healthcare proactive deal identification tracker

TRANSCRIPT

Sample – Disguised and AbridgedDigital Transformations

Sample Deliverable

Healthcare Proactive Deal Identification TrackerSub-segment Prioritisation Analysis

Table of Contents▪ Module I: Ophthalmic and Optical Devices

Segment Prioritisation

▪ Module II: Healthcare Segments Prioritisation

© RocSearch. All Rights Reserved. 3

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation

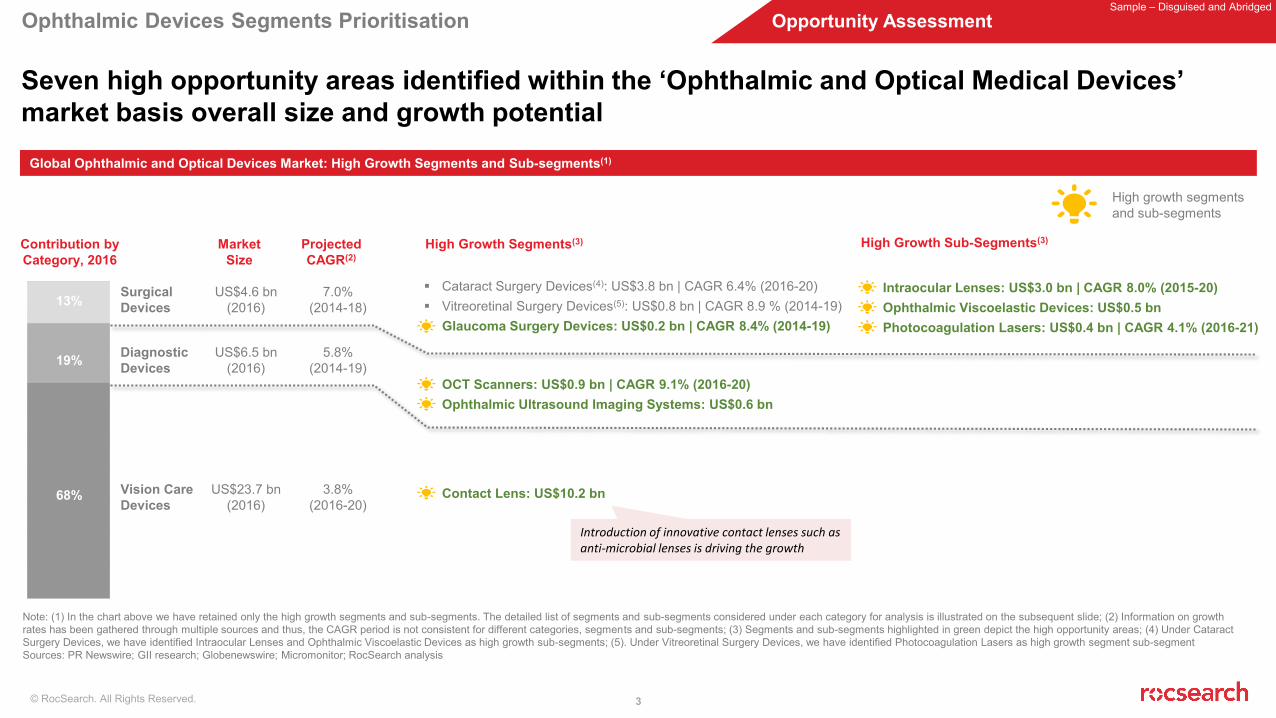

Seven high opportunity areas identified within the ‘Ophthalmic and Optical Medical Devices’ market basis overall size and growth potential

Opportunity Assessment

Note: (1) In the chart above we have retained only the high growth segments and sub-segments. The detailed list of segments and sub-segments considered under each category for analysis is illustrated on the subsequent slide; (2) Information on growth rates has been gathered through multiple sources and thus, the CAGR period is not consistent for different categories, segments and sub-segments; (3) Segments and sub-segments highlighted in green depict the high opportunity areas; (4) Under Cataract Surgery Devices, we have identified Intraocular Lenses and Ophthalmic Viscoelastic Devices as high growth sub-segments; (5). Under Vitreoretinal Surgery Devices, we have identified Photocoagulation Lasers as high growth segment sub-segmentSources: PR Newswire; GII research; Globenewswire; Micromonitor; RocSearch analysis

Global Ophthalmic and Optical Devices Market: High Growth Segments and Sub-segments(1)

Vision Care Devices

DiagnosticDevices

Surgical Devices

Contribution by Category, 2016

13%

19%

68%

Market Size

ProjectedCAGR(2)

US$23.7 bn(2016)

US$6.5 bn(2016)

US$4.6 bn(2016)

3.8%(2016-20)

5.8%(2014-19)

7.0% (2014-18)

High Growth Segments(3) High Growth Sub-Segments(3)

High growth segments and sub-segments

Introduction of innovative contact lenses such as anti-microbial lenses is driving the growth

▪ Intraocular Lenses: US$3.0 bn | CAGR 8.0% (2015-20)▪ Ophthalmic Viscoelastic Devices: US$0.5 bn▪ Photocoagulation Lasers: US$0.4 bn | CAGR 4.1% (2016-21)

▪ Cataract Surgery Devices(4): US$3.8 bn | CAGR 6.4% (2016-20)▪ Vitreoretinal Surgery Devices(5): US$0.8 bn | CAGR 8.9 % (2014-19)▪ Glaucoma Surgery Devices: US$0.2 bn | CAGR 8.4% (2014-19)

