hlc008-01-820 hc2020 volume to value revolution volume to value revolution ... pub lic information...

TRANSCRIPT

© 2011 OLIVER WYMANHEALTH AND LIFE SCIENCES

Thomas J. MainPartner and US Market Leader

THE VOLUME TO VALUE REVOLUTION HEALTHCARE 2020

Scripps Green Hospital Grand RoundsWednesday, December 14, 2011

1© 2011 OLIVER WYMAN | HLC008-01-820

Report qualifications/assumptions and limiting conditions

December 12, 2011

This report is for the exclusive use of the Oliver Wyman client named herein. This report is not intended for general circulation or publication, nor is it to be reproduced, quoted or distributed for any purpose without the prior written permission of Oliver Wyman. There are no third party beneficiaries with respect to this report, and Oliver Wyman does not accept any liability to any third party.

Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been independently verified, unless otherwise expressly indicated. Public information and industry and statistical data are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information. The findings contained in this report may contain predictions based on current data and historical trends. Any such predictions are subject to inherent risks and uncertainties. Oliver Wyman accepts no responsibility for actual results or future events.

The opinions expressed in this report are valid only for the purpose stated herein and as of the date of this report. No obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof.

All decisions in connection with the implementation or use of advice or recommendations contained in this report are the soleresponsibility of the client. This report does not represent investment advice nor does it provide an opinion regarding the fairness of any transaction to any and all parties.

2© 2011 OLIVER WYMAN | HLC008-01-820

Four mega forces reshaping healthcare – the volume to value revolution

Information, integration and actionable insights

Science, genomics and personalization

Healthcare affordability

and value

Retail market, consumerism and social media

Healthcare 2020 Market Convergence

The move to a value-based retail healthcare marketplace

December 12, 2011

3© 2011 OLIVER WYMAN | HLC008-01-820

The new rule of innovation and value – .95p + 1.2v + 2t

Job’s Law 75% of last year’s price and 3 times

the value Every 3 years

Bezos’s Law 50% of last year’s price and 3 times

the value Every 2 years

Healthcare Law 108% of last year’s price and 90% of

the value Every year

Price (P) Value (V) Time (T)

December 12, 2011

4© 2011 OLIVER WYMAN | HLC008-01-820

Old school or new school – the market is desperate to reward value

• Benefit design

• Financial engineering

• Integrated reward systems

• Employer culture of health with promotion programs

• On-site clinics

• Consumer engagement

• Health advocacy and coaching

• Health management

• Network contracting

• Population segmentation (15/55)

• Patient registries

• Predictive modeling

• Personalized health itinerary

• Health engagement (integrated consumer experience)

• Connected practices – inclusion of clinical data

• Real time clinical and biometric triggers (home monitoring)

• Value based care models (VBP) – IOCP– PCMH– e-health – ACOs– Retail clinics

• Health information enablement (EBM at point of care, virtual MDTs, etc.)

• Social media

• Behavioral/social/clinical science

The Race

to Value.95p + 1.2v every 2t

• Demand or supply management – how do you unlock the value (30/70)?

• Value chain integration and convergence – can you get there in disconnected silos?

• Virtual integration and cloud computing – will it offset massive fragmentation and capital andskill barriers?

Old school New school

December 12, 2011

5© 2011 OLIVER WYMAN | HLC008-01-820

Accelerating the shift to a value-based market – the diffusion cycle is broken

December 12, 2011

Innovation Adoption Mastery Monetization

• Market fragmentation• FFS economics• Wholesale buyers• Lack of consumer

buying power• Capital rotation

• Basis of competition• Craft skills• Liability• Information gaps• Culture• Leadership

Diffusion barriers

6© 2011 OLIVER WYMAN | HLC008-01-820

Table of contents

• Section 1: The consumer driven industry transformation

• Section 2: Health management company implications

• Section 3: The volume of value revolution

• Section 4: The race to value

December 12, 2011

7© 2011 OLIVER WYMAN | HLC008-01-820 December 12, 2011

THE CONSUMER DRIVEN INDUSTRY TRANSFORMATION

Section 1

8© 2011 OLIVER WYMAN | HLC008-01-820

Consumers buying patterns will shatter the traditional wholesale buying model and reshape the healthcare marketplace

As consumers make real tradeoff decisions between benefits, health management programs, personal accountability, physician relationships and financial exposure (risk and cost)…

…they will make different choices than their employers made for them and drive industry transformation.

December 12, 2011

9© 2011 OLIVER WYMAN | HLC008-01-820

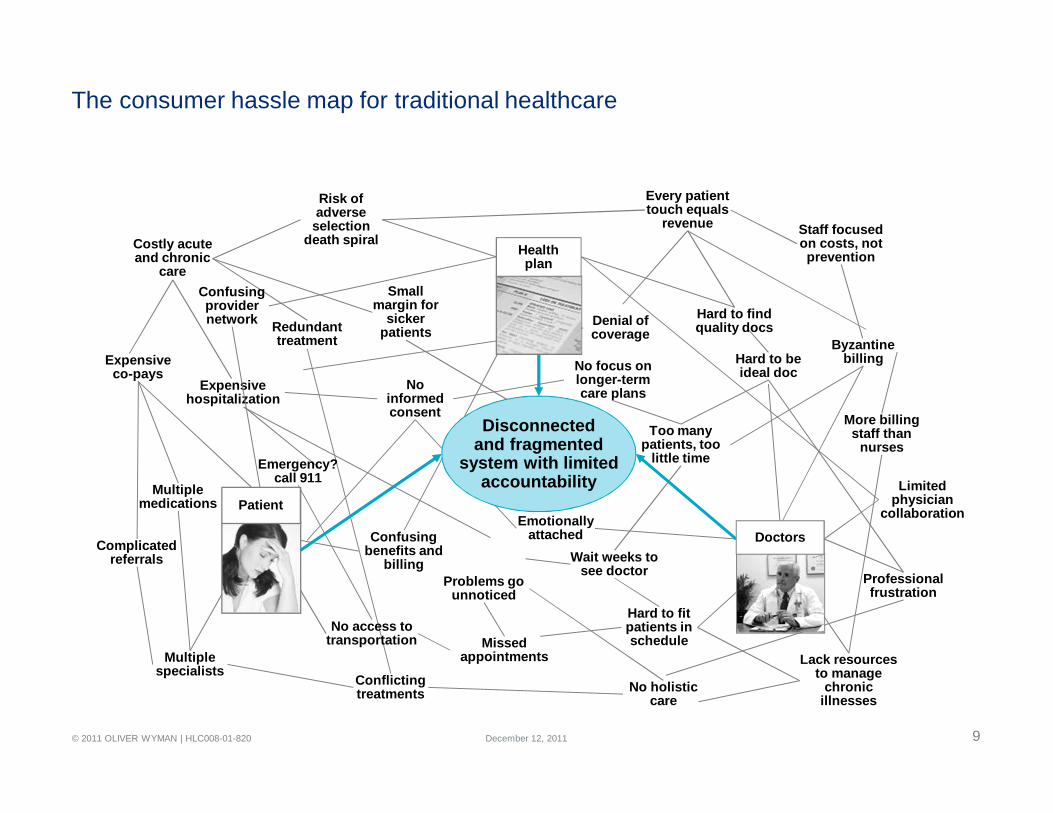

The consumer hassle map for traditional healthcare

Hard to fit patients in schedule

Lack resources to manage

chronic illnesses

Wait weeks to see doctor

Too many patients, too

little time

No focus on longer-term care plans

Emotionally attached

Byzantine billing

More billing staff than

nurses

Hard to be ideal doc

Professional frustration

Missed appointments

Problems go unnoticed

Complicated referrals

Multiple medications

Expensive hospitalization

Multiple specialists Conflicting

treatments No holistic care

Expensive co-pays

No informed consent

Redundant treatment

Hard to find quality docs

Costly acute and chronic

care

Risk of adverse

selection death spiral

Every patient touch equals

revenue Staff focused on costs, not prevention

Small margin for

sicker patients

Confusing benefits and

billing

Confusing provider network

Limited physician

collaboration

Disconnectedand fragmented

system with limitedaccountability

Emergency? call 911

Denial of coverage

No access to transportation

Healthplan

Doctors

Patient

December 12, 2011

10© 2011 OLIVER WYMAN | HLC008-01-820

Traditionalists

Percentage of Buyers 29% 26% 11% 25% 9%

Attitudes

• View insurance as a commodity, want basic coverage

• Not looking for help, advice or a relationship with their health plan

• Very willing to engage with insurers in health management activities

• Want help making healthcare decisions

• Experienced with the healthcare system and trust their doctor

• Price is most important• Willing to compromise

convenience and access to save $

• Willing to stay healthy to save on premiums

• No desire to engagewith insurers

• Like status quo• See greater engagement

as an unnecessary inconvenience

• Want easy, convenient access to healthcare

• Value technology, willing to try new things

• Willing to spend $for value

Demographics

• Less educated (~40% only finished high school), less employed, struggling to makeends meet

• Mix of singles and small families

• Largely middle-class• 30-40-somethings• Mix of single and families

• Lower middle class• 30-40-somethings• Mix of single and families

• Aging baby boomer• Employed or homemaker• Financially stable• Many empty nesters,

some dependents

• Younger, dualincome families

• Well-educated, majority have at least a college degree

Health Status and Lifestyle

• >75% currently uninsured

• Healthy, but riskier lifestyles

• ~50% currently uninsured

• At-Risk/Chronic, but attempting to get better with positive lifestyles

• ~50% insured (Indiv)• Healthy with good

lifestyles

• ~70% insured (SG)• At-Risk/Chronic• Avoid smoking or

drinking, but don’t exercise

• ~80% insured (SG/Indiv)• Healthy & At-Risk• Protect health with

exercise

Busy FamiliesWant to Be Healthier

Engaged to Save

Struggling & Unengaged

Source: Oliver Wyman Consumer Survey and Analysis. Health Status based on self-reported health conditions.

