halifax+gateway+council+strategic+plan+200602

TRANSCRIPT

s t r a t e g i ct r a n s p o r t a t i o n& t o u r i s ms o l u t i o n s

P r e p a r e d i n a s s o c i a t i o n w i t h

a n d

Halifax Gateway Council Strategic Plan

Prepared for

November 2005

Final Report

Halifax Gateway Council Strategic Plan Page ii

November 2005

Table of Contents

Executive Summary .......................................................................................................................iii

1.0 Introduction ........................................................................................................................11.1 Background............................................................................................................................ 11.2 Purpose and Scope ............................................................................................................... 2

2.0 Halifax Gateway Today ......................................................................................................32.1 Airport .................................................................................................................................... 32.2 Port – Shipping .................................................................................................................... 152.3 Port – Cruise........................................................................................................................ 262.4 Ground Transportation......................................................................................................... 33

3.0 Changing Environment....................................................................................................453.1 Global Marketplace.............................................................................................................. 453.2 Government Policy .............................................................................................................. 493.3 Aviation Trends.................................................................................................................... 683.4 Shipping Trends................................................................................................................... 803.5 Cruise Trends ...................................................................................................................... 873.6 Ground Transportation Trends............................................................................................. 96

4.0 Strategic Assessment......................................................................................................984.1 SWOT Analysis.................................................................................................................... 984.2 Halifax Gateway Potential.................................................................................................. 1024.3 Vision ................................................................................................................................. 1054.4 Regional Economic Impact ................................................................................................ 1064.5 Key Strategic Issues .......................................................................................................... 1064.6 Best Practices.................................................................................................................... 113

5.0 Action Plan .....................................................................................................................123

Halifax Gateway Council Strategic Plan Page iii

November 2005

Executive Summary

The Halifax Gateway Council was established in 2004 with the purpose of providing meaningful input intolocal, provincial, and federal policy discussions on improving the competitiveness and efficiency of theHalifax Gateway (in the future, efforts will be undertaken to examine how the gateway council concept canbe broadened to include all four Atlantic provinces). The purpose of this Strategic Plan is to develop a newvision for the Halifax Gateway and establish a detailed Action Plan to achieve it. This plan is based on theextensive research and analysis undertaken during the course of the assignment, as well as on feedbackobtained during consultations with over 20 industry organisations and government agencies.

The Halifax Gateway is an important transportation complex on North America’s east coast for themovement of international cargo and passengers. The region’s Gateway infrastructure is made up of thePort of Halifax, the Halifax International Airport, and the rail and road infrastructure connecting thesefacilities to each other, and to the east-west and north-south road and rail corridors. Presently, the Gatewayhandles roughly 14 million metric tonnes of cargo, over 3 million air passengers, and approximately 200,000cruise passengers. The Gateway is also a major generator of employment in Nova Scotia with an estimated11,930 jobs generated by Gateway-related activities, equivalent to 11,200 person years of employment.

Although global developments are intensifying competition amongst gateways, they are also generatingsignificant opportunities for growth in the transportation industry by expanding international trade. With acapacity crisis occurring at west coast North American ports, and the expected explosion of the Chinese andIndian economies in the years ahead, the Halifax region is well positioned to take advantage of emergingmarket opportunities for the economic benefit and social wellbeing of Atlantic Canada.

The Halifax Gateway has several strengths which positions it well for future growth. It also faces severalweaknesses that must be addressed if it is to retain and expand its share of the market.

Strengths Weaknesses

Strategic location

Proximity to large market (U.S. east coast)

Well developed infrastructure

Land availability for development

Skilled labour pool

Technology (Smart City)

Natural attractions

Marine access and conditions

Jones Act exemption

Unrestricted airport operations

Surplus capacity

Strong stakeholder alignment

Low population density

Local economy

Distance to inland markets

Low market awareness

U.S.-Canada border

Lack of air capacity to key markets

Limited hotel room inventory in high season

Less efficient than east coast port competitors

Canadian dollar exchange rate

Regulatory/bureaucratic processes

Some infrastructure deficiencies

Lack of rail competition

Limited funding capacity by all levels of government

Lack of political influence

Halifax Gateway Council Strategic Plan Page iv

November 2005

There is an opportunity for Halifax to increase its gateway market position. The region benefits from astrategic geographic location (astride major trade corridors and proximate to the large U.S. market),favourable year round marine conditions, and well-developed infrastructure with surplus capacity.

The following vision is recommended to guide the strategic development of the Halifax Gateway:

To become North America’s preferred eastern gatewayfor the economic and social benefit of Atlantic Canada

Achieving this vision would result in the following activity:

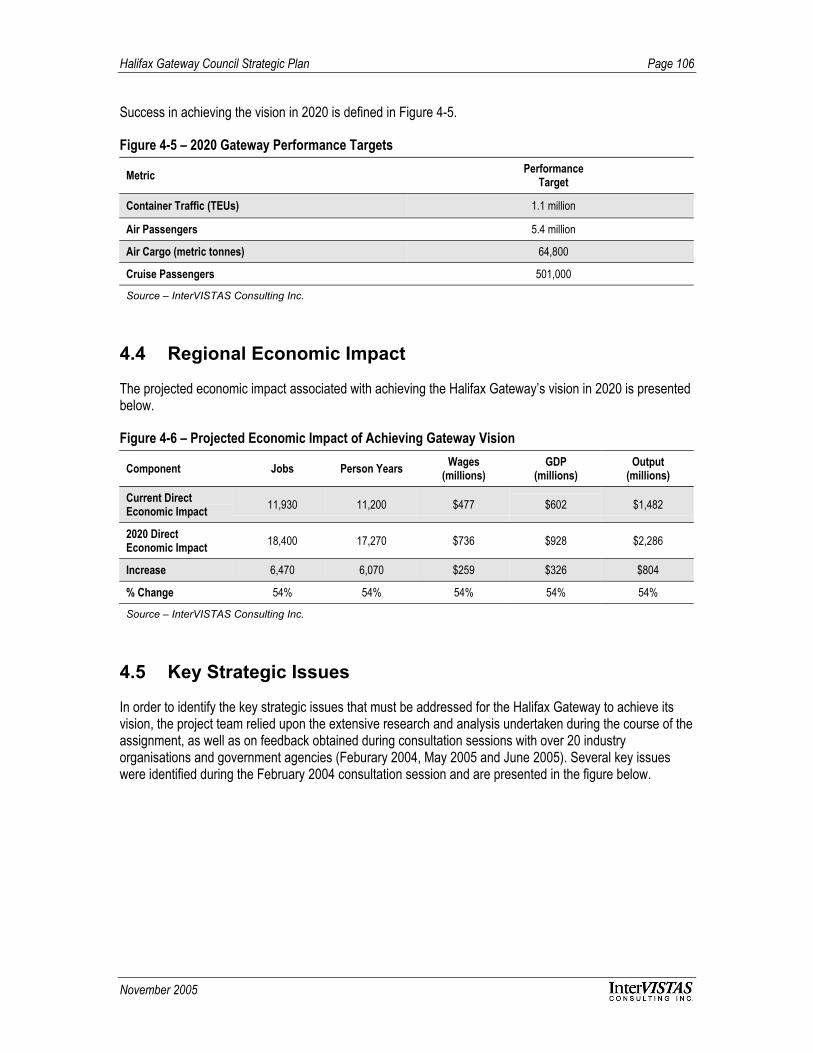

Metric PerformanceTarget

Container Traffic (TEUs) 1.1 million

Air Passengers 5.4 million

Air Cargo (metric tonnes) 64,800

Cruise Passengers 501,000

The projected economic impact associated with achieving the vision in 2020 is:

Component Jobs Person Years Wages(millions)

GDP(millions)

Output(millions)

Current DirectEconomic Impact 11,930 11,200 $477 $602 $1,482

2020 DirectEconomic Impact 18,400 17,270 $736 $928 $2,286

Increase 6,470 6,070 $259 $326 $804

% Change 54% 54% 54% 54% 54%

In order for the Gateway to realise its vision, the following four issues must be addressed:

Government policy – government policy was identified as a key area that needs to be addressed inorder to expand business through the Gateway;

Infrastructure development and funding – Gateway infrastructure must be expanded and improved tobetter serve trade and industry;

Market development – marketing and business development activities will play a critical role in thecontinued development of the Halifax Gateway; and

Economic and industrial development – additional economic growth is required in the region for theGateway to prosper.

Halifax Gateway Council Strategic Plan Page v

November 2005

A detailed Action Plan has been developed to address each of these issues. The plan, provided below,contains four strategies and roughly thirty specific initiatives to be completed during the next five years tobuild the Gateway and achieve the ambitious vision described above. Success will only accrue to theGateway, however, if industry and government work together as partners towards the common goal ofincreasing the competitiveness of the region’s international trade and tourism industries through thedevelopment of a better transportation system.

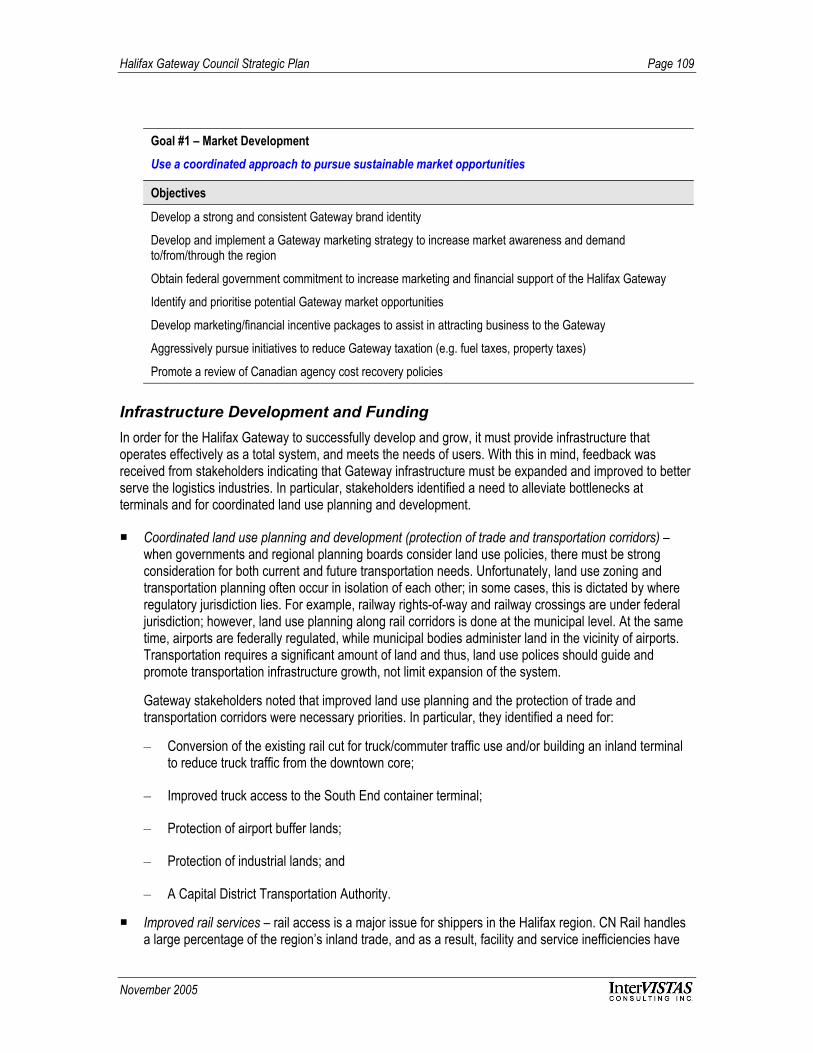

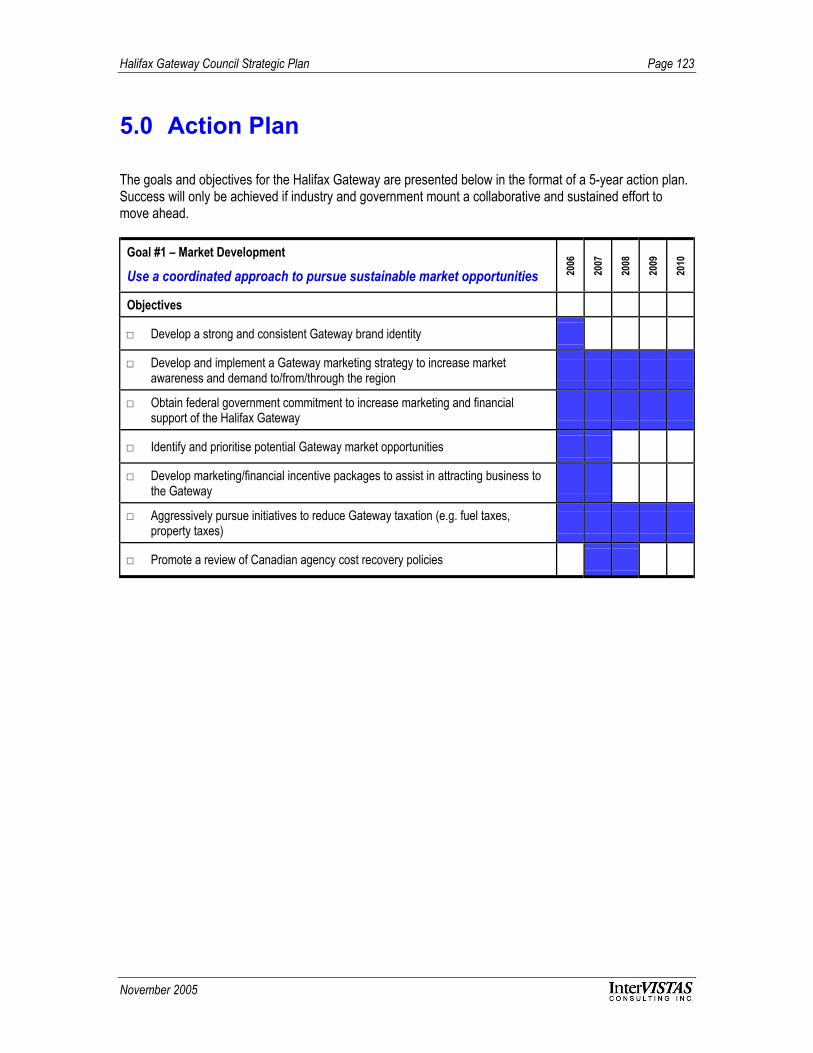

Goal #1 – Market Development

Use a coordinated approach to pursue sustainable market opportunities 2006

2007

2008

2009

2010

Objectives

□ Develop a strong and consistent Gateway brand identity

□ Develop and implement a Gateway marketing strategy to increase marketawareness and demand to/from/through the region

□ Obtain federal government commitment to increase marketing and financialsupport of the Halifax Gateway

□ Identify and prioritise potential Gateway market opportunities

□ Develop marketing/financial incentive packages to assist in attracting business tothe Gateway

□ Aggressively pursue initiatives to reduce Gateway taxation (e.g. fuel taxes,property taxes)

