higher education solutions 1 internal audit for colleges and universities by: wally wetherill,...

TRANSCRIPT

1

Higher Education Solutions

Internal Audit for Colleges and Universities

By:

Wally Wetherill, Regional Industry Partner – East Region

John McKay, Supervisory Consultant

OACUBO Conference

2

Higher Education Solutions

Internal Audit (IA)Assessing Risk Internal Audit Process-developing audit plans

and processExamples if IA workQuestions

Agenda

3

Higher Education Solutions

Internal Audit

Is the path to: Assessing and maintaining sufficiency in

compliance

Proactively addressing public scrutiny

Enabling transparency

4

Higher Education Solutions

Internal Audit Defined

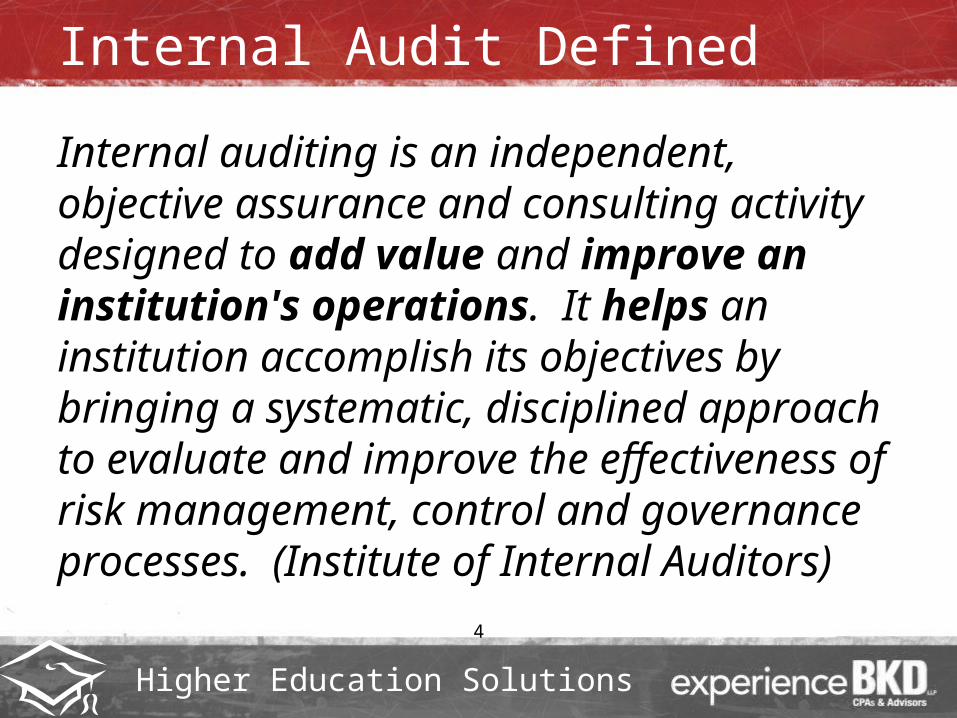

Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an institution's operations. It helps an institution accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control and governance processes. (Institute of Internal Auditors)

