i touristics + shoreplan engineering limited - culture... · 2020-07-31 · touristics and...

TRANSCRIPT

i TOURISTICS + Shoreplan Engineering Limited

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

i TOURISTICS + Shoreplan Engineering Limited

TABLE OF CONTENTS LIST OF TABLES ......................................................................................................................................... iii

LIST OF FIGURES ....................................................................................................................................... iii

LIST OF EXHIBITS ....................................................................................................................................... iii

EXECUTIVE SUMMARY ............................................................................................................................. vii

SECTION 1 - INTRODUCTION .................................................................................................................... 1

1.0 Background ......................................................................................................................................... 1

1.1 Study Approach ................................................................................................................................... 1

1.3 Report Format ..................................................................................................................................... 2

SECTION 2 – EXISTING RECREATIONAL BOATING FACILITIES IN HALTON REGION ...................... 3

2.0 Boating Facilities ................................................................................................................................. 3

2.1 Amenities and Services ....................................................................................................................... 3

2.2 Seasonal and Transient Slip Users ..................................................................................................... 8

2.3 Assessment of Infrastructural Features at Boating Facilities .............................................................. 9

2.3.1 La Salle Park ................................................................................................................................ 9

2.3.2 Bronte Harbour........................................................................................................................... 10

2.3.3 Oakville Harbour ........................................................................................................................ 11

2.3.4 Oakville Harbour Marina - Oakville Harbour .............................................................................. 11

2.3.5 Oakville Yacht Squadron ........................................................................................................... 12

2.3.6 The Oakville Club ....................................................................................................................... 12

2.3.7 Wai Nui O Kanaka Outrigger Canoe Club ................................................................................. 13

2.3.8 Oakville Power Boat Club .......................................................................................................... 13

2.3.9 Burloak Canoe Club ................................................................................................................... 13

2.4 Other Boating Facilities in Halton ...................................................................................................... 13

2.5 Comparison of Halton’s Boating Facilities with those of the GTA/Golden Horseshoe Area ............. 14

2.5.1 Boating Facilities ........................................................................................................................ 14

2.5.2 Amenities and Services ............................................................................................................. 14

2.5.3 Seasonal and Transient Slip Users............................................................................................ 14

2.5.4 Facilities in Halton Compared with the GTA/Golden Horseshoe Area ...................................... 14

2.5.5 Marina Rates and Fees in Halton Compared with the GTA/Golden Horseshoe Area ............... 15

2.5.6 Annual Rate Increases ............................................................................................................... 16

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

ii TOURISTICS + Shoreplan Engineering Limited

SECTION 3 – PROFILE OF BOATERS AND POPULATION CHARACTERISTICS ................................ 19

3.0 Introduction........................................................................................................................................ 19

3.1 Socio-demographic Profile of Sail and Power Boaters ..................................................................... 19

3.2 Socio-demographic Characteristics of Burlington, Oakville and Halton Residents .......................... 19

3.3 Projected Population of Halton 2013 to 2031 ................................................................................... 22

3.4 Projected Growth in Boating Activities .............................................................................................. 22

SECTION 4 – EXISTING AND PROJECTED NUMBER OF BOATS IN ONTARIO ................................. 27

4.0 Introduction........................................................................................................................................ 27

4.1 Historical Number of Boats by Length, Beam and Draft, 2007 to 2012 ............................................ 27

4.1.1 Length ........................................................................................................................................ 27

4.1.2 Beam .......................................................................................................................................... 29

4.1.3 Draft ........................................................................................................................................... 29

4.2 Projected Number of Boats ............................................................................................................... 30

4.2.1 Length of Ontario Boats ............................................................................................................. 30

4.2.2 Beam of Ontario Boats ............................................................................................................... 32

4.2.3 Draft of Ontario Boats ................................................................................................................ 32

4.2.4 Length of New York State Boats ................................................................................................ 32

4.2.5 Beam of New York State Boats ................................................................................................. 33

4.2.6 Draft of New York State Boats ................................................................................................... 33

SECTION 5 – CURRENT AND PROJECTED NEED FOR SEASONAL AND TRANSIENT SLIPS AND LAUNCH RAMPS IN HALTON REGION ................................................................................................... 35

5.0 Introduction........................................................................................................................................ 35

5.1 Need for Seasonal Slips .................................................................................................................... 35

5.2 Need for Transient Slips .................................................................................................................... 36

5.2.1 Transient Boater Market ............................................................................................................ 36

5.2.2 Existing Number of Transient Boats in Market Area .................................................................. 37

5.2.3 Projected Number of Transient Boats in Market Area ............................................................... 37

5.2.4 What Transient Boaters are Interested In .................................................................................. 38

5.3 Need for Launch Ramps ................................................................................................................... 39

SECTION 6 – PLANNING FOR FUTURE BOATER NEEDS IN HALTON ............................................... 41

6.0 Introduction........................................................................................................................................ 41

6.1 Monitoring Current Demand Situation ............................................................................................... 43

6.1.1 Meeting Future Seasonal Slips and Boater Demand................................................................. 43

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

iii TOURISTICS + Shoreplan Engineering Limited

LIST OF TABLES

Table 1 – Boating Facilities in Halton ........................................................................................................ 3

Table 2 – Boating Facilities in Halton Compared to the GTA/Golden Horseshoe Area ......................... 15

Table 3 – Evaluation of Halton’s Harbours Boating Facilities ................................................................. 17

Table 4 – Strengths, Weaknesses, Opportunities and Threats for Recreational Boating in Halton ....... 42

LIST OF FIGURES

Figure 1 – La Salle Park ............................................................................................................................ 4

Figure 2 – Oakville Harbour ...................................................................................................................... 5

Figure 3 – Bronte Harbour ........................................................................................................................ 6

Figure 4 – Launch Ramp Locations .......................................................................................................... 7

Figure 5 – Residence of Boat Owners at Seasonal Slips ......................................................................... 9

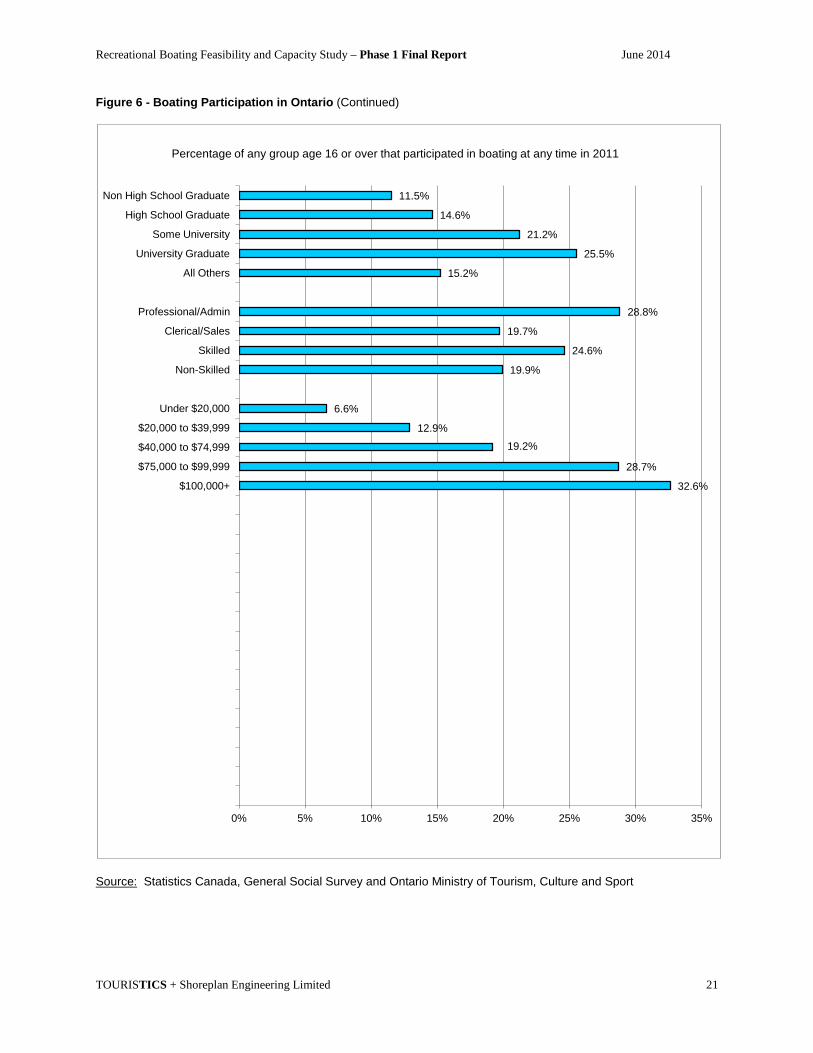

Figure 6 – Boating Participation in Ontario ............................................................................................. 20

Figure 7 – Halton Population Projections 2011 to 2031 (25 and over) ................................................... 23

Figure 8 – Projected Growth in Halton’s Share of Ontario’s Power and Sail Boaters ............................ 24

Figure 9 – Projected Growth in Percentage of Ontario’s Population Participating in Selected Boating Activities .................................................................................................................................................. 24

Figure 10 – Projected Growth in Number of Power and Sail Boaters in Halton (2013 to 2031) ............. 25

Figure 11 – Historical Growth of Ontario’s and New York’s Recreational Boats – 6 metres to less than 8 metres (2007 to 2012) ............................................................................................................................. 28

Figure 12 – Historical Growth in Length of Largest Ontario’s Recreational Boats (2007 to 2012) ......... 28

Figure 13 – Historical Growth in Length of Largest New York State’s Recreational Boats (2007 to 2012)................................................................................................................................................................. 29

Figure 14 – Percentage Share of Ontario’s Boat Market by Length of Boat (2007 to 2031) .................. 31

