guernsey’s corporate tax...

TRANSCRIPT

Guernsey’s Corporate Tax Regime

February 2016

Executive Summary

European and western economies have seen turmoil, change and contraction over the last 10 years, particularly in financial services markets. Throughout that period, the economy of Guernsey and its financial services sector has been resilient and robust.

The Island’s success as an international finance centre is built on a stable business environment with a high quality legal and regulatory framework.A key element of that framework is its straightforward business tax regime which complies with international standards.

All financial service businesses operating on the Island need to be able to offer some form of “tax neutral product” to their clients or investors. They do not require zero tax for their own operations, although as global service providers they need a competitive rate.

In order to comply with the EU Code of Conduct on Business Taxation, Guernsey had to reform its corporate tax regime in 2008. At that time, Zero-10 was the only option that allowed a broad-based zero tax product.

It was anticipated that any shortfall in tax revenues would be filled by economic growth and increased receipts on payroll taxes. The global financial crisis in 2009 meant that the anticipated growth did not emerge, although in the years following the crisis Guernsey’s economy continued to perform relatively successfully.

In 2014, corporate tax generated 16.5% of total tax revenues. This is more than double the OECD average of 8% of total taxes.

The EU Code Group approved Zero-10 in 2012. Since the original intention behind Zero-10 was to deliver a tax regime that met international standards and sustained the finance sector, it has been a success.

There are no current alternative regimes that can ensure compliance with international standards, deliver relative simplicity and sustain the finance sector. At the same time, there is no immediate external demand for the Island to reform its business tax regime.

1

GUERNSEY’S CORPORATE TAX REGIME

Guernsey, in common with many developed countries, is facing unprecedented pressures on its public services and as a result fiscal challenges. At the same time, typical models adopted by governments for taxing their business sectors have been evolving. It is therefore appropriate that Guernsey ensure that its own business tax regime is appropriate for its economy.

In this report, we have sought to draw on our expertise as tax advisers to apply relevant data and analysis to a consideration of the appropriateness of the Island’s business tax regime.

As part of this, we have recalled why Zero-10 was introduced in the first place and, importantly, how it has evolved over the years since it was first introduced in 2008. In so doing, we acknowledge that further evolution is likely to be necessary and, therefore, we have looked at other tax regimes that exist around the world, examining how these regimes might be applied to the Guernsey economy, particularly the financial services sector. We have also taken into account the competitive international environment in which Guernsey businesses operate.

Foreword

2

The international tax landscape is undergoing seismic changes, many of which may impact on Guernsey. In October 2015, the OECD issued a package of reports to address Base Erosion and Profit Shifting (BEPS), as well as a plan for follow-up work and a timetable for implementation. The project includes 15 key areas for identifying and curbing aggressive tax planning and practices, and modernising the international tax system.

In January 2016, the European Commission unveiled its new Anti-Tax Avoidance Package. This includes proposals addressing similar issues to the OECD BEPS work, as well as a common approach to tax good governance aimed at third countries. It is too early to assess the likely impact on Guernsey of this package, but it seems likely to have long-term implications as the work on the package develops.

The finance sector globally is already implementing the systems required under the recent international agreements on sharing tax information, such as FATCA and the Common Reporting Standard (CRS).

Alongside this, there has been a trend in recent years for governments to introduce certain territorial features within their existing tax regimes. For example, the UK now has a number of territorial aspects to its tax regime, including the new carried interest and disguised investment management fees rules that were introduced during 2015.

Across the globe there is increased tax competition, and corporate tax rates are generally on a downward trend. The worldwide average top corporate tax rate has declined from 30 percent to 23 percent over the decade to 2014, according to research by the OECD. We live in a fiercely competitive global business environment, with a growing number of International Finance Centres vying for Guernsey’s business. Guernsey needs to remain competitive in these challenging times.

Along with many other developed economies, Guernsey is facing strains on its public finances. The Island is experiencing the same level of modest growth that the UK and other developed nations have, whilst also facing the demands of an ageing population and decreasing birth rates. Inevitably, there is internal pressure for the States to rebalance the Island’s tax base, which includes consideration of how taxes are raised from the corporate sector, and how much of the Island’s total tax take this represents.

This report considers the scope that the Island has to reform its corporate tax regime, and what the impact of any potential alternative regimes might be on the Island’s economy.

