holcim-ambuja-acc unlocking synergies. really? holcimambujaacc.pdfholcim-ambuja-acc unlocking...

TRANSCRIPT

Holcim-Ambuja-ACC Unlocking synergies. Really?

August 2013 *

Confidential

* Updated for regulatory clarifications

2

This presentation updates the original August 2013 presentation wrt to the clarifications by the Reserve Bank of India and by SEBI. Please see page 27 and 28.

Introduction

Should Holcim be paid Rs 35 bn given its stewardship of Ambuja and ACC?

What does IiAS recommend?

How should minority shareholders vote?

What are the other issues with this restructuring?

Do the synergies really exist?

3

Introduction

Should Holcim be paid Rs 35 bn given its stewardship of Ambuja and ACC?

What does IiAS recommend?

How should minority shareholders vote?

What are the other issues with this restructuring?

Do the synergies really exist?

4

Post transaction structure

Holcim

Ambuja

ACC

61.39%

50.01%

0.29%

Proposed restructuring of Holcim’s India Operations

• Should Holcim be paid Rs 35 bn given its stewardship of Ambuja and ACC?

• To answer this, we have assessed the performance of ACC and Ambuja under Holcim

• Do the “Synergies” really exist?

• To answer this, we have assessed the possible benefits to Ambuja shareholders from this

restructuring

Just two questions

Existing structure

Holcim

Holcim India

Ambuja

100%

40.79%

9.76% ACC

0.29%

50.01%

5

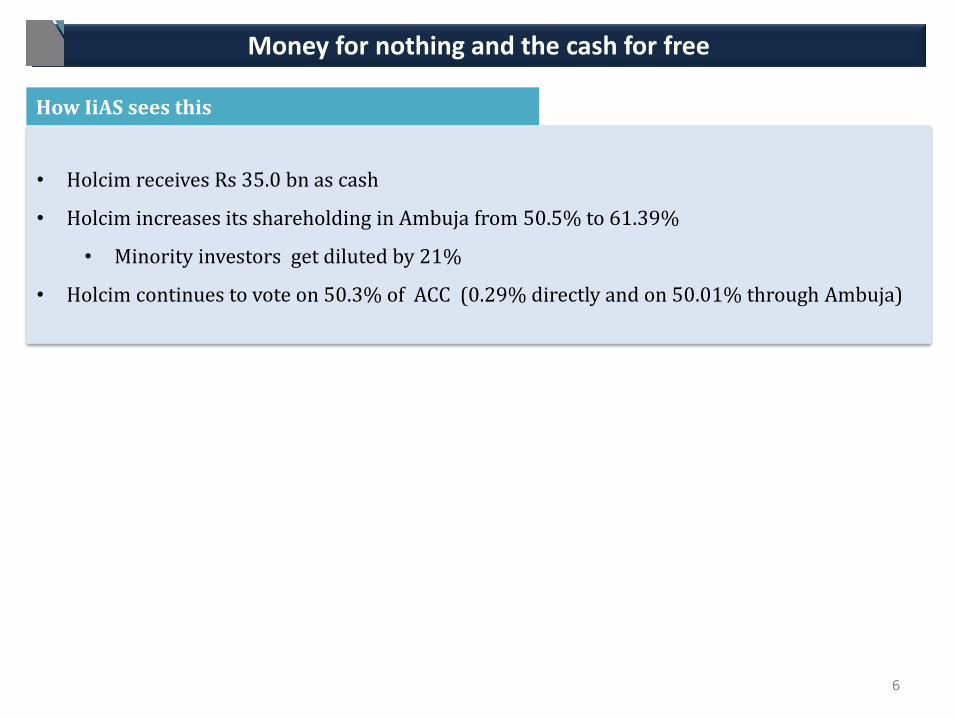

Money for nothing and the cash for free

• Holcim receives Rs 35.0 bn as cash

• Holcim increases its shareholding in Ambuja from 50.5% to 61.39%

• Minority investors get diluted by 21%

• Holcim continues to vote on 50.3% of ACC (0.29% directly and on 50.01% through Ambuja)

How IiAS sees this

6

Introduction

Should Holcim be paid Rs 35 bn given its stewardship of Ambuja and ACC?

What does IiAS recommend?

How should minority shareholders vote?

What are the other issues with this restructuring?

Do the synergies really exist?

7

Ambuja and ACC under Holcim

Operational performance

Financial performance

Corporate governance record

8

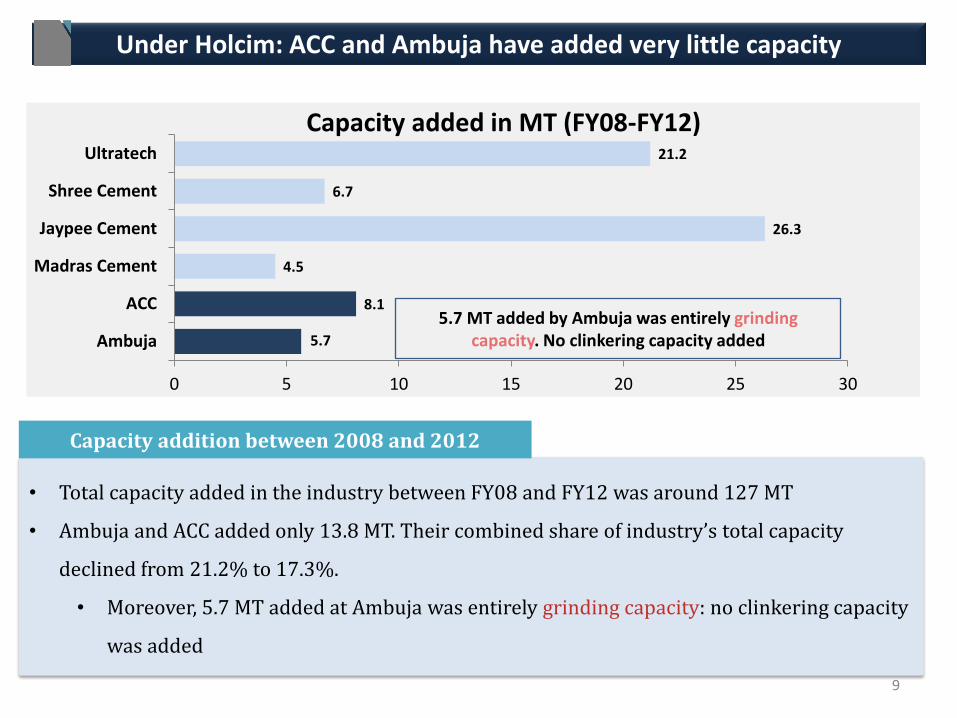

Under Holcim: ACC and Ambuja have added very little capacity

• Total capacity added in the industry between FY08 and FY12 was around 127 MT

• Ambuja and ACC added only 13.8 MT. Their combined share of industry’s total capacity

declined from 21.2% to 17.3%.

