grupo carso - carso.com.mx reports... · 2 grupo carso grupo carso plays an important role in...

TRANSCRIPT

Grupo CarsoMiguel de Cervantes Saavedra 255

Col. GranadaMexico City 11520

www.carso.com.mx

GRUPO CARSOANNUAL REPORT 2007

Gru

po C

arso

ann

ual r

epor

t 200

7

CONTENTS Financial Highlights 1

Relevant businesses 2

Letter to Shareholders 4

Report of the Chief Executive Officer 5

• INDUSTRIAL DIVISION 6

Grupo Condumex 9

Telecommunications division 9

Construction and energy division 9

Automotive division 9

• INFRASTRUCTURE AND CONSTRUCTION DIVISION 11

Carso Infraestructura y Construcción 12

Manufacturing and Services for the Oil and Chemical Industries 12

Infrastructure proyects 15

Installations of ducts 15

Civil construction 15

Housing sector 15

• COMMERCIAL DIVISION 17

Grupo Sanborns 18

Board Members 20

Report of the Audit and Corporate Practices Committee 21

Financial Statements 23

François-Auguste-René Rodin(Paris, France, 1840 – Meudon, France, 1917)The CathedralLa cathédrale1908Bronze brown and green veneer62.2 x 28 x 30.5 cmForger: Alexis Rudier, ParisSignature: «A. Rodin», at the base

INVESTOR INFORMATION

Investor Relations

Jorge Serrano [email protected]

Jesús Granillo Rodrí[email protected]

ADR´s InformationSymbol: GPOVYChange: 2 stock´s: 1 ADRCUSIP Number: 400485207

Depositoty BankThe Bank of New York

Investor RelationsP.O. Box 11258Church Street StationNew York, NY 10286-1258Phone: 1-888-BNY-ADRS (269-2377)Phone (International): [email protected]

desi

gn: s

ign

i

1

FINANCIALHIGHLIGHTS

(Thousands of pesos as of December 31, 2007*)

2005 2006 2007

Sales 64,883,097 74,270,251 74,973,084

Operating Income 8,130,706 11,575,171 9,403,169

Net Income 9,288,783 8,029,372 19,459,643

EBITDA 10,143,815 13,605,853 11,526,947

Total Assets 90,097,040 94,076,236 101,720,275

Total Liabilities 40,084,929 45,692,455 36,494,724

Stockholders´Equity 50,012,110 48,383,781 65,225,551

Shares Outstanding 2,364,540,000 2,338,690,900 2,329,205,000

Earnings per Share** 3.8995 3.4228 8.3313

* Except for shares outstanding and earnings per share.

** Net income divided by weighted average of shares outstanding.

SALES CONTRIBUTIONBY SUBSIDIARY

(million pesos)

OPERATING INCOME BY SUBSIDIARY

(million pesos)

• Grupo Sanborns $31,064• Grupo Condumex $31,496• CICSA $12,864• Other -$461Total 74,973

• Grupo Sanborns $4,098• Grupo Condumex $4,399• CICSA $600• Other $306Total 9,403

• Operating Margin (%)• EBITDA Margin (%)

41.4%

42.0%

17.2%

-0.6%

43.6%

46.8%

6.4% 3.3%

SALES(million pesos)

74,973,084

64,883,097

05 06 07

74,270,251

12.5

15.6

12.5

15.6 15.4

18.3

2

GRUPO CARSO

Grupo Carso plays an important

role in various sectors of the

domestic economy. Although

its primary business divisions

are: Industrial, Construction and

Infrastructure, and Commercial,

Carso also operates in other

sectors such as automotive, and

mining industries.

INDUSTRIAL DIVISION

SERVICES / PRODUCTS› Cooper telephone cable› Electronic cable› Coaxial cable› Power cable› Fiber optic cable› Construction cables› Installation› Copper products (strips, sheets,

coils, tubes, pipes, valves)› Aluminum products (strips, coils,

extruded shapes, etc.)› PVC (tubes, joints, water

tanks,etc.)› Transformers› Magnet Wire› Power Plants

MAIN BRANDSCONDUMEXCDMSELMECNACOBREALMEXAEQUITERCONTICONPROCISASINERGIAMICROM

MARKETS› Fixed and mobile phone companies in

Mexico and Latin America› Construction industry, from

housing to heavy construction. Home Remodeling Domestic Energy Related Companies

The INDUSTRIAL DIVISIONmanufactures a range of products running from electric and telecommunications cable to auto parts, including generators, power transformers and electronic components.

CONDUMEX maintains its technological vanguard position, which allows it to hold its leadership position in the manufacture of a wide range of products for the construction, energy, telecommunication and automotive sectors.

CICSA participates in the construction of various infrastructure projects related to diverse sectors, such as: oil, communications, transportation, water and housing.

3

COMMERCIAL DIVISION

SERVICES / PRODUCTS› Department stores› Stores and Restaurant› Restaurant› Music Stores

MARKETS› Middle and high end segments

MAIN BRANDSSANBORNSMIXUPSEARSDORIAN’SSAKS FIFTH AVENUE

INFRASTRUCTURE AND CONSTRUCTION DIVISION

SERVICES / PRODUCTS› Oil platform construction› Shopping Center, Industrial facilities and Corporate Buildings Con-

struction› Highway construction› Water treatment plants› Steel tubes› Design and installation of telecommunication networks› Installation of mobile phone radio bases› Low income housing› Mid income housing› Residencial housing

MARKETS› Domestic oil related companies› Retail and Industrial Companies› Fixed and mobile phone companies in Mexico and Latin America

MAIN BRANDSPRECITUBOSWECOMEXURVITEC

SWECOMEX specializes in the design, construction and procurement of projects for the petroleum and chemical industries; highlighted are oil rigs, petrochemical plants or oil drilling.

ThE COMMERCIAL DIVISION, in its various formats, serves all segments of the population.

Among the principal formats operated by Grupo Sanborns are: Sanborns, Sears, Dorian’s, Saks Fifth Avenue and Mixup.

4

In 2007, the total number of insured in the Mexican Social Se-curity Institute rose by more than 526 thousand; however, this growth had no significant effect on the General Unemployment Rate which registered 3.72%, slightly higher than last year.

The Peso appreciated against the Dollar by 0.1% in the year, notwithstanding a parity of $10.8755 Pesos per Dollar at the close of 2006 to $10.8662 at the close of 2007.

Direct foreign investment increased by 20.8% over last year standing at US$23 billion 230 million. Remittances to Mexico in 2007 increased 1.0% over last year, totaling US$23 billion 979 million. The deficit in the current account stood at US$7 billion 370 million, equivalent to -0.8% of the GDP.

The Commercial Balance registered a deficit of US$11 billion 189.1 million, 82.4% higher than the 2006 deficit despite the 9.9% increase in oil exports due to the high prices of crude oil that prevailed throughout the year and the 8.7% increase in non-oil exports. The average price of the Mexican Mix increased by 16.4% in 2007, from US$53.0 per Barrel in 2006 to US$61.7 per barrel in 2007.

The Banco de México was successful in meeting its 3% inflation goal for 2007 plus/minus one percentage point. The National Consumers Price Index rose by 3.76% during the year, which translated into a lower inflation rate than the 4.05% registered in 2006. The underlying inflation stood at 4.0% during the year,

which signified an increase of 39 basis points in respect to the 3.61% of the previous year.

The CETES rate at 28 days maintained an average level of 7.20% in 2007, closing the year at a 7.44% rate.

In 2007, Mexico maintained macroeconomic stability, notwith-standing the slowdown of the economy in the United States of America. For 2008, the country will have to maintain a balance at the macroeconomic level and, on the other hand, stimulate economic growth and new jobs, without overlooking the need of structural reforms to modernize the country.

Grupo CarsoIn 2007 Grupo Carso consolidated its strategy in respect to the three strategic sectors: Industrial, through Grupo Condumex, with a wide range of products directed mainly to the mining, construction, energy and telecommunications sectors; construc-tion and infrastructure, where Carso Infraestructura y Construc-ción (CICSA) maintained its position as one of the most solid construction companies in the country; in addition, it entered the housing sector with the incorporation of Casas Urvitec, S.A. de C.V., through a merger; and lastly, the commercial sector in which Grupo Sanborns maintains a very significant presence with its traditional formats, and entered a new niche, the high purchasing power segment, with the opening of the first Saks Fifth Avenue in Mexico.

