hedge fund issues and performance 1 l6: hedge fund issues and performance

TRANSCRIPT

Hedge Fund Issues and Performance

1 L6: Hedge Fund Issues and Performance

Hedge Fund Performance 2008 was a watershed year in the hedge fund industry Assets under management (AUM) by hedge funds dropped by

unprecedented levels and the concept of managing for absolute returns (positive returns) was, in part, invalidated by significant losses

As a result of these losses, investor withdrawals increased substantially

This withdrawal activity, combined with reductions in asset values, resulted in a drop in AUM by approximately 25%, from almost $1.9 trillion at the end of 2007 to just over $1.4 trillion by the end of 2008

Part of the problem during 2008 was that too many funds bought the same assets and as markets fell, many hedge funds sold these assets to gain liquidity, pushing prices even lower

Compounding this problem was the need for some institutions to raise cash when the equity market decline caused minimum equity allocation benchmarks to be breached, triggering a need to take money out of hedge funds and reinvest directly in equity instruments.

2 L6: Hedge Fund Issues and Performance

Hedge Fund Performance The Fund Weighted Composite Index tracked by Hedge Fund

Research (HFR) fell by 19.0% during the year compared to the drop in Standard & Poor’s 500 stock index of 38.5%, including dividends

Therefore, even though hedge fund losses were significant, they were substantially less than the broader equity market

2008 marked only the second calendar year of negative returns for hedge funds since 1990

Approximately two thirds of the decline in assets during 2008 was a result of poor hedge fund performance and the remaining one-third came from clients withdrawing their assets

Fund of hedge funds underperformed hedge funds, losing 21.3% for the year.

Despite the overall poor performance, however, it is important to reemphasize that hedge funds (both in aggregate and across the major investment strategies) still outperformed the broader market

3 L6: Hedge Fund Issues and Performance

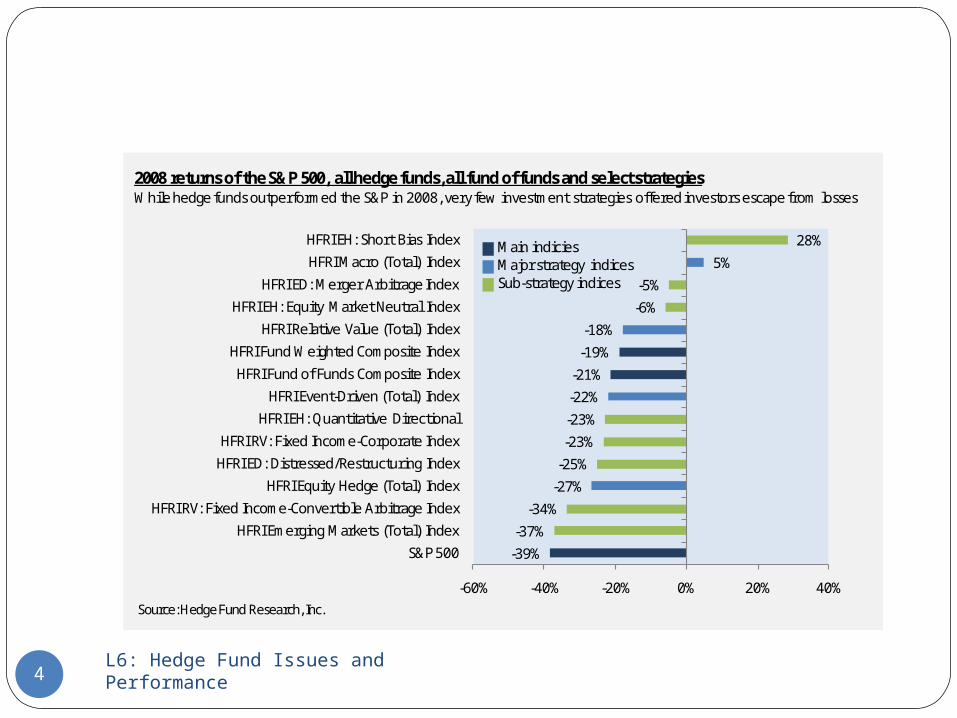

2008 returns of the S&P 500, all hedge funds, all fund of funds and select strategiesWhile hedge funds outperformed the S&P in 2008, very few investment strategies offered investors escape from losses

Source: Hedge Fund Research, Inc.

