harmonized approach to cash transfers framework · harmonized approach to cash transfers framework...

TRANSCRIPT

UNITED NATIONS IN BHUTAN GROSS NATIONAL HAPPINESS COMMISSION

2012

Harmonized Approach to

Cash Transfers

Framework A Reference Manual

T H I M P H U , B H U T A N

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmrtyuiopasdfghjk

lzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasdfghjkl

zxcvbnmqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqwertyui

This reference manual was complied by:

Vathinee Jitjaturunt, Former Deputy Representative, UNICEF

Tashi Dorji, Programme Coordinator, GNHC

Kesang Choden, Operations Manager, UNDP

Pem Chuki Wangdi, Head, Management Support Unit, UNDP

Kinlay Penjor, Programme Officer, UNICEF

Kalpana Humagai, Operations Officer, UNICEF

Sonam Dhendup, Former Finance Associate, UNFPA

Phurpa Tshering, Finance Associate, UNDP

Tshering Wangdi, Finance Associate, UNFPA

Phub Delma, Finance Associate, WFP

Royal Government of Bhutan

Gross National Happiness Commission

FOREWORD

Under the current United Nations Development Assistance Framework (UNDAF 2008-2013)

support to the Royal Government of Bhutan (RGoB), agencies, both Government and Civil

Society, implement its approved activities under the purview of a set of common UN procedures

and rules for requesting cash and reporting on its utilization. Activities and assurance of

utilization of provided cash is also agreed on and coordinated through joint assessments and

assurance activities thereby strengthening national capacities and control systems for

management and accountability.

As agencies receiving UN support use common procedures for requesting cash and reporting on

utilization of fund against approved activities, this HACT manual will provide both

Implementing Partners and UN colleagues, a one place reference for all issues related to HACT

implementation and ensure effective harmonization and coordination of UN support in Bhutan

with the national priorities, needs and systems.

Toward this end, I would like to extend my sincere gratitude to the UN Agencies, both within

and outside Bhutan, who have continuously rendered their continuous support and guidance

in assisting the RGoB in meeting its national priorities and needs as well as in strengthening

our national systems and capacities. I would also like to take the opportunity to commend the

members of HACT Working Group for taking the initiative of putting together a very useful

document such as this.

I, on behalf of the RGoB would like to encourage all agencies receiving UN support to use this

manual as their principal reference for effective programme financial delivery.

Tashi Delek.

Karma Tshiteem

Secretary

i

FOREWORD

It is with great pleasure that we bring to you the Harmonized Approach to Cash Transfers

(HACT) Framework: A Reference Manual. This manual has been developed for our Implementing

Partners and UN colleagues, and is intended to provide guidelines and reference in one place

for all issues related to HACT implementation.

For your information, HACT was introduced in Bhutan in 2008 in parallel with the 2008-2013

United Nations Development Assistance Framework (UNDAF). Bhutan achieved full HACT

compliance in 2010. Full HACT compliance means that the three elements of the Framework

(Assessments; Assurance Activities and the use of FACE forms) are in place and are being used

and referred to by our Implementing Partners.

Bhutan is a “Delivering As One (DAO)” country, and HACT ensures that the implementation of

the DAO approach is focused on strong national ownership and aligned to national systems.

This manual will also be used as the common reference document for all trainings on HACT.

I would like to extend my sincere gratitude to the Gross National Happiness Commission and

our Implementing Partners for their contribution and commitment in ensuring that HACT

implementation is a success in Bhutan. I will also like to take this opportunity to thank the

members of the UN-RGoB HACT Working Group for taking the initiative of compiling this

manual.

We encourage all agencies receiving UN support and UN staff to use this manual as their

principal reference for effective programme financial delivery.

Tashi Delek.

Claire Van der Vaeren

Resident Coordinator

ii

Table of Contents

Message from Secretary, Gross National Happiness Commission…………………………….………..i

Message from UN Resident Coordinator, UN Bhutan……………………………………………….…….ii

Table of Contents…………………………………………………………………………………………….……iii

Abbreviations………………………………………………………………………………………………………iv

Chapter 1 : Rationale Behind the Harmonized Approach to Cash Transfers Framework…….1

Chapter 2 : Elements of HACT………………………………………………………………………..…….3

2.1 Assessments: Macro and Micro-Assessment

2.1.1 Macro-Assessment 2.1.2 Micro-Assessment

2.2 Assurance Activities

2.2.1 On-site Reviews of IPs

2.2.2 HACT Audits

2.2.3 Programmatic Assurance 2.3 Funding Authorization and Certification of Expenditure (FACE) Form

Chapter 3 : Country Programming Process, Common Country Programme Action Plan……20

(CPAP), 18 month Rolling Work Plan (RWP) and Standard Progress Report

(SPR)

3.1 Common Country Programme Action Plan 3.2 18 Month Rolling Work Plan

3.3 Standard Progress Report

Chapter 4 : Cash Transfer Procedures…………………………………………………………………..27

4.1 Harmonized Cash Transfer Procedures 4.2 Cash Transfer Framework on the Programming Process

Annexes

Annex 1: Frequently Asked Questions………………………………………………………………v

Annex 2: HACT Implementation Milestones………………………………………….…………..xx

Annex 3: Delegation of Signing Authority for the Funding Authorization and Certificate

of Expenditure (FACE)Form ……………………………………………………………xxi

Annex 4: Guidance Note on Annual Fixed Asset (Non-Expendable Property………….xxiii

Report) Form

Annex 5: Financial Procedures for UN Assisted Projects……………………………………xxvi

Annex 6: Guidelines: Standard Progress Reports……………………………………………xxxii

iii

HACT)

Abbreviations

CCA : Common Country Assessment

CP : Country Programming cCPAP :common Country Programme Action Plan

CPD : Country Programme Document

CPP : Country Programming Process

DCT : Direct Cash Transfer

DP : Direct Payment

FACE : Funding Authorization and Certificate of Expenditure GNHC: Gross National Happiness Commission

HACT : Harmonized Approach to Cash Transfer

IPs : Implementing Partners

JSM : Joint Strategic Meeting

MOF: Ministry of Finance M&E : Monitoring & Evaluation

MDG : Millennium Development Goal

NGO : Non Governmental Organization

OR : Other Resource

PFM : Public Finance Management

PRSP : Poverty Reduction Strategy Paper/Plan RAA: Royal Audit Authority

RR : Regular Resource

SAI : Supreme Audit Institution

SPR : Standard Progress Report

UNCT : United Nations Country Team UNDAF : United Nations Development Assistance Framework

UNDG : United Nations Development Group

UNICEF : United Nations Children Fund

UNDP : United Nations Development Programme

UNFPA : United Nations Population Fund

WFP : World Food Programme Training Manual Harmonized Approach to Cash Transfer (HACT)

Training Manual Harmonized Approach to Cash Transfer (HACT

iv

Chapter 1 Rationale behind the Harmonized Approach to Cash Transfers

Pursuant to the UN General Assembly Resolution 56/201 on the triennial policy review of

operational activities for development of the United Nations system, UNDP, UNICEF, UNFPA

and WFP (UNDG ExCom Agencies) adopted a common operational framework for transferring

cash to government and non-government Implementing Partners. Its implementation will

significantly reduce transaction costs and lessen the burden that the multiplicity of UN

procedures and rules creates for its partners.

Implementing Partners (IPs) will use common forms and procedures for requesting cash and

reporting on its utilization. Agencies1 will adopt a risk management approach and will select

specific procedures for transferring cash on the basis of the joint assessment of the financial

management capacity of Implementing Partners. They will also agree on and coordinate

activities to maintain assurance over the utilization of the provided cash. Such jointly

conducted assessments and assurance activities will further contribute to the reduction of

costs.

The adoption of the harmonized approach is a further step in implementing the Rome

Declaration on Harmonization and Paris Declaration on Aid Effectiveness, which call for a

closer alignment of development aid with national priorities and needs. The approach allows

efforts to focus more on strengthening national capacities for management and accountability,

with a view to gradually shift to utilizing national systems. It will also help Agencies shape their

capacity development interventions and provide support to new aid modalities.

What is different with HACT?

