how value creation (and destruction) from climate change ...€¦ · how value creation (and...

TRANSCRIPT

A

A 2001380520/487408_11/487408/487408

How value creation (and destruction) from climate change will shape the investment landscape

Wellington Management Company LLP

For institutional use only. Not intended for reproduction or use with the public. Any views expressed herein are those of the author(s), are based on available information, and are subject to change without notice. Individual portfolio management teams may hold di�erent views and may make di�erent investment decisions for di�erent clients. The material and/or its contents are current as of the most recent quarter end, unless otherwise noted. Certain data provided is that of a third party. While data is believed to be reliable, no assurance is being provided as to its accuracy or completeness. Alan Hsu Global Industry Analyst and Portfolio Manager

Copyright © 2018 All Rights Reserved2001392649/487408_11/487408/487408A

A

About meTitle Line 2

Born and raised in Houston, Texas

Son of petroleum engineer

University of Texas

Information technology experience

Research coverage on energy, renewables, utilities, and sustainability

A

A13 September 2018 A1 2

Copyright © 2018 All Rights Reserved2001392651/487408_10/487408/487408A

A

Conventional investment wisdomTitle Line 2

The trend is your friend

Heads I win, tails I don’t lose

Think long term

Buy low, sell high

A

A13 September 2018 A1 3

Copyright © 2018 All Rights Reserved

Source: https://climate.nasa.gov/interactives/climate-time-machine

A

A13 September 2018

Temperature change is realTitle Line 2

1950 2017

2001380948/487408_3/487408/487408

A1 4

Copyright © 2018 All Rights Reserved

Source: NOAA, August 2018 | https://www.ncdc.noaa.gov/cag/global/time-series/globe/land_ocean/p12/12/1880-2018.csv

A

A13 September 2018

Weather adversity trendingTitle Line 2

Global land and ocean temperature anomalies (1880 – 2018) Degrees Celsius

2001381797/487408_3/487408/487408

1880 1892 1905 1917 1930 1942 1955 1968 1980 1993 2005 2018-1.0

-0.5

0.0

0.5

1.0

1.5

A1 5

Copyright © 2018 All Rights Reserved

Source: realclimate.org, January 2018

A

A13 September 2018

Predictable and more reliable than most forecastsTitle Line 2

2001389722/487408_11/487408/487408

1980 1985 1990 1995 2000 2005 2010 2015 2020-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Hindcast Forecast

Years

CMIP5 Ensemble mean (95% spread)Forcing-adjusted CMIP5 mean + spread

HadCRUT4Cowtan & WayNOAA NCEIGISTEMP

Global mean surface temperature anomaliesAnomaly (°C, w.f.t. 1980 – 1999)

A1 6

Copyright © 2018 All Rights Reserved

Source: Munich Re NatCatSERVICE, January 2018 | Losses from natural catastrophes 1980 – 2017: Volatility of loss volumes is increasing

A

A13 September 2018

Climate adversity is becoming increasingly costlyTitle Line 2

Insured versus uninsured natural catastrophe losses, 1980 – 2017US$ billion

2001381802/487408_4/487408/487408

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013 20160

100

200

300

400Overall losses in 2016 values Insured losses

A1 7

Copyright © 2018 All Rights Reserved

Note: The term “country” refers to a country or statistically equivalent entity. | Source: US Census Bureau, 2007 – 2011, American Community Survey

Sources: Economist.com, CEIC; World Bank

A

A13 September 2018

Climate costs truly ‘human made’Title Line 2

2001381040/487408_4/487408/487408

2

U.S. C

ensu

s Bureau

Number of High-Income Households for Each County in the United States: 2007–2011Figure 1.

Source: U.S. Census Bureau, 2007–2011 American Community Survey.Note: The term "county" refers to a county or statistically equivalent entity.

