hotel istana, kuala lumpur filehotel istana, kuala lumpur. 2 presentation outline 1. sales tax &...

TRANSCRIPT

1

ENFORCEMENT, PENALITIES AND OFFENCES GOVERNING SST (2018) IN MALAYSIA

PRESENTED BY D.MARTIN JOSEPH

NATIONAL SEMINAR ON SST IMPLEMENTATION20TH SEPTEMBER 2018

HOTEL ISTANA, KUALA LUMPUR

2

PRESENTATION OUTLINE

1. SALES TAX & SERVICE TAX LEGISLATION 2018

2. RESPONSIBILITIES & LIABILITIES OF SST REGISTRANTS 2018

3. SALES TAX OFFENCES & PENALTIES 2018

4. SERVICE TAX OFFENCES & LIABILITIES 2018

5. GENERAL PENALITIES & COMPOUNDING OF OFFENCES,REVIEW & APPEAL

6. ENFORCEMENT OF SALES TAX & SERVICE TAX 2018

7. ANTI PROFITEERING LEGISLATION

3

SALES TAX LEGISLATION1. Sales Tax Act 2018

2. Regulation2.1 Sales Tax Regulation 20182.2 Sales Tax (Determination of Sales Value of Taxable Goods) Regulation 2018 (valuation)2.3 Sales Tax (Compounding of Offences) Regulation 2018 (List of Offences)2.4 Sales Tax (Customs Ruling) Regulation 2018

3. Orders3.1 Appointment of Date of Coming into Operation3.2 Sales Tax (Exemption from Registration) Order 2018 (20 items)3.3 Sales Tax (Exemption from Tax) Order 2018 (Nil ST)3.4 Sales Tax (Imposition of Tax in Respect of Designated Area) Order 2018 (Labuan & Tioman)3.5 Sales Tax (Imposition of Tax in Respect of Special Area) Order 2018 (Free Zones)3.6 Sales Tax (Persons Exempted from Payment of Tax) Order 2018 (Sch. A, B, C)3.7 Sales Tax (Rate of Tax) Order 2018 (Sch. 1 & 2)3.8 Sales Tax (Total Value of Taxable Goods) Order 2018 (threshold)

4

1. Service Tax Act 2018

2. Regulation

2.1 Service Tax Regulation 20182.2 Service Tax (Compounding of Offences) Regulation 2018 (List of Offences)2.3 Service Tax (Customs Ruling) Regulation 2018

3. Orders3.1 Appointment of Effective Date for Charging & Levying of Service Tax 3.2 Service Tax Appointment of Coming into Operation (the Act)3.3 Service Tax (Imposition of Tax for Taxable Service in Respect of Designated & Special Areas) Order 20183.4 Service Tax (Rate of Tax) Order 2018

SERVICE TAX LEGISLATION

5

RESPONSIBILITIES AND LIABILITIES OF AN SALES TAX REGISTRANT

1. Imposition of Sales Tax (s.8) [ taxable goods sold, disposed off or used &taxable goods imported]

2. Determination of value (s.9) [ valuation of manufactured & imported goods]

3. Rate of Tax (s.10) [10%, 5% or specific]

4. Sales Tax due (s.11) [ sold, disposed of otherwise than by sale or first used otherwise than in mfg.]

5. Application for registration (s.13) [ liable to be registered 1st day of following month]

6. Notification of cessation of liability (s.18) [notify DG within 30days of cessation]

7. Invoices (s.21) [ Bahasa or English, prescribed particulars]

8. Duty to keep records (s.24) [all records relating to sales tax, Bahasa or English, 7 years]

9. Furnishing of returns (s.26) [according to taxable period & payment of sales tax]

10. Evasion of sales tax (s.86) [ incorrect info, false statement , omits info to fraud in return]

11. Giving incorrect information (s.87) [relating to liability to sales tax]

12. Improperly obtaining refund (s.88) [obtaining refund thru fraud]

13. Obstruction (s.92) [obstructs, assaults or hinders officer ]

14. Offence by companies (s.93) [directors, partners , compliance officer, secretary & manager of company]

6

RESPONSIBILITIES AND LIABILITIES OF AN SERVICE TAX REGISTRANT

1. Imposition of Service Tax (s.7) [prescribed taxable service by registrant]

2. Taxable service (s.8) [prescribe by minister]

3. Determination of value of taxable service (s.9) [ connected, not connected, free, betting & gamming, insurance]

4. Rate of service tax (s.10) [6% & specific]

5. Service tax due (s.11) [when payment received by registrant]

6. Liability to be registered (s.12) [ threshold reached, historical or future method whichever is the earlier]

7. Application for registration (s.13) [not later than the last day of the month following the month he is liable]

8. Notification of cessation of liability (s.19) [notification to DG within 30 days of cessation]

9. Invoices (s.21) [prescribed particulars, national language & English]

10. Duty to keep records (s.24) [all records relating to tax , National Language or English , 7 years]

7

RESPONSIBILITIES AND LIABILITIES OF AN SERVICE TAX REGISTRANT

11. Furnishing of returns and payment of tax (s.26) [last day of the month following taxable period with payment]

12. Liability of directors (s.33) [directors, partners , compliance officer, secretary & manager of company, office bearers