LETTER TO SHAREHOLDERS

Economic Panorama

The Gross Domestic Product rose by 3.3% in 2007, standing at $9 billion762.9 million current Pesos

at year end. The growth of the GDP is due mainly to the transportation, communication and financial

service sectors which registered an 8.7% and 5.0% increase, respectively, in their GDP.

The manufacturing sector in Mexico was affected by the poor economic growth in the United States of

America, which posted a 2.2% growth of its GDP, a real 1.0% decrease of manufacturing activity in

the country.

Moreover, a restructuring of the Grupo Carso portfolio of assets was observed. Among the most important adjustments are: its reduced participation in the tobacco business (Cigatam – Philip Morris México) from 50% to 20%, the divestment of its partici-pation in the ceramic tile business (Porcelanite) and the sale of the 51% holding which Condumex had in the business of the manufacture of automotive rings and cylinder liners.

Total assets of Grupo Carso were 101 billion 720 million Pesos, 8.1% higher than at the close of 2006. On the other hand, net worth at year end was 65 billion 226 million Pesos, a 34.8% increase over the previous year.

The debt of the Group was 11 billion 688 million Pesos at year end, while cash balance and securities amounted to 23 billion 191 million Pesos, resulting in a net negative debt of 11 billion 503 mil-lion Pesos, which compares with a net debt of 9 billion 375 million Pesos at the close of 2006. The lower net debt than that of 2006 results mainly from the divestments made during the year, in addi-tion to a lower integrated financing cost.

In terms of the foregoing, in March 2008 Grupo Carso paid an extraordinary dividend of 7.00 Pesos per share, a disbursement

Consolidated sales of the Group were 74 billion 973 mil-lion Pesos during the year, an increase in real terms of 0.9% over last year. Operation profit was 9 billion 403 million Pesos, while the generation of operating flow (EBITDA) was 11 billion 527 million Pesos, lower by 18.8% and 15.3% respectively than the results of 2006.

The lower operating results of Grupo Carso are due to the lower results reported by three divisions which, in turn, were affected by market conditions. There was

greater competition in some markets in the Industrial Division, particularly at the end of the year and, in the mining sector, the price of some metals dropped; the margins of the Infrastructure and Construction Divisions were affected mainly by extraordinary expenses in a Swecomex project, while the Commercial Division felt the impact of reduced consumer spending as the year progressed.

Net profit for 2007 was 19 billion 460 million Pesos, considerably higher than the 8 billion 029 million Pe-sos obtained in 2006, due mainly to the profit obtained from the sale of assets.

During the year, Grupo Carso made capital investments of 4 billion 491 million Pesos, distributed among the projects of its three divisions.

Net profit was 19,460 million Pesos, a

significant increase over last year.

REPORT OF THECHIEF EXECUTIVE OFFICER

of approximately of 16 billion 285 million Pesos. Grupo Carso considers that the financial structure of the Company, after pay-ing the dividend, is adequate to handle the various investment projects required by the various subsidiaries.

On behalf of the Board of Directors I wish to express my apprecia-tion to the staff of directors of Grupo Carso for their foresight and their dedication, both basic for the success of the Group, and to all our employees for their efforts and their commitment in reaching our goals, and to our shareholders who have placed their trust in us. Grupo Carso will continue its path to success thereby contrib-uting to the successful development of our country.

Very truly yours.

Carlos Slim DomitChairman of the Board

5

6

The Industrial Division of Grupo Carso, is represented by Grupo Condumex, an industrial conglomerate mainly focused on the telecom, energy, construction, mining and auto parts sectors.

INDUSTRIALDIVISION

$31,496 million Pesos reported by Grupo

Condumex as revenue

T h E O P E R A T I N G F L O w G E N E R A T E D

B Y C O N D U M E x w A S

$5,420 M I L L I O N P E S O S

7

The slowdown of the economy in the United States of America

generated a greater offer in the domestic market

8

Grupo Condumex

Grupo Condumex reported consolidated sales of 31 billion 496 million Pesos in 2007, 1.6% lower than the 32 billion

011 million Pesos of the preceding year. Operation profit was reported at 4 billion 399 million Pesos during the year, an

18.5% decrease in respect to 2006. Operating flow was 5 billion 420 million Pesos, 14.5% lower than the previous year.

Operating results of Grupo Condumex were affected by lower volumes of minerals produced in the mining division, while

other product lines were affected by a greater offer in

the domestic market, resulting from a slowdown of the

U.S. economy.

Sales(million pesos)

Operating Margin(%)

EBITDA Margin(%)

06 07 06 07 06 07

19.8

16.932,011

17.2

14.0

31,496

ThE TELECOMMUNICATIONS DIVISION reported lower volumes in copper cable, but a significant increase in fiber optic and coaxial cable.

ThE CONSTRUCTION AND ENERgy DIVISION maintained volumes in power cable, metals, transformers and turnkey projects, similar to those of 2006, as is the case with the Nacobre Aluminum Division; on the other hand, the other divisions of Nacobre, Copper and Plastics, reported lower volumes than those of the preceding year.

During the year the AUTOMOTIVE DIVISION reported growth in vol-umes of harnesses and automotive cable.

The milling volumes of the Mining Division rose 9.2% over 2006. How-ever, the volumes of gold, silver, lead, zinc and copper were lower than those reported in 2006. Capital investments during the year were approximately US$98 million, used mainly for programs to maintain industrial assets, as well as various investments in the mining sector.

9

A T Y E A R E N D , T h E B A C K L O G O F

C I C S A w A S

$14,334 M I L L I O N P E S O S

10

11

Carso Infraestructura y Construcción (CICSA) has its businesses grouped into five sectors: the Installation of Ducts (telecommunications, gas, water, oil) through CICSA; Manufacture and Services for the Oil and

Chemical Industries through Swecomex; Infrastructure Projects, through its subsidiary Constructora de Infraestructura Latinoamericana (CILSA); Civil Construction, through its subsidiary Grupo PC Constructores; and the Housing Sector, incorporated in November 2007, through Urvitec.

INFRASTRUCTURE AND CONSTRUCTION

DIVISION

$12,864 million Pesos, consolidated

sales of CICSA.

Carso Infrastructure and Construction

Total assets of CICSA were 14 billion 080 million Pesos at year end, representing a 20.2% increase over the close of 2006; on the

other hand, at the end of 2007 net worth was 8 billion 397 million Pesos, a 9.3% increase over the previous year.

The CICSA debt was 1 billion 325 million Pesos at year end, while the balance of cash and securities was 1 billion 835 million

Pesos, resulting in a negative net debt of 510 million Pesos,

compared with a negative net debt of 2 billion 192 million

Pesos at the close of 2006.

Carso Infraestructura y Construcción reported annual consolidated sales of 12 billion 864 million Pesos, 5.4% higher than the previous year. Operation profit during the year was 600 million Pesos, 57.2% lower than the profit reported a year ago, while operating flow was 881 million Pesos during the year, a decrease of 45.6% in comparison with 2006. Net profit during the year was 297 million Pesos, 69.7% lower than in 2006. Operating results were affected mainly by extraordinary expenses related to a project of the Swecomex Division.

At the close of December 2007, the backlog of CICSA was 14 billion 334 million Pesos, 73% of which will be executed in 2008.

In 2007 CICSA made capital investments of approximately US$80 million, used mainly to construct a structural steel piping plant and for the execution of various projects.

MANUFACTURING AND SERVICES FOR THE OIL AND CHEMICAL INDUSTRIES The Manufacturing and Services for the Oil and Chemical Sector reported revenue of 4 billion 623 million Pesos, 22.0% higher than the preceding year. Operation profit was 33 million Pesos, a significant reduction in comparison with the 560 million Pesos reported in 2006. Operating flow was 73 million Pesos in 2007, in contrast to the 598 million Pesos reported the previous year. Operating results of Swecomex were affected mainly by extraordinary expenses related to a project.

