hme home properties sept 2010 presentation slides deck

TRANSCRIPT

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 1/53

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 2/53

Welcome

Charis Warshof Vice President, Investor Relations

2

This presentation was created as of the specific date indicated and reflectsmanagement views as of that date. Such information may include certainforward-looking statements that are subject to risks and uncertainties that maycause results to differ materially and are described in our filings with the

Disclosure Statement

Securities and Exchange Commission. The presentation may include statementsthat may not be accurate after the date indicated. The Company disclaims anyduty to update such information.

Any reference to guidance relates to guidance previously provided publiclyby the Company, which it typically updates on a quarterly basis. Nothing in thispresentation should be construed as confirmation of any guidance previouslygiven. Any third party information and/or analyst estimates are provided for

. ,analysts' projections. Non-GAAP financial measures in this presentation arereconciled to the most directly comparable financial measures calculated inaccordance with GAAP in the Company’s public filings, news releases andsupplemental information for the specific fiscal period, all of which are availableon the Home Properties website at homeproperties.com.

3

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 3/53

Introduction

President andChief Executive Officer

4

The Right Focus

• Introduction Ed Pettinella• Financial commentary David Gardner

Presentation Agenda

• Acquisitions John Smith• Property management and operations Scott Doyle

Rosemarie Cook-ManleyLes EisenbergKeith Knight

• Development Don Hague• Summar Ed Pettinella• Q&A• Property tour at 10:30 AM

5

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 4/53

Financial Commentary

Executive Vice Presidentand Chief Financial Officer

6

We’re Prepared

Future Guidance

2010 Guidance Update

7

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 5/53

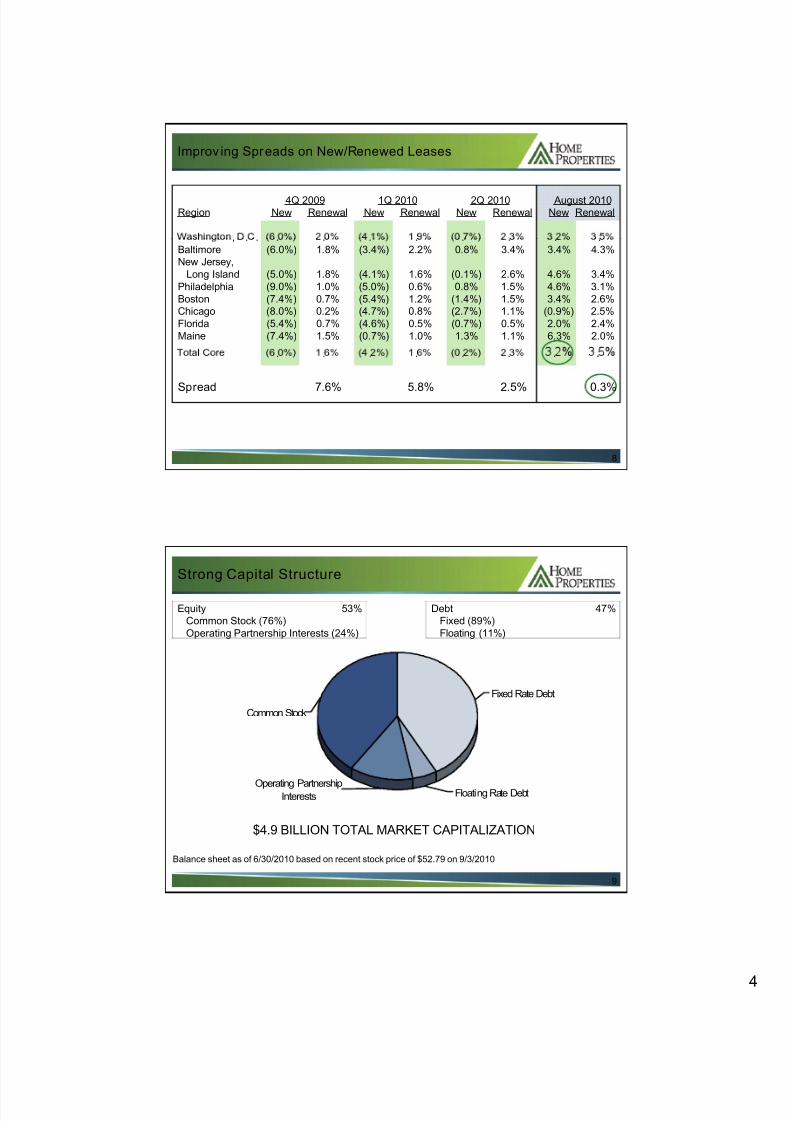

4Q 2009 1Q 2010 2Q 2010 August 2010Region New Renewal New Renewal New Renewal New Renewal