of society severely liable]

13. Persons bound to give information (s.57) [bound to give information anything relating to tax]

14. Access to places or premises (s.58) [ provide facilities, provide , all documents , goods, articles , take copies of

documents]

15. Evasion of tax (s.71) [ incorrect info, false statement , omits info to fraud in return]

16. Giving incorrect information (s.72) [incorrect info relating to his liability to tax]

17. Improperly obtaining refunds (s.73) [obtaining refund thru fraud]

18. Obstruction (s.77) [obstructs, assaults or hinders officer ]

19. Offence by companies (s.78) [directors, partners , compliance officer, secretary & manager of company]

SALES TAX ACT 2018

OFFENCES AND PENALTIES

8

9

OFFENCES PENALTIES

LIABILITY TO BE REGISTERED S.12

- Any manufacturer who is liable to be registered

shall apply not later than the last day of the month

following the month he is liable to be registered)

Any manufacturer who fails to register

commits an offence S13(5)

• Fine : Not exceeding RM 30,000;(S.94)

• Imprisonment : Not exceeding 2 years

• Or both

NOTIFICATION OF CESSATION OF LIABILITY S. 18

- A manufacturer who ceases manufacturing taxable

goods or who ceases to be liable to be registered, shall

notify DG within 30 days from the date of cessation.

Any person who contravenes commits an

offence S18(2)

• Fine : Not exceeding RM 30,000;(S.94)

• Imprisonment : Not exceeding 2 years

• Or both

INVOICES S.21(1)- (1) Every registered manufacturer who sells any taxable

goods shall issue an invoice.- (2) No invoice showing sales tax if not taxable goods or if

not a registered manufacturer- (3) Amount of ST shall be collected for the taxable goods

Any person who contravenes subsection (1),

(2) or (3) commits an offence

• Fine : Not exceeding RM 30,000;(S.94)

• Imprisonment : Not exceeding 2 years

• Or both

SALES TAX ACT 2018

10

OFFENCES PENALTIES

DUTY TO KEEP RECORDS S.24

- Every taxable person shall keep complete & true records

up to date of all transactions

- Kept for 7 years; in BM or English in Malaysia

- Records readily accessible; admissible in court

Any manufacturer who contravenes commits

an offence & shall be liable to a fine not

exceeding Fifty thousand ringgit or

imprisonment Not exceeding 3 years or to

both S24(6)

FURNISHING OF RETURNS & PAYMENT OF SALES

TAX DUE AND PAYABLE S.26

- A registered person is required to furnish a return and

shall pay to the DG the amount of Sales Tax due and

payable.

A taxable person who contravenes section

26; OR furnishes an incorrect return commits

an offence & shall be liable to a fine not

exceeding Fifty thousand ringgit or

imprisonment Not exceeding 3 years or to

both

LATE PAYMENT PENALTY s.26(9)- Where any Sales Tax due & payable is not paid wholly or partly, the taxable person shall pay late penalty charges

First 30 days – Penalty of 10 %

Second 30 days – Penalty of 15 %

Third 30 days – Penalty of 15 %

(of the amount unpaid)

SALES TAX 2018

11

EVASION OF SALES TAX (S.86)

Any person who, with intent to evade or to assist any other

person to evade Sales Tax –

Omits from a return any information;

Makes any false statement or entry in any return, claim or application;

Gives any false answer to any Question or information under this Act;

Prepares or maintains any false book of accounts; invoices or falsifies any records; or

Makes use of any fraud, artifice (deception) or contrivance

Any person who commits the above offence shall, on conviction be liable –

o First offence - Fine not less than 10 x & not more than 20 x of amount of Sales Tax

OR Imprisonment Not exceeding 5 years or to both

o Second or subsequent offence – Fine not < than 20 x & not > than 40 x of amount of

Sales Tax OR Imprisonment Not exceeding 7 years or to both

o If amount of Sales Tax cannot be ascertained – Fine of not < than RM50,000.00 & not

> than RM500,000.00 or to imprisonment Not exceeding 7 years or to both.