-39%

-37%

-34%

-27%

-25%

-23%

-23%

-22%

-21%

-19%

-18%

-6%

-5%

5%

28%

-60% -40% -20% 0% 20% 40%

S&P 500

HFRI Emerging Markets (Total) Index

HFRI RV: Fixed Income-Convertible Arbitrage Index

HFRI Equity Hedge (Total) Index

HFRI ED: Distressed/Restructuring Index

HFRI RV: Fixed Income-Corporate Index

HFRI EH: Quantitative Directional

HFRI Event-Driven (Total) Index

HFRI Fund of Funds Composite Index

HFRI Fund Weighted Composite Index

HFRI Relative Value (Total) Index

HFRI EH: Equity Market Neutral Index

HFRI ED: Merger Arbitrage Index

HFRI Macro (Total) Index

HFRI EH: Short Bias Index Main indiciesMajor strategy indicesSub-strategy indices

4 L6: Hedge Fund Issues and Performance

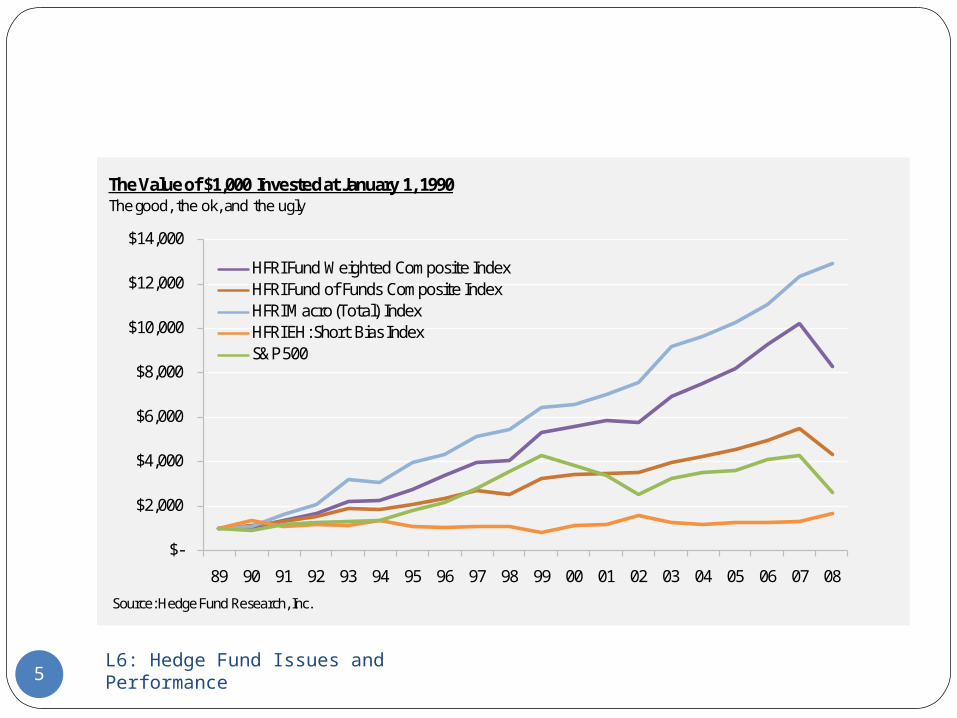

The Value of $1,000 Invested at January 1, 1990The good, the ok, and the ugly

Source: Hedge Fund Research, Inc.

