guide to the markets · us bull and bear markets 56. europe earnings 57. europe equity valuations...

TRANSCRIPT

Guide to the Markets

MARKET INSIGHTS

Europe | |1Q 2020 As of 31 December 2019

2

Global Market Insights Strategy Team

Vincent JuvynsLuxembourg

Tilmann Galler, CFAFrankfurt

Maria Paola ToschiMilan

Shogo MaekawaTokyo

Lucia Gutierrez MelladoMadrid

Tai HuiHong Kong

Marcella ChowHong Kong

Ian HuiHong Kong

Yoshinori ShigemiTokyo

Kerry Craig, CFAMelbourne

Dr. Jasslyn Yeo, CFASingapore

Karen WardLondon

Ambrose Crofton, CFALondon

Chaoping Zhu, CFAShanghai

Jai Malhi, CFALondon

Manuel Arroyo Ozores, CFAMadrid

Agnes LinTaipei

Michael Bell, CFALondon

Alex Dryden, CFANew York

Samantha AzzarelloNew York

Dr. David Kelly, CFANew York

Dr. Cecelia MundtNew York

Meera Pandit, CFANew York

John ManleyNew York

Tyler Voigt, CFANew York

Gabriela SantosNew York

David LebovitzNew York

Jordan JacksonNew York

Jennie LiNew York

Hannah AndersonHong Kong

Hugh Gimber, CFALondon

3

Page reference Global economy

4. Global growth5. Global Purchasing Managers’ Index (PMI) for manufacturing6. Global unemployment7. Global inflation8. Global core inflation and inflation expectations9. Global central bank policy10. Global currencies11. Global trade12. Productivity and population growth13. US GDP14. US economic health monitor15. US business surveys16. US business investment17. US consumer18. US labour market19. US non-farm payrolls and initial jobless claims20. US Conference Board indicators21. US household and corporate finances22. US inflation23. US Federal Reserve policy rate24. US politics25. US focus: Labour market and confidence26. Eurozone GDP27. Eurozone business investment28. Eurozone consumer29. Eurozone labour market30. Eurozone unemployment31. Eurozone inflation32. European Central Bank policy rate33. Eurozone debt34. Eurozone government debt and bond spreads35. Eurozone focus: Trade and the manufacturing sector36. UK GDP37. UK consumer38. UK inflation39. UK focus: Business investment and fiscal spending40. Japan GDP41. China GDP42. China debt43. China inflation and policy rates44. Emerging market currencies and current account45. Emerging market structural dynamics46. Emerging market focus: China trade and relative EM equity

performance

Equities

47. Global earnings expectations and equity valuations48. Global income49. Global equity sector weights50. Equity issuance and buybacks51. US earnings52. US equity valuations53. US valuations and subsequent returns54. Equities and interest rates55. US bull and bear markets56. Europe earnings57. Europe equity valuations58. Europe equity market and currency59. Europe large, mid and small capitalisation equities60. UK earnings61. UK equity market and currency62. Japan earnings63. Japan equity market and currency64. Emerging market equity drivers65. Emerging market equity valuations and subsequent returns66. Equity focus: Margin pressures67. World stock market returns

Fixed income

68. Fixed income yields and interest rate risk69. Global government bond yields70. US yield curve71. US investment-grade bonds72. US high yield bonds73. Europe and UK investment-grade bonds74. Europe high yield bonds75. Emerging market bonds76. Fixed income focus: Negative-yielding debt and bond market

returns77. Global fixed income spreads and returns

Other assets

78. Commodities79. Gold80. Stock-bond correlation and downside protection81. Alternative investments82. Sustainable investment strategies83. Sustainable investment policy interventions and market size84. Asset return expectations85. The cost of hedging

Investing principles

86. Life expectancy87. The effect of compounding88. Cash investments89. Long-term asset returns90. Annual returns and intra-year declines91. Asset class risk-return trade-off92. S&P 500 and fund flows93. US asset returns by holding period94. Asset class returns (EUR)

4

|GTM – Europe

2020consensus forecast

1,8%

1,1%

1,0%

0,3%

Global growth

Real GDP growth Contribution to global real GDP growth% change year on year % change year on year

Source: (Left) BEA, Bloomberg, Eurostat, Japan Cabinet Office, ONS, Refinitiv Datastream, J.P. Morgan Asset Management. Forecasts are from Bloomberg contributor composite. (Right) Refinitiv Datastream, World Bank, J.P. Morgan Asset Management. EM is emerging markets. DM is developed markets. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

4

Glob

al e

cono

my

UK

US

Eurozone

Japan

China EM ex-ChinaDM ex-USUS

Global

-3

-2

-1

0

1

2

3

4

5

'85 '88 '91 '94 '97 '00 '03 '06 '09 '12 '15 '18-10

-8

-6

-4

-2

0

2

4

6

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

5

50,3 50,1

49,5 49,1

51,0 51,0

46,9 46,3

51,7 50,4

44,1 43,7

47,6 46,2

47,5 47,4

54,1 53,9

49,7 49,5

45,7 47,1

48,8 50,2

48,9 47,5

52,6 52,4

48,9 48,4

51,8 51,5

48,2 49,5

49,4 50,1

49,8 50,8

51,2 52,7

52,9 50,2

48,0 47,1

45,6 47,5

2011 20122008 2009 20102019

2013 2014 2015 2016 2017 2018 2019

India

Indonesia

Greece

Germany

China

USUK

EurozoneFrance

ItalySpain

Ireland

Japan

Korea

Global

Developed

Emerging

Taiwan

MexicoBrazil

Russia

SwitzerlandSweden

Euro

zone

Dev

elop

edEm

ergi

ngGlobal Purchasing Managers’ Index (PMI) for manufacturing

Source: Markit, J.P. Morgan Asset Management. The Global Purchasing Managers’ Index (PMI) for manufacturing assesses the economic health of the sector by surveying manufacturing businesses regarding output, new orders, stocks of purchases, supplier delivery times and employment. A score of 50 indicates that economic activity is neither expanding nor contracting, above 50 indicates expansion. The colours range from red to yellow to green, where red is below 50, yellow is at 50 and green is above 50. Quarterly averages are shown, except the two most recent monthly data points. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

GTM – Europe |

Glob

al e

cono

my

5

Nov Dec

6

|GTM – Europe

0

2

4

6

8

10

12

14

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Global unemployment

Unemployment rates%

Source: BLS, Eurostat, Japan Ministry of Internal Affairs & Communications, ONS, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

6

US

Eurozone

Japan

UK

7

Global inflation

Source: Bank of Mexico, DGBAS, ECB, Federal Reserve, Goskomstat of Russia, IBGE, India Ministry of Statistics & Programme Implementation, Japan Ministry of Internal Affairs & Communication, Korean National Statistical Office, National Bureau of Statistics China, ONS, Refinitiv Datastream, Riksbank, Statistics Indonesia, Swiss National Bank, J.P. Morgan Asset Management. Figures shown are for headline inflation and are % change year on year. Heatmap colours are based on the respective central bank target inflation rates. Blue is below target, white is at target and red is above target. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

GTM – Europe | 7

India

Indonesia

Greece

Germany

USUK

EurozoneFrance

ItalySpain

Ireland

JapanChina

Korea

GlobalDevelopedEmerging

Taiwan

MexicoBrazil

Russia

SwitzerlandSweden

Euro

zone

Dev

elop

edEm

ergi

ng

2,2 2,1 2,3 2,2 2,2 2,4 2,6 2,7 2,7 2,7 2,8 2,4 2,1 1,9 1,9 2,2 2,4 2,3 2,1 2,1 2,0 1,9 2,0 2,4

1,8 1,8 1,8 1,9 1,8 2,2 2,3 2,4 2,3 2,1 2,3 1,9 1,6 1,4 1,4 1,6 1,8 1,5 1,5 1,4 1,3 1,3 1,2 1,5

2,9 2,5 3,1 2,7 2,7 2,7 3,0 3,1 3,2 3,5 3,5 3,1 2,9 2,7 2,6 3,1 3,3 3,4 3,2 3,2 3,1 3,0 3,3 3,8

1,3 1,3 1,1 1,4 1,2 2,0 2,0 2,2 2,1 2,1 2,3 1,9 1,5 1,4 1,5 1,4 1,7 1,2 1,3 1,0 1,0 0,8 0,7 1,01,2 1,5 1,3 1,7 1,8 2,3 2,3 2,6 2,6 2,5 2,5 2,2 1,9 1,4 1,6 1,3 1,5 1,1 1,4 1,3 1,3 1,1 0,9 1,21,5 1,5 1,2 1,7 1,3 2,5 2,1 2,2 2,1 2,2 2,6 2,2 1,7 1,7 1,7 1,4 2,1 1,3 1,5 1,1 1,0 0,9 0,9 1,21,0 1,2 0,5 0,9 0,6 1,0 1,4 1,9 1,6 1,5 1,7 1,6 1,2 0,9 1,1 1,1 1,1 0,9 0,8 0,3 0,5 0,2 0,2 0,21,2 0,7 1,2 1,3 1,1 2,1 2,3 2,3 2,2 2,3 2,3 1,7 1,2 1,0 1,1 1,3 1,6 0,9 0,6 0,6 0,4 0,2 0,2 0,51,0 0,2 0,4 0,2 0,5 0,8 1,0 0,8 0,9 1,1 1,8 1,1 0,6 0,5 0,8 1,0 1,1 0,6 0,2 0,4 0,1 0,2 -0,3 0,50,5 0,3 0,7 0,5 -0,1 0,7 0,7 1,0 0,9 1,2 1,1 0,8 0,8 0,8 0,7 1,1 1,7 1,0 1,1 0,5 0,6 0,6 0,6 0,81,7 1,6 1,6 2,0 1,8 2,0 2,1 2,2 2,1 2,5 2,4 2,1 2,2 2,0 1,9 1,8 2,1 2,1 1,6 1,5 1,3 1,3 1,6 1,81,1 0,8 0,5 0,7 0,4 1,0 0,9 1,2 1,3 1,1 1,1 1,0 0,8 0,7 0,7 0,7 1,1 0,5 0,7 0,4 0,5 0,1 -0,3 -0,33,0 3,0 2,7 2,5 2,4 2,4 2,4 2,5 2,7 2,4 2,4 2,3 2,1 1,8 1,9 1,9 2,1 2,0 2,0 2,1 1,7 1,7 1,5 1,52,1 2,1 2,2 2,4 2,5 2,8 2,9 2,9 2,7 2,3 2,5 2,2 1,9 1,6 1,5 1,9 2,0 1,8 1,6 1,8 1,7 1,7 1,8 2,11,0 1,4 1,5 1,1 0,6 0,7 0,7 0,9 1,3 1,2 1,4 0,8 0,3 0,2 0,2 0,5 0,9 0,7 0,7 0,5 0,3 0,2 0,2 0,51,8 1,5 2,9 2,1 1,8 1,8 1,9 2,1 2,3 2,5 2,5 2,2 1,9 1,7 1,5 2,3 2,5 2,7 2,7 2,8 2,8 3,0 3,8 4,53,6 3,3 3,2 3,4 3,4 3,2 3,1 3,2 3,2 2,9 3,2 3,2 3,1 2,8 2,6 2,5 2,8 3,3 3,3 3,3 3,5 3,4 3,1 3,01,4 0,8 1,3 1,2 1,5 1,5 1,5 1,1 1,4 2,1 2,0 2,0 1,3 0,8 0,5 0,4 0,6 0,7 0,7 0,6 0,0 -0,4 0,0 0,21,2 0,9 2,2 1,6 2,0 1,8 1,4 1,8 1,5 1,7 1,2 0,3 -0,1 0,2 0,2 0,6 0,7 0,9 0,9 0,4 0,4 0,4 0,4 0,65,2 5,1 4,4 4,3 4,6 4,9 4,9 4,2 3,7 3,7 3,4 2,3 2,1 2,0 2,6 2,9 3,0 3,0 3,2 3,1 3,3 4,0 4,6 5,52,9 2,9 2,8 2,7 2,8 2,9 4,4 4,5 4,2 4,5 4,6 4,0 3,7 3,8 3,9 4,6 4,9 4,7 3,4 3,2 3,4 2,9 2,5 3,36,8 5,6 5,3 5,0 4,6 4,5 4,7 4,8 4,9 5,0 4,9 4,7 4,8 4,4 3,9 4,0 4,4 4,3 4,0 3,8 3,2 3,0 3,0 3,02,5 2,2 2,2 2,3 2,4 2,4 2,3 2,5 3,1 3,4 3,5 3,8 4,3 5,0 5,2 5,3 5,2 5,1 4,7 4,6 4,3 4,0 3,8 3,5