0 100 Miles

0 100 Miles

0 500 Miles

Number of households by county

107–251

252–883

43–106

Less than 43

884 or more

Concentration of high-income households for each county in the United States: 2007 – 2011

Uncommon prosperityChina’s GDP per person (2015)

Over 14

$’000

12 – 1410 – 128 – 106 – 8Under 6

Hainan

Hong KongGuangdong

Fujian

Zhejiang

Shanghai

Jiangsu

Shandong

TianjinBeijing

Liaoning

JilinInner Mongolia

Heilongjiang

Xinjiang

Qinghai

Tibet

YunnanGuangxi

Guizhou

Sichuan

GansuShaanxi

Shanxi

Henan

Hunan

HubeiChongqing

Anhui

Jiangxi

NingxiaHebei

Macau

A1 8

Copyright © 2018 All Rights Reserved

As of 31 December 2016. | Sources: Climate Change Laws of the World database, Grantham Research Institute on Climate Change and the Environment, Sabin Center for Climate Change Law.

A

A13 September 2018

Climate risk is not JUST about weatherTitle Line 2Regulatory and litigation risk is also rising

2001389724/487408_4/487408/487408

1994and

before

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 20160

200

400

600

800

1,000

1,200

1,400

Total legislative

Total executive

Climate laws and regulations have been on the rise

Total legislative and executive acts or policies

A1 9

Copyright © 2018 All Rights Reserved

Source: http://www.air-worldwide.com/Publications/AIR-Currents/2015/The-Growing-Value-of-U-S--Coastal-Property-at-Risk/

A

A13 September 2018

No evidence that behavior is changingTitle Line 2

2001381134/487408_3/487408/487408

AlabamaConneticut

Deleware

FloridaGeorgia

Louisiana

MaineMaryland

Massachussetts

Mississippi

New Hampshire

New Jersey

New York

North Carolina

Rhode Island

South Carolina

TexasVirgina

0

25

50

75

100

2004 2012

2004 20120

3,000

6,000

9,000

12,000

% of insured value of coastal properties (east coast and Gulf Coast)

Insured $ (billions)

A1 10

Copyright © 2018 All Rights Reserved2001380547/487408_11/487408/487408A

A

Nature can’t keep upTitle Line 2

Source: World Wildlife Foundation, 2018

A

A13 September 2018

Deforestation impact from high levels of consumption is an area equivalent to 28 football (soccer) fields of forest per minute

A1 11

Copyright © 2018 All Rights Reserved2001391254/487408_10/487408/487408A

A

Nature can’t keep upTitle Line 2

Source: World Wildlife Foundation, 2018

A

A13 September 2018

Deforestation impact from high levels of consumption each year is an area equivalent to the size of Panama

A1 12

Copyright © 2018 All Rights Reserved2001380549/487408_11/487408/487408A

A

Risks beget more risksTitle Line 2

Permafrost

Hurricanes

Urban islands

Hotter temps

Regulation, policy, capital markets

A

A13 September 2018 A1 13

Copyright © 2018 All Rights Reserved

Source: MFS 2016

A

A13 September 2018

Investors should take a more holistic approach to integrating risksTitle Line 2

2001381290/487408_11/487408/487408

Hedge Funds

Mututal Funds

Private High Net Worth

PensionsInsurance

Sovereign Wealth Funds

Endowments

0

10

20

30

40

50

60Asset owners have long liabilities (years)

A1 14

Copyright © 2018 All Rights Reserved2001381291/487408_11/487408/487408

¼ 1 3 5 6 – 1011 – 20

21 – 5051

0

5

10

15

20

25

30

20062007

20082009

20102011

20122013

20142015

0.6

0.9

1.2

1.5

1.8

Assets under management % of total (RHS)

Earning momentum model

Stock price and volume patterns

Dividend discount model

Multiples – Price to earning

Expected value analysis

Discounted cash ow model

Economic value added model

Residual income model

-5-4-3-2-1012345

10.005.00

3.332.50

2.001.67

1.431.25

1.111.00

0.910.83

0.770.71

0.670.53

0.590.56

0.530.50

0

100

200

300

0

10

20

30

40

Turnover (# of funds, LHS)

