has s&p’s core earnings lived up to expectations

TRANSCRIPT

Has S&P’s Core Earnings lived up to expectations? Assessing the usefulness of Core Earnings relative to GAAP earnings

Dahlia Robinson *

College of Business University of South Florida

Tampa, FL 33620 [email protected]

Mark C. Dawkins Terry College of Business

University of Georgia Athens, GA 30602

M. Babajide Wintoki School of Business

University of Kansas Lawrence, KS 66045

Michael T. Dugan Culverhouse College of Commerce

University of Alabama Tuscaloosa, AL 35487-0220

September 5, 2008 JEL classification: G14; M40; M41 Keywords: Pro forma earnings; Core Earnings; Predictive ability; Information content; Acknowledgements: We thank Ben Ayers, Steve Baginski, Linda Bamber, Michael Bamber, Keji Chen, Jennifer Gaver, Robert Ingram, Ken Klassen, Stacie Laplante, Mary Stone, Gary Taylor, Eric Yeung, and participants at the Southeast Summer Accounting Research Colloquium for comments and suggestions that significantly improved the paper. * Corresponding author; Contact information: Tel: 813-974-6888; Fax: 813-974-6528; Email: [email protected].

Has S&P’s Core Earnings lived up to expectations? Assessing the usefulness of Core Earnings relative to GAAP earnings

ABSTRACT

In 2002, after deliberations with financial analysts, portfolio managers, corporate executives, and academic researchers, Standard & Poor’s (S&P) released a new measure of after-tax earnings from ongoing operations called Core Earnings. S&P maintained that Core Earnings should ostensibly improve U.S. financial reporting relative to GAAP earnings since it is a uniform measure of earnings and would be a more consistent indicator of firms’ future earnings and performance. This study uses valuation and predictive ability tests to examine how Core Earnings performs relative to GAAP earnings. The study documents that aggregate Core Earnings is less value relevant and has lower predictive ability than GAAP earnings. However, when the individual reconciling items used to derive Core Earnings are included with GAAP earnings, the explanatory power of the regression models increases significantly. Specifically, stock option expense, gains and losses from asset sales, goodwill impairment charges, reversals of prior year charges, and pension costs are incrementally significant to GAAP earnings. These results suggest that corporate disclosure of the reconciliation between GAAP and Core Earnings could improve investors’ and creditors’ assessments of current and future earnings.

Data availability: Data are available from public sources identified in this paper.

1

I. INTRODUCTION

In 2002, citing the ad hoc nature of calculating pro forma earnings prevailing at that time,

Standard & Poor’s (hereafter S&P) proposed a uniform earnings measure called Core Earnings.1

The calculation of Core Earnings was intended to adjust for managers’ and analysts’ arbitrary

and inconsistent inclusion and exclusion of revenues or expenses in earnings and to facilitate

across firms and within firm comparability.2 Supporters of the new earnings measure, including

many in the academic and business community, hailed it as a step “toward restoring uniformity,

clarity, and reliability to Corporate America’s financial statements….” (Business Week 2002).

Jeremy Siegel, a well-known and often-quoted University of Pennsylvania economics professor,

said “Core Earnings is exactly what investors need” (Business Week 2002), and The New York

Times included Core Earnings in its “Best Ideas of the Year” 2002 review. However, critics

argued that the increased volatility in the earnings measure induced by S&P’s aggressive

treatment of pension gains would ultimately decrease its usefulness to investors (Lahart 2002).

Given the divergent views on the potential usefulness of S&P’s Core Earnings measure, this

study assesses whether Core Earnings conveys incrementally useful information to market

participants by evaluating the valuation relevance and predictive ability of Core Earnings relative

to GAAP earnings.

Several studies document that pro forma earnings are value relevant and have information

content above GAAP earnings (e.g., Abarbanell and Lehavy 2002, Bradshaw and Sloan 2002,

1 “Standard & Poor’s Core Earnings” is a trademark of The McGraw-Hill Companies, Inc. 2 S&P Core Earnings differs from the “Core Earnings” referenced in studies such as Bhattacharya et al. (2003) and McVay (2006). These studies use “Core Earnings” to refer to firms’ continuing or ongoing operating earnings, regardless of whether there is intra-industry and intra-firm consistency in its calculation. S&P Core Earnings is calculated identically for all firms across all time periods.

2

Bhattacharya et al. 2003, Brown and Sivakumar 2003).3 However, the lack of uniformity or

consistency in the calculation of pro forma earnings creates difficulties in fully assessing the

value of pro forma earnings relative to GAAP earnings (Grant and Parker 2001). As noted by

S&P (2005), “The ability to compare costs across company and sectors is vital to the investing

community,” and this “ability depends on an accepted set of accounting rules observed by all”

(i.e., GAAP). The importance of resolving these difficulties has increased since the collapse of

Enron and WorldCom and the subsequent subprime meltdown, as capital market participants

have expressed concerns regarding the quality of earnings information released by U.S.

corporations.4 Additionally, regulators, standard setters, and investors have expressed concerns

about the reporting of customized and managed pro forma earnings.5

While S&P claims its Core Earnings measure will improve U.S. financial reporting since

it calculates earnings consistently across firms and within firm, there are indications it may be

less informative to investors. For example, S&P eliminates what it believes to be inappropriate

treatment of “one-time” expenses or non-recurring items. Specifically, the seven adjustments

S&P makes to GAAP earnings to arrive at Core Earnings are subtracting stock option expenses,

3 The term “pro forma earnings” refers to GAAP earnings adjusted for items deemed by management to be unusual or nonrecurring (Bhattacharya et al. 2003). Some studies refer to ad hoc pro forma earnings as STREET earnings (e.g., Brown and Sivakumar 2003). GAAP earnings can include non-recurring or one-time charges and non-cash items that have little impact on future earnings (Bray 2001, Pitt 2001, Weil 2001a). 4 Other firms that recently encountered financial difficulties and/or financial reporting issues include Global Crossing, Adelphia Communications, US Airways, PSINet, Pacific Gas and Electric, Covad, Winstar, Dynegy, TXU, Nortel Networks, Lucent, Tyco International. Firms entangled in or significantly impacted by the subprime meltdown include Fannie Mae, Freddie Mac, Merrill Lynch, Bear Stearns, and Lehman Brothers. 5 The SEC, regulators, and standard setters claim that reporting and emphasizing pro forma earnings confuse (less informed) investors, or are self-serving to managers (Derby 2001, Dreman 2001, Elstein 2001, Liesman and Weil 2001a,b). Bradshaw and Sloan (2002) find evidence supporting this viewpoint when they find that pro forma earnings tracked by analysts are increasingly inflated by the exclusion of income decreasing “special items” and “non-cash items.” Additionally, several academic studies find that less informed or naïve investors are misled or confused by pro forma earnings, and tend to transfer wealth to more informed or sophisticated investors (Johnson and Schwartz 2003, Doyle et al. 2003).

3

gains and losses from asset sales, settlements and litigation proceeds, and reversals of prior-year

charges, while adding goodwill impairment charges, post-retirement costs and pension costs.6

Assuming S&P’s notion of a uniform earnings measure is valid, S&P treats pension costs

inconsistently in the calculation of Core Earnings, which is likely to induce significant volatility

in Core Earnings relative to GAAP earnings.7 Goel and Thakor (2003) suggest that investors

dislike earnings volatility and are likely to pay less for firms with higher earnings volatility.

More importantly, they argue that earnings volatility leads to a bigger information advantage for

informed investors over uninformed investors. Given this fundamental characteristic of Core

Earnings, investors may not find Core Earnings as useful as GAAP earnings unless the other

S&P adjustments are value relevant.