LIST OF EXHIBITS

EXHIBIT 1A MARINAS, YACHT AND BOAT CLUBS WITHIN HALTON REGION – NUMBER AND SIZE OF SLIPS ....................................................................................................................................... 45

EXHIBIT 1B MARINAS, YACHT AND BOAT CLUBS WITHIN HALTON REGION – FACILITIES AND SERVICES .............................................................................................................................................. 47

EXHIBIT 1C MARINAS, YACHT AND BOAT CLUBS WITHIN HALTON REGION – FEES AND USER PATTERNS ............................................................................................................................................. 49

EXHIBIT 1D MARINAS, YACHT AND BOAT CLUBS WITHIN HALTON REGION – ASSESSMENT OF DOCKS, FAIRWAYS, BREAKWATER AND FUEL DOCKS .................................................................. 52

EXHIBIT 1E MARINAS, YACHT AND BOAT CLUBS WITHIN HALTON REGION – ASSESSMENT OF PUMPOUT STATIONS, LAUNCH RAMPS AND SECURITY MEASURES ........................................... 53

EXHIBIT 2A PROGRAMS OFFERED BY BOATING CLUBS WITHIN HALTON REGION .................. 54

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

iv TOURISTICS + Shoreplan Engineering Limited

EXHIBIT 2B PROGRAMS OFFERED BY YACHT AND SAILING CLUBS WITHIN HALTON REGION................................................................................................................................................................. 57

EXHIBIT 3 KELSO CONSERVATIN BOAT RENTALS.......................................................................... 59

EXHIBIT 4A MARINAS AND YACHT CLUBS WITHIN THE GREATER TORONTO AREA (GTA)/GOLDEN HORSESHOE – NUMBER AND SIZE OF SLIPS ....................................................... 60

EXHIBIT 4B MARINAS AND YACHT CLUBS WITHIN THE GREATER TORONTO AREA (GTA)/GOLDEN HORSESHOE – FACILITIES AND SERVICES ........................................................... 64

EXHIBIT 4C MARINAS AND YACHT CLUBS WITHIN THE GREATER TORONTO AREA (GTA)/GOLDEN HORSESHOE – FEES ................................................................................................. 70

EXHIBIT 5 COMPARISON OF 2014 SUMMER AND WINTER MARINA FEES IN HALTON REGION AND THE GTA/GOLDEN HORSESHOE AREA ..................................................................................... 84

EXHIBIT 6 ANNUAL SUMMER AND WINTER RATES AND FEES 2014 (30 foot boat) ...................... 86

EXHIBIT 7 MARINA FACILITIES AND SERVICES RATING ................................................................ 86

EXHIBIT 8 EVALUATION OF MARINA SERVICES AND FACILITIES IN HALTON REGION AND GTA/GOLDEN HORSESHOE AREA ...................................................................................................... 87

EXHIBIT 9 SELECTED SOCIO-DEMOGRAPHIC CHARACTERISTICS OF RESIDENTS WITHIN HALTON REGION................................................................................................................................... 88

EXHIBIT 10 POPULATION PROJECTIONS FOR HALTON REGION BY AGE AND GENDER CATEGORIES IMPORTANT TO RECREATIONAL BOATING .............................................................. 90

EXHIBIT 11 POPULATION PROJECTIONS FOR ONTARIO BY AGE AND GENDER CATEGORIES IMPORTANT TO RECREATIONAL BOATING ....................................................................................... 92

EXHIBIT 12 LENGTH OF BOATS REGISTERED WITHIN ONTARIO AND NEARBY U.S. STATES .. 94

EXHIBIT 13 BEAM OF BOATS REGISTERED WITHIN ONTARIO AND NEARBY U.S. STATES ...... 96

EXHIBIT 14 DRAFT OF BOATS REGISTERED WITHIN ONTARIO AND NEARBY U.S. STATES .... 97

EXHIBIT 15 TYPE OF BOAT REGISTERED IN ONTARIO AND NEARBY U.S. STATES ................... 99

EXHIBIT 16 NUMBER OF BOATS IN OTHER CANADIAN PROVINCES AND TOP 12 U.S. STATES IN 2012 .................................................................................................................................................. 100

EXHIBIT 17 PLEASURE CRAFT LICENSES GRANTED BY TRANSPORT CANADA IN 2013 ........ 101

EXHIBIT 18 PLEASURE CRAFT LICENSES CANCELLED BY TRANSPORT CANADA IN 2013 .... 102

EXHIBIT 19 PROJECTED GROWTH BY LENGTH OF BOATS REGISTERED IN ONTARIO (2013 to 2031) ..................................................................................................................................................... 103

EXHIBIT 20 PROJECTED GROWTH BY BEAM (WIDTH) OF BOATS REGISTERED IN ONTARIO (2013 to 2031) ....................................................................................................................................... 104

EXHIBIT 21 PROJECTED GROWTH BY DRAFT OF BOATS REGISTERED IN ONTARIO (2013 to 2031) ..................................................................................................................................................... 105

EXHIBIT 22 PROJECTED GROWTH BY TYPE OF BOATS REGISTERED IN ONTARIO (2013 to 2031) ..................................................................................................................................................... 106

EXHIBIT 23 PROJECTED GROWTH BY LENGTH OF BOATS REGISTERED IN NEW YORK STATE (2013 to 2031) ....................................................................................................................................... 107

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

v TOURISTICS + Shoreplan Engineering Limited

EXHIBIT 24 PROJECTED GROWTH BY WIDTH OF BOATS REGISTERED IN NEW YORK STATE (2013 to 2031) ....................................................................................................................................... 108

EXHIBIT 25 PROJECTED GROWTH BY DRAFT OF BOATS REGISTERED IN NEW YORK STATE (2013 to 2031) ....................................................................................................................................... 109

EXHIBIT 26 PROJECTED GROWTH BY TYPE OF BOATS REGISTERED IN NEW YORK STATE (2013 to 2031) ....................................................................................................................................... 110