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

HFRI Fund Weighted Composite IndexHFRI Fund of Funds Composite IndexHFRI Macro (Total) IndexHFRI EH: Short Bias IndexS&P 500

5 L6: Hedge Fund Issues and Performance

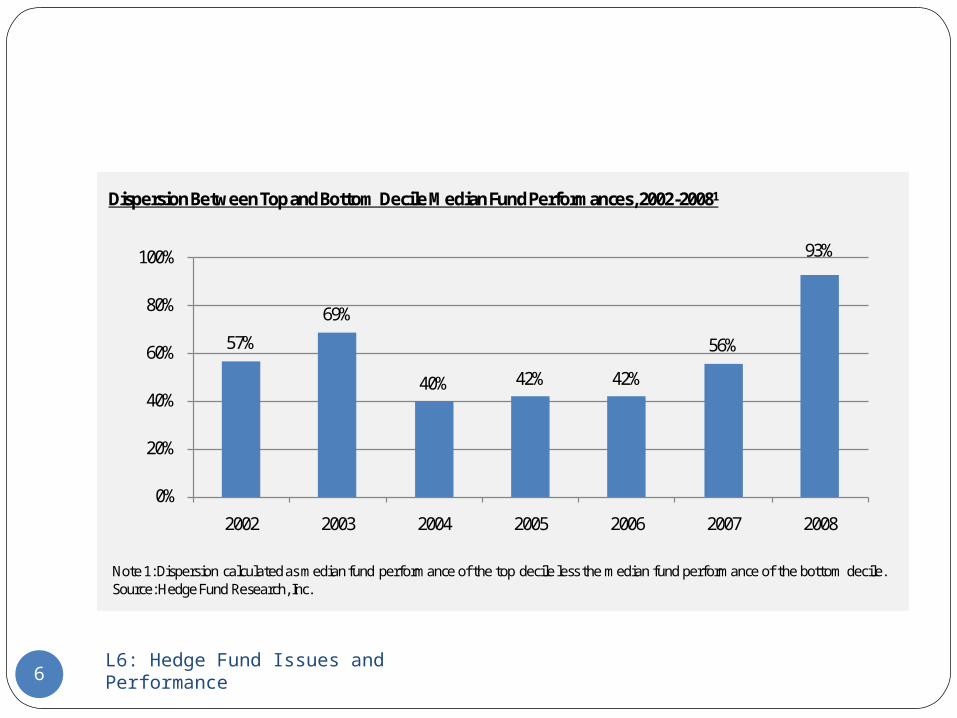

Dispersion Between Top and Bottom Decile Median Fund Performances, 2002-20081

Note 1: Dispersion calculated as median fund performance of the top decile less the median fund performance of the bottom decile.Source: Hedge Fund Research, Inc.

57%

69%

40% 42% 42%

56%

93%

0%

20%

40%

60%

80%

100%

2002 2003 2004 2005 2006 2007 2008

6 L6: Hedge Fund Issues and Performance

Searching For Returns Hedge funds have traditionally been associated with “alpha based”

returns which are independent of market conditions, but, increasingly, hedge funds participate in the same investment activity as traditional fund managers

To differentiate themselves, hedge fund managers have had to search for new sources of returns in new markets, but this search has pushed them into less liquid investments, including private equity investments and other private transactions

This activity extends their investment horizon, requires longer lock-ups and results in the need to hire new managers who have long-term investment expertise

Hedge funds have become active participants in leveraged bank loans, mezzanine financings, insurance-linked securities and in LBO transactions

In other words, hedge funds have moved a significant amount of their investment base from public transactions to private transactions in their search for alpha-based returns

7 L6: Hedge Fund Issues and Performance

Fund of Funds 2008 ended on a bad note with the disclosure of over $20 billion in

losses experienced by those who invested in Bernard Madoff’s investment funds

While Madoff wasn’t a hedge fund manager, a number of fund of funds that allocate investor money to hedge funds also allocated money to Madoff through feeder funds

This created concern about the quality of fund of funds due diligence processes and the ensuing crisis of confidence in fund of funds resulted in many investors withdrawing money from these funds, which in turn, caused money to be taken out of hedge funds