This study examines the usefulness of Core Earnings on dimensions identified in prior

research. Specifically, we investigate how Core Earnings performs relative to GAAP earnings by

assessing its valuation relevance and predictive ability. Valuation relevance measures the

association of earnings with stock returns, and predictive ability is the ability of lagged earnings

to predict current period operating cash flows. Our sample consists of annual data from 6,817

firms over the five-year period from 2001-2005, yielding 26,744 firm-year observations for the

main tests.8

The results are as follows. The equity valuation test results show that GAAP earnings are

more value relevant than aggregate Core Earnings. However, Core Earnings disaggregated into

GAAP earnings and the various S&P adjustments, is more value relevant than GAAP earnings

6 Details of the specific differences in calculating Core Earnings versus GAAP earnings are discussed in section II. 7 In its technical bulletin issued on October 24, 2002, S&P (2002b) acknowledges that its treatment of pension income/ expense could add volatility to the Core Earnings estimates. 8 Firm observations are included in the sample for each year in which they have Core Earnings and GAAP earnings.

4

alone. Specifically, stock option expense, gains and losses from asset sales, goodwill impairment

charges, reversals of prior year charges, and pension costs are incrementally significant to GAAP

earnings in our valuation tests. Similarly, the predictive ability test shows that lagged GAAP

earnings predict current period operating cash flows more accurately than lagged aggregate Core

Earnings, while adding several components of disaggregated lagged Core Earnings to lagged

GAAP earnings predicts current period operating cash flows more accurately than lagged GAAP

earnings alone. In summary, the results suggest that the disclosure of the reconciliation between

GAAP and Core Earnings in annual financial statements may enhance investors’ and creditors’

assessments of current and future earnings.

The remainder of the paper is structured as follows. Section II provides details on S&P’s

calculation of Core Earnings. Section III summarizes the prior literature. Section IV presents and

discusses the research methodology and empirical results, and the paper concludes in Section V.

II. OVERVIEW OF S&P’S CORE EARNINGS MEASURE

In 2001 S&P distributed to targeted analysts, commentators, and journalists a note titled

“Measures of Corporate Earnings” (Standard & Poor’s 2001) that identified three measures of

earnings: as reported earnings, operating earnings, and pro forma earnings. The purpose of the

note was to generate discussion about how to calculate a uniform measure of earnings, and the

note proposed a new approach to calculating operating earnings. After distributing the note, S&P

spoke with securities and accounting analysts, portfolio managers, corporate executives,

academic researchers, and other investment professionals to see if a consensus could be reached

regarding a uniform earnings definition, and the result was a revised “Measures of Corporate

Earnings” published on May 14, 2002 (Standard & Poor’s 2002a). This document proposed

5

S&P’s new Core Earnings measure, which refers to firms’ after-tax earnings from ongoing

operations.

S&P’s Core Earnings Committee made refinements to Core Earnings on October 24,

2002 in a publication titled “Standard & Poor’s Core Earnings Technical Bulletin” (Standard &

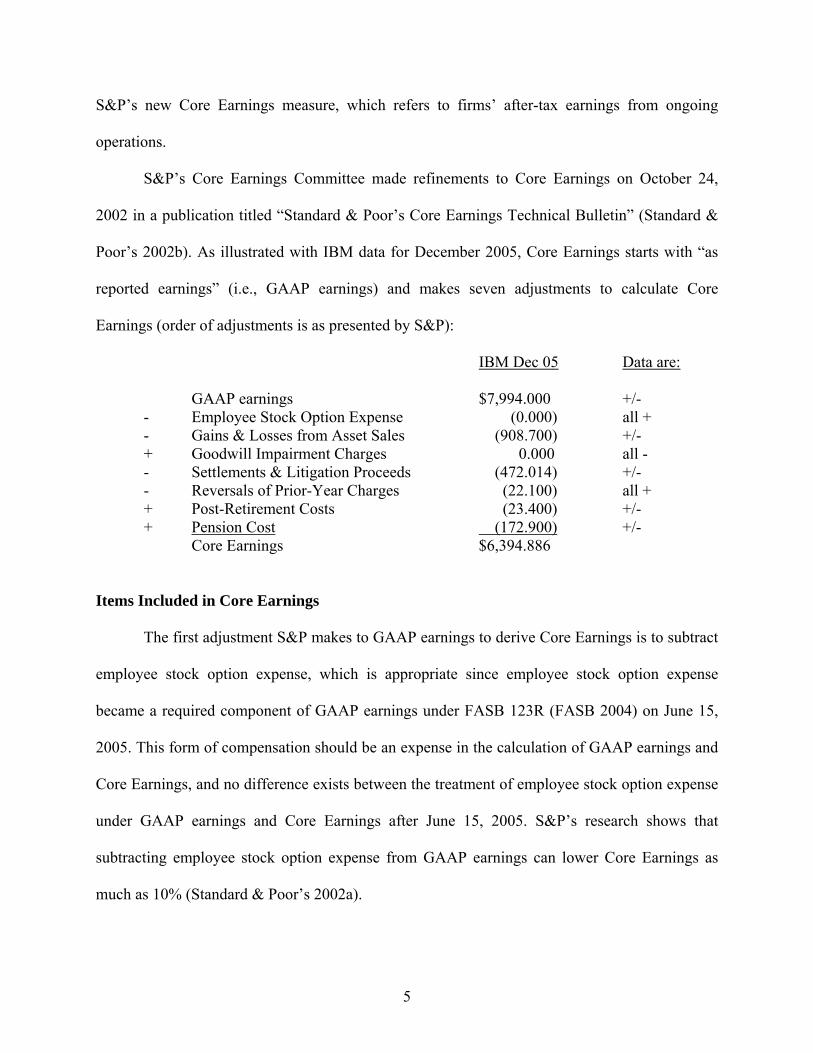

Poor’s 2002b). As illustrated with IBM data for December 2005, Core Earnings starts with “as

reported earnings” (i.e., GAAP earnings) and makes seven adjustments to calculate Core

Earnings (order of adjustments is as presented by S&P):

IBM Dec 05 Data are:

GAAP earnings $7,994.000 +/- - Employee Stock Option Expense (0.000) all + - Gains & Losses from Asset Sales (908.700) +/- + Goodwill Impairment Charges 0.000 all - - Settlements & Litigation Proceeds (472.014) +/- - Reversals of Prior-Year Charges (22.100) all + + Post-Retirement Costs (23.400) +/- + Pension Cost (172.900) +/-

Core Earnings $6,394.886 Items Included in Core Earnings

The first adjustment S&P makes to GAAP earnings to derive Core Earnings is to subtract

employee stock option expense, which is appropriate since employee stock option expense

became a required component of GAAP earnings under FASB 123R (FASB 2004) on June 15,

2005. This form of compensation should be an expense in the calculation of GAAP earnings and

Core Earnings, and no difference exists between the treatment of employee stock option expense

under GAAP earnings and Core Earnings after June 15, 2005. S&P’s research shows that

subtracting employee stock option expense from GAAP earnings can lower Core Earnings as

much as 10% (Standard & Poor’s 2002a).

6

The second adjustment S&P makes to GAAP earnings to derive Core Earnings is to

remove gains/losses from asset sales since most firms “are not in the business of buying and

selling their own operating assets” as part of their principal business, and gains/losses from asset

sales are incidental to the continuing operations of most firms (Standard & Poor’s 2002a, 10).9

The third adjustment S&P makes to GAAP earnings to derive Core Earnings is to add

goodwill impairment charges. FASB 142 (FASB 2001) became effective on December 15, 2001,

and requires firms to write-off goodwill if it is impaired (i.e., its market value is less than its

book value). S&P’s justification for adding goodwill impairment charges is based on the fact that

“the amortization of goodwill is not considered a period cost expended in the creation of

revenues, the inclusion of goodwill impairment charges would distort the company’s operating

performance. Since any goodwill impairment implies that the company’s earnings will suffer in

the future, including a charge for goodwill impairment in Core Earnings would doubly penalize

the company’s performance” (Standard & Poor’s 2002a, 10).

