guide to completing the closing disclosure · pdf fileguide to completing the closing...

TRANSCRIPT

1

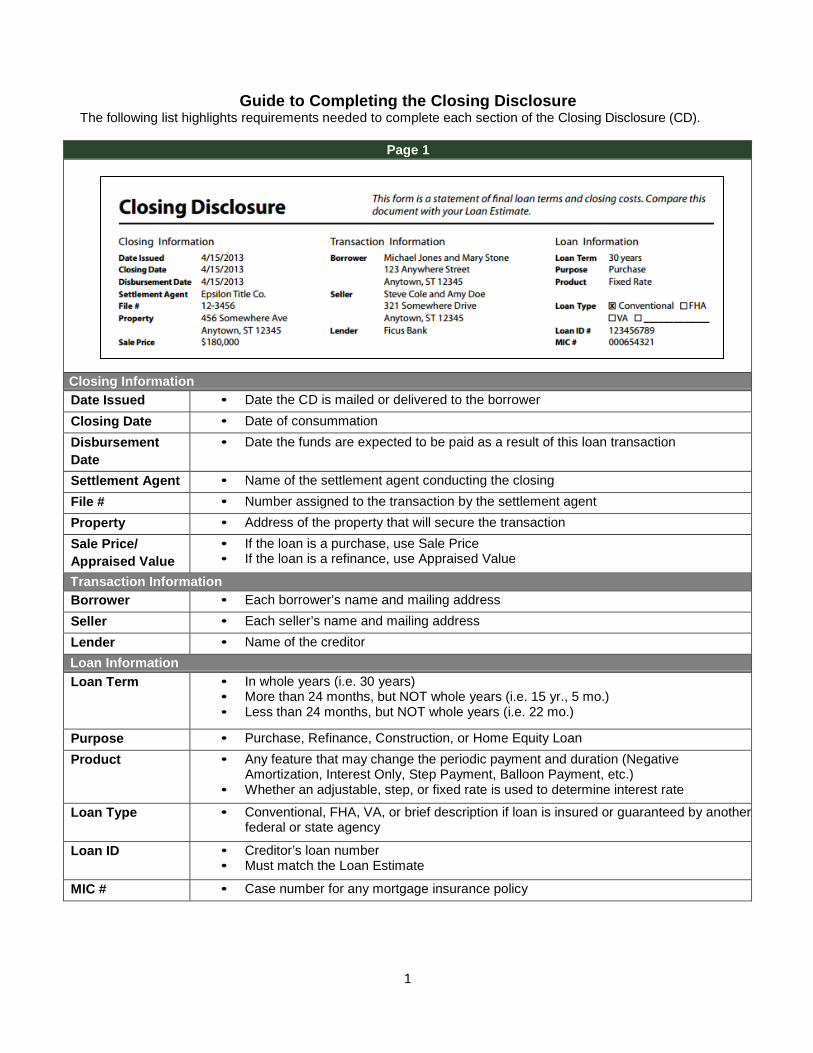

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD).

Page 1

Closing Information Date Issued • Date the CD is mailed or delivered to the borrower Closing Date • Date of consummation Disbursement Date

• Date the funds are expected to be paid as a result of this loan transaction

Settlement Agent • Name of the settlement agent conducting the closing File # • Number assigned to the transaction by the settlement agent Property • Address of the property that will secure the transaction Sale Price/ Appraised Value

• If the loan is a purchase, use Sale Price • If the loan is a refinance, use Appraised Value

Transaction Information Borrower • Each borrower’s name and mailing address Seller • Each seller’s name and mailing address Lender • Name of the creditor Loan Information

Loan Term • In whole years (i.e. 30 years) • More than 24 months, but NOT whole years (i.e. 15 yr., 5 mo.) • Less than 24 months, but NOT whole years (i.e. 22 mo.)