HACT Procedures Old Procedures

UN agencies assess the environment in

which government and other implementing

partners work (done through assessments

of the public financial management system; or macro-assessments)

The public financial management systems, or

the environment under which cash is

transferred to partners, is not assessed

UN agencies assess the financial

management capacity of individual

partners (micro-assessments)

UN agencies do not formally assess the

partners‟ financial management systems

Based on the findings of the macro- and micro assessments, the UN agencies adjust

their assurance and capacity building

activities

All partners and situation are treated the same

Implementing partners provide a

certificate of expenditure (FACE form)

which is subject to audit

For UNICEF: Implementing partners submit

receipts for their expenditures

For UNDP: the specifically created project account is audited annually

Closer programming monitoring through

more intense field visits and mid year and

UN agencies tend to rely on accounting

information to assure themselves that

1 Throughout this Manual the term “Agencies” will be used to refer to the UNDG ExCom Agencies and any

other UN Agencies that choose to adopt these procedures.

1

annual reviews, HACT audits, on-site

reviews and – if needed special audits are

conducted to receive assurance that

activities and funds were implemented and

used as planned

activities have taken place as planned

The focus is on implementation of agreed

activities and results

The focus is on providing accounting reports

Funds are provided for activities to take

place during the next three months, as

agreed in the RWP

Funds are provided for activities to take place

during the next three months but requests are

often received on an ad-hoc basis

Possibility of re-programming unutilized funds, for other activities agreed in the

RWP

Possibility of reprogramming exists, but must be dealt with on a case-to-case basis

Monitoring reports (FACE form and SPR) to

be received quarterly, summing up all

received and outstanding installments

Piecemeal reporting on use of funds

No receipts required except for FACE form-

implementing partners keep their original

documentation and the integrity of their

accounts

Receipts have to be provided (to UNICEF) or

separate project accounts have to be

maintained (UNDP)- in both cases the

accounting systems of implementing partners

require additional efforts or systems.

2

Chapter 2

Elements of HACT

The Harmonized Approach to Cash Transfers has three main elements which have been

detailed in the following sections:

2.1 Assessments: Macro and Micro-Assessment

Introduction

With the shift from the control management system to a risk management system under

harmonized procedures, the UN agencies are required to assess the Implementing Partner‟s risks associated with the transactions before initiating cash transfers to be aware of the IP‟s

Public Financial Management (PFM) environment. Two types of assessments, Macro and Micro,

are required to be conducted and have the following objectives:

1. Developmental Objective:

Ensure awareness of National/IP PFM system including the strengths and weaknesses.

Identify areas for capacity development.

2. Financial Management Objectives:

Provide background information to identify the most appropriate cash transfer modality and assurance methods.

Indicate if the Supreme Audit Authority can be used to audit the IPs.

The assessments do not impose conditionality for any assistance from the UN agencies to the

IPs.

2.1.1 Macro Assessment:

The Macro Assessment is a desk review of existing assessments of the National PFM system

under which the UN provides cash transfers before the introduction of the harmonized

procedures. The assessment is undertaken once per programme cycle (preferably during the

Common Country Assessment preparation).

The review covers areas of the national budget development and execution process, the

functioning of the public sector accounting and internal control mechanisms, audit and

oversight, financial recording systems and staff qualifications.

The macro-assessment report should include the following:

• Summary of finding in key areas

• Summary of risks

• Assessment of the national Supreme Audit Institution

• Capacity gaps and opportunities for capacity development

• Completed checklist.

The Macro Assessment for Bhutan for the current programme cycle )2008-2012 (extended to

3

2013) was completed in 2006 and the report has been annexed to the United Nations

Development Assistance Framework (UNDAF). The Macro Assessment for Bhutan is based on

the following relevant studies/document of the World Bank (WB):

1. Country Financial Accountability and Assessment (CFAA) in 2002.

2. Note on Public Financial Accountability and Management (PFAM) in 2005. 3. Roadmap towards Universal Reliance in Bhutan‟s Country Systems; Public Financial

Management in 2006.

The assessment indicates the existence of a reliable and transparent public financial

management system and Royal Audit Authority‟s (RAA) independence with some risk areas:

insufficient staff qualifications and financial management skills, limited internal control system

and delay in transferring fund to project level. The table below combines the checklist results,

WB‟s recommendations from PFAM (2005) and the Road Map.

Sl. Indicator Risk Recommendation Remarks*

1 Budget Information Low

2 Budget Performance Moderate Introduce multiyear rolling budget

with links to the Medium Term Fiscal Framework- Ongoing

World Bank/

IDF Grant

3 Internal Control Significant Establish organizational structure

and independence including clear

mandate for internal audit units and;

staff to be trained in the use of

professional audit methods.

Update FRR 2001 as part of GG+ recommendations.

World Bank

4 Bank Reconciliation Moderate Upgrade BAS to monitor suspense

and advance accounts and provide

ageing information on suspense

balance.

NA

5 Transfer of cash

resources

High Development of e-transfer system –

ongoing

NA

6 Cash and asset position

Moderate Improve cash planning and forecasting. Provide information on

liabilities and probable contingencies.

DANIDA (feasibility

study)

7 Coverage of external

audit

Low Introduce selective audits using

sampling techniques; train audit and

accounts personnel

World

Bank/IDF

Grant

8 Follow up action to

audit reports

Moderate Mechanism needed in MOF to actively

track and monitor response to audit observations.

NA

9 Transparency of

Audit Process

Moderate World Bank/

IDF Grant

10 Staff qualification

and skills

Significant Greater professional leadership; Equal

opportunities for regular in-service

training: training for senior managers.

Expansion in opportunities and

enrolment at the RIM for finance staff.

NA

11 Financial Systems Moderate Enhance database networking

User training

DANIDA

4

2.1.2 Micro Assessment

The Micro Assessment is to assess the risks related to cash transfers to the IPs and is

conducted once every programme cycle or whenever a significant change is noticed in the IP's

organizational management.

The Micro Assessments are conducted for IPs who receive or are expected to receive cash

transfers above an annual amount of US$ 100,000 combined from all UNDG agencies as

initially defined in the cCPAP/RWP or as agreed locally among the UN agencies.

The assessments provide an overall risk rating on the financial management of IP related to

accounting, reporting, auditing and internal control. The overall risk of an IP is rated “low” if their system is considered capable of correctly recording the transactions and balances,

support the preparation of regular and reliable financial statements, safeguard the asset and is

subject to acceptable auditing arrangements. It should be conducted in a transparent manner

with participation from the IPs.

The UN agencies use two checklists for the micro-assessment. Checklist A is used when

adequate information exists and confirms that overall risk related to cash transfers to the IP is

low. Checklist B is used when a second-stage, more detailed assessment of IP is required if the

information is inadequate or overall risk is high (Checklist B).

Each Micro Assessment concludes with a statement of the overall risk related to cash transfers,

rated as either “low,” “moderate,” “significant” or “high” as below:

Risk level Description

High System & control framework is weak and inadequate to assure that

most cash transfers are used and reported as agreed with the ExCom

Agencies

Significant System & control framework is weak and inadequate to assure that

some cash transfers are used and reported as agreed with the ExCom

Agencies

Moderate Some weakness in the financial system & functioning control framework

Low A well developed financial system and functioning control framework

l Harmonized Approach to Cash Transfer (HACT)

In exceptional situations, when a Micro Assessment of an IP cannot be conducted, the Agencies

will apply modalities and procedures applicable to a high-risk partner.

The Royal Audit Authority (Bhutan‟s SAI) conducts the Micro Assessment for the UN agencies.

5

2.2 Assurance Activities

Introduction

Assurance activities promote accountability and strengthen the financial management system

and internal control mechanism of the IPs. It will ensure whether funds transferred to the IPs

were used for the appropriate purpose; ensure achievement of project targets and expected

results.

The HACT framework requires the UN agencies to conduct assurance activities based on the

risk level/ratings determined by micro-assessments reports. The specific combination,

frequency and scale of assurance activities for each IP will be determined by risk ratings of the

micro-assessment report of the IPs. For each Implementing Partner, the results of the

assurance activities may lead to changes in the procedures and modalities for disbursing cash

transfers, and the type and frequency of future assurance activities.

