heeding daedalus: optimal inflation and the zero … · heeding daedalus: optimal inflation and the...

TRANSCRIPT

FEDERAL RESERVE BANK OF SAN FRANCISCO

WORKING PAPER SERIES

Heeding Daedalus: Optimal Inflation and the Zero Lower Bound

John C. Williams Federal Reserve Bank of San Francisco

October 2009

Working Paper 2009-23 http://www.frbsf.org/publications/economics/papers/2009/wp09-23bk.pdf

The views in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Federal Reserve Bank of San Francisco or the Board of Governors of the Federal Reserve System.

Heeding Daedalus:

Optimal Inflation and the Zero Lower Bound

John C. Williams∗

Federal Reserve Bank of San Francisco

October 12, 2009

Abstract

This paper reexamines the implications of the zero lower bound on interest rates formonetary policy and the optimal choice of steady-state inflation in light of the experienceof the recent global recession. There are two main findings. First, the zero lower bound didnot materially contribute to the sharp declines in output in the United States and manyother economies through the end of 2008, but it is a significant factor slowing recovery.Model simulations imply that an additional 4 percentage points of rate cuts would have keptthe unemployment rate from rising as much as it has and would bring the unemploymentand inflation rates more quickly to steady-state values, but the zero bound precludes theseactions. This inability to lower interest rates comes at the cost of $1.7 trillion of foregoneoutput over four years. Second, if recent events are a harbinger of a significantly moreadverse macroeconomic climate than experienced over the preceding two decades, then a 2percent steady-state inflation rate may provide an inadequate buffer to keep the zero boundfrom having noticeable deleterious effects on the macroeconomy assuming the central bankfollows the standard Taylor Rule. In such an adverse environment, stronger systematiccountercyclical fiscal policy and/or alternative monetary policy strategies can mitigate theharmful effects of the zero bound with a 2 percent inflation target. However, even with suchpolicies, an inflation target of 1 percent or lower could entail significant costs in terms ofmacroeconomic volatility.

Keywords: Liquidity trap, monetary policy, fiscal policy.

∗This draft has benefitted greatly from comments by Richard Dennis, Ben Friedman, David Romer, Justin

Wolfers, Michael Woodford, and other participants at the Brookings Papers on Economic Activity conference,

September 10-11, 2009. I thank Justin Weidner for excellent research assistance. The opinions expressed

are those of the author and do not necessarily reflect views of the Federal Reserve Bank of San Francisco,

the Board of Governors of the Federal Reserve System, or anyone else in the Federal Reserve System.

Correspondence: Federal Reserve Bank of San Francisco, 101 Market Street, San Francisco, CA 94105, Tel.:

(415) 974-2240, e-mail: [email protected].

Icarus, my son, I charge you to keep at a moderate height, for if you fly too low

the damp will clog your wings, and if too high the heat will melt them.

Daedalus’ warning

1 Introduction

Japan’s sustained deflation and near-zero short-term interest rates beginning in the 1990s

ignited an outpouring of research on the implications of the zero lower bound (ZLB) on

nominal interest rates for monetary policy and the macroeconomy. In the presence of

nominal rigidities, the ZLB will at times constrain the central bank’s ability to reduce

nominal interest rates in response to negative shocks to the economy. This inability to

reduce real interest rates as low as desired impairs the ability of monetary policy to stabilize

output and inflation. The quantitative importance of the ZLB depends on the frequency

and degree to which the constraint binds, a key determinant of which is the steady-state,

or “target,” inflation rate. If the steady-state inflation rate is sufficiently high, the ZLB

will rarely impinge on monetary policy and the macroeconomy. With a sufficiently low

steady-state inflation rate, however, the ZLB may have more deleterious effects. All else

equal, the presence of the ZLB argues for a higher steady-state inflation rate. Of course, not

all else is equal. Since Bailey (1956), economists have identified and studied other sources

of distortions related to inflation besides the ZLB.

Balancing these opposing influences on the choice of the optimal inflation rate, central

banks around the globe have sought to heed Daedalus’ advice by choosing an inflation goal

neither too low nor too high. In practice, many central banks have articulated inflation

goals centered on 2 to 3 percent (Kuttner 2004). Simulations of macroeconomic models

where monetary policy follows a version of the Taylor (1993) rule indicate that an inflation

target of 2 percent will entail relatively frequent episodes of the ZLB acting as a binding

constraint on monetary policy (Reifschneider and Williams 2000, Coenen, Orphanides and

Wieland 2004; and Billi 2008). Nonetheless, these simulations predict that with an inflation

target as low as 2 percent, the deleterious effects of the ZLB on macroeconomic volatility

1

would be relatively modest because the magnitude and duration of the constraints on policy

actions are relatively mild. Only with inflation targets of 1 percent or lower does the ZLB

engender significantly higher variability of output and inflation in these simulations. In

summary, a 2 percent inflation target was found to be an adequate buffer from the point of

view of the ZLB.

The economic tumult of the past two years, with short-term rates near zero in most

major industrial economies, has challenged the conclusion that a 2 percent inflation target

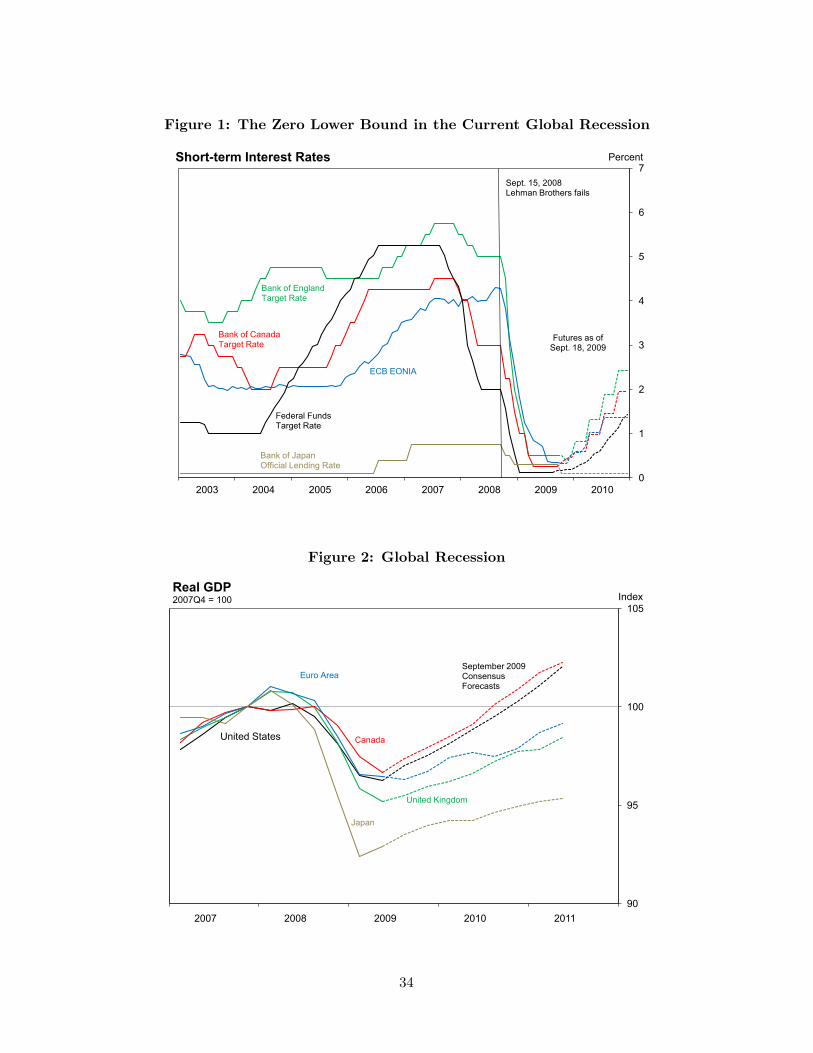

is sufficiently high to avoid substantial costs from the ZLB. As shown in Figure 1, the

global financial crisis and recession has driven many major central banks to cut short-term

interest rates effectively to zero. Other central banks constrained by the ZLB include the

Swedish Riksbank and the Swiss National Bank. Despite these monetary policy actions and

considerable stimulus from fiscal policy, these economies are suffering their worst downturns

in memory. Figure 2 shows the actual and forecasted paths for real GDP for major industrial

economies. In addition, fears of deflation have intensified as falling commodity prices and

growing slack put downward pressure on prices. As shown in Figure 3, overall consumer

price index (CPI) inflation rates have fallen sharply in all major economies. Much of this

decline is due to commodity prices, especially energy prices, but core measures of CPI

inflation have come down in these economies over the past year as well.

Given these conditions, a strong case can be made for the desirability of additional

monetary stimulus in the United States and in many other countries. But, with rates already

effectively at zero, this is not an option, at least in terms of conventional monetary actions.

