halliburton retirement & savings plan retirement & savings plan summary plan description...

TRANSCRIPT

BENEFITSin our

Choose your

Summary Plan DescriptionEffective January 2009

Halliburton Retirement & Savings Plan

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

The Halliburton Retirement and Savings Plan (the “Plan”) is a defined contribution plan sponsored by the Halliburton Company (the

“Company”). Certain employers that are affiliated with the Company have adopted the Plan for purposes of providing benefits for their

employees and beneficiaries. As used in this Summary Plan Description (“SPD”), the term “Company” also refers to such employers.

This SPD is designed to provide a summary of the features of the Plan. It is not intended to provide investment advice in any way, or

to be a solicitation of any investment or asset classes.

Every effort has been made to provide clear and accurate information about the Plan. However, in the event of a discrepancy between

the material presented in this SPD and the official Plan document, the official document and administrative practice will always govern.

The Company reserves the right to change, amend or terminate the benefit plans and the information set forth herein in whole or in

part at any time. Any such change or termination shall be made at the sole discretion of the Company.

It is intended that the Plan shall constitute a plan described in Section 404(c) of the Employee Retirement Income Security Act of 1974

and Title 29 of the Code of Federal Regulations Section 2550.404(c)-1, and that the fiduciaries of the Plan may be relieved of liability for

any losses that are the direct and necessary result of investment instructions given by a Plan participant or beneficiary.

This document constitutes part of a prospectus covering securities that have been registered under the Securities Act of 1933, as amended.

Halliburton has filed a registration statement on Form S-8 (Registration No. 333-86080) ( the “Registration Statement”) with the Securities and

Exchange Commission ( the “Commission”) in connection with the offer and sale of Halliburton’s common stock, par value $2.50 per share

(“Halliburton stock”) and the interests in the Plan, pursuant to the Plan. This Summary Plan Description and the documents incorporated by

reference in the Registration Statement, taken together, constitute a prospectus (this “Prospectus”) covering shares of Halliburton stock and the

interests in the Plan that have been registered under the Securities Act of 1933, as amended (the “Securities Act”).

Halliburton will provide without charge to any person, including any beneficial owner, to whom a copy of this Prospectus is delivered, upon

written or oral request of such person, a copy of the Plan and a copy of any and all documents incorporated by reference in the Registration

Statement or this Prospectus (other than exhibits to such documents that are not incorporated by reference into the Registration Statement or

this Prospectus), as well as any other documents required to be delivered to such persons, pursuant to Rule 428(b) under the Securities Act.

Such requests should be directed to the attention of the Halliburton Benefits Center, at 1-800-535-8130. If outside the U.S., call 866-373-

3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-free number).

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Overview .................................................................................................................................................................... 1

Participating in the Halliburton Retirement and Savings Plan ...................................................................................... 4 Eligibility ..................................................................................................................................................................................................................................................5 Participation and Enrollment ..................................................................................................................................................................................................................5 How to Enroll...........................................................................................................................................................................................................................................5 Automatic Enrollment .............................................................................................................................................................................................................................6 Automatic Escalation ..............................................................................................................................................................................................................................6 What If I Forget My Password? ...............................................................................................................................................................................................................7 Naming a Beneficiary .............................................................................................................................................................................................................................7 Vesting .....................................................................................................................................................................................................................................................7 Cost of Administering the Plan ...............................................................................................................................................................................................................8

Service With Halliburton ............................................................................................................................................. 9 Hours of Service and Service Computation Period ..............................................................................................................................................................................10 Years of Service .....................................................................................................................................................................................................................................10

Plan Contributions .................................................................................................................................................... 11 Tax-Deferred Savings Contributions .....................................................................................................................................................................................................12 Company Matching Contributions........................................................................................................................................................................................................14 Halliburton Basic Contribution .............................................................................................................................................................................................................15 Rollover Contributions ..........................................................................................................................................................................................................................17

Investing Your Money ............................................................................................................................................... 18 How to Make or Change Your Investment Options ..............................................................................................................................................................................19 Your Investment Fund Options .............................................................................................................................................................................................................20 Premixed Portfolios ...............................................................................................................................................................................................................................20 Single Focus Funds ................................................................................................................................................................................................................................21 If You Have Investments in the Halliburton Stock Fund ......................................................................................................................................................................22 Understanding Risk and Return ...........................................................................................................................................................................................................23 Investment Transfer Policy ....................................................................................................................................................................................................................25 Keeping Track of Your Account ..............................................................................................................................................................................................................26

Loans, Withdrawals and Distributions ........................................................................................................................ 27 Loans .....................................................................................................................................................................................................................................................28 In-Service Withdrawals .........................................................................................................................................................................................................................30 Distributions ..........................................................................................................................................................................................................................................32 Qualified Domestic Relations Orders (QDROs) .....................................................................................................................................................................................35 Distributions For Participants With a Balance Prior to June 1, 1998 ...................................................................................................................................................36 Distributions For Participants Who Began Participating in the Plan On or After June 1, 1998 .........................................................................................................38

The Halliburton Benefits Center ................................................................................................................................ 40

Administrative Information....................................................................................................................................... 42 Plan Information ...................................................................................................................................................................................................................................43 Plan Amendment and Termination ......................................................................................................................................................................................................45 Claims Procedures .................................................................................................................................................................................................................................45 Your Rights Under ERISA ......................................................................................................................................................................................................................48 USERRA and FLMA ................................................................................................................................................................................................................................50 Miscellaneous Information ...................................................................................................................................................................................................................50

Terms to Know .......................................................................................................................................................... 52

Table of Contents

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Overview

1

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

The Company is committed to helping you prepare for your financial future. By sponsoring this Plan, the Company has made it

easier for you to save for retirement and other long-term financial goals. Listed below are some of the features of the Plan that can

help you reach your retirement and savings goals:

• You can save from 1% to 50% of your eligible pay on a tax-deferred (pre-tax) basis. The amount of eligible pay that can

be taken into consideration for Plan purposes is subject to the Internal Revenue Code (IRC) limits.

• Your savings are matched by the Company. The Company matches every dollar you invest up to the first 4% of eligible pay

each pay period. Beginning January 1, 2009, the Company will also match 50 cents for each dollar you invest that is between

4% and 6% of eligible pay each pay period. You are immediately vested in the Company matching contributions if you were hired

prior to January 1, 2009. If you are hired on or after January 1, 2009, you become vested in the Company matching contributions

after you complete two years of vesting service.

• Automatic Company contributions. The Company makes an automatic contribution to your account if you are employed

on the last day of the year equal to 4% of your eligible compensation. This contribution is referred to as the Halliburton Basic

Contribution. You will receive this contribution even if you do not elect to make contributions to the Plan. You become vested

in the Halliburton Basic Contribution after you complete three years of vesting service.

• You are automatically enrolled. If you are an eligible employee hired on or after January 1, 2006, and you do not make

any enrollment elections with respect to the Plan during your first 30 days of employment, you will be automatically enrolled

to contribute 4% of your eligible pay per pay period into the Plan. Your automatic tax-deferred savings contributions will begin

approximately 30 days after your date of hire and such contributions will continue to be made until you take action to change

the contribution percentage. Further, if you were hired prior to January 1, 2009, and you did not affirmatively make any

contribution elections with respect to the Plan or if you were not previously automatically enrolled, 4% of your eligible pay per

pay period will be taken from your pay and contributed to the Plan effective with respect to your first paycheck in 2009. Unless

you choose a different investment fund or funds, your Plan account will automatically be invested in the Moderate Premixed

Portfolio.