There are three mechanisms through which assurance activities will be carried out:

On-site reviews

HACT audits and Special audits (if needed)

Programmatic assurance

2.2.1 On-site reviews of IPs:

The Terms of Reference for On-Site Reviews for the Cash Transfers to the Implementing

Partners was developed jointly with the representatives of the Ministry of Finance (MoF), Royal

Audit Authority (RAA) and GNHC. It determines the scope and the task of the on-site review.

The schedule of the on-site reviews, as well as other assurance activities are reflected in the

RWP once agreement has been reached between the IP and the UN agency on the timeline of

the review.

The scope of on-site site review will be adjusted to the specific needs of each assignment. On-

site review of IPs with internal controls assessed as weak, or made in response to a particular

concern may be more detailed, than those of IPs whose management capacity has been rated

as high.

On-site review may take up from 1 day to 3 days. However, the duration may vary according to the level of expenditures. The review will take place at the IPs location. The on-site review will

be conducted by the UN Interagency On-site Review Team or an external consultant (if needed)

following standard guidelines.

The frequency of the on-site review is based on the risk ratings as shown in the table below:

6

Overall Risk Assessment Frequency of on-site review

High Risk Quarterly

Significant Risk Three times in a year

Moderate Risk Twice a year

Low Risk Once a year

The on-site review team will focus on:

1. Financial transaction

Review a sample transaction of the expenditure reported in the FACE Form to ensure the following:

o Accuracy of the total expenditure with the government records

o Whether expenditure reported in the FACE Form is in line with approved

budget as per RWP

o Liquidation of advance

o Whether fund released by UN agencies is received by IPs within agreed time

frame

2. Procurement

Review the procurement system followed by the IPs

Support the IP in submitting the year-end inventory report through review of inventory management and physical verification.

3. Internal control mechanism

Review segregation of duties/ functions

Internal check and balance

Strengthen the internal control mechanism with consultation with the relevant IP, GNH and other relevant govt. partners

Responsibilities of IPs for the on-site review include:

Facilitation of on-site review by ensuring access to documents, and records;

Provision of clarification as and when requested by the review team during the on-site review

UN Interagency On-site Review Team:

The review team will consist of staff from Programme sections/unit and Operations

section/unit from the relevant UN agencies, and when possible staff from GNHC and Internal

Auditor from the concerned IP. The review team is responsible for informing the exact date and

the members of the on-site review to the IPs and conduct on-site review as per the on-site

review calendar.

Upon the completion of the on-site review, prepare a report containing: 7

o A summary of the findings, with the indication of risks

o A list of transactions tested. For any exceptions the report should list, by

Agency, the payment details, findings and the nature of the exception. o Conduct a meeting with the IP Programme Manager

o Provide recommendations to the IP and get the final comments from the IP.

On-site review reports will be reviewed quarterly by the Interagency HACT Working Group.

The report will be shared with the Head of the Implementing Partner, GNHC and with copies to

the Heads of UN Agencies.

Co-ordination for the On-Site Reviews:

o In case of IPs jointly supported by different UN agencies, the concerned programme

section/unit of the lead UN agency will co-ordinate with concerned IPs and inform

relevant programme colleagues in the other UN agencies, GNHC, and its agency‟s Operations section/unit on the time.

o In case of the specific agency supported IPs, the concerned Programme section/unit of

the UN agency will co-ordinate with concerned IPs and inform GNHC and its agency‟s

Operations section/unit for the exact dates of the on-site review.

2.2.2 HACT Audits

IPs who receive (or are planned to receive) more than $500,000 in cash transfers collectively

from the UN Agencies during the period covered by the cCPAP will be audited once or more

during the programme period. Implementing Partners who receive (or are planned to receive)

less than $500,000 over the programme period may be audited if one or more Agency requires

it.

The Royal Audit Authority (SAI) will conduct the HACT audit of the IPs. Towards this end, the

ToR for HACT audit was developed in consultation with the RAA in compliance with Technical

Note on HACT audit available in the HACT Framework.

Purpose of HACT Audit:

The HACT audit will assess the existence and functioning of an Implementing Partners‟ internal

controls for the receipt, recording and disbursement of cash transfers and the fairness of a sample of expenditures reported in the FACE forms for the period under review.

It will strive to obtain reasonable assurance that:

All cash transfers to the IP and reported expenditures were based on 18 month Rolling Work Plan agreed between the respective IP and the UN agency(ies) within the specified period being audited.

Disbursements are made in accordance with applicable procedures

There is adequate supporting documentation/evidence for the expenses

Balance of OFA as per the IP‟s records agrees with UN agency(ies)‟ records and there is an accurate reconciliation between these two balances

Any major findings of the macro- and micro-assessments, and previous audits, or any observations from on-going programme and financial monitoring have been adequately

8

addressed.

Approach to HACT Audit:

The Interagency HACT Working Group will share the list of IPs to be audited in the next

calendar year with the RAA at the end of the current year. The aim is to align the HACT audit

period with that of the RAA‟s annual audit plan and with the government‟s fiscal year period.

The list will provide the names of the implementing partners including the physical address,

telephone numbers, fax numbers, and relevant e-mail addresses of relevant officials

responsible for the management of the programmes and projects. It also provides the amount

of funds transferred/received till date by the IP

Prior to and during the audit, the audit team will conduct consultations including:

Hold an inception meeting between the auditors, IP and the UN agencies to clarify the objectives and scope of the audit (coordinated by Interagency HACT Group) and brief on

the programme activities of the IPs that will be audited.

Agree on the timeline for submission of the final audit report.

Meet with senior officials of the IP, to understand how cooperation with the UNDG Group Agencies is managed, and any issues of concerns they may have

Upon completion of the draft report, the auditor should first hold a debriefing meeting with the IP, to discuss findings and recommendations for future improvements, as well

as to seek their feedback thereon.

The auditor will then meet with the UN agencies to discuss the draft report prior to its finalization.

The HACT audit will cover the following areas:

Review of the IP‟s programme management system o Review whether activities were implemented as planned and whether activities

deviated significantly from the original work plan(s), establish whether this was by

mutual agreement between the IP and the agency(ies).

o Review the IP‟s system of monitoring progress and review of reports

o Review whether recommendations recorded in the field/project monitoring reports

have been implemented by the IP

Assess the IP‟s internal control system o Review whether internal control system exist to ensure check and balance and in

safe guarding the project resources and assets.

o Review whether segregation of duties exists in the IPs.

o Processes used by the IP for authorizing expenditures and assess whether they are

in accordance with the work plan and authorized by designated authority.

Review of processes followed by IP

o Review FACE forms, including records for requests for direct payments, and

reimbursements to assess whether they were signed by designated officials of the IP

o Assess procurement/contracting of supplies and services to ensure transparency and competitiveness

o Assess use, control and disposal of non-expendable equipment to ensure whether

the equipment procured met the identified needs and used in accordance with its 9

intended purpose

o Assess adequacy for maintaining accurate and complete records of receipt of funds

provided by the UNDG Agency o Review of the FACE forms and perform Transaction Testing

o Assess whether the release from UN agencies received by DPA and review further

release to the IPs and assess the fund balance with DPA and fund balance with the

IP

o Reconcile the expenditure totals, per activity, on the FACE form to the list of

individual transactions (i.e the IP‟s accounting records)

The final audit report should include:

An opinion on the functioning of internal controls

An executive summary with the key findings/observations, risks and recommendations

A summary of the main identified risks to the management of agreed activities and the use of funds provided by the Agencies, arising from weak internal controls

Any identified specific internal control weaknesses in the financial management of the IP

Observations/management response: o Recommendations on how the identified risks may be better managed, how the IP‟s

internal controls can be strengthened. Recommendations should clearly identify those responsible for their implementation within the IP. Comments of the IP

should be included in the report, under the recommendation

o Comments on the follow-up to the recommendations from the previous audits or

assessments and the management response to those

o A list of transactions tested. For any exceptions identified, the report should list the

transaction details and the nature of the exception o If applicable, any „good practices‟ that were developed by the IP and could be shared

with other IPs

o An overall risk rating of the IP‟s internal controls and process to update the micro-

assessment data

The IPs will:

Receive and review the audit report issued by the auditors.

