how to demystify cross-border payments in travel

TRANSCRIPT

Demystifying cross-border

payments in travel

Webinar

January 29, 2015

K

Kevin May

Editor & ModeratorGene Quinn

CEO & Producer

Your panelists

K

Kristin Mollison

Technical Product

Manager

WEX Inc.

Noel Goddard

Founder

FTT Global

Your panelists

Kristin Mollison, WEX Inc.Noel Goddard, FTT Global Ltd.

Demystifying cross-border payments in travel

Agenda• Introduction

• Foreign Exchange Basics

• Foreign Exchange and Cross Border Fees

• Questions

Who We Are

Cross Border Payments

• Two elements

1. Switching from one currency to another currency (FX)

2. Making the payment from one party to another in a different geography

Agenda

• The Basics of Foreign Exchange• What is an “exchange rate”

• Who sets the rates

• How does the FX “market” work

• Risk in a Multi-Currency World• Why is multi-currency becoming so risky these days

• What is the impact of Central Banks on your business

• Opportunities in Cross-Currency and Cross-Border Deals• How to capture Foreign Exchange Profits and retain it

• Managing Cross-border charges and reducing costs

What is an “Exchange Rate”

1.52

“ I will take your 1 Great British Pound and in return, you will receive 1.52 United States Dollars from me”

What is an “Exchange Rate”

1.52

If an apple in the UK costs £1 GBP, the exact same apple should cost you $1.52 US Dollars in the US*

What is an “Exchange Rate”

1.52

The relative value of a “Share” of UK Plc. against the relative value of a “Stock” in USA Inc.

What is an Exchange Rate

1.52

If a holiday in the US costs $15,200 USD then it should also cost £10,000 if purchased from the UK !!

Who sets the Exchange Rate?

I want to sell 10,000 GBPand will accept USD 15,200 for them ?

I want to buy 10,000 GBPand will pay USD 15,200 for them ?