In 2007, Swecomex continued working on various projects, among which is a project for drilling and termination of oil wells for an approximate value of 1 billion 432 million Pesos and US$280 million. Among the new contracts obtained by this sector during the year is one for the expansion of an eth-ylene oxide plant in the Morelos Petrochemical Complex at Coatzacoalcos, Veracruz, for an approximate value of 485 million Pesos.

At the close of 2007, the backlog in this sector was 4 billion 580 million Pesos, with work to be performed in 2008 and 2009.

Sales(million pesos)

06 07

12,86412,200

12

The Manufacturing and Services for the Oil and Chemical Industries

Sector reported revenue of

$4,623 million Pesos

13

CICSA started operations in the housing sector

with the acquisition of Casas Urvitec

14

INfRASTRUCTURE PROjECTS The CICSA infrastructure projects sector reported sales of 3 billion 292 million Pesos during the year, a 16.9% increase over 2006. Operation profit was 205 million Pesos, a 39.1% reduction compared with 2006. Operating and EBITDA margins were 6.2% and 6.4%, respectively.

In 2007, CILSA concluded the construction of the Tepic - Villa Unión High-way, the Northeastern Bypass of the Metropolitan Zone of the City of Toluca, and continued the construction of the Northern Bypass in Mexico City as well as the construction of two water treatment plants in the City of Saltillo, Coahuila. Moreover, during the year CILSA launched two hydroelectric projects in Panama, which together have an approxi-mate value of US$250 million. Lastly, in the bidding procedure held by the Panama Canal authority (ACP) to execute the project referred to as PAC-2, CILSA was awarded the contract for the sum of US$25 million; the project consists of ground removal from the Panama Canal.

At the close of 2007, this sector had an approximate backlog of 4 billion 636 million Pesos, to be executed in 2008 and 2009.

INSTALLATION Of DUCTS The Installation of Telecommunications Ducts sector reported sales of 3 billion 607 million Pesos during the year, a 14.3% reduction compared with 2006 revenue. Lower sales are due to a decrease in the installation of networks by its principal domestic clients which, nev-ertheless, was partially offset by various contracts obtained in Central and South America. Operation profit was 182 million Pesos, 39.3% below that of the preceding year, and a reduction of 207 basis points in operating margin which stood at 5.0%. Operating flow dropped 32.3% in comparison with 2006; the EBITDA margin was 6.9%, 182 basis points lower than the previ-ous year.

At year end, this sector had contracted works for 2 billion 611 million Pesos.

Operating Margin(%)

06 07

13.3

6.8

EBITDA Margin(%)

06 07

11.5

4.7

CIVIL CONSTRUCTION Grupo PC Constructores reported annual sales of 1 billion 897 million Pesos, 25.5% higher than 2006. Operation profit was 78 million Pesos, an 8.4% increase over 2006. Operating margin was 4.1% during the year.

In 2007, the company was awarded various projects in Mexico, among which are: the construction of the first stage of Corporativo Polanco in Mexico City, the construction of the Ciudad Azteca Stopping Place, the construction of the Altabrisa shopping center in Mérida, Yucatán, and the construction of a shopping center in Nezahualcóyotl, State of Mexico.

At the end of 2007, Grupo PC Constructores had a backlog of approxi-mately 2 billion 507 million Pesos.

hOUSINg SECTOR Urvitec merged with CICSA on November 1, 2007; consequently, for 2007, the consolidated figures of CICSA present only the results of the two month period November to December, 2007.

During said period, the housing sector reported revenue of 229 million Pesos, 2.7% lower than 2006. Operation profit was 46 million Pesos, while the EBITDA was 48 million Pesos. Sales margins were 19.9% and 20.8% respectively.

In 2007, Urvitec used land reserves for the construction of 3,049 residen-tial units, which were concluded the same year. Toward the end of 2007, projects were launched in the State of Mexico, Nuevo León and Tamaulipas, with investments of close to 125 million Pesos. It is considered that the construction of these projects will conclude in the first semester of 2008.

15

G R U P O S A N B O R N S O P E R A T E S 418

U N I T S I N M E x I C O A N D C E N T R A L A M E R I C A

16

17

In 2007 sales of Grupo Sanborns were 31 billion 065 million Pesos, a 2.2% decrease in comparison with the previous year.

Revenue was affected by reduced consumer spending, although this was partially offset by greater promotional activity.

COMMERCIALDIVISION

Grupo Sanborns reported consolidated sales of

$31,065 million Pesos

Grupo Sanborns

Operating profit was 4 billion 098 million Pesos, a 9.4% reduction, while the operating margin stood at 13.2%. Operating

flow (EBITDA) was 4 billion 859 million during the year, 7.6% lower than 2006. The EBITDA margin was 15.6%. Operat-

ing margins were affected by greater promotional activity.

In 2007, Grupo Sanborns continued strengthening its presence in Mexico through its shopping centers and principal formats,

maintaining emphasis on the location of its new units. During the year, 8 Sanborns stores were opened to total 157 units; 6

Sears stores were opened, although 3 units of this format were closed and now total 59 units; 5 music stores were opened and

2 were closed, resulting in the existence of 79 music stores

at year end. In November, Grupo Sanborns opened the first

Saks Fifth Avenue store in Mexico, in the Santa Fe Shopping

Center, a top level development in Mexico City.

In total, Grupo Sanborns operates 413 units in Mexico and 5 in Central America under different formats which, in addition to those mentioned, include: Dorian’s, Dax, Más, Sanborns Café, The Coffee Factory, Café Caffe and some specialized boutiques.

Combined annual sales of Sanborns, Sanborns Café and the music stores rose by 1.3% over the previous year, while same store sales decreased by 2.3% during the year. Operating margins and EBITDA stood at 10.0% and 12.9%, respectively.

Revenues of Sears stores increased by 4.5% in 2007, while same store sales rose by 0.5% during the year. Sears reported operating and EBITDA margins of 14.4% and 16.3% respectively.

Annual sales of Dorian’s dropped 7.8% in comparison with 2006, while operating and EBITDA margins were 4.2% and 6.7%, respectively.

During the year, Grupo Sanborns made capital investments of approximate-ly US$ 218 million, principally in the openings mentioned in the preceding paragraphs.

Very truly yours,

Humberto Gutiérrez-Olvera ZubizarretaChief Executive Officer

Sales(million pesos)

Sanborns

Sears

Dorian’sOther

Sears 47.3% $ 14,696 Sanborns 41.1% $ 12,753 Dorian’s 10.1% $ 3,122 Other 1.5% $ 493 Total 100.0% $ 31,065

Sales (million pesos)

• Operating Margin (%)• EBITDA Margin (%)

31,065

06 07

30,410

Operating Income(million pesos)

Sanborns

Sears

Dorian’s

Sears 51.67% $ 2,117 Sanborns 31.17% $ 1,277 Dorian’s 3.22% $ 132 Other 13.94% $ 571 Total 100.0% $ 4,098

Other

17.3

14.9

15.6

13.2

18

Saks Fifth Avenue opened

its first store in Mexico in the Santa Fe

Shopping Center

19

years as Type of Board Members Position* Board Member** Board Member*

Carlos Slim Domit COB Grupo Carso Seventeen Patrimonial Related COB and CEO – Grupo Sanborns COB – U.S. Commercial Corp. Co-Chairman – Teléfonos de México Vicechairman – Carso Global TelecomRubén Aguilar Monteverde Member of National Advisory Board – Three Independent Banco Nacional de México, S.A.Antonio Cosío Ariño CEO – Cía. Industrial de Tepeji del Río Sixteen IndependentJaime Chico Pardo COB – Teléfonos de México Eigthteen Related COB and CEO – Carso Global Telecom Co-Chairman – Impulsora del Desarrollo y el Empleo en América LatinaArturo Elías Ayub Director of Strategical Alliances, Communication Ten Related and Institutional Relations – Teléfonos de México CEO – Fundación TelmexClaudio x. González Laporte COB – Kimberly Clark de México Seventeen IndependentJosé humberto Gutiérrez Olvera Zubizarreta CEO – Grupo Carso Seventeen Related COB and CEO – Grupo CondumexDaniel hajj Aboumrad CEO – América Móvil Thirteen RelatedRafael Moisés Kalach Mizrahi COB and CEO – Grupo Kaltex Fourteen IndependentJosé Kuri harfush COB – Janel Eigthteen IndependentJuan Antonio Pérez Simón COB – Sanborn hermanos Eigthteen Independent Vicechairman – Teléfonos de MéxicoAgustín Santamarina Vázquez Board Member – Santamarina y Steta Sixteen IndependentFernando Senderos Mestre COB – Grupo Kuo One Independent COB – DinePatrick Slim Domit Vicechairman – Grupo Carso Twelve Patrimonial Related COB – América Móvil Director of Retail – Teléfonos de México COB – Grupo TelvistaMarco Antonio Slim Domit COB and CEO – Grupo Financiero Inbursa Seventeen Patrimonial Related COB – Inversora Bursátil COB – Seguros InbursaFernando Solana Morales CEO – Solana y Asociados, S.C. Three Independent

