helter shelter what to recommend for married clients whose estate planning documents provide for the...

TRANSCRIPT

HELTER SHELTER

WHAT TO RECOMMEND FOR MARRIED CLIENTS WHOSE ESTATE PLANNING DOCUMENTS PROVIDE FOR THE ESTABLISHMENT OF A CREDIT SHELTER TRUST ON THE FIRST DEATH

HOW THESE RULES AND STRATEGIES HAVE CHANGED

A Presentation by:Alan S. Gassman, J.D., LL.M. and Christopher J. Denicolo, J.D., LL.M.

[email protected]@gassmanpa.com

Thursday, June 16, 2011

1

The attached PowerPoint being used for our presentation makes use of pages and exhibits that have been contributed in the past by Professor Jerry Hesch and pages from the outline entitled 2011 Estate Tax Law Changes which is also attached as a separate enclosure.

2

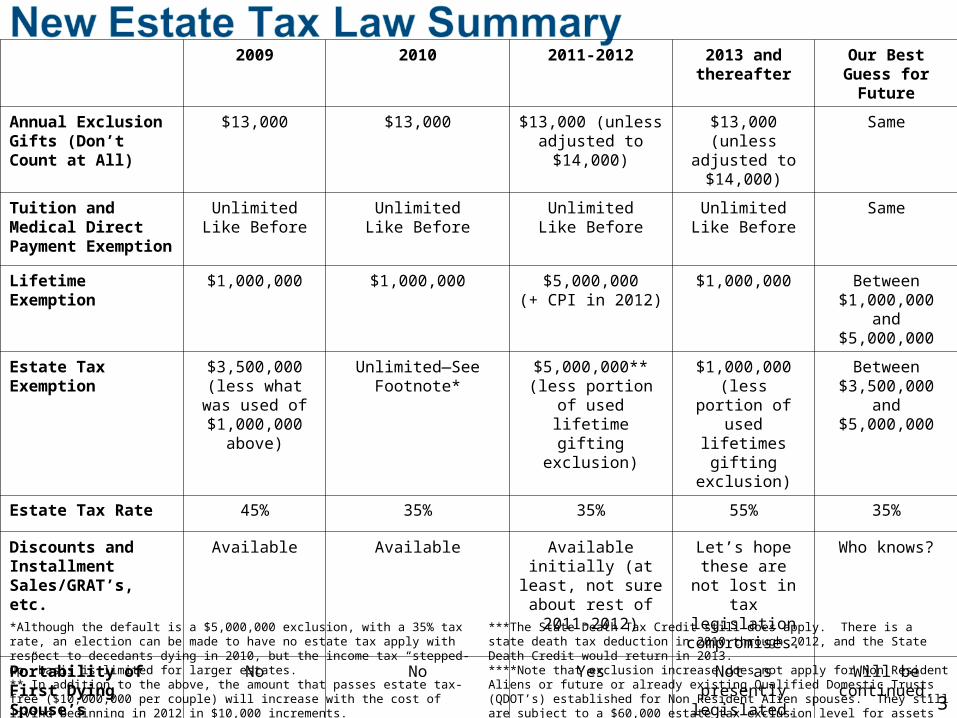

2009 2010 2011-2012 2013 and thereafter

Our Best Guess for Future

Annual Exclusion Gifts (Don’t Count at All)

$13,000 $13,000 $13,000 (unless adjusted to $14,000)

$13,000 (unless adjusted to $14,000)

Same

Tuition and Medical Direct Payment Exemption

UnlimitedLike Before

UnlimitedLike Before

UnlimitedLike Before

UnlimitedLike Before

Same

Lifetime Exemption $1,000,000 $1,000,000 $5,000,000(+ CPI in 2012)

$1,000,000 Between $1,000,000 and

$5,000,000

Estate Tax Exemption

$3,500,000 (less what was used of $1,000,000

above)

Unlimited—See Footnote*

$5,000,000** (less portion of used lifetime gifting

exclusion)

$1,000,000 (less portion of used lifetimes gifting

exclusion)

Between $3,500,000 and

$5,000,000

Estate Tax Rate 45% 35% 35% 55% 35%

Discounts and Installment Sales/GRAT’s, etc.

Available Available Available initially (at least, not sure

about rest of 2011-2012)

Let’s hope these are not lost in tax

legislation compromises.

Who knows?

Portability of First Dying Spouse’s $5,000,000 Exemptions

No No Yes Not as presently legislated.

Will be continued.

*Although the default is a $5,000,000 exclusion, with a 35% tax rate, an election can be made to have no estate tax apply with respect to decedants dying in 2010, but the income tax “stepped-up” basis is limited for larger estates.** In addition to the above, the amount that passes estate tax-free ($10,000,000 per couple) will increase with the cost of living beginning in 2012 in $10,000 increments.

***The State Death Tax Credit still does apply. There is a state death tax deduction in 2010 through 2012, and the State Death Credit would return in 2013.****Note that exclusion increase does not apply for Non Resident Aliens or future or already existing Qualified Domestic Trusts (QDOT’s) established for Non Resident Alien spouses. They still are subject to a $60,000 estate tax exclusion level for assets subject to US estate tax and need planning as much as ever! 3

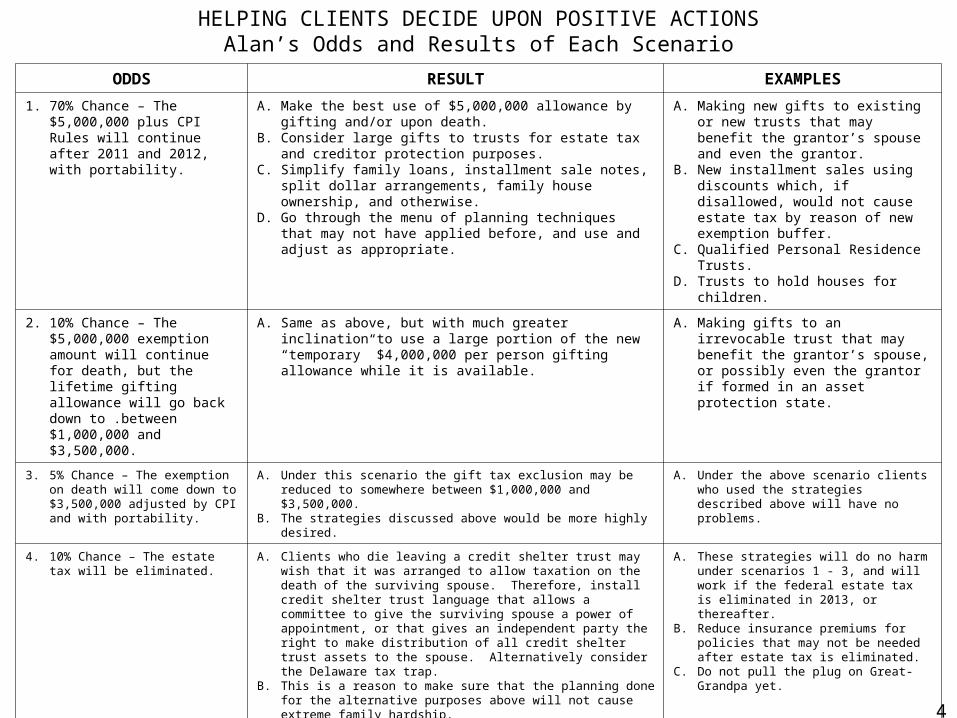

ODDS RESULT EXAMPLES

1. 70% Chance – The $5,000,000 plus CPI Rules will continue after 2011 and 2012, with portability.

A. Make the best use of $5,000,000 allowance by gifting and/or upon death.

B. Consider large gifts to trusts for estate tax and creditor protection purposes.

C. Simplify family loans, installment sale notes, split dollar arrangements, family house ownership, and otherwise.

D. Go through the menu of planning techniques that may not have applied before, and use and adjust as appropriate.

A. Making new gifts to existing or new trusts that may benefit the grantor’s spouse and even the grantor.

B. New installment sales using discounts which, if disallowed, would not cause estate tax by reason of new exemption buffer.

C. Qualified Personal Residence Trusts.D. Trusts to hold houses for children.

2. 10% Chance – The $5,000,000 exemption amount will continue for death, but the lifetime gifting allowance will go back down to .between $1,000,000 and $3,500,000.

A. Same as above, but with much greater inclination to use a large portion of the new “temporary” $4,000,000 per person gifting allowance while it is available.

A. Making gifts to an irrevocable trust that may benefit the grantor’s spouse, or possibly even the grantor if formed in an asset protection state.

3. 5% Chance – The exemption on death will come down to $3,500,000 adjusted by CPI and with portability.

A. Under this scenario the gift tax exclusion may be reduced to somewhere between $1,000,000 and $3,500,000.

B. The strategies discussed above would be more highly desired.

A. Under the above scenario clients who used the strategies described above will have no problems.

4. 10% Chance – The estate tax will be eliminated.

A. Clients who die leaving a credit shelter trust may wish that it was arranged to allow taxation on the death of the surviving spouse. Therefore, install credit shelter trust language that allows a committee to give the surviving spouse a power of appointment, or that gives an independent party the right to make distribution of all credit shelter trust assets to the spouse. Alternatively consider the Delaware tax trap.

B. This is a reason to make sure that the planning done for the alternative purposes above will not cause extreme family hardship.

