guidance on the process for selecting alternatives to hcfcs in foams

TRANSCRIPT

Guidance on the Process for selectinG alternatives to hcfcs in foams

Sourcebook on technology options for safeguarding the ozone layer and the global climate system

ph

as

e-o

ut o

f h

cfs in

th

e f

le

xib

le a

nd r

igid

fo

am

se

ct

or

2

Guidance on the Process for Selecting Alternatives to HCFCs in Foams Sourcebook on technology options for Safeguarding the Ozone Layer and the Global Climate System

Prepared by:

Caleb Management Services Ltd

The Old Dairy, Woodend Farm

Cromhall, Wotton-Under-Edge

Gloucestershire, GL12 8AA

United Kingdom

July 2010

Copyright © United Nations Environment Programme, 2010

This publication may be reproduced in whole or in part and in any form for educational or non-profit purposes without special permission from the copyright holder, provided acknowledgement of the source is made. UNEP would appreciate receiving a copy of any publication that uses this publication as a source.

No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the United Nations Environment Programme.

Disclaimer

The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the United Nations Environment Programme concerning the legal status of any country, territory, city or area or of its authorities, or concerning delimitation of its frontiers or boundaries. Moreover, the views expressed do not necessarily represent the decision or the stated policy of the United Nations Environment Programme, nor does citing of trade names or commercial processes constitute endorsement.

UNEP Job number: DTI/1281/PA

UNEP DTIE Foam Sourcebook - 2010

3

I ACKNOWLEDGEMENTSThis publication was produced by the UNEP Division of Technology, Industry and Economics (DTIE) OzonAction Branch as part of UNEP’s work programme as an Implementing Agency of the Multilateral Fund for the Implementation of the Montreal Protocol.

The project was managed by the following team in the OzonAction Branch, UNEP DTIE, France:

Mr. Rajendra Shende, Head

Mr. James S. Curlin, Interim Network and Policy Manager

Mr. Ruperto De Jesus, Programme Assistant

This publication was written by:

Mr. Paul Ashford, Managing Director, Caleb Management Services Limited

Prof. Miguel Quintero, Consultant

with support from

Dr. Jason Yapp, Senior Consultant, Caleb Management Services Limited

Ms Hookyung Kim, Project Officer, Caleb Management Services Limited

The quality reviewers were:

Dr. Mike Jeffs, Consultant

Mr. Bert Veenendaal, Principal, RAPPA Inc.

Mr. Bob Russell, President, RJR Consulting

Other reviewers were:

Dr. Ezra Clark, Programme Officer, OzonAction Branch, UNEP DTIE, France

Mr. Etienne Gonin Project Coordinating Consultant, EC JumpStart Project, OzonAction Branch, UNEP DTIE, France

Dr. Janusz Kozakiewicz, Associate Professor, Head of Ozone Layer and Climate Protection Unit, ICRI, Poland

Design:

Mr. Andrew Laver, Creative Director, UK Design

II GLOSSARYABS – Acrylonitrile-butadiene-styrene

CAR – Climate Action Reserve

CDM – Clean Development Mechanism

CEIT – Countries with Economies in Transition

CFC – Chlorofluorcarbons

CHP – Combined Heat and Power

COC – Polyether(C-O-C stretch)

COOC – Polyester(C-O-O-C stretch)

DME – Dimethyl Ether

Executive Committee – Executive Committee of the Multilateral Fund of the Montreal Protocol

FTOC – The UNEP Foams Technical Options Committee

FUA – The functional unit approach

GEF – The Global Environment Fund

GWP – Global Warming Potential

HC – Hydrocarbons

HCFCs – Hydrochlorofluorocarbons

HFC – Hydrofluorocarbons

HFO – Hydrofluoroolefin – an alternative name for unsaturated HFCs

HIPS – High Impact Polystyrene

HPMP – HCFC Phase-out Management Plan

IOC – Incremental Operating Costs

IPCC/TEAP – Intergovernmental Panel on Climate Change, the Technology and Economic Assessment Panel

ISF – Integral skin foam

ISO – International Standards Organisation

ITH – the Integrated Time Horizon

LCA – Lifecycle Assessment

LCCP – Lifecycle Climate Performance

LVC – Low volume ODS consuming country

MCII – The Climate Indicator under development at the MLF secretariat

MDI – Methylene Di-phenyl Di-isocyanate

MF – Methyl Formate

MLF –United Nations Multilateral Fund for the Implementation of the Montreal Protocol

NCO – Polymers containing isocyanate groups

ODP – Ozone Depletion Potential

ODS – Ozone Depleting Substances

OEL – An occupational exposure level

OH – Hydroxyl

World Bank/OORG – The World Bank’s Ozone Operations Resource Group

ORNL – the US Department of Energy’s Oak

Ridge National Laboratory

PFC – Perfluorocarbon

PIR – Polyisocyanurate

PU OCF – Polyurethane One Component Foam

PUR – Rigid Polyurethane

RAC – Refrigeration and Air Conditioning

s-HFCs – Saturated HFCs

SME – Small Medium Enterprises

SNAP – Significant New Alternatives Program

SROC – Special Report on Ozone and Climate (IPCC/TEAP, 2005)

TDI – Toluene diisocyanate

TEWI – Total Equivalent Warming Impact

TLV – Threshold Limit Value

u-HFCs – Unsaturated HFCs

VCM – The Voluntary Carbon Market

VCS – The Voluntary Carbon Standard

VOC – Volatile Organic Compounds

XPS – Extruded polystyrene foams

4

III Why this sourcebook is important

At the Meeting of the Parties that fittingly took place in Montreal in October 2007 to celebrate the establishment of the Montreal Protocol on Substances that Deplete the Ozone Layer 20 years earlier, the Parties entered into an agreement which has taken the Protocol community into a new phase of activity.

Noting that the projected on-going use of hydrochlorofluorocarbons (HCFCs) was likely to place additional and avoidable ozone and climate burdens on the atmosphere, the Parties, in Decision XIX/6 (see full text in Annex 10-3), created a framework within which the phase-out of use of HCFCs could be accelerated over and above the 2016 freeze and final phase-out in 2040 originally foreseen within the Beijing Amendment. The new steps introduced as a result of the Decision imposed an earlier freeze, together with a step-wise country-level reduction in the intervening years leading to a phase-out of HCFC use in most applications by 2030.

For many, the step was clearly necessary in view of the rapid growth in consumption of HCFCs in developing (Article 5) countries as existing HCFC uses continued to grow in importance (e.g. commercial refrigeration) and chlorofluorocarbon (CFC) phase-out requirements necessitated the selection of interim HCFC-based technologies, often on economic grounds.

In practice, the Decision has created a number of precedents, perhaps the most important of which is the fact that Decision XIX/6 is the first under the Montreal Protocol to explicitly address climate concerns in its framework. Although it does not mandate technology choices that are optimal from a climate perspective, the Decision identifies and allocates the responsibilities for consideration of the climate component of technology selection. In doing so, it also requires the development of appropriate methods for assessing climate impacts, not only at product level but also at enterprise level, since the Montreal Protocol continues to provide its technology transition support to the enterprise itself or to the government agencies managing national transitions.

With the ozone obligations from Decision XIX/6 mandated, and the climate components (as well as other environmental effects) requiring assessment and prioritisation, there is now a more complex set of criteria to be managed than has ever been the case before. It is not always the case that what is the best for ozone is best for climate and therefore value judgements need to be made, not only at enterprise level, but also at national compliance level. The introduction of HCFC Phase-out Management Plans (HPMPs) by the Executive Committee of the Multilateral Fund for the implementation of the Montreal Protocol (Executive Committee) aims at ensuring that the overall objectives of Decision XIX/6 are

achieved. However, to be fully effective, these need to straddle the whole phase-out period from 2010 to 2030. This is not possible, at the enterprise level and much of the high-level planning needs to be completed at sectoral level, at the very least. A list of possible legislative and policy options that may facilitate HCFC phase out is included in the booklet published recently by UNEP that can be found at http://www.unep.fr/ozonaction/topics/hcfc.asp

The two main sectors using substantial quantities of HCFCs currently are the refrigeration and air conditioning (RAC) sector on the one hand and the foam sector on the other (see pie chart). The current HCFC usage patterns themselves are only part of the story, since these will change with time depending on the availability of alternative technologies. In addition, factors such as the emission profiles through the lifecycle of the products and equipment using HCFCs affect overall climate impact and all vary considerably between sectors. As a consequence, all of these factors need to be considered in parallel in order to build up the full climate picture (see Section 3). In practice, however, both consumption and emissions from the RAC sector are likely to dominate the consumption and emissions patterns for the foreseeable future.

Even though the RAC sector will remain the primary focus for major climate benefits, the foam sector is still a critical part of

UNEP DTIE Foam Sourcebook - 2010

5!

Estimated Consumption of HCFCs in Developing Countries in 2010(~445,000 tonnes)

Other 2%

Refrigeration and AC 77%

Foams 21%

most HPMPs, since these are driven by consumption criteria only. Accordingly, this Sourcebook provides guidance to the foam sector itself, and those operating both in it and with it, regarding the factors to be considered when choosing alternative technologies within the framework of Decision XIX/6. The guidance also gives consideration to methods of quantifying and potentially financing climate benefits, although notes that not all alternative technologies are, by definition, favourable to climate.

This Sourcebook builds on earlier technology and policy materials, developed by UNEP OzonAction to assist the foam industry in Article 5 countries to phase out CFCs, and seeks to continue and further develop that same capacity-building and information sharing service.