3

GUERNSEY’S CORPORATE TAX REGIME

deemed distributions provisions, the Group ruled that the regimes were compliant with the Code. Businesses that dealt with international clients at that time will recall that during this process there was a certain amount of unease, as clients do not like uncertainty. The positive ruling from the EU was a welcome and very important step for all three islands, as it provided the certainty that our clients sought at that time. It also provided credible international recognition that few other of the Island’s competitors have received for their tax regimes. Coupled with the relative simplicity of operating Zero-10, from 2012 Guernsey was in a strong position to compete for international business.

Prior to 2008 and the Zero-10 regime, the finance sector was able to offer a tax neutral product through exempt companies, international business companies, a special insurance regime and various concessions. While they could provide this, most service providers, the banks, trust companies, fund administrators and captive insurance managers were happy to pay 20% tax on their own profits.

In the late 1990s, the EU developed its Code of Conduct on Business Taxation (“the Code”). Under the Code, countries were not supposed to offer “special tax regimes”. All of the above measures that Guernsey had were deemed to be such special regimes. If the Island was to maintain its long-held policy of adhering to international standards in tax, it was necessary to abolish these regimes. However, if it was to continue to allow the finance sector (the engine room of its economy) to operate, any new corporate tax regime had to allow a tax neutral product and to be compliant with the Code. At the time, Zero-10 was the only option that achieved this.

The original thinking was to have a general corporate tax rate of 0%, thus providing a tax neutral product that would be available to the trust, insurance and investment funds sectors, and a 10% rate for all service providers. But, in 2006, it became clear that the focus should be not only on compliance with the Code but on the broader competitive environment.

This became clear when the Isle of Man chose to introduce a very narrow scope to its 10% rate, which applied only to banking profits. In 2006, the States voted to follow suit in a bold move to attract high value business by offering 0% to service providers. The likely gap in tax revenues was to be filled by economic growth and increased receipts on payroll taxes.

The financial crisis in 2009 meant that the anticipated growth did not emerge, although in the years following the crisis Guernsey’s economy continued to perform relatively successfully.

The Zero-10 regimes of the three Crown Dependencies were reviewed by the EU Code Group in 2012 and, after changes were made to the

Why do we have Zero-10?

Guernsey’s success as an international finance centre is built on a stable business environment that comprises quality regulation and company law, service capability and a zero tax product. All financial service businesses that operate on the Island need to be able to offer some form of a “tax neutral product” to their clients or investors. Whilst they do not require zero tax for their own operations, they do require a competitive rate. The international users of investment funds, trusts and captive insurance companies require a tax neutral entity to maintain efficient returns on capital.

4

repatriation of profits from businesses in Guernsey to a parent company in say, the UK, France or Germany, would not be taxable there. So any local tax suffered in the Island could not be offset against tax paid by the parent company and, therefore, would be a real cost to the business.

Aside from the other Crown Dependencies, competition comes from further afield. Governments use tax rates as a competitive tool. The UK has reduced its corporate tax rate to 20% and aims to take it lower. Ireland and Cyprus offer 12.5%, Hong Kong offers 15% and Singapore has rates ranging from 5%-17%. There are certain disadvantages to doing business in Guernsey compared with many other jurisdictions, and other non-tax costs can often be higher here. When a tax rate differential of 12.5% can be offered, these disadvantages will be tolerated. If the differential is 2.5% the likelihood is that they will not, as the differential will be eroded by those disadvantages.

If it were possible to design a tax regime based on emerging territorial principles that worked for Guernsey, or the States decided to take the risk of losing elements of the finance sector and not attracting new business, what would be achieved?

What is clear from looking at the territorial regimes that already exist in Gibraltar and Hong Kong and those other global tax regimes that include territorial features is that they are not simple or straightforward. The requirement to determine the “source” of business is complex and not always clear, and is in many cases (Hong Kong in particular) dependent upon interpreting intricate case law.

Furthermore, no territorial regime has been reviewed and approved by the EU Code Group (or any other comparable group or body), whereas Zero-10 has.