Improv ing Spreads on New/Renewed Leases

, . . . . . . . . . .Baltimore (6.0%) 1.8% (3.4%) 2.2% 0.8% 3.4% 3.4% 4.3%New Jersey,

Long Island (5.0%) 1.8% (4.1%) 1.6% (0.1%) 2.6% 4.6% 3.4%Philadelphia (9.0%) 1.0% (5.0%) 0.6% 0.8% 1.5% 4.6% 3.1%Boston (7.4%) 0.7% (5.4%) 1.2% (1.4%) 1.5% 3.4% 2.6%Chicago (8.0%) 0.2% (4.7%) 0.8% (2.7%) 1.1% (0.9%) 2.5%Florida (5.4%) 0.7% (4.6%) 0.5% (0.7%) 0.5% 2.0% 2.4%Maine (7.4%) 1.5% (0.7%) 1.0% 1.3% 1.1% 6.3% 2.0%

. . . . . . . .

Spread 7.6% 5.8% 2.5% 0.3%

8

Strong Capital Structure

Equity 53%Common Stock (76%)Operating Partnership Interests (24%)

Debt 47%Fixed (89%)Floating (11%)

Common Stock

Fixed Rate Debt

Operating PartnershipInterests Floating Rate Debt

9

Balance sheet as of 6/30/2010 based on recent stock price of $52.79 on 9/3/2010

$4.9 BILLION TOTAL MARKET CAPITALIZATION

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 6/53

600

Well-Managed Mortgage Debt Maturi tiesWe’re Prepared

$

Total Debt Maturities

299

126

205 190

353

271

153

202184200

300

400

500

233

600

100

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Thereafter

10

As of 6/30/2010

60

Ac qu is it ion Strateg y

Seizing Only the Right Opportunities

John Smith

Senior Vice Presidentand Chief Investment Officer

11

We Buy Right

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 7/53

• High barrier-to-entry, high growth, close-in suburban markets ofmajor selected MSAs

Ac qu is it ion Strateg yRight Focus + Integrity = Proven Success

• ast oast ocus: oston to - t ant c• High average home prices• Favorable supply/demand equation• Positive demographic trends: immigrants, echo boomers, seniors• UPREIT transactions• Additional development potential• cqu re - an -c ass proper es w so cons ruc on, oor p ans an

upgradeable to B+ and C+-class

12

• Acquisition team – Combined experience of 180 years

How We Buy Right

Measure Twice, Cut Once

• Thorough due diligence – Comprehensive market studies – Measure real estate tax reassessment risk – Property Management input – Environmental research – Construction and cap ex projections