12

SERVICE TAX ACT 2018

OFFENCES AND PENALITIES

13

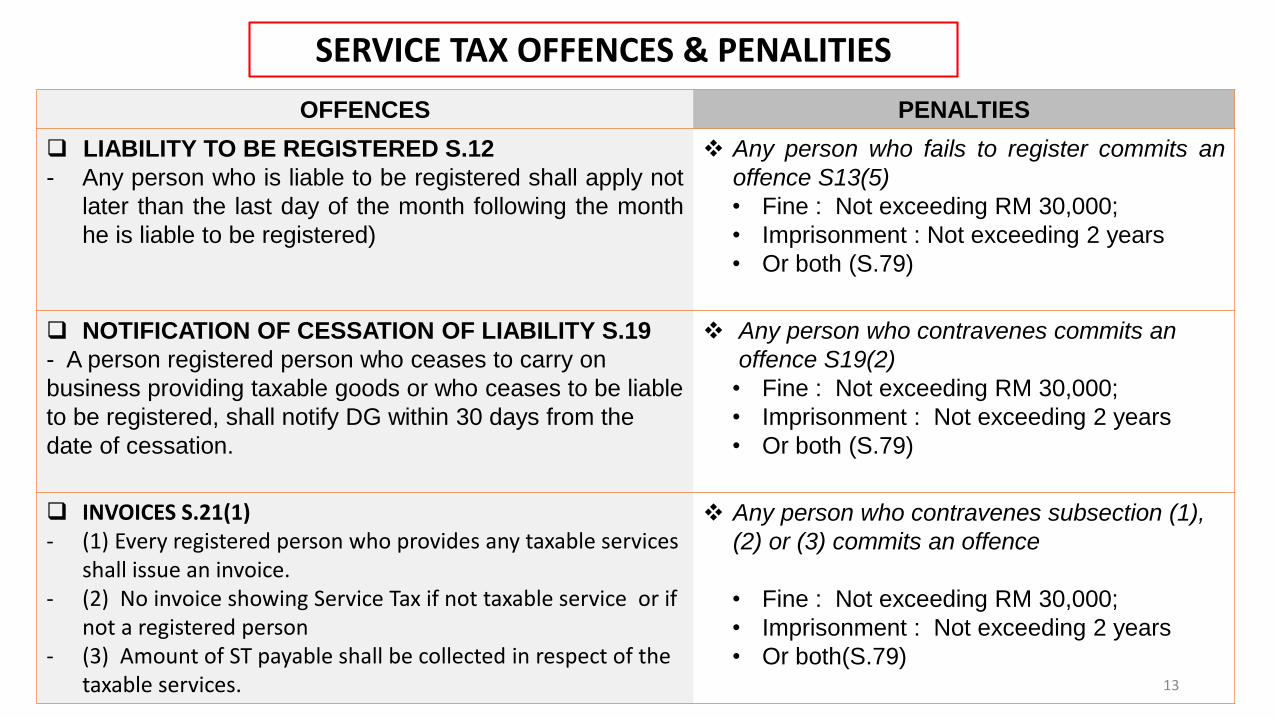

OFFENCES PENALTIES

LIABILITY TO BE REGISTERED S.12

- Any person who is liable to be registered shall apply not

later than the last day of the month following the month

he is liable to be registered)

Any person who fails to register commits an

offence S13(5)

• Fine : Not exceeding RM 30,000;

• Imprisonment : Not exceeding 2 years

• Or both (S.79)

NOTIFICATION OF CESSATION OF LIABILITY S.19

- A person registered person who ceases to carry on

business providing taxable goods or who ceases to be liable

to be registered, shall notify DG within 30 days from the

date of cessation.

Any person who contravenes commits an

offence S19(2)

• Fine : Not exceeding RM 30,000;

• Imprisonment : Not exceeding 2 years

• Or both (S.79)

INVOICES S.21(1)- (1) Every registered person who provides any taxable services

shall issue an invoice.- (2) No invoice showing Service Tax if not taxable service or if

not a registered person- (3) Amount of ST payable shall be collected in respect of the

taxable services.