• Moreover, 5.7 MT added at Ambuja was entirely grinding capacity: no clinkering capacity

was added

Capacity addition between 2008 and 2012

5.7

8.1

4.5

26.3

6.7

21.2

0 5 10 15 20 25 30

Ambuja

ACC

Madras Cement

Jaypee Cement

Shree Cement

Ultratech

Capacity added in MT (FY08-FY12)

5.7 MT added by Ambuja was entirely grinding capacity. No clinkering capacity added

9

Under Holcim: Capex plans of Ambuja have been delayed

2007 2008 2009 2010 2011 2012 2013

Project 1: Clinker expansion of 2.2 MT each at Bhatapara and Rauri

Project 2: Grinding expansion of 5.5 MT at Dadri, Nalagarh, Ahmedabad, Barh

Project 3: Grinding expansion of 2 MT at Bhatapara and Maratha

Project 4: Clinker addition of 2.2 MT at Nagaur, Marwar Mundwa expansion of 4.5 MT

Company had to purchase 0.725 MT of clinker in 2008,

reducing EBITDA margin by 200 bps.

Company had to purchase 1.7 MT of clinker in 2009,

reducing EBITDA Margin by a further 400 bps.

Impact of delays

Projects at Ahmedabad and Barh abandoned.

Costs escalate from Rs. 1.6 bn per MT to Rs.

3.6 bn per MT at a time of weak economic

growth.

Estimated timeline for completion. (Commencement of construction in case of project 4 )

