helping you to reduce stress and build a happier and more financially-secure future

TRANSCRIPT

w w w . e d u c a t o r s f i n a n c i a l g r o u p . c a

THE KEYS TO FINANCIAL WELLNESS

Presented by: Karen Hubbard, CFP Moderated by: Bruce Sellery

The Keys to Financial Wellness

Meet your moderator

Founder of Moolala (a personal finance training company)

Bruce Sellery

The Keys to Financial Wellness

Meet your subject matter expert

Financial Planner – CFPEducators Financial Group

Karen Hubbard

The Keys to Financial Wellness

About the webinar

Will I be able to get a copy of the slides after the webinar?

Is this webinar being taped so it can be

viewed afterwards?

The Keys to Financial Wellness

STRESSED?

Does the topic of money make you

The Keys to Financial Wellness

Our financial wellness agenda

• What is stress?• How to deal with the top three

financial stress factors:- High debt levels- Low savings- Lack of financial literacy

• Q&A/wrap up

The Keys to Financial Wellness

Ice breaker

What isSTRESS

The Keys to Financial Wellness

The Keys to Financial Wellness

Common symptoms of stress

• Increased anxiety• Extreme mood swings (irritability)• Inability to cope (feeling loss of control)• Chronic fatigue (even after excessive sleep)• Inaction (due to feeling so overwhelmed)

The Keys to Financial Wellness

There are several contributing factors, however we’re going to focus on the top three:

1. High debt levels

2. Low savings

3. Lack of financial literacy

What causes financial stress?

The Keys to Financial Wellness

1. Communicate: Open the dialogue about money with your spouse and your Educators financial specialist.

2. Plan: Get your head out of sand and come up with a plan to get a handle on your money.

3. Care: Take care of your physical and mental health.

The keys to financial wellness

The Keys to Financial Wellness

HighDEBTLevels

How to deal with:

The Keys to Financial Wellness

The Keys to Financial Wellness

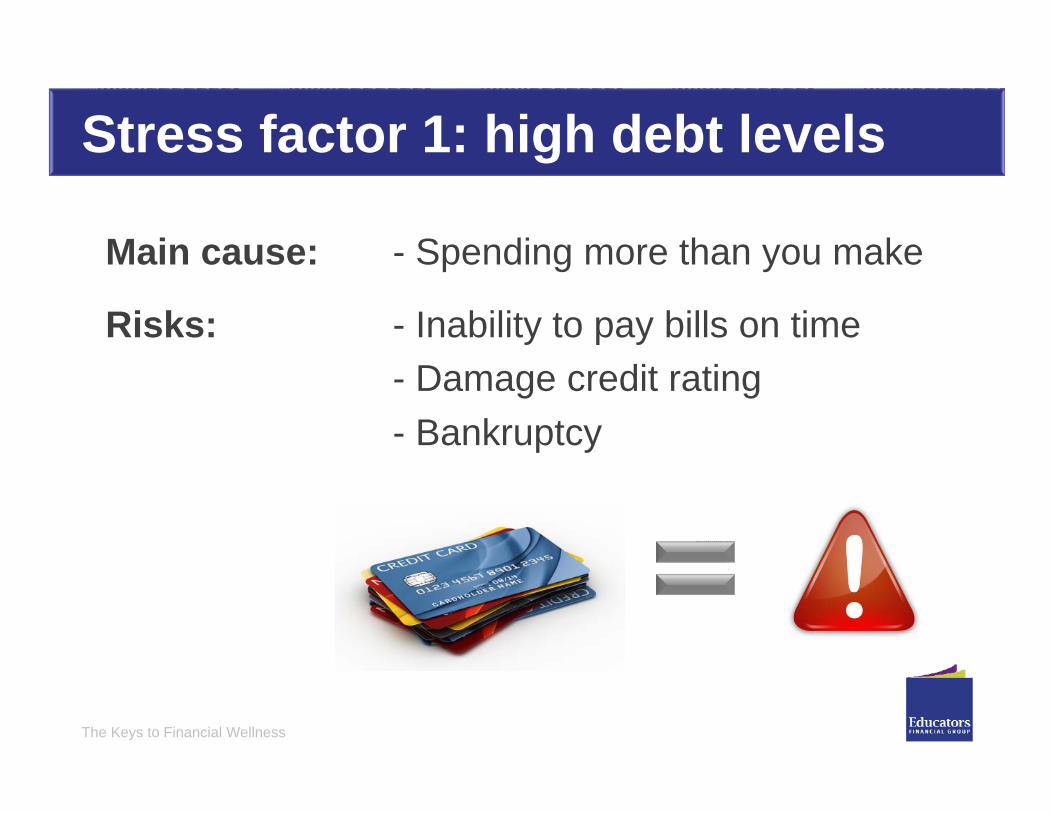

Main cause: - Spending more than you make

Risks: - Inability to pay bills on time- Damage credit rating- Bankruptcy

Stress factor 1: high debt levels

The Keys to Financial Wellness

Types of debt: the pros and cons

Vehicle Pro Con

Personal Loan • Set payment term• Can be paid off anytime

• Higher rate of interest

Credit Card• Low minimum payment• Revolving limit

• High interest rate• Can have debt for life

Line Of Credit• Revolving limit• Can be paid off anytime• Like a low-interest

credit card

• No set payment term• Can have debt for life

Mortgage• Set payment term• Lowest borrowing rate

• Pre-payment restrictions• Long amortization• Not easily refinanced

The Keys to Financial Wellness

Stop paying high interest rates

=The average department store credit card charges 20%

The average bank credit card interest rate = 14%

Educators Financial Group 5-year mortgage rate = 3.04%

Consolidating high-interest debt into your mortgage can help you become debt-free faster.