Apr

Mar

2017

Dec

Jan

Feb

2018

Mar

May

Jun

Jul

Aug

Nov

Sep

Oct

Dec Jan

2019

Feb

May

Apr

Jul

Jun

Aug

Sep

Oct

Nov

8

|GTM – Europe

-2

-1

0

1

2

3

4

5

'07 '09 '11 '13 '15 '17 '19

Global core inflation and inflation expectations

Core inflation Market-based inflation expectations% change year on year %, 5y5y inflation swap

Source: (Left) Bank of Japan, BLS, Eurostat, ONS, Refinitiv Datastream, J.P. Morgan Asset Management. CPI is the Consumer Price Index. Core inflation for the US is defined as CPI excluding food and energy. Core inflation for Japan is defined as CPI excluding fresh food and energy. Core inflation for the UK and the eurozone is defined as CPI less energy, food, alcohol and tobacco. Japan core CPI has been adjusted down by 2% from April 2014 to March 2015 to remove the estimated impact of the consumption tax hike over this period. (Right) Bloomberg, J.P. Morgan Asset Management. 5y5y inflation swap represents the market’s expectation of five-year average inflation, starting in five years’ time. Data for Japan starts in March 2007 due to data availability. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Headline inflation target

-2

-1

0

1

2

3

4

5

'07 '09 '11 '13 '15 '17 '19

Japan

UK

US

Eurozone

8

Glob

al e

cono

my

US

Eurozone

Japan

UK

9

|GTM – Europe

0

2

4

6

8

10

12

14

16

18

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Global central bank balance sheet

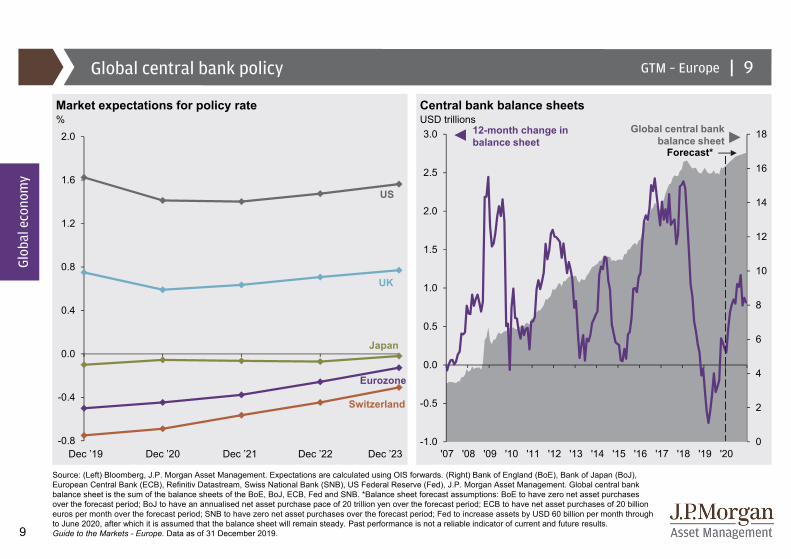

Global central bank policy

Market expectations for policy rate Central bank balance sheets% USD trillions

Source: (Left) Bloomberg, J.P. Morgan Asset Management. Expectations are calculated using OIS forwards. (Right) Bank of England (BoE), Bank of Japan (BoJ), European Central Bank (ECB), Refinitiv Datastream, Swiss National Bank (SNB), US Federal Reserve (Fed), J.P. Morgan Asset Management. Global central bank balance sheet is the sum of the balance sheets of the BoE, BoJ, ECB, Fed and SNB. *Balance sheet forecast assumptions: BoE to have zero net asset purchases over the forecast period; BoJ to have an annualised net asset purchase pace of 20 trillion yen over the forecast period; ECB to have net asset purchases of 20 billion euros per month over the forecast period; SNB to have zero net asset purchases over the forecast period; Fed to increase assets by USD 60 billion per month through to June 2020, after which it is assumed that the balance sheet will remain steady. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

9

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

US

Eurozone

Japan

UK

Switzerland

Dec ’19 Dec ’20 Dec ’22Dec ’21 Dec ’23

Forecast*

12-month change in balance sheet

10

|GTM – Europe

60

70

80

90

100

110

120

130

140

150

160

'75 '77 '79 '81 '83 '85 '87 '89 '91 '93 '95 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

Global currencies

Real effective exchange ratesIndex level rebased to 100 in 2010, broad real effective exchange rate (REER)

Source: J.P. Morgan Securities Research, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

10

USD

EUR

JPY

GBP

11

|GTM – Europe

0 5 10 15 20 25 30 35 40 45-4

-2

0

2

4

6

8

'12 '13 '14 '15 '16 '17 '18 '19

Global trade

Exports of goods Global export volumes% of nominal GDP, 2018 % change year on year, three-month moving average

Source: (Left) IMF Direction of Trade, IMF World Economic Outlook, J.P. Morgan Asset Management. (Right) CPB Netherlands, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe.Data as of 31 December 2019.

Glob

al e

cono

my

11

Brazil

US

Eurozone

Canada

India

China

Russia

Mexico

Japan

Korea

UK

EMGlobalDM

ChinaEM ex-China

US

EurozoneOther

12

|GTM – Europe

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

'58 - '67 '68 - '77 '78 - '87 '88 - '97 '98 - '07 '08 - '18

Productivity and population growth

Drivers of US GDP growth Global working-age population growthAnnualised % change Annualised % change

Source: (Left) BEA, BLS, J.P. Morgan Asset Management. GDP drivers are calculated as the average annualised growth between 4Q from the preceding year in the period and 4Q of the last year of the period. (Right) United Nations (UN) Department of Economic and Social Affairs, J.P. Morgan Asset Management. Working-age population is defined as aged 15-69. Data from 2020 onwards are UN forecasts. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

2000-2020 2020-20401980-2000

Growth in workers + Growth in real output per worker

Growth in real GDP

12

US UK Eurozone Japan

1,6%

2,2%

1,9%

1,4%1,1%

0,7%

2,8% 1,0% 1,3% 1,6% 1,9% 1,1%

4,5%

3,2% 3,2%3,0% 3,0%

1,8%

13

|GTM – Europe

30

35

40

45

50

55

60

65

-8

-6

-4

-2

0

2

4

6

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

US GDP

Contribution to US real GDP growth and ISM composite% change year on year (LHS); index level (RHS)

Source: BEA, Bloomberg, ISM, Refinitiv Datastream, J.P. Morgan Asset Management. The Institute for Supply Management (ISM) composite is an economy-weighted average of the manufacturing and non-manufacturing surveys. A score of 50 indicates that economic activity is neither expanding nor contracting, above 50 indicates expansion. ISM data is shown with quarterly frequency. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Average since 2000 3Q19

2,1% 2,1%

13

Change in inventories

Net exports

Investment

Consumption

Government

ISM composite (RHS)

14

|GTM – Europe

0

10

20

30

40

50

60

70

80

90

100

US economic health monitor

US economic indicatorsPercentile rank relative to historic data since 1990

Source: BLS, Conference Board, ISM, Refinitiv Datastream, J.P. Morgan Asset Management. Elevated recession risk flags are shown when the underlying indicator is at a level consistent with the onset of any of the past three US recessions, as determined by NBER. Transformations used for each of the indicators are: % change year on year for the Leading Economic Index and consumer confidence present situation, index level for Leading Credit Index, ISM non-manufacturing and ISM manufacturing new orders and three-month moving average of monthly absolute change for non-farm payrolls. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Broad indicators

Latest

Higher recession risk

Consumer and services Manufacturing Labour marketElevated

recession risk

Lower recession risk

Key:

14

ConferenceBoard Leading

Economic Index

ConferenceBoard Leading Credit Index

Consumer confidence:

Present situation

ISM non-manufacturing

ISMmanufacturing:

New orders

Non-farm payrolls

15

|GTM – Europe

25

30

35

40

45

50

55

60

65

70

75

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '2035

40

45

50

55

60

65

'98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

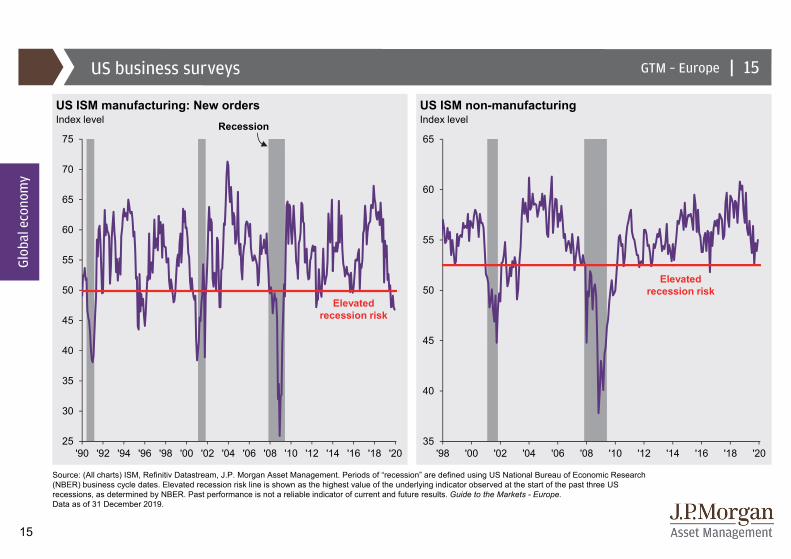

US business surveys

US ISM manufacturing: New orders US ISM non-manufacturingIndex level Index level

Source: (All charts) ISM, Refinitiv Datastream, J.P. Morgan Asset Management. Periods of “recession” are defined using US National Bureau of Economic Research (NBER) business cycle dates. Elevated recession risk line is shown as the highest value of the underlying indicator observed at the start of the past three US recessions, as determined by NBER. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Recession

15

Elevated recession risk

Elevated recession risk

16

|GTM – Europe

-20

-10

0

10

20

30

40

-20

-15

-10

-5

0

5

10

15

20

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

US business investment

US future capex intentions and business investment% change year on year (LHS); index level (RHS)