¼ 1 3 5 6 – 1011 – 20

21 – 5051

0

5

10

15

20

25

30

20062007

20082009

20102011

20122013

20142015

0.6

0.9

1.2

1.5

1.8

Assets under management % of total (RHS)

Earning momentum model

Stock price and volume patterns

Dividend discount model

Multiples – Price to earning

Expected value analysis

Discounted cash ow model

Economic value added model

Residual income model

-5-4-3-2-1012345

10.005.00

3.332.50

2.001.67

1.431.25

1.111.00

0.910.83

0.770.71

0.670.53

0.590.56

0.530.50

0

100

200

300

0

10

20

30

40

Turnover (# of funds, LHS)

1Source: 2˚ii Equity Research Analyst Survey 2016, n=6 | 2Source: BlackRock 2016 | 3Sources: 2˚ii, Mercer & The Generation Foundation 2007 | 4Sources: Authors 2017, from 2˚ii Equity Research Analyst Survey 2016, Damodaran 2010 and CFA Institute, 2016

A

A13 September 2018

... but they don’tTitle Line 2

Equity processes explicitly short-term4Equity holders invest for 2 years3

Bond holders invest for 2 years2Analyst focus on five years or less1

A1 15

Copyright © 2018 All Rights Reserved

Source: Federal Reserve Bank of St. Louis, 2008

Source: Chuanshu Ji, 2008

A

A13 September 2018

“Mr. Market” often misses big mispricingsTitle Line 2

Monthly supply of unsold homesRating agencies did not downgrade securities until it was too late

2001381314/487408_11/487408/487408

1/055/05

9/051/06

5/069/06

1/075/07

9/071/07

5/079/07

1/085/08

9/08

0

3

6

9

12

Monthly ratio of unsold homes to sold homes

3Q064Q06

1Q072Q07

3Q074Q07

1Q082Q08

0

200

400

600

800

1,000

10

14

18

22

26

Ratin

gs d

owng

rade

s

Percent

Mortgage-backed securities downgrade (LHS)

Late payment rate (RHS)

A1 16

Copyright © 2018 All Rights Reserved2001392656/487408_10/487408/487408A

A

Climate change is a trend with no obvious endTitle Line 2

We know the trend is• Morepredictablethanmostotherforecasts• Indicatingmateriallyworserisk(andbetteropportunities)everyday• Likelytomateriallyimpactglobalassetvalues• Beingignoredinmanywaysbycapitalmarkets

A

A13 September 2018 A1 17

Copyright © 2018 All Rights Reserved2001381321/487408_11/487408/487408

A

A13 September 2018

Capital market opportunitiesTitle Line 2

Some things are timeless...

A1 18

Copyright © 2018 All Rights Reserved

Source: Stratfor

A

A13 September 2018

Refrigerator sales, AC salesTitle Line 2

World heating and air conditioning energy demandCooling is on track to overtake heating as the larger consumer of residential energy. Cooling is predominantly powered by electricity.

50 thousand petajoules

2001381322/487408_2/487408/487408

1971 1991 2011 2031Projected

2051Projected

2071Projected

2091Projected

0

5

10

15

20

25

30

35

40

45

Air conditioning Heat

A1 19

Copyright © 2018 All Rights Reserved

Source: US Energy Information Administration, Annual Energy outlook (for years 2010 – 2017), https://www.eia.gov/outlooks/aeo/, accessed 17 May 2017

A

A13 September 2018

Renewables are cost competitive todayTitle Line 2

2001389729/487408_8/487408/487408

2011 2012 2013 2014 2015 2016 2017 20180

100

200

300

400

Coal – carbon capture

Solar PV

Coal – convention

Wind (onshore)