5

Higher Education Solutions

Internal Audit Simplified

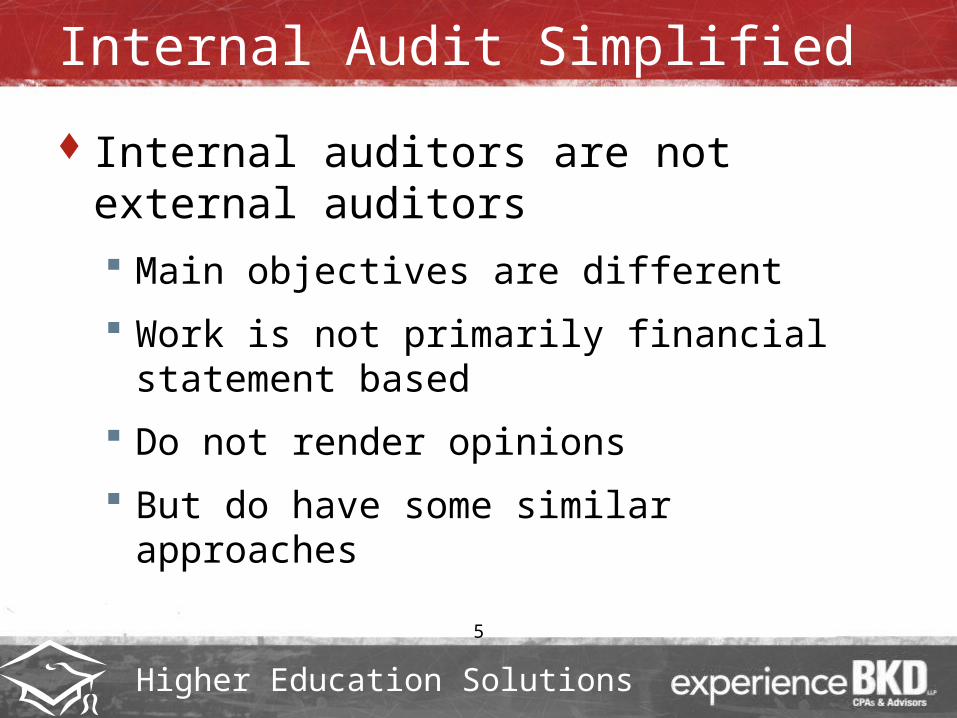

Internal auditors are not external auditors Main objectives are different

Work is not primarily financial statement based

Do not render opinions

But do have some similar approaches

6

Higher Education Solutions

Internal Audit Simplified Internal auditors

Are independent on their institutional reporting (direct report to Audit Committee)

Develop annual work plans through risk assessment and collaboration with senior and departmental management

Focus of audit work is on:• Laws and regulations (compliance)

• Policy and procedures (adherence)

• Efficiencies

• Process improvements

7

Higher Education Solutions

Internal Audit Simplified

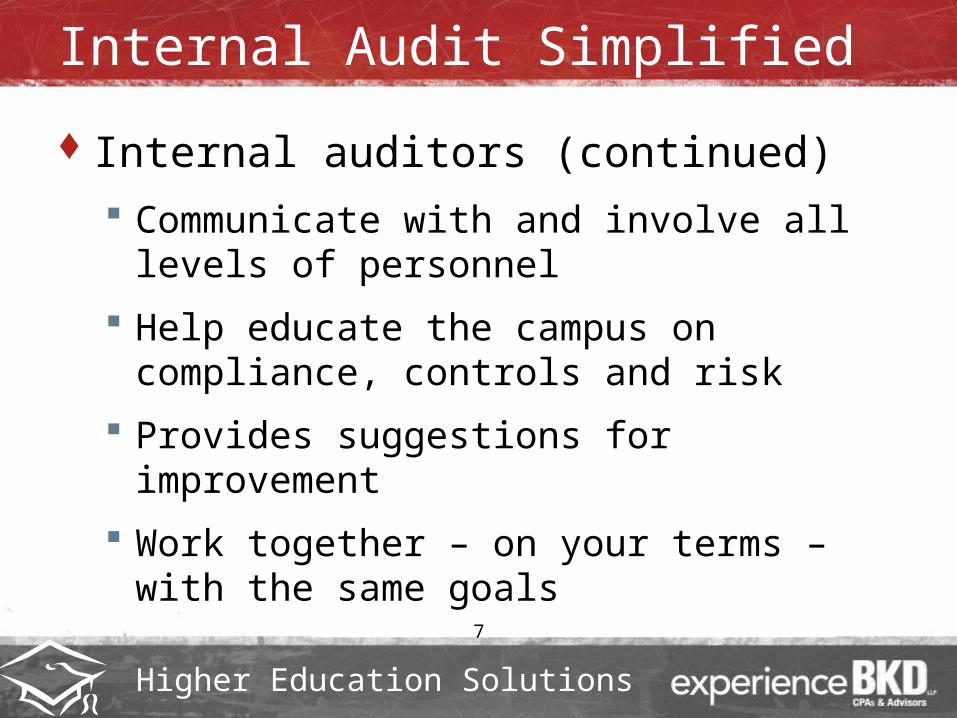

Internal auditors (continued) Communicate with and involve all levels of

personnel

Help educate the campus on compliance, controls and risk

Provides suggestions for improvement

Work together – on your terms – with the same goals

8

Higher Education Solutions

The Look of Internal Audit

In houseCo-sourcedOutsourced

* Regardless of how it is established, the process for conducting IA work remains the same

9

Higher Education Solutions

Establishing the IA Function

Define your look/structureAudit Charter – defines reporting structure

and authorityAudit Committee and Charter

10

Higher Education Solutions

Assess Risk

Enterprise Risk Management Management deploys and oversees ERM for the institution

• Define risk and opportunity

• Assess the risks and opportunities identified

• Management develops a means to proactively address the risks and opportunities identified:

► Avoid the risk – exit the activity giving rise to significant risk

► Reduce the risk – take action to reduce the likelihood or impact related to risk

► Share or insure the risk – transfer or share a portion of the risk in an effort to reduce the risk level