• Your contributions automatically increase. The automatic escalation feature increases the percentage you contribute to the

Plan each year until you reach a target deferral goal. This feature automatically applies to you if you are automatically enrolled

in the Plan. You may opt out of the automatic escalation feature at any time. The automatic escalation feature can be elected at

any time if you are not automatically enrolled in the Plan.

• You can rollover money from other plans. You may be able to roll benefits from a previous employer’s qualified retirement

plan or from an individual retirement account into the Plan.

• You can save on taxes. Your tax-deferred savings contributions can lower your current tax liability, and your earnings also

grow tax-deferred, which means you have more money working for you today. You pay taxes on the money when you

withdraw it, presumably at retirement when your tax bracket may be lower.

• You decide how to invest your money. You decide how to invest the money in your account by choosing from 12 core plan

funds.

Overview

2

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

• You can access your money if you need it. Subject to certain Plan limitations and restrictions, you may be eligible to borrow or

make withdrawals from your Plan account while you are an employee.

• You can take your account when leave. You’re eligible to receive a distribution once you are no longer employed by the

Company.

• It is easy to participate. You contribute to the Plan through automatic payroll deductions, making saving a part of your normal

routine.

• You have online access to your account. You can access your account at: http://resources.hewitt.com/halliburtonbenefits.

Enter your social security number and password or use the Halliburton Benefits Center’s automated telephone system at 1-800-

535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-free

number).

• You can speak with a customer service representative. You can speak with a customer service representative by calling

the Halliburton Benefits Center’s automated telephone system between 8:30 a.m. and 5:00 p.m. Central Standard Time, Monday

through Friday.

• Terms to Know Throughout this SPD, terms appearing in italics are defined in the “Terms to Know” section.

Overview

3

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Participating in the Halliburton Retirement

and Savings Plan

4

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

EligibilityAs an employee of the Company, you are eligible to participate in the Plan beginning on your date of hire. You are not eligible if

you are:

• Coveredbyacollectivebargainingagreement,unlesstheCompanyhasspecificallyextendedparticipationtotheemployeegroup;

• Anon-residentalienwithnoearnedincomefromtheCompanyfromsourceswithintheU.S.;

• Coveredbyanotherfundedplanand/oradeferredcompensationplanofaforeignsubsidiarywithrespecttoU.S.employment;

• Anemployeewhoiseligibletoparticipateinanyotherqualifiedplan,excepttheHalliburtonRetirementPlan;or

• DesignatedorcompensatedbytheCompanyasaleasedemployeeoranindependentcontractor.

Participation and EnrollmentAs an eligible employee, you are entitled to participate in the Plan on the first day of your employment. You can elect to make tax

deferred contributions as soon as administratively feasible after your date of hire. Employees hired on or after January 1, 2006, will

be automatically enrolled in the Plan after 30 days of employment unless they choose to opt out. You may elect to enroll and begin

participating in the Plan prior to 30 days of employment. (For more information on enrollment see the “How to Enroll” in this section.)

How to EnrollThe Your Benefits ResourcesTM Web site is the fastest, easiest and most convenient way to enroll in your Retirement and Savings Plan. Go

to http://resources.hewitt.com/halliburtonbenefits through the Internet (from any computer with Internet access) or connect

through HalWorld, the Halliburton Intranet site. The Your Benefits Resources (“YBR”) Web site is available Monday through Saturday, 24

hours a day, and Sunday after 12 p.m. Central Standard Time.

• ToaccesstheYour Benefits Resources Web site, the Halliburton Benefits Center’s automated telephone system, or a Halliburton

Benefits Center representative, you will need your Social Security number and password.

• Ifyouareanewhire,youcanselectapasswordthefirsttimeyoucontacttheHalliburtonBenefitsCenter,eitherthroughthe Your

Benefits Resources Web site or by phone. You also can create a hint to help you remember your password.

• IfyoudonothaveInternetaccess,youmayenrollbycallingtheHalliburtonBenefitsCenter’sautomatedtelephonesystemat

1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-

free number). The automated phone system is available Monday through Saturday, 24 hours a day, and Sunday after 12 p.m.

Central Standard Time.

• Ifyouneedpersonalassistance,call1-800-535-8130, enter your Social Security number, select the option for the 401(k) Savings

Plan, then press the star key and zero (*0) to be connected to a Halliburton Benefits Center representative. If outside the U.S.,

call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-free number). Representatives are

available Monday through Friday between 8:30 a.m. and 5 p.m. Central Standard Time.

Participating in the Halliburton Retirement and Savings Plan

5

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Automatic EnrollmentIf you are an eligible employee hired on or after January 1, 2006, you are automatically enrolled to contribute 4% of your eligible pay

per pay period to the Plan, unless you choose to opt out. These automatic payroll deductions will begin approximately 30 days after

your date of hire. Further, if you were hired prior to January 1, 2009, and you did not affirmatively make any contribution elections

with respect to the Plan or if you were not previously automatically enrolled, you have been automatically enrolled to contribute 4%

of your eligible pay per pay period to the Plan effective with respect to your first paycheck in 2009. This means that 4% of your eligible

pay will automatically be deducted from your paycheck each pay period on a pre-tax basis and deferred into the Plan as tax-deferred

savings contributions unless you take actions to opt out of this process. Once these amounts are deferred into the Plan, they

cannot be refunded to you. If you do not want 4% of your eligible pay to automatically be deferred into the Plan, you

must affirmatively take action to opt out of the Plan within the appropriate time frame. You will receive detailed information

regarding this automatic enrollment process, including information regarding the approximate date the automatic payroll deductions

will begin and when and how you can opt out of the Plan before the automatic deductions begin.

All contributions made under automatic enrollment will be invested in the Moderate Premixed Portfolio unless you affirmatively take

actions to change this investment election. Please refer to the Your Benefits Resources Web site for a description of the Moderate

Premixed Portfolio Fund.

You can always modify or cancel the default deduction and investment elections anytime through the Your Benefits Resources Web site

or by calling the Halliburton Benefits Center at 1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T

access code) or 847-883-0702 (not a toll-free number).

Automatic EscalationIn an effort to help you reach your contribution rate goal, the Plan has an automatic escalation feature. Under this feature, you can elect

an annual percentage increase for your tax-deferred savings contributions to the Plan and set a target deferral percentage of your salary

goal. Then, the feature automatically increases your annual tax-deferred savings contributions each year in January until your target

deferral percentage of salary is reached.

The “Change Contributions” option under the Retirement and Savings section of the Your Benefits Resources Web site allows you to

select the annual rate increase for your contribution. You can then input your target contribution rate and your contribution rate will

increase each January until your target goal is reached. You must make your contribution choices before December 1 of each year

otherwise your contribution amount will not automatically increase until the following year.

If you have been automatically enrolled in the Plan, the automatic escalation feature is automatically established for you.

Your contribution rate will increase by 1% each January for three years beginning with the January following the first anniversary of

your date of hire until it reaches 7% of your eligible pay.