Purpose • Purchase, Refinance, Construction, or Home Equity Loan Product • Any feature that may change the periodic payment and duration (Negative

Amortization, Interest Only, Step Payment, Balloon Payment, etc.) • Whether an adjustable, step, or fixed rate is used to determine interest rate

Loan Type • Conventional, FHA, VA, or brief description if loan is insured or guaranteed by another federal or state agency

Loan ID • Creditor’s loan number • Must match the Loan Estimate

MIC # • Case number for any mortgage insurance policy

2

Loan Terms

Loan Amount • In whole dollars • Indicate whether items can change after closing

• Answering “Yes” requires additional information: • Indication of maximum principal balance for the transaction, • Due date (year or month in which it occurs rather than exact date) • Whether that maximum balance may occur under the terms of the

legal obligation

Interest Rate • Initial interest rate that is applicable at consummation • Indicate whether items can change after closing

• Answering “Yes” requires additional information: • Disclosure of frequency of interest rate adjustments, • The date the interest rate may first adjust, • The maximum interest rate, and • The first date when the loan can reach the maximum interest rate

(year in which the event occurs, counting from the date that the interest for the first scheduled periodic payment begins to accrue after consummation)

• The Adjustable Interest Rate (AIR) Table on page 4

Monthly Principal & Interest

• Initial principal and interest payment due under the terms of the loan • Indicate whether payment can change after closing

• Answering “Yes” requires additional information: • Disclosure of frequency of payment adjustments, • The date the principal and interest payment may first adjust, • The maximum payment possible, and • The first date when the loan can reach the maximum payment.

Prepayment Penalty • Answering “Yes” requires additional information:

• Indicate the maximum amount and • Date when the period during which the penalty may be imposed terminates

Balloon Payment • Answering “Yes” requires the amount and due date of such payment Projected Payments

3

Estimated Total Monthly Payment

• Disclose in one column the initial Period Payment for Principal & Interest, Mortgage Insurance, Estimated Escrow and Estimated Total Monthly Payment.

• Depending on the features of the loan, subsequent payments also may be required to be disclosed.

• Refer to discussion of the standards that must be met for completing this chart in pages 21-27 of the TILA – RESPA Integrated Disclosure – Guide to the Loan Estimate and Closing Disclosure forms

Estimated Taxes, Insurance & Assessments

• Disclose the total monthly amount due for Property Taxes, Homeowner’s Insurance, HOA fees and certain insurance premiums or charges, if required by the lender.

• Include these amounts even if an escrow account will not be established

Costs at Closing

Closing Costs

• The total amount disclosed as Total Closing Costs in the Other Costs table disclosed on page 2 of the CD.

Cash to Close • The estimated amount of cash the borrower will pay at, or receive from, closing.

• This amount is the same as the Cash to Close calculated in the Calculating Cash to Close table on page 3 of the CD.

4

Page 2 Loan Costs

A. Origination Charges

• The items disclosed in the Origination Charges section should generally be the same as they were disclosed on the LE, updated to reflect the terms of the legal obligation at consummation, except:

• Loan originator compensation is disclosed on the CD, even though it is not disclosed on the LE

• Borrower paid compensation to a third-party loan originator is designated as Borrower-Paid At Closing or Before Closing

• Lender paid compensation to a third-party loan originator is designated as Paid by Others

• Compensations to individual loan originators is not disclosed on the CD

B. Services Borrower Did Not Shop For

• Services provided by third parties that borrower was not allowed to select, and • Services that the borrower could have shopped for, but did not, regardless of

where the item was disclosed on the LE. • If the borrower was provided a written list of service providers and the

borrower selected a provider from the list, the fee for the service should be disclosed in section B on the CD.

• Any title-related service or charge must be preceded with the word “Title-” at the beginning

5

C. Services Borrower Did Shop For

• Services provided by third parties that borrower was allowed to select • A written list of settlement service providers that the borrower can consider

when choosing a service (can be as little as one option for each; no limitations on number you have to list), must be provided with the initial LE in order to consider a fee shoppable.

• Any title-related service or charge must be preceded with the word “Title-” at the beginning.