Source: IPCC/UNEP data

6

Contents

UNEP DTIE Foam Sourcebook - 2010

7

I ACKNOWLEDGEMENTS 3

II Glossary 3

III WHY THIS SOURCEBOOK IS IMPORTANT 4

1 INTRODUCTION 8

1.1 THE CHALLENGE OF ACCELERATED HCFC PHASE-OUT 9

1.2 GUIDANCE ON THE USE OF THIS SOURCEBOOK 10

2 THE INTERFACE BETWEEN OZONE DEPLETION & CLIMATE CHANGE 12

2.1 MEASURING IMPACTS – ODP, GWP AND CARBON INTENSITY 13

2.2 DECISION XIX/6 AND THE FRAMEWORK FOR MITIGATION 15

2.3 POTENTIAL BENEFITS FOR BUSINESS AND THE ENVIRONMENT 16

3 METHODS OF QUANTIFYING CLIMATE IMPACT 18

3.1 LIFECYCLE APPROACHES BASED ON DIRECT EMISSIONS ONLY 19

3.2 LIFE CYCLE APPROACHES ALSO CONSIDERING ENERGY 20

3.3 HYBRID APPROACHES (e.g. Functional Unit & Climate Indicators) 21

4 FOAM MANUFACTURE AND EXISTING FLUOROCARBON TECHNOLOGIES 24

4.1 AN INTRODUCTION TO FOAM TYPES25 25

4.2 FOAM MANUFACTURE AND THE ROLE OF BLOWING AGENTS 29

4.3 POINTS IN THE SUPPLY CHAIN WHERE CONSUMPTION OCCURS (fully formulated polyol issue) 31

4.4 REASONS FOR ORIGINAL SELECTION OF CFCs & HCFCs 32

4.5 REASONS WHY HFCs ARE POTENTIAL REPLACEMENTS FOR HCFCs 34

4.6 WHY HFCs CAN BE SUB-OPTIMAL SOLUTIONS FOR CLIMATE 35

5 GENERAL REVIEW OF ALTERNATIVE BLOWING AGENTS 40

5.1 HYDROCARBONS (both directly added and pre-blended) 41

5.2 LIQUID CARBON DIOXIDE 42

5.3 IN-SITU CARBON DIOXIDE (water blown foams) 42

5.4 OXYGENATED HYDROCARBONS (Methyl Formate, Methylal and Dimethyl Ether) 42

5.5 CHLORINATED HYDROCARBONS (Methylene Chloride, Trans-1,2 di-chloroethylene and 2-chloropropane) 44

5.6 SATURATED HFCs 45

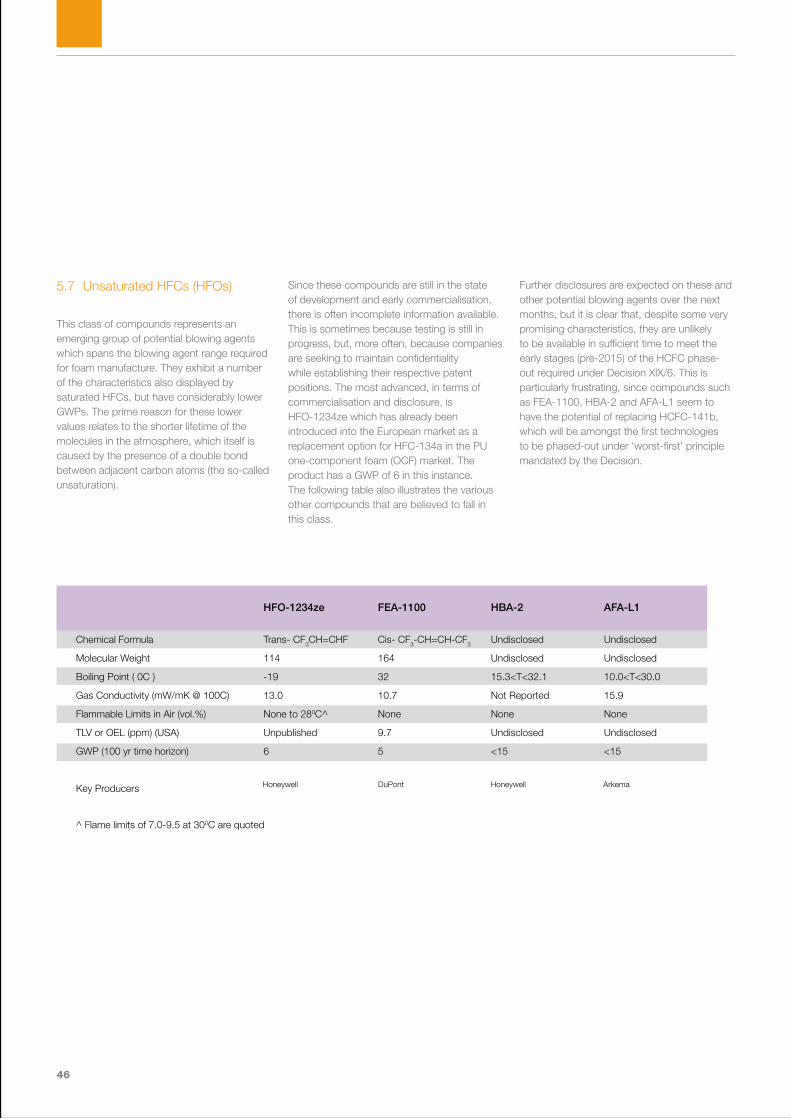

5.7 UNSATURATED HFCS (HFOS) 46

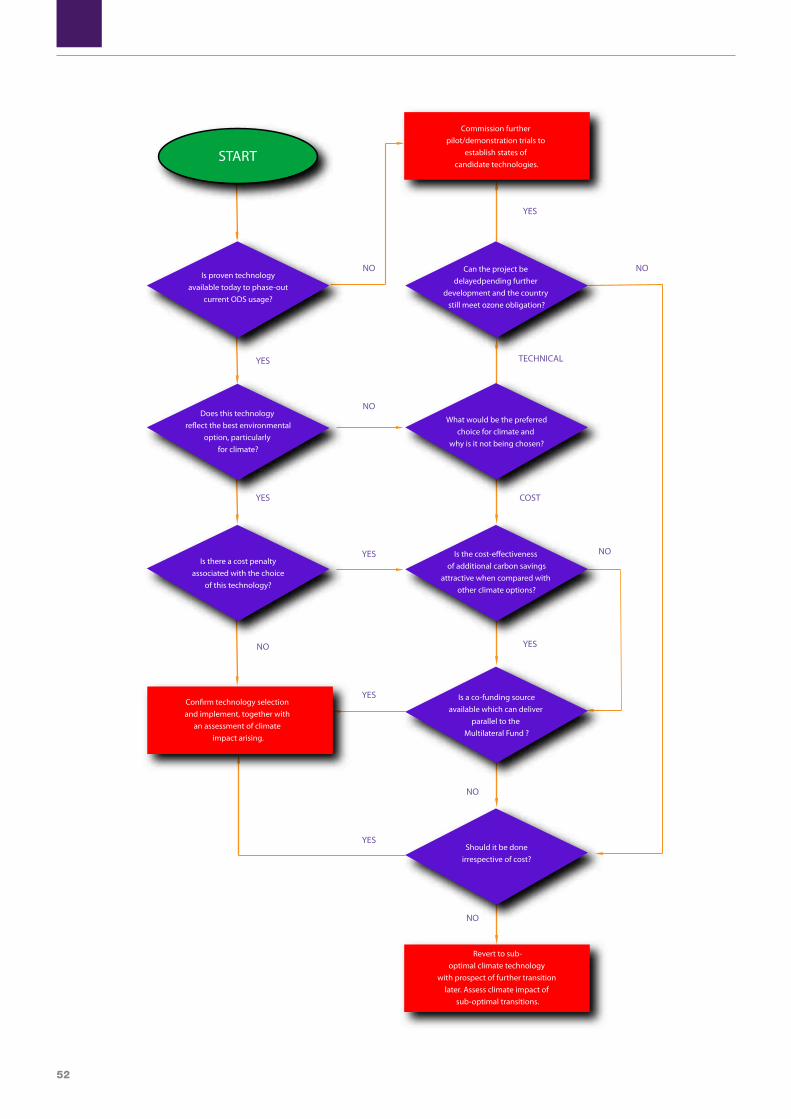

6 DECISION-MAKING PROCESS 48

6.1 ESTABLISHING TECHNICAL FEASIBILITY & ECONOMIC VIABILITY 49

6.2 EVALUATING SAFETY ASPECTS & ENVIRONMENTAL IMPACT 50

6.3 ASSESSING COST EFFECTIVENESS AND PRACTICALITY 51

6.4 SUMMARY DECISION TREE 51

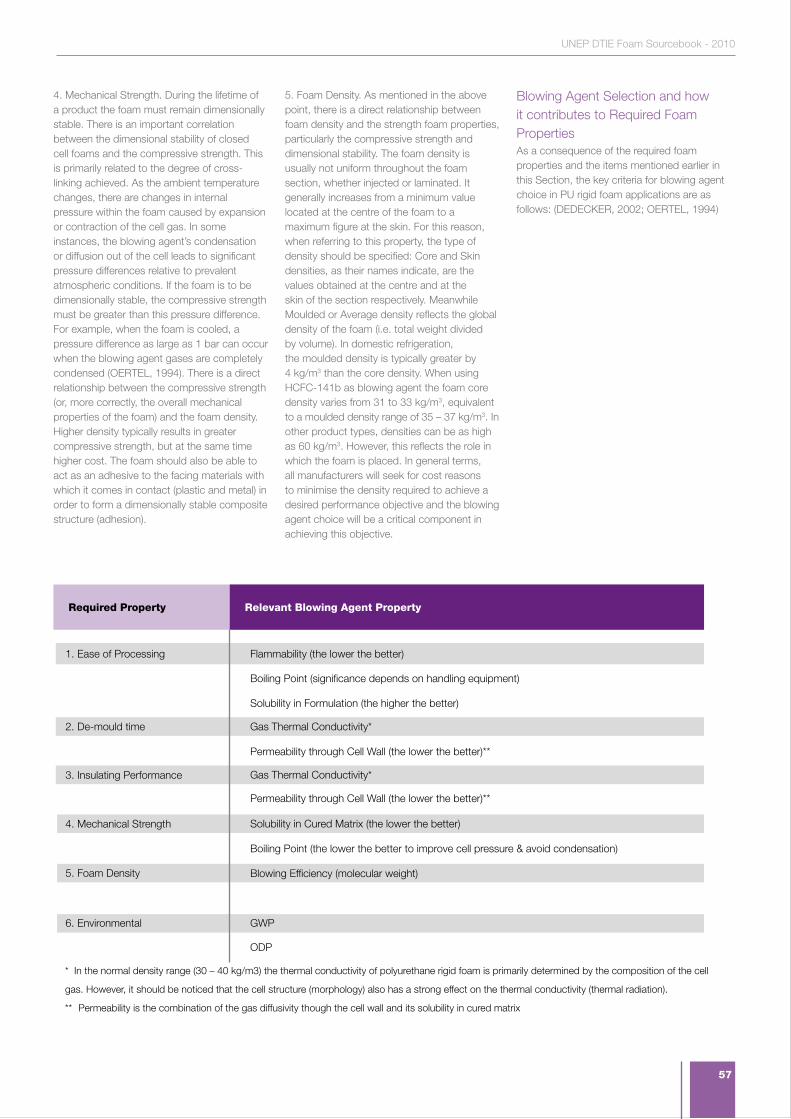

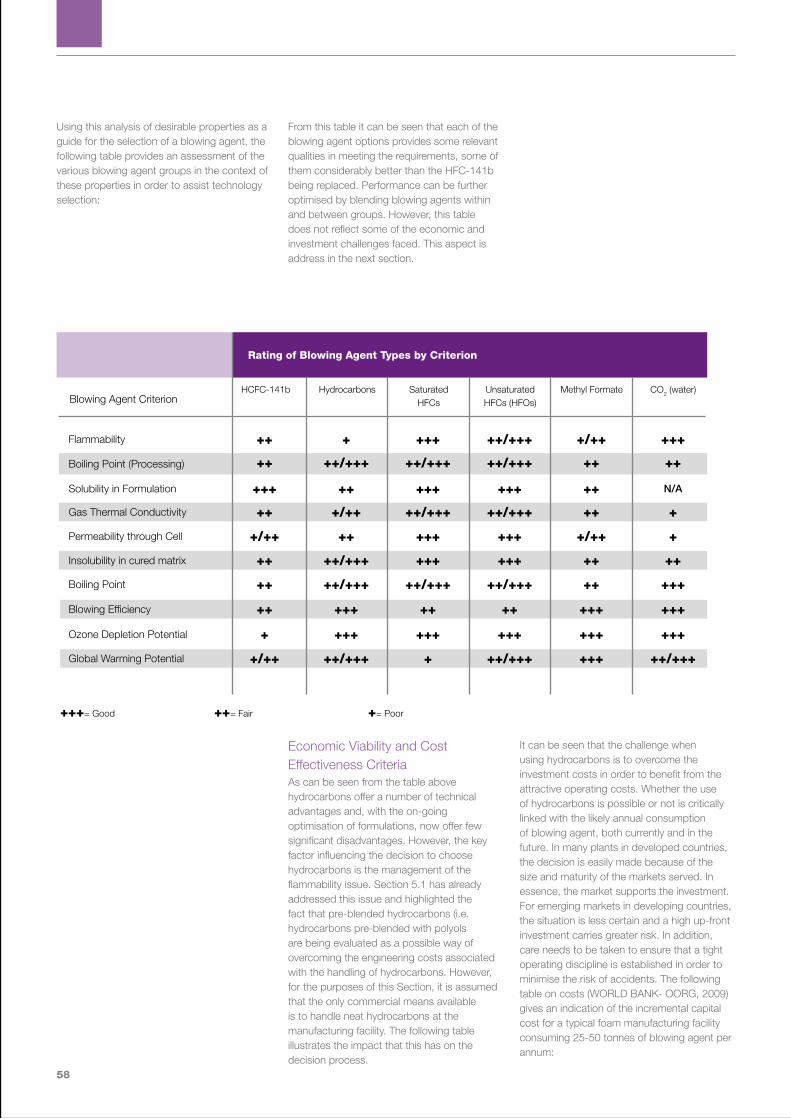

7 REVIEW OF SPECIFIC FACTORS INFLUENCING THE SELECTION OF ALTERNATIVE TECHNOLOGIES AT APPLICATION LEVEL 54

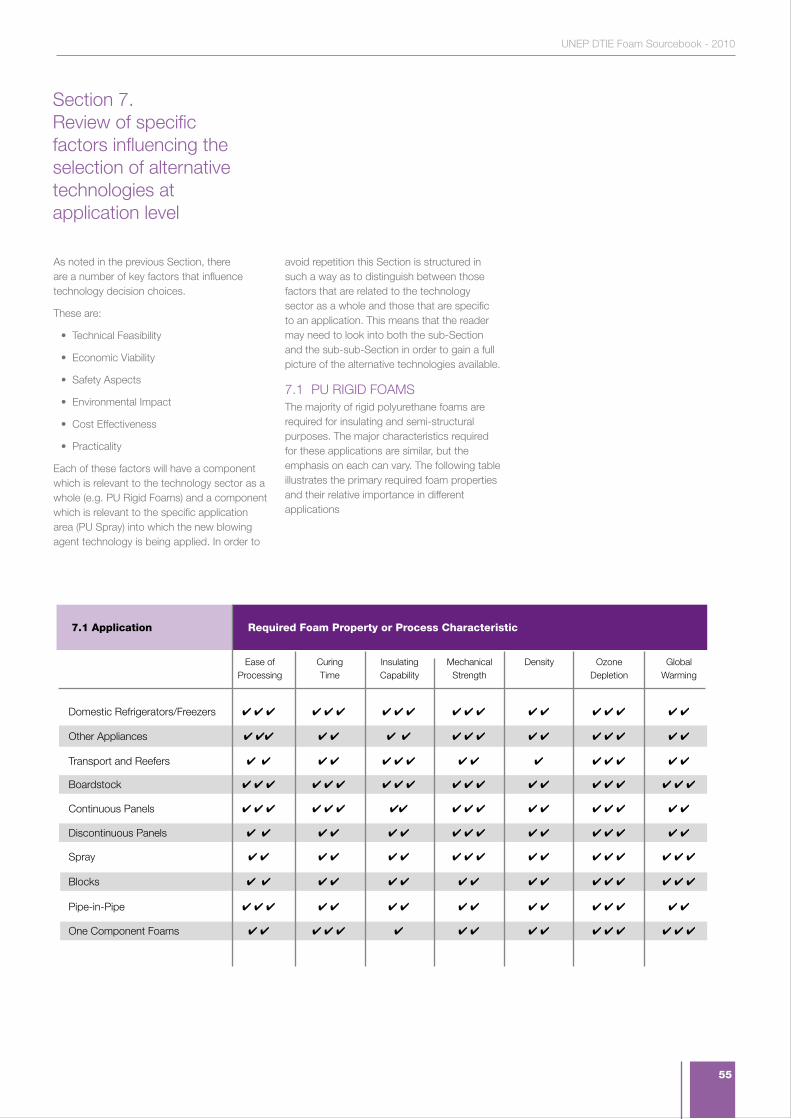

7.1 PU RIGID 55

7.1.1 PU RIGID – Domestic Refrigerators & Freezers 61

7.1.2 PU RIGID – Other Appliances 63

7.1.3 PU RIGID – Transport and Reefers 65

7.1.4 PU RIGID - Boardstock 67

7.1.5 PU RIGID – Continuous Panels 68

7.1.6 PU RIGID – Discontinuous Panels 69

7.1.7 PU RIGID – Spray 70

7.1.8 PU RIGID – Blocks 72

7.1.9 PU RIGID – Pipe-in-Pipe 73

7.1.10 PU RIGID – One Component Foam 74

7.2 PU FLEXIBLE FOAMS 75

7.2.1 PU FLEXIBLE – Integral Skin (Automotive) 79

7.2.2 PU FLEXIBLE – Integral Skin (Automotive) 80

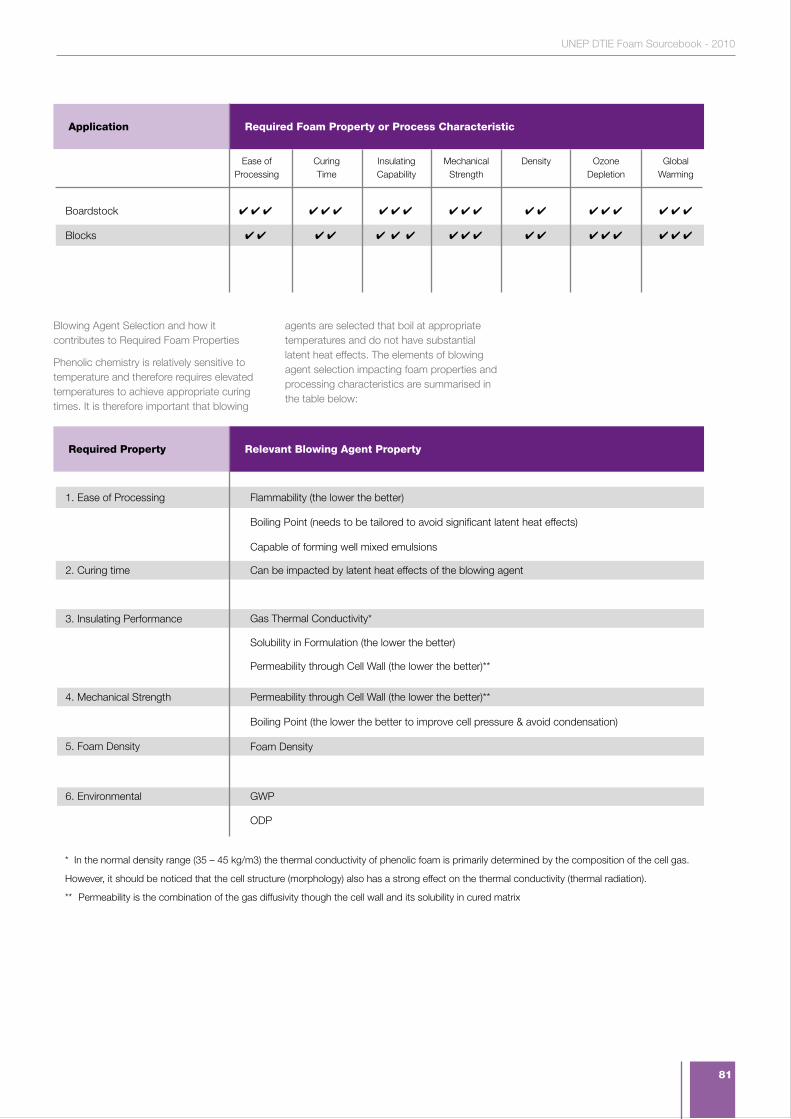