As the impact of the Code was being considered in the period 2002-2006, it was generally accepted that a “normal” onshore tax regime would not enable Guernsey to offer that important tax neutral product. Since then, various countries, including the UK, have started to introduce provisions within their tax regimes that, in some shape or form, do not tax income earned outside the home territory. These trends have helped to generate the concept known as “territorial tax”. Indeed, the States gave serious consideration to a territorial tax regime in 2009-10 when Zero-10 was under review by the EU Code Group.

What does this mean, and how might it apply in Guernsey today and in the future?

Under a territorial approach, a country collects tax only on income earned or “sourced” within its borders. There are really only two countries whose tax regimes are truly “territorial” –Gibraltar and Hong Kong. However, many countries have territorial aspects to their corporate tax regimes, including the UK, as already mentioned, as well as France, Germany, Australia and the Netherlands, amongst others. Appendix 1 provides an overview of the relevant territorial aspects of these countries’ tax regimes. It is a common feature of all these regimes that there is no tax exemption for non-local investment income and bank interest.

It is commonplace to exempt investment funds from taxation; indeed, this is permitted under the Code. Guernsey retained its exempt regime for funds because of this. So a

tax neutral product for funds can be accommodated. However, the absence of a wider exemption for investment income would severely impact the viability of the trust sector.

Aside from that significant problem, a new regime would need to accommodate:— The captive insurance sector,

where the business is done in Guernsey;

— Active fund management businesses (this area is particularly important now with AIFMD and BEPS, which both crucially require substance and decision making to be undertaken appropriately in Guernsey);

— The growing number of trading businesses run from Guernsey, which may also increase due to the likely changes prompted by BEPS; and

— Future new business sectors that may arise, such as fintech, wider digital businesses and new finance offerings.

These types of business can only derive maximum benefit from substantive activity in the country of domicile. Given that, these important sectors could not be excluded from an acceptable territorial-based corporate tax regime.

If these sectors cannot be excluded from the regular, headline, tax rate, then the competitive position becomes very important. If any move to a territorial regime was made unilaterally, for a period of time our closest competitors could be offering a tax rate of 0% to business that Guernsey would tax at 10%. In this context, it is important to bear in mind that, as a consequence of territorial regimes in many jurisdictions,

Are there alternatives?Ideally, any alternative business tax regime would retain two key elements of Zero-10: its simplicity and its international recognition. However, the primary aim of an alternative would be to accommodate the Island’s business sector.