▪ OCT Scanners: US$0.9 bn | CAGR 9.1% (2016-20)▪ Ophthalmic Ultrasound Imaging Systems: US$0.6 bn

▪ Contact Lens: US$10.2 bn

© RocSearch. All Rights Reserved. 4

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation

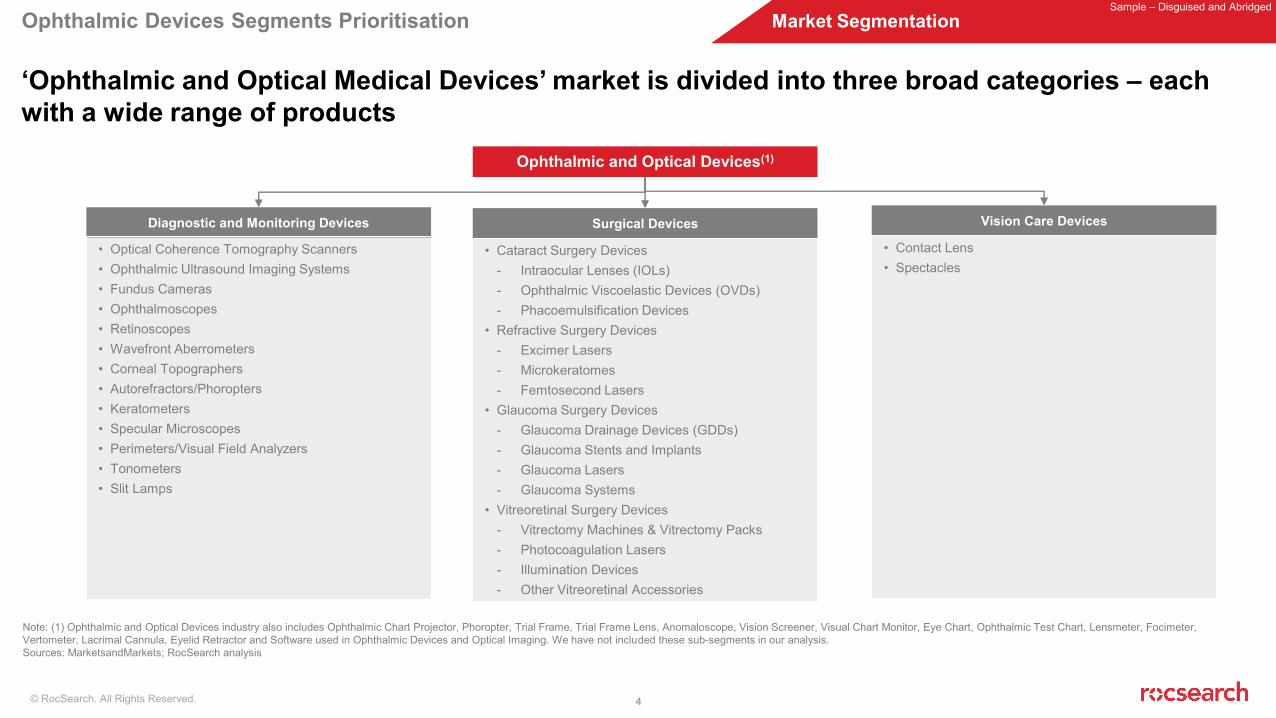

‘Ophthalmic and Optical Medical Devices’ market is divided into three broad categories – each with a wide range of products

Market Segmentation

Ophthalmic and Optical Devices(1)

Diagnostic and Monitoring Devices Surgical Devices Vision Care Devices

• Optical Coherence Tomography Scanners• Ophthalmic Ultrasound Imaging Systems• Fundus Cameras• Ophthalmoscopes• Retinoscopes• Wavefront Aberrometers• Corneal Topographers• Autorefractors/Phoropters• Keratometers• Specular Microscopes• Perimeters/Visual Field Analyzers• Tonometers• Slit Lamps

• Cataract Surgery Devices- Intraocular Lenses (IOLs)- Ophthalmic Viscoelastic Devices (OVDs)- Phacoemulsification Devices

• Refractive Surgery Devices- Excimer Lasers- Microkeratomes- Femtosecond Lasers

• Glaucoma Surgery Devices- Glaucoma Drainage Devices (GDDs)- Glaucoma Stents and Implants- Glaucoma Lasers- Glaucoma Systems

• Vitreoretinal Surgery Devices- Vitrectomy Machines & Vitrectomy Packs- Photocoagulation Lasers- Illumination Devices- Other Vitreoretinal Accessories

• Contact Lens• Spectacles

Note: (1) Ophthalmic and Optical Devices industry also includes Ophthalmic Chart Projector, Phoropter, Trial Frame, Trial Frame Lens, Anomaloscope, Vision Screener, Visual Chart Monitor, Eye Chart, Ophthalmic Test Chart, Lensmeter, Focimeter, Vertometer, Lacrimal Cannula, Eyelid Retractor and Software used in Ophthalmic Devices and Optical Imaging. We have not included these sub-segments in our analysis.Sources: MarketsandMarkets; RocSearch analysis