A. These strategies will do no harm under scenarios 1 - 3, and will work if the federal estate tax is eliminated in 2013, or thereafter.

B. Reduce insurance premiums for policies that may not be needed after estate tax is eliminated.

C. Do not pull the plug on Great-Grandpa yet.

5. 5% Chance – Congress and the President will not agree until after January 1, 2013 so for at least a few days, weeks or months we go back to a $1,000,000 gift tax exemption and a $1,000,000 death exemption, and thereafter one of the above applies.

A. Consider a 9 month disclaim-able late 2012 gift - clients who are somewhat reluctant to use their new $4,000,000 gifting allowance might consider a late 2012 transfer to a trust that allows the spouse to withdraw what is placed into the trust within 9 months of funding, or to disclaim the right to withdraw in which case a completed $4,000,000 gift will have occurred.

B. Clients who are candidates for making $4,000,000 gifts may hem-and-haw until late 2012, so this strategy can be mentioned in 2011 so that they know it is available.

A. Pull the plug on Great-Grandpa in December of 2012.

B. Accelerate gifts as described in scenario 2 above.

C. Use flexible trust documents, as described above, to take into account that this may happen.

HELPING CLIENTS DECIDE UPON POSITIVE ACTIONSAlan’s Odds and Results of Each Scenario

4

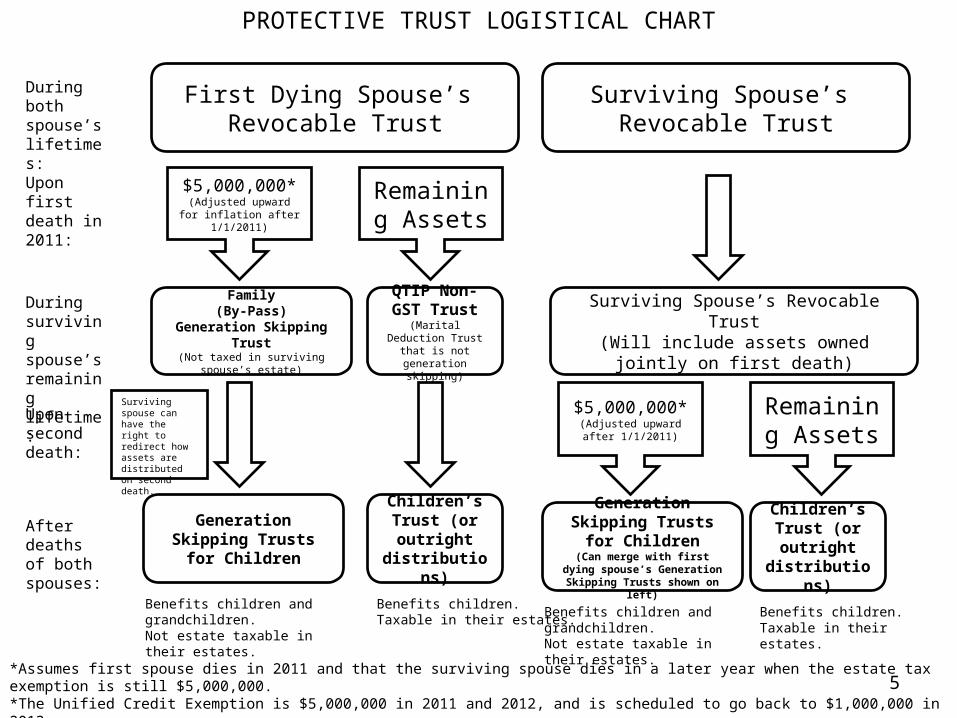

PROTECTIVE TRUST LOGISTICAL CHART

First Dying Spouse’s Revocable Trust

Surviving Spouse’s Revocable Trust

$5,000,000*(Adjusted upward for

inflation after 1/1/2011)

Remaining Assets

Family(By-Pass)

Generation Skipping Trust(Not taxed in surviving spouse’s

estate)

QTIP Non-GST Trust

(Marital Deduction Trust that is not

generation skipping)

Generation Skipping Trusts for Children

Children’s Trust (or outright

distributions)

Surviving spouse can have the right to redirect how assets are distributed on second death.

Benefits children and grandchildren.Not estate taxable in their estates.

Benefits children.Taxable in their estates.

Surviving Spouse’s Revocable Trust(Will include assets owned jointly on first

death)

$5,000,000*(Adjusted upward after

1/1/2011)

Remaining Assets

Generation Skipping Trusts for Children(Can merge with first dying

spouse’s Generation Skipping Trusts shown on left)

Children’s Trust (or outright

distributions)

Benefits children and grandchildren.Not estate taxable in their estates.

Benefits children.Taxable in their estates.

During both spouse’s lifetimes:

Upon first death in 2011:

During surviving spouse’s remaining lifetime:

Upon second death:

After deaths of both spouses:

*Assumes first spouse dies in 2011 and that the surviving spouse dies in a later year when the estate tax exemption is still $5,000,000.*The Unified Credit Exemption is $5,000,000 in 2011 and 2012, and is scheduled to go back to $1,000,000 in 2013. 5

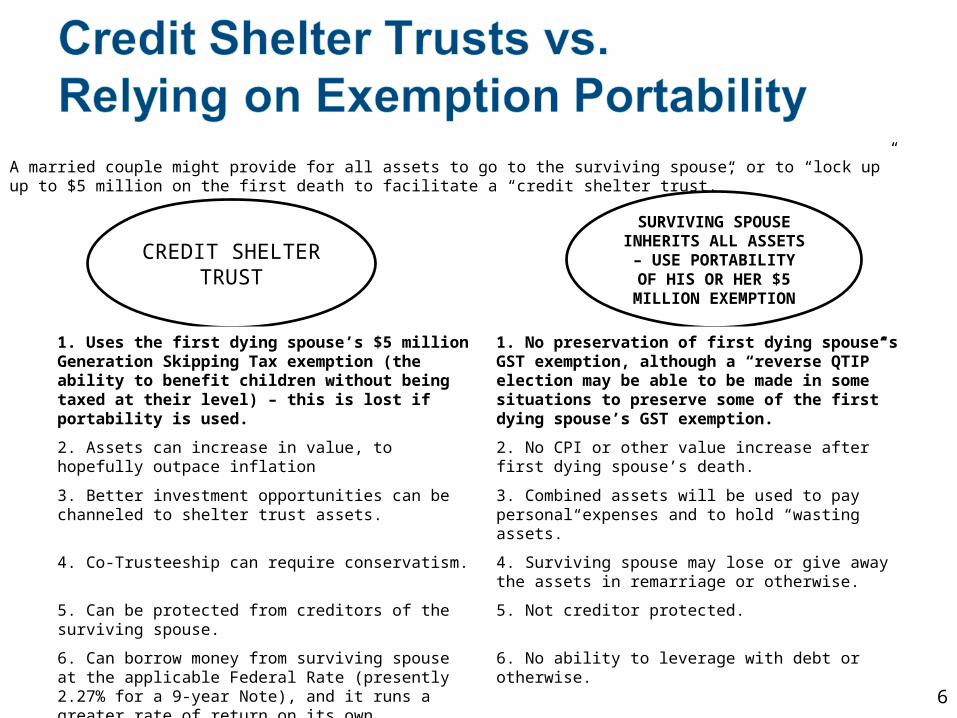

A married couple might provide for all assets to go to the surviving spouse, or to “lock up” up to $5 million on the first death to facilitate a “credit shelter trust.”

CREDIT SHELTER TRUST

SURVIVING SPOUSE INHERITS ALL ASSETS – USE PORTABILITY OF HIS OR HER $5 MILLION

EXEMPTION

1. Uses the first dying spouse’s $5 million Generation Skipping Tax exemption (the ability to benefit children without being taxed at their level) – this is lost if portability is used.

1. No preservation of first dying spouse’s GST exemption, although a “reverse QTIP” election may be able to be made in some situations to preserve some of the first dying spouse’s GST exemption.

2. Assets can increase in value, to hopefully outpace inflation

2. No CPI or other value increase after first dying spouse’s death.

3. Better investment opportunities can be channeled to shelter trust assets.

3. Combined assets will be used to pay personal expenses and to hold “wasting assets.”

4. Co-Trusteeship can require conservatism. 4. Surviving spouse may lose or give away the assets in remarriage or otherwise.

5. Can be protected from creditors of the surviving spouse. 5. Not creditor protected.

6. Can borrow money from surviving spouse at the applicable Federal Rate (presently 2.27% for a 9-year Note), and it runs a greater rate of return on its own investment.