5

GUERNSEY’S CORPORATE TAX REGIME

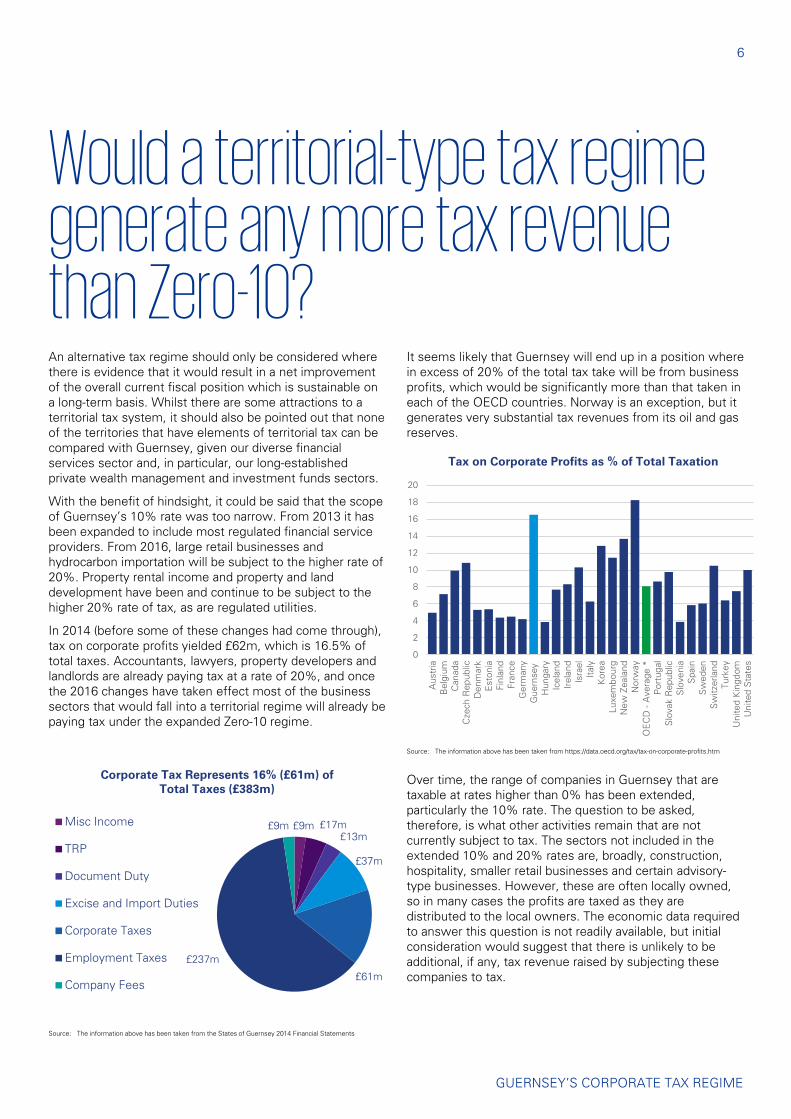

Would a territorial-type tax regime generate any more tax revenue than Zero-10? An alternative tax regime should only be considered where there is evidence that it would result in a net improvement of the overall current fiscal position which is sustainable on a long-term basis. Whilst there are some attractions to a territorial tax system, it should also be pointed out that none of the territories that have elements of territorial tax can be compared with Guernsey, given our diverse financial services sector and, in particular, our long-established private wealth management and investment funds sectors.

With the benefit of hindsight, it could be said that the scope of Guernsey’s 10% rate was too narrow. From 2013 it has been expanded to include most regulated financial service providers. From 2016, large retail businesses and hydrocarbon importation will be subject to the higher rate of 20%. Property rental income and property and land development have been and continue to be subject to the higher 20% rate of tax, as are regulated utilities.

In 2014 (before some of these changes had come through), tax on corporate profits yielded £62m, which is 16.5% of total taxes. Accountants, lawyers, property developers and landlords are already paying tax at a rate of 20%, and once the 2016 changes have taken effect most of the business sectors that would fall into a territorial regime will already be paying tax under the expanded Zero-10 regime.

£9m £17m£13m

£37m

£61m

£237m

£9m

Corporate Tax Represents 16% (£61m) of Total Taxes (£383m)

Misc Income

TRP

Document Duty

Excise and Import Duties

Corporate Taxes

Employment Taxes

Company Fees

It seems likely that Guernsey will end up in a position where in excess of 20% of the total tax take will be from business profits, which would be significantly more than that taken in each of the OECD countries. Norway is an exception, but it generates very substantial tax revenues from its oil and gas reserves.

Over time, the range of companies in Guernsey that are taxable at rates higher than 0% has been extended, particularly the 10% rate. The question to be asked, therefore, is what other activities remain that are not currently subject to tax. The sectors not included in the extended 10% and 20% rates are, broadly, construction, hospitality, smaller retail businesses and certain advisory-type businesses. However, these are often locally owned, so in many cases the profits are taxed as they are distributed to the local owners. The economic data required to answer this question is not readily available, but initial consideration would suggest that there is unlikely to be additional, if any, tax revenue raised by subjecting these companies to tax.

0

2

4

6

8

10

12

14

16

18

20

Aus

tria

Bel

gium

Can

ada

Cze

ch R

epub

licD

enm

ark

Est

onia

Finl

and

Fran

ceG

erm

any

Gue

rnse

yH

unga

ryIc

elan

dIr

elan

dIs

rael

Ital

yK

orea

Luxe

mbo

urg

New

Zea

land

Nor

way

OE

CD

- A

vera

ge *

Por

tuga

lS

lova

k R

epub

licS

love

nia

Spa

inS

wed

enS

witz

erla

ndTu

rkey

Uni

ted

Kin

gdom

Uni

ted

Sta

tes

Tax on Corporate Profits as % of Total Taxation

Source: The information above has been taken from https://data.oecd.org/tax/tax-on-corporate-profits.htm

Source: The information above has been taken from the States of Guernsey 2014 Financial Statements

6

Is there a need to change now?Currently, there is no external pressure on Guernsey to review or make any changes to its corporate tax regime. None of the work coming out of the BEPS initiative suggests that Zero-10 is under threat. The European Commission’s package on tax avoidance indicates that the work of the Code Group will be renewed and it is likely that new principles on tax governance will be developed to encourage jurisdictions to adopt various aspects of the OECD BEPS Actions. This may well bring new focus on Zero-10 in the future, but, at present, it is not certain where the work of the Code Group or the wider package will lead.