© RocSearch. All Rights Reserved. 5

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation

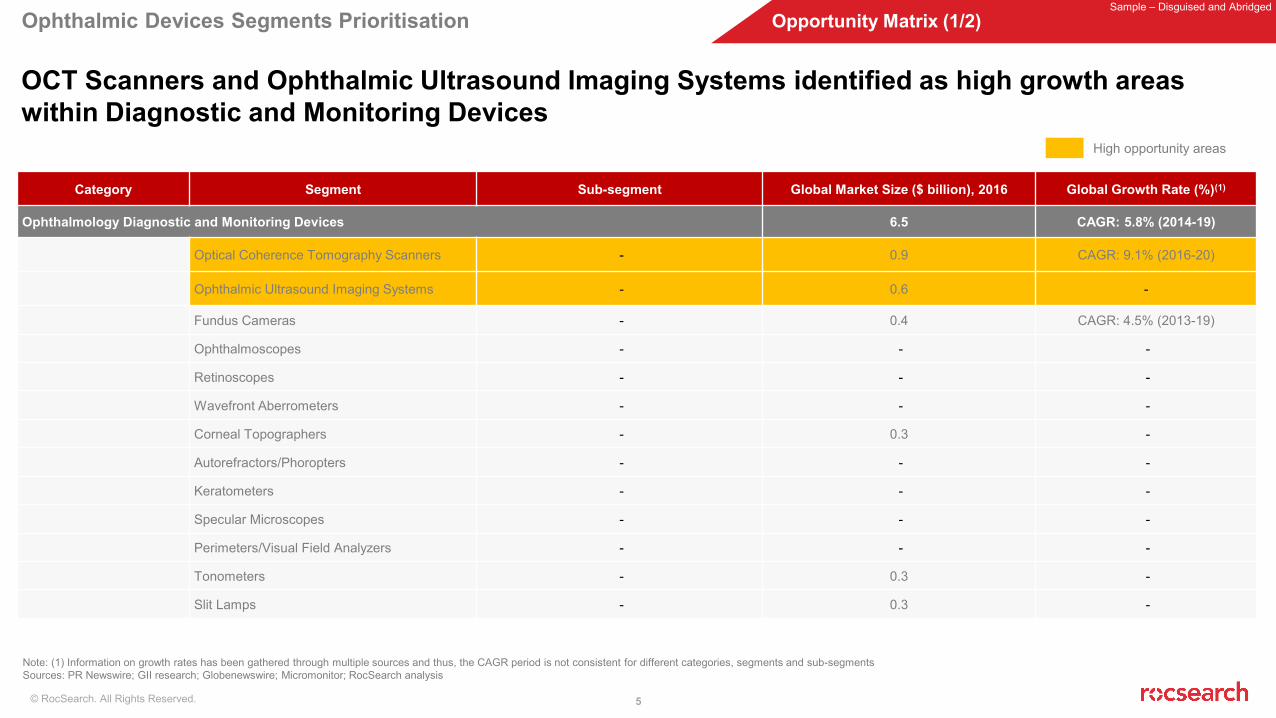

OCT Scanners and Ophthalmic Ultrasound Imaging Systems identified as high growth areas within Diagnostic and Monitoring Devices

Opportunity Matrix (1/2)

Category Segment Sub-segment Global Market Size ($ billion), 2016 Global Growth Rate (%)(1)

Ophthalmology Diagnostic and Monitoring Devices 6.5 CAGR: 5.8% (2014-19)

Optical Coherence Tomography Scanners - 0.9 CAGR: 9.1% (2016-20)

Ophthalmic Ultrasound Imaging Systems - 0.6 -

Fundus Cameras - 0.4 CAGR: 4.5% (2013-19)

Ophthalmoscopes - - -

Retinoscopes - - -

Wavefront Aberrometers - - -

Corneal Topographers - 0.3 -

Autorefractors/Phoropters - - -

Keratometers - - -

Specular Microscopes - - -

Perimeters/Visual Field Analyzers - - -

Tonometers - 0.3 -

Slit Lamps - 0.3 -

Note: (1) Information on growth rates has been gathered through multiple sources and thus, the CAGR period is not consistent for different categories, segments and sub-segments Sources: PR Newswire; GII research; Globenewswire; Micromonitor; RocSearch analysis