6. No ability to leverage with debt or otherwise.

6

7

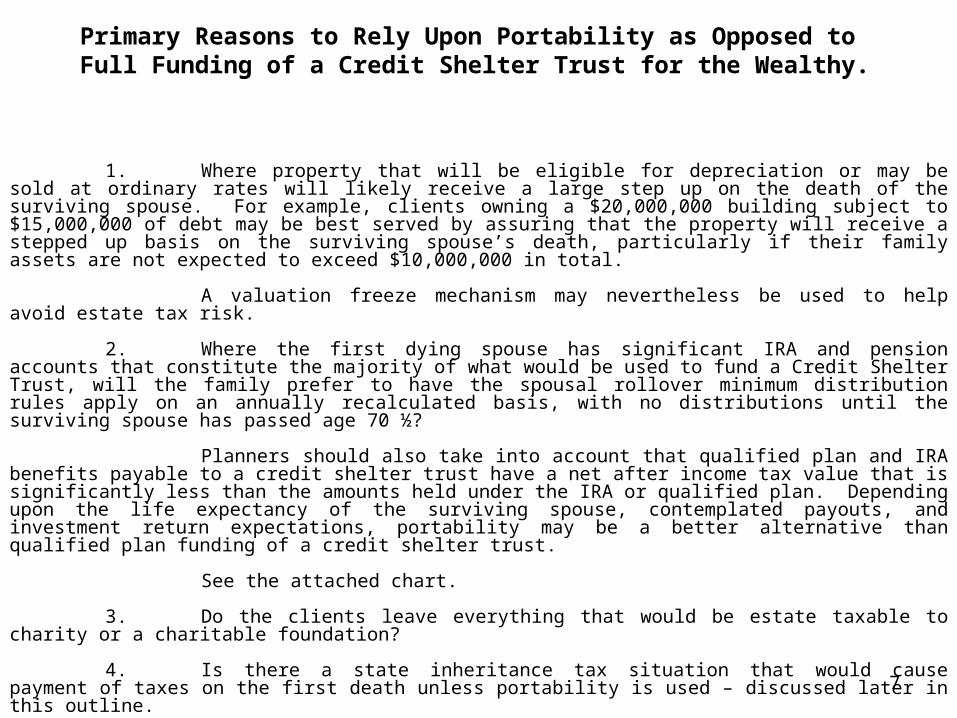

1. Where property that will be eligible for depreciation or may be sold at ordinary rates will likely receive a large step up on the death of the surviving spouse. For example, clients owning a $20,000,000 building subject to $15,000,000 of debt may be best served by assuring that the property will receive a stepped up basis on the surviving spouse’s death, particularly if their family assets are not expected to exceed $10,000,000 in total.

A valuation freeze mechanism may nevertheless be used to help avoid estate tax risk.

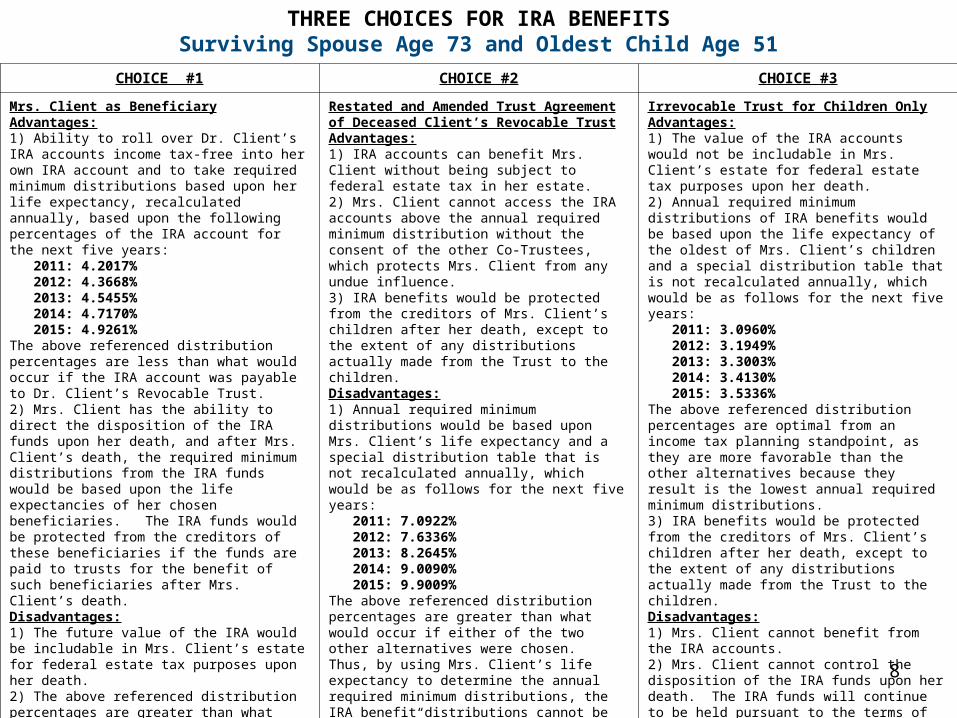

2. Where the first dying spouse has significant IRA and pension accounts that constitute the majority of what would be used to fund a Credit Shelter Trust, will the family prefer to have the spousal rollover minimum distribution rules apply on an annually recalculated basis, with no distributions until the surviving spouse has passed age 70 ½?

Planners should also take into account that qualified plan and IRA benefits payable to a credit shelter trust have a net after income tax value that is significantly less than the amounts held under the IRA or qualified plan. Depending upon the life expectancy of the surviving spouse, contemplated payouts, and investment return expectations, portability may be a better alternative than qualified plan funding of a credit shelter trust.

See the attached chart.

3. Do the clients leave everything that would be estate taxable to charity or a charitable foundation?

4. Is there a state inheritance tax situation that would cause payment of taxes on the first death unless portability is used – discussed later in this outline.

Primary Reasons to Rely Upon Portability as Opposed to Full Funding of a Credit Shelter Trust for the Wealthy.

THREE CHOICES FOR IRA BENEFITSSurviving Spouse Age 73 and Oldest Child Age 51

CHOICE #1 CHOICE #2 CHOICE #3

Mrs. Client as BeneficiaryAdvantages:1) Ability to roll over Dr. Client’s IRA accounts income tax-free into her own IRA account and to take required minimum distributions based upon her life expectancy, recalculated annually, based upon the following percentages of the IRA account for the next five years: 2011: 4.2017% 2012: 4.3668% 2013: 4.5455% 2014: 4.7170% 2015: 4.9261%The above referenced distribution percentages are less than what would occur if the IRA account was payable to Dr. Client’s Revocable Trust.2) Mrs. Client has the ability to direct the disposition of the IRA funds upon her death, and after Mrs. Client’s death, the required minimum distributions from the IRA funds would be based upon the life expectancies of her chosen beneficiaries. The IRA funds would be protected from the creditors of these beneficiaries if the funds are paid to trusts for the benefit of such beneficiaries after Mrs. Client’s death. Disadvantages:1) The future value of the IRA would be includable in Mrs. Client’s estate for federal estate tax purposes upon her death. 2) The above referenced distribution percentages are greater than what would occur if the IRA accounts were disclaimed so that they are payable to the Client Irrevocable Trust.

Restated and Amended Trust Agreement of Deceased Client’s Revocable TrustAdvantages:1) IRA accounts can benefit Mrs. Client without being subject to federal estate tax in her estate.2) Mrs. Client cannot access the IRA accounts above the annual required minimum distribution without the consent of the other Co-Trustees, which protects Mrs. Client from any undue influence.3) IRA benefits would be protected from the creditors of Mrs. Client’s children after her death, except to the extent of any distributions actually made from the Trust to the children. Disadvantages:1) Annual required minimum distributions would be based upon Mrs. Client’s life expectancy and a special distribution table that is not recalculated annually, which would be as follows for the next five years: 2011: 7.0922% 2012: 7.6336% 2013: 8.2645% 2014: 9.0090% 2015: 9.9009%The above referenced distribution percentages are greater than what would occur if either of the two other alternatives were chosen. Thus, by using Mrs. Client’s life expectancy to determine the annual required minimum distributions, the IRA benefit distributions cannot be “stretched” out over life expectancies of Mrs. Client’s children after her death. 2) Mrs. Client will have to forfeit her ability to direct the disposition of the IRA funds after her death. The IRA funds will instead pass in separate trusts for the benefit of Mrs. Client’s children upon her death.

Irrevocable Trust for Children OnlyAdvantages:1) The value of the IRA accounts would not be includable in Mrs. Client’s estate for federal estate tax purposes upon her death.2) Annual required minimum distributions of IRA benefits would be based upon the life expectancy of the oldest of Mrs. Client’s children and a special distribution table that is not recalculated annually, which would be as follows for the next five years: 2011: 3.0960% 2012: 3.1949% 2013: 3.3003% 2014: 3.4130% 2015: 3.5336%The above referenced distribution percentages are optimal from an income tax planning standpoint, as they are more favorable than the other alternatives because they result is the lowest annual required minimum distributions. 3) IRA benefits would be protected from the creditors of Mrs. Client’s children after her death, except to the extent of any distributions actually made from the Trust to the children. Disadvantages:1) Mrs. Client cannot benefit from the IRA accounts.2) Mrs. Client cannot control the disposition of the IRA funds upon her death. The IRA funds will continue to be held pursuant to the terms of the Trust.

8

3. Facilitate having Credit Shelter Trust language be flexible to allow trust assets to be includable in the estate of the surviving spouse to get an income tax basis step-up.

9

The Planner's Idea and Checklist for Helping Clients During the 2011 and 2012, $5 Million Bump Years

PROTECTIVE TRUST LOGISTICAL CHART

First Dying Spouse’s Revocable Trust

Surviving Spouse’s Revocable Trust

$5,000,000*(Adjusted upward for

inflation after 1/1/2011)

Remaining Assets

Family(By-Pass)

Generation Skipping Trust(Not taxed in surviving spouse’s

estate)

QTIP Non-GST Trust

(Marital Deduction Trust that is not

generation skipping)

Generation Skipping Trusts for Children

Children’s Trust (or outright

distributions)

Surviving spouse can have the right to redirect how assets are distributed on second death.