Businesses and advisers who use Guernsey talk about the importance of reliability and stability in placing business here. When the States considered changing the regime in 2010 in answer to the initial challenge from the EU Code Group, this created uncertainty in the international market. Zero-10 has since been approved by the Code Group, and this approval holds credence with international clients. Zero-10 is now a credible and widely-understood tax regime.

When Zero-10 was introduced by us in 2008, the Isle of Man had done the same in 2006 and Jersey followed in 2009. However, all three Crown Dependencies had announced their intentions to move to a Zero-10 model several years earlier. Neither of the other two islands is currently publicly contemplating a major overhaul of its corporate tax regime.

Zero-10 was introduced to provide Guernsey with a corporate tax regime that would allow its diverse financial services sector to retain existing business and compete for new business, whilst complying with international standards. It has achieved that aim and therefore should be viewed a success. There is no alternative regime that can make this claim at the moment.

It is right that the States should be aware that this situation may change, especially as BEPS evolves, as the Commission’s package develops and as the Code Group is refocused. In the future, it may become harder to sustain a regime based on a 0% tax rate and something like a territorial regime, at least in part, may at that point be an answer. However, right now, with no pressure to change and no currently viable alternative, Zero-10 is the best option that Guernsey has.

7

Appendix

Overview of territorial tax regimes

Source: KPMG Global Corporate Tax Handbook 2014

Hong Kong

Companies that carry on a trade, profession or business in Hong Kong are subject to tax on income from that trade, profession or business to the extent that the income arises in or is derived from Hong Kong. Since only profits arising in or derived from Hong Kong are taxable, the source of profits is an extremely important concept in tax law. No guidance is provided in legislation in order to determine whether income has a source in Hong Kong and, as a result, has been considered in numerous tax cases. However, certain profits, which may otherwise be characterised as having a capital nature or having a source other than Hong Kong, are deemed to be income arising in or derived from Hong Kong and thus subject to profits tax. The main items include:

— interest from sources outside Hong Kong received by or accrued to a financial institution as a result of carrying on a business in Hong Kong, and profits made by a financial institution from the sale or redemption on maturity of any certificate of deposit or bill of exchange;

— Hong Kong-source profits from the sale or redemption on maturity or presentation of a certificate of deposit or bill of exchange, except for individuals in a non-business capacity;

— sums received by a person in consideration for the transfer of a right to receive income from property;

— sums received from the exhibition or use in Hong Kong of cinematograph or television film or tape, any sound recording or any advertising material connected with such film, tape or recording;

— royalties received from the use or right to use in Hong Kong of a patent, design, trademark, copyright material, secret process or formula, or other property of a similar nature;

— royalties for the use of, or for the right to use, most intellectual property outside Hong Kong if they are deductible in determining the taxable income of a person for Hong Kong tax purposes;

— grants, subsidies or similar financial assistance related to a trade, profession or business carried on in Hong Kong (other than sums in connection with capital expenditure); and

— sums received by way of hire, rental or similar charges for the use of or the right to use movable property in Hong Kong.

Gibraltar

The territorial basis of taxation applies whereby Gibraltar tax resident companies are subject to tax only on taxable income accruing in, or derived from, Gibraltar.

The location in which profits are accrued or from which they are derived is defined as the location of

the activities that give rise to the profits. The activities are deemed to take place in Gibraltar where a business:

— requires a licence and is regulated under any law of Gibraltar; or

— engages in transactions in Gibraltar by virtue of the fact that it is licensed in another jurisdiction that has passportingrights into Gibraltar, and for which it would otherwise have needed a licence in Gibraltar.

Singapore

Companies resident in Singapore are subject to tax on any income accruing in or derived from Singapore, or received in Singapore from outside Singapore. Foreign income is therefore taxed only when it is received in Singapore.

Resident companies are exempted from tax on the following specified income received from outside Singapore, if tax has been paid in the foreign jurisdiction and that jurisdiction’s highest corporate tax rate is at least 15%:

— foreign dividends;

— foreign branch profits arising from a trade or business; and

— foreign-source income from professional, technical, consultancy or other services provided in the course of a trade, profession or business, through a fixed place of operation outside Singapore.