7.3 PHENOLIC 80

7.3.1 PHENOLIC – Boardstock 83

7.3.2 PHENOLIC – Blocks 84

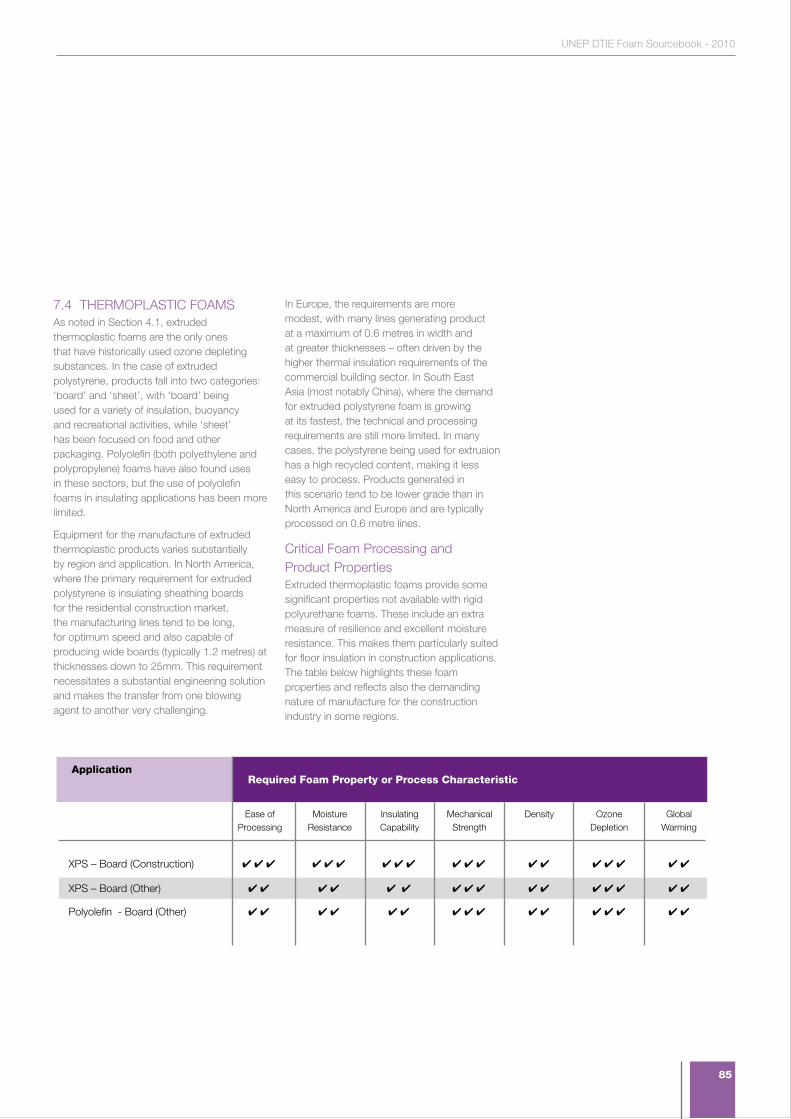

7.4 THERMOPLASTIC FOAMS 85

7.4.1 EXTRUDED POLYSTYRENE – Board 89

7.4.2 POLYOLEFIN FOAMS 90

8 FUNDING STRATEGIES 92

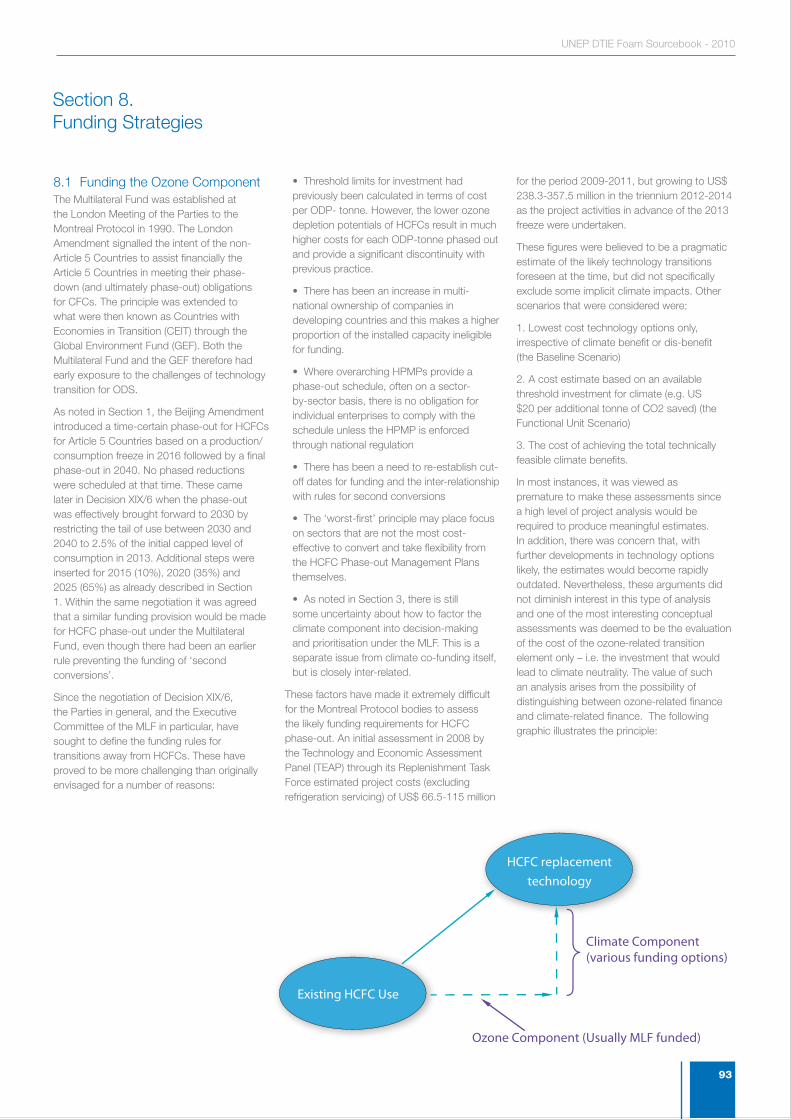

8.1 FUNDING THE OZONE COMPONENT 93

8.2 CLIMATE CO-FUNDING OPPORTUNITIES WITHIN THE MONTREAL PROTOCOL FRAMEWORK 95

9 CONCLUSIONS 96

10 ANNEXES 100

10.1 SOURCES OF INFORMATION15 101

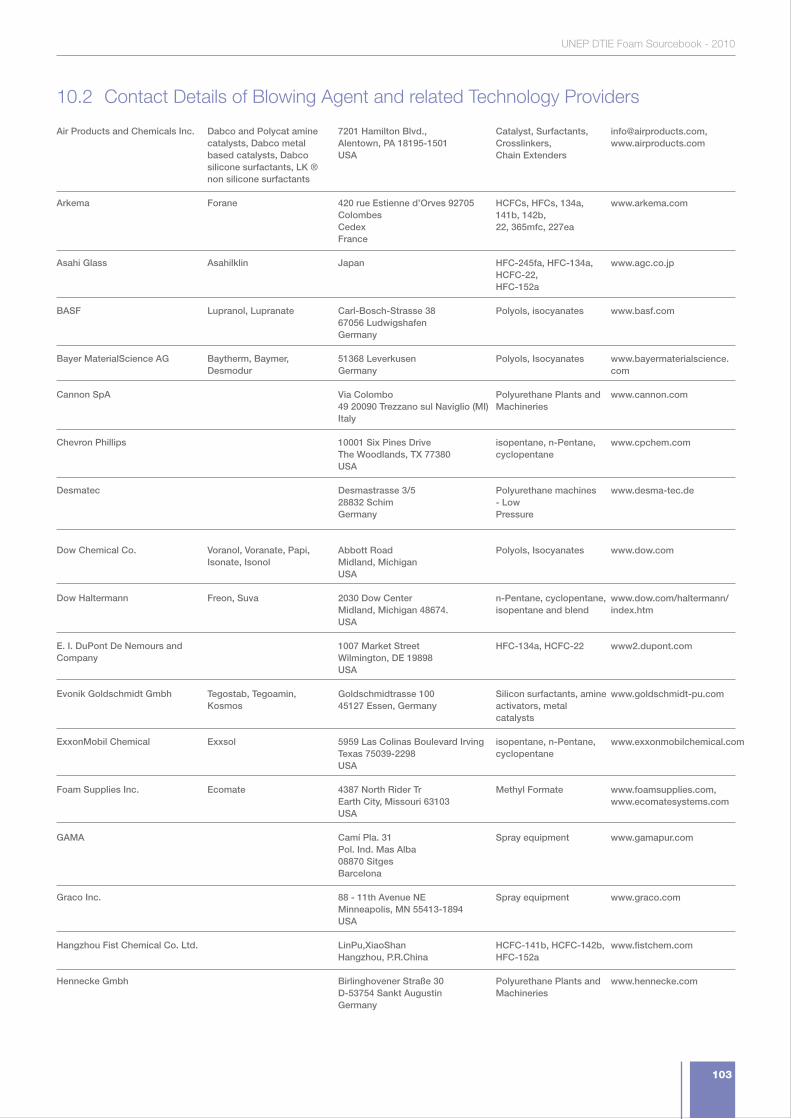

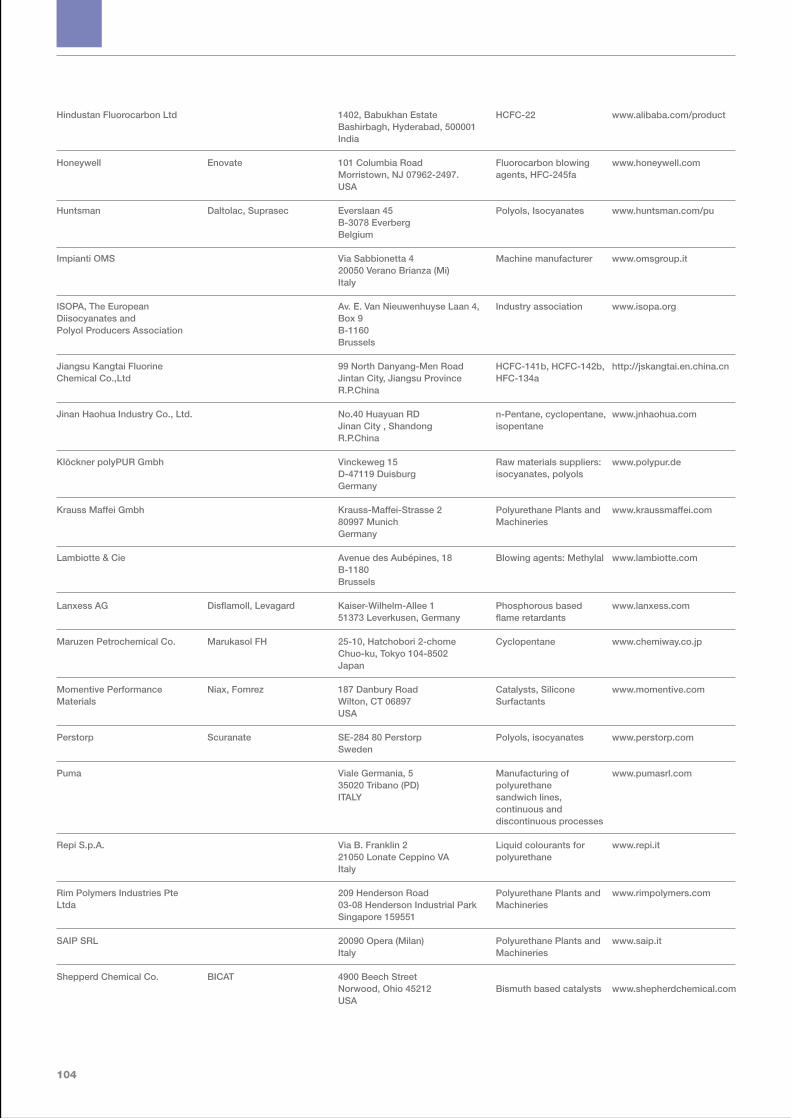

10.2 CONTACT DETAILS OF BLOWING AGENT & OTHER PROVIDERS 103

10.3 FULL TEXT OF DECISION XIX/6 106

8

Section 1. Introduction

“Decision XIX/6 is the first Montreal Protocol decision to take active account of climate in its language”

9

UNEP DTIE Foam Sourcebook - 2010

1.1 The Challenge of Accelerated HCFC Phase-outThe Beijing Amendment of the Montreal Protocol, negotiated in 1999, set out the commitment of countries operating under Article 5 of the Protocol (developing countries) to freeze their consumption of HCFCs at 2015 levels ahead of final phase-out in 2040. This commitment was made alongside a more accelerated commitment of non-Article 5 countries (developed countries) to substantially phase down their use of HCFCs by 2015 and finally phase-out the small remaining ‘tail’ of use by 2030.

It was envisaged that, by the time technology transitions out of HCFCs in Article 5 countries were required, the non-HCFC technology in developed countries would already be well established. However, what was not fully foreseen was the fact that the backdrop for transition in Article 5 countries would be significantly different than for non-Article 5 countries in at least two respects:

I. The preponderance of small, medium enterprises (SMEs) in Article 5 countries would make it impossible to take advantage of the economies of scale available in non-Article 5 countries

II. By the time technology transition was being contemplated in Article 5 countries, the impact on climate of a number of HCFC alternatives would be fully understood and would need to be taken into consideration

Indeed, the concern over the climate impact of HCFCs themselves was to become another critical factor in the policy debate. Rapid growth in HCFC use, particularly in the consumption of HCFC-22, became increasingly evident through the early years of the 21st century, leading to predictions that much of the inadvertent climate benefit gained from the Montreal Protocol could be lost through increased emissions of HCFCs. It was in this spirit that Parties met at the 19th Meeting of the Parties to the Montreal Protocol in Montreal in 2007 to address this issue.