D. Total Loan Costs • Sum of the amounts of Origination Charges, Services You Cannot Shop For, and Services You Can Shop For, disclosed as Borrower-Paid

Other Costs

E. Taxes and Other Government Fees

• An itemization of each amount that is expected to be paid to State and local governments for taxes and government fees

F. Prepaids • Include: Homeowner’s Insurance, Mortgage Insurance, Prepaid Interest, Property Taxes (all four of which are preprinted on form), and space for additional items, as needed

• Must include the applicable time period covered by the amount paid and total amount to be paid

G. Initial Escrow Payment at Closing

• The amount the creditor will require the borrower to place into an escrow account at consummation to be applied to recurring charges for property taxes, homeowner’s and similar insurance, mortgage insurance, HOA dues, and other periodic charges.

• Must include the monthly payment amount and number of months collected at closing.

6

H. Other • An itemization of charges that are required or obtained in the real estate closing by the borrower, seller, or other party that are in addition to the charges disclosed in the other sections

• Items that may go here: Real estate commissions, separate insurance, warranty, guarantee or event- coverage products (Owner’s title insurance, credit life insurance, debt suspension/cancellation coverage, warranties of home appliances & systems)

• Items that disclose any premiums paid for separate insurance, warranty, guarantee, or event-coverage products that are NOT required by creditor MUST include “(optional)” at the end of label

• Any title-related service or charge must be preceded with the word “Title-” at the beginning

I. Total Other Costs (Borrower-Paid)

• Sum of the subtotals of Taxes and Other Government Fees, Prepaids, Initial Escrow Payment at Closing, and Other

J. Total Closing Costs (Borrower-Paid)

• Sum of Total Loan Costs, Total Other Costs, and Lender Credits • When the borrower receives a generalized credit from the creditor for

closing costs, the amount of the credit must be disclosed here as Lender Credits.

• If such a credit is designated for a specific loan cost or other cost, that amount should be reflected in the Paid by Others column in the Closing Cost Details tables and can be designated with an “(L)”.

Page 3 Calculating Cash to Close

Total Closing Costs • Same as the amount disclosed as J. Total Closing Costs in the Other Costs

Section on page 2 of the CD Closing Costs Paid Before Closing

• Same amount designated as Borrower-Paid Before Closing in the Closing Costs Subtotals of the Other Costs table on page 2 of the CD

Closing Costs Financed (Paid from Your Loan Amount)

• List the actual amount of the closing costs that are to be paid out of loan proceeds, if any, stated as a negative number.

7

Down Payment/Funds from Borrower

• Purchase transaction • Difference between purchase price and principal amount of credit

extended, disclosed as a positive number • If loan amount exceeds purchase price, disclose $0

• Non-purchase transaction • Difference between principal amount of credit extended and the total

amount of all existing debt being satisfied in transaction • If positive number, use as your Down Payment • If negative or $0, report $0

Deposit • Only occurs in purchase transaction where borrower has paid money in advance to seller, trust, or escrow held by an attorney/other party under terms of the purchase contract

Funds for Borrower • The amount to be disbursed to the borrower at the time of consummation. • Determined by subtracting from the total amount all existing debt being

satisfied in the transaction. It is disclosed as either a negative number or $0.

Seller Credits • The amount of funds given by the seller to the borrower for generalized credits for closing costs or for allowances for items purchased separately.

• Seller credits are distinguished from payments by the seller for items attributable to periods of time prior to consummation, which are listed under “Adjustments and Other Credits”.

Adjustments and Other Credits

• Calculated by taking the amounts in Section K: Adjustments for Items Paid by Seller in Advance and subtracting Section L: Other Credits, Adjustments, and Adjustments for Items Unpaid by Seller

• May include: proration of taxes or HOA fees, utilities used but not paid for by the seller, rent collected in advance by the seller from a tenant for a period extending beyond the consummation, and interest on loan assumptions.

Cash to Close • Sum of the amounts disclosed above

Summaries of Transactions – Borrower’s Transaction

K. Due from Borrower at Closing

• Sum of Sale Price of Property, Sale Price of Any Personal Property Included in Sale, Closing Costs Paid at Closing (Section J), Other consumer charges not previously disclosed on page 2 of the CD, Adjustments, and Adjustments for Items Paid by Seller in Advance

8

L. Paid Already by or on Behalf of Borrower at Closing

• Sum of Deposit, Loan Amount, Existing Loan(s) Assumed or Taken Subject to, Seller Credits not previously disclosed on page 2, Other Credits not previously disclosed on page 2, and Adjustments for Items Unpaid by Seller

Cash to Close To/From Borrower

• Under the Calculation subheading: • Disclose Total Due from Borrower at Closing (K) as a positive number • Disclose Total Paid Already by or on Behalf of Borrower at Closing (L)

as a negative number • Disclose the sum as Cash to Close From Borrower when the result is a positive

number, and disclose the sum as Cash to Close To Borrower when the result is a negative number. Either way, the sum is shown as a positive number on the disclosure.

