high performance investment teams - panthera · high performance investment teams they have to go...

TRANSCRIPT

1PANTHERA SOLUTIONS HIGH PERFORMANCE INVESTMENT TEAMS Page:

HIGH PERFORMANCE INVESTMENT TEAMSWHITE PAPER – FEBRUARY 2016INVESTMENT DECISION ARCHITECTS ™

How to establish High Performance Investment Teams (HPIT©)?Regular readers of Panthera Solutions publications know about our track record as asset allocation intelligence provider with a strong research engine, allowing us to develop proprietary asset allocation tools and solutions. An initial retrospection will support the reader in categorizing the thought process of this article. Exemplarily, we highlight

§ that already back in 2012 – against the mainstream – we uncovered structural weaknesses of risk parity strategies (here),

§ our categorization of the Smart Beta factor zoo in autumn 2014, together with emphasizing the limitations of the Alternative Beta approach (here),

§ our unique effort in defining distinguishing characteristics of ethical and unethical asset allocation methodologies (here)

§ or our ground-breaking research in 2015 on comprehensively measuring the global capital stock (here).

This list is not self-promotion but should point out that it corresponds to our standard to work independent, clear and evidence-based. We perceive this introduction as necessary given the presumably soft theme of this article, in which we intend to categorize our academic and practical insights in establishing High Performance Investment Teams.

As we concluded in our article “Man at the centre of the investment decision” in mid 2015, the underperformance of professional investors versus the market portfolio is dominated by two structural factors. See Illustration A.

This article will highlight areas of improvement for professional investors to make better asset allocation decisions. Readers will learn in which areas investors can expect quick wins and where challenges will most likely occur. Examples will illustrate the insights found.

MARKET RETURN

COST PENALTY

BEHAVIOR GAP PENALTY

INVESTOR RETURN

Illustration A Structural Factors for UnderperformanceSource: Panthera Solutions, Vanguard, Carl Richards

Cost PenaltyDefined as the amount of under-performance caused by transaction costs, management fees, distribution fees, etc.

Behavior Gap PenaltyDefined as the contribution of the human factor to a biased perception of reality caused by cognitive dissonances. Indicators of the penalty along the investment process can be certain market timing techniques, the application of flawed portfolio optimization techniques, minimizing career-risk as primary objective and other expressions of cognitive biases.

ESSENCE

HIGH PERFORMANCE INVESTMENT TEAMSCategorization of academic and practical insights