“I work 2 jobs to pay for food and a place to live, I’m not sick, so I just want basic insurance to cover me in case”

“I’ll do whatever it takes to get a better price on health insurance. I don’t need a lot”

“I want to be healthier, but its not easy. I’d like less expensive insurance, but am not willing to limit my options, I like my doctor.”

“The health insurance I already have works well for me, why fix something that isn’t broken?”

“I’m too harried to spend much time thinking about health insurance for me and my family, but I want care when I need it”

Oliver Wyman consumer segments – five distinct markets with unmet needs

December 12, 2011

11© 2011 OLIVER WYMAN | HLC008-01-820

Consumers will buy differently than employers bought for them – and their $500 BN in buying power will reshape the marketplace

• Lower cost through benefit buy downs and cost shifting to employees; facilitated through brokers and consultants

• Reduce employee noise through a broad access one-size-fits-all provider network

• Limited offering of opt-in health management programs focused on reducing medical cost

• Transactional service and administrative efficiency to lower cost and minimize employee feedback

1

2

3

4

• Buy an affordable product by balancing benefits, personalized engagement, and physician/health system choices with cost and exposure

• Select a personalized set of physicians and health systems to meet your needs and your budget

• Consumer-focused engagement programs to improve health and reduce consumer costs

• Personalized, integrated, simple and effective service focused on the consumer’s needs

NETWORK

PRODUCT

HEALTHMANAGEMENT

SERVICE

Employer-driven wholesale model Consumer-driven retail model

December 12, 2011

12© 2011 OLIVER WYMAN | HLC008-01-820 December 12, 2011

HEALTH MANAGEMENT COMPANY IMPLICATIONS

Section 2

13© 2011 OLIVER WYMAN | HLC008-01-820

Leading the volume to value revolution

Traditionalhealthcare

organizations

Value-basedhealthcarecompanies

• CEO and Board driven vision

• CEO-driven change agenda

• CEO actions to address barriers

• Physician-led disease-focused businesses

• Commercializing value-based care

• Rebuilding the business model

• Shifting organizational culture

Transforming the healthcare system requires a redesign of how healthcare is managed and delivered and the underlying economics

Healthcare CEO perspectives

December 12, 2011

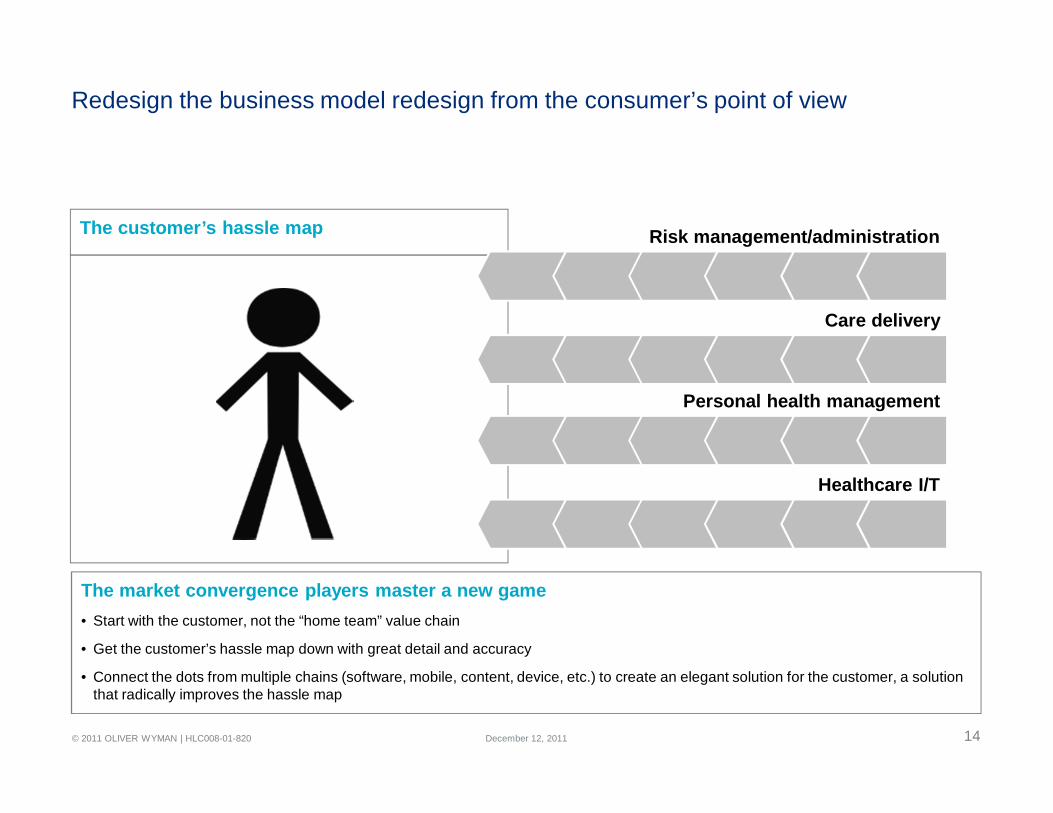

14© 2011 OLIVER WYMAN | HLC008-01-820

The Customer’s Hassle Map

The customer’s hassle map

Redesign the business model redesign from the consumer’s point of view

Risk management/administration

Care delivery

Healthcare I/T

Personal health management

The market convergence players master a new game• Start with the customer, not the “home team” value chain

• Get the customer’s hassle map down with great detail and accuracy

• Connect the dots from multiple chains (software, mobile, content, device, etc.) to create an elegant solution for the customer, a solution that radically improves the hassle map

December 12, 2011

15© 2011 OLIVER WYMAN | HLC008-01-820

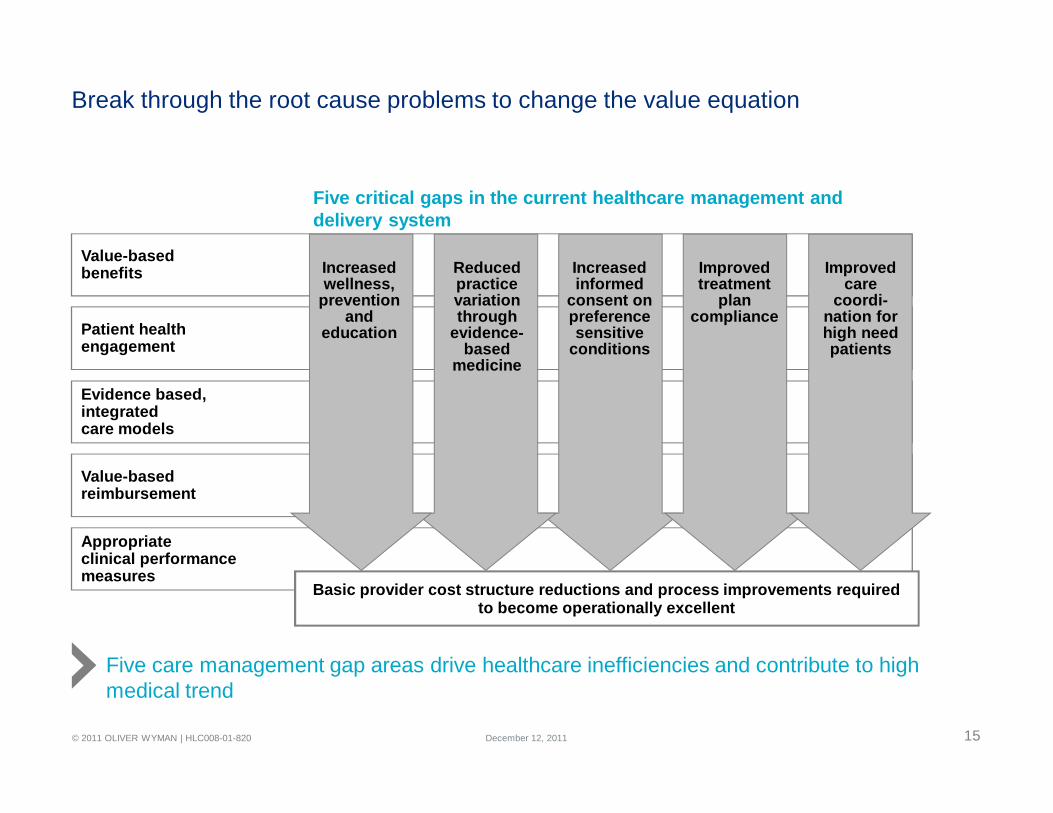

Break through the root cause problems to change the value equation

Evidence based, integratedcare models

Patient health engagement

Value-based benefits

Value-based reimbursement

Appropriate clinical performancemeasures

Improved care

coordi-nation for high need patients

Improved treatment

plan compliance

Reduced practice variation through

evidence-based

medicine

Increased informed

consent on preference sensitive

conditions

Increased wellness,

prevention and

education

Basic provider cost structure reductions and process improvements required to become operationally excellent