Several central banks have therefore implemented unconventional monetary actions, such as

changes in the composition and size of the asset side of their balance sheets. But, the short-

and long-term effects of these unconventional monetary policies remain highly uncertain

and such policies are at best imperfect substitutes for standard interest rate cuts.

This paper examines the effects of the ZLB on the current recession and reevaluates

the expected future effects associated with the ZLB and the optimal inflation rate in light

of new information and research.1 There are two main findings. First, the ZLB did not1I do not examine issues related to multiple equilibria studied by Benhabib et al (2001). Instead, as in

2

materially contribute to the sharp declines in output in the United States and many other

economies through the end of 2008, but it is a significant factor slowing recovery. Model

simulations imply that an additional 4 percentage points of rate cuts would have kept the

unemployment rate from rising as much as it has and would bring the unemployment and

inflation rates more quickly to steady-state values, but the ZLB precludes these actions.

This inability to lower interest rates comes at the cost of $1.7 trillion of foregone output

over four years. Second, if recent events are a harbinger of a significantly more adverse

macroeconomic climate than experienced over the preceding two decades, then a 2 percent

steady-state inflation rate may provide an inadequate buffer to keep the ZLB from having

noticeable deleterious effects on the macroeconomy, assuming the central bank follows the

standard Taylor Rule. In such an adverse environment, stronger systematic countercyclical

fiscal policy and/or alternative monetary policy strategies can mitigate the harmful effects

of the ZLB with a 2 percent inflation target. However, even with such policies, an inflation

target of 1 percent or lower could entail significant costs in terms of macroeconomic volatility.

The paper is organized as follows. Section II examines the effects of the ZLB on the

U.S. economy during the current episode. Section III reexamines the assumptions and

results from past calculations of the macroeconomic effects of the ZLB under the Taylor

Rule. Section IV evaluates alternative monetary and fiscal policies designed to mitigate the

effects of the ZLB. Section V concludes.

2 Lessons from the Current Recession

The ongoing global recession provides compelling proof that the ZLB can be a significant

constraint on monetary policy with potentially enormous macroeconomic repercussions.

This section investigates two questions regarding the role of the ZLB in the current episode.

First, how should one interpret the widespread occurrence of central banks lowering rates

to near zero? Second, what are the consequences of the ZLB in terms of the depth of the

recession and the speed of recovery?

Evans et al (2008), I assume that discretionary fiscal policy will intervene to assure that a unique steady-stateexists and the economy tends back to that steady state.

3

The fact that central banks have been constrained by the ZLB should not not surprising;

in fact, one of the three main “lessons” of Reifschneider and Williams (2000) was that

central banks that pursue inflation goals of around 2 percent would encounter the ZLB

relatively frequently.2 For example, Reifschneider and Williams (2002) find that with a 2

percent inflation target, roughly in line with the practices of many major central banks, a

calibrated version of the Taylor rule (1993) hits the ZLB about 10 percent of the time in

simulations of the Federal Reserve Board’s FRB/US macroeconometric model. Given that

inflation has been centered around 2 percent in the United States since the early 1990s, it

was fully predictable that the ZLB would become an issue–either as a threat, as in 2004, or

as a reality, as it is today.

Indeed, the widespread occurrence of central banks running into the ZLB is evidence

that they have learned a second lesson from research that policymakers should not shy

away from the ZLB, but should instead “embrace” it. A common theme in research on the

ZLB is that when the economy weakens significantly or deflation risks arise, central banks

should act quickly and aggressively to get rates down as soon as possible to maximize the

monetary stimulus in the system when the economy is weakening. “Keeping your powder

dry” is precisely the worst thing to do. Figure 4 shows nominal and ex post real rates on

short-term Treasury securities going back to the 1920s. Despite the low rate of inflation and

three recessions, nominal interest rates did not once approach the ZLB back then. That

the ZLB appears to be a greater problem today than in the 1950s and early 1960s, when

inflation was also low, may reflect “better” monetary policy in the more recent period.

Indeed, a comparison of estimated Taylor-type rules covering that period and the more

recent past indicates that short-term interest rates were far less sensitive to movements in

output and inflation during the earlier period (Romer and Romer, 2002). Of course, the2Note that the lower bound does not necessarily equal zero. On one hand, lowering the interest rate

below a small positive value may incur costly disruptions to money and other short-term financing markets.In this case, central banks may choose not to lower rates all the way to zero, making the effective lowerbound a small positive number. On the other hand, a central bank can in principle lower interest rates belowzero by charging interest on reserves. However, there are still limits to how low interest rates can go becausebanks and other agents can choose to hold currency instead, which yields zero interest less an holding costκ, equal to the cost of safely storing and transporting cash). So, instead of a “zero bound,” there is a −κlower bound on short-term interest rates.

4

U.S. economy and financial system were very different 50 years ago so other factors may

also explain the differences in interest rate behavior.

To answer the second question, I conduct counterfactual simulations of the Federal Re-

serve’s FRB/US model where the Federal Reserve is not constrained by the ZLB.3 The

simulations are best thought of as scenarios where the economy entered the current episode

with a higher steady-state inflation rate and therefore the Federal Reserve had a large inter-

est rate buffer to work with. I consider experiments in which the Federal Reserve is able to

lower the funds rate by up to 600 basis points more than it has. For comparison, Rudebusch

(2009) finds that the funds rate would be predicted to fall to about -5 percent based on an

estimated monetary policy rule and FOMC forecasts. Of course, these experiments are not

real policy options available to the Fed. But they allow me to quantify the effects of the

ZLB on the evolution of the U.S. economy.

In evaluating the role played by the ZLB, it is important to get the timing of events

correctly. Private forecasters did not anticipate that the ZLB would be a binding constraint

on monetary policy until very late in 2008. Figure 5 shows the expected path of the fed

funds rate according to the Blue Chip forecasts at various points in 2008 and 2009. At the

beginning of September 2008–right before the failure of Lehman Brothers and the ensuing

panic–forecasters did not expect the funds rate to fall below 2 percent. It was not until

early December 2008, when the full ramifications of the panic became clear, that forecasters

came to anticipate a sustained period of rates below 1 percent and the zero lower bound

clearly came into in play. In fact, the Federal Open Market Committee (FOMC) cut the

target funds rate from 1 percent to a 0 to 1/4 percentage point range on December 16, 2008.

A similar pattern is seen in forecasts of policy rates in other major industrial economies,

where central banks except for Japan made their final rate cuts later than the FOMC.

The preceding argument is based on evidence from point forecasts, which typically

correspond to modal forecasts. In theory, economic decisions depend on the full distribution3See Brayton et al 1997 for a description of the FRB/US model. In the counterfactual simulations I use

the version of FRB/US with VAR expectations. In the stochastic simulations used to evaluate alternativepolicy rules discussed in Sections III and IV of the paper, I use the version of FRB/US with rationalexpectations.

5

of the forecasts, not just the mode. The possibility that the ZLB could bind in the future

may have introduced significant downward asymmetry in forecast distributions of output

and inflation in late 2008. Such an increase in the tail risk of a severe recession could have

caused households and businesses to curtail spending more than they would have if the

ZLB was not looming on the horizon. Although the evidence is not definitive, forecasts in

late 2008 do not appear to provide much support for such a channel. Based on options on

fed funds futures (see Carlson et al 2005), even as late as early November 2008, market

participants placed only about a 25 percent probability of a target rate equal of 50 basis

points or lower in January 2009. In addition, the distribution of forecasts for real GDP

growth in 2009 from the Survey of Professional Forecasters in the fourth quarter of 2008

does not display obvious signs of asymmetric downside risks.

In summary, the available evidence suggests that through late 2008, that is, until the

ramifications of the financial panic following the failure of Lehman Brothers were recog-

nized, the ZLB was not viewed by forecasters as a binding constraint on policy. Therefore,

it is unlikely that it had a major impact on the economy before that time outside Japan.

Importantly, this is the period in which the economy was contracting most rapidly. Ac-

cording to monthly GDP figures constructed by Macroeconomic Advisors, the period of

sharp declines in real GDP ended in January 2009, with real GDP falling by 2 percent in

December 2008 and 0.7 percent in January 2009. Real GDP was roughly flat from January

through July 2009.