13

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 8/53

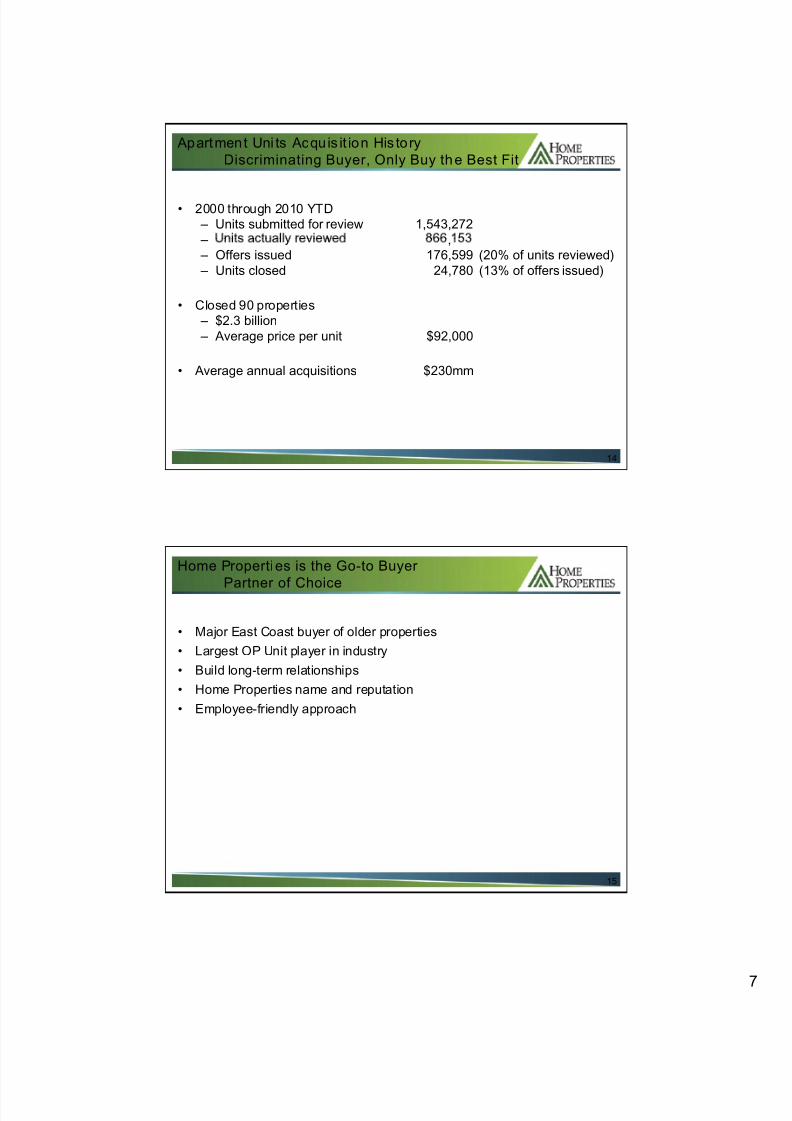

• 2000 through 2010 YTD – Units submitted for review 1,543,272

Apart men t Uni ts Acqu is it ion His to ryDiscriminating Buyer, Only Buy th e Best Fit

– , – Offers issued 176,599 (20% of units reviewed) – Units closed 24,780 (13% of offers issued)

• Closed 90 properties – $2.3 billion – Average price per unit $92,000

• Average annual acquisitions $230mm

14

• Major East Coast buyer of older properties• Largest OP Unit player in industry

Home Properti es is the Go-to Buyer

Partner of Choice

• Build long-term relationships• Home Properties name and reputation• Employee-friendly approach

15

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 9/53

Inventory in Target MarketsTremendous Acqui sition Growth Potential

Estimated Current HMEB/C-Class Market

Target Region Apartments* HME Owned Penetration

D.C. Metro 434,000 9,911 2.3%Baltimore 166,000 8,582 5.2%Philadelphia 267,000 5,603 2.1%Northern New Jersey 229,000 3,578 1.6%Long Island 435,000 3,390 0.8%Boston 399,000 2,382 0.6%Chicago 628,000 2,242 0.4%

16

* Source: Witten Advisors

, , , .

Recent Example: Westb rook e and Middlebrooke

Buy Right – Rehab – Enhance Value

Acquired 4/1/2010Occupancy at acquisition 88.0%Occu anc 9/1/2010 94.0%

Westbrooke Apartments

17

Middlebrooke ApartmentsWestminster, MD

208 Units

,110 Units

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 10/53

Market Cap 2

10E Acq 1 10E Disp 1 Net Acq/Disp 6/30/2010 Net Acq/Disp as($ mil) ($ mil) ($ mil) ($ mil) % Market Cap

2010E Net Acquis itio ns as % of Market Cap Am ong t he Gr owth Leaders

HME 330 0 330 4,709 7.01%

AIV 120 -250 -130 8,117 -1.60% AVB 70 -190 -120 12,837 -0.93%BRE 80 -120 -40 4,410 -0.91%CPT 130 -100 30 6,100 0.49%CLP 50 -10 40 3,354 1.19%EQR 1,250 -850 400 23,222 1.72%

- , .MAA 250 -30 220 3,355 6.56%PPS 0 0 0 2,376 0.00%UDR 80 0 80 6,929 1.15%

18

Source:(1) Green Street Advisors “Residential REITs August ‘10 Update” August 20, 2010 – net acquisitions 2010E(2) Citigroup Global Markets “Weekly REIT and Lodging Strategy” August 20, 2010 – market cap

7.0 6.6

5

6

7

2010E Net Acquis itio ns as % of Market Cap (1)

Am ong t he Gr owth Leaders%

2.21.7

1.2 1.2 0.90.5

0.00

1

2

3

4

(2)