□ Promote a review of Canadian agency cost recovery policies

Halifax Gateway Council Strategic Plan Page vi

November 2005

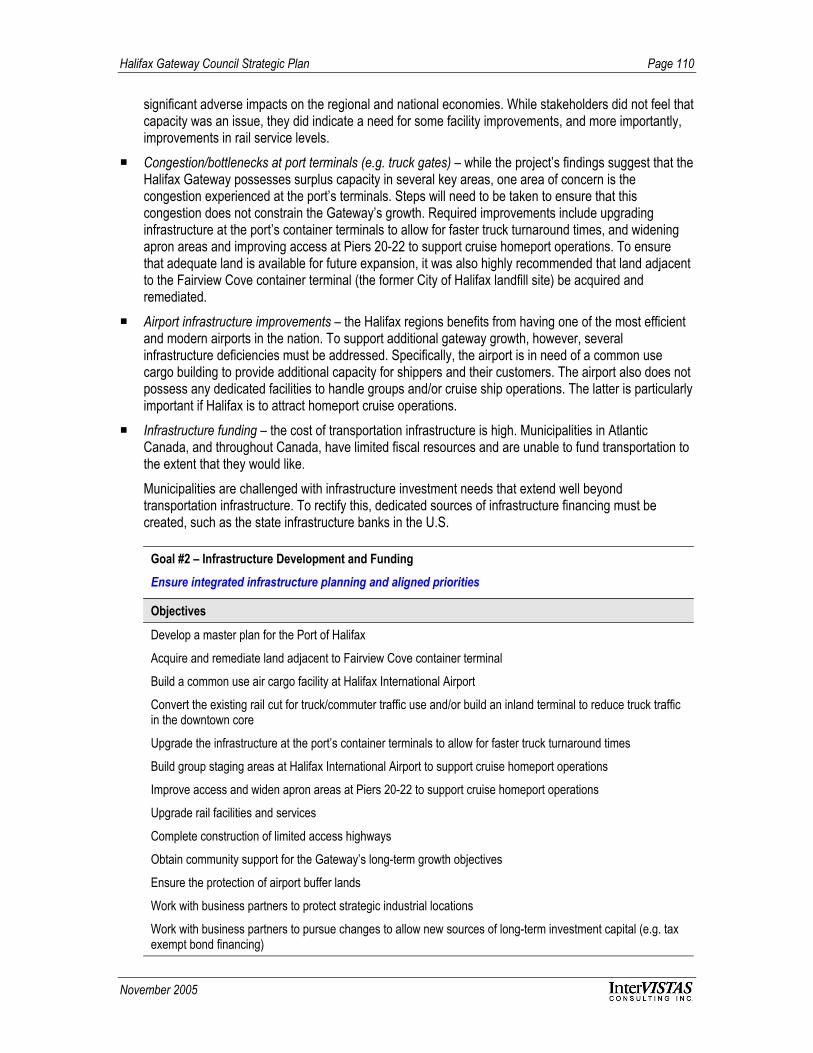

Goal #2 – Infrastructure Development and Funding

Ensure integrated infrastructure planning and aligned priorities 2006

2007

2008

2009

2010

Objectives

□ Develop a master plan for the Port of Halifax

□ Acquire and remediate land adjacent to Fairview Cove container terminal

□ Build a common use air cargo facility at Halifax International Airport

□ Convert the existing rail cut for truck/commuter traffic use and/or build an inlandterminal to reduce truck traffic in the downtown core

□ Upgrade the infrastructure at the port’s container terminals to allow for faster truckturnaround times

□ Build group staging areas at Halifax International Airport to support cruisehomeport operations

□ Improve access and widen apron areas at Piers 20-22 to support cruise homeportoperations

□ Upgrade rail facilities and services

□ Complete construction of limited access highways

□ Obtain community support for the Gateway’s long-term growth objectives

□ Ensure the protection of airport buffer lands

□ Work with business partners to protect strategic industrial locations

□ Work with business partners to pursue changes to allow new sources of long-terminvestment capital (e.g. tax exempt bond financing)

Halifax Gateway Council Strategic Plan Page vii

November 2005

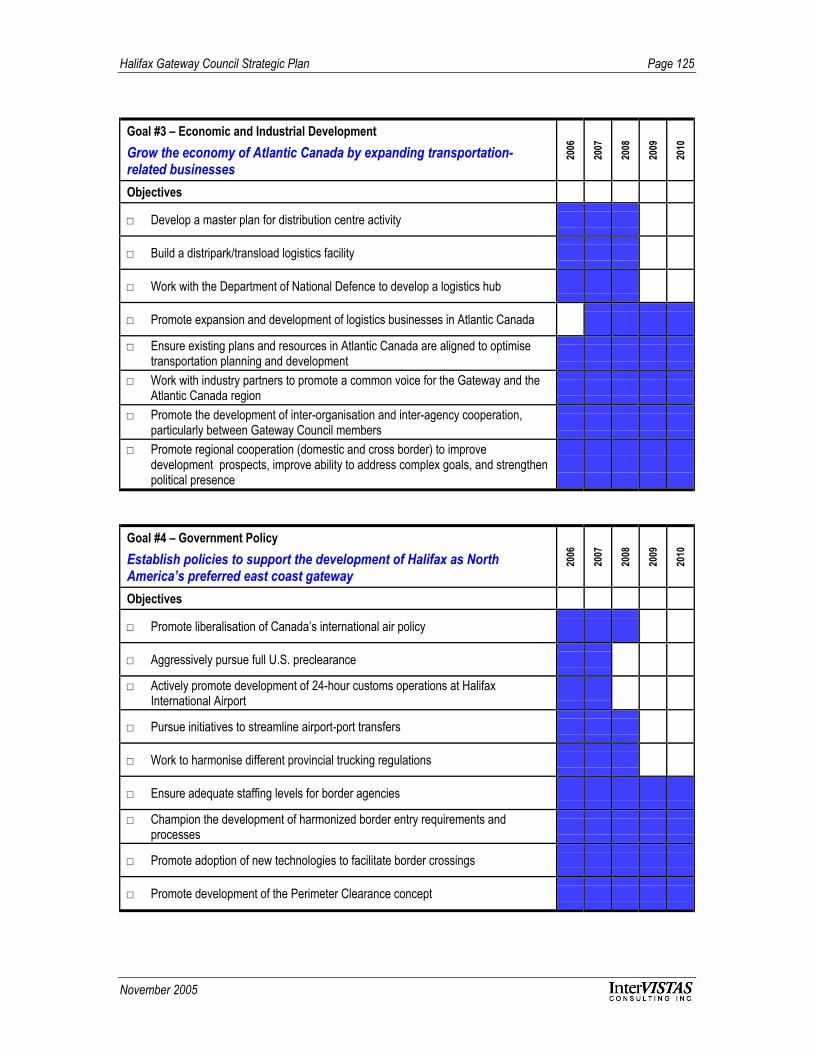

Goal #3 – Economic and Industrial DevelopmentGrow the economy of Atlantic Canada by expanding transportation-related businesses

2006

2007

2008

2009

2010

Objectives

□ Develop a master plan for distribution centre activity

□ Build a distripark/transload logistics facility

□ Work with the Department of National Defence to develop a logistics hub

□ Promote expansion and development of logistics businesses in Atlantic Canada

□ Ensure existing plans and resources in Atlantic Canada are aligned to optimisetransportation planning and development

□ Work with industry partners to promote a common voice for the Gateway and theAtlantic Canada region

□ Promote the development of inter-organisation and inter-agency cooperation,particularly between Gateway Council members

□ Promote regional cooperation (domestic and cross border) to improvedevelopment prospects, improve ability to address complex goals, and strengthenpolitical presence

Goal #4 – Government PolicyEstablish policies to support the development of Halifax as NorthAmerica’s preferred east coast gateway

2006

2007

2008

2009

2010

Objectives

□ Promote liberalisation of Canada’s international air policy

□ Aggressively pursue full U.S. preclearance

□ Actively promote development of 24-hour customs operations at HalifaxInternational Airport

□ Pursue initiatives to streamline airport-port transfers

□ Work to harmonise different provincial trucking regulations

□ Ensure adequate staffing levels for border agencies

□ Champion the development of harmonized border entry requirements andprocesses

□ Promote adoption of new technologies to facilitate border crossings

□ Promote development of the Perimeter Clearance concept

Halifax Gateway Council Strategic Plan Page 1

November 2005

1.0 Introduction

1.1 Background

With an excellent airport and modern port infrastructure, Halifax is an international gateway to the world.Halifax International Airport is one of Canada’s fastest growing airports and the Port of Halifax is Canada’sthird largest container port. In addition, Halifax is a major origin and destination point in Atlantic Canada forboth rail and trucking. With a capacity crisis occurring at west coast North American ports, and the expectedexplosion of the Chinese and Indian economies in the years ahead, the time is ripe to take proactive actionto further develop the Halifax Gateway for the economic and social benefit and wellbeing of Atlantic Canada.

To realize its true potential, the Halifax Gateway will need to deal with the real competition posed by severalCanadian and U.S. airports and ports, including Toronto, Montreal, New York, and Boston. In addition, theGateway and its transportation partners in Halifax will need to address several key issues, includinggovernment policy, infrastructure development and funding, market development, and economic andindustrial development in the region.

As a multimodal transportation hub, the Gateway plays a critical role in the economy of Atlantic Canada.The Halifax Gateway Council was established in 2004 with the purpose of providing meaningful input intofederal, provincial, and local region policy discussions on improving the competitiveness and efficiency ofthe Halifax Gateway. Gateway Council members include:

Atlantic Container Line

Air Canada Jazz

CanJet Airlines

CN Rail

Armour Transportation Group

Halifax International Airport Authority

Halifax Port Authority

Destination Halifax

Greater Halifax Partnership

Halifax Chamber of Commerce

Halifax Regional Municipality

Nova Scotia Business Inc.

Nova Scotia Office of EconomicDevelopment

Nova Scotia Department of Transportationand Public Works

Transport Canada

Atlantic Canada Opportunities Agency

Going forward, efforts will be undertaken to examine how the gateway council concept can be broadened toinclude all four Atlantic provinces (Nova Scotia, New Brunswick, Prince Edward Island, and Newfoundland).

Halifax Gateway Council Strategic Plan Page 2

November 2005

1.2 Purpose and Scope

InterVISTAS Consulting Inc. (InterVISTAS), in association with Bermello, Ajamil & Partners Inc. (B&A) andassociate consultant Patrick Morin, was retained by the Halifax Gateway Council to develop a five-yearstrategic plan that would establish a vision for the Gateway, and develop a clear set of priorities and policyinitiatives. The Executive Director of the Gateway Council, James Frost, also worked on this assignmentand made significant contributions to the project.

The project team was guided by a Steering Committee that provided input into the assignment, ensured theco-ordination and support of critical departments and agencies, and provided information as required. ThisSteering Committee was composed of:

James Frost, Halifax Gateway Council;

Jill McLean, Halifax Port Authority;

Alastair Cox, Halifax International Airport Authority;

Fred Morley/Ruth Blades, Greater Halifax Partnership; and

Bill MacDonald, Atlantic Canada Opportunities Agency.

The development of this Plan involved a number of key components, including market and industry analysis,a strategic assessment of the Gateway, and a planning workshop with members of the Gateway Council.

Halifax Gateway Council Strategic Plan Page 3

November 2005

2.0 Halifax Gateway Today

The Halifax Gateway provides the citizens and businesses of Atlantic Canada with a variety of aviation,maritime, and ground transportation services. The Gateway also contributes significantly to the regional andnational economies. The following sections review the basic characteristics – facilities, traffic levels,services, and market/competitive positioning – of the Gateway’s key components (the Port of Halifax, theHalifax International Airport, and the ground transportation services/facilities in the region).

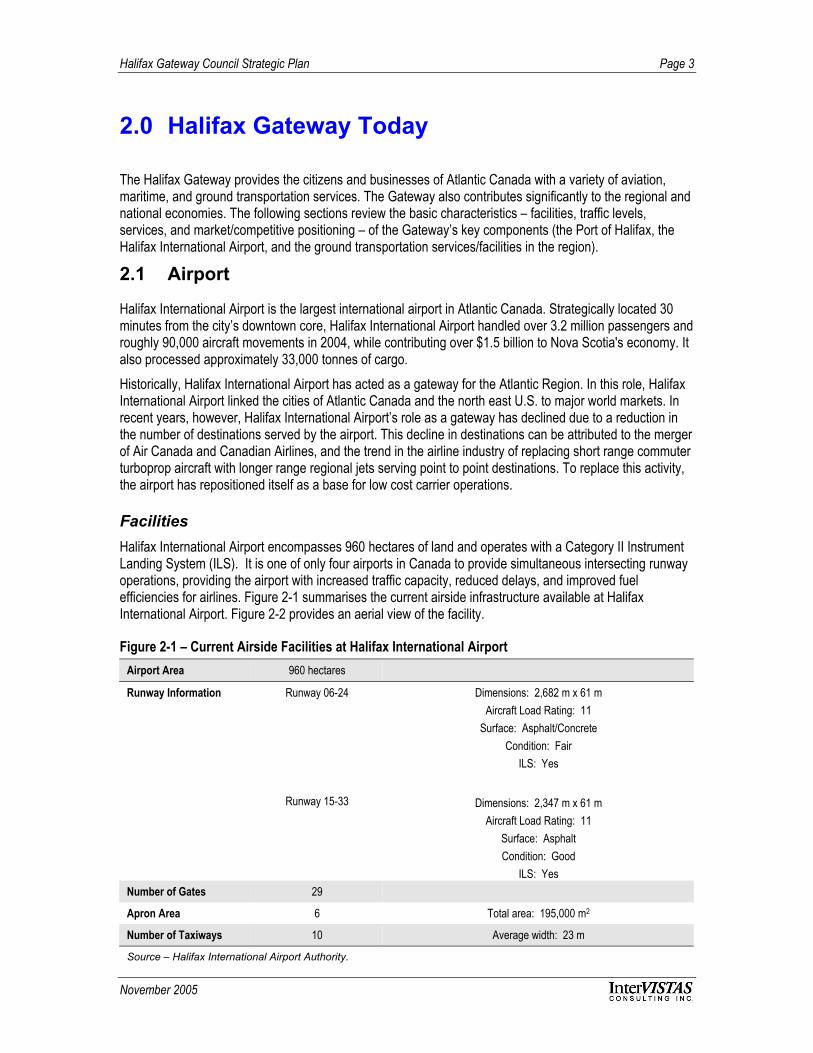

2.1 Airport

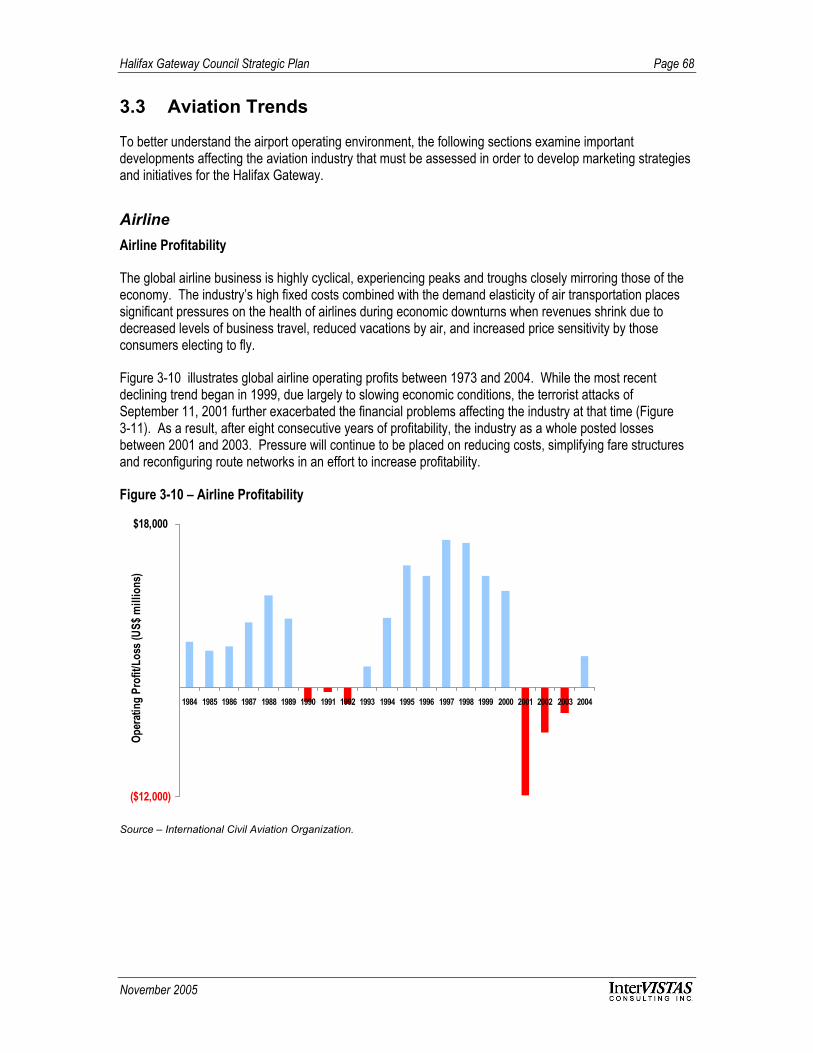

Halifax International Airport is the largest international airport in Atlantic Canada. Strategically located 30minutes from the city’s downtown core, Halifax International Airport handled over 3.2 million passengers androughly 90,000 aircraft movements in 2004, while contributing over $1.5 billion to Nova Scotia's economy. Italso processed approximately 33,000 tonnes of cargo.Historically, Halifax International Airport has acted as a gateway for the Atlantic Region. In this role, HalifaxInternational Airport linked the cities of Atlantic Canada and the north east U.S. to major world markets. Inrecent years, however, Halifax International Airport’s role as a gateway has declined due to a reduction inthe number of destinations served by the airport. This decline in destinations can be attributed to the mergerof Air Canada and Canadian Airlines, and the trend in the airline industry of replacing short range commuterturboprop aircraft with longer range regional jets serving point to point destinations. To replace this activity,the airport has repositioned itself as a base for low cost carrier operations.