Provide a timely statement of the acceptance or rejection of any audit recommendation concerning the audited projects.

Undertake timely actions to address the accepted audit recommendations.

Report on the actions taken to implement accepted recommendations to both RAA and UN agencies.

The UN Agencies will:

Regularly monitor the implementation of the audit recommendations

The RAA will:

Accept or further recommend actions of the implementation of the recommendations.

Special Audits:. Special Audits will be undertaken when significant weakness is confirmed in

the Implementing Partner‟s internal controls over cash transfers as a result of the on-site

10

review or audit findings. The principle difference between the HACT and Special audit is that

the latter is commissioned to address specific suspected weaknesses and can be implemented

on short notice while the HACT audits are based on annual plan of routine audits.

2.2.4 Programmatic Assurance

Programmatic assurance is maintained following standards and guidance established by each

Agency and includes receipt of implementation reports such as the standard progress reports

(SPR) from Implementing Partners, site visits by UN Agency staff, joint mid-term reviews, joint

annual reviews, and evaluations.

2.3 Funding Authorization and Certificate of Expenditure (FACE) Form

Introduction

The harmonized Funding Authorization and Certificate of Expenditures (FACE) form

simplifies the paperwork to authorize expenditure or transfer cash to Implementing Partners.

The FACE supports several important functions:

Request for funding authorization: The section “Requests / Authorizations” will be used by the Implementing Partner to enter the amount of funds to be disbursed for use in the

new reporting period. Against this request, the Agency can accept, reject or modify the

amount approved.

Reporting of expenditures: The section “Reporting” will be used by the Implementing Partner to report to the Agency the expenditures incurred in the reporting period. The

Agency can accept, reject or request an amendment to the reported expenditures.

Certification of expenditures: The section “Certification” will be used by the designated official from the Implementing Partner to certify the accuracy of the data and information provided.

In the process of certification, the designated official attests to one or both of the following

statements:

That the funding request shown represents estimated planned expenditures as per the common Country Programme Action Plan (cCPAP)/RWP and itemized cost estimates have

been attached and/or;

That the actual expenditures for the reported period have been disbursed in accordance with the cCPAP/RWP and previously approved itemized cost estimates. Further, the designated official attests that the supporting accounting documentation will be made

available, upon request, for a period of five years.

When processing a payment to an Implementing Partner, a copy of the approved FACE should

be returned to the Implementing Partner along with the notice of disbursement, cheque, etc. A

detailed discussion of each segment of FACE follows below.

Overall Approach and Guiding Principles

The FACE is intended to replace all other documentation used by partners for requesting

11

funds and reporting expenditure. Not all sections of the form will be used at all times. For

instance, for an initial disbursement, only the request section of the form will be completed.

For a final payment upon RWP completion, only the reporting section will be used.

The FACE will be used for direct cash transfers, reimbursements to Implementing Partners and direct payments.

No FACE will be processed without the appropriate signature from the designated official.

The FACE is aligned with the RWP. The activities for which funds authorisation is requested, or for which expenditure is reported, will be the activities specified in the RWP.

The FACE is normally certified by the designated official who signs the RWP. In all other circumstances, the RWP will specify any other official authorized to certify the FACE. For

instance, the designated official signing the RWP may be from the central Ministry of Health

while the actual expenditures may be incurred by a regional health office. In such cases,

the RWP should specify whether the central authority will process and sign a consolidated FACE or whether individual FACE forms will be processed by other authorized officials from

the sub-ordinate offices and Implementing Partners. The respective reporting relationship

must be specified in the RWP.

A request for funding included in FACE must be accompanied with an itemized cost estimate of the activities to be funded as per individual Agency guidelines. The nature and

detail of this list can be negotiated at the country level.

The normal disbursement cycle for the FACE will be quarterly.

Components of FACE Form.

2.3.1 Header Area The header area of the FACE allows the Implementing Partner to report on the reason and

12

purpose of the funding/ reporting request. This data is usually needed for correct coding in

financial and management accounting systems.

The specific data elements include:

Name of the Agency

Date of the request

Type of request (direct cash transfer, direct payment, reimbursement)

Country where the programme takes place

Programme title and code (as appropriate)

AWP title and code

Responsible officer(s)

Implementing Partner

Currency of the request/disbursement

2.3.2 Body of the Form

Activity Description: This is a text field containing a short description of the activity as it

appears in the underlying RWP, as well as its duration. This data is normally needed for the

Agency‟s programme or project management systems.

Coding Column: The second column will allow the Agency to enter its own account codes. This

data is required for the Agency‟s financial accounting system. The Agency may enter this data

itself or it may require the Implementing Partner to fill it in. If the latter, the training of the

counterpart staff will be required.

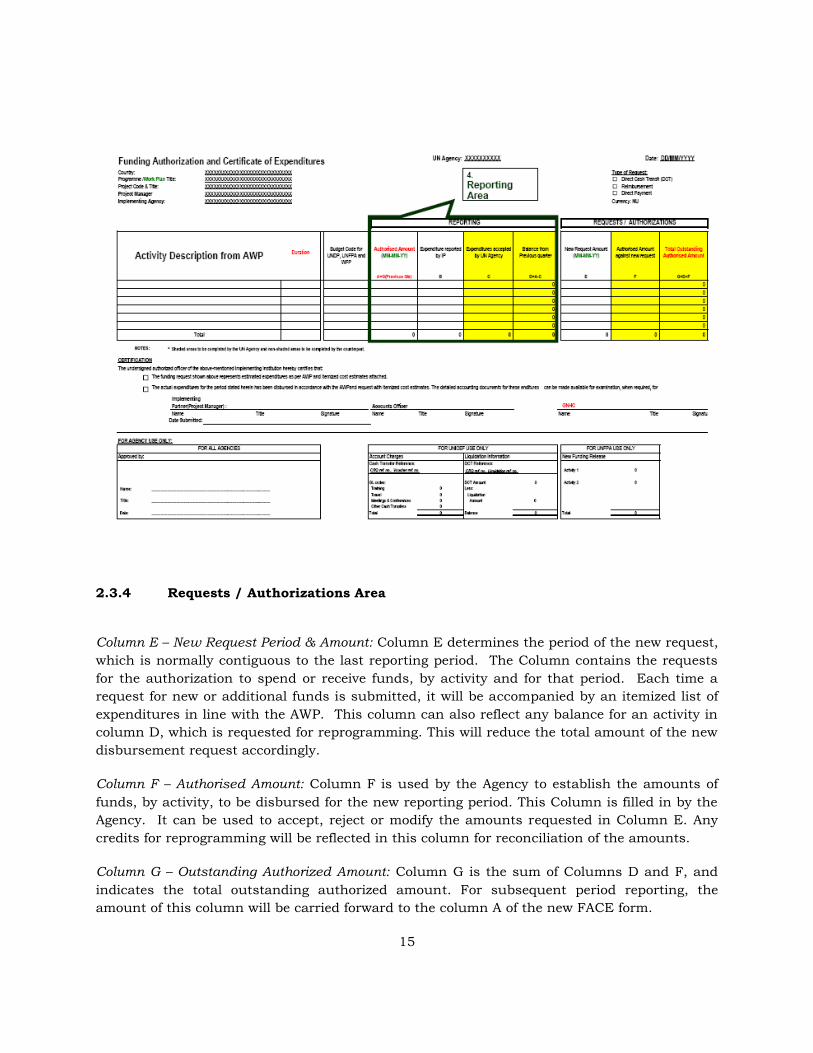

2.3.3 Reporting Area

The FACE is a dynamic form that must balance and reconcile from one reporting period to the

next. The first column on the new form, Column A, therefore repeats the last one, Column G,

from the previously submitted and authorized FACE form. Note that Column C, D, F and G are

shaded. They are blank when the FACE is submitted to the Agency. They are filled out by the

Agency prior to the financial processing of the form. All non-shaded Columns are to be

completed by the Implementing Partner.

Column A – Authorized Amount: Column A will be blank for the first request from an

Implementing Partner. It should include the date of the most recent previous authorization.