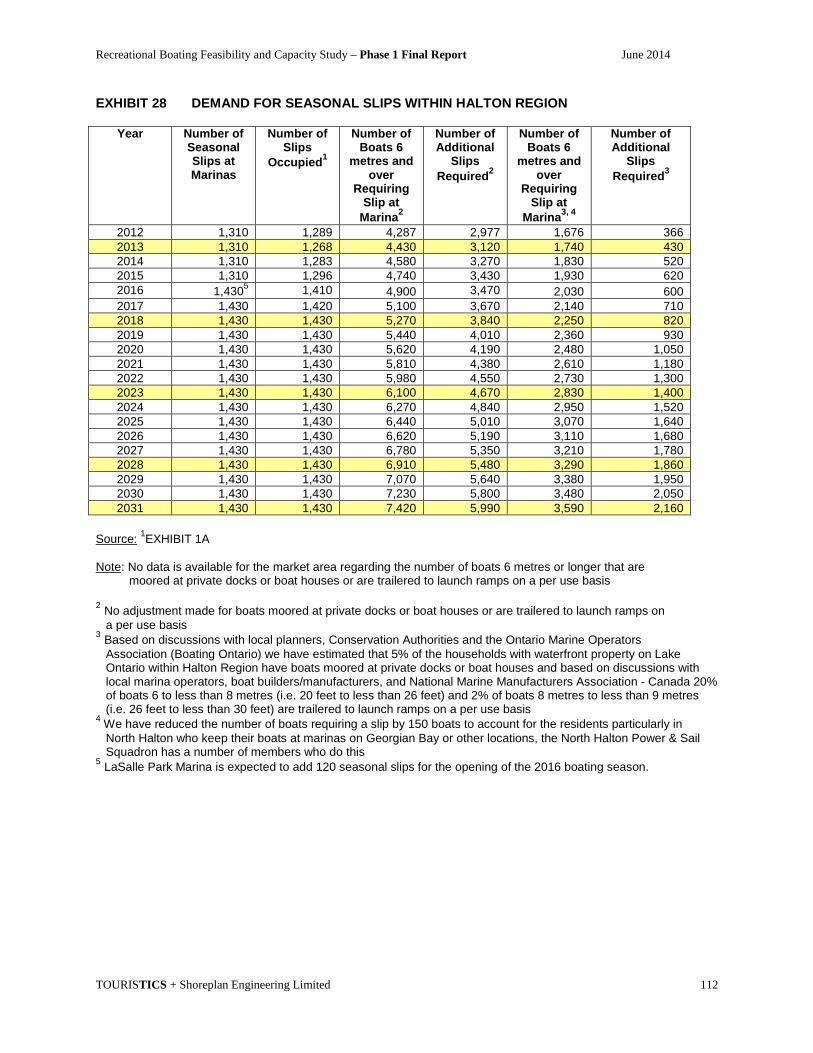

EXHIBIT 27 ESTIMATED NUMBER OF SEASONAL BOATS WITHIN HALTON REGION ............... 111

EXHIBIT 28 DEMAND FOR SEASONAL SLIPS WITHIN HALTON REGION .................................... 112

EXHIBIT 29 AVERAGE DISTANCE TRAVELLED AWAY FROM MARINA ........................................ 113

EXHIBIT 30 AVERAGE NUMBER OF DAYS USING A BOAT ........................................................... 113

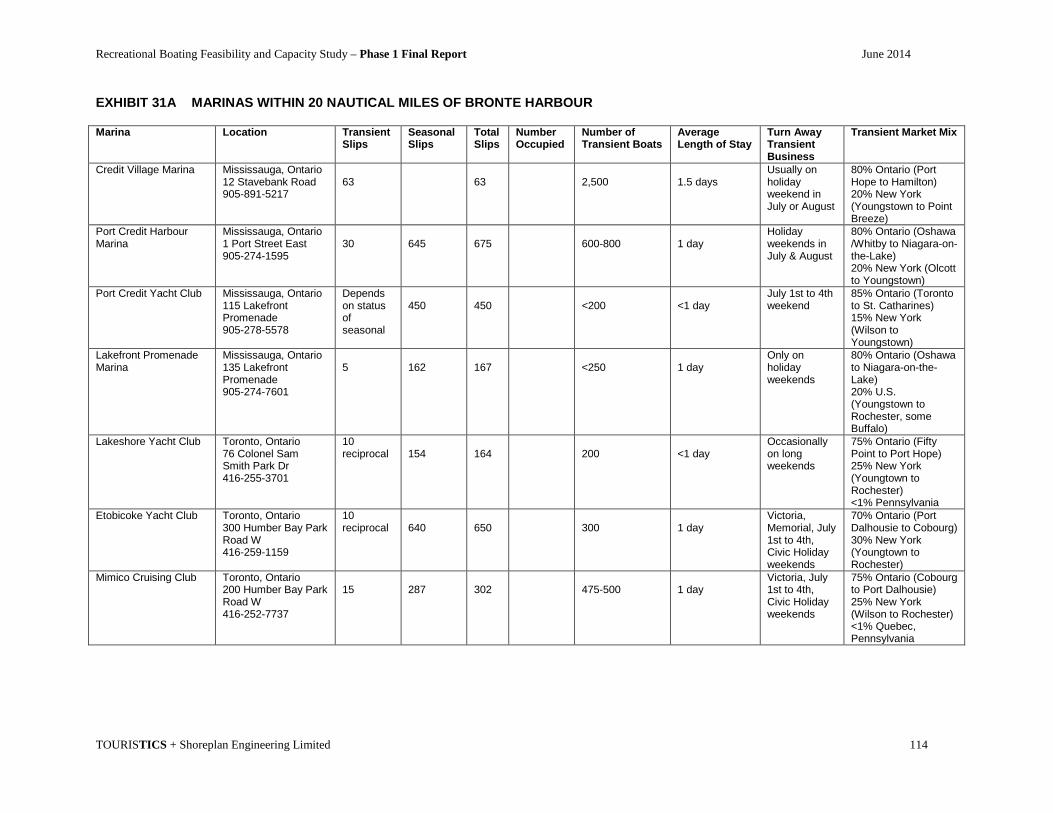

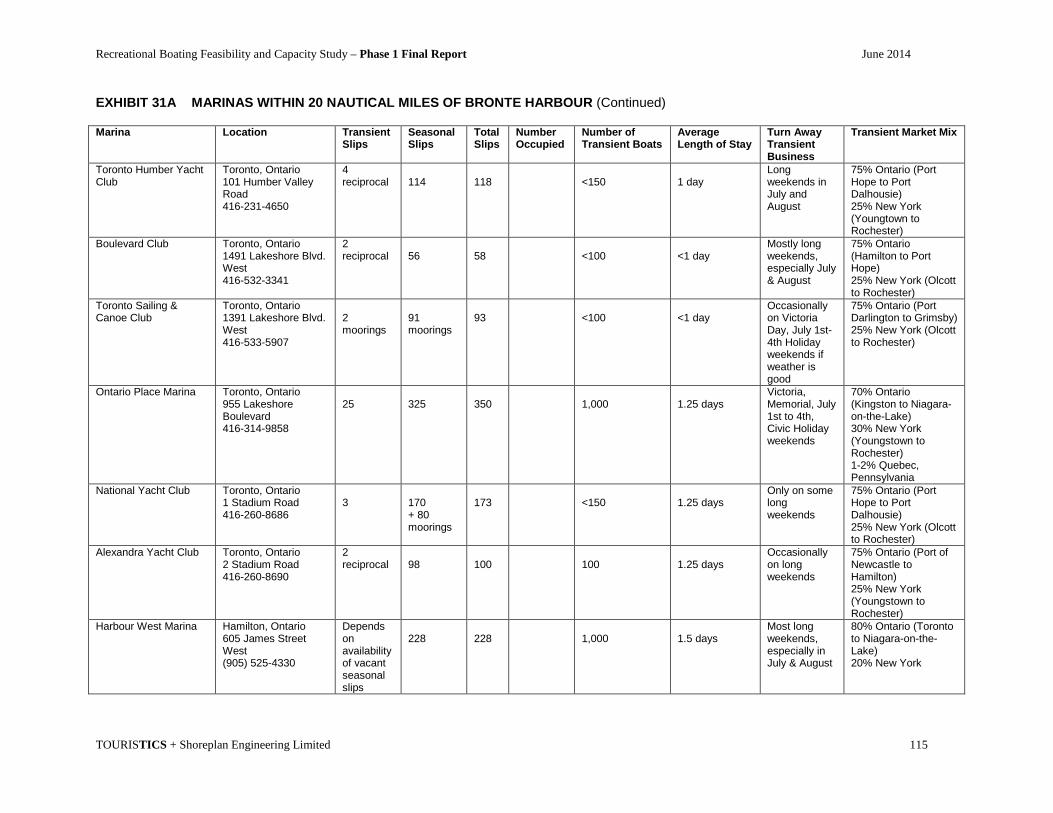

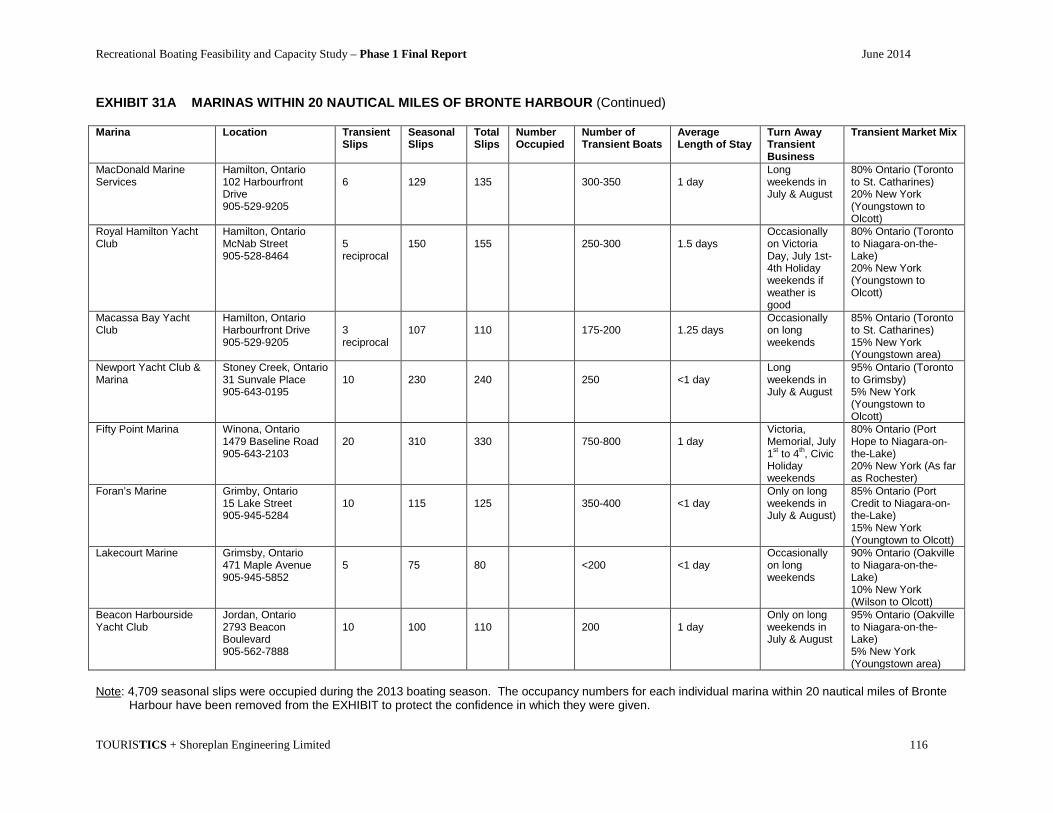

EXHIBIT 31A MARINAS WITHIN 20 NAUTICAL MILES OF BRONTE HARBOUR ........................... 114

EXHIBIT 31B MARINAS WITHIN 21 TO 40 NAUTICAL MILES OF BRONTE HARBOUR ................ 117

EXHIBIT 31C MARINAS WITHIN 41 TO 60 NAUTICAL MILES OF BRONTE HARBOUR ................ 122

EXHIBIT 31D MARINAS WITHIN 61 TO 80 NAUTICAL MILES OF BRONTE HARBOUR ................ 124

EXHIBIT 32 NUMBER OF SEASONAL AND TRANSIENT SLIPS WITHIN TRANSIENT MARKET AREA OF HALTON REGION BOATING FACILITIES .......................................................................... 126

EXHIBIT 33 NUMBER OF POWER AND SAIL BOATS WITHIN TRANSIENT MARKET AREA OF HALTON REGION BOATING FACILITIES ........................................................................................... 126

EXHIBIT 34 POTENTIAL TRANSIENT BOATS WITHIN MARKET AREA OF HALTON REGION BOATING FACILITIES IN 2013 ............................................................................................................ 126

EXHIBIT 35 PROJECTED NUMBER OF BOATS WITHIN 80 NAUTICAL MILES OF HALTON REGION BOATING FACILITIES 2013 TO 2031 .................................................................................. 127

EXHIBIT 36 PROJECTED NUMBER OF TRANSIENT BOATERS WITHIN 80 NAUTICAL MILES OF HALTON REGION BOATING FACILITIES 2013 TO 2031 ................................................................... 128