Decision XIX/6 was the result of that deliberation and was the first Montreal Protocol decision to take active account of climate in its language, while avoiding any binding commitments which might be considered as global climate legislation based around consumption rather than emission control. The Parties concluded that, in addition to efforts to reduce consumption by promoting good servicing practices in the refrigeration sector, the most effective way of avoiding the

climate impact of rapid growth in HCFCs was to accelerate their phase-out by advancing the freeze in production/consumption to 2013, based on the consumption in years 2009 and 2010, while introducing phase-down steps in the subsequent years of 2015, 2020, 2025 and 2030. The ‘old’ and the ‘new’ regimes are shown in the graphic below.

However, what became self-evident during the finalisation of the decision was that these additional climate benefits would be contingent on the use of HCFC substitutes that displayed lower climate impacts. This had not been considered as a significant factor when the bulk of HCFC phase-out had taken place in non-Article 5 countries and had led to technology transitions which were often no better in their climate profiles than the HCFCs they replaced. Recognising this reality, Parties were keen not to repeat this pattern in Article 5 countries but equally believed that they would have some influence on the outcome through the funding mechanisms available under the Montreal Protocol (primarily the Multilateral Fund).

In order to highlight this opportunity, the Parties included within the Decision language that required the Executive Committee of the Multilateral Fund to ‘give priority’ to cost-effective projects and technologies that

0%

20%

40%

60%

80%

100%

120%

140%

2008 2012 2016 2020 2024 2028 2032 2036 2040

NewBase

OldBase

Year

New A5 HCFC Measures

Old A5 HCFC Measures

Annual Growth Rate: 5%

Percentage of 2009-10 Baseline

Montreal Protocol HCFC phase-out schedule for Article 5 countries

Section 1. Introduction

Source: UNEP/Caleb

10

minimise other impacts on the environment, including on the climate, taking into account global warming potential, energy use and other relevant factors’. One of the key aspects of this language is that it includes not only the global warming potential of the substitute itself but also the lifecycle implications resulting from energy use. This will be explored further in Section 3.

As a consequence, the Parties had set a very challenging timeline for HCFC phase-out, with all the legal compliance issues that this entails, while making the selection of alternatives more demanding than it had hitherto been in non-Article 5 countries. As stakeholders began to assess this, there was a growing realisation that the priorities, both in terms of sectoral phase-out and technology choice might not be aligned to achieve both ozone compliance and maximum climate benefit simultaneously.

In an effort to approach the subject holistically, the Executive Committee of the Multilateral Fund introduced the concept of an HCFC Phase-out Management Plan (HPMP) which would be established for each Article 5 Party seeking to comply with Decision XIX/6. This would focus primarily on the early steps to accommodate the 2013 freeze and the 2015 reduction of 10% of HCFC consumption. However, it would also need to consider the overarching plan to meet the later phase-out objectives, while minimising climate impact. To plan at this level over such a long period is proving to be a major challenge and this Sourcebook is an attempt to assist foam sector stakeholders in assessing the relevant aspects.

In addition, further analysis of HCFC consumption in Article 5 countries revealed that the bulk of consumption was limited to just a few countries which had significant manufacturing capacity for refrigeration

equipment and/or foams. For other countries, HCFC consumption might be limited to servicing activities in the refrigeration sector. The challenges of meeting specific phase-down targets would be very different in these countries and might lead to different priorities, projects and programmes. This is an issue that is largely beyond the scope of this Sourcebook, since phase-out in the foam sector will take place at the manufacturing enterprises themselves or, where fully formulated polyols are used, in combination with their suppliers.. Nevertheless, care is needed to see the foam sector strategy as part of a larger HPMP and to realise that the pace of that strategy may be heavily influenced by the on-going HCFC needs in other areas.

A further factor may be the ‘worst first’ component of the Decision which states that:

11. To agree that the Executive Committee, when developing and applying the funding criteria for projects and programmes, and taking into account paragraph 6, gives priority to cost-effective projects and programmes which focus on, inter alia:

(a) phasing-out first those HCFCs with higher ozone depleting potential, taking into account national circumstances

….and may predicate against HCFC-141b (see Section 7).

1.2 Guidance on the use of this SourcebookThis Sourcebook is primarily intended to provide overarching guidance to National Ozone Units, Implementing Agencies and Project Proponents on the processes and techniques used to select alternative technologies. It does this by outlining the key factors to be considered and the principles that need to be applied to assess their significance. In Section 7 of the document, the state of technology development in each foam sector and the alternatives currently available are outlined. However, this is not done to provide definitive recommendations, but to offer real-life examples of the decision processes in action. These decision-processes are themselves outlined in Section 6.

The authors would stress that it would be impossible to provide definitive guidance on technology selection in a Sourcebook of this type, since it would very rapidly become outdated. Readers are therefore encouraged to use this Sourcebook alongside other sources of information such as the regular reports of the UNEP Foams Technical Options Committee (FTOC), publications by the Implementing Agencies (e.g. those from the Ozone Operations Resource Group of the World Bank), National Ozone Units, the outputs from Regional Workshops and Industry Conferences/Publications.

11

UNEP DTIE Foam Sourcebook - 2010

12

Section 2. The interface between ozone depletion and climate change

“Knowledge of the key environmental benefits of technology selection has been shown to provide a significant competitive advantage in the foam sector”

13

UNEP DTIE Foam Sourcebook - 2010

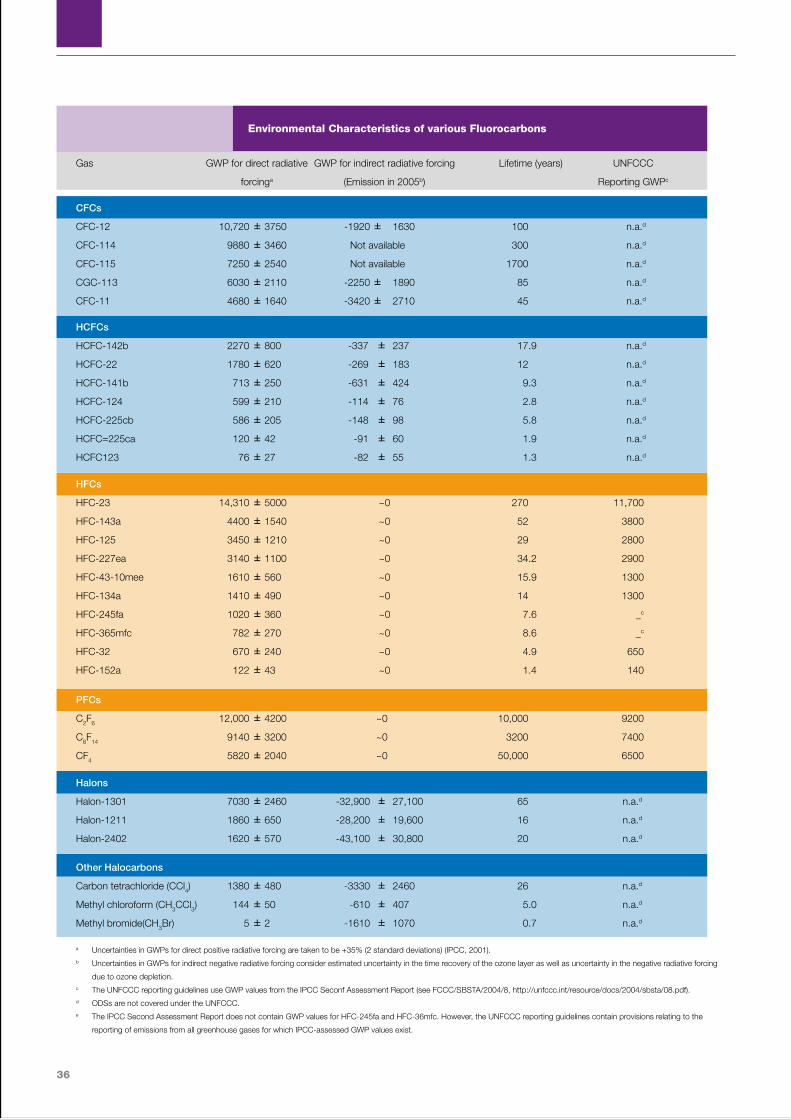

2.1 Measuring Impacts - ODP, GWP and Carbon Intensity of Energy UseThe scientific inter-relationship between ozone depletion and climate change is complex - partly because it occurs at a number of levels simultaneously and partly because there are feedback loops whereby changes on one side lead to changes on the other. These inter-linkages are extensively explained in the IPCC/TEAP Special Report on Ozone and Climate (SROC, 2005) and it is not the purpose of this Sourcebook to repeat those arguments here. Responsible technology selection, while phasing out HCFC use, can create a substantial overall climate benefit even when the offset of increased ozone levels (a greenhouse gas in its own right) is taken into account. The Montreal Protocol community has underpinned this principle by making clear that compliance with HCFC phase-out targets will not be compromised for reasons of climate protection as Decision XIX/6 is implemented.

In order to help policy-makers and other stakeholders to assess the competing claims of the alternatives in this complex scientific environment, a series of metrics have been introduced to provide guidance on the comparative impacts of options on both the ozone layer and on climate. These include, ozone depletion potential (ODP), global warming potential (GWP) and carbon intensity of energy, each of which will be considered in turn.

Ozone Depletion Potential (ODP) This measure of assessing the damage that a given substance could do to the stratospheric ozone layer was first introduced by the UNEP Scientific Assessment Panel in the years running up to the instigation of the Montreal Protocol in 1987. In simple terms, the impact of all substances is compared to a baseline centred on CFC-11 and CFC-12, which are both considered to have an ODP of 1. This process is usually called normalisation and is a common technique for this type of comparative analysis. Therefore HCFC-141b, the HCFC most commonly used as a foam

blowing agent, has an ODP of 0.11 because a molecule of HCFC-141b is likely to do only 11% of the damage in its stratospheric lifetime that would have been done by a molecule of CFC-11. It can be noted that all ozone depleting substances controlled by the Montreal Protocol have either chlorine or bromine atoms, or sometimes both, in their molecules. This is often combined with fluorine. Therefore, if a molecule contains fluorine but not bromine or chlorine atoms, it can be recognised as not controlled by the Montreal Protocol.

In practice, substances with lower ODPs often have shorter atmospheric lifetimes than those they replace. However, assessing precise atmospheric lifetimes can be complex and it may be necessary occasionally to revise ODPs based on new scientific evidence. This can create particular issues for policy-makers who normally require certainty to implement policies which need to be consistent over a number of years. Hence, there is sometimes an ‘official’ value (as stated in the Annexes of the Montreal Protocol) and a latest scientific value, which might be marginally different. Enterprises are encouraged to always use the official value in their assessments.

In some instances, the atmospheric lifetime of a substance can be so short that, even though it might contain chlorine or bromine, it is unlikely to reach the stratosphere at all. These substances therefore have no ozone depleting potential in practice. However, this does not mean that there are no circumstances under which a stray molecule might get to the stratosphere. Care should therefore be taken in using terms such as “zero-ODP”, even though they are widely used in marketing literature and, unfortunately, as a requirement in a number of product and building codes. Better terminology would be negligible ODP, but this seems to be rejected in practice because it is less emphatic.

Stakeholders should also note that there are a number of short life-time substances that are not controlled under the Montreal Protocol

even though they have measurable ODPs. The reason for this is that they are not considered sufficiently significant by policy-makers to have any bearing on the environmental outcome. Enterprises could well be best served, therefore, by using terms such as ‘controlled under the Montreal Protocol’ or ‘not controlled under the Montreal Protocol’, when referring to their blowing agents. It should be further noted that compliance with the Montreal Protocol is measured in terms of avoidance of controlled substances, not avoidance of ozone depleting substances (ODS).

Section 2. The interface between ozone depletion and climate chnange

14

Global Warming Potential (GWP) The metric described as Global Warming Potential (GWP) has a lot of similarities with ODP in that it is a comparative assessment of climate impact which is normalised against carbon dioxide (CO2 = 1). Many other parallels exist with ODP. For example, it is quite common for substances to have an official GWP (often based on the Assessment Reports of the Inter-Governmental Panel on Climate Change) and a latest scientific GWP. Therefore care needs to be taken in deciding which one to use.

Since the climate impact of a substance is also dependent on its lifetime, decisions have to be made about the period over which the comparison is made. Carbon oxide itself is a relatively long-lived molecule (50-200 years, depending on the circumstances) and therefore a comparison over 100 years has become accepted as something of a standard for policy-making purposes. The selected period is known technically as the Integrated Time Horizon or ITH. The approach taken under the Kyoto Protocol in adopting a ‘basket of gases approach’ to target setting required clear GWPs for each of the gases involved and these were quoted in the Second Assessment Report on the basis of a 100 year ITH. This has also become the basis for most carbon trading activities globally. However, the debate goes on about whether different time horizons would be more appropriate.

The level of contribution to global warming that can be attributed to a substance is primarily based on the ‘space’ it occupies in the radiative spectrum. This is referred to technically as its degree of radiative forcing. It so happens that chlorine and fluorine containing compounds (CFCs, HCFCs and HFCs) occupy a particular part of the spectrum that is otherwise uncluttered. This means that their impact is considerably higher than would normally be expected and leads to a high GWP. This subject is covered more specifically in Sections 4 and 5.

The main impact of the GWP of a gas is experienced only when it is released. Therefore efforts to reduce releases will either delay or, at best, totally avoid the climate impact of that gas within the lifecycle of the product or equipment in which it is being used. For foams, the main points of potential release are during foam manufacture and at end-of-life. In general, there is little emission during the use phase – particularly from insulating foams, where retention of blowing agent is critical performance.