-0.9 -0.9-1.6-2

-

HME MAA ESS EQR CLP UDR Average CPT PPS BRE AVB AIV

19

(1) Apartment REITs with market cap >$1B(2) Average excluding HMESource: Green Street Advisors “Residential REITs August ‘10 Update” August 20, 2010 – net acquisitions 2010E;

Citigroup Global Markets “Weekly REIT and Lodging Strategy” August 20, 2010 – market cap

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 11/53

• Cap rates – Dropping recently, but steady now

Street Level ObservationThe Right Focus on B/C-Class Opportunities

– – General differential of 25-75 bps between A- and B/C-class – Cap rate range in our markets of 5.75% up to 6.5%

• Portfolio average of approximately 6%

• Deal flow – Strong B/C-class opportunities – Still lent of ca ital chasin deals

• A-class: 30 to 40 bidders• B/C-class: fewer bidders

20

• Excellent reputation for closing, which generates transaction network• B/C-class acquisition and repositioning strategy generates positive results

Ac qu is it ions Strateg y

Seizing Only the Right Opportunities

• Acquisition engine roaring and driving NOI growth

21

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 12/53

Property Management

Scott Doyle

Senior Vice PresidentStrategic Property Managemen t

’

22

e ve a se e ar

Road to NOI Growth

RealEstate

Technology

Marketing

23

Operations

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 13/53

• Reposition strategy tailored to each community based on – Current physical condition

Property Repositioni ng

– – Future target demographic – Maximization of return

• Target a minimum of 10% initial unlevered yield on revenue-enhancinginterior renovations

2424

Property Repositioni ng - Before

25

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 14/53

Property Repositioning - Before

26

Property Repositioning - Before

27

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 15/53

Property Repositioning - Before

28

Example of Property Repositionin g

n t

$

M o n

t h l y A p a r t m e n

t R

29

Apartment Quality

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 16/53

Braddoc k Lee Apartments, Alexandri a, VA

Renovated vs. Unrenovated Rent$

30

Property Age # Units* % Not Upgraded20+ years 35,290 42%

Future Potential from Unit Upgrades

10-20 years 1,826 97%<10 years 1,367 0%Total 38,483 43%

31

* Includes 1,222 units scheduled to close by 9/30/2010

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 17/53

Varying Demographics

Virginia Village• Primarily 30s & 40s• Families with children• High school education

Alexandria, VA submarket

• English is 2nd language• Blue collar workers• Pay rent with money order • Renter by necessity; can ’t

afford a houseBraddock Lee

• Wide variety of ages• Very few children• Highly educated• Professional jobs

• Pay rent online and withchecks• Renter by choice; highly

mobile due to career

32

Road to NOI Growth

RealEstate

• Flexible approach allows us to

Technology

Marketing

repositioning opportunity

• Over 40% of current portfolioavailable for interior upgrade

33

Operations

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 18/53

Rosemarie Cook-ManleyVice President

Les EisenbergVice President

Strategic Business Systems

34

Vice President

Capital Improvements andNational Accounts

Customer LifecyclePersonalized Communication & Technolo gy

Reach

•Advertising

Acquisition Conversion Retention Loyalty

•Searchengines

•Social media

•Mobile

35

DRIVING NOI RESULTS

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 19/53

Mobile Av ail able Whenev er, Wherever

www.MtVernonSquareVA.com

36

Adver ti si ng

Driving Down Costs

ver ave

37

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 20/53

Customer LifecyclePersonalized Communication & Technology

Reach

•Advertising

Acquisition

•Contact

Conversion Retention Loyalty

•Searchengines

•Social media

•Mobile

•Web 2.0

•Prospectprogram

38

DRIVING NOI RESULTS

Web 2.0

Enhancing Interactive Communication

39

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 21/53

Prospect ProgramMaking a Difficult Decision Easier

40

Customer Lifecycle

Personalized Communication & Technology

Reach

•Advertising

Acquisition

•Contact

Conversion

• Consultative

Retention Loyalty

•Searchengines

•Social media

•Mobile

•Web 2.0

•Prospectprogram

saes

• Onlinereservations

41

DRIVING NOI RESULTS

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 22/53

Online ReservationsStreamlining th e Process f or the Prospect

30

35VaultWare Reservations per Property

5

10

15

20

25

42

0

Sep ‐09 Oct ‐0 9 Nov ‐09 Dec ‐09 Jan ‐1 0 Feb ‐1 0 M ar ‐1 0 Apr ‐1 0 May ‐1 0 Jun ‐10 Jul ‐10 Aug ‐10

Home Properties Major ILS Aggregate

Market Index Public REIT Index

Customer Lifecycle

Personalized Communication & Technology

Reach Acquisition

•Contact

Conversion Retention

•Customer

Loyalty

• Consultative•Advertising

•Web 2.0

•Prospectprogram

serv ce

•Social media

•CustomerRelationshipManagement

•Residentportals

saes

• Onlinereservations

•Searchengines

•Social media

•Mobile

43

DRIVING NOI RESULTS

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 23/53

Customer Relationship ManagementWelcome Home!