Fund of funds have sold themselves to investors on the basis that they offer three key benefits: diversification, access to sought-after managers and due diligence

The financial crisis weakened the first two benefits from the perspective of many investors

The Madoff scandal significantly undermined the third benefit

8 L6: Hedge Fund Issues and Performance

Fund of Funds Compounding the difficulties of fund of funds was the leverage

employed by these funds. Many fund of funds borrowed money to supplement investor money

when they made investments in various hedge funds Since most of the hedge funds they invested in were already leveraged,

this doubling up of leverage created enhanced losses beyond the losses of the underlying funds

In part, because of this leverage, average losses from fund of hedge funds during 2008 were 21%, compared to average losses for hedge funds of 19%

With lenders retracting credit, fund of funds were forced to dump assets, putting further pressure on hedge funds and the markets in general

As a result, a number of high profile hedge funds liquidated or froze redemptions during 2008, traumatizing the investor base and triggering additional requests for redemption by some investors who sought liquidity wherever they could find it (even from hedge funds that were generating positive returns)

9 L6: Hedge Fund Issues and Performance

Benefits Revisited Historically, hedge fund managers have articulated the

following benefits for investors who place money in their funds Attractive risk-adjusted returns, focusing on positive

returns, low volatility and capital preservationLow correlation with major equity and bond marketsInvestment flexibility to invest long or short, using a

variety of instruments, investing in segments of the market that suffer from structural inefficiencies and in smaller asset pools

Focus on marketable securitiesStructural advantages including performance-based

compensation, managers’ personal investment (which aligned interests) and the ability to attract the “best and brightest”

10 L6: Hedge Fund Issues and Performance

Benefits Revisited An analysis of these benefits in light of the major dislocations

of the market during 2007 and 2008 suggests the following about hedge fundsAchievement of positive (absolute) returns has become a

problematic objective during periods of major market dislocation

Achievement of low correlation with major equity and bond markets is difficult to obtain during periods of major market dislocation

Investment flexibility continues to be a major benefit of hedge funds

Some hedge funds have invested a portion of their assets in nonmarketable securities, creating a mismatch between asset maturities and investor withdrawal requirements

Structural advantages, including performance-based compensation and aligned interests

11 L6: Hedge Fund Issues and Performance

Transparency Hedge fund investors historically have not required a significant amount of

investment transparency from hedge fund managers Many investors are now pushing for greater position-level transparency,

but some managers resist this based on their concern that disclosure of strategies will benefit competitors and cause arbitrage opportunities to disappear

Managers are generally willing to provide organizational and process transparency regarding assets under management, profit and loss attribution, key investment themes, new product initiatives, and personnel

In addition, risk transparency is usually provided through disclosure of credit exposure, volatility exposure, long verses short positions, leverage, geographic focus, portfolio concentration, industry focus and market capitalization focus

However, hedge fund managers will attempt to keep specific investment strategies, ideas, and short positions confidential, so investors must decide whether the level of overall transparency provided is adequate in the context of the risks and benefits associated with investing in hedge funds

12 L6: Hedge Fund Issues and Performance

Fees Following the poor industry performance during 2008, some hedge

funds decided to reduce fees from 2% to 1% Renaissance Technologies, one of the largest and most successful

hedge funds, waived all management fees for 2009 for its Renaissance Institutional Futures fund and the fund agreed to not receive any performance fees until 2008 losses of 12% were recovered

Other funds, including Highbridge Capital Management, launched new share classes with lower fees in exchange for longer lock-up periods

At the end of 2008, Citadel Investment Group gave back about $300 million in fees it had previously collected, after completing a money-losing year and other firms also gave back fees and remained committed to not receiving performance fees until they reached their high water marks

At some funds, fee cuts came principally from performance fees, rather than management fees, based on the view that management fees are essential to keeping the funds operational