Column B – Actual Expenditure: Column B reports the actual expenditures by the Implementing

Partner for the period. The expenditures reported by the Implementing Partner are, at this

point, still subject to review and approval by the Agency. The designated official of the

Implementing Partner is certifying that these expenditures are reported in accordance with the

stipulation of the AWP, CPAP and/or other related agreements with the Agency.

Column C – Expenditures Accepted by Agency: Column C is used by the Agency to review and

approve, reject or request an amendment to expenditures reported by the Implementing

Partner. If the amounts are accepted as reported, no further adjustments to this part of the

FACE or communication with the Implementing Partner about these expenditure is required.

However, if changes are made (e.g., to query or reject a reported expenditure), then the amount

recorded by the Agency in Column C will differ from that reported in Column B. In this case,

the change needs to be communicated with the Implementing Partner.

Column D – Balance: Column D records the balance of funds authorized for use in the reporting

period that remained unspent as of the date of the form. The term unspent can also reflect

expenditures which are either known or ongoing as of the date of the FACE, but which cannot

be certified by the Implementing Partner due to timing or internal reporting delays. The

outstanding balance of funds authorized by activity can be carried forward, reprogrammed or

refunded, depending on the internal policies of each Agency.

14

2.3.4 Requests / Authorizations Area

Column E – New Request Period & Amount: Column E determines the period of the new request,

which is normally contiguous to the last reporting period. The Column contains the requests

for the authorization to spend or receive funds, by activity and for that period. Each time a

request for new or additional funds is submitted, it will be accompanied by an itemized list of

expenditures in line with the AWP. This column can also reflect any balance for an activity in

column D, which is requested for reprogramming. This will reduce the total amount of the new

disbursement request accordingly.

Column F – Authorised Amount: Column F is used by the Agency to establish the amounts of

funds, by activity, to be disbursed for the new reporting period. This Column is filled in by the

Agency. It can be used to accept, reject or modify the amounts requested in Column E. Any

credits for reprogramming will be reflected in this column for reconciliation of the amounts.

Column G – Outstanding Authorized Amount: Column G is the sum of Columns D and F, and

indicates the total outstanding authorized amount. For subsequent period reporting, the

amount of this column will be carried forward to the column A of the new FACE form.

15

2.3.5 Certification Area

The Certification Area is used by the designated official of the Implementing Partner to request

funds and/or to certify expenditures. This area requires a date, the signature of the official

and his/her title.

16

NOTE: IPs are required to submit a delegation of signing authority for the FACE to the

UN agencies and the GNHC. Only the persons identified as the signing authority can sign

on behalf of the IP on the FACE form. Refer Annex 3: Delegation of Signing Authority for

Funding Authorization and Certification of Expenditure (FACE). This form must be

submitted to the UN Agencies and GNHC following the signing of the RWP.

2.3.6 For Agency Use Only Area

Approvals Box: The “For All Agencies” box in the lower left hand corner of the FACE form

should be signed by the appropriate Agency official. This indicates the review and approval of

the request for funds and authorizes the recording of the reported expenditures. The official

should sign, date and provide his/her title.

Accounting Coding Boxes: The remainder of the form is used by Agencies to complete the coding

as required by their financial and management accounting systems. Usage is by individual

Agency.

17

2.3.7 Supporting Documentation to the FACE form

AAggeenncciieess RReeppoorrttiinngg aanndd RReeqquueessttiinngg SSttaannddaarrdd PPrrooggrreessss RReeppoorrtt

((SSPPRR)) AAnnnnuuaall FFiixxeedd AAsssseett

FFoorrmm** FFAACCEE FFoorrmm IItteemmiizzeedd

ccoosstt//SShheeeett

UNICEF

UNDP

UNFPA

WFP Detail

estimates of

activities discussed

with IPs

before FACE

submission.

* Refer Annex 5: Guidance Note on Annual Fixed Asset (Non-Expendable Property Report)

Form

2.3.8 FACE Work flow

Approval PhaseConsultation Phase

IPPrepare

/Revise FACE

Enter UN agency data

Review FACE

UN Agency

Sign FACE

GNHC signature

Yes

No

The FACE work flow has been categorized into two phases: Consultative and Approval.

18

During the Consultative phase, the FACE form is prepared by the IP in consultation with the

concerned UN agency. The UN agency will review the FACE form for the verification of

account/fund codes, accuracy of funds reported and return to the IP for their submission to

GNHC for approval. Both the IP‟s project manager and Finance Officer must sign on the

relevant section of the form before its submission to GNHC.

During the Approval phase, the GNHC reviews the FACE for the appropriate signatures before

endorsing the FACE form and forwarding it to the concerned UN agency for fund

release/reporting.

NOTE TO UN AGENCIES: Once the FACE form has been formally endorsed by the UN agency,

copies of the IP, GNHC and UN agency endorsed form must be shared with the IP and GNHC.

NOTE TO IPs: The fully signed FACE form is required to be made available to the auditors

during the scheduled audit or to the UN Interagency On-site review team during the on-site

review.

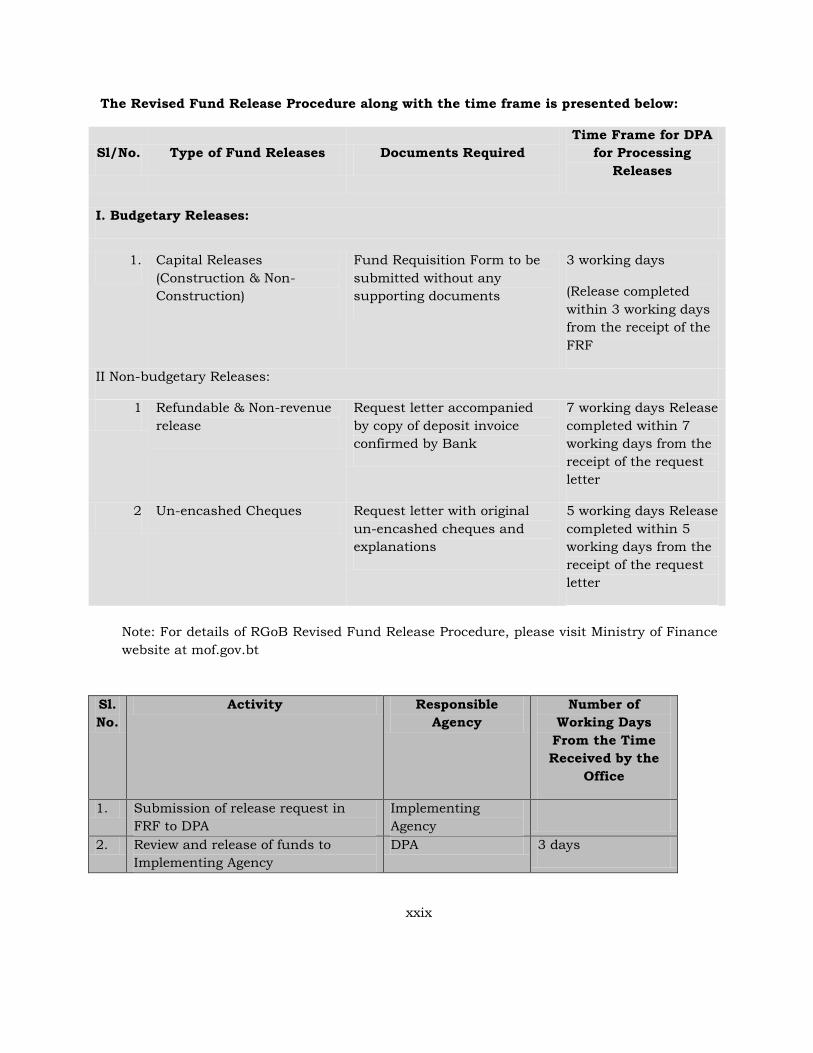

Please also refer to Annex 5: Financial Procedures for UN Assisted Projects. The Procedures

provide guidelines for the request and release of funds.