High opportunity areas

© RocSearch. All Rights Reserved. 6

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation

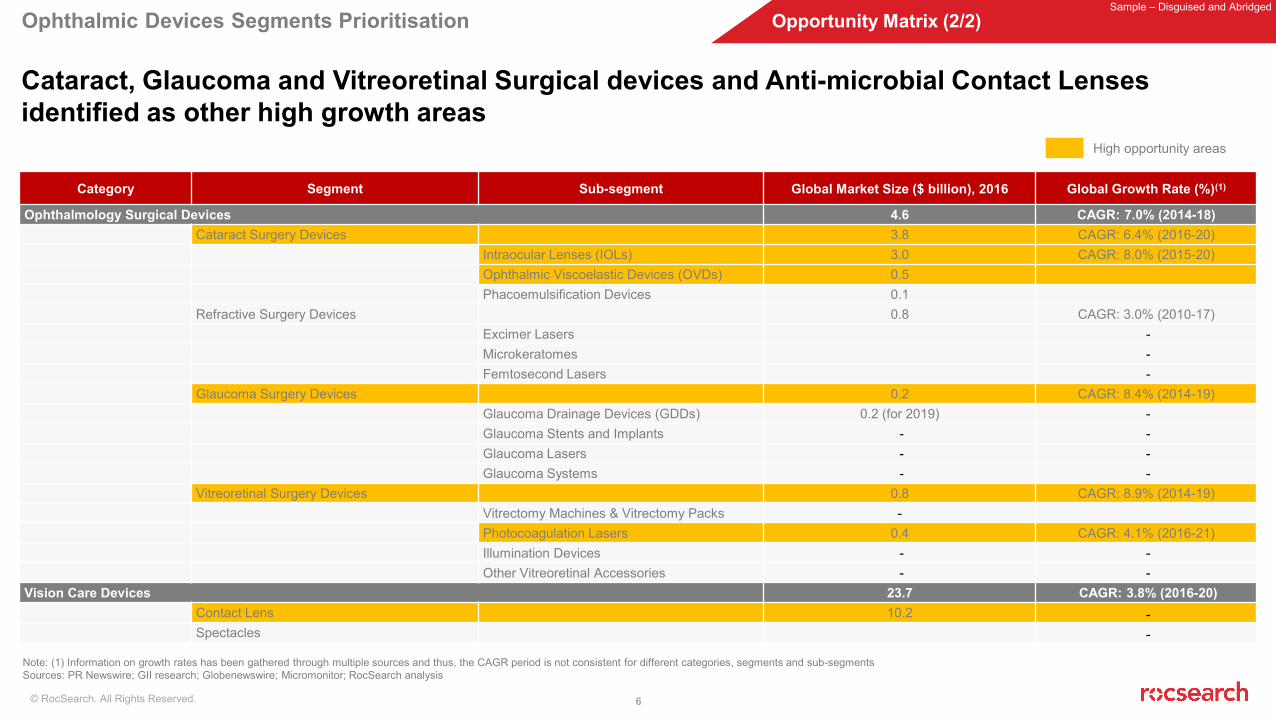

Cataract, Glaucoma and Vitreoretinal Surgical devices and Anti-microbial Contact Lenses identified as other high growth areas

Opportunity Matrix (2/2)

Category Segment Sub-segment Global Market Size ($ billion), 2016 Global Growth Rate (%)(1)

Ophthalmology Surgical Devices 4.6 CAGR: 7.0% (2014-18)Cataract Surgery Devices 3.8 CAGR: 6.4% (2016-20)

Intraocular Lenses (IOLs) 3.0 CAGR: 8.0% (2015-20)Ophthalmic Viscoelastic Devices (OVDs) 0.5Phacoemulsification Devices 0.1

Refractive Surgery Devices 0.8 CAGR: 3.0% (2010-17)Excimer Lasers -Microkeratomes -Femtosecond Lasers -

Glaucoma Surgery Devices 0.2 CAGR: 8.4% (2014-19)Glaucoma Drainage Devices (GDDs) 0.2 (for 2019) -Glaucoma Stents and Implants - -Glaucoma Lasers - -Glaucoma Systems - -

Vitreoretinal Surgery Devices 0.8 CAGR: 8.9% (2014-19)Vitrectomy Machines & Vitrectomy Packs -Photocoagulation Lasers 0.4 CAGR: 4.1% (2016-21)Illumination Devices - -Other Vitreoretinal Accessories - -

Vision Care Devices 23.7 CAGR: 3.8% (2016-20)Contact Lens 10.2 -Spectacles -

High opportunity areas

Note: (1) Information on growth rates has been gathered through multiple sources and thus, the CAGR period is not consistent for different categories, segments and sub-segments Sources: PR Newswire; GII research; Globenewswire; Micromonitor; RocSearch analysis