Source: BEA, Dallas Fed, Duke CFO Global Business Outlook, Haver Analytics, Kansas City Fed, New York Fed, Philadelphia Fed, Refinitiv Datastream, Richmond Fed, J.P. Morgan Asset Management. Future capex intentions is an average index level of the five aforementioned Fed districts equally-weighted, displayed using a three-month moving average. Duke CFO future capex intentions is expected growth in the next 12 months. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Future capex intentionsBusiness investment

Glob

al e

cono

my

16

Duke CFO future capex intentions

17

|GTM – Europe

-100

-75

-50

-25

0

25

50

75

100

125

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

US consumer

US consumer confidence: Present situation US house prices relative to income% change year on year Index level

Source: (Left) Conference Board, Refinitiv Datastream, J.P. Morgan Asset Management. (Right) OECD, Refinitiv Datastream, J.P. Morgan Asset Management. Periods of “recession” are defined using US National Bureau of Economic Research (NBER) business cycle dates. Elevated recession risk line is shown as the highest value of the underlying indicator observed at the start of the past three US recessions, as determined by NBER. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Recession

17

80

90

100

110

120

130

140

'79 '84 '89 '94 '99 '04 '09 '14 '19

Elevated recession risk

18

|GTM – Europe

0

2

4

6

8

10

12

'67 '72 '77 '82 '87 '92 '97 '02 '07 '12 '17

US labour market

US unemployment rate and wage growth%, wage growth is year on year

Source: BLS, Refinitiv Datastream, J.P. Morgan Asset Management. Wage growth is average hourly earnings of total private production and non-supervisory employees. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Unemployment

Wage growth

18

Dec 2019: 3,5%

Dec 2019:3,0%

19

|GTM – Europe

-500

-400

-300

-200

-100

0

100

200

300

400

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

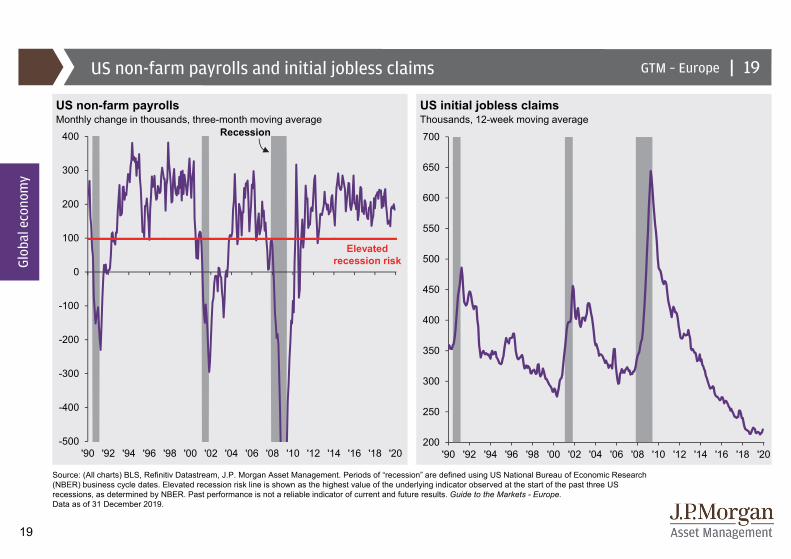

US non-farm payrolls and initial jobless claims

US non-farm payrolls US initial jobless claimsMonthly change in thousands, three-month moving average Thousands, 12-week moving average

Source: (All charts) BLS, Refinitiv Datastream, J.P. Morgan Asset Management. Periods of “recession” are defined using US National Bureau of Economic Research (NBER) business cycle dates. Elevated recession risk line is shown as the highest value of the underlying indicator observed at the start of the past three US recessions, as determined by NBER. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

19

Recession

Elevated recession risk

200

250

300

350

400

450

500

550

600

650

700

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

20

|GTM – Europe

-15

-10

-5

0

5

10

15

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18-4

-2

0

2

4

6

8

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Recession

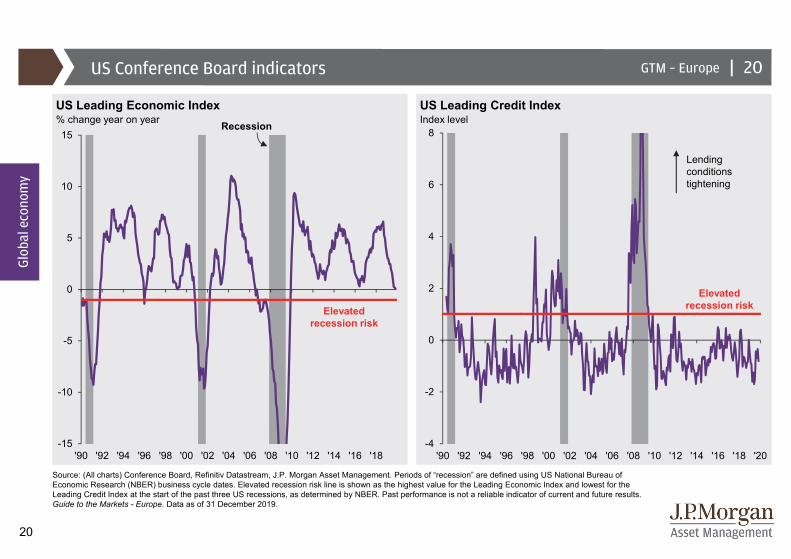

US Conference Board indicators

US Leading Economic Index US Leading Credit Index% change year on year

Source: (All charts) Conference Board, Refinitiv Datastream, J.P. Morgan Asset Management. Periods of “recession” are defined using US National Bureau of Economic Research (NBER) business cycle dates. Elevated recession risk line is shown as the highest value for the Leading Economic Index and lowest for the Leading Credit Index at the start of the past three US recessions, as determined by NBER. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Elevated recession risk

Index level

Elevated recession risk

Lending conditions tightening

Glob

al e

cono

my

20

21

|GTM – Europe

-6

-4

-2

0

2

4

6

50

55

60

65

70

75

80

'90 '94 '98 '02 '06 '10 '14 '180

1

2

3

4

5

6

7

8

9

50

60

70

80

90

100

110

'90 '94 '98 '02 '06 '10 '14 '18

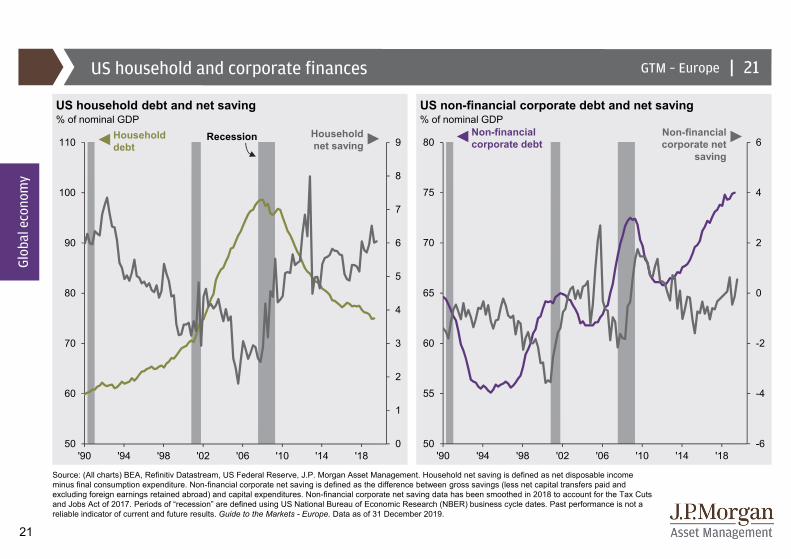

US household debt and net saving US non-financial corporate debt and net saving% of nominal GDP % of nominal GDP

Source: (All charts) BEA, Refinitiv Datastream, US Federal Reserve, J.P. Morgan Asset Management. Household net saving is defined as net disposable income minus final consumption expenditure. Non-financial corporate net saving is defined as the difference between gross savings (less net capital transfers paid and excluding foreign earnings retained abroad) and capital expenditures. Non-financial corporate net saving data has been smoothed in 2018 to account for the Tax Cuts and Jobs Act of 2017. Periods of “recession” are defined using US National Bureau of Economic Research (NBER) business cycle dates. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Recession

US household and corporate finances

Non-financial corporate debt

Non-financial corporate net

saving

Householddebt

Household net saving

Glob

al e

cono

my

21

22

|GTM – Europe

-3

-2

-1

0

1

2

3

4

5

6

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18-2

-1

0

1

2

3

4

5

6

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18

Average since 2000

November2019

Headline CPI 2,2% 2,1%

Core CPI 2,0% 2,3%

US inflation

US headline and core inflation US core goods and services inflation% change year on year % change year on year

Source: (All charts) BLS, Refinitiv Datastream, J.P. Morgan Asset Management. CPI is the Consumer Price Index. Core CPI is defined as CPI excluding food and energy. Core goods CPI is defined as goods CPI excluding food and energy. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

22

Average since 2000

November2019

Services CPI 2,8% 2,9%

Core goods CPI 0,0% 0,1%

Headline inflation target

23

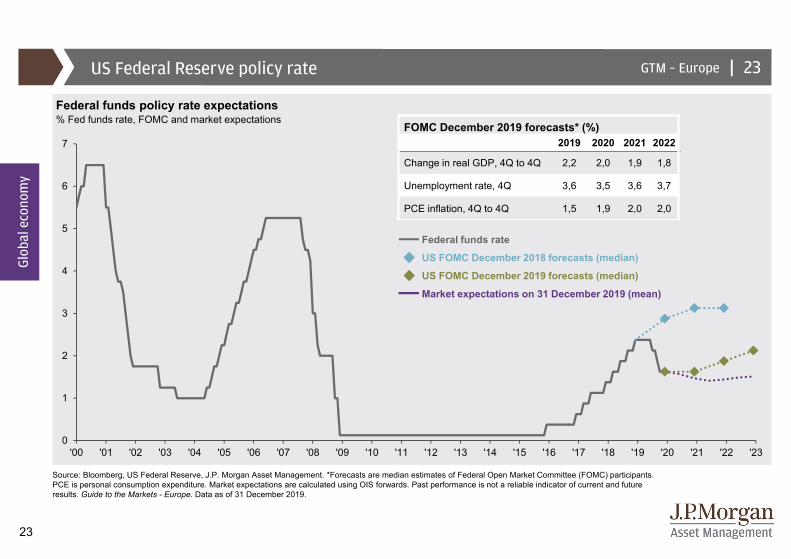

|GTM – EuropeUS Federal Reserve policy rate

Federal funds policy rate expectations% Fed funds rate, FOMC and market expectations

Source: Bloomberg, US Federal Reserve, J.P. Morgan Asset Management. *Forecasts are median estimates of Federal Open Market Committee (FOMC) participants. PCE is personal consumption expenditure. Market expectations are calculated using OIS forwards. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

23

FOMC December 2019 forecasts* (%) 2019 2020 2021 2022

Change in real GDP, 4Q to 4Q 2,2 2,0 1,9 1,8

Unemployment rate, 4Q 3,6 3,5 3,6 3,7

PCE inflation, 4Q to 4Q 1,5 1,9 2,0 2,0

Federal funds rate

Market expectations on 31 December 2019 (mean)

US FOMC December 2019 forecasts (median)

US FOMC December 2018 forecasts (median)