FacilitiesHalifax International Airport encompasses 960 hectares of land and operates with a Category II InstrumentLanding System (ILS). It is one of only four airports in Canada to provide simultaneous intersecting runwayoperations, providing the airport with increased traffic capacity, reduced delays, and improved fuelefficiencies for airlines. Figure 2-1 summarises the current airside infrastructure available at HalifaxInternational Airport. Figure 2-2 provides an aerial view of the facility.

Figure 2-1 – Current Airside Facilities at Halifax International AirportAirport Area 960 hectares

Runway Information Runway 06-24

Runway 15-33

Dimensions: 2,682 m x 61 mAircraft Load Rating: 11

Surface: Asphalt/ConcreteCondition: Fair

ILS: Yes

Dimensions: 2,347 m x 61 mAircraft Load Rating: 11

Surface: AsphaltCondition: Good

ILS: YesNumber of Gates 29

Apron Area 6 Total area: 195,000 m2

Number of Taxiways 10 Average width: 23 m

Source – Halifax International Airport Authority.

Halifax Gateway Council Strategic Plan Page 4

November 2005

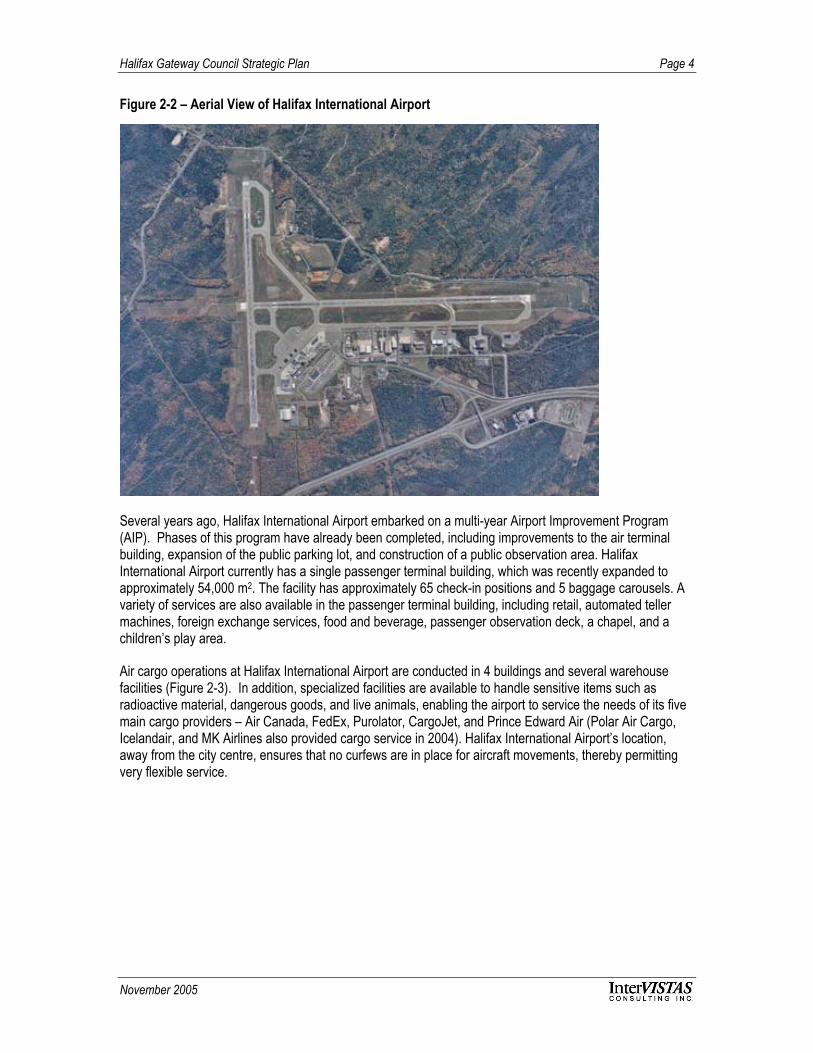

Figure 2-2 – Aerial View of Halifax International Airport

Several years ago, Halifax International Airport embarked on a multi-year Airport Improvement Program(AIP). Phases of this program have already been completed, including improvements to the air terminalbuilding, expansion of the public parking lot, and construction of a public observation area. HalifaxInternational Airport currently has a single passenger terminal building, which was recently expanded toapproximately 54,000 m2. The facility has approximately 65 check-in positions and 5 baggage carousels. Avariety of services are also available in the passenger terminal building, including retail, automated tellermachines, foreign exchange services, food and beverage, passenger observation deck, a chapel, and achildren’s play area.

Air cargo operations at Halifax International Airport are conducted in 4 buildings and several warehousefacilities (Figure 2-3). In addition, specialized facilities are available to handle sensitive items such asradioactive material, dangerous goods, and live animals, enabling the airport to service the needs of its fivemain cargo providers – Air Canada, FedEx, Purolator, CargoJet, and Prince Edward Air (Polar Air Cargo,Icelandair, and MK Airlines also provided cargo service in 2004). Halifax International Airport’s location,away from the city centre, ensures that no curfews are in place for aircraft movements, thereby permittingvery flexible service.

Halifax Gateway Council Strategic Plan Page 5

November 2005

Figure 2-3 – Air Cargo Facilities at Halifax International AirportNumber of Terminals 4

Warehouse Facilities 110,051 m2

(including bonded warehouse space)

Special Services

Aircraft Maintenance

Mechanical Handling

Health Officials

X-Ray Equipment

Express/Courier Centre

Special Storage Facilities

Heated Storage

Air-Conditioned Storage

Refrigerated Storage

Animal Quarantine

Fresh Meat Inspection

Dangerous Goods

Radioactive Goods

Operational Curfew No

Source – Halifax International Airport Authority and A-Z World Airports Guide.

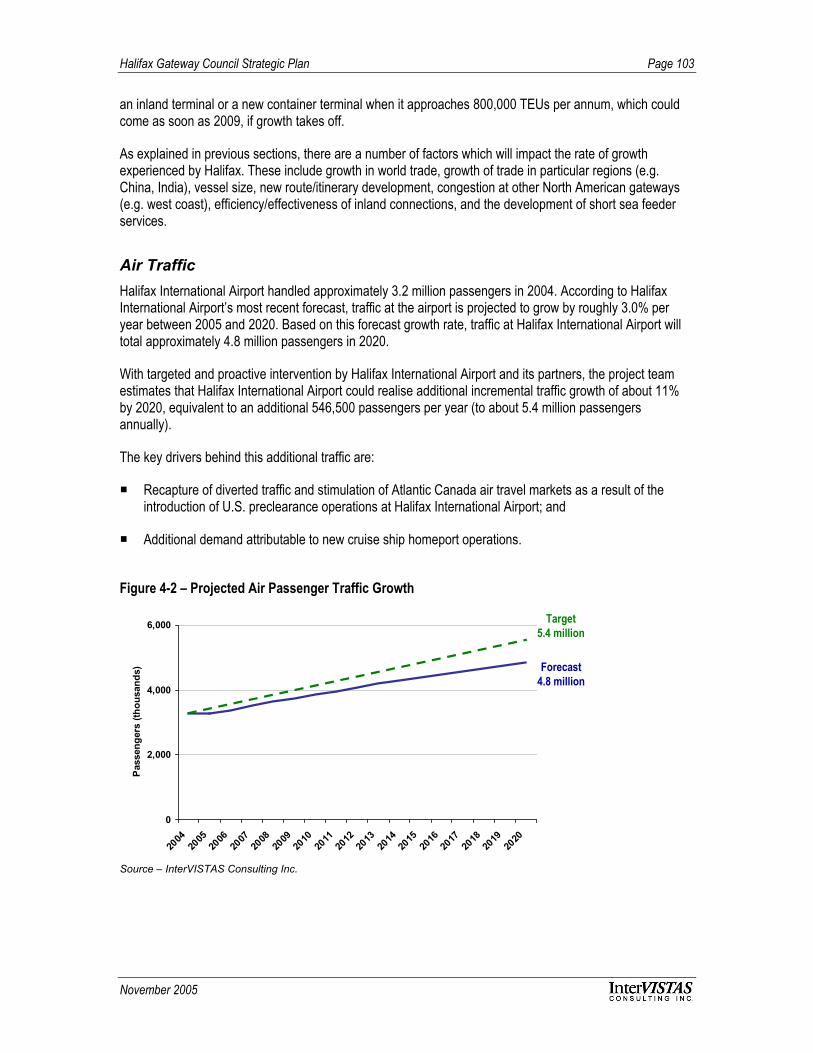

TrafficPassenger traffic has grown steadily at Halifax International Airport during the past 10 years, with theexception of the period between 2000 and 2001 (Figure 2-4). During the latter period, traffic at the airport fellby approximately 8% due to changing economic and industry conditions, and the September 11, 2001terrorist attacks in the U.S. Since 2002, traffic at Halifax International Airport has increased steadily,reaching a record high of 3.2 million passengers in 2004.

Figure 2-4 – Halifax International Airport Passenger Traffic

2,662 2,7452,934

3,089 2,9812,852 2,854

2,973

3,2423,007

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Pas

seng

ers

(thou

sand

s)

Source – Halifax International Airport Authority.

Halifax Gateway Council Strategic Plan Page 6

November 2005

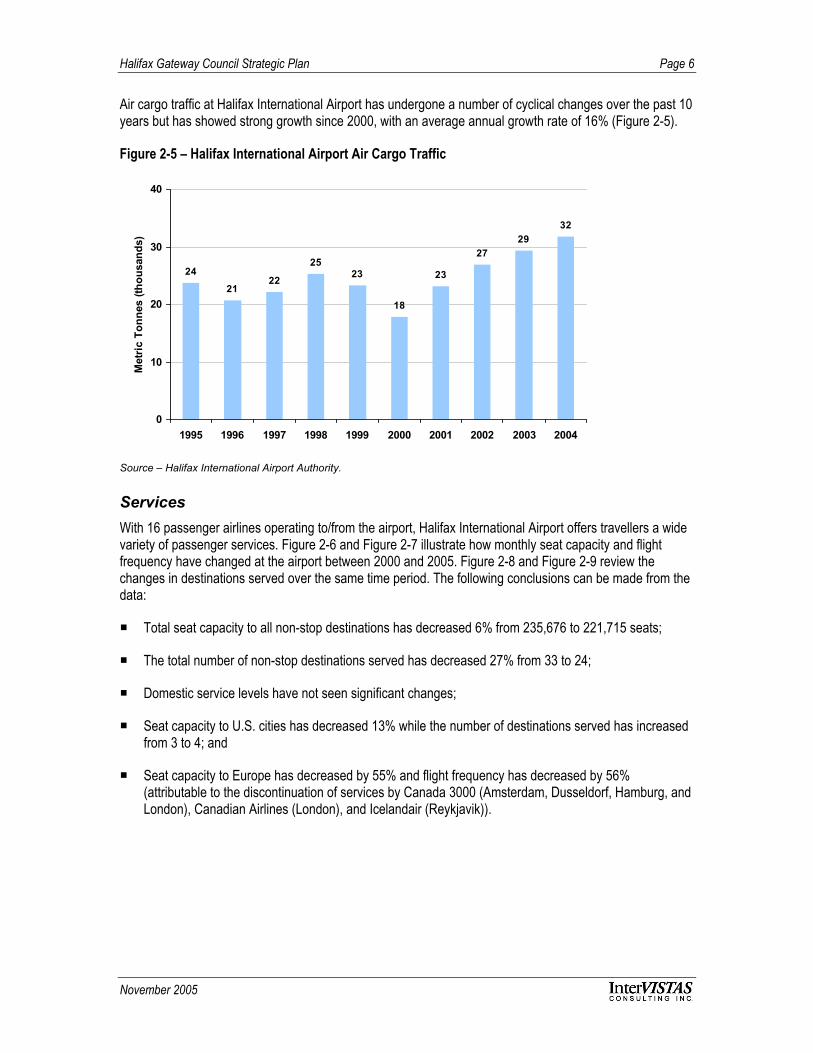

Air cargo traffic at Halifax International Airport has undergone a number of cyclical changes over the past 10years but has showed strong growth since 2000, with an average annual growth rate of 16% (Figure 2-5).

Figure 2-5 – Halifax International Airport Air Cargo Traffic

24

2122 23

18

23

2729

32

25

0

10

20

30

40

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Met

ric T

onne

s (th

ousa

nds)

Source – Halifax International Airport Authority.

ServicesWith 16 passenger airlines operating to/from the airport, Halifax International Airport offers travellers a widevariety of passenger services. Figure 2-6 and Figure 2-7 illustrate how monthly seat capacity and flightfrequency have changed at the airport between 2000 and 2005. Figure 2-8 and Figure 2-9 review thechanges in destinations served over the same time period. The following conclusions can be made from thedata:

Total seat capacity to all non-stop destinations has decreased 6% from 235,676 to 221,715 seats;

The total number of non-stop destinations served has decreased 27% from 33 to 24;

Domestic service levels have not seen significant changes;

Seat capacity to U.S. cities has decreased 13% while the number of destinations served has increasedfrom 3 to 4; and

Seat capacity to Europe has decreased by 55% and flight frequency has decreased by 56%(attributable to the discontinuation of services by Canada 3000 (Amsterdam, Dusseldorf, Hamburg, andLondon), Canadian Airlines (London), and Icelandair (Reykjavik)).

Halifax Gateway Council Strategic Plan Page 7

November 2005

Figure 2-6 – Comparison of Halifax International Airport Seat Capacity by RegionJuly 2000 July 2005 % change

Seats Destinations Seats Destinations Seats Destinations

Canada 193,275 18 190,483 14 - 1% - 22%

U.S. 27,933 3 24,419 4 - 13% + 33%

Europe 13,808 11 6,213 5 - 55% - 55%

Central America 660 1 600 1 - 9% 0%

South America - - - - - -

Asia - - - - - -

Total 235,676 33 221,715 24 - 6% -27%

Source – Planet System.

Figure 2-7 – Comparison of Halifax International Airport Flight Frequency by RegionJuly 2000 July 2005 % change

Canada 2271 2270 -

U.S. 570 478 -16%

Europe 57 25 -56%

Central America 5 5 -

South America - - -

Total 2903 2778 -4%

Source – Planet System.

Figure 2-8 – Halifax International Airport Non-Stop Destinations in 2000 (33 destinations)

YHZ

BDA

BOS

YYC

YYG

YDF

FRA

YFC

GLA

YYR

YGR

LGWYQM

YUL MUC

EWR

YOW

YSJYYT

FSPYJT

AMS

DUS

YEG

YQXHAM

LHRYQB

KEF

YVR

IAD

YQIYYZ

Source – Planet System.

Halifax Gateway Council Strategic Plan Page 8

November 2005

Figure 2-9 – Halifax International Airport Non-Stop Destinations in 2005 (24 destinations)

YHZ

BDA

BOS

YYC

YYG

YDF

FRA

YFC

GLA

YYR

YGR

LGWYQM

YUL MUC

EWR

YOW

YSJYYT

FSPYJT

YHMDET

YYZ

JFK

Source – Planet System.

