housing finance market in poland - efbs

TRANSCRIPT

Housing Finance Market in Poland

Regulations & Initiatives

Dr. Jacek Furga

Chairman of the Real Estate Finance Committee

at Polish Banks Association

Situation on housing loans market

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1 - Q22016

112 141 162 218

302 314 287 189 230 231 197 177 174 181

94

290 405

521

717

945

1.136

1.303 1.374

1.449

1.631 1.732

1.820 1.897

1.995 2.028

number of new loan agreements [thousand] total number of active housing loans [thousand]

Source: Polish Banks Association - SARFiN

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1 - Q22016

7,4 11,3 15,2 24,2

42,0 55,9 57,1

38,7 48,7 49,2

39,1 36,5 36,8 39,3 20,0 19,5

29,6 35,8 50,4

77,7

116,8

192,6

214,9

263,6

313,7 316,3 330,8

350,4

374,1 382,9

value of new loan agreements [PLN billion] total debt from housing loans [PLN billion]

Situation on housing loans market

Source: Polish Banks Association - SARFiN

Average value of a housing loan (in PLN; € 1 = PLN 4,3)

76

.22

0

81

.34

0

94

.24

0

10

9.5

50

13

9.1

40

18

7.2

90

20

5.1

80

20

2.4

48

20

5.9

54

20

7.5

71

19

5.5

99

20

0.0

70

20

6.5

52

21

2.6

49

21

2.5

64

0

50.000

100.000

150.000

200.000

250.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1 - Q22016

Source: Polish Banks Association - SARFiN

Currency structure of the value of new loans

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q 12008

Q 32008

Q 12009

Q 32009

Q 12010

Q 32010

Q 12011

Q 32011

Q 12012

Q 32012

Q 12013

Q 32013

Q 12014

Q 32014

Q 12015

Q 32015

Q 12016

PLN CHF EUR Other

Source: Polish Banks Association - SARFiN

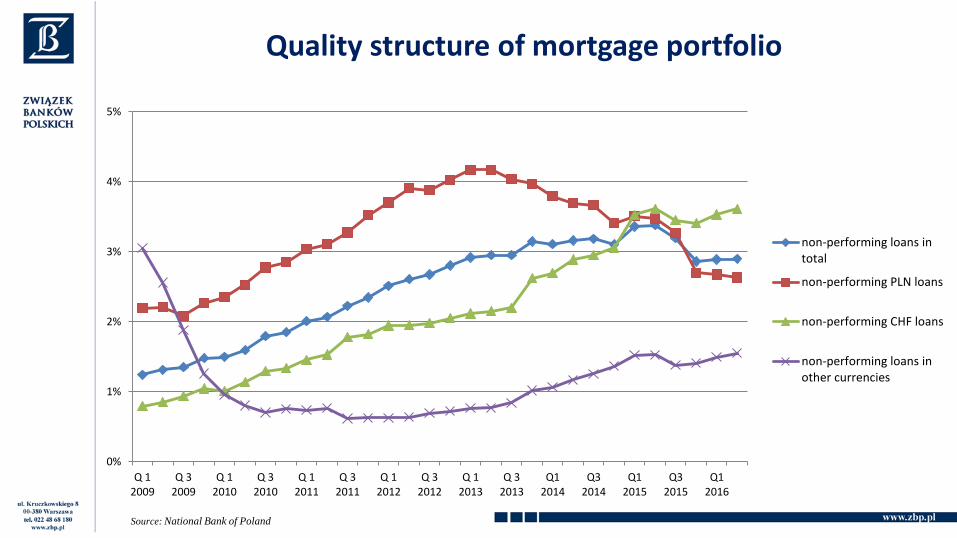

0%

1%

2%

3%

4%

5%

Q 12009

Q 32009

Q 12010

Q 32010

Q 12011

Q 32011

Q 12012

Q 32012

Q 12013

Q 32013

Q12014

Q32014

Q12015

Q32015

Q12016

non-performing loans intotal

non-performing PLN loans

non-performing CHF loans

non-performing loans inother currencies

Quality structure of mortgage portfolio

Source: National Bank of Poland

Number of new housing loans granted under the ’Family On Its Own’ Programme (RnS)

0

10.000

20.000

30.000

40.000

50.000

60.000

2007 2008 2009 2010 2011 2012 2013

4.0

01

6.6

45

30

.88

2

43

.12

0 51

.32

8

48

.79

2

10

.59

2

Source: BGK

Number of new housing loans granted under the ’Flat for Youth’ (MdM) Programme

0

5000

10000

15000

20000

25000

30000

2014 2015 2016 2017 2018

9.1

41

21

.88

8 2

7.1

09

12

.56

4

33

5

Source: BGK

Source: National Bank of Poland, Ministry of Finance

Households savings [PLN billion]