Delays

10

Ambuja and ACC under Holcim

Operational performance

Financial performance

Corporate governance record

11

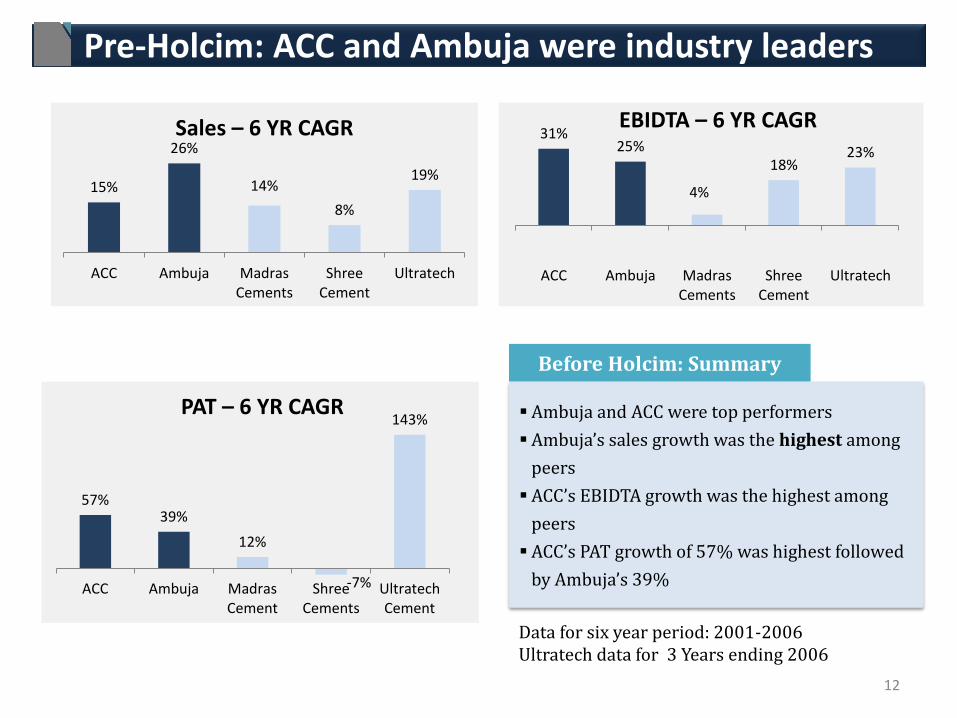

Pre-Holcim: ACC and Ambuja were industry leaders

Ambuja and ACC were top performers

Ambuja’s sales growth was the highest among

peers

ACC’s EBIDTA growth was the highest among

peers

ACC’s PAT growth of 57% was highest followed

by Ambuja’s 39%

Before Holcim: Summary

15%

26%

14%

8%

19%

ACC Ambuja MadrasCements

ShreeCement

Ultratech

Sales – 6 YR CAGR 31% 25%

4%

18% 23%

ACC Ambuja MadrasCements

ShreeCement

Ultratech

EBIDTA – 6 YR CAGR

12

Data for six year period: 2001-2006 Ultratech data for 3 Years ending 2006

57% 39%

12%

-7%

143%

ACC Ambuja MadrasCement

ShreeCements

UltratechCement

PAT – 6 YR CAGR

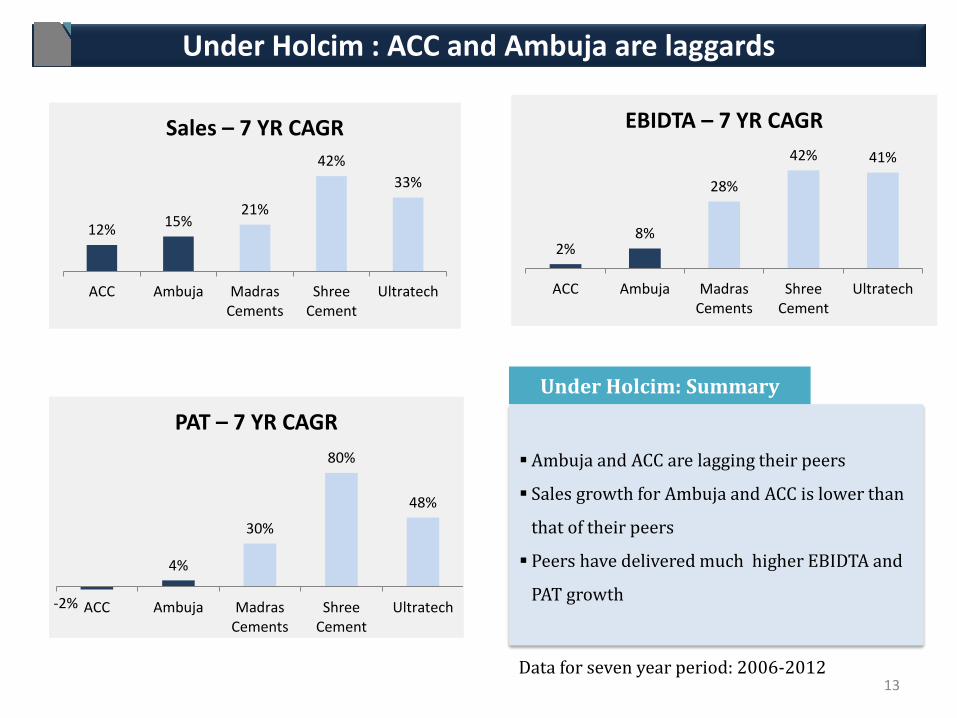

Under Holcim : ACC and Ambuja are laggards

Ambuja and ACC are lagging their peers

Sales growth for Ambuja and ACC is lower than

that of their peers

Peers have delivered much higher EBIDTA and

PAT growth

Under Holcim: Summary

12% 15%

21%

42%

33%

ACC Ambuja MadrasCements

ShreeCement

Ultratech

Sales – 7 YR CAGR

2% 8%

28%

42% 41%

ACC Ambuja MadrasCements

ShreeCement

Ultratech

EBIDTA – 7 YR CAGR

-2%

4%

30%

80%

48%

ACC Ambuja MadrasCements

ShreeCement

Ultratech

PAT – 7 YR CAGR

13 Data for seven year period: 2006-2012

Profitability eroded at Ambuja and ACC ; improved at peers

EBIDTA margins and PAT margins have improved across the industry between 2006 and

2012, except at ACC and Ambuja; margins almost halved at ACC and Ambuja saw a 29% and

42% decline in EBIDTA margin and PAT margin respectively

Profitability

14

30% 34%

18%

28%

16% 17%

24% 27% 28%

22%

ACC Ambuja Madras Cement Shree Cements Ultratech

EBITDA Margin (2006 vs 2012)

2006

2012

19% 21%

7%

2%

6% 8%

12% 11%

9% 12%

ACC Ambuja Madras Cement Shree Cements Ultratech Cement

PAT Margin (2006 vs 2012)