0

1

2

3

4

5

6

7

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23

24

|GTM – Europe

Timeline of the 2020 US presidential election

Jan 2020

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan 2021

Feb-Jun PrimariesDetermine each party’s candidate for the general election

13-16 Jul Democratic National ConventionDemocratic candidate is selected

24-27 Aug Republican National ConventionRepublican candidate is selected

3 Nov Election Day

20 Jan 2021Inauguration Day

29 Sep, 15 Oct, 22 OctPresidential debates

US politics

US voters who have an unfavourable opinion of China%

Source: (Left) Pew Research Center (Spring 2019 Global Attitudes Survey), J.P. Morgan Asset Management. (Right) J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

0

20

40

60

80

100

'05 '07 '09 '11 '13 '15 '17 '19

70%

59%

Republican / Lean Republican

Democrat / Lean Democrat

Glob

al e

cono

my

24

25

|GTM – Europe

1

2

3

4

5

6

7

8

9

'01 '03 '05 '07 '09 '11 '13 '15 '17 '19

US focus: Labour market and confidence

US job openings and hires US CEO and consumer confidenceMillions, monthly Index level

Source: (Left) BLS, Refinitiv Datastream, J.P. Morgan Asset Management. Periods of “recession” are defined using US National Bureau of Economic Research (NBER) business cycle dates. (Right) Conference Board, Refinitiv Datastream, J.P. Morgan Asset Management. Consumer confidence is a three-month moving average. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Job openings

Job hires

10

20

30

40

50

60

70

80

20

40

60

80

100

120

140

160

'90 '93 '96 '99 '02 '05 '08 '11 '14 '17 '20

Consumer confidence

CEO confidence

Recession

25

26

|GTM – Europe

30

35

40

45

50

55

60

65

-8

-6

-4

-2

0

2

4

6

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

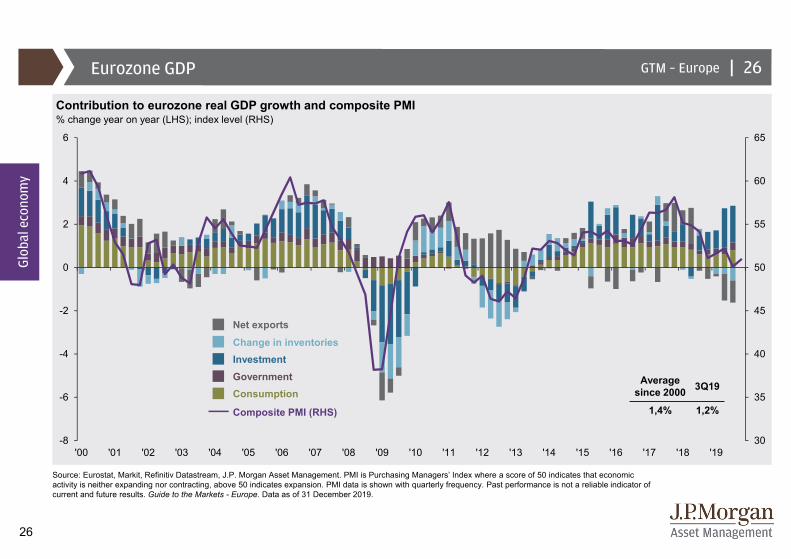

Eurozone GDP

Contribution to eurozone real GDP growth and composite PMI% change year on year (LHS); index level (RHS)

Source: Eurostat, Markit, Refinitiv Datastream, J.P. Morgan Asset Management. PMI is Purchasing Managers’ Index where a score of 50 indicates that economic activity is neither expanding nor contracting, above 50 indicates expansion. PMI data is shown with quarterly frequency. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Average since 2000 3Q19

1,4% 1,2%

26

Change in inventoriesNet exports

Investment

ConsumptionGovernment

Composite PMI (RHS)

27

|GTM – EuropeEurozone business investment

Eurozone future capex intentions and business investment% change year on year (LHS); index level, four-quarter moving average (RHS)

Source: Eurostat, IFO, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

27

-60

-40

-20

0

20

40

60

-16

-12

-8

-4

0

4

8

12

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Future capex intentionsBusiness investment

28

|GTM – Europe

0

50

100

150

200

250

'80 '84 '88 '92 '96 '00 '04 '08 '12 '16 '20-25

-20

-15

-10

-5

0

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Eurozone consumer

Eurozone consumer confidence Eurozone house prices relative to incomeIndex level Index level

Source: (Left) European Commission, Refinitiv Datastream, J.P. Morgan Asset Management. (Right) OECD, Refinitiv Datastream, J.P. Morgan Asset Management. Light grey columns indicate recession in the eurozone. Pre-2000, recessions are determined by a recession occurring in either Germany or at an EU-15 level. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

28

Germany

SpainFrance

Italy

Recession

29

|GTM – Europe

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

4

5

6

7

8

9

10

11

12

13

'98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

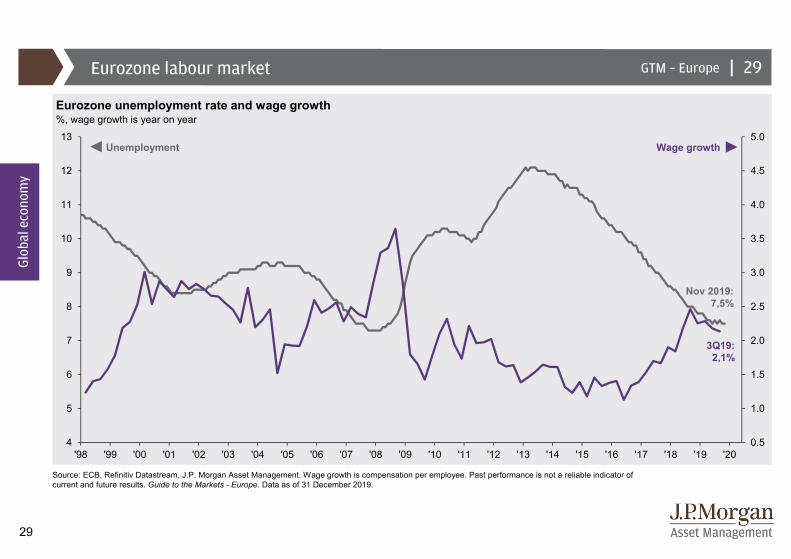

Eurozone labour market

Eurozone unemployment rate and wage growth%, wage growth is year on year

Source: ECB, Refinitiv Datastream, J.P. Morgan Asset Management. Wage growth is compensation per employee. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

29

Wage growthUnemployment

Nov 2019:7,5%

3Q19:2,1%

30

|GTM – Europe

0

4

8

12

16

20

24

28

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Eurozone unemployment

Germany, France, Italy and Spain unemployment rates%

Source: Eurostat, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

30

Spain

Germany

France

Italy

Glob

al e

cono

my

31

|GTM – Europe

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20-1

0

1

2

3

4

5

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

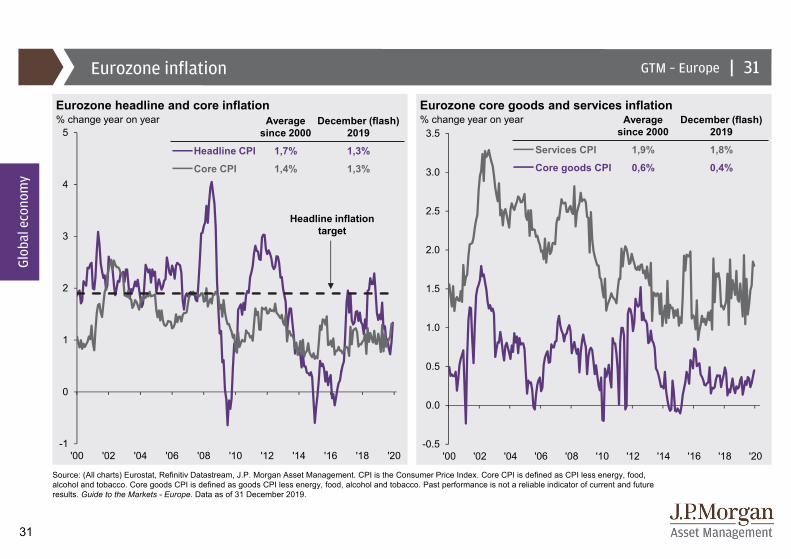

Average since 2000

December (flash)2019

Services CPI 1,9% 1,8%

Core goods CPI 0,6% 0,4%

Eurozone inflation

Eurozone headline and core inflation Eurozone core goods and services inflation% change year on year % change year on year

Source: (All charts) Eurostat, Refinitiv Datastream, J.P. Morgan Asset Management. CPI is the Consumer Price Index. Core CPI is defined as CPI less energy, food, alcohol and tobacco. Core goods CPI is defined as goods CPI less energy, food, alcohol and tobacco. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

31

Headline inflation target

Average since 2000

December (flash)2019

Headline CPI 1,7% 1,3%

Core CPI 1,4% 1,3%

32

|GTM – Europe

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23

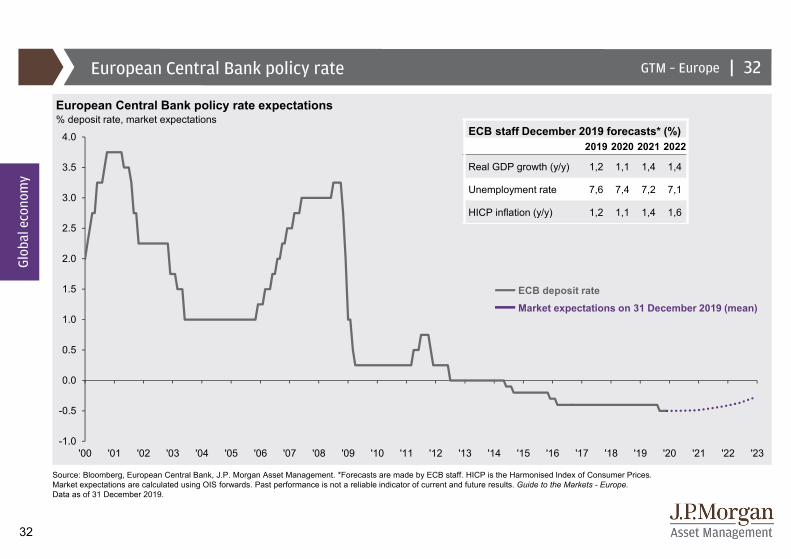

European Central Bank policy rate

European Central Bank policy rate expectations% deposit rate, market expectations

Source: Bloomberg, European Central Bank, J.P. Morgan Asset Management. *Forecasts are made by ECB staff. HICP is the Harmonised Index of Consumer Prices. Market expectations are calculated using OIS forwards. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

ECB deposit rateMarket expectations on 31 December 2019 (mean)

32

ECB staff December 2019 forecasts* (%)2019 2020 2021 2022

Real GDP growth (y/y) 1,2 1,1 1,4 1,4

Unemployment rate 7,6 7,4 7,2 7,1

HICP inflation (y/y) 1,2 1,1 1,4 1,6

33

|GTM – EuropeEurozone debt

Eurozone debt to GDP ratios Eurozone debt service ratios% of nominal GDP % of disposable income