Air cargo capacity between 2000 and 2005 is reviewed in Figure 2-10. The following observations can bemade:

Halifax International Airport’s overall monthly capacity has decreased 3% from 2,676,000 kilograms in2000 to 2,594,000 kilograms in 2005;

Domestic cargo capacity has decreased by 8% or approximately 162,000 kilograms;

New services have been established to U.S. markets that were not available in 2000 (total cargocapacity to the U.S. was estimated to be 46,000 kilograms in July 2005; this increase in U.S. cargocapacity has offset some of the decreases in domestic capacity); and

Service to Europe increased roughly 5% during this period.

Figure 2-10 – Comparison of Halifax International Airport Air Cargo Capacity July 2000 July 2005

Kilograms % Share Kilograms % share% Change

Canada 1,992,000 74% 1,830,000 68% -8%

U.S. - - 46,000 2% -

Europe 684,000 26% 718,000 27% 5%

Central America - - - - -

South America - - - - -

Asia - - - - -

Total 2,676,000 2,594,000 -3%

Source – Planet System.

Halifax Gateway Council Strategic Plan Page 9

November 2005

Market/Competitive PositionIn its efforts to attract passenger and air cargo traffic, Halifax International Airport competes with otherfacilities in the region. For the purposes of this analysis, Halifax International Airport’s key competitors weredetermined to be Boston Logan International Airport, Toronto Pearson International Airport, Montreal PierreElliot Trudeau International Airport, and Ottawa International Airport (Figure 2-11).

Figure 2-11 – Halifax International Airport Competitors

Halifax

Montreal

BostonToronto

Ottawa

Facilities

The airside infrastructure available at Halifax International Airport and at competing facilities on the eastcoast is displayed in Figure 2-12. The following observations can be drawn:

Halifax International Airport is the smallest airport in terms of land size, just behind Boston;

Halifax International Airport’s longest runway is 2,682 metres in length, which can accommodate aBoeing 777, but is shorter than the longest runways at competing airports; and

Halifax International Airport ranks 5th with respect to gate capacity (29 gates).

Figure 2-12 – Comparison of Airside FacilitiesBoston Toronto Montreal Ottawa Halifax

Airport Area (hectares) 971 1,792 ~2,024 1,821 960

Number of Runways 5 5 3 3 2

Number of Gates 94 84 43 22 29

Longest Runway (m) 3,073 3,368 3,650 3,048 2,682

Source – Individual airports.

Halifax Gateway Council Strategic Plan Page 10

November 2005

The passenger terminal infrastructure available at Halifax International Airport and at competing facilities isdisplayed in Figure 2-13. The following observations can be made:

None of the airports have operating restrictions that would limit their capability to handle late nightservices; and

Halifax International Airport has the lowest number of check-in positions (44 in total).

Figure 2-13 – Comparison of Passenger FacilitiesBoston Toronto Montreal Ottawa Halifax

Number of Terminals 5 3 1 1 1Terminal Size (m2) 600,000+ 500,000+ 190,000+ 62,000 54,000Number ofCheck-In Positions 96 370 190 50 44

Number of BaggageCarousels 14 6 4 5

Operational Curfews No No No No NoTotal Carriers 60 57 28 11 25Source – Individual airports.

The cargo terminal infrastructure available at Halifax International Airport and at competing facilities isdisplayed in Figure 2-14. Halifax International Airport’s competitive position is highlighted below:

Halifax International Airport has the largest warehouse space among the competing airports; and

Halifax International Airport, Boston, and Toronto offer a wide range of services for handling specialisedgoods.

Figure 2-14 – Comparison of Air Cargo FacilitiesComponent Boston Toronto Montreal Ottawa Halifax

Number of Terminals 2 4 4 3 4

Number of All Cargo Airlines 9 10 23 2 6

Warehouse Space (m2) 51,000 82,000 64,000 - 110,051

Total Ramp Space (m2) 156,000 125,000 88,000 - 112,000

Heated Storage Yes Yes Yes Yes Yes

Agricultural Inspection Yes Yes Yes(70 kms away)

- Yes

Air Conditioned Storage Yes Yes Yes Yes

Refrigerated Storage Yes Yes Yes Yes Yes

Animal Quarantine Yes Yes Yes - Yes

Fresh Meat Inspection - Yes Yes Yes Yes

Dangerous Goods Yes Yes Yes Yes Yes

Radioactive Goods Yes Yes Yes Yes Yes

Customs Yes Yes Yes Yes Yes

Source – Individual airports.

Halifax Gateway Council Strategic Plan Page 11

November 2005

Traffic

Figure 2-15 compares total enplaned and deplaned passenger traffic at the competing airports in 2000 and2004. The following observations can be made:

From 2000 to 2004, total enplaned and deplaned passengers at these airports decreased 0.8% from71.6 million to 71,0 million;

Total enplaned and deplaned traffic at Halifax International Airport increased from 3.0 million in 2000 to3.2 million in 2004; and

Halifax International Airport’s market share increased from 4% to 5%.

Figure 2-15 – Comparison of Passenger Traffic

9,415

27,727

3,434

28,930

2,981

8,493

26,143

3,610

28,616

3,242

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Halifax Montreal Toronto Ottawa Boston

Pas

seng

ers

(thou

sand

s)

2000 2004

Source – Planet System.

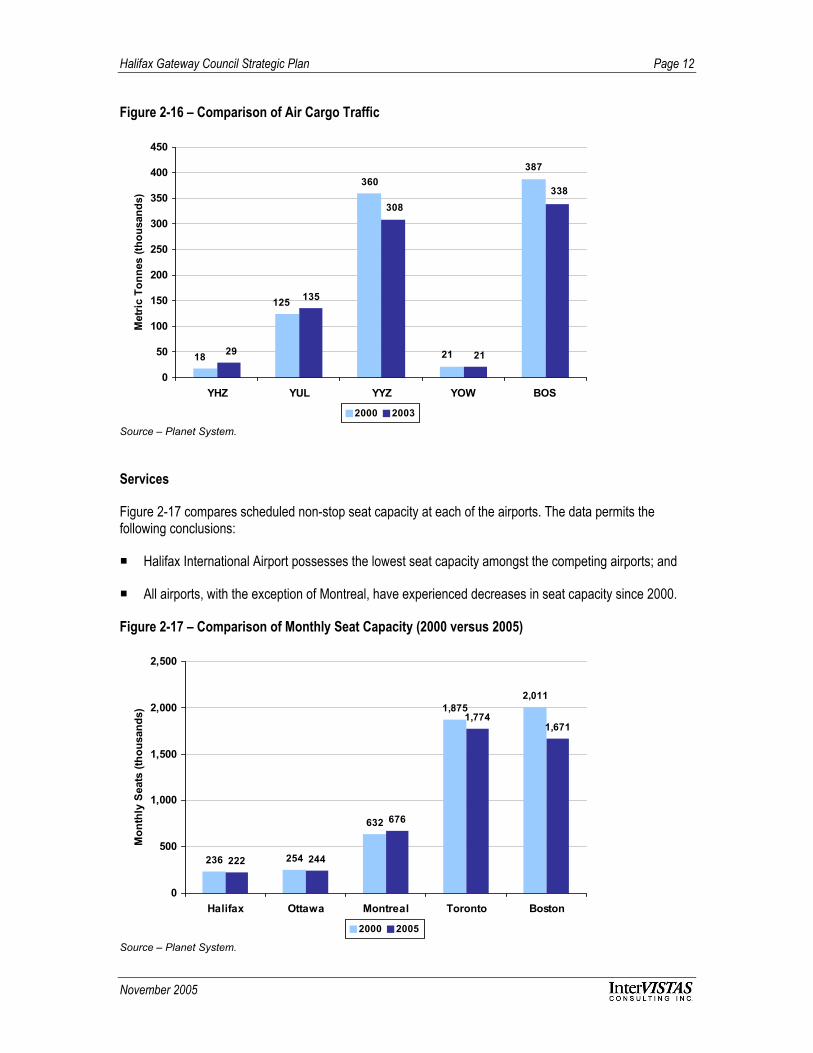

Figure 2-16 compares total air cargo traffic at the competing airports in 2000 and 2003 (the most recent dataavailable). The following observations can be drawn from the data:

Between 2000 and 2003, total air cargo traffic at these airports decreased by 9% from 911,000 tonnesto 832,000 tonnes;

Halifax International Airport traffic levels increased from 18,000 tonnes in 2000 to 29,000 tonnes in2003; and

Halifax International Airport’s market share increased from 2% in 2000 to 4% in 2003.

Halifax Gateway Council Strategic Plan Page 12

November 2005

Figure 2-16 – Comparison of Air Cargo Traffic

135

387

21

360

18

125

338

21

308

29

0

50

100

150

200

250

300

350

400

450

YHZ YUL YYZ YOW BOS

Met

ric T

onne

s (th

ousa

nds)

2000 2003

Source – Planet System.

Services

Figure 2-17 compares scheduled non-stop seat capacity at each of the airports. The data permits thefollowing conclusions:

Halifax International Airport possesses the lowest seat capacity amongst the competing airports; and

All airports, with the exception of Montreal, have experienced decreases in seat capacity since 2000.

Figure 2-17 – Comparison of Monthly Seat Capacity (2000 versus 2005)

236 254

632

1,8752,011

222 244

676

1,7741,671

0

500

1,000

1,500

2,000

2,500

Halifax Ottawa Montreal Toronto Boston

Mon

thly

Sea

ts (t

hous

ands

)

2000 2005

Source – Planet System.

Halifax Gateway Council Strategic Plan Page 13

November 2005

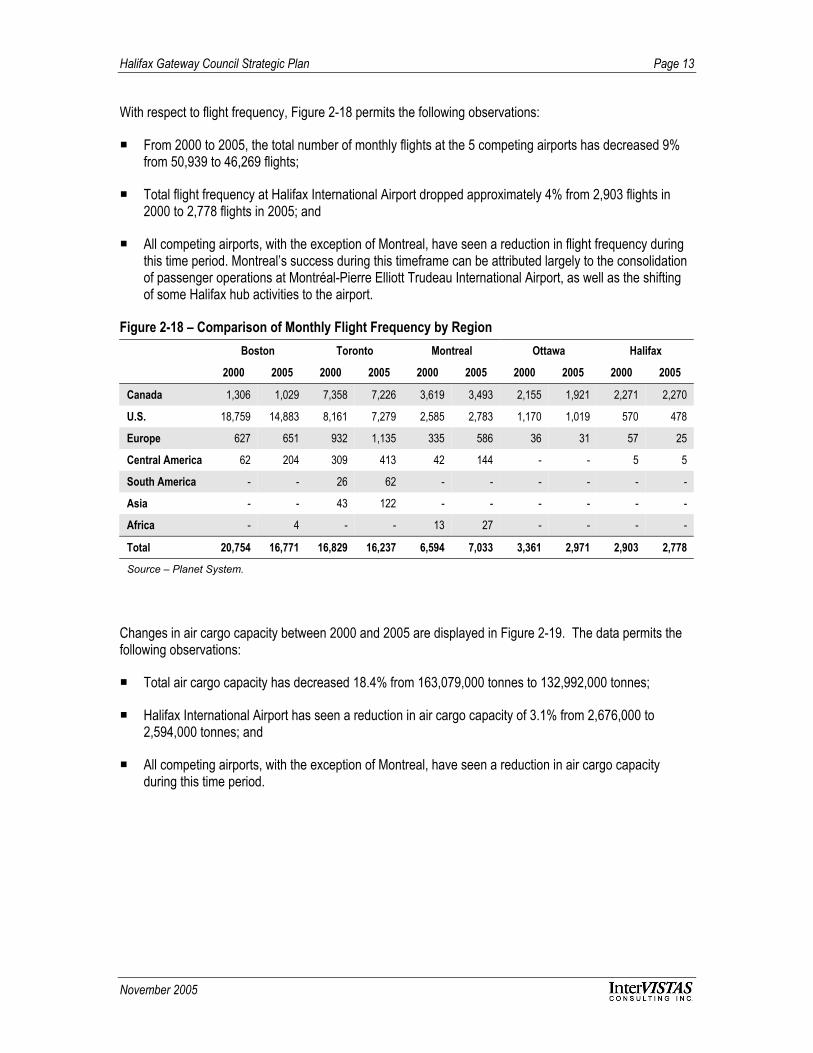

With respect to flight frequency, Figure 2-18 permits the following observations:

From 2000 to 2005, the total number of monthly flights at the 5 competing airports has decreased 9%from 50,939 to 46,269 flights;

Total flight frequency at Halifax International Airport dropped approximately 4% from 2,903 flights in2000 to 2,778 flights in 2005; and

All competing airports, with the exception of Montreal, have seen a reduction in flight frequency duringthis time period. Montreal’s success during this timeframe can be attributed largely to the consolidationof passenger operations at Montréal-Pierre Elliott Trudeau International Airport, as well as the shiftingof some Halifax hub activities to the airport.

Figure 2-18 – Comparison of Monthly Flight Frequency by RegionBoston Toronto Montreal Ottawa Halifax

2000 2005 2000 2005 2000 2005 2000 2005 2000 2005

Canada 1,306 1,029 7,358 7,226 3,619 3,493 2,155 1,921 2,271 2,270

U.S. 18,759 14,883 8,161 7,279 2,585 2,783 1,170 1,019 570 478

Europe 627 651 932 1,135 335 586 36 31 57 25

Central America 62 204 309 413 42 144 - - 5 5

South America - - 26 62 - - - - - -

Asia - - 43 122 - - - - - -

Africa - 4 - - 13 27 - - - -

Total 20,754 16,771 16,829 16,237 6,594 7,033 3,361 2,971 2,903 2,778

Source – Planet System.

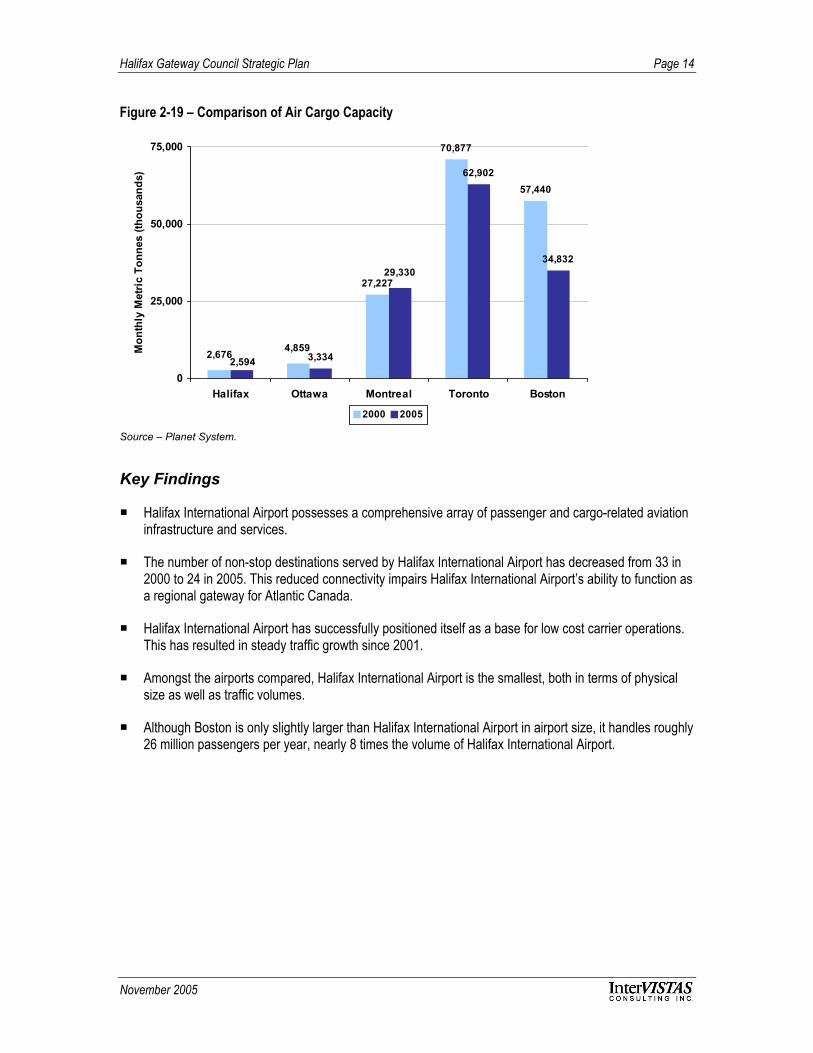

Changes in air cargo capacity between 2000 and 2005 are displayed in Figure 2-19. The data permits thefollowing observations:

Total air cargo capacity has decreased 18.4% from 163,079,000 tonnes to 132,992,000 tonnes;

Halifax International Airport has seen a reduction in air cargo capacity of 3.1% from 2,676,000 to2,594,000 tonnes; and

All competing airports, with the exception of Montreal, have seen a reduction in air cargo capacityduring this time period.