Summaries of Transactions – Seller’s Transaction

M. Due to Seller at Closing

• Sum of Sale Price of Property, Sale Price of Any Personal Property Included in Sale, Adjustments, and Adjustments for Items Paid by Seller in Advance.

9

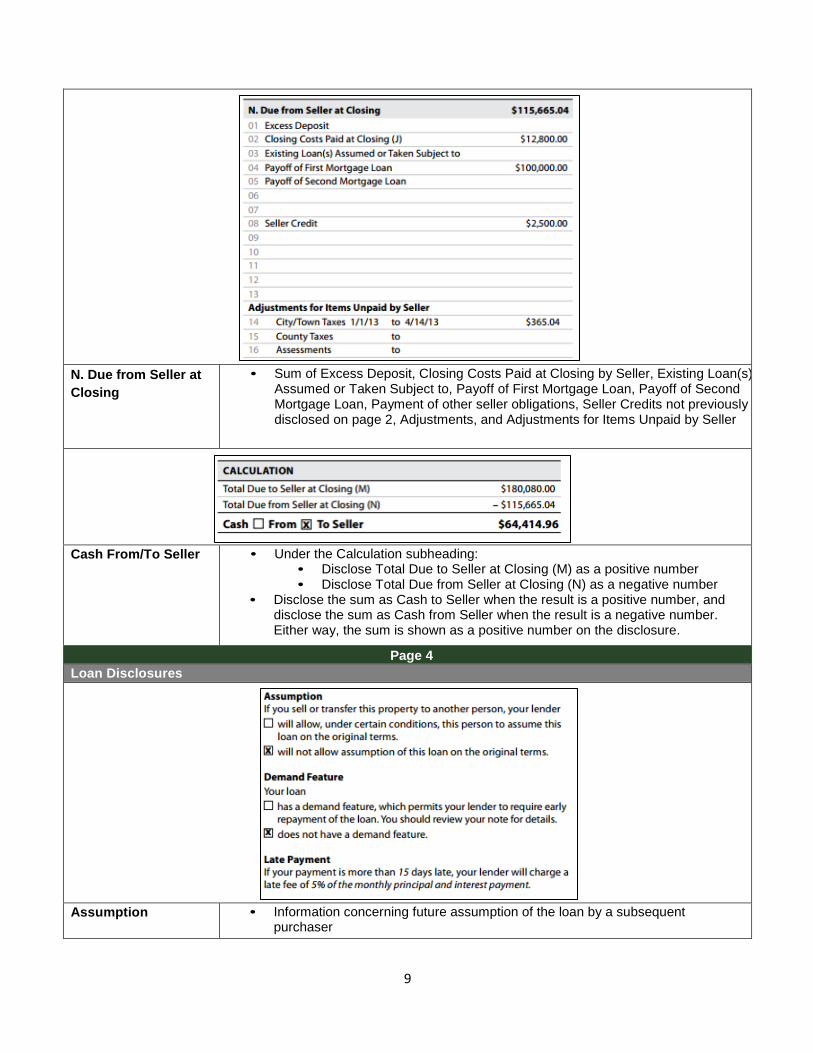

N. Due from Seller at Closing

• Sum of Excess Deposit, Closing Costs Paid at Closing by Seller, Existing Loan(s) Assumed or Taken Subject to, Payoff of First Mortgage Loan, Payoff of Second Mortgage Loan, Payment of other seller obligations, Seller Credits not previously disclosed on page 2, Adjustments, and Adjustments for Items Unpaid by Seller

Cash From/To Seller • Under the Calculation subheading: • Disclose Total Due to Seller at Closing (M) as a positive number • Disclose Total Due from Seller at Closing (N) as a negative number

• Disclose the sum as Cash to Seller when the result is a positive number, and disclose the sum as Cash from Seller when the result is a negative number. Either way, the sum is shown as a positive number on the disclosure.

