i fondi di investimento a lussemburgo la direttiva … · i fondi di investimento a lussemburgo la...

TRANSCRIPT

I FONDI DI INVESTIMENTO A LUSSEMBURGO La direttiva AIFM Moderatore: Charles Muller

Partner, KPMG Luxembourg S.à r. l. Relatori: Gilles Dusemon

Partner, Arendt & Medernach

Jacques Linon Partner, Deloitte Tax & Consulting S.à r. l.

Serge d’Orazio Head of Investment Funds & Global Custody, KBL European Private Bankers Carmen von Nell-Breuning Associate Director, Ernst & Young S.A.

Enrico Turchi Managing Director, Pioneer Asset Management S.A.

INTRODUCTION AND BACKGROUND

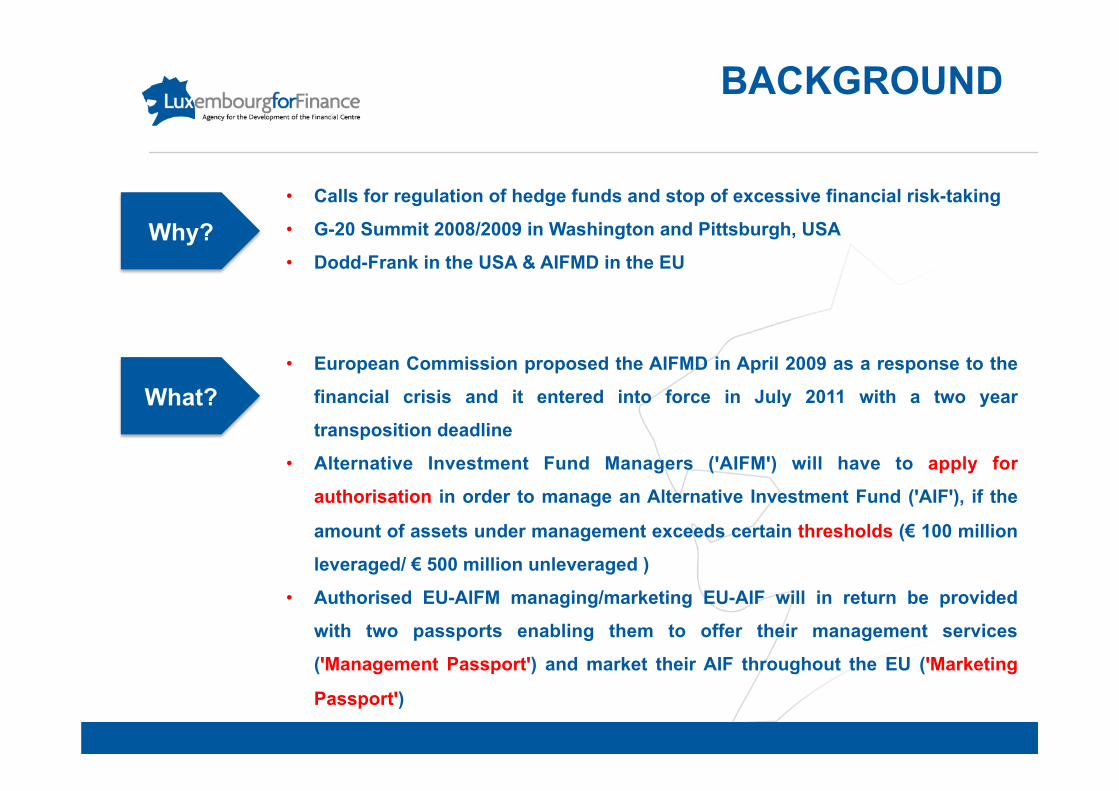

• Calls for regulation of hedge funds and stop of excessive financial risk-taking

• G-20 Summit 2008/2009 in Washington and Pittsburgh, USA

• Dodd-Frank in the USA & AIFMD in the EU

• European Commission proposed the AIFMD in April 2009 as a response to the

financial crisis and it entered into force in July 2011 with a two year

transposition deadline

• Alternative Investment Fund Managers (ꞌAIFMꞌ) will have to apply for

authorisation in order to manage an Alternative Investment Fund (ꞌAIFꞌ), if the

amount of assets under management exceeds certain thresholds (€ 100 million

leveraged/ € 500 million unleveraged )

• Authorised EU-AIFM managing/marketing EU-AIF will in return be provided

with two passports enabling them to offer their management services

(ꞌManagement Passportꞌ) and market their AIF throughout the EU (ꞌMarketing

Passportꞌ)

BACKGROUND

Why?

What?

• Any UCI other than UCITS

• which raises capital from a number of investors

• with a view to investing it in accordance with a defined investment

policy for the benefit of those investors

• Legal person whose regular business is managing one or more AIFs

• An entity performing either portfolio management and/or risk

management is considered as ‘managing an AIF’

• In addition, an AIFM may also perform other functions such as

administration, marketing or activities related to the assets of AIF

• UCITS management companies can obtain an additional AIFM licence

• ꞌExternal AIFMꞌ = legal person appointed by or on behalf of the AIF

• ꞌSelf-managed AIFMꞌ = where the corporate legal form allows it

DEFINITIONS

AIF

AIFM

• direct or indirect offering or placement

• at the initiative of the AIFM or on behalf of the AIFM

• of units or shares of an AIF it manages

• to investors domiciled or with a registered office in the Union

• Passive marketing

• Marketing to retail investors

National Law

AIFMD

MARKETING

COVERED

NOT COVERED

5

TIMELINE AND TRANSITIONAL MEASURES

7

2015

Review of co existing PPM regime

Entry into force

non-EU AIFM / (non)-EU AIF Passport in return for full compliance with AIFMD rules

Transposition

2011

2012

2013

2014

2016

2010

2017

2018

ESMA recommendations

EU AIFM / EU AIF Passport AIFM to adapt to the Directive between 2013 and 2014

non-EU AIFM / (non-)EU AIF Private Placement if transparency provisions and cooperation arrangements are complied with

non-EU EU

End of national private placement regimes

ESMA recommandations 24 August 2012:

Bill passed to Luxembourg Parliament including transposition of AIFMD

March 2013: Voting of the law

7

HOW TO STRUCTURE YOUR OPERATIONS?