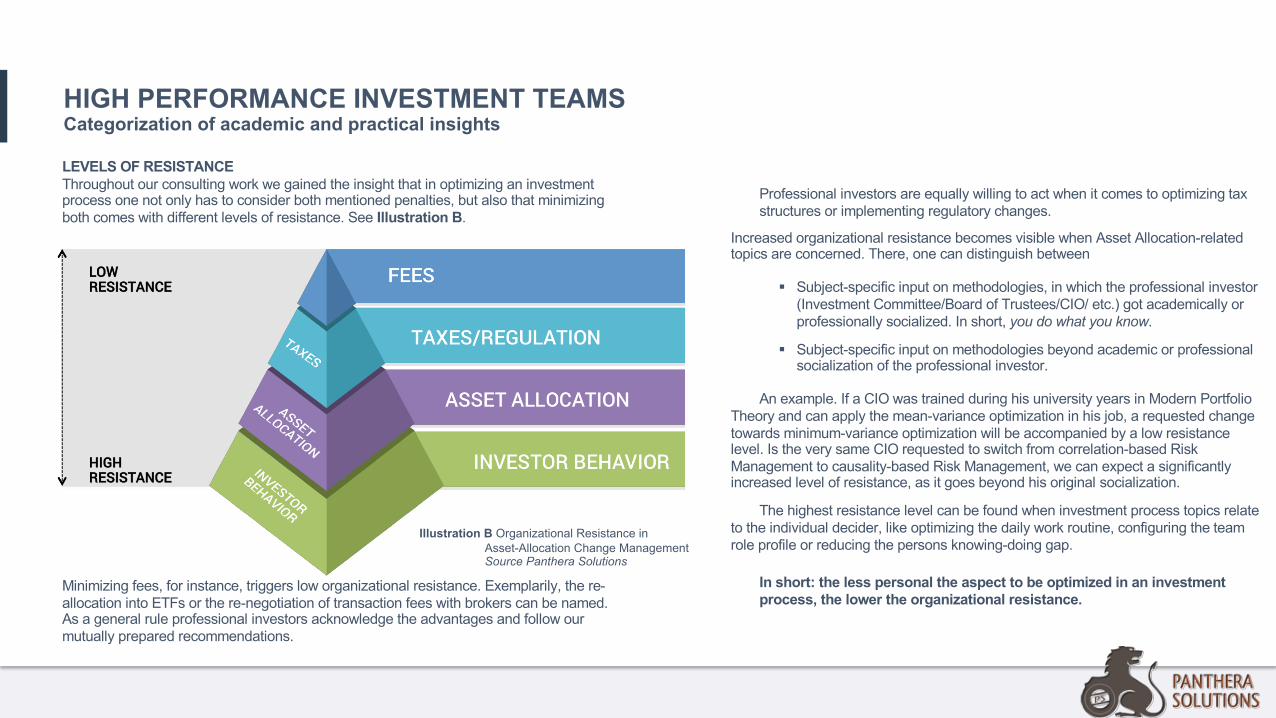

LEVELS OF RESISTANCEThroughout our consulting work we gained the insight that in optimizing an investment process one not only has to consider both mentioned penalties, but also that minimizing both comes with different levels of resistance. See Illustration B.

Minimizing fees, for instance, triggers low organizational resistance. Exemplarily, the re-allocation into ETFs or the re-negotiation of transaction fees with brokers can be named. As a general rule professional investors acknowledge the advantages and follow our mutually prepared recommendations.

Professional investors are equally willing to act when it comes to optimizing taxstructures or implementing regulatory changes.

Increased organizational resistance becomes visible when Asset Allocation-related topics are concerned. There, one can distinguish between

§ Subject-specific input on methodologies, in which the professional investor (Investment Committee/Board of Trustees/CIO/ etc.) got academically or professionally socialized. In short, you do what you know.

§ Subject-specific input on methodologies beyond academic or professional socialization of the professional investor.

An example. If a CIO was trained during his university years in Modern Portfolio Theory and can apply the mean-variance optimization in his job, a requested change towards minimum-variance optimization will be accompanied by a low resistance level. Is the very same CIO requested to switch from correlation-based Risk Management to causality-based Risk Management, we can expect a significantly increased level of resistance, as it goes beyond his original socialization.

The highest resistance level can be found when investment process topics relate to the individual decider, like optimizing the daily work routine, configuring the team role profile or reducing the persons knowing-doing gap.

In short: the less personal the aspect to be optimized in an investment process, the lower the organizational resistance.

Illustration B Organizational Resistance inAsset-Allocation Change ManagementSource Panthera Solutions

HIGH PERFORMANCE INVESTMENT TEAMSCategorization of academic and practical insights

COMPETITIVE ADVANTAGE AS SURVIVAL STRATEGY

As highlighted in this previous article of ours, professional managers of other people´s money like regional banks, private banks, wealth managers, investment companies, (multi-) family offices, etc. are confronted for the first time in decades with a situation that forces them to

either grow aggressively in size to play a shaping role in the industry´s concentration process,

take on the competition with investment management fintechs in offering low-cost, fully automated wealth management solutions,

position themselves as leaders in an investment management niche via innovation-driven competitive edge,

or accept to be squeezed out of the market.

Options 1 and 2 are out of reach for most of the afore listed investment service providers as they are too small, too conservative and/or too loaded with overhead costs. Their will to survive assumed, Option 3 is the only one left.If Option 3 it is, picking up on pseudo-innovations like running after fashion trends a la risk parity will be insufficient. Therefore, a learning organization with a continuous improvement cycle is a prerequisite for establishing and maintaining the innovation-driven competitive edge of the investment process in the chosen niche.

ESTABLISHING HIGH PERFORMANCE INVESTMENT TEAMS

A learning organization with a continuous improvement cycle depends on knowing if and how it learns. For about 20 years, Knowledge Management has been a well understood and established driver of organizational change in other industries. The Asset Management industry widely ignores Knowledge Management in academia and praxis (see a meta-study of Stanford University, 2015). We regularly ask the investment management deciders/investment committees how they learn. Silence is the most frequent response.

To succeed in Option 3, a High Performance Investment Team (HPIT©) is key, being able and willing to oscillate between operational and meta-level in its qualitative and quantitative optimization of the investment process. Only then it can more consciously and therefore more rationally take decisions on whether certain parts of the investment process should be outsourced to quantitative tools (algorithms, big data analysis, neural networks, etc.), which rituals should support them to proactively manage minimizing their cognitive biases or how clients can be embedded in the learning process via expectation management techniques. Evidently, a HPIT© has to work on investment process issues of low and high resistance levels. Only working on low resistance levels will not lead to a sufficiently significant competitive edge to succeed in Option 3. In other words, to transform investment teams into High Performance Investment Teams they have to go where it hurts. It therefore becomes inevitably personal. This is not a walk in the park. Though, if an industry has exceptionally high relevance for society and is rewarded over-proportionally well for it, equally high expectations have to be met. A logic that is considered surprisingly new in our industry.