Since early 2009, however, the ZLB has clearly been a constraint on monetary policy

in the United States and abroad. Interestingly, forecasters and market participants expect

the ZLB to be a relatively short-lived problem outside Japan. The dashed lines in Figure

1 show market expectations of overnight interest rates derived from future contracts as of

September 2009. Market participants expect major central banks except for the Bank of

Japan to start raising rates by early 2010. As seen in Figure 5, Blue Chip forecasters have

likewise consistently predicted that the Fed would start raising rates after about a year

of near-zero rates. Even those forecasters in the bottom tail of the interest rate forecast

6

distribution of the Blue Chip panel expect the ZLB to constrain policy for only about a

year and a half. Based on these expectations that central banks will raise rates relatively

soon, one might be tempted to conclude that the effects of the ZLB have been relatively

modest. Arguing against that conclusion is that four quarters is the mean duration in

which the ZLB constrained policy in model simulations with a 2 percent inflation target

reported in Reifschneider and Williams (2000) and that such episodes can inflict costs on

the macroeconomy. Moreover, these forecasts of the future paths of interest rates may prove

to be inaccurate.

I construct the counterfactual simulations based upon a baseline forecast set equal to

the August 2009 Survey of Professional Forecasters (SPF) forecast (Federal Reserve Bank

of Philadelphia, 2009). The baseline forecast for the short-term interest rate, the unemploy-

ment rate, and the core personal consumption price (PCE) index inflation rate are shown in

Figures 6, 7, and 8, respectively.4 The SPF also foresees the unemployment rate remaining

above 7 percent through 2012 and core PCE price inflation remaining below the median

value of the FOMC’s long-run inflation forecasts of 2 percent through 2011. Interestingly,

this forecast has the core inflation rate rising over 2010-11 despite the high rate of unem-

ployment during that period. Such a forecast is consistent with a Phillips curve model of

inflation in which inflation expectations are well anchored around 2 percent (Williams 2009).

Note that these forecasts incorporate the effects of the fiscal stimulus and unconventional

monetary policy actions taken in the United States and abroad.

I consider three alternative paths for the nominal funds rate and examine the resulting

simulated values of the unemployment rate and the core PCE price inflation rate. Based

on the evidence presented above that the ZLB was not a binding constraint until the very

end of 2008, I assume that the additional nominal rate cuts occur in 2009q1. I assume the

entire additional cut occurs in that quarter and that the rates are held below the baseline

values through 2010q4, after which the short-term nominal rate returns to its baseline (SPF4The SPF does not provide a forecast for the fed funds rate, but does provide a forecast for the 3-month

Treasury rate, which I use as a proxy for the fed funds rate. In addition, the SPF does not report quarterlyfigures for 2011 and 2012. I interpolated quarterly figures based on annual figures for those years and themulti-year forecasts for PCE price index inflation.

7

forecast) value. I assume no modifications of the discretionary fiscal policy actions and

unconventional monetary policy actions that are assumed in the baseline forecast. I further

assume that the monetary transmission mechanism works as predicted by the FRB/US

model; that is, the disruptions in financial sectors do not change the marginal effect of

additional rate cuts.5 Admittedly, these are strong assumptions, but I do not see better

alternatives. The results of the simulations are shown in Figures 6, 7, and 8.

I evaluate the simulated outcomes using a standard ad hoc loss function of the form:

L =2012q4∑

t=2009q1

{(πt − 2)2 + λ(ut − u∗)2

}, (1)

where π is the core PCE price index inflation rate, u is the unemployment rate, and u∗ is

the natural rate of unemployment. The inflation goal is assumed to be 2 percent. The SPF

forecast only runs through late 2012, so I cannot extend the calculation of the loss beyond

that point, nor can I use the optimal control techniques developed by Svensson and Tetlow

(2005). Table 1 summarizes the outcomes for the baseline forecast and the alternative policy

simulations. The first four columns of numbers in the table report the central bank losses

for different weights on unemployment stabilization in the loss function, λ, and different

values for the natural rate of unemployment, u∗, assumed in the loss function.6 The values

for the natural rate included in the table cover the range of recent estimates. The median

estimate of the natural rate of unemployment in the most recent SPF survey percent was 5

percent, while the highest reported estimate was 6 percent. Weidner and Williams (2009)

provide evidence suggesting the natural rate of unemployment may currently be as high

as 7 percent. The final two column report the simulated values of the unemployment and

inflation rates at the end of the forecast period (2012q4).

The additional 200 basis points of rate cuts speeds the pace of economic recovery relative

to the baseline forecast, bringing the unemployment rate near 6-1/2 percent by the end of5Some argue that monetary policy may be more or less effective than usual in the current environment,

but there is little empirical evidence to guide any modifications of the model.6Note that I assume the same baseline forecast independent of the value of the natural rate of unem-

ployment used in computing the central bank loss. That is, I treat the natural rate of unemployment asan unobservable variable that underlies the baseline forecast. In particular, I do not consider alternativebaseline forecasts predicated on alternative views of the natural rate of unemployment.

8

Table 1: Effects of Alternative Monetary Policy Paths

LSimulation λ = 0 λ = 1 2012q4 Value

u∗ = 5 u∗ = 6 u∗ = 7 u πBaseline forecast 4.4 248.0 142.0 68.0 7.3 2.02 percentage point lower interest rate 2.5 193.5 103.8 46.1 6.6 2.24 percentage point lower interest rate 1.4 151.0 77.5 36.0 5.9 2.36 percentage point lower interest rate 1.3 120.2 63.0 37.8 5.2 2.5This table reports the central bank losses and the simulated unemployment and inflation ratesin 2012q4 from FRB/US model simulations of alternative monetary policy paths over 2009-2012.The baseline is the August 2009 Survey of Professional Forecasters forecast. The natural rateof unemployment is denoted by u∗. The assumed inflation target is 2 percent.The loss is given by: L =

∑2012q4t=2009q1

{(πt − 2)2 + λ(ut − u∗)2

}

2012. The reduction in slack and the lower exchange value of the dollar cause core price

inflation to rise more quickly back to 2 percent. In fact, core inflation slightly overshoots

2 percent by the end of 2012. As seen in the second row of the table, this policy reduces

the central bank loss function by a considerable amount, for all combinations of parameters

reported in the table. In the baseline forecast, inflation is below target for nearly the entire

forecast period and the unemployment rate is consistently above the natural rate, so the

200 basis points of rate cuts move both objective variables closer to target. Only in the

final few quarters of the simulation do tradeoffs materialize.

The second simulation of 400 basis points of easing relative to baseline is more effective

at bringing the unemployment rate down and inflation closer to the assumed 2 percent

target over most of the forecast period. This policy yields a much lower central bank loss

for all parameter combinations reported in the table. The results are striking. Even when

the sole objective is the stabilization of inflation, an additional 400 basis points of easing is

called for. Similarly, when the central bank cares about stabilizing unemployment around

its natural rate, even with a 7 percent natural rate of unemployment, 400 basis points of

easing reduces the central bank loss. One concern with this policy is that inflation is above

2 percent by the end of 2012 and trending upward. Policy needs to be tightened at some

point to bring inflation back down to 2 percent. Of course, in all cases, the appropriate

path for policy in 2012 and beyond depends on the natural rate of unemployment and the

9

evolution of the economy in later years.

The third simulation of 600 basis points of easing relative to baseline yields mixed

results. It yields a smaller loss over the simulation period as long as the natural rate of

unemployment is below 7 percent. But, it accomplishes this at the cost of an inflation rate

that is 1/2 percent above the assumed target at the end of 2012. Based on these results,

such a sharp reduction in rates would only be beneficial if the natural rate of unemployment

is not much higher than 5 percent and if it were followed by a much sharper increase in

interest rates in 2011 and 2012 than assumed in the simulation.

Based on these results, a compelling case can be made that at least an additional 400

basis points of rate reductions would have been beneficial in terms of stabilizing inflation

around a 2 percent target and the unemployment around its natural rate. The magnitude

of the costs of the ZLB can be measured in terms of the differences in real output between

the baseline forecast and the alternative simulation of an additional 400 basis points of rate

cuts. In that simulation, real GDP averages about 3 percent above the baseline forecast

over 2009-2012 (the unemployment rate averages about 1 percentage point below baseline

over this period). An additional 4 percentage points of monetary stimulus yields a total

increase in output over these four years of about $1.7 trillion. This translates to an increase

in per capita output of a total of about $5500, summing over these four years. The implied

increase in consumption is about 2 percent on average, which translates into total increase

in per capita consumption of about $2600, again summing over the four years. These

calculations abstract from the additional effects on output outside the forecast window. By

any measure, these are sizable losses from the ZLB and much larger than estimates of the

typical cost of business cycles.7

A final caveat regarding these simulations is in order. A notable feature of these al-

ternative scenarios is that they entail sizable negative real interest rates for two years. In

the second alternative scenario of a 400 basis point reduction in interest rates, the real7The current episode, as projected by the SPF forecast, is an outlier in both depth and duration compared

to past post World War II recessions. But, as argued in this paper, the ZLB has played a key role in thisoutcome, a situation that has not occurred since the Great Depression.