19

Chapter 3 Country Programming Process: Common Country Programme Action Plan

(cCPAP) and the 18 Month Rolling Work Plan (RWP); Standard Progress Report (SPR)

Training Manual Harmonized Approach to Cash Transfer (HACT)

Introduction

The common country programming process begins with an agreement to adopt a harmonized

programme cycle. The Common Country Assessment (CCA) is the instrument that allows the agencies to identify key development challenges based on existing national analysis. The CCA

is the UN‟s collective analysis and programming in support of national goals and priorities,

including the MDGs. The CCA and UNDAF demonstrate the linkages with national

development plans and strategies. The macro-assessment (as required by the HACT Framework

is conducted at this stage.

Step 1: Agreement on key development challenges

Once CCA has completed and the gaps or opportunities to support national development plans

have been identified, the UN and its partners use that information to design interventions to

address those gaps or opportunities and focus on national capacity building as per the Paris

Declaration and the current aid environment. These responses will be described in the UNDAF

and detailed in the UNDAF Results Matrix.

Step 2: Agreement on common expected results and division of labour

A Joint Strategy Meeting is conducted next to ensure agreement with government. The meeting

allows both the UN and the government to review and validate the Results Matrix, including

identification of opportunities for joint and collaborative programming, monitoring and

evaluation and for wider partnerships, and establishment of thematic groups; and for each

agency to agree on the key outcomes and outputs of its programme of cooperation and its

implementation strategy with government, implementing Ministries and key non-governmental partners.

20

Step 3: Agreement with the government on main programme strategies

Agencies revise/complete and validate CP outcomes and indicative outputs at this JSM in

order to submit their draft Country Programme Documents (CPD) to their Executive Board

Secretariats, with a signed UNDAF to secure resources for the proposal country programme. At this point in the HACT process, micro-assessments, and an inventory of Implementing Partners

are conducted. The micro-assessments involve the identification of the partners to be assessed,

and looks at the soundness of the Implementing Partner‟s financial management system.

Step 4: Secure resources for the proposed country programme

Once the programming planning process is completed, the programme implementation process

begins. Subsequent to the submission, discussion and approval of the country programme, the

common Country Programme Action Plan (cCPAP) is signed between the UN and the

Government. The cCPAP is the UN‟s management plan for its country programme, and it spells

out commitments between the agencies and the government. Specific clauses on cash transfer

modalities, assessments, assurance and use of FACE are incorporated in the cCPAP.

Step 5: Prepare and signed the agreement on the new country programme with the government

The 18 month rolling plans are then developed with the implementing partners to support the

implementation of the country programme.

Step 6: Support the implementation through 18 month rolling work plan with the implementing partners

The Annual Review meetings are organized at the end of the calendar year and takes into

account of findings of the on-site reviews, HACT audits and programmatic monitoring of

activities and results, to plan and sign the next year‟s RWPs. While the financial reporting is

facilitated by the FACE form, the programme results are reported through the common

standard progress reports.

Step 7: Review, adjust and plan for next year

UNDAF Midterm review: The UNDAF mid term review is organized in the middle of the UNDAF

cycle (2010) to review progress against the UNDAF/cCPAP outcomes and to accommodate

emerging priorities. The mid term review includes an assessment of progress made across the

five UNDAF Outcomes based on outcome evaluations, self assessments by the UNDAF theme

groups, and the Country Programme Board progress reports. It is conducted in collaboration

with the GNH Commission. The Mid term Report is endorsed by the Country Programme

Board. The recommendations inform the formulation of the future year rolling work plans as

well as the next UNDAF preparation.

22

The diagram below illustrates the linkages between the common country programme cycle and

its annual implementation cycle:

3.1 Common Country Programme Action Plan

cCPAP is the common Country Programme Action Plan. It specifies the development challenges,

and expected results, budget, implementation strategies, management responsibilities, and

commitments of the government, the 4 UNDG agencies and the participating agencies, and is a

legally binding document for the 4 UNDG agencies.

In Bhutan, the current cCPAP covers the period 2008-2012 (extended to 2013) and

encompasses the planned results of 14 UN agencies (resident and non-resident). It is signed

between the Royal Government of Bhutan and the UN agencies.

The cCPAP is the key reference document for the development of the 18 month rolling work plans. The 18 month rolling work plan forms the basis for filling in the FACE form.

Relevant clauses of the HACT on cash transfer, assurance activities and assessments are

included in the cCPAP.

23

Bhutan‟s cCPAP 2008-2012 (extended to 2013) is available on www.unct.org

Training Manual Harmonized Approach to Cash Transfer (HACT) 3.2 18 Month Rolling Work Plan (RWP)

The 18 month rolling work plans are prepared every year on the basis of intended results,

strategies, budgets and implementing partners identified in the cCPAP, reflecting on

achievements and lessons learned of the previous year. They set out interventions organized around outcomes, outputs, and/or implementing partners. It covers a period of 18 months starting from January through December to June of the following year. The 18 months RWP was adopted to align the UN’s calendar year system of January to December with the government’s fiscal year system of July to June. The mismatch of 6 months of planning period resulted in not reflecting the UN‟s activities for Jan-

June within the RGoB‟s budget. This in turn resulted with substantial amount of supplementary budget incorporations. The 18 months RWP within the ‘Delivering as One’

approach was devised and adopted which helped in furthering the Aid effectiveness agenda of aligning with the Government‟s system. The approach would also facilitate in continuation of activities in the event of late formulation and signing of next work plan.

The RWP details both the activities to be carried out by Implementing Partners and the

associated budgets. The RWP is the basis for disbursement and efforts that should be undertaken to determine reasonable costing of the planned activities. The RWP should indicate

among other elements, the resource transfer modalities to be applied.

The RWP contains the following:

Expected outputs with indicators, baseline and target 24

Activities to be carried out towards the achievement of the expected outputs

Timeframe for undertaking the planned activities

Indication of the parties responsible for carrying out the activities

Timeframe for the assurance activities, including on-site reviews, HACT audits and programme monitoring

The completion of the activities should over time lead to the achievement of the cCPAP outputs,

which in turn contribute to its outcomes.

The RWP is jointly prepared by the relevant UN agencies and the Implementing Partner usually

at the start of the calendar year following the joint annual review meetings, or at the beginning

of a new project. Once a RWP is agreed between the UN agencies and the IP, it is finalized and

signed by the GNHC, UN agencies and the IP. The RWP should be linked for the UNDAF/cCPAP

M&E Framework, and are the building blocks for the quarterly and annual standard progress

reports.

25

3.3 Standard Progress Report

The Standard Progress Report (SPR) is the progress report generated from the RGoB‟s PlaMS

system within the National Monitoring and Evaluation system. The SPR is designed to facilitate

evidence-based decision making. It describes the progress made towards achieving the

activities, and outputs of the RWP and outlines the contributions made towards the UNDAF

Outcomes of the UNDAF/cCPAP. The SPR also summarizes the key achievements, challenges

faced and proposed recommendations. This report is prepared by the implementing partner

and is submitted every quarter along with the FACE form, and an annual SPR is submitted at

the end of year and is presented by the implementing partner at the annual review meeting.

The completed SPR and the FACE form constitute the basis for reporting on results, financial

liquidation and new request for funds. Refer Annex 6: Guidelines: Standard Progress

Report.

26

Chapter 4

Cash Transfer Procedures

Introduction

Three cash transfer modalities are available to the UN Agencies, within the HACT framework

and as described in the common Country Programme Actions Plan (CPAP):

Direct cash transfers to Implementing Partners, for expenditures to be made by them in

support of activities agreed in the RWP;

Direct payments to vendors and other third parties, for expenditures incurred by the

Implementing Partner in support of activities agreed in RWPs.

Reimbursement to Implementing Partners for obligations made and expenditure incurred

by them in support of activities agreed in RWPs;

Under these modalities, IPs are required to comply with their own financial and procurement rules and regulations for the implementation of activities. All supporting documents will be

maintained with the IP, and will be subject to assurance activities.

Agencies agree on a preferred common modality for each Implementing Partner based on the

micro-assessment of the IP, but each Agency may choose the most appropriate modality for

specific and timebound programmes/activities following endorsement from the GNHC..