The fourth adjustment S&P makes to GAAP earnings to derive Core Earnings is to

subtract settlements and litigation proceeds since they are ancillary to firms’ principal business

activities. GAAP earnings include settlements and litigation proceeds.

The fifth adjustment S&P makes to GAAP earnings to derive Core Earnings is to subtract

reversals of prior year charges (e.g., restructuring charges) since “these reversals distort income

in the period in which they are recognized because they relate to activities and the expenses of

those activities in prior periods” (Standard & Poor’s 2002b, 2). GAAP earnings include reversals

of prior year charges.

9 Notable exceptions include banks, mortgage and leasing companies, real estate development companies and Real Estate Investment Trusts, and they are specifically excluded from the sample.

7

The sixth and seventh adjustments S&P makes to GAAP earnings to derive Core

Earnings are to add post-retirement costs and pension costs since these costs are part of

employee compensation even though they are not reflected in employee paychecks. Core

Earnings has been criticized because S&P includes interest costs as part of pension costs, and

then treats interest costs as a charge against Core Earnings only when actual pension plan returns

do not cover the interest cost, which results in increased volatility of Core Earnings. According

to S&P, “The use of actual market returns may add to the volatility of the pension components

and the overall Standard & Poor's Core Earnings figures. Standard & Poor's Core Earnings are

designed to measure the actual results of a company’s core business. This differs from some of

the considerations that may have been involved in the preparation of the rules under SFAS 87

covering pension expense, which used an expected return on plan assets” (Standard and Poor’s

2002b, 2-3).

Volatility of Core Earnings

When S&P introduced its Core Earnings measure in 2002, Lahart (2002) expressed

concerns about the usefulness of Core Earnings year-to-year comparisons as a result of the

volatility added by the pension adjustments. Specifically, Core Earnings excludes pension plan

gains yet includes pension plan shortfalls, which means that pension plan shortfalls (i.e., interest

cost or expense) are charged against Core Earnings. A pension plan shortfall occurs when a

pension plan’s actual returns do not cover the increase in a firm’s retirement obligations to its

workers. S&P makes this charge against earnings even if a pension plan is overfunded, whereas a

pension plan overage or excess is not added to Core Earnings.

Lahart (2002) notes that “…throwing pension interest cost into the [Core Earnings]

equation gums up the whole works, discrediting the venture and ensuring that investors

8

ultimately don’t pay it much heed.” The editors of Business Week (Business Week 2002) note

that “…Core Earnings…would also be more genuine…”, yet they and Coy (2002) acknowledge

the volatility concerns regarding the treatment of pension interest cost. Howard Silverblatt of

S&P acknowledges the volatility problem, yet defends the methodology by noting that S&P

provides the data so investors can exclude pension interest expense from Core Earnings if they

choose.10 However, for investors and creditors to use Core Earnings, they must be able to assess

its usefulness as an earnings measure relative to GAAP earnings. Thus, we assess the valuation

relevance and predictive ability of Core Earnings relative to GAAP earnings. We next review

relevant prior studies that focus on the usefulness of GAAP earnings.

III. SUMMARY OF PRIOR RESEARCH

Three prior studies are directly relevant to this study because they compare the relative

performance of various earnings measures: Bradshaw and Sloan (2002), Brown and Sivakumar

(2003), and Bhattacharya et al. (2003). Bradshaw and Sloan (2002) investigate the reporting of

GAAP and pro forma earnings over 1986-1997, and find a significant increase in the frequency

and magnitude of differences between GAAP earnings and pro forma earnings. Additionally,

they find that firms tend to report pro forma earnings when it exceeds GAAP earnings, and that

pro forma earnings are more associated with future stock prices than GAAP earnings (i.e.,

investors generally price pro forma earnings over GAAP earnings).

Brown and Sivakumar (2003) assess the quality of three earnings measures: (1)

Compustat quarterly EPS (basic) before extraordinary items, (2) Compustat quarterly EPS from 10 In “Standard & Poor’s Core Earnings Technical Bulletin” released on October 24, 2002 (Standard & Poor’s 2002b), S&P changed “the treatment of interest cost in the calculation of pension and other post-employment benefit plan income/expense.” Specifically, S&P now includes interest cost in the calculation of net pension and OPEB income expense. If interest cost is covered by the actual returns of the pension fund, interest cost is not charged against S&P Core Earnings. S&P acknowledges that using actual market returns may increase the volatility of the pension components and Core Earnings, and defend their methodology by noting that “Core Earnings are designed to measure the actual returns of a company’s core business.”

9

operations, and (3) the actual EPS figure published by I/B/E/S, which they label as “street

earnings.” They report that I/B/E/S actual earnings has higher quality relative to GAAP basic and

GAAP operating income in terms of predictive ability and value relevance.

Bhattacharya et al. (2003) compare pro forma earnings, I/B/E/S earnings, and GAAP

earnings to determine which earnings measure is viewed as more informative and more

persistent by capital market participants. Their GAAP measure is GAAP diluted operating EPS,

their I/B/E/S measure is actual EPS from the I/B/E/S database, and their pro forma measure is

pro forma diluted EPS from actual press releases (hand-collected). Their short-window abnormal

return tests suggest that pro forma earnings are more informative than GAAP earnings, while

their analyst forecast revision tests suggest that pro forma earnings are more persistent than

GAAP earnings.

This study differs from the previous studies in three substantive ways. First, none of the

studies examines the performance of aggregate Core Earnings relative to other earnings metrics

such as GAAP earnings. Since S&P’s intent in calculating this new measure was to improve the

usefulness of earnings reports to analysts and investors (S&P 2001), it is important to empirically

document how Core Earnings performs relative to GAAP earnings on dimensions assessing its

informativeness to investors.

Second, we analyze more recent data. The sample period is 2001-2005 because we

require all firms to have Core Earnings and GAAP earnings. Core Earnings is available on

Wharton Research Data Services and Standard & Poor’s Research Insights database for years

2001 and later. Bradshaw and Sloan’s sample covers 1986-1997, Brown and Sivakumar’s sample

covers 1989-1997, and Bhattacharya et al.’s sample covers 1998-2000.

10

Third, this study examines the impact of the seven adjustments S&P makes to GAAP

earnings to calculate Core Earnings: subtracting stock option expenses, gains and losses from

asset sales, settlements and litigation proceeds, and reversals of prior-year charges, while adding

goodwill impairment charges, post-retirement costs and pension costs. Specifically, we assess

whether each adjustment conveys incrementally useful information to market participants by

evaluating the valuation relevance and predictive ability of disaggregated Core Earnings relative

to GAAP earnings.

Other pro forma studies include Abarbanell and Lehavy 2002, Doyle et al. 2003, Johnson

and Schwartz 2003, Frederickson and Miller 2004, Bhattacharya et al. 2007a, Bhattacharya et al.

2007b, Lougee and Marquardt 2004, Bhattacharya et al. 2004, Bowen et al. 2005, Doyle and

Soliman 2005, Elliott 2006, Entwistle et al. 2006, and McVay 2006. None of these studies

incorporate S&P’s Core Earnings measure, making our study the first we know of that assesses

S&P Core Earnings as an alternative earnings measure.