10

funds rate averages below -5 percent during 2009 and 2010. As seen in Figure 4, there

have been few peacetime episodes of large sustained negative real interest rates. Although

clearly helpful from the perspective of stimulating the economy, there is the possibility that

such a lengthy period of very negative real interest rates could have harmful unintended

consequences, such as fueling another speculative boom and bust cycle (see, for example,

Taylor 2007).

3 Reexamining the Lessons from Research

These simulations illustrate the large costs associated with the ZLB in the current situation.

If this recession represents a unique, extraordinary incident, it has had no implications for

the choice of inflation goal or design of a policy rule regarding the ZLB. Indeed, a third

“lesson” from Reifschneider and Williams (2000) is that there will be rare instances when

the ZLB is very destructive to the macroeconomy, requiring fiscal or other policies to avoid

a complete economic collapse. The recent episode–characterized by reckless risk taking

on a global scale, poor risk management, lax regulatory oversight, and a massive asset

bubble–may be such a 100-year flood. Alternatively, this episode may have exposed some

cracks in the analysis of the ZLB’s effects on the ability of central banks to achieve their

macroeconomic stabilization goals. In this section, I review key assumptions from the

literature and conduct “stress tests” of past research, applying lessons from the past few

years.

The magnitude of the welfare loss owing to the ZLB depends critically on four factors:

the model of the economy, the steady-state nominal interest rate buffer (equal to the sum

of the steady-state inflation rate, π∗, and the steady-state, or “equilibrium,” real interest

rates, r∗), the nature of the disturbances to the economy, and the monetary and fiscal policy

regime. Recent events have challenged a number of assumptions regarding the structure of

the macro models used in past research on the ZLB. Eventually, new models will emerge

from the experience of the past few years, but for now I am limited to the models that

exist.8 Because the effects of the ZLB depend on the extent of nominal and real frictions8Beyond the need for better models of financial frictions, the global nature of the crisis has important

11

(Coenen 2003) and the full set of shocks buffeting the economy, quantitative research into

the effects of the ZLB is best done with richer models that incorporate such frictions. For

this reason, in this paper, I use the Federal Reserve Board’s FRB/US model for my analysis,

rather than a small-scale stylized model.

One critical aspect of model specification is the assumption that inflation expectations

would remain well anchored. As discussed in Reifschneider and Williams (2000) and Evans

et al (2008), absent anchored inflation expectations, the ZLB could give rise to a calamitous

deflationary spiral with rising rates of deflation sending real interest rates soaring and the

economy into a tailspin. In the event, inflation expectations have been remarkably well

behaved in all major industrial economies. The dashed lines in Figure 3 show consensus

forecasts of overall inflation in several countries. Despite the severity of the downturn,

forecasters expect inflation rates to bounce back up over this year and next. Long-run

inflation expectations in these countries, shown in Figure 9, have also been very stable over

the past several years, despite the large swings in commodity prices and the severe global

recession. Thus far, at least, inflation expectations appear to be well anchored. But, there

remains a risk that inflation expectations could become unmoored, in which case the ZLB

poses a larger threat.

A second key assumption is the steady-state real interest rate, which, along with the

steady-state inflation rate, provides the buffer for monetary policy actions to stabilize the

economy. A worrying development over the past decade is a decline in real interest rates.

The long-run average of the real interest rate–defined to be the nominal federal funds

rate less the PCE price index inflation rate–is about 2-1/2 percent, the figure used by

Reifschneider and Williams (2000). But, the Kalman filter estimate of the equilibrium real

rate of interest has fallen to about 1 percent, as shown in Figure 10. Other time-series based

estimates show similar, or even larger, declines. For example, the trend real interest rate

computed using the Hodrick-Prescott filter (with smoothing parameter of 1600) is around

zero in the second quarter of 2009.

implications for the effects of the ZLB and the ability of monetary policy to stabilize the economy (Bodensteinet al 2009).

12

As seen in Figure 10, the decline in the Kalman filter estimate of the equilibrium real

interest rate is associated with the recent severe downturn and may prove to be an over-

reaction to the deep recession. This conclusion receives some support from data from

inflation-indexed Treasury securities. Evidently, investors expect real interest rates to re-

main low over the next five years, but to be closer to historically normal levels thereafter.

Nonetheless, given the massive loss in wealth here and abroad and the resulting increase in

private saving, there is a risk that the steady-state real interest rate will remain low for some

time (Glick and Lansing, 2009). Based on this evidence, a reasonable point estimate of the

steady-state real fed funds rate is about 2-1/2 percent, but there is a real risk that it could

be as low as 1 percent. Of course, the steady-state real rate could be higher than 2-1/2

percent, possibly owing to large fiscal deficits in the United States and abroad (Laubach

2009). In that case, the effects of the ZLB would be correspondingly muted.

The third key assumption is the nature of the disturbances to the economy. Because the

ZLB affects events in the lower tail of the distribution of interest rates, the distribution of

the shocks is a critical factor determining the effects of the ZLB. Reifschneider and Williams

(2000, 2002) based their analysis on the covariance of estimated disturbances from the mid-

1960s through the 1990s. Other research is based on disturbances from the period of the

Great Moderation from the early 1980s on (Coenen, Orphanides, and Wieland 2004; Adam

and Billi 2006; Williams 2006). Recent events hint that what were once thought to be

negative “tail” events may occur frequently and that the period of the Great Moderation

may provide an overly optimistic view of the future macroeconomic landscape. Given the

limited number of observations since the start of the financial crisis, it is not yet possible

to ascertain whether these events represent a sustained break from the past behavior of

disturbances.

Given the great deal of uncertainty–much of it difficult or even impossible to quantify–

regarding the future economic environment, I take a minimax approach to evaluating poli-

cies. Specifically, I look for policies that perform well in very adverse or “worst-case” sce-

narios as well as in the baseline scenario. I take the baseline scenario to be a steady-state

13

real interest rate of 2-1/2 percent and disturbances drawn from a joint normal distribution

based on model disturbances from 1968-2002. I consider alternative adverse scenarios char-

acterized by a steady-state real interest rate of 1 percent and disturbances drawn from more

adverse distributions. Of course, these two sources of uncertainty represent only a slice of

the spectrum of uncertainty relevant for the ZLB. By taking worst cases from these two

sources, the aim is provide insurance against a wide variety of other forms of uncertainty,

including model misspecification, unanchored inflation expectations, etc..

I follow the simulation methodology of Reifschneider and Williams (2000) with two

relatively minor modifications. First, the simulation results reported here are based on a

more recent vintage of the FRB/US model from 2004. Second, following Orphanides et

al (2000) and Reifschneider and Williams (2002), I assume that the output gap included

in the monetary policy rule is subject to exogenous, serially-correlated mismeasurement.

The estimates of the simulated moments are based on two sets of stochastic simulations,

lasting a total of 25,000 years of simulated data.9 The use of such extremely long simulations

provides reasonably accurate estimates of model-implied moments, effectively eliminates the

effects of initial conditions, and implies that rare events occur in the simulations. Finally, I

assume that automatic stabilizers and other endogenous responses of fiscal variables behave

as usual, but that discretionary fiscal policy is not used except in extreme downturns.

In the following, unless otherwise indicated, monetary policy is assumed to follow a

Taylor-type policy rule of the form:

it = max {0, r∗t + πt + 0.5(πt − π∗) + φyt} , (2)

where it is the nominal interest rate, r∗t is the steady-state real interest rate, π is the four-

quarter percent change in the PCE price index, π∗ is the inflation target, and yt is the

output gap. 10 Following Orphanides and Williams (2002), I refer to the specification with

φ = 0.5 as the “Classic” Taylor (1993) rule and other specifications as “Taylor-type” rules.9In the simulations using disturbances following the t distribution, I conduct twice the normal number

of simulations.10I have included an upward bias in the notional inflation target in the policy rule that is needed for the

inflation rate to equal the true target level. As discussed in Reifschneider and Williams (2002) and Coenen,Orphanides, and Wieland (2004), the asymmetric nature of the ZLB implies that the inflation rate will onaverage be lower than the inflation target in the rule. The magnitude of this upward bias is larger, the more

14

The simulated outcomes are evaluated using a central bank loss function (that slightly

differs from that used earlier)of the form:

L = E{(π − π∗)2 + y2 + 0.25 ∗ (i− i∗)2

}, (3)

where π is the overall PCE price index inflation rate, i∗ = π∗ + r∗ is the unconditional

mean of the nominal short-term interest rate, and E denotes the unconditional expectation.

Note that I consider only the costs of inflation variability and not the costs of steady-state

inflation, on the grounds that our understanding of the costs of steady-state inflation is

very limited.11 Thus, I stop short of finding optimal inflation targets. I return to the issue

of the costs of steady-state inflation briefly in the conclusion.