AGREED….THE DEAL IS DONE

AT

1.52

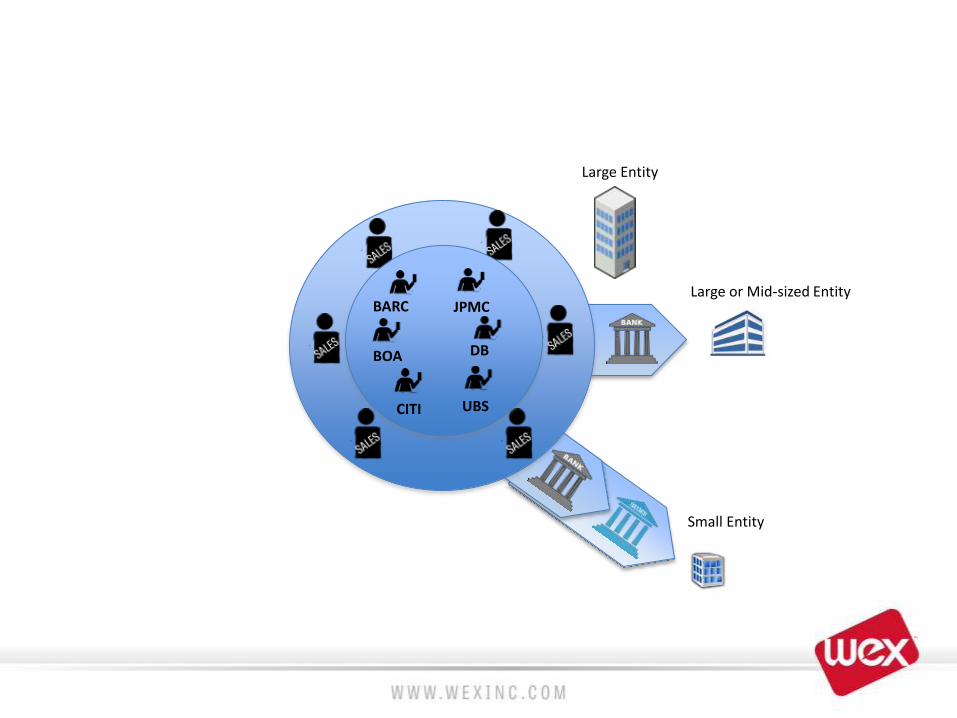

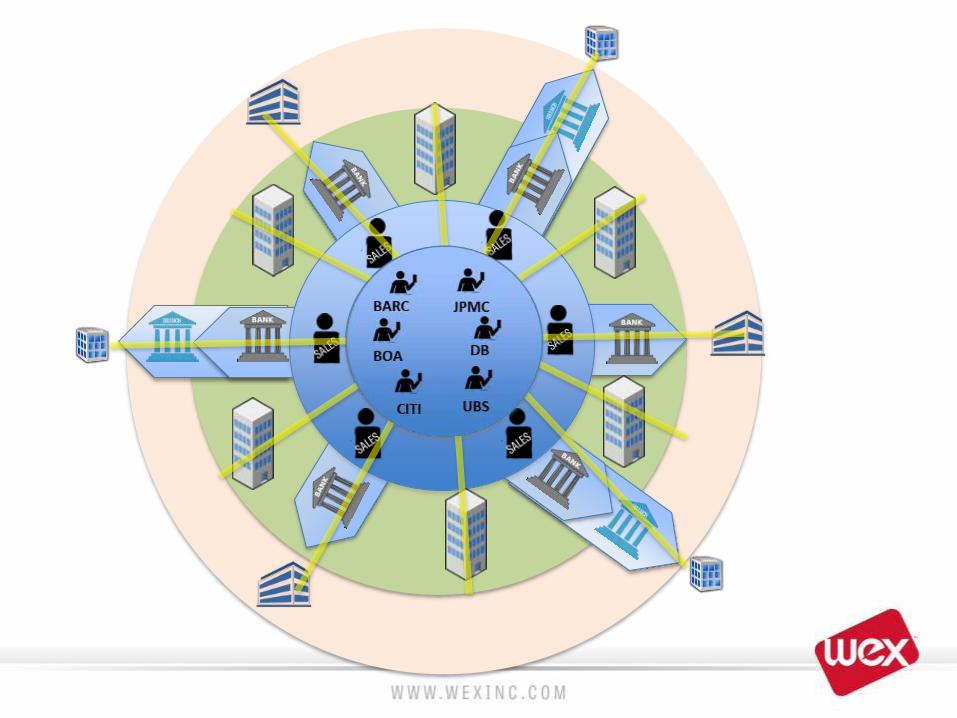

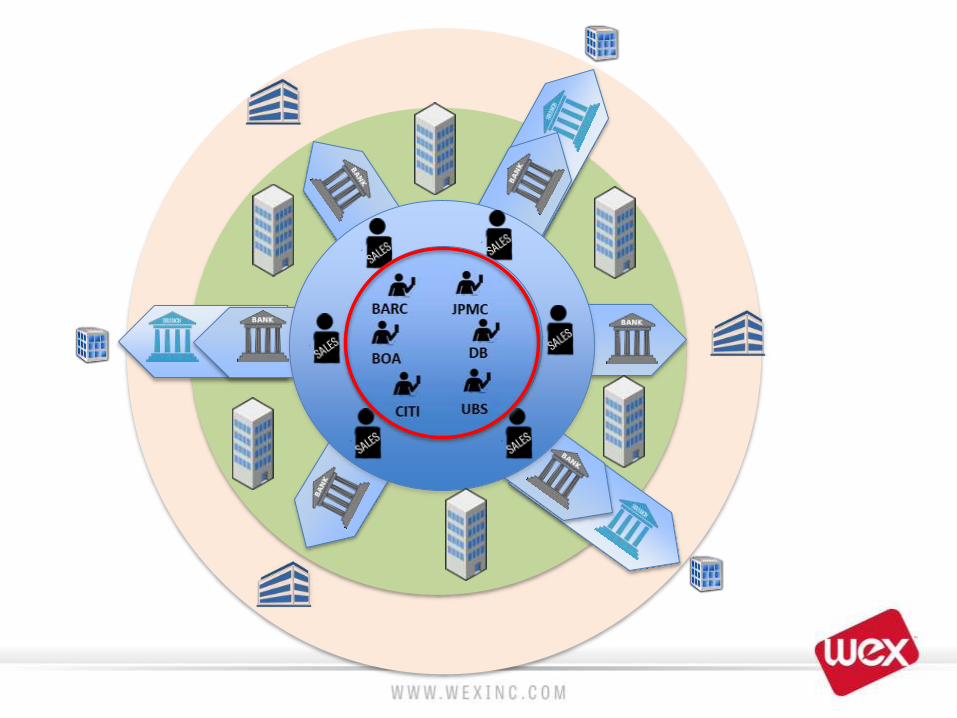

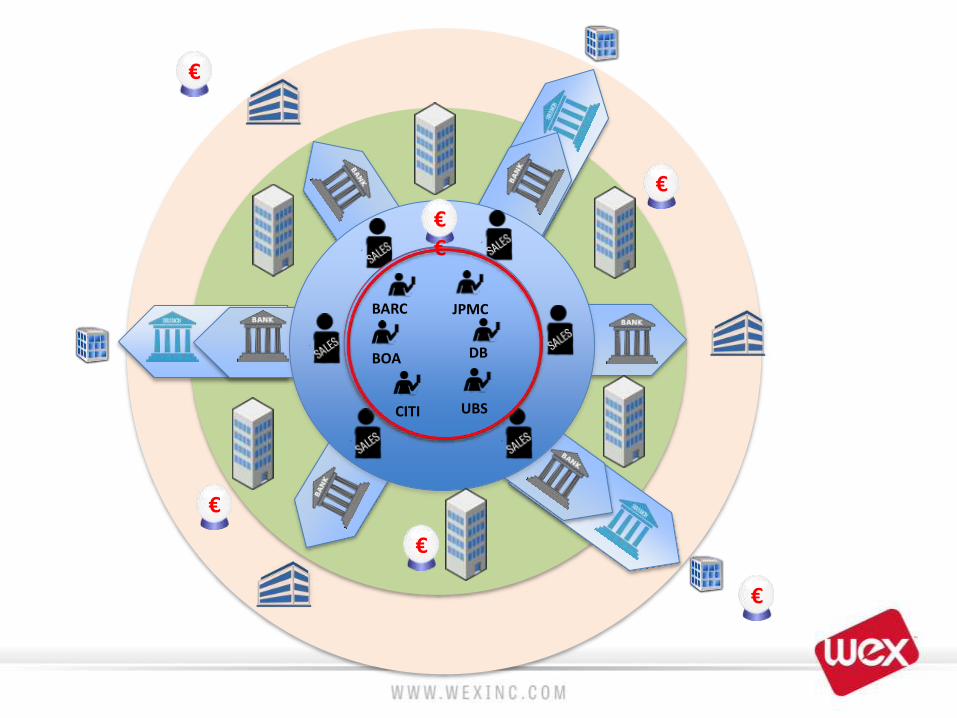

The FX Market

BARC JPMC

BOA DB

CITI UBS

Large Entity

Large Entity

Large or Mid-sized EntityBARC JPMC

BOA DB

CITI UBS

Large Entity

Large or Mid-sized Entity

Small Entity

BARC JPMC

BOA DB

CITI UBS

BARC JPMC

BOA DB

CITI UBS

BARC JPMC

BOA DB

CITI UBS

BARC JPMC

BOA DB

CITI UBS

The FX Market

• No central marketplace and no single source of pricing

• Every FX deal is between two people or entities alone

• The rate you receive will always depend on:

• What rate the person you buy from paid or thinks they will have to pay

• What their margin expectation is

Risk in Multi-Currency

• The lack of a central market place introduces both Risks and Opportunity

• Why is currency risk much greater than a week ago, a month ago or 2 decades ago ?

• How can this risk be mitigated and turned into a profit opportunity ?