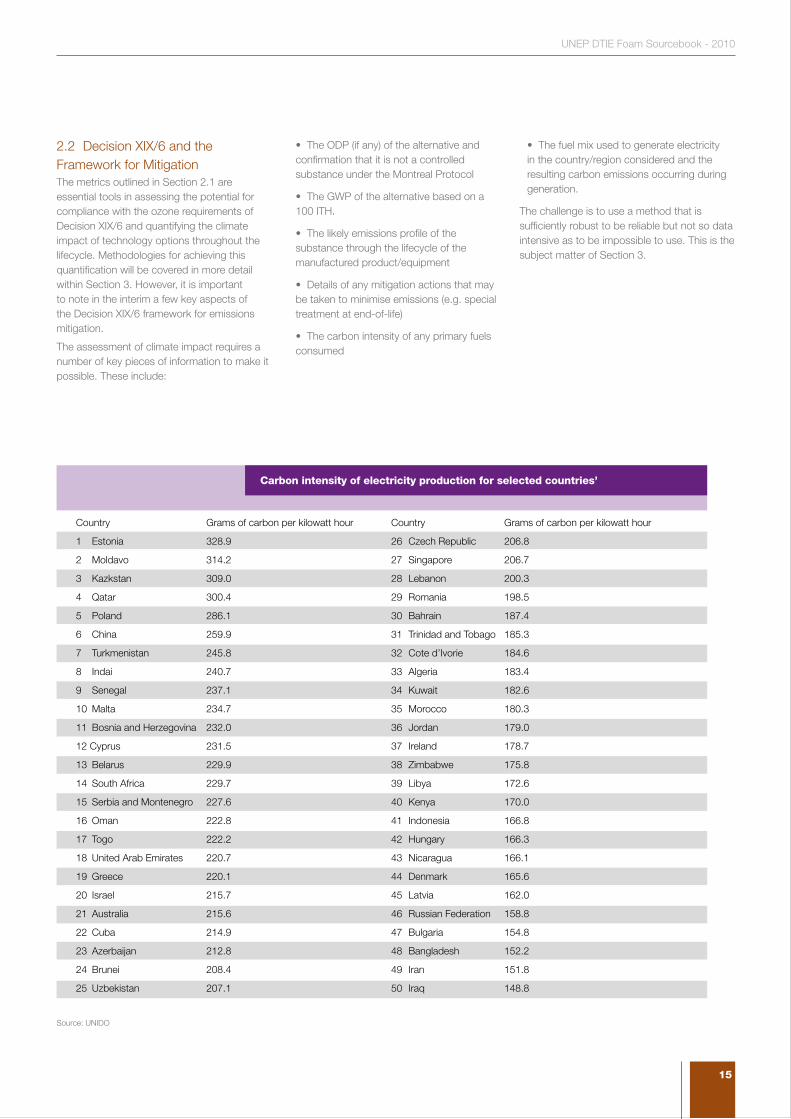

Carbon Intensity of Energy Use Decision XIX/6 requests the Executive Committee of the Multilateral Fund to include energy use in its consideration of technology options. This may arise from primary consumption of fuel or from the use of fuels to generate electricity. Where primary consumption occurs (e.g. in the transport sector or in the direct burning of gas, coal or oil) the values of carbon intensity are relatively consistent globally. The following graphic illustrates the point for a number of fuels and bio-fuels:

However, where fuels are used to generate electricity, the mix of fuels will have a bearing on the overall carbon intensity of the electricity consumed. This can vary substantially by country/region and will be influenced significantly by the amount of renewable energy (e.g. hydro) available. For large portions of the refrigeration, air conditioning and appliance sectors, electricity is the key source of energy and hence knowledge of the carbon intensity of local electricity is required.

In practice, the first determination that needs to be made is in respect to the contribution of energy efficiency impacts on overall energy consumption. Once this value is available it can be combined with information on the carbon intensity of the supply to assess the overall impact on carbon emissions. This means that the adoption of the same technology may have different impacts in different regions. It may even mean that the relative ranking of a range of technologies changes by region. An example would be where a particularly energy efficient technology is deployed in a region with very high ‘renewables’ content in its electricity supply. In such a region, the impact of its use would be much less significant than in a heavily coal burning environment.

Tables exist (see below) giving average carbon intensities for electricity in specific countries and regions, but care needs to be taken with these to ensure that they are representative of the particular supply being drawn on by the project and its manufactured products.

0 20 40 60 80 100 120

!

Cooking Oil and Tallow

Oilseed Rape (UK)

Oilseed Rape (Ukraine)

Oilseed Rape (Poland)

Oilseed Rape (Germany)

Oilseed Rape (France)

Oilseed Rape (Finland)

Oilseed Rape (Canada)

Oilseed Rape (Australia)

Soy (USA)

Soy (Brasil)

Soy (Argentina)

Palm Oil (Malaysia)

Palm Oil (Indonesia)

Natural Gas

Diesel

Gasoline

Coal

Biodiesels

Gram of Carbon Dioxide produced per Megajoule of energy (UK Government �gures)

13

55

59

45

47

46

52

54

55

42

38

38

62

86

85

112

63

73

Data taken from http://www.dft.gov.uk/pgr/roads/environment/rtfo/govrecrfa.pdf

15

UNEP DTIE Foam Sourcebook - 2010

2.2 Decision XIX/6 and the Framework for Mitigation The metrics outlined in Section 2.1 are essential tools in assessing the potential for compliance with the ozone requirements of Decision XIX/6 and quantifying the climate impact of technology options throughout the lifecycle. Methodologies for achieving this quantification will be covered in more detail within Section 3. However, it is important to note in the interim a few key aspects of the Decision XIX/6 framework for emissions mitigation.

The assessment of climate impact requires a number of key pieces of information to make it possible. These include:

• The ODP (if any) of the alternative and confirmation that it is not a controlled substance under the Montreal Protocol

• The GWP of the alternative based on a 100 ITH.

• The likely emissions profile of the substance through the lifecycle of the manufactured product/equipment

• Details of any mitigation actions that may be taken to minimise emissions (e.g. special treatment at end-of-life)

• The carbon intensity of any primary fuels consumed

• The fuel mix used to generate electricity in the country/region considered and the resulting carbon emissions occurring during generation.

The challenge is to use a method that is sufficiently robust to be reliable but not so data intensive as to be impossible to use. This is the subject matter of Section 3.

Country Grams of carbon per kilowatt hour Country Grams of carbon per kilowatt hour

1 Estonia 328.9 26 Czech Republic 206.8

2 Moldavo 314.2 27 Singapore 206.7

3 Kazkstan 309.0 28 Lebanon 200.3

4 Qatar 300.4 29 Romania 198.5

5 Poland 286.1 30 Bahrain 187.4

6 China 259.9 31 Trinidad and Tobago 185.3

7 Turkmenistan 245.8 32 Cote d’Ivorie 184.6

8 Indai 240.7 33 Algeria 183.4

9 Senegal 237.1 34 Kuwait 182.6

10 Malta 234.7 35 Morocco 180.3

11 Bosnia and Herzegovina 232.0 36 Jordan 179.0

12 Cyprus 231.5 37 Ireland 178.7

13 Belarus 229.9 38 Zimbabwe 175.8

14 South Africa 229.7 39 Libya 172.6

15 Serbia and Montenegro 227.6 40 Kenya 170.0

16 Oman 222.8 41 Indonesia 166.8

17 Togo 222.2 42 Hungary 166.3

18 United Arab Emirates 220.7 43 Nicaragua 166.1

19 Greece 220.1 44 Denmark 165.6

20 Israel 215.7 45 Latvia 162.0

21 Australia 215.6 46 Russian Federation 158.8

22 Cuba 214.9 47 Bulgaria 154.8

23 Azerbaijan 212.8 48 Bangladesh 152.2

24 Brunei 208.4 49 Iran 151.8

25 Uzbekistan 207.1 50 Iraq 148.8

Carbon intensity of electricity production for selected countries’

Source: UNIDO

16

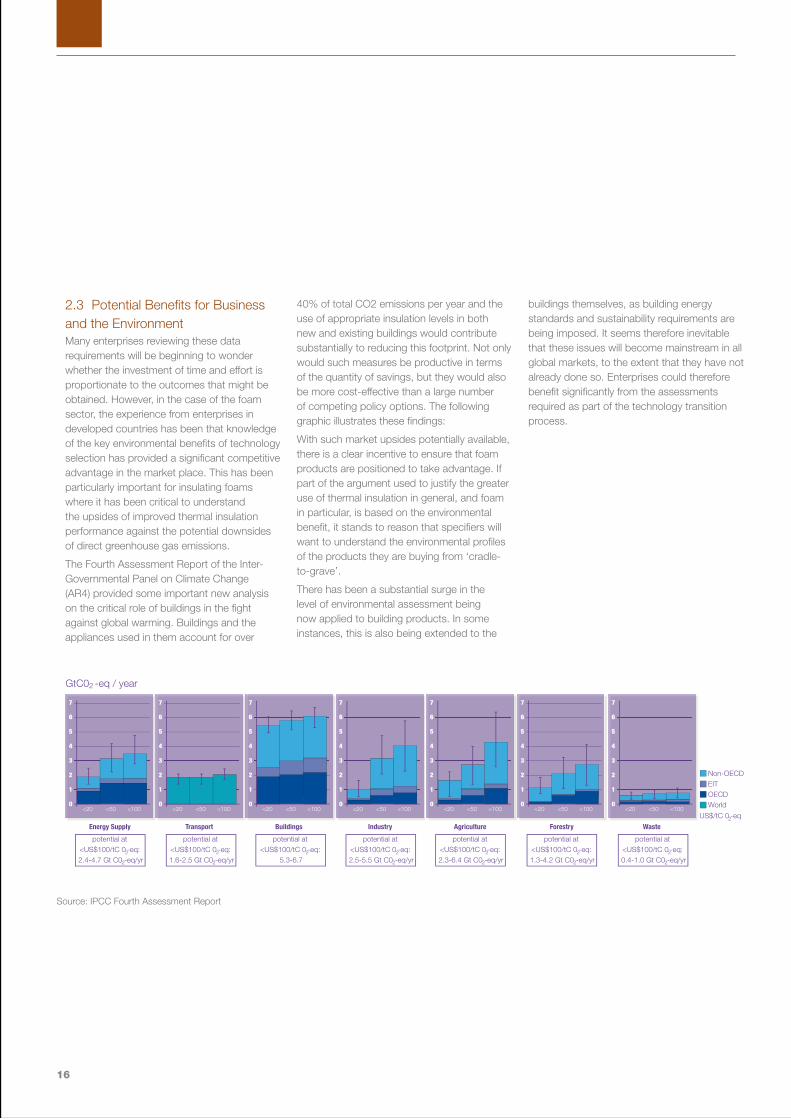

2.3 Potential Benefits for Business and the Environment Many enterprises reviewing these data requirements will be beginning to wonder whether the investment of time and effort is proportionate to the outcomes that might be obtained. However, in the case of the foam sector, the experience from enterprises in developed countries has been that knowledge of the key environmental benefits of technology selection has provided a significant competitive advantage in the market place. This has been particularly important for insulating foams where it has been critical to understand the upsides of improved thermal insulation performance against the potential downsides of direct greenhouse gas emissions.

The Fourth Assessment Report of the Inter-Governmental Panel on Climate Change (AR4) provided some important new analysis on the critical role of buildings in the fight against global warming. Buildings and the appliances used in them account for over

40% of total CO2 emissions per year and the use of appropriate insulation levels in both new and existing buildings would contribute substantially to reducing this footprint. Not only would such measures be productive in terms of the quantity of savings, but they would also be more cost-effective than a large number of competing policy options. The following graphic illustrates these findings:

With such market upsides potentially available, there is a clear incentive to ensure that foam products are positioned to take advantage. If part of the argument used to justify the greater use of thermal insulation in general, and foam in particular, is based on the environmental benefit, it stands to reason that specifiers will want to understand the environmental profiles of the products they are buying from ‘cradle-to-grave’.

There has been a substantial surge in the level of environmental assessment being now applied to building products. In some instances, this is also being extended to the

buildings themselves, as building energy standards and sustainability requirements are being imposed. It seems therefore inevitable that these issues will become mainstream in all global markets, to the extent that they have not already done so. Enterprises could therefore benefit significantly from the assessments required as part of the technology transition process.

0

1

2

3

4

5

6

7

<20 <50 <1000

1

2

3

4

5

6

7

<20 <50 <1000

1

2

3

4

5

6

7

<20 <50 <1000

1

2

3

4

5

6

7

<20 <50 <1000

1

2

3

4

5

6

7

<20 <50 <100

Energy Supply Transport Buildings Industry Agriculture

0

1

2

3

4

5

6

7

<20 <50 <1000

1

2

3

4

5

6

7

<20 <50 <100

Forestry Waste

GtC0 -eq / year2

potential at <US$100/tC 0 -eq: 2.4-4.7 Gt C0 -eq/yr

2

2

potential at <US$100/tC 0 -eq: 1.6-2.5 Gt C0 -eq/yr

2

2

potential at <US$100/tC 0 -eq: 2.5-5.5 Gt C0 -eq/yr

2

2

potential at <US$100/tC 0 -eq: 2.3-6.4 Gt C0 -eq/yr

2

2

potential at <US$100/tC 0 -eq: 1.3-4.2 Gt C0 -eq/yr

2

2

potential at <US$100/tC 0 -eq: 0.4-1.0 Gt C0 -eq/yr

2

2

potential at <US$100/tC 0 -eq:

5.3-6.72

US$/tC 0 -eq

Non-OECDEITOECDWorld

2

Source: IPCC Fourth Assessment Report

17

UNEP DTIE Foam Sourcebook - 2010

18

Section 3. Methods for quantifying climate impact

“the impact of technology choice on energy consumption will be an additional source of potential climate contributions”

19

UNEP DTIE Foam Sourcebook - 2010

Section 2.2 has already made reference to the fact that quantitative assessments of climate impact need to take account of activities that occur throughout the lifecycle of the products and/or equipment manufactured as a result of the implementation of a project.

However, when assessing technology transition projects at enterprise level, this can be a relatively complex and uncertain exercise, since the quantity and scope of products and/or equipment manufactured by an enterprise will not be known in full at the point of investment.

This challenge, however, is not insurmountable if the primary purpose for quantifying the climate impact of a measure is to compare technology options. In such cases, it is possible to take defined units of manufacture/production, based on typical demand patterns, and compare the relative climate impacts arising from specific technology choices prior to making a final decision. It is in this context, that this Sourcebook reviews the options available for quantifying climate impact.

3.1 Life Cycle Approaches based on Direct Emissions only (e.g. GWP)It is well known that the direct emissions of chlorinated and fluorinated substances over the lifecycle of products and/or equipment can lead to significant climate impacts. The graph below illustrates the significance of the global warming impacts of common CFCs, HCFCs and HFCs, when compared with carbon dioxide. If aspects such as initial charge sizes and emission profiles are well understood, it is possible to make relatively precise estimates of the climate impact of emissions including their significance with time. However, even where the focus of attention is only on direct emissions of refrigerants and/or blowing agents, care must be taken to ensure that the comparisons are appropriate. In the foams sector, the following questions might be part of a useful checklist to ensure that ‘like is compared with like’:

I. Do the boiling points of the respective alternative blowing agents influence the losses in production?

II. Does the technology choice involve co-blowing with another blowing agent?

III. How do the blowing efficiencies of different technology options impact the level of blowing agent required in the respective formulations?

