gst impact on various legislation

TRANSCRIPT

THE IMPACT OF GST ON VARIOUS LEGISLATION

Loh Boon How, CA

Budget 2017

2

1) Non allowable revenue expenses - Sec 39(1)(o)

a) Input tax– If the tax payer fail to register as a GST

registrar even thought he or she is liable under the Goods and Services Tax Act 2014.

– The tax payer is allow to claim an input tax from Royal Custom Department Of Malaysia.

INCOME TAX ACT 1967

B. H. Loh & Associates

1) Non allowable revenue expenses – Sec 39(1)(p)

b) Output tax• If the tax payer who borne the output tax

by himself,

• The tax payer who are liable to be registered under Goods And Services Tax Act 2014

INCOME TAX ACT 1967

B. H. Loh & Associates

• Non allowable revenue expenses – Sec 39(1)(p)(c) BIK, Perquisite and Value Of Living

Accommodation Benefit• The employer cannot claim an expenditure on

output tax on the purchase of benefit

INCOME TAX ACT 1967

Description RM

Employee benefits 5,000.00

Input tax (Not an allowable expenses S39(1)(p) 300.00

Total expenses 5,300.00

Budget 2017

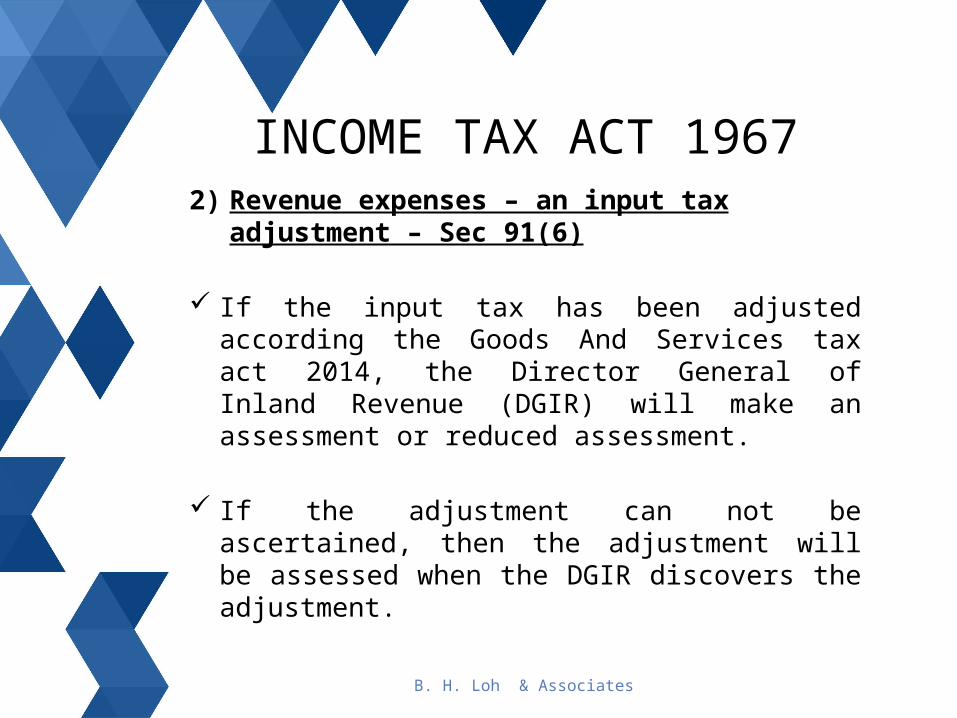

2) Revenue expenses – an input tax adjustment – Sec 91(6)

If the input tax has been adjusted according the Goods And Services tax act 2014, the Director General of Inland Revenue (DGIR) will make an assessment or reduced assessment.

If the adjustment can not be ascertained, then the adjustment will be assessed when the DGIR discovers the adjustment.

INCOME TAX ACT 1967

B. H. Loh & Associates

3) Capital allowance – Para 2E, Sch 34) Reinvestment allowance – Para 1D, Sch 7A5) Investment allowance – Para 1A, Sch 7B

Input tax claim or claimable will be not be part of qualifying expenditure.

