headlines - microsoft · • china warned it may hit back if the us implements aluminium and steel...

TRANSCRIPT

Monday, 19 February 2018

P. 1

Rates: Room for consolidation ahead of Wednesday’s FOMC Minutes?

We expect trading to be sentiment-driven and technically in nature today amid an empty eco calendar. Volumes will be low in absence of US traders (President’s Day Holiday). Underlying sentiment remains bearish for core bonds, but we’d argue in favour of some consolidation in the run-up to Wednesday’s FOMC Minutes.

Currencies: USD decline slows, at least for now

The dollar tested key support area’s on Friday, but rebounded later in the session. The econ calendar is thin today. The rebound in equities went hand-in-hand with a weaker dollar recently. Will this link persist? At least this morning, there are tentative signs that it might become less tight.

Calendar

• US stock markets ended near opening levels on Friday, but last week’s

performance was the strongest in 5 years. Asian risk sentiment is ebullient with China still closed for Lunar New Year.

• A Russian propaganda arm oversaw a criminal and espionage conspiracy to tamper in the 2016 US presidential campaign to support Donald Trump and disparage Hillary Clinton, said an indictment released on Friday.

• China warned it may hit back if the US implements aluminium and steel restrictions as recommended by the Commerce Department on Friday.

• Fitch upgraded the Greek rating from B- to B (positive outlook). Fitch expects reduced political risks, general government primary surpluses and legislated fiscal measures to improve Greece’s general government debt sustainability.

• London’s property market has moved out of its boom phase and home sellers need to be more realistic about their price demands, according to Rightmove. Asking prices were down 1% Y/Y, a sixth consecutive fall.

• Buoyant sales of cars and electronics led Japan's exports to a 14th straight month of growth in January (12.2% Y/Y). Imports increased by 7.9% Y/Y. The adjusted trade surplus rose more than forecast, to ¥373.3bn.

• Today’s eco calendar contains only second tier EMU eco data. The Eurogroup choses the next ECB vice-president out of Spanish economy minister de Guindos and Irish ECB governor Lane. US markets are closed for President’s Day.

Headlines

S&PEurostoxx 50NikkeiOilCRB

Gold2 yr US10 yr US

2yr DE10 yr DEEUR/USDUSD/JPYEUR/GBP

Monday, 19 February 2018

P. 2

Room for consolidation on core bond markets?