STRUCTURING CHALLENGES

• Delegation – letter-box rule: • AIFM Passport:

9

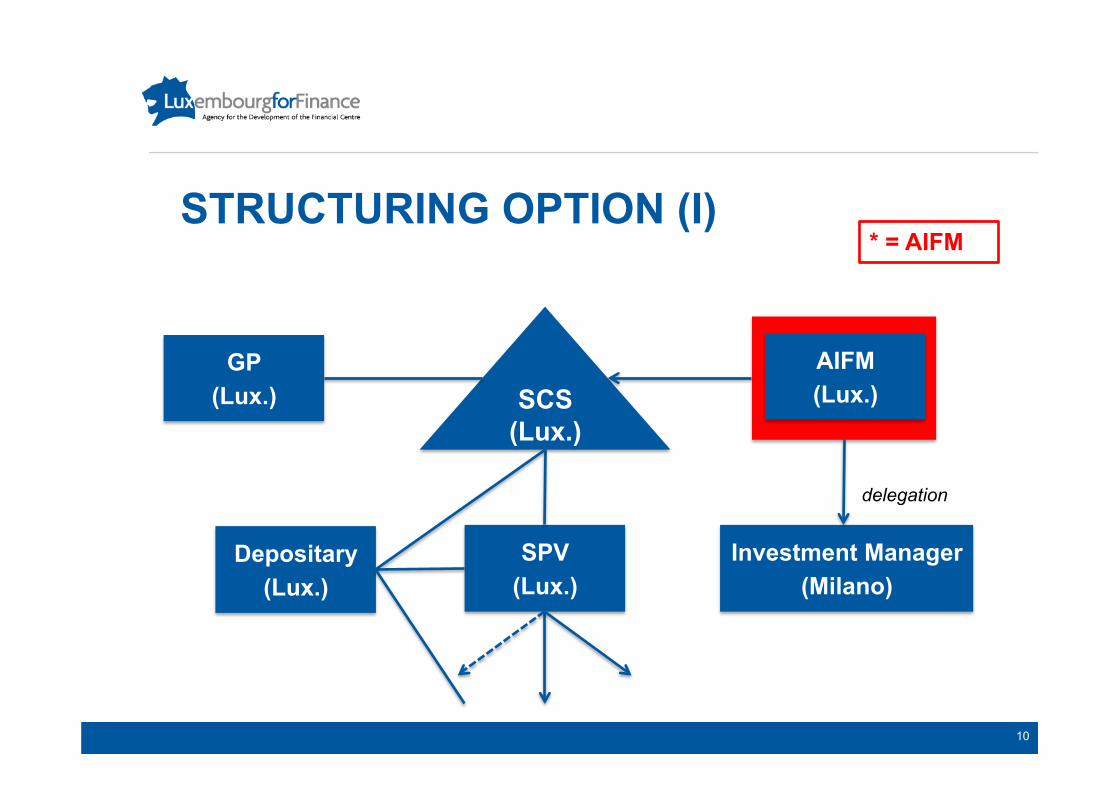

STRUCTURING OPTION (I)

delegation

Investment Manager (Milano)

GP (Lux.)

* = AIFM

SCS (Lux.)

AIFM (Lux.)

Depositary (Lux.)

SPV (Lux.)

10

STRUCTURING OPTION (II)

GP (Lux.)

* = AIFM

SCS (Lux.)

AIFM (Lux.)

Depositary (Lux.)

SPV (Lux.)

Branch (Milano)

11

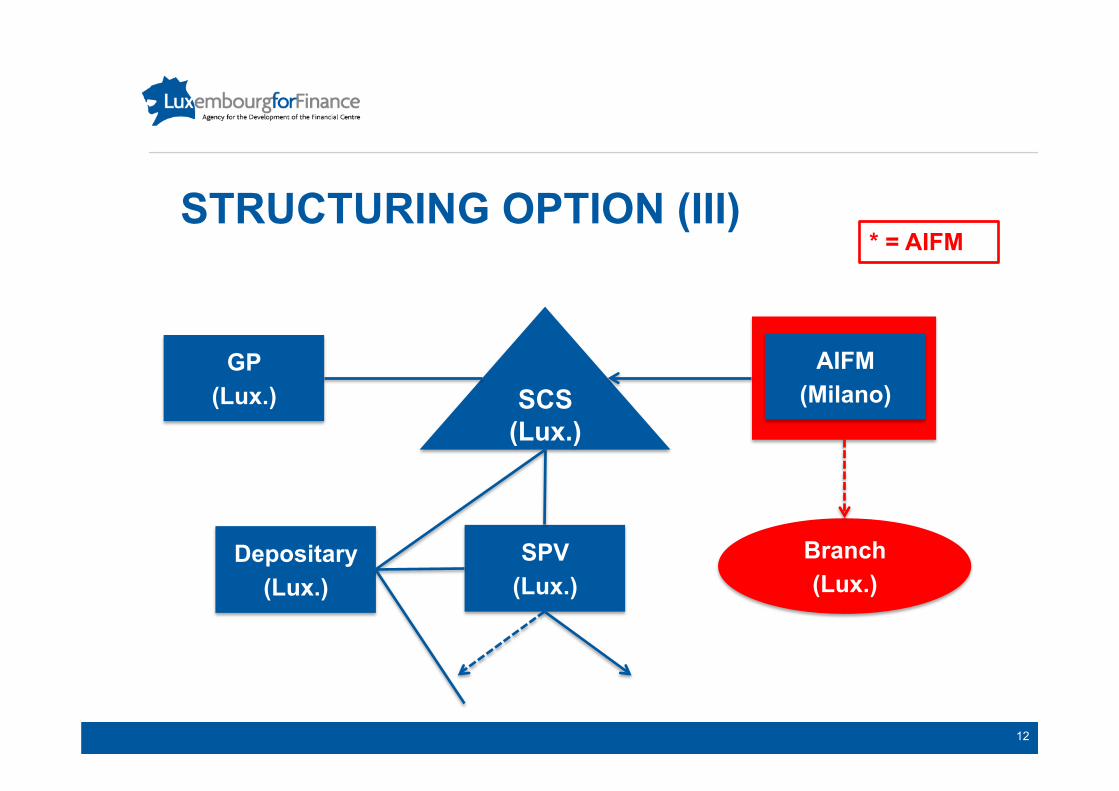

STRUCTURING OPTION (III)

GP (Lux.)

* = AIFM

SCS (Lux.)

AIFM (Milano)

Depositary (Lux.)

SPV (Lux.)

Branch (Lux.)