If the tax payer fail to register as a GST registrar even thought he or she is liable under the Goods and Services Tax Act 2014.

The tax payer is allow to claim an input tax from Royal Custom Department Of Malaysia (RCDM).

INCOME TAX ACT 1967

B. H. Loh & Associates

RM

Asset cost 90,000Input tax (Block input tax) 5,400Qualifying expenditure 95,400

INCOME TAX ACT 1967

RM RM

QE 95,400Initial allowance 20% 19,080Annual allowance 10% 9,540 28,620Residual expenditure (RE) 66,780

B. H. Loh & Associates

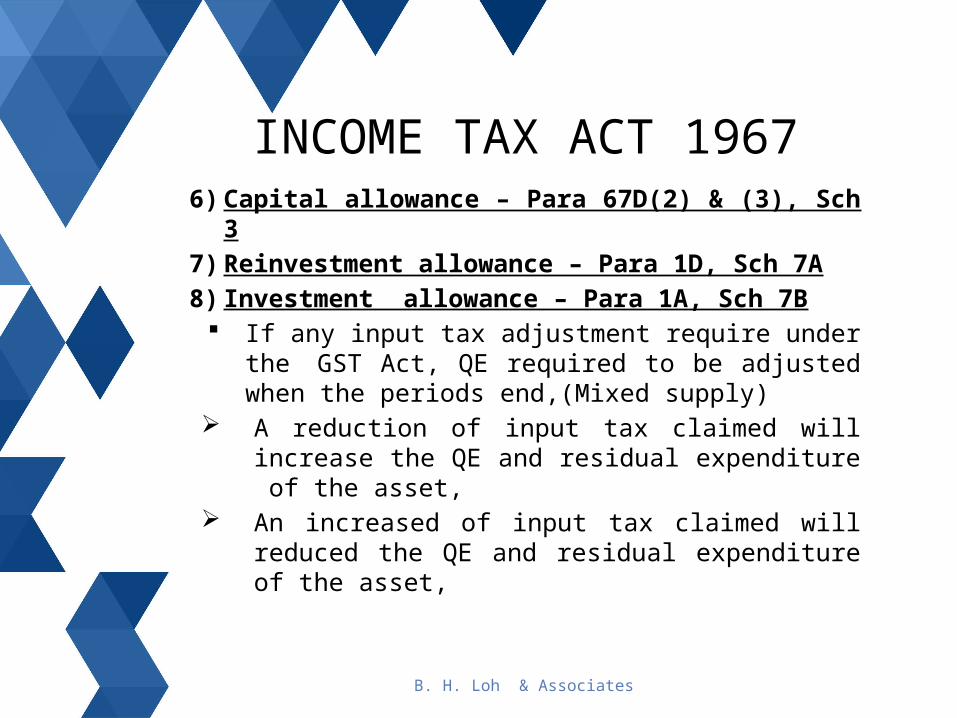

6) Capital allowance – Para 67D(2) & (3), Sch 37) Reinvestment allowance – Para 1D, Sch 7A8) Investment allowance – Para 1A, Sch 7B

If any input tax adjustment require under the GST Act, QE required to be adjusted

when the periods end,(Mixed supply) A reduction of input tax claimed will increase

the QE and residual expenditure of the asset, An increased of input tax claimed will reduced

the QE and residual expenditure of the asset,

INCOME TAX ACT 1967

B. H. Loh & Associates

Capital allowance – Para 67D(5) & (6), Sch 3

If the asset disposed, adjustment will be done in the year the asset disposed,

The amendment is also applicable for transfer between related party. (Para 38 & 40, Sch 3)

INCOME TAX ACT 1967

B. H. Loh & Associates

• Asset acquired at the price RM1,036,000 by A S/B in YA 2016,

• The same asset is transfer under control transfer to B S/B in YA 2019.