Five critical gaps in the current healthcare management and delivery system

Five care management gap areas drive healthcare inefficiencies and contribute to high medical trend

December 12, 2011

16© 2011 OLIVER WYMAN | HLC008-01-820

Develop a clinical strategy based on population health needs – reinvent the care models accordingly

TransactionalEfficiency (FFS)

Episodic Care Models(payment model driven)

Condition Based Care Models(care model driven)

Population Based Care Models(integrated whole person)

Simple service based models that can continue to deliver highly efficient care in aFFS environment

Complex service based models that can deliver efficient care through high levels of specialization and low operational variability

Specialized care delivery model that is organized along specific condition and/or disease etiologies

High value-based delivery model that manages the clinical risk of targeted or whole patient populations

• Stand-alone ERs• Urgent care facilities• Dermatologists• Ophthalmologists• Dentists• Walk-in-clinics

• Orthopedics (Hips and knees)

• CV surgery• General/

specialty surgery

Definition

Example Model Types

• Cardiology• Cancer• Diabetes • Pulmonary• Kidney

• Partial Pop. Managers• Frail elder• High risk• Poly-chronic• Full Pop Managers• ACOs• Globally capitated models

December 12, 2011

17© 2011 OLIVER WYMAN | HLC008-01-820

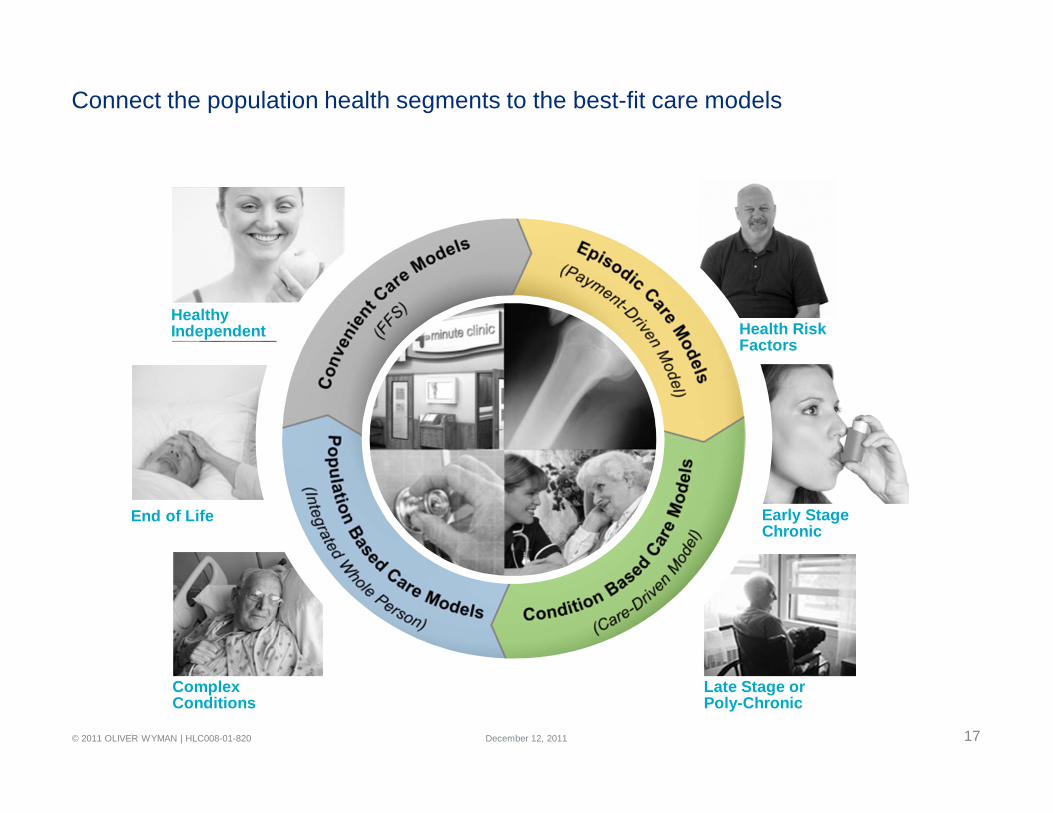

Connect the population health segments to the best-fit care models

End of Life

ComplexConditions

HealthyIndependent Health Risk

Factors

Late Stage orPoly-Chronic

Early StageChronic

December 12, 2011

18© 2011 OLIVER WYMAN | HLC008-01-820

Bring the missing capabilities to market – they are required for long-term success

INFRASTRUCTURE

Electronic Health Record (Integrated EHR)

Clinical Data Repository (CDR)

HEALTH MANAGEMENT ENABLEMENT

Clinical Performance Management

Patient Care Programs Clinical Risk Management andPayer Contracting

Clinical Model Redesign

Population Management, Patient Registriesand Personalized MedicineTreatment Management and

Multidisciplinary Teams

ACO or IDN CommercializationProvider and Service Network Development

Evidenced Based Guidelines andClinical Trial Programs

Clinical Strategy andLeadership Model

Care model redesign

Performance management

Commercial-ization

December 12, 2011

19© 2011 OLIVER WYMAN | HLC008-01-820

Replace fee for service networks with value based care models over time

Intensive OP Care Programs(80% of improvement opportunity)

Proactive Prevention(17%)

Routine Care (3%)

% Members 20% 24% 56%

% Costs 58% 17% 25%

IOCP

Prevention & Chronic Care Management

Routine Care

Intensive active management of the sickest individuals within the population

Proactive engagement for early chronic and at-risk individuals

Efficient routine and urgent care services for everyone

Complex/Poly-chronic Early Stage Chronic/At Risk HealthyPopulation

Model Description

Integrated Community Care Model

Source: Sample claims data, OW Analysis

PCMH (3 in 1 model)

UrgentCare

HomeCare

Social Services

Transport

Nutrition& Meals

Drug & Alcohol

Programs

CommunityPrograms

Fitness

3 in 1 PCMH and IOCP model improves cost and value for the complex poly chronic patients

December 12, 2011

20© 2011 OLIVER WYMAN | HLC008-01-820

Replace fee for service networks with value based care models over time

Offices Services

Offices Services

Diagnostic Imaging Diagnostic

Imaging

Pre-Hab Services Pre-Hab

Services

Surgical Center

Surgical Center

Anesthesia

Anesthesia

Implant or Device

Implant or Device

Pharmacy

Pharmacy

Rehab Services

Rehab Services

FFS Revenue Management FFV Integrated Cost and QualityManagement

TODAY100%

FUTURE85%

ILLUSTRATIVE

• Pain management effectiveness

• Functional improvement services

• Return to work

• Patient satisfaction

The shift

to value

Integrated orthopedic care model lowers costs by 15% Performance outcome measures