12

AIFMD TAX IMPACTS

SPECIFIC TAX PROVISIONS OF LUXEMBOURG DRAFT LAW IMPLEMENTING AIFMD

• Introduction of new Luxembourg special partnership and carried interest

regime for new Luxembourg residents

• Tax residence of AIFs: AIFs established outside Luxembourg treated as non residents for Luxembourg tax purposes even if AIF Manager is established in Luxembourg (ensure removal of any tax obstacle for Luxembourg AIF Managers managing foreign AIF from Luxembourg / same provision as for UCITS IV Directive)

• Application of the existing VAT exemption to management fees paid by AIFs to AIF managers

14

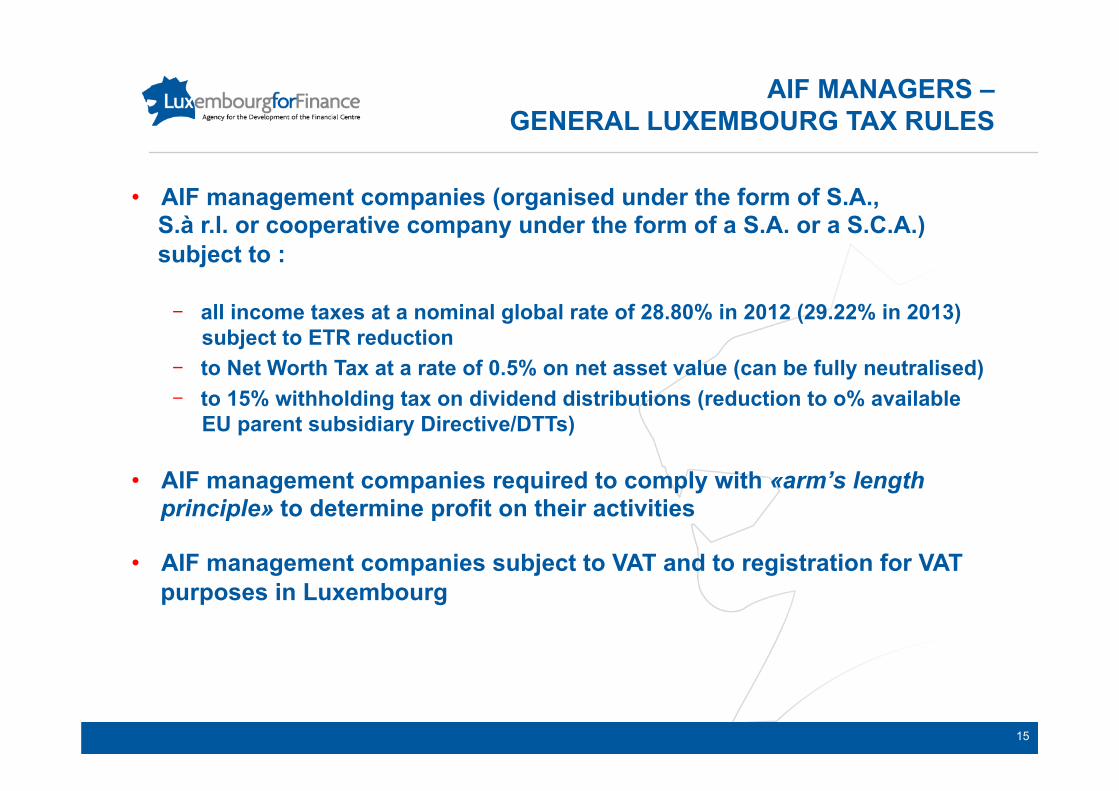

AIF MANAGERS – GENERAL LUXEMBOURG TAX RULES

• AIF management companies (organised under the form of S.A., S.à r.l. or cooperative company under the form of a S.A. or a S.C.A.) subject to :

- all income taxes at a nominal global rate of 28.80% in 2012 (29.22% in 2013) subject to ETR reduction

- to Net Worth Tax at a rate of 0.5% on net asset value (can be fully neutralised) - to 15% withholding tax on dividend distributions (reduction to o% available

EU parent subsidiary Directive/DTTs) • AIF management companies required to comply with «arm’s length

principle» to determine profit on their activities

• AIF management companies subject to VAT and to registration for VAT purposes in Luxembourg

15

Reorganisations of

AIF Managers Business model and related new costs & general expenses impacts the income tax position

Transfer pricing impacts linked to redefinition of AIF Managers roles and functions within delegation rules

Need to achieve tax neutrality in legal transformation process (mergers, transfer of seat ,…)

VAT impacts of reorganization of roles & functions and on delegation to be considered

Tax residency & beneficial ownership in connection with defined operationality

AIF MANAGERS – REORGANISATIONS TAX IMPLICATIONS TO BE MONITORED

Branch model vs. subsidiaries entities model

16

AIF MANAGEMENT COMPANIES – VAT ASPECTS

• Application of the existing VAT exemption to management fees paid by AIFs to AIF managers

• Luxembourg vehicles already in scope: UCITs, SIFs, SICARs, ASSEPs, SEPCAVs, pensions funds and securitisation vehicles under 2004 law

• Luxembourg draft law expands the scope of VAT exemption to similar investment vehicles located in other EU member states (VAT treatment in the recipient country still to monitor)

17

AIFS – LUXEMBOURG ATTRACTION

• Luxembourg AIFs: mainly Part II UCIs, SIFs, SICARs and SOPARFI’s with their diversified tax features

− à a valuable toolkit now complemented by the new SCS tax transparent regime

• Tax implications at the level of AIFs investments in particular - Benefit of existing exemptions or reduced WHT rates or beneficial tax regimes in

investment countries - Access of AIFs to Double Tax Treaties and EU Directives to be considered - Need for structuring to be valuated - Impact of Tax transparency

• Tax implications at the level of AIFs investors to be considered

− Exemption /non exemption/CFC rules − Flat rate/marginal rate of taxation − Tax reporting