INCOME TAX ACT 1967

YA 2016 - YA 2018 (A S/B) RM RM

QE 1,036,000Initial allowance 20% - YA 2016 (207,200)Annual allowance 10% - YA 2016 (103,600) (310,800)Residual expenditure (RE) 725,200

B. H. Loh & Associates

INCOME TAX ACT 1967YA 2016 - YA 2018 (A S/B) RM

Residual expenditure (RE) 725,200Annual allowance 10% - YA 2017 (103,600)Residual expenditure (RE) 621,600Annual allowance 10% - YA 2018 (103,600)Residual expenditure (RE) 518,000An adjustment (decrease of QE) - YA 2019 (10,800)Residual expenditure (RE) 507,200

B. H. Loh & Associates

INCOME TAX ACT 1967YA 2019 – YA 2023(B S/B) RM

Residual expenditure (RE) 507,200Annual allowance 10% - YA 2019 (102,520)Residual expenditure (RE) 404,680Annual allowance 10% - YA 2020 (102,520)Residual expenditure (RE) 302,160Annual allowance 10% - YA 2021 (102,520)Residual expenditure (RE) 199,640Annual allowance 10% - YA 2022 (102,520)Residual expenditure (RE) 97,120Annual allowance 10% - YA 2023 (97,120)

B. H. Loh & Associates

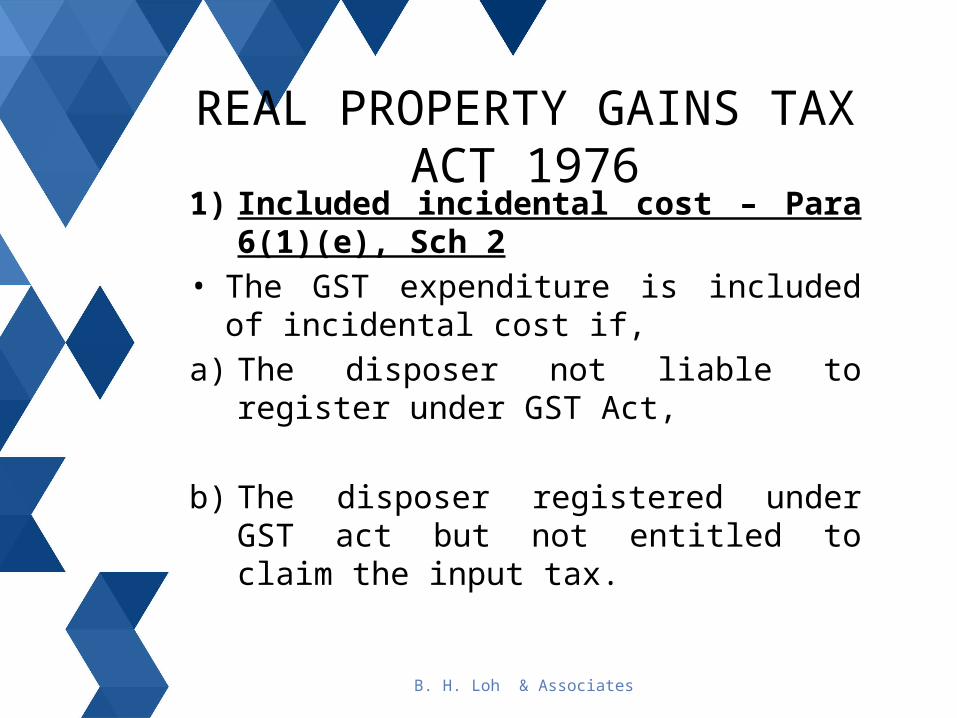

1) Included incidental cost – Para 6(1)(e), Sch 2• The GST expenditure is included of incidental

cost if,a) The disposer not liable to register under GST

Act,

b) The disposer registered under GST act but not entitled to claim the input tax.