December 12, 2011

21© 2011 OLIVER WYMAN | HLC008-01-820

Total Care

Treat the tumor Treat the patientCoordinated Oncology Care

Patient

Interventional Radiology

Histopathology

Molecular Profiling

Research

Surgical Oncology

Medical Oncology

Radiation Oncology

Imaging/Radiology

Evidenced-based Pathways

Focal Therapy

Psychological Support

Nutrition

Financial Guidance/Support

Hospice

Hair and Beauty

Complimentary Therapy

Palliative Care

Information

Fitness/Rehabilitation

Survivorship

Multi-Disciplinary Team/ Treatment

Planning

Patient Navigation

PCP/Cancer Physician Alignment

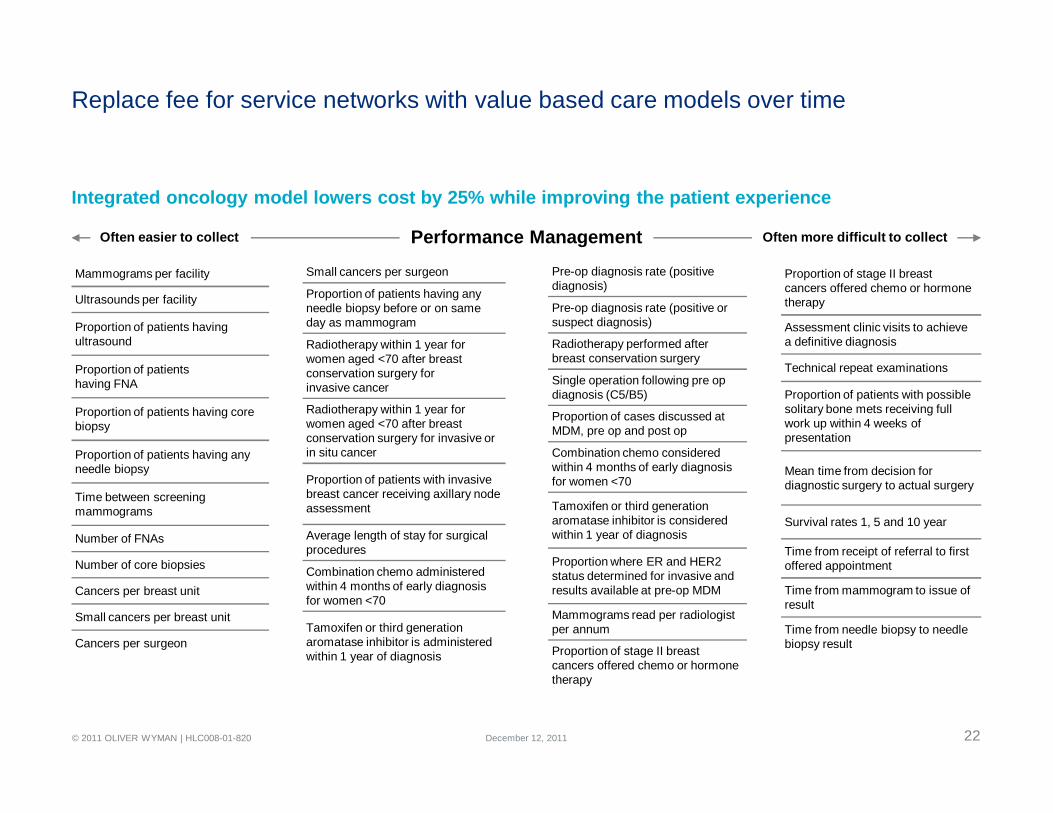

Replace fee for service networks with value based care models over time

Integrated oncology model lowers cost by 25% while improving the patient experience

December 12, 2011

22© 2011 OLIVER WYMAN | HLC008-01-820 December 12, 2011

Mammograms per facility

Ultrasounds per facility

Proportion of patients having ultrasound

Proportion of patientshaving FNA

Proportion of patients having core biopsy

Proportion of patients having any needle biopsy

Time between screening mammograms

Number of FNAs

Number of core biopsies

Cancers per breast unit

Small cancers per breast unit

Cancers per surgeon

Small cancers per surgeon

Proportion of patients having any needle biopsy before or on same day as mammogram

Radiotherapy within 1 year for women aged <70 after breast conservation surgery forinvasive cancer

Radiotherapy within 1 year for women aged <70 after breast conservation surgery for invasive or in situ cancer

Proportion of patients with invasive breast cancer receiving axillary node assessment

Average length of stay for surgical procedures

Combination chemo administered within 4 months of early diagnosis for women <70

Tamoxifen or third generation aromatase inhibitor is administered within 1 year of diagnosis

Pre-op diagnosis rate (positive diagnosis)

Pre-op diagnosis rate (positive or suspect diagnosis)

Radiotherapy performed after breast conservation surgery

Single operation following pre op diagnosis (C5/B5)

Proportion of cases discussed at MDM, pre op and post op

Combination chemo considered within 4 months of early diagnosis for women <70

Tamoxifen or third generation aromatase inhibitor is considered within 1 year of diagnosis

Proportion where ER and HER2 status determined for invasive and results available at pre-op MDM

Mammograms read per radiologist per annum

Proportion of stage II breast cancers offered chemo or hormone therapy

Proportion of stage II breast cancers offered chemo or hormone therapy

Assessment clinic visits to achieve a definitive diagnosis

Technical repeat examinations

Proportion of patients with possible solitary bone mets receiving full work up within 4 weeks of presentation

Mean time from decision for diagnostic surgery to actual surgery

Survival rates 1, 5 and 10 year

Time from receipt of referral to first offered appointment

Time from mammogram to issue of result

Time from needle biopsy to needle biopsy result

Replace fee for service networks with value based care models over time

Integrated oncology model lowers cost by 25% while improving the patient experience

Often easier to collect Often more difficult to collectPerformance Management

23© 2011 OLIVER WYMAN | HLC008-01-820

Replace fee for service networks with value based care models over time

Health care goes retail

Closed ACO with patient-directed care

Closed ACO withpatient navigator

ACO with patient-centered medical home

• $500 per month premium• $150 monthly contribution

after subsidy • No co-pay• Silver benefits

• $425 per month premium• $75 monthly contribution

after subsidy • No co-pay • Silver benefits

• $400 per month premium• $50 monthly contribution after subsidy • No co-pay• Gold benefits

• Good community brand• Reputable physician panel

• Good community brand• Affiliation with an academic• Reputable physician panel• Patient navigator• 24-hour telephonic triage

• Good community brand• Reputable physician panel• 24-hour telephonic triage • Wellness program with

integrated fitness• Health coach

ACOs become exchange eligible community products and complete on value

December 12, 2011

24© 2011 OLIVER WYMAN | HLC008-01-820

Replace fee for service networks with value based care models over time

Health care goes retail

Healthy independentconsumer network

Lower income working classfamily network

Poly-chronic consumer network?

• Retailer walk-in clinic (Walgreens)• e-health primary care access

(American Well or Google +)• Social media community • Local community health system• Center of excellence (Mayo)

• Walmart exclusive for pharmacy and walk-in clinic

• Designated patient centered medical home with integrated AICU

• Community ACO with a value specialist network

• Meets key needs• Saves money• Offers Value-adds (fitness center,

life insurance, etc.)

• Meets critical family healthcare needs• Affordable• Better patient care

Consumer needs driven network models

December 12, 2011

25© 2011 OLIVER WYMAN | HLC008-01-820

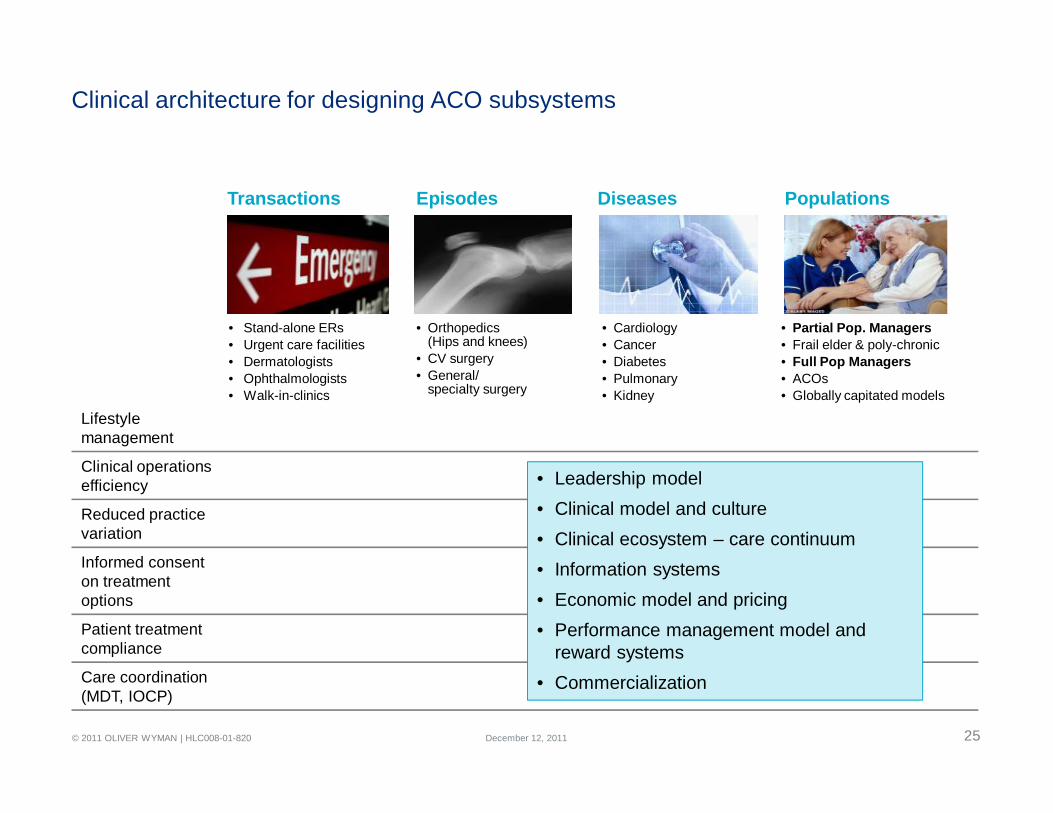

Clinical architecture for designing ACO subsystems

Transactions Episodes Diseases Populations

• Stand-alone ERs• Urgent care facilities• Dermatologists• Ophthalmologists• Walk-in-clinics