Source: (All charts) Bank for International Settlements, Refinitiv Datastream, J.P. Morgan Asset Management. Debt refers to gross debt. Debt service ratios are a GDP-weighted average of France, Germany, Italy and Spain. For the household sector, gross disposable income is the amount of money that all of the individuals in the household sector have available for spending or saving after income distribution measures (for example, taxes, social contributions and benefits) have taken effect. For the non-financial corporate sector, gross disposable income is essentially akin to gross operating surplus before dividends or interest are paid. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Non-financial corporatesHouseholds

33

32

33

34

35

36

37

38

39

40

5.0

5.5

6.0

6.5

7.0

7.5

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '2040

50

60

70

80

90

100

110

120

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Households

Non-financial corporates

Government

34

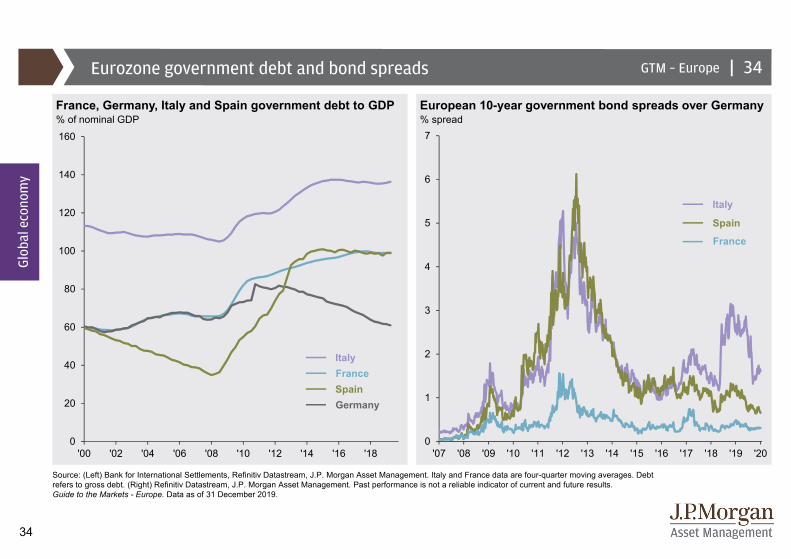

|GTM – EuropeEurozone government debt and bond spreads

France, Germany, Italy and Spain government debt to GDP European 10-year government bond spreads over Germany% of nominal GDP % spread

Source: (Left) Bank for International Settlements, Refinitiv Datastream, J.P. Morgan Asset Management. Italy and France data are four-quarter moving averages. Debt refers to gross debt. (Right) Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results.Guide to the Markets - Europe. Data as of 31 December 2019.

GermanySpainFranceItaly

Glob

al e

cono

my

Spain

France

Italy

34

0

1

2

3

4

5

6

7

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '200

20

40

60

80

100

120

140

160

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18

35

|GTM – EuropeEurozone focus: Trade and the manufacturing sector

Eurozone exports to countries outside the eurozone Manufacturing employment by country% change quarter on quarter, annualised % of total employment

Source: (Left) Eurostat, Refinitiv Datastream, J.P. Morgan Asset Management. Data is using a 12-month rolling sum of the real index value of extra-eurozone exports. (Right) OECD, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

35

-3

-2

-1

0

1

2

3

4

5

6

7

'16 '17 '18 '19

Emerging markets

Total

UK

Rest of world

US

Germany Italy Spain France US0

2

4

6

8

10

12

14

16

18

20

36

|GTM – Europe

30

35

40

45

50

55

60

65

-8

-6

-4

-2

0

2

4

6

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

UK GDP

Contribution to UK real GDP growth and composite PMI% change year on year (LHS); index level (RHS)

Source: Markit, ONS, Refinitiv Datastream, J.P. Morgan Asset Management. PMI is Purchasing Managers’ Index where a score of 50 indicates that economic activity is neither expanding nor contracting, above 50 indicates expansion. PMI data is shown with quarterly frequency. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Average since 2000 3Q19

1,9% 1,1%

36

Glob

al e

cono

my

Change in inventoriesNet exports

Investment

ConsumptionGovernment

Composite PMI (RHS)

37

|GTM – EuropeUK consumer

UK consumer confidence UK house prices relative to incomeIndex level, three-month moving average Index level

Source: (Left) GfK, Refinitiv Datastream, J.P. Morgan Asset Management. (Right) OECD, Refinitiv Datastream, J.P. Morgan Asset Management. Light grey columns indicate recession. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Recession

37

Glob

al e

cono

my

-40

-30

-20

-10

0

10

20

'87 '92 '97 '02 '07 '12 '1740

50

60

70

80

90

100

110

120

130

'87 '92 '97 '02 '07 '12 '17

38

|GTM – Europe

-6

-4

-2

0

2

4

6

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20-1

0

1

2

3

4

5

6

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

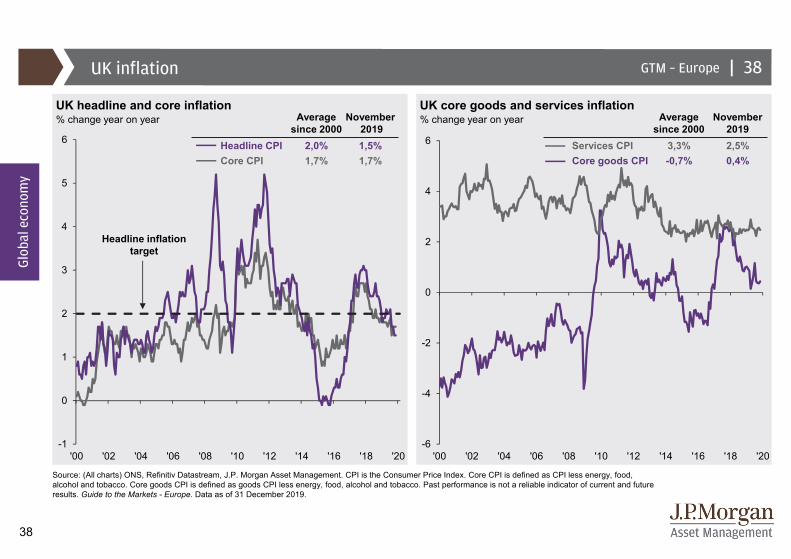

UK inflation

UK headline and core inflation UK core goods and services inflation% change year on year % change year on year

Source: (All charts) ONS, Refinitiv Datastream, J.P. Morgan Asset Management. CPI is the Consumer Price Index. Core CPI is defined as CPI less energy, food, alcohol and tobacco. Core goods CPI is defined as goods CPI less energy, food, alcohol and tobacco. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Average since 2000

November2019

Headline CPI 2,0% 1,5%Core CPI 1,7% 1,7%

Average since 2000

November 2019

Services CPI 3,3% 2,5%Core goods CPI -0,7% 0,4%

38

Glob

al e

cono

my

Headline inflation target

39

|GTM – Europe

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

UK focus: Business investment and fiscal spending

UK and G7 ex-UK real business investment UK real public sector day-to-day spendingIndex level, rebased to 100 in 1Q 2007 % change on 2009-2010

Source: (Left) BoE, J.P. Morgan Asset Management. (Right) Office for Budget Responsibility (OBR), J.P. Morgan Asset Management. Grey line is based on data from the OBR’s March 2019 Economic and fiscal outlook. The purple dot reflects the planned increase in public sector spending for fiscal year 2020/2021 announced in the September 2019 spending review. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Brexit referendum

G7 ex-UK

UK

Glob

al e

cono

my

70

80

90

100

110

120

130

140

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

39

Post Sep ’19 Spending Review: -2.6%

40

|GTM – Europe

30

34

38

42

46

50

54

58

62

-10

-8

-6

-4

-2

0

2

4

6

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Japan GDP

Contribution to Japan real GDP growth and manufacturing PMI% change year on year (LHS); index level (RHS)

Source: Japan Cabinet Office, Markit, Refinitiv Datastream, J.P. Morgan Asset Management. PMI is Purchasing Managers’ Index where a score of 50 indicates that economic activity is neither expanding nor contracting, above 50 indicates expansion. PMI data is shown with quarterly frequency. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Average since 2000 3Q19

0,9% 1,9%

40

Glob

al e

cono

my

Change in inventories

Net exports

Investment

Consumption

Government

Manufacturing PMI (RHS)

41

|GTM – Europe

-5

0

5

10

15

20

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '180

5

10

15

20

25

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

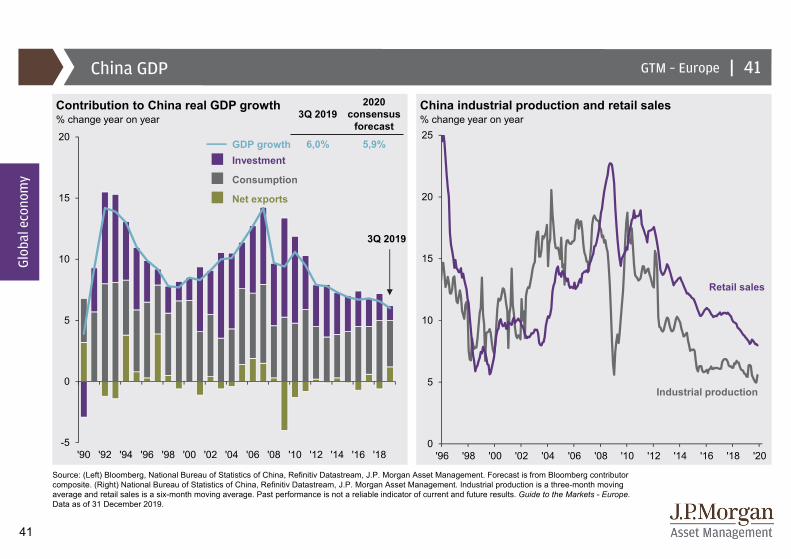

China GDP

Contribution to China real GDP growth China industrial production and retail sales% change year on year % change year on year

Source: (Left) Bloomberg, National Bureau of Statistics of China, Refinitiv Datastream, J.P. Morgan Asset Management. Forecast is from Bloomberg contributor composite. (Right) National Bureau of Statistics of China, Refinitiv Datastream, J.P. Morgan Asset Management. Industrial production is a three-month moving average and retail sales is a six-month moving average. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

41

Industrial production

Consumption

GDP growthInvestment

Net exports

3Q 20192020

consensus forecast

6,0% 5,9%

Retail sales

3Q 2019

42

|GTM – EuropeChina debt

China debt to GDP ratios China credit growth% of nominal GDP % change year on year

Source: (Left) Bank for International Settlements, Refinitiv Datastream, J.P. Morgan Asset Management. Debt refers to gross debt. (Right) People’s Bank of China (PBoC), J.P. Morgan Asset Management. This chart includes three measures of credit ranging from the narrowest – RMB bank lending – to the more extensive broad credit. Specifically, RMB bank lending is the sum of all loans made by the commercial banking system to domestic borrowers. Total social financing (TSF) is all funding to domestic borrowers that is not explicitly backed by the sovereign and thus includes bank lending, trust loans, entrusted loans, bankers’ acceptances, corporate bonds and equity financing by non-financial enterprises, asset-backed securities, loan write-offs and local government “special” bonds. Broad credit is total social financing plus all finance provided by local and central governments. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Households

Government

Glob

al e

cono

my

Non-financial corporates

42

Total social financing

Broad credit

RMB bank lending

0

5

10

15

20

25

30

35

40

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '190

20

40

60

80

100

120

140

160

180

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

43

|GTM – Europe

5

10

15

20

25

30

0

1

2

3

4

5

6

7

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20-10

-5

0

5

10

15

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

China inflation and policy rates

China inflation China interbank rate and reserve requirement ratio (RRR)% change year on year % rate

Source: (Left) Bloomberg, Refinitiv Datastream, J.P. Morgan Asset Management. CPI is the Consumer Price Index. Core CPI is defined as CPI excluding food and energy. PPI is the Producer Price Index. (Right) People’s Bank of China, Refinitiv Datastream, J.P. Morgan Asset Management. Average RRR for large and small banks. SHIBOR is the three-month interbank rate. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Average since 2007

November2019

Headline CPI 2,8% 4,5%Core CPI 1,3% 1,4%Headline PPI 1,1% -1,4%

RRRSHIBOR

Glob

al e

cono

my

43

44

|GTM – Europe

-30

-20

-10

0

10

20

30

'92 '96 '00 '04 '08 '12 '16 '20-2.4

-2.0

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Emerging market currencies and current account

EM currencies vs. US dollar EM current account balance% from fair value, relative to US dollar % of nominal GDP

Source: (Left) J.P. Morgan Asset Management. Fair value is based on nominal exchange rates relative to PPP exchange rates and is adjusted for GDP per capita. (Right) Bloomberg, J.P. Morgan Asset Management. EM currencies and current account balances are created using the current weighted average of JPM GBI-EM Global Diversified Index countries. Current account balance is the balance of a country’s net trade in goods and services, its net earnings on cross-border investments and its net transfer payments. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

44

EM currencies expensive relative to USD

EM current account balance improving

+1 std. dev.