REAL PROPERTY GAINS TAX ACT 1976

B. H. Loh & Associates

2. Excluded incidental cost – Para 7(d) & (e), Sch 2• The GST expenditure is excluded of incidental

cost if,a) The disposer fails to register even if liable under

GST Act,b) The disposer entitled to claim an input tax,c) The output tax paid or to be paid borne by the

disposer, if he / she registered or liable to be registered.

REAL PROPERTY GAINS TAX ACT 1976

B. H. Loh & Associates

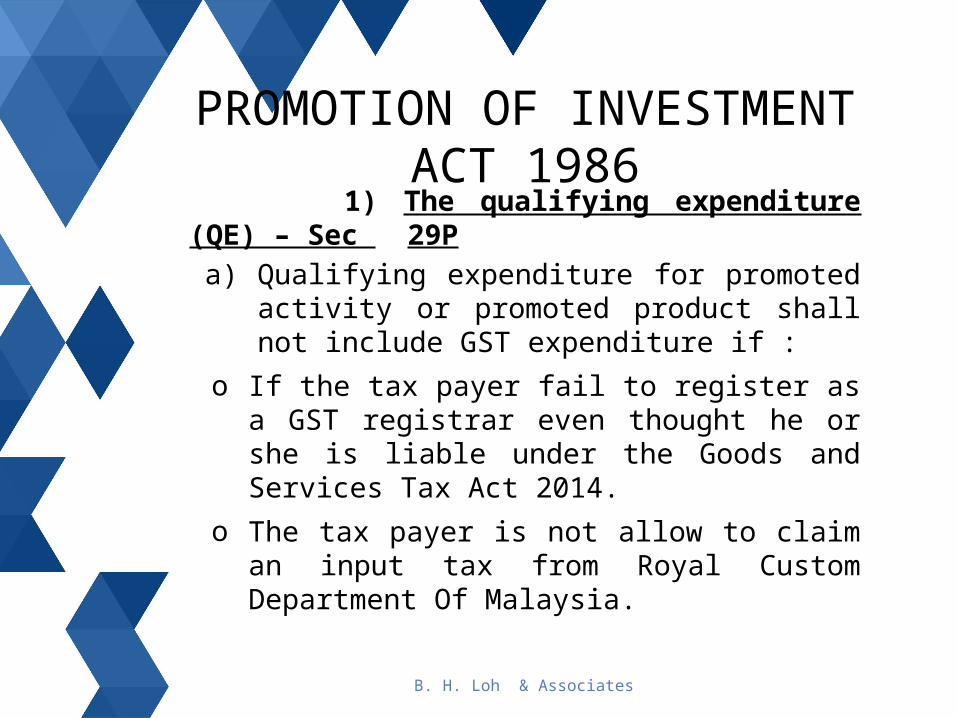

1) The qualifying expenditure (QE) – Sec 29P

a) Qualifying expenditure for promoted activity or promoted product shall not include GST expenditure if :

o If the tax payer fail to register as a GST registrar even thought he or she is liable under the Goods and Services Tax Act 2014.

o The tax payer is not allow to claim an input tax from Royal Custom Department Of Malaysia.

PROMOTION OF INVESTMENT ACT 1986

B. H. Loh & Associates

2) Investment tax allowance – Para 29Q(1) & (2)– If any input tax adjustment require under the

GST Act, QE required to be adjusted when the periods end,

A reduction of input tax claimed will increase the QE and residual expenditure of the asset,

An increased of input tax claimed will reduced the QE and residual expenditure of the asset,

PROMOTION OF INVESTMENT ACT 1986

B. H. Loh & Associates

3) An adjustment – Sec 29Q(3) If the input tax has been adjusted according the

Goods And Services tax act 2014, the Director General of Inland Revenue (DGIR) will make a necessary adjustment.

PROMOTION OF INVESTMENT ACT 1986

B. H. Loh & Associates

B. H. Loh & AssociatesAddress :

No. 1-3-15, Goldhill Complex, Tingkat Paya Terubong 1,

11060 Penang.

H/P No. : 016-4893382Email : [email protected]

Web-site / facebook : bhloh.com.my

THANK YOU

B. H. Loh & Associates