The upper panel of Table 2 reports the simulated outcomes under the classic Taylor

rule assuming the shocks are drawn using a normal distribution from the covariance matrix

computed from the full sample of disturbances (1968-2002). The first two columns report

the steady-state inflation rates corresponding to alternative values of the steady-state real

interest rate, r∗. In terms of the model simulations, the key statistic is the nominal interest

rate buffer, which equals the sum of the steady-state inflation rate, π∗, and the steady-state

real interest rate, r∗. In the baseline scenario, the steady-state real interest rate is assumed

to be 2-1/2 percent. For this case, the numbers indicated in the first column of the table

correspond to the values of the steady-state inflation target. In the case of a steady-state

real interest rate of 1 percent, the numbers in the second column of the table correspond

to the values of the steady-state inflation target. The third and fourth columns report the

share of time that the nominal federal funds rate is below 0.1 and 1 percentage points,

respectively. The fifth column reports the share of the time that the output gap is below

-4 percent, representing a major recession of the type that has occurred in 1958, 1975,

1982-83, and 2009. For comparison, over 1955q1-2009q2 about 6 percent of the time, the

CBO estimate of the output gap was below -4 percent. The sixth through ninth columns

the ZLB constrains policy. I correct for this downward bias by adjusting the inflation target in the policyrule.

11Alternatively, this approach can be justified by assuming that firms increase prices at the steady-stateinflation rate without occurring adjustment costs (in an adjustment cost model) or reoptimizing (in a Calvomodel).

15

report the standard deviations of the output gap, the PCE price index inflation rate, and

the nominal federal funds rate. The final column reports the central bank loss.

In the baseline scenario, if policy follows the classic Taylor rule, then the ZLB has only

minor affects on the magnitude of macroeconomic fluctuations if the inflation target is 1-1/2

percent or higher. Under these assumptions, a 1-1/2 percent inflation target implies that

the funds rate will fall below 1 percent 10 percent of the time, and will be below 10 basis

points 6 percent of the time. The standard deviation of the unconstrained interest rate is

only about 2-1/2 percent. So, with a 4 percentage point buffer, most episodes where the

ZLB is binding are relatively mild and effects are minor. These results are consistent with

those of many studies that with a steady-state nominal interest rate of 4 percent or higher,

the ZLB has very modest macroeconomic effects under the Taylor rule.

If the steady-state real interest rate is only 1 percent, then under the classic Taylor rule

a 3 percent inflation objective is sufficiently high to avoid most costs from the ZLB. With a

2 percent inflation goal, the ZLB binds 13 percent of the time and causes a more noticeable

rise in output gap variability (a rise of 0.3 percentage points relative to a 5 percent or

higher inflation goal). The incidence of deep recessions rises as well, but remains below 10

percent. Based on this evidence, a lower steady-state real interest rate argues for a higher

inflation goal to reduce the costs associated with the ZLB. But, it alone does not overturn

the basic result of past research that a 2 percent inflation goal is associated with relatively

modest costs from the ZLB. This conclusion is reinforced when one considers alternative

policy rules that mitigate the problems associated with the ZLB, as discussed below.

As noted above, the assumption of normally distributed disturbances may understate

the likelihood of tail events of the type that we have recently experienced. To gauge the

sensitivity of the results to this assumption, I conduct simulations where the disturbances

have the same covariance as before (that is, based on the full 1968-2002 sample), but

are assumed to follow the t distribution with 5 degrees of freedom. This distribution is

characterized by excess (relative to the normal distribution) kurtosis of 6; that is, it displays

significantly fatter tails than the normal distribution. For example, the probability of a three

16

Table 2: Outcomes for Different Shock DistributionsInflation Target Probability Std. Dev.r∗ = 2.5 r∗ = 1 i < 0.1 i < 1 y < −4 y π i L

Shocks drawn from 1968-2002 covariance; normally distributed-0.5 1 .23 .31 .12 3.1 1.5 2.4 13.30.5 2 .13 .20 .08 2.8 1.5 2.4 11.51.5 3 .06 .10 .06 2.6 1.5 2.5 10.62.5 4 .04 .08 .06 2.6 1.5 2.6 10.53.5 5 .02 .03 .06 2.5 1.5 2.6 10.15.5 7 .00 .00 .05 2.5 1.5 2.6 9.97.5 9 .00 .00 .05 2.5 1.5 2.6 9.9

Shocks drawn from 1968-2002 covariance; t(5) distributed-0.5 1 .24 .33 .13 3.1 1.5 2.4 13.20.5 2 .13 .20 .08 2.8 1.5 2.5 11.51.5 3 .08 .13 .07 2.7 1.5 2.5 10.82.5 4 .04 .07 .06 2.6 1.5 2.7 10.63.5 5 .03 .05 .06 2.6 1.5 2.7 10.65.5 7 .00 .00 .05 2.5 1.5 2.6 9.97.5 9 .00 .00 .05 2.5 1.5 2.6 9.9

Shocks drawn from 1968-1983 covariance; normally distributed-0.5 1 .29 .38 .18 3.7 1.7 2.6 18.40.5 2 .16 .23 .12 3.3 1.6 2.8 15.51.5 3 .09 .14 .11 3.2 1.6 2.8 14.52.5 4 .04 .07 .09 3.0 1.6 2.8 13.63.5 5 .03 .06 .09 2.9 1.6 2.9 13.45.5 7 .02 .03 .08 2.9 1.6 2.9 13.07.5 9 .00 .00 .08 2.9 1.6 2.9 13.0

Notes: This table reports simulated moments for different assumptions regardingthe distribution of shocks. Results are shown for two values of the steady-statereal interest rate, r∗. The first column indicates the inflation target assumingr∗ = 2.5; the second column indicates the inflation target assuming r∗ = 1.Monetary policy rule: it = max {0, r∗t + πt + 0.5(πt − π∗) + 0.5yt}.Central bank loss: L = E

{(π − π∗)2 + y2 + 0.25 ∗ (i− i∗)2

}, where i∗ = π∗ + r∗.

standard deviation (or greater) event is over 4 times greater with this t(5) distribution than

the normal distribution.12

Allowing for a fatter-tailed distribution of distributions does not materially affect the

results regarding the effects of the ZLB. The middle panel of Table 2 reports the results

from these simulations. The ZLB is encountered slightly more often, and the standard

deviations of the output gap are in some cases higher, but these effects are nearly lost in

rounding. Note that the shocks being used differ from those used in the other simulations,12The choice of the degrees of freedom of 5 is somewhat arbitrary, but near the lower bound of allowable

values for the purpose at hand. In particular, the degrees of freedom of the t distribution must exceed 4 forfinite second and fourth moments to exist.

17

so comparison to the simulations using normally distributed disturbances is not exact due

to the finite samples of the simulations. Similar results (not reported) were obtained when

the disturbances were assumed to follow a Laplace distribution, which has excess kurtosis

of 3. There may be more exotic distributions with even greater kurtosis that would have

greater effects on these results, but a more critical issue appears to be the covariance of the

shocks, rather than the precise shape of the distribution.

The effects of the ZLB are far more pronounced when the shocks are drawn from the pre-

Great Moderation period. In the simulations reported in the lower portion of the table, the

disturbances are drawn from a normal distribution where the covariance of disturbances

is estimated from the 1968-1983 sample of model disturbances. As a result, the ZLB is

encountered more frequently and with greater costs in terms of stabilization of the output

gap. With a steady-state real interest rate of 2-1/2 percent, a 2 percent inflation target is

just on the edge of the region where the ZLB has nontrivial costs in terms of macroeconomic

variability. Inflation goals of 1-1/2 percent or lower entail moderate increases in output gap

variability.

The combination of a 1 percent steady-state real interest rate and greater volatility of

disturbances poses the greatest threat to macroeconomic stabilization in a low inflation

environment. Inflation goals of 2 to 3 percent are associated with some increase in output

gap variability, while a 1 percent inflation goal entails a significant increase in output gap

variability. Even in these extreme cases, the effects on inflation variability are quite modest,

reflecting the effects of assumption of well-anchored expectations.

How big are these losses? One metric is the fraction of the time the output gap is

below -4 percent. In the adverse environment of shocks drawn from the 1968-1983 shock

covariance and a steady-state real interest rate of 1 percent, this figure rises from 9 percent

to 18 percent when the inflation target is reduced from 4 to 1 percent. The standard

deviation of the output gap rise by 0.7 percentage point. For comparison, the standard

deviation of the output gap during the “Great Moderation” period of 1985-2006 was 2

percentage points, according to CBO estimates. The comparable figure for 1965-1980 was

18

2.7 percentage points. Thus, moving from a 4 percent inflation target to a 1 percent inflation

target yields an increase in output gap variability in these model simulations comparable

to switching from the Great Moderation period to the 1965-1980 period. Moving from a 4

percent inflation target to a 2 percent target entails an increase in output gap variability

comparable to switching from the Great Moderation period to the period of 1955-1965,

when the standard deviation of the output gap was 2.3 percentage points, 0.3 percentage

points above that during the Great Moderation period.

