henley outlook march

TRANSCRIPT

Henley Market OutlookMARCH 2013

Alice would be proud!

Hong Kong | Singapore | Shanghai THE WEALTH MANAGEMENT PROFESSIONALS

The Henley Outlook March 2013Hong Kong, Singapore & Shanghai

EquiTiES

Global Overview ............................................................................................................................................. 3

Cash & Currencies ............................................................................................................................................. 5

Fixed Income .............................................................................................................................................. 6

Property ............................................................................................................................................. 7

Equities US .............................................................................................................................. 8

Japan ................................................................................................................................ 8

UK ....................................................................................................................................... 9

Europe Ex UK ................................................................................................................. 9

Australia ....................................................................................................................... 10

ASEAN .......................................................................................................................... 10

Greater China ............................................................................................................... 11

India ............................................................................................................................. 11

Other Emerging Markets ........................................................................................ 12

Commodities Energy ..............................................................................................................................13

Precious Metals ............................................................................................................13

Industrial Metals ......................................................................................................... 13

Agriculture ............................................................................................................. 14

Alternative Investments ............................................................................................................................................15

2

CONtENt

tHE INvEStMENt COMMIttEE

Peter Wynn WilliamsInvestment Director

& Partner

Andrew KellyPartner

David ReynoldsPartner

George RipponPartner

Simon LiuHead of Investment

Research

Paul BradyPartner

Chris SkinnerPartner

the Henley Investment Committee combines more than 110 years’ experience and is unique in being backed by a full-time team of five investment professionals to optimise asset allocation and manager selection.

EquitiEs

3

GLOBAL OvERvIEW

“Why, sometimes I’ve believed as many as six impossible things before breakfast.” The White Queen, through the Looking-Glass (Lewis Carroll, England, 1832-1898)

After a rollicking, if Alice-in-Wonderland start to the Gregorian year, the dawning of the Year of the Snake ushered in an end to the markets’ scramble up the ladder, borne aloft by a rising confetti soufflé of freshly-printed dollars and yen. Whether this slither down the snake will prove terminal for the markets’ revived animal spirits remains to be seen, but it seems to me that for as long as they keep printing, asset prices will keep inflating. Until they do not.

the supposed cause of the correction initially was the release of the minutes of the February meeting of the US Federal Reserve’s Federal Open Markets’ Committee (FOMC). the committee reportedly discussed stopping or slowing the programme of quantitative easing (QE), currently running at USD85bn per month.

There is clearly a significant degree of disagreement and confusion at the Federal Reserve. Some committee members clearly believe that open-ended and unlimited QE is a mistake and should be rectified as soon as possible. Others believe that aggressive QE could be continued indefinitely, until the economy can prosper under its own steam.

This reflects the fact that the world is now monetarily in uncharted waters. Zero interest rates and QE have never been tried like this before. Ever.

What last month’s correction should have made clear to everyone was that the Federal Reserve is trapped. there is no way that they can dispose of their treasury bond holdings in an orderly manner. Any hint of them doing so in FOMC minutes or anywhere else will result in a stampede of investors trying to front run the Federal Reserve and sell first.

there is also no way that central banks can break records for the amount of money being printed without it leading to rising consumer prices. Self evidently, we already have rising asset prices. It ought to be equally obvious that central banks cannot exit QE because to do so would lead to rapidly-rising interest rates, which would strangle whatever economic growth survived at that point.

In this context, it is also important to realise that, when it comes to interest rates, it is not the central banks who are in charge, it is the bond market. When the bond markets raise interest rates, the printing presses will have to go into overdrive to cover governments’ rising interest costs. Ask the PIIGS!

that means it is the paper currencies which will be left to take the strain through debasement/inflation. ‘Twas ever thus, in fact, and recently we have seen sterling and the yen take their turns to be on the receiving end. Every cloud has a silver lining, however, and for clients intending to relocate to the UK sooner or later, who own gold (or silver!), or who are planning to use foreign currency to buy UK property, their situation is improving. there is no need to rush, however. the debasement of sterling (and the yen) will be an enduring phenomenon.

Which takes us neatly on to the monetary metals, gold and silver. After five years of money printing, it ought to be obvious to everyone, except perhaps the most ardent Keynesians, that it is not working.

that really leaves gold and silver as the only way out of re-balancing the books. One Sunday evening in Basel, Switzerland, before the markets open in Japan on their Monday morning, the Bank of International Settlements will announce that, henceforth, it will agree to buy unlimited quantities of gold at, say, USD10,000 per ounce. Hey presto, balance sheets re-balanced. Banks and sovereigns re-liquefied.

Peter Wynn WilliamsInvestment [email protected]

The Henley Outlook March 2013Hong Kong, Singapore & Shanghai

EquiTiES

4

GLOBAL OvERvIEW

Far fetched? Well, not really. It’s been done before. In April 1933, during the Great Depression, US presidential Executive Order 6102 criminalised the possession of more than five ounces of gold by any US person or entity. Within a three-week period, gold had to be surrendered to the Federal Reserve in exchange for then market price of USD20.67 per ounce. In January 1934, the US Gold Reserve Act re-valued gold by 70% to USD35 per ounce, where it stayed until 1971. Incidentally, it was not legal for Americans to own gold again until 1975!

the idea of using gold to re-liquefy balance sheets is at last gaining traction in the mainstream (the idea of confiscating gold is not – gold is owned globally these days, but it was not in 1933). Indeed, the World Bank suggested it two years ago.

Before this can happen, however, the Chinese must be allowed to hedge their huge dollar position, and back the yuan in preparation for its full convertibility by accumulating a respectable reserve of monetary gold. to re-value gold before this had happened might be thought, in Beijing, to be inconsiderate.