You can always modify or cancel the feature anytime through the Your Benefits Resources web site. Go to http://resources.hewitt.

com/halliburtonbenefits through the Internet (from any computer with Internet access) or connect through HalWorld, the

Halliburton Intranet site. The Your Benefits Resources (“YBR”) Web site is available Monday through Saturday, 24 hours a day, and Sunday

after 12 p.m. Central Standard Time.

Participating in the Halliburton Retirement and Savings Plan

6

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

What If I Forget My Password?If you do not have your password, you can request a new one by selecting “I Forgot My Password” on the Your Benefits Resources (YBR)

Web site, or by calling 1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-

883-0702 (not a toll-free number). Your new password will be e-mailed to you at the e-mail address on file with the Halliburton

Benefits Center. If you do not have an e-mail address on file, your new password will be mailed to the address on file. Please allow

seven to 10 days to receive a password by mail.

Naming a BeneficiaryYour beneficiary is the person you name to receive your Plan benefits in the event of your death. If you are legally married, your spouse

is automatically your primary beneficiary. If you want to name someone other than or in addition to your spouse as your primary

beneficiary, your spouse must consent in writing to your choice. If you are married at the time of death and someone other than your

surviving spouse is designated as your beneficiary, such designation will be automatically void unless your surviving spouse consented

to such designation.

To designate a beneficiary, go to the Your Benefits Resources Web site or call the Halliburton Benefits Center and speak with a

representative.

In the event of a divorce, your beneficiary designation of your former spouse is automatically void unless you specify otherwise by

contacting the Halliburton Benefits Center. In addition, if you are divorced, you may designate anyone as your beneficiary unless a

Qualified Domestic Relations Order (QDRO) limits your ability to name a beneficiary.

Upon your death, your benefit is paid to your named beneficiary. If there is no valid beneficiary form on file with the Plan Administrator,

your spouse (if you are married) or your estate (if you are single) automatically becomes your beneficiary.

Every beneficiary who becomes entitled to a benefit upon your death has the right to designate a beneficiary to receive payment in the

event of their death. Beneficiary elections can be made by calling the Halliburton Benefits Center at 1-800-535-8130. If outside the

U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-free number). If your beneficiary dies

without naming a beneficiary or if the designation is invalid for any reason, your benefit will revert back to your estate.

VestingVesting defines the portion of your account that you own and can take with you when you leave the Company. When you become

100% vested in your account balance, you have earned ownership of your entire balance.

• Youalwaysare100%vestedinyourtax-deferred savings contributions, after-tax savings contributions* and rollover contributions, any

earnings on those contributions and, if you have a balance in the Halliburton Stock Fund, any dividends from Halliburton stock.

• Youalwaysare100%vestedinHalliburton’scompany matching contributions if you were hired prior to January 1, 2009 .**

• Youbecome100%vestedinHalliburton’scompany matching contributions after two years of service if you were hired on or after

January 1, 2009. If you have two or more years of service at the time the contribution is made, you automatically will be vested in

the full contribution amount.

Participating in the Halliburton Retirement and Savings Plan

7

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

• Youbecome100%vestedintheHalliburton Basic Contribution after three years of service. If you have three or more years of service

at the time the contribution is made, you automatically will be vested in the full contribution amount.

• Youautomaticallyare100%vestedinallofyourPlanaccountbalancesifyoudie,becomedisabled or reach age 65 while employed

by the Company or a controlled entity of the Company.

• VestedPlanaccountbalancescanonlybewithdrawnaccordingtoPlanrules.

* As of January 1, 2004, after-tax savings contributions are no longer permitted.

** The Plan may be amended or terminated at any time. With respect to vesting, you will be subject to the Plan’s vesting schedule in effect as of your employment commencement date.

Cost of Administering the PlanMany of the fees, costs and expenses associated with sponsoring and maintaining the Plan are paid by the Company. However,

certain reasonable expenses of administering the Plan may be paid out of the Plan’s assets. Some fees and expenses, if they become

applicable, will be fully charged to and paid from your account. An example of a type of fee that will be fully charged to your account

is a $50 loan initiation fee if you obtain a general purpose loan or a home loan from the Plan.

The administrative fees and expenses which are paid out of the Plan’s assets and which are not charged to individual accounts as

described above will be allocated among and charged to the accounts of all participants in the Plan on either a pro rata or per

capita basis.

Participating in the Halliburton Retirement and Savings Plan

8

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Service With Halliburton

9

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Service With Halliburton

Your period of service with the Company is important under the Plan in order to determine your:

• VestedinterestintheHalliburton Basic Contribution and Company matching contributions;

• Eligibilityforretirement;and

• Eligibilitytoreceiveadistributionuponretirement.

Hours of Service and Service Computation PeriodYour service with the Company is measured by the “hours of service” you complete during a “service computation period.”

An hour of service is any hour for which you are paid or entitled to be paid by the Company (directly or indirectly). An hour of

service also includes each hour not credited for which you receive back pay. Hours of service with an employer that is a member of

a controlled group of employers (as defined in the Internal Revenue Code) with the Company will count as hours of service with the

Company.

Your service computation period is the 12-consecutive-month period that begins on your date of hire and on each anniversary of

your date of hire. If your service is disregarded due to a break in service, you will start a new service computation period when you are

rehired after the break in service.

If you complete 500 or less hours of service in a service computation period, you will have a one-year break in service. This means you

will not receive any credit towards your years of service with respect to that service computation period. For purposes of determining

whether a one-year break in service has occurred, there is a special rule for absences from work due to your pregnancy, the birth of

your child, your adoption of a child or your caring for your child during the period immediately following such birth or adoption. You

will be credited with hours of service during these absences to prevent a one-year break in service in the service computation period

when the absence begins, if you do not otherwise complete 500 hours of service in that period, or in the immediately following

period.

Years of ServiceYou will be credited with a “year of service” for each service computation period in which you are credited with 1,000 or more hours of

service, regardless of your employment status on your employment anniversary date.

If you have a one-year break in service, you will not receive any credit towards your years of service with respect to that service

computation period. If you are rehired, any years of service you were credited prior to your incurring a one-year break in service will

be added to the years of service you earn after your one-year break in service.

Special rules apply when determining your years of service in order to determine whether your age and years of service total 70

to qualify you for retirement. For this purpose, age is determined in years and fractions of years. In addition if, during the service

computation period in which you terminate employment, you did not complete 1,000 hours of service so as to receive credit for a full

year of service, you will be credited with a fraction of a year of service, based on the number of months in which you worked during

that service computation period.

10

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Plan Contributions

11

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Contributions are made to your Retirement and Savings Plan through:

•Yourtax-deferred savings contributions;

•Company matching contributions;

•Halliburton Basic Contributions; and

•Rollover contributions.

Tax-Deferred Savings ContributionsYour tax-deferred savings contributions are taken from your paycheck before income taxes are taken out. You will not pay federal income

taxes on your tax-deferred savings contributions or on your account earnings until you take the money out of the Plan. This means you

may pay less in current taxes, and may potentially pay less in future taxes, because you may be in a lower tax bracket when you elect

a distribution of your account. In most cases, state and local taxes also are deferred. Social Security taxes remain calculated on the full

amount of your gross pay.