Any person who contravenes subsection (1),

(2) or (3) commits an offence

• Fine : Not exceeding RM 30,000;

• Imprisonment : Not exceeding 2 years

• Or both(S.79)

SERVICE TAX OFFENCES & PENALITIES

14

OFFENCE PENALTIES

GIVING INCORRECT INFORMATION

RELATING TO LIABILITY OF SERVICE TAX

S.72

• Fine : not exceeding RM30,000;

• Imprisonment : not exceeding 2 years

• Or both (s.79)

IMPROPERLY OBTAINING REFUND S.73 • Fine : Not exceeding RM 30,000;

• Imprisonment : Not exceeding 2 years

• Or both (s.79)

OFFENCES BY AUTHORIZED &

UNAUTHORIZED PERSONS S.76

(defrauds, embezzles, uses position to deal

wrongfully)

• Fine : not exceeding RM 30,000;

• Imprisonment : Not exceeding 2 years

• Or both (s.79)

OBSTRUCTION S.77 • Fine : Not exceeding RM100,000;

• Imprisonment : Not exceeding 5 years

• Or both (s.77)

GENERAL PENALTY S.79

(Any offence under this Act for which no penalty is

expressly provided)

• Fine : Not exceeding RM 30,000;

• Imprisonment : Not exceeding 2 years

• Or both

SERVICE TAX OFFENCES & PENALITIES

15

OFFENCES PENALTIES

DUTY TO KEEP RECORDS S.24

- Every taxable person shall keep complete & true

records up to date of all transactions

- Kept for 7 years; in BM or English in Malaysia

- Records readily accessible; admissible in court

Any taxable person who contravenes

commits an offence & shall be liable to a fine

Not exceeding Fifty thousand ringgit OR

Imprisonment Not exceeding 3 years or to

both; S24(6)

FURNISHING OF RETURNS & PAYMENT OF

SALES TAX DUE AND PAYABLE S.26

- A registered person is required to furnish a return and

shall pay to the DG the amount of Service Tax due and

payable.

A taxable person who contravenes section

26 OR furnishes an incorrect return

commits an offence & shall be liable to a

fine not exceeding Fifty thousand ringgit or

imprisonment Not exceeding 3 years or to

both S.26(6)

LATE PAYMENT PENALTY s.26(8)- Where any Sales Tax due & payable is not paid wholly or partly, the taxable person shall pay late penalty charges

First 30 days – Penalty of 10 %

Second 30 days – Penalty of 15 %

Third 30 days – Penalty of 15 %

(of the amount of service tax unpaid) S.26(8)

SERVICE TAX OFFENCES & PENALITIES

16

EVASION OF SERVICE TAX (S.71)

Any person who, with intent to evade or to assist any other

person to evade Service Tax –

Omits from a return any information;

Makes a false statement or entry in any return, claim or application;

Gives any false answer to any Question or information under this Act;

Prepares or maintains any false book of accounts; invoices or falsifies any records; or

Makes use of any fraud, artifice or contrivance

Any person who commits the above offence shall, on conviction be liable –

o First offence - Fine not less than 10 x & not more than 20 x of amount of Sales Tax

OR Imprisonment Not exceeding 5 years or to both

o Second or subsequent offence – Fine not < than 20 x & not > than 40 x of amount of

Sales Tax OR Imprisonment Not exceeding 7 years or to both

o If amount of Sales Tax cannot be ascertained – Fine of not < than RM50,000.00 & not

> than RM500,000.00 or to imprisonment Not exceeding 7 years or to both. S.71(2)

17

GENERAL PENALTIES ,COMPOUNDING OF OFFENCES, REVIEW & APPEAL

18

GENERAL PENALTIES, COMPOUNDING OF OFFENCES, REVIEW & APPEAL

SALES TAX SERVICE TAX

• GENERAL PENALITIES S.94

• FINE NOT EXCEEDING RM30K OR 2 YEARS JAIL OR BOTH

• COMPOUNDING OF OFFENCES S.95(2)

• NOT EXCEEDING 50% OF THE MAXIMUM FINE PROVIDED

• Sales Tax (Compounding of Offences) Regulation 2018

• Review & Appeal S. 96• Appeal to DG within 30 days of

notification (except compound)

• GENERAL PENALITIES S.79

• FINE NOT EXCEEDING RM30K OR 2 YEARS JAIL OR BOTH

• COMPOUNDING OF OFFENCES S.80

• NOT EXCEEDING 50% OF THE MAXIMUM FINE PROVIDED

• Service Tax (Compounding of Offences) Regulation 2018

• Review & Appeal S.81 • Appeal to DG within 30 days of

notification (except compound)

