h.b. fuller company 2009 open enrollment: helping you buy well, use well, be well october, 2008

Post on 21-Dec-2015

219 views

TRANSCRIPT

H.B. Fuller Company

2009 Open Enrollment:

Helping you Buy Well, Use Well, Be Well

October, 2008

2

An overview of your plan options for 2009 Market 400

Value 750

High Deductible Health Plan (HDHP)with a Health Savings Account (HSA)

Key differences between plan options

Tools and resources to find the information you need

How and when to enroll

Today’s Discussion

PURPOSE OF TODAY’S MEETING:To help you understand your new choices in medical plan options

3

Market 400 Value 750 HDHP w/ HSA

Deductible $400 Single

$800 Family

$750 Single

$1,500 Family

$2,000 Single

$4,000 Family

Fuller contribution to HSA

N/A N/A $500 Single

$1,000 Family (active employees only)

Out of pocket maximum

$1,500 Single

$3,000 Family

$3,000 Single

$6,000 Family

Same as your deductible

Preventive care (in-network only)

100% 100% 100%

Office visit copay

$30 $30 N/A

Medical Plan Options Summary

4

Market 400 Value 750 HDHP w/ HSA

Pharmacy

Generic

Brand

Non-formulary

Specialty

You pay 20% with:

Minimum Maximum

$10 $20

$20 $40

$40 $80

$80 $160

You pay 20% with:

Minimum Maximum

$10 $20

$20 $40

$40 $80

$80 $160

100% after deductible

Coinsurance 80% after deductible 80% after deductible 100% after deductible

Out-of-network coverage

60% (deductible and OOP max doubled)

60% (deductible and OOP max doubled)

100% - no network restrictions

Premium (Month)

Employee

Employee + 1

Family

$79.80

$159.60

$239.40

$57.80

$115.60

$173.40

$54.80

$109.40

$164.40

Medical Plan Options Summary (cont.)

5

This option is the most similar to what you have today, with the deductible and out–of- pocket maximum adjusted to be at the mid-point of the market. As this option has the lowest deductible and out-of-pocket limit, it carries the highest premium contribution.

Pharmacy: 20% member copay with a min/max of:

Key Features of Market 400

Deductible – $400 single $800 familyOut of Pocket - $1,500 single $3,000 family

Office visit copay -- $30

Preventive care 100% in-network only

Deductible and coinsurance applies to X-ray and imaging, inpatient and outpatient hospital, emergency room (+$75 copay) and durable medical equipment

Office visit, pharmacy and emergency room copays do not apply to deductible or out-of-pocket maximum.

Generic – $10/$20 Brand – $20/$40 Non-Formulary Brand – $40/$80 Specialty Pharmacy – $80/$160

6

The other plan features are identical to the Market 400. Eligible expenses are paid in the same manner in both options. Office visit copay -- $30 Preventive care – 100% in-network only Pharmacy: 20% member copay with a min/max of: Generic – $10/$20 Brand – $20/$40

Non-Formulary Brand – $40/$80 Specialty Pharmacy – $80/$160 Deductible and coinsurance applies to X-ray and imaging, inpatient and outpatient

hospital, emergency room (+$75 copay) and durable medical equipment Office visit, pharmacy and emergency room copays do not apply to deductible or

out-of-pocket maximum.

Key Features of Value 750Choosing a higher

deductible is similar to the decision you make when you buy car insurance.

You balance what you can afford to fix yourself vs.

what you want your insurance to cover. It is always more expensive when you have a low

deductible.

This option lets you pay less in monthly premium. In exchange, you may need to pay a higher deductible before the plan begins to pay.

Deductible -- $750, $1,500 Out of pocket limit -- $3,000, $6,000 Premium: 40% less than Market 400

7

Key Features of HBF’s HDHP with HSA

This means: High Deductible Health Plan with a Health Savings Account

High Deductible Health Plan

$2,000/$4,000 deductible (total family deductible must be met)

The out-of-pocket maximum matches the deductible. The plan pays 100% after the deductible is met for eligible expenses.

Same definition of eligible expenses as in Market 400 and Value 750

Prescription drugs must apply toward the deductible

Preventive care is covered at 100% in-network

Health Savings Account

Employees have the option to use pre-tax dollars to fund their account up to the IRS limits. For 2009, the limits are $3,000 single/ $5,950 family.

For 2009, HBF will contribute $500/ single

and $1,000/ family

8

Tax-free contributions to pay for current and/or future medical expenses

No “use it or lose it”

Interest earned tax free

Investment opportunity with tax-free growth

Flexible – you choose when or whether to use the account for health care expenses

Portable – you own the account

Banking services provided by JPMorgan Chase Bank. Some fees required.

Easy access to funds through debit card

Key Features of an HSA

What is an HSA?It is a savings account that is owned by you

and is associated with a High Deductible Health Plan

9

Includes expenses such as: Deductibles Coinsurance Not covered but eligible

IRS expenses Prescription drugs

It also includes expenses for: COBRA-continuation coverage Health plan coverage while receiving unemployment compensation Medicare premiums and out-of-pocket expenses Qualified long-term care insurance

Employees are responsible for keeping all receipts and records, demonstrating that HSA dollars were used for qualified health

care expenses.