2006

2012

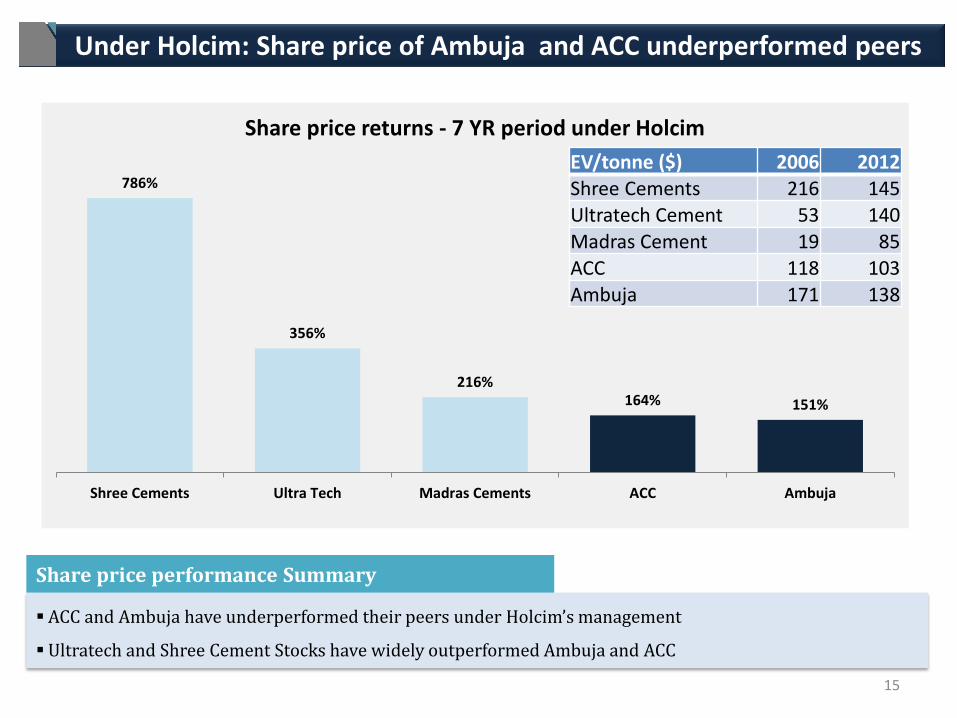

Under Holcim: Share price of Ambuja and ACC underperformed peers

786%

356%

216% 164% 151%

Shree Cements Ultra Tech Madras Cements ACC Ambuja

Share price returns - 7 YR period under Holcim

ACC and Ambuja have underperformed their peers under Holcim’s management

Ultratech and Shree Cement Stocks have widely outperformed Ambuja and ACC

Share price performance Summary

EV/tonne ($) 2006 2012 Shree Cements 216 145 Ultratech Cement 53 140

Madras Cement 19 85 ACC 118 103

Ambuja 171 138

15

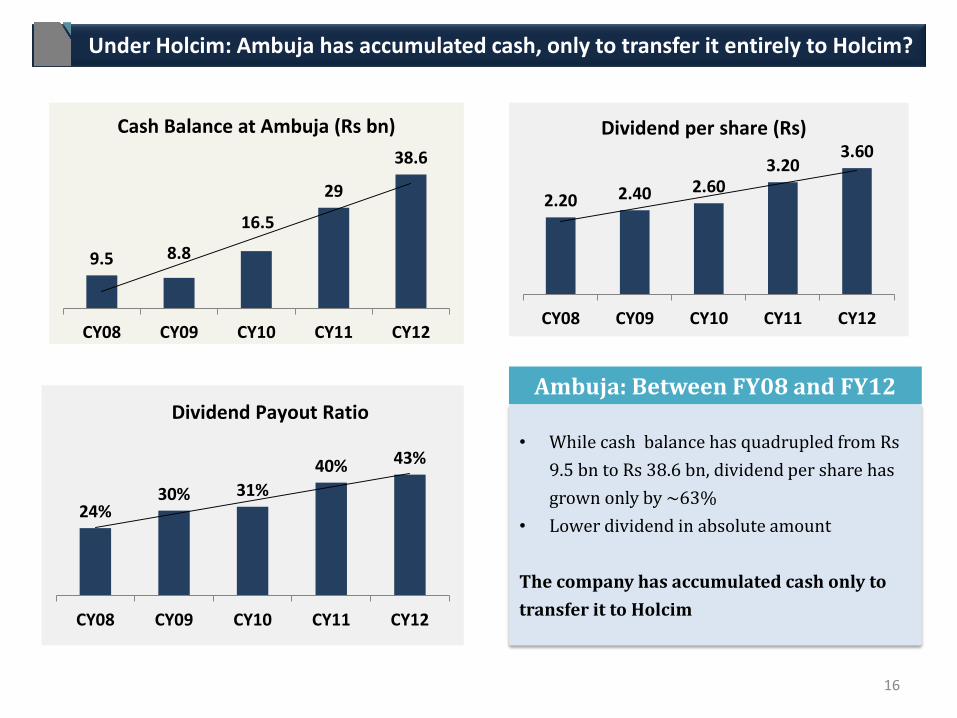

Under Holcim: Ambuja has accumulated cash, only to transfer it entirely to Holcim?

9.5 8.8

16.5

29

38.6

CY08 CY09 CY10 CY11 CY12

Cash Balance at Ambuja (Rs bn)

• While cash balance has quadrupled from Rs

9.5 bn to Rs 38.6 bn, dividend per share has

grown only by ~63%

• Lower dividend in absolute amount

The company has accumulated cash only to

transfer it to Holcim

Ambuja: Between FY08 and FY12

2.20 2.40 2.60 3.20

3.60

CY08 CY09 CY10 CY11 CY12

Dividend per share (Rs)

24% 30% 31%

40% 43%

CY08 CY09 CY10 CY11 CY12

Dividend Payout Ratio

16

Ambuja and ACC under Holcim

Operational performance

Financial performance

Corporate governance record

17

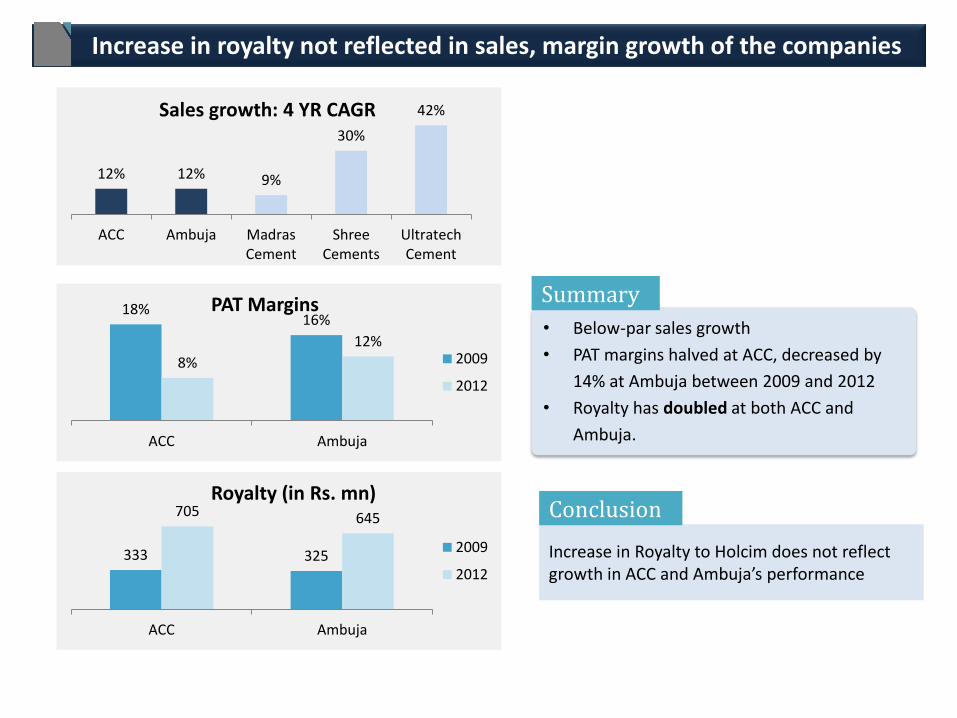

Increase in royalty not reflected in sales, margin growth of the companies

• Below-par sales growth

• PAT margins halved at ACC, decreased by

14% at Ambuja between 2009 and 2012

• Royalty has doubled at both ACC and

Ambuja.

Summary

Increase in Royalty to Holcim does not reflect growth in ACC and Ambuja’s performance

Conclusion

18% 16%

8%

12%

ACC Ambuja

PAT Margins

2009

2012

333 325

705 645

ACC Ambuja

Royalty (in Rs. mn)

2009

2012

12% 12% 9%

30%

42%

ACC Ambuja MadrasCement

ShreeCements

UltratechCement

Sales growth: 4 YR CAGR

19

Holcim missed the message that shareholders gave while voting on the royalty resolution

11%

89%

ACC

FOR

AGAINST

17%

83%

Ambuja

FOR

AGAINST

• More than 80% of minority shareholders voted AGAINST the proposal, in both ACC and Ambuja

• Resolution would have been defeated under the new SEBI rules that require a majority of minority shareholders

(i.e. more than 50% of non-promoter investors)

• Both companies have paid royalties in the region of 0.7% of net sales.

• In February 2013, Ambuja and ACC passed resolutions to approve payment of royalty to Holcim, up to 1% of

net sales.