Alternate Board Members

Eduardo Valdés Acra Vicechairman – Grupo Financiero Inbursa Sixteen Related COB – Banco Inbursa CEO – Inversora BursátilJulio Gutiérrez Trujillo Business Consultant Three IndependentAntonio Cosío Pando General Manager – Cía. Industrial de Tepeji del Río Six IndependentFernando G. Chico Pardo CEO – Promecap, S.C. Eigthteen IndependentAlfonso Salem Slim CEO – Impulsora del Desarrollo Seven Independent y el Empleo en América LatinaDavid Ibarra Muñoz CEO – Despacho David Ibarra Muñoz Six IndependentAntonio Gómez García CEO – Carso Infraestructura y Construcción Four RelatedCarlos hajj Aboumrad CEO – Sears Roebuck de México Ten IndependentIgnacio Cobo González COB – Grupo Calinda Six IndependentAlejandro Aboumrad Gabriel COB – Grupo Proa Seventeen IndependentLuis hernández García CEO – Cigatam One Independent

Treasurer

Quintín humberto Botas hernández Comptroller – Grupo Condumex Five

Secretary

Sergio F. Medina Noriega Legal Director – Teléfonos de México Eigthteen

Pro-secretario

Alejandro Archundia Becerra Legal General Manager – Grupo Condumex Six

* Based on Board Members information.** Years as board member are considered since 1990, year of inscription in the Bolsa Mexicana de Valores.

Board of Directors

20

Grupo Carso, S.A.B. de C.V. and Subsidiaries

2121

Annual report of the Committee in charge of Auditing, Corporate Practices, Finance and Planning

To the Board of Directors:

As the chairman of the Committee for Corporate Practices and Auditing of Grupo Carso, S.A.B. de C.V. (the “Company”), I pres-ent the following annual activities report of said committee for the 2007 corporate period.

Auditing functionsThe internal control system and internal auditing of Grupo Carso, S.A.B. de C.V., and of the corporate entities it controls is satis-factory and complies with the guidelines approved by the Board of Directors, as observed from the information provided to the committee by Company management and contained in the certification of the external auditor.

We received no information of any relevant default on the guidelines and operation policies and accounting registries of the Company or of the entities it controls and, consequently, no preventative or corrective measure was taken.

The performance of the accounting firms Galaz, Yamazaki, Ruiz Urquiza, S.C. and Camacho, Camacho y Asociados, S.C., the enti-ties that performed the audit of the financial statements at December 31, 2007, of Grupo Carso, S.A.B. de C.V. and subsidiaries, as well as of the external auditor in charge of the audit, was satisfactory and the objectives desired at the time they were con-tracted were achieved. Pursuant to the information provided by said firms to Company management, their fees for the external audit represented a percentage inferior to 20% of their total revenue. On the other hand, the Committee authorized Galaz, Yamazaki, Ruiz Urquiza, S.C., to provide to one of the Company subsidiaries additional services consisting of a determination of the fiscal bases for payment of the Value-Added Tax.

As a result of the review of the financial statements at December 31, 2007 of the Company and of the corporate entities con-trolled by it, no adjustments were required of the audited figures or of any other aspects revealed in said statements.

The accounting policies followed by the Company were amended to comply with the following Financial Information Standards: B-3 relative to the statement of results; B-13 relative to revealing facts subsequent to the date of the financial statements; C-13 regarding related parties; D-6 regarding the capitalization of the integrated finance result; B-10 regarding the effects of infla-tion; and D-3 regarding benefits to employees, as well as D-4 regarding taxes on profits.

In respect to financial guidelines B-10 and D-4, as of 2008 all amounts corresponding to results by the holding of non-monetary assets and the initial accumulated effect of deferred taxes, respectively, were reclassified to accumulated results, as established in said standards; the modification that was made in respect to the other guidelines had no significant effect.

As we were informed by Company management and to the best of our knowledge, there were no relevant observations made by shareholders, members of the board, relevant executives, employees and, in general, any third party, in respect to the ac-

José Kuri HarfushChairman

Rafael Moisés Kalach MizrahiAntonio Cosío AriñoClaudio X. González LaporteAgustín Santamarina Vázquez

Audit and Corporate Practices Committee

Grupo Carso, S.A.B. de C.V. and Subsidiaries

22

counting, internal controls and matters related to the internal or external audit or any claims made by said persons regarding irregularities in the Company administration.

During the period to which this report relates, we verified that the resolutions adopted by shareholders’ meetings and Board of Directors of the Company were duly complied with.

Moreover, pursuant to the information provided by Company management, we verified that the Company has controls that allow for determining that it complies with provisions applicable to it in respect to the securities market and that the legal de-partment reviews at least once a year said compliance and no observations were made in this respect nor was there any adverse change in the legal situation.

Regarding the financial information prepared by the Company which it files with the Bolsa Mexicana de Valores and the Na-tional Banking and Securities Commission, we verified that said information is prepared under the same principles, criteria and accounting practices as those with which the annual information is prepared.

Functions in corporate practicesThe Chief Executive Officer of the Company and the relevant executives of the corporate persons controlled by the Company satisfactorily complied with the objectives assigned to them and with their responsibilities.

Transactions with related parties carried out by certain Company subsidiaries were approved; they were audited by Galaz, Yamazaki, Ruiz Urquiza, S.C., as required in note 15 of certified financial statements of Grupo Carso, S.A.B. de C.V. and sub-sidiaries at December 31, 2007, among which are the following significant transactions which represent more than 1% of the consolidated assets of the Company, executed successively: Teléfonos de México, S.A.B. de C.V., for installation services of an external plant and optic fiber; Autopista Arco Norte, S.A. de C.V., for the construction of highways; Delphi Packard Electric Sys-tems, for the sale of harnesses, cable and automotive engineering services, and Radiomóvil Dipsa, S.A. de C.V., for the purchase of equipment and telephone cards.

Grupo Carso, S.A.B. de C.V. has no employees. The Chief Executive Officer of the Company receives no remuneration for the performance of his activities. As to the integrated remunerations of the relevant executives of the companies controlled by the Company, we verified that they comply with the policies approved by the Board of Directors.

The Board of Directors of the Company granted no dispensation for a member of the board, relevant executive or individual with a power to authorize used business opportunities for himself or in favor of third parties, that correspond to the Company or to the corporate entities controlled by it or in which he has a significant influence. On the other hand, the Committee did not grant dispensations for the transactions referred to in paragraph c), Section III of Article 28 of the Securities Market Law.

The sale of all the shares of Porcelanite Holding, S.A. de C.V., to Grupo Lamosa, S.A.B. de C.V., was approved; it was also ap-proved for Grupo Carso, S.A.B. de C.V. to sell to Dumas B.V., a subsidiary of Philip Morris International Inc., 30% of its partici-pation in the tobacco business. Approval was also granted for the donation to Fundación Carso, A.C., of a piece of property, two paintings and the cultural and historical collection of lithographs and chromes of the “Galas de México” collection, which includes various assets.

Finance and planning functionsAs to the functions of the Committee in matters of finance and planning, in the 2007 fiscal period, the Company and some of the entities it controls effected some important investments; we verified that the financing for the foregoing was carried out in accordance with the medium and long-term strategic plan of the Company. In addition, we evaluated from time to time that the strategic position of the company conformed to said plan. We also reviewed and evaluated the budget for the 2007 fiscal period, together with the financial projections taken into account for preparing them, in which are included the principal invest-ments and finance transactions of the Company, which we consider to be viable and congruent with investment and finance policies and with the company’s strategic vision.

