hedging with foreign exchange derivatives hedging with foreign exchange derivatives alex russell ben...

TRANSCRIPT

Hedging with Foreign Hedging with Foreign Exchange DerivativesExchange Derivatives

Alex Russell Alex Russell

Ben DavidsonBen Davidson

Mona LisaMona Lisa

HistoryHistory August 21,1911 Louis Béroud, a painter, walked into the August 21,1911 Louis Béroud, a painter, walked into the

Louvre and went to the Salon Carré where the Mona Louvre and went to the Salon Carré where the Mona Lisa had been on display for five years. However, where Lisa had been on display for five years. However, where the Mona Lisa should have stood, he found four iron the Mona Lisa should have stood, he found four iron pegs. pegs.

Béroud contacted the section head of the guards, who Béroud contacted the section head of the guards, who thought the painting was being photographed. A few thought the painting was being photographed. A few hours later, Béroud checked back with the section head hours later, Béroud checked back with the section head of the museum, and it was confirmed that the Mona Lisa of the museum, and it was confirmed that the Mona Lisa was not with the photographers. The Louvre was closed was not with the photographers. The Louvre was closed for an entire week to aid in the investigation of the theft.for an entire week to aid in the investigation of the theft.

History ContinuedHistory Continued At the time, the painting was believed lost forever. It At the time, the painting was believed lost forever. It

turned out that on August 20,1911 Louvre employee turned out that on August 20,1911 Louvre employee Vincenzo Peruggia stole it by simply by entering the Vincenzo Peruggia stole it by simply by entering the building during regular hours, hiding in a broom closet, building during regular hours, hiding in a broom closet, and walking out with it hidden under his coat after the and walking out with it hidden under his coat after the museum had closed. museum had closed.

Con-man Eduardo de Valfierno master-minded the theft, Con-man Eduardo de Valfierno master-minded the theft, and had commissioned the French art forger Yves and had commissioned the French art forger Yves Chaudron to make copies of the painting so he could sell Chaudron to make copies of the painting so he could sell them as the missing original. Because he didn't need the them as the missing original. Because he didn't need the original for his con, he never contacted Peruggia again original for his con, he never contacted Peruggia again after the crime. After keeping the painting in his after the crime. After keeping the painting in his apartment for two years, Peruggia grew impatient and apartment for two years, Peruggia grew impatient and was caught when he attempted to sell it to a Florence art was caught when he attempted to sell it to a Florence art dealer; it was exhibited all over Italy and returned to the dealer; it was exhibited all over Italy and returned to the Louvre in 1913.Louvre in 1913.

Present Day Present Day A short time after the theft Yves Chaudron A short time after the theft Yves Chaudron

escaped to the United States where he hid from escaped to the United States where he hid from the international art community. Two weeks ago, the international art community. Two weeks ago, his great grandson Frances contacted us with a his great grandson Frances contacted us with a business proposal. business proposal.

Frances Chaudron, grandson of the great art Frances Chaudron, grandson of the great art forger Yves Chaudron is currently one of the forger Yves Chaudron is currently one of the best painters in the world. As an artist, he has best painters in the world. As an artist, he has made a small fortune painting old masterpieces. made a small fortune painting old masterpieces. Recently, in his studio in Salem, Oregon, Francis Recently, in his studio in Salem, Oregon, Francis presented a profitable scheme inspired by his presented a profitable scheme inspired by his great grandfather. great grandfather.

The PlanThe Plan Francis wants us to steal the Mona Lisa so that he can Francis wants us to steal the Mona Lisa so that he can

make precise forgeries to sell on the black market. make precise forgeries to sell on the black market. Current technology requires that he actually have the Current technology requires that he actually have the original painting in his possession so that the borders original painting in his possession so that the borders match that of the original. Although the borders are not match that of the original. Although the borders are not seen by the public, and are never photographed, a few seen by the public, and are never photographed, a few collectors know their exact composition. collectors know their exact composition.