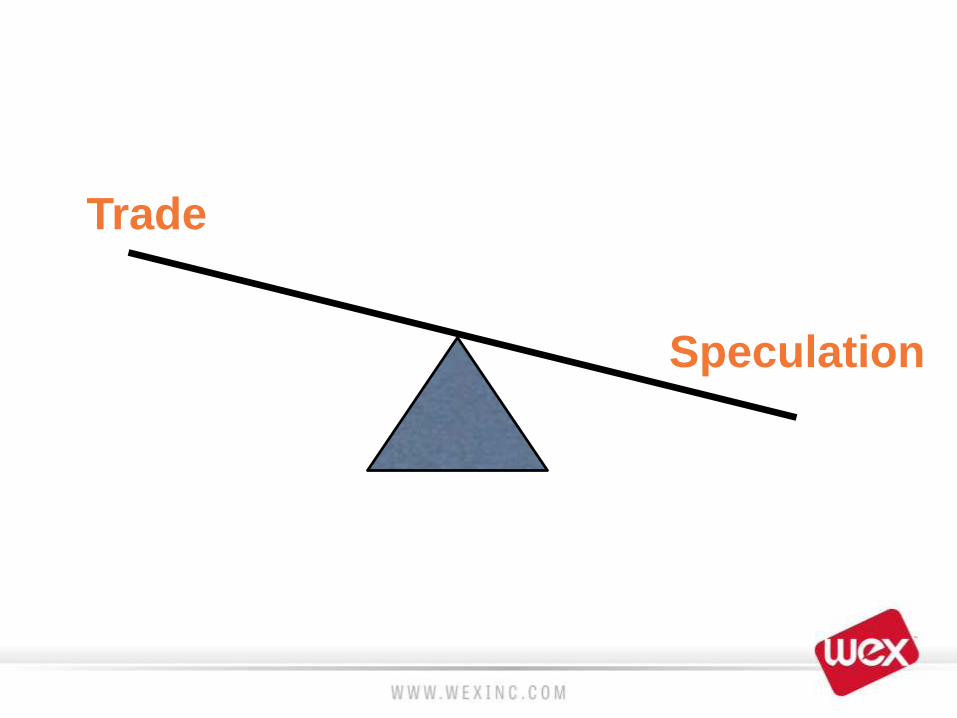

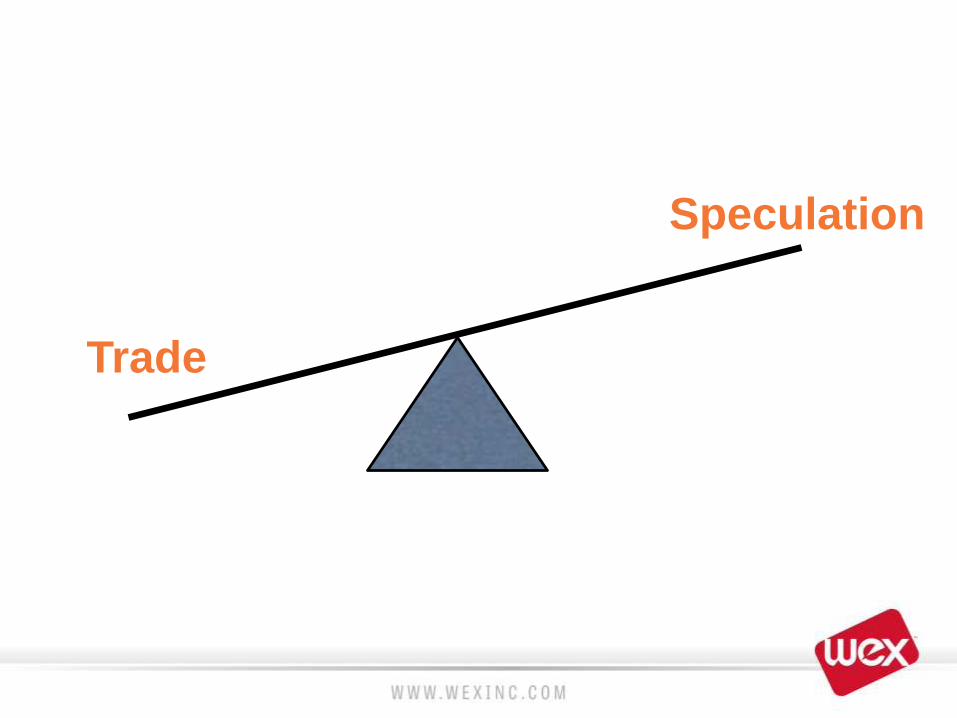

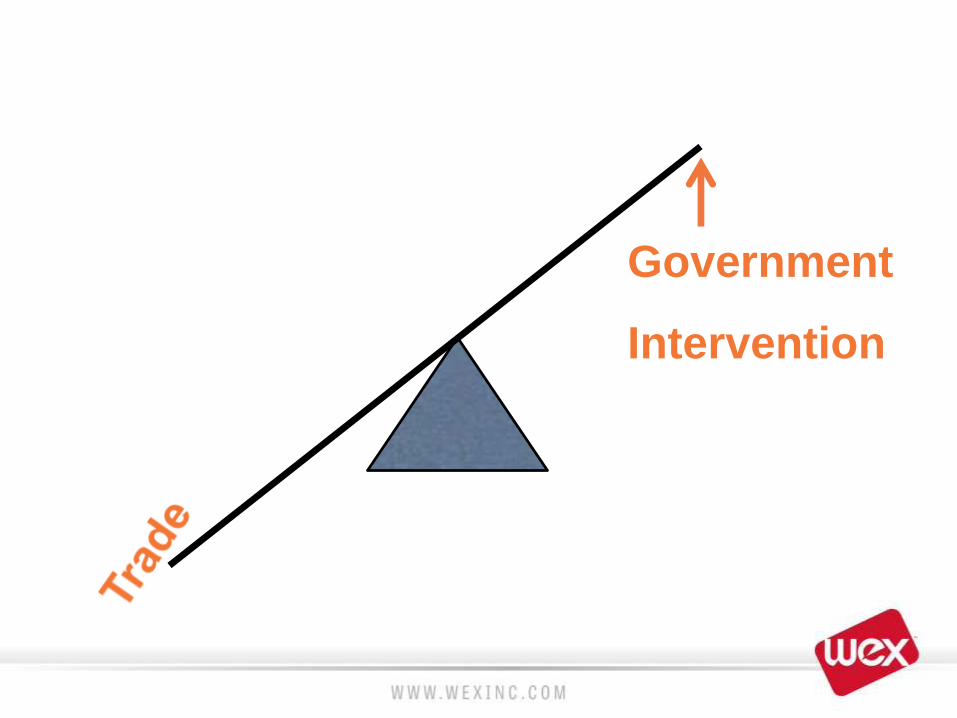

What is the Purpose of Currency ?

Who is the real Market Trader ?

Who needs the other more?

BARC JPMC

BOA DB

CITI UBS

€

€

€

€€

€

€

Speculation

Trade

Speculation

Trade

Algorithmic

Speculation

Trade

Government

Intervention

Case Study – Swiss National Bank

• 2010 – The global economy is in deep recession and many Hedge Funds are seeking “Safe Havens” for their billions (usually US Dollar and Gold) and selling EUR.

• 2011 - The US Dollar is under pressure of weakening due to QE (Quantitative Easing), so the funds start buying CHF and selling EUR instead

• SNB warns them to desist as the increase in value of CHF against the EUR is killing exports and tourism.

• SNB acts and tells the market that they will sell CHF against the EUR without limit to hold the EUR.CHF rate at 1.20

• The Hedge Funds set up Algorithmic Trading models to continually test the floor and SNB do likewise to constantly buy at 1.20

Case Study – Swiss National Bank

• 2013 – Many retail gamblers enter the EUR.CHF deal to also capture free profits from this artificial intervention

• 2014 – SNB is now holding 45% of the value of GDP in EUR denominated products (cash, bonds, etc.)

• 2014 – European Central Bank considers 1.1Trn of QE and Greece election risks destabilizing the EUR

• 2015 – SNB takes snap decision to pull the 1.20 policy and instead charge 0.75% negative interest on those holding CHF

• Speculators are caught unawares and algorithmic models all have similar instructions to act and protect losses …

Case Study – Swiss National Bank

How to protect yourself

• Understand the currency risks and exposure in your business today (the risks may have been hidden by luck/low volatility)

• Do not be the company holding one currency (EUR) and needing to buy another currency (CHF) when the movement comes

• As soon as you have any exposure, pass the risk on to someone else, ideally immediately but soon as possible

• Don’t assume that “it will be OK, the rate will recover at some point”

Seize currency opportunities

• Once you have the risks under control, multi-currency pricing delivers significant revenue opportunities, without risk.

• If you control the presentation of pricing to the customer, you should be capturing the FX Revenues, rather than passing it to a 3rd party to manage, price and control.

• In traditional models, this would also mean either absorbing currency risk or giving away the majority of the revenue to protect the 3rd Party.

• With real-time management of currency risk, the potential exists to capture all the revenue, deliver a better service to customers and still outsource the risk to a 3rd party.