Page 4 Loan Disclosures

Assumption Information About This

• Information concerning future assumption of the loan by a subsequent purchaser

10

Demand Feature • Whether the legal obligation contains a demand feature that can require early payment of the loan

Late Payment • The terms of the legal obligation that impose a fee for a late payment including the amount of time that passes before a fee is imposed and the amount of the fee or how it is calculated

Negative Amortization • Whether the regular periodic payments can cause the principal balance of the

loan to increase, creating negative amortization

Partial Payments • The creditor’s policy in relation to partial payments by the consumer Security Interest • A statement that the consumer is granting a security interest in the property,

along with identification of the property

11

Escrow Account • When an escrow account is established, disclose: • Amount of Escrowed Property Costs over Year 1, with a list of the

costs that will be paid by the Escrow Account, • Amount of Non-Escrowed Property Costs over Year 1, with a list of the

costs that will not be paid by the Escrow Account, • Initial Escrow Payment, and • Monthly Escrow Payment.

• When an escrow account is not established, disclose: • Amount of Estimated Property Costs over Year 1, and • Amount of any Escrow Waiver Fee imposed for waiving the creation of

an escrow account. • Property Costs include:

• Property Taxes, Homeowner’s Insurance, HOA dues, Ground rent, Leasehold payments, and certain insurance premiums or charges, if required by the lender.

• The Initial Escrow Payment is the same amount disclosed as the subtotal of the Initial Payment at Closing on page 2 of the CD.

12

Adjustable Interest Rate (AIR) Table

Adjustable Interest Rate (AIR) Table

• Used only when the loan’s interest rate may INCREASE after consummation • The same information that was disclosed in the AIR Table on the LE is disclosed

in the AIR Table on the CD, updated to reflect the terms of the loan at consummation

Index and Margin • The index in which adjustments to the interest rate will be based and the margin that is added to the index to determine the interest rate

Initial Interest Rate • Initial Interest Rate at consummation

Minimum/Maximum Interest Rate

• If no maximum interest rate specified in contract, disclose any maximum rate specified in any applicable state law (i.e. State usury law)

• If no minimum interest rate specified in contract or in State law, your margin will serve as minimum interest rate

Change Frequency • For First Change, list the month when the first interest rate change may occur after closing.

• For Subsequent Changes, list the frequency of interest rate adjustments after the initial adjustment.

Limits on Interest Rate Changes

• If multiple limits apply at different points in time or based on different circumstances, you must disclose the greatest limit on changes in the interest rate when making these disclosures

13

Page 5

Loan Calculations Total of Payments • List the total dollar amount the borrower will have paid through the end of the

loan term after the due date of the first periodic payment: • Principal • Interest • Mortgage Insurance • Loan Costs – already disclosed on Page 2, Item D under Loan Costs

Total Interest Percentage (TIP)

• Total amount of interest the borrower will pay over the loan term, expressed as a percentage of the loan amount.

• Use the same standards used when calculating the amount of the interest component of Finance Charges for your old Fed Box Reg Z disclosures.

Other Disclosures Appraisal • A statement related to the consumer’s rights in relation to any appraisal

conducted for the property must be provided for Higher-priced Mortgage Loans (HPML), and Loans covered by the Equal Credit Opportunity Act (ECOA).

Contract Details • A statement informing the consumer of consequences of nonpayment, what constitutes default, when a creditor can accelerate maturity, and prepayment rebates and penalties pursuant to contract details

Liability After Foreclosure

• Must include in the Other Considerations disclosures if the purpose of the credit transaction is to refinance an extension of credit, a brief statement that certain State law protections against liability for any deficiency after foreclosure may be lost, the potential consequences of the loss of such protections, and a statement that the borrower should consult an attorney for additional information

14

Refinance • A statement concerning the consumer’s ability to refinance the loan

Tax Deductions • A statement concerning the extent that interest on the loan can be included as a tax deduction by the borrower

Loan Acceptance • Must be included only in circumstances where page 5 does not contain a Confirm Receipt section which includes a similar type of disclosure to applicant

• Must read as follows: • “You do not have to accept this loan because you have received this form

or signed a loan application.”