58,6 52,2 58,0 63,0 61,5 65,1 65,2 63,6 65,2 65,1

0

200

400

600

800

1000

1200

1400

2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1 - Q2 2016

in PLN billion in relation to GDP [%]

Source: ‚Polish attitudes towards finances’ Report, Kronenberg Foundation

at Citi Handlowy Bank, 2015

Propensity to save in Poland

35%

43%

16%

6%

don't save occasional saving systematic saving no answer

Source: National Bank of Poland, Central Statistical Office, Ministry of Finance

57,7%

13,6%

11,2%

4,6% 8,5%

0,5% [WARTOŚĆ] 2,9%

deposits cash

OFE capital insurance funds

investment funds foreign investment funds

government bonds stocks

Structure of household savings in June 2016 (total € 279 billion)

Source: National Bank of Poland

Structure of bank deposits of households in June 2016 (total € 160 billion)

54,0%

43,5%

2,5%

overnight deposits

deposits with agreed maturity of up and including two years

other fixed-term deposits

Prices of dwellings in major Polish cities (PLN per sq. m.)

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Warsaw Bialystok Katowice agglomeration Wroclaw Gdansk Cracow Poznan Lodz

Source: AMRON Centre

14

First pillar : Apartments for rent constructed on the State land:

Dedicated to families who do not have credit worthiness to get a

mortgage and their incomes are sufficient to pay the market rent;

Assumed rental fee: PLN 10-20 per sq. m. per month (construction cost) + building operation costs

′The ownership path’ as a possible option (rental fee higher by 20%);

Construction projects financed by selling the land from the ′land bank′ (the State Treasury, local government units and private entities land transferred in exchange for the investment certificates enabling to participate in the National Housing Fund profits);

Start of construction projects: first half of 2018

National Housing Programme (′Flat Plus′ Programme)

15

Second pillar: State’s support for the social rental housing:

Programme supporting construction of housing with low or moderate rent, used in the formula of social rental housing;

Programme intended for people whose income is too high to get a house from the municipality and too low to purchase or rent an apartment on the market;

Local governments allowed to apply for funding in the amount of 35-55% of the project construction costs;

Local governments, municipal companies and social housing societies allowed to apply for preferential loans at Bank Gospodarstwa Krajowego

Start of application process: year 2018

National Housing Programme ('Flat Plus' Programme)

16

Third pillar: State’s support for saving for housing purposes:

Savings collected on Individual Housing Accounts (IKM), held by banks and credit unions;

Tax exemptions (concerning interest accrued on deposited savings) and additional support in the form of State’s bonuses are planned;

Planned value of the suport: approx. PLN 1 billion per year ;

Implementation schedule: adoption of the draft law by the Council of Ministers in the second quarter of 2017, first saving accounts (IKM) in 2018.

National Housing Programme ('Flat Plus' Programme)

17

Savings collected on Individual Housing Accounts (IKM)

saving rules:

minimum period of saving: 60 months,

no limit on the length of saving period,

one saving account (IKM) per one saver,

maximum limit of savings entitling to tax exemption and maximum level of State bonus to be specified in the Act;

National Housing Programme ('Flat Plus' Programme)

18

A comprehensive plan to create a voluntary capital saving system and long-term investment products in Poland

8 key pillars of the Programme:

1. Employee Capital Plans (PPK); 2. Individual Capital Plans (IPK) for microenterprises;

3. Polish Development Fund;

4. Central Electronic Registry of pension schemes;

5. Public Real Estate Funds (′Polish REITs′);

6. Premium bonds and project bonds;

7. Lower taxes on income from long-term investments lasting more than 1 year;

8. Reconstruction model of the Open Pension Funds (OFE).

Responsible Development Strategy (Capital Building Programme)

19

Estimated total cost of PPK and IPK fiscal incentives: approx. PLN 2.2 billion (0.11 percent. of GDP) during the first two years and PLN 1.7 billion (0.08 percent) in the following years.

• Capital Building Programme expected results:

5.5 million more participants of the third pillar pension system (assumptions: participation of 75% employees ),

more than PLN 12 billion new savings in the third pillar per year at an average premium of 4%,

more than PLN 120 million (nearly 5 percent of GDP) inflow of the new funds to the Polish capital market after 10 years,

Capital Building Programme