-1 std. dev.

Average

45

|GTM – Europe

USA

JPNDEU

GBRFRA

CAN

ITAESP

AUSNLD

CHN

IND

BRAMEX

TUR

KOR

RUS

IDN

ARG

SAU

THA

HKG

ZAF

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

0 20 40 60 80 100

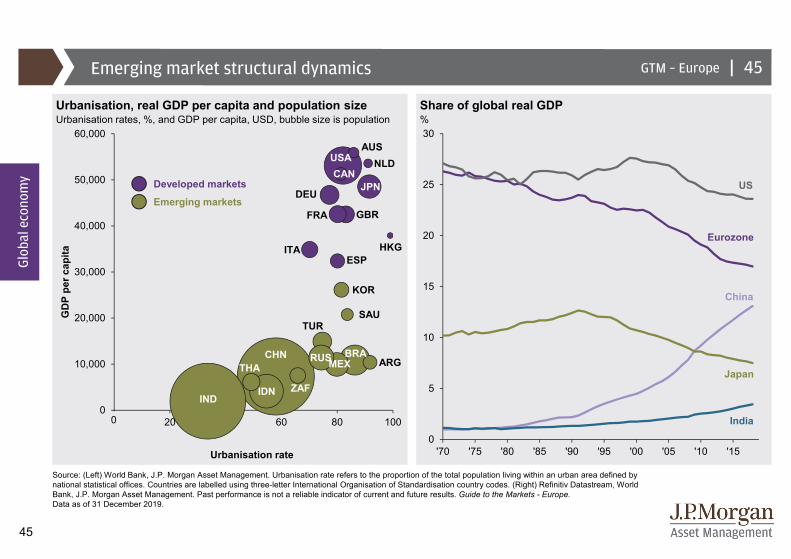

Emerging market structural dynamics

Urbanisation, real GDP per capita and population size Share of global real GDPUrbanisation rates, %, and GDP per capita, USD, bubble size is population %

Source: (Left) World Bank, J.P. Morgan Asset Management. Urbanisation rate refers to the proportion of the total population living within an urban area defined by national statistical offices. Countries are labelled using three-letter International Organisation of Standardisation country codes. (Right) Refinitiv Datastream, World Bank, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe.Data as of 31 December 2019.

GD

P pe

r cap

ita

Urbanisation rate

Glob

al e

cono

my

45

Emerging markets

Developed markets

0

0

5

10

15

20

25

30

'70 '75 '80 '85 '90 '95 '00 '05 '10 '15

US

Eurozone

China

Japan

India

46

|GTM – Europe

35

40

45

50

55

60

65

-50

-40

-30

-20

-10

0

10

20

30

40

50

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

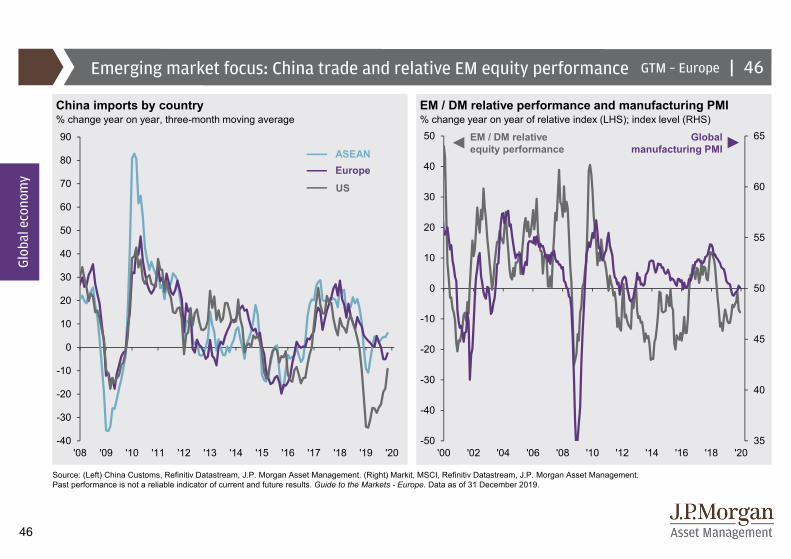

Emerging market focus: China trade and relative EM equity performance

EM / DM relative performance and manufacturing PMI% change year on year of relative index (LHS); index level (RHS)

Source: (Left) China Customs, Refinitiv Datastream, J.P. Morgan Asset Management. (Right) Markit, MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Glob

al e

cono

my

Europe

US

ASEAN

46

China imports by country% change year on year, three-month moving average

Global manufacturing PMI

EM / DM relative equity performance

-40

-30

-20

-10

0

10

20

30

40

50

60

70

80

90

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

47

|GTM – Europe

0x

5x

10x

15x

20x

25x

30x

35x

40x

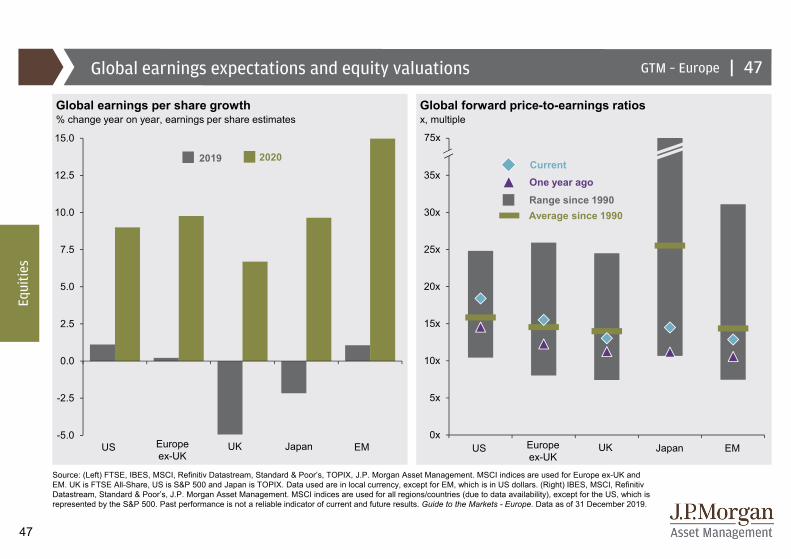

Global earnings expectations and equity valuations

Global earnings per share growth Global forward price-to-earnings ratios % change year on year, earnings per share estimates x, multiple

Source: (Left) FTSE, IBES, MSCI, Refinitiv Datastream, Standard & Poor’s, TOPIX, J.P. Morgan Asset Management. MSCI indices are used for Europe ex-UK and EM. UK is FTSE All-Share, US is S&P 500 and Japan is TOPIX. Data used are in local currency, except for EM, which is in US dollars. (Right) IBES, MSCI, RefinitivDatastream, Standard & Poor’s, J.P. Morgan Asset Management. MSCI indices are used for all regions/countries (due to data availability), except for the US, which is represented by the S&P 500. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

47

Equi

ties

US UKEuropeex-UK

Japan EM

75x

2019 2020

US UKEuropeex-UK

EM

Range since 1990Average since 1990

CurrentOne year ago

Japan-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

15.0

48

|GTM – Europe

0

1

2

3

4

5

6

S&P 500FTSE All-Share MSCI JapanMSCI Europe ex-UK MSCI EMMSCI World

-0.2

0.0 0.5

2.3 2.63.4 4.1 4.2 4.8 4.8 5.5

9.4

-2

0

2

4

6

8

10

MSCI Europe

Cash Global convertibles

EM equity Global REITsGermanBunds

DM high yieldEM debt Global transport

Global infrastructure

Euro IG DM equity

Global income

Equity index yields% yield

Source: (Top) Bloomberg Barclays, BofA/Merrill Lynch, Clarkson, DrewryMaritime Consultants, MSCI, RefinitivDatastream, J.P. Morgan Asset Management.Additional yield often comes with associated capital and/or liquidity risk. Global infrastructure and global transport yields are as of March 2019 and June 2019, respectively. Yields for the bond indices are yield to worst and dividend yields for the equity indices. Global transport levered yield is rental income minus operating expenses, debt amortisation and interest expenses, expressed as a percentage of equity value. Global convertibles: Bloomberg Barclays Global Convertibles; DM equity: MSCI World; EM equity: MSCI EM; German bunds: Germany 10-year yield; Euro IG: Bloomberg Barclays Euro Agg. – Corporates; Global REITs: FTSE NAREIT Index; DM high yield: BofA/Merrill Lynch Developed Markets High Yield Constrained; EM debt: J.P. Morgan EMBI Global; Global infrastructure: MSCI Global Infrastructure Asset Index – Low risk. (Bottom) Bloomberg, FTSE, MSCI, RefinitivDatastream, Standard & Poor’s, J.P. Morgan Asset Management. Buyback yield is last twelve months buybacks divided by the market cap of the index. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

48

Average Europe inflation: 1,5%(12 months to November 2019)

Fixed incomeEquity

Alternatives

% yieldAsset yield comparison

Buyback yield

Dividend yield

49

|GTM – Europe

0

5

10

15

20

25

30

IndustrialsHealth Care Cons. StaplesCons. Discr. EnergyIT MaterialsUtilitiesFinancials Comm. Serv.

0

5

10

15

20

25

IndustrialsHealth Care Cons. StaplesCons. Discr. EnergyIT MaterialsUtilitiesFinancials Comm. Serv.