Proposal to hike royalty

Voting pattern among minority shareholders on the proposal to increase royalty

Observations

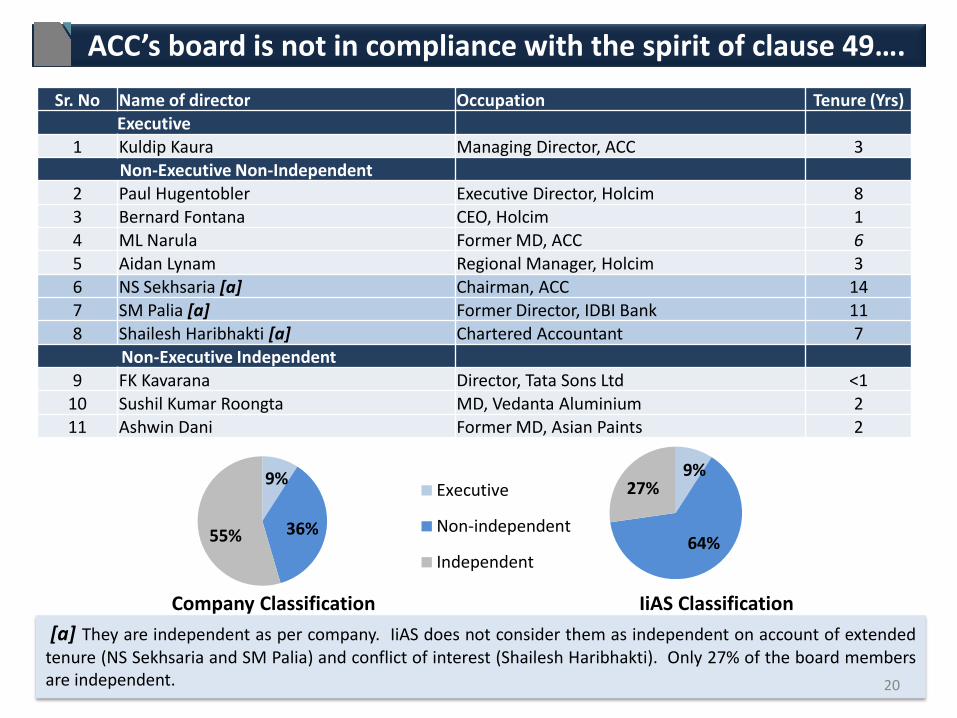

ACC’s board is not in compliance with the spirit of clause 49….

Sr. No Name of director Occupation Tenure (Yrs) Executive

1 Kuldip Kaura Managing Director, ACC 3 Non-Executive Non-Independent

2 Paul Hugentobler Executive Director, Holcim 8 3 Bernard Fontana CEO, Holcim 1

4 ML Narula Former MD, ACC 6

5 Aidan Lynam Regional Manager, Holcim 3

6 NS Sekhsaria [a] Chairman, ACC 14 7 SM Palia [a] Former Director, IDBI Bank 11 8 Shailesh Haribhakti [a] Chartered Accountant 7

Non-Executive Independent 9 FK Kavarana Director, Tata Sons Ltd <1

10 Sushil Kumar Roongta MD, Vedanta Aluminium 2 11 Ashwin Dani Former MD, Asian Paints 2

[a] They are independent as per company. IiAS does not consider them as independent on account of extended tenure (NS Sekhsaria and SM Palia) and conflict of interest (Shailesh Haribhakti). Only 27% of the board members are independent.

IiAS Classification Company Classification

20

9%

36% 55%

Executive

Non-independent

Independent

9%

64%

27%

…..neither is the board of Ambuja Cements

IiAS Classification Company Classification

21

18%

27% 55%

Executive

Non-independent

Independent

16%

67%

17%

Sr. No Name of director Occupation Tenure (Yrs) Executive

1 Ajay Kapur CEO, Ambuja <1

2 Onne Van Der Weijde (Promoter Director) MD, Ambuja 4

Non-Executive Non-Independent 3 Paul Hugentobler (Promoter Director) Vice Chairman, Ambuja 7

4 Bernard Fontana (Promoter Director) CEO, Holcim 1

5 BL Taparia Fmr whole-time director, Ambuja 11

6 NS Sekhsaria [a] Chairman, Ambuja 31

7 Nasser Munjee [a] Advisor & Consultant 12

8 Rajendra Chitale [a] Managing Partner, Chitale & Associates 11

9 Shailesh Haribhakti [a] Chartered Accountant 7

Non-Executive Independent 10 Dr. Omkar Goswami Founder & Chairman, CERG Advisory Pvt.Ltd 7

11 Haigreve Khaitan Partner, Khaitan & Co. <1

[a] They are independent as per company. IiAS does not consider them as independent on account of their extended tenure on the board and conflict of interest (in case of Shailesh Haribhakti). Only 17% of the board members are independent

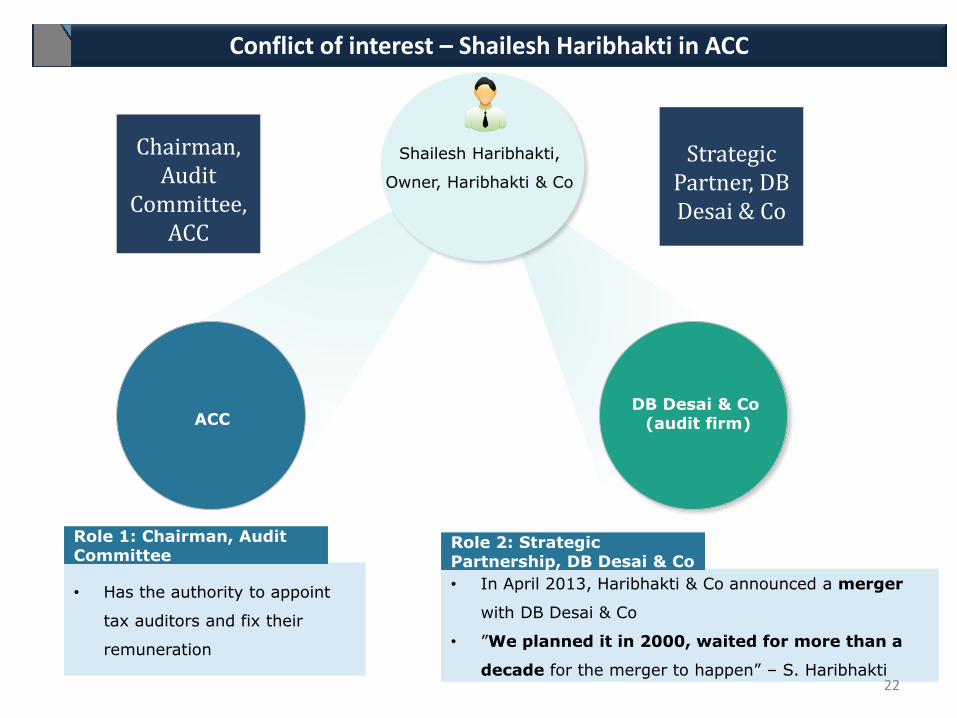

Conflict of interest – Shailesh Haribhakti in ACC

ACC DB Desai & Co

(audit firm)

Shailesh Haribhakti,

Owner, Haribhakti & Co

Chairman, Audit

Committee, ACC

Strategic Partner, DB Desai & Co

• In April 2013, Haribhakti & Co announced a merger

with DB Desai & Co

• ”We planned it in 2000, waited for more than a

decade for the merger to happen” – S. Haribhakti

Role 2: Strategic Partnership, DB Desai & Co

• Has the authority to appoint

tax auditors and fix their

remuneration

Role 1: Chairman, Audit Committee

22

ACC shareholders lost because of this conflict of interest

ACC DB Desai & Co (audit firm)

Shailesh Haribhakti,

Owner, Haribhakti & Co

A staggering sum of Rs. 220 mn paid for tax audit in FY12

• Shailesh Haribhakti approves

the choice of DB Desai as tax

auditor of ACC, and fixed

their remuneration

Actions

• A staggering sum of Rs. 220 mn paid to DB Desai for tax audit.