The average line of credit interest rate = 8%

The Keys to Financial Wellness

Chart out your debt strategy

Strategy VISA Loan PLC Consolidation

Balance $10,000 $25,000 $15,000 $50,000

MonthlyPayment

$300* $506.91 $470.05 $920**

Interest Charged 19% 8% 8% 4%

*Monthly payment is 3% of balance. **Based on an Educators line of credit (in partnership with Teachers’ Credit Union) at a 4% interest rate and paid out in 5 years.

Combined monthly payment: $1276.96 Save: $356.96/mo.

Consolidating the various high interest rate debts above into one lower rate monthly payment has the potential to save you $21,417.60 in interest over the duration**.

The Keys to Financial Wellness

Accelerate your mortgage payments:

Look for more ways to save

*Over the duration of the mortgage – based on a $200,000 mortgage at a 5-year fixed term/25-year amortization period and a 4% rate.

Payment Strategy

Total Mort.Payment

Interest/Time Saved*

(Over life of mortgage)

Slow and steady(Regular)

$1,052.00(per month)

None

Accelerated $526.00(bi-weekly)

$16,849.00(plus 3 years off amortization)

Accelerated +(Add $180)

$706.00(bi-weekly)

$53,826.00(plus 11 years off amortization)

Turbo charged(Add $180 + $5,000 annual lump sum)

$526.00(bi-weekly)

$72,513.00(plus 15 years off amortization)

The Keys to Financial Wellness

Take control – take action

• Stop paying high interest rates• Consolidate high-interest debt if possible• Increase amount/frequency of payment(s)• Round up payment to nearest $100• List all balances from highest to lowest

- Record interest rates for each debt- Pay the highest rate with the lowest balance first

The Keys to Financial Wellness

You can do this by:• Always paying at least the minimum payment

on time

• Never exceeding your credit card limit

• Minimizing the number of credit applications you make

• Use your card regularly

Protect your credit rating

Keep tabs of your credit rating online:www.equifax.ca and www.transunion.ca

The Keys to Financial Wellness

sessionThe Keys to Financial Wellness

The Keys to Financial Wellness

Stress factor #2

savings

How to deal with:

The Keys to Financial Wellness

The Keys to Financial Wellness

Main causes: - Other financial commitments(pension contributions, day-to-day living expenses)

- No budget in place- Frivolous spending- Low cash flow

Risks: - No emergency fund- Potential to keep using credit- Possible pension income gap

