this industry requires firms to invest a significant amount of capital and labor in order to maintain the properties which they manage. These significant expenses relate to both capital and labor, with maintenance and other staffing requirements being key

contributors to total expenses (i.e. kitchen hands, gardeners, ground-keepers, managerial and administrative

�Operating�ConditionsCapital�Intensity�� |�� Technology�&�Systems�� |�� Revenue�VolatilityRegulation�&�Policy�� |�� Industry�Assistance

Tools�of�the�Trade:�Growth�Strategies�for�Success

SOURCE: WWW.IBISWORLD.COM

Labo

r�Int

ensi

veCapital�Intensive

Change�in�Share�of�the�Economy

New�Age�Economy

Recreation,�Personal�Services,�Health�and�Education. Firms benefi t from personal wealth so stable macroeconomic conditions are imperative. Brand awareness and niche labor skills are key to product differentiation.

Traditional�Service�Economy

Wholesale�and�Retail. Reliant on labor rather than capital to sell goods. Functions cannot be outsourced therefore fi rms must use new technology or improve staff training to increase revenue growth.

Old�Economy

Agriculture�and�Manufacturing.�Traded goods can be produced using cheap labor abroad. To expand fi rms must merge or acquire others to exploit economies of scale, or specialize in niche, high-value products.

Investment�Economy

Information,�Communications,�Mining,�Finance�and�Real�Estate.�To increase revenue fi rms need superior debt management, a stable macroeconomic environment and a sound investment plan.