• 200x higher than tax audit fees at peer cement cos.

• 1.5% of PAT

• The conflict of interest is not only bad governance, it has a

substantially negative impact on profitability.

Impact

Shailesh Haribhakti continues to serve as independent director and chairman of the audit committee at ACC.

23

Introduction

Should Holcim be paid Rs 35 bn given its stewardship of Ambuja and ACC?

What does IiAS recommend?

How should minority shareholders vote?

What are the other issues with this restructuring?

Do the synergies really exist?

24

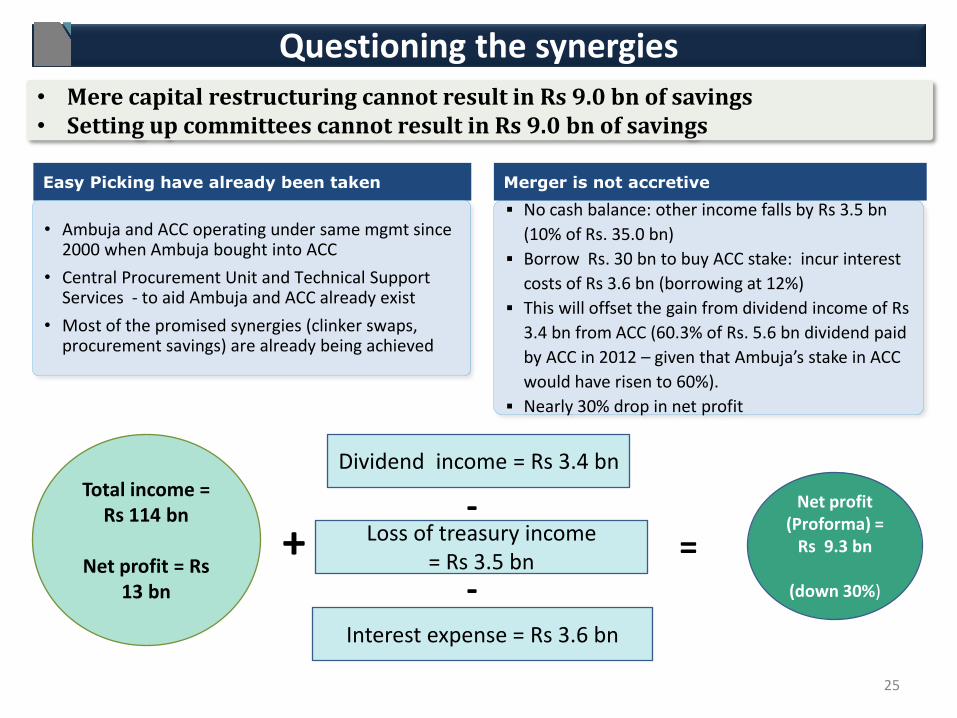

Questioning the synergies

No cash balance: other income falls by Rs 3.5 bn

(10% of Rs. 35.0 bn)

Borrow Rs. 30 bn to buy ACC stake: incur interest

costs of Rs 3.6 bn (borrowing at 12%)

This will offset the gain from dividend income of Rs

3.4 bn from ACC (60.3% of Rs. 5.6 bn dividend paid

by ACC in 2012 – given that Ambuja’s stake in ACC

would have risen to 60%).

Nearly 30% drop in net profit

Merger is not accretive Easy Picking have already been taken

• Ambuja and ACC operating under same mgmt since 2000 when Ambuja bought into ACC

• Central Procurement Unit and Technical Support Services - to aid Ambuja and ACC already exist

• Most of the promised synergies (clinker swaps, procurement savings) are already being achieved

• Mere capital restructuring cannot result in Rs 9.0 bn of savings • Setting up committees cannot result in Rs 9.0 bn of savings

Total income = Rs 114 bn

Net profit = Rs

13 bn

Dividend income = Rs 3.4 bn

Interest expense = Rs 3.6 bn

Loss of treasury income = Rs 3.5 bn

+ = -

- Net profit (Proforma) =

Rs 9.3 bn

(down 30%)

25

Introduction

Should Holcim be paid Rs 35 bn given its stewardship of Ambuja and ACC?

What does IiAS recommend?

How should minority shareholders vote?

What are the other issues with this restructuring?

Do the synergies really exist?

26

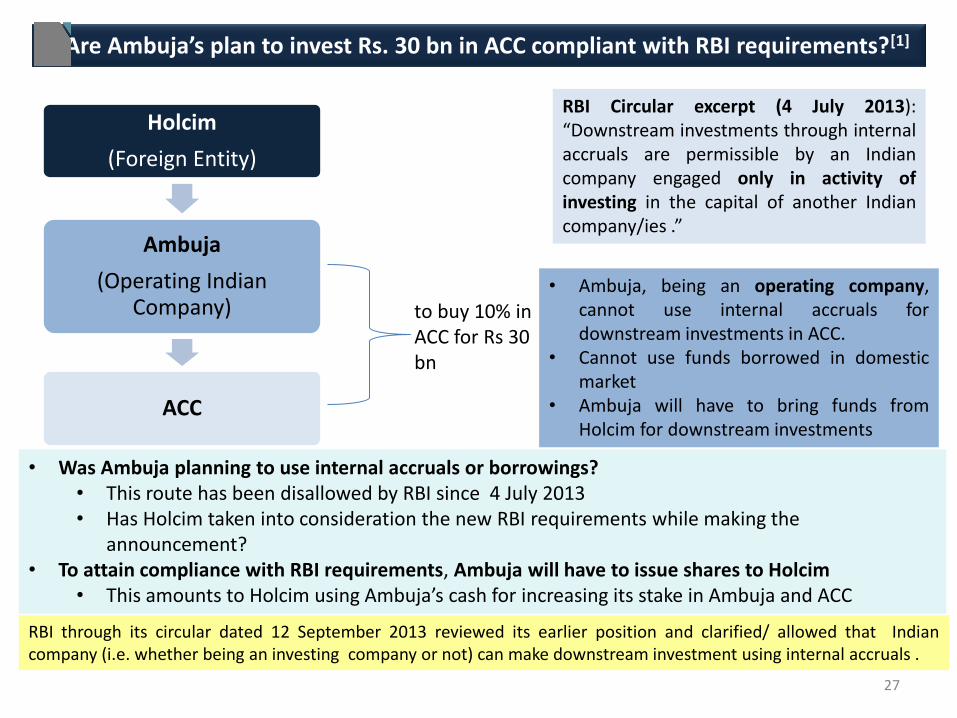

Are Ambuja’s plan to invest Rs. 30 bn in ACC compliant with RBI requirements?[1]