Acting in our capacity as an art broker, we were intrigued Acting in our capacity as an art broker, we were intrigued by the idea and contacted our associate in Rome, Italy. by the idea and contacted our associate in Rome, Italy. She believes that she can steal the painting and She believes that she can steal the painting and transport it to the United States, but requires payment of transport it to the United States, but requires payment of € 15,000,000 upon delivery. € 15,000,000 upon delivery.

After consulting our thief, we decided to take the job on After consulting our thief, we decided to take the job on the condition that Francis pays us for our services up the condition that Francis pays us for our services up front. He agrees, but says that we will only deal with front. He agrees, but says that we will only deal with dollars since foreign exchange rates confuse him. dollars since foreign exchange rates confuse him. Because of this complication, he offers us $ 19,000,000 Because of this complication, he offers us $ 19,000,000 for the painting.for the painting.

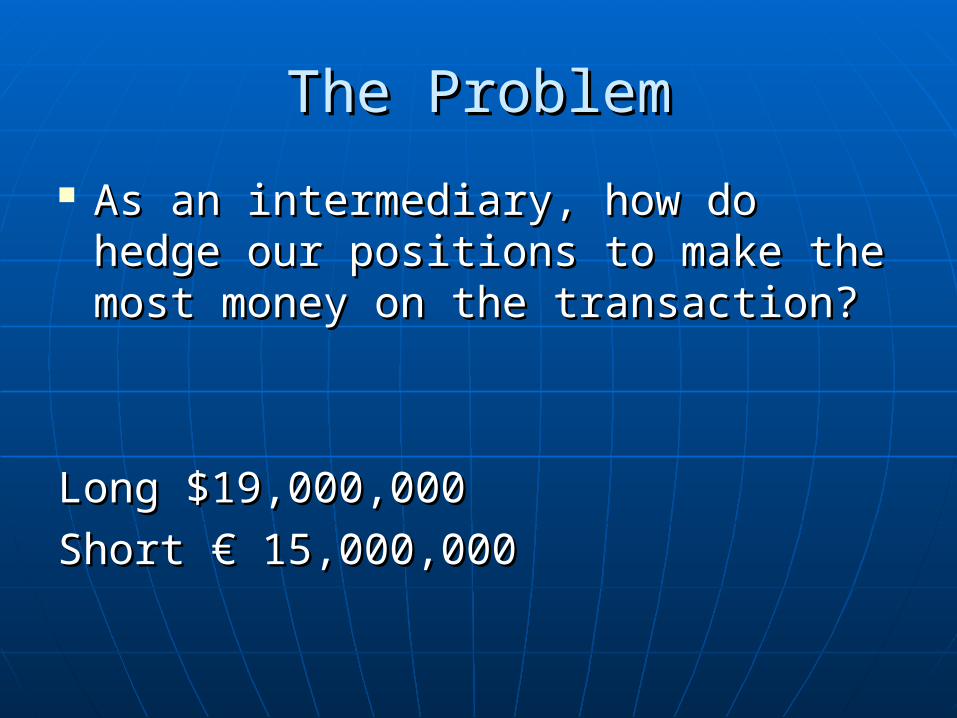

The ProblemThe Problem

As an intermediary, how do hedge our As an intermediary, how do hedge our positions to make the most money on the positions to make the most money on the transaction?transaction?

Long $19,000,000Long $19,000,000

Short Short € 15,000,000€ 15,000,000

HedgingHedging

Used to manage against riskUsed to manage against risk Delta Hedge—attempts to offset the Delta Hedge—attempts to offset the

change in the value of the exposure with change in the value of the exposure with an opposite change in the value of the an opposite change in the value of the hedge position.hedge position.

Matching ‘longs’ and ‘shorts’.Matching ‘longs’ and ‘shorts’.

Hedging With a Currency FutureHedging With a Currency Future

To hedge a foreign exchange exposure, the To hedge a foreign exchange exposure, the customer assumes a position in the opposite customer assumes a position in the opposite direction of the exposure.direction of the exposure.