HIGH PERFORMANCE INVESTMENT TEAMSCategorization of academic and practical insights

OPTION 1

OPTION 2

OPTION 3

OPTION 4

4 LEVELS OF CHANGE MANAGEMENT INTERVENTIONSNow, how to establish High Performance Investment Teams? We classify 4 levels of Change Management interventions in establishing HPITs as part of the investment process optimization – see Illustration C.

The very same is true for the game arrangement in an investment process. If a certain overachieving behavior of the individual decider, say high work ethics, is expected, while the same standard is not set as part of the team or organizational culture, it only is a matter of time until the individual aligns his behavior to the established organizational culture or leaves the organization. Example IIf an employee is expected to openly experiment with new asset allocation methodologies, following an evidence-driven trial and error process, but the organization remains driven by a culture based on fear and therefore responds

destructively to errors, it only is a matter of time, until the employee either returns to the rituals that come with a fear-based culture or leaves the organization.

Example IIIf an investment management employee is expected to act as intra-preneur, but the organizational decision-making process and compensation schemes are rather aligned to public authorities for civil servants, it only is a matter of time, until the employee either returns to the rituals that come with a bureaucratic culture or leaves the organization.

All 4 levels consists of quantitative and qualitative optimization methods. For instance, working on the Individual level of investment process deciders, work has to be done in establishing/facilitating certain skills, rituals and traits. The same has to take place on the Team-level by establishing/facilitating certain rituals and calibrating certain team characteristics.Culture and Process define the game arrangement of an investment process. The meaning of it can be described as follows: we all know that the more often one plays at a Casino, the more likely it is that the house wins, even if a player can temporarily enjoy a lucky streak. A certain asymmetry in favour of the house is structurally embedded in the game.

Illustration C 4 Levels of Change Management InterventionsSource Panthera Solutions

HIGH PERFORMANCE INVESTMENT TEAMSCategorization of academic and practical insights

HIGH PERFORMANCE INVESTMENT TEAMSCategorization of academic and practical insights

Taken all together, investment process optimization can be started at the Individual or Team level to initially harvest low-hanging fruits, but if the Change Management process should leave a lasting impact on the organization, it also requires to be worked on the Process and Culture that is embedded in the investment decision making.

Establishing HPIT© goes beyond individual back-patting, some placebo-feel-good changes that work only on sunny days, some esoteric interventions waited-out by employees, knowing that the moment rough sea appears at the horizon old conflicts or rituals will emerge. The opposite is the case. HPIT© tend to continue their learning also during tough times. HPIT© are about lasting behavior modification of the individual, embedded in an eco-system of Team-, Process- and Cultural setting, facilitating a learning organization with a continuous improvement cycle.

EXTERNAL EMPOWERMENTCan the 4 introduced levels of change management interventions be effective only through intra-organizational impulses or do they require external guidance? When issues of low resistance are affected, it can work without external guidance (Illustration B). Issues of medium and high resistance levels should seek external empowerment as internal impulses cause intra-organizational conflicts of roles and interests to appear and lead to a reduced intervention effect, if not causing counterproductive effects.