EXHIBIT 37 ESTIMATED NUMBER OF BOATS IN HALTON REGION LIKELY TO USE A LAUNCH RAMP FOR THEIR BOATING ACTIVITY ............................................................................................. 129

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

vi TOURISTICS + Shoreplan Engineering Limited

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

vii TOURISTICS + Shoreplan Engineering Limited

EXECUTIVE SUMMARY Study Objectives TOURISTICS and Shoreplan Engineering Limited were retained by the Town of Oakville, City of Burlington (in partnership with LaSalle Park Marina Association) and Halton Region to conduct the first of a two phased study to determine the current and anticipated demand for recreational boating facilities within Halton and the Greater Toronto Area (GTA)/Golden Horseshoe Region over the period from 2013 until 2031 and the need to accommodate any future demand for additional slips. The intent of the study was to provide a comprehensive analysis of current harbour capacity within the GTA/Golden Horseshoe region and specifically within Halton Region. It was also the intent of the study to assess the changing demographic profile or the area and the impacts of these changes on the anticipated demand for recreational boating, the sources and location of this demand, trends in the type of boating and berth requirements with the aim of making recommendations on whether or not additional harbour capacity is warranted within Halton. The demand for additional slips and launch ramps in Halton will be dependent on three major factors:

• The ability of the existing marina facilities within the market area to meet the current and future demand, and the overall occupancy rate of the marinas within the seasonal market area;

• The growth in the number of power and sail boats in the seasonal market area and the changes

in their length, beam and draft; and,

• The market area for seasonal slips and launch ramps exhibiting socio-demographic characteristics that are strong determinants of power and sail boating demand.

Key Findings Boating Facilities in Halton There are four marinas, three yacht clubs, one power boat club, and four boating clubs in Halton Region. They provide recreational boating enthusiasts with opportunities for canoeing, kayaking, sailing, and the use of catamarans, outrigger canoes, and stand up paddle boards. In addition, the reservoir at Kelso Conservation Area, lake at Mountsberg Conservation Area and Fairy Lake at Prospect Park all in the northern part of Halton provide areas suitable to launch and use small aluminum boats, canoes, kayaks, paddle boats and stand up paddle boards. In addition to the marinas, yacht and power boat clubs, Halton is also home to four boating clubs (Burloak Canoe Club, Burlington Sailing and Boating Club, Burlington Beach Catamaran Club, Wai Nui O Kanata Outrigger Canoe Club) catering to non-motorized boating activities. The four clubs offer opportunities for participation with canoes, outrigger canoes, kayaks, war canoes, dragon boats, dinghies, keel boats, paddle boats and stand up paddle boards. All report an increase in the number members, programs offered and participants in 2013. The programs are offered to members and non-members and both children and adults. The physical conditions of the boating infrastructure at the three existing harbour locations on Lake Ontario (Oakville Creek, Bronte Creek and LaSalle Park), are, with one exception, generally adequate with some poor conditions mostly related to dock spacing. The dock spacing tends to be less than suggested in current marina guidelines for public facilities and the docks are less stable than some currently available products for commercial facilities. Much of the docking is provided without finger docks. Most locations do not offer water and power on dock, as is commonly done. The one exception is Bronte Outer Harbour where the docks and their layout meet current guidelines and supporting infrastructure appears to be very in good condition.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

viii TOURISTICS + Shoreplan Engineering Limited

It is acknowledged that the Oakville is improving harbour infrastructure on ongoing basis, particularly as it relates to shoreline improvements. Further improvements are being planned. Burlington and LaSalle Park Marina Association recently completed a class environmental assessment for major wave protection improvements at La Salle Park Marina. Boating Facilities in Halton Compared with the GTA/Golden Horseshoe Area There are 41 boating facilities in the GTA/Golden Horseshoe Area between Scarborough in the east and St. Catharines in the west. Fourteen are marinas and the remaining 27 are yacht and sailing clubs. As shown in the Table following, although the occupancy rates and percentage of slips by length are similar, boaters at marinas and yacht clubs in Halton appear to be less well served than those in GTA/Golden Horseshoe area. As a percentage of total slips available, the GTA/Golden Horseshoe area offers twice as many transient slips as Halton and as a percentage of facilities, twice as many fuel docks. Although a higher percentage of facilities in the GTA/Golden Horseshoe area offer a pump out service, the number of slips per pump out is similar (i.e. 292 versus 336 in Halton). Both areas have insufficient on-site capacity to accommodate all the seasonal boats for winter storage (i.e. 71% in Halton versus 87% in the GTA). The demand for additional slips is much higher in Halton than the GTA/Golden Horseshoe area as expressed by the number of boats on the waiting list as a percentage of occupied seasonal slips (i.e. 36% in Halton versus 16% in the GTA). Halton GTA/Golden Horseshoe Area Number of Marinas, Yacht, Sailing and Power Boat Clubs

8 41

Seasonal Slips Occupied 1,310 96.8% 8,833 98.6% Transient Slips as Percentage of Total Slips

2.5% 5.4%

Percentage of Slips <30 feet 33.2% 20.2% Percentage of Slips 30 feet to <36 feet 44.0% 48.1% Percentage of Slips 36 feet to <46 feet 20.2% 22.9% Percentage of Slips 46 feet and over 2.6% 8.8% Percentage of Facilities with Fuel Docks 25% 53.7% Number of Slips Per Fuel Dock 672 424 Percentage of Facilities with Pump Out 50% 78.0% Number of Slips Per Pump Out 336 292 Percentage of Facilities with Launch Ramp

37.5% 53.6%

Percentage of Slips with 30 amp or more power

51.5% 78.6%

Percentage of Seasonal Boats Accommodated On-site for Winter Storage

70.8% 87.4%

Number of Boats on Waiting List 470 1,470 Boats on Waiting List as a Percentage of Occupied Seasonal Slips

35.9% 16.4%

Marina Rates and Fees The rates charged at Bronte Outer Harbour Marina, Bronte Harbour, Oakville Harbour, and LaSalle Park Marina are comparable with those in the GTA/Golden Horseshoe Area given the product offering. Marina operators throughout the GTA/Golden Horseshoe Area indicated that annual rate increases are typically held to three to four percent due to the highly competitive nature of the market place. Since there are no indications that marina operating costs will decrease in the future, it is expected that rates will continue to rise at this rate. One-time increases above three to four percent do occur when additional revenue is required for capital improvements. Rate increases at Bronte Outer Harbour Marina, Bronte and Oakville Harbours, and LaSalle Park Marina have consistently fallen within the area norms.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

ix TOURISTICS + Shoreplan Engineering Limited

Projected Population of Halton 2013 to 2031 The population of Halton 25 and older is projected to increase from 359,130 in 2013 (169,690 males, 189,440 females) to 403,450 by 2018 (196,980 males, 206,470 females), to 451,130 by 2023 (219,850 males, 231,280 females), to 498,180 by 2028 (243,090 males, 255,090 females), and reach 528,100 by 2031 (258,100 males, 269,850 females). This represents a 47 percent increase in the population between 2013 and 2031. During this same time period the population of Ontario 25 and older is projected to increase by only 26 percent from 9,614,530 (4,661,300 males, 4,953,230 females) in 2013, to 12,064,180 (5,850,820 males, 6,213,360 females) in 2031. The period from 2011 to 2031 will also see a 54 percent increase in employment in Halton while that of the province will increase by 27 percent. The increased growth in the age groups with high participation rates in boating (i.e. 35 to 44 and 45 to 54) and employment in Halton indicates a likely large increase in the demand for recreational boating activities and a larger share of Ontario’s power and sail boaters. Projected Growth in Boating Activities Between 2011 and 2030 participation in power boating, sailing, canoeing, kayaking and rowing are all projected to increase. There are no comparable projections available for outrigger canoeing, paddle boating, and stand up paddle boarding, although anecdotal information based on the increased number of members at area clubs suggests that participation in these activities is also in a growth mode. Over the 20 years between 2011 and 2030 participation in power boating, sailing, canoeing, kayaking and rowing is projected to increase as follows:

Activity 2011 2020 2030 Power Boating 10.8% 13.0% 14.6% Sailing 3.6% 4.3% 4.8% Canoeing 6.8% 7.6% 8.3% Kayaking 2.4% 4.4% 5.4% Rowing 3.0% 3.1% 3.3% Projected Growth in Power and Sail Boats 2013 to 2031 Between 2013 and 2031 the number of boats in Ontario is projected to grow as follows:

Length 2013 2023 2031 Percentage Increase

6 m. to <8 m. (20 ft. to <26 ft.) 64,700 71,950 74,230 14.7% 8 m. to <9 m. (26 ft. to <30 ft.) 12,780 14,760 15,440 20.8% 9 m. to <11 m. (30 ft. to <36 ft.) 19,400 29,720 39,010 101.1% 11 m. to <14 m. (36 ft. to <46 ft.) 11,590 16,810 21,120 82.2% 14 m. and longer (46 ft. or more) 6,470 9,980 13,180 103.7% This projected increased growth in the length of boats will have a particularly strong impact on the facilities in Oakville and Bronte Harbour where there is already a shortage of longer slips and many of the fairways are sub-standard in terms of width. This shortage will be further exacerbated as there will be a need to either modify the number of slips to accommodate wider beam widths or add more slips. Conclusions Need for Seasonal Slips By comparing the number of seasonal slips available in 2013 with the number of boats requiring a slip, it is evident that demand exceeds supply and additional slips are needed. It is estimated that at the end of