Your Contribution Rate

While you are actively employed as an eligible employee with the Company, you may contribute 1% to 50% of your eligible pay per

pay period through payroll deductions on a tax-deferred basis. Your contributions cannot exceed 50% of your eligible pay. Your savings

contribution rate must be a whole-number percentage. The Plan does not have a flat dollar contribution option.

Eligible Pay

Your contributions to the Plan and your share of any Company contributions to the Plan are based, in part, on your eligible pay from

the Company. For purposes of the Plan, your eligible pay includes:

• YourannualbasecompensationfromtheCompanywhileyouareaneligibleemployee;

• Anyovertimeandshiftdifferentialearnings;

• Yourtax-deferred savings contributionstothePlan;and

• Yoursection125tax-deferredcontributionstocompanysponsoredhealthandwelfareplans.

The following types of compensation are excluded from eligible pay:

• Bonuses;

• Geographicallowancesandforeignserviceorhardshippremiums;

• Reimbursementorotherexpenseallowances;

• Fringebenefits;

• Welfareplanbenefitsotherthanpaidtimeoffbenefits;

• Movingexpenses;

• Companycontributionstothisoranyotherdeferredcompensationprogram;

• Dividendsonrestrictedstock;and

• Certaintypesofcompensationsubjecttospecialtaxtreatment,suchasstockoptions.

Plan Contributions

12

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Annual Compensation Limit

For purposes of the Plan, your eligible pay is subject to a maximum annual compensation limit set by the Internal Revenue Code

($245,000 for 2009). This limit is adjusted periodically for cost-of-living increases.

Contribution Limits

Generally, you can contribute from 1% to 50% of your eligible pay each pay period. However, there are certain additional Internal

Revenue Code (IRC) rules that may affect some participants.

• Tax-deferred savings contribution limit: The IRC limits the amount of money you may contribute on a tax-deferred basis in any

one year. For 2009, the limit is $16,500. This limit is adjusted periodically for cost-of-living increases. If you are age 50 or older, or will

reach age 50 during the Plan year, you are eligible to make an additional tax-deferred catch-up contribution, which will allow you to

exceed the annual contribution limit by your catch-up amount. See “Catch-up Contributions.”

• Limit on combined contributions: The IRC also limits the total amount that may be contributed to the Plan and all other plans

on your behalf by both you and the Company. For 2009, the limit is 100% of your total compensation or $49,000, whichever is

less. This limit is adjusted periodically for cost-of-living increases. Contributions and allocable earnings in excess of this limit will be

refunded after year-end.

• Contributions to other qualified Plans: The 2009 IRC limit of $16,500 on tax-deferred contributions applies to an individual

taxpayer’s limit across all plans. For example, if you are a new hire who previously contributed $5,000 to another plan during 2009,

you can only contribute $11,500 to the Plan during 2009 on a tax-deferred basis. It is your responsibility to stop your contributions

before hitting the combined limit.

Catch-up Contributions

If you are age 50 or older, or will reach age 50 during a Plan year, you will be eligible to make tax-deferred “Catch-up Contributions”

each year (beginning in the calendar year in which you reach age 50). These contributions allow you to exceed the regular tax-deferred

savings contribution limit. If you elect a catch-up contribution and do not reach the tax-deferred savings contribution limit for the year,

your catch-up contribution will be considered tax-deferred savings.

If you meet the age requirement and would like to make catch-up contributions, you must make an election that is separate from your

regular contribution rate election. You may make your election at any time during the year.

To make your catch-up contribution election:

• First, decide what your total catch-up contribution will be. The IRC maximum allowable contribution for 2009 is $5,500.

Plan Contributions

13

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

• Decide how much you want deducted from each paycheck to reach your total catch-up contribution. The per paycheck

amount will be entered as your election. Your election must be a whole-dollar amount. The larger your deduction, the sooner

you will maximize your total catch-up contribution. Payroll automatically will stop your deductions once you reach the annual

maximum. After you make your election, your catch-up deduction will begin as soon as administratively possible. When calculating

your deduction amount, allow for a one to two pay period lapse before deductions begin. For this reason, you may wish to elect a

deduction amount that will enable you to reach your total catch-up contribution in less than the maximum number of pay periods

in the year.

Catch-Up Contribution Example

Assume you want to make a $2,400 catch-up contribution during the year. First, determine your payroll schedule. If you are paid

semi-monthly you would divide $2,400 by 24 to find that you should elect $100 per pay period. If you are paid bi-weekly, you would

divide $2,400 by 26 to find that you should elect $93 per pay period. If you make your election after the 1st of the year you should

reduce the number of pay periods accordingly in your calculation and round to the next highest dollar amount to determine your per

pay period catch-up contribution for the remainder of the year.

After you make your catch-up contribution election, you can change or stop it at any time during the year or in subsequent years.

Your initial election will remain in effect until you change it. If the IRC maximum changes, you will need to adjust your election

if you want to take advantage of any increases in the allowable catch-up contribution.

You can make your catch-up contribution election in one of two ways:

• GototheYour Benefits Resources Web site at http://resources.hewitt.com/halliburtonbenefits. Follow the instructions to make

your election. The site will not allow you to elect a catch-up contribution election if you will not be age 50 or older by December 31

of the current year.

• CalltheHalliburtonBenefitsCenter’sautomatedtelephonesystemat1-800-535-8130. If outside the U.S., call 866-373-3422

(toll-free using the AT&T access code) or 847-883-0702 (not a toll-free number). If you have questions or need special

assistance, Halliburton Benefits Center representatives are available Monday through Friday between 8:30 a.m. and 5 p.m. Central

Standard Time.

Company Matching ContributionsThe Company will match every dollar you save through your tax-deferred savings contributions each pay period up to 4% of your eligible

pay. Beginning January 1, 2009, the Company will also match 50 cents for each dollar of your tax-deferred savings contributions each

pay period that are between 4% and 6% of your eligible pay. If you contribute less than 6% of your eligible pay during any one pay

period, you will not maximize the Company match. Therefore, you should consider contributing at least 6% of your eligible

pay during all pay periods of the year to receive the maximum Company match of 5% of your eligible pay.

If you expect to contribute up to the IRC annual maximum ($16,500 for 2009), you will want to plan your per pay period

contributions so that they are spread out over the entire year. The reason is this: matching contributions are made on a per

pay period basis and once you reach the IRC contribution limit, you will not be permitted to make deferrals into the Plan in future pay

periods and thus, you will not receive any Company matching contributions after that point.