Gas – conventional combined cycle

$/MWh

A1 20

Copyright © 2018 All Rights Reserved2001380785/487408_8/487408/487408A

A

Solar value proposition depends on locationTitle Line 2

A

A13 September 2018

MA

A1 21

Copyright © 2018 All Rights Reserved2001380788/487408_10/487408/487408

A

A13 September 2018

Agriculture risks: arable land and waterTitle Line 2“Small and shrinking fraction of total global land mass”

37 billion acres of land on earth

A1 22

Copyright © 2018 All Rights Reserved2001394586/487408_9/487408/487408

A

A13 September 2018

Agriculture risks: arable land and waterTitle Line 2“Small and shrinking fraction of total global land mass”

37 billion acres of land on earth

11 billion acres of arable land

A1 23

Copyright © 2018 All Rights Reserved2001394587/487408_10/487408/487408

A

A13 September 2018

Agriculture risks: arable land and waterTitle Line 2“Small and shrinking fraction of total global land mass”

37 billion acres of land on earth

11 billion acres of arable land

7 billion acres of land free of weeds & pests

A1 24

Copyright © 2018 All Rights Reserved2001380790/487408_11/487408/487408

A

A13 September 2018

Dirt matters, and we are losing soil rapidlyTitle Line 2

Each year lose 0.66% of cropland due to soil erosion

Global soil

Global soil after 30 years

Global soil after 50 years

15 million hectare of cropland lost due to soil erosion each year

1.5 billion hectare of cropland under cultivation for crop production

A1 25

Copyright © 2018 All Rights Reserved2001389488/487408_11/487408/487408

A

A13 September 2018

Agriculture risks: arable land and waterTitle Line 2

And much of the planet’s arable land is located in high-climate-risk geographies• Brazilishometo30%ofsoybeanproduction,etc.• Californiaprovides~50%ofUSfruits,nuts,andvegetables

A1 26

Copyright © 2018 All Rights Reserved2001380792/487408_11/487408/487408A

A

Fashion pollution and waste likely underappreciatedTitle Line 2

Fashion industry is 2nd most polluting on the planet

Production of 1 t-shirt produces same amount of CO2 as driving a car 10 miles

Americans will on average discard 80 pounds of clothing (equivalent of ~28 t-shirts)

A

A13 September 2018

Sources: 13-D, August 2018; World Economic Forum, 2018; Savers, State of Reuse Report, 2018

CO2 from driving One t-shirt

A1 27

Copyright © 2018 All Rights Reserved

Sources: Cires, NOAA, April 2018

A

A13 September 2018

If looks could killTitle Line 2

2001389733/487408_11/487408/487408

Emission from personal care products tracked benzene (transport) emissions

People use 15x the fuel in non-petroleum products as they do petroleum

0:00 5:00 10:00 15:00 20:00 25:000:00 5:00 10:00 15:00 20:00 25:006

8

10

12

14

16

18

100

150

200

250

300

350

400

6

8

10

12

14

16

18

100

150

200

250

300

350

400

D5 siloxane emissions (LHS)

Benzene emissions (RHS)