18

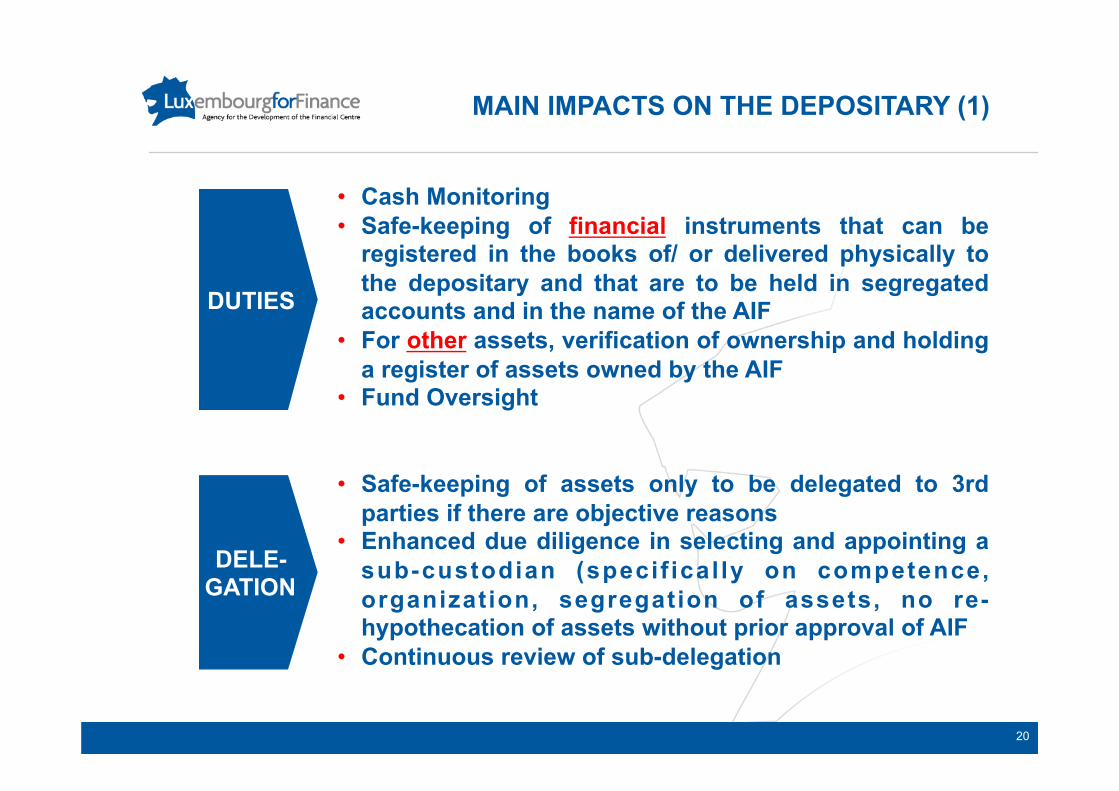

THE ROLE OF THE DEPOSITARY : DUTIES AND LIABILITY

• Cash Monitoring • Safe-keeping of financial instruments that can be

registered in the books of/ or delivered physically to the depositary and that are to be held in segregated accounts and in the name of the AIF

• For other assets, verification of ownership and holding a register of assets owned by the AIF

• Fund Oversight

• Safe-keeping of assets only to be delegated to 3rd parties if there are objective reasons

• Enhanced due diligence in selecting and appointing a sub-custodian (specif ical ly on competence, organization, segregation of assets, no re-hypothecation of assets without prior approval of AIF

• Continuous review of sub-delegation

DUTIES

DELE- GATION

MAIN IMPACTS ON THE DEPOSITARY (1)

20

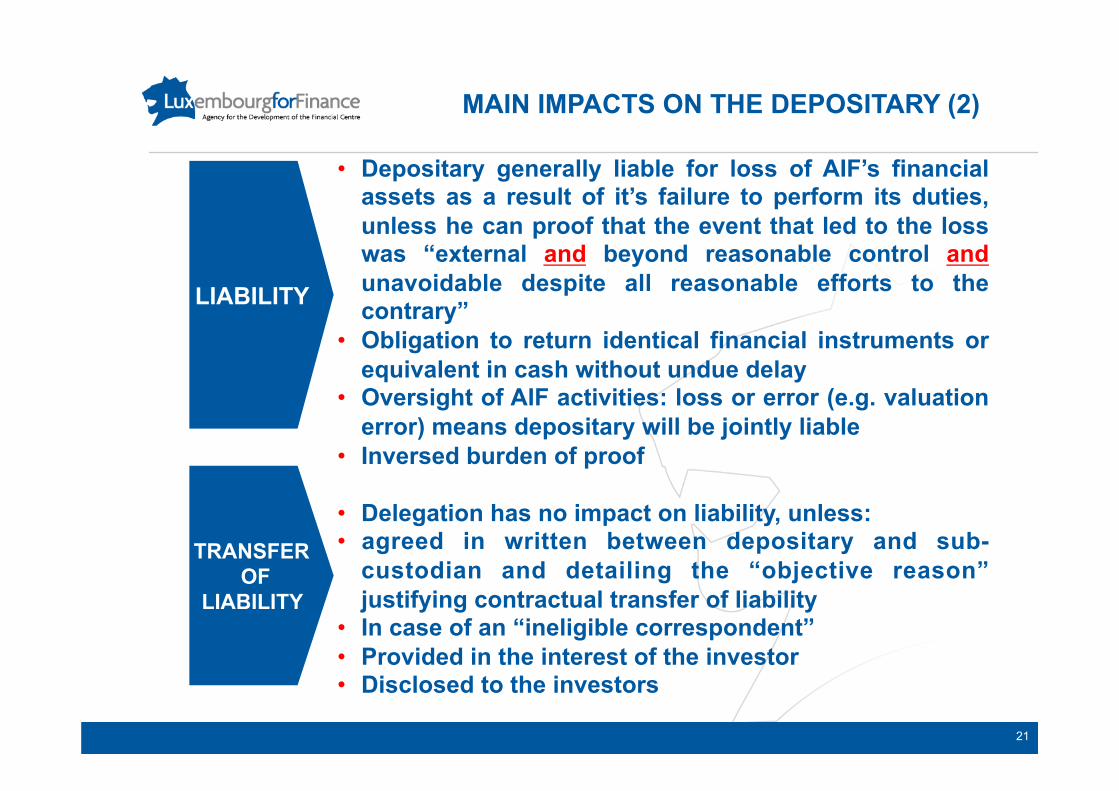

• Depositary generally liable for loss of AIF’s financial assets as a result of it’s failure to perform its duties, unless he can proof that the event that led to the loss was “external and beyond reasonable control and unavoidable despite all reasonable efforts to the contrary”

• Obligation to return identical financial instruments or equivalent in cash without undue delay

• Oversight of AIF activities: loss or error (e.g. valuation error) means depositary will be jointly liable

• Inversed burden of proof

• Delegation has no impact on liability, unless: • agreed in written between depositary and sub-

custodian and detailing the “objective reason” justifying contractual transfer of liability

• In case of an “ineligible correspondent” • Provided in the interest of the investor • Disclosed to the investors

LIABILITY

MAIN IMPACTS ON THE DEPOSITARY (2)