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

x TOURISTICS + Shoreplan Engineering Limited

the boating season in 2013 there was a need for 430 additional slips. By 2018 the need for additional slips will rise to 820; by 2023 to 1,400; by 2028 to 1,860; and reach 2,160 by 2031. By comparison to existing facilities within Halton, this would mean four additional marinas at least the size of Bronte Outer Harbour Marina. The trend toward longer and wider boats will have a significant impact on the number of slips in Oakville and Bronte Harbours where the finger docks are short and the fairways narrow. It is evident that there is a current and future need for seasonal slips in the 10.67 metre (35 foot), 12.12 metre (40 foot), and 13.72 metre (45 foot) range. Need for Transient Slips According to the 2009 Great Lakes Boating Survey, 60 percent of boater’s days away from their home marina are spent within 20 nautical miles. A further 20 percent are spent within 21 and 40 nautical miles, 10 percent within 41 to 60 nautical miles, 6 percent within 61 to 80 nautical miles, and the final 4 percent beyond 80 nautical miles. During the 2013 boating season, there were 54,190 boaters at the 75 marinas, yacht and power boat clubs within 80 nautical miles of Bronte Harbour. The number of transient boaters visiting the Halton facilities is dependent on the number of boaters within the market and their distance from Halton. Of the 54,190 within 80 nautical miles of Halton, 37,880 were within 20 nautical miles and would have the greatest likelihood of visiting on one or more occasions. The least likely are those 640 boaters within 61 to 80 nautical miles. By 2018 the total number of transient boater days within the overall market area is projected to increase to 59,900; to 65,170 by 2023; to 69,930 by 2028; and reach 72,700 by 2031. There is clearly an existing and growing transient boater market that the facilities in Halton would be in a position to attract. The Oakville Harbour, Bronte Harbour and Bronte Outer Harbour Marina are in easy walking distance of the type of shops and restaurants of interest to transient boaters. The numbers provided by the marinas, yacht and power boat clubs within Halton and those within the GTA/Golden Horseshoe Area and beyond confirm there is significant transient boater market to be attracted. Oakville, Burlington and Halton should increase the number of transient slips available; but should not exceed the industry average of approximately 15 percent of the total slips available. Based on the number of transient boaters attracted to the marinas, yacht and power boat clubs in the GTA/Golden Horseshoe Area, 200 transient slips in Halton Region (i.e. 1,344 x 0.15 = 200) could be expected to attract a minimum of 6,000 transient boaters annually. Need for Launch Ramps Boats that are trailered to launch ramps are typically less than 8 metres (less than 26 feet). Approximately 20 percent of boats 6 metres to less than 8 metres (i.e. 20 feet to less than 26 feet), and 2 percent of boats 8 metres to less than 9 metres (i.e. 26 feet to less than 30 feet) are trailered to launch ramps on a per use basis. Launch ramp use is usually concentrated during a three-hour launch period (morning) and three-hour retrieval period (afternoon). Launch ramps require a large amount of parking space. Typically a one lane ramp should have at least 35 to 45 vehicle and boat trailer parking spaces. A two lane launch ramp should have between 45 and 75 spaces. While we have determined that there is a sizable number of boats in Halton that would likely use a launch ramp, there is little data available to indicate the current level of use, as the two facilities in LaSalle Park in Burlington are free of charge and are not monitored. The Bronte and Oakville launch ramps had 2,200 documented users in 2013. Additional undocumented users frequent the facilities in LaSalle Park and the facilities in Hamilton and Mississauga due to the poor condition and limited parking at the Burlington, Bronte and Oakville launch ramps. The number of boats likely to use a launch ramp in Halton is projected to increase from 14,300 in 2013; to 15,440 by 2018; to 16,470 by 2023; to 17,370 by 2028; and reach 17,890 by 2031. Ideally, based on the existing data, one additional launch ramp will be required by 2018, two additional launch ramps (for a total of 6) will be required by 2023, and three more by 2031 for a

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

xi TOURISTICS + Shoreplan Engineering Limited

total of seven. However, until more detailed user data is available for the existing launch ramps we recommend that the municipalities concentrate on improving the existing facilities rather than adding additional ones. It should be noted that the Ministry of Natural Resources considers there is a world class fishery off Bronte/Oakville Harbours, especially for salmon fishing. There are currently eight fishing charter boat operators in Oakville and Bronte, and the Ministry feels that the fishery could support at least 12 fishing charter boats. In addition, the 34,100 licensed anglers in Halton spend hundreds of dollars each annually within the Region on fishing and boating equipment.

Purchases Wholly Attributable to Recreational Fishing

Average Annual Expenditure per Active Licensed Angler

Boating Equipment $342.54 Fishing Equipment $77.21 Recommendations Monitoring Current Demand Situation In order to provide boating facilities in a timely fashion it will be necessary to monitor the level of demand in an ongoing manner. For marinas this means maintaining a permanent waiting list which indicates the length, width and beam of the boat requiring a slip or mooring. For boating clubs (i.e. canoeing, kayaking, rowing, etc.) it means documenting the number of persons turned away from program offerings or membership categories. When an individual marina has reached capacity (i.e. 95% occupancy or more) and the marina manager has a documented waiting list approaching one-half the number of seasonal slips, a new or expanded facility is warranted. Given that the environmental, planning and construction steps involved in bringing a new marina to fruition will likely take a minimum of four years (i.e. planning, environmental assessment process and design; approvals by various government agencies; and construction); the waiting list likely will have reached a point where when combined with industry average trade-ups, the new facility will be assured of success as there will be no shortage of demand for slips. Meeting Future Seasonal Slip and Boater Demand The study clearly indicates that there is a demand for boating facilities much beyond the capacity of the existing facilities. It is also clear that the existing facilities and the three main existing locations cannot meet this demand by gradual expansion. The two river locations at Oakville and Bronte cannot expand further within the existing channel to any degree while respecting environmental objectives. The one location on the open lake in Bronte (i.e. Bronte Outer Harbour Marina) is bound by fixed breakwaters and cannot expand within the footprint of the breakwaters. The La Salle Park Marina is proposing provision of fixed breakwaters which then could accommodate some future expansion. No decision has been made on this location as of the writing of this report. As the identified demand for slips is beyond the capacity of the existing sites in the Region, new locations will need to be considered on a go forward basis. Selection of any new site will be a complex process that will be subject to an individual environmental assessment process and a thorough review by all levels of government and conservation authorities, as well as the general public. The projections suggest that if the demand were to be met with the typical size marina found on the Great Lakes, it would require the construction of four facilities at least as large as Bronte Outer Harbour Marina along the Halton waterfront by 2031. Clearly, this is a task that will call for extensive public consultations, creativity, and out of box thinking. In addition, the Burloak Canoe Club requires an additional 70 to 75 feet of shoreline dockage for a total of 100 feet to meet current demand, let alone future demand. Additional space and secured parking for

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

xii TOURISTICS + Shoreplan Engineering Limited

people with disabilities would allow the Wai Nui O Kanaka Outrigger Canoe Club to expand its membership as well.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 1

SECTION 1 – INTRODUCTION 1.0 Background TOURISTICS and Shoreplan Engineering Limited were retained by the Town of Oakville (Oakville), City of Burlington (Burlington) [in partnership with LaSalle Park Marina Association] and the Region of Halton (Halton) to conduct the first of a two phased study to determine the current and anticipated demand for recreational boating facilities within Halton and the Greater Toronto Area (GTA)/Golden Horseshoe Region over the period from 2013 until 2031 and the need to accommodate any future demand for additional slips. The intent of the study was to provide a comprehensive analysis of current harbour capacity within the GTA/Golden Horseshoe region and specifically within Halton. It was also the intent of the study to assess the changing demographic profile of the area and the impacts of these changes on the anticipated demand for recreational boating, the sources and location of this demand, trends in the type of boating and berth requirements with the aim of making recommendations on whether or not additional harbour capacity is warranted within Halton. This information will be used by Oakville, Burlington and Halton (the Partners) for park and harbour master planning initiatives, business planning, and in other strategy documents. It will help the Partners understand more clearly what the future demand and supply requirements are in terms of marina facilities to meet the recreational boating demand of Halton. Many areas of Halton are identified as “Urban Growth Centres” by the Province of Ontario and there is a belief that the current harbour capacity will not keep pace with the forecasted population growth in the area and demand for such facilities. As both Burlington and Oakville are lakefront communities, and Halton has invested significant funding into a Regional Waterfront Parks program, boating/sailing is considered synonymous with Halton. Fiscally viable and sustainable harbours and recreational boating, along with a vibrant waterfront within Halton is important from a quality of life perspective and aligns with the community values of many residents. 1.1 Study Approach In order to complete a detailed assessment of the current and future need for recreational boating facilities in Halton, the following steps were undertaken:

• Conducted a site visit to each of the boating facilities (i.e. marinas, yacht and boat clubs within Halton) to assess the current product offering.

• Contacted a representative of each of the facilities to obtain information on the number and size

of slips, facilities and services offered, fees charged and user patterns.

• Conducted a site visit to each of the marinas, yacht and boats clubs from the Scarborough Bluffs Sailing Club in the east to St. Catharines Marina in the west.

• Conducted in person or telephone interviews with the owner/operators/commodores of each of

the facilities within the GTA/Golden Horseshoe area to obtain information on the number and size of slips, facilities and services offered, fees charged and user patterns.

• Conducted telephone interviews with power and sail boat builders/manufacturers in Canada and

the United States to obtain data on the current and future length, beam, and draft of boats sold and registered in Ontario, New York, and Michigan, and any forecasts for growth in boating.

• Contacted Transport Canada for information regarding the number of licensed pleasure craft in

Ontario and the rest of Canada.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 2

• Contacted the National Marine Manufacturers Association regarding the number of recreational boats in Canada and the United States.

• Contacted each of the municipalities and conservation authorities within the GTA/Golden Horseshoe area regarding planned or rumoured new marina facilities.