Global equity sector weights

Global equity sector weights

MSCI World Growth and Value sector weights

% of total market cap

% of total market cap

Source: (Top) MSCI, Refinitiv Datastream, Standard & Poor’s, J.P. Morgan Asset Management. Indices are all MSCI, except for US, which is S&P 500. (Bottom) MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. Real estate is not included in these sector breakdowns due to the small size of the weight in each index. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

49

Europe ex-UK EMUS UK

MSCI World Growth MSCI World Value

50

|GTM – EuropeEquity issuance and buybacks

Breakdown of US net equity issuance Breakdown of European net equity issuanceUSD billions, 12-month rolling USD billions, 12-month rolling

Source: (All charts) Bernstein, Bloomberg, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Buybacks

Net issuanceIssuance

Buybacks

Net issuanceIssuance

Equi

ties

50

-1,200

-1,000

-800

-600

-400

-200

0

200

400

-1,200

-1,000

-800

-600

-400

-200

0

200

400

'04 '06 '08 '10 '12 '14 '16 '18-400

-300

-200

-100

0

100

200

300

400

-400

-300

-200

-100

0

100

200

300

400

'04 '06 '08 '10 '12 '14 '16 '18

51

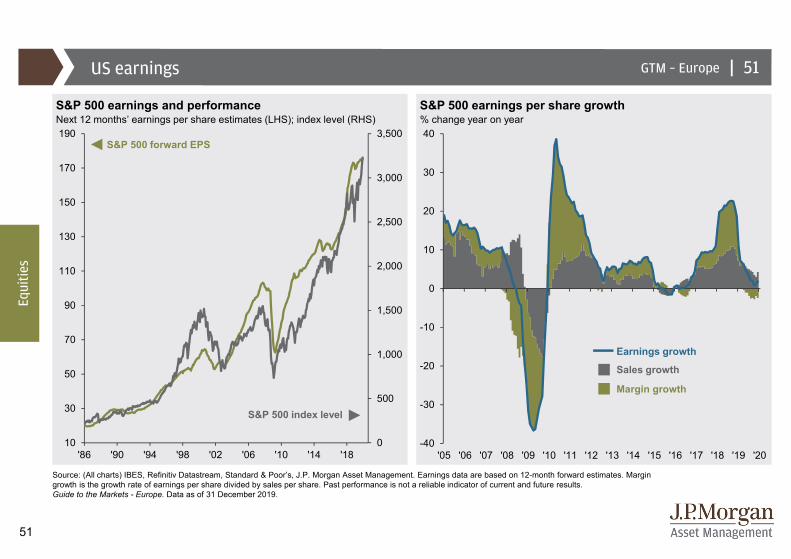

|GTM – EuropeUS earnings

S&P 500 earnings and performance S&P 500 earnings per share growthNext 12 months’ earnings per share estimates (LHS); index level (RHS) % change year on year

Source: (All charts) IBES, Refinitiv Datastream, Standard & Poor’s, J.P. Morgan Asset Management. Earnings data are based on 12-month forward estimates. Margin growth is the growth rate of earnings per share divided by sales per share. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

51

S&P 500 index level

S&P 500 forward EPS

Margin growth

Sales growth

Earnings growth

0

500

1,000

1,500

2,000

2,500

3,000

3,500

10

30

50

70

90

110

130

150

170

190

'86 '90 '94 '98 '02 '06 '10 '14 '18-40

-30

-20

-10

0

10

20

30

40

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

52

|GTM – Europe

-2

-1

0

1

2

3

4

5

6

10

12

14

16

18

20

22

24

26

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20H

ealth

Car

e

Ene

rgy

Fina

ncia

ls

Indu

stria

ls IT

Con

s. S

tapl

es

S&

P 5

00

Com

m. S

erv.

Mat

eria

ls

Con

s. D

iscr

.

Util

ities

US equity valuations

S&P 500 forward P/E ratio S&P 500 forward P/E ratio sector breakdownx, multiple Difference between current P/E multiple and average P/E since 1990

Source: (Left) FactSet, IBES, Refinitiv Datastream, Robert Shiller, Standard & Poor’s, J.P. Morgan Asset Management. P/E ratio calculated using IBES earnings estimates for next 12 months. P/E data may differ from Guide to the Markets - US, which uses FactSet earnings estimates. Shiller cyclically-adjusted P/E (CAPE) is price-to-earnings ratio adjusted using trailing 10-year average inflation-adjusted earnings. P/B ratio is trailing price-to-book ratio. (Right) IBES, Refinitiv Datastream, Standard & Poor’s, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Valuation measureAverage

since 1990

Latest

Shiller CAPE ratio 25,8x 30,0xP/B ratio 2,9x 3,5x

Equi

ties

52

16,2 17,3 13,3 17,0 21,7 20,2 18,4 18,8 18,3 22,1 19,8Current forward P/E ratio

Average: 15,9x

31 Dec 2019:18,4x

Expensive relative to history

53

|GTM – Europe

-20

-15

-10

-5

0

5

10

15

20

25

30

8.0x 11.0x 14.0x 17.0x 20.0x 23.0x-60

-40

-20

0

20

40

60

8.0x 11.0x 14.0x 17.0x 20.0x 23.0x

US valuations and subsequent returns

Forward P/E ratios and subsequent 1-year returns Forward P/E ratios and subsequent 10-year returns%, annualised total return* %, annualised total return*

Source: (All charts) IBES, Refinitiv Datastream, Standard & Poor’s, J.P. Morgan Asset Management. *Dots represent monthly data points since 1988, which is earliest available. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

53

Current levelCurrent level

54

|GTM – EuropeEquities and interest rates

US Fed funds rate and equities/government bonds relative performance% (LHS); relative total return index level, rebased to 100 in 1997 (RHS)

Source: MSCI, Refinitiv Datastream, US Federal Reserve, J.P. Morgan Asset Management. Developed market (DM) equities: MSCI World and DM government bonds: BofA/Merrill Lynch Global Government Index. Index levels are total return in US dollars. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

US Fed funds rate

54

Equi

ties

DM equities outperforming DM

government bonds

DM equities / DM government bonds

50

70

90

110

130

150

170

0

1

2

3

4

5

6

7

8

'97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

55

|GTM – Europe

-60

-50

-40

-30

-20

-10

0

'58 '60 '62 '64 '66 '68 '70 '72 '74 '76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

US bull and bear markets

S&P 500 bull markets, %

S&P 500 bear markets, %

Source: Bloomberg, Standard & Poor’s, J.P. Morgan Asset Management. A bear market represents a 20% or more decline from the previous market high using a monthly frequency; a bull market represents a 20% increase from a market trough. Chart and labels refer to price return. Median values are calculated excluding data from current cycle. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

60 months101%

Duration: 129 monthsPrice return: 378%

147 months582%

32 months74%

50 months86%

74 months126%

60 months229%

43 months80% 26 months

48%

Duration: 17 monthsPrice return: -57%

30 months-49%

3 months-34%

20 months-27%

21 months-48%

18 months-36%

8 months-22%6 months

-28%

Median return in final stages of bull market

12 months: 17% 24 months: 33%

55

Equi

ties 0

100

200

300

400

500

600

'58 '60 '62 '64 '66 '68 '70 '72 '74 '76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

56

|GTM – Europe

-50

-40

-30

-20

-10

0

10

20

30

40

50

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

MSCI Europe earnings per share growth

Europe earnings

MSCI Europe earnings and performanceNext 12 months’ earnings per share estimates, EUR (LHS); index level (RHS) % change year on year

Source: (All charts) IBES, MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. Earnings data are based on 12-month forward estimates. Margin growth is the growth rate of earnings per share divided by sales per share. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

56

MSCI Europe index level

MSCI Europe EPS

Margin growth

Sales growth

Earnings growth

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

20

40

60

80

100

120

140

'88 '92 '96 '00 '04 '08 '12 '16 '20

57

|GTM – Europe

-4

-3

-2

-1

0

1

2

3

4

7

9

11

13

15

17

19

21

23

25

27

'90 '94 '98 '02 '06 '10 '14 '18

Europe equity valuations

MSCI Europe forward P/E ratio MSCI Europe forward P/E ratio sector breakdownx, multiple Difference between current P/E multiple and average P/E since 1995

Source: (Left) FactSet, IBES, MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. P/E ratio calculated using IBES earnings estimates for next 12 months. Cyclically-adjusted P/E (CAPE) is price-to-earnings ratio adjusted using trailing 10-year average inflation-adjusted earnings. P/B ratio is trailing price-to-book ratio. (Right) IBES, MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

31 Dec 2019:14,9x

Average: 14,3x

Valuation measure

Average since 1990 Latest

CAPE ratio 19,4x 19,3xP/B ratio 2,1x 1,9x

57

Equi

ties

14,2 10,9 10,5 21,7 17,3 14,7 14,9 15,3 18,6 15,5 17,7Current forward P/E ratio

Com

m. S

erv.

Ene

rgy IT

Fina

ncia

ls

Indu

stria

ls

MS

CI E

urop

e

Mat

eria

ls

Con

s. S

tapl

es

Con

s. D

iscr

.

Util

ities

Hea

lth C

are

Expensive relative to history

58

|GTM – EuropeEurope equity market and currency

MSCI Europe and euro vs. US dollarIndex level (LHS); US dollars per euro (RHS)

Source: MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

EURUSD

MSCI Europe

Equi

ties

58

Euro depreciating

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

400

600

800

1,000

1,200

1,400

1,600

1,800

'99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

59

|GTM – Europe

50

100

150

200

250

300

350

400

450

500

'95 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

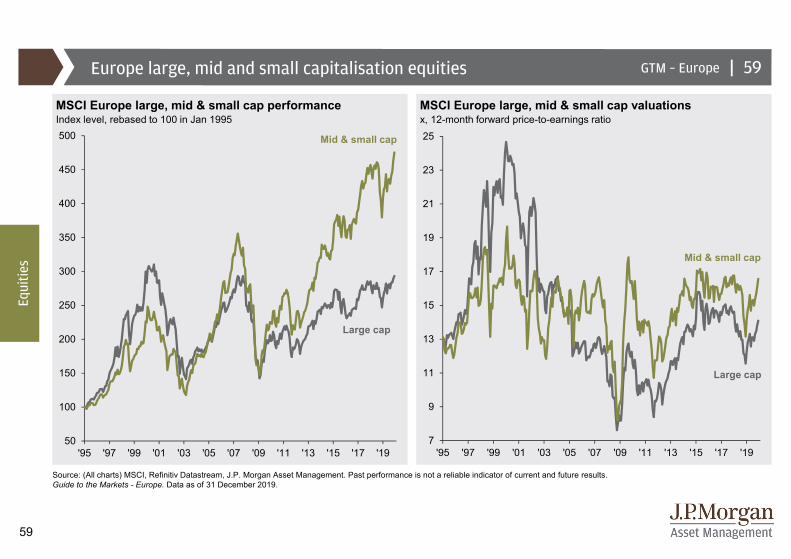

Europe large, mid and small capitalisation equities

MSCI Europe large, mid & small cap performance MSCI Europe large, mid & small cap valuationsIndex level, rebased to 100 in Jan 1995 x, 12-month forward price-to-earnings ratio

Source: (All charts) MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Mid & small cap