13 L6: Hedge Fund Issues and Performance

High Water Mark A hedge fund high water mark is a mechanism that is implemented

to make sure that managers do not take a performance fee in the current period when the fund has had negative performance over previous performance fee periods

The high water mark is the colloquial term for a “cumulative loss account”

A cumulative loss account starts with a zero balance at the beginning of any performance period (monthly, quarterly, or yearly, as determined by the firm) and it records net losses during that period

It was estimated that only one in 10 hedge funds received performance fees during 2008 because of losses and application of high water marks

This created significant compensation pressures for many funds since their management fees were insufficient to keep the business going, which resulted in significant downsizing of headcount and office space

14 L6: Hedge Fund Issues and Performance

High Water Mark The high water mark may create a perverse incentive for the

hedge fund manager to either take extra risk to generate returns high enough to deplete the cumulative loss account so that a performance fee will be paid, or to close down the fund and start again

Both of these actions could be damaging to investors, forcing them to either make a redemption at an inopportune time, or continue with their investment with a potentially higher risk profile

If a hedge fund manager shuts down a fund, the investor might suffer disproportionate losses as assets are sold in a fire sale environment

However, to keep money invested in the fund under a higher risk profile may also not be in the investor’s best interest and taking money out to invest with another manager might subject the investor to the same high water mark issue

15 L6: Hedge Fund Issues and Performance

High Water Mark As a result of this conundrum, in some cases, it might make

sense for investors to consider modification of the high water mark

An alternative to the standard hedge fund high water mark is a modified high water mark: resetting the high water mark to the current fund level under circumstances where to do so better aligns everyone’s interest, amortizing losses over a several year period to enable some modest level of performance fees during this period, or rolling the high water mark over a more extended period

A modified high water mark may create value for investors by keeping a manager in the game and reducing the incentive of the manager to take excessive risk

As a quid pro quo, some hedge fund managers may be willing to accept lower performance fees

16 L6: Hedge Fund Issues and Performance

High Water MarkHigh Water Mark Example

An example of the mechanical application of the cumulative loss account and high water mark calculation is below:

Hedge fund NAV 01/01/06: $1,000,000

Hedge fund NAV 12/31/06: $1,200,000 (total after expenses, including the management fee expense)Gain: $200,000Less Performance fee: $40,000 [20% of $200,000]Cumulative loss account: $0

Hedge fund NAV 01/01/07: $1,160,000

Hedge fund NAV 12/31/07: $1,000,000 (total after expenses, including the management fee expense)Gain: ($160,000)Less Performance fee: $0Cumulative loss account: $160,000

Hedge fund NAV 01/01/08: $1,000,000Hedge fund NAV 12/31/08 $1,100,000 (total after expenses, including the management fee expense)Gain: $100,000Less Performance fee: $0Cumulative loss account: $60,000

Hedge fund NAV 01/01/09: $1,100,000

Hedge fund NAV 12/31/09 $1,300,000 (total after expenses, including the management fee expense)Gain: $200,000Less Performance fee: $28,000 [20% of $140,000]Cumulative loss account: $0

The concept of the high water mark is theoretically similar to the "claw-back" provision found in many private equity funds in that its purpose is to make sure the manager is not overcompensated for underperformance. However, the high water mark is distinctly different in that it is prospective in nature (whereas the claw-back is retrospective in nature). The high water mark is applied to a hedge fund manager on a going forward basis and so the manager will need to get the fund's account back up to the high water mark before a performance fee can be taken.