IV. Is the rate of permeation of blowing agent through the cell walls the same for all blowing agents?

V. If not, how are these diffusion differences accounted for in the respective emissions profiles?

VI. Are there any constraints from the technology choice that would prevent recovery at end of life?

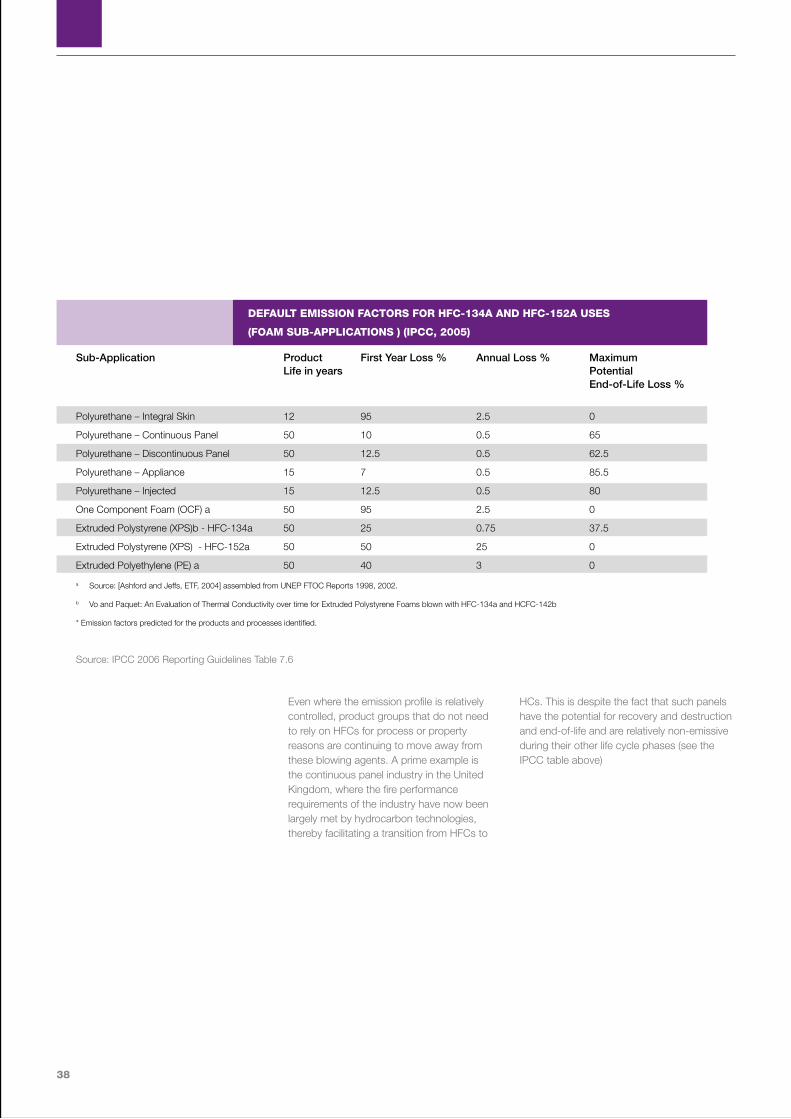

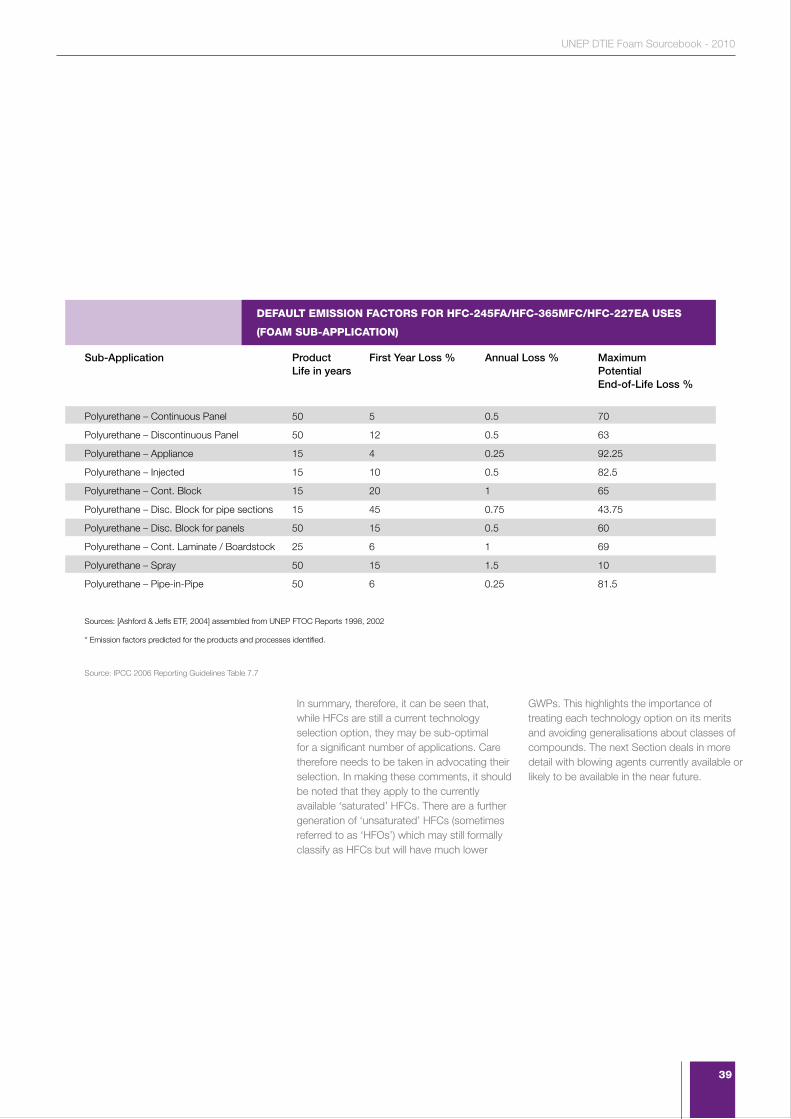

Section 4.6 of this Sourcebook provides tables illustrating the current default emission profiles for various foam processes and applications using liquid and gaseous blowing agents. Annual emission rates are provided for each basic lifecycle stage. These tables are typically used as an initial basis of assessment for direct emissions from foams. Where no further adjustments are made for items II-VI above, the choice of blowing agent from a climate perspective is generally directly linked to its GWP, which is why it is sometimes referred to as the GWP method. Although this provides a temptingly simple basis for evaluation, care needs to be taken that all appropriately adjustments are made before conclusions are drawn.

!

Refrigerator TEWI Contributors(Typical for HFC product in USA)

RefrigerantDirect GWP

0.4%

Power PlantEmissions

92.4%

Blowing AgentDirect GWP

7.2%

Section 3. Methods for quantifying climate impact

Source A.D. Little (2002)

20

3.2 Life Cycle Approaches also considering energy (e.g. LCA, LCCP, TEWI) For both foam and refrigeration applications, it is well understood that the impact of technology choice on energy consumption will be an additional source of potential climate contributions. In many applications, the energy consumption component can be a dominant factor in the overall carbon footprint of the product or equipment. An example of this would be a domestic refrigerator where the following pie chart illustrates the relevant components of greenhouse gas emission over the lifecycle.

Although such graphs rightly draw attention to the fact that the focus of appliance designers should be on improving energy efficiency, they do not automatically lead to the conclusion that the choice of refrigerant or blowing agent is unimportant.

Where the choice of blowing agent can influence the energy efficiency of a refrigerator significantly, it may be that this effect will offset the direct emissions from eventual blowing agent release. However, the level to which this is the case will depend largely on the sensitivity of energy efficiency to such choices, which will in turn depend on the geometry of the appliance and the levels of insulation used. In practice, it is often the case that energy efficiency is only marginally influenced by these technology choices and, in such situations the comparative process reverts largely to a comparison of direct emissions only. This said, the inclusion of ‘energy use’ within the factors that must be considered under Decision XIX/6 requires that an appropriate lifecycle model is used. The following section outlines three options that have found application for this purpose.

All three methods featured below - Lifecycle Assessment (LCA), Total Equivalent Warming Impact (TEWI) and Lifecycle Climate Performance (LCCP) - focus on the performance of individual products or pieces of equipment. In this respect, they are amongst the most rigorous analyses available. However, as will be highlighted, they are data hungry and often limited in their application because of their focus on individual installations. They are of most use where the product/equipment is mass produced and where the performance

is largely independent of the local environment (e.g. domestic refrigerators). Accordingly, such techniques are typically used by product designers and also academics, seeking to make comparisons and plot trends. However, these techniques are of less value in assessing climate implications at enterprise or project

level.

Life Cycle Assessment (LCA) Life Cycle Assessment is effectively the ‘gold standard’ for such comparisons and not only includes climate related elements but many other environmental impacts. It has been the subject of a large degree of standardisation around the world and the current LCA principles are set out in detail within the International Standards Organisation (ISO) 14040 series of standards. As a result of its comprehensive nature, it is a very “data hungry” approach and requires substantial resources for satisfactory completion. Where the primary purpose of the activity is for technology comparison (as in this instance), Life Cycle Assessment would normally be considered as too cumbersome for the purpose. This has led practitioners to consider two other approaches which are focused solely on components relating to climate impact.

Total Equivalent Warming Impact (TEWI) Total Equivalent Warming Impact was first developed and introduced by the US Department of Energy’s Oak Ridge National Laboratory (ORNL) in the mid-1990s as a means of making relevant comparisons of climate impact for differing technology options. It was an effective initial tool, but came under later criticism because it did not fully consider the footprints associated with the earlier steps in the manufacturing process (for example, of the blowing agents themselves). In reality, this should never have been a criticism of the method, since every lifecycle comparative method has to define its boundaries. The failing was probably in not making them clear enough to those reviewing the outputs.

This experience highlights a further important point when developing and using lifecycle comparison tools - “always be sure to understand the boundary conditions of the model (i.e. what is included and what isn’t.)”

Life Cycle Climate Performance (LCCP) This method emerged in the wake of the TEWI experience and explicitly included the earlier climate footprints associated with the production of chemicals and other precursors. The term Life Cycle Climate Performance was used in earnest for the first time in the 1999 TEAP Task Force Report entitled “The Implications to the Montreal Protocol of the inclusion of HFCs and PFCs in the Kyoto Protocol”, in which the comparative impacts of a number of technology choices were assessed.

As with LCA, LCCP remains relatively “data hungry” despite its climate focus and is best applied to situations where there are a large number of replicated units (e.g. domestic refrigerators, mobile air conditioners etc.). Where applications are less well defined and are typically specified by their surroundings (e.g. building insulation or stationary air conditioning), there is a need for a less complex hybrid approach.

21

UNEP DTIE Foam Sourcebook - 2010

3.3 Hybrid Approaches (e.g. Functional Unit and Climate Indicators) Hybrid approaches of the type included in this section are targeted at addressing the more practical challenges of evaluating the climate impact of technology choices at enterprise or project level. This may also extend to the overall evaluation of HPMPs themselves. This higher level evaluation (which some have called ‘climate proofing’) is a critical part of the objectives of National Ozone Units, Implementing Agencies and other interested parties. In practice, hybrid approaches are expected to be more widely used in the implementation of Decision XIX/6 than the more formal methods of LCA, TEWI and LCCP. However, as pointed out in the sections that follow, care needs to be taken to maintain sufficient rigour to give reliable predictions of climate impact.

In addressing this concern for both practicality and rigour, and following the negotiation and finalisation of Decision XIX/6, there were substantial discussions about how the language concerning the evaluation of climate impact might be interpreted in practice. Some felt that a GWP-based approach would be sufficient, arguing that LCCP was too complex, particularly in applications where there were uncertainties about the use conditions. Others felt that LCCP was the only way in which the full text of the Decision could be implemented.

As a potential means of bridging this difference in view, two new approaches have emerged. These are the functional unit approach (FUA) and the Multilateral Fund Climate Indicator (MCII). Both methods have sought to provide guidance in technology selection specifically in the context of Decision XIX6.

Calculations HCFC-141b n-Pentane

Annual Foam Volume 7,143 m3 7,143 m3

Area of Insulation Created 128,571.17 m2 128,571.17 m2

Energy Transmitted in Lifetime 121722.17 MWh 189345.60 MWh

Carbon equivalent 23127.21 t-CO2-equiv 35975.66 t-CO2-equiv

Energy difference 67623.43 MWh

Carbon equivalent difference 12848.5 t-CO2-equiv

Blowing Agent Losses 25.00 tonnes 16.15 tonnes

Carbon equivalent 17825 t-CO2-equiv 178 t-CO2-equiv

Carbon equivalent difference -17647 t-CO2-equiv

Total Carbon Equivalents 17825 t-CO2-equiv 13026 t-CO2-equiv

Example of Foam Comparisons using the Functional Unit Approach for Foams (Constant Thickness)

22

Functional Unit Approach (FUA) This approach was originated in the foam sector and seeks to establish a basis for comparison of insulation foams in typical building or appliance applications. In doing so, it has needed to take account of matters such as building energy sources, local carbon intensity values for electricity generation and local building insulation standards. Since these vary between residential buildings and commercial/industrial buildings, it can be necessary to take into account the likely split of foam sales to each sector. However, by considering the fate of a typical unit of foam (the functional unit), the scenario for a particular manufacturing plant or enterprise can be established. As with other techniques, the fact that the tool is being used for comparative purposes means that the sensitivity to the assumptions used is somewhat diminished.

The table below provides an indication of the type of output obtained using the functional unit approach when comparisons are made between the old HCFC-141b technology and a replacement n-Pentane technology at constant thickness (constant thermal performance being the other typical basis of comparison). The calculations are based on the lifecycle impact of the annual production of an enterprise currently using 25 tonnes of HCFC-141b per year.

It can be seen that the better thermal performance of HCFC-141b results in less energy being transmitted through the foam during its lifetime and hence less CO2 emitted from power generation. However, the quantity of n-Pentane used in the foam is reduced because it has better blowing efficiency and its lower GWP also contributes to a net saving of around 4,800 tonnes CO2-equiv. when compared with the HCFC-141b baseline. If the comparison had been conducted on the basis of constant thermal performance, the n-Pentane option would have required additional thickness of foam and hence the embodied energy of the additional foam would have also needed to have been included in the comparison.