When push comes to shove (as it is doing, slowly) and growing deficits need to be financed, governments always trump central banks. Witness what is happening now in Japan, with the government ordering massive monetisation and inflation targeting, while dispensing with the services of its uncooperative central banker, Masaaki Shirakawa, and replacing him with the more congenial Haruhiko Kuroda. Other central banks are likely to see their hard-won independence eroded, too.

In a nutshell, politicians are unwilling to raise taxes or cut spending. they will wave their magic golden wand instead.

the Italians, too, must be tempted to wave the golden wand following the result of their General Election, which was effectively a referendum on austerity. Fifty-seven percent of the votes went to parties who want to turn their backs on austerity. the largest single party (25%) wants to leave the euro.

Of all the nations in the euro, Italy is perhaps in the best position to leave. It has low private debt and about EUR9tn in private wealth. Its total debt level is 265% of GDP, lower than in France, Holland, the UK, the US or Japan. Its budget is near primary balance, and so is its international investment position (in contrast to Spain and Portugal). It could in theory return to the lira without facing a funding crisis, and this may be the only way to avoid a crisis if the European Central Bank (ECB) withdraws support.

The great fear is that the ECB will find it impossible to prop up the Italian bond market under its Outright Monetary transactions (OMt) scheme if there is no coalition in Rome willing or able to comply with the tough conditions imposed by the EU at Berlin’s behest. Europe’s rescue strategy could start to unravel. Will Berlin now have to re-think its strategy? German leaders need to keep up the appearance that the euro-zone crisis has been solved, at least until their elections in September.

With the fourth largest gold reserves in the world (2452 tonnes) after the US, Germany and the IMF (oh – and probably China by now, but they prefer to keep everybody in the dark), the magic wand of gold re-valuation must be appealing to Italy, too (assuming, of course, that their gold is not held at the Federal Reserve and has not already been secretly sold to China!).

Alice would be proud!

Peter Wynn Williams Investment Director

EquitiEs

5

CASH & CURRENCIES

Summary ■ Of all currencies, the GBP has had the worst start to the year, trading at its lowest level to

USD since June 2010. Confidence in the GBP has fallen sharply since Christmas and this was compounded by February’s inflation report from the BoE. Negative real interest rates and huge additional supply through QE has left the GBP undesirable. this is however exactly what the BoE needs in order to devalue for growth and inflate away the debt. This new trend is set to continue, but expect short-term corrections along the way. the GBP has much further to fall.

■ Although aiming for similar results as the GBP, the USD has the benefit of being the world’s reserve currency and indeed the currency for the trade of commodities globally. It will take a much greater crisis of confidence to impact its value in the same way as we have seen with the GBP.

■ the JPY is losing value steadily against the USD as expected, totally in line with the increase of the Nikkei. This is Abe’s fundamental strategy, pushing for inflation rather than deflation, as well as export growth through a cheaper JPY.

■ the SGD remains the new safe haven currency as a result of the strength of the city state’s economy, and also the way the currency is managed. We expect this trend to continue, and do not expect policy change from the Monetary Authority of Singapore (MAS) meeting in April.

HENLEY ASSESSMENTStrongly negative

Mostly negative GBP, followed by JPY. USD and EUR to still fare poorly over medium-to-long term against a trade-weighted basket of currencies given that all of these currencies are debasing and devaluing through significant quantitative easing (QE). We still favour SGD as a safe haven, and commodity currencies for yield.

GBP

/USD

(Sou

rce:

Dai

lyfx

.com

)

The Henley Outlook March 2013Hong Kong, Singapore & Shanghai

EquiTiES

6

FIxED INCOME

Points of General Interest ■ It was undoubtedly a significant moment in Feb13 when the outgoing Governor of the BoE,

Mervyn King, was outvoted in his desire to add more QE to the UK Economy. this has set the scene for an interesting battle when the incoming chairman, Mark Carney, arrives as he has publically stated his willingness to do what it takes to stimulate the economy. this new rhetoric and presence at the head of the bank along with the recent topics discussed in the UK Monetary Policy Committee minutes suggests that the BoE is going to allow inflation to rise above the targeted 2% in order to give the economy the best possible chance to grow.

Government Bonds ■ After the previous rush away from the perceived safe haven of US treasury bonds at the start

of the year, the concerns over the outcome of the Italian election at the end of February saw these outlays return to being inflows; a stark reminder of how the political outcomes of Europe still have the ability to derail the positive momentum enjoyed at the start of this year. this serves to remind us that however counterintuitive it may seem given time of panic, investors still see US debt as a safe haven.

■ February also saw the UK finally join the long list of previous sovereign heavyweights who have had their AAA rating downgraded by one of the ratings agencies; an act that will not endear Moody’s to the current coalition government. However, if previous recent downgrades are anything to go by, it is a move that will not create too many issues with regards to increasing the rate at which the UK borrows money from international markets.

Corporate Bonds ■ With the concern surrounding the Italian election it was not only US treasury bonds that

benefited from a temporary move away from equities, but also corporate bonds, with the final Monday of February seeing the corporate bond markets having to digest nearly USD10b of new corporate bonds being purchased.

Offshore Bank Accounts- Best Buys GBP ■ No Notice Account- Nationwide International 1.60%pa. ■ 95-day Notice- Nationwide International- 1.80%%pa.

Offshore Bank Accounts- Best Buys USD ■ No Notice Account- Lloyds tSB International 1.51% (inclusive of a 1% bonus paid at month 12).

HENLEY ASSESSMENtBroadly negative, however we see opportunity in some emerging market and corporate debt.