17 L6: Hedge Fund Issues and Performance

Merging of Functions Hedge funds, private equity funds and investment banks compete against

each other and are, at the same time, major sources of revenue for each other

Each of the largest participants in these three industries conducts business activities in all three areas

Goldman Sachs has an industry leading sales and trading business, providing trading and lending services to hedge funds and a large investment banking business that provides services to private equity funds

In fact, private equity funds and hedge funds are the two most important clients of Goldman Sachs’ investment banking division and trading division, respectively

In addition, Goldman Sachs historically conducted one of the world’s largest hedge fund businesses between their proprietary trading desk and their Asset Management Division and one of the world’s largest private equity businesses between their principal investment area and their Asset Management Division

As a result, Goldman Sachs is both an important provider of services to hedge funds and private equity funds, as well as one of their principal competitors

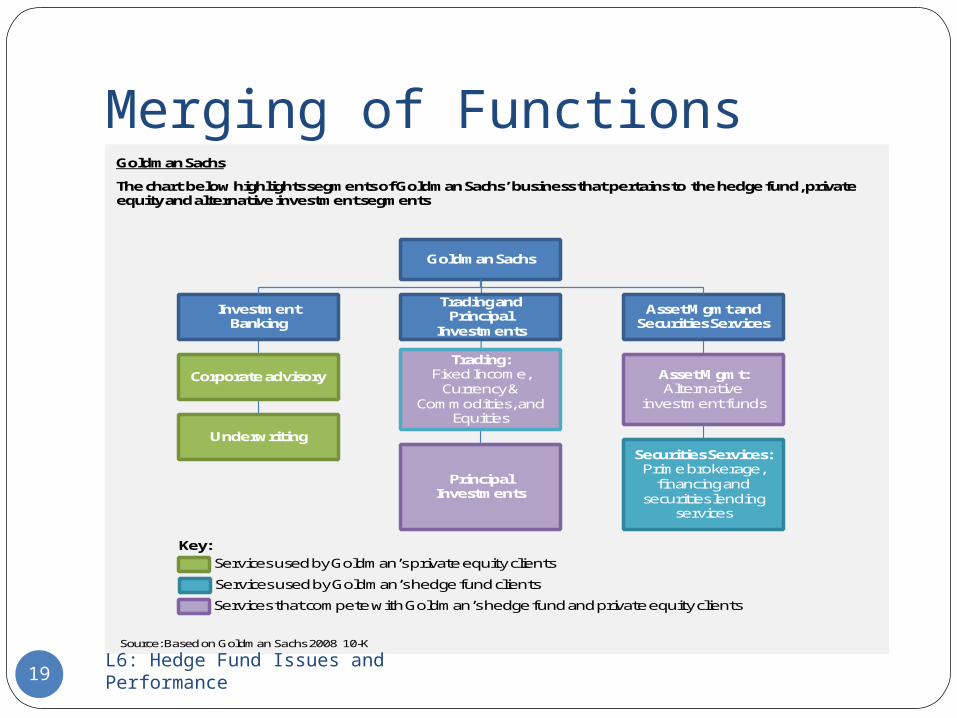

18 L6: Hedge Fund Issues and Performance

Merging of FunctionsGoldman Sachs

The chart below highlights segments of Goldman Sachs’ business that pertains to the hedge fund, private equity and alternative investment segments

Goldman Sachs

Investment Banking

Trading and Principal

Investments

Asset Mgmt and Securities Services

Securities Services: Prime brokerage,

financing and securities lending

services

Asset Mgmt:Alternative

investment funds

Corporate advisory

Underwriting

Services used by Goldman’s private equity clients

Services used by Goldman’s hedge fund clients

Services that compete with Goldman’s hedge fund and private equity clients

Trading: Fixed Income,

Currency & Commodities, and

Equities

Principal Investments

Key:

Source: Based on Goldman Sachs 2008 10-K

19 L6: Hedge Fund Issues and Performance

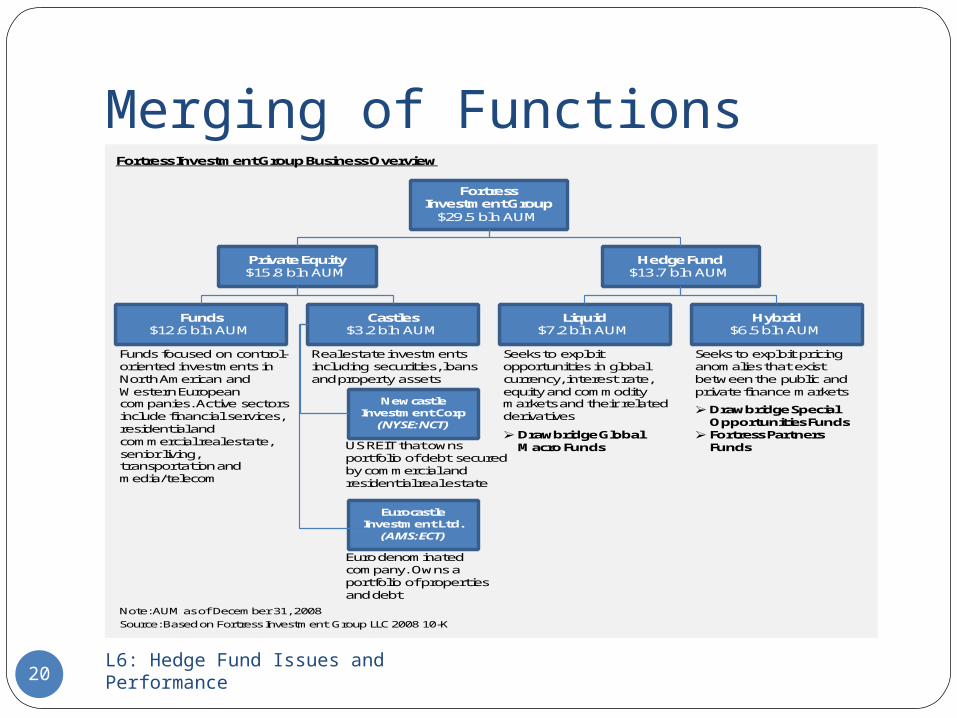

Merging of FunctionsFortress Investment Group Business Overview

Fortress Investment Group

$29.5 bln AUM

Castles$3.2 bln AUM

Private Equity$15.8 bln AUM

Funds$12.6 bln AUM

Newcastle Investment Corp

(NYSE:NCT)

Eurocastle Investment Ltd.

(AMS:ECT)

Hybrid$6.5 bln AUM

Hedge Fund$13.7 bln AUM

Liquid$7.2 bln AUM

Real estate investments including securities, loans and property assets

US REIT that owns portfolio of debt secured by commercial and residential real estate

Euro denominated company. Owns a portfolio of properties and debt

Funds focused on control-oriented investments in North American and Western European companies. Active sectors include financial services, residential and commercial real estate, senior living, transportation and media/telecom

Seeks to exploit opportunities in global currency, interest rate, equity and commodity markets and their related derivatives

Drawbridge Global Macro Funds

Seeks to exploit pricing anomalies that exist between the public and private finance markets

Drawbridge Special Opportunities Funds

Fortress Partners Funds

Source: Based on Fortress Investment Group LLC 2008 10-KNote: AUM as of December 31, 2008