44

Resident Portals

Building a Sense of Community

45

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 24/53

Customer LifecyclePersonalized Communication & Technology

Reach

•Advertising

Acquisition

•Contact

Conversion

•Consultative

Retention Loyalty

•Choice•Customer

•Searchengines

•Social media

•Mobile

Center

•Web 2.0

•Prospectprogram

sales

•Onlinereservations

•Our Pledge

•Referrals

service

•Social media

•CustomerRelationshipManagement

•Residentportals

46

DRIVING NOI RESULTS

Customer Lifecycle

Personalized Communication & Technology

Reach

•Advertising

Acquisition

•Contact

Conversion

•Consultative

Retention Loyalty

•Choice•Customer

•Searchengines

•Social media

•Mobile

en er

•Web 2.0

•Prospectprogram

saes

•Onlinereservations

•Our Pledge

•Referrals

service

•Social media

•CustomerRelationshipManagement

•Residentportals

47

16% CostReduction

PersonalizedInteraction

Over 3xReservations

vs. Peers

LowestTurnover in Sector

27% ofLeases fro m

Referrals

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 25/53

Rosemarie Cook-ManleyVice President

Les EisenbergVice President

Strategic Business Systems

48

Vice President

Capital Improvements andNational Accounts

Customer Lifecycle

Understanding the Pricing Puzzle

Reach

•Advertising

Acquisition

•Contact

Conversion

• Consultative

Retention Loyalty

••Customer

•Searchengines

•Social media

•Mobile

Center

•Web 2.0

•Prospectprogram

sales

• Onlinereservations

•Our Pledge

•Referrals

service

•Social media

•CustomerRelationshipManagement

•Residentportals• LRO

49

• Analytics

FORWARD-LOOKING STRATEGY

Maximizing NOI

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 26/53

Customer LifecycleCustom Alerts LRO

50

Customer Lifecycle

Custom Pricing Snapshots

51

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 27/53

Customer LifecycleCustom Upgrade Pricing Analysis

723 Saddle Brooke Apartments

2A11 256 UnitsRented Units

Amenity Code

#RentedUnits

Avg.Days Avail

H/(L)Base

Units inDays

Avg. RentalRate

$ H/(L) RentUnits

TargetPremium

BASE UNIT 53 45 --- $918 --- $0BATH 2 37 -8 $952 $34 $30NUPK 16 48 3 $1,003 $85 $80PREM 7 30 -15 $1,068 $150 $136Total Upgraded Units 25 42 -3 $1,017 $99 ---

Total All Units 78 44 --- $950 --- ---

52

Customer Lifecycle

Understanding the Pricing Puzzle

Reach

•Advertising

Acquisition

•Contact

Conversion

• Consultative

Retention Loyalty

••Customer

•Searchengines

•Social media

•Mobile

Center

•Web 2.0

•Prospectprogram

sales

• Onlinereservations

•Our Pledge

•Referrals

service

•Social media

•CustomerRelationshipManagement

•Residentportals• LRO

• Inte rated• Lease terms

53

FORWARD-LOOKING STRATEGY

Maximizing NOI

• Analyti cs renewals• r ceexceptions

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 28/53

Customer Lifecycle2010 Price Improv ements

1.6 1.5 1.62.0

3.2

3.53.12.6

2.33

4%

-2.7

-1.9

-0.3

1.31.7

-3

-2

-1

0

1

-5.0 -4.8

-6

-5

-

Jan Feb Mar Apr May Jun Jul Aug

2010 Renewal Increases 2010 New Lease vs. Old Lease

54

Rosemarie Cook-ManleyVice President

Les EisenbergVice President

Strategic Business Systems

55

Vice President

Capital Improvements andNational Accounts

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 29/53

• Design team – Exterior finishes

Property Repositioni ngExecution

– – Interior Design/decorating – “3D” color renderings – Finish and design standards