TRANSFER OF

LIABILITY

21

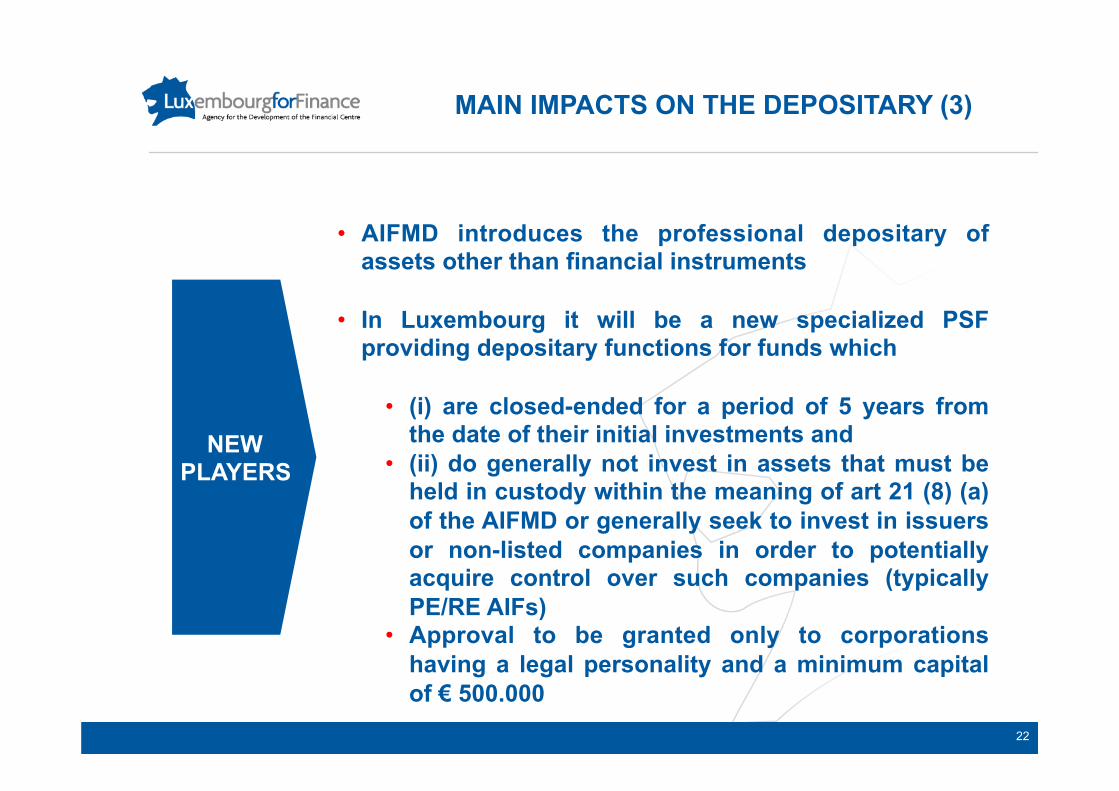

• AIFMD introduces the professional depositary of assets other than financial instruments

• In Luxembourg it will be a new specialized PSF providing depositary functions for funds which

• (i) are closed-ended for a period of 5 years from the date of their initial investments and

• (ii) do generally not invest in assets that must be held in custody within the meaning of art 21 (8) (a) of the AIFMD or generally seek to invest in issuers or non-listed companies in order to potentially acquire control over such companies (typically PE/RE AIFs)

• Approval to be granted only to corporations having a legal personality and a minimum capital of € 500.000

NEW PLAYERS

MAIN IMPACTS ON THE DEPOSITARY (3)

22

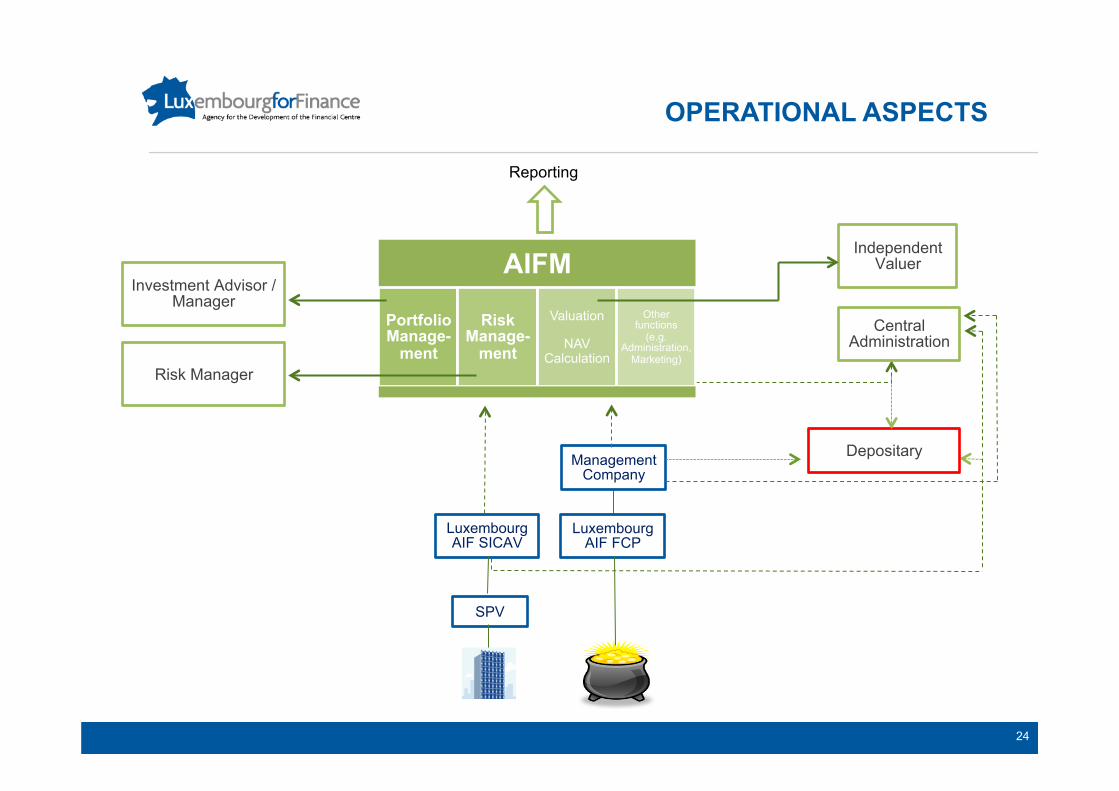

OPERATIONAL ASPECTS THIRD COUNTRIES

Luxembourg AIF FCP

SPV

Luxembourg AIF SICAV

Management Company

Risk Manager

Investment Advisor / Manager

Depositary

Independent Valuer

Central Administration

Reporting

AIFM

Portfolio Manage-

ment

Risk Manage-

ment

Valuation

NAV Calculation

Other functions

(e.g. Administration,

Marketing)

OPERATIONAL ASPECTS

24

• 2013

• 2015

• 2013-2018 Private Placement regime:

EU Passport

EU AIF

EU Passport

EU AIFM

non-EU AIFM EU AIF

for and

EU AIF

for and

non-EU AIFM non-EU AIF

for and

and

pour

non-EU AIF EU AIFM

for and

non-EU AIF EU AIFM

for and

for and

Cayman

non-EU AIFM

non-EU AIFM non-EU AIF

THIRD COUNTRIES

25

CURRENT RULES FOR PRIVATE PLACEMENT REGIME

Marketing via private placement allowed

Marketing via private placement forbidden or restricted

26

ALLYING UCITS AND AIFMD : A SUPER MANCO?

