healthcare reform: an update and it's tax effect on your firm

TRANSCRIPT

Health Reform: The Tax Effect

FDR’s New Deal – Social Security introduced; FICA Tax

Social Security and Medicare

History of FICA (Federal Insurance Contributions Tax) as Imposed on Wages

No federally mandated benefits

Lyndon Johnson and Congress - Medicare passed

1920’s………………………………….1933………………………………………………….1965………………………………………………………………….2013 (Health Care Reform)

Affordable Care Act – 3.8% on investment income; .9% additional Medicare

Decoupling of Medicare Tax from Social Security Tax

No limit on Medicare tax paid @ 1.45%

Now, based on AGI limit, additional .9% for total of 2.35%

AGI limits - $200k single, $250k married filing jointly (MFJ)

It’s Complicated, but...

Rate is 3.8% on

Lesser of Net Investment Income or amount by which AGI exceeds $250k MFJ, $200k single

So,

Possible top rate is:39.6% 3.8%43.4%

Add MD 9.0%52.4%

Net Investment Income Tax (NIIT Tax)

Interest

Dividends

Rents

Royalties

Capital Gains

Passive Activities

What is Net Investment Income?

Salaries

Self Employment Income

Non-Passive Business Income

Social Security

Tax-exempt Interest

Qualified Pension Income

IRA Distributions

Annuity Income

What is not Net Investment Income?

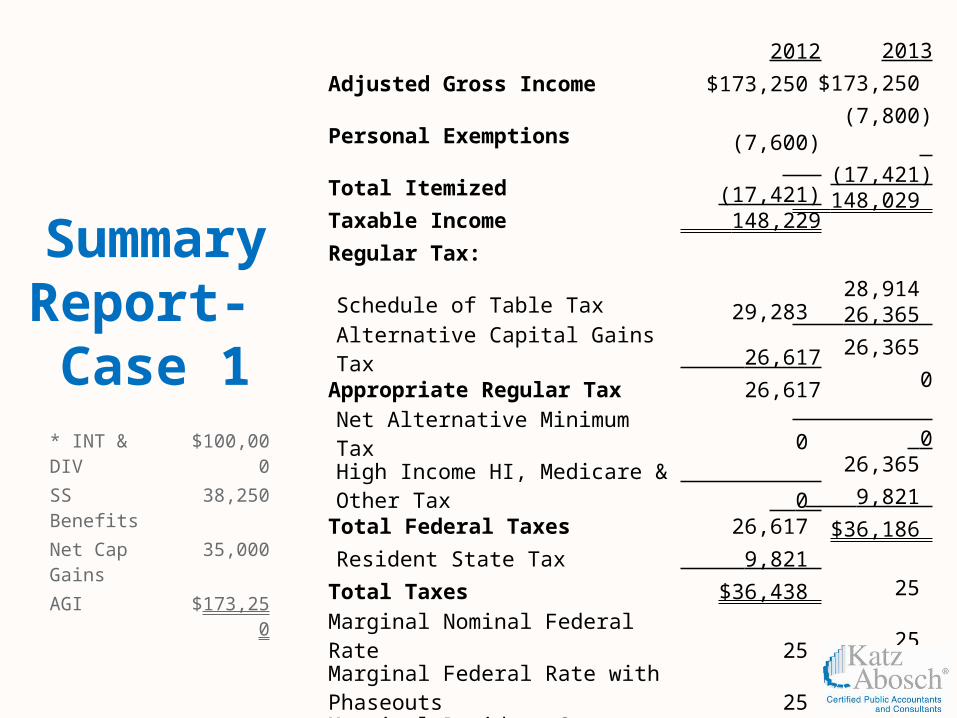

Summary Report- Case 1

2012

Adjusted Gross Income $173,250

Personal Exemptions (7,600)

Total Itemized (17,421)

Taxable Income 148,229

Regular Tax:

Schedule of Table Tax 29,283

Alternative Capital Gains Tax 26,617

Appropriate Regular Tax 26,617

Net Alternative Minimum Tax 0

High Income HI, Medicare & Other Tax 0

Total Federal Taxes 26,617

Resident State Tax 9,821

Total Taxes $36,438

Marginal Nominal Federal Rate 25

Marginal Federal Rate with Phaseouts 25

Marginal Resident State Rate 8

2013

$173,250

(7,800)

(17,421)

148,029

28,914

26,365

26,365

0

0

26,365

9,821

$36,186

25

25

8

* INT & DIV $100,000

SS Benefits 38,250

Net Cap Gains 35,000

AGI $173,250

Summary Report- Case 2

2012

Adjusted Gross Income $373,250

Personal Exemptions (7,600)

Total Itemized (34,725)

Taxable Income 330,925

Regular Tax:

Schedule of Table Tax 86,112

Alternative Capital Gains Tax 81,612

Appropriate Regular Tax 81,612

Net Alternative Minimum Tax 9,341

High Income HI, Medicare & Other Tax 0

Total Federal Taxes 90,953

Resident State Tax 27,125

Total Taxes $118,078

Marginal Nominal Federal Rate 28

Marginal Federal Rate with Phaseouts 35

Marginal Resident State Rate 9

2013

$373,250

(3,120)

(32,570)

337,560

87,708

83,208

83,208

6,808

4,684

94,700

27,168

$121,868

28

35

9

*$200,000 additional INT & DIV.

Summary Report- Case 3

2012

Adjusted Gross Income $623,250

Personal Exemptions (7,600)

Total Itemized (57,100)

Taxable Income 558,550

Regular Tax:

Schedule of Table Tax 164,632

Alternative Capital Gains Tax 159,632

Appropriate Regular Tax 159,632

Net Alternative Minimum Tax 7,820

High Income HI, Medicare & Other Tax 0

Total Federal Taxes 167,452

Resident State Tax 49,500

Total Taxes $216,952

Marginal Nominal Federal Rate 28

Marginal Federal Rate with Phaseouts 28

Marginal Resident State Rate 9

2013

$623,250

0

(47,517)

_575,733

175,636

170,736

170,736

0

_ 10,646

181,382

49,615

$230,997

40

41

9

*$250,000 wages added

Small Business Tax Credit

No more than 25 full-time equivalent employees Average annual wages for the employees cannot

exceed $50,000 in 2014, (will be adjusted for inflation)

Must purchase coverage through the SHOP Marketplace (Small Business Health Options)

Credit = to approx. 50% of employer contributions to health care premium

Available to certain eligible employees

Must cover at least 50% of the cost of employee-only coverage for each employee

Medical Device Excise Tax

Only for manufacturers and importers of “medical devices”

Confusion in definition of taxable “medical device”Must be “intended for humans”Retail exemption i.e. eyeglasses, contact, hearing aids,

etc.

Rate 2.3%

Annual Fee on Health Insurance Providers

In 2014, the fee is $5.25 per member per month ($63 per year)Includes not only the employee, but dependents – ALL COVERED LIVES

In 2015, the fee is $3.67 per member per month ($44 per year)Insurers will raise premiums to pass on to customers

• Assessed on insurance carriers, HMO’s, etc.

• Fee is NOT tax deductible

• First year is 2014

• Fee is permanent

PCORI Fee – Patient-Centered Outcomes Research Institute Fee

Period – 2012 to 2019

Amount $1 to $2 per member per year

Insurers have/will add to premium

THANK YOU!

Contact Info:

Steven Gershman, CPA, PFS, CFEShareholder443.539.3201sgershman@katzabosch.comwww.katzabosch.com