IV. RESEARCH METHOD AND EMPIRICAL RESULTS

Sample Selection

We start with a sample of all firms on Compustat with S&P Core Earnings over the 2001-

2005 period. This sample includes 8,991 firms and 34,769 firm-years. Our analysis requires

annual stock returns data, and so we merge the initial S&P Core Earnings sample with CRSP.

This gives us an unbalanced panel consisting of 6,817 unique firms and 26,744 firm years for

which there are both Core Earnings and annual stock returns data for at least one year between

2001 and 2005. This panel forms the base sample for our subsequent analysis. We are restricted

to using annual rather than quarterly earnings/returns data, since S&P provides data only on the

annual adjustments to GAAP that form the Core Earnings numbers.

11

Descriptive Statistics

Table 1 provides descriptive statistics for the variables in our analyses, and reports the

mean, median, minimum, maximum, Pr > |t| and t-value for a difference from zero. As evident

from Table 1, the mean (median) Core EPS of 0.2409 (0.4229) exceeds the mean (median)

GAAP EPS of 0.1294 (0.3234). Thus, S&P’s uniform earnings measure produces mean and

median EPS that exceed GAAP EPS for the years 2001-2005. This difference is primarily driven

by the following Core Earnings adjustments: stock option expense of 0.1156 (0.0490), gains and

losses from asset sales of 0.0202 (0.0000), goodwill impairment charges of -0.0324 (0.0000), and

pension costs of -0.0199 (0.0000).

Research Methodology

We measure earnings quality on two dimensions: (1) value relevance (Easton and Harris

1991; Aboody and Lev 1998; Brown and Sivakumar 2003) and (2) predictive ability (Aboody

and Lev 1998; Barth, Cram and Nelson 2001; Brown and Sivakumar 2003).

Value Relevance Tests

Our first test of earnings follows the methodology originally developed by Easton and

Harris (1991). Using this method, we examine how well the level of earnings divided by the

price at the beginning of the year explains the stock returns over the year. Easton and Harris

(1991) provide two value relevance models. The first involves a regression of returns on the level

of earnings divided by price at the beginning of the period, and the second involves a regression

of returns on the change in earnings over a period, also divided by the price at the beginning of

the period.

12

In our first set of tests, we regress returns on the levels of earnings. Thus, we estimate the

following model (1) to assess the valuation relevance of GAAP earnings, and model (2) to assess

the valuation relevance of Core Earnings:

tititGAAPiti PEPSR ,1,,10, εαα ++= − (1)

titiCOREti PEPSR ,1,20, εαα ++= − (2)

We then estimate the following seven models to assess the incremental valuation relevance of

each specific Core Earnings adjustment:

tititCOREititGAAPiti PSOPTEXPPEPSR ,1,,31,,10, εααα +++= −− (3)

titiCOREtitGAAPiti PSGAINLOSSPEPSR ,1,41,,10, εααα +++= −− (4)

titiCOREtitGAAPiti PSGWIMPAIRPEPSR ,1,51,,10, εααα +++= −− (5)

titiCOREtitGAAPiti PSSETTLEMTPEPSR ,1,61,,10, εααα +++= −− (6)

titiCOREtitGAAPiti PSREVERSALPEPSR ,1,71,,10, εααα +++= −− (7)

titiCOREtitGAAPiti PSPRCOSTSPEPSR ,1,81,,10, εααα +++= −− (8)

titiCOREtitGAAPiti PSPENCOSTSPEPSR ,1,91,,10, εααα +++= −− (9) where: Ri,t = Raw return or size-adjusted return for year t; Pi,t-1 = Stock price at the end of year t-1; EPSGAAPi,t = Operating EPS (diluted) reported by Compustat (Q181) for year t;EPSCOREi,t = Core EPS (diluted) reported by S&P (SPCEDQ) for year t; SOPTEXPCOREi,t = Employee stock option expense for year t; SGAINLOSSCOREi,t = Gains and losses from asset sales for year t; SGWIMPAIRCOREi,t = Goodwill impairment charges for year t; SSETTLEMTCOREi,t = Settlements and litigation proceeds for year t; SREVERSALCOREi,t = Reversals of prior-year charges for year t; SPRCOSTSCOREi,t = Post-retirement costs for year t; SPENCOSTSCOREi,t = Pension costs for year t; The results from the regressions in models 1-9, using raw returns are presented in Table

2, and the size-adjusted return results are presented in Table 3. Since we are using panel data, it

is possible that the residuals for a given firm can be correlated across years (serial correlation), or

13

that the residuals of a given year may be correlated across different firms (cross-sectional

dependence); both of these could bias the standard errors downwards and inflate t-statistics (see

Petersen (2008)). Thus, to avoid biased inference, we report t-statistics that are clustered by firm

and by year in all our regression results.

In Table 2 (raw returns), Model 1 shows an adjusted R2 of 3.08% for GAAP earnings,

and model 2 shows an adjusted R2 of 2.90% for aggregate Core Earnings. We conduct a

statistical test of model 1 versus model 2 using Vuong (1989), and the results indicate that the

GAAP earnings model is significantly better than the aggregate Core Earnings model at α ≤ 0.00

(z-statistic = -4.67). When we disaggregate the seven Core Earnings adjustments in models 3-9

we find that five of the adjustments are incrementally significant to GAAP earnings.

Specifically, stock option expense, gains and losses from asset sales, goodwill impairment

charges, reversals of prior year charges, and pension costs are incrementally significant to GAAP

earnings, with each adjustment’s Vuong (1989) z-statistic indicating significance at α ≤ 0.00.

Thus, disaggregating the Core Earnings adjustments improves the performance of five of the

seven adjustment models relative to the GAAP earnings model (i.e., model 1).

In Table 3 (size-adjusted returns), Model 1 shows an adjusted R2 of 2.59% for GAAP

earnings, and model 2 shows an adjusted R2 of 2.44% for aggregate Core Earnings. The Vuong

(1989) test of model 1 versus model 2 indicates that the GAAP earnings model is significantly

better than the aggregate Core Earnings model at α ≤ 0.00 (z-statistic = -2.64). When we

disaggregate the seven Core Earnings adjustments in models 3-9, we find that five of the

adjustments are incrementally significant to GAAP earnings. Specifically, stock option expense,

gains and losses from asset sales, goodwill impairment charges, reversals of prior year charges,

and pension costs are incrementally significant to GAAP earnings, with each adjustment’s

14

Vuong (1989) z-statistic indicating significance at α ≤ 0.00. Thus, consistent with the raw return

results in Table 2, disaggregating the Core Earnings adjustments improves the performance of

five of the seven adjustment models relative to the GAAP earnings model (i.e., model 1).