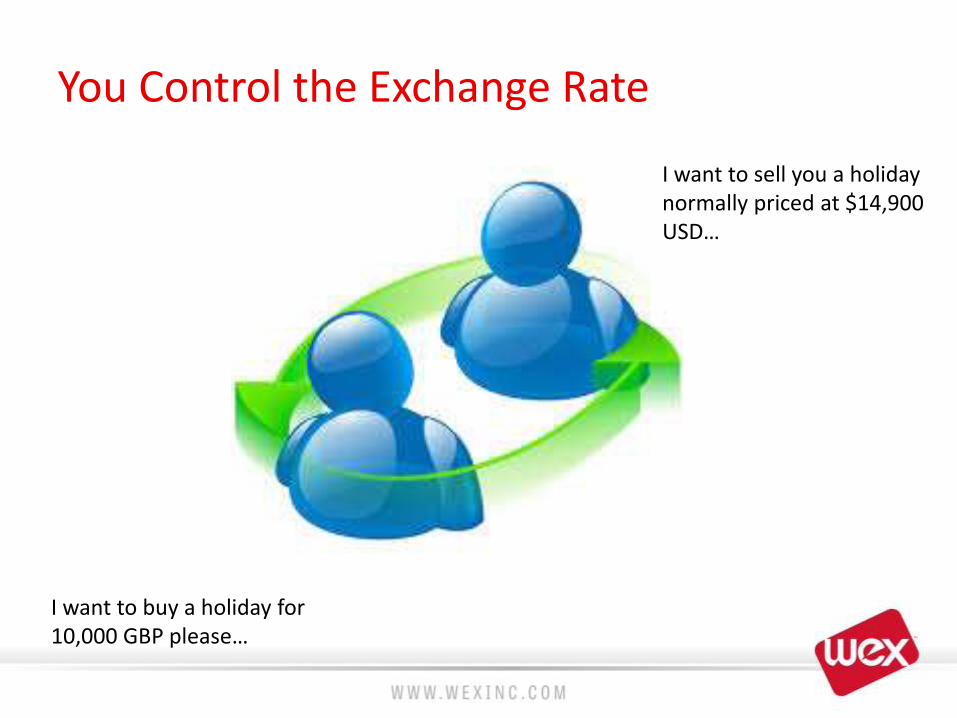

You Control the Exchange Rate

I want to sell you a holiday normally priced at $14,900 USD…

I want to buy a holiday for 10,000 GBP please…

You Control the Exchange Rate

I will sell you the holiday at 10,000 GBP (The rate of exchange is 1.52 therefore generating 300USD or 2% of FX Revenue).

I get the holiday I wanted at the price in GBP that I wanted without FX Risk

WEX Solutions

By booking the transaction via WEX Virtual Platform, I have booked the 10,000 GBP and the WEX solution has automatically sold the GBP 10,000 and I will receive 15,200 USD, locking in my 300 USD of FX Revenue.