While there may be some short-term relief in fixed income from the volatility seen in equity markets and also a comparative positive return when compared to holding straight cash, we are of the opinion that such short-term relief has the potential to come at a costly price in the medium to long term.

With the developed economies committed to the path of continued monetary easing, we believe that inflation will become a serious concern in the future. this fear appears to have been proven right by the rhetoric from the most recent G20 meeting in which world leaders appeared to vindicate further monetary easing without too much regard to the potential inflationary pressures that such a policy will likely create. Such an environment would see the relatively low yields enjoyed by fixed interest overrun by severe inflationary pressures. Following this argument a stage further we feel that traditional fixed interest has transferred from being a safe haven asset class to one that in the post-GFC world holds significant risk for the medium to long term.

EQUItIES

Source: ONS

EquitiEs

7

PROPERtY

Positives ■ US residential property is rebounding as traditional homebuyers compete with investors for

a shrinking inventory of homes. the S&P/Case-Shiller index of property values in 20 US cities increased 5.5% in November YOY, the biggest gain since August 2006 (19 of the 20 cities in the index posted gains). Prices were up 0.6% MOM. A plunge in US house listings to a 12-year low is helping to drive prices up, as sellers are delaying until property values rise further.

■ Prime central London property prices are up 53% since the market trough in 2009. It is estimated that overseas buyers purchased GBP2.2bn of central London property in 2012, up 22% from GBP1.8bn in 2011. Knight Frank has identified three major factors underpinning demand for London property: first capital growth potential; secondly, a weak currency for foreign investors; and thirdly London’s continued leadership in top-flight education.

■ Singapore home sales rose 43% MOM in January as buyers rushed in after the government announced its seventh round of cooling measures since 2009 to control the rise of residential property prices. the latest cooling measures include increased stamp duty on purchases and higher deposits. Singapore home prices reached a record level in Q412.

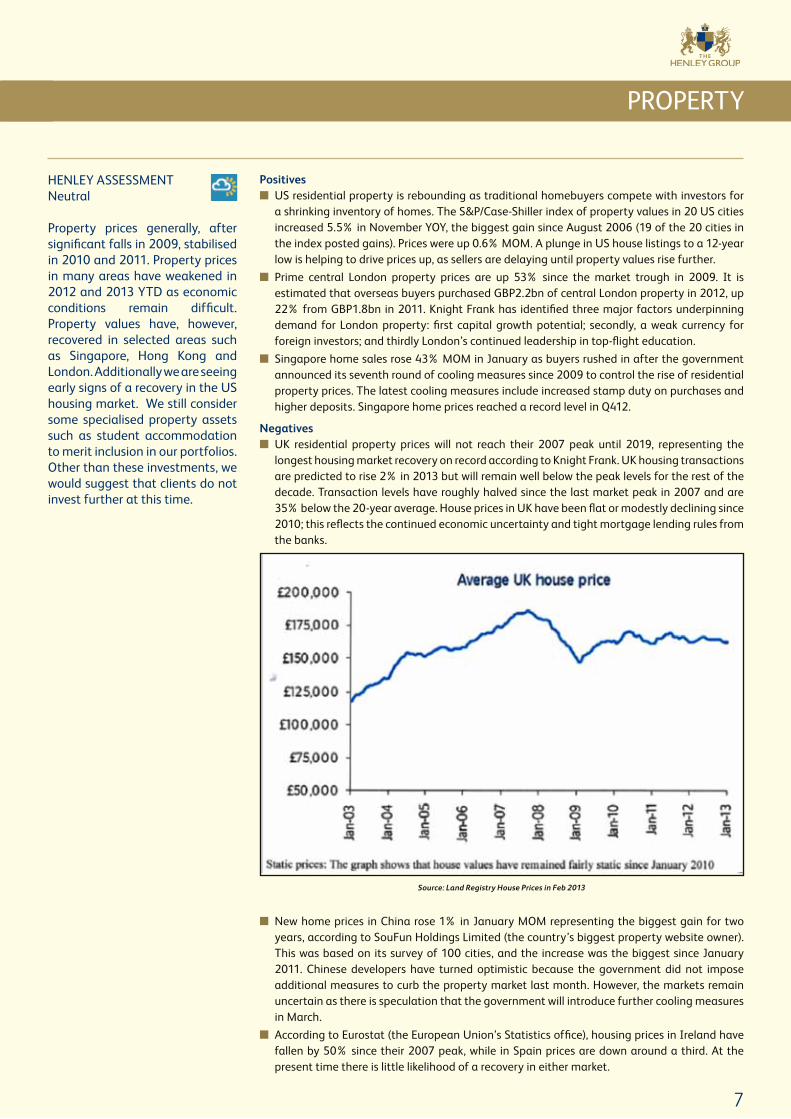

Negatives ■ UK residential property prices will not reach their 2007 peak until 2019, representing the

longest housing market recovery on record according to Knight Frank. UK housing transactions are predicted to rise 2% in 2013 but will remain well below the peak levels for the rest of the decade. transaction levels have roughly halved since the last market peak in 2007 and are 35% below the 20-year average. House prices in UK have been flat or modestly declining since 2010; this reflects the continued economic uncertainty and tight mortgage lending rules from the banks.

Source: Land Registry House Prices in Feb 2013

■ New home prices in China rose 1% in January MOM representing the biggest gain for two years, according to SouFun Holdings Limited (the country’s biggest property website owner). this was based on its survey of 100 cities, and the increase was the biggest since January 2011. Chinese developers have turned optimistic because the government did not impose additional measures to curb the property market last month. However, the markets remain uncertain as there is speculation that the government will introduce further cooling measures in March.