We also compare the valuation relevance of GAAP earnings and Core Earnings by

regressing raw returns and size-adjusted returns on EPS and changes in EPS, both divided by

price. Thus, we estimate model 10 to assess the valuation relevance of GAAP earnings and

change in GAAP earnings, and model 11 to assess the valuation relevance of Core Earnings and

change in Core Earnings:

tititGAAPititGAAPiti PPSPEPSR ,1,,101,,10, E εααα +Δ++= −− (10)

tititCOREititCOREiti PEPSPEPSR ,1,,111,,20, εααα +Δ++= −− (11)

We then estimate the following seven models to assess the incremental valuation relevance of each

specific Core Earnings adjustment and change in the adjustment:

tititCOREititCOREititGAAPititGAAPiti PSOPTEXPPSOPTEXPPPSPEPSR ,1,,121,,31,,101,,10, E εααααα +Δ++Δ++= −−−− (12)

tititCOREititCOREititGAAPititGAAPiti PSGAINLOSSPSGAINLOSSPPSPEPSR ,1,,131,,41,,101,,10, E εααααα +Δ++Δ++= −−−−

(13) tititCOREititCOREititGAAPititGAAPiti PSGWIMPAIRPSGWIMPAIRPPSPEPSR ,1,,141,,51,,101,,10, E εααααα +Δ++Δ++= −−−−

(14) tititCOREititCOREititGAAPititGAAPiti PSSETTLEMTPSSETTLEMTPPSPEPSR ,1,,151,,61,,101,,10, E εααααα +Δ++Δ++= −−−−

(15) tititCOREititCOREititGAAPititGAAPiti PSREVERSALPSREVERSALPPSPEPSR ,1,,161,,71,,101,,10, E εααααα +Δ++Δ++= −−−−

(16) tititCOREititCOREititGAAPititGAAPiti PSPRCOSTSPSPRCOSTSPPSPEPSR ,1,,171,,81,,101,,10, E εααααα +Δ++Δ++= −−−−

(17) tititCOREititCOREititGAAPititGAAPiti PSPENCOSTSPSPENCOSTSPPSPEPSR ,1,,181,,91,,101,,10, E εααααα +Δ++Δ++= −−−−

(18) where: Ri,t = Raw return or size-adjusted return for year t; Pi,t-1 = Stock price at the end of year t-1; EPSGAAPi,t = Operating EPS (diluted) reported by Compustat (Q181) for year t;

15

ΔEPSGAAPi,t = Change in operating EPS (diluted) reported by Compustat (Q181) for year t;

EPSCOREi,t = Core EPS (diluted) reported by S&P (SPCEDQ) for year t; SOPTEXPCOREi,t = Employee stock option expense for year t; ΔSOPTEXPCOREi,t = Change in employee stock option expense for year t; SGAINLOSSCOREi,t = Gains and losses from asset sales for year t; ΔSGAINLOSSCOREi,t = Change in gains and losses from asset sales for year t; SGWIMPAIRCOREi,t = Goodwill impairment charges for year t; ΔSGWIMPAIRCOREi,t = Change in goodwill impairment charges for year t; SSETTLEMTCOREi,t = Settlements and litigation proceeds for year t; ΔSSETTLEMTCOREi,t = Change in settlements and litigation proceeds for year t; SREVERSALCOREi,t = Reversals of prior-year charges for year t; ΔSREVERSALCOREi,t = Change in reversals of prior-year charges for year t; SPRCOSTSCOREi,t = Post-retirement costs for year t; ΔSPRCOSTSCOREi,t = Change in post-retirement costs for year t; SPENCOSTSCOREi,t = Pension costs for year t; ΔSPENCOSTSCOREi,t = Change in pension costs for year t;

Table 4 presents the model 10-18 raw return results, and Table 5 presents the model 10-

18 size-adjusted return results. In Table 4 (raw returns), model 10 shows an adjusted R2 of 3.98%

for GAAP earnings, and model 11 shows an adjusted R2 of 3.66% for aggregate Core Earnings.

The Vuong (1989) test comparing model 10 versus model 11 indicates that the GAAP earnings

model is significantly better than the aggregate Core Earnings model at α ≤ 0.00 (z-statistic = -

6.40). When we disaggregate the seven Core Earnings adjustments in models 12-18, we find that

six of the seven adjustments are incrementally significant to GAAP earnings. Specifically, stock

option expense, gains and losses from asset sales, goodwill impairment charges, settlements and

litigation proceeds, reversals of prior year charges, and pension costs are incrementally

significant to GAAP earnings, with each adjustment’s Vuong (1989) z-statistic indicating

significance at α ≤ 0.03 (five of six significant at α ≤ 0.00). Thus, disaggregating the Core

Earnings adjustments improves the performance of six of the seven adjustment models relative to

16

the GAAP earnings model (i.e., model 10), with the only insignificant adjustment being post-

retirement costs.

In Table 5 (size-adjusted returns), model 10 shows an adjusted R2 of 3.89% for GAAP

earnings, and model 11 shows an adjusted R2 of 3.66% for aggregate Core Earnings. The Vuong

(1989) test comparing models 10 and 11 indicates that the GAAP earnings model is significantly

better than the aggregate Core Earnings model at α ≤ 0.00 (z-statistic = -6.40). When we

disaggregate the seven Core Earnings adjustments in models 12-18 we again find that six of the

adjustments are incrementally significant to GAAP earnings. Specifically, stock option expense,

gains and losses from asset sales, goodwill impairment charges, settlements and litigation

proceeds, reversals of prior year charges, and pension costs are incrementally significant to

GAAP earnings, with each adjustment’s Vuong (1989) z-statistic indicating significance at α ≤

0.03 (five of six significant at α ≤ 0.00). Thus, consistent with the raw return results in Table 4,

disaggregating the Core Earnings adjustments improves the performance of six of the seven

adjustment models relative to the GAAP earnings model (i.e., model 10), with the only

insignificant adjustment again being post-retirement costs.

Predictive Ability Test

Our second test of the quality of the earnings numbers is a predictive ability test (similar

in spirit to that in Brown and Sivakumar (2003) and Barth, Cram and Nelson 2001). In this test,

we measure the ability of the earnings per share at the end of one year to predict operating cash

flow (per share) at the end of the next year. Thus, we estimate model (1) (below) to assess the

predictive ability of GAAP earnings, and model (2) to assess the predictive ability of Core

Earnings:

titGAAPiti EPSCF ,1,10, εαα ++= − (1)

17

titCOREiti EPSCF ,1,20, εαα ++= − (2)

We then estimate the following seven models to assess the incremental predictive ability of each

specific Core Earnings adjustment:

titCOREitGAAPiti SOPTEXPEPSCF ,1,31,10, εααα +++= −− (3)

titCOREitGAAPiti SGAINLOSSEPSCF ,1,41,10, εααα +++= −− (4)

titCOREitGAAPiti SGWIMPAIREPSCF ,1,51,10, εααα +++= −− (5)

titCOREitGAAPiti SSETTLEMTEPSCF ,1,61,10, εααα +++= −− (6)

titCOREitGAAPiti SREVERSALEPSCF ,1,71,10, εααα +++= −− (7)

titCOREitGAAPiti SPRCOSTSEPSCF ,1,81,10, εααα +++= −− (8)

titCOREitGAAPiti SPENCOSTSEPSCF ,1,91,10, εααα +++= −− (9) where: CFi,t = Cash flow for year t; EPSGAAPi,t-1 = Operating EPS (diluted) reported by Compustat (Q181) for year t-1;EPSCOREi,t-1 = Core EPS (diluted) reported by S&P (SPCEDQ) for year t-1; SOPTEXPCOREi,t-1 = Employee stock option expense for year t-1; SGAINLOSSCOREi,t-1 = Gains and losses from asset sales for year t-1; SGWIMPAIRCOREi,t-1 = Goodwill impairment charges for year t-1; SSETTLEMTCOREi,t-1 = Settlements and litigation proceeds for year t-1; SREVERSALCOREi,t-1 = Reversals of prior-year charges for year t-1; SPRCOSTSCOREi,t-1 = Post-retirement costs for year t-1; SPENCOSTSCOREi,t-1 = Pension costs for year t-1;

The results of the predictive ability tests are presented in Table 6. Again, we report t-

statistics based on standard errors clustered by both firm and year to account for serial

correlation and cross-sectional dependence of the residuals.