• Met with the Association of Oakville Harbours’ Stakeholders regarding local boater input and their

2012 Rates and Fees Study. Throughout the study process the consultants met with representatives from the Town of Oakville Parks and Open Space, City of Burlington Parks and Recreation Department (along with LaSalle Park Marina Association representation) and Region of Halton, Planning Services. Special thanks is extended to the of Commodores of each of the Yacht and Boat Clubs in Oakville and Burlington and the Marina Managers/Presidents in Oakville, Bronte and Burlington for their unending provision of data and information for this study. 1.3 Report Format The report is divided into six sections or chapters. Section 2 describes and maps the existing boating facilities within Halton. Section 3 provides a profile of power and sail boaters in Ontario and population and boating activity projections for the period between 2013 and 2031. The historical and projected number, length, beam, and draft of boats in Halton’s seasonal and transient market are detailed in Section 4. The level of demand for seasonal and transient slips and launch ramps is described in Section 5. Section 6 provides an indication of the steps necessary to ensure that future recreational boating needs are met to the extent possible; the approach required to meet the future demand; and the result of a strengths, weaknesses, opportunities and threats analysis. Figures and tables are inserted in the text of the report as close to the first reference as practical. Detailed EXHIBITS are included in the appendix in the order in which they are referred.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 3

SECTION 2 – EXISTING RECREATIONAL BOATING FACILITIES IN HALTON REGION 2.0 Boating Facilities There are four marinas, three yacht clubs, one power boat club, and four boating clubs (providing opportunities for canoe, kayak, sailing, catamaran, outrigger canoe, and stand up paddle boards). In addition, the 25 hectare reservoir at Kelso Conservation Area (Milton), 202 hectare lake at Mountsberg Conservation Area (Milton) and 26 hectare Fairy Lake at Prospect Park (Acton-Halton Hills) all in the northern part of Halton provide launch ramps and the opportunity to use small aluminum boats, canoes, kayaks, paddle boats and stand up paddle boards. Each of these facilities is listed in Table 1 below and shown in Figures 1 to 4 following. Table 1 - Boating Facilities in Halton

Facility Location Boating Activity Marina Oakville Harbours Marina - Oakville Harbour

Lakeshore Road East Sail boats, power boats

Oakville Harbours Marina - Bronte Harbour

2508 Lakeshore Road West Sail boats, power boats

Bronte Outer Harbour Marina 2340 Ontario Street, Bronte Sail boats, power boats, Halton Police Marine Unit

LaSalle Park Marina 831 LaSalle Park Road, Burlington Sail boats, power boats Yacht Club Oakville Club 56 Water Street, Oakville Sail boats, kayaks, stand up paddle

boards Oakville Yacht Squadron 146 Lakeshore Road West, Oakville Sail boats Bronte Harbour Yacht Club 2514 Lakeshore Road West, Bronte Sail boats, power boat, dinghies Power Boat Club Oakville Power Boat Club 150 Water Street, Oakville Power boats Boating Club Burloak Canoe Club 160 Water Street, Oakville Canoes, kayaks, war canoes, dragon

boats Burlington Sailing and Boating Club 841 LaSalle Park Road, Burlington Dinghies, keel boats, power boats Burlington Beach Catamaran Club Lakeshore Road, Burlington Catamarans Wai Nui O Kanaka Outrigger Canoe Club 2479 Hixon Street, Oakville Outrigger canoes, stand up paddle

boards Conservation Area and Park Kelso Conservation Area 5234 Kelso Road, Milton Canoes, kayaks, paddle boats, stand up

paddle boards, small aluminum boats (motorized boats prohibited)

Mountsberg Conservation Area 2259 Milburough Line, Campbellville (Milton)

Canoes, kayaks, paddle boats, stand up paddle boards, small aluminum boats (powered by electric trolling motors permitted, gas powered motor prohibited )

Fairy Lake, Prospect Park 30 Park Avenue, Acton (Halton Hills) Canoes, kayaks, stand up paddle boards, small aluminum boats (powered by electric trolling motors permitted, gas powered motor prohibited)

Coronation Park 1426 Lakeshore Road West, Oakville Canoes, kayaks, paddle boats, stand up paddle boards, small aluminum boats

Burloak Waterfront Park 5420 Lakeshore Road East, Burlington Canoes, kayaks, paddle boats, stand up paddle boards, small aluminum boats

2.1 Amenities and Services The four marinas, three yacht clubs and one power boat club have 1,344 slips and moorings, of which 137 are mediterranean bow in moorings1 (i.e. Oakville Club 43, Oakville Yacht Squadron 76, Bronte Harbour Yacht Club 18). Of the 1,344 slips available in Halton only 34 are transient and none of these

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 4

Figure 1 - LaSalle Park Marina

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 5

Figure 2 - Oakville Harbour

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 6

Figure 3 - Bronte Harbour

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 7

Figure 4 - Halton Region Facilities

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 8

are at the Oakville or Bronte Harbour Marinas. All but 10 are available at the Bronte Outer Harbour Marina. 446 of the slips are less than 30 feet; 592, 30 feet to less than 36 feet; 271, 36 feet to less than 46 feet; and 35, 46 feet and over (EXHIBIT 1A). Only Bronte Outer Harbour Marina and Bronte Harbour have permanent lift facilities; cranes are brought in in the spring and fall for the launch and haulout at the other six facilities. Bronte Harbour offers repairs through a marine shop operated by an independent owner. The facility is leased from the Town of Oakville. Only two of the eight facilities provide a fuel dock (i.e. Oakville Power Boat Club, Bronte Outer Harbour Marina) and only the fuel dock at Bronte Outer Harbour Marina is available to both power and sail boats as only boats that clear the bridges’ (32 foot clearance) can make it to the Oakville Power Boat’s fuel dock. There are four launch ramps; one in Oakville Harbour, one in Bronte Harbour, and two at the LaSalle Park Marina in Burlington. The five launch ramps at Kelso and Mountsberg Conservation Areas, Fairy Lake, and Coronation Park are only suitable for canoes, kayaks and small boats as there are either physical or other operational restrictions on the use of motorized boats at these locations (Figure 4). There is potential for a launch ramp at Burloak Waterfront Park suitable for canoes, kayaks and small boats. A master plan review of the park is currently underway. Oakville Power Boat Club, Bronte Outer Harbour Marina, Oakville Harbour Marina, and LaSalle Park Marina (shared with BSBC) offer the only pump out services in Halton. Just over half of the slips (i.e. 687) have access to 30 or more amp. power pedestals. Only 71 percent or 928 of the 1,310 seasonal boats at the eight facilities can be accommodated on-site for winter storage. Another 40 could be accommodated within Oakville Harbours Marina if the abandoned boats were removed (EXHIBIT 1B). 2.2 Seasonal and Transient Slip Users During the 2013 boating season 96.8 percent of the 1,310 seasonal slips were occupied. Anything over 95 percent is considered full occupancy by industry standards. Some slips were not occupied in 2013 due to spring storm damage to the marina infrastructure at LaSalle Park Marina and wet moorings required for the pilot dredging project in Bronte Harbour. As shown in Figure 5 below, 84.8 percent (1,075) of the seasonal slips at the eight facilities were occupied by residents of Halton, 57.7 percent (732) by residents of Oakville, 22.7 percent (288) by residents of Burlington, and 4.4 percent (55) by residents in the rest of Halton. Sixty percent or 767 of the 1,268 seasonal boats in 2013 were sail boats and 501 power boats (EXHIBIT 1C). There were 470 boats on the waiting lists of the eight facilities with 73 percent looking for a slip 36 feet or more in length. This represents 37.1 percent of the occupied slips in 2013 Despite the low number of transient slips available within Halton, 1,287 boaters visited the area facilities in 2013, staying for an average of 1.5 days. This number of transient visits is primarily due to the reciprocal arrangements at the yacht clubs where visiting boats can use member slips when they are vacant. If transient slips were available within Oakville Harbour and Bronte Harbour we believe this number would be substantially higher. _____ 1 In a Mediterranean mooring, the bow (front) of the boat is tied to a fixed structure (in the case of the harbours, a dock) while the stern (back) is tied off to two floating devices, customarily tires that are themselves anchored to the bottom of the harbour and that are usually deployed only during the boating season. The boat approaches the shoreline at a perpendicular angle, runs two lines to the shore (dock) and another two to the floating moorings. The advantage of Mediterranean mooring is that many more boats can be accommodated along a fixed length of shoreline as there are no finger docks separating the boats. The disadvantage is that embarking and disembarking the boat must be made from the bow of the boat which is not as easy as, and is less stable than using a finger dock alongside.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 9

Figure 5 - Residence of Boat Owners at Seasonal Slips

2.3 Assessment of Infrastructural Features at Boating Facilities The conditions of the existing facilities were reviewed at the three main boating locations within the Region. These locations include LaSalle Park in Burlington, Bronte Harbour and Oakville Harbour. The review was limited to a visual assessment of the facilities and observations of their function and boater use (EXHIBIT 1D and 1E). No surveys, measurements or testing of the structures were undertaken. The review did not include buildings or club houses. Comments with respect to adequacy of fairways are based on a review of aerial photography. A fairway twice the length of a boat using the adjacent dock is considered good and a fairway width of one and one-half of the length of the boat is considered adequate. Water depth requirements depend on boat mix but generally water depths of 1.8 metres are considered adequate for public marinas. Chart datum is taken as reference water level. Comments with respect to stability of docks are based on experiences during site visits and comments received from boaters and may be considered somewhat subjective. Comments regarding launch ramp parking follow published recommendations that suggest 40 car/trailer combination parking spaces are required per launch lane. However, it is recognized that demand for parking varies from location to location and by time of day. Plans of the facilities are provided on the previously noted Figures 1 to 3. The reader should refer to these figures while reading the description in this sub-section of the report. 2.3.1 La Salle Park LaSalle Park provides the base of LaSalle Park Marina and the Burlington Sailing and Boating Club. The facilities are located on or adjacent to the LaSalle Park Pier. The La Salle Park Marina facilities are located on the east side of the pier and include floating docks and a floating breakwater. The docks and the breakwater are removed every fall and reinstated in the spring. The docks and their use are being hampered by excessive wave activity due to a functionally inadequate floating breakwater. Damage to the docks and boats is frequent. The operation of the marina and specifically the provision of proper wave protection for the marina was the subject of a recently completed Class Environmental Assessment (Dillon Consulting Limited, 2013). The Environmental Study Report concludes that a fixed breakwater is the preferred method of resolving the ongoing wave related