■ According to Eurostat (the European Union’s Statistics office), housing prices in Ireland have fallen by 50% since their 2007 peak, while in Spain prices are down around a third. At the present time there is little likelihood of a recovery in either market.

HENLEY ASSESSMENt Neutral

Property prices generally, after significant falls in 2009, stabilised in 2010 and 2011. Property prices in many areas have weakened in 2012 and 2013 YtD as economic conditions remain difficult. Property values have, however, recovered in selected areas such as Singapore, Hong Kong and London. Additionally we are seeing early signs of a recovery in the US housing market. We still consider some specialised property assets such as student accommodation to merit inclusion in our portfolios. Other than these investments, we would suggest that clients do not invest further at this time.

The Henley Outlook March 2013Hong Kong, Singapore & Shanghai

EquiTiES

8

HENLEY ASSESSMENtNeutral

We doubt if “Abenomics” are sustainable and sound economic policies in the medium term; that is Japan waiving the debt limit of JPY44tn (USD514bn) for the fiscal year and targeting higher (2%) inflation. Japan has accumulated debts worth some USD14.6tn, or 230% of GDP. A quarter of Japan’s budget now goes to servicing debt. So far tokyo has done little to change its course.

Positives ■ the Secretary General of OECD defended Japan’s monetary easing. He argued Japan is

aiming to beat deflation rather than simply weakening JPY against currencies of other competitor economies. the incident was seen as an endorsement of a weaker JPY by the developed countries led by the US.

■ JPY further weakened to Y93 after the Governor of Bank of Japan (BoJ) announced that he will step down on 19 March, three weeks prior to his official term ends. The market is expecting a fundamental shift in Japan’s monetary policy as Prime Minister Abe stepped up his pressure on BoJ.

Negatives ■ Japan remained in technical

recession through Q4, with GDP falling 0.1% QOQ and 0.4% annualised. Private investment fell sharply over the last quarter. Both exports and imports fell sharply highlighting a case for aggressive monetary easing.

■ Japan’s trade deficit nearly tripled in 2012 to JPY6.93tn (USD77bn). A sharp expansion of deficit from JPY2.56tn (2011) highlights the increasingly complex challenges faced by Japan which has promised aggressive measures to end two decades of disappointing growth.

HENLEY ASSESSMENtNegative on fundamentals, positive on markets short term.

Chances of Congress and the White House addressing the long-term solvency issues of the US government in a meaningful manner remain nil. the changes required to balance the system are too politically painful, so a currency crisis within the next couple of years seems the most likely outcome – especially if there is a black-swan event, such as an assassination, a COMEx default or a bomb on Iran, for example. Meanwhile the economy continues to bottom bounce, fundamentals continue to deteriorate, and markets continue not to care, buoyed by a rising tide of confetti (and nothing else).

Positives ■ QE to infinity will inflate asset prices. ■ the US Federal Reserve has forecast rates will remain unchanged until at least 2015. ■ In the long term, demographics and returned energy self-sufficiency bode well.

Negatives ■ National debt: USD16.5tn and rising; debt to GDP: 106% and rising. This is absurdly

unsustainable. ■ QE to infinity promises currency debasement, rising prices and lower discretionary spending. ■ Foreigners are buying fewer, and selling more US treasury bonds. ■ The debt ceiling “temporarily suspended” plus QE to infinity may result in a currency crisis in

a couple of years.

EQUItIES

UNITED STATES

JAPAN

Source: Der Spiegel

EquitiEs

9

Positives ■ The euro zone December unemployment rate was unchanged at 11.7%; better than expected.

The report from the EU’s statistics office provided some much needed positive news that the euro zone labour market at least did not get any worse in Dec12.

Negatives ■ the economy across the 17-nation shared-currency bloc shrank 0.6% in 4Q12, compared to

analysts’ expectations of a 0.4. the German economy, Europe’s largest, shrank 0.6% over the same period while economic activity shrank 0.3% in the quarter.

■ Barclays’ analysis of ECB data suggests that companies based in the “core” of the bloc have been the main beneficiaries of the central bank’s promise last June to do “whatever it takes” to save the euro zone. Companies based in France, Germany, Belgium and Holland were able to borrow a net EUR37bn of ultra-cheap debt from the markets in the second half of last year following the announcement. Companies based in Italy, Spain, Portugal and Greece added only about EUR12bn of market borrowing, with only the biggest companies such as telecom Italia and telefonica able to access the capital markets.

■ A strong appreciation of the single currency has fuelled fears that a nascent recovery for the bloc may be in jeopardy. the EUR’s relative strength comes amid heightened tensions that loose monetary policy adopted by major central banks around the world could spill over into a series of competitive devaluations.

HENLEY ASSESSMENtStrongly Negative

the GDP data from the euro zone show that the 17 countries have not expanded as a group since the autumn of 2011; a vivid reminder that the more optimistic mood in European financial markets – and recent meetings of European governments – has yet to leave much of a mark on the real economy. For the likes of Italy and Spain, the 4Q figures are the culmination of a dismal year, which has seen their economies shrink by upwards of 2%. Portuguese national output shrank by nearly that much in 4Q12 alone, ending 2012 nearly 4% smaller than at the end of 2011. Even the optimists are not expecting the crisis economies to actually grow for many months yet. the worry for European policymakers right now ought to be how that continued gloom is going to play out politically.