In a further enhancement of the Functional Unit Approach an attempt was made to assess likely differences in cost resulting from technology choices. This permitted the calculation of cost per unit of climate benefit for the first time. However, to do this, the model needed to assess the cost of a climate neutral transition (i.e. one with the same climate profile as the HCFC-141b technology being replaced). One of the interesting aspects to emerge from this assessment was that the climate mitigation costs (measured in US$ per tonne of CO2 saved) increased dramatically for technologies requiring significant capital investment as the size of the plant diminished. This observation was no more than a demonstration of the basic principles relating to economies of scale, first mentioned in Section 1 and elaborated further in Section 4.5 and elsewhere. Nevertheless, it did highlight the fact that climate mitigation costs in excess of US$200/tonne of CO2-equiv. might be incurred in the most extreme cases. Further detail on the basis for these analyses is found in the relevant MLF Executive Committee publication on the treatment of Environmental Issues in technology transition (Annex V of UNEP/OzL.Pro/ExCom/55/47).

Climate Indicators (e.g. MCII) Although foam scenarios could be relatively well modelled using the Functional Unit Approach, a further level of simplification was seen as necessary for the refrigeration sector. The UN Multilateral Fund Secretariat took direct responsibility for this further step and developed, in conjunction with experts in the field, a simplified model that essentially limited the refrigeration and air conditioning sector to five primary cooling scenarios. This further level of simplification has been seen to make the absolute comparative values less reliable but continues to provide sufficient certainty to allow for technology-ranking to take place.

As with the FUA, comparison with the technology being replaced is an important element of the assessment, since this has a strong bearing on whether it should be prioritised in an overall HCFC Phase-out Management Plan (HPMP) or not. In addition, the relative climate performance against such a benchmark can be used to incentivise or discourage certain technology selection options. Stakeholders are certainly advised to review periodically how quantified climate impacts might be used to assess technology appropriateness, funding eligibility and levels of support in future. This Sourcebook will return to this point in Section 8 where ‘Funding Strategies’ are considered.

23

UNEP DTIE Foam Sourcebook - 2010

24

Section 4.Foam manufacture and existing fluorocarbon technologies

“The characteristics of CFC-11 and CFC-12 were so appropriate for polymeric foams that they seemed ‘designed-for-purpose”

25

UNEP DTIE Foam Sourcebook - 2010

4.1 An introduction to Foam Types.

Polyurethane Foams (including Polyisocyanurate) Polyurethane Foam technologies were developed as early as the 1930s in flexible, rigid and semi-rigid forms, and have played a dominant role in the field of foamed polymers ever since. This is largely because of the technology’s basic capacity to produce materials with a wide range of critical end properties such as low density, consistent foam morphology, mechanical strength and resilience. In most cases, these properties can be achieved by relatively simple formulation adjustments, indicating the versatility of polyurethane chemistry.

Flexible foams, which demonstrate excellent elastic and deformation characteristics, find their major applications in the area of furniture cushioning (bedding, seating, carpet backing, etc.) and packaging (electronic, computer, china, equipments). Semi-rigid foams are used in the automotive industry (dash panel, liner, visors) and footwear (shoe soles) [Lee, 2006]. However, the largest single application for polyurethane rigid foam is in thermal insulation, although similar foams can also be used to provide structural integrity and buoyancy. For thermal insulation applications, old and modern buildings, transport systems and household appliances all take advantage of the excellent energy performance offered through the low thermal conductivity of the foam.

It is in the area of thermal insulation that the contribution of the blowing agent is at its most significant, since the gas in the foam cell is the major contributor to the overall thermal performance of the insulation. This subject is explored further in Section 4.2.

A variant of basic polyurethane chemistry is polyisocyanurate, which has greater rigidity and provides improved fire performance. However, it is less resilient and is therefore not a replacement for polyurethane in all applications.

Phenolic FoamsPhenolic foams take the characteristics of polyisocyanurate a step further and are very highly cross-linked. This makes them very rigid (high modulus) and, historically, has led to unacceptable friability where vibration or thermal shock is a factor. Nonetheless, more recent technologies have achieved very fine cell structures which have both improved the resilience of the foam and its thermal performance. Indeed, phenolic foam now typically delivers the best thermal performance among the insulating foam types available. However, this is not the primary reason for its use. Phenolic foam has made ground primarily because of its overall fire performance and, most importantly, low smoke generation.

As with polyurethane and polyisocyanurate, phenolic foams were historically blown with CFCs and have progressed through a number of alternatives which are documented in Sections 5 and 7.

Extruded Polystyrene

A number of polystyrene foam product types exist. Expanded polystyrene foams are blown from beads of polystyrene which already contain a hydrocarbon blowing agent (typically pentane). These beads are then expanded in hot moulds to create blocks and moulded shapes. For this reason, the foams have been used more for packaging than for demanding thermal insulation applications. These foams, sometimes referred to as bead foams, have never used CFCs as blowing agents and are not the subject of this [Sourcebook].

An alternative type of polystyrene foam is extruded polystyrene foam which, as its name suggests, is manufactured by an extrusion process at elevated temperatures. This product has historically used CFCs and their substitutes. The nature of the extrusion process is such that it creates more integral foams than those generated from beads and provides better thermal properties as a result. Some extruded products are manufactured specifically for construction applications and are typically referred to as ‘board’, while others are manufactured for packaging purposes, sometimes with a thermal component (e.g. disposable food packaging) and are typically known as ‘sheet’ products.

Section 4. Foam manufacture and existing flurocarbon tecnologies

26

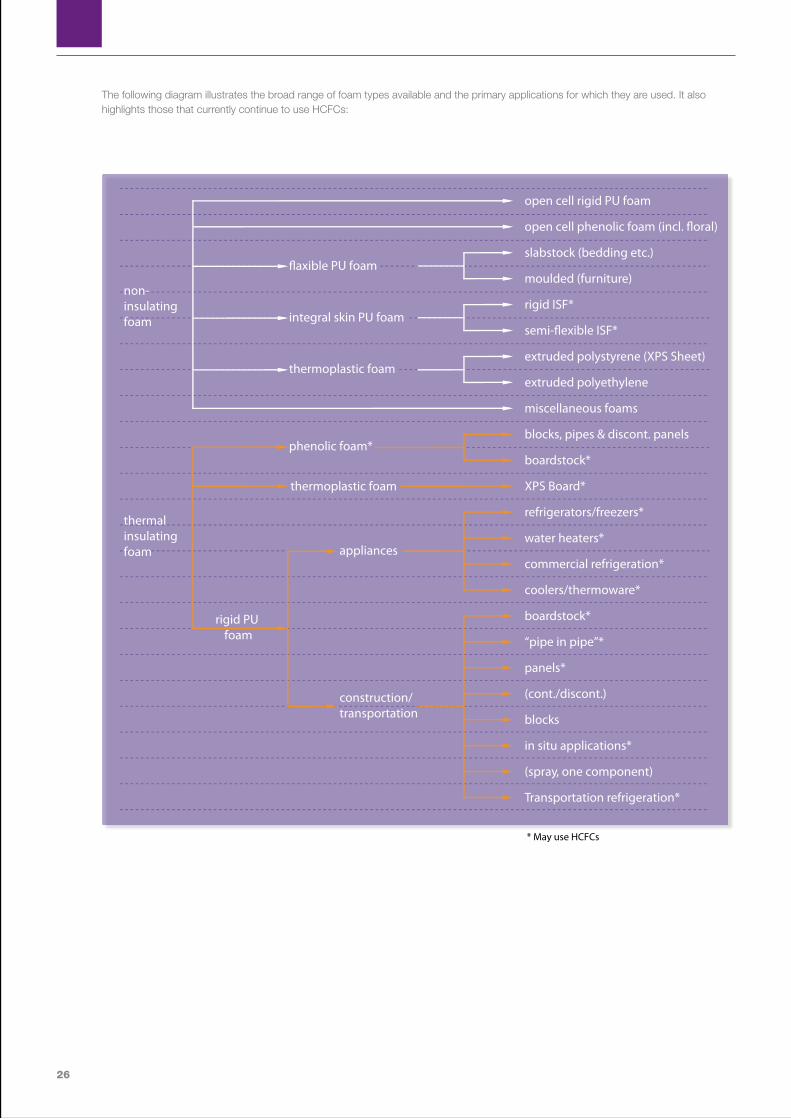

The following diagram illustrates the broad range of foam types available and the primary applications for which they are used. It also highlights those that currently continue to use HCFCs:

integral skin PU foam

�axible PU foam

thermoplastic foam

phenolic foam*

thermoplastic foam

construction/transportation

rigid PU foam

* May use HCFCs

open cell rigid PU foam

slabstock (bedding etc.)

moulded (furniture)

rigid ISF*

extruded polystyrene (XPS Sheet)

extruded polyethylene

miscellaneous foams

blocks, pipes & discont. panels

boardstock*

XPS Board*

refrigerators/freezers*

water heaters*

commercial refrigeration*

coolers/thermoware*

boardstock*

“pipe in pipe”*

panels*

(cont./discont.)

blocks

in situ applications*

(spray, one component)

Transportation refrigeration*

open cell phenolic foam (incl. �oral)

semi-�exible ISF*

appliances

non-insulating foam

thermalinsulating foam

27

UNEP DTIE Foam Sourcebook - 2010

Polyolefin (Polyethylene/Polypropylene) Foams Polyolefin foams are processed similarly to extruded polystyrene foams and have largely similar characteristics and applications. They have additional resilience in packaging applications and are often selected as the material of choice. Again polyolefin foams historically used CFCs and have progressed to other alternatives over the last 20 years.

Non-Foam Insulation Products A variety of non-foam products are used for thermal insulating purposes. Although this Sourcebook is focused on polymeric foams, it is important to understand that these co-exist with other insulation types in a competitive market, where changes in the cost-structure of foams can have consequences for market share. The most widespread product is mineral fibre, which can be based on spun rock (rock fibre) or glass (glass fibre). The low

density of these products makes them both inexpensive and comparable in embodied energy, despite the high energy intensity of the manufacturing process. However, since they rely on entrapped air for their thermal insulating properties they are losing ground against the more thermally efficient foamed products in many markets, particularly in chilled applications where moisture ingress can result in degradation of properties.

There are a number of other insulation materials available, often marketed on their apparent environmental credentials. These include naturally sourced materials such as sheep’s wool and recycled materials such as cellulose fibre. However, none of these products have broken through to the mass market.

There are also specialist insulation products such as calcium silicate, which is particularly good for high temperatures applications.

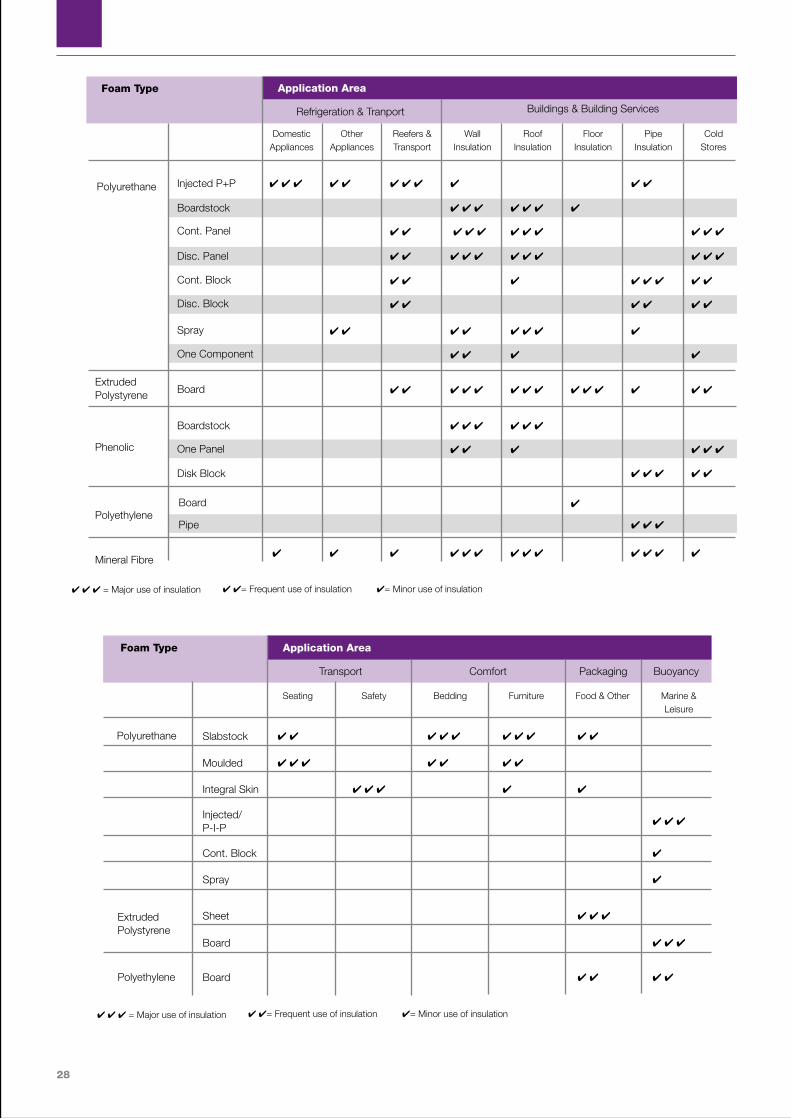

The following tables add to the earlier diagram in that, while they similarly relate the application areas with the type of foam, they also provide an indication of prevalence of use and a comparison with non-foam alternatives. They are based on an assessment generated for the IPCC/TEAP Special Report on Ozone and Climate . In this chapter, after a brief introduction on rigid foam and the role of the blowing agent, the different technology options will be reviewed by application.