57.7% 22.7%

4.4%

15.2%

Oakville Burlington Milton-Halton Hills Outside of Halton Region

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 10

problems. Any comments with respect to the docks are not material until the basin is properly protected. The spacing of the docks and fairway widths are appropriate for the size of the slips. Water depth is greater than required in most of the basin. Approximately 20 percent of the dock area in the north part of the basin has a water depth of less than 1.8 metres at Chart Datum. Boats with shallow draft are assigned to this part of the basin. The park also includes two launch ramps, one located on the east side of the pier and another located on the west side of the pier. The east ramp is used by the public to launch small to moderate size boats transported on trailers behind cars and trucks. The ramp surface accommodates two launching lanes. The slope of the ramp appears to be within an acceptable slope gradient and deep enough to accommodate launching under a typical range of water levels. Fixed piers and extended floating docks are provided on both sides of the ramp. Segregated parking for the launch ramp is not provided. The west ramp is located directly in front (south) of the Burlington Sailing and Boating Club (BSBC). Although not dedicated for exclusive use of the club, it is not readily accessible from the public parking lot. It is a single lane structure. The launch ramp had a number of problems including rough surfaces and inadequate depth in the past and is presently under re-construction. It is re-designed to operate under the full range of water levels experienced during a typical boating season. The launch ramp is flanked with floating docks installed by BSBC in the spring and removed in the fall. 2.3.2 Bronte Harbour The Bronte Harbour area includes two distinct boating facilities. The Bronte Outer Harbour Marina is located east of the mouth of the Bronte Creek and is a privately operated facility under a long term lease from the Region. The boating facilities within the mouth of the creek include the municipal facilities operating as Oakville Harbour Marina and the Bronte Harbour Yacht Club. The Bronte Outer Harbour Marina is the most recently constructed boating facility on the Halton waterfront. The facility has floating docks. They appear to be stable and well secured. Access to the docks is controlled with security gates. The shore treatments are in good condition. There appears to be no physical deficiencies in these facilities. Reports of excessive wave penetration into the basin under southwest wind conditions were provided by boaters. The docking facilities along the river within the Oakville Harbour Marina are generally arranged directly off the shore walls of the creek with three additional main docks extending into the creek beyond the shore connected docks. Two of the three additional main docks have fingers attached. The third main dock supports boats docked bow-in with stern float anchors. The stability of the main docks and main docks with fingers is considered to be adequate. The stability of the finger docks attached directly to the shore walls is considered poor. The width of fairways varies in various parts of the harbour from adequate to inadequate. There are parts of the harbour where fairways are just equal to the length of boats docked in the area. The seawalls are constructed of various materials but most commonly of concrete blocks or steel sheet piles. The concrete block walls appear to be functional. The walls do not show excessive settlement or lean. The backshore, which is mostly made up of interlocking pavement surfaces or boardwalk also does not show an excessive amount of settlement or movement. This is considered important given that the soils around the harbour are very soft sediments with organic content. There are two launch ramps within the river channel. A public launch ramp is located on the south side of the river and specific car/trailer parking is provided adjacent to the ramp. The launch ramp has two lanes. There are nine parking spots provided which is considered substandard for the launch ramp. Public parking related to the park is available and is configured in such a way that it can be used as overflow for the launch ramp. The ramp surface appears relatively steep but not excessively so. We observed no docks available to assist in launching. A second set of launch ramps are available in the Bronte Harbour Yacht Club compound. These are single lane launch ramps and are separated by a mast crane slip. These launch ramps appear to be available for the use of the club members only.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 11

The water depth within the mooring area of the river varies. Oakville undertakes regular dredging operations and dredges the river to 2 m below Chart Datum regularly. The interval between dredging operations is approximately seven years, but may vary. The water depth in the mooring areas will gradually decrease after dredging and the operations will become hindered by reduced water depth over time. Oakville experimented with ongoing dredging operations using a small suction dredge and filtering the dredged material through geotextile bags. The results of the experimental operation are not known at this time. Oakville is also undertaking a sediment management study at Bronte Harbour at present time to better understand the sources of sediment and deposition process in the harbour. 2.3.3 Oakville Harbour Six marinas and boat clubs operate within the river mouth of Sixteen Mile Creek. These include Oakville Harbour Marina – Oakville Harbour, Oakville Yacht Squadron, Oakville Club, Wai Nui O Kanaka Outrigger Canoe Club, Oakville Power Boat Club and the Burloak Canoe Club. Given the multiple operations, the descriptions are provided on club/marina basis. The entrance to Oakville Harbour is formed with two breakwaters. The west breakwater is a steel sheet pile pier with a concrete cap. At the north end of the west breakwater is a short armour stone groyne which extends approximately 30 m into the entrance channel. The armour stone groyne breaks waves that propagate up the entrance channel. The east breakwater is formed by a SSP pier with a concrete cap. Repairs to the east breakwater were carried out in 2012. The Town of Oakville Water Air Rescue Force (TOWARF) is at the north end of the east breakwater. The shore along TOWARF is protected with rip rap and armour stone. Two slips used by TOWARF are located along this section of the shore. The TOWARF facility was not included in the review. The water depth within the mooring areas of Sixteen Mile Creek varies. Oakville regularly dredges the creek to 2 m below Chart Datum. The interval between dredging operations is typically ten years, but may vary. The water depth in the mooring areas will gradually decrease after dredging and the operations will become hindered by reduced water depth over time. Oakville last dredged Sixteen Mile Creek in the fall/winter of 2010. 2.3.4 Oakville Harbour Marina - Oakville Harbour Oakville Harbour Marina operations within Sixteen Mile Creek include three locations. There are operations within the Oyster Bay area near the mouth of the creek, operations within the central part of the harbour south of the Lakeshore Bridge to Randall Street bridge and docking facilities in the uppermost part of the harbour. Each of these locations is described separately. Oyster Bay is the embayment along the west side of the river north of Tannery Park and south of Oakville Yacht Squadron (OYS). Oyster Bay’s shore is protected with a pre-cast concrete block wall and armour stone wall. Oakville is now reconstructing the shoreline protection within Oyster Bay. The pre-cast concrete block wall is being replaced with a boulder berm and armour stone wall. The Oakville Harbour Marina docks within Oyster Bay are floating docks configured in a standard main dock/finger dock arrangement. They extend north from the south shore. The docks are adequate with respect to their width and stability. The width of the fairways within this area varies depending on the position along the dock. They are adequate on the river channel side in some areas and inadequate or substandard in most other areas. Fairways just marginally greater than the length of the boats were noted. The central part of the Oakville Harbour Marina operations includes both sides of the river south of the Randall Street bridge to OYS (Shipyard Park) on the west side and to Oakville Club on the east side. It also includes a launch ramp at the south end of Shipyard Park. The launch ramp is in poor condition and Oakville is in the process of redesigning the ramp as part of their Oakville Harbour West Master Plan redevelopment.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 12

The west shore north of the launch ramp is protected with a concrete block wall constructed in the 1990’s. The block wall extends along the shore of Shipyard Park and ends at the north side of Shipyard Lagoon. The wall appears to be in good condition. The shore north of Shipyard Lagoon is protected with an anchored SSP wall that was constructed in 2011. The north portion of the SSP wall under the bridge is protected with an armour stone wall constructed in 2011. North of the armour stone wall, the west shore is natural with no formal structures. Boats along the west shore mostly tie off bow-in along the shore with stern floating anchors. This same arrangement is used within the Shipyard Lagoon. The only exception to this is the shore under and within approximately 25 meters of the Lakeshore Road bridge. Here the docking is provided along a shore parallel floating dock tied off to shore anchor piles. Large boats dock parallel to the dock. The fairways within this part of the river are adequate except at the mouth of the Shipyard Lagoon. The east side of the river, north of the Oakville Club to the south side of the launch ramp near the Randall Street Bridge, is protected with a pre-cast concrete block wall similar in construction to the wall in Shipyard Park. The wall appears to be in good condition. Floating finger docks are secured to the wall and boats tie off to the finger docks. Boats dock either bow or stern-in. The stability of the finger docks is judged to be marginal. North of the Burloak Canoe Club, along the upper reach of the harbour, boats dock along both sides of a shore parallel floating dock. The larger boats dock along the creek side. One shore connection is centrally located along the dock. A set of stairs leads from the shore wall to the northeast corner of the public parking lot off Water Street. The stairs are gated. The dock appears adequate for its width and stability. The fairways are adequate. 2.3.5 Oakville Yacht Squadron The Oakville Yacht Squadron (OYS) is located north of Oyster Bay. The shoreline is protected with a pre-cast concrete block wall and steel sheet pile (SSP) walls. The pre-cast concrete block wall extends along short sections of the north shore of Oyster Bay. The concrete wall appears to be in good condition. The steel sheet pile wall that runs along the south side of the OYS building is poor condition. A mast crane is located near the east end of the wall. The steel sheet pile wall along the east of the OYS site was reconstructed in 2011. It is in good shape and supports a public boardwalk located along the east side of the OYS site. The new wall ends at the public launch ramp at the south end of Shipyard Park. There are two main docks that extend south from the OYS site into Oyster Bay. The boats docks bow-in with stern anchors in a very tight configuration. There are no finger docks. The main docks are stable and width is considered adequate but the use is hindered by the bow of some boats extending over the dock. Boats also dock bow-in along the new wall on the east side of the site. Stern anchors are used to tie-off the boats from the wall. 2.3.6 The Oakville Club The shore along The Oakville Club (OC) from the tennis court to the north side of the building is protected with a SSP wall. The wall is covered with a timber deck. Steel rings are attached either to the cap of the SSP wall or to the timber deck. Boats tie off to the steel rings secured to the SSP wall and deck. Short finger docks supported off the deck provide access to the boats. The wall is rusted and sections of the wall are leaning toward the lake. The shore north of the OC building is protected with a gabion basket wall. The gabion basket wall is covered by a timber deck. Short finger docks supported from the timber deck and gabion baskets provide access to the boats moored along the shore. All boats are docked bow into the shore with stern floating anchors. The fairway, or the open channel of the river, is of appropriate width.

