how the financial aid process works ruth pusich director of financial aid elmhurst college

TRANSCRIPT

How the Financial Aid

Process Works

Ruth PusichDirector of Financial Aid

Elmhurst College

Topics• Federal Methodology

• CSS Profile

• Types, Categories and Sources of Financial Aid

• Educational Loans

• Understanding the Financial Aid Award/Package

• Net Price Calculators

Federal Methodology• The Federal Need Analysis Methodology is used by the federal

and state governments, as well as colleges, to award federal and state financial aid. It is regulated by the U.S. Congress and is administered by the U.S. Department of Education. The FM takes into consideration income, assets, expenses, family size, and other factors to help evaluate a family's financial strength. The information used for FM analysis is collected on the Free Application for Federal Student Aid (FAFSA).

• The FM determines a student's expected family contribution (EFC) for an award year for the student financial aid programs authorized under title IV of the Higher Education Act of 1965.

• An EFC is the amount that a student and his or her family may reasonably be expected to contribute toward the student's postsecondary educational costs for purposes of determining financial aid eligibility.

Financial Aid is money that is gifted, earned or borrowed

to pay for educational expenses

Federal Methodology• Free Application for Federal Student Aid (FAFSA)

o Calculates the EFCo Foundation for special circumstances and professional

judgments

• Self-report web-based applicationo Requires a PIN to sign application

• Gathers data from student and parentso Demographics of student and parent(s)

• Family size• Enrolled college students

o Income /Assets o May need to use 2011 income tax information if 2012 taxes are

not completed

• Information is forwarded to reported state of residence

• State of Illinois and many Schools have deadlines• Schools may require FAFSA for scholarships• Annual application

• Website: www.fafsa.gov o Available on January 1, 2013

for 2013-2014

• FAFSA on the Web Worksheet:o “Pre-application” worksheeto Questions follow order of

FAFSA

• Website: www.pin.ed.govo Sign FAFSA electronicallyo Not required, but speeds

processingo Used by students and parents

throughout aid process, including subsequent school years

FAFSA• Student is the “OWNER” of the FAFSA• Each college student in a family would need separate

FAFSA• Eligibility:

o US Citizen or eligible non citizeno Enrolled in an accredited institution, working towards a degree, earning

credit, and making good academic progress

• Who is a dependent student?o 13 questions to determine dependency statuso If a student is dependent based on the questions, the income

of the parent(s) MUST be included on the FAFSA

• Size of family and number in college• Can send to 10 schools• Calculation will give the EFC• Used by all schools to determine “need”

FAFSA• Who is the parent?

o Traditional family – both biological parents

o Separated or Divorced parents• Use the income information from the parent

that the student lives with most of the time (51% of the time)

• If this parent is married – income of stepparent would also be included

• If other biological parent is providing child support, it would be reported as “untaxed” income

What You Need• Student’s Information

o Legal nameo Birthdateo Social Security Numbero High School nameo If the student is male, are they registered for Selective

Service?o Income Information

• 2012 taxes if filed; and/or• W2s if student worked in 2012 but did not file taxes

o Asset Information• Cash, savings, savings bonds, UTMAs, UGMAs, stocks,

bonds• Investments

o PIN Number for signature

What You Need• Parent(s) Information

o At least one parent• Legal name • Birthdate • Social Security Number

o Income Information• 2012 taxes if filed; and/or• W2s (income from work)

o Asset Information• Cash, savings, savings bonds, 529 plans, stocks, bonds• Investments

o PIN Number for signature

What You Need

What are Assets?• Include:

o Real Estate other than your personal homeo Cash, savingso Stocks, bonds, investmentso 529 plans

• Do Not Include:o Value of homeo Value of Retirement accountso Value of Life Insurance policieso Value of family business with less than 100 FT employees

IRS Data Retrieval NOT REQUIRED

RECOMMENDED FOR ACCURACY• May submit real-time request to IRS for tax

data

• IRS authenticates taxpayer’s identity (PIN)

• If match found, IRS sends real-time results to applicant in new window

• Applicant chooses whether or not to transfer data to FAFSA

Federal Methodology• Income Protection

o Students - $6,000 threshold• 50% of income over $6000 factored into EFC

o Parents• Employee expenses• State and other tax allowances • Social Security tax calculation

• Asset protectiono Students

• 20% of every dollar in cash, savings, investments, etc.

o Parents• Exclusion - based on age (45/$41,300 or 55/$53,400)• 7% of discretionary net worth