Benefits children and grandchildren.Not estate taxable in their estates.

Benefits children.Taxable in their estates.

Surviving Spouse’s Revocable Trust(Will include assets owned jointly on first

death)

$5,000,000*(Adjusted upward after

1/1/2011)

Remaining Assets

Generation Skipping Trusts for Children(Can merge with first dying

spouse’s Generation Skipping Trusts shown on left)

Children’s Trust (or outright

distributions)

Benefits children and grandchildren.Not estate taxable in their estates.

Benefits children.Taxable in their estates.

During both spouse’s lifetimes:

Upon first death in 2011:

During surviving spouse’s remaining lifetime:

Upon second death:

After deaths of both spouses:

*Assumes first spouse dies in 2011 and that the surviving spouse dies in a later year when the estate tax exemption is still $5,000,000.*The Unified Credit Exemption is $5,000,000 in 2011 and 2012, and is scheduled to go back to $1,000,000 in 2013. 10

CHOICE ADVANTAGES DISADVANTAGES

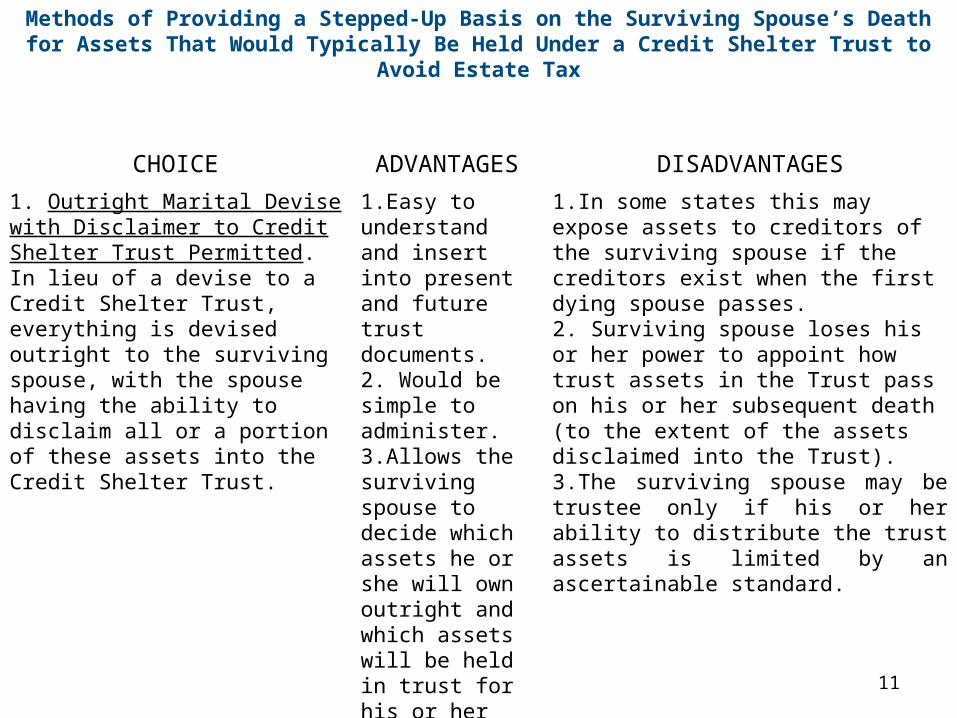

1. Outright Marital Devise with Disclaimer to Credit Shelter Trust Permitted. In lieu of a devise to a Credit Shelter Trust, everything is devised outright to the surviving spouse, with the spouse having the ability to disclaim all or a portion of these assets into the Credit Shelter Trust.

1.Easy to understand and insert into present and future trust documents.2. Would be simple to administer.3.Allows the surviving spouse to decide which assets he or she will own outright and which assets will be held in trust for his or her benefit.

1.In some states this may expose assets to creditors of the surviving spouse if the creditors exist when the first dying spouse passes.2. Surviving spouse loses his or her power to appoint how trust assets in the Trust pass on his or her subsequent death (to the extent of the assets disclaimed into the Trust).3.The surviving spouse may be trustee only if his or her ability to distribute the trust assets is limited by an ascertainable standard.

Methods of Providing a Stepped-Up Basis on the Surviving Spouse’s Death for Assets That Would Typically Be Held Under a Credit Shelter Trust to Avoid Estate Tax

11

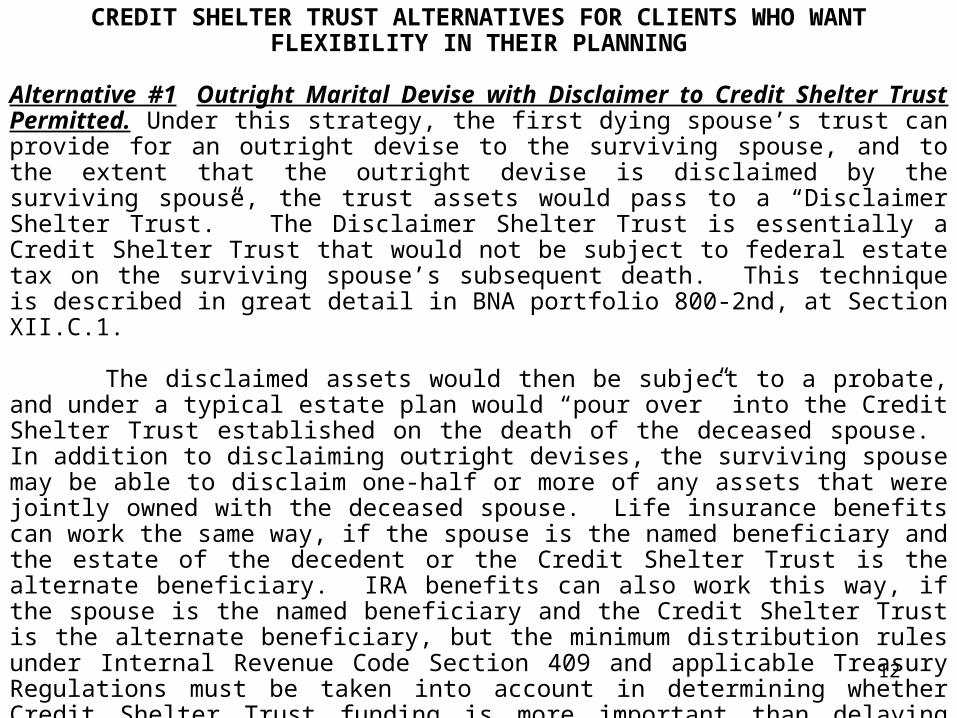

CREDIT SHELTER TRUST ALTERNATIVES FOR CLIENTS WHO WANT FLEXIBILITY IN THEIR PLANNING

Alternative #1 Outright Marital Devise with Disclaimer to Credit Shelter Trust Permitted. Under this strategy, the first dying spouse’s trust can provide for an outright devise to the surviving spouse, and to the extent that the outright devise is disclaimed by the surviving spouse, the trust assets would pass to a “Disclaimer Shelter Trust.” The Disclaimer Shelter Trust is essentially a Credit Shelter Trust that would not be subject to federal estate tax on the surviving spouse’s subsequent death. This technique is described in great detail in BNA portfolio 800-2nd, at Section XII.C.1.

The disclaimed assets would then be subject to a probate, and under a typical estate plan would “pour over” into the Credit Shelter Trust established on the death of the deceased spouse. In addition to disclaiming outright devises, the surviving spouse may be able to disclaim one-half or more of any assets that were jointly owned with the deceased spouse. Life insurance benefits can work the same way, if the spouse is the named beneficiary and the estate of the decedent or the Credit Shelter Trust is the alternate beneficiary. IRA benefits can also work this way, if the spouse is the named beneficiary and the Credit Shelter Trust is the alternate beneficiary, but the minimum distribution rules under Internal Revenue Code Section 409 and applicable Treasury Regulations must be taken into account in determining whether Credit Shelter Trust funding is more important than delaying distributions until the year after the surviving spouse reaches the age 70 1/2. The “stretch trust” techniques that can be used for Credit Shelter Trusts may become more important for clients who would have otherwise had sufficient assets to fund a Credit Shelter Trust with non-IRA assets before the exclusion went up to $5,000,000.

12

CHOICE ADVANTAGES DISADVANTAGES

2. Special Trustees May Cause Credit Shelter Trust Assets to be Transferred to Surviving Spouse. An independent advisor or committee will have the power to cause Credit Shelter Trust assets to be devised directly to the surviving spouse to get a stepped up basis on his or her death.

1. Easy to understand and insert into present and future trust documents.2. Would be simple to administer.

1. Giving the surviving spouse outright ownership of assets can be unwise from a creditor protection, spendthrift, remarriage and undue influence standpoint, and this could result in many fortunes being lost.2. Would cause the distributed assets to be included in the estate of the surviving spouse, which could be problematic if portability is not applicable at that time.3. What fiduciary duties are involved with monitoring health and circumstances to know if and when to activate this?