Plan Contributions

14

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

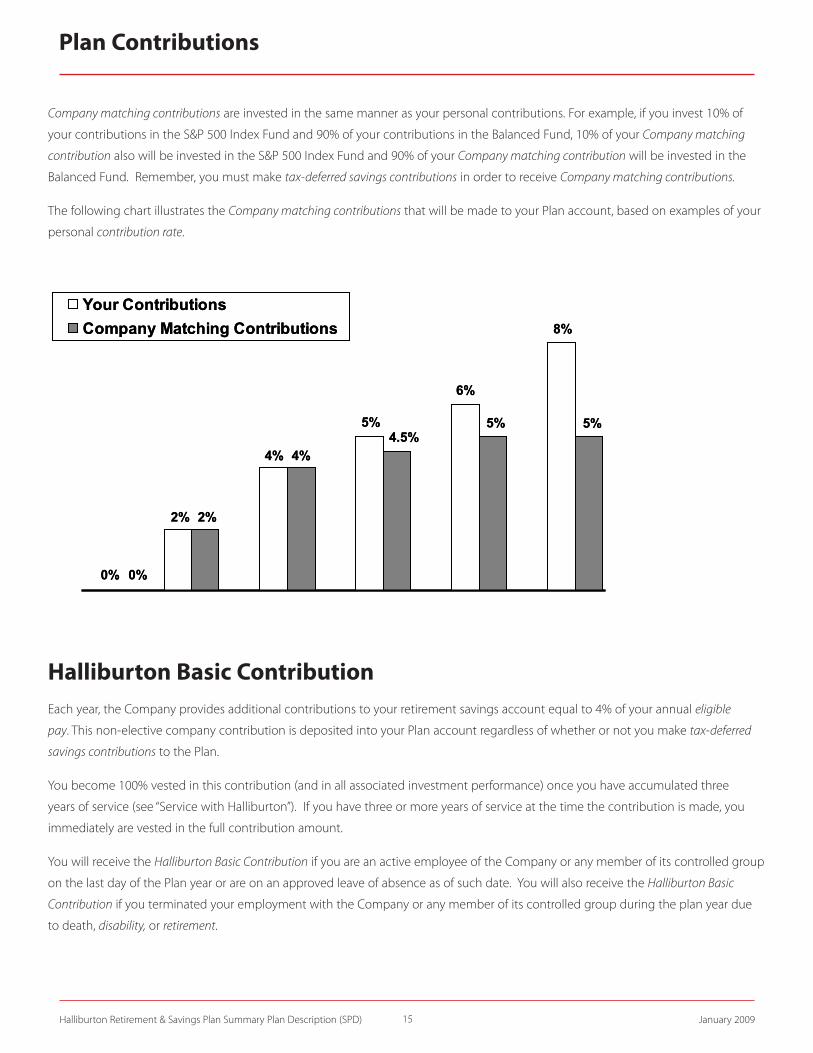

Company matching contributions are invested in the same manner as your personal contributions. For example, if you invest 10% of

your contributions in the S&P 500 Index Fund and 90% of your contributions in the Balanced Fund, 10% of your Company matching

contribution also will be invested in the S&P 500 Index Fund and 90% of your Company matching contribution will be invested in the

Balanced Fund. Remember, you must make tax-deferred savings contributions in order to receive Company matching contributions.

The following chart illustrates the Company matching contributions that will be made to your Plan account, based on examples of your

personal contribution rate.

Halliburton Basic ContributionEach year, the Company provides additional contributions to your retirement savings account equal to 4% of your annual eligible

pay. This non-elective company contribution is deposited into your Plan account regardless of whether or not you make tax-deferred

savings contributions to the Plan.

You become 100% vested in this contribution (and in all associated investment performance) once you have accumulated three

years of service (see “Service with Halliburton”). If you have three or more years of service at the time the contribution is made, you

immediately are vested in the full contribution amount.

You will receive the Halliburton Basic Contribution if you are an active employee of the Company or any member of its controlled group

on the last day of the Plan year or are on an approved leave of absence as of such date. You will also receive the Halliburton Basic

Contribution if you terminated your employment with the Company or any member of its controlled group during the plan year due

to death, disability, or retirement.

Plan Contributions

15

Your ContributionsCompany Matching Contributions

0% 0%

5%4.5%

6%

5%

8%

5%

2% 2%

4% 4%

Your ContributionsCompany Matching Contributions

0% 0%

5%4.5%

6%

5%

8%

5%

2% 2%

4% 4%

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

The Halliburton Basic Contribution will be allocated to investment funds based on your most current investment election on file. If you

have not affirmatively made any investment elections, the Basic Contribution will be allocated to a fund chosen by the Company. The

default fund for the Basic Contribution is the Moderate Premixed Portfolio.

If you transfer your employment to another member of the Company’s controlled group and are no longer eligible to participate in

this Plan, but are still an employee of one of the Halliburton Company’s controlled group members on the last day of the plan year,

you will receive the Halliburton Basic Contribution. This contribution will be based on the eligible pay you earned while you were

eligible to participate in this Plan. You will not receive a contribution based on any earnings you received while you were not eligible

to participate in this Plan.

Savings Example with Match

Assume you have a household income of $45,000, and are in the 15% tax bracket. The chart below compares take home pay if you

save at 6% in the Plan to not saving:

In this example, if you save at 6% or $2,700, your take home pay would be only $2,295 less and your retirement savings would increase

from $1,800 to $6,750.

*Your individual tax savings will depend on your household income, your tax status, your financial situation and the annual amount you contribute to the Plan.

Plan Contributions

16

Not Saving

401(k) Eligible EarningsTax-deferred Savings (6%)Taxable Income

Federal Income Taxes (15%)*Social Security/Medicare TaxesNet (Take Home) Earnings

Company Match401(k) SavingsBasic ContributionTotal Retirement Savings

Saving at 6%

$45,000- 0

$45,000

- 6,750- 3,443

$34,807

$0$0

$1,800$1,800

$45,000- 2,700

$42,300

- 6,345- 3,443

$32,512

$2,250$2,700$1,800$6,750

Not Saving

401(k) Eligible EarningsTax-deferred Savings (6%)Taxable Income

Federal Income Taxes (15%)*Social Security/Medicare TaxesNet (Take Home) Earnings

Company Match401(k) SavingsBasic ContributionTotal Retirement Savings

Saving at 6%

$45,000- 0

$45,000

- 6,750- 3,443

$34,807

$0$0

$1,800$1,800

$45,000- 2,700

$42,300

- 6,345- 3,443

$32,512

$2,250$2,700$1,800$6,750

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Making Changes to My Contribution Rate

You can request to change your savings contribution rate, suspend contributions, or resume contributions at any time. Changes are

effective as soon as administratively possible. You may request a contribution rate change via the Your Benefits Resources Web site at

http://resources.hewitt.com/halliburtonbenefits or by calling the Halliburton Benefits Center’s automated telephone system at

1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-free

number).

Rollover ContributionsIf, before joining the Company, you participated in a qualified savings or retirement plan sponsored by another employer, or if you

received a distribution from a qualified plan and rolled the distribution into a certain type of Individual Retirement Account (IRA), you

may be able to roll over tax-deferred savings contributions and earnings from your former employer’s qualified plan into the Halliburton

Retirement and Savings Plan.

• YoumustprovidecertaininformationtotheHalliburtonBenefitsCenterasindicatedontheHalliburtonRetirementandSavings

Plan Rollover Form. You must contact the Halliburton Benefits Center and request the form before beginning the rollover process.

• Rolloversof tax-deferred savings contributions and earnings from your former plan must be either transferred directly from your

former plan or made within 60 days after you receive payment from your former plan (after-tax account rollovers are not permitted).

• Arollover contribution must be made in the form of a check payable to “Halliburton Company Employee Benefit Master Trust.”

• Any rollover contribution or transfer will be held in your rollover account. You always will have a non-forfeitable right to the

amounts in your rollover account.