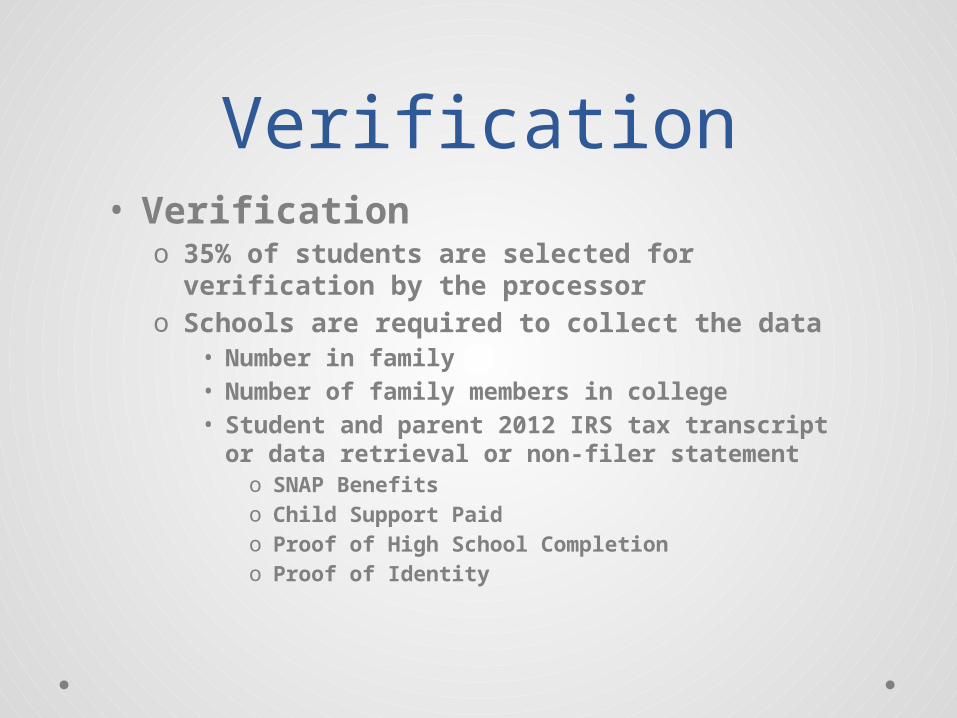

Verification• Verification

o 35% of students are selected for verification by the processor

o Schools are required to collect the data• Number in family• Number of family members in college• Student and parent 2012 IRS tax transcript or

data retrieval or non-filer statemento SNAP Benefitso Child Support Paido Proof of High School Completion o Proof of Identity

Verification• Some schools “verify” every student every

year

• Some schools ask for data based on the answers to the questions on the FAFSA

• Schools cannot disburse federal funds if they do not receive required paperwork

• Must provide the requested information only to the school that the student attends

Institutional Methodology

CSS/Financial Aid ProfileThough the federal government may be the largest single source of

financial assistance for families, a significant amount of aid comes from the colleges themselves. The IM is used by many colleges and private scholarship programs to determine students' eligibility for their own private funds. These institutions or programs may require students to complete the CSS/Financial Aid PROFILE® in addition to the FAFSA.

• Financial Aid application service of the College Boardo Over 400 colleges and scholarship programs use data

• $9 application feeo $16 for each college or scholarship program

• Includes more detailed financial informationo Institutional methodology is used to determine awards

• Can begin to complete after October 1

Assembling Financial Aid

oVariables:o Cost of Attendance (COA)

o FAFSA results (EFC)

o Need (COA – EFC = Need)

o Academic credentials

o Eligibility for specific aid programs

Cost of AttendanceVaries between schools:

• Direct Costso Tuition/feeso Roomo Board

• Indirect Costo Bookso Travel expenseso Miscellaneous Personal expenses

Financial Need and EFC

X

Y

Z

Cost of Expected Family NeedAttendance Contribution (Va ria b le ) (Va ria b le ) (Co ns ta n t)