Methods of Providing a Stepped-Up Basis on the Surviving Spouse’s Death for Assets That Would Typically Be Held Under a Credit Shelter Trust to Avoid Estate Tax

13

CREDIT SHELTER TRUST ALTERNATIVES FOR CLIENTS WHO WANT FLEXIBILITY IN THEIR PLANNING

Alternative #2 Having Special Trustees Who Can Later Cause Credit Shelter Trust Assets to be Transferred to Surviving Spouse. As described in the above chart, this strategy is a relatively simple solution to providing flexibility with respect to the decision of whether to fund a Credit Shelter Trust or to use portability on the death of the first dying spouse. Language can be added to clients’ revocable trusts to provide this flexibility on the death of the first dying spouse, and can also allow the Trustee or Trust Protectors to bestow a general power of appointment on the surviving spouse to provide for greater flexibility. Sample language is as follows:

In order to provide for possible future tax planning under the XYZ Credit Shelter Trust, if and when formed and funded, I hereby appoint __________, __________ and __________ as Distribution Advisors, and, by majority vote of them, any assets held under said Family Trust may be distributed to or for my said spouse, regardless of need, provided that I request that her interests and the interests of our decedents be carefully considered before any such distribution is made. Such transfer may be outright to my spouse, or into a separate trust created by the Distribution Advisors which would be identical to this trust, but may provide my spouse with a testamentary power of appointment exercisable in favor of creditors of my spouse’s estate, which I am advised may be beneficial from a tax planning standpoint.

Further, said Distribution Advisors shall have the power to provide for my spouse to have a Power of Appointment over all or a portion of the assets of the XYZ Credit Shelter Trust, exercisable in favor of the creditors of my spouse’s estate, if they deem this to be appropriate after receiving written advice from a lawyer who is Board Certified in Estate Planning or Taxation.

If a majority of __________, __________ and __________ are unable to act, then the party that would appoint Trustees in the event of a vacancy in the office of Trustee under Section _______of this Trust Agreement shall appoint one or more of a duly licensed lawyer that is Board Certified by the _______________ Bar in Wills, Trusts & Estates, a CPA who has done work for our family for at least 15 years, or a Licensed Trust Company to serve as Distribution Advisors. Notwithstanding the previous sentence, in no event can any person or entity be appointed if such person or entity is considered as a “related or subordinate party” with respect to me or to my said spouse as such term is defined under Internal Revenue Code Section 672(c). 14

REVISED PROTECTIVE TRUST LOGISTICAL CHART SHOWING CLAYTON QTIPS

First Dying Spouse’s Revocable Trust

Surviving Spouse’s Revocable Trust

$5,000,000*(Adjusted upward for inflation after 1/1/2011)

Remaining Assets

Family(By-Pass)

Generation Skipping Trust

(Not taxed in surviving spouse’s estate)

QTIP Non-GST Trust

(Marital Deduction Trust that is not

generation skipping)

Generation Skipping Trusts for Children

Children’s Trust (or outright

distributions)

Surviving spouse can have the right to redirect how assets are distributed on second death.

Benefits children and grandchildren.Not estate taxable in their estates.

Benefits children.Taxable in their estates.

Surviving Spouse’s Revocable Trust(Will include assets owned jointly on first

death)

$5,000,000*(Adjusted upward after

1/1/2011)

Remaining Assets

Generation Skipping Trusts for Children(Can merge with first dying

spouse’s Generation Skipping Trusts shown on left)

Children’s Trust (or outright

distributions)

Benefits children and grandchildren.Not estate taxable in their estates.

Benefits children.Taxable in their estates.

During both spouse’s lifetimes:

Upon first death in 2011:

During surviving spouse’s remaining lifetime:

Upon second death:

After deaths of both spouses:

*Assumes first spouse dies in 2011 and that the surviving spouse dies in a later year when the estate tax exemption is still $5,000,000.*The Unified Credit Exemption is $5,000,000 in 2011 and 2012, and is scheduled to go back to $1,000,000 in 2013.

QTIP MECHANISM

The assets in the Clayton QTIP would be includable in the surviving spouse’s gross estate, but the surviving spouse can use some of his or her DSUEA, and could make a “reverse QTIP election” to utilize any portion of the first dying spouse’s unused GST exemption.

15

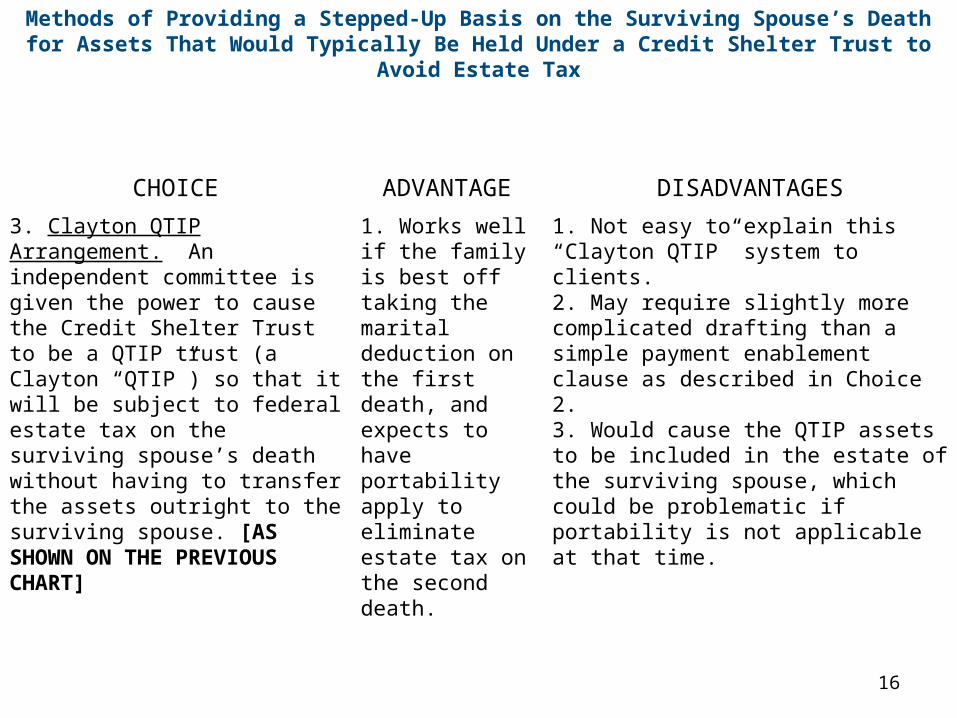

Methods of Providing a Stepped-Up Basis on the Surviving Spouse’s Death for Assets That Would Typically Be Held Under a Credit Shelter Trust to Avoid Estate Tax

CHOICE ADVANTAGE DISADVANTAGES

3. Clayton QTIP Arrangement. An independent committee is given the power to cause the Credit Shelter Trust to be a QTIP trust (a Clayton “QTIP”) so that it will be subject to federal estate tax on the surviving spouse’s death without having to transfer the assets outright to the surviving spouse. [AS SHOWN ON THE PREVIOUS CHART]

1. Works well if the family is best off taking the marital deduction on the first death, and expects to have portability apply to eliminate estate tax on the second death.

1. Not easy to explain this “Clayton QTIP” system to clients.2. May require slightly more complicated drafting than a simple payment enablement clause as described in Choice 2.3. Would cause the QTIP assets to be included in the estate of the surviving spouse, which could be problematic if portability is not applicable at that time.

16

CREDIT SHELTER TRUST ALTERNATIVES FOR CLIENTS WHO WANT FLEXIBILITY IN THEIR PLANNING

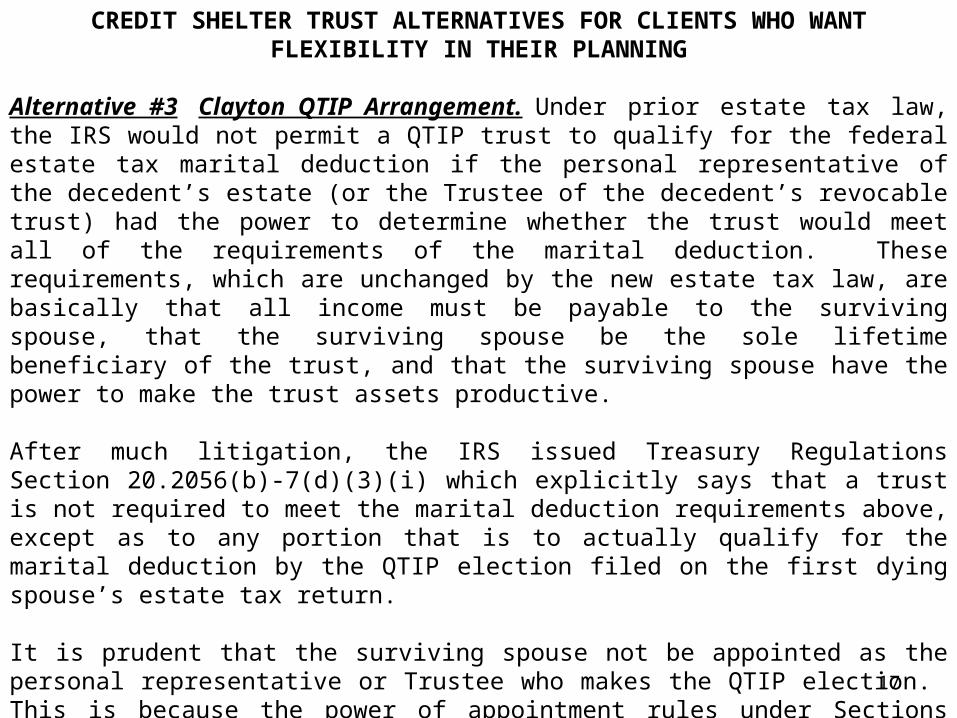

Alternative #3 Clayton QTIP Arrangement. Under prior estate tax law, the IRS would not permit a QTIP trust to qualify for the federal estate tax marital deduction if the personal representative of the decedent’s estate (or the Trustee of the decedent’s revocable trust) had the power to determine whether the trust would meet all of the requirements of the marital deduction. These requirements, which are unchanged by the new estate tax law, are basically that all income must be payable to the surviving spouse, that the surviving spouse be the sole lifetime beneficiary of the trust, and that the surviving spouse have the power to make the trust assets productive.