HENLEY ASSESSMENtNegative the pressure continues to intensify on the Chancellor George Osborne. As predicted in our Outlook last month, Moody’s became the first of the major agencies to remove the UK from the elite club of AAA countries, blaming “subdued growth” and a “high and rising debt burden” for the decision to cut the rating by one notch to AA1. the rating is significant because it can affect a country’s cost of borrowing and is also symbolic to governments determined to prove their economic credentials. Within the G7 economies, only Germany and Canada currently still hold the coveted AAA rating. In the short term sterling will continue to come under pressure on foreign exchange markets.

Positives ■ The Chancellor George Osborne has ordered Treasury officials to draw up plans for a

government “give-away” of Royal Bank of Scotland shares to boost the economy – and the coalition’s electoral prospects – by 2015. Mr Osborne has concluded that continued taxpayer ownership of the bank is politically “untenable” amid rows over bankers’ bonuses, interest-rate manipulation and the mis-selling of financial products. Advisers also believe that there is no realistic prospect of the government recouping its full GBP45bn investment in the bank and are proposing a scheme to “hand it back to taxpayers” as early as 2015. Under one plan being developed, every taxpayer or voter in Britain would be given shares in RBS that would be worth, according to one treasury insider, between GBP300 and GBP400 at current prices. If this was to proceed, it would certainly help to stimulate the economy in the short term.

Negatives ■ Britain has been through the “Winter of Discontent”, the miners’ strikes, the recessions of the

1980s and 1990s, the implosion of the banks and five years of the euro zone debt crisis to boot – yet has never lost its AAA credit rating, until now. Entering into these uncharted waters, Britain’s economic skipper George Osborne has insisted he will not change course. However the chancellor will now come under intense pressure to re-think his austerity plans ahead of next month’s Budget. One things markets hate is uncertainty.

UNITED KINGDOM

EUROPE EX UNITED KINGDOM

EQUItIES

The Henley Outlook March 2013Hong Kong, Singapore & Shanghai

EquiTiES

10

HENLEY ASSESSMENtPositive

Consumer goods companies, retailers, education and health-care industries are attractive as urbanisation spurs more people to move into cities, forming a large pool of middle class, especially in the bigger economies of Singapore, Malaysia, Indonesia, thailand, the Philippines and vietnam. the relative stability and continuous growth in the region is an attractive proposition; ASEAN look attractive amid global challenges including low growth in the US, Europe’s sovereign debt crisis and limited growth prospects in China and India.

HENLEY ASSESSMENtNeutral

the RBA’s assessment of the need for additional rate cuts will be shaped by the housing sector’s response to lower interest rates, developments in the labour market and prospects for non-mining business investment. the CAPEx survey, published 28Feb13, provides a critical input into this assessment. We see the risk that the pending downturn in mining investment will not be offset sufficiently by an upturn in non-mining business investment (and housing activity). Current domestic economic conditions are patchy and the risks to the RBA’s central case forecast are to the downside – hence the need for additional stimulus.

Positives ■ Indonesia, thailand and Singapore have announced airport expansion plans in response to

surging travel demand. Asia Pacific overtook North America as the world’s biggest aviation market in 2009. the region’s passenger growth, both domestic and international, is expected to add about 380m travelers between 2012 and 2016 to 1.2bn.

■ thailand’s fourth-quarter growth accelerated more than economists estimated, joining ASEAN nations from Indonesia to Philippines in showing resilience to the faltering global economy as local demand rises.

Negatives ■ the Indonesian president is under growing pressure to raise the price of subsidised fuel to

curb the current-account deficit as his window to act narrows ahead of elections in 2014. A 44% increase in the minimum wage in Jakarta and a 15% rise in electricity prices this year are adding to the inflationary pressure.

■ The Philippine central bank is considering measures to counter excessive capital inflows lured by growth, joining Singapore in warning that policy makers need to consider more steps to reduce the impact of such funds.

ASEAN

AUSTRALIA

Positives ■ the RBA decided to leave interest rates unchanged, following rate cuts in May, June, October

and December 2012. ■ the bank also announced that it is encouraged that interest-rate sensitive parts of the

economy had shown some signs of responding to these lower rates, which were well below their longer-run averages, and further effects could be expected over time.

■ The Westpac–Melbourne Institute Index of Consumer Sentiment posted a strong 7.7% rise in February, moving from “neutral” to “optimistic” territory.

■ Australian house prices rose last quarter by the most since Jun10 as lower rates lured buyers back into the market. the nation’s benchmark stock index climbed 4.9% last month.

Negatives ■ In the Australian government monthly financial statements for Dec12 released 15Feb13, the

government revealed a material slippage in its 2012/13 budget position over the initial six months of the financial year, centred on lower-than-expected company tax revenues, and a shortfall in resource rent taxes.

■ In its quarterly statement released 8Feb13, the RBA predicted “below trend” 2013 growth of about 2.5%, compared with the around 2.75% forecast in November.

■ A government report showed retail sales unexpectedly fell for a third month in Dec12, the longest stretch of declines in 13 years.

EQUItIES

EquitiEs

11

Positives ■ India’s headline inflation Wholesale Price Index (WPI) decelerated to 6.62% in Jan13 from

7.18% in Dec12, leaving enough room for the central bank, the Reserve Bank of India (RBI), to cut rates and spur growth.

■ total new business in the private sector increased to a 11-month high with the PMI expanding sharply from 55.6 in Dec12 to 57.5 in Jan13.

■ In a bid to spread financial services into the rural market – comprising 600,000 villages, 90% of which do not have a single bank – the RBI has now offered new banking licences.

Negatives ■ Corporate investment sector declined by 2.8% of the GDP in 2011-12 compared to the earlier

year thanks to the policy bottle necks and tight monetary policy. ■ Annual growth of private consumption expenditure declined to 4% in 2012-13 compared to

8% in the previous year while household financial savings too were reduced from 10.4% of GDP in 2010-11 to 8% in 2011-12.