For example, if the customer is short the Euro, For example, if the customer is short the Euro, they would go long in the futures market (which they would go long in the futures market (which we will do).we will do).

A customer that is long in the futures market is A customer that is long in the futures market is betting on an increase in the value of the betting on an increase in the value of the currency, whereas with a short position they are currency, whereas with a short position they are betting on a decrease in the value of the betting on a decrease in the value of the currency.currency.

Futures ContractsFutures Contracts

Four fixed Dates a year; 3Four fixed Dates a year; 3rdrd Wednesday of Wednesday of March, June, September and December.March, June, September and December.

Exchange traded, price determined Exchange traded, price determined through market trading, Liquidity.through market trading, Liquidity.

Standard sizes (by Date).Standard sizes (by Date). Available only in a few currencies (Cross-Available only in a few currencies (Cross-

hedge).hedge). Daily settlement and Margin Daily settlement and Margin

Requirements.Requirements.

Forward ContractsForward Contracts

Written by BanksWritten by Banks Tailor Size and Date (large and precise, Tailor Size and Date (large and precise,

respectively). respectively). Traded Inter-BankTraded Inter-Bank No Settlement, only on Date.No Settlement, only on Date.

Our Homework AppliedOur Homework Applied

Remember the last assignment?Remember the last assignment? We buy 120 (E15 mil / E125,000) June Euro We buy 120 (E15 mil / E125,000) June Euro

Futures contracts at ($1.2247 * E125,000) * 120 Futures contracts at ($1.2247 * E125,000) * 120 costing us $18,370,500. costing us $18,370,500.

Break even (just on the contract) at $2.4494.Break even (just on the contract) at $2.4494. Current Profit = $629,500Current Profit = $629,500 Change in Account; (Buy Price – Settle) * Change in Account; (Buy Price – Settle) *

Contracted Amount.Contracted Amount. Maintain Margin Levels.Maintain Margin Levels.

Futures Time LineFutures Time Line

When hedging with a foreign currency there When hedging with a foreign currency there are three important dates that you must are three important dates that you must consider.consider.

t--------------t+n-------------------Tt--------------t+n-------------------T

Inception liquidation MaturityInception liquidation Maturity

Future Equation (To Maturity)Future Equation (To Maturity)

Gain(Loss)= X[(St+n- bSt) - (Zt+n,T-Zt,T)]Gain(Loss)= X[(St+n- bSt) - (Zt+n,T-Zt,T)]

X = Amount of ExposureX = Amount of Exposure

b= [1+it,t+n]1/a^/ [1+ i*t,t+n]1/a^ (The interest rate b= [1+it,t+n]1/a^/ [1+ i*t,t+n]1/a^ (The interest rate ratio)ratio)

a^= annualized factor for the interval from t to t+na^= annualized factor for the interval from t to t+n

(S t+n - bSt) = is the deviation of the future spot (S t+n - bSt) = is the deviation of the future spot exchange rate (or forward rate) at inception of the exchange rate (or forward rate) at inception of the position position

(Z t+n,T-Z t,T) = is the change the price of a futures (Z t+n,T-Z t,T) = is the change the price of a futures contract maturing time T, over the time period from ,t contract maturing time T, over the time period from ,t inception of the position, to t+n, liquidation of the inception of the position, to t+n, liquidation of the positionposition

Futures Equation 2Futures Equation 2

Previous equation was for a contract held Previous equation was for a contract held to maturity. to maturity.

If a futures contract is held to maturity, it is If a futures contract is held to maturity, it is the same as a forward contract.the same as a forward contract.

Why?Why?