Stress factor 2: low savings

The Keys to Financial Wellness

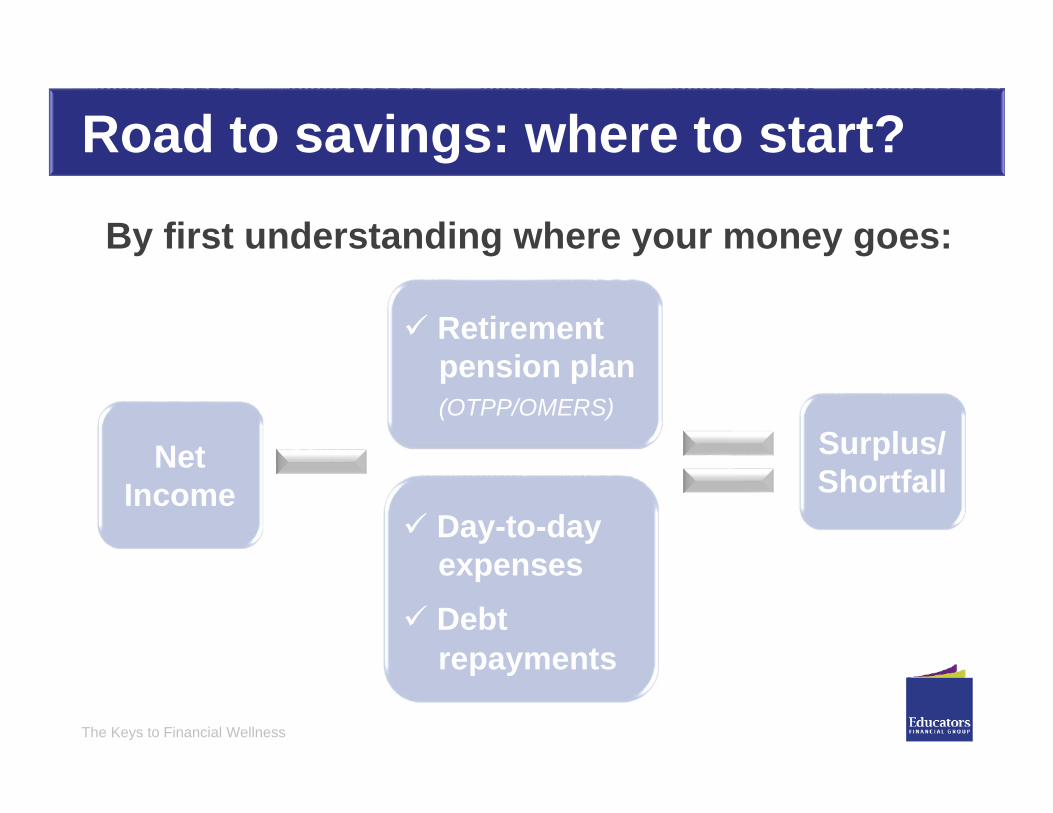

By first understanding where your money goes:

Road to savings: where to start?

Net Income

Day-to-dayexpenses

Debt repayments

Surplus/Shortfall

Retirement pension plan(OTPP/OMERS)

The Keys to Financial Wellness

Start by penciling in your budgetMonthly Net Income(after pension contributions) $3,000

Monthly ExpensesMortgage/Rent $1,220Food $500Cable/Internet $85Insurance $150Student Loan $200Entertainment $250Misc. $300Income Minus Total Expenses $2,705

Use our Go Figure calculator online to figure out your budget: www.educatorsfinancialgroup.ca

The Keys to Financial Wellness

Set your savings goals

Do you want to:• Create an emergency fund?• Travel a few times a year?• Take advantage of a Deferred Salary Plan?• Purchase a home/pay down your mortgage?• Save for children’s

education?

The Keys to Financial Wellness

Putting away just $100 a month with 5% growth:

Start saving then watch it grow

Compounding Amount Actual Monthly Contributions

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034$0K

$10K

$20K

$30K

$40K

$50K

$60K

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034$0K

$10K

$20K

$30K

$40K

$50K

$60K

$6,000$6,808

$13,200$17,503

$58,801

$30,000

Source: Go Figure calculations based on $100/month contributions at 5% growth.

The Keys to Financial Wellness

Don’t cut – cut back:

Think before you buy:

Spend smart:

Reduce spending

Set yourself limitations – reduce trips to mall/online spending

Ask yourself “why?” – do you really need this or simply want it?

Spend in positive ways that contribute to improving your health and wealth

The Keys to Financial Wellness

sessionThe Keys to Financial Wellness

The Keys to Financial Wellness

How to improve your

FINANCIAL

The Keys to Financial Wellness

The Keys to Financial Wellness

Stress factor 3: lack of financial literacy

Did you know…According to the Canadian Council for Learning, only 50% of adult Canadians are financially literate.

The Keys to Financial Wellness

Learn about educator-specific challenges

Education-specific item Learn how to…

OTPP / OMERS pension• Minimize potential income gaps• Navigate pension income

fluctuations• Manage cash flow challenges

Gratuities • Minimize tax implications

Summer time • Optimize cash flow (i.e. Summer Freedom mortgage)

Deferred Salary Plan • Develop a plan for DSP while minimizing the income pinch

The Keys to Financial Wellness

Tap into free resources such as…

• Workshops and webinars• Our quarterly newsletter, Insights• Online through The Learning Centre• Regular eNews – our email communications• Free one-on-one financial

planning sessions

The Keys to Financial Wellness

sessionThe Keys to Financial Wellness

The Keys to Financial Wellness

Create your budget (i.e. use our Go Figure online tool)

Determine your financial goals

Take advantage of our free educational resources (i.e. sign up for The Learning Centre and eNews)

Call us/visit us online: 1.800.263.9541,www.educa to rs f i nanc ia lg roup .ca

Homework

The Keys to Financial Wellness

1. Communicate: Open up the dialogue about money with your spouse and your Educators financial specialist.

2. Plan: Get your head out of sand and come up with a plan to get a handle on your money.

3. Care: Take care of your physical and mental health.

The Keys to Financial Wellness

The Keys to Financial Wellness

DisclaimerThe information provided is general in nature and is provided with the understanding that it may not be

relied upon as, nor considered to be, the rendering of tax, legal, accounting or professional advice.

Attendees and readers should consult a financial planner and their own accountant and/or legal advisor

for specific advice related to their circumstances. Educators Financial Group will not be held

responsible or liable for any losses, costs, damages or expenses incurred by reason of reliance as a

result of the aforementioned information. The information presented was obtained from sources that are

believed to be reliable. However, Educators Financial Group can not guarantee their completeness or

accuracy. Commissions, trailing commissions, management fees and expenses may all be associated

with mutual funds. Please read the simplified prospectus before investing. Mutual funds are not

guaranteed, their value changes frequently and past performance may not be repeated.

The Keys to Financial Wellness