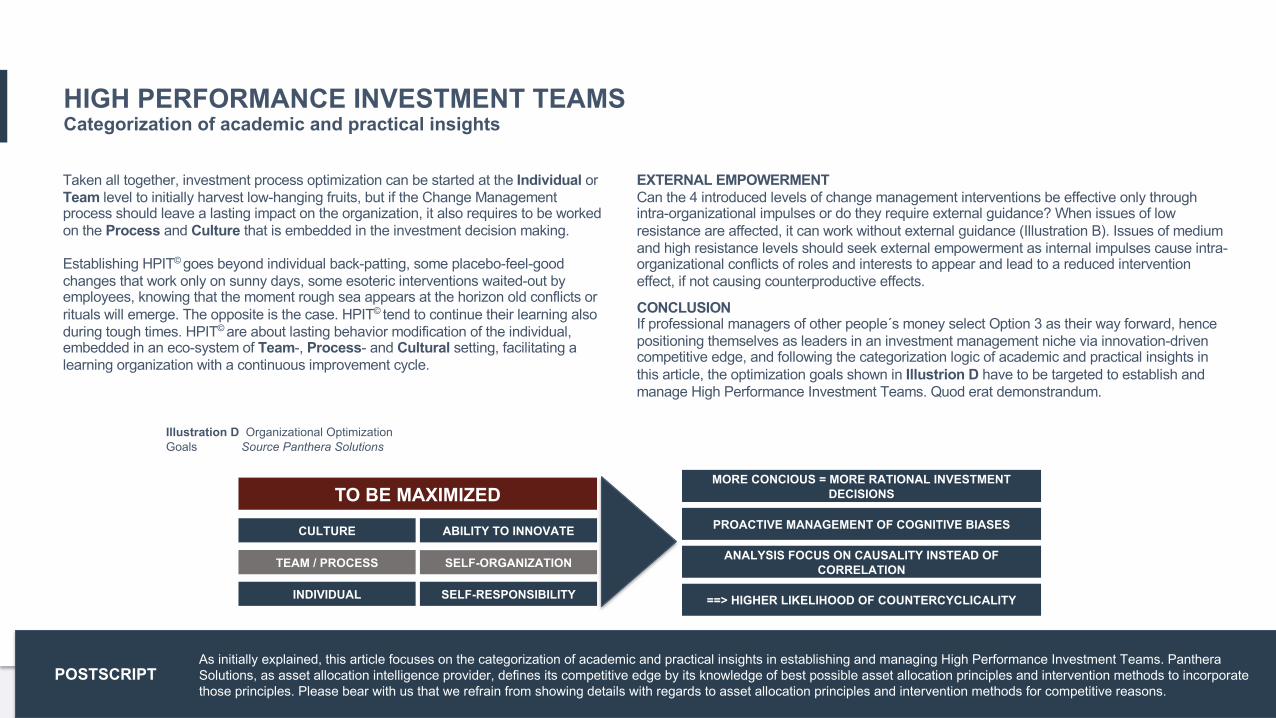

CONCLUSIONIf professional managers of other people´s money select Option 3 as their way forward, hence positioning themselves as leaders in an investment management niche via innovation-driven competitive edge, and following the categorization logic of academic and practical insights in this article, the optimization goals shown in Illustrion D have to be targeted to establish and manage High Performance Investment Teams. Quod erat demonstrandum.

Illustration D Organizational Optimization Goals Source Panthera Solutions

As initially explained, this article focuses on the categorization of academic and practical insights in establishing and managing High Performance Investment Teams. Panthera Solutions, as asset allocation intelligence provider, defines its competitive edge by its knowledge of best possible asset allocation principles and intervention methods to incorporate those principles. Please bear with us that we refrain from showing details with regards to asset allocation principles and intervention methods for competitive reasons.

POSTSCRIPT

CULTURE ABILITY TO INNOVATE

TEAM / PROCESS SELF-ORGANIZATION

INDIVIDUAL SELF-RESPONSIBILITY

TO BE MAXIMIZEDMORE CONCIOUS = MORE RATIONAL INVESTMENT

DECISIONS

PROACTIVE MANAGEMENT OF COGNITIVE BIASES

ANALYSIS FOCUS ON CAUSALITY INSTEAD OF CORRELATION

==> HIGHER LIKELIHOOD OF COUNTERCYCLICALITY

7PANTHERA SOLUTIONS HIGH PERFORMANCE INVESTMENT TEAMS Page:

CONTACT US

DISCLAIMERThis material is for your information only and is not intended to be used by anyone other than you. It is directed at professional clients and eligible counterparties only and is not intended for retail clients. The information contained herein should not be regarded as an offer to sell or as a solicitationof an offer to buy any financial products, including an interest in a fund, or an official confirmation of any transaction. Any such offer or solicitation will be made to qualified investors only by means of an offering memorandum. The material is intended only to facilitate your discussions with Panthera Solutions as to the opportunities available to our clients. The given material is subject to change and, although based upon information which we consider reliable, it is not guaranteed as to accuracy or completeness and it should not be relied upon as such. The material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations. Past performance is not a guide to future performance. Future returns are not guaranteed and a loss of principal money may occur.

© 2019 Panthera Solutions Sarl. All rights reserved.

Panthera Solutions SarlPark Palace 3ACS25, Av de la CostaMC 98000 Monaco

+33 674 274 986

www.panthera.mc

@panthera_s

[email protected] VATFR 77 00008502 6Company ID18S07917