Golf�Driving�Ranges�&�Family�Fun�Centers

Aircraft,�Marine�&�Railroad�Transportation�Equipment�Wholesaling

Hotels�&�MotelsSporting�Goods�Wholesaling

Casino�Hotels

Golf�Courses�&�Country�Clubs

Capital intensity

0.5

0.0

0.1

0.2

0.3

0.4

SOURCE: WWW.IBISWORLD.COMDotted line shows a high level of capital intensity

Capital units per labor unit

Golf Courses & Country Clubs

Arts, Entertain-ment and Recreation

Economy

Level��The level of capital intensity is Medium

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 28

Operating�Conditions

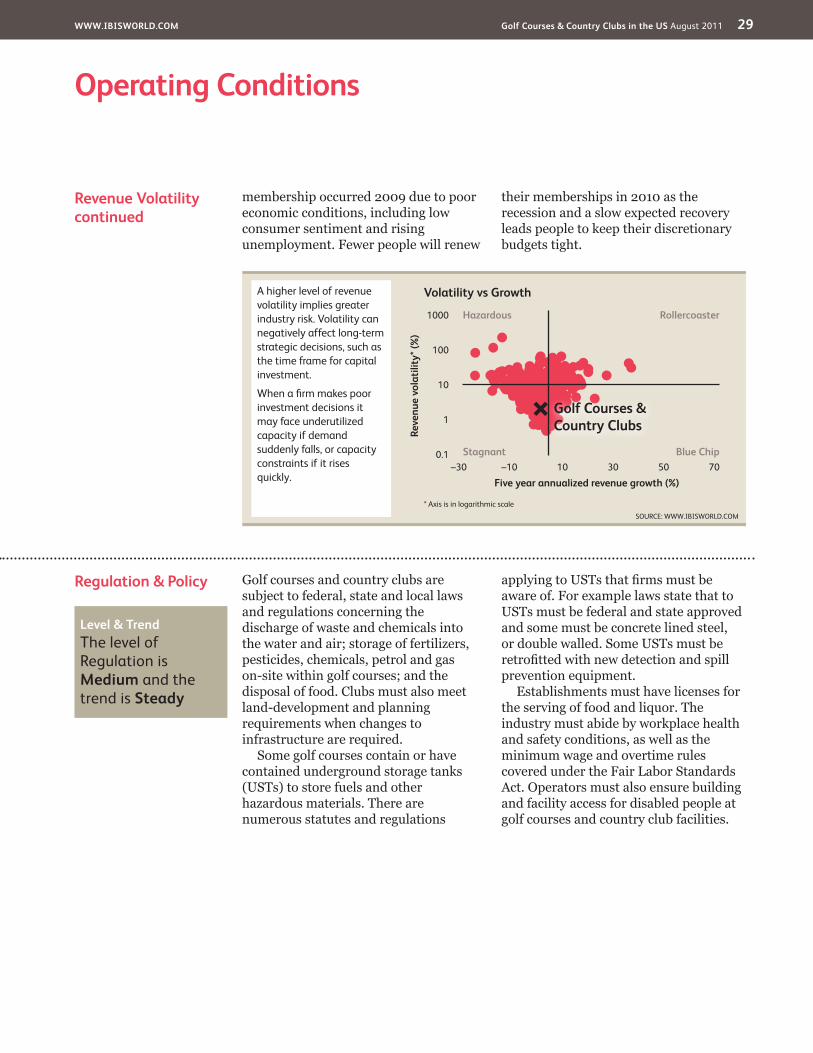

Revenue�Volatility The industry benefits from a low level of revenue volatility. The largest proportion of industry revenue is sourced from membership fees, which provide a steady stream of income. Many golf courses have substantial waiting periods to become a member, and will charge a joining fee in addition to the annual membership fees, which discourages people from letting their memberships lapse. For the more prestigious clubs, there is an excess of demand over supply (despite high levels of competition in the industry) supporting stable revenue growth.

Growing golf participation rates create additional demand for golf and country club facilities. Golfers make a substantial outlay initially to purchase their golf equipment and to pay up their membership. This provides the incentive to play regularly.

Adverse weather conditions can limit opportunities for playing golf and cause a reduction in demand. A poor economic environment can reduce leisure time for consumers and limit golf and country club demand. A decline in golf participation and country club

Technology&�Systems

Technological change and development within the industry is at a low level, as the industry is in the mature stage of its life cycle. Many golf courses and country clubs have existing vehicles and equipment, and tend to repair items rather than replace them. Also, the tradition of labor intensity within the industry works against the introduction of new technology.

The industry observes low revenue growth, which is not conducive to capital

investment. Capital investment in infrastructure, such as buildings and irrigation, may not occur regularly, particularly for older public courses in lower socioeconomic regions. This lowers the overall level of technological change.

The implementation of computerized booking and ordering systems can create benefits for golf courses and country clubs, and many of the larger establishments would have introduced these systems already.

Capital�Intensitycontinued

staff). Capital intensity has declined in recent years as firms reduced expenditure on maintenance vehicles and extended the life of golf carts in an attempt to cut costs.

Golf courses and country clubs have substantial capital investment costs for buildings, facilities and infrastructure. The overall level of capital investment within the industry should increase in the future as firms consolidate facilities and become more innovative in course management and marketing processes. Also, firms will attempt to gain a competitive advantage over other companies by offering new and updated equipment and services. In addition to

maintaining properties, firms also spend discretionary capital to expand existing properties and to enter into new business opportunities.

Specialized golf course and country club establishments have been able to develop niche markets, supplying consumers with additional sporting experiences. Examples of niche products include exclusive country clubs that charge extremely high membership fees and provide an extensive array of luxury sporting and non-sporting facilities. Establishments that offer services such as tennis, squash, swimming, massage, and others, invest in higher levels of capital equipment.

Level��The level of Technology Change is Low

Level��The level of Volatility is Low

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 29

Operating�Conditions

Regulation�&�Policy Golf courses and country clubs are subject to federal, state and local laws and regulations concerning the discharge of waste and chemicals into the water and air; storage of fertilizers, pesticides, chemicals, petrol and gas on-site within golf courses; and the disposal of food. Clubs must also meet land-development and planning requirements when changes to infrastructure are required.

Some golf courses contain or have contained underground storage tanks (USTs) to store fuels and other hazardous materials. There are numerous statutes and regulations

applying to USTs that firms must be aware of. For example laws state that to USTs must be federal and state approved and some must be concrete lined steel, or double walled. Some USTs must be retrofitted with new detection and spill prevention equipment.

Establishments must have licenses for the serving of food and liquor. The industry must abide by workplace health and safety conditions, as well as the minimum wage and overtime rules covered under the Fair Labor Standards Act. Operators must also ensure building and facility access for disabled people at golf courses and country club facilities.

Revenue�Volatilitycontinued

membership occurred 2009 due to poor economic conditions, including low consumer sentiment and rising unemployment. Fewer people will renew

their memberships in 2010 as the recession and a slow expected recovery leads people to keep their discretionary budgets tight.

SOURCE: WWW.IBISWORLD.COM

Volatility�vs�Growth

Reve

nue�

vola

tility

*�(%

)�

1000

100

10

1

0.1

Five�year�annualized�revenue�growth�(%)�–30 –10 10 30 50 70

Hazardous

Stagnant

Rollercoaster

Blue�Chip

* Axis is in logarithmic scale

Golf�Courses�&�Country�Clubs

A higher level of revenue volatility implies greater industry risk. Volatility can negatively affect long-term strategic decisions, such as the time frame for capital investment.

When a fi rm makes poor investment decisions it may face underutilized capacity if demand suddenly falls, or capacity constraints if it rises quickly.