After much litigation, the IRS issued Treasury Regulations Section 20.2056(b)-7(d)(3)(i) which explicitly says that a trust is not required to meet the marital deduction requirements above, except as to any portion that is to actually qualify for the marital deduction by the QTIP election filed on the first dying spouse’s estate tax return.

It is prudent that the surviving spouse not be appointed as the personal representative or Trustee who makes the QTIP election. This is because the power of appointment rules under Sections 2041 and 2514 may cause the value of the assets in the non-QTIP portion of the trust to be included in the spouse’s gross estate upon his or her subsequent death, or the spouse may be deemed to have made a gift to the extent that assets are not used to fund a QTIP trust.

17

CREDIT SHELTER TRUST ALTERNATIVES FOR CLIENTS WHO WANT FLEXIBILITY IN THEIR PLANNING

Alternative #3 Clayton QTIP Arrangement Continued. The following is potential language to amend a client’s revocable trust to allow a Credit Shelter Trust to become a

Clayton QTIP with outright disposition rights, in the instance that the family elects to use portability.

I hereby appoint _______________, ________________ and ____________ as Independent Fiduciaries for the purpose of allowing them to determine whether there should be an alteration of the CLIENT Credit Shelter Trust established under Section 4.02(d) of this Trust Agreement whereby some or all of such assets may be held as a QTIP Marital Deduction Trust, as separate QTIP Marital Deduction Trusts, and/or paid, in whole or in part, outright to my spouse for income and estate tax planning purposes in view of the new estate tax law.

In order to facilitate this, said Independent Fiduciaries shall have the power on a timely filed federal estate tax return filed with respect to my estate, to designate that all or a portion of the CLIENT Credit Shelter Trust shall qualify as a Qualified Terminal Interest Property Trust under Internal Revenue Code Section 2056(b)(7) in which case such Trust shall meet the following requirements, and shall be construed to have the following provisions effective upon my death: (a) the Trustee shall pay all income to my spouse beginning upon my date of death, no less frequently than annually; (b) the Trust assets shall be used solely for my spouse during said spouse’s lifetime, with any and all distributions to be made solely to said spouse; and (c) the Trustee shall be required to keep the Trust assets under such Trust productive, provided that such requirements shall not apply except to the extent that my Personal Representative, upon the written instructions from the majority of the Independent Fiduciaries, elects for such Trust to qualify for the federal estate tax marital deduction by making a “Clayton QTIP Election” pursuant to Internal Revenue Code Section 2056 and Treasury Regulation 20.2056(b)-7)(d)(3)(i). In addition, if determined appropriate by the Independent Fiduciaries, the Trust assets may be paid in whole or in part outright to my said spouse.

If a majority of __________, __________ and __________ are unable to act, then the party that would appoint Trustees in the event of a vacancy in the office of Trustee under Section _________ of this Trust Agreement shall appoint one or more of a duly licensed lawyer that is Board Certified by the Florida Bar in Wills, Trusts & Estates, a CPA who has done work for our family for at least 15 years, and/or a Licensed Trust Company to serve as Independent Fiduciaries, provided that at all times there shall be at least two individuals or a Licensed Trust Company serving as Independent Fiduciaries. Notwithstanding the previous sentence, in no event can any person or entity be appointed if such person or entity is considered as a “related or subordinate party” with respect to me or to my said spouse as such term is defined under Internal Revenue Code Section 672(c).

18

Methods of Providing a Stepped-Up Basis on the Surviving Spouse’s Death for Assets That Would Typically Be Held Under a Credit Shelter Trust to Avoid Estate Tax

CHOICE ADVANTAGE DISADVANTAGES

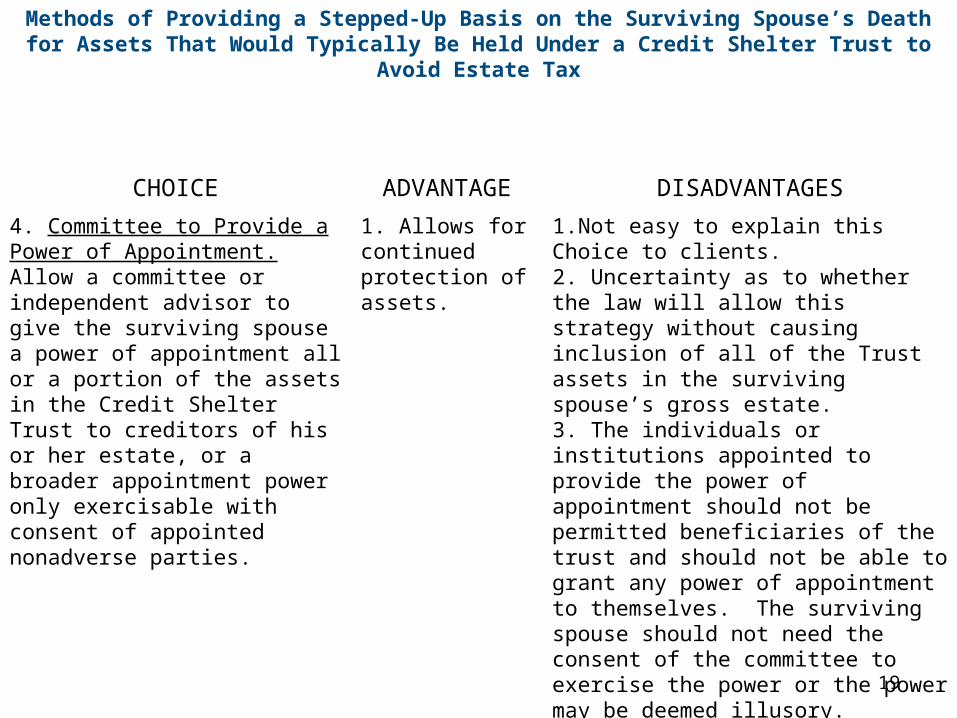

4. Committee to Provide a Power of Appointment. Allow a committee or independent advisor to give the surviving spouse a power of appointment all or a portion of the assets in the Credit Shelter Trust to creditors of his or her estate, or a broader appointment power only exercisable with consent of appointed nonadverse parties.

1. Allows for continued protection of assets.

1.Not easy to explain this Choice to clients.2. Uncertainty as to whether the law will allow this strategy without causing inclusion of all of the Trust assets in the surviving spouse’s gross estate.3. The individuals or institutions appointed to provide the power of appointment should not be permitted beneficiaries of the trust and should not be able to grant any power of appointment to themselves. The surviving spouse should not need the consent of the committee to exercise the power or the power may be deemed illusory.

19

CREDIT SHELTER TRUST ALTERNATIVES FOR CLIENTS WHO WANT FLEXIBILITY IN THEIR PLANNING

Alternative #4 Committee to Provide a Power of Appointment. The authors are concerned that if a couple opts to use portability, surviving spouses will not be as well protected as if they had funded a Credit Shelter Trust to benefit the surviving spouse for his or her lifetime. Asking someone who has just lost his or her lifelong spouse to make a significant financial decision within nine months of death by disclaimer, and to also give up the power to appoint how the trust assets will pass by power of appointment, is not an optimal solution. Neither is transferring assets outright to a surviving spouse who may lose them to creditors, divorce claims, or overly aggressive son and daughter-in-laws an ideal option.

The Clayton QTIP strategy typically works well, but the decision must be made on the first dying spouse’s estate tax return, which will be due no later than 15 months after the death of the first spouse, and explaining the mechanism to clients may be challenging.