Table 1: Responsibilities for Obligations and Payments for Cash Transfer Modalities

Modality Obligation Payment

Direct Cash Transfer Implementing Partner Implementing Partner

Direct Payment Implementing Partner UN Agency

Reimbursement Implementing Partner Implementing Partner

4.1 Harmonized Cash Transfer Procedures

The procedures for transferring cash, including the periodicity of disbursements, reporting on

cash utilization, and maintaining assurance over the accuracy of the reports, are essentially the

same for the modalities. Whenever an Implementing Partner receives cash transfers from more

than one Agency, the Agencies will use the same procedures. All Implementing Partners will

use the same standard format (FACE form) for requesting cash transfers and reporting on their

use. Agencies will continue to account for cash transfers in accordance with their established

polices and procedures.

The basic elements of the cash transfer procedures are:

Basis for disbursements:

The basis for the cash transfer modality, are the activities to be carried out by an Implementing Partner, as described in RWPs;

Implementing Partners will submit a request to the Agency for release of funds or for agreement that the Agency will reimburse or directly pay for a planned expenditure.

This request is part of the FACE form.

Periodicity of disbursements:

Direct cash transfers are expected to be requested and released for programme implementation periods not exceeding three months.

Reimbursements for previously authorized expenditures are expected to be requested and released quarterly or after completion of activities.

Direct payments for previously authorized activities shall be made based on a request signed by a designated official of an implementing partner.

Reporting on cash utilization:

Implementing Partners who receive cash will use the FACE form to report on the utilization of cash received, or to request reimbursement for expenditure already

incurred. A designated official of the Implementing Partner will authorize direct

payments to vendors.

The same FACE form is also used for requesting new transfers, or requesting authorization to incur future expenditure (for reimbursement or direct payment to

vendors).

Cash disbursed but not utilized by the Implementing Partner may be re-programmed by mutual agreement if it is consistent with the purpose and timeframe of the funding

source; or may be refunded.

Cash not utilized for more than six months have to be refunded following the prescribed procedures for refunds to the UN.

Direct Agency Implementation: An additional implementation modality, Direct agency implementation is available under the HACT Framework. Under this modality, the UN Agency

on the request of the IP (following endorsement of the GNHC) implements the activities and

incurs expenditure in support of activities agreed in RWPs.

28

Assurance over accuracy of reporting:

The coverage, type and frequency of assurance activities is guided by the level of risk

associated with the Implementing Partner, as determined through the micro assessment.

Implementing Partners assessed as “high risk” will, when compared to “low risk” partners, be

subject to more frequent on-site review, more frequent and in-depth programmatic monitoring activities, and more frequent audits. Unfavourable findings of assurance activities may result

in a reconsideration of the modalities, procedures and assurance activities for that partner. The

assurance activities will include at least one audit for each Implementing Partner who is

expected to receive a minimum of US$500,000 within the programme cycle.

4.2 CASH TRANSFER FRAMEWORK ON THE PROGRAMME PROCESS

Decisions about the modalities, procedures, and assurance activities for cash transfers are an

integral part of the common country programming process.

7.3.1 Common Country Assessment (CCA) – section on financial accountability

The key findings of the Macro Assessment should be summarized in the CCA. Among them

should be one that specifies areas where national capacity is lacking. While working on

UNDAF, the UNCT should collectively discuss the results of the CCA analysis and agree on

what interventions they may undertake to address the identified gaps and name the Agency

best positioned to do so.

7.3.2 Common Country Programme Action Plan (cCPAP)

The cCPAP sets out the expected key results and strategies of the country programme and

programme management arrangements. For the management of cash transfers the following

should be recorded in it:

the available resource transfer modalities which the Agency and Government agree to utilize;

that applicable procedures depend on risk ratings for transfer of cash to each 29

Periodicity of Disbursement and Reporting

Type

Periodicity of

disbursement Reporting

Direct cash transfer Quarterly FACE

Direct payment to vendors Activity based FACE

Reimbursement of expenses Activity based FACE

Direct agency implementation N/A By Agency

Implementing Partner;

that a (micro) financial capacity assessment will be undertaken for each Implementing Partner;

the principles and scope of the assurance activities;

that cash transfer modalities and procedures applied with a particular Implementing Partner may change subject to experience and the results of assurance activities,

the commitments of both government partners and Agencies for the transfer and utilization of cash resources, reporting, and assurance activities, including audits.

18 Month Rolling Work Plan (RWP)

The RWPs detail both the activities to be carried out by Implementing Partners, and the

associated budgets. The RWP is the basis of disbursements and efforts should be undertaken to determine reasonable costing of the planned activities. The RWP should indicate, among

other elements, the resource transfer modalities to be applied.

Joint Mid-term & Annual Review

Each RWP is subject to a joint mid-term and annual review by the Implementing Partner and

the UN Agency. In the case of joint programmes, the mid-term and annual review is to be

carried out jointly by participating Agencies. This is a good opportunity to also review the

effectiveness of the applied resource transfer modalities and procedures, based on the findings

of the assurance activities undertaken during the year.

30

Annex 1:

FREQUENTLY ASKED QUESTIONS

Funding Authorization and Certificate of Expenditures (FACE)

1. Will the Agencies have to undertake partner assessments before the FACE can be

used?

Before using FACE, micro assessments for all non-UN Implementing Partners that are expected

to receive more than $100,000 in one year have to be completed. For Implementing Partners

who receive less than $100,000 in one year, Agencies will need to determine the modality and

assurance activities before using the FACE form.

2. Can FACE be used to track monthly expenditures?

Cash transfers should, as a general rule, be requested and released for activities to be

completed within a period of three months. Therefore, FACE should be used to report on the

expenditures incurred over the three months period. In exceptional cases, subject to a joint decision of the local ExCom team, FACE could be used to track monthly expenditures.

3. Preparation of an expenditure report takes some time and the release of funds

based on one and the same report/request form (FACE) might disrupt programme

implementation. Can we increase the first advance to ensure flexibility and

continuous flow of resources?

No, this should not be done. FACE has been designed as a flowing form, which is meant to

provide a cumulative statement of funds disbursed and used/reported on. As the preparation

of an expenditure report will take a certain amount of time, Agencies may release the next

advance/installment based on partial utilization of the previous transfer. If reports of

utilization of funds are outstanding for more than 6 months, disbursements will be stopped.

4. Why 3 months? Is it in line with what other donors do? Are Agencies supposed to

coordinate with donors and other partners locally?

According to Agencies‟ global experience, three months present a good compromise that allows

the tracking of activities, expenditure and results without overburdening partners with too

many reporting obligations.

5. Reporting in a joint programme: is it necessary to use FACE?

Yes, in case of joint programmes FACE should be used.

6. Does FACE provide information on the “age” of balances?

No, FACE only provides information on the totality of balances for each activity line.

7. Will FACE be used to replace UN Agencies’ internal financial reports?

FACE was designed, primarily, to lessen the burden on national counterparts. Internal reporting may be adjusted by Agencies to take advantage of the use of FACE by

v

Implementing Partners.

8. How will the opening balances be recorded on the FACE form?

The first request will be recorded in the “request” columns of FACE (the reporting columns

remain blank). For subsequent submissions, the first column will indicate the cumulative un-

liquidated amounts.

9. What other documents will be used to request funds, record expenditure, or to

liquidate amounts whose use is being reported in FACE?

For funding requests, the „FACE‟ form will have an itemized cost estimate attached.

For expenditure reporting, the „FACE‟ form is the only document required, as all the supporting

documents will be retained with the Implementing Partner.

10. Although FACE should be used for Direct Payments, it does not have a dedicated

space for information related to service providers (i.e. names, account numbers etc.).

What back-up documentation will be needed?

A “Direct Payment” is defined as a transfer of cash to vendors or third parties for obligations

incurred by the Implementing Partners on the basis of requests signed by the designated

official of the Implementing Partner. Thus, the minimum requirement for an Agency to proceed

with a direct payment on behalf of an Implementing Partner for an obligation incurred by this

Partner is an Authorized Request. If FACE is used to request a direct payment and is duly

certified by a designated official of the Implementing Partner (in this case FACE will have the

function of the Authorized Request), no supporting documents are, strictly speaking, required.

An annex can be used to describe the payments to be done, the vendor and its bank details.