Level�&�Trend��The level of Regulation is Medium and the trend is Steady

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 30

Operating�Conditions

Industry�Assistance The Golf Courses and Country Clubs Industry is not directly subject to international trade and the associated import tariffs and quotas. Some public courses are exempt from paying federal taxes.

There are a number of industry associations that are relevant to US Golf Courses and Country Clubs, including: United States Golf Association; PGA

Tour and LPGA Tour; Professional Golf Association of America; American Junior Golf Association; National Golf Course Owners Association; Club Managers Association of America; National Club Association; International Health, Racquet and Sports Club Association; National Restaurant Association; and the National Golf Foundation.

Level�&�Trend��The level of Industry Assistance is None and the trend is Steady

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 31

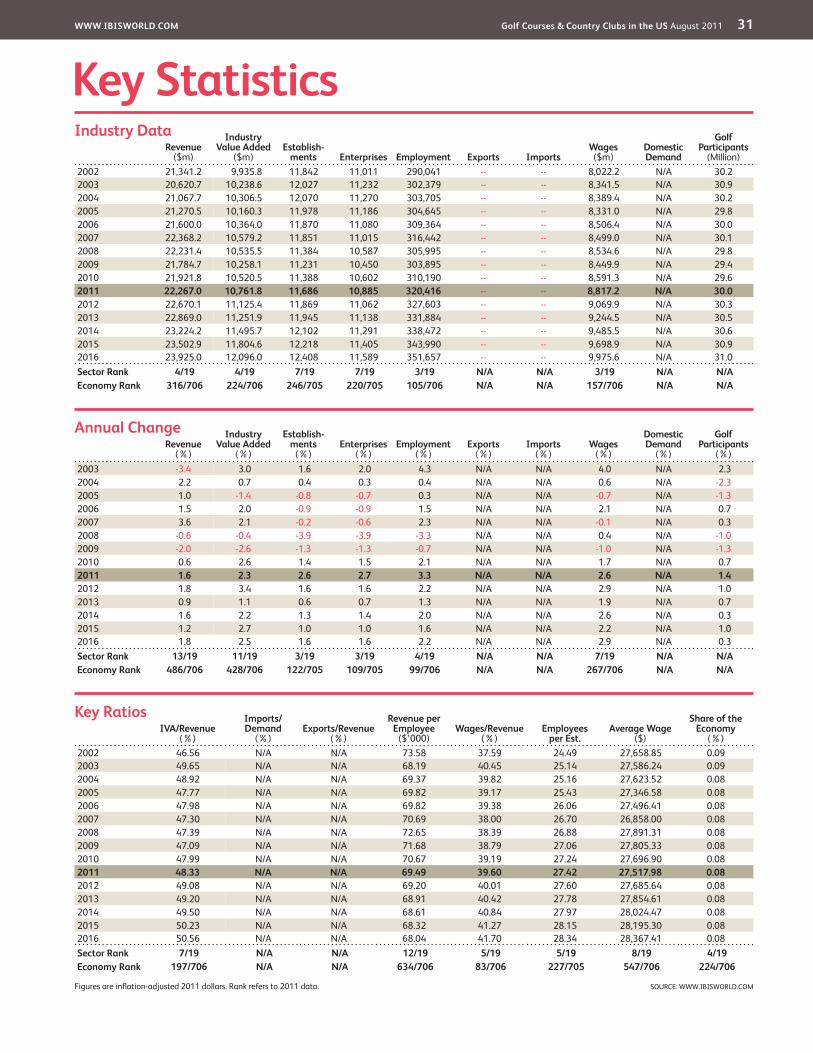

�Key�StatisticsRevenue�

($m)

Industry�Value�Added�

($m)Establish-

ments Enterprises Employment Exports ImportsWages�($m)