• The combination of UCITS IV and AIFMD regulations make now technically possible to have a single legal entity authorised and regulated to manage UCITS and AIF and offer investment management and non-core services in its home country and in host EU member states under EU regime for passporting cross-border services

• This offers opportunities for leveraging on existing ManCos structures,

already meeting many of the AIFMD requirements (minimum capital, experienced senior management, remuneration and conflict of interest policies, delegation and oversight arrangements, etc.)

• Asset Management firms have enhanced possibilities for adapting set-up of group structures to own strategies and requirements, enabling achievements of economies of scale and full utilisation of centers of competences, reducing internal complexity and optimising use of resources

28

LUXEMBOURG SPECIFICITIES

SIF SICAR

UCI II

Soparfi

Lightly Regulated

UCITS I

Non Regulated

More Regulated

… since efficiency can be achieved with any of these vehicles or a combination

thereof !

Mainly based on:

Investors regulatory needs and Investments regulatory constraints …

Securiti-sation

SPF

INVESTMENT VEHICLES IN LUXEMBOURG: CHOICE OF THE VEHICLE

SCS

30

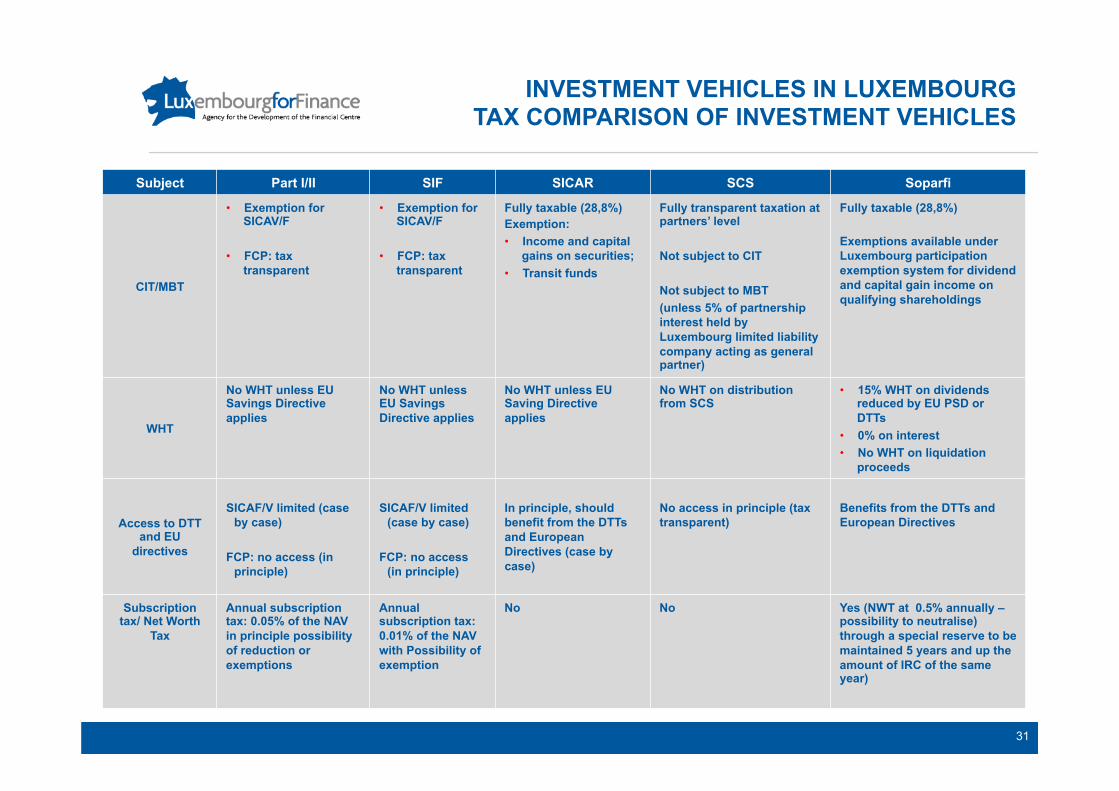

INVESTMENT VEHICLES IN LUXEMBOURG TAX COMPARISON OF INVESTMENT VEHICLES

Subject Part I/II SIF SICAR SCS Soparfi

CIT/MBT

• Exemption for SICAV/F

• FCP: tax transparent

• Exemption for SICAV/F

• FCP: tax transparent

Fully taxable (28,8%) Exemption: • Income and capital

gains on securities; • Transit funds

Fully transparent taxation at partners’ level Not subject to CIT Not subject to MBT (unless 5% of partnership interest held by Luxembourg limited liability company acting as general partner)

Fully taxable (28,8%) Exemptions available under Luxembourg participation exemption system for dividend and capital gain income on qualifying shareholdings

WHT

No WHT unless EU Savings Directive applies

No WHT unless EU Savings Directive applies

No WHT unless EU Saving Directive applies

No WHT on distribution from SCS

• 15% WHT on dividends reduced by EU PSD or DTTs

• 0% on interest • No WHT on liquidation

proceeds

Access to DTT and EU

directives

SICAF/V limited (case by case)

FCP: no access (in

principle)

SICAF/V limited (case by case)

FCP: no access

(in principle)

In principle, should benefit from the DTTs and European Directives (case by case)

No access in principle (tax transparent)

Benefits from the DTTs and European Directives

Subscription tax/ Net Worth

Tax

Annual subscription tax: 0.05% of the NAV in principle possibility of reduction or exemptions

Annual subscription tax: 0.01% of the NAV with Possibility of exemption

No No Yes (NWT at 0.5% annually – possibility to neutralise) through a special reserve to be maintained 5 years and up the amount of IRC of the same year)

31

LUXEMBOURG LIMITED PARTNERSHIP

• How? – AIFMD Bill

• When? - expected Q1 2013 • Outcome?