28

Slabstock 4 4 4 4 4 4 4 4 4 4

Seating Safety Bedding Furniture Food & Other Marine & Leisure

Application Area

Moulded 4 4 4 4 4 4 4

Integral Skin 4 4 4 4 4

Injected/ P-I-P

4 4 4

Cont. Block 4

Spray 4

Sheet 4 4 4

Board 4 4 4

Board 4 4 4 4

Foam Type

Polyurethane

Extruded Polystyrene

Polyethylene

Transport Comfort Packaging Buoyancy

4 4 4 = Major use of insulation 4 4= Frequent use of insulation 4= Minor use of insulation

4 4 4 4 4 4 4 4 4 4 4

4 4 4 4 4 4 4 4 4 4 4

4 4 4 4 4 4 4

4 4 4 4 4 4 4 4

4 4 4 4 4 4 4 4

4 4 4 4 4 4 4 4 4 4 4

4 4 4 4 4 4

4 4 4 4

4 4 4 4 4 4 4 4 4 4 4 4 4 4

4 4 4 4 4 4

4 4 4 4 4 4

4 4 4 4 4

4

4 4 4

4 4 4 4 4 4 4 4 4 4 4 4 4

Domestic Appliances

Other Appliances

Reefers & Transport

Wall Insulation

Roof Insulation

Floor Insulation

Pipe Insulation

Cold Stores

Application AreaFoam Type

Polyurethane Injected P+P

Boardstock

Cont. Panel

Disc. Panel

Cont. Block

Disc. Block

Spray

One Component

Board

Boardstock

One Panel

Disk Block

Board

Pipe

Extruded Polystyrene

Phenolic

Polyethylene

Mineral Fibre

Refrigeration & Tranport Buildings & Building Services

4 4 4 = Major use of insulation 4 4= Frequent use of insulation 4= Minor use of insulation

29

UNEP DTIE Foam Sourcebook - 2010

4.2 Foam Manufacture and the Role of Blowing Agents Both tables shown in Section 4.1 give the first indication of the wide range of processes that are available for the processing of polymeric foams. The challenges relating to technology selection for each of these processes are covered in detail in Section 7. However, this section focuses primarily on the basic principles surrounding foam manufacture.

In general terms, a blowing agent is present in a foam formulation to ensure that the polymer matrix expands prior to solidifying. This expansion can be created by raising the temperature of the mix and causing the blowing agent to volatilise, or by reducing the pressure to which the mix is exposed (typical in extrusion processes), or a combination of both. The amount of blowing agent added and the processing conditions applied dictates the final density of the foams generated. For insulating foams, densities are typically in the range of 25-40 kg/m3. For packaging foams the densities will be lower and for comfort foams they will be lower still – often well below 20kg/m3.

Some products and processes lend themselves to the selection of blowing agents which are gaseous at room temperature. These are typically those products and processes in which expansion is controlled by pressure. In some cases, these types of processes are known as ‘froth foaming’, since the formulations froth when the pressure is released. Other processes rely on the blowing agent being in liquid form for the early stages of the process, with foam expansion and curing usually achieved by the application of heat. The following paragraphs use the example of polyurethane foam to illustrate the basic process involved.

Polyurethane rigid foams are prepared by the reaction under controlled conditions -reactants ratio, temperature and pressure- of a “fully formulated polyol” with an isocyanate, normally polymeric MDI. The term “fully formulated polyol” describes a blend of polyols with a variety of additives such as catalysts, surfactants, water, flame retardants (not typically in appliances), including the blowing agent (FTOC, 2001).

A wide spectrum of polyols of different chemical nature -polyether and polyester- and molecular architecture -functionality and equivalent weight- is used. Water is commonly added to generate CO2 by the reaction with the polymeric MDI; the polyurea groups which are simultaneously formed contribute to the build-up of the polymer skeleton. Optimum processing characteristics and end foam properties cannot usually be achieved with a single polyol and the same holds for catalysts and the other additives. As a consequence, in today´s industrial practice, a large number of formulations has been and continue to be developed to meet the different application requirements. The formulation process of polyurethane rigid foam can be graphically described as follows:

Network Formation

+

Polyether PolyolsPolyether Polyols Catalysts

SurfactantsWater

Blowing Agents

Polymeric MDI

Kinetics Control

Stabilizers

CO2

30

No

Yes

No

Yes

No

No

Yes

No

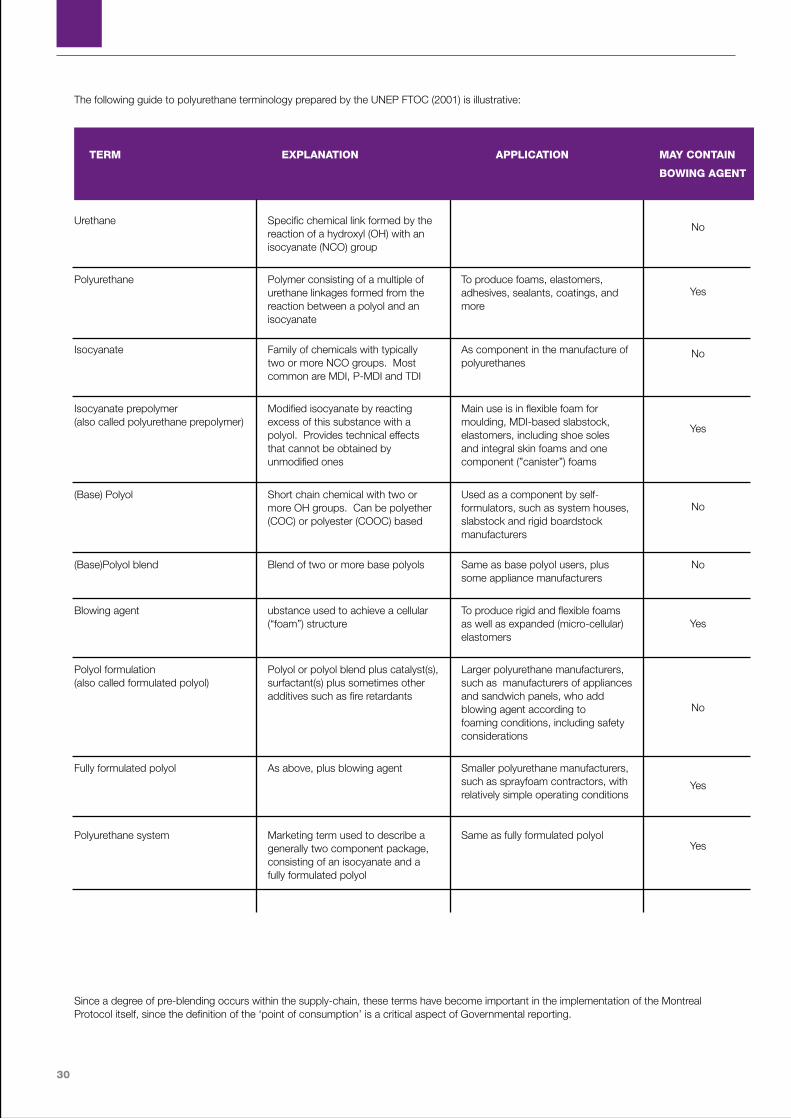

Yes

Yes

Urethane Specific chemical link formed by the reaction of a hydroxyl (OH) with an isocyanate (NCO) group

TERM EXPLANATION APPLICATION MAY CONTAIN

BOWING AGENT

Polyurethane Polymer consisting of a multiple of urethane linkages formed from the reaction between a polyol and an isocyanate

To produce foams, elastomers, adhesives, sealants, coatings, and more

Isocyanate Family of chemicals with typically two or more NCO groups. Most common are MDI, P-MDI and TDI

As component in the manufacture of polyurethanes

Isocyanate prepolymer (also called polyurethane prepolymer)

Modified isocyanate by reacting excess of this substance with a polyol. Provides technical effects that cannot be obtained by unmodified ones

Main use is in flexible foam for moulding, MDI-based slabstock, elastomers, including shoe soles and integral skin foams and one component (”canister”) foams

(Base) Polyol Short chain chemical with two or more OH groups. Can be polyether (COC) or polyester (COOC) based

Used as a component by self-formulators, such as system houses, slabstock and rigid boardstock manufacturers

(Base)Polyol blend Blend of two or more base polyols Same as base polyol users, plus some appliance manufacturers

Blowing agent ubstance used to achieve a cellular (“foam”) structure

To produce rigid and flexible foams as well as expanded (micro-cellular) elastomers

Polyol formulation (also called formulated polyol)

Polyol or polyol blend plus catalyst(s), surfactant(s) plus sometimes other additives such as fire retardants

Larger polyurethane manufacturers, such as manufacturers of appliances and sandwich panels, who add blowing agent according to foaming conditions, including safety considerations

Fully formulated polyol As above, plus blowing agent Smaller polyurethane manufacturers, such as sprayfoam contractors, with relatively simple operating conditions

Polyurethane system Marketing term used to describe a generally two component package, consisting of an isocyanate and a fully formulated polyol

Same as fully formulated polyol

The following guide to polyurethane terminology prepared by the UNEP FTOC (2001) is illustrative:

Since a degree of pre-blending occurs within the supply-chain, these terms have become important in the implementation of the Montreal Protocol itself, since the definition of the ‘point of consumption’ is a critical aspect of Governmental reporting.

31

UNEP DTIE Foam Sourcebook - 2010

4.3 Where HCFC consumption occurs in the foam sector supply chain (polyols) When proposing foam sector projects for funding, it is important to understand the various related polyol definitions in order to accurately report the HCFC consumption related to the project and to make it consistent with national HCFC data reporting:

• Polyol: Short chain chemical with two or more OH groups.

• Polyol blend: Blend of two or more polyols.

• Formulated polyol: Polyol or polyol blend plus catalyst(s), surfactant(s) plus, in some cases, other additives such as fire retardants.

• Fully formulated polyol: Formulated polyol plus blowing agent.

• Polyurethane pre-polymer: Modified isocyanate by reacting excess of this substance with a polyol.

• Polyurethane system: Marketing term used to describe a generally two component package, consisting of an isocyanate and a fully formulated polyol.

Historically the Parties of the Montreal Protocol, when reporting to the Ozone Secretariat under the requirements of Article 7, have not necessarily considered CFCs or HCFCs contained in “fully formulated polyols” to be controlled substances. This has had consequences for data reporting and the establishment of national baselines. If the use (i.e. the point at which ODS finally cease to be controlled substances by becoming products or parts thereof) is consistently reported either at the point at which the “fully formulated polyol” is being created or where the “fully formulated polyols” are used, the consumption (production + imports - exports) figures are not distorted at the global level. The only time that “reported consumption” is distorted is where reporting practices are inconsistent and consumption is either double-counted or missed altogether. Accordingly, it is important that a consistent approach is adopted. This is also important when it comes to the appropriate allocation of funding along a supply chain.

Annex D to the Montreal Protocol itself makes reference to ‘pre-polymers’ as “products containing controlled substances”, while ‘polyurethane pre-polymers’ are described as “use systems to be considered as products” in Decision I/12. However, there is no explicit

suggestion that the Parties ever intended to cover fully formulated polyols under these references, nor would the relevant technical definitions support this. Accordingly, the Parties to the Protocol are currently reconsidering the implications of adopting a definition which sees fully formulated polyols as physical mixtures still containing controlled substances (ODS). Under these circumstances, trade in fully formulated polyols is still trade in mixtures containing controlled substances. This is fully consistent with the treatment of physical mixtures in decisions which have focused primarily on refrigerant blends (e.g. Decision XIV/7).

Since the significance of reporting practice to the establishing of national baselines and the allocation of funding for the projects came to light, some Article 5 countries have adopted the policy of reporting the import of ODS contained in “fully formulated polyols” as part of their baseline consumption, while others have stayed with the historical interpretation. The Executive Committee has made it clear that the phase-out of HCFC in fully formulated polyols can be eligible for funding provided that it is included in the HPMP and that the funding is proportionate to the processes being performed.

32

The goal of consistent future reporting will depend on further considerations by the Parties. The Parties are currently reviewing how to resolve this in such a way as to avoid double-counting at the same time as avoiding the omission of actual consumption in Article 7 reporting. Readers of this Sourcebook are encouraged to check with their National Ozone Unit on the reporting policy that is currently being adopted within their own countries in order to confirm that stated baselines in HPMPs properly reflect their uses and that the legitimate funding requirements for projects in the foam sector are met.

4.4 Reasons for Original Selection of CFCs and HCFCs For a large proportion of the foams in which ODS have been used historically, and particularly those in which HCFCs are currently used, the blowing agent has two principal functions:

1. The physical expansion of the foaming mixture to produce the desired foam density. In PU rigid foam the expansion is normally achieved by the combination of two mechanisms:

• the generation of CO2 as a consequence of the water/isocyanate reaction

and

• the evaporation of the blowing agent by the exothermically reaction mixture.

The boiling temperature of the blowing agent influences how these two mechanisms are combined in time, which strongly affects the foam ability to flow. Lower the boiling point, better the flow (KHUN, 1993). Immediately after the foam is produced there are usually two gases simultaneously present in the cells: carbon dioxide and the selected blowing agent (HCFC-141b, HFC-245fa, cyclo pentane, etc.).

2. Contribution to the thermal insulating performance of the foam. The blowing agent should remain in the closed celled foam and have a low gaseous thermal conductivity plus a low rate of diffusion through the foam (polymer matrix) so that the good insulating properties are retained for many years.

A number of publications have highlighted the preferable characteristics for a blowing agent. However, these have changed over time. Prior to the existing concerns over ozone depletion and climate change, the list would have appeared as follows:

• Physiologically non hazardous (low toxicity)

• Non flammable

• Chemically/physically stable

• Advantageous boiling point for ease of handling

• Good solubility in polyols (for polyurethane systems)

• Commercially available, and

• Economically viable.

As an additional set of characteristics for thermally insulating foams, the following were deemed as advantageous:

• Low gaseous thermal conductivity

• Boiling point to minimize condensation of the blowing agent in the final foam at operational temperatures

• Low solubility in the foam polymer to avoid matrix plasticisation which can cause dimensional stability problems.

• Low diffusion rate through the polymer matrix.

When the polymeric foam industry was emerging in the early 1960s, CFCs had already been in use as refrigerants within the refrigeration sector for some years. They were, therefore, relatively plentiful, inexpensive and offered virtually all of the characteristics listed above. In particular, the gaseous thermal conductivities of the substances were low, reflecting the thermodynamic properties that had also made them suitable as refrigerants. Coupled with low toxicity and chemical stability, CFC-11 and CFC-12 were seen as virtually designed-for-purpose and dominated the industry for 25 years. Of course, it was the chemical stability of CFCs which finally became their downfall.

33

UNEP DTIE Foam Sourcebook - 2010

When, in 1974, Rowland and Molina made the first linkage between ozone depletion and chlorine in the stratosphere, few, if any, from the polymeric foams industry were watching developments. However, the discovery of the Antarctic ozone hole in 1985 added urgency to the debate and began to implicate the foam industry, both in flexible and in rigid products.

As the industry began to look for immediate alternative blowing agents, it was already known that very few, if any, alternatives could provide the package of characteristics displayed by the CFCs.

HCFC-22 was already well established as a refrigerant in the commercial refrigeration sector and it was known that the presence of the hydrogen atom in the molecule reduced the stability and resulting atmospheric lifetime of the substance somewhat. However, its boiling point was inappropriate for a large section of the industry, and, even where it wasn’t (e.g. extruded polystyrene), the molecule was found to permeate the cell walls too quickly. This situation therefore led to the search for alternative HCFCs that could fulfil the same role as CFCs with less likely damage on the environment.