4 Alternative Monetary and Fiscal Policies

The results reported above indicate that in a particulary adverse macroeconomic environ-

ment of large shocks and a low steady-state real interest rate, the ZLB may cause a signifi-

cant deterioration in macroeconomic performance when monetary policy follows the classic

Taylor rule with a very low inflation target. As discussed in Reifschneider and Williams

(2000, 2002) and Eggertsson and Woodford (2003), alternative monetary policy strategies

improve upon the performance of the classic Taylor rule in a low inflation environment. Sev-

eral such modifications are examined here. In addition, I consider the use of countercyclical

fiscal policy to mitigate the effects of the ZLB. Throughout the following discussion, I as-

sume the worst-case adverse macroeconomic environment of a 1 percent steady-state real

interest rate and disturbances drawn from the covariance matrix computed from the shocks

of the pre-Great Moderation period.

4.1 Modifying the Taylor rule

One way to achieve greater stabilization of the output gap even at low steady-state inflation

rates and in an adverse environment is for the policy rule to respond more aggressively to

movements in the output gap. Table 3 reports simulation results for alternative values of the

coefficient on the output gap, φ, in the monetary policy rule. A larger response to output

gap reduces output gap variability and allows the central bank to reach output and inflation

goals at some cost of interest rate variability, even at inflation goals as low as 2 percent. For

example, assume the goal is to have outcomes like those under classic Taylor rule (φ = 0.5)

19

unconstrained by the ZLB, but with an inflation target of 2 percent. The Taylor-type rule

with the stronger response to the output gap of φ = 1.5 yields outcomes for output gap

and inflation rate variability close to that of the Classic Taylor rule unconstrained by the

ZLB, at the cost of somewhat greater interest rate variability. Similarly, outcomes similar

to the unconstrained classic Taylor rule can be achieved with an inflation goal of 3 percent

by setting φ = 1.

Interestingly, too strong a response to the output gap can be counterproductive at very

low steady-state interest rates. This outcome likely reflects the asymmetry of the policy

response resulting from the ZLB. When the output gap is positive, policy tightens sharply.

But, when the output gap is negative, the policy response is more likely to be truncated by

the ZLB. This strongly asymmetric response causes output gap variability to rise at very

low inflation targets in the adverse macroeconomic environment. A stronger response to

inflation in the Taylor-type rule does not have much effect on the effects of the ZLB (not

shown).13

None of these modified Taylor Rules performs well with an inflation target of 1 percent

in the adverse macroeconomic environment. In all three cases, the standard deviation of

the output gap rises sharply with an inflation target of 1 percent. The fraction of time that

the output gap is below -4 percent is extremely high, between 17 and 20 percent. These

figures decline dramatically when the inflation target is raised to 2 percent.

Other modifications to the Taylor-type rule can also be effective at offsetting the effects

of the ZLB in low inflation environments. The upper panels of Table 4 report the results

from a modified Taylor-type rule proposed by Reifschneider and Williams (2000). According

to this policy rule, realized deviations of the interest rate from that prescribed by the rule

owing to the ZLB are later offset by negative deviations of equal magnitude. Note that this

does not necessarily imply the central bank is promising to raise inflation above its target in

the future, but only that it makes up for “lost monetary stimulus” by holding the interest13There are other reasons, however, for a stronger response to inflation, such as the better anchoring of

inflation expectations in an economy with imperfect knowledge, as discussed in Orphanides and Williams2002, 2007.

20

Table 3: Alternative Responses to Output Gap (φ) in Adverse Environment

(1968-83 shock covariance and r∗ = 1)Inflation Probability Std. Dev.Target i < 0.1 i < 1 y < −4 y π i L

φ = 0.51 .29 .38 .18 3.7 1.7 2.6 18.42 .16 .23 .12 3.3 1.6 2.8 15.53 .09 .14 .11 3.2 1.6 2.8 14.54 .04 .07 .09 3.0 1.6 2.8 13.65 .03 .06 .09 2.9 1.6 2.9 13.47 .02 .03 .08 2.9 1.6 2.9 13.09 .00 .00 .08 2.9 1.6 2.9 13.0

φ = 11 .34 .41 .17 4.6 2.1 2.6 27.32 .16 .22 .08 3.1 1.7 3.3 15.23 .11 .15 .06 2.7 1.6 3.4 13.14 .08 .12 .06 2.6 1.6 3.4 12.45 .06 .10 .06 2.5 1.6 3.5 12.07 .02 .03 .05 2.5 1.6 3.6 12.09 .00 .01 .05 2.5 1.6 3.6 12.0

φ = 1.51 .42 .49 .20 4.9 2.1 3.3 31.22 .24 .30 .09 2.9 1.7 3.8 17.13 .19 .24 .06 2.6 1.6 4.0 13.44 .17 .22 .06 2.5 1.6 4.0 12.85 .11 .15 .05 2.3 1.6 4.2 12.57 .05 .07 .04 2.3 1.7 4.4 13.09 .02 .03 .04 2.3 1.7 4.6 13.2

Notes: This table reports simulated moments for different assumptions regardingthe response of monetary policy to the output gap (φ) in the adverse economicenvironment, characterized by shocks drawn from the 1968-1983 covariance and ansteady-state real interest rate (r∗) of 1 percent.Policy follows Taylor-type rule: it = max {0, r∗t + πt + 0.5(πt − π∗) + φyt}.Central bank loss: L = E

{(π − π∗)2 + y2 + 0.25 ∗ (i− i∗)2

}, where i∗ = π∗ + r∗.

rate low for a period after the ZLB no longer binds.

This modified rule nearly eliminates the effects of the ZLB for inflation targets as low

as 3 percent, and significantly reduces them for lower inflation targets. If the inflation goal

is 2 percent, the modified rule with a greater response to output of φ = 1 yields the same

outcomes as the unconstrained Taylor rule in this adverse environment.

In rational expectations models like FRB/US, policies with inertial responses to move-

ments in inflation and output gaps perform much better than static Taylor-type rules and

closely approximate the outcomes under fully optimal policies (Woodford 2003, Levin and

21

Table 4: Alternative Monetary Policy Rules in Adverse Environment

(1968-83 shock covariance and r∗ = 1)Inflation Probability Std. Dev.Target i < 0.1 i < 1 y < −4 y π i L

Classic Taylor rule with lagged adjustment (φ = 0.5)1 .18 .26 .12 3.7 1.6 2.8 19.42 .12 .19 .10 3.2 1.6 2.8 14.73 .07 .13 .09 3.0 1.6 2.8 13.64 .04 .08 .08 3.0 1.6 3.0 13.75 .03 .05 .08 2.9 1.6 2.9 13.07 .00 .01 .08 2.9 1.6 2.9 13.09 .00 .00 .08 2.9 1.6 2.9 13.0

Taylor-type rule with lagged adjustment (φ = 1)1 .32 .40 .12 3.6 1.6 3.2 27.62 .21 .28 .07 2.9 1.6 3.4 13.63 .16 .22 .06 2.5 1.6 3.4 11.74 .05 .15 .06 2.5 1.6 3.5 11.75 .02 .09 .06 2.5 1.6 3.5 11.87 .00 .03 .05 2.5 1.6 3.6 12.09 .00 .01 .05 2.5 1.6 3.6 12.0

Optimized inertial policy rule1 .24 .33 .10 3.4 1.4 2.4 14.52 .15 .22 .08 2.9 1.4 2.6 11.93 .11 .16 .07 2.7 1.4 2.6 11.04 .05 .08 .06 2.5 1.4 2.6 10.25 .02 .04 .06 2.5 1.4 2.7 10.17 .00 .01 .06 2.5 1.4 2.7 10.29 .00 .00 .06 2.5 1.4 2.7 10.2

Notes: This table reports simulated moments for different assumptions regardingthe response of monetary policy to the output gap (φ) in an adverse economicenvironment, characterized by shocks drawn from the 1968-1983 covariance and ansteady-state real interest rate (r∗)of 1 percent.Alternative monetary policies are described in the text.Inertial policy: iut = 0.96iut−1 + 0.04 ∗ (r∗ + πt) + 0.04(πt − π∗) + 0.12yt,

Williams 2003). In particular, I examine the performance of the policy rule taking the form:

iut = 0.96iut−1 + 0.04 ∗ (r∗ + πt) + 0.04(πt − π∗) + 0.12yt, (4)

where iut is the prescription for the federal funds rate unconstrained by the ZLB. The

coefficient on the lagged interest rate of near unity imparts a great deal of inertia policy

(also frequently referred to as “interest rate smoothing”). The actual setting of the interest

rate must satisfy the ZLB:

it = max {0, iut } . (5)

22

As shown in Reifschneider and Williams (2000), policy rules like this perform very well in

the presence of the ZLB because they promise to keep interest rates low in the future and to

allow inflation to rise above its long-run target following bouts of excessively low inflation.