Table of Contents▪ Module I: Ophthalmic and Optical Devices

Segment Prioritisation

▪ Module II: Healthcare Segments Prioritisation

© RocSearch. All Rights Reserved. 8

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation

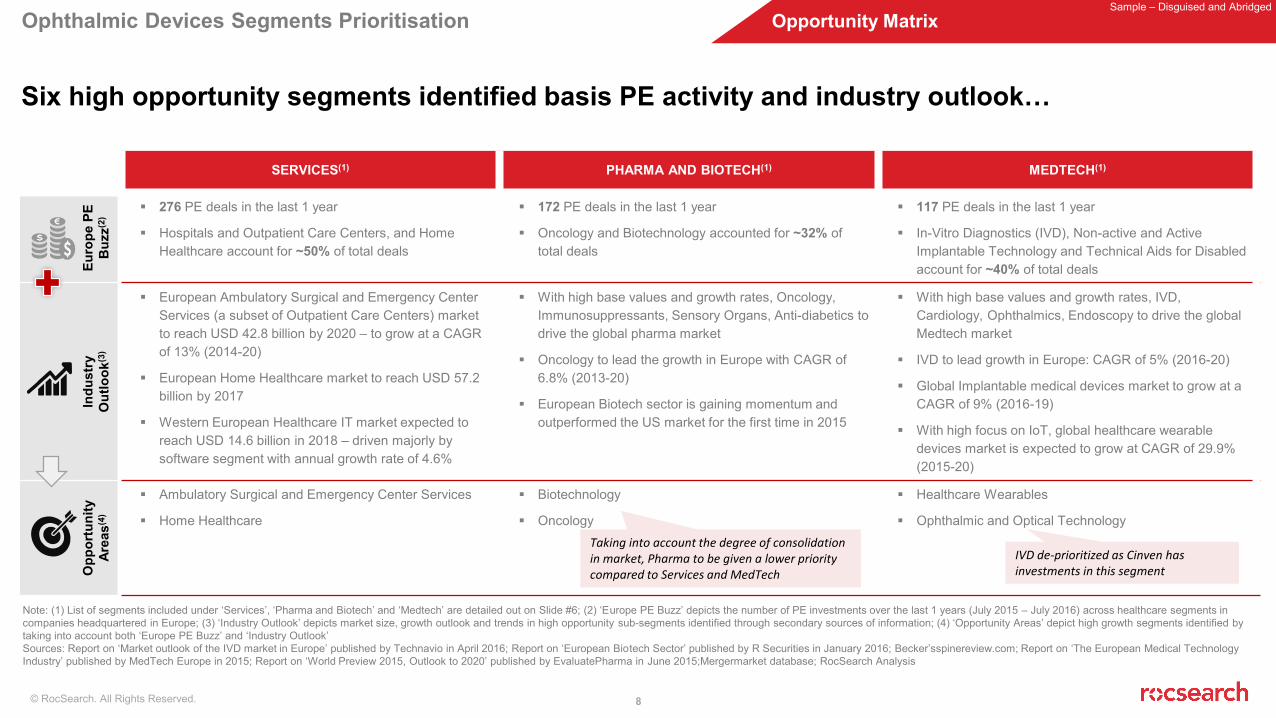

Six high opportunity segments identified basis PE activity and industry outlook…

Opportunity Matrix

SERVICES(1) PHARMA AND BIOTECH(1) MEDTECH(1)

Euro

pe P

EB

uzz(

2)

▪ 276 PE deals in the last 1 year

▪ Hospitals and Outpatient Care Centers, and Home Healthcare account for ~50% of total deals

▪ 172 PE deals in the last 1 year

▪ Oncology and Biotechnology accounted for ~32% of total deals

▪ 117 PE deals in the last 1 year

▪ In-Vitro Diagnostics (IVD), Non-active and Active Implantable Technology and Technical Aids for Disabled account for ~40% of total deals

Indu

stry

Out

look

(3)

▪ European Ambulatory Surgical and Emergency Center Services (a subset of Outpatient Care Centers) market to reach USD 42.8 billion by 2020 – to grow at a CAGR of 13% (2014-20)

▪ European Home Healthcare market to reach USD 57.2 billion by 2017

▪ Western European Healthcare IT market expected to reach USD 14.6 billion in 2018 – driven majorly by software segment with annual growth rate of 4.6%

▪ With high base values and growth rates, Oncology, Immunosuppressants, Sensory Organs, Anti-diabetics to drive the global pharma market

▪ Oncology to lead the growth in Europe with CAGR of 6.8% (2013-20)

▪ European Biotech sector is gaining momentum and outperformed the US market for the first time in 2015

▪ With high base values and growth rates, IVD,Cardiology, Ophthalmics, Endoscopy to drive the global Medtech market

▪ IVD to lead growth in Europe: CAGR of 5% (2016-20)

▪ Global Implantable medical devices market to grow at a CAGR of 9% (2016-19)

▪ With high focus on IoT, global healthcare wearable devices market is expected to grow at CAGR of 29.9% (2015-20)

Opp

ortu

nity

Ar

eas(

4)

▪ Ambulatory Surgical and Emergency Center Services

▪ Home Healthcare

▪ Biotechnology

▪ Oncology

▪ Healthcare Wearables

▪ Ophthalmic and Optical Technology

Note: (1) List of segments included under ‘Services’, ‘Pharma and Biotech’ and ‘Medtech’ are detailed out on Slide #6; (2) ‘Europe PE Buzz’ depicts the number of PE investments over the last 1 years (July 2015 – July 2016) across healthcare segments in companies headquartered in Europe; (3) ‘Industry Outlook’ depicts market size, growth outlook and trends in high opportunity sub-segments identified through secondary sources of information; (4) ‘Opportunity Areas’ depict high growth segments identified bytaking into account both ‘Europe PE Buzz’ and ‘Industry Outlook’ Sources: Report on ‘Market outlook of the IVD market in Europe’ published by Technavio in April 2016; Report on ‘European Biotech Sector’ published by R Securities in January 2016; Becker’sspinereview.com; Report on ‘The European Medical Technology Industry’ published by MedTech Europe in 2015; Report on ‘World Preview 2015, Outlook to 2020’ published by EvaluatePharma in June 2015;Mergermarket database; RocSearch Analysis

IVD de-prioritized as Cinven has investments in this segment

Taking into account the degree of consolidation in market, Pharma to be given a lower priority compared to Services and MedTech