1

2

3

EFC EFC

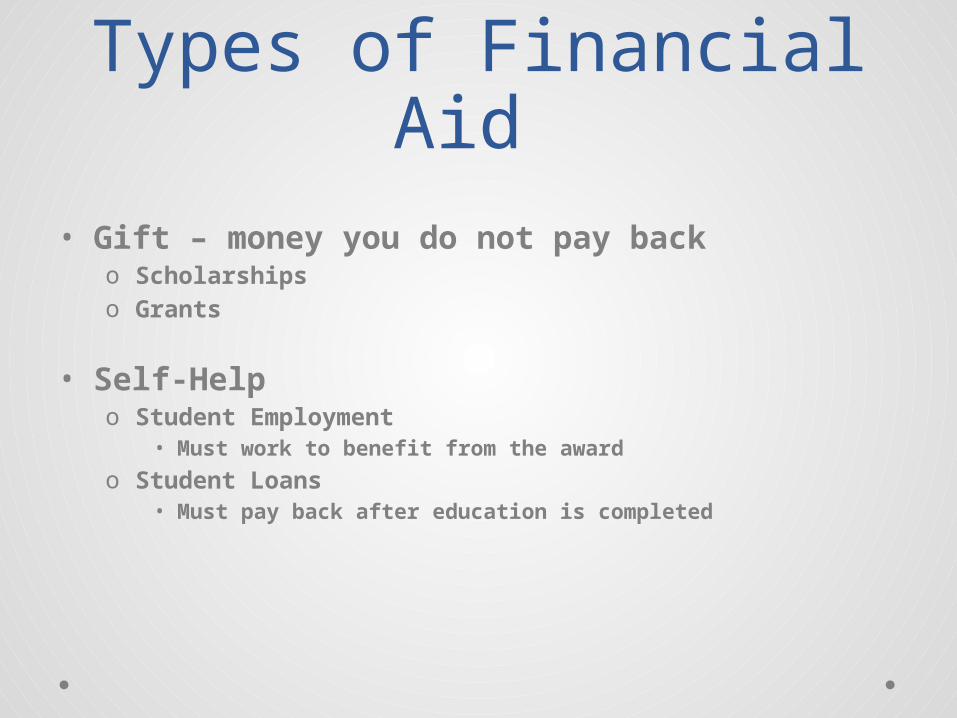

Types of Financial Aid • Gift – money you do not pay back

o Scholarshipso Grants

• Self-Helpo Student Employment

• Must work to benefit from the awardo Student Loans

• Must pay back after education is completed

Categories of Financial Aid

• Need Based (considers income of family)o Grantso Federal work studyo Perkins and subsidized loans

• Non-Need Based (does not consider income or assets)o Merit/talent based scholarshipso Unsubsidized and Parent loans

Sources of Financial Aid

FederalPell Grant/FSEOG Federal Work StudyStudent and Parent Loans

StateIL – Monetary Award ProgramTeacher Scholarships

Golden Apple

InstitutionMerit-based ScholarshipsTalent/Athletic ScholarshipsNeed-based Grants

Local organizations

Usually limited to one-year

EmployersTuition Reimbursement

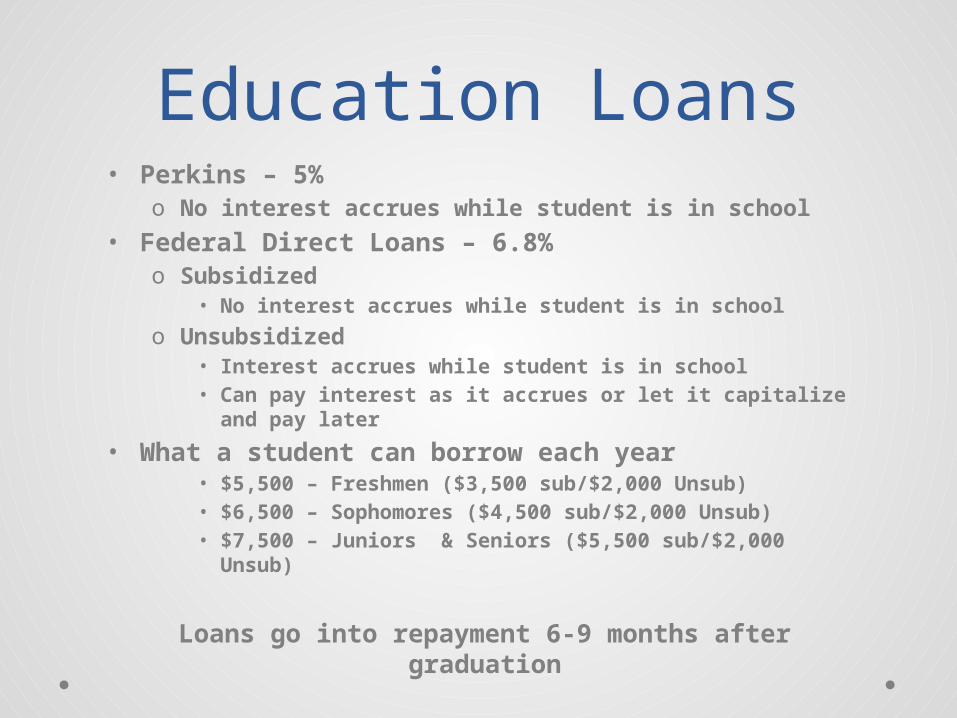

Education Loans• Perkins – 5%

o No interest accrues while student is in school

• Federal Direct Loans – 6.8%o Subsidized

• No interest accrues while student is in schoolo Unsubsidized

• Interest accrues while student is in school• Can pay interest as it accrues or let it capitalize

and pay later

• What a student can borrow each year• $5,500 – Freshmen ($3,500 sub/$2,000 Unsub)• $6,500 – Sophomores ($4,500 sub/$2,000 Unsub)• $7,500 – Juniors & Seniors ($5,500 sub/$2,000