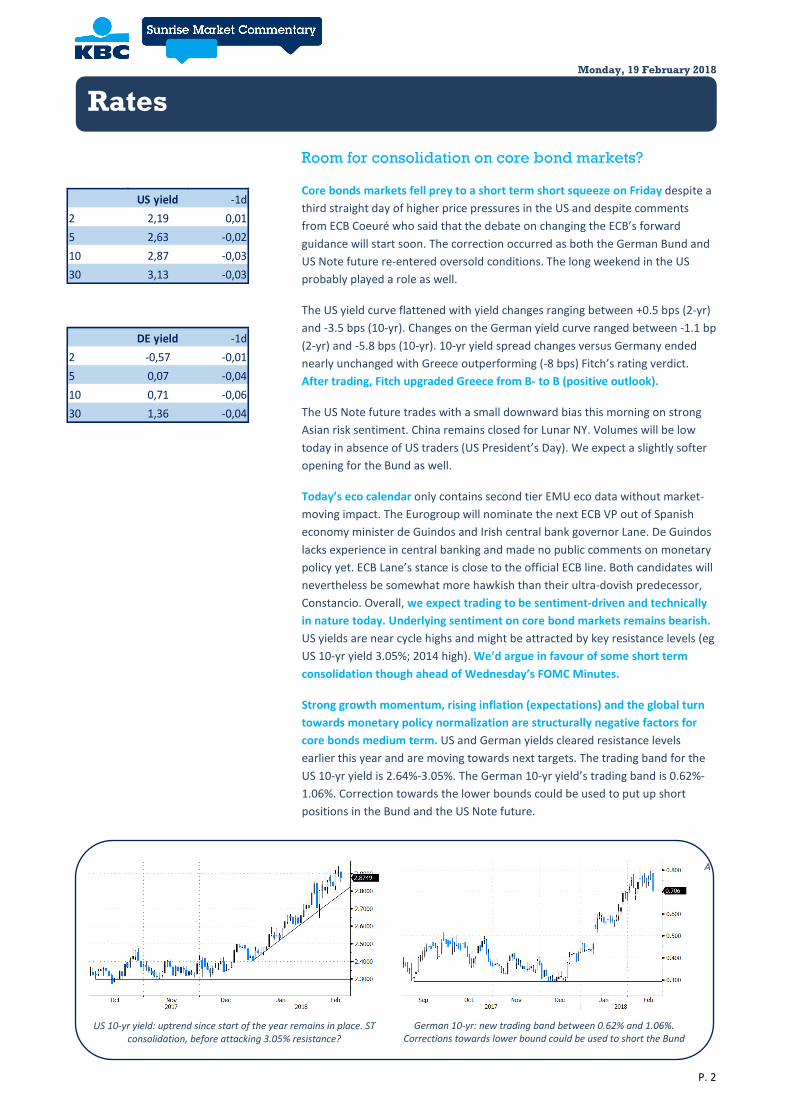

Core bonds markets fell prey to a short term short squeeze on Friday despite a third straight day of higher price pressures in the US and despite comments from ECB Coeuré who said that the debate on changing the ECB’s forward guidance will start soon. The correction occurred as both the German Bund and US Note future re-entered oversold conditions. The long weekend in the US probably played a role as well.

The US yield curve flattened with yield changes ranging between +0.5 bps (2-yr) and -3.5 bps (10-yr). Changes on the German yield curve ranged between -1.1 bp (2-yr) and -5.8 bps (10-yr). 10-yr yield spread changes versus Germany ended nearly unchanged with Greece outperforming (-8 bps) Fitch’s rating verdict. After trading, Fitch upgraded Greece from B- to B (positive outlook).

The US Note future trades with a small downward bias this morning on strong Asian risk sentiment. China remains closed for Lunar NY. Volumes will be low today in absence of US traders (US President’s Day). We expect a slightly softer opening for the Bund as well.

Today’s eco calendar only contains second tier EMU eco data without market-moving impact. The Eurogroup will nominate the next ECB VP out of Spanish economy minister de Guindos and Irish central bank governor Lane. De Guindos lacks experience in central banking and made no public comments on monetary policy yet. ECB Lane’s stance is close to the official ECB line. Both candidates will nevertheless be somewhat more hawkish than their ultra-dovish predecessor, Constancio. Overall, we expect trading to be sentiment-driven and technically in nature today. Underlying sentiment on core bond markets remains bearish. US yields are near cycle highs and might be attracted by key resistance levels (eg US 10-yr yield 3.05%; 2014 high). We’d argue in favour of some short term consolidation though ahead of Wednesday’s FOMC Minutes.

Strong growth momentum, rising inflation (expectations) and the global turn towards monetary policy normalization are structurally negative factors for core bonds medium term. US and German yields cleared resistance levels earlier this year and are moving towards next targets. The trading band for the US 10-yr yield is 2.64%-3.05%. The German 10-yr yield’s trading band is 0.62%-1.06%. Correction towards the lower bounds could be used to put up short positions in the Bund and the US Note future.

Rates

US yield -1d2 2,19 0,015 2,63 -0,0210 2,87 -0,0330 3,13 -0,03

DE yield -1d2 -0,57 -0,015 0,07 -0,0410 0,71 -0,0630 1,36 -0,04

US 10-yr yield: uptrend since start of the year remains in place. ST consolidation, before attacking 3.05% resistance?

German 10-yr: new trading band between 0.62% and 1.06%. Corrections towards lower bound could be used to short the Bund