© RocSearch. All Rights Reserved. 9

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation

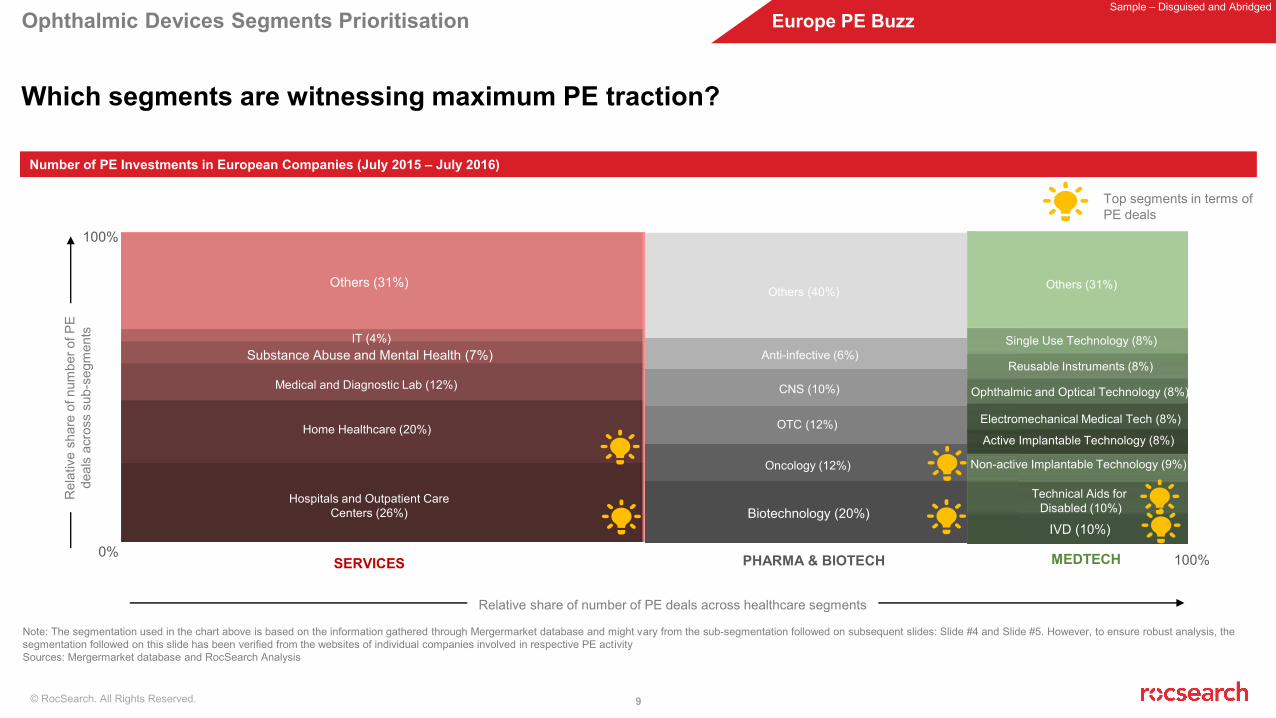

Which segments are witnessing maximum PE traction?

Europe PE Buzz

Note: The segmentation used in the chart above is based on the information gathered through Mergermarket database and might vary from the sub-segmentation followed on subsequent slides: Slide #4 and Slide #5. However, to ensure robust analysis, the segmentation followed on this slide has been verified from the websites of individual companies involved in respective PE activitySources: Mergermarket database and RocSearch Analysis

Top segments in terms of PE deals

Number of PE Investments in European Companies (July 2015 – July 2016)

0%

100%

100%SERVICES PHARMA & BIOTECH MEDTECH

Relative share of number of PE deals across healthcare segments

Rel

ativ

e sh

are

of n

umbe

r of P

E de

als

acro

ss s

ub-s

egm

ents

Hospitals and Outpatient Care Centers (26%)

Home Healthcare (20%)

Medical and Diagnostic Lab (12%)

Substance Abuse and Mental Health (7%) IT (4%)

Others (31%)

Biotechnology (20%)

Oncology (12%)

OTC (12%)

CNS (10%)

Anti-infective (6%)

Others (40%)

IVD (10%)

Technical Aids forDisabled (10%)

Non-active Implantable Technology (9%)

Active Implantable Technology (8%)

Electromechanical Medical Tech (8%)

Ophthalmic and Optical Technology (8%)

Reusable Instruments (8%)

Single Use Technology (8%)

Others (31%)

© RocSearch. All Rights Reserved. 10

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation

What is the relative growth scenario for Pharma segments?

Pharma Industry Outlook Analysis

Global Pharma Market by Top 10 Therapy Area, Market Share and Sales Growth (2014-20)

Segments driving global Pharma market

Anti-hypertensives

Bronchodilators

Anti-rheumatics

MS therapies

Anti-virals

Vaccines

Anti-diabetics

Sensory Organs

Immunosuppressants

Oncology

18.0%

16.0%

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

-2.0%-4.0% -2.0% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

Glo

bal M

arke

t Sha

re in

202

0

Sales Growth: CAGR 2014-20

Note: Size of the bubble depicts relative worldwide sales in 2020Sources: Report on ‘World Preview 2015, Outlook to 2020’ published by EvaluatePharma in June 2015