Virtual Payments - Cross Border and FX Fees

Virtual Payments – Cross Border Fees

Payer

Merchant

Non-Domestic

CB = 80 bps

Virtual Payments – Cross Border Fees

Payer

Merchant

Intra - SEPA

CB = 3 bps

Virtual Payments – FX Fees

CAD $

USD $

MXN $

BRL R$

GBP £

EUR €

SEK kr

NOK kr

CHF

ZAR R

HKD $

THB ฿

MYR RMSGD $

AUD $

NZD $

AED

DKK kr

JPY ¥

PLN

Virtual Payments – FX Fees

CAD $

USD $

MXN $

BRL R$

GBP £

EUR €

SEK kr

NOK kr

CHF

ZAR R

HKD $

THB ฿

MYR RMSGD $

AUD $

NZD $

AED

DKK kr

Payer

Merchant

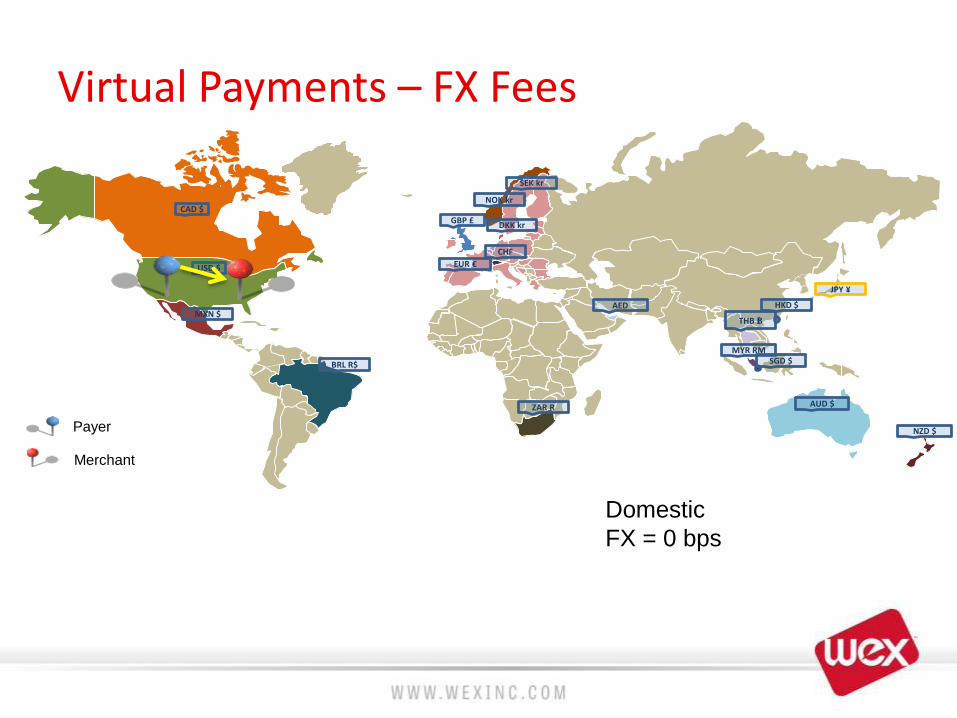

Domestic

FX = 0 bps

JPY ¥

Virtual Payments – FX Fees

CAD $

USD $

MXN $

BRL R$

GBP £

EUR €

SEK kr

NOK kr

CHF

ZAR R

HKD $

THB ฿

MYR RMSGD $

AUD $

NZD $

AED

DKK kr

Payer

Merchant

Non-Domestic

FX = 20 bps

JPY ¥

Virtual Payments – FX Fees

CAD $

USD $

MXN $

BRL R$

GBP £

EUR €

SEK kr

NOK kr

CHF

ZAR R

HKD $

THB ฿

MYR RMSGD $

AUD $

NZD $

AED

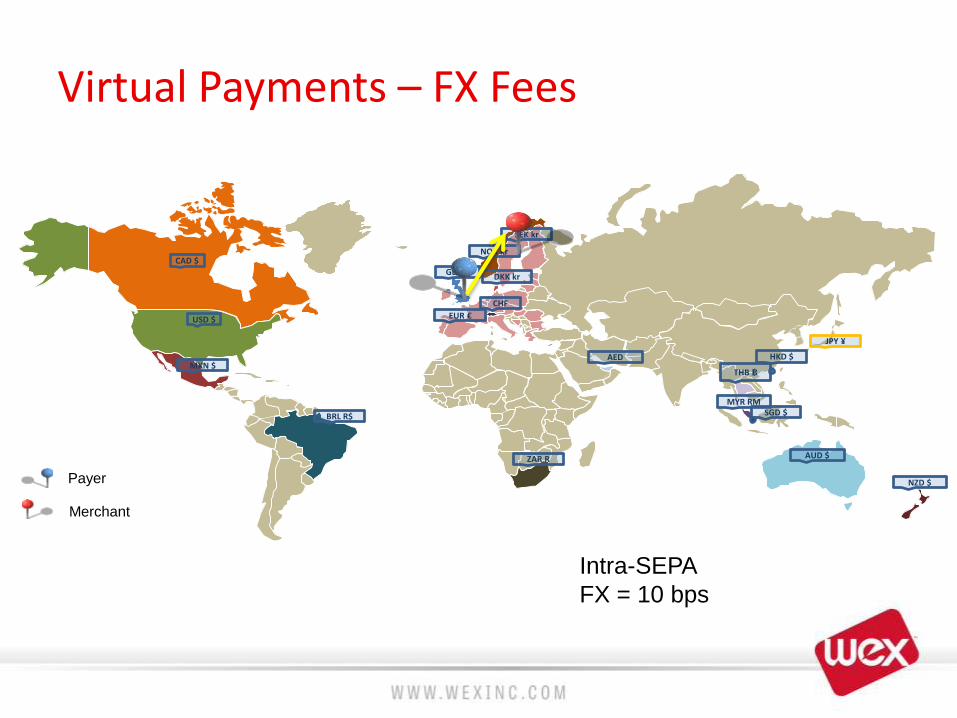

DKK kr

Payer

Merchant

Intra-SEPA

FX = 10 bps

JPY ¥

Virtual Payments - CB and FX Fees Summary

• Cross Border Fees

– Issuing country vs. Merchant country

– Can be reduced by issuing from multiple countries

• FX Fees

– Virtual Card Billing Currency vs Merchant Currency

– Can be reduced by issuing in multiple currencies

Thank you!

Send your questions and comments to

Replay and presentation of webinar will be available on

www.tnooz.com