• Orthopedics (Hips and knees)

• CV surgery• General/

specialty surgery

• Cardiology• Cancer• Diabetes • Pulmonary• Kidney

• Partial Pop. Managers• Frail elder & poly-chronic• Full Pop Managers• ACOs• Globally capitated models

Lifestylemanagement

Clinical operations efficiency

Reduced practice variation

Informed consent on treatment options

Patient treatment compliance

Care coordination (MDT, IOCP)

• Leadership model• Clinical model and culture• Clinical ecosystem – care continuum• Information systems• Economic model and pricing• Performance management model and

reward systems• Commercialization

December 12, 2011

26© 2011 OLIVER WYMAN | HLC008-01-820

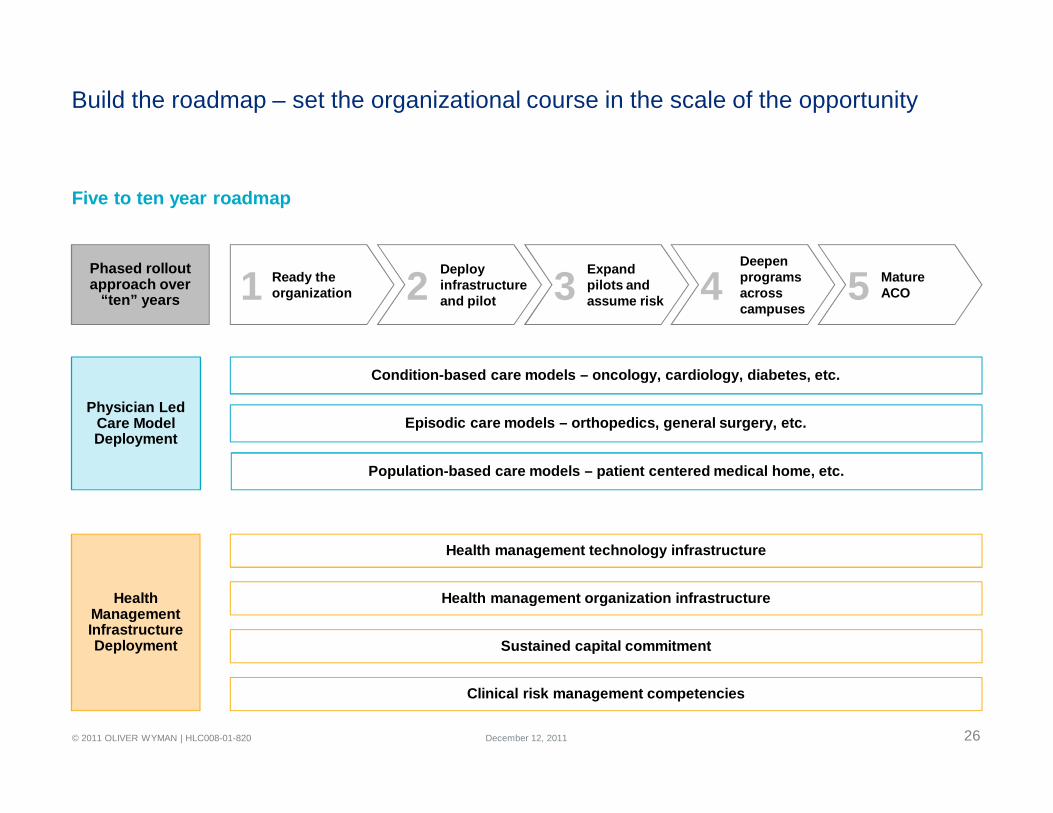

Build the roadmap – set the organizational course in the scale of the opportunity

Condition-based care models – oncology, cardiology, diabetes, etc.

Episodic care models – orthopedics, general surgery, etc.

Population-based care models – patient centered medical home, etc.

Health management technology infrastructure

Health management organization infrastructure

Sustained capital commitment

Clinical risk management competencies

Phased rollout approach over

“ten” years

Physician Led Care Model Deployment

Health Management Infrastructure Deployment

Mature ACO

Deepen programs across campuses

Expandpilots andassume risk

Deployinfrastructureand pilot

Ready the organization1 2 3 4 5

Five to ten year roadmap

December 12, 2011

27© 2011 OLIVER WYMAN | HLC008-01-820

Keep your eye on the prize – shift the value formula and commercialize the ACO

Health System

Medical Beds(Designated hospitalist)

Intensive Care Unit Post Acute Care Rehabilitation (physical,

stroke, etc.) Skilled nursing Home care Hospice

OR #1 OR #2 OR #3 OR #4

Cardiac CareSurgical Beds

Wellness and FitnessAmbulatory Surgery (Day services)Neurology

Urology Diagnostic Services Psychiatry Emergency Department Remote MonitoringWomen’s Services Radiation Therapy

IBD & Crohn’s Diagnosis and stage

specific capitation payment model

Gastroenterologist is the care QB

Use of multi-disciplinary care teams with GI coordination

MolecularDiagnostics for

Drug Metabolism

Orthopedics Acuity adjusted case

rate with performance measures

Orthopedist contracts for and manages all aspects of patient care

Ambulatory Surgery Center

PhysicalTherapy

Device Maker

Anesthesiology

SocialServices

Fitness &Nutrition

HospitalOR/ICU

Surgical Center of Excellence

Acuity adjusted caserate with performance measures

Surgeon contracts for and manages allaspects of patient care

Ambulatory Surgery Center

PhysicalTherapy

Device Maker

Anesthesiology

Social Services

Fitness & Nutrition

Hospital OR/ICU

Episodic Ecosystems

Rehab Services

Condition Ecosystem

Patient biopsy, referral & MDT

Patient referral to surgeon

Coordination of diabetic patient’s disease related

surgical needs

Routine Care or

Walk in Clinic

Dermatology

Chiropractic

Cancer patient referraland survivorship

management

Hospital Emergency

Services

Nutrition & Fitness

Patient Engagement

Programs

Social Services

QB for PatientCare (PCP andMedications)

Hospital Medical Intensive Care

MDT Lead forInvasive Treatment

Plans

Medication Management

PersonalizedMedicine

Chronic AcuteEcosystem

Patient referral to orthopedist

Population Management Ecosystem

Patient CV referral

Patientreferral to CAM

Patient referral to surgeon and MDT

coordination

Optometry

Oncology Diagnosis and stage specific

capitation payment model Medical oncologist care QB Use of Multi-disciplinary care

teams

Hospital Diagnostic

Imaging

AmbulatorySurgical Services

Hospice & Palliative Care

ClinicalTrials

Social Services

Fitness,Nutrition & Beauty

Hospital-Based Radio-Therapy

Hospital Medical Intensive Care

Hospital OR

Personalized Medicine

(MDX, TissueBanking)

InfusionTherapy

Fitness & Wellness Services

Primary Care Medical Home Acuity adjusted clinical risk for non

emergent services Coordination of all care Integration of wellness, nutrition and

social programs

Bio Metric Monitoring

Chronic Care Management

Hospital Emergency

Services

Specialty Care Coordination

Health Risk Assessment &

Care Plan

Hospitalist Program

Social & Educational

Services

Routine Care

Urgent Care Triage

Wellness, Prevention

Referral andco-management

of diabetes patient

Behavioral Health

Diabetes with Complications Diagnosis and stage specific

capitation payment model Endocrinologist is the care QB Use of multi-disciplinary care

teams with PCP coordination

Hospital Emergency

Services

Nutrition & Fitness

Patient Engagement

Programs

PodiatryServices

Social Services

QB MDT for interdependent

conditions

Ophthalmology Services

Medication Management

Bio Metric Monitoring

Hospital Medical Intensive Care

InpatientRehabilitation

Diagnosis/stage specific capitation payments for designated conditions

Acuity-adjusted population paymentmodel for chronic conditions

Cardiologist is the care QB Use of multi-disciplinary

care teams with PCP partners

Nutrition & Fitness

Hospital Emergency

Services

Hospital Medical Intensive Care

QB MDT for interdependent

conditions

Bio Metric Monitoring

Patient Engagement

Programs

DiagnosticImaging

HospitalOR/ICU

CardiacCath Lab

InpatientRehabilitation

InpatientStroke Clinic Cardiovascular Disease

EHR updates for the ecosystem

Referral and co-management of

IBD patient

Pharmacy

Pharmacy

Population management ecosystem

Episodic care ecosystem

Condition ecosystem

Transactional market services

Health system

Chronic acute ecosystem

CommunityPharmacy

CommunityPharmacy

CommunityPharmacy

CommunityPharmacy

December 12, 2011

28© 2011 OLIVER WYMAN | HLC008-01-820 December 12, 2011

THE VOLUME TO VALUE REVOLUTIONSection 3

29© 2011 OLIVER WYMAN | HLC008-01-820

Healthcare 2020 drivers

• The current system will be bankrupt without change – CMS, Medicaid, employers and individuals