• Ifyouwouldliketomakearollover contribution, go to the Your Benefits Resources Web site or call the Halliburton Benefits Center’s

automated telephone system at 1-800-535-8130 and go to the “Rollovers” option. If outside the U.S., call 866-373-3422 (toll-

free using the AT&T access code) or 847-883-0702 (not a toll-free number).

Plan Contributions

17

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Investing Your Money

18

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Investing Your Money

The Plan offers 12 investment options, including four lifestyle-type funds called Premixed Portfolios and eight Single Focus Funds.

The investment funds offer a range of risk and return characteristics and represent different asset classes. More information about the

investment funds, performance, and expenses is available in the Investment Highlights booklet. You may request a copy of this booklet

by calling the Halliburton Benefits Center at 1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T

access code) or 847-883-0702 (not a toll-free number). Detailed fund information also appears on the Your Benefits Resources

Web site at http://resources.hewitt.com/halliburtonbenefits.

How to Make or Change Your Investment OptionsThe Plan allows you to control how your contributions are invested. Your options include:

• Investment elections. You invest your contributions based on your investment elections, which can be changed at any time via

the Your Benefits Resources Web site at http://resources.hewitt.com/halliburtonbenefits or by calling the Halliburton Benefits

Center’s automated telephone system at 1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T

access code) or 847-883-0702 (not a toll-free number). Your investment elections must be in whole percentages. Changes are

effective the next business day.

• Fund reallocation. When you elect a fund reallocation, you are changing how your current total account balance is invested. You

can request a fund reallocation at any time in accordance with Plan provisions via the Your Benefits Resources Web site at http://

resources.hewitt.com/halliburtonbenefits or by calling the Halliburton Benefits Center’s automated telephone system at

1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-

free number). Fund reallocations must be in whole percentages and are subject to the restrictions set forth in the Investment

Transfer Policy. (See the “Investment Transfer Policy” section for more details.) Your reallocation will be effective the same

business day if the request is made before the close of market (typically, 3 p.m. Central Standard Time) and in accordance with

the Investment Transfer Policy. Your fund reallocation will be reflected on the Your Benefits Resources Web site and the automated

telephone system the next business day.

• Direct fund transfers. You can make a direct fund transfer by selecting what funds to take money out of and what funds will

receive that money. A direct fund transfer is a one-time only event and will not change your future fund investment allocations.

Fund transfers are also subject to the restrictions set forth in the Investment Transfer Policy.

Effective January 1, 2007, the Halliburton Stock Fund was closed to new investments. Participants in the Plan are not allowed to

make contributions, rollovers, transfers, or loan repayments (from any source) into the Halliburton Stock Fund. Only transfers out of

the fund are permitted effective January 1, 2007.

19

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Your Investment Fund OptionsYour investment fund options are broken into four Premixed Portfolios and eight Single Focus Funds. Before you make your investment

decisions, you should carefully consider your investment goals and may wish to consult a financial advisor.

Premixed Portfolios Single Focus FundsStableValuePremixedPortfolio Bond Index Fund

Conservative Premixed Portfolio Balanced Fund

Moderate Premixed Portfolio S&P 500 Index Fund

Aggressive Premixed Portfolio LargeCapValueEquityFund

Large Cap Growth Equity Fund

Non-U.S. Equity Fund

Mid Cap Equity Index Fund

Small Cap Equity Index Fund

Premixed PortfoliosThe Premixed Portfolios were designed to provide diversified, auto-balancing portfolios according to targeted risk and return profiles.

Any one of them can be used as a complete investment strategy.

Stable Value Premixed Portfolio

TheStableValuePremixedPortfolioisthemostconservativeinvestmentoptioninthePlan.Itisdesignedtopreserveyourinvestment

principal(themoneyyouinvestinthePlan)andtoearnarelativelystablerateofreturn.TheStableValuePremixedPortfoliomay

experience a negative rate of return over shorter time periods, but it is managed with the intent of reducing this possibility.

Conservative Premixed Portfolio

The Conservative Premixed Portfolio’s objective is to achieve long-term growth with a relatively low level of risk. The portfolio aims

for a competitive investment return, while minimizing risk by diversifying its investment among different types of assets. Further

diversification is achieved by using several external investment managers with different investment styles. The Conservative Premixed

Portfolio is a highly diversified portfolio that invests in asset-backed investment contracts, bonds and stocks (both U.S. and non-U.S.).

Moderate Premixed Portfolio

The Moderate Premixed Portfolio seeks long-term growth as a major objective. The portfolio aims for a competitive investment return

while minimizing risk by diversifying its investments among different types of assets. Further diversification is achieved by using several

external investment managers with different investment styles. The Moderate Premixed Portfolio maintains a static asset allocation and

avoids market-timing strategies.

Aggressive Premixed Portfolio

The objective of the Aggressive Premixed Portfolio is to achieve long-term growth by primarily investing in stocks (including non-U.S.

stocks) and related securities. Further diversification is accomplished by using several external investment managers with different

investment styles. The Aggressive Premixed Portfolio maintains a static asset allocation and avoids market-timing strategies.

Investing Your Money

20

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Single Focus FundsThe Plan provides eight Single Focus Funds from which to choose. Investors wishing to create their own diversified portfolio can

choose from the Single Focus Funds which cover a range of asset classes and risk profiles.

Bond Index Fund

The Bond Index Fund is passively managed. This means it seeks returns that are approximately equal to the performance of the

Barclays Aggregate Bond Index, instead of following a manager’s active investment strategy. The Barclays Aggregate Bond Index is

used to represent returns of the general U.S. bond market.

Balanced Fund

The investment objectives of the Balanced Fund are long-term capital appreciation and reasonable current income. The Fund

composition can vary, with a maximum of 70% of assets invested in U.S. and non-U.S. stocks.

S&P 500 Index Fund

Similar to the Bond Index Fund, the S&P 500 Index Fund is passively managed. This means it seeks risks and returns that are

approximately equal to the performance of the Standard & Poor’s (S&P) 500 Index. The S&P 500 Index is a popular standard for

measuring large-cap U.S. stock market performance.

Large Cap Value Equity Fund

TheLargeCapValueEquityFundseekslong-termgrowthofcapitalandincomefromdividends.TheFundinvestsinstocksthatare,as

a group, selling at prices below the overall market average compared to their dividend income and future return profile. When other

investors recognize the company’s “true” value, the stock price is expected to increase.

Large Cap Growth Equity Fund

The objective of the Large Cap Growth Equity Fund is to seek long-term growth of capital. Dividend income is considered incidental.

The Fund primarily invests in the equity securities of established companies that the fund managers consider to have above-average

prospects for growth. Generally, these are rapidly growing large companies.

Non-U.S. Equity Fund

The Non-U.S. Equity Fund seeks long-term capital growth through investments in stocks of companies based outside of the U.S. The

Fund strategy is based upon the belief that the best companies for investment are not located just in the U.S. Non-U.S. stocks have

differentriskandreturncharacteristics;thus,theycanprovideexcellentdiversificationasapartofatotalportfolio.

Mid Cap Equity Index Fund

The Mid Cap Equity Index Fund is passively managed. This means it seeks risks and returns that are approximately equal to the

performance of the Standard & Poor’s (S&P) MidCap 400 Index, instead of following a manager’s active investment strategy. The S&P

MidCap 400 Index is a popular standard for measuring mid-cap U.S. stock market performance.