► Accept the risk - take no action

11

Higher Education Solutions

Assess Risk

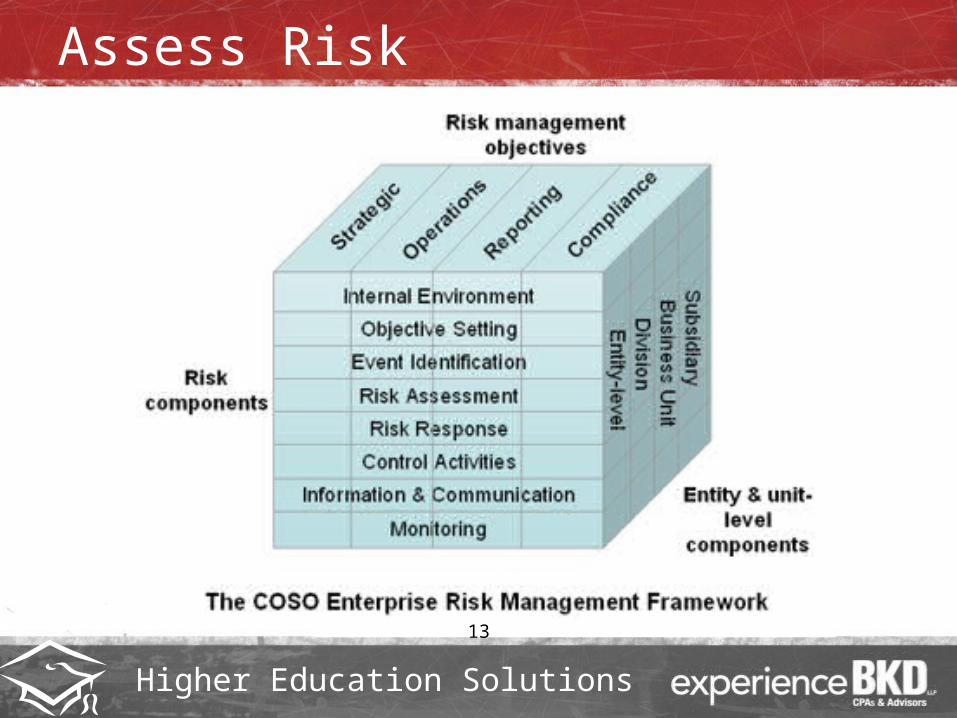

Enterprise Risk Management (continued) ERM may be based on COSO’s ERM Framework

model• As defined:

► A process, effected by an institution’s board of trustees, management and other personnel, applied a strategy setting and across the enterprise, designed to identify potential events that may affect the institution, and manage risks to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objections. (Committee of Sponsoring Organizations of the Treadway Commission _ COSO)

12

Higher Education Solutions

Assess Risk

Enterprise Risk Management (continued) COSO framework

• Framework consists of five interrelated components:► Control environment

► Risk assessment

► Control activities

► Information and communication

► Monitoring

13

Higher Education Solutions

Assess Risk

14

Higher Education Solutions

Assess Risk

Enterprise Risk Management (continued) Four major areas of risk

• Operational (process and procedures)