• $3 TN market with 5% growth and unhappy customers will stimulate investment and disruptive innovation

• Consumer demand will reshape the basis of competition

• CMS-led value based payment models will drive health systems to organize around value

• Cloud computing – digitization and integration (EHR, PHR, EBM) will enable vastly improved healthcare organizations

• Personalized medicine and genomics will drive “market of one” thinking

• Healthcare will be much more virtual and global – even service delivery

• Social media, gaming and communities will reshape consumer expectations and accelerate change

• Industry convergence (four chain) will create new world healthcare organizations – health, media, finance, lifestyle, IT

Reshaping healthcare for the next generationThree quarters of the cost, one and half times the value with a radically improved patient experience

December 12, 2011

30© 2011 OLIVER WYMAN | HLC008-01-820

The Customer’s Hassle Map

The customer’s hassle map

Business model redesign starts with the customer hassle map

Risk Management/Administration

Care Delivery

Healthcare I/T

Personal Health Management

The market convergence players master a new game

• Start with the customer, not the “home team” value chain

• Get the customer’s hassle map down with great detail and accuracy

• Connect the dots from multiple chains (software, mobile, content, device, etc.) to create an elegant solution for the customer, a solution that radically improves the hassle map

December 12, 2011

31© 2011 OLIVER WYMAN | HLC008-01-820

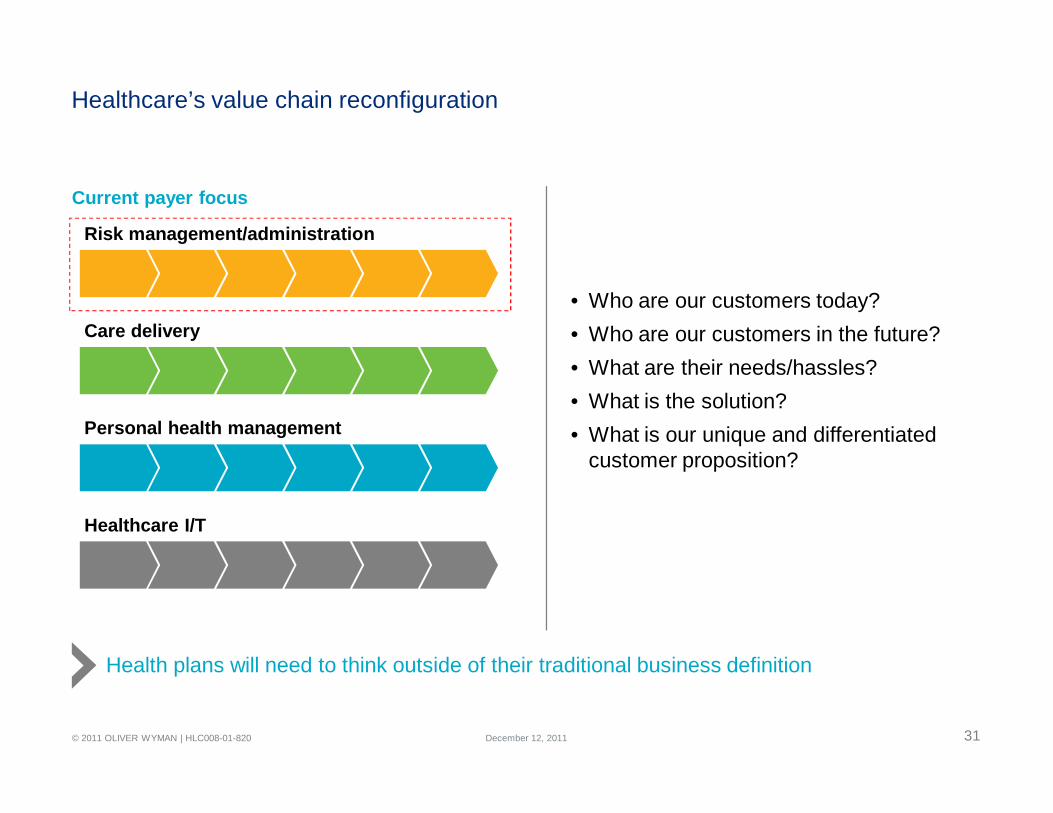

Current payer focus

Healthcare’s value chain reconfiguration

• Who are our customers today? • Who are our customers in the future?• What are their needs/hassles?• What is the solution?• What is our unique and differentiated

customer proposition?

Risk management/administration

Personal health management

Care delivery

Healthcare I/T

Health plans will need to think outside of their traditional business definition

December 12, 2011

32© 2011 OLIVER WYMAN | HLC008-01-820

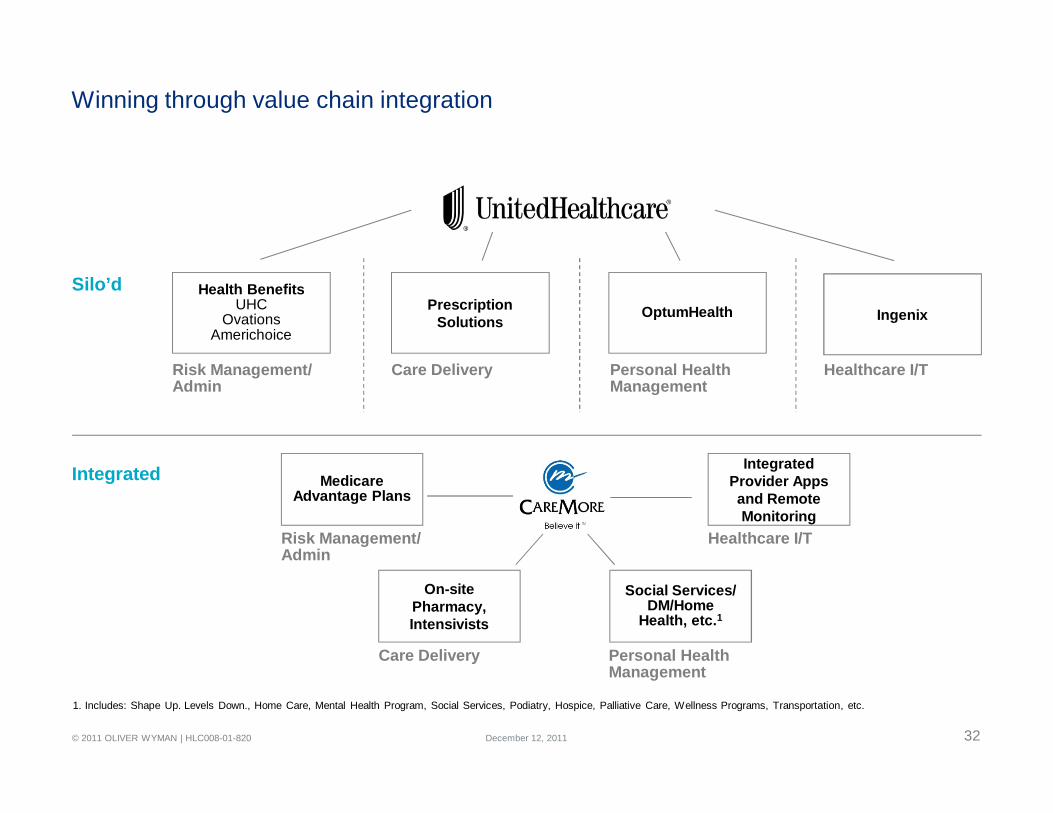

Winning through value chain integration

Health BenefitsUHC

OvationsAmerichoice

OptumHealth

Risk Management/ Admin

Ingenix

Healthcare I/TPersonal Health Management

PrescriptionSolutions

Care Delivery

Medicare Advantage Plans

On-site Pharmacy, Intensivists

Social Services/DM/Home

Health, etc.1

Integrated Provider Apps and Remote Monitoring

Healthcare I/T

Care Delivery

Risk Management/ Admin

Personal Health Management

Silo’d

Integrated

1. Includes: Shape Up. Levels Down., Home Care, Mental Health Program, Social Services, Podiatry, Hospice, Palliative Care, Wellness Programs, Transportation, etc.