Investing Your Money

21

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Small Cap Equity Index Fund

The Small Cap Equity Index Fund seeks long-term capital appreciation. It primarily invests in small companies that tend to be growing

in size as well as having strengthening financial performance. The Fund is diversified across both the growth and value investment

styles. Thus, a portion of the Fund is invested in companies considered to have above-average prospects for growth, while the

remainder of the Fund invests in stocks selling at prices below the overall market average compared to their dividend and future

return profile.

Plan Assets

Plan assets are held in a Trust by State Street Bank and Trust Company, based in Boston, Massachusetts, which serves as both the

trustee and custodian for all the investment funds. By law, Trust assets must be used for the benefit of Plan participants and are not

subject to the claims of any Company creditors. These assets cannot be used by the trustee, the Company, or any other party.

If You Have Investments in the Halliburton Stock Fund Effective January 1, 2007, the Halliburton Stock Fund (“HSF”) was closed to new investments. Plan participants are not allowed to make

new contributions (tax-deferred savings contributions), transfers, or loan repayments into the HSF on or after January 1, 2007.

If you had tax-deferred savings contributions allocated to the HSF prior to January 1, 2007 and have not taken action subsequent to that

date to redirect your contributions to other available funds within the Plan, those contributions have been redirected to the Moderate

Premixed Portfolio. To change your investment allocations, access the Your Benefits Resources Web site at http://resources.hewitt.

com/halliburtonbenefits or call the Halliburton Benefits Center’s automated telephone system at 1-800-535-8130. If outside the

U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-free number).

In addition, beginning January 1, 2007, the Company is providing a three-year “sunset period” for Plan participants who have a balance

in the HSF. A sunset period allows Plan participants to move their stock fund balance into other funds within the Plan over a defined

period of time. During the sunset period, you are encouraged to begin moving your HSF balance to another investment fund. Any

balance remaining in the HSF at the conclusion of the three-year sunset period (December 31, 2009) will automatically be redirected

to another investment fund chosen by the Company. You will receive more information and notices about any redirection before the

end of the sunset period.

TheCompanywillmonitortheHSFduringthesunsetperiodandreservestherighttoimplementperiodictransfersand/orchangeor

accelerate the three-year sunset period at any time. You will receive notice before any such transfer or change.

Prior to January 1, 2007, if you rebalanced your Plan account by moving funds into or out of the HSF, the percentage of your

Plan account balance invested in the HSF was automatically reduced to 15 percent of your portfolio. Effective January 1, 2007,

the Company eliminated this rebalancing requirement to allow more flexibility in moving out of the HSF. As of January 1, 2007,

rebalancing your Plan account will no longer trigger the automatic reduction of your HSF to 15 percent of your total portfolio. This

change allows you to gradually move your money out of the HSF. You may transfer existing balances out of the HSF by accessing the

Your Benefits Resources Web site at http://resources.hewitt.com/halliburtonbenefits or by calling the Halliburton Benefits Center’s

automated telephone system at 1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or

847-883-0702 (not a toll-free number).

Investing Your Money

22

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Note: The Halliburton Stock Fund is not a diversified fund and invests only in Halliburton Company stock (with a minimal

amount of cash and cash equivalents). This Fund invests in only one stock; therefore, the value of the fund can increase

and decrease significantly. If you have investments in the Halliburton Stock Fund, you are strongly encouraged to

carefully review the Company’s public filings with the Security and Exchange Commission, including the Company’s most

recent annual report on Form 10-K and each quarterly report on Form 10-Q.

Dividend Pass-Through

The Halliburton Stock Fund features an Employee Stock Ownership Plan (ESOP). This feature, known within the Company as “Dividend

Pass-through,” permits you to elect to:

• HaveyourshareofeachHalliburtoncommonstockdividendreinvestedinyourHalliburtonStockFundbalance;or

• Receivethedividendincash.

Dividends on Halliburton common stock usually are declared four times a year at the discretion of the Board of Directors. If you

elect to reinvest your dividends, or if you do not have an election on file as of the close of business on the business day prior to the

ex-dividend date, your dividends automatically will be reinvested in your Halliburton Stock Fund balance. Reinvested dividends will be

credited as tax-deferred earnings and will continue to grow tax-deferred until they are withdrawn.

If you elect to receive a dividend in cash, you will receive a check seven to 10 business days after the dividend payable date. Cash

paymentsaresubjecttoincometaxesintheyearyoureceivethem;however,theyarenotsubjecttothe10%IRStaxpenaltythat

appliestoearlyPlandistributions.Notaxeswillbewithheldfromdividendchecks;youwillberesponsibleforanytaxliabilitywhenyou

file your income tax return.

You can make or change your election at any time via the Your Benefits Resources Web site at http://resources.hewitt.com/

halliburtonbenefits or by calling the Halliburton Benefits Center at 1-800-535-8130 and speaking with a representative. If outside

the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-free number).

Understanding Risk and ReturnAny investment comes with some level of market risk (the likelihood that an investment will go up or down in value, especially over

the short term), but it also comes with the potential for return. All 12 current investment fund options and the closed Halliburton

Stock Fund are plotted on the graph below to show the varying degrees of market risk and potential return offered by the fund options

in relation to one another. Investments with lower market risk may help protect you against the volatility of the stock market. But,

historically, funds with higher market risk have offered the potential for greater returns.

Investing Your Money

23

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Transaction Fees and Expenses

There are no transaction fees or expenses (e.g., commissions, sales loads, deferred sales charges, and redemption or exchange fees)

associated with the purchase or sale of shares or units of investment funds offered under the Plan. However, each investment fund

contains other fees and expenses, which are reflected in the fund’s net investment return. Detailed information regarding these fees

and expenses is set forth in the Plan’s Investment Highlights booklet. You may request a copy of this booklet by calling the Halliburton

Benefits Center at 1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-

0702 (not a toll-free number). Detailed fund information also appears on the Your Benefits Resources Web site at http://resources.

hewitt.com/halliburtonbenefits.

Voting Rights

Except for investments in the Halliburton Stock Fund, voting and similar rights associated with shares of the investment funds held in

your accounts will be exercised by the Plan’s trustee and will not be passed to you.