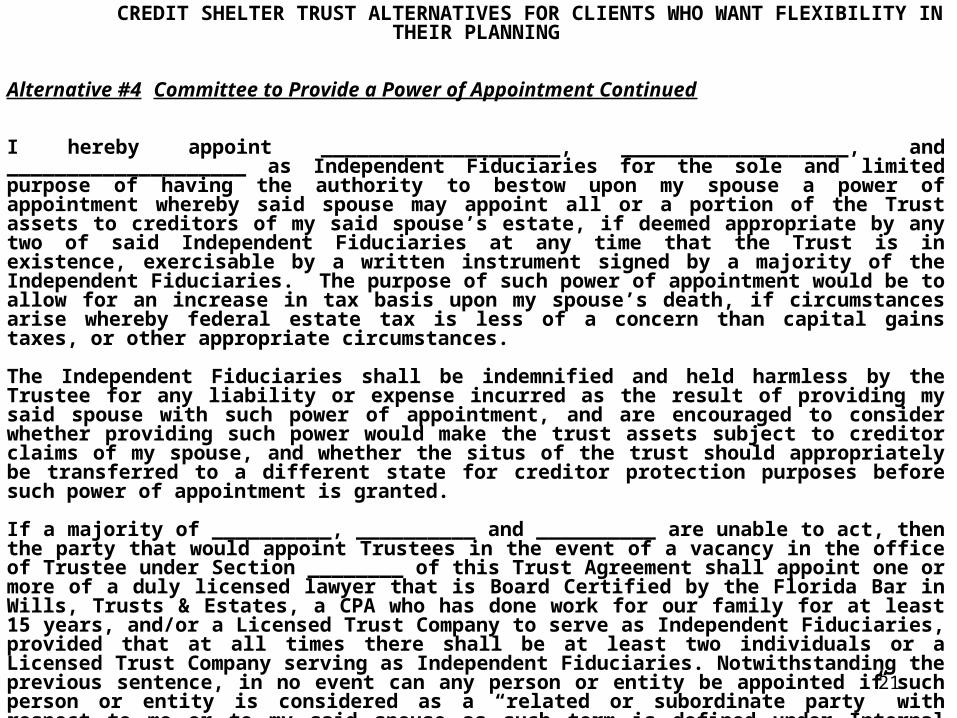

The authors therefore favor providing a committee of impartial advisors, who have the right to give the surviving spouse a power to appoint the trust assets to creditors of his or her estate. As a result, the surviving spouse will be considered the owner of the assets under the trust for estate tax and income tax step-up basis purposes, even though the power given to the surviving spouse may not be exercisable unless he or she has consent from one or more unrelated parties. If the estate tax is eliminated and a family wants to receive a stepped-up basis on the death of the surviving spouse, then the following clause may be used:

20

CREDIT SHELTER TRUST ALTERNATIVES FOR CLIENTS WHO WANT FLEXIBILITY IN THEIR PLANNING

Alternative #4 Committee to Provide a Power of Appointment Continued

I hereby appoint ____________________, ___________________, and ____________________ as Independent Fiduciaries for the sole and limited purpose of having the authority to bestow upon my spouse a power of appointment whereby said spouse may appoint all or a portion of the Trust assets to creditors of my said spouse’s estate, if deemed appropriate by any two of said Independent Fiduciaries at any time that the Trust is in existence, exercisable by a written instrument signed by a majority of the Independent Fiduciaries. The purpose of such power of appointment would be to allow for an increase in tax basis upon my spouse’s death, if circumstances arise whereby federal estate tax is less of a concern than capital gains taxes, or other appropriate circumstances. The Independent Fiduciaries shall be indemnified and held harmless by the Trustee for any liability or expense incurred as the result of providing my said spouse with such power of appointment, and are encouraged to consider whether providing such power would make the trust assets subject to creditor claims of my spouse, and whether the situs of the trust should appropriately be transferred to a different state for creditor protection purposes before such power of appointment is granted. If a majority of __________, __________ and __________ are unable to act, then the party that would appoint Trustees in the event of a vacancy in the office of Trustee under Section ________ of this Trust Agreement shall appoint one or more of a duly licensed lawyer that is Board Certified by the Florida Bar in Wills, Trusts & Estates, a CPA who has done work for our family for at least 15 years, and/or a Licensed Trust Company to serve as Independent Fiduciaries, provided that at all times there shall be at least two individuals or a Licensed Trust Company serving as Independent Fiduciaries. Notwithstanding the previous sentence, in no event can any person or entity be appointed if such person or entity is considered as a “related or subordinate party” with respect to me or to my said spouse as such term is defined under Internal Revenue Code Section 672(c).

21

22

CHOICE ADVANTAGES DISADVANTAGES

5. The Delaware Tax Trap. Allow the surviving spouse to exercise a power of appointment that creates a new trust that someone else holds a power of appointment over which would permit extension of the existence of trust arrangements beyond the initial state law rule against perpetuities.

1. Allows for inclusion under circumstances presently existing under some credit shelter trusts.

2. Does not require significant drafting changes from how trusts may now be situated.

1. A complex area of law.

2. No way to predict whether the law may change in the future with respect to this archaic doctrine.

3. The laws of most states will presently prevent the exercise of a power of appointment to effectively extend the rule against perpetuities.

IDEA – Will the trust be moveable to a state that will permit the Delaware tax trap to be triggered?

Methods of Providing a Stepped-Up Basis on the Surviving Spouse’s Death for Assets That Would Typically Be Held Under a Credit Shelter Trust to Avoid Estate Tax

23

CREDIT SHELTER TRUST ALTERNATIVES FOR CLIENTS WHO WANT FLEXIBILITY IN THEIR PLANNING

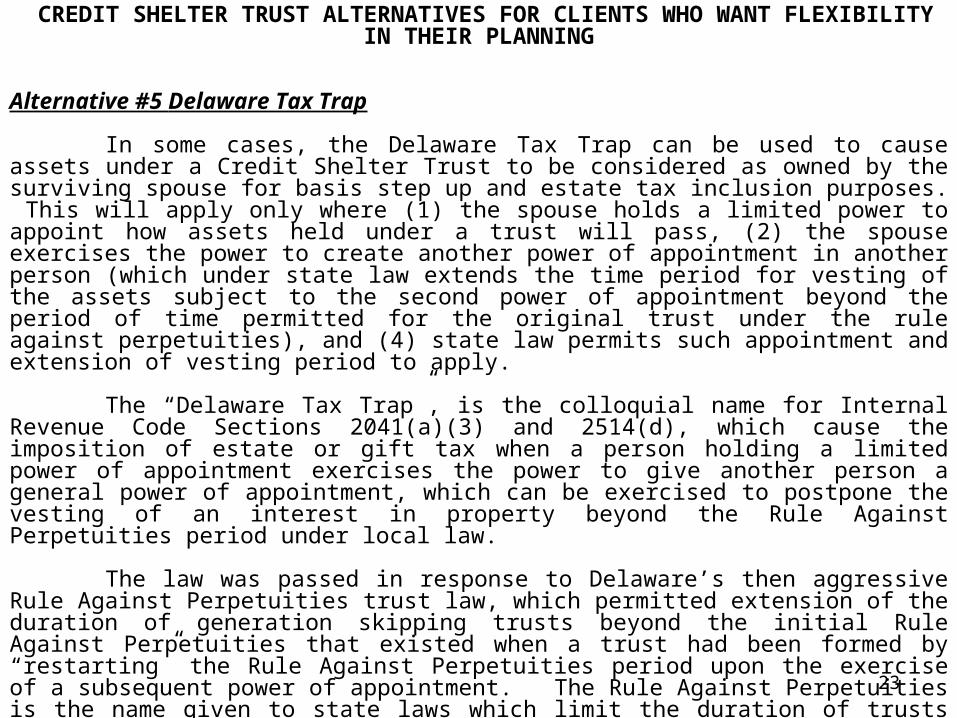

Alternative #5 Delaware Tax Trap

In some cases, the Delaware Tax Trap can be used to cause assets under a Credit Shelter Trust to be considered as owned by the surviving spouse for basis step up and estate tax inclusion purposes. This will apply only where (1) the spouse holds a limited power to appoint how assets held under a trust will pass, (2) the spouse exercises the power to create another power of appointment in another person (which under state law extends the time period for vesting of the assets subject to the second power of appointment beyond the period of time permitted for the original trust under the rule against perpetuities), and (4) state law permits such appointment and extension of vesting period to apply.

The “Delaware Tax Trap”, is the colloquial name for Internal Revenue Code Sections 2041(a)(3) and 2514(d), which cause the imposition of estate or gift tax when a person holding a limited power of appointment exercises the power to give another person a general power of appointment, which can be exercised to postpone the vesting of an interest in property beyond the Rule Against Perpetuities period under local law.

The law was passed in response to Delaware’s then aggressive Rule Against Perpetuities trust law, which permitted extension of the duration of generation skipping trusts beyond the initial Rule Against Perpetuities that existed when a trust had been formed by “restarting” the Rule Against Perpetuities period upon the exercise of a subsequent power of appointment. The Rule Against Perpetuities is the name given to state laws which limit the duration of trusts established under a will or trust.1 Under the common law, this required that non-charitable trusts terminate within 21 years after the death of every person named as a beneficiary in the original document upon formation.

4.Assuming the desire for use of a Credit Shelter Trust, evaluate resituate assets to facilitate full funding of the Credit Shelter Trust on first death.

24

The Planner's Idea and Checklist for Helping Clients During the 2011 and 2012, $5 Million Bump Years

25

Bob Burke’s Rule: For every complex situation there is a

simple answer…and it is the wrong answer. Complex problems almost always

call for complex solutions.

Determining How To Best Allocate Assets As Between A Married CouplePart I

SEE NEXT PAGE FOR SECOND TIER PLANNING

A COMMON SOLUTION - to use a limited partnership or similar mechanisms and have no assets directly in the "high risk" spouse's trust, half to two-thirds of the assets held as tenants by the entireties, and half to two-thirds of assets directly in the "low risk" spouse's trust.

General Rules:-Typically want each trust funded with at least $3,500,000 worth of assets on death for estate tax planning.

-May be funded from ½ of tenancy by entireties assets via disclaimer and probate or by life insurance/pension/IRA assets.