Domestic�Demand

Golf�Participants�

(Million)2002 21,341.2 9,935.8 11,842 11,011 290,041 -- -- 8,022.2 N/A 30.22003 20,620.7 10,238.6 12,027 11,232 302,379 -- -- 8,341.5 N/A 30.92004 21,067.7 10,306.5 12,070 11,270 303,705 -- -- 8,389.4 N/A 30.22005 21,270.5 10,160.3 11,978 11,186 304,645 -- -- 8,331.0 N/A 29.82006 21,600.0 10,364.0 11,870 11,080 309,364 -- -- 8,506.4 N/A 30.02007 22,368.2 10,579.2 11,851 11,015 316,442 -- -- 8,499.0 N/A 30.12008 22,231.4 10,535.5 11,384 10,587 305,995 -- -- 8,534.6 N/A 29.82009 21,784.7 10,258.1 11,231 10,450 303,895 -- -- 8,449.9 N/A 29.42010 21,921.8 10,520.5 11,388 10,602 310,190 -- -- 8,591.3 N/A 29.62011 22,267.0 10,761.8 11,686 10,885 320,416 -- -- 8,817.2 N/A 30.02012 22,670.1 11,125.4 11,869 11,062 327,603 -- -- 9,069.9 N/A 30.32013 22,869.0 11,251.9 11,945 11,138 331,884 -- -- 9,244.5 N/A 30.52014 23,224.2 11,495.7 12,102 11,291 338,472 -- -- 9,485.5 N/A 30.62015 23,502.9 11,804.6 12,218 11,405 343,990 -- -- 9,698.9 N/A 30.92016 23,925.0 12,096.0 12,408 11,589 351,657 -- -- 9,975.6 N/A 31.0Sector�Rank 4/19 4/19 7/19 7/19 3/19 N/A N/A 3/19 N/A N/AEconomy�Rank 316/706 224/706 246/705 220/705 105/706 N/A N/A 157/706 N/A N/A

IVA/Revenue�(%)

Imports/Demand�

(%)Exports/Revenue�

(%)

Revenue�per�Employee�

($’000)Wages/Revenue�

(%)Employees�

per�Est.Average�Wage�

($)

Share�of�the�Economy�

(%)2002 46.56 N/A N/A 73.58 37.59 24.49 27,658.85 0.092003 49.65 N/A N/A 68.19 40.45 25.14 27,586.24 0.092004 48.92 N/A N/A 69.37 39.82 25.16 27,623.52 0.082005 47.77 N/A N/A 69.82 39.17 25.43 27,346.58 0.082006 47.98 N/A N/A 69.82 39.38 26.06 27,496.41 0.082007 47.30 N/A N/A 70.69 38.00 26.70 26,858.00 0.082008 47.39 N/A N/A 72.65 38.39 26.88 27,891.31 0.082009 47.09 N/A N/A 71.68 38.79 27.06 27,805.33 0.082010 47.99 N/A N/A 70.67 39.19 27.24 27,696.90 0.082011 48.33 N/A N/A 69.49 39.60 27.42 27,517.98 0.082012 49.08 N/A N/A 69.20 40.01 27.60 27,685.64 0.082013 49.20 N/A N/A 68.91 40.42 27.78 27,854.61 0.082014 49.50 N/A N/A 68.61 40.84 27.97 28,024.47 0.082015 50.23 N/A N/A 68.32 41.27 28.15 28,195.30 0.082016 50.56 N/A N/A 68.04 41.70 28.34 28,367.41 0.08Sector�Rank 7/19 N/A N/A 12/19 5/19 5/19 8/19 4/19Economy�Rank 197/706 N/A N/A 634/706 83/706 227/705 547/706 224/706

Figures are inflation-adjusted 2011 dollars. Rank refers to 2011 data.

Revenue�(%)

Industry�Value�Added�

(%)

Establish-ments�

(%)Enterprises�

(%)Employment�

(%)Exports�

(%)Imports�

(%)Wages�

(%)

Domestic�Demand�

(%)

Golf�Participants�

(%)2003 -3.4 3.0 1.6 2.0 4.3 N/A N/A 4.0 N/A 2.32004 2.2 0.7 0.4 0.3 0.4 N/A N/A 0.6 N/A -2.32005 1.0 -1.4 -0.8 -0.7 0.3 N/A N/A -0.7 N/A -1.32006 1.5 2.0 -0.9 -0.9 1.5 N/A N/A 2.1 N/A 0.72007 3.6 2.1 -0.2 -0.6 2.3 N/A N/A -0.1 N/A 0.32008 -0.6 -0.4 -3.9 -3.9 -3.3 N/A N/A 0.4 N/A -1.02009 -2.0 -2.6 -1.3 -1.3 -0.7 N/A N/A -1.0 N/A -1.32010 0.6 2.6 1.4 1.5 2.1 N/A N/A 1.7 N/A 0.72011 1.6 2.3 2.6 2.7 3.3 N/A N/A 2.6 N/A 1.42012 1.8 3.4 1.6 1.6 2.2 N/A N/A 2.9 N/A 1.02013 0.9 1.1 0.6 0.7 1.3 N/A N/A 1.9 N/A 0.72014 1.6 2.2 1.3 1.4 2.0 N/A N/A 2.6 N/A 0.32015 1.2 2.7 1.0 1.0 1.6 N/A N/A 2.2 N/A 1.02016 1.8 2.5 1.6 1.6 2.2 N/A N/A 2.9 N/A 0.3Sector�Rank 13/19 11/19 3/19 3/19 4/19 N/A N/A 7/19 N/A N/AEconomy�Rank 486/706 428/706 122/705 109/705 99/706 N/A N/A 267/706 N/A N/A

Annual�Change

Key�Ratios

Industry�Data

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM� Golf�Courses�&�Country�Clubs�in�the�US August 2011 32

Jargon�&�Glossary

BARRIERS�TO�ENTRY Barriers to entry can be High, Medium or Low. High means new companies struggle to enter an industry, while Low means it is easy for a firm to enter an industry.