Model 1 shows an adjusted R2 of 2.68% for GAAP earnings, and model 2 shows an

adjusted R2 of 2.67% for aggregate Core Earnings. The Vuong (1989) test comparing model 1

and model 2 indicates that the GAAP earnings model is significantly better than the aggregate

Core Earnings model at α ≤ 0.00 (z-statistic = -2.63). When we disaggregate the seven Core

Earnings adjustments in models 3-9, we find that five of the adjustments are incrementally

18

significant to GAAP earnings. Specifically, stock option expense, goodwill impairment charges,

settlements and litigation proceeds, reversals of prior year charges, and post-retirement costs are

incrementally significant to GAAP earnings, with each adjustment’s Vuong (1989) z-statistic

indicating significance at α ≤ 0.04 or better. Thus, disaggregating the Core Earnings adjustments

improves the performance of five of the seven adjustment models relative to the GAAP earnings

model (i.e., model 1).

Summary

The raw return and size-adjusted return valuation tests in Tables 2 and 3 regress raw

returns and size-adjusted returns on EPS. The results indicate that GAAP earnings outperforms

aggregate Core Earnings, yet disaggregating the Core Earnings adjustments improves the

performance of five of the seven adjustment models relative to the GAAP earnings model.

Specifically, stock option expense, gains and losses from asset sales, goodwill impairment

charges, reversals of prior year charges, and pension costs are incrementally significant to GAAP

earnings, with the only insignificant adjustments being settlements and litigation proceeds and

post-retirement costs.

The raw return and size-adjusted return valuation tests in Tables 4 and 5 regress raw

returns and size-adjusted returns on EPS and changes in EPS. Similar to Tables 2 and 3, the

results indicate that GAAP earnings outperforms aggregate Core Earnings, yet disaggregating

the Core Earnings adjustments improves the performance of six of the seven adjustment models

relative to the GAAP earnings model. Specifically, stock option expense, gains and losses from

asset sales, goodwill impairment charges, settlements and litigation proceeds, reversals of prior

year charges, and pension costs are incrementally significant to GAAP earnings, with the only

insignificant adjustment being post-retirement costs.

19

The predictive ability tests regress cash flow on lagged earnings in Table 6, and the

results indicate that GAAP earnings outperform aggregate Core Earnings. When we

disaggregate the seven Core Earnings adjustments we find that five of the adjustments are

incrementally significant to GAAP earnings. Specifically, stock option expense, goodwill

impairment charges, settlements and litigation proceeds, reversals of prior year charges, and

post-retirement costs are incrementally significant to GAAP earnings. Thus, the predictive ability

tests provide corroborating evidence for the value relevance tests, and both sets of tests indicate

that disaggregated Core Earnings potentially provide useful information to investors and

creditors.

V. CONCLUSION

S&P began reporting Core Earnings in 2002 with the intent of improving U.S. financial

reporting by providing a uniform measure of earnings. S&P makes seven adjustments to GAAP

earnings to calculate Core Earnings: stock option expense, gains and losses from asset sales,

goodwill impairment charges, settlements, reversals of prior-year charges, and post retirement

and pension costs. This study examines the value relevance of Core Earnings relative to GAAP

earnings on two dimensions of earnings quality – equity valuation and predictive ability. Critics

expected Core Earnings would not be useful to investors because it would induce higher

volatility in earnings.

We find that aggregate Core Earnings is less value relevant and has lower predictive

ability than GAAP earnings, while disaggregated Core Earnings is more value relevant and has

higher predictive ability than GAAP earnings. Specifically, stock option expense, gains and

losses from asset sales, goodwill impairment charges, reversals of prior year charges, and

pension costs are incrementally significant to GAAP earnings. The results suggest that

20

accounting policy makers and standard setters should consider requiring the disclosure of the

reconciliation between GAAP and Core Earnings in annual financial statements since the

measure may enhance investors’ and creditors’ assessments of current and future earnings.

21

REFERENCES

Abarbanell, J., and R. Lehavy. 2002. Differences in commercial database reported earnings.

Working paper, University of North Carolina and University of California, Berkeley. Aboody, D., and B. Lev. 1998. The value relevance of intangibles: The case of software

capitalization. Journal of Accounting Research 36 (Supplement): 161-190. Barth, M.E., D.P. Cram, K.K. Nelson. 2001. Accruals and the Prediction of Future Cash Flows.

The Accounting Review 76 (1): 27-58 Bhattacharya, N., E.L. Black, T.E. Christensen, and C.R. Larson. 2003. Assessing the relative

informativeness and permanence of pro forma earnings and GAAP operating earnings. Journal of Accounting and Economics 36: 285-319.

Bhattacharya, N., E.L. Black, T.E. Christensen, and R.D. Mergenthaler. 2004. Empirical

evidence on recent trends in pro forma reporting. Accounting Horizons 18 (1): 27-43. Bhattacharya, N., E.L. Black, T.E. Christensen, and R.D. Mergenthaler. 2007a. Who trades on

pro forma earnings information? The Accounting Review 82 (3): 581-619. Bhattacharya, N., E.L. Black, T.E. Christensen, and K. Allee. 2007b. Pro forma disclosure and

investor sophistication: External validation of experimental evidence using archival data. Accounting Organizations of Society 32 (3): 201-222.

Bowen, R., A. Davis, and D. Matsumoto. 2005. Emphasis on pro forma versus GAAP earnings

in quarterly press releases: Determinants, SEC intervention, and market reactions. The Accounting Review 80 (4): 1011–1038.

Bradshaw, M., and R. Sloan. 2002. GAAP versus the Street: An empirical assessment of two

alternative definitions of earnings. Journal of Accounting Research 40 (1): 41–66. Bray, C. 2001. SEC looking at pro forma earnings with ‘purpose in mind’. Dow Jones News

Service (November 8). Brown, L. and K. Sivakumar 2003. “Comparing the value relevance of two operating income

measures. Review of Accounting Studies 8 (4): 561-572. Business Week. 2002. A good idea about earnings. Business Week (May 27). Coy, P. 2002. Why better numbers really matter. Business Week (May 27). Derby, M. 2001. Investors getting more data, but is it the right data? Capital Markets Report

(August 31).

22

Doyle, J., R. Lundholm, and M. Soliman. 2003. The predictive value of expenses excluded from pro forma earnings. Review of Accounting Studies 8 (2–3): 145–174.

Doyle, J., and M. Soliman. 2005. Do managers define “Street” exclusions to meet or beat analyst

forecasts? Working paper, University of Utah and Stanford University. Dreman, D. 2001. Fantasy earnings. Forbes (October 1): 134. Easton, P., and T. Harris. 1991. Earnings as an explanatory variable for returns. Journal of

Accounting Research 29 (1): 19-36. Elliott, W. 2006. Are investors influenced by pro forma emphasis and reconciliations in earnings

announcements? The Accounting Review 81 (1): 113-133. Elstein, A. 2001. ’Unusual expenses’ raise concerns. The Wall Street Journal (August 23): C1. Entwistle, G., G. Feltham, and C. Mbagwu. 2006. Financial reporting regulation and the

reporting of pro forma earnings. Accounting Horizons 20 (1): 39-55. Financial Accounting Standards Board (FASB). 2001. Goodwill and Other Intangible Assets.

Statements of Financial Accounting Standards No. 142. Norwalk, CT: FASB. Financial Accounting Standards Board (FASB). 2004. Share-Based Payments. Statements of

Financial Accounting Standards No. 123R. Norwalk, CT: FASB. Frederickson, J., and J. Miller. 2004. The effects of pro forma earnings disclosures on analysts’

and nonprofessional investors equity valuation judgments. The Accounting Review 79 (3): 667-686.