■ Current account deficit continues to balloon from 2.6% (of the GDP) in 2010-11 to 4.2% in 2011-12 and 4.6% in H1 of this financial year to 5% in Q3.

HENLEY ASSESSMENtPositive

the bullish sentiment continues. Progress towards a domestic, consumption-led economy is definitely taking place, and seems likely to continue at a rapid pace, a necessary part of the longer-term structural changes in the economy, as well as a necessary step towards correcting global current account imbalances. the middle class doubled in the last five years and will probably double again in the next ten. On the other hand, the Chinese government appears to be embracing lower but more sustainable levels of economic growth. this provides the opportunity for the continuation of measures to ease credit conditions and support expenditure on social housing projects, the development of infrastructure and the promotion of domestic consumption.

HENLEY ASSESSMENtNeutral

the powerful monetary response to tame inflation has significantly impacted consumption; as such the projected growth rate of 6.1-6.7% in 2013-14 is much lower than expected for a country the size of India. With the threat of a possible downgrade looming large, all eyes are now set on 28 February when the finance minister is expected to address the fiscal deficit and current account deficit through a prudent rather than populist budget.

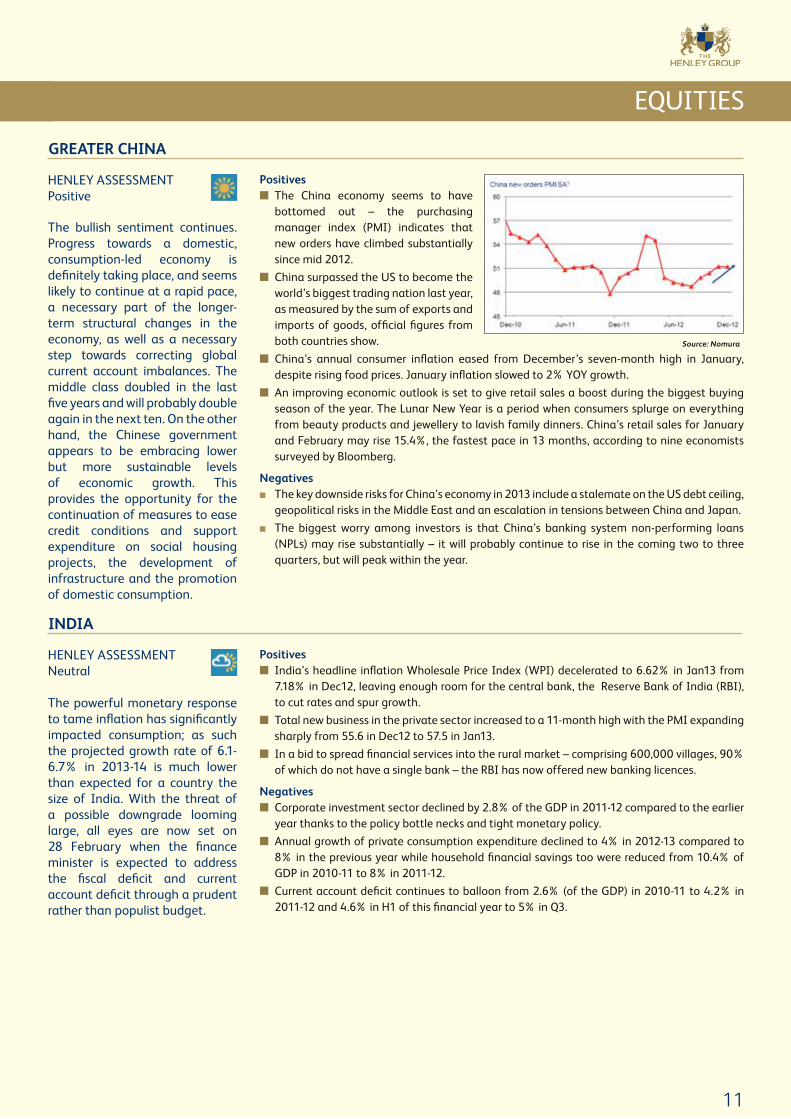

Positives ■ the China economy seems to have

bottomed out – the purchasing manager index (PMI) indicates that new orders have climbed substantially since mid 2012.

■ China surpassed the US to become the world’s biggest trading nation last year, as measured by the sum of exports and imports of goods, official figures from both countries show.

■ China’s annual consumer inflation eased from December’s seven-month high in January, despite rising food prices. January inflation slowed to 2% YOY growth.

■ An improving economic outlook is set to give retail sales a boost during the biggest buying season of the year. the Lunar New Year is a period when consumers splurge on everything from beauty products and jewellery to lavish family dinners. China’s retail sales for January and February may rise 15.4%, the fastest pace in 13 months, according to nine economists surveyed by Bloomberg.

Negatives ■ the key downside risks for China’s economy in 2013 include a stalemate on the US debt ceiling,

geopolitical risks in the Middle East and an escalation in tensions between China and Japan. ■ the biggest worry among investors is that China’s banking system non-performing loans

(NPLs) may rise substantially – it will probably continue to rise in the coming two to three quarters, but will peak within the year.