vs

Personal Transport

A1 28

Copyright © 2018 All Rights Reserved2001380793/487408_10/487408/487408

A

A13 September 2018

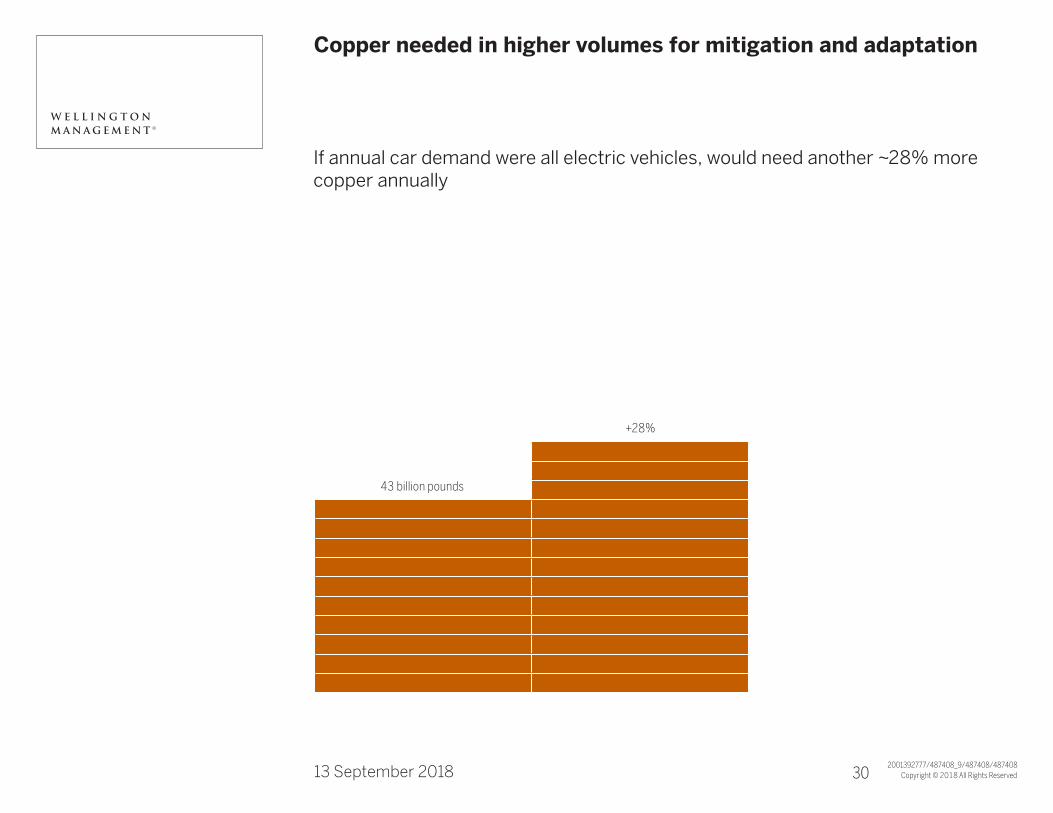

Copper needed in higher volumes for mitigation and adaptationTitle Line 2

Copper demand today is ~43 billion pound

43 billion pounds

A1 29

Copyright © 2018 All Rights Reserved2001392777/487408_9/487408/487408

A

A13 September 2018

Copper needed in higher volumes for mitigation and adaptationTitle Line 2

If annual car demand were all electric vehicles, would need another ~28% more copper annually

43 billion pounds

+28%

A1 30

Copyright © 2018 All Rights Reserved2001392780/487408_11/487408/487408

A

A13 September 2018

Copper needed in higher volumes for mitigation and adaptationTitle Line 2

New air conditioning units add another 74% copper to satisfy demand needed through 2050

43 billion pounds

+28%

+74%

A1 31

Copyright © 2018 All Rights Reserved2001380794/487408_9/487408/487408A

A

Utilities are leading providers of alternative energyTitle Line 2

#1 owner of solar in N America

#1 owner of wind in N America

#1 owner of electric charging infrastructure

A

A13 September 2018 A1 32

Copyright © 2018 All Rights Reserved2001389567/487408_11/487408/487408A

A

Internet infrastructure concentrated on coastsTitle Line 2

Why this matters: Impacts to be felt next 15 years

Impacted assets: 4,000 miles of fiber conduit and 1,000 connection nodes

Impacted cities: New York, Miami, and Seattle

Impacted companies: CenturyTel, AT&T, and InteliquentSource: University of Oregon and Axios, 2018 | Sea Level Rise Costing Billions in Home Prices

A

A13 September 2018 A1 33

Copyright © 2018 All Rights Reserved2001380795/487408_3/487408/487408A

A

Catalysts to climate re-ratingTitle Line 2

Carbon tax

Climate legislation

Natural disasters

A

A13 September 2018 A1 34

Copyright © 2018 All Rights Reserved

Base: Americans 18+ who are registered to vote. | Data collected from size tracking studies con-ducted from March 2012 to October 2014 | Source: Forbes, January 2015

A

A13 September 2018

Carbon regulation politically acceptableTitle Line 2

Majority of republicans support regulation of carbon dioxide as a pollutant

% strongly/somewhat support the policy

Question: How much do you support or oppose the following policies – regulate carbon dioxide (the primary greenhouse gas) as a pollutant?