VotingandsimilarrightsassociatedwiththeHalliburtonStockFundwillbepassedthroughtoparticipantsinvestedintheHalliburton

Stock Fund. Any shares of Halliburton Company stock not voted by such participants will be voted by the Plan’s trustee. Procedures

have been designed to safeguard the confidentiality of any participant’s or beneficiary’s rights with respect to the participant’s

or beneficiary’s shares of Halliburton Company stock held under the Plan, including the right to sell, hold, or exercise voting, or

similar rights. In addition, access to your decisions to sell or hold Halliburton Company stock are restricted to those assisting in the

administration of the Plan. The Halliburton Company Investment Committee is responsible for ensuring that these procedures are

being followed. If this Committee determines that a situation has potential for undue influence by your employer with respect to

your rights as a shareholder of the Company, the Committee will appoint an independent fiduciary to perform such activities as are

Investing Your Money

24

EX

PE

CTE

D R

ATE

OF

RE

TUR

NLo

w R

etur

nH

igh

Ret

urn

Halliburton Stock Fund

Small Cap Equity Index Fund

Mid Cap Equity Index Fund

Non-US Equity Fund

Large Cap Growth Equity Fund

Large Cap Value Equity Fund

S&P 500 Index Fund

Balanced Fund

Bond Index Fund

EXPECTED RISK LEVELLow Risk High Risk

Premixe

d Port

folios

Single

Focus

Funds

Stable

Value

Premixe

d

Portfol

io

Conse

rvativ

e

Premixe

d

Portfol

io

Modera

te

Premixe

d

Portfol

io

Aggres

sive

Premixe

d

Portfol

io

EX

PE

CTE

D R

ATE

OF

RE

TUR

NLo

w R

etur

nH

igh

Ret

urn

Halliburton Stock Fund

Small Cap Equity Index Fund

Mid Cap Equity Index Fund

Non-US Equity Fund

Large Cap Growth Equity Fund

Large Cap Value Equity Fund

S&P 500 Index Fund

Balanced Fund

Bond Index Fund

EXPECTED RISK LEVELLow Risk High Risk

Premixe

d Port

folios

Single

Focus

Funds

Stable

Value

Premixe

d

Portfol

io

Conse

rvativ

e

Premixe

d

Portfol

io

Modera

te

Premixe

d

Portfol

io

Aggres

sive

Premixe

d

Portfol

io

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

necessary to prevent undue influence. These situations may include tender offers, exchange offers, or contested Board of Director

elections. You will be notified of such appointment and of the name, address and phone number of the independent fiduciary. If

you have questions about this procedure, you may contact the Investment Committee at the Master Trust Office, 10200 Bellaire Blvd,

Houston, Texas 77072, or call 281-575-3540.

Information Available Upon Request

Upon request, you may receive (based on the latest information available to the Plan):

• AdescriptionoftheannualoperatingexpensesofeachinvestmentfundavailableunderthePlan(e.g.,investmentmanagement

fees, administrative fees, transaction costs), which reduce the rate of return you receive, and the aggregate amount of such

expensesexpressedasapercentageofaveragenetassetsoftheinvestmentfund;

• Copiesofanyprospectuses,financialstatementsandreports,andofanyothermaterialsrelatingtotheinvestmentfundsavailable

underthePlan,totheextentsuchinformationisprovidedtothePlan;

• Alistofassetscomprisingtheportfolioofcertaininvestmentfundsconstituting“Planassets”(generallycollectiveorcommontrust

funds, but not mutual funds) available under the Plan, the value of each such asset (or the proportion of the investment alternative

which it comprises) and, with respect to each such asset which is a fixed-rate investment contract issued by a bank or savings and

loanassociation,thenameoftheissuer,termofthecontract,andspecifiedrateofreturn;

• Informationconcerningthevalueofsharesorunits in each investment fund offered under the Plan, as well as the past and current

investmentperformanceofeachfunddeterminednetofexpenses;and

• Informationconcerningthevalueofsharesorunits in each investment fund offered under the Plan held in your accounts.

If you would like to receive any of the above information, please contact the Halliburton Benefits Center at 1-800-535-8130. If

outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not a toll-free number).

It is intended that the Plan shall constitute a plan described in Section 404(c) of the Employee Retirement Income Security Act of 1974

and Title 29 of the Code of Federal Regulations Section 2550.404(c)-1, and that the fiduciaries of the Plan may be relieved of liability for

any losses that are the direct and necessary result of investment instructions given by a Plan participant or beneficiary.

Investment Transfer PolicyEffective January 1, 2006, the Halliburton Investment Committee adopted a Transfer Policy, which places waiting periods on transfers

and reallocations into and out of all Plan funds.

• 20-day Incoming Restriction. Forallofthefundsandportfolios,excepttheStableValuePremixedPortfolio,ifyoumakeatransfer

or a fund reallocation out of a fund, you cannot transfer money into that same fund for 20 calendar days. For example, if on

January 1 you make a transfer or a fund reallocation out of the Mid Cap Equity Fund, you will have to wait until January 21 to make

any transfers or reallocations into that fund. Each time a transfer or fund reallocation is made out of a fund, the waiting period resets

to the date of the latest transaction. Therefore, if you decide on January 10 that you want to transfer additional money out of the

Mid Cap Equity Fund, you will have to wait until January 31 to make any transactions back into that fund.

Investing Your Money

25

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

• 20-day Outgoing Restriction. ThepolicygoverningtheStableValuePremixedPortfolioworksdifferently.Ifmoneyistransferred

orfundsarereallocatedintotheStableValuePremixedPortfolio,thenumberofunits that money represented on the day of the

transaction are locked in and cannot be transferred out of the Portfolio for 20 calendar days. For example, if on January 1 you

transfer$150intotheStableValuePremixedPortfolioandeach$15equalsoneunit, then you have added 10 units to your portfolio

and those 10 units cannot be transferred out for 20 calendar days. However, any balance in this portfolio prior to the transaction is

not subject to the waiting periods.

Inordertoprovideprotectionagainstpossiblemarketdownturns,youcanalwaysreallocateortransfermoneyintotheStableValue

Premixed Portfolio from other Premixed Portfolios or Single Focus Funds.

Keeping Track of Your AccountYour account will be valued on a daily basis. You can access current information about your account via the Your Benefits Resources

Web site at http://resources.hewitt.com/halliburtonbenefits or by calling the Halliburton Benefits Center’s automated telephone

system at 1-800-535-8130. If outside the U.S., call 866-373-3422 (toll-free using the AT&T access code) or 847-883-0702 (not

a toll-free number).

You can access:

• Youraccountandfundbalancesasofthepriorbusinessday’scloseofmarket;

• Yourinvestment elections;

• Yoursavingscontribution rate; and

• Ratesofreturnforeachinvestmentfund.RatesareavailableontheYour Benefits Resources Web site for the past day, four weeks,

year-to-date and trailing three-, five-, and 10-year periods as of December 31st of the prior year. The automated telephone system

tracks returns daily, for the past four weeks and year-to-date.

At any time, you can request an account statement via the Your Benefits Resources Web site or the automated telephone system that

will show current quarter-to-date activity or prior quarter activity.

Typically, each business day after close of the U.S. stock market, your account balance will be updated and any transactions will be

processed. There may be times when daily valuation of your account may not be possible due to unexpected circumstances. If this

happens, your account will be updated as soon as administratively possible.

Investing Your Money

26

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Loans, Withdrawals and Distributions

27

Halliburton Retirement & Savings Plan Summary Plan Description (SPD) January 2009

Although the Plan is designed to allow you to save for your future financial security, the Company realizes that you may need access to

some of your savings when certain situations arise. The following matrix outlines loan, withdrawal and distribution options under the

Plan.

LOAN WITHDRAWAL DISTRIBUTIONWith a loan, you borrow from your account balance in accordance with Plan rules while you are an active employee or on approved leave of absence.

An in-service withdrawal is a withdrawal of all or part of your Plan account while you are an active employee.

A distribution is a payment of your vested account balance when you retire or terminate employment with the Company.

You repay the amount of the loan, plus interest, to your Plan account through payroll deduc-tion.

Withdrawals are limited to the circumstances described in the “Withdrawals” sections.

Payment may be in one of the forms described in either the “Withdrawals” or “Distributions” sections.