19

ENFORCEMENT OF SALES & SERVICE TAX

20

ENFORCEMENT POWERS UNDER SST 2018

1. Power to assess (s.27)

2. Recovery of tax as civil debt (s.28)

3. Power to collect tax from persons owing (s.29)

4. Persons bound to give information (s.62)

5. Power to take samples (s.63)

6. Access to places or premises (s.64)

7. Access to recorded information (s.65)

8. Search with warrant (s.66)

9. Search without warrant (s.67)

10. Power to stop & search conveyance(s.68)

11. Seizure of goods (s.69)

12. Power of arrest (s.72)

1. Power to assess (s.27)

2. Recovery of tax as civil debt (s.28)

3. Power to collect tax from persons owing (s.29)

4. Persons bound to give information (s.57)

5. Access to places or premises (s.58)

6. Access to recorded information (s.59)

7. Search with warrant (s.60)

8. Search without warrant (s.61)

9. Seizure of goods (s.62

10. Power of arrest (s.63)

SALES TAX SERVICE TAX

21

POWER TO ASSESS S.27 SALES TAX

WHERE ANY TAXABLE PERSON –

(a) Fails to apply for registration under section 13;

(b) Fails to furnish a return under section 26; or

(c) Furnishes a return which appears to the DG to be

incomplete or incorrect

THE DG MAY ASSESS –

To the best of his judgement;

Amount of Sales Tax due and payable

The penalty payable under section 26(9)

Notify him in writing

22

LIABILITY OF DIRECTORS S.34 SALES TAX

Where Sales Tax due & payable, surcharge is accrued, or penalty,

fee or other money is payable by any Co, LLP, Firm , Society or

other body of persons -

The Directors of the Company;

Partners of the firm;

Office-bearers of the society;

Compliance officer of LLP; etc

Shall together with the Co, LLP, Firm, Society or other body of

persons be jointly & severally be liable for Sales Tax due &

payable, surcharge, or penalty, fee or other money.

23

ACCESS TO PREMISES OR PLACES S.58 SERVICE TAX

Any senior officer of service tax shall at all times have access to any place

or premise –

Persons to provide reasonable facilities (failure to provide is an offence under s.58(5)

Produce any goods, documents, articles or things which relates to the Act;

Examine any goods , documents, articles or things & take copies;

Seize & detain any goods, documents, articles or things as evidence

Require any person present therein to answer any questions relating to goods etc.

Require any container, envelope, or other receptacle therein to be opened or

At the risk & expense of the person therein open & examine any package or goods

If necessary use force to enter premise & open receptacle as he thinks fit

24

SEARCH MAY BE MADE WITHOUT WARRANT S.61 SERVICE TAX

Senior officer with reasonable cause to believe that items are concealed in any place,

premise or conveyance any goods, documents, articles or things which may afford

evidence of offence;

Reasonable grounds to believe that by reason of delay in obtaining a warrant the goods etc.

are likely to be removed;

He may enter the place

Arrest any person

Break open outer or inner door

Remove by force any obstruction

Detain every person therein

25

LEGISLATION – ANTI

PROFITEERING

26

LEGISLATION – ANTI PROFITEERING

The objective of the anti-profiteering laws –

NOT to prevent businesses from making any profit.

To Protect Consumers by from unethical traders & businesses

from making unreasonable high profit or profiteering

To ensure the Rights of consumers are not jeopardised

Price Control & Anti Profiteering Act 2011

Price Control & Anti Profiteering (Amendment) Act 2014

Price Control & Anti Profiteering (Mechanism to Determine

Unreasonably High Profit of Goods) Regulations 2018

27

The Price Control and Anti-Profiteering (Mechanism to Determine

Unreasonably High Profit) Regulations 2018 effective 6 June 2018

all businesses in supply of goods & services are governed by the 2018

Regulations

IMPLICATIONS FOR BUSINESSES

Businesses should undertake review of its pricing policies

Consumer awareness – Price comparison & initiate complaints

Businesses must ensure compliance & be able to substantiate the price

increase (adequate documentation & justification) to MDTCA (KPDNKK)

ANTI PROFITEERING LEGISLATION

28

PRICE CONTROL & ANTI – PROFITEERING ACT 2011

OFFENCE TO PROFITEER S.14 Any person who, in the course of trade or business, profiteers in selling or offering to sell

or supplying or offering to supply any goods or services commits an offence

“Profiteer” means making profit unreasonably high

OFFENDERS FIRST OFFENCE SECOND OFFENCE

Individual Fine – Not more than RM100,000

Imprisonment – Not > than 3

years

Or both

Fine – Not more than RM100,000

Imprisonment – Not > than 3

years

Or both

Body Corporate Fine – Not more than

RM500,000

Fine – Not more than

RM1,000,000

PENALTY

29

THANK YOU

D. Martin Joseph(hp. No. +60123759121)