2001381323/487408_4/487408/487408

Totalregistered

voters(n=5,513)

TotalRepublicans(n=2,330)

LiberalRepublicans

(n=105)

ModerateRepublicans

(n=540)

ConservativeRepublicans

(n=1,271)

Tea PartyRepublicans

(n=412)

0

50

100

70

56

7174

54

36

A1 35

Copyright © 2018 All Rights Reserved

Source: World Bank Group

A

A13 September 2018

Carbon taxes for the massesTitle Line 2

2001389715/487408_10/487408/487408

Northwest territories

Alberta

Canada

British Columbia

WashingtonOregon

California

Saskatchewan

Manitoba

Québec

Japan

Republic of korea

VietnamThailand

New ZealandAustraliaSouth Africa

TurkeyChina

KaakhstanUkraineEU

Iceland

Mexico

Colombia

Chile Argentina

São Paulo

Rio Dejaneiro

Brazil

Côte d’Ivoire

Ontario

Newfoundland and labrador

Prince Edward Island

New BrunswickNova Scotia

MassachusettsRggi

ETS implemented or scheduled for implementation ETS and carbon tax implemented or scheduledCarbon tax implemented or scheduled for implementation Carbon tax implemented or scheduled, ETS under considerationETS or carbon tax under consideration ETS implemented or scheduled, carbon tax under consideration

A1 36

Copyright © 2018 All Rights Reserved

Source: World Bank Group

A

A13 September 2018

Carbon pricing intitiatives climbing steadilyTitle Line 2

2001389716/487408_7/487408/487408

Figure 5 / Regional, national and subnational carbon pricing in itiatives: share of global emissions covered

Shar

e of

glo

bal a

nnua

l GH

G e

miss

ions

25%

20%

15%

10%

5%

0%

1990

1992

1995

2000

1998

2003

2004

2005

1991

1994

1997

2002

1993

1996

2001

1999

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2018

2019

2020

2017

4 5 6 7 8

9 10 15 16 1921

24

32

3738

41

2

Number of implemented initiatives

46 47

50

51

Finland carbon tax (1990 Ò)

Poland carbon tax (1990 Ò)

Norway carbon tax (1991 Ò)

Sweden carbon tax (1991 Ò)

Denmark carbon tax (1992 Ò)

Slovenia carbon tax (1996 Ò)

Estonia carbon tax (2000 Ò)

Latvia carbon tax (2004 Ò)

EU ETS (2005 Ò)

Alberta SGER (2007 Ò)

Switzerland ETS (2008 Ò)

New Zealand ETS (2008 Ò)

Switzerland carbon tax (2008 Ò)

Liechtenstein carbon tax (2008 Ò)

BC carbon tax (2008 Ò)

RGGI (2009 Ò)

Iceland carbon tax (2010 Ò)

Tokyo CaT (2010 Ò)

Ireland carbon tax (2010 Ò)

Ukraine carbon tax (2011 Ò)

Saitama ETS (2011 Ò)

California CaT (2012 Ò)

Japan carbon tax (2012 Ò)

Australia CPM (2012 - 2014)

Québec CaT (2013 Ò)

Kazakhstan ETS (2013 Ò)

Ò)

Shenzhen pilot ETS (2013 Ò)

Shanghai pilot ETS (2013 Ò)

Beijing pilot ETS (2013 Ò)

Guangdong pilot ETS (2013 Ò)

Tianjin pilot ETS (2013 Ò)

France carbon tax (2014 Ò)

Mexico carbon tax (2014 Ò)

Spain carbon tax (2014 Ò)

Hubei pilot ETS (2014 Ò)