• Financial

• Regulatory

• Reputational

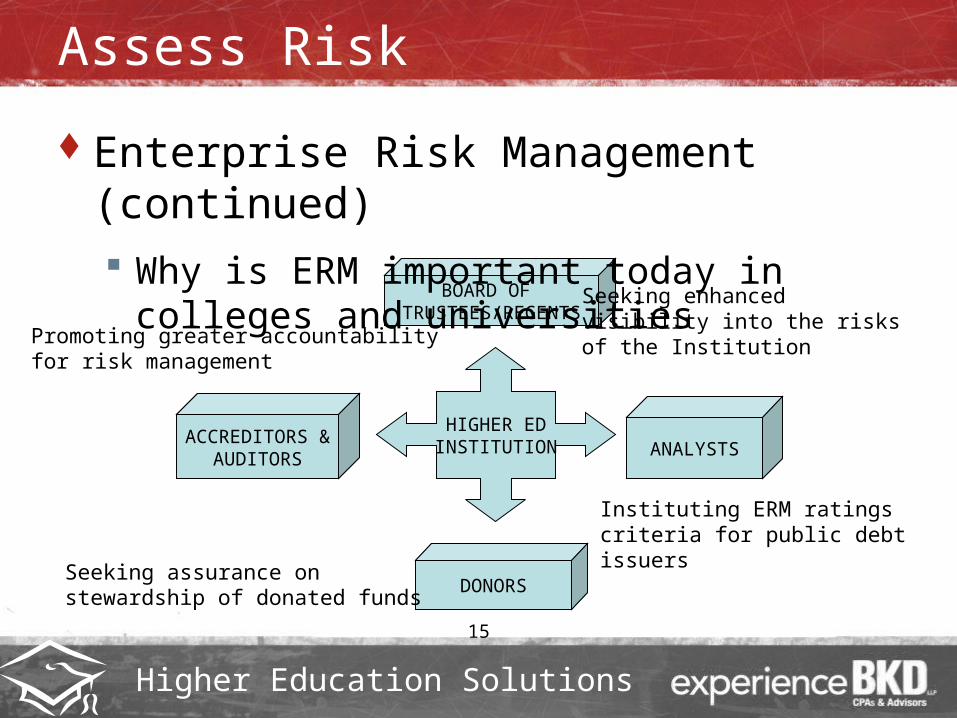

Why is ERM important today in colleges and universities?

15

Higher Education Solutions

Assess Risk

BOARD OF TRUSTEES/REGENTS

ACCREDITORS &AUDITORS ANALYSTS

DONORS

HIGHER EDINSTITUTION

Seeking enhancedvisibility into the risksof the Institution

Instituting ERM ratingscriteria for public debtissuers

Seeking assurance onstewardship of donated funds

Promoting greater accountabilityfor risk management

Enterprise Risk Management (continued) Why is ERM important today in colleges and

universities

16

Higher Education Solutions

Assess Risk

Internal audit risk assessment Process

• Considers results of ERM• Defines the audit universe and auditable areas• Establishes a consistent scoring structure

Examine scores Apply risk rating

• Rank each auditable unit/function• Becomes basis for allocating audit resources

17

Higher Education Solutions

Assess RiskRisk Profile – Heat Map

High

Moderate

Low

HighModerateLow

Off-CampusFacilities

ConstructionManagement (Facilities)

Central BillingOffice

UtilitiesOffice of ResearchAdministrationDeferred

MaintenanceEndowment

UniversityRelations

Gifts &RestrictedFunds

Financial Reporting

Auxiliary Services

PropertyManagement

InformationTechnology

18

Higher Education Solutions

Assess Risk Internal audit risk assessment (continued)

Areas of risk assessment at a college (representative list)• Student billing and collections• Financial aid and grants• Information technology• Business office• Athletics• President’s office• Purchasing and accounts payable• Payroll and benefits• Human resources• Security• Contract management• Facilities/construction management• Student clubs• International programs

19

Higher Education Solutions

Develop Audit Plans

Audit plan Identify the audit schedule for each auditable

unit/function based on risk assessment• High risk areas first

Determine plan rotation• Typically 3 to 5 years

Plan is fluid and can (and probably will) change based on audit work

20

Higher Education Solutions

Develop Audit Plans

Annual audit plan List of areas to cover in the year

Should detail time line and lead individuals

Should have status meetings or communication tool to provide updates and status of plan

Include audit committee reporting time line

21

Higher Education Solutions

Internal Audit Project Process

Meet with area personnel to identify: Processes

Policies and procedures

Laws and regulations

Management concerns

Review information to develop an internal audit program

Request additional information

22

Higher Education Solutions

Internal Audit Project Process

Perform testing Documentation

Inquiry

Observation

Share and obtain input on results with area management

Prepare written observations and recommendations

23

Higher Education Solutions

Internal Audit Project Process

Obtain management’s responsesPrepare audit report Issue report to departmental management,

upper management and the audit committee/ board

Follow up on status of previous findings is important

24

Higher Education Solutions

Examples of Internal Audit Work Process improvement analysis

Eliminate duplication of effort Eliminate unnecessary steps Streamline to promote efficiency

Compliance testing (more specific to regulatory or statutory rules) Financial aid Human resources Payroll and benefits Fund development and administration Grants Contracts

25

Higher Education Solutions

Examples of Internal Audit Work Policy and procedure adherence Internal control advisory services for process or system

changes/enhancements Internal control testing External audit assistance Special projects to address items of immediate concern

Athletics Student groups International programs Travel and expenses Off site programs

26

Higher Education Solutions

Conclusions – Internal Audit

Proactively addresses compliance by being aware of and testing of laws and regulations

Serves as a tool to address public scrutiny Indicates management and the board are interested in

doing things the right way and correcting items that may be off the mark

Provides a resource to the board and management to complete special assignments to address items of concern

Results provided by an independent party carry more weight with the public and stakeholders

27

Higher Education Solutions

Conclusions – Internal Audit

Promotes transparency in campus processes Results are formally reported

Results include statements from management as to how any issues will be addressed

Results provide ownership for corrective plan

Results indicate cases in which everything is being performed as intended when there are no or few written findings

Results available for management and the board

28

Higher Education Solutions

Thank you!

Questions?