Questions • A statement directing the borrower to use the contact information disclosed at the bottom of page 5, if they have any questions regarding their loan

• A reference to the CFPB’s website to obtain more information or to submit a complaint

Contact Information

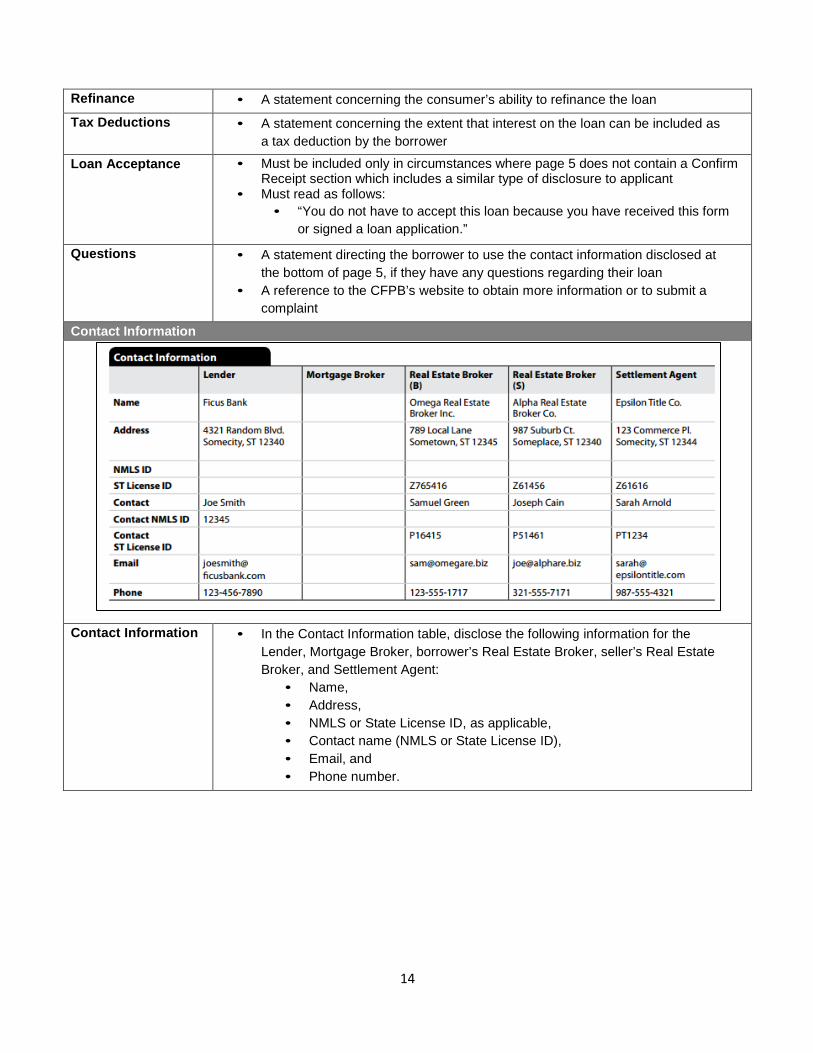

Contact Information • In the Contact Information table, disclose the following information for the

Lender, Mortgage Broker, borrower’s Real Estate Broker, seller’s Real Estate Broker, and Settlement Agent:

• Name, • Address, • NMLS or State License ID, as applicable, • Contact name (NMLS or State License ID), • Email, and • Phone number.

15

Confirm Receipt

Confirm Receipt • The creditor, at its option, may include a line for the signatures of the borrowers to

confirm receipt. If the creditor includes a signature line, the creditor must also include a statement that the signature only signifies receipt of the CD.

• If the creditor does not include statement line or the consumer’s signature, add a statement to the Other Disclosures concerning Loan Acceptance that states: “You do not have to accept this loan because you have received this form or signed a loan application.”