December 12, 2011

33© 2011 OLIVER WYMAN | HLC008-01-820

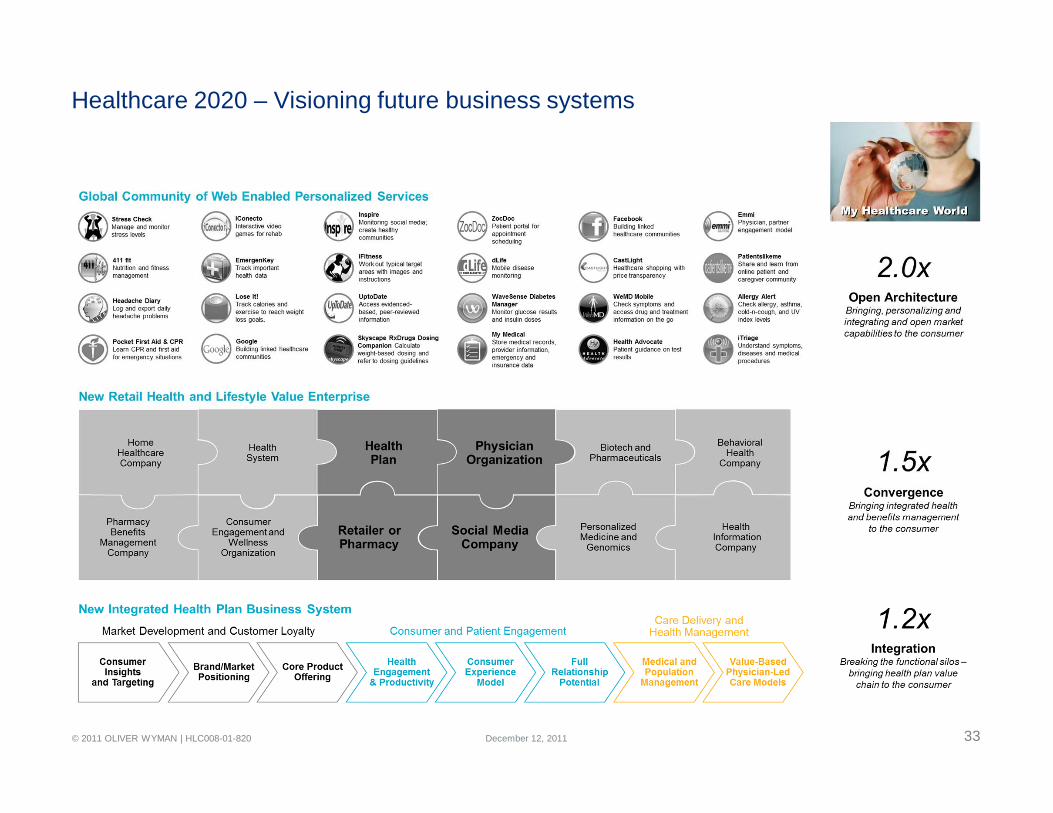

Healthcare 2020 – Visioning future business systems

December 12, 2011

34© 2011 OLIVER WYMAN | HLC008-01-820

Early signs of convergence

+

+ + +

+ ++ +

Health Plan and Health System

National Plan and HIT

Retail Pharmacy and Clinic

+

+

+ + +

+

+

+Powered by:

December 12, 2011

35© 2011 OLIVER WYMAN | HLC008-01-820 December 12, 2011

THE RACE TO VALUESection 4

36© 2011 OLIVER WYMAN | HLC008-01-820

Consumer demand redefines competition – web 2.0 expectations meet healthcare

• Personalized networks• Value based benefit plans • Integrated product and service lifestyle

packages • Health coaches – with connected homes• Web based healthcare shopping services

with performance transparency• e-pharmacist access models• Social communities with expert advisors• Personalized integrated mobile applications • Gaming and personalized avatar applications• 24 hour e-health triage services

• Personalized hassle free easy-to-use healthcare services

• Personalized solutions leading to greater engagement

• Personalized provider networks • Integrated solutions – meeting health,

lifestyle and financial needs• Value based benefits creating aligned

incentives to motivate behavioral changes• Personalized coaching and lifestyle/health

itinerariesLose It!

Track calories and exercise.

iFitnessWork out typical target areas with images and

instructions.

Natural CuresTreat conditions with natural and prescription therapies.

WaveSense Diabetes Manager

Monitor glucose results and insulin doses.

iTriageUnderstand diseases and medical procedures.

My MedicalStore medical records,

provider information, and insurance data.

WebMD Mobile Check symptomson the go.

Allergy Alert

Patientslikeme Online patient and caregiver community.

Stress Check Manage and monitor stress levels

Health Cloud Access Google Health records.

Headache Diary

Consumer engagementTransforming the consumer experience – a bridge to better health

Improving healthcare quality while bending the trend through active consumer engagement

Staying on top of your healthcare needs

December 12, 2011

37© 2011 OLIVER WYMAN | HLC008-01-820

Empowered point-of-care with personalized actionable insights – the last mile

• Meaningful use – $44 BN

• Electronic health record adoption

• Embedded order sets

• Patient history

• Embedded pharmacy formulary

• Lifestyle factors

• Patient itinerary

• Patient portals

• Mobile applications

• More complete health evaluation

• Improved patient engagement

• Improved treatment compliance

• Preventative focus where there arerisk factors

• Reduction of unwarranted practice variation

• Improved quality – drug interaction, care alerts, screening, etc.

Electronic health record Transforming the point-of-care

Improving healthcare quality whilebending the trend

Perfecting thepoint of care

December 12, 2011

38© 2011 OLIVER WYMAN | HLC008-01-820

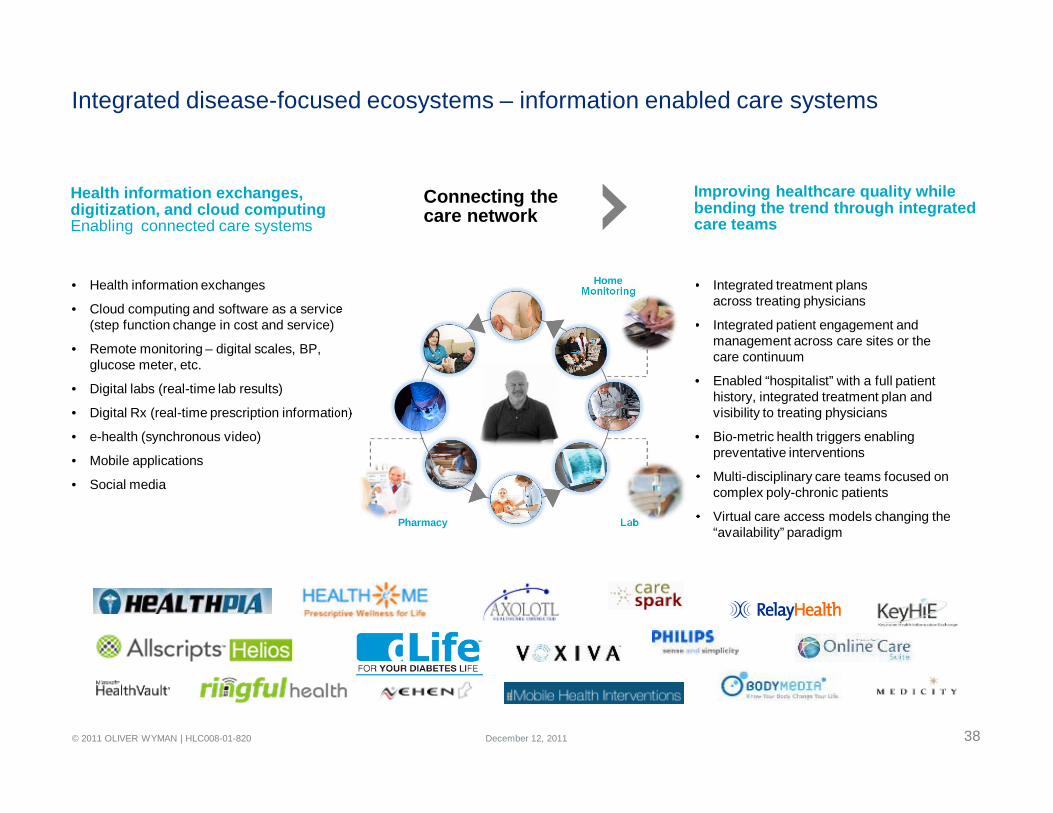

Integrated disease-focused ecosystems – information enabled care systems

• Health information exchanges

• Cloud computing and software as a service (step function change in cost and service)

• Remote monitoring – digital scales, BP, glucose meter, etc.