For the preparation of this report, the Committee for Corporate Practices and Audit based its conclusions on the information provided to it by the Chief Executive Officer of the Company, the relevant executives of the corporate entities controlled by the company and the external auditor.

Chairman

José Kuri Harfush

22

Grupo Carso, S.A.B. de C.V. and Subsidiaries

23

To the Board of Directors and Stockholders of Grupo Carso, S.A.B. de C.V.

We have audited the accompanying consolidated balance sheets of Grupo Carso, S.A.B. de C.V. and subsidiaries (the “Company”) as of December 31, 2007 and 2006, and the related consolidated statements of income, changes in stockholders’ equity and changes in financial position for the years then ended, all expressed in thousands of Mexican pesos of purchasing power as of December 31, 2007. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in Mexico. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement and that they are prepared in accordance with Mexican Financial Reporting Standards. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the financial reporting standards used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, such consolidated financial statements present fairly, in all material respects, the financial position of Grupo Carso, S.A.B. de C.V. and subsidiaries as of December 31, 2007 and 2006, and the results of their operations, changes in their stockholders’ equity and changes in their financial position for the years then ended in conformity with Mexican Financial Reporting Standards.

The accompanying consolidated financial statements have been translated into English for the convenience of users.

Galaz, Yamazaki, Ruiz Urquiza, S.C.A Member of Deloitte Touche Tohmatsu

C.P.C. Walter Fraschetto

March 7, 2008(March 13, 2008 with respect to Note 22)

Independent auditors’ report

Grupo Carso, S.A.B. de C.V. and Subsidiaries

24

Consolidated balance sheetsAs of December 31, 2007 and 2006 (In thousands of Mexican pesos of purchasing power as of December 31, 2007)

Assets 2007 2006

Current assets: Cash and cash equivalents $ 21,269,666 $ 6,763,222 Investments in financial instruments 1,920,950 2,085,377 Notes and accounts receivable: Trade (net of allowances for doubtful accounts of $372,498 in 2007 and $323,861 in 2006) 15,344,815 14,730,252 Other 1,805,346 779,122 Due from related parties 1,751,992 1,887,414 18,902,153 17,396,788 Derivative financial instruments 456,089 520,739 Inventories – Net 16,191,220 16,045,592 Prepaid expenses 249,061 178,530 Discontinued operations 1,618,984 5,843,348 Total current assets 60,608,123 48,833,596Long-term receivables 46,759 46,202Property, machinery and equipment: Buildings and leasehold improvements 22,950,154 23,000,486 Machinery and equipment 26,679,872 26,877,106 Vehicles 1,330,674 1,197,357 Furniture and equipment 3,211,875 2,900,265 Computers 1,775,327 1,797,283 55,947,902 55,772,497 Accumulated depreciation (32,606,740) (32,009,767) 23,341,162 23,762,730 Land 8,852,752 8,652,150 Construction in progress 2,763,055 1,211,294 34,956,969 33,626,174Investment in shares of associated companies and others 5,266,855 4,458,069Net asset projected for labor obligations 588,369 488,955Other assets – Net 239,134 156,523Long-term assets from discontinued operations 14,066 6,466,717Total $ 101,720,275 $ 94,076,236

Liabilities and stockholders’ equityCurrent liabilities: Borrowings from financial institutions $ 610,589 $ 6,979,460 Current portion of long-term debt 2,109,600 904,391 Trade accounts payable 7,847,111 5,971,629 Accrued expenses and taxes other than income taxes 3,973,284 4,566,379 Derivative financial instruments 284,071 830,747 Advances from customers 1,430,668 1,099,819 Due to related parties 1,054,516 33,442 Income tax payable 1,659,580 690,531 Employee statutory profit sharing 435,496 432,232 Discontinued operations 552,788 3,533,754 Total current liabilities 19,957,703 25,042,384Long-term debt 8,967,585 10,339,998Deferred income taxes 7,384,748 6,875,635Deferred statutory employee profit sharing 20,076 31,998Other long-term liabilities 135,000 141,252Deferred income – net 29,612 26,251Long-term liabilities from discontinued operations – 3,234,937 Total liabilities 36,494,724 45,692,455Stockholders’ equity: Capital stock 6,608,043 6,611,744 Net share placement premium 2,160,658 2,160,658 Contributed capital 14,902 14,902 Retained earnings 91,798,563 74,012,889 Insufficiency in restated stockholders’ equity (34,949,720) (34,141,587) Initial cumulative effect of deferred income taxes (8,364,341) (8,364,341) Derivative financial instruments and unrealized result on investments (59,862) (62,757) Majority stockholders’ equity 57,208,243 40,231,508 Minority interest in consolidated subsidiaries 8,017,308 8,152,273 Total stockholders’ equity 65,225,551 48,383,781Total $ 101,720,275 $ 94,076,236

See accompanying notes to consolidated financial statements.

Grupo Carso, S.A.B. de C.V. and Subsidiaries

25

Consolidated statements of incomeFor the years ended December 31, 2007 and 2006(In thousands of Mexican pesos of purchasing power as of December 31, 2007, except per share information)

See accompanying notes to consolidated financial statements.

2007 2006

Net sales $ 74,973,084 $ 74,270,251

Cost of sales 54,134,082 52,024,841 Gross profit 20,839,002 22,245,410 Operating expenses 11,435,833 10,670,239 Income from operations 9,403,169 11,575,171

Other (income) expense - net (14,008,414) 293,199

Net comprehensive financing result: Interest expense 2,945,546 3,472,216 Interest income (2,224,663) (1,878,634) Exchange (gain) loss - net (373,308) 324,815 Monetary position (gain) loss 23,821 (72,547) 371,396 1,845,850

Equity in income of associated companies and others (1,150,192) (1,151,104)

Income from continuing operations before income taxes 24,190,379 10,587,226

Income taxes 5,353,649 2,722,730

Income from continuing operations 18,836,730 7,864,496

Income from discontinued operations (1,974,679) (1,929,332)

Consolidated net income $ 20,811,409 $ 9,793,828

Net income of majority stockholders $ 19,459,643 $ 8,029,372Net income of minority stockholders 1,351,766 1,764,456

$ 20,811,409 $ 9,793,828

Basic earnings per share $ 8.33 $ 3.42

Income from continuing operations $ 8.06 $ 3.35Discontinued operations - net 0.85 0.82