© RocSearch. All Rights Reserved. 11

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation

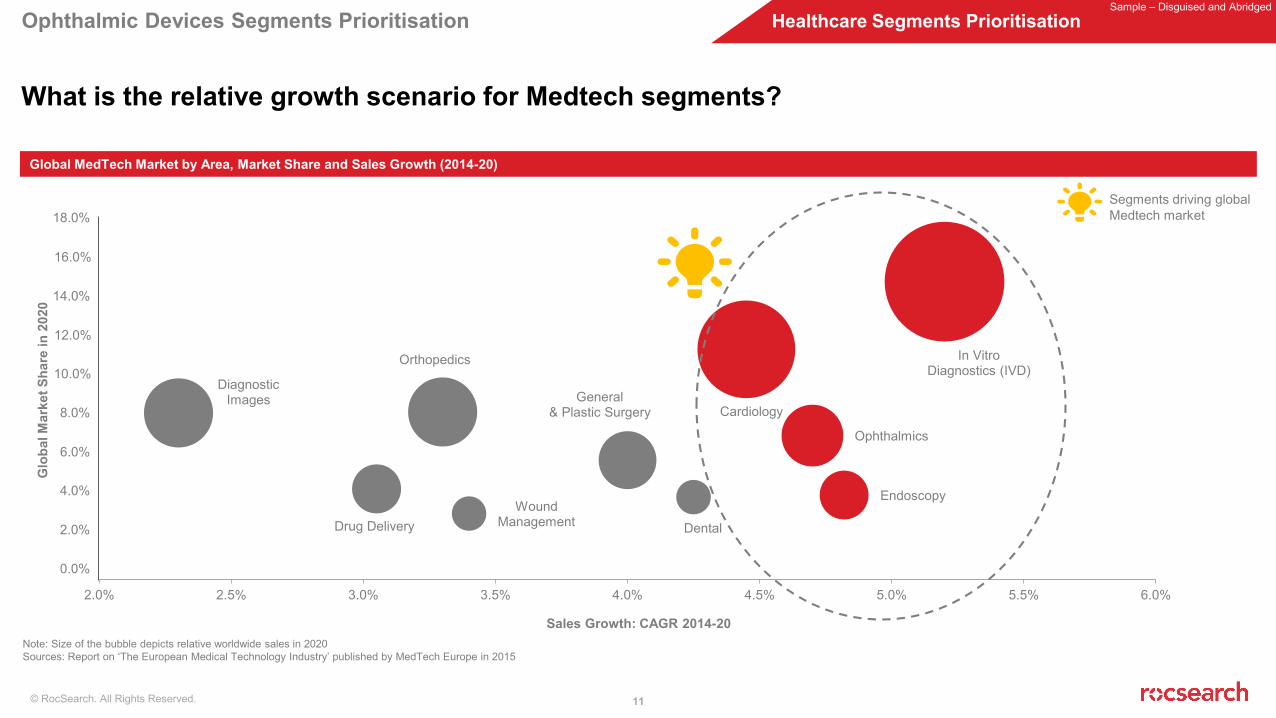

What is the relative growth scenario for Medtech segments?

Healthcare Segments Prioritisation

Global MedTech Market by Area, Market Share and Sales Growth (2014-20)

Segments driving global Medtech market

Note: Size of the bubble depicts relative worldwide sales in 2020Sources: Report on ‘The European Medical Technology Industry’ published by MedTech Europe in 2015

Diagnostic Images

Orthopedics

Drug DeliveryWound

Management

General & Plastic Surgery

Dental

Endoscopy

Ophthalmics

Cardiology

In Vitro Diagnostics (IVD)

2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 5.0% 5.5% 6.0%

Sales Growth: CAGR 2014-20

18.0%

16.0%

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

Glo

bal M

arke

t Sha

re in

202

0

© RocSearch. All Rights Reserved. 12

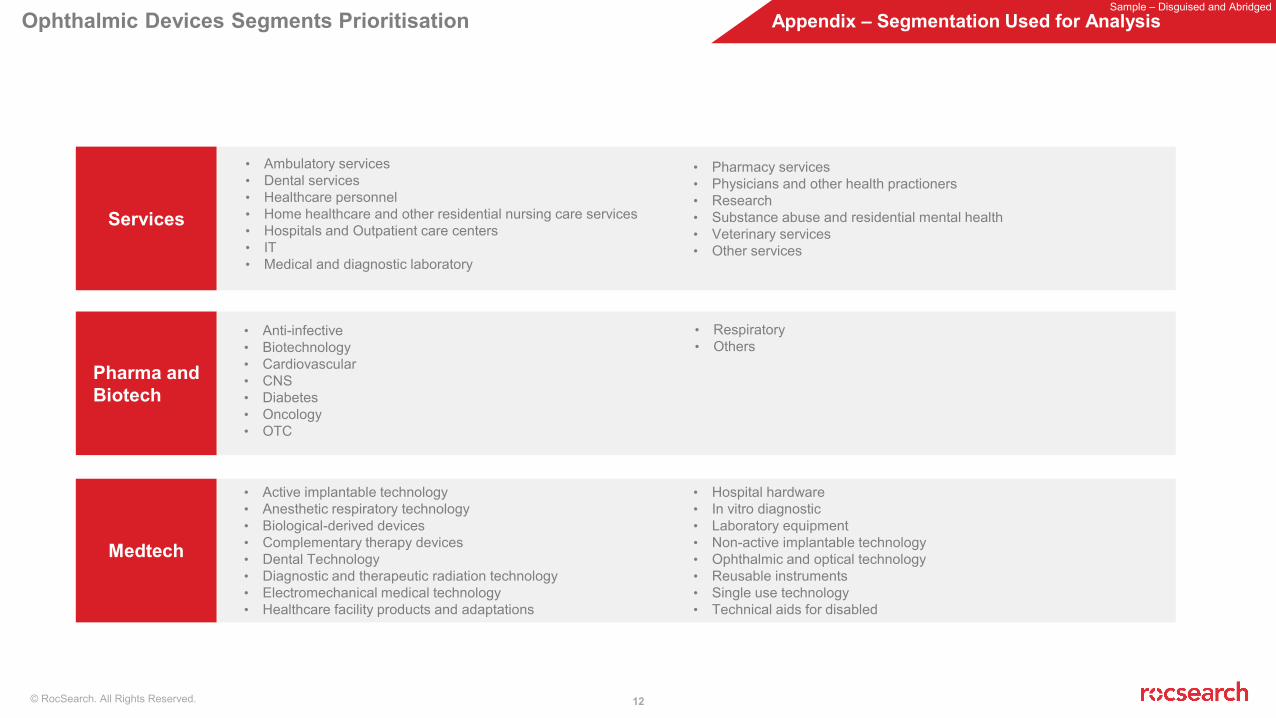

Sample – Disguised and AbridgedOphthalmic Devices Segments Prioritisation Appendix – Segmentation Used for Analysis