Unsub)

Loans go into repayment 6-9 months after graduation

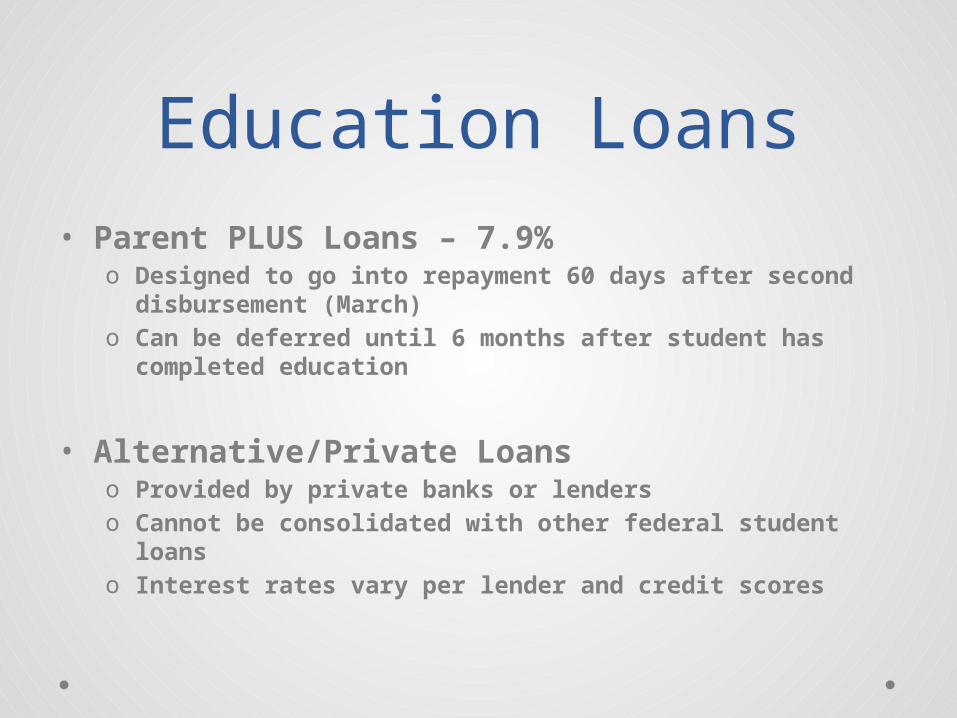

Education Loans• Parent PLUS Loans – 7.9%

o Designed to go into repayment 60 days after second disbursement (March)

o Can be deferred until 6 months after student has completed education

• Alternative/Private Loanso Provided by private banks or lenderso Cannot be consolidated with other federal student loanso Interest rates vary per lender and credit scores

Award Letter/Package• Formal presentation of types and

amount of financial aid a student is eligible to receive at a specific school

• Result of either a scholarship award or the submission of the FAFSA

• May be delivered via email or in paper form – or both

• Will provide Cost of Attendance and uncovered expenses

Award Letter/Package• Will include all forms of financial aid (most

schools)

• Will also include very important consumer information

• May include a “Shopping Sheet”

• May have deadlines to respond

• Award letters do not constitute a commitment to attend an institution unless you have made a binding commitment with a schoolo Early Decision

Award Letter/Package• May need to provide verification

information to the schoolo Some schools require all paperwork prior to the award o Other schools will send the award package and request

information

• Read everything to understand the restrictions of various awardso Enrollment statuso Renewabilityo Grade maintenance

Award Letter/Package• Each school will have directions on

methods of responding to letter or package

• Accept scholarships and/or grantso May need to return a signed paper copy of lettero May be directed to a secure website for acceptance

• Loans may or may not be included in award package depending upon type of schoolo May need to decline student loans (passive)o Accept student loans (active)

• Master Promissory Note• Entrance Counseling

Award Letter/Package• Compare Award Packages with schools on your hot list

o Add up Direct Costs (charges billed by the school)• Tuition/fees• Room/board

o Add up “Gift” aid only (do not include FWS or loans)• Scholarships• Grants

o Real Cost of a school:

Direct Costs - Gift Aid

Bottom Line

Net Price Calculator• Federally mandated law as of October 29, 2011

• All undergraduate schools must have a calculator easily accessible on their website

• Designed for the first-time new freshman student

• Calculators will vary by school

• Amount of information received will vary by school

• Will ask for income and asset information – basic

• For estimated EFC use FAFSA4caster on www.FAFSA.gov

CONCLUSION• Read everything you receive

• Do not make any assumptions

• Ask questions when in doubt

?

Be very cautious about paying money to an individual to file the FAFSA or

search for scholarships