Note: Some offices require Implementing Partners to attach supporting documentation to the

request for direct payment and they review this documentation as part of their monitoring

activities. Implementation of HACT is an opportunity to re-think the overall scope of

monitoring and, possibly, discontinue this requirement assuming that adequate assurance can

be achieved through other activities.

11. If there are two cash transfer modalities used with an Implementing Partner, will

this require 2 sets of FACE forms?

Yes, one form cannot accommodate more than one modality.

12. How does one reflect currency of the form?

The FACE form includes an area to record the currency of the transactions. Separate FACE

forms should be prepared for expenditures in each currency. There is no need for laborious

reconciliations of expenditures in different currencies.

13. How does one record gains and losses as a result of currency fluctuations on the

form?

The form is meant only to reflect only local currency values of transactions. Each Agency

vi

has its own procedures for allocating exchange gains/losses to individual projects. Multiple FACE forms may be submitted for multiple currency disbursements. At any given time, the

official levels of expenditures are those recorded in the UN Agency accounts and valued in US

dollars.

14. How is the form filled out?

Implementing Partners fill in the white sections and UN Agencies fill out the shaded sections.

15. How should Agencies keep track of the FACE forms?

There should be a FACE form for each quarter, even if there is no activity. These should be

filed and kept in the country office.

16. FACE appears to assign both the Authorizing/Approving AND Certifying functions to the same person, i.e. the person completing column C is the same person signing the

FACE. Does this contradict the internal control procedures of Agencies that separate

these two functions?

ExCom Agencies have not harmonized their internal control procedures. Division of duties is a

basic internal control point but its method of application and terminology varies between the 4

Agencies.

Most Agencies use a separate voucher to make entries to systems and to capture and evidence

points of internal control and the officers responsible, and to which they routinely attach

supplier invoices and other accounts payable including FACE. We therefore expect this to be

applied by each Agency as they process FACE forms and make appropriate accounting entries

and payments.

In other words, FACE form does not impose a given internal control process, and it does not

prevent each Agency from following its own internal control procedures.

In particular, note that column C of FACE is only used by a UN Agency to accept, reject or modify the expenditures reported by the Implementing Partner. It does not certify the

correctness of the financial statement submitted by the partner.

17. Is there more Agency-specific or DGO guidance for approving officers to accept or not accept expenditure?

HACT expands the more traditional role of checking expenditures against an agreed budget in

the RWP to include programmatic and substantive issues. Through on-site reviews and

programmatic monitoring there is a clearer link between financial accountability and programme results.

To put it more simply, if on-site reviews and ongoing assurance activities indicate that the

programme is being implemented according to plan, then this gives support to the acceptance

of expenditures as reported in FACE form. If there has been no evidence that activities have been carried out as planned, and even if expenditures are within budget, the Agency should

vii

consider rejecting the FACE on the grounds of a lack of adequate programme implementation

by the Implementing Partner.

18. If the Government signs an RWP but Agencies directly support various local entities

(e.g) district offices of the ministry), will each such entity need to submit a FACE?

Entities who receive funds from Agencies will have to request and report on FACE forms. The

signatories on the FACE must also be on the RWP to ensure a consistent approach to

accountability.

19. The Coding column of FACE (2nd column from the left) is not specific enough to

encompass the range of different codes needed. Are modifications possible?

Yes, the coding column can be adapted to specific Agency needs, as long as the basic format of

the form is kept intact.

20. How does one record in the FACE yearly expenditures such as salaries of technical

assistance staff at the ministries?

These expenditures should be authorized and certified quarterly like all other programme

expenses.

21. FACE requires a shift from line budgeting to budgeting based on activities – where

are the aggregate line budgets represented?

The activity budget lines are defined in and come from the RWP.

22. Is the FACE form time-bound? How should Agencies deal with carry-overs?

Any FACE records the available balance plus disbursements meant to cover activities for the

next three months. Any unreported or unliquidated balance as of the year end will have to

show in the first FACE of the new year. Obviously, the RWP of the new year will have to reflect

the activities that the unspent balance is meant to cover.

23. What happens with carry-overs in the last quarter of the programme cycle?

Agencies should discuss with partners during the preparation of RWP for the first year of the

new cycle and re-programme, or reimburse or refund carry-overs to start over at $0.

24. How should Agencies manage FACE with partners and how to handle multiple

amendments over the year?

The process to follow is set forth below:

First, FACE is prepared in hard copy for signature by the certifying officer of the Implementing Partner and by the Agency;

Changes within any given quarter should be noted by hand on the FACE in the Requests/ Authorizations section and shared with partners;

The next quarter‟s FACE is then amended to reflect the change;

vii

Auditors will use a random sample of FACEs for any given partner to assess whether actual expenditures matched reported ones;

Where amendments are expected, the hard copy FACE with notations is an essential part of the paper trail.

25. Which are the key changes in work load for programme staff, when FACE form is

used?

Programme officers are responsible for the management of cash inputs to the programme they

are assigned to. FACE reflects this by requiring those officers to approve / amend / reject

disbursement requests or reported expenditure by signing or not signing the FACE. This does

not represent any change in workload.

Where a programme officer had previously delegated this to someone else, then this improved

working practice would represent an increase in the workload of the programme officer.

26. In a rapidly changing programme environment, does FACE allow Agencies to be

opportunistic and shift resources to new activities?

Yes, FACE does not prevent changes in activities. It merely requires that these changes be

properly approved by Agencies and properly communicated to Implementing Partner, and

reflected in the FACE form.

27. When a UN Agency accepts the expenditure in FACE, does it assume accountability

for these funds? Based on what info, should the Agency accept expenditures in FACE?

UN Agency staff “accept” the expenditure in FACE based on the results of the assurance

activities, including programmatic monitoring. Thus, more attention should be paid to regular

monitoring. Micro assessments are also really important, as they provide the UN team with an

indication of how closely it should monitor the activities of some Implementing Partners. More

staff should be involved in monitoring larger programmes.

28. Who is ultimately accountable for the use of UN funds – an Implementing Partner or

the UN Agency?

It is the Implementing Partner that is ultimately accountable for the funds received, unless a

direct agency implementation has been chosen as a cash transfer modality. Nonetheless, UN

staff who authorize transfers of cash to Implementing Partners and certify expenditures should

exercise due diligence when authorizing additional transfers. Agencies will also be accountable

for ensuring proper assurance.

29. The implementing partner can request a direct payment to a supplier on its behalf.

Who is accountable for such transaction? Should UN Agencies insist on the submission

of key supporting documentation, e.g. a contract, invoice, etc.? Otherwise, what

grounds would the Agency’s office have to agree to pay?

In case of direct payments, vouchers are not entered in the books of the Implementing Partner.

viii

Hence, when the IP is audited, the respective transactions will not be subjected to audit

scrutiny. Such payments will be audited by the internal audits of Agencies and, thus, some

Agencies prefer to still request supporting documents, even though HACT does not have such a

requirement.

30. Will anything change in the way offices record advances of funds in their ERPs

with the introduction of FACE?

No, no changes are envisaged.

31. Should NGOs be included in the list of signatories of FACE (for example, in cases

when the signature of FACE needs to be delegated to an NGO by a Ministry responsible

for implementation, i.e. an NGO is a sub-implementer)?

FACE should be signed by the signatory of the RWP. In case the signature of FACE form is

delegated to a different institution‟s official, a proper designation of such responsibility should

be done.

32. Should the principle of a FACE per each Direct Payment apply? This may lead to a

large number of FACEs to be prepared. How to keep track of them? Should FACEs be

numbered?

It is possible to have several requests for direct payment included into one FACE. In this case

the FACE will have several attachments specifying necessary banking and other info for each

direct payment.

33. Some teams suggested removing the yellow color from the CODE BUDGET box. They

believe this should be filled in by the partners. Could/Should this be done?

The code-box should remain yellow, as it would not be in the spirit of simplification and

reduced transaction costs if the partners would have to learn UN coding of activities. Even if it

is the Implementing Partner that completes the code-box, a UN staff should verify the

accurateness.

34. There is a proposal, in the box in the right lower corner, to add a Reference to the

Receipt, so the beneficiary may be able to trace the reason for the payment.

Could/Should this be done?

It would be useful to make a reference to a check or a voucher number, rather than a receipt.