Goel, A., and A. Thakor. 2003. Why do firms smooth earnings? Journal of Business 76: 151-

192. Grant, J., and L. Parker. 2001. EBITDA. Research in Accounting Regulation 15: 205-211. Johnson, W.B. and W.C. Schwartz. 2003. Are investors misled by pro forma earnings?

Working paper, University of Iowa. Lahart, J. 2002. S&P’s core earnings fall flat. CNN/Money website, October 24. Liesman, S. and J. Weil. 2001a. Two profit calculations for S&P 500 differ – ‘Special items’ are

key to gap between First Call, S&P figures. The Wall Street Journal (August 24): A2. Liesman, S. and J. Weil. 2001b. S&P to wade into pro-forma earnings mess. The Wall Street

Journal (November 7): C1.

23

Lougee, B. and C. Marquardt. 2004. Earnings informativeness and strategic disclosure: An empirical examination of “pro forma” earnings. The Accounting Review 79 (3): 769-795.

McVay, S. 2006. Earnings management using classification shifting: An examination of Core

Earnings and special items. The Accounting Review 81 (3): 501-531. Petersen, M.A. 2008. Estimating Standard Errors in Finance Panel Data Sets: Comparing

Approaches. Review of Financial Studies, forthcoming. Pitt, H. 2001. Remarks before the AICPA governing council. Miami Beach, FL (October 22). Standard and Poor’s. 2001. Measures of corporate earnings. Originally released November 7. Standard and Poor’s. 2002a. Measures of corporate earnings. Revised May 14. Standard and Poor’s. 2002b. Standard & Poor’s Core Earnings technical bulletin. October 24. Standard and Poor’s. 2005. Impact of Option Expensing on the S&P 500 Earnings. November

21. Vuong, Q. 1989. Likelihood ratio tests for model selection and non-nested hypotheses.

Econometrica 57 (2): 307-333. Weil, J. 2001a. SEC threatens to sue companies for misleading ‘pro forma’ results. The Wall

Street Journal (December 5): A2. Weil, J. 2001b. Moving target: What's the P/E ratio? Well, depends on what is meant by earnings

- Terms like `operating,' `core,' `pro forma' catch fire, leave investors muddled - `earnings before bad stuff'. The Wall Street Journal (August 21): A1

24

TABLE 1: DESCRIPTIVE STATISTICS FOR GAAP AND CORE EARNINGS VARIABLES

Variable N Mean Median Minimum Maximum Pr > |t| t Value

EPSGAAPi,t 26744 0.129404 0.323437 -13.2196 5.513333 <.0001 9.28 EPSCOREi,t 26744 0.240876 0.42285 -13.5435 5.828636 <.0001 16.81

SOPTEXPCOREi,t 26744 0.115568 0.049025 0 1.3849 <.0001 92.22 SGAINLOSSCOREi,t 26744 0.020188 0 -0.54922 1.027444 <.0001 21.06 SGWIMPAIRCOREi,t 26744 -0.03241 0 -1.58406 0 <.0001 -27.63 SSETTLEMTCOREi,t 26744 -0.00084 0 -0.26067 0.212121 0.0013 -3.22 SREVERSALCOREi,t 26744 0.001241 0 0 0.053228 <.0001 30.31 SPRCOSTSCOREi,t 26744 0.000164 0 -0.04498 0.049572 0.0014 3.20

SPENCOSTSCOREi,t 26744 -0.0199 0 -0.74667 0.164388 <.0001 -30.61 CFi,t 26744 0.454949 0.58158 -6.7375 13.01697 <.0001 20.63

PRICEi,t-1 26744 18.56339 14 0.15 83.80 <.0001 174.09 RAW RETURNi,t 26744 0.152338 0.077359 -0.86023 3.676228 <.0001 34.75 SIZE-ADJUSTED

RETURNi,t 26744 0.033764 -0.04824 -0.92893 3.378242 <.0001 8.21

Notes to Table 1: EPSGAAPi,t = Operating EPS (diluted) reported by Compustat (Q181) for year t;EPSCOREi,t = Core EPS (diluted) reported by S&P (SPCEDQ) for year t; SOPTEXPCOREi,t = Employee stock option expense for year t; SGAINLOSSCOREi,t = Gains and losses from asset sales for year t; SGWIMPAIRCOREi,t = Goodwill impairment charges for year t; SSETTLEMTCOREi,t = Settlements and litigation proceeds for year t; SREVERSALCOREi,t = Reversals of prior-year charges for year t; SPRCOSTSCOREi,t = Post-retirement costs for year t; SPENCOSTSCOREi,t = Pension costs for year t; CFi,t = Cash flow for year t; PRICEi,t-1 = Stock price at the end of year t-1; RAW RETURNi,t = Raw return for year t; SIZE-ADJUSTED RETURNi,t = size-adjusted return for year t;

25

TABLE 2: VALUATION TESTS USING THE EASTON AND HARRIS (1991) APPROACH: REGRESSIONS OF (RAW) RETURNS ON EARNINGS

Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9 Intercept -0.0697

(-1.26)*** -0.0711 (-1.29)***

-0.0415 (-0.77)

-0.0697 (-1.25)

-0.0654 (-1.16)

-0.0690 (-1.24)

-0.0671 (-1.21)

-0.0696 (-11.25)

-0.0675 (-1.23)

GAAP 0.0131 (11.23)***

0.0131 (8.57)***

0.0154 (9.66)***

0.0049 (2.73)***

0.0138 (11.03)***

0.0129 (9.83)***

0.0127 (7.60)***

0.0082 (4.84)***

CORE 0.0127 (10.18)***

SOPTEXP -1.1123 (-10.49)***

SGAINLOSS -0.1039 (-3.70)***

SGWIMPAIR 0.1126 (4.22)***

SSETTLEMT -0.0701 (-0.81)

SREVERSAL -4.7763 (-11.04)***

SPRCOSTS 0.2191 (0.39)

SPENCOSTS 0.1489 (5.76)***

Adjusted R2 3.08% 2.90% 7.75% 3.20% 3.50% 3.05% 3.68% 3.07% 3.24% Vuong Z-statistic relative to GAAP (p-value)

-4.67 (0.00)***

29.04 (0.00)***

3.65 (0.00)**

6.83 (0.00)**

0.39 (0.35)

8.87 (0.00)***

0.41 (0.34)

4.10 (0.00)***

Notes to Table 2:

Variables are as defined in Table 1. T-statistics are in parentheses. *** = α ≤ .01, ** = α ≤ .05, * = α ≤ .10.

26

TABLE 3: VALUATION TESTS USING THE EASTON AND HARRIS (1991) APPROACH: REGRESSIONS OF (SIZE-ADJUSTED) RETURNS ON EARNINGS

Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9 Intercept -0.1637

(-53.89)*** -0.1651 (-54.41)***

-0.1345 (-6.39)***

-0.1633 (-6.56)***

-0.1597 (--6.45)***

-0.1632 (-6.49)***

-0.1610 (-6.49)***

-0.1633 (-6.49)***

-0.1617 (-6.38)***

GAAP 0.0117 (32.31)***

0.0114 (8.17)***

0.0136 (11.34)***

0.0041 (2.16)***

0.0122 (7.64)***

0. 0111 (9.57)***

0.0114 (7.49)***

0.0074 (5.77)***

CORE 0.0114 (31.36)***

SOPTEXP -1.1651 (-11.00)***

SGAINLOSS -0.1100 (-4.03)***

SGWIMPAIR 0.0994 (6.08)***

SSETTLEMT -0.0960 (-1.35)

SREVERSAL -4.6527 (-15.43)***

SPRCOSTS -0.0427 (-0.07)

SPENCOSTS 0.1192 (2.33)***

Adjusted R2 2.59% 2.44% 7.43% 2.68% 2.94% 2.53% 3.20% 2.59% 2.70% Vuong Z-statistic relative to GAAP (p-value)

-2.64 (0.00)***

20.97 (0.00)***

0.45 (0.33)

2.29 (0.01)**

-2.37 (0.01)**

7.12 (0.00)***

0.12 (0.45)

3.54 (0.00)***

Notes to Table 3:

Variables are as defined in Table 1. T-statistics are in parentheses. *** = α ≤ .01, ** = α ≤ .05, * = α ≤ .10.