HSA Tax-Qualified Expenses

10

HSA Eligibility Requirements to Contribute

Member is not eligible to be claimed on another’s tax return1

Member does not have benefits from another qualified health plan2

Member is not currently enrolled in Medicare benefits3

Eligibility

11

HSA Investment Options

12

Health Coverage

Deductible

HSA Pre

ven

tive

Ca

re• Financial stake• Employer and /or employee dollars• Potential rollover and / or savings / investment incentives

100% coverage for preventive care services based on age and gender as recommended under U.S. guidelines

• Peace of mind• Out-of-pocket maximums

• Clearly defined out-of-pocket potential

• Option to reimburse from account

• Financial stake

How the HDHP with HSA Works

13

Len -- Year One –

Note: Assumes all in-network care.

Preventive Care $ 750

HSA funded $ 2,000

Non-Preventive3 Physician’s visits $36012 Prescriptions 840

$ 1,200

Health CoverageEmployee Pays $ 0Health Plan Pays $ 750

Remains in HSA for 2nd year $ 800

HSA Pays $ 1,200

Pre

ven

tive C

are

: 1

00

%$

75

0

Health Coverage100% CoinsuranceMax OOP $2,000

Health Coverage

$800 Remaining

$1,200HSA Paid

$1,200

$2,000 HSA

$2,000 Deductible

Example with Moderate Utilization

14

Len – Year Two –

Moderate Utilization

Health Coverage100% Coins.

Max OOP $2,000

Pre

ven

tive C

are

: 1

00

%$

30

0$900

$1900 Remaining

$900

$2,000 Deductible $2,800

HSA

HSA Rollover fromyear one $ 800HSA funded $ 2,000

New HSA balance $ 2,800

Immunizations $ 300Non-Preventive

5 Prescriptions $ 350Lab work 2503 Physician’s visits300

$ 900HSA Pays $ 900

Employee Pays $ 0

Health Plan Pays $ 300Remains in HSAfor year three $ 1,900

Note: Assumes all in-network care.

15

How Claims Get Filed

Aetna processes the claim, applies the

discounted rate and sends an Explanation of Benefits based on High Deductible Health Plan

Benefits

You visit the doctor

Doctor sendsbill to Aetna

You receive a bill from the provider

You decide whether or not to use HSA funds

You paythe doctor

16

Market 400/Value 750

Member copay is 20%

($20min/$40 Max) You pay $25 The plan pays $100

HDHP and HSA

$125 applies to the deductible You pay $125 at the pharmacy You decide when or if you get