This inertial policy rule delivers better macroeconomic performance with a 2 percent

inflation target than the classic Taylor rule unconstrained by the ZLB. The lower part of

Table 4 reports the simulated outcomes from inertial version of the Taylor-type rule where

the parameters of the rule were chosen to yield minimum weighted variances of inflation,

the output gap, and the nominal interest rate. Nonetheless, in this worst case adverse

environment, there are limits to what this simple rule can accomplish, and performance

suffers noticeably as the inflation goal is lowered to much below 2 percent. I obtain very

similar results for a policy rule that targets the price level growing at a deterministic trend

rather than the inflation rate, which Eggerston and Woodford (2003) find to perform well

in the presence of the ZLB. Based on this evidence, there is little gain from switching from

an optimized inertial policy to an explicit price-level targeting regime, even with very low

steady-state inflation rates.

A potential problem with these alternative policy approaches is that the public may be

confused by monetary policy intentions in the vicinity of the ZLB. For example, the asym-

metric policy rule described represents a significant deviation from the standard reaction

function, which could have unintended undesirable consequences(Taylor 2007). More gen-

erally, all of these alternative policies rely extensively on the expectations of future policy

actions to influence economic outcomes. As shown by Reifschneider and Roberts (2006)

and Williams (2006), if agents do not have rational expectations, episodes of the ZLB may

distort expectations, reducing the benefits of policies that work very well under rational

expectations. In particular, inertial and price-level targeting policies cause inflation to rise

above the long-run target following an episode where the ZLB constrains policy. Such a

period of high inflation could conceivably undermine the public’s confidence in the central

bank’s commitment to price stability and lead to an untethering of inflation expectations.

Indeed, central banks have averse to declaring a desire to see a sustained rise in inflation

23

rise above the target level (Kohn 2009, Walsh 2009).

One method to minimize the public confusion is for the central bank to clearly commu-

nicate the central bank’s expectations, including the anticipated policy path, as discussed

by Woodford (2005) and Rudebusch and Williams (2008).14 Another approach is to back

up the communication with interventions in foreign exchange–as proposed by McCallum

(2000), Svensson (2001), and Coenen and Wieland (2003)–or by targeting the short to mid-

dle end of the yield curve of Treasury securities as analyzed by McGough, Rudebusch and

Williams (2005).

An additional potential problem with highly inertial and price-level targeting policies is

that historically, the price level and interest rates tend to be relatively high as the economy

enters a recession because of high inflation rates near the end of expansions.15 In these

circumstances, such policies imply delayed policy responses early in a downturn. The current

episode illustrates this dilemma. As seen in Figure 3, inflation had been consistently running

above 2 percent in several countries well into 2008. Although model simulations do not bear

out these concerns, perhaps there is something missing from the dynamics in the models or

the assumed monetary policies.

4.2 Counter-cyclical Fiscal Policy

The active use of counter-cyclical fiscal policy was excluded from consideration in most

quantitative research on the ZLB and the simulations reported above. The experience

of the past decade suggests that this assumption is too stringent. In this respect, by

ignoring the ways in which fiscal policy is used to substitute for monetary policy, the

future effects of the ZLB may be overstated. The past decade has seen the active use

of sizable discretionary countercyclical fiscal policy in many countries. Japan aggressively

used fiscal policy to stimulate the economy during the 1990s and the current recession. The14Although a few central banks publish interest rate paths and the Bank of Canada recently made clear

statements about its intended path, most central banks remain unwilling to provide such clear communicationof their future policy intents.

15This observation is related to the strong correlation between the slope of the yield curve and recessions(Rudebusch and Williams, 2009). Past recessions are preceded by periods of monetary tightening in responseto periods of high inflation.

24

International Monetary Fund (IMF, 2009) expects discretionary fiscal policy to average 1

percent of GDP in the G-20 economies over the period of 2008-2010, above and beyond

automatic stabilizers and measures to support the financial sector.

Economic theory is clear that in the presence of nominal rigidities government spending

can be useful at reducing the macroeconomic costs associated with the ZLB (see, for ex-

ample, Eggertsson 2009; Christiano, Eichenbaum, and Rebelo 2009; and Erceg and Linde

2009). Consider the case where, due a negative shock to the economy, the short-term in-

terest rate declines but cannot fall enough to offset the shock. As a result, the real interest

rate rises, consumption falls, and inflation falls. These consequences reduce household wel-

fare. A temporary increase in government purchases increases output and raises wages and

thereby marginal cost. This increase in marginal cost boosts the inflation rate and the

expected rate of inflation. Given a fixed short-term nominal interest rate constrained by

the ZLB, the rise in expected inflation lowers the real interest rate, causing consumption to

rise. As a result, the increase in government spending reduces the fluctuations in inflation

and the output gap and raises welfare.16

In principle, any number of ways of strengthening automatic stabilizers or introduc-

ing stronger counter-cyclical fiscal policy more generally could help mitigate the problems

caused by the ZLB. Reifschneider and Roberts (2006) provide an example of the effects of

fiscal policy stimulus when the ZLB is constraining policy using simulations of the FRB/US

model. I consider one simple experiment based on a systematic fiscal policy rule for the

category of federal government purchases excluding employee compensation and investment

purchases (a category that makes up about one half of federal government purchases). The

estimated fiscal reaction function for this category in the FRB/US model is given by:

gt = 0.55gt−1 + 0.07gt−2 + 0.19gt−3 − 0.0004yt + 0.0027yt−1 + γ(it−1 − iut−1) + εt, (6)

where g is the log of government purchases in this category, yh is the output gap, and iu

16In contrast to the case of government spending, the effects of income taxes with respect to the ZLBcan be counterintuitive. In models without credit and liquidity constraints, lowering income taxes can becounterproductive because it lowers marginal costs and and inflation (Eggertsson and Woodford 2004). Insuch a model, raising taxes during a downturn can improve welfare. In models with liquidity-constrainedconsumers, tax cut can also raise demand.

25

is the setting of the unconstrained federal funds rate that would occur absent the ZLB.

In the baseline model, γ = 0. I consider the effects of a sustained increase in federal

government purchases when the ZLB constrains monetary policy by setting γ = 0.02. This

value implies that a one percentage point interest rate gap owing to the ZLB causes overall

federal government purchases to rise by 1 percent in the next period. Lags in fiscal policy

implementation are approximated by the lag structure of this equation.

The modified fiscal reaction function cuts in half the macroeconomic effects of the ZLB

for low steady-state interest rates of 3 and 4 percent. The lower part of Table 5 shows the

outcomes from this experiment for the Taylor-type rule with φ = 1. The upper part of

the table shows the same rule without the fiscal response. In the worst case scenario, an

inflation target of 3 percent is sufficient to avoid effects from the ZLB. An inflation target

of 2 percent suffers a small increase in output variability. This specification for the fiscal

reaction function is in no way meant to be optimal or even desirable, but rather to illustrate

the effects of countercyclical fiscal policy aimed at mitigating the effects of the ZLB on the

economy. Further research is needed in this area to devised better countercyclical fiscal

policy rules.