CAPITAL/LABOR�INTENSITY An indicator of how much capital is used in production as opposed to labor. Level is stated as High, Medium or Low. High is a ratio of less than $3 of wage costs for every $1 of depreciation; Medium is $3 – $8 of wage costs to $1 of depreciation; Low is greater than $8 of wage costs for every $1 of depreciation.

CONSTANT�PRICES The dollar figures in the Key Statistics table, including forecasts, are adjusted for inflation using 2011 as the base year. This removes the impact of changes in the purchasing power of the dollar, leaving only the ‘real’ growth or decline in industry metrics. The inflation adjustments in IBISWorld’s reports are made using the US Bureau of Economic Analysis’ implicit GDP price deflator.

DOMESTIC�DEMAND The use of goods and services within the US; the sum of imports and domestic production minus exports.

EARNINGS�BEFORE�INTEREST�AND�TAX�(EBIT)� IBISWorld uses EBIT as an indicator of a company’s profitability. It is calculated as revenue minus expenses, excluding tax and interest.

EMPLOYMENT The number of working proprietors, partners, permanent, part-time, temporary and casual employees, and managerial and executive employees.

ENTERPRISE A division that is separately managed and keeps management accounts. The most relevant measure of the number of firms in an industry.

ESTABLISHMENT The smallest type of accounting unit within an Enterprise; usually consists of one or more locations in a state or territory of the country in which it operates.

EXPORTS The total sales and transfers of goods produced by an industry that are exported.

IMPORTS The value of goods and services imported with the amount payable to non-residents.

INDUSTRY�CONCENTRATION IBISWorld bases concentration on the top four firms. Concentration is identified as High, Medium or Low. High means the top four players account for over 70% of revenue; Medium is 40 –70% of revenue; Low is less than 40%.

INDUSTRY�REVENUE The total sales revenue of the industry, including sales (exclusive of excise and sales tax) of goods and services; plus transfers to other firms of the same business; plus subsidies on production; plus all other operating income from outside the firm (such as commission income, repair and service income, and rent, leasing and hiring income); plus capital work done by rental or lease. Receipts from interest royalties, dividends and the sale of fixed tangible assets are excluded.

INDUSTRY�VALUE�ADDED The market value of goods and services produced by an industry minus the cost of goods and services used in the production process, which leaves the gross product of the industry (also called its Value Added).

INTERNATIONAL�TRADE The level is determined by: Exports/Revenue: Low is 0 –5%; Medium is 5 –20%; High is over 20%. Imports/Domestic Demand: Low is 0 –5%; Medium is 5 –35%; and High is over 35%.

LIFE�CYCLE All industries go through periods of Growth, Maturity and Decline. An average life cycle lasts 70 years. Maturity is the longest stage at 40 years with Growth and Decline at 15 years each.

NON-EMPLOYING�ESTABLISHMENT Businesses with no paid employment and payroll are known as non-employing establishments. These are mostly set-up by self employed individuals.

VOLATILITY The level of volatility is determined by the percentage change in revenue over the past five years. Volatility levels: Very High is greater than ±20%; High Volatility is between ±10% and ±20%; Moderate Volatility is between ±3% and ±10%; and Low Volatility is less than ±3%.

WAGES The gross total wages and salaries of all employees of the establishment.

Industry�Jargon

IBISWorld�Glossary

GREEN�FEE A fee paid to play a round of golf at a course.

OCCASIONAL�GOLFER A golfer who only plays up to seven times a year and does not have a significant impact on industry revenue levels.

REGULAR�GOLFER An avid golfer who plays at least 25 rounds annually, accounts for most golf-related spending and tends to have a greater influence on the industry.

Disclaimer

This product has been supplied by IBISWorld Inc. (‘IBISWorld’) solely for use by its authorized licenses strictly in accordance with their license agreements with IBISWorld. IBISWorld makes no representation to any other person with regard to the completeness or accuracy of the data or information contained herein, and it accepts no responsibility and disclaims all liability (save for liability which cannot be lawfully disclaimed) for loss or damage whatsoever suffered or incurred by any other person resulting from the use