1. Complete overhaul of the common limited partnership (SCS/CLP) 2. Creation of the special limited partnership (SCSp/SLP) 3. Modernisation of the corporate partnership limited by shares (SCA)

• Objectives ? – modernise/expand Luxembourg legal/product toolbox

MODERNISATION OF LUXEMBOURG PARTNERSHIP REGIMES

33

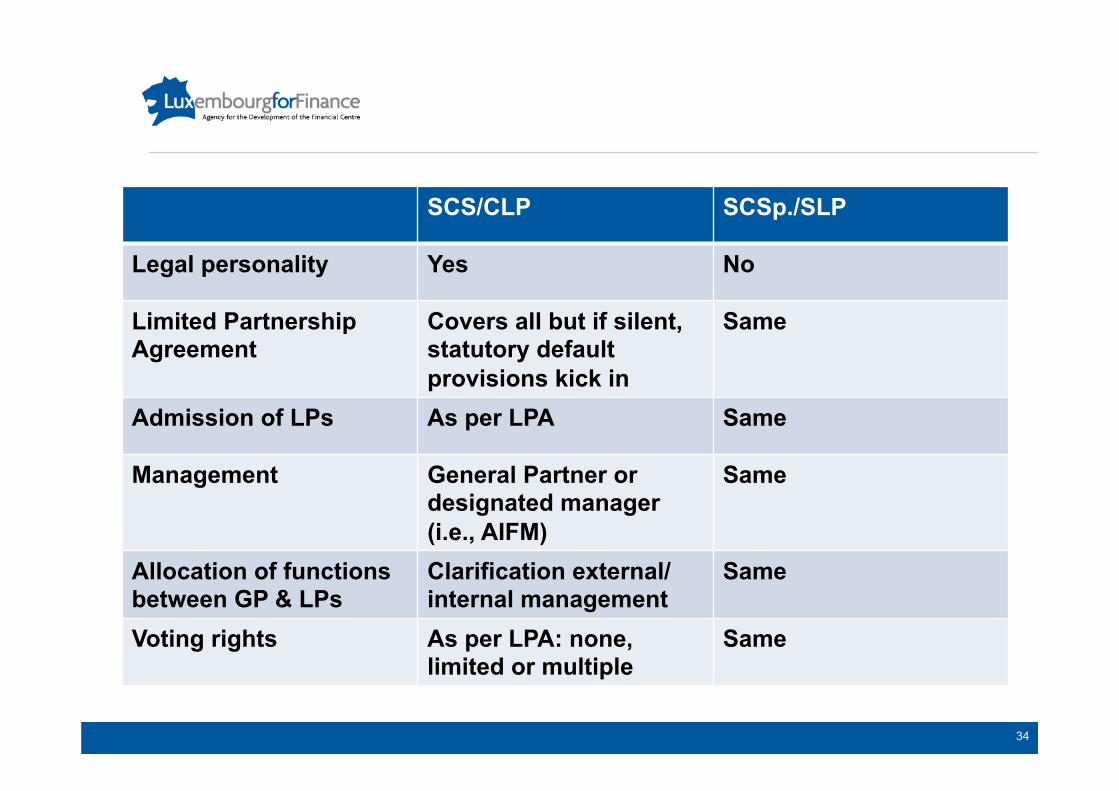

SCS/CLP SCSp./SLP

Legal personality Yes No

Limited Partnership Agreement

Covers all but if silent, statutory default provisions kick in

Same

Admission of LPs As per LPA Same

Management General Partner or designated manager (i.e., AIFM)

Same

Allocation of functions between GP & LPs

Clarification external/internal management

Same

Voting rights As per LPA: none, limited or multiple

Same

34

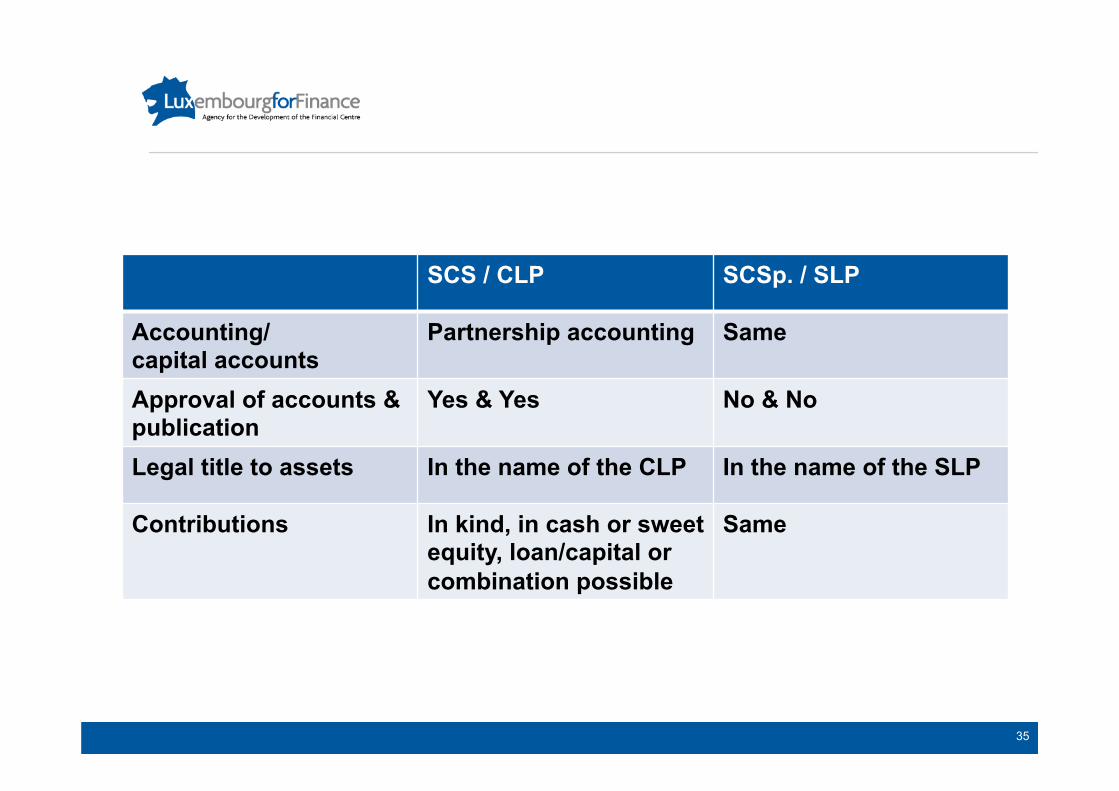

SCS / CLP SCSp. / SLP

Accounting/ capital accounts

Partnership accounting Same

Approval of accounts & publication

Yes & Yes No & No

Legal title to assets In the name of the CLP In the name of the SLP

Contributions In kind, in cash or sweet equity, loan/capital or combination possible