Consolidated net income $ 8.91 $ 4.17

Weighted average of shares outstanding (thousands) 2,335,728 2,345,841

Grupo Carso, S.A.B. de C.V. and Subsidiaries

2626

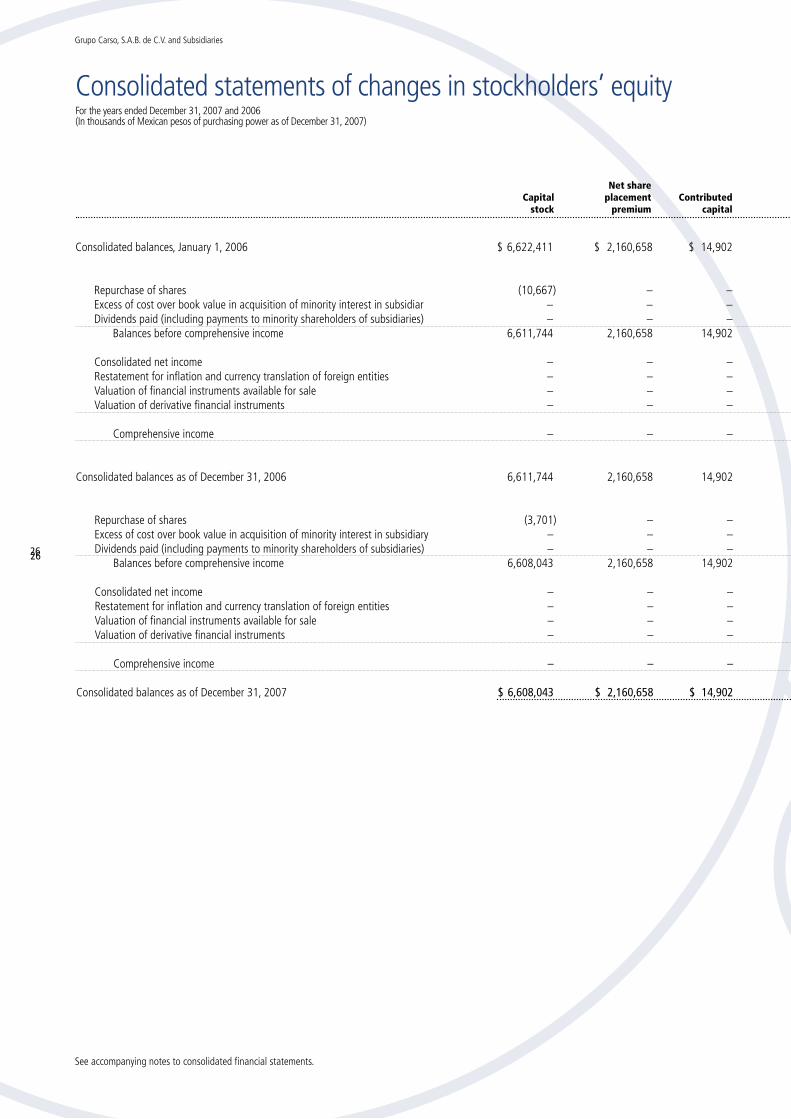

Consolidated statements of changes in stockholders’ equityFor the years ended December 31, 2007 and 2006(In thousands of Mexican pesos of purchasing power as of December 31, 2007)

Consolidated balances, January 1, 2006 $ 6,622,411 $ 2,160,658 $ 14,902 $ 73,918,631 $ (34,355,412) $ (8,364,341) $ 321,592 $ 40,318,441 $ 9,693,670 $ 50,012,111

Repurchase of shares (10,667) – – (690,979) – – – (701,646) – (701,646) Excess of cost over book value in acquisition of minority interest in subsidiar – – – (1,640,992) – – – (1,640,992) (2,813,295) (4,454,287) Dividends paid (including payments to minority shareholders of subsidiaries) – – – (5,603,143) – – – (5,603,143) (391,937) (5,995,080) Balances before comprehensive income 6,611,744 2,160,658 14,902 65,983,517 (34,355,412) (8,364,341) 321,592 32,372,660 6,488,438 38,861,098

Consolidated net income – – – 8,029,372 – – – 8,029,372 1,764,456 9,793,828 Restatement for inflation and currency translation of foreign entities – – – – 213,825 – – 213,825 (93,412) 120,413 Valuation of financial instruments available for sale – – – – – – (25,182) (25,182) – (25,182) Valuation of derivative financial instruments – – – – – – (359,167) (359,167) (7,209) (366,376)

Comprehensive income – – – 8,029,372 213,825 – (384,349) 7,858,848 1,663,835 9,522,683

Consolidated balances as of December 31, 2006 6,611,744 2,160,658 14,902 74,012,889 (34,141,587) (8,364,341) (62,757) 40,231,508 8,152,273 48,383,781

Repurchase of shares (3,701) – – (391,499) – – – (395,200) – (395,200) Excess of cost over book value in acquisition of minority interest in subsidiary – – – (81,625) – – – (81,625) (465,056) (546,681) Dividends paid (including payments to minority shareholders of subsidiaries) – – – (1,200,845) – – – (1,200,845) (861,867) (2,062,712) Balances before comprehensive income 6,608,043 2,160,658 14,902 72,338,920 (34,141,587) (8,364,341) (62,757) 38,553,838 6,825,350 45,379,188

Consolidated net income – – – 19,459,643 – – – 19,459,643 1,351,766 20,811,409 Restatement for inflation and currency translation of foreign entities – – – – (808,133) – – (808,133) (161,145) (969,278) Valuation of financial instruments available for sale – – – – – – (14,335) (14,335) – (14,335) Valuation of derivative financial instruments – – – – – – 17,230 17,230 1,337 18,567

Comprehensive income – – – 19,459,643 (808,133) – 2,895 18,654,405 1,191,958 19,846,363

Consolidated balances as of December 31, 2007 $ 6,608,043 $ 2,160,658 $ 14,902 $ 91,798,563 $ (34,949,720) $ (8,364,341) $ (59,862) $ 57,208,243 $ 8,017,308 $ 65,225,551

Derivative Initial financial Insufficiency in cumulative instruments Minority Net share restated effect of and unrealized Majority interest Total Capital placement Contributed Retained stockholders’ deferred result on stockholders’ in consolidated stockholders’ stock premium capital earnings equity income taxes investments equity subsidiaries equity

See accompanying notes to consolidated financial statements.

Grupo Carso, S.A.B. de C.V. and Subsidiaries

2727

Consolidated balances, January 1, 2006 $ 6,622,411 $ 2,160,658 $ 14,902 $ 73,918,631 $ (34,355,412) $ (8,364,341) $ 321,592 $ 40,318,441 $ 9,693,670 $ 50,012,111

Repurchase of shares (10,667) – – (690,979) – – – (701,646) – (701,646) Excess of cost over book value in acquisition of minority interest in subsidiar – – – (1,640,992) – – – (1,640,992) (2,813,295) (4,454,287) Dividends paid (including payments to minority shareholders of subsidiaries) – – – (5,603,143) – – – (5,603,143) (391,937) (5,995,080) Balances before comprehensive income 6,611,744 2,160,658 14,902 65,983,517 (34,355,412) (8,364,341) 321,592 32,372,660 6,488,438 38,861,098

Consolidated net income – – – 8,029,372 – – – 8,029,372 1,764,456 9,793,828 Restatement for inflation and currency translation of foreign entities – – – – 213,825 – – 213,825 (93,412) 120,413 Valuation of financial instruments available for sale – – – – – – (25,182) (25,182) – (25,182) Valuation of derivative financial instruments – – – – – – (359,167) (359,167) (7,209) (366,376)

Comprehensive income – – – 8,029,372 213,825 – (384,349) 7,858,848 1,663,835 9,522,683

Consolidated balances as of December 31, 2006 6,611,744 2,160,658 14,902 74,012,889 (34,141,587) (8,364,341) (62,757) 40,231,508 8,152,273 48,383,781

Repurchase of shares (3,701) – – (391,499) – – – (395,200) – (395,200) Excess of cost over book value in acquisition of minority interest in subsidiary – – – (81,625) – – – (81,625) (465,056) (546,681) Dividends paid (including payments to minority shareholders of subsidiaries) – – – (1,200,845) – – – (1,200,845) (861,867) (2,062,712) Balances before comprehensive income 6,608,043 2,160,658 14,902 72,338,920 (34,141,587) (8,364,341) (62,757) 38,553,838 6,825,350 45,379,188

Consolidated net income – – – 19,459,643 – – – 19,459,643 1,351,766 20,811,409 Restatement for inflation and currency translation of foreign entities – – – – (808,133) – – (808,133) (161,145) (969,278) Valuation of financial instruments available for sale – – – – – – (14,335) (14,335) – (14,335) Valuation of derivative financial instruments – – – – – – 17,230 17,230 1,337 18,567

Comprehensive income – – – 19,459,643 (808,133) – 2,895 18,654,405 1,191,958 19,846,363

Consolidated balances as of December 31, 2007 $ 6,608,043 $ 2,160,658 $ 14,902 $ 91,798,563 $ (34,949,720) $ (8,364,341) $ (59,862) $ 57,208,243 $ 8,017,308 $ 65,225,551

Derivative Initial financial Insufficiency in cumulative instruments Minority Net share restated effect of and unrealized Majority interest Total Capital placement Contributed Retained stockholders’ deferred result on stockholders’ in consolidated stockholders’ stock premium capital earnings equity income taxes investments equity subsidiaries equity

Grupo Carso, S.A.B. de C.V. and Subsidiaries

28

2007 2006

Operating activities: Consolidated net income $ 20,811,409 $ 9,793,828 Income from discontinued operations – (1,929,332) 20,811,409 7,864,496