• Regional construction teams – Depth of understanding of property management – Ex erience in new a artment construction and renovations – Established pool of local trades

56

Property Repositioning – Before

Curb Appeal

57

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 30/53

Property Repositioning – After Enhancing Curb Appeal Increases Traffic

58

Property Repositioning – Before

Property Lost to Landscaping

59

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 31/53

Property Repositioning – After Curb Appeal & Reduced Maintenance

60

Property Repositioning – Before

As phalt Park ing Jung le

61

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 32/53

Property Repositioning – After Reducing Hardscape

62

Property Repositioning – Before

Existing Community Room

63

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 33/53

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 34/53

Property Repositioning – After Enhancing Selling Features

66

Property Repositioning – Before

Prohibitive Environment

67

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 35/53

Property Repositioning – After Enabling Ancillary Revenue

68

Property Repositioning – Before

Lack of Visual Appeal

69

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 36/53

Property Repositioning – After Elegant Entrance Features

70

Property Repositioning – Before

Common Area Hallway

71

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 37/53

Property Repositioning – DesignPlan - Design - Execute

72

Property Repositioning – After

Welcome Home!

73

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 38/53

Property Repositioning – BeforeClosed-in Kitchen

74

Property Repositioning – After

10.4% ROI

75

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 39/53

Property Repositioni ngNight and Day

76

Property Repositioning – Before

End of Life Cycle

77

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 40/53

Property Repositioning – BeforeEnd of Life Cycle

78

Property Repositioning – After

12.2 % ROI

79

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 41/53

Property Repositioning – BeforeOutdated Kitchen

80

Property Repositioning – After

11.5% ROI

81

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 42/53

Traditional Upgrade

82

Transitional I Upgrade

83

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 43/53

Transitional II Upgrade

84

Contemporary Upgrade

85

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 44/53

Property Repositioni ng Execution

86

Property Repositioning – C.A.D. / C.G.I.

Build It Right The First Time

87

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 45/53

Financial Improvement Initiatives

Revenue

•Revenue sharing

Expense

•Supplies agreement

CapEx

• Supplies agreement

•Advertising fees

•Utility billing fee

•Utility conservation

•Trash

•Renter’s insurance

•Automation

• Appliances

• Cabinets

• Carpeting

88

$1.6mm $1.1mm $1.9mm

NOI $2.7mm

Development

Senior Vice President, Development

’

89

–

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 46/53

• Focus on Mid-Atlantic Region

Development StrategyIt’s Working

• Low-risk approach with limited pre-construction investment – Emphasis on transit-oriented developments close to shopping,

entertainment, education and work opportunities – Density/adjacent opportunities on existing properties – Acquisition of entitled land

• Target average unlevered stabilized yield of 7.00% and minimum.

90

• Began ground-up development in 2004• To date, 885 units delivered

Track Record Since 2004

• Current pipeline of 2,861 new units• Potential to grow to 4,355 new units• Assembled experienced go-to team with key capabilities• Delivered first A-class units in 2010

91

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 47/53

Location Alexandria, VARegion Washington, D.C.Units 421

The Courts at Huntington Station

Initial occupancy 2Q 2010Completion 2Q 2011Total cost $127mmCost per unit $302K

92

1200 East West Highway

Location Silver Spring, MDRegion Washington, D.C.Units 247

,Start date 2Q 2007Initial occupancy 1Q 2010Total cost $87mmCost per apartment $332K

93

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 48/53

Ripley StreetEntitled Land

94

Location Silver Spring, MDRegion Washington, D.C.

Ripley Street

Entitled Land

Units 368Retail square footage 5,100Possible start Summer 2011Features - 800 feet to new Transit Center