• Was Ambuja planning to use internal accruals or borrowings? • This route has been disallowed by RBI since 4 July 2013 • Has Holcim taken into consideration the new RBI requirements while making the

announcement? • To attain compliance with RBI requirements, Ambuja will have to issue shares to Holcim

• This amounts to Holcim using Ambuja’s cash for increasing its stake in Ambuja and ACC

Holcim

(Foreign Entity)

Ambuja

(Operating Indian Company)

ACC

to buy 10% in ACC for Rs 30 bn

• Ambuja, being an operating company, cannot use internal accruals for downstream investments in ACC.

• Cannot use funds borrowed in domestic market

• Ambuja will have to bring funds from Holcim for downstream investments

RBI Circular excerpt (4 July 2013): “Downstream investments through internal accruals are permissible by an Indian company engaged only in activity of investing in the capital of another Indian company/ies .”

27

RBI through its circular dated 12 September 2013 reviewed its earlier position and clarified/ allowed that Indian company (i.e. whether being an investing company or not) can make downstream investment using internal accruals .

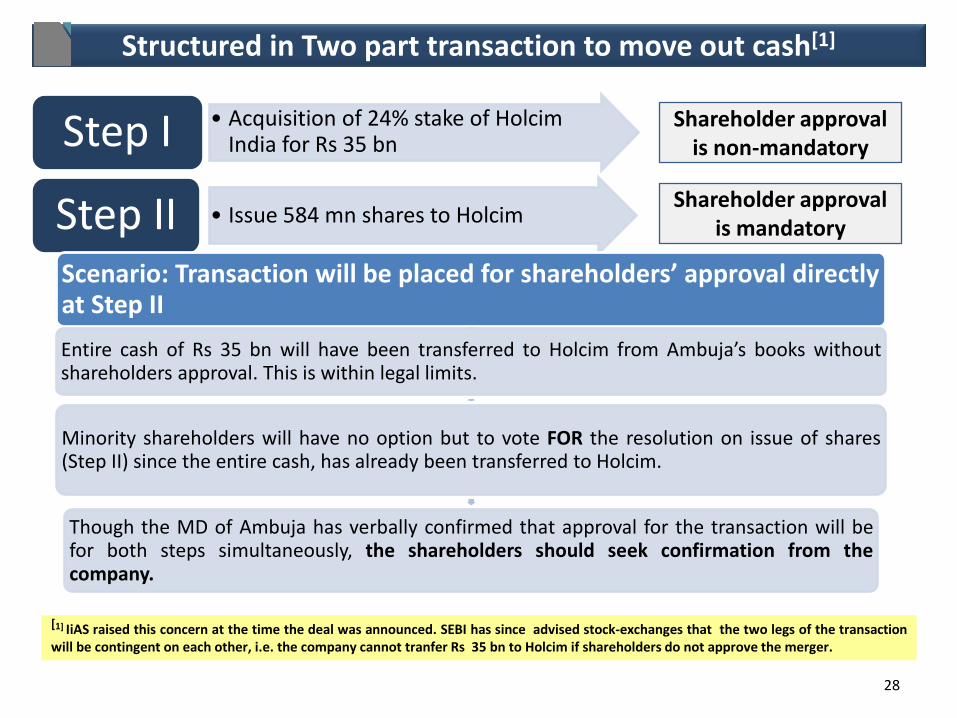

Structured in Two part transaction to move out cash[1]

28

• Acquisition of 24% stake of Holcim India for Rs 35 bn Step I

• Issue 584 mn shares to Holcim Step II Scenario: Transaction will be placed for shareholders’ approval directly at Step II

Entire cash of Rs 35 bn will have been transferred to Holcim from Ambuja’s books without shareholders approval. This is within legal limits.

Minority shareholders will have no option but to vote FOR the resolution on issue of shares (Step II) since the entire cash, has already been transferred to Holcim.

Though the MD of Ambuja has verbally confirmed that approval for the transaction will be for both steps simultaneously, the shareholders should seek confirmation from the company.

Shareholder approval is non-mandatory

Shareholder approval is mandatory

[1] IiAS raised this concern at the time the deal was announced. SEBI has since advised stock-exchanges that the two legs of the transaction will be contingent on each other, i.e. the company cannot tranfer Rs 35 bn to Holcim if shareholders do not approve the merger.

Consequences of the merger

Commitments to buy another Rs. 30 bn in ACC shares will lead to lower dividend payouts

Holcim may use the Rs. 35 bn cash to increase its stake in Ambuja This amounts to using

the company’s cash (as opposed to own funds) to make creeping acquisitions

Holcim will continue to charge royalty to ACC, even after ACC becomes a subsidiary of Ambuja

Depletion of Rs. 35 bn in cash

Investments will have to be funded by debt – i.e. from a positive cash company, Ambuja will become a debt-holding company

Royalty Cash depletion

Creeping acquisitions

Dividend and investments

Dilution Minority shareholders in Ambuja face dilution of 21%

Consequences of the merger

29

Introduction

Should Holcim be paid Rs 35 bn given its stewardship of Ambuja and ACC?

What does IiAS recommend?

How should minority shareholders vote?

What are the other issues with this restructuring?

Do the synergies really exist?