Add (deduct) items that did not require (generate) resources: Depreciation and amortization 2,123,778 2,030,682 Impairment of long-lived assets 28,532 260,206 Deferred income taxes and statutory employee profit sharing 401,619 (650,253) Gain from sale of shares of subsidiaries (15,017,142) (81,971) Equity in income of associated companies and others (net of dividends received) 343,092 77,355 Other – net 101,227 3,141 8,792,515 9,503,656 Changes in operating assets and liabilities: (Increase) decrease in: Financial instruments held for trading purposes 13,824 175,027 Notes and accounts receivable (1,596,595) (1,684,603) Inventories (1,154,073) (2,310,521) Prepaid expenses (70,531) 48,266 Other assets (45,885) 23,996 Net asset projected for labor obligations (99,414) (57,831) Increase (decrease) in: Trade accounts payable 1,902,416 (573,829) Accrued expenses and taxes other than income taxes (281,586) 468,078 Derivative financial instruments – net (463,459) (83,001) Due to related parties 1,021,074 (296,376) Other liabilities 1,300,271 1,091,357 Net resources generated by operating activities 9,318,557 6,304,219

Financing activities: Borrowings from financial institutions (6,368,871) 642,148 Long-term debt (167,204) 3,911,296 Repurchase of shares (395,200) (701,646) Dividends paid (including payments to minority shareholders of subsidiaries) (2,062,712) (5,995,080)

Net resources used in financing activities (8,993,987) (2,143,282)

Investing activities: Financial instruments available-for-sale and held-to-maturity 136,268 28,428 Sale (investment) in shares of associated companies and others 18,503,157 (3,810,199) Acquisition of property, machinery and equipment – Net (4,172,735) (2,571,868) Other assets (345,717) (99,464) Effects of discontinued subsidiaries, net – 2,340,292

Net resources generated by (used in) investing activities 14,120,973 (4,112,812)

Cash and cash equivalents: Net increase 14,445,543 48,126 From acquired or sold subsidiaries 60,901 – Balance at beginning of year 6,763,222 6,715,096

Balance at end of year $ 21,269,666 $ 6,763,222

Consolidated statements of changes in financial positionFor the years ended December 31, 2007 and 2006(In thousands of Mexican pesos of purchasing power of December 31, 2007)

See accompanying notes to consolidated financial statements.

Grupo Carso, S.A.B. de C.V. and Subsidiaries

29

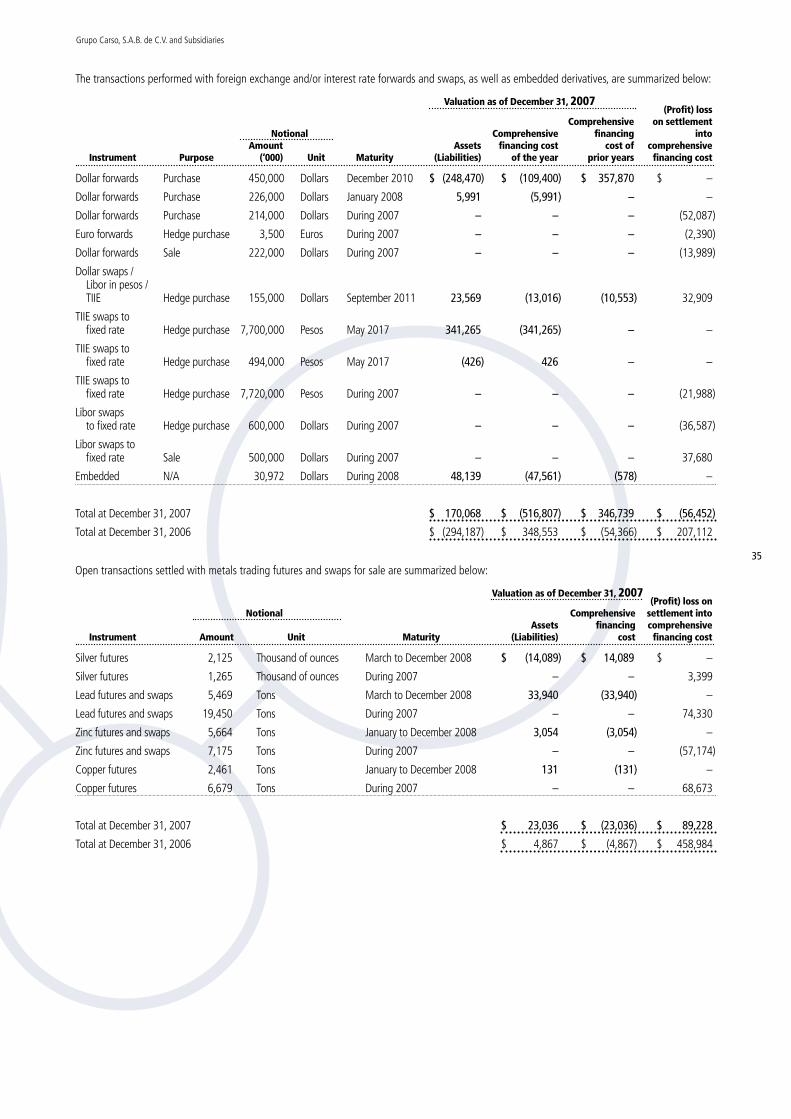

Notes to consolidated financial statementsFor the years ended December 31, 2007 and 2006(In thousands of Mexican pesos of purchasing power of December 31, 2007)

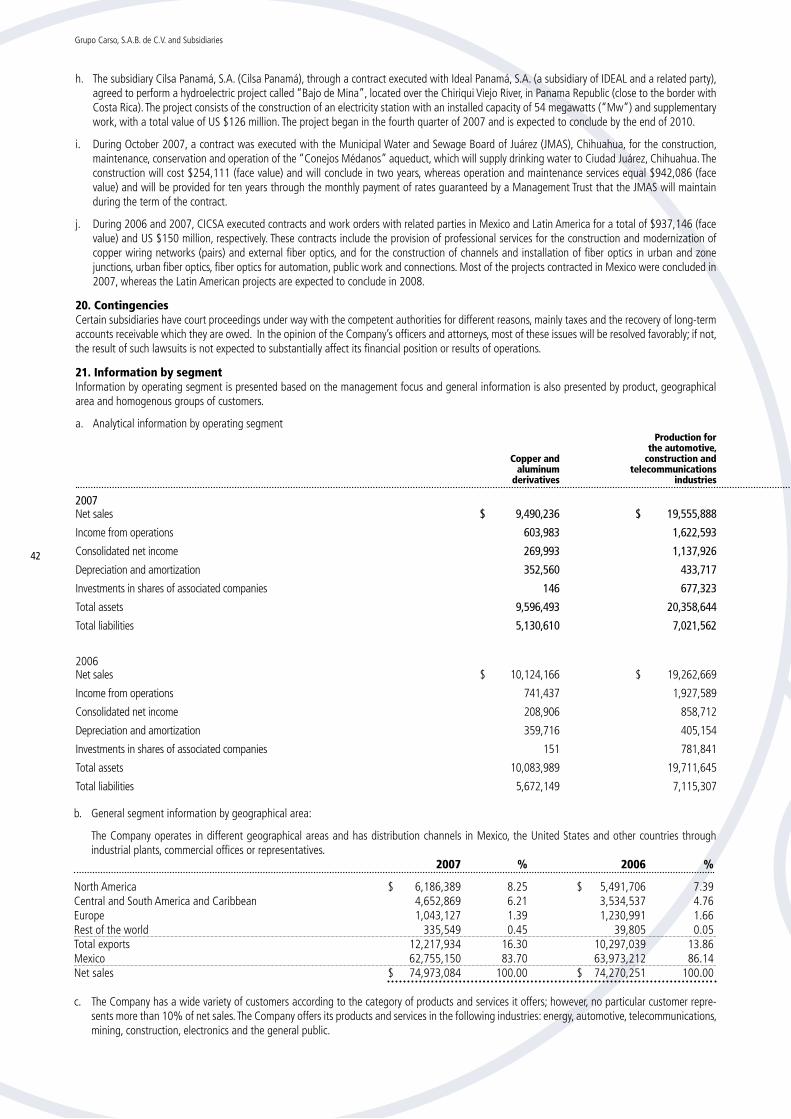

1. Activities and significant eventsa. ActivitiesThe consolidated financial statements include the financial statements of Grupo Carso, S.A.B. de C.V. and Subsidiaries (“the Company” or “Grupo Carso”) as though a single entity.