reimbursed for the $125

Participating Pharmacy Brand Rx- $125

Claim Payment Comparison

17

Claim Payment Comparison

In-Network Preventive Care Office Visit-

$150 Contracted Rate

Market 400/Value 750

Plan pays 100% You pay nothing

HDHP and HSA

Plan pays 100% You pay nothing

18

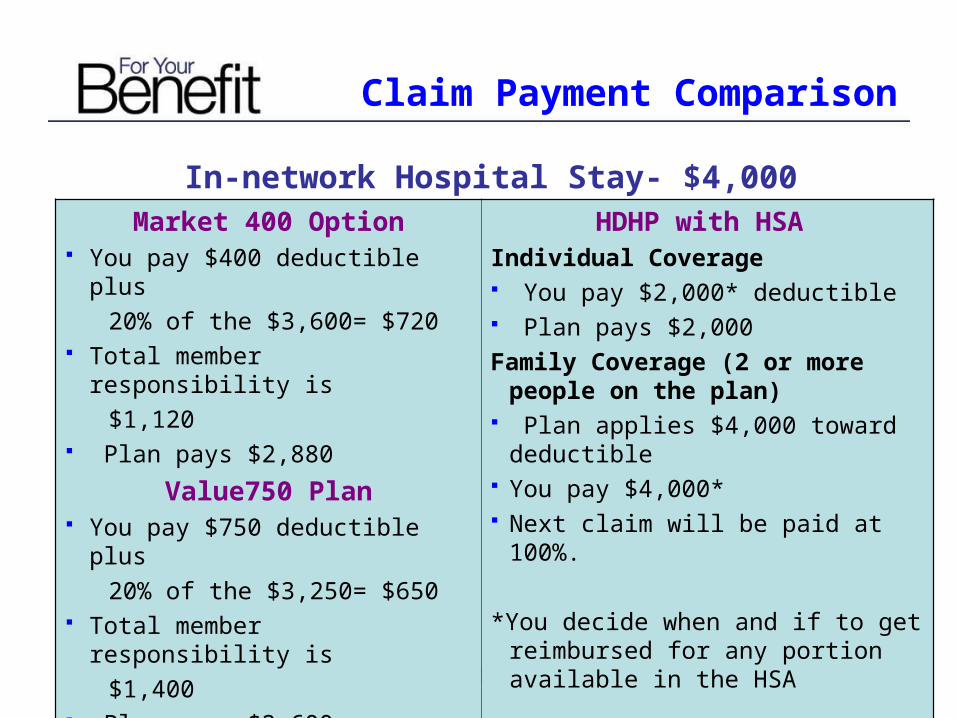

Claim Payment Comparison

In-network Hospital Stay- $4,000 Contracted RateMarket 400 Option

You pay $400 deductible plus

20% of the $3,600= $720 Total member responsibility is

$1,120 Plan pays $2,880

Value750 Plan You pay $750 deductible plus

20% of the $3,250= $650 Total member responsibility is

$1,400 Plan pays $2,600

HDHP with HSA Individual Coverage You pay $2,000* deductible Plan pays $2,000

Family Coverage (2 or more people on the plan)

Plan applies $4,000 toward deductible You pay $4,000* Next claim will be paid at 100%.

*You decide when and if to get reimbursed for any portion available in the HSA

19

Important things to consider when making your choice:

Understand how the deductible works Individual vs. family What counts, what doesn’t

Annual premium difference – do the math!

If you are considering the HSA, here are additional considerations:

Prescription coverage – You pay 100% up to the deductible

Tax advantaged, portable savings. Great for retiree medical!

Key Differences

20

For help in choosing the right medical plan option

Read newsletters and Enrollment Guide Visit the Aetna website and sign up for Aetna Navigator Try the Plan Selection and Cost Estimator Tool Use Aetna’s Cost Estimator to determine cost of care For “in-person” help, call

the HBF Benefits Connection (formerly FlexPlus) Aetna

Tools for Choosing a Medical Plan

21

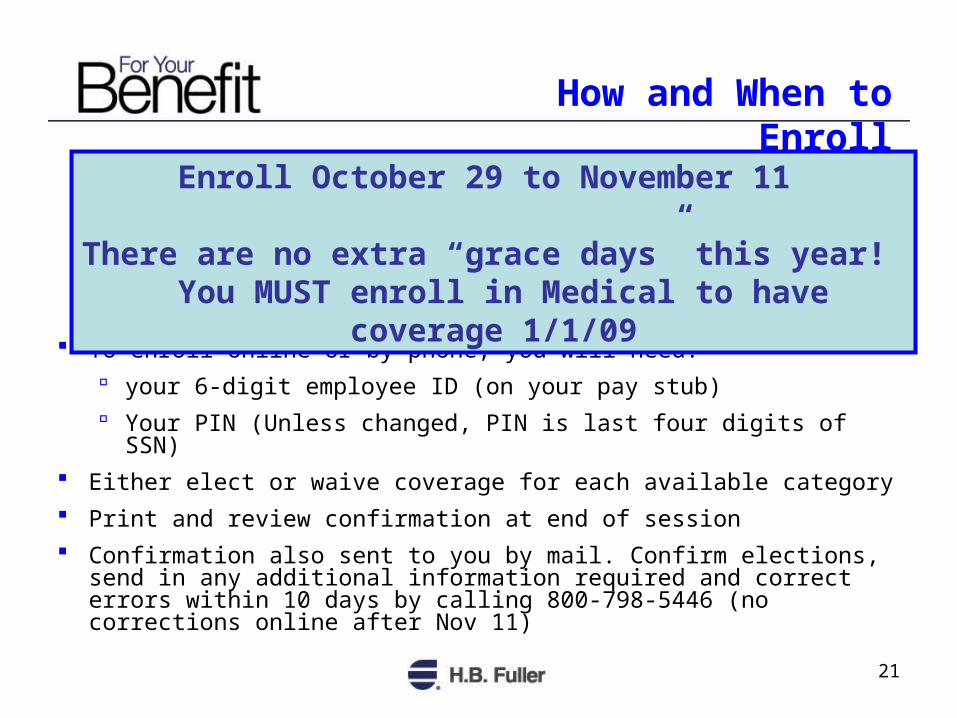

To enroll online or by phone, you will need:

your 6-digit employee ID (on your pay stub)

Your PIN (Unless changed, PIN is last four digits of SSN)

Either elect or waive coverage for each available category

Print and review confirmation at end of session

Confirmation also sent to you by mail. Confirm elections, send in any additional information required and correct errors within 10 days by calling 800-798-5446 (no corrections online after Nov 11)

How and When to Enroll

Enroll October 29 to November 11

There are no extra “grace days” this year! You MUST enroll in Medical to have coverage 1/1/09

22

Thank you for your time!

Questions?

23

Appendix

24

Why Changes Are Being Made

Assure benefits program is competitive at mid-point to the market

Provide choice to employees Consolidate vendors in order to:

Offer same benefits to all employees Better maximize value Reduce administrative cost and complexity

Adjust contribution and rate setting processes to: Better manage high cost of program More fairly share costs between employees and retirees Involve employees in data-driven decisions Build a Culture of Health