Halifax Gateway Council Strategic Plan Page 14

November 2005

Figure 2-19 – Comparison of Air Cargo Capacity

27,227

70,877

57,440

3,334

62,902

34,832

4,8592,676

29,330

2,5940

25,000

50,000

75,000

Halifax Ottawa Montreal Toronto Boston

Mon

thly

Met

ric

Tonn

es (t

hous

ands

)

2000 2005

Source – Planet System.

Key Findings

Halifax International Airport possesses a comprehensive array of passenger and cargo-related aviationinfrastructure and services.

The number of non-stop destinations served by Halifax International Airport has decreased from 33 in2000 to 24 in 2005. This reduced connectivity impairs Halifax International Airport’s ability to function asa regional gateway for Atlantic Canada.

Halifax International Airport has successfully positioned itself as a base for low cost carrier operations.This has resulted in steady traffic growth since 2001.

Amongst the airports compared, Halifax International Airport is the smallest, both in terms of physicalsize as well as traffic volumes.

Although Boston is only slightly larger than Halifax International Airport in airport size, it handles roughly26 million passengers per year, nearly 8 times the volume of Halifax International Airport.

Halifax Gateway Council Strategic Plan Page 15

November 2005

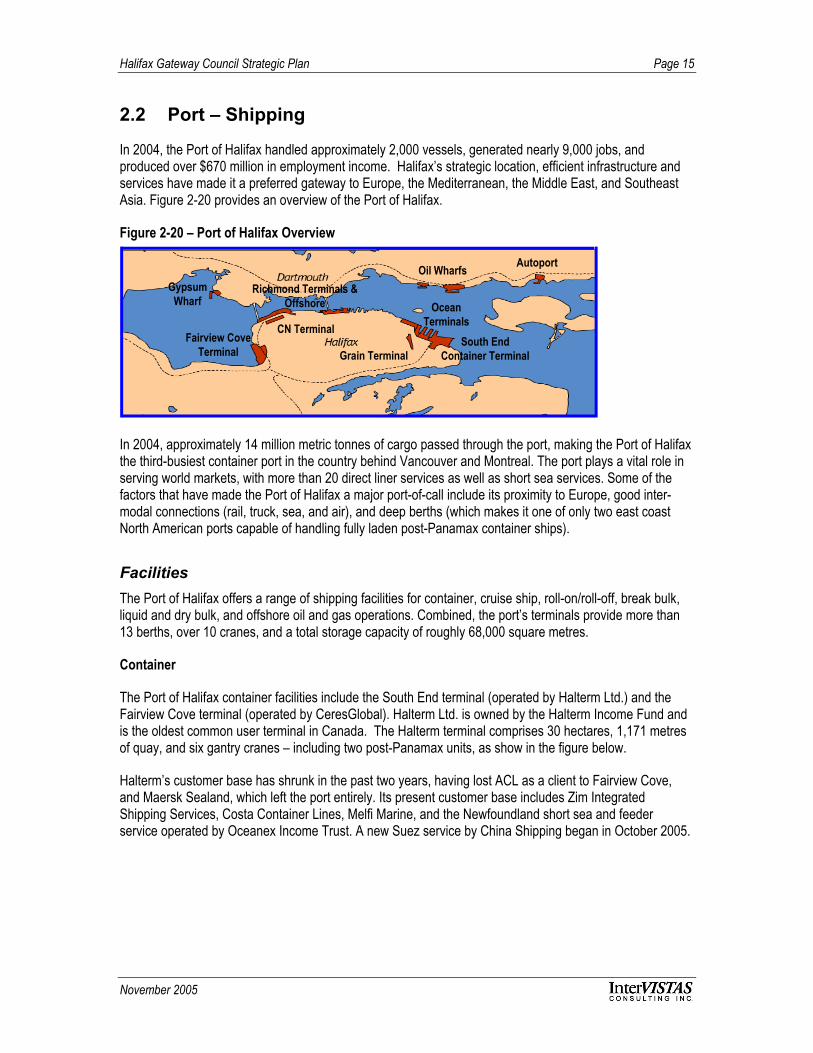

2.2 Port – Shipping

In 2004, the Port of Halifax handled approximately 2,000 vessels, generated nearly 9,000 jobs, andproduced over $670 million in employment income. Halifax’s strategic location, efficient infrastructure andservices have made it a preferred gateway to Europe, the Mediterranean, the Middle East, and SoutheastAsia. Figure 2-20 provides an overview of the Port of Halifax.

Figure 2-20 – Port of Halifax Overview

Fairview CoveTerminal

South EndContainer Terminal

Autoport

CN Terminal

GypsumWharf

Grain Terminal

OceanTerminals

Richmond Terminals &Offshore

Oil Wharfs

In 2004, approximately 14 million metric tonnes of cargo passed through the port, making the Port of Halifaxthe third-busiest container port in the country behind Vancouver and Montreal. The port plays a vital role inserving world markets, with more than 20 direct liner services as well as short sea services. Some of thefactors that have made the Port of Halifax a major port-of-call include its proximity to Europe, good inter-modal connections (rail, truck, sea, and air), and deep berths (which makes it one of only two east coastNorth American ports capable of handling fully laden post-Panamax container ships).

Facilities The Port of Halifax offers a range of shipping facilities for container, cruise ship, roll-on/roll-off, break bulk,liquid and dry bulk, and offshore oil and gas operations. Combined, the port’s terminals provide more than13 berths, over 10 cranes, and a total storage capacity of roughly 68,000 square metres.

Container

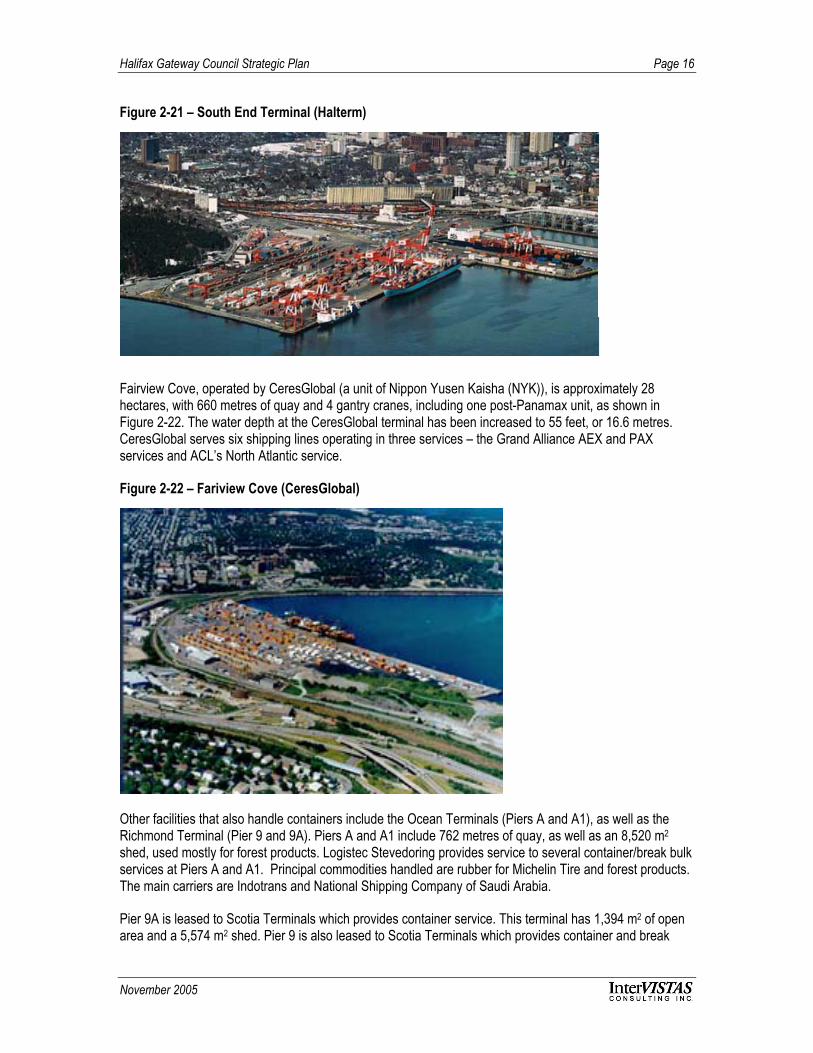

The Port of Halifax container facilities include the South End terminal (operated by Halterm Ltd.) and theFairview Cove terminal (operated by CeresGlobal). Halterm Ltd. is owned by the Halterm Income Fund andis the oldest common user terminal in Canada. The Halterm terminal comprises 30 hectares, 1,171 metresof quay, and six gantry cranes – including two post-Panamax units, as show in the figure below.

Halterm’s customer base has shrunk in the past two years, having lost ACL as a client to Fairview Cove,and Maersk Sealand, which left the port entirely. Its present customer base includes Zim IntegratedShipping Services, Costa Container Lines, Melfi Marine, and the Newfoundland short sea and feederservice operated by Oceanex Income Trust. A new Suez service by China Shipping began in October 2005.

Halifax Gateway Council Strategic Plan Page 16

November 2005

Figure 2-21 – South End Terminal (Halterm)

Fairview Cove, operated by CeresGlobal (a unit of Nippon Yusen Kaisha (NYK)), is approximately 28hectares, with 660 metres of quay and 4 gantry cranes, including one post-Panamax unit, as shown inFigure 2-22. The water depth at the CeresGlobal terminal has been increased to 55 feet, or 16.6 metres.CeresGlobal serves six shipping lines operating in three services – the Grand Alliance AEX and PAXservices and ACL’s North Atlantic service.

Figure 2-22 – Fariview Cove (CeresGlobal)

Other facilities that also handle containers include the Ocean Terminals (Piers A and A1), as well as theRichmond Terminal (Pier 9 and 9A). Piers A and A1 include 762 metres of quay, as well as an 8,520 m2

shed, used mostly for forest products. Logistec Stevedoring provides service to several container/break bulkservices at Piers A and A1. Principal commodities handled are rubber for Michelin Tire and forest products.The main carriers are Indotrans and National Shipping Company of Saudi Arabia.

Pier 9A is leased to Scotia Terminals which provides container service. This terminal has 1,394 m2 of openarea and a 5,574 m2 shed. Pier 9 is also leased to Scotia Terminals which provides container and break

Halifax Gateway Council Strategic Plan Page 17

November 2005

bulk service to Cuba via Nirint Shipping Line. The principal break bulk commodity is nickel sulphite, which isshipped by rail to Alberta.

Roll-On/Roll-Off

Autoport is a 41-hectare facility, as displayed in Figure 2-23, with a 201-metre wharf that handles roll-on androll-off cargo. It also has five rail sidings for inward and outward vehicle processing. Autport processesEuropean import vehicles and domestic vehicles destined for Atlantic Canada. Autoport is 100% owned byCN Rail, and North American network of similar facilities under the same brand is managed from Halifax.

Figure 2-23 – Autoport

Autoport processes approximately 100,000 autos per annum through Eastern Passage. These compriseEuropean imports, well as domestic autos destined for the Atlantic Canada market, including all vehiclesexcept DaimlerChrysler products, going to Newfoundland. Other roll-on/roll-off cargoes are handled at theSouth End, Fairview Cove, and Piers A1 and A.

Offshore Oil and Gas

The port has two offshore supply bases, one at Richmond Offshore (Pier 9B, 9C and Area 9D), which isleased to EnCana Corporation, and another owned and operated by ExxonMobil at Woodside. RichmondOffshore includes two berths of 216 metres and 140 metres, and one 5,853 m2 shed. It also includes twoopen areas of 9,290 m2 and 21,368 m2, respectively. The EnCana base is operated on a common userbasis, whereas the ExxonMobil base is not.

Intermodal

CN operates Halifax Intermodal Terminal (HIT) near Richmond Terminals in the north end of the city. Itoffers on-dock double stack train service direct to Montreal, Toronto, and Chicago. Two gantry cranes canhandle 150 units per day, with total annual lift capacity of 52,000 units. CN handles about 25,000intermodal units per annum at HIT. The facility handles CN’s own intermodal cargo, as well as truckers’ andmajor retailers’ 53 foot domestic intermodal containers.

Halifax Gateway Council Strategic Plan Page 18

November 2005

Break Bulk

Richmond Terminal and Offshore Pier 9 (includes 9, 9A, 9B and 9C) offers 4 sizeable berthing areas – 213metres, 241 metres, 216 metres, and 140 metres, as well as three sheds of 8,175, 5,574, and 5,853 m2.Piers 23-24 include a combination of open area and shedded space suitable for break bulk operations.There are two berths of 213 metres and 142 metres, and a shed of 4,706 m2. Piers 23 and 24, as well as A1and A also handle break bulk cargoes such as drill pipe and rubber.

Gypsum

National Gypsum owns and operates a facility in Wright’s Cove for the shipment of raw gypsum mined attheir site in Milford. The berth is 197 metres and the open area is 10 hectares. The facility has storagecapacity for 180,000 metric tonnes of cargo and receives cargo in unit trains powered by CN Rail directlyfrom the mine. National Gypsum ships about 3.8 million tonnes of gypsum annually through the Port ofHalifax, in approximately 200 vessel loads.

Grain

The Halifax grain elevator, operated by Halifax Grain Elevator Company, has 140,000 tonnes of storagecapacity, with maximum loading capacity of 2,000 tonnes per hour. The marine leg can unload at 700tonnes per hour and the self-unloading marine facility can discharge at 1,200 tonnes per hour. The facilityhas both on dock rail and truck access and well as direct ship discharge.

Crude and Refined Oil

Crude and refined petroleum account for the largest tonnages handled at the Port of Halifax. Imperial Oiloperates docks at Woodside for unloading crude oil and loading refined product for consumption in AtlanticCanada. The facilities include three berths of 67 metres, 122 metres, and 67 metres. The refinery alsoprovides bunkering facilities, either directly at the refinery or via a bunker barge. The largest vessel that canbe accommodated at Imperial Oil is 70,000 tonnes.

Marine Industry

Nova Scotia Business Inc. owns a common user dock in Woodside Atlantic Wharf, which has 229 metres ofberth and an open area of over 2 hectares. Water depths are 8.8 metres. The common user dock inWoodside is used for vessel lay ups, and ship repairs and rebuilds. It is mainly used to support oil and gasdrilling activities.