• Digital labs (real-time lab results)

• Digital Rx (real-time prescription information)

• e-health (synchronous video)

• Mobile applications

• Social media

• Integrated treatment plans across treating physicians

• Integrated patient engagement and management across care sites or the care continuum

• Enabled “hospitalist” with a full patient history, integrated treatment plan and visibility to treating physicians

• Bio-metric health triggers enabling preventative interventions

• Multi-disciplinary care teams focused on complex poly-chronic patients

• Virtual care access models changing the “availability” paradigm

Health information exchanges, digitization, and cloud computing Enabling connected care systems

Improving healthcare quality while bending the trend through integrated care teams

Home Monitoring

LabPharmacy

Connecting thecare network

December 12, 2011

39© 2011 OLIVER WYMAN | HLC008-01-820

New cloud enabled ACOs – from information to actionable insights

• Patient registries or databases

• Comprehensive patient or consumer profiles – health history, health status, lifestyle, behaviors

• Genomic profiles and tissue banking

• Evidence based guidelines – integrated health literature, clinical trial results, published studies

• Physician and health system databases with related attributes – treatment, cost and outcomes

• Clinical population segment information –treatment, costs and outcomes

• Disease and condition information –treatment, costs and outcomes

• Consumer stratification and clinical segmentation by health need – 15%/55% rule

• Patient-panel stratification for physician practices to shift to population management

• Real-time EBM guidelines with clinical economics at point of care

• Virtual shared treatment plans enabling MDTs – reducing practice variation and duplicate services

• Poly chronic patient care guidelines –addressing high cost clinical segments

• Social media with leader boards and information transparency – accelerating positive change

Health informatics and cloud computingTransforming the system though personalized actionable insights

Improving healthcare quality while bending the trend through actionable insights

Home Monitoring

LabPharmacy

Labfeeds

ResearchStudies

Clinical Trials

GenomicsCMSData

ProviderDB

PersonalizedActionable

Insights

HealthyIndependent

Health RiskFactors

Complex/Polychronic

Connected carenetwork

PatientDB

VBEBM

Powering the system thru the health cloud

December 12, 2011

40© 2011 OLIVER WYMAN | HLC008-01-820

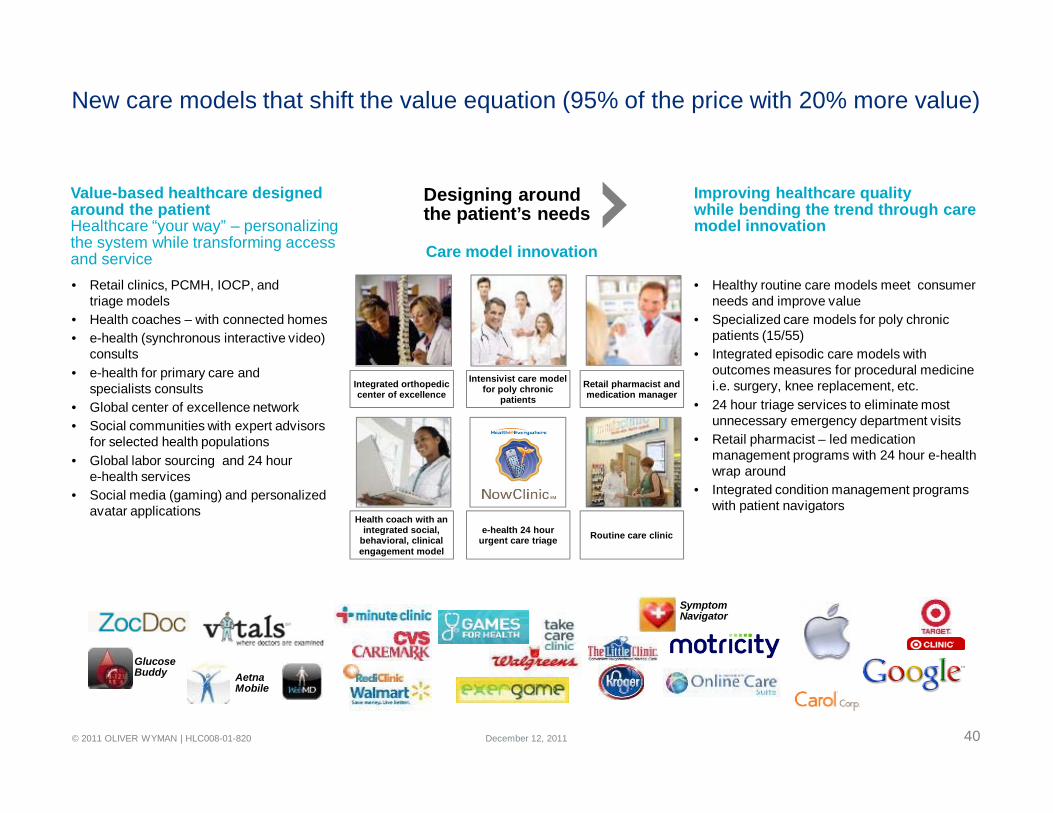

New care models that shift the value equation (95% of the price with 20% more value)

• Retail clinics, PCMH, IOCP, and triage models

• Health coaches – with connected homes• e-health (synchronous interactive video)

consults• e-health for primary care and

specialists consults • Global center of excellence network• Social communities with expert advisors

for selected health populations• Global labor sourcing and 24 hour

e-health services• Social media (gaming) and personalized

avatar applications

• Healthy routine care models meet consumer needs and improve value

• Specialized care models for poly chronic patients (15/55)

• Integrated episodic care models with outcomes measures for procedural medicine i.e. surgery, knee replacement, etc.

• 24 hour triage services to eliminate most unnecessary emergency department visits

• Retail pharmacist – led medication management programs with 24 hour e-health wrap around

• Integrated condition management programs with patient navigators

Glucose Buddy

Symptom Navigator

Aetna Mobile

Care model innovation

Integrated orthopedic center of excellence

Intensivist care model for poly chronic

patientsRetail pharmacist and medication manager

Health coach with an integrated social,

behavioral, clinical engagement model

e-health 24 hour urgent care triage Routine care clinic

Value-based healthcare designed around the patientHealthcare “your way” – personalizing the system while transforming access and service

Improving healthcare quality while bending the trend through care model innovation

Designing around the patient’s needs

December 12, 2011

41© 2011 OLIVER WYMAN | HLC008-01-820

Value-based payment models – fueling the volume to value revolution

Health value-driven business model• Performance bonuses based on

comparative transparent clinical cost/quality information

• Service fees for adding new services into a practice – care coaching

• Risk adjusted episodes of care – with a clinical bill of material and outcomes measures

• Risk adjusted disease-basedcapitation – with outcomes measures

• Risk adjusted condition-based capitation – with outcomes measures

• Risk adjusted population-based capitation – like Medicare Advantage

• Creates economic motivation for ACOs, PCMHs and other coordinated care models to invest in needed changes to patient management

• Motivates the formation of care models around the high cost poly-chronic patients

• Enables care coordinators to “integrate the health ecosystem” and manage care across the care continuum

• Creates the foundation for shiftingthe basis of competition between competing systems

• Enables providers to commercialize their value to consumers and health plans

Value-based payment modelsNew healthcare economics align incentives and power the change

Improving healthcare quality while bending the trend through aligned incentives

Per diems Case rates Bundled payments

Risk adjusted capitation

Visit orvolume-based economic model

Population healthvalue-based

economic model

From visits to diseases and people

Getting what you pay for

December 12, 2011

42© 2011 OLIVER WYMAN | HLC008-01-820

Commercializing value-based solutions – public and private exchanges

Finding theperfect healthcare

Consumer segment specific products

Value based competitionwith lots of choice

• 76% of the 51 MM uninsured expressed intent to buy on the public exchanges –39 MM new insureds

• Small group and self funded employers will send another 46 MM shopping

• Consumers will be shopping for “best value” health benefits – measured by expected out-of-pocket costs and value

• Exchanges will provider consumers with tools to easily compare health plan offerings

• Web application players will bring personalized decision engines and advisors to guide consumer decision making

• Private exchanges will embrace a wide variety of health and lifestyle services

• Federalized bronze/silver product standards motivates new entrants

• Health plans differentiate on value – mostly through new network strategies

• Consumers shop for healthcare through the exchange – net costs drives decisions

• Web applications enable consumer shopping• Social media creates a “dialog” about what

to buy – transparent rating systems• Private exchanges for non-Federally

subsidized consumers offer a broad menu of services

• e-brokers bring personalization and shopping advice

• Mobile web applications help consumer predict future health needs

Shopping exchangesConsumers will make very different decisions than their employers made for them

85 MM consumers with $500 BN of purchasing power will change healthcare forever

December 12, 2011

43© 2011 OLIVER WYMAN | HLC008-01-820

Unlocking value?

December 12, 2011