Copyright © 2011 Gassman, Bates & Associates, P.A.26

Determining How To Best Allocate Assets As Between A Married CouplePart IISubsidiary Entity Techniques:

Limited partnerships can be used to facilitate discounts, for estate tax purposes, and forcharging order protection.Limited partnerships and LLCs can also be used to provide "firewall protection" from activitiesor properties owned.

A COMMON SOLUTION - to use a limited partnership or similar mechanisms and have no assets directly in the "high risk" spouse's trust, half to two-thirds of the assets held as tenants by the entireties, and half to two-thirds of assets directly in the "low risk" spouse's trust.

Copyright © 2011 Gassman, Bates & Associates, P.A.27

ESTATE AND ASSET PROTECTION PLANNING FOR THE SINGLE PROFESSIONAL

IRA AccountAutomobile

401k/Pension Account

Annuity Contracts

Life Insurance

Can deposit wages into a wage account

97% 97%

Furniture, equipment, accounts receivable

Long Term Lease

Wages

SINGLE (NON-MARRIED)

INDIVIDUAL

PROFESSIONAL PRACTICE

CORPORATION

LIVING TRUST

HOMESTEAD

PROFESSIONAL BUILDING AND/OR EQUIPMENT LLC

WAGE ACCOUNT?

3%3%

1% 99%

Brokerage Accounts

Building 1 Lot 1 Condo 1

S Corporation Stock

SECURITIES FLP

GIFTING TRUST

REAL ESTATE FLP

LLC LLCLLC

OFFSHORE ASSET

PROTECTION TRUST

ALASKA ASSET PROTECTION

TRUST

Child or Children

529 Plans

UGMA Accounts (Subject to Creditors of the Child)

Child's or Children's Automobiles?(Who signed for driving priviledges?)

Copyright © 2011 Gassman, Bates & Associates, P.A.28

a. Are there $5 million worth of assets under each spouse’s revocable trust?

b. To the extent that a spouse has less than $5 million of assets under his or her revocable trust, consider having assets being held jointly by the spouses that can be disclaimed to the Credit Shelter Trust. This will generally be one-half of assets held jointly by the spouses, except for 100% of joint accounts that were funded solely by the first dying spouse?c. Consider using a joint trust, with each spouse having a full general power of appointment to facilitate funding of a Credit Shelter Trust with all joint trust assets on the first death. See Private Letter Rulings 200101021 and 200210051.d. Consider adding term or other life insurance to make best use of first dying spouse’s allowance, if high income earner or inheritor situation indicates need for full funding.

The Planner's Idea and Checklist for Helping Clients During the 2011 and 2012, $5 Million Bump Years

29

30

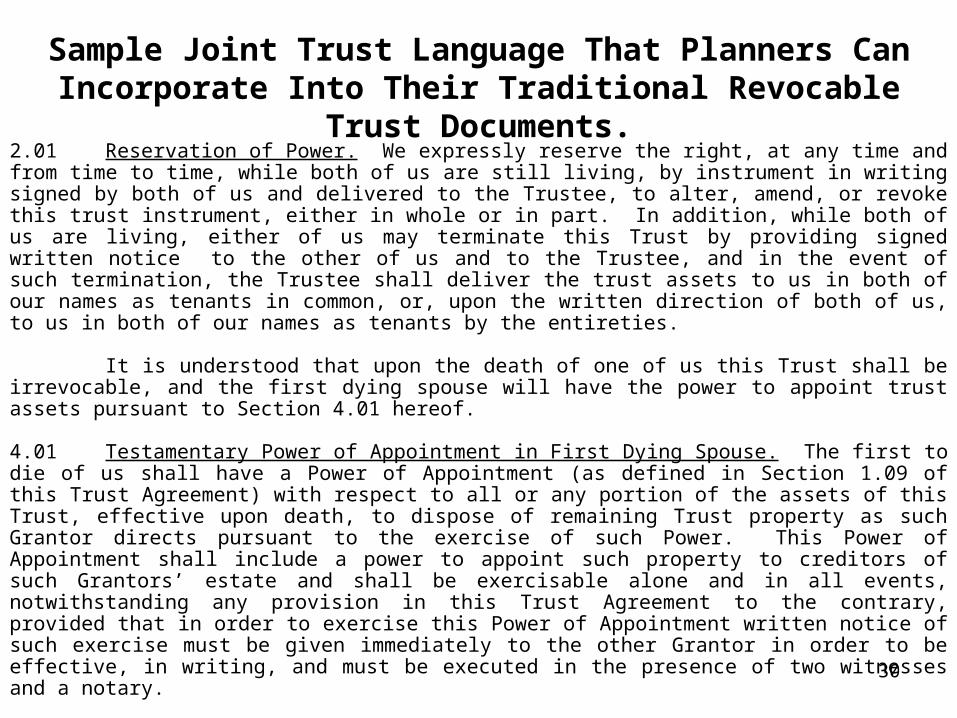

Sample Joint Trust Language That Planners Can Incorporate Into Their Traditional Revocable Trust Documents.

2.01 Reservation of Power. We expressly reserve the right, at any time and from time to time, while both of us are still living, by instrument in writing signed by both of us and delivered to the Trustee, to alter, amend, or revoke this trust instrument, either in whole or in part. In addition, while both of us are living, either of us may terminate this Trust by providing signed written notice to the other of us and to the Trustee, and in the event of such termination, the Trustee shall deliver the trust assets to us in both of our names as tenants in common, or, upon the written direction of both of us, to us in both of our names as tenants by the entireties.

It is understood that upon the death of one of us this Trust shall be irrevocable, and the first dying spouse will have the power to appoint trust assets pursuant to Section 4.01 hereof.

4.01 Testamentary Power of Appointment in First Dying Spouse. The first to die of us shall have a Power of Appointment (as defined in Section 1.09 of this Trust Agreement) with respect to all or any portion of the assets of this Trust, effective upon death, to dispose of remaining Trust property as such Grantor directs pursuant to the exercise of such Power. This Power of Appointment shall include a power to appoint such property to creditors of such Grantors’ estate and shall be exercisable alone and in all events, notwithstanding any provision in this Trust Agreement to the contrary, provided that in order to exercise this Power of Appointment written notice of such exercise must be given immediately to the other Grantor in order to be effective, in writing, and must be executed in the presence of two witnesses and a notary.

e. Wealthier spouse may give less wealthy spouse a power to appoint sufficient assets under wealthier spouse’s revocable trust, exercisable on death of less wealthy spouse, to fund a Credit Shelter Trust with assets held under wealthier surviving spouse’s own revocable trust. See Private Letter Ruling 200403094.

31

The Planner's Idea and Checklist for Helping Clients During the 2011 and 2012, $5 Million Bump Years

32

Sample Language To Fund a Credit Shelter Trust at Less Wealthier Spouse’s Death with Assets Held Under Wealthier

Spouse’s Living TrustSAMPLE LANGUAGE FOR WEALTHIER SPOUSE’S LIVING TRUST:

Lifetime Power of Appointment in Mary L. Smith. During my lifetime, and so long as I am married to JOHN B. SMITH, MARY L. SMITH shall have a lifetime testamentary power of appointment, exercisable by a written instrument executed by her in the presence of two witnesses and a notary, to be effective upon her death, to appoint an amount in value of Trust assets equal to the excess of (a) the maximum amount that she may pass without being subject to federal estate tax at the time of her death, and (b) the amount of her personal assets and the value of any other assets includable in her gross estate, less any assets includable in her gross estate which qualify for the federal estate tax marital deduction, but in no event more than $2,500,000. I recognize that the maximum amount that she would be able to pass free of estate tax will be based upon the then applicable estate tax exemption amount, less lifetime taxable gifts that she will have made. For example, if MARY L. SMITH survives me and has $400,000 in personal assets, we have a $1,000,000 joint with right of survivorship account, and upon her death I therefore own the entire joint account outright and inherit $25,000 of the $400,000 in assets that she has under her Will, then if at the time of her death the federal estate tax exemption is $2,500,000 but she has made a $500,000 taxable gift during her lifetime, then the amount subject to this power will be based upon $2,500,000 minus the $500,000 lifetime gift minus $375,000 for a total of $1,625,000. All valuation shall be based upon date of death values. Such power of appointment may be exercisable by her only under a Last Will and Testament or applicable Codicil duly admitted to probate in a court of competent jurisdiction.

SAMPLE LANGUAGE FOR LESS WEALTHIER SPOUSE’S LAST WILL AND TESTAMENT:

Exercise of Testamentary Power of Appointment. I recognize that I have a testamentary power of appointment provided to me under the JOHN B. SMITH REVOCABLE TRUST being amended and restated this date, and in the event that I predecease JOHN B. SMITH, I hereby exercise such testamentary power of appointment, but only to the extent that property under the JOHN B. SMITH REVOCABLE TRUST that does not exceed the maximum amount that can pass free of estate tax in the matter of my estate after taking into consideration any and all marital deduction devise, and in no event exceeding the amount of $2,500,000.

The amount so devised shall be devised to the MARY L. SMITH LIVING TRUST, with the residue of my estate as set forth in Section 4.1 of this Last Will and Testament, in order to facilitate funding of the SMITH FAMILY TRUST with the maximum amount that can pass estate tax free to benefit my said husband without being subject to federal estate tax in his estate.