Services

• Ambulatory services• Dental services• Healthcare personnel• Home healthcare and other residential nursing care services• Hospitals and Outpatient care centers• IT• Medical and diagnostic laboratory

• Pharmacy services• Physicians and other health practioners • Research• Substance abuse and residential mental health• Veterinary services• Other services

Pharma and Biotech

• Anti-infective• Biotechnology• Cardiovascular• CNS• Diabetes • Oncology• OTC

• Respiratory• Others

Medtech

• Active implantable technology• Anesthetic respiratory technology• Biological-derived devices• Complementary therapy devices• Dental Technology• Diagnostic and therapeutic radiation technology• Electromechanical medical technology• Healthcare facility products and adaptations

• Hospital hardware• In vitro diagnostic• Laboratory equipment• Non-active implantable technology• Ophthalmic and optical technology• Reusable instruments• Single use technology• Technical aids for disabled

Sample – Disguised and Abridged

© RocSearch. All Rights Reserved.

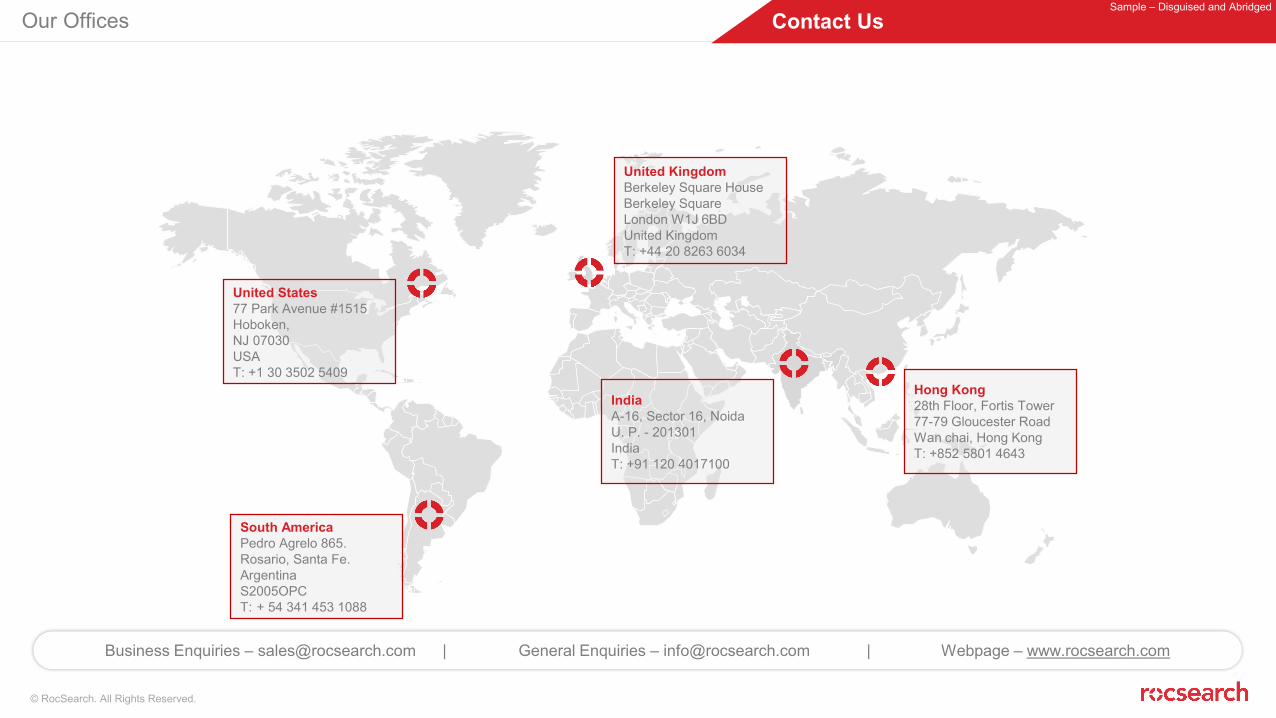

Sample – Disguised and AbridgedOur Offices

United KingdomBerkeley Square HouseBerkeley SquareLondon W1J 6BDUnited KingdomT: +44 20 8263 6034

India A-16, Sector 16, NoidaU. P. - 201301IndiaT: +91 120 4017100

Hong Kong28th Floor, Fortis Tower77-79 Gloucester RoadWan chai, Hong KongT: +852 5801 4643

United States77 Park Avenue #1515Hoboken, NJ 07030USAT: +1 30 3502 5409

Business Enquiries – [email protected] | General Enquiries – [email protected] | Webpage – www.rocsearch.com

South America Pedro Agrelo 865. Rosario, Santa Fe. ArgentinaS2005OPCT: + 54 341 453 1088

Contact Us

About RocSearchPlease visit www.rocsearch.com for more details on the company

© RocSearch. All Rights Reserved.

Disclaimer

This document is proprietary to RocSearch and the information contained herein is confidential. Not without prior writtenpermission from RocSearch, may this document be reproduced, either in whole or in part, or disclosed to others outside your firm.

Whilst care and attention has been exercised in the preparation of this document, RocSearch does not accept responsibility forany inaccuracy or error or any action taken in reliance on the information contained within. All warranties whether expressed orimplied by statute, law or otherwise are hereby disclaimed and excluded to the extent permitted by law.

In case of any questions on this document, please reply to the sender.