Af

Monday, 19 February 2018

P. 3

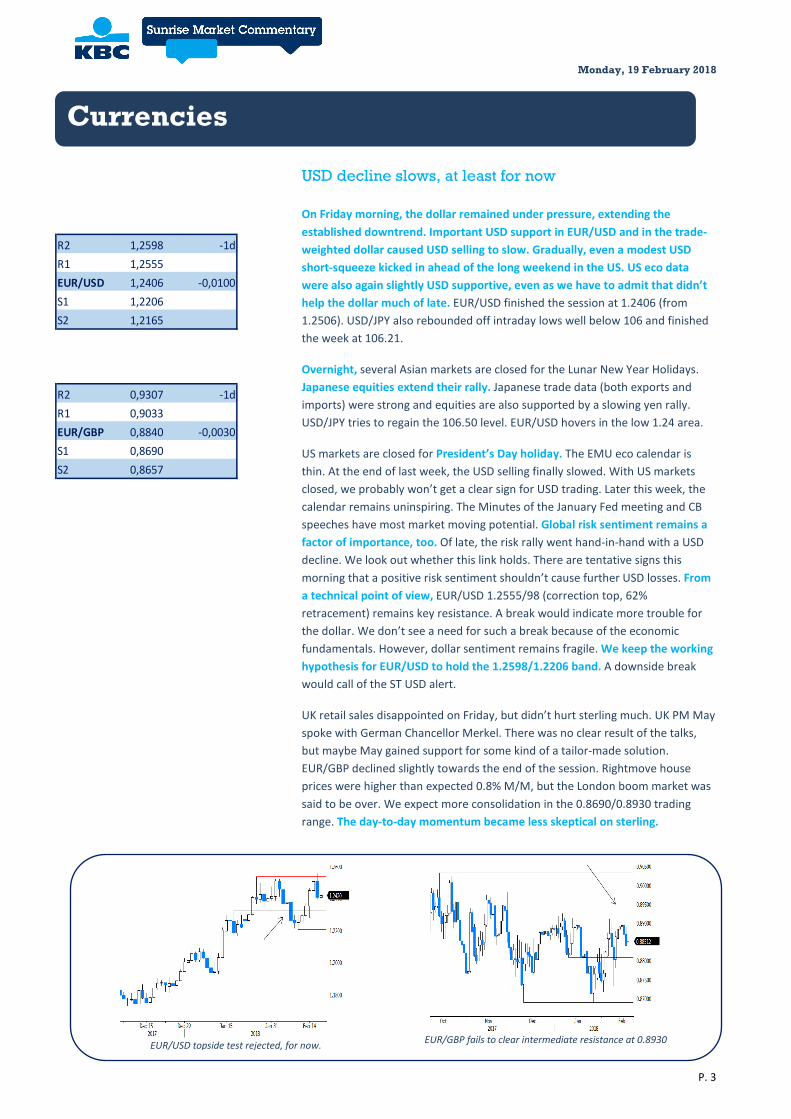

EUR/USD topside test rejected, for now.

EUR/GBP fails to clear intermediate resistance at 0.8930

USD decline slows, at least for now

On Friday morning, the dollar remained under pressure, extending the established downtrend. Important USD support in EUR/USD and in the trade-weighted dollar caused USD selling to slow. Gradually, even a modest USD short-squeeze kicked in ahead of the long weekend in the US. US eco data were also again slightly USD supportive, even as we have to admit that didn’t help the dollar much of late. EUR/USD finished the session at 1.2406 (from 1.2506). USD/JPY also rebounded off intraday lows well below 106 and finished the week at 106.21.

Overnight, several Asian markets are closed for the Lunar New Year Holidays. Japanese equities extend their rally. Japanese trade data (both exports and imports) were strong and equities are also supported by a slowing yen rally. USD/JPY tries to regain the 106.50 level. EUR/USD hovers in the low 1.24 area.

US markets are closed for President’s Day holiday. The EMU eco calendar is thin. At the end of last week, the USD selling finally slowed. With US markets closed, we probably won’t get a clear sign for USD trading. Later this week, the calendar remains uninspiring. The Minutes of the January Fed meeting and CB speeches have most market moving potential. Global risk sentiment remains a factor of importance, too. Of late, the risk rally went hand-in-hand with a USD decline. We look out whether this link holds. There are tentative signs this morning that a positive risk sentiment shouldn’t cause further USD losses. From a technical point of view, EUR/USD 1.2555/98 (correction top, 62% retracement) remains key resistance. A break would indicate more trouble for the dollar. We don’t see a need for such a break because of the economic fundamentals. However, dollar sentiment remains fragile. We keep the working hypothesis for EUR/USD to hold the 1.2598/1.2206 band. A downside break would call of the ST USD alert.

UK retail sales disappointed on Friday, but didn’t hurt sterling much. UK PM May spoke with German Chancellor Merkel. There was no clear result of the talks, but maybe May gained support for some kind of a tailor-made solution. EUR/GBP declined slightly towards the end of the session. Rightmove house prices were higher than expected 0.8% M/M, but the London boom market was said to be over. We expect more consolidation in the 0.8690/0.8930 trading range. The day-to-day momentum became less skeptical on sterling.