4.3 Unconventional monetary policy actions

The preceding discussion and analysis abstracted from unconventional monetary actions,

implicitly assumes that these are not used or are ineffective. However, the events of the

past year provide ample evidence that central banks possess and are willing to use tools

other than the overnight interest rate. Clouse et al (2003) and Bernanke and Reinhart

(2004) describe alternative policy tools available to the Federal Reserve. In the current

crisis, a number of alternative approaches have been put to use. Several central banks,

including the Bank of England, the European Central Bank, the Federal Reserve, and the

Bank of Japan, have instituted programs to buy or guarantee assets such as commercial

paper and mortgage-backed securities. Finally, the Bank of Japan, the Bank of England

,and the Federal Reserve have expanded their holdings of longer-term securities through

the creation of reserves. Many of these programs are aimed at improving the functioning

26

Table 5: Alternative Fiscal Policy in Adverse Environment

(1968-83 shock covariance and r∗ = 1)Inflation Probability Std. Dev.Target i < 0.1 i < 1 y < −4 y π i L

Baseline fiscal policy2 .34 .41 .17 4.6 2.1 2.6 27.33 .16 .22 .08 3.1 1.7 3.3 15.24 .11 .15 .06 2.7 1.6 3.4 13.15 .08 .12 .06 2.6 1.6 3.4 12.46 .06 .10 .06 2.5 1.6 3.5 12.08 .02 .03 .05 2.5 1.6 3.6 12.010 .00 .01 .05 2.5 1.6 3.6 12.0

Government spending increase at zero bound2 .31 .39 .12 3.9 2.0 2.8 21.23 .16 .23 .07 2.8 1.6 3.2 13.34 .12 .17 .06 2.6 1.6 3.3 12.25 .08 .12 .06 2.5 1.6 3.4 11.86 .06 .10 .06 2.5 1.6 3.5 11.98 .02 .03 .05 2.5 1.6 3.6 12.010 .00 .01 .05 2.5 1.6 3.6 12.0

Notes: This table reports simulated moments for different assumptions regardingthe response of fiscal policy in the presence of the ZLB, in an adverse macroeconomicenvironment, characterized by shocks drawn from the 1968-1983 covariance and ansteady-state real interest rate (r∗)of 1 percent.Monetary policy rule: it = max {0, r∗t + πt + 0.5(πt − π∗) + yt}.Central bank loss: L = E

{(π − π∗)2 + y2 + 0.25 ∗ (i− i)2

}, where i∗ = π∗ + r∗.

of impaired or distressed markets. Similarly, the Federal Reserve’s purchases of agency

debt and mortgage-backed securities were aimed at market segment that appeared to be

functioning poorly. Future recessions may not be accompanied by severe financial market

disruptions, in which case these tools would not be as useful at offsetting the shocks hitting

the economy.

An open question is whether balance sheet policies such as quantitative easing or

purchases of longer-term government securities are effective at stimulating the economy.

Bernanke et al (2004) provide evidence that shocks to the supply of government securi-

ties affect their price and yield. Announcements by the Bank of England and the Federal

Reserve regarding plans to buy longer-term government securities were followed by large

movements in yields, providing additional support that such policy actions can affect yields

(see Meier 2009, for a summary of the experience in the UK). Nonetheless, there is a great

27

deal of uncertainty regarding the magnitude and duration of these effects. In addition,

some observers fear adverse consequences of such actions if taken on a large scale, including

the risk of large losses and the concerns that inflation expectations may become unmoored.

Further careful study and analysis is needed before these policy options can be counted on

as effective substitutes for more traditional monetary policy actions.

5 Conclusion

The zero lower bound has significantly constrained the ability of many central banks to stim-

ulate the economy in the current recession. Counterfactual simulations suggest that the ZLB

will impose significant costs on the U.S. economy in terms of lost output. Although these

simulation focus on the effects of lower U.S. interest rates on the U.S. economy, comparable

simulations for other economies where the ZLB has constrained monetary policy–such as

in Japan and Europe–would no doubt show that the ZLB has also entailed significant costs

in those places during the recent episode. A useful extension of the simulations reported in

this paper would be to calculate the costs of the ZLB in a model of the global economy.

If the recent recession represents an unique, extraordinary incident, it has no particular

implications for future monetary policy with respect to the ZLB. In particular, a 2 percent

inflation target should provide an adequate buffer for monetary policy in the future. If,

however, the era of the Great Moderation is over and the steady-state real interest rate

remains very low, then the ZLB may regularly interfere with the ability of central banks

to achieve macroeconomic stabilization goals. The analysis in this paper argues that an

inflation target of 2 percent may be insufficient to keep the ZLB from imposing sizable costs

in terms of macroeconomic stabilization in a much more adverse macroeconomic climate if

monetary policy follows the standard Taylor Rule.

Given these results, it is important to study and develop monetary and fiscal policies

that effectively counter the effects of the ZLB in preparation for the contingency of an

adverse macroeconomic environment. Arguably, the application of aspects of many of these

approaches over the past two years has helped combat the massive shocks that have buffeted

28

the global economy. Improving these policies and developing new ones into systematic,

predictable responses to economic conditions will help make them more effective in the

future. An important lesson from the financial crisis, not addressed in this paper, is the

critical need for effective regulation and supervision of financial markets to avoid the shocks

to the global economy that ignited the current global financial crisis and recession.

Finally, this paper examines only the costs associated with the ZLB, abstracting from

the many other sources of distortions related to steady-state inflation. Several of these–

including transaction costs, real distortions associated with non-zero rates of inflation, and

non-neutralities in the tax system–argue for zero or negative steady-state inflation rates.

Others–including asymmetries in wage setting, imperfections in labor markets, distortions

related to imperfect competition, and measurement bias–argue for positive steady-state

inflation (see, for example, Akerlof et al 1996). Unfortunately, there has been relatively

little research that weighs the costs of the ZLB against these other influences in a coherent,

empirically-supported framework (see Billi and Kahn, 2008, for a review).17 More research

on these issues is needed.17Much of the literature focuses on welfare costs related to holding zero interest bearing assets, which

both Feldstein (1997) and Attansio et al (2002) convincing show are trivial. These costs are even lower nowthat the Federal Reserve and many other central banks pay interest on reserves.

29

References

Adam, Klaus, and Roberto M. Billi, “Optimal Monetary Policy under Commitment with aZero Bound on Nominal Interest Rates,” Journal of Money, Credit and Banking, 38(7),2006, 1877-1905.

Akerlof, George, William Dickens, and George Perry, “The Macroeconomics of Low Infla-tion,” Brookings Papers on Economic Activity 47(1), 1996, 1-59.

Attansio, Orazio P., Luigi Guiso, L. and Tullio Jappelli, “The Demand for Money, Finan-cial Innovation and the Welfare Cost of Inflation: An Analysis with Household Data,”Journal of Political Economy, 110(2), 2002, 317-351.

Bailey, Martin J., “The Welfare Cost of Inflationary Finance,” The Journal of PoliticalEconomy, 64(2), April 1956, 93-110.

Benhabib, Jess, Stephanie Schmitt-Grohe, and Martin Uribe, “The Perils of Taylor Rules,”Journal of Economic Theory, 96(1-2), January 2001, 40-69.

Bernanke, Ben S., and Vincent R. Reinhart, “Conducting Monetary Policy at Very LowShort-Term Interest Rates,” American Economic Review, Papers and Procedings, 94(2),2004, 85-90.

Bernanke, Ben S., Vincent R. Reinhart, and Brian P. Sack, “Monetary Policy Alternativesat the Zero Bound: An Empirical Assessment,” Brookings Papers on Economic Activity,2, 2004, 1-78.

Billi, Roberto M., and George A. Kahn, “What Is the Optimal Inflation Rate?,” FederalReserve Bank of Kansas City Economic Review, Second Quarter, 2008.

Bodenstein, Martin, Christopher J. Erceg, and Luca Guerrieri, “The Effects of ForeignShocks when Interest Rates are at Zero,” Board of Governors of the Federal Reserve,International Finance Discussion Papers 981, 2009.

Brayton, Flint, Eileen Mauskopf, David Reifschneider, Peter Tinsley, and John Williams,“The Role of Expectations in the FRB/US Macroeconomic Model,”, Federal ReserveBulletin, April 1997, 227-245.

Carlson, John B., Ben Craig, and William R. Melick, “Recovering Market Expectations ofFOMC Rate Changes with Options on Federal Funds Futures,” The Journal of FuturesMarkets, 25(12), December 2005, 1203-44.

Christiano, Lawrence, Martin Eichenbaum, and Sergio Rebelo, “When is the GovernmentSpending Multiplier Large?” Northwestern University, mimeo, September 2009.

Clouse, James, Dale Henderson, Athanasios Orphanides, David Small, and Peter Tinsley,“Monetary Policy when the Short-term Intreest Rate is Zero,” Topics in Macroeco-nomics, 3(1), 2003.

Coenen, Guenter, “Zero Lower Bound: Is It a Problem in the Euro Area?,” ECB Workingpaper No. 269, September 2003.

Coenen , Guenter, Athansios Orphanides, and Volker Wieland, “Price Stability and Mone-tary Policy Effectiveness when Nominal Interest Rates are Bounded at Zero,” Advancesin Macroeconomics, 4(1), 2004.

30

Coenen, Guenter, and Volker Wieland, “The Zero-Interest Rate Bound and the Role of theExchange Rate for Monetary Policy in Japan,” Journal of Monetary Economics, 50(5),July 2003, 1071-1101.

Eggertsson, Gauti B., “What Fiscal Policy is Effective at Zero Interest Rates?” FederalReserve Bank of New York, August 2009.

Eggertsson, Gauti B., and Michael Woodford, “The Zero Interest-Rate Bound and OptimalMonetary Policy,” Brookings Papers on Economic Activity, 1, 2003, 139-211.