Large cap

Mid & small cap

Large cap

59

Equi

ties

7

9

11

13

15

17

19

21

23

25

'95 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

60

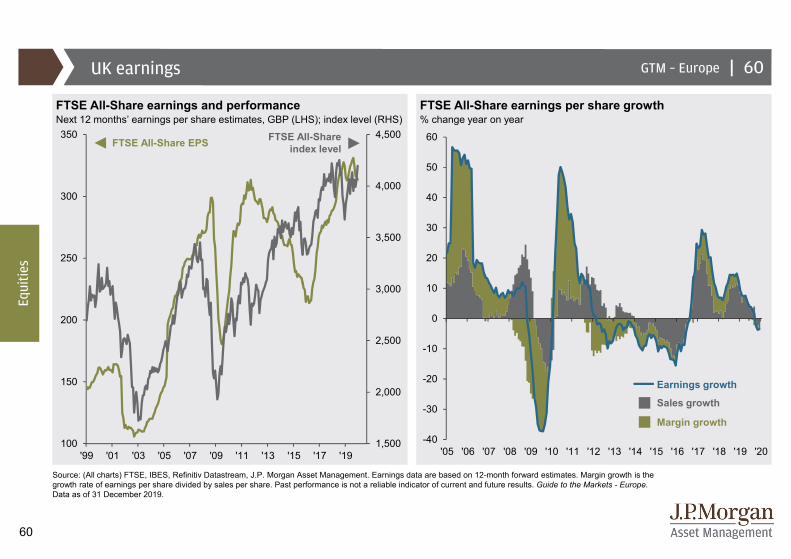

|GTM – EuropeUK earnings

FTSE All-Share earnings and performance FTSE All-Share earnings per share growthNext 12 months’ earnings per share estimates, GBP (LHS); index level (RHS) % change year on year

Source: (All charts) FTSE, IBES, Refinitiv Datastream, J.P. Morgan Asset Management. Earnings data are based on 12-month forward estimates. Margin growth is the growth rate of earnings per share divided by sales per share. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

60

FTSE All-Share index levelFTSE All-Share EPS

Margin growth

Sales growth

Earnings growth

-40

-30

-20

-10

0

10

20

30

40

50

60

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '201,500

2,000

2,500

3,000

3,500

4,000

4,500

100

150

200

250

300

350

'99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

61

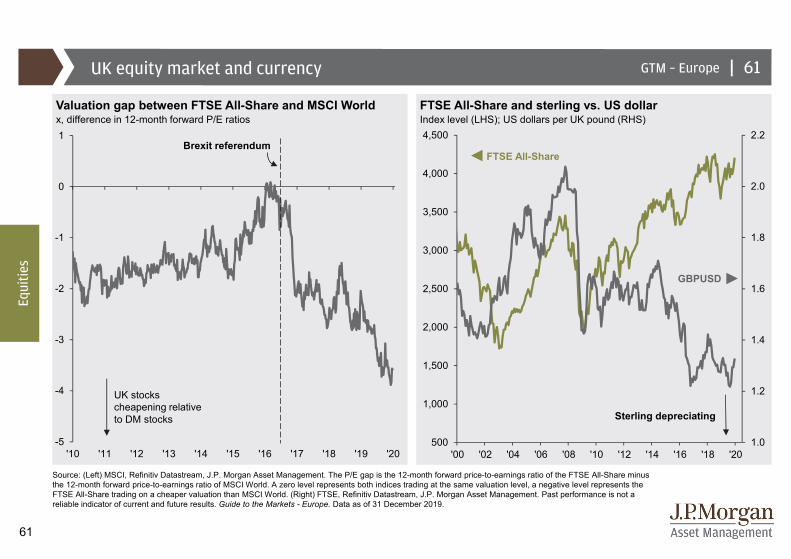

|GTM – EuropeUK equity market and currency

Index level (LHS); US dollars per UK pound (RHS)

Source: (Left) MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. The P/E gap is the 12-month forward price-to-earnings ratio of the FTSE All-Share minus the 12-month forward price-to-earnings ratio of MSCI World. A zero level represents both indices trading at the same valuation level, a negative level represents the FTSE All-Share trading on a cheaper valuation than MSCI World. (Right) FTSE, Refinitiv Datastream, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

61

UK stocks cheapening relative to DM stocks

Valuation gap between FTSE All-Share and MSCI Worldx, difference in 12-month forward P/E ratios

FTSE All-Share and sterling vs. US dollar

1.0

1.2

1.4

1.6

1.8

2.0

2.2

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

GBPUSD

FTSE All-Share

Sterling depreciating

-5

-4

-3

-2

-1

0

1

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Brexit referendum

62

|GTM – Europe

0

500

1,000

1,500

2,000

2,500

3,000

0

20

40

60

80

100

120

140

160

180

'88 '92 '96 '00 '04 '08 '12 '16 '20

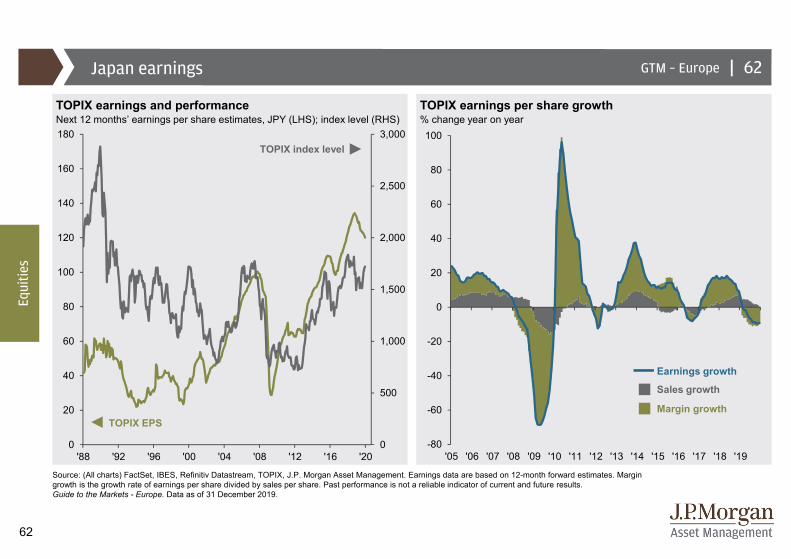

Japan earnings

TOPIX earnings and performance TOPIX earnings per share growthNext 12 months’ earnings per share estimates, JPY (LHS); index level (RHS)

Source: (All charts) FactSet, IBES, Refinitiv Datastream, TOPIX, J.P. Morgan Asset Management. Earnings data are based on 12-month forward estimates. Margin growth is the growth rate of earnings per share divided by sales per share. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

62

% change year on year

TOPIX index level

TOPIX EPSMargin growth

Sales growth

Earnings growth

-80

-60

-40

-20

0

20

40

60

80

100

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

63

|GTM – EuropeJapan equity market and currency

TOPIX and the yen vs. US dollarIndex level (LHS); Japanese yen per US dollar (RHS)

Source: Refinitiv Datastream, TOPIX, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

USDJPY (inverted)

TOPIX

Equi

ties

Yen depreciating

63

70

80

90

100

110

120

130

140400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

64

|GTM – EuropeEmerging market equity drivers

EM / DM relative equity performance and growth gap EM / DM relative equity performance and USD REERRelative index level (LHS); %, next 12 months’ growth estimates (RHS) Relative index level (LHS); index level (RHS)

Source: (Left) Consensus Economics, Refinitiv Datastream, J.P. Morgan Asset Management. “EM minus DM GDP growth” is consensus estimates for emerging markets growth in the next 12 months minus consensus estimates for developed markets growth in the next 12 months, provided by Consensus Economics. (Right) J.P. Morgan Securities Research, MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. For all charts, EM equity is MSCI Emerging Markets and DM equity is MSCI World. Relative equity performance is calculated from price indices in USD, and is rebased to 100 in 1997. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

64

EM equity outperformance & USD weakening

EM growth & equity outperformance

EM minus DM GDP growth

EM / DM relative equity performance

USD REER (inverted)

EM / DM relative equity performance

-1

0

1

2

3

4

5

10

40

70

100

130

160

'97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

85

95

105

115

125

13520

40

60

80

100

120

140

160

180

'97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

65

|GTM – Europe

-20

-10

0

10

20

30

0.8x 1.3x 1.8x 2.3x 2.8x 3.3x0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Emerging market equity valuations and subsequent returns

MSCI EM price-to-book ratio MSCI EM price-to-book ratio and subsequent 10-year returnsx, multiple %, annualised total return*

Source: (All charts) MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. *Dots represent monthly data points since 1996, which is earliest available. MSCI EM Index returns are in USD. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Average: 1,8x

Equi

ties

65

31 Dec 2019:1,7x

Current level

66

|GTM – Europe

0

4

8

12

16

20

24

28

32

36

'86 '90 '94 '98 '02 '06 '10 '14 '186

8

10

12

14

16

18

20

22

24

'86 '90 '94 '98 '02 '06 '10 '14 '18

Equity focus: Margin pressures

US National Federation of Independent Business survey US corporate profit margins% of surveyed companies, three-month moving average %, corporate profits as % of gross value added of corporate business

Source: (Left) NFIB, Refinitiv Datastream, J.P. Morgan Asset Management. Net % of companies planning to raise prices is % of companies planning to increase prices less those planning to reduce prices. (Right) BEA, Refinitiv Datastream, J.P. Morgan Asset Management. Periods of “recession” are defined using US National Bureau of Economic Research (NBER) business cycle dates. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

Equi

ties

Net % companies planning to raise prices

% companies planning to raise wages

After tax

Before tax

Recession

66

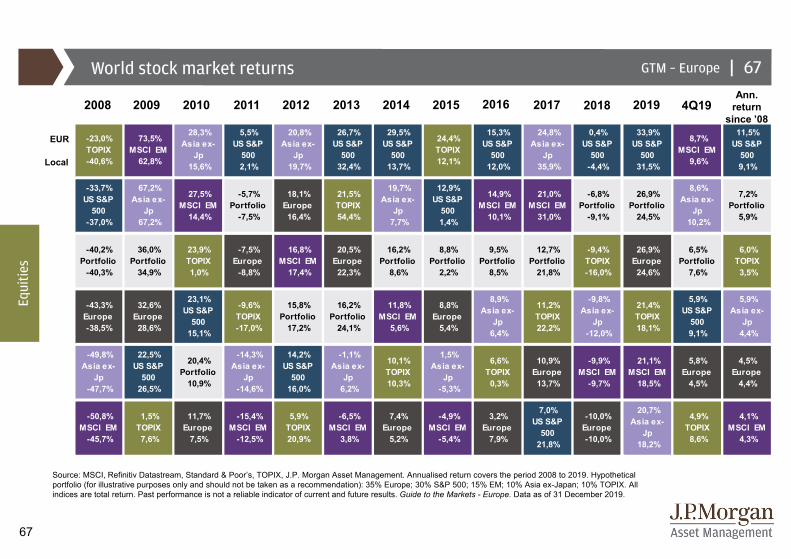

67

-23,0% TOPIX -40,6%

73,5% MSCI EM

62,8%

28,3% Asia ex-

Jp 15,6%

5,5% US S&P

500 2,1%

20,8% Asia ex-

Jp 19,7%

26,7% US S&P

500 32,4%

29,5% US S&P

500 13,7%

24,4% TOPIX 12,1%

15,3% US S&P

500 12,0%

24,8% Asia ex-

Jp 35,9%

0,4% US S&P

500 -4,4%

33,9% US S&P

500 31,5%

8,7% MSCI EM

9,6%

11,5% US S&P

500 9,1%

-33,7% US S&P

500 -37,0%

67,2% Asia ex-

Jp 67,2%

27,5% MSCI EM

14,4%

-5,7% Portfolio

-7,5%

18,1% Europe 16,4%

21,5% TOPIX 54,4%

19,7% Asia ex-

Jp 7,7%

12,9% US S&P

500 1,4%