20 L6: Hedge Fund Issues and Performance

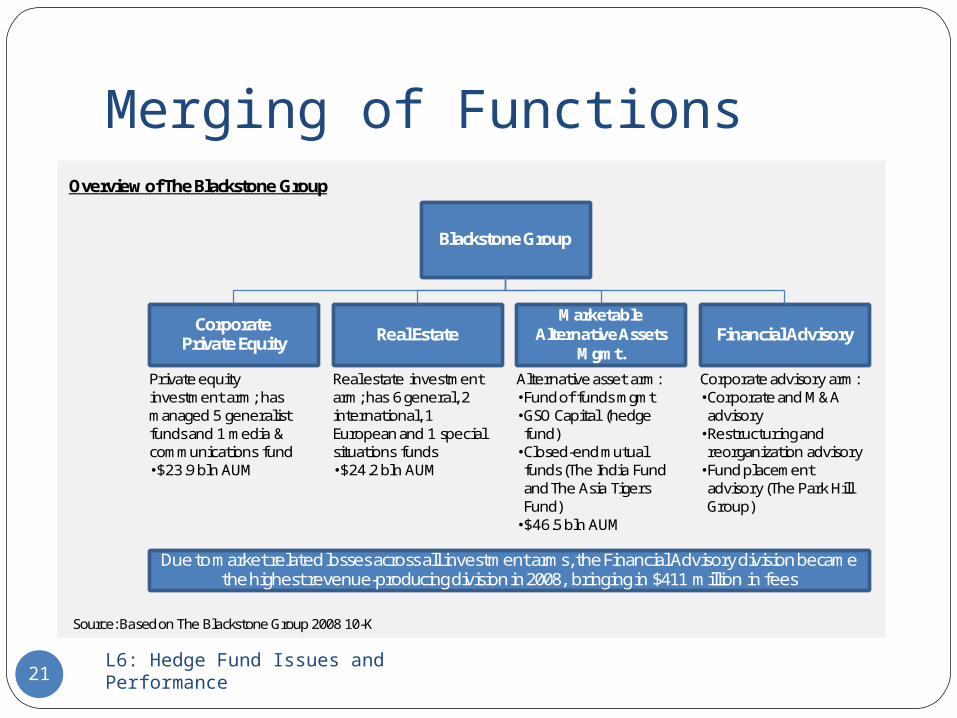

Merging of FunctionsOverview of The Blackstone Group

Blackstone Group

Corporate Private Equity Real Estate

Marketable Alternative Assets

Mgmt.Financial Advisory

Private equity investment arm; has managed 5 generalist funds and 1 media & communications fund•$23.9 bln AUM

Real estate investment arm; has 6 general, 2 international, 1 European and 1 special situations funds•$24.2 bln AUM

Alternative asset arm: •Fund of funds mgmt•GSO Capital (hedge

fund)•Closed-end mutual

funds (The India Fund and The Asia Tigers Fund)•$46.5 bln AUM

Corporate advisory arm:•Corporate and M&A

advisory•Restructuring and

reorganization advisory•Fund placement

advisory (The Park Hill Group)

Due to market related losses across all investment arms, the Financial Advisory division became the highest revenue-producing division in 2008, bringing in $411 million in fees

Source: Based on The Blackstone Group 2008 10-K

21 L6: Hedge Fund Issues and Performance

Future Developments Hedge funds suffered significant pain during 2007-2009: redemptions

created loss of income and forced sales of assets that compounded losses, fees were reduced as performance waned, regulators reached toward greater regulation and more taxes, and many investors became concerned with the hedge fund model. As a result, a number of significant, lasting developments have occurred:Hedge funds have more limited access to leveraged financing,

which, in particular, impacts convertible arbitrage, fixed income arbitrage and statistical arbitrage investment strategies

The ability to maintain confidentiality over investment strategies has been reduced as investors demand more transparency and liquidity

Losses, gates and fraud have forced hedge funds to become more open in their activities and more willing to share details of their business and associated risks with investors

Fees have been reduced from the typical 2/20 schedule to a lesser fee system that allows greater returns to investors and acknowledges the lower return environment

22 L6: Hedge Fund Issues and Performance

Future Developments (continued)

The decline in alpha is well documented and many hedge funds are now viewed as creating diversified beta instead of finding significant returns from market inefficiencies

This still represents value added, but differentiation from many well-managed traditional investment funds is more difficult

Hedge funds are subject to additional regulatory constraints, which limit somewhat their flexibility, especially in long/short equity, event driven and other equity based strategies

A less favorable tax environment will result in reduction in after-tax compensation received by hedge fund managers

As hedge funds adjust to the new realities of the market they are developing longer lock-up arrangements that better match the lengthening maturity profile of their investments, enabling them, in turn, to expand long-term investment activity to take advantage of higher yields available for patient capital

The balance of power has shifted from general partners to limited partners The result is that limited partners have been successful in obtaining better

transparency, improved liquidity and the other benefits described above

23 L6: Hedge Fund Issues and Performance