27

TABLE 4: VALUATION TESTS USING THE EASTON AND HARRIS (1991) APPROACH: REGRESSIONS OF (RAW) RETURNS ON EARNINGS AND CHANGE IN EARNINGS

Model 10 Model 11 Model 12 Model 13 Model 14 Model 15 Model 16 Model 17 Model 18 Intercept --0.0651

(-1.20) -0.0668 (-1.23)

-0.0382 (-0.71)

-0.0648 (-1.19)

-0.0618 (-1.11)

-0.0655 (-1.20)

-0.0614 (-1.13)

-0.0654 (-1.20)

-0.0630 (-1.14)

GAAP 0.0141 (14.25)***

0.0135 (8.80)***

0.0176 (15.62)***

0.0068 (8.80)***

0.0165 (15.34)***

0.0138 (12.32)***

0.0152 (11.46)***

0.0099 (10.04)***

CORE 0.0139 (13.34)***

SOPTEXP -1.0634 (-10.85)***

SGAINLOSS -0.1563 (-5.66)***

SGWIMPAIR 0.0997 (3.02)***

SSETTLEMT -0.2262 (-2.36)***

SREVERSAL -6.6429 (-8.89)***

SPRCOSTS -0.6047 (-0.99)

SPENCOSTS 0.1227 (3.99)***

ΔGAAP -0.0140 (-18.01)***

-0.0104 (-7.51)***

-0.0148 (-24.16)***

-0.0120 (-8.55)***

-0.0146 (-16.99)***

--0.0130 (-10.90)***

-0.0142 (-14.55)***

-0.0120 (-10.17)***

ΔCORE

-0.0126 (-15.47)***

ΔSOPTEXP

0.1198 (3.31)***

ΔSGAINLOSS

0.0534 (1.81)*

ΔSGWIMPAIR

-0.0269 (-1.59)*

ΔSSETTLEMT

0.1006 (2.91)***

Δ SREVERSAL

3.6210 (8.41)***

Δ SPRCOSTS

0.1439 (0.10)

Δ SPENCOSTS

-0.2749 (-2.72)***

Adjusted R2 3.89% 3.66% 8.25% 4.09% 4.16% 3.92% 4.73% 3.89% 4.16% Vuong Z-statistic relative to GAAP (p-value)

-6.40 (0.00)***

26.23 (0.00)***

5.12 (0.00)***

5.31 (0.00)***

1.88 (0.03)**

11.16 (0.00)***

0.87 (0.19)

5.31 (0.00)***

Notes to Table 4: Variables are as defined in Table 1. T-statistics are in parentheses. *** = α ≤ .01, ** = α ≤ .05, * = α ≤ .10.

28

TABLE 5: VALUATION TESTS USING THE EASTON AND HARRIS (1991) APPROACH: REGRESSIONS OF (SIZE-ADJUSTED) RETURNS ON EARNINGS AND CHANGE IN EARNINGS

Model 10 Model 11 Model 12 Model 13 Model 14 Model 15 Model 16 Model 17 Model 18 Intercept -0.1592

(-6.28)*** -0.1606 (-6.30)***

-0.1318 (-6.23)***

-0.1588 (-6.36)***

-0.1564 (-6.31)***

--0.1594 (-6.30)***

-0.1557 (-6.33)***

-0.1594 (-6.30)***

-0.1574 (-6.20)***

GAAP 0.0123 (11.91)***

0.0118 (9.14)***

0.0159 (12.40)***

0.0060 (2.53)***

0.0150 (9.36)***

0.0120 (11.21)***

0.0138 (8.77)***

0.0090 (9.00)***

CORE 0.0120 (10.63)***

SOPTEXP -1.1034 (-10.27)***

SGAINLOSS -0.1603 (-6.65)***

SGWIMPAIR 0.0864 (4.05)***

SSETTLEMT -0.2543 (-3.65)***

SREVERSAL -6.6429 (-8.89)***

SPRCOSTS -0.8347 (-1.65)*

SPENCOSTS 0.0973 (3.00)***

ΔGAAP -0.0129 (-9.04)***

-0.0097 (-7.00)***

-0.0138 (-9.37)***

-0.0112 (-6.29)***

-0.0135 (-8.97)***

-0.0120 (-6.38)***

-0.0132 (-8.52)***

-0.0112 (-6.18)***

ΔCORE

-0.0116 (-7.75)***

ΔSOPTEXP

0.1207 (3.88)***

ΔSGAINLOSS

0.0545 (1.92)*

ΔSGWIMPAIR

-0.0218 (-1.67)*

ΔSSETTLEMT

0.1194 (6.28)***

Δ SREVERSAL

3.5313 (8.38)***

Δ SPRCOSTS

0.1835 (0.13)

Δ SPENCOSTS

-0.2745 (-3.14)***

Adjusted R2 3.89% 3.66% 8.25% 4.09% 4.16% 3.92% 4.73% 3.89% 4.16% Vuong Z-statistic relative to GAAP (p-value)

-6.40 (0.00)***

26.23 (0.00)***

5.12 (0.00)***

5.31 (0.00)***

1.88 (0.03)**

11.16 (0.00)***

0.87 (0.19)

5.31 (0.00)***

Notes to Table 5: Variables are as defined in Table 1. T-statistics are in parentheses. *** = α ≤ .01, ** = α ≤ .05, * = α ≤ .10.

29

TABLE 6: PREDICTIVE ABILITY TESTS: REGRESSIONS OF CASH FLOW ON LAGGED EARNINGS

Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9 Intercept -0.1050

(-2.03)** -0.1059 (-55.39)***

-0.1050 (-2.03)**

-0.1060 (-2.06)***

-0.1049 (-2.05)**

-0.1057 (-2.05)**

-0.1055 (-2.05)**

0.1052 (-2.05)**

-0.1054 (-2.05)**

GAAP 0.0088 (29.70)***

0.0083 (5.67)***

0.0089 (5.51)***

0.0001 (10.36)***

0.0070 (5.23)***

0.0089 (5.44)***

0.0080 (6.07)***

0.0115 (5.19)***

CORE 0.0086 (29.62)***

SOPTEXP -0.0595 (-6.54)***

SGAINLOSS -0.0293 (-7.71)***

SGWIMPAIR 0.1230 (4.45)***

SSETTLEMT 0.1479 (5.42)***

SREVERSAL 0.3483 (6.61)***

SPRCOSTS 0.7573 (2.22)***

SPENCOSTS -0.0841 (5.87)***

Adjusted R2 2.68% 2.67% 2.95% 2.50% 3.15% 2.70% 2.77% 2.91% 2.51% Vuong Z-statistic relative to GAAP (p-value)

-2.63 (0.00)***

3.10 (0.00)***

-1.92 (0.03)**

1.75 (0.04)**

2.16 (0.02)**

2.02 (0.02)**

4.28 (0.00)***

-1.70 (0.04)**

Notes to Table 6:

Variables are as defined in Table 1. T-statistics are in parentheses. *** = α ≤ .01, ** = α ≤ .05, * = α ≤ .10.