30

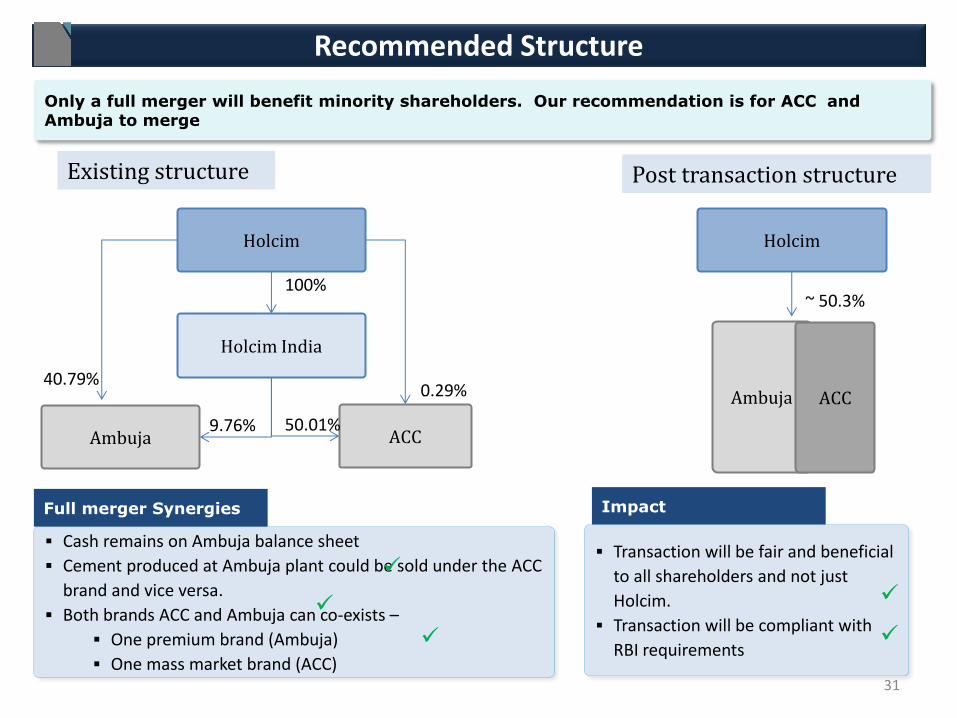

Recommended Structure

Only a full merger will benefit minority shareholders. Our recommendation is for ACC and Ambuja to merge

Existing structure

Holcim

Holcim India

Ambuja

100%

40.79%

9.76% ACC

0.29%

50.01%

Post transaction structure

Holcim

Ambuja

~ 50.3%

ACC

Cash remains on Ambuja balance sheet

Cement produced at Ambuja plant could be sold under the ACC

brand and vice versa.

Both brands ACC and Ambuja can co-exists –

One premium brand (Ambuja)

One mass market brand (ACC)

Full merger Synergies Impact

Transaction will be fair and beneficial

to all shareholders and not just

Holcim.

Transaction will be compliant with

RBI requirements

31

Introduction

Should Holcim be paid Rs 35 bn given its stewardship of Ambuja and ACC?

What does IiAS recommend?

How should minority shareholders vote?

What are the other issues with this restructuring?

Do the synergies really exist?

32

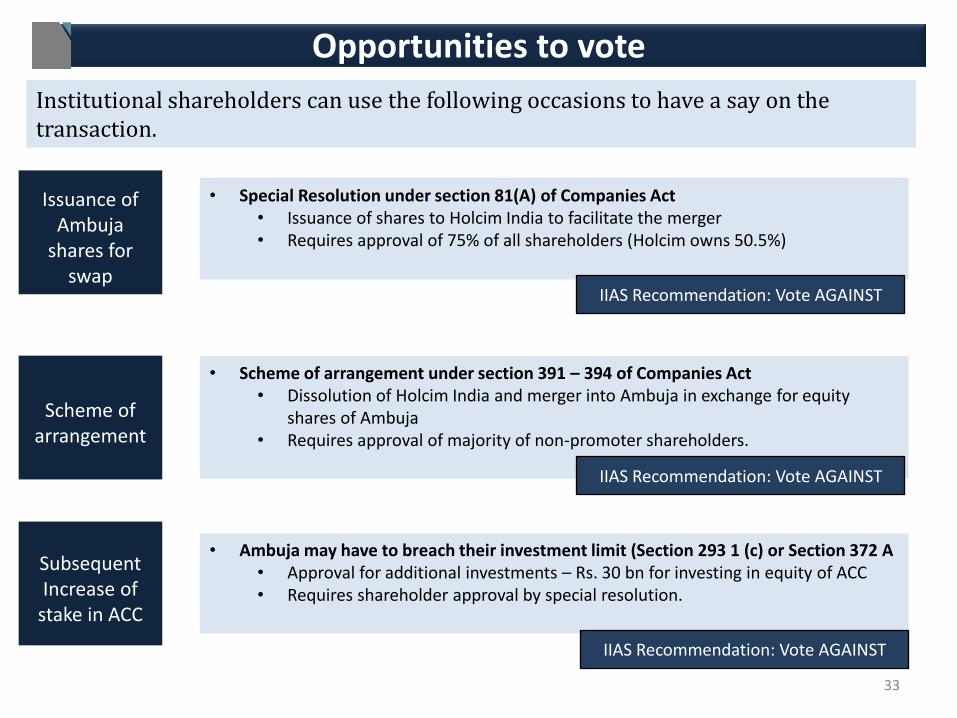

Issuance of Ambuja

shares for swap

• Special Resolution under section 81(A) of Companies Act • Issuance of shares to Holcim India to facilitate the merger • Requires approval of 75% of all shareholders (Holcim owns 50.5%)

IIAS Recommendation: Vote AGAINST

Institutional shareholders can use the following occasions to have a say on the transaction.

Scheme of arrangement

• Scheme of arrangement under section 391 – 394 of Companies Act • Dissolution of Holcim India and merger into Ambuja in exchange for equity

shares of Ambuja • Requires approval of majority of non-promoter shareholders.

IIAS Recommendation: Vote AGAINST

Subsequent Increase of

stake in ACC

• Ambuja may have to breach their investment limit (Section 293 1 (c) or Section 372 A • Approval for additional investments – Rs. 30 bn for investing in equity of ACC • Requires shareholder approval by special resolution.

IIAS Recommendation: Vote AGAINST

Opportunities to vote

33

IiAS: Related research

34

Holcim-Ambuja Restructuring Ambuja Postal Ballot ACC Postal Ballot Missing the message Royalty payments and minority investors

15th Floor, West Wing, PJ Tower, Dalal Street, Fort, Mumbai 400 001 T +91(0) 22 22721570 - 3 F +91(0) 22 2272 1574 E [email protected] W iias.in

Contact IiAS