Chongqing pilot ETS (2014 Ò)

Korea ETS (2015 Ò)

Portugal carbon tax (2015 Ò)

BC GGIRCA (2016 Ò)

Australia ERF Safeguard Mechanism (2016 Ò)

Fujian pilot ETS (2016 Ò)

Washington CAR (2017 Ò)

Ontario CaT (2017 Ò)

Alberta carbon tax (2017 Ò)

Chile carbon tax (2017 Ò)

Colombia carbon tax (2017 Ò)

Massachusetts ETS (2018 Ò)

Argentina carbon tax (2019 Ò)

South Africa carbon tax (2019 Ò)

Singapore carbon tax (2019 Ò)

China national ETS (2020 Ò)

A1 37

Copyright © 2018 All Rights Reserved

Source: Climate Change Litigation of the World

A

A13 September 2018

Climate lawsuits on the riseTitle Line 2

Number of litigation cases in 25 jurisdictions, 1994 – 2016

2001389717/487408_6/487408/487408

1994 1995 1996 1997 1998 1999 20002001 200220032004200520062007200820092010 2011 2012 2013 2014 2015 2016

0

15

30

45

A1 38

Copyright © 2018 All Rights Reserved

A

A13 September 2018

California climate risks evident in recent eventsTitle Line 2

2001392782/487408_11/487408/487408

Wildfires Droughts

A1 39

Copyright © 2018 All Rights Reserved2001392660/487408_11/487408/487408A

A

In Summary...Title Line 2

The trend is NOT your friend

Climate investing = Heads I win, tails I lose

Think long term – climate risks grow by the day

Buy low, sell high – climate risk is a significant mispriced bet

A

A13 September 2018 A1 40

Copyright © 2018 All Rights Reserved2001380597/487408_11/487408/487408A

A

Rating agencies aren’t looking far enoughTitle Line 2

How Does S&P Global Ratings Incorporate Environmental, Social and Governance Risk Into its Rating AnalysisOur ratings are forward-looking and they incorporate our financial forecasts. These forecasts reflect the period over which we consider we have a clearer view of an entity’s potential financial performance, taking into account capital structure, and the potential impact of relevant factors (including ESG risks and opportunities). Generally, our forecasts cover a time horizon of up to two years for speculative-grade corporate entities (that is, those rated ‘BB+’ and below) and no more than five years for investment-grade entities (rated ‘BBB-’ and above).

A

A13 September 2018

Source: https://www.spglobal.com/our-insights/How-Does-SP-Global-Ratings-Incorporate-Environmental-Social-and-Governance-Risks-Into-its-Ratings-Analysis-.html

A1 A1

Copyright © 2018 All Rights Reserved2000000298/487408_11/G1422/G1422

A

A13 September 2018

Important noticeTitle Line 2

©2018 Wellington Management. All rights reserved. | As of April 2018

Wellington Management Company llp (WMC) is an independently owned investment adviser registered with the US Securities and Exchange Commission (SEC). WMC is also a commodity trading advisor (CTA) registered with the US Commodity Futures Trading Commission. In certain circumstances, WMC provides commodity trading advice to clients in reliance on exemptions from CTA registration. In the US for ERISA clients, WMC is providing this material solely for sales and marketing purposes and not as an investment advice fiduciary under ERISA or the Internal Revenue Code. WMC has a financial interest in offering its products and services and is not committing to provide impartial investment advice or give advice in a fiduciary capacity in connection with those sales and marketing activities. WMC, along with its affiliates (collectively, Wellington Management), provides investment management and investment advisory services to institutions around the world. Located in Boston, Massachusetts, Wellington Management also has offices in Chicago, Illinois; Radnor, Pennsylvania; San Francisco, California; Beijing; Frankfurt; Hong Kong; London; Luxembourg; Singapore; Sydney; Tokyo; Toronto; and Zurich. This material is prepared for, and authorized for internal use by, designated institutional and professional investors and their consultants or for such other use as may be authorized by Wellington Management. This material and/or its contents are current at the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the express written consent of Wellington Management. This material is not intended to constitute investment advice or an offer to sell, or the solicitation of an offer to purchase shares or other securities. Investors should always obtain and read an up-to-date investment services description or prospectus before deciding whether to appoint an investment manager or to invest in a fund. Any views expressed herein are those of the author(s), are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may make different investment decisions for different clients.