INDIA

GREATER CHINA

Source: Nomura

EQUItIES

The Henley Outlook March 2013Hong Kong, Singapore & Shanghai

EquiTiES

12

HENLEY ASSESSMENtNeutral

The scale of fiscal stimulus in South Korea will be limited as the new Finance Minister, Hyun Oh Seok, will not compromise on the country’s fiscal healthy by engaging in aggressive fiscal spending. The short-term challenge will be to find way to secure a rapid economic growth without printing more money. Similarly, nations like Russia and Brazil are finding it tough to stoke economic growth without inflation spiking up. Inflation is at a 15-month high in Russia, while Brazilian consumer prices rose the fastest in Jan13 at the fastest pace in eight years. Other emerging economies are looking more attractive relative to these nations.

Positives ■ Russia will probably refrain from easing borrowing costs this month after inflation surged to

a 15-month high and the central bank indicated it would not yield to government calls for lower rates.

■ Mexico’s four-year-old expansion, slowing inflation and debt ratios half those in the US are factors winning over investors searching for stable returns as Europe’s economy heads for a contraction. Latin America’s second-biggest economy, which is about half the size of Brazil’s, outgrew its larger regional peer in each of the past two years, posting annual expansions of about 4% as construction and auto production jumped.

Negatives ■ South Korea’s economy expanded 2% in 2012, the slowest pace since annual growth fell

to 0.3% in 2009. that compares with a potential rate of 3.8% estimated by central bank governor Choongsoo Kim. Policy makers also face the problem of a working population that’s expected to start shrinking in 2017, according to a finance ministry report last year.

■ the Bovespa index fell to an 11-week low as economists covering Brazil reduced their 2014 growth forecasts, rekindling concern that a slower recovery will hurt corporate earnings.

■ Russia, the largest emerging nation to raise rates in 2012, is facing growing government pressure to ease monetary policy after economic growth last year slowed to 3.4%, the weakest since the 2009 recession.

■ Shares of BRIC nations are lagging behind as their economic growth advantage shrinks and investors shift money to smaller emerging markets, including turkey and the Philippines. GDP in the BRICs probably increased 4.2% on average in 2012, versus 3.2% for the world economy, according to the IMF. the 1%point gap would be the smallest since 1998.

OTHER EMERGING MARKETS (SOUTH KOREA, RUSSIA, BRAzIL)

EQUItIES

EquitiEs

13

HENLEY ASSESSMENtNeutral

We remain neutral. the global economy remains in a precarious state and with the impending sequester budget cuts looming in the US, we see better opportunities elsewhere.

HENLEY ASSESSMENtPositive

February was a difficult month for gold as speculators pushed the price down on the minutes of the Federal Reserve policy meeting, which showed some members suggesting that QE should come to an end sooner than expected. However, there was a significant bounce following the comments of Federal Reserve Chairman Bernanke during his half yearly testimony to Congress, when he signaled that the Federal Reserve is prepared to keep buying bonds at its present pace. Central banks continue to be buyers of gold, particularly those in developing countries. The official reserves of these countries continue to grow and as these reserves are heavily biased to the USD and EUR, gold is an attractive option as they look for ways to diversify.

Positives ■ Risk of supply disruption from countries such as Iran has kept oil price high. ■ Emerging market demand pushed the oil price higher.

Negatives ■ Concerns about the euro zone and the Italian election result, and thoughts of growing US

stockpiles. ■ US sequester budget cuts.

Positives ■ Gold is a good hedge against currency debasement and future inflation. ■ Gold and gold mining shares remain an under-owned asset class compared to financial assets.

Negatives ■ Short-term price volatility as speculation exists about an end to QE in the US.

ENERGY

PRECIOUS METALS

COMMODItIES

The Henley Outlook March 2013Hong Kong, Singapore & Shanghai

EquiTiES

14

HENLEY ASSESSMENtNeutral

We remain neutral on this sector. the global economy continued to shrink in 2012 and this took its toll on producers of base metals. Prices for copper, iron ore and aluminium fell sharply with decreased demand, and the import price for iron ore in China has increased by over 75% in the past five months.

COMMODItIES

HENLEY ASSESSMENtPositive and negative

two very different markets are playing out in this sector – physical and equity. Many physical soft commodity prices have exploded due to changing global weather patterns over the past few months, however these sharp price increases tend to be followed with just as sharp falls; there is a very seasonal and cyclical pattern. With many soft commodity prices at or near record highs we have a negative view on investing and encourage profit taking. On the equity side, the largest weighting funds have to this sector is via fertilizer and seed companies, which are having a significantly more important role to play to help increase yield and in the case of seed companies, invent seed which is more tolerant to changing global weather patterns. We remain positive on agriculture equity funds.

Positives ■ Warren Buffett’s investment powerhouse Berkshire Hathaway and 3G Capital have

announced they will take over US tomato sauce and baked beans maker Heinz in a deal worth USD23bn. this could lead to broad cost-cutting measures across the industry and a possible rerating in the valuation of similar companies.

■ UN’s Food and Agriculture Organization estimates there will be over nine billion mouths to feed on the planet by 2050.

■ Middle class consumers in BRIC economies are increasingly demanding more varied and protein-rich foods. As affluence increases protein from beef, sheep, poultry, pigs, cows and fish may in turn displace grains in diets.

■ Urbanisation and life expectancy is expected to increase.

Negatives ■ Prices are subject to

many uncontrollable risks, eg, weather and natural disasters, politics and other pests.

■ Due to recent drought conditions in the American Mid-West and Russian Black Sea regions, we have seen corn, wheat and soy prices increase on average over 50% within a few months.

AGRICULTURE

INDUSTRIAL METALS

Positives ■ China continues to restock commodities to the benefit of major commodity-exporting

countries.

Negatives ■ Sluggish global economies and austerity continue to weigh heavily on the sector.