9

GUERNSEY’S CORPORATE TAX REGIME

Singapore (cont.)

Companies engaged in substantial business activities overseas that are unable to qualify for tax exemption for specified foreign income may also be granted exemption if they remit the foreign income under specific scenarios as set out by the Singaporean tax authority, and satisfy the qualifying conditions. The tax exemption is granted if the taxpayer is able to track the source of the foreign income. In addition, the tax authority must be satisfied that there is no round-tripping of Singapore-sourced income via the overseas investment, and that the Singaporean recipient is not a shell company.

Taxpayers who receive specified foreign income that is not covered under any of the scenarios may still apply for tax exemption, stating why they believe they should merit consideration for exemption. Tax exemption may be granted if it is determined that the remittance of the foreign income would generate economic benefits for Singapore.

An exemption is also available for foreign interest income from an offshore qualifying infrastructure project/asset, provided qualifying conditions are met, and that the ownership of, or investment in, the offshore qualifying infrastructure project/asset is substantially managed in Singapore.

A qualifying infrastructure project/asset is one that invests in specified sectors, including electricity generation, waste management, infrastructure, ports, telecommunications, water treatment, hospitals and/or clinics and schools.

United Kingdom

Companies that are tax resident in the UK are taxed on their worldwide income. However, a company may elect for the profits attributable to its foreign permanent establishments to effectively be exempt from UK corporation tax. If this election is

made, foreign losses attributable to the permanent establishment are not allowable for UK tax purposes. This election is irrevocable once made.

There is an exemption for foreign dividends received by large and medium-sized companies and, in certain cases, by small companies. Where the exemption is not available, relief is available for the foreign tax suffered. A company may also opt for the exemption not to apply.

During 2015, the UK also introduced further changes to its tax regime that are territorial in nature. Such changes included rules relating to disguised fee income that arises to investment fund executives, as well as carried interest taxation rules that include provisions whereby UK tax applies to the extent that services are performed in the UK, regardless of the tax residence position of the individual who performs the services.

Australia

Companies that are resident in Australia for tax purposes are subject to income tax on their worldwide income, including net capital gains. However, foreign business income and capital gains derived from foreign permanent establishments that carry on an active business, as well as capital gains from the disposal of shares in a foreign company engaged in an active business (subject to conditions), are not subject to tax in Australia.

Foreign non-portfolio dividends are generally not subject to tax in Australia, and no foreign tax credit is allowed in respect of such dividends.

France

Although there are some exceptions, generally speaking business income derived from a permanent establishment operating outside France is not taken into account for French tax purposes, nor are foreign permanent establishments’ losses allowable for French tax purposes.

Capital gains realised on business assets are subject to tax in France under the general rules unless such assets relate to a foreign permanent establishment, in which case they are exempt from French tax. Capital gains derived directly from the disposal of shares in foreign companies are subject to French tax at the general tax rate, and are therefore included in the taxable income of an entity. Such gains derived by parent companies resident in another EEA country may also qualify for exemption from French tax under the conditions described. However, capital gains realised on shares held in a company located in a Non-Cooperative State or Territory (“NCST”) do not benefit from the exemption regime and are subject to the standard rate of tax of 33.33%.

Germany

Taxable income for business tax is generally determined in the same way as for income tax purposes, subject to certain adjustments.

Deductions that are allowable for business tax purposes include profits attributable to permanent establishments located abroad and profit shares derived from domestic or foreign partnerships.

Netherlands

Generally speaking, Dutch tax resident companies are taxed in the Netherlands on their worldwide income. The notable items of exempt income are domestic and foreign dividends and capital gains that qualify for the exempt regime.

Foreign-source business income, interest and royalties are fully taxable in the Netherlands. Foreign dividends are also fully taxable, unless they qualify for the exempt regime. Capital gains derived through a permanent establishment abroad are treated as business income. Exemption from tax may also apply to capital gains on the disposal of a qualifying asset.

10

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2016 KPMG Channel Islands Limited a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

The KPMG name and logo are registered trademarks of KPMG International

kpmg.com/channelislands

kpmg.com/socialmedia