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 13

2.3.7 Wai Nui O Kanaka Outrigger Canoe Club A steel sheet pile wall extends along the south and north sides of the launch ramp adjacent to the Randall Street bridge, under the bridge and a short distance into the Power Boat Club basin. The wall is heavily rusted at the water line. The Wai Nui O Kanaka Outrigger Canoe Club uses this area and the launch ramp. There appears to be no docks used by the club. The launch ramp surface accommodates one launching lane. The slope of the ramp appears to be within an acceptable slope gradient and deep enough to accommodate launching of the Canoe Club boats. 2.3.8 Oakville Power Boat Club There are two distinct parts to the Oakville Power Boat Club facilities. A basin is located directly north of the Randall Street bridge and additional docking is provided along the east side of the river. Descriptions are provided below for these two parts. The shore along the south side of the Power Boat Club basin is protected with a rip rap revetment. The east and north shore of the basin is protected with a stone filled timber crib. The timbers are round and the stone fill is visible in the gaps. A timber deck extends along the top of the crib. The deck is uneven. Vertical steel piles are intermittently driven in front of the crib. They may be used to support the deck. Some of the vertical piles are leaning into the basin. Overall, these structures are in very poor condition and their stability is uncertain. Finger docks supported on steel tube piles are located along the east and west sides of the basin. A floating main dock with fingers extends south from the north shore of the basin. Boats dock along shore-parallel floating docks on the south shore. The stability of the main and finger docks is unknown. The fairway width in the basin varies from inadequate to adequate. The north side of the entrance to the basin and the east shore of the creek north of the entrance are protected with gabion baskets. The baskets are broken and they have lost their stone fill. A timber deck supported on steel tube piles covers the gabion baskets along this shoreline. The portions of the structure reviewed are considered to be in poor condition. Finger docks supported on steel tube piles and channels extend from the deck into the creek. The docks are narrow but appear to be stable. The docks are constructed using various types and sizes of materials and do not appear to be designed to a uniform appearance and standard. Fuel can be purchased at the Power Boat Club. The fuel dock is supported on steel tube piles. A gas pump and a store are located on shore. Boats can moor along either side of the fuel dock. The dock appears narrow and stable. 2.3.9 Burloak Canoe Club The Burloak Canoe Club is located north of the Power Boat Club. A shore parallel dock, supported on steel tube piles, extends north along the east shore of the creek. Boats are moored along the dock and the dock appears stable. The fairway, or open channel of the river, is adequate. 2.4 Other Boating Facilities in Halton In addition to the marinas and yacht clubs, Halton is also home to four boating clubs (Burloak Canoe Club, Burlington Sailing and Boating Club, Burlington Beach Catamaran Club, Wai Nui O Kanata Outrigger Canoe Club) catering to non-motorized boating activities. The four clubs offer opportunities for participation with canoes, outrigger canoes, kayaks, war canoes, dragon boats, dinghies, keel boats, paddle boats and stand up paddle boards (EXHIBIT 2). All of these boating facilities report an increase in the number of programs offered and participants in these programs in 2013. The programs are offered to both children and adults. The Burlington Sailing and Boating Club and Wai Nui O Kanata Outrigger Canoe Club also offer programs for the disabled. The Oakville Club, Oakville Yacht Squadron and Bronte

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 14

Harbour Yacht Club offer junior and adult sailing schools for their members, and indicate that the numbers of participants in their sailing programs are also growing. The Oakville Yacht Squadron and Bronte Harbour Yacht Club also offer sailing lessons to the general public. The Bronte Harbour Yacht Club also offers a one week blind sailing program each summer. Kelso Conservation Area, Mountsberg Conservation Area and Fairy Lake in the northern part of Halton and Burloak Waterfront Park offer an opportunity for use of canoes, kayaks, paddle boats, stand up paddle boards, and small aluminum boats. Motorized boats are prohibited at Kelso, but boats with electric trolling motors are permitted at Mountsberg and Fairy Lake. There are no restrictions on motorized boats at Burloak Waterfront Park but physical barriers exist that limit access to the lakeshore. Mountsberg Reservoir caters mostly to fishermen than to the other forms of boating and sees as many as 200 boats involved in fishing on a good day. As a result of the tree stumps and occasional low water levels, stand up paddle boards are not encouraged at Mountsberg. Fairy Lake is also used more by fishermen than other forms of boating. The Town of Halton Hills does not monitor the level of use on the Lake; as a result there are no data available regarding the different activity uses. Kelso offers boat rentals from late April to early October for single and double kayaks, canoes, paddle boats, and stand up paddle boards (EXHIBIT 3). 2.5 Comparison of Halton’s Boating Facilities with those of the GTA/Golden Horseshoe Area 2.5.1 Boating Facilities There are 41 boating facilities in the GTA/Golden Horseshoe Area between Scarborough in the east and St. Catharines in the west. Of these 14 are marinas and the remaining 27 are yacht, sailing and cruising clubs. 2.5.2 Amenities and Services The 41 boating facilities offer 9,339 slips or moorings of which 8,833 are seasonal and 506 dedicated as transient or reciprocal slips or moorings. 1,830 of the slips are less than 30 feet; 4,361, 30 feet to less than 36 feet; 2,077, 36 feet to less than 46 feet; and 800, 46 feet and over (EXHIBIT 4A). Twenty two of the facilities provide a fuel dock. Thirty two have a pump out. There are 29 launch ramps available for use by boats typically 26 feet or less in length (i.e. 7.9 metres). Almost 80 percent (78.6%) of the slips (i.e. 7,130) have access to 30 or more amp. power. More than 85 percent (87.4%) of the 8,709 seasonal boats can be accommodated on-site for winter storage (EXHIBIT 4B). 2.5.3 Seasonal and Transient Slip Users During the 2013 boating season 98.6 percent of the 8,833 seasonal slips were occupied. The remaining slips were not occupied due to long-term maintenance repairs and unsuitable lengths for the boats requiring a slip. Seasonal boats were almost evenly split between power (50.9%) and sail (49.1%). There were 1,450 boats on the waiting lists of the 41 facilities with 22 percent looking for a slip 46 feet or more in length (EXHIBIT 4C). This represents an additional 16.4 percent of needed supply. 2.5.4 Facilities in Halton Compared with the GTA/Golden Horseshoe Area As shown in Table 2 following, although the occupancy rates and percentage of slips by length are similar, boaters at marinas and yacht clubs in Halton appear to be less well served than those in GTA/Golden Horseshoe area. As a percentage of total slips available, the GTA/Golden Horseshoe area offers twice as many transient slips as Halton and as a percentage of facilities, twice as many fuel docks. Although a higher percentage of facilities in the GTA/Golden Horseshoe area offer a pump out service, the number of slips per pump out is similar (i.e. 292 versus 336 in Halton). Both areas have insufficient

Recreational Boating Feasibility and Capacity Study – Phase 1 Final Report June 2014

TOURISTICS + Shoreplan Engineering Limited 15

on-site capacity to accommodate all the seasonal boats for winter storage (i.e. 70.8% in Halton versus 87.4% in the GTA). The demand for additional slips is much higher in Halton than the GTA as expressed by the number of boats on the waiting list as a percentage of occupied seasonal slips (i.e. 37.1% in Halton versus 16.9% in the GTA/Golden Horseshoe area). Table 2 - Boating Facilities in Halton Compared to the GTA/Golden Horseshoe Area Halton GTA/Golden Horseshoe Area Number of Marinas, Yacht, Sailing and Power Boat Clubs

8 41

Seasonal Slips Occupied 1,310 96.8% 8,833 98.6% Transient Slips as Percentage of Total Slips

2.5% 5.4%

Percentage of Slips <30 feet 33.2% 20.2% Percentage of Slips 30 feet to <36 feet 44.0% 48.1% Percentage of Slips 36 feet to <46 feet 20.2% 22.9% Percentage of Slips 46 feet and over 2.6% 8.8% Percentage of Facilities with Fuel Docks 25% 53.7% Number of Slips Per Fuel Dock 672 424 Percentage of Facilities with Pump Out 50% 78.0% Number of Slips Per Pump Out 336 292 Percentage of Facilities with Launch Ramp

37.5% 53.6%

Percentage of Slips with 30 amp or more power

51.5% 78.6%

Percentage of Seasonal Boats Accommodated On-site for Winter Storage

70.8% 87.4%

Number of Boats on Waiting List 470 1,470 Boats on Waiting List as a Percentage of Occupied Seasonal Slips

37.1% 16.9%