Same

35

SCS / CLP SCSp. / SLP

Default, Excuse, Transfer Provisions

Confirmed Same

Profit allocations As per LPA Same

Return of capital Unrestricted as per LPA Same

Termination As per LPA Same

36

LUXEMBOURG COMMON LIMITED PARTNERSHIP (CLP))

• Current tax treatment:

– Tax transparent vehicle in principle not subject to CIT, WHT or MBT except if business-tainted (Geprägetheorie): i. MBT applies ii. Non-resident partners are deemed to have a permanent

establishment in Luxembourg

– Business-taint theory not applicable to SCS with SICAR or SIF status

– Possible structuring options: non corporate GP (SCOSA) (foreign GP is not a viable option from a corporate perspective)

37

CLP/SLP PROPOSED TREATMENT

• Proposed tax changes:

– Assimilation of SLP (new regime) to CLP

– Limitation of business-taint theory applicable to CLP and SLP Business-taint only if the GP is a Luxembourg limited liability company, which holds at least 5% of the partnership interests

38

CARRIED INTEREST

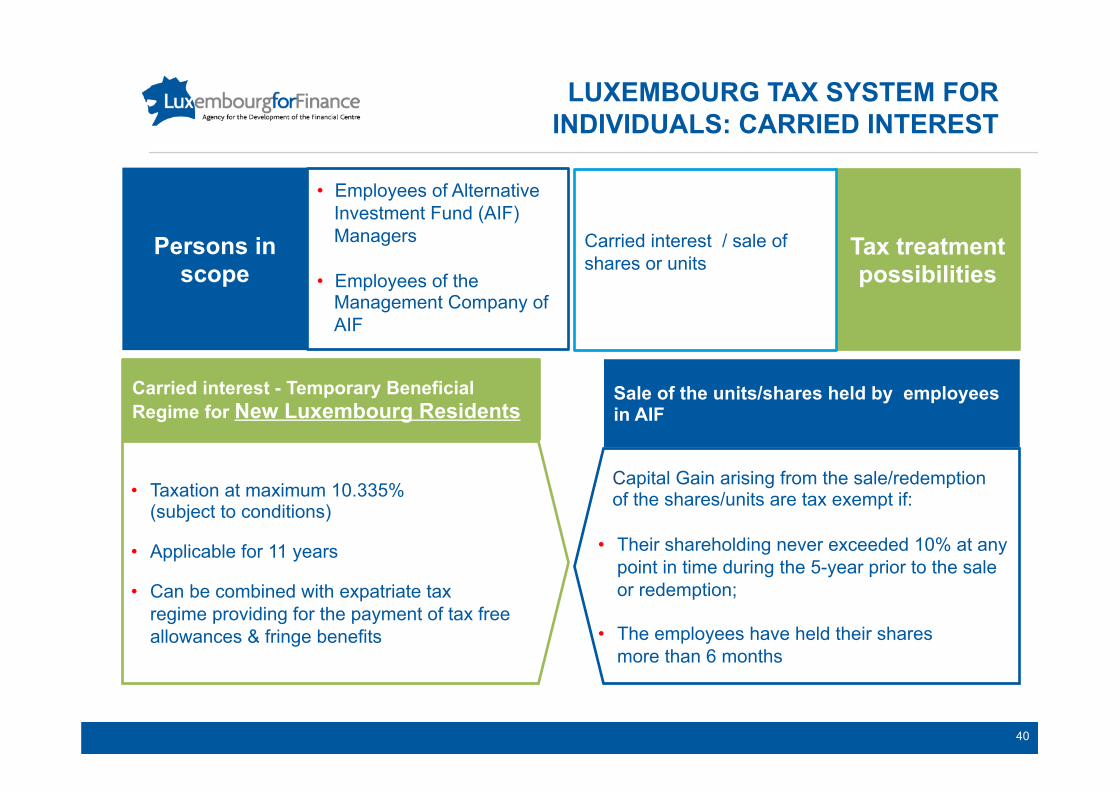

LUXEMBOURG TAX SYSTEM FOR INDIVIDUALS: CARRIED INTEREST

Persons in scope

Tax treatment possibilities

Carried interest / sale of shares or units

• Employees of Alternative Investment Fund (AIF) Managers

• Employees of the Management Company of AIF

• Taxation at maximum 10.335% (subject to conditions)

• Applicable for 11 years

• Can be combined with expatriate tax regime providing for the payment of tax free allowances & fringe benefits

Capital Gain arising from the sale/redemption of the shares/units are tax exempt if:

• Their shareholding never exceeded 10% at any

point in time during the 5-year prior to the sale or redemption;

• The employees have held their shares more than 6 months

Carried interest - Temporary Beneficial Regime for New Luxembourg Residents

Sale of the units/shares held by employees in AIF

40

HOW WE ARE PREPARING GAP ANALYSIS/CHANGES

• On the level of the AIF: in/out/ exempt • On the level of the AIFM: in/out • On the level of the service providers

• Fund Administration • Depositary • …

• Decision by the AIFM on the business model • Improvements on Systems and processes • In vs Outsourcing of tasks (compliance/ audit,

valuation,…) • Decision on business alliances • Review of the operational and contractual framework

GAP ANALYSIS

HOW WE ARE PREPARING GAP ANALYSIS/ CHANGES

KEY ACTIONS

42

WHY CHOOSE LUXEMBOURG?

• UCITS - an European success story and a recognised global brand • Luxembourg UCITS represent more than 75% of UCITS funds distributed

internationally - largest fund centre in Europe • Over 2,000 UCITS vehicles and around 1,500 non-UCITS, total AuM >

2.3bio €ur

• Efficient and reliable fund infrastructure : more than 60 custodians with world-wide networks, more than 100 central administrations, specialised investment professionals experienced in the fund industry, multi-lingual workforce

• Expertise to cater for custom-made requirements facilitating distribution (operational solutions for multi-class funds, tax reporting requirements, etc.)

• Easy of access to government and regulator, well-defined legal framework, long-term relationship established with authorities of UCITS distribution markets outside Europe

• Active investment industry association promoting consultative approach

44

THANK YOU! WWW.LUXEMBOURGFORFINANCE.LU

45