The principal subsidiaries and associated companies and their activities are as follows:

Ownership percentageSubsidiaries 2007 2006 Activity

Carso Infraestructura y Construcción, 65.28 71.07 Performance of several branches of engineering, including: drilling oil wells and S.A.B. de C.V. and Subsidiaries the projection and construction of oil rigs and all types of civil, industrial and (“CICSA”) electromechanical projects and facilities; construction and maintenance of highways, water pipes, water treatment plants and hydroelectric stations; manufacturing and selling of cold-formed carbon steel tubes; and installation of telecommunication and telephone networks. (1)

Grupo Calinda, S.A. de C.V. 100 100 Hotel related services. and Subsidiaries (“Calinda”)

Grupo Condumex, S.A. de C.V. 99.57 99.57 Manufacture and sale of products used by the construction, automotive, energy and Subsidiaries (“Condumex”) and communications industries; manufacture and sale of copper and aluminum derivative products and their alloys and pipes manufactured with vinyl polychlorine; mining metallurgical industry.

Grupo Sanborns, S.A. de C.V. 99.97 99.93 Operation of department stores, gift shops, record stores, restaurants, cafeterias and Subsidiaries (“Sanborns”) and management of shopping malls through thefollowing commercial brands, principally: Sanborns, Sears, Sacks Fifth Avenue, Mix-up, and Dorian’s. (4)

Inmuebles Cantabria, S.A. de C.V. 100 100 Holding company of shares of companies in the real estate leasing, hospitality, and Subsidiaries (“Cantabria”) manufacture of flexible packing materials sectors, as well as lithography, bookbinding and printing (up to February 2006). (5)

Porcelanite Holding, S.A. de C.V. – 99.96 Manufacture and sale of all kinds of coverings for floors, walls and other similar and Subsidiaries (“Porcelanite”) applications. (3)

Associated 2007 2006 Activity

Infraestructura y Transportes 16.75 16.75 Railroad transportation. México, S.A. de C.V. (“ITM”)

Philip Morris de México, S.A. de C.V. 20.00 49.99 Sale of tobacco products (up to November 2007); manufacture and sale of (“Philip Morris”) cigarettes (on November 1, 2007). (2)

b. Significant events(1) As of November 1, 2007, CICSA merged Casas Urvitec, S.A. de C.V., which disappeared in its capacity as the merged company; through this

transaction, CICSA began operating in the Mexican housing development market, and Casas Urvitec, S.A. de C.V. is subject to fair value deter-mination.

(2) On November 1, 2007, the Company transferred 30% of its equity in the tobacco business to Philip Morris International Inc. (“PMI”). Conse-quently, as of that date, the Company’s equity in that segment, through its associate Philip Morris, is 20%. The value of this transaction was approximately US $1,100 million.

Prior to November 1, 2007, the subsidiary Cigarros la Tabacalera Mexicana, S. A. de C.V. (50.01% owned by Grupo Carso) manufactured ciga-rettes, which were distributed by its associate Philip Morris (previously 49.99% owned by Grupo Carso). The latter and its subsidiaries currently perform both activities. Due to its significance to these consolidated financial statements, the tobacco business is presented as a discontinued operation (see Note 18).

(3) On November 30, 2007, the Company sold its equity in Porcelanite to Grupo Lamosa, S.A.B. de C.V. The value of this transaction was approxi-mately US $710 million. Due to its significance to these consolidated financial statements, this figure is presented as a discontinued operation (see Note 18).

(4) In August 2006, Grupo Carso carried out a public offering to acquire the totality of the shares of Sanborns listed on the Mexican Stock Exchange (“BMV”). As of December 31, 2007 and 2006, the excess of cost over book value in the purchase of such shares was $3,725 and $1,640,992, respectively, which amount is recorded in retained earnings as a capital distribution.

(5) In February 2006, Inmuebles y Servicios Mexicanos, S.A. de C.V. (a subsidiary of Cantabria), sold 100% of the shares in its subsidiary Artes Gráfi-cas Unidas, S.A. de C.V. for the amount of $529,193 ($493,771 nominal pesos), generating a gain of $81,971 ($76,485 nominal pesos), which is recorded within other revenues, net in the consolidated statement of income. Given its immateriality within the context of these consolidated financial statements, it is not presented as a discontinued operation.

Grupo Carso, S.A.B. de C.V. and Subsidiaries

30

2. Basis of presentationa. Explanation for translation into English - The accompanying consolidated financial statements have been translated from Spanish into

English for use outside of Mexico. These consolidated financial statements are presented on the basis of Mexican Financial Reporting Standards (“MFRS”). Certain accounting practices applied by the Company that conform with MFRS may not conform with accounting principles generally accepted in the country of use.

b. Consolidation of financial statements - The consolidated financial statements include the financial statements of the holding company and its subsidiaries as though a single entity. Significant intercompany balances and transactions have therefore been eliminated from these consolidated financial statements.

c. Translation of financial statements of foreign subsidiaries - To consolidate the financial statements of foreign subsidiaries that operate independently of the Company in terms of finances and operations, the same accounting policies of the Company are applied. The financial state-ments are restated for inflation of the country in which such foreign subsidiary operates to express amounts in purchasing power of the foreign currency as of the most recent year-end. All assets, liabilities, revenues, costs and expenses are translated into Mexican pesos using the closing exchange rate in effect at the most recent balance sheet date presented. Translation effects are presented in stockholders’ equity.

To consolidate the financial statements of foreign subsidiaries that do not operate independently of the Company in terms of finances and opera-tions, monetary assets and liabilities are translated by using the exchange rate in effect at the year end, and nonmonetary assets and liabilities and stockholders’ equity are translated by using at the historical exchange rate on the transaction date. Revenues, costs and expenses are translated by using the weighted average exchange rate for the year. The resulting amounts are restated to Mexican pesos of purchasing power as of the end of the latest year presented using the Mexican National Consumer Price Index (“NCPI”). The translation effects are recorded in results for the year under net comprehensive financing cost.

d. Comprehensive income - Represents changes in stockholders’ equity during the year, for concepts other than distributions and activity in con-tributed common stock, and is comprised of the net income (loss) of the year, plus other comprehensive income (loss) items of the same period, which are presented directly in stockholders’ equity without affecting the consolidated statements of income. In 2007 and 2006, other comprehen-sive income (loss) items consist of the excess (insufficiency) in restated stockholders’ equity, the translation effects of foreign entities, unrealized gain and losses on available-for-sale securities and the valuation of derivative financial instruments.

e. Reclassifications - Certain amounts in the consolidated financial statements as of and for the year ended December 31, 2006 have been reclas-sified basically for the discontinued operations, in order to conform to the presentation of the consolidated financial statements as of and for the year ended December 31, 2007.

3. Summary of significant accounting policiesThe accompanying consolidated financial statements have been prepared in conformity with MFRS, individually referred to as Normas de Información Financiera (“NIFs”) issued by the Consejo Mexicano para la Investigación y Desarrollo de Normas de Información Financiera, A. C. (“CINIF”). MFRS require that management make certain estimates and use assumptions to obtain certain figures. The Company’s management, upon applying its profes-sional judgment, considers that the estimates made and assumptions used were adequate under the circumstances.

The significant accounting policies applied to obtain the figures included in the consolidated financial statements are as follows:

a. Accounting changes due to issuance of NIFs - Beginning January 1, 2007, the following NIFs became effective and were adopted by the Company, with the following effects:

1. NIF B-3, Statement of income – Establishes the general standards for presentation and structure of that financial statement, the minimum content requirements and the general disclosure standards. It provides a new classification for revenues, costs and expenses into ordinary and non-ordinary. Ordinary items, even if they are infrequent, are derived from primary activities representing an entity’s main source of revenues. Non-ordinary items are derived from activities other than those representing an entity’s main source of revenues. Consequently, the classification of certain transactions as “special” or “extraordinary” was eliminated. The main effect of the adoption of this NIF was the reclassification