Source: DWS

EquitiEs

HENLEY ASSESSMENt Neutral

We have to admit that for the past two years it has been unusually difficult for active management styles to generate returns. In hedge fund space, those managers, who tend to eschew traditional sources of return such as static market exposure, have been particularly problematic. A material improvement in the global economic landscape made us believe markets this year will be more reactive to fundamental data rather than political influence. Higher level of dispersion within markets and lower systemic risk both give us confidence that hedge funds of some strategies should have huge potential to generate non-correlated returns in 2013, more so than they have for the past two years.

Positives ■ Hedge funds made money in January. the HFRx Global Hedge Fund index ended the month

with a gain of positive 2.0%. Overall, there was a slight increase in gross and net exposure across managers.

■ the best return for this year so far came from security selection specialists in equity long-short space.

■ A number of fundamentally-oriented managers reported excellent trading profits in 2012. Managers with longer-term holding periods and higher conviction positions tended to be the winners as equity moves appeared to depend on value-based metrics.

Negatives ■ We are still having concerns that Managed Futures return would be under threat in the event

of a sell-off in the bond market. ■ Despite total assets under management surpassing its previous high in 2008, managers and

investors are largely cautious going into 2013. New regulations created an added burden for fund managers, and high-profile SEC enquiries into leading hedge fund names, and continued market volatility which led to performance concerns, resulted in further investor dissatisfaction.

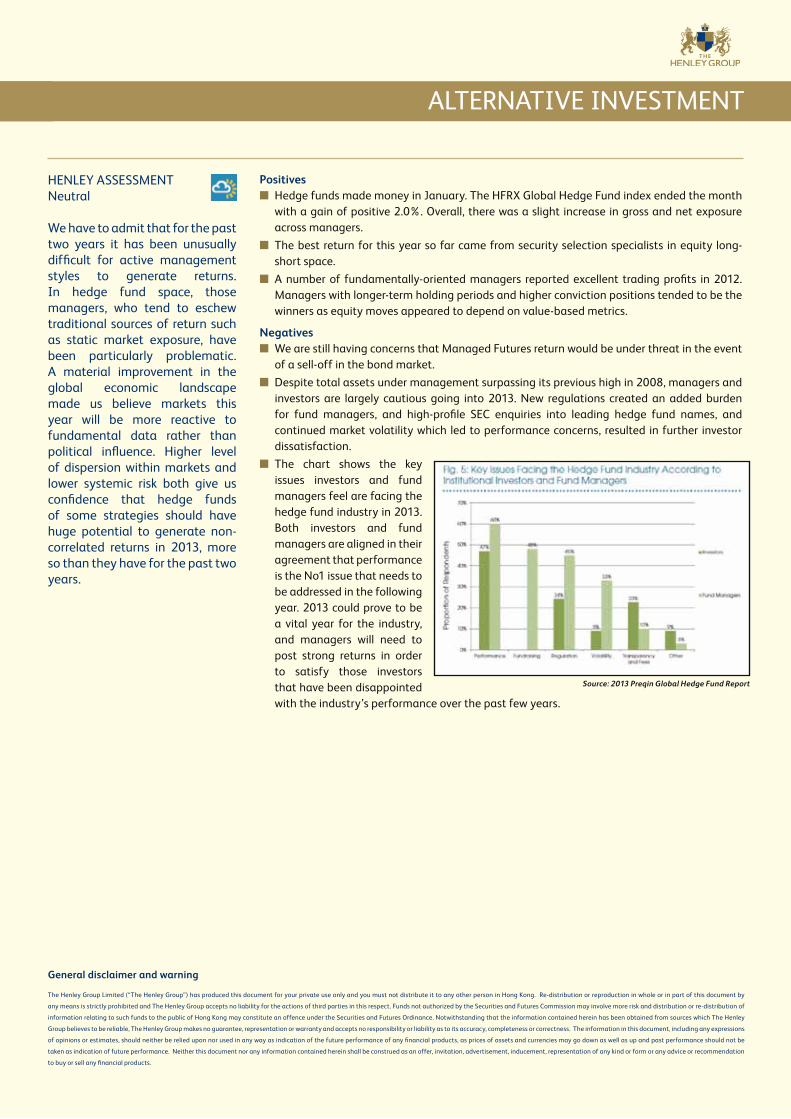

■ the chart shows the key issues investors and fund managers feel are facing the hedge fund industry in 2013. Both investors and fund managers are aligned in their agreement that performance is the No1 issue that needs to be addressed in the following year. 2013 could prove to be a vital year for the industry, and managers will need to post strong returns in order to satisfy those investors that have been disappointed with the industry’s performance over the past few years.

ALtERNAtIvE INvEStMENt

General disclaimer and warning

the Henley Group Limited (“the Henley Group”) has produced this document for your private use only and you must not distribute it to any other person in Hong Kong. Re-distribution or reproduction in whole or in part of this document by

any means is strictly prohibited and the Henley Group accepts no liability for the actions of third parties in this respect. Funds not authorized by the Securities and Futures Commission may involve more risk and distribution or re-distribution of

information relating to such funds to the public of Hong Kong may constitute an offence under the Securities and Futures Ordinance. Notwithstanding that the information contained herein has been obtained from sources which the Henley

Group believes to be reliable, the Henley Group makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy, completeness or correctness. the information in this document, including any expressions

of opinions or estimates, should neither be relied upon nor used in any way as indication of the future performance of any financial products, as prices of assets and currencies may go down as well as up and past performance should not be

taken as indication of future performance. Neither this document nor any information contained herein shall be construed as an offer, invitation, advertisement, inducement, representation of any kind or form or any advice or recommendation

to buy or sell any financial products.

Source: 2013 Preqin Global Hedge Fund Report