Futures Equation (Not held to Futures Equation (Not held to Maturity)Maturity)

Gain (loss) =Gain (loss) =

X((St+n – bSt) – c (St+n –bSt)X((St+n – bSt) – c (St+n –bSt)

C isC is

C = (1+it+n,T)^1/a / (1+i*t+n,T)^1/aC = (1+it+n,T)^1/a / (1+i*t+n,T)^1/a

Futures Contracts (Not held to Futures Contracts (Not held to Maturity) 2Maturity) 2

Remaining time to maturity prices using Covered Remaining time to maturity prices using Covered Interest Parity.Interest Parity.

Interest rates at liquidation are not known in Interest rates at liquidation are not known in advance, and subject to change during the advance, and subject to change during the interval.interval.

Futures price has not had the full interval to Futures price has not had the full interval to converge to spot price.converge to spot price.

Optimal hedge involves 1/c units of foreign Optimal hedge involves 1/c units of foreign currency futures, since c(1/c) = 1.currency futures, since c(1/c) = 1.

C > 1 smaller amount, C < 1 larger amount.C > 1 smaller amount, C < 1 larger amount.

DifficultiesDifficulties

Using a hedge ratio of 1/c sets the Using a hedge ratio of 1/c sets the expected gain (loss) to zero, but does not expected gain (loss) to zero, but does not create a perfect hedge.create a perfect hedge.

C is stochasticC is stochastic Interest rates, etc. are unpredictable.Interest rates, etc. are unpredictable. Frequently adjusted.Frequently adjusted.

How much risk can we Hedge?How much risk can we Hedge?

% of un-hedged risk eliminated by futures % of un-hedged risk eliminated by futures contracts;contracts;

(1- (Var(St+n – bSt) – (Zt+n,T – Zt,T)) / (1- (Var(St+n – bSt) – (Zt+n,T – Zt,T)) / (Var(St+n – bSt))) * 100(Var(St+n – bSt))) * 100

Or as a % of open risk;Or as a % of open risk;

SQRT (Var(St+n – bSt) – (Zt+n,T – Zt,T)) / SQRT (Var(St+n – bSt) – (Zt+n,T – Zt,T)) / (Var(St+n – bSt))) * 100(Var(St+n – bSt))) * 100

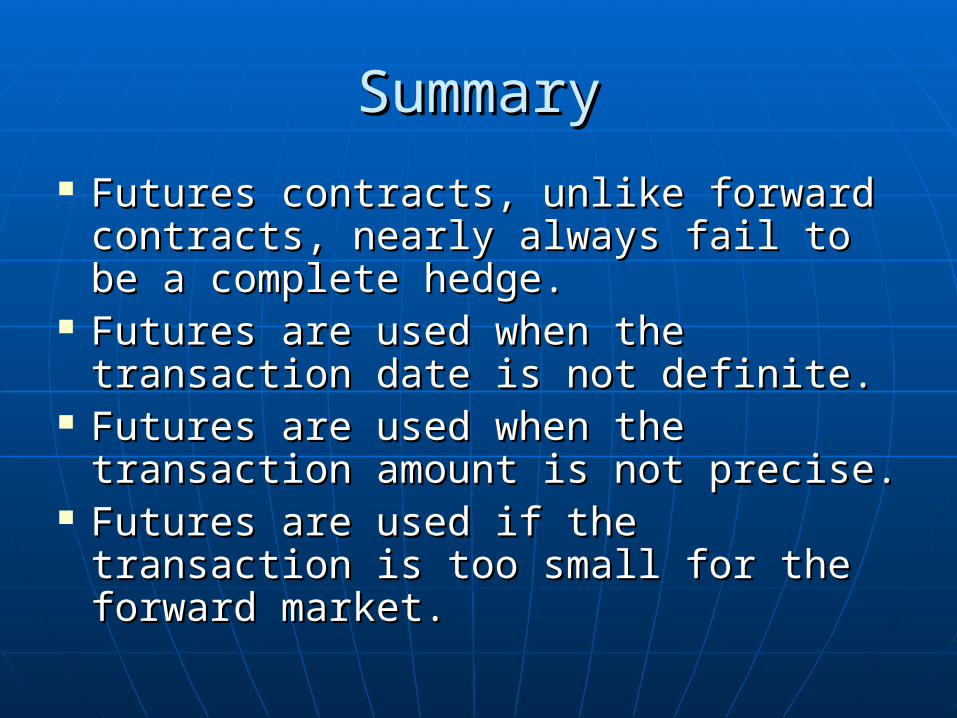

SummarySummary

Futures contracts, unlike forward Futures contracts, unlike forward contracts, nearly always fail to be a contracts, nearly always fail to be a complete hedge.complete hedge.