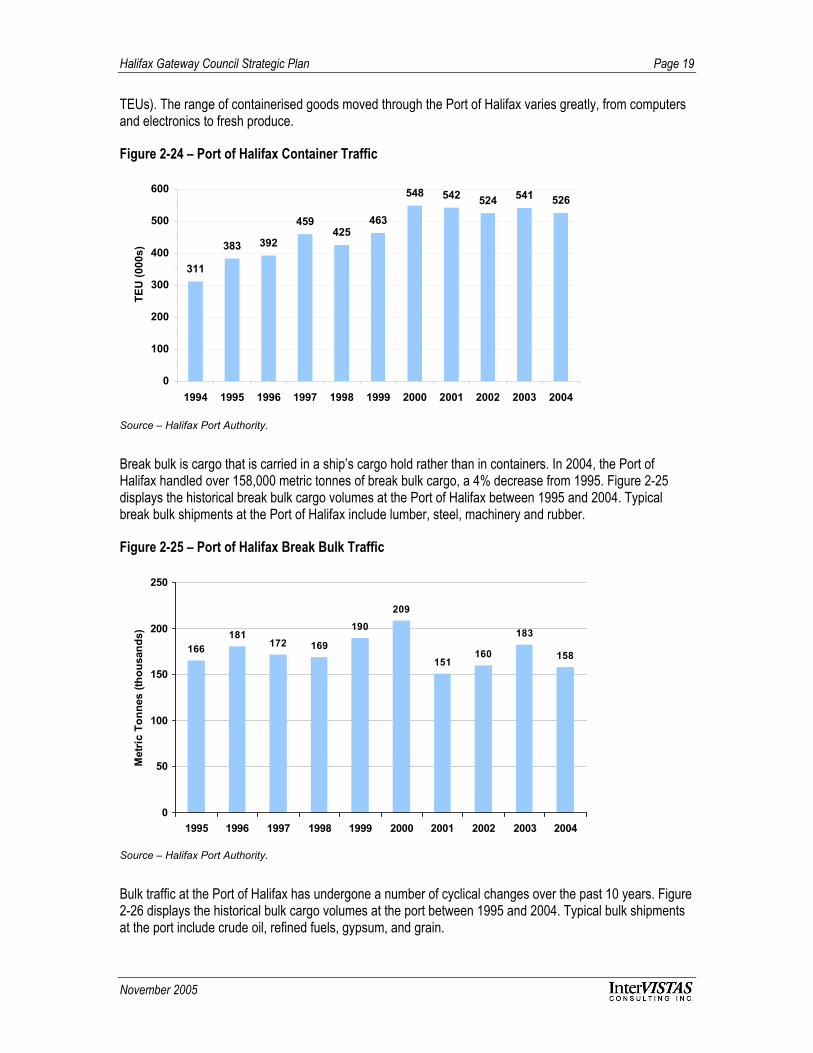

TrafficContainer traffic at the Port of Halifax has undergone a number of cyclical changes over the past 10 years,due largely to changing economic and industry conditions (Figure 2-24). Between 1995 and 2004, containertraffic at the port increased by over 37%. In 2000, the Port of Halifax handled a record 548,000 TEUs1; sincethen, traffic has remained fairly flat albeit with annual fluctuations (2004 traffic totalled almost 526,000

1 A twenty-foot equivalent unit is a measure of containerised cargo equal to one standard 20 ft (length) × 8 ft (width) × 8.5 ft (height)

container (approximately 39 m3).

Halifax Gateway Council Strategic Plan Page 19

November 2005

TEUs). The range of containerised goods moved through the Port of Halifax varies greatly, from computersand electronics to fresh produce.

Figure 2-24 – Port of Halifax Container Traffic

311

383 392

459425

463

548 542 524 541 526

0

100

200

300

400

500

600

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

TEU

(000

s)

Source – Halifax Port Authority.

Break bulk is cargo that is carried in a ship’s cargo hold rather than in containers. In 2004, the Port ofHalifax handled over 158,000 metric tonnes of break bulk cargo, a 4% decrease from 1995. Figure 2-25displays the historical break bulk cargo volumes at the Port of Halifax between 1995 and 2004. Typicalbreak bulk shipments at the Port of Halifax include lumber, steel, machinery and rubber.

Figure 2-25 – Port of Halifax Break Bulk Traffic

166181

172 169

190

209

151160

183

158

0

50

100

150

200

250

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Met

ric T

onne

s (th

ousa

nds)

Source – Halifax Port Authority.

Bulk traffic at the Port of Halifax has undergone a number of cyclical changes over the past 10 years. Figure2-26 displays the historical bulk cargo volumes at the port between 1995 and 2004. Typical bulk shipmentsat the port include crude oil, refined fuels, gypsum, and grain.

Halifax Gateway Council Strategic Plan Page 20

November 2005

Figure 2-26 – Port of Halifax Bulk Traffic

9,476 9,3389,880

9,3019,823

8,999 9,248

8,2068,800 9,000

0

2,000

4,000

6,000

8,000

10,000

12,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Met

ric T

onne

s (th

ousa

nds)

Source – Halifax Port Authority.

Roll-on and roll-off traffic, including automobiles, accounted from roughly 1% of the total cargo movedthrough the Port of Halifax in 2004. Almost 200,000 metric tonnes of roll-on/roll-off cargo was handledduring the year, representing an 8% decrease from the previous year.

Market/Competitive PositionMarket Position

Halifax serves a number of key markets, including Atlantic Canada, Quebec, Ontario, New England, and theU.S. mid-west. Figure 2-27 outlines the four major geographic markets and their population base.

Figure 2-27– Port of Halifax Market Regions and PopulationMarket Population

Atlantic Canada 2.3 million

Quebec 7.4 million

Ontario 11.8 million

U.S. Midwest 67.9 million

Source – Statistics Canada, Census of Canada, and U.S. Census.

Most of the Port of Halifax’s cargo is origin and destination to/from Atlantic Canada, Quebec, and Ontario.The Maritime provinces (Nova Scotia, New Brunswick, and Prince Edward Island) are served by truck.Quebec, Ontario, and the U.S. mid-west are served by rail.

With a bi-weekly short sea service, Halifax also handles cargo moving between the Canadian mainland andNewfoundland, a significant portion of which is overseas transhipment cargo. It also handles New Englandto Portland and Boston cargo via feeder. Another weekly service provides transhipment service to St. Pierreet Miquelon. Figure 2-28 summarises the Port of Halifax’s container traffic by origin and destination.

Halifax Gateway Council Strategic Plan Page 21

November 2005

Figure 2-28 – Port of Halifax Container Tonnage by Origin/Destination 2004

Province/State Tonnes Laden TEUs(10 tonnes per TEU)

Atlantic Canada 848,698 84,870

Inland Canada 2,060,379 206,037

- Quebec 903,729 90,373

- Ontario 953,010 95,301

- Western Canada 203,640 20,364

Total Canada 2,909,077 290,907

Inland U.S.

- U.S. Midwest 724,485 72,448

- New England 345,381 34,538

- Rest of U.S. 527,533 52,753

Total U.S. 1,597,399 159,739

Other Markets 518,178 52,753

Total 4,497,123 450,649

Source – Halifax Port Authority.

Most importantly from the point of view of the Halifax Gateway, the Port of Halifax is Atlantic Canada’sgateway to world markets. Even though it has a smaller market share than Montreal, it offers more servicesto more world ports than any other port in eastern Canada, with services to and from the United Kingdom,North Europe, Baltic, Mediterranean, Middle East, Indian sub-continent, South East Asia, Far East, andAustralia/New Zealand ports. The volume of regional cargo is comparatively small, and to provide the rangeof services available, is very dependant upon the larger volumes of cargo going to or from larger inlandmarkets. The total export and import volumes for the combined mix of shipping lines offering service at thePort of Halifax is shown in Figure 2-29.

Halifax Gateway Council Strategic Plan Page 22

November 2005

Figure 2-29 – Port of Halifax Container Traffic by Region

Route/Region Export(tonnes)

Import(tonnes)

Total(tonnes)

U.K. Continent 469,685 683,675 1,153,360

Mediterranean 222,682 511,684 734,547

China and Indian SubContinent 402,613 185,740 588,353

Far East 351,490 108,450 459,940

Other Canada/U.S. 229,951 30,995 260,946

Caribbean 173,296 69,016 242,313

Middle East 102,746 72,791 175,537

Central America 120,835 40,154 160,989

Scandinavia 32,959 98,566 131,525

South America 107,903 18,255 126,058

Eastern Europe 22,857 1,177 24,034

Africa 17,289 619 17,908

Oceania 1,482 2,092 3,574

Transhipment 245,044 172,995 418,039

Total 2,500,732 1,996,390 4,497,123

Source – Halifax Port Authority.

Competitive Position

In its efforts to attract cargo and passenger traffic, the Port of Halifax competes with other ports in the NorthAtlantic region. For the purposes of this analysis, Port of Halifax’s key competitors were determined to bethe Port of New York/New Jersey, the Port of Virginia, and the Port of Montreal (Figure 2-30). The followingsections review the Port of Halifax’s competitive position relative to these facilities.

Halifax Gateway Council Strategic Plan Page 23

November 2005

Figure 2-30 – Port of Halifax Shipping Competitors

Halifax

Montreal

New York

Norfolk

Facilities

Port of New York/New Jersey

The Port of New York/New Jersey is located at the centre of one of the world’s most concentrated andaffluent consumer markets. In 2004, more than 25 million tonnes of oceanborne general cargo movedthrough the port, including 4.5 million TEUs of containerised cargo. The majority of this cargo is processedthrough four terminals managed by the Port Authority of New York/New Jersey:

Port Newark/Elizabeth-Port Authority Marine Terminal complex (NJ) (2 terminals);

PA Auto Marine Terminal (NJ) (1 terminal);

Brooklyn Piers Red Hook Container Terminal (NY) (1 terminal and 2 piers); and

Howland Hook Marine Terminal (NY) (1 terminal).

The remaining cargo is handled by private operators such as Global Marine Terminal, the City of New York'sSouth Brooklyn Terminal, and a number of marine terminals operated by private oil companies along thesouthern coastline of New Jersey (which handle loads such as imported liquid bulk crude oil). The port isequipped with a variety of cranes, including Paceco, Paceco Post-Panamax, and ZPMC Post-Panamax.

Ports of Virginia

The Virginia ports are located just 18 nautical miles from the open sea in a year-round, ice-free harbouroffering deep waters of up to 15.2 metres. The ports provide an unobstructed channel that allows easyaccess and manoeuvring room for very large container vessels. The Ports of Virginia own four general

Halifax Gateway Council Strategic Plan Page 24

November 2005

cargo terminals – Norfolk International Terminals, Portsmouth Marine Terminal, Newport News MarineTerminal, and the Virginia Inland Port in Front Royal. All facilities are operated by Virginia InternationalTerminals Inc., a non-profit operating affiliate of the Virginia Port Authority. The port is equipped with chassisstackers, container cranes, a gantry crane, PACECO cranes, Kone cranes, a CEMCO crane, a Deer Parkcrane, and a Clyde Gantry crane.

In addition, the port is connected to an extensive, modern network of interstate and local highways thatpermit direct inland motor-freight transportation to any point in the U.S. Currently, more than 50 motor-carrier companies offer full freight-handling and load-consolidation services at the port.

Port of Montreal

Montreal is one of the busiest inland ports in the world, and a key transfer point for transatlantic cargo.Approximately half of its containerised cargo traffic is destined to/from from the Canadian market, mainlyQuebec and Ontario, with the other half to/from the U.S. market. The Port of Montreal has excellent raillinks that provide shippers with faster transit times to several U.S. destinations – such as Chicago andDetroit – than the port of New York. The port operates six container terminals – Bickerdike Complex (9berths), Racine Terminal (8), Maisonneuve Terminal (4), Cast Terminal (6) and 4 specialised terminals(Grain Terminal (3 berths), Contrecoeur Terminal (2), Petroleum Berths (11), and Logistics Berths (20)).The port is equipped with 30-60 tonne dockside gantry and yard gantry cranes.

Figure 2-31– Comparison of Shipping FacilitiesNY/NJ Norfolk Montreal Halifax

Number of Terminals 5 4 6 6

Terminal Size (acres) 1,423 acres 1,330 acres 175 acres 145 acres

Number of Berths 21+ 30+ 13+

Number of Cranes 34+ 19+ 31+ 10+

Berth Depth Range (m) 9.9 – 12.8 9.2 – 15.2 7.6 – 10.7 8.8 – 16.8

Cargo CapabilitiesContainer, roll-on/

roll-off, bulk,breakbulk, neobulk

Container, roll-on/roll-off, bulk,breakbulk

Container, roll-on/roll-off, bulk,breakbulk

Container, roll-on/roll-off, bulk,breakbulk

Specialized ServicesAuto exports,

fumigation facilities,wallboard

manufacturing- -

Gypsum, oil, autoimports, ship repair,

grain elevator

Storage Capacity(tonnes) - - -

68,000 m2 (excludingspecialized service

areas)

Intermodal ConnectionsOn-dock rail

connection, truck andhighway access

On-dock double-stackrail service, on-dockrail service, truck and

highway access

On-dock double-stackrail service, on-dockrail service, truck and

highway access

Source – Individual ports.

Halifax Gateway Council Strategic Plan Page 25

November 2005

Traffic

In terms of this analysis, the two most relevant market positions are those for container traffic and cruisevessel throughput. While container cargo grew around the turn of the 21st century, the Port of Halifax’smarket share, in terms of its North Atlantic competitors, has fallen almost continuously in the past decade. Inthe past five years, its traffic has stagnated or declined in an overall market that has grown 32% during thepast five years.

Figure 2-32 shows the amount of container traffic at all four ports between 2000 and 2004. Overall,container traffic has risen an average of 5.7% per annum from 6,088,379 TEUs in 2000 to 8,039,282 TEUsin 2004.

Figure 2-32 – Comparison of Container Traffic (TEUs)Port 2000 2001 2002 2003 2004

Halifax 548,404 541,640 524,336 541,650 525,553

Montreal 1,014,148 989,427 1,054,603 1,108,837 1,226,296

Norfolk 1,347,517 1,303,797 1,437,779 1,646,279 1,808,953

New York 3,178,310 3,316,275 3,749,014 4,067,811 4,478,480

Total 6,088,379 6,151,139 6,765,732 7,364,577 8,039,282

Source – Individual ports.

Figure 2-33 displays the relative market shares of each port during this same time period. In terms of marketshare, the Port of Halifax’s market share has declined from roughly 9% in 2000 to approximately 6.5% in2004. By comparison, the Port of New York/New Jersey has seen its market share grow by 3.5 points duringthis period.

Figure 2-33 – Comparison of Market SharePort 2000 2001 2002 2003 2004

Halifax 9.0% 8.8% 7.7% 7.4% 6.5%

Montreal 16.7% 16.1% 15.6% 15.1% 15.3%

Norfolk 22.1% 21.2% 21.3% 22.4% 22.5%

New York 52.2% 53.9% 55.4% 55.2% 55.7%

Total 100.0% 100.0% 100.0% 100.0% 100.0%

Source – Individual ports.

Key Findings

The Port of Halifax possesses a comprehensive array of uncongested shipping infrastructure andservices.

The Port of Halifax’s overall container traffic and market share declined between 2000 and 2004. Thishas occurred in a market that experienced growth of 32% during the period.

Even though it has a smaller market share than Montreal, the Port of Halifax offers more services tomore world ports than any other port in eastern Canada.

Halifax Gateway Council Strategic Plan Page 26

November 2005

2.3 Port – Cruise

FacilitiesPassenger Terminals

The Pier 21 Cruise Pavilion currently offers the best cruise line and passenger experience in terms of port-of-call and potential homeport operations in Halifax. For Piers 20 to 22, the largest issue for homeportinglies in the width of the apron area and access onto the apron by supply trucks. Piers 30 and 31 are preferredfor homeport operations due to the size of the aprons and additional walking room for passengers. Overall,both pier length and height of the berths are sufficient for all of the major cruise ships operating in theregion.

The Pier 21 Cruise Pavilion, in many ways, reflects the current thinking regarding cruise vessel port-of-callfacilities. It is a renovated structure situated close to the downtown area where passengers can enjoy thedestination and where there is a mix of retail and other uses incorporated into the cruise complex. It is in thisproximity to the downtown area that the Pier 21 Cruise Pavilion serves as a significant strength for Halifax,an observation supported by responses from cruise line operational personnel.

Apron and Gangways

Apron areas for cruise ship operations are small and would present significant challenges for cruise vesselhomeport operations, especially those requiring provisions associated with a homeport operation. Apronwidths are generally less than 25-feet (7.6 metres) for the Seawall – Piers 20 to 23. By comparison, cruiselines generally prefer apron widths of approximately twice this amount (50-feet/15.2-metres.) for homeportoperations.

Ground Transportation Area

Ground transportation areas within the Pier 20 and 21 areas provide adequate marshalling space for up to40 motorcoaches, however, with more than one tour operator supporting ship operations on a given call,communication and cooperation will be an essential element for further development. Incorporating ahomeport operational plan will assist in overall efforts to attract cruise homeporting operations.