In Canada, this material is provided by Wellington Management Canada ulc, a British Columbia unlimited liability company registered in the provinces of Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, Quebec, and Saskatchewan in the categories of Portfolio Manager and Exempt Market Dealer. In the UK, this material is provided by Wellington Management International Limited (WMIL), a firm authorized and regulated by the Financial Conduct Authority (FCA). This material is directed only at persons (Relevant Persons) who are classified as eligible counterparties or professional clients under the rules of the FCA. This material must not be acted on or relied on by persons who are not Relevant Persons. Any investment or investment service to which this material relates is available only to Relevant Persons and will be engaged in only with Relevant Persons. In Germany, this material is provided by Wellington Management International Limited, Niederlassung Deutschland, the German branch of WMIL, which is authorized and regulated by the FCA and in respect of certain aspects of its activities by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin). This material is directed only at persons (Relevant Persons) who are classified as eligible counterparties or professional clients under the German Securities Trading Act. This material does not constitute investment advice, a solicitation to invest in financial instruments or financial analysis within the meaning of Section 34b of the German Securities Trading Act. It does not meet all legal requirements designed to guarantee the independence of financial analyses and is not subject to any prohibition on dealing ahead of the publication of financial analyses. This material does not constitute a prospectus for the purposes of the German Capital Investment Code, the German Securities Sales Prospectus Act or the German Securities Prospectus Act. In Hong Kong, this material is provided to you by Wellington Management Hong Kong Limited (WM Hong Kong), a corporation licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities), Type 2 (dealing in futures contracts), Type 4 (advising on securities), and Type 9 (asset management) regulated activities, on the basis that you are a Professional Investor as defined in the Securities and Futures Ordinance. By accepting this material you acknowledge and agree that this material is provided for your use only and that you will not distribute or otherwise make this material available to any person. In Singapore, this material is provided for your use only by Wellington Management Singapore Pte Ltd (WM Singapore) (Registration Number 201415544E). WM Singapore is regulated by the Monetary Authority of Singapore under a Capital Markets Services Licence to conduct fund management activities and is an exempt financial adviser. By accepting this material you represent that you are a non-retail investor and that you will not copy, distribute or otherwise make this material available to any person. In Australia, Wellington Management Australia Pty Ltd (WM Australia) (ABN19 167 091 090) has authorized the issue of this material for use solely by wholesale clients (as defined in the Corporations Act 2001). By accepting this material, you acknowledge and agree that this material is provided for your use only and that you will not distribute or otherwise make this material available to any person. Wellington Management Company llp is exempt from the requirement to hold an Australian financial services licence (AFSL) under the Corporations Act 2001 in respect of financial services. A registered investment adviser regulated by the SEC, among others, is exempt from the need to hold an AFSL for financial services provided to Australian wholesale clients on certain conditions. Financial services provided by Wellington Management Company llp are regulated by the SEC under the laws and regulatory requirements of the United States, which are different from the laws applying in Australia. In Japan, Wellington Management Japan Pte Ltd (WM Japan) (Registration Number 199504987R) has been registered as a Financial Instruments Firm with registered number: Director General of Kanto Local Finance Bureau (Kin-Sho) Number 428. WM Japan is a member of the Japan Investment Advisers Association (JIAA) and the Investment Trusts Association, Japan (ITA). WMIL, WM Hong Kong, WM Japan, and WM Singapore are also registered as investment advisers with the SEC; however, they will comply with the substantive provisions of the US Investment Advisers Act only with respect to their US clients.

A1 A2