Futures are used when the transaction Futures are used when the transaction date is not definite.date is not definite.

Futures are used when the transaction Futures are used when the transaction amount is not precise.amount is not precise.

Futures are used if the transaction is too Futures are used if the transaction is too small for the forward market. small for the forward market.

OptionsOptions

Foreign Currency options: are financial Foreign Currency options: are financial contracts that give the holder the right, but contracts that give the holder the right, but not the obligation, to buy or sell a specified not the obligation, to buy or sell a specified amount of foreign currency on or before a amount of foreign currency on or before a specified maturity date.specified maturity date.

Types of OptionsTypes of Options• AmericanAmerican• European European

Calls and PutsCalls and Puts

CallsCalls• Gives the owner of the option the right but not Gives the owner of the option the right but not

the obligation to the obligation to buybuy currency at a specified currency at a specified exercise price (X)exercise price (X)

This is a This is a longlong position position PutsPuts

• Gives the owner of the option the right but not Gives the owner of the option the right but not the obligation to the obligation to sellsell currency at a specified currency at a specified exercise priceexercise price

This is a This is a shortshort position position

Why use an Option?Why use an Option?

Your exposure to foreign exchange rate Your exposure to foreign exchange rate risk is uncertainrisk is uncertain• We are not sure that our thief will succeedWe are not sure that our thief will succeed

If our thief fails we no longer have exchange If our thief fails we no longer have exchange exposureexposure

With Futures and Forwards we now will have an With Futures and Forwards we now will have an open positionopen position

You are uncertain about exchange rates in You are uncertain about exchange rates in the future and want to capture the upsidethe future and want to capture the upside• Allows you still to hedge against riskAllows you still to hedge against risk

Black Scholes Pricing Black Scholes Pricing

Developed by Fischer Black and Myron Developed by Fischer Black and Myron Scholes in 1973Scholes in 1973

AssumptionsAssumptions• European exercise terms are usedEuropean exercise terms are used• Markets are efficientMarkets are efficient• No commissionsNo commissions• Interest rates are known and remain constantInterest rates are known and remain constant