Availability of Other Cruise Berthing Areas

As noted above, additional cruise berthing – apart from the Pier 21 and 20 berths – is available for use asrequired, although at present, Halifax would primarily be a one-ship homeport operation utilising the Pier 21Cruise Pavilion. Within the context of the general cruise homeport market in the region, this is not presentlya significant constraint for the future growth of cruise homeport operations in Halifax.

Provisioning

The availability of provisions is a strong point for Halifax, and with potential exchange rate savings on theCanadian dollar, may serve as a strength for the destination overall. While the provisioning area along theapron is small, the availability of provisions and stores is reported as good.

TrafficCruise passenger traffic at the Port of Halifax has grown considerably over the past 10 years from roughly30,000 passengers in 1995 to approximately 213,000 passengers in 2004 (an increase of over 600%).

Halifax Gateway Council Strategic Plan Page 27

November 2005

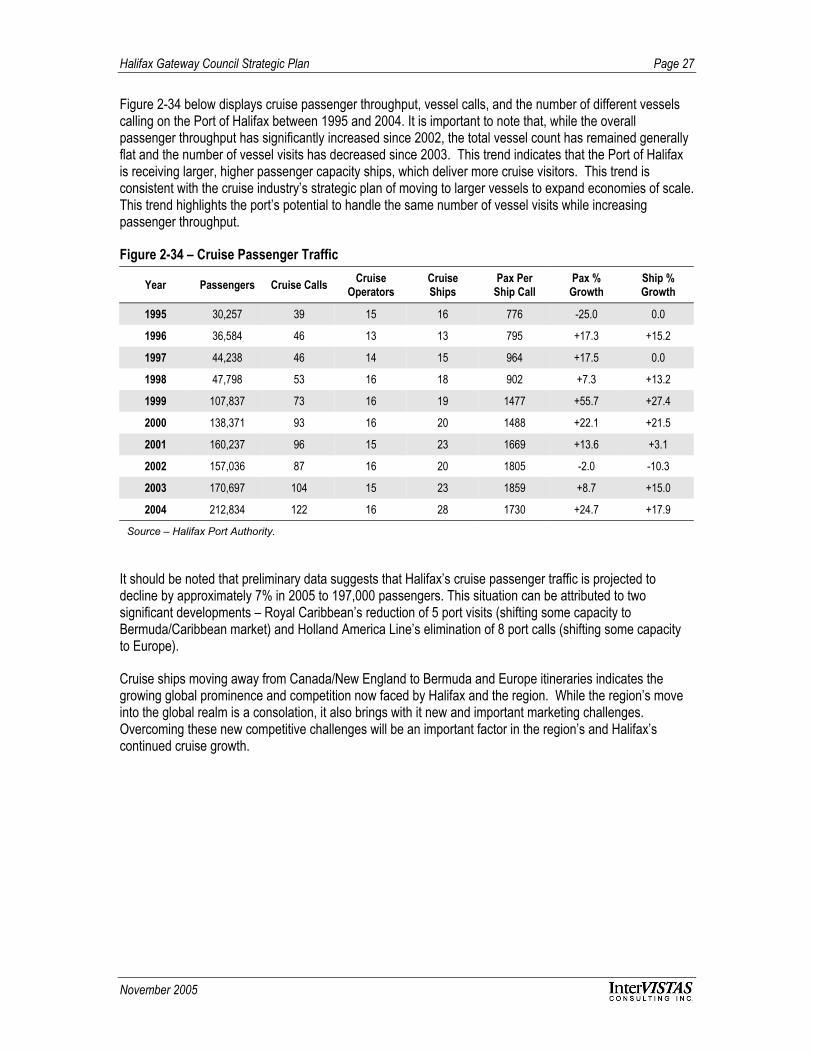

Figure 2-34 below displays cruise passenger throughput, vessel calls, and the number of different vesselscalling on the Port of Halifax between 1995 and 2004. It is important to note that, while the overallpassenger throughput has significantly increased since 2002, the total vessel count has remained generallyflat and the number of vessel visits has decreased since 2003. This trend indicates that the Port of Halifaxis receiving larger, higher passenger capacity ships, which deliver more cruise visitors. This trend isconsistent with the cruise industry’s strategic plan of moving to larger vessels to expand economies of scale.This trend highlights the port’s potential to handle the same number of vessel visits while increasingpassenger throughput.

Figure 2-34 – Cruise Passenger Traffic

Year Passengers Cruise Calls CruiseOperators

CruiseShips

Pax PerShip Call

Pax %Growth

Ship %Growth

1995 30,257 39 15 16 776 -25.0 0.0

1996 36,584 46 13 13 795 +17.3 +15.2

1997 44,238 46 14 15 964 +17.5 0.0

1998 47,798 53 16 18 902 +7.3 +13.2

1999 107,837 73 16 19 1477 +55.7 +27.4

2000 138,371 93 16 20 1488 +22.1 +21.5

2001 160,237 96 15 23 1669 +13.6 +3.1

2002 157,036 87 16 20 1805 -2.0 -10.3

2003 170,697 104 15 23 1859 +8.7 +15.0

2004 212,834 122 16 28 1730 +24.7 +17.9

Source – Halifax Port Authority.

It should be noted that preliminary data suggests that Halifax’s cruise passenger traffic is projected todecline by approximately 7% in 2005 to 197,000 passengers. This situation can be attributed to twosignificant developments – Royal Caribbean’s reduction of 5 port visits (shifting some capacity toBermuda/Caribbean market) and Holland America Line’s elimination of 8 port calls (shifting some capacityto Europe).

Cruise ships moving away from Canada/New England to Bermuda and Europe itineraries indicates thegrowing global prominence and competition now faced by Halifax and the region. While the region’s moveinto the global realm is a consolation, it also brings with it new and important marketing challenges.Overcoming these new competitive challenges will be an important factor in the region’s and Halifax’scontinued cruise growth.

Halifax Gateway Council Strategic Plan Page 28

November 2005

Market/Competitive PositionMarket Position

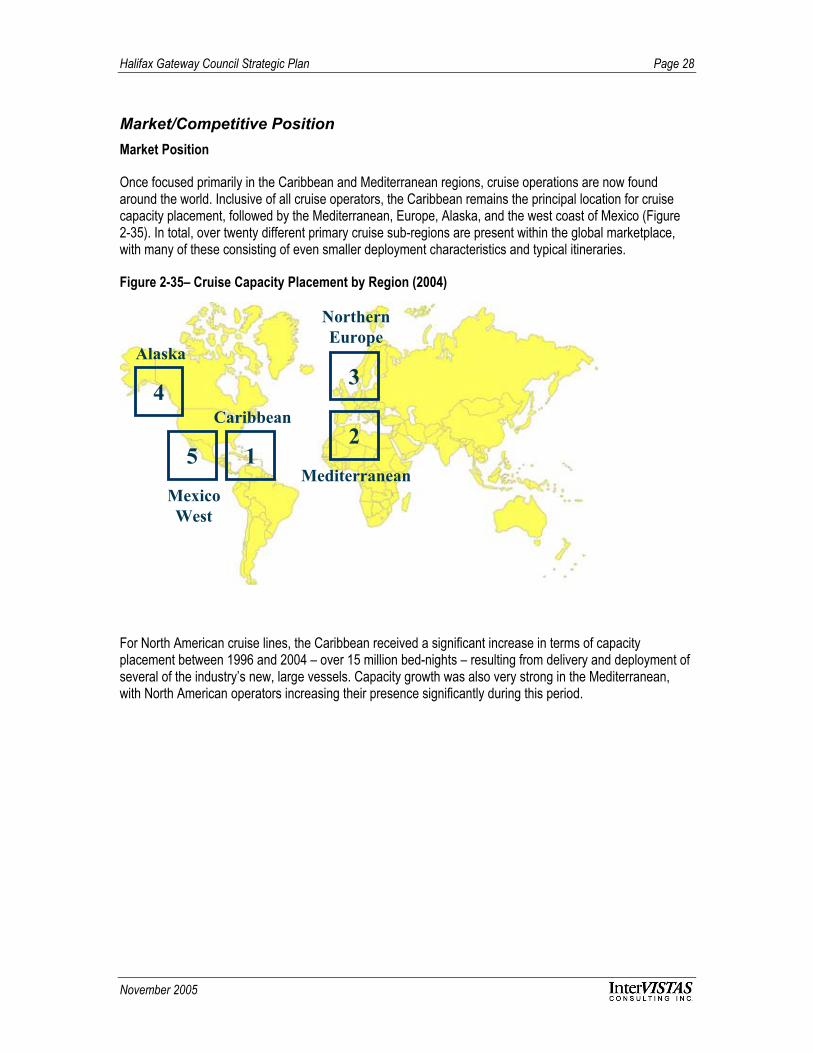

Once focused primarily in the Caribbean and Mediterranean regions, cruise operations are now foundaround the world. Inclusive of all cruise operators, the Caribbean remains the principal location for cruisecapacity placement, followed by the Mediterranean, Europe, Alaska, and the west coast of Mexico (Figure2-35). In total, over twenty different primary cruise sub-regions are present within the global marketplace,with many of these consisting of even smaller deployment characteristics and typical itineraries.

Figure 2-35– Cruise Capacity Placement by Region (2004)

4

Alaska

5MexicoWest

1

Caribbean

3

NorthernEurope

2Mediterranean

For North American cruise lines, the Caribbean received a significant increase in terms of capacityplacement between 1996 and 2004 – over 15 million bed-nights – resulting from delivery and deployment ofseveral of the industry’s new, large vessels. Capacity growth was also very strong in the Mediterranean,with North American operators increasing their presence significantly during this period.

Halifax Gateway Council Strategic Plan Page 29

November 2005

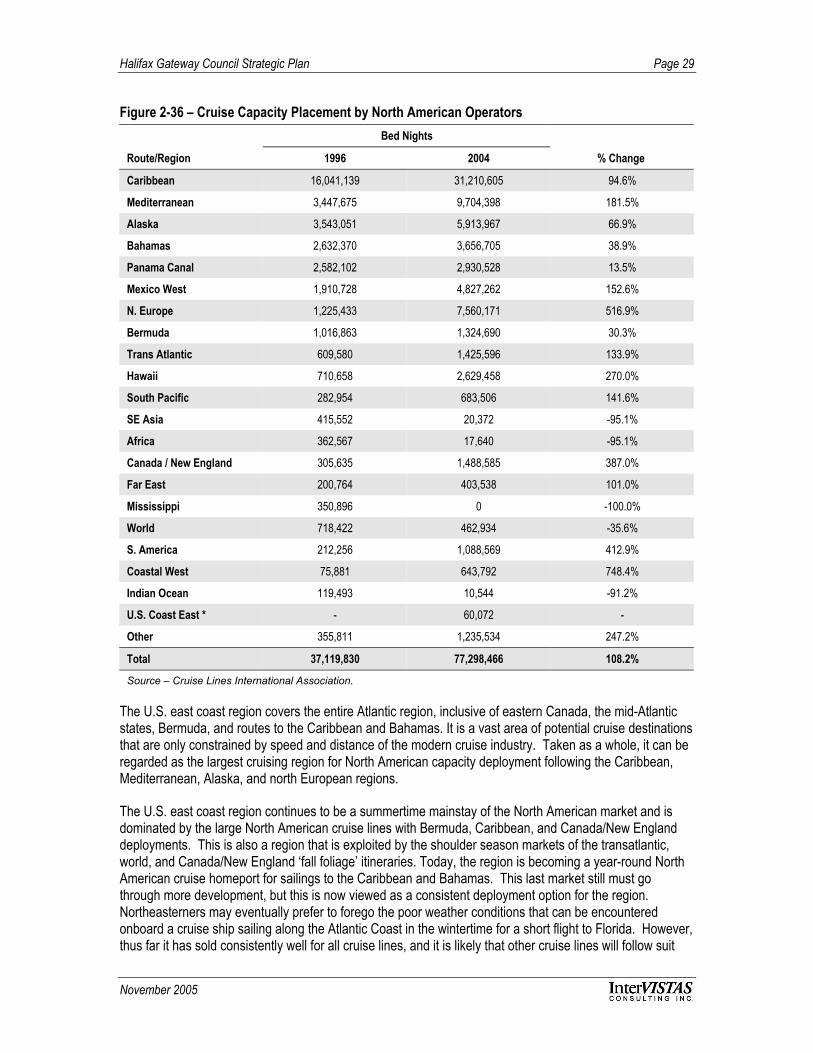

Figure 2-36 – Cruise Capacity Placement by North American OperatorsBed Nights

Route/Region 1996 2004 % Change

Caribbean 16,041,139 31,210,605 94.6%

Mediterranean 3,447,675 9,704,398 181.5%

Alaska 3,543,051 5,913,967 66.9%

Bahamas 2,632,370 3,656,705 38.9%

Panama Canal 2,582,102 2,930,528 13.5%

Mexico West 1,910,728 4,827,262 152.6%

N. Europe 1,225,433 7,560,171 516.9%

Bermuda 1,016,863 1,324,690 30.3%

Trans Atlantic 609,580 1,425,596 133.9%

Hawaii 710,658 2,629,458 270.0%

South Pacific 282,954 683,506 141.6%

SE Asia 415,552 20,372 -95.1%

Africa 362,567 17,640 -95.1%

Canada / New England 305,635 1,488,585 387.0%

Far East 200,764 403,538 101.0%

Mississippi 350,896 0 -100.0%

World 718,422 462,934 -35.6%

S. America 212,256 1,088,569 412.9%

Coastal West 75,881 643,792 748.4%

Indian Ocean 119,493 10,544 -91.2%

U.S. Coast East * - 60,072 -

Other 355,811 1,235,534 247.2%

Total 37,119,830 77,298,466 108.2%

Source – Cruise Lines International Association.

The U.S. east coast region covers the entire Atlantic region, inclusive of eastern Canada, the mid-Atlanticstates, Bermuda, and routes to the Caribbean and Bahamas. It is a vast area of potential cruise destinationsthat are only constrained by speed and distance of the modern cruise industry. Taken as a whole, it can beregarded as the largest cruising region for North American capacity deployment following the Caribbean,Mediterranean, Alaska, and north European regions.

The U.S. east coast region continues to be a summertime mainstay of the North American market and isdominated by the large North American cruise lines with Bermuda, Caribbean, and Canada/New Englanddeployments. This is also a region that is exploited by the shoulder season markets of the transatlantic,world, and Canada/New England ‘fall foliage’ itineraries. Today, the region is becoming a year-round NorthAmerican cruise homeport for sailings to the Caribbean and Bahamas. This last market still must gothrough more development, but this is now viewed as a consistent deployment option for the region.Northeasterners may eventually prefer to forego the poor weather conditions that can be encounteredonboard a cruise ship sailing along the Atlantic Coast in the wintertime for a short flight to Florida. However,thus far it has sold consistently well for all cruise lines, and it is likely that other cruise lines will follow suit

Halifax Gateway Council Strategic Plan Page 30

November 2005

with a similar deployment. This cruise capacity placement is illustrated in Figure 2-37, where the destinationanalyses over the past five years are indicative of the growth of the cruise region. Overall capacity in theprimary east coast markets has grown by 27.7% between 2000 and 2004 with the total North Americanmarket share projected at 3.8%.

In addition, to the small, but steady growth of the primary feeder markets for the region, as illustrated below,the impact of the strong Caribbean and Bahamas market has been the driving force in growth from 2003. In2004, we estimate that the east coast region will be responsible for 2,352,000 bed nights, which translatesinto approximately 8.1% of the total Caribbean and Bahamas North American market share. Thetransatlantic, world and small ship coastal markets are also factors for regional growth.

Figure 2-37– Cruise Capacity Placement in U.S. East Coast Region by North American OperatorsBed Nights

Route/Region 2000 2004 % Change

Bermuda(Bed Nights)* 988,391 1,324,690 25.4%

Bermuda(Passengers)** 152,060 203,798 -

Canada/New England(Bed Nights)* 1,107,689 1,488,585 25.6%

Canada/New England(Passengers)** 170,414 229,013 -

U.S. Coastal East(Bed Nights)* 1,402,429 60,072 -22.3%

U.S. Coastal East(Passengers)** 215,758 9,242 -

Source – Cruise Lines International Association.