Currencies

R2 1,2598 -1dR1 1,2555EUR/USD 1,2406 -0,0100S1 1,2206S2 1,2165

R2 0,9307 -1dR1 0,9033EUR/GBP 0,8840 -0,0030S1 0,8690S2 0,8657

Monday, 19 February 2018

P. 4

Monday, 19 February Consensus Previous Japan 00:50 Trade Balance Adjusted (Jan) A:¥373.3b ¥90.7b 00:50 Exports YoY / Imports YoY (Jan) A:12.2%/7.9% 9.3%/14.9% UK 01:01 Rightmove House Prices MoM / YoY (Feb) A: 0.8%/1.5% 0.7%/1.1% EMU 10:00 ECB Current Account SA (Dec) -- 32.5b 11:00 Construction Output MoM / YoY (Dec) --/-- 0.5%/2.7% Belgium 15:00 Consumer Confidence Index (Feb) -- 4 Events US markets closed for President’s Day 15:00 Eurogroup meeting including nomination new ECB VP

10-year Close -1d 2-year Close -1d Stocks Close -1dUS 2,87 -0,03 US 2,19 0,01 DOW 25219,38 19,01DE 0,71 -0,06 DE -0,57 -0,01 NASDAQ 7239,465 -16,97BE 0,98 -0,05 BE -0,46 -0,01 NIKKEI 22149,21 428,96UK 1,58 -0,06 UK 0,66 -0,04 DAX 12451,96 105,79

JP 0,07 0,01 JP -0,15 0,00 DJ euro-50 3426,8 37,17

IRS EUR USD GBP EUR -1d -2d USD -1d -2d3y 0,08 2,59 1,16 Eonia -0,3660 -0,00305y 0,49 2,73 1,38 Euribor-1 -0,3690 0,0000 Libor-1 1,5938 0,003810y 1,13 2,89 1,65 Euribor-3 -0,3280 0,0000 Libor-3 1,8849 0,0124

Euribor-6 -0,2740 0,0020 Libor-6 2,1061 0,0097

Currencies Close -1d Currencies Close -1d Commodities Close -1d

EUR/USD 1,2406 -0,0100 EUR/JPY 131,88 -0,85 CRB 193,58 0,12USD/JPY 106,21 0,08 EUR/GBP 0,8840 -0,0030 Gold 1356,20 0,90GBP/USD 1,4026 -0,0073 EUR/CHF 1,1511 -0,0019 Brent 64,84 0,51AUD/USD 0,7905 -0,0040 EUR/SEK 9,8864 -0,0415USD/CAD 1,2558 0,0077 EUR/NOK 9,6563 -0,0563

If you no longer wish to receive this mail, please contact us: “[email protected] ‘ to unsubscribe

Calendar

Monday, 19 February 2018

P. 5

Brussels Research (KBC) Global Sales Force Mathias van der Jeugt +32 2 417 51 94 Brussels Peter Wuyts +32 2 417 32 35 Corporate Desk +32 2 417 45 82 Institutional Desk +32 2 417 46 25 Dublin Research France +32 2 417 32 65 Austin Hughes +353 1 664 6889 London +44 207 256 4848 Shawn Britton +353 1 664 6892 Singapore +65 533 34 10 Prague Research (CSOB) Jan Cermak +420 2 6135 3578 Prague +420 2 6135 3535 Jan Bures +420 2 6135 3574 Petr Baca +420 2 6135 3570 Bratislava Research (CSOB) Marek Gabris +421 2 5966 8809 Bratislava +421 2 5966 8820 Budapest Research David Nemeth +36 1 328 9989 Budapest +36 1 328 99 85

ALL OUR REPORTS ARE AVAILABLE VIA OUR KBC RESEARCH APP (iPhone, iPad, Android) This non exhaustive information is based on short term forecasts for expected developments

This non-exhaustive information is based on short-term forecasts for expected developments on the financial markets. KBC Bank cannot guarantee that these forecasts will materialize and cannot be held liable in any way for direct or consequential loss arising from any use of this document or its content. The document is not intended as personalized investment advice and does not constitute a recommendation to buy, sell or hold investments described herein. Although information has been obtained from and is based upon sources KBC believes to be reliable, KBC does not guarantee the accuracy of this information, which may be incomplete or condensed. All opinions and estimates constitute a KBC judgment as of the data of the report and are subject to change without notice.

Contacts