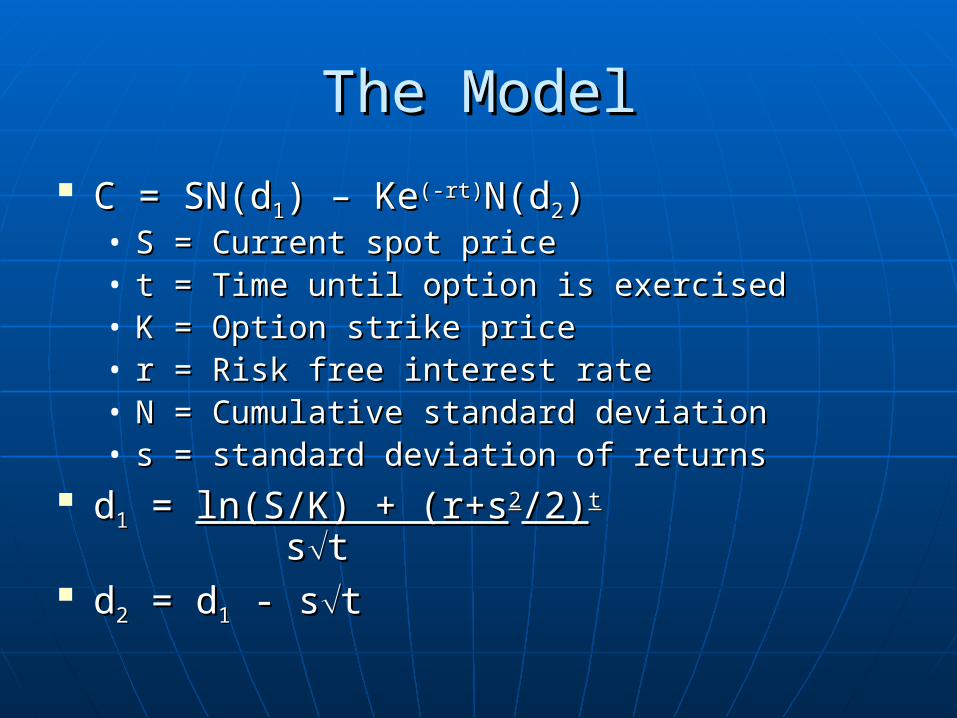

The ModelThe Model

C = SN(dC = SN(d11) – Ke) – Ke(-rt)(-rt)N(dN(d22))• S = Current spot priceS = Current spot price• t = Time until option is exercisedt = Time until option is exercised• K = Option strike priceK = Option strike price• r = Risk free interest rater = Risk free interest rate• N = Cumulative standard deviationN = Cumulative standard deviation• s = standard deviation of returnss = standard deviation of returns

dd11 = = ln(S/K) + (r+sln(S/K) + (r+s22/2)/2)tt

sstt dd22 = d = d11 - s - stt

Results of the ModelResults of the Model Spot price = 1.2178Spot price = 1.2178 Risk free rate = 4.75%Risk free rate = 4.75%62,500 Euro – European style62,500 Euro – European style

StrikeStrike DateDate Call Call Put Put11801180 JunJun 0.04660.0466 0.030.03

12001200 JunJun 0.02770.0277 0.0150.015

12201220 JunJun 0.01290.0129 0.0660.066

12401240 JunJun 0.0430.043 0.0180.018

How do we Hedge our Position?How do we Hedge our Position?

We are short We are short € 15,000,000€ 15,000,000• We need to take a long position to offset this positionWe need to take a long position to offset this position• This requires 240 contractsThis requires 240 contracts

€ € 62,500 each62,500 each

The price of each 1200 contract is $1,731.25The price of each 1200 contract is $1,731.25• Equals the number of Euros in the contract times Equals the number of Euros in the contract times

price per Europrice per Euro• Total price of the position = $415,500Total price of the position = $415,500