From a North American operator perspective, the east coast region has been one of the main beneficiariesof the expansion of the U.S. homeland cruising industry and the diversification of itineraries away from thetraditional Caribbean sailings departing from southern U.S. homeports.

Halifax continues as the most visited destination in all the major cruise lines’ Canada/New Englanditineraries. This valued positioning is expected to continue for the near to mid-term. Halifax is a naturalchoice for the cruise industry to conduct port-of-call operations and the strongest port for potential, futurehomeport actions. Halifax’s regional reputation as a premier city with superior tourism infrastructure, and itsstrategic location all serve as significant pluses for cruise lines considering future operations in AtlanticCanada.

Challenges to Port of Halifax’s market position and its desire to attract homeport operations continue to existand require on-going attention. In addition to the previously stated operational concerns, recent marketactivity has also produced new challenges to Atlantic Canada, and in turn, Port of Halifax’s cruise businessgrowth. The identified factors influencing passenger throughput at Halifax generally fall within one of twocategories. They are:

Cruise line marketing strategy as it relates to revenue demands; and

Local Halifax market conditions with respect to global market competition.

Halifax Gateway Council Strategic Plan Page 31

November 2005

Competitive Position

Port of Halifax’s competitiveness is measured with respect to homeport operations. The Port of Halifax’s keycompetitors in this endeavour have been determined to be the Port of New York/New Jersey, the Port ofMontreal, and the Port of Boston (Figure 2-38). The following sections review the Port of Halifax’scompetitive position relative to these ports.

Figure 2-38 – Port of Halifax Cruise Homeport Competitors

Halifax

Montreal

BostonNew York

Figure 2-39 compares total cruise passenger throughput at competing ports in 2000 and 2004. The followingobservations can be drawn from the data:

Between 2000 and 2004, cruise passenger throughput at competing ports increased roughly 166% from581,000 to 1.55 million passengers;

Total cruise passenger throughput at the Port of Halifax has increased approximately 54% from138,000 passengers in 2000 to 213,000 passengers in 2004; and

Between 2000 to 2004, all competing ports experienced an increase in cruise passenger throughput.

Halifax Gateway Council Strategic Plan Page 32

November 2005

Figure 2-39 – Comparison of Cruise Passenger Traffic

138

25

220 198213

43

1,093

199

0

300

600

900

1,200

Halifax Montreal New York Boston

Pas

seng

ers

(thou

sand

s)

2000 2004

Source – Individual ports.

The Port of Halifax has historically been a port-of-call, that is, where cruise lines call at Halifax in the middleof their itineraries. The Port of Halifax is currently working to entice cruise lines to utilise Halifax as ahomeport, thereby further stimulating the overall of the region. Figure 2-40 displays the relative ratings ofHalifax as a port-of-call and as a homeport by target market.

Figure 2-40 – Port of Halifax Cruise Service Presence by Target Markets

Key: Strong ( ), Fair ( ), Weak ( )

/ n/aBermuda

n/an/aDry-dock/Ship Servicing

/ Newfoundland & Labrador

North Atlantic

/ Round-the-World

Transatlantic

Atlantic Coast Repositioning

/ Canada & New England

Halifax as a HomeportHalifax as a Port-of-CallTarget Market

Source – Bermello, Ajamil & Partners.

Halifax Gateway Council Strategic Plan Page 33

November 2005

Not surprisingly, other nearby ports are also vying for homeport positions. Figure 2-41 identifies keycompetitors and their relative competitive threat level.

Figure 2-41 – Port of Halifax Cruise Competitors Threat Potential

/ (Homeport)Port of Quebec City, Quebec

(Port-of-Call) (Homeport)

Port of Portland, Maine

(Homeport)Port of New York City, New York

(Port-of-Call) (Homeport)

Port of Saint John, New Brunswick

Key: Strong ( ), Fair ( ), Weak ( )

(Homeport)Port of St. John’s, Newfoundland

(Homeport)Port of Boston, Massachusetts

(Port-of-Call)Port of Sydney, Nova Scotia

Competitive Threat PotentialCompetitor

Source – Bermello, Ajamil & Partners.

Key Findings In general, no significant marine conditions or access issues were identified that serve as a constraint

for present or future cruise operations. In fact, in combination with its weather, safe-harbour access,and cruise pier location (within walking distance of the city’s downtown core), the Port of Halifaxexceeds general industry standards for cruise ports.

The Canada/New England cruise market sector has experienced impressive growth over the pastdecade, but the pace has slowed in recent years.

Halifax continues as the most visited destination in all the major cruise lines’ Canada/New Englanditineraries. This valued positioning is expected to continue for the near to mid-term.

Halifax has the strongest potential to secure future cruise homeport operations.

2.4 Ground Transportation

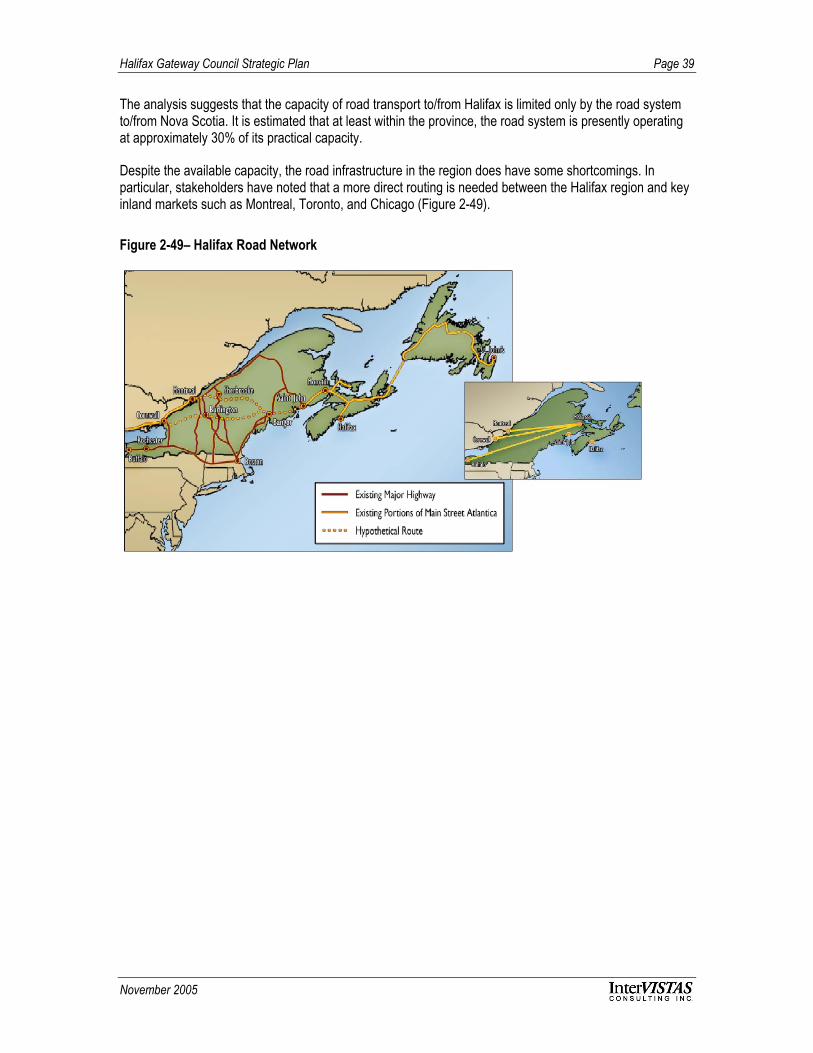

FacilitiesRoad

The main road infrastructure in and out of Halifax consists of a number of 100 series highways, some ofwhich are part of the National Highway System (Figure 2-42). Highway 103 leads to destinations on theSouth Shore, Highway 101 leads to the Annapolis Valley, and Highway 102 is the main transportationcorridor connecting Halifax to the Trans-Canada Highway at Truro. Highway 102 also serves as the accessroute to Halifax International Airport. Highway 107 serves the Eastern Shore.

Halifax Gateway Council Strategic Plan Page 34

November 2005

Two bridges provide access to Halifax Peninsula. The Macdonald Bridge has three lanes, one in eachdirection and one reversing depending on the predominant traffic flow. Access to this bridge is limited toautomobiles and very light pick-up trucks. The MacKay Bridge has two lanes in each direction and handlesa large amount of truck traffic since it is the most convenient route between the container terminals onHalifax Peninsula and the major industrial centre of Burnside Industrial Park. The MacKay Bridge alsoprovides convenient access to the 102, via the 111 and 118, rather than taking the normally congestedBedford Highway towards the 102, or alternatively, the Joseph Howe Drive in the opposite direction to reachHighway 102.

Figure 2-42 – Halifax Road Network

Rail

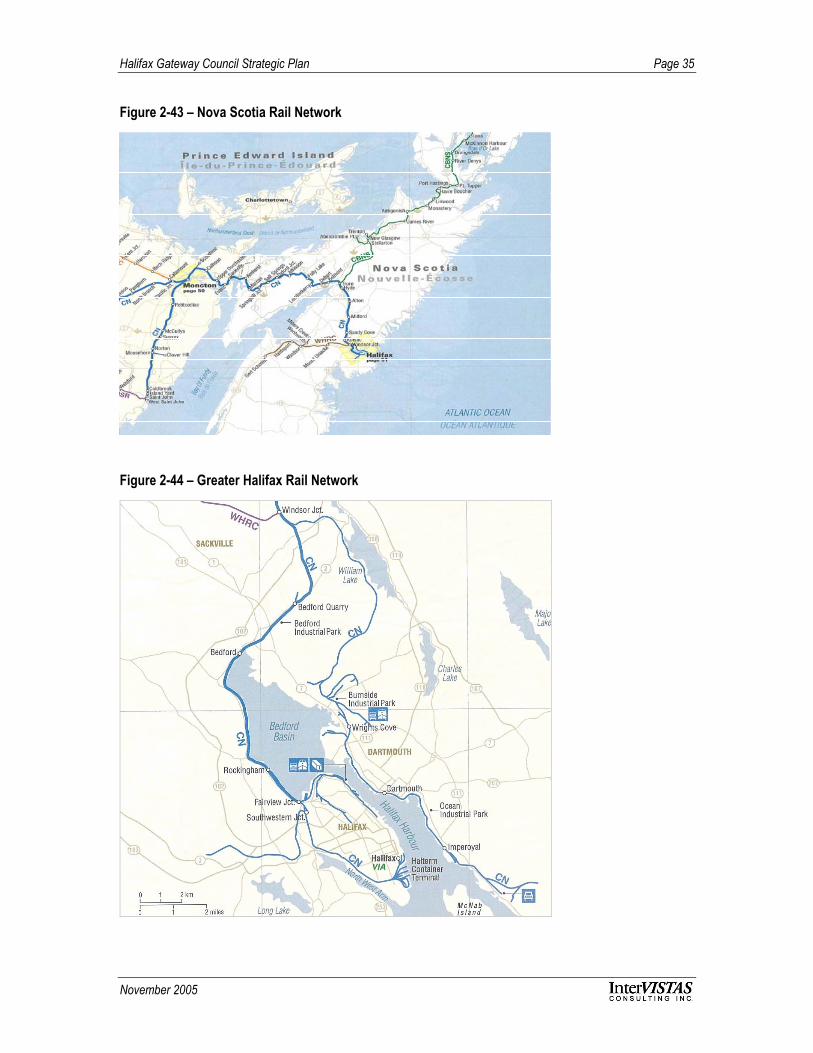

In the Greater Halifax region, CN Rail is the only Class 1 rail carrier that provides rail service to inlandmarkets. Halifax is CN Rail’s eastern terminus for its transcontinental mainline (Figure 2-43). Freight trainsgenerally arrive at or depart from Rockingham yard, and traffic is dispatched from the Rockingham yardtowards the port terminals of Fairview Cove, the South End as well as the Halifax Intermodal Terminal,which is the CN operated domestic terminal for Halifax.

Halifax Gateway Council Strategic Plan Page 35

November 2005

Figure 2-43 – Nova Scotia Rail Network

Figure 2-44 – Greater Halifax Rail Network

Halifax Gateway Council Strategic Plan Page 36

November 2005

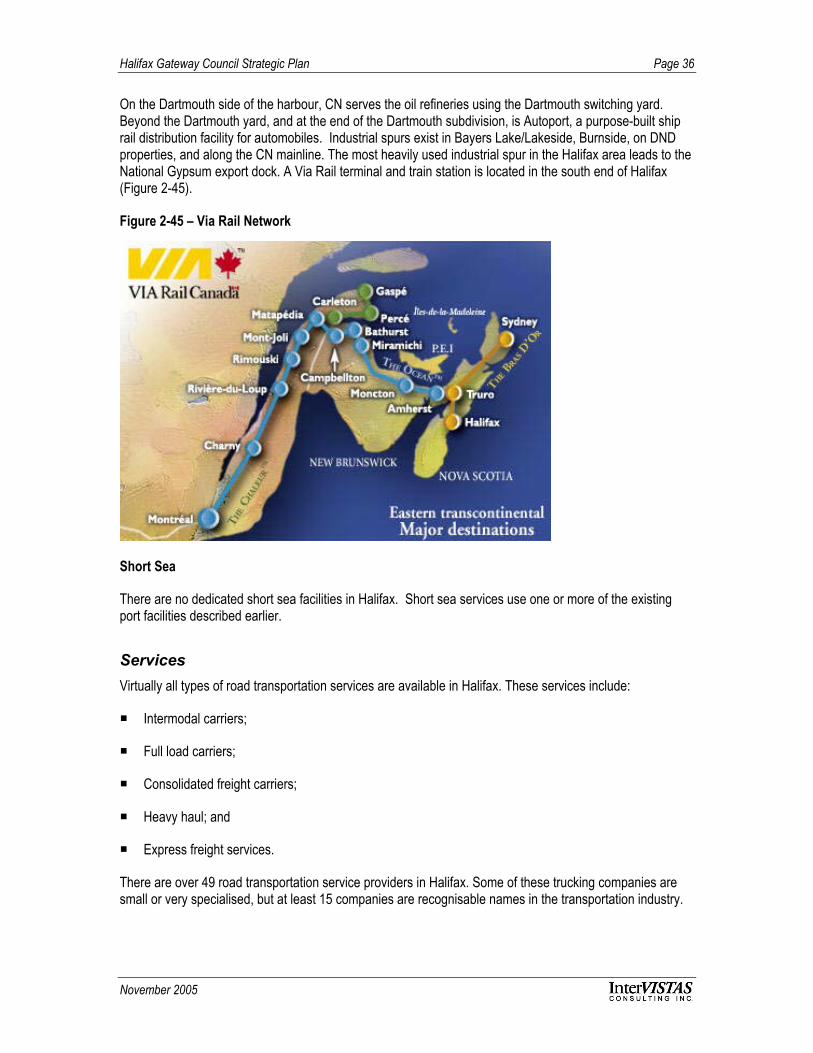

On the Dartmouth side of the harbour, CN serves the oil refineries using the Dartmouth switching yard.Beyond the Dartmouth yard, and at the end of the Dartmouth subdivision, is Autoport, a purpose-built shiprail distribution facility for automobiles. Industrial spurs exist in Bayers Lake/Lakeside, Burnside, on DNDproperties, and along the CN mainline. The most heavily used industrial spur in the Halifax area leads to theNational Gypsum export dock. A Via Rail terminal and train station is located in the south end of Halifax(Figure 2-45).

Figure 2-45 – Via Rail Network

Short Sea

There are no dedicated short sea facilities in Halifax. Short sea services use one or more of the existingport facilities described earlier.

ServicesVirtually all types of road transportation services are available in Halifax. These services include:

Intermodal carriers;

Full load carriers;

Consolidated freight carriers;

Heavy haul; and

Express freight services.

There are over 49 road transportation service providers in Halifax. Some of these trucking companies aresmall or very specialised, but at least 15 companies are recognisable names in the transportation industry.

Halifax Gateway Council Strategic Plan Page 37

November 2005