- 3 blocks to pedestrian shopping mall,Whole Foods, American Film Institute

- Tallest buildin in central business district

95

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 49/53

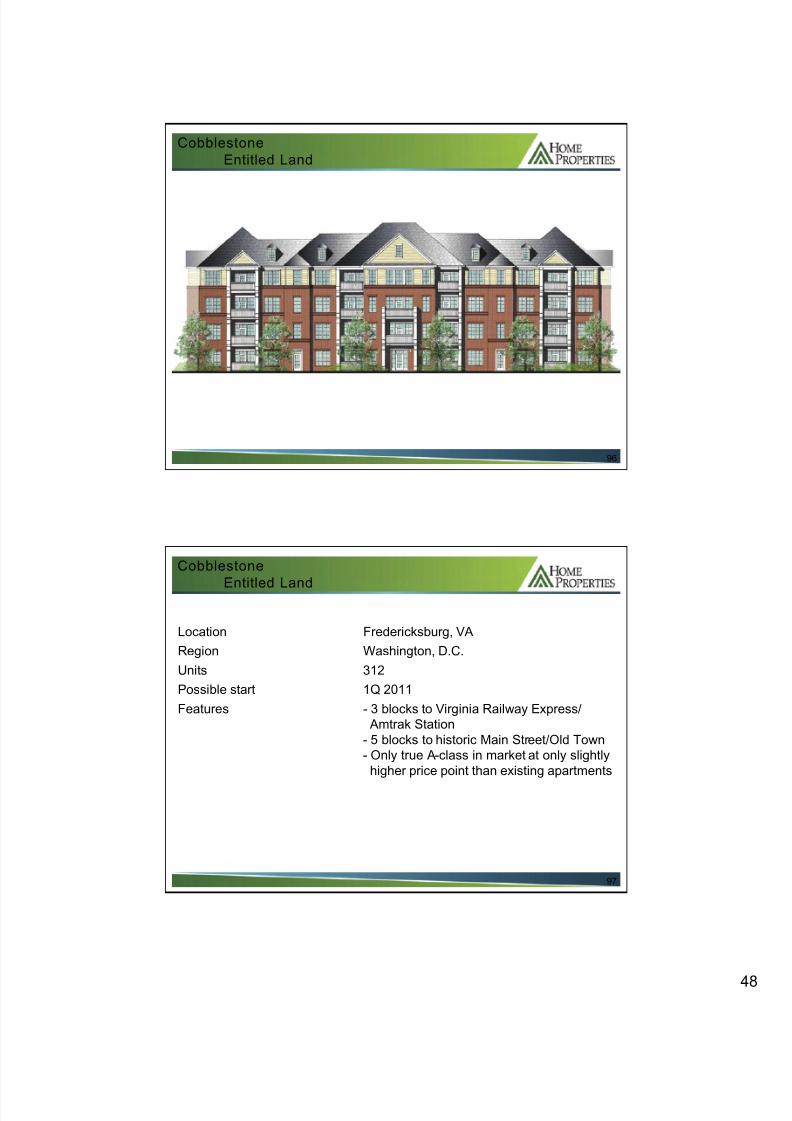

CobblestoneEntitled Land

96

Location Fredericksburg, VARegion Washington, D.C.

Cobblestone

Entitled Land

Units 312Possible start 1Q 2011Features - 3 blocks to Virginia Railway Express/

Amtrak Station- 5 blocks to historic Main Street/Old Town- Only true A-class in market at only slightly

higher price point than existing apartments

97

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 50/53

Falkland North UpdateUnlocking Land Value

Ripley

98

1200East West

Location Silver Spring, MDRegion Washington, D.C.

Falkland North Update

Unlocking Land Value

Units Up to 1,200 apartments, 65,000 square feet retailPossible start 2 to 3 years

99

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 51/53

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 52/53

Concluding Remarks

President andChief Executive Officer

102

The Right Focus

• Refinancin o ortunities roduce lower borrowin costs

The Right Focus

Higher Earnings Growth2011 Projected

FFO Impact

……10 cents

• B/C-class acquisition deal flow is strong

• Marketing, technology, property operations drive NOI growth – Tailored approach – Pricing optimization – Ancillary revenue/cost reduction

………………….……. 5 cents

………………….……….... 3 cents

103

The amounts above represent the 2011 impact the Company expects solely from these three specific items. This information is not intended tobe construed as guidance for 2011, which may include offsetting factors that may affect 2011 earnings results. The Company expects toprovide 2011 guidance in its earnings release for the fourth quarter and full year 2010.

8/8/2019 HME Home Properties Sept 2010 Presentation Slides Deck

http://slidepdf.com/reader/full/hme-home-properties-sept-2010-presentation-slides-deck 53/53

• Strong capital structure – We’re prepared• Seizing accretive acquisitions in prime apartment markets – We buy righ t

The Right Focus

• Maximizing repositioning business model – We’ve raised the bar – Tailored approach to resident communications & value enhancements – Strategic use of technology – Pricing power + insightful analytics = optimized revenue – Increased ancillary revenue and reduced costs

• Development strategy – It’s working

104