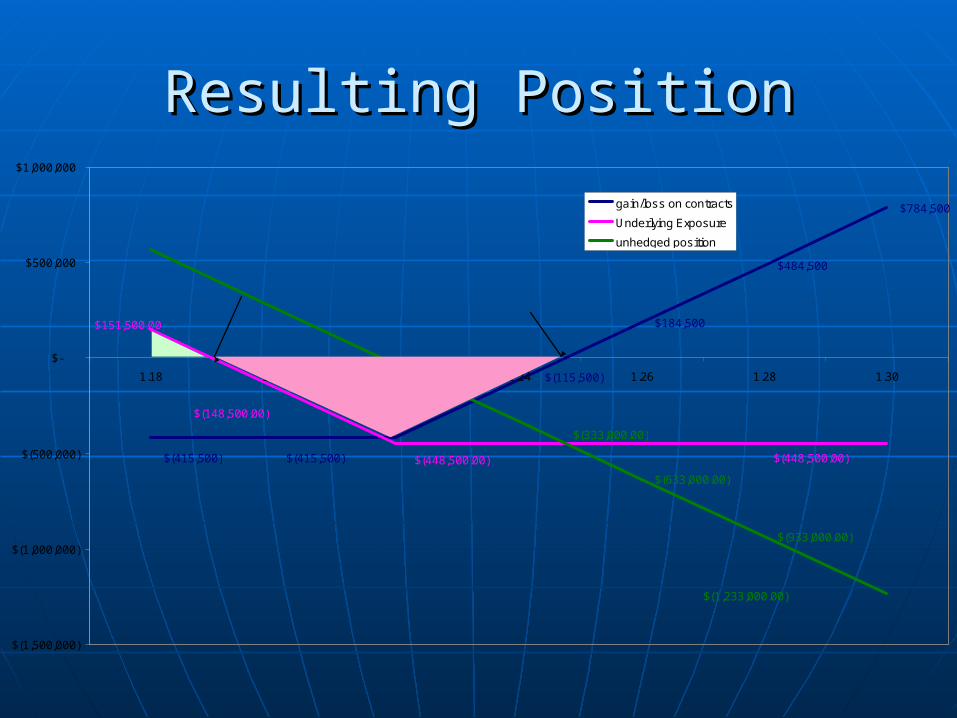

Our PositionOur Position

$184,500

$484,500

$784,500

$567,000.00

$267,000.00

$(633,000.00)

$(933,000.00)

$(115,500)

$(415,500)$(415,500)

$151,500.00

$(148,500.00)

$(448,500.00)$(448,500.00)

$(1,233,000.00)

$(333,000.00)

$(1,500,000)

$(1,000,000)

$(500,000)

$-

$500,000

$1,000,000

1.18 1.20 1.22 1.24 1.26 1.28 1.30

gain/loss on contracts

Underlying Exposure

unhedged position

Efective Rate = 1.2477

The Resulting PositionThe Resulting Position

The 1200 contract gives us an effective The 1200 contract gives us an effective rate of:rate of:• 1.2477 $/1.2477 $/€€

Why is this so much more than the Why is this so much more than the Forward contracts?Forward contracts?• Protects against the appreciation of the EuroProtects against the appreciation of the Euro• Allows for capture of falling Euro pricesAllows for capture of falling Euro prices• Locks in the maximum lossLocks in the maximum loss• No maximum gainNo maximum gain

Resulting PositionResulting Position

$184,500

$484,500

$784,500

$(633,000.00)

$(933,000.00)

$(415,500) $(415,500)

$(115,500)

$(448,500.00) $(448,500.00)

$(148,500.00)

$151,500.00

$(333,000.00)

$(1,233,000.00)

$(1,500,000)

$(1,000,000)

$(500,000)

$-

$500,000

$1,000,000

1.18 1.20 1.22 1.24 1.26 1.28 1.30

gain/loss on contracts

Underlying Exposure

unhedged position

Efective Rate = 1.2477Profit Point = 1.1901

ExitExit The foreign exchange options market is very The foreign exchange options market is very

liquidliquid Time of payment is not dependant upon the Time of payment is not dependant upon the

contract datecontract date• Execution of the options are not requiredExecution of the options are not required

Buy Buy € 15,000,000 at the spot rate€ 15,000,000 at the spot rate Sell 240, 1200 Euro Call optionsSell 240, 1200 Euro Call options

Final cost = $ 18,115,500 to $18,715,500Final cost = $ 18,115,500 to $18,715,500• Compare to $ 17,700,000 to $19,500,000 at original Compare to $ 17,700,000 to $19,500,000 at original

spot ratespot rate 1.18 $/€ to 1.30 $/€ 1.18 $/€ to 1.30 $/€

Methods of Offsetting the Price of Methods of Offsetting the Price of OptionsOptions

StraddleStraddle• Requires selling puts offsetting the gain when Requires selling puts offsetting the gain when

the price of the Euro falls against the dollarthe price of the Euro falls against the dollar The premium from the sale (price) offsets the cost The premium from the sale (price) offsets the cost

of the call optionsof the call options Generally used when both the call and the put are Generally used when both the call and the put are

bought and sold out of the moneybought and sold out of the money

• Straddle using the same strike price for both Straddle using the same strike price for both calls and putscalls and puts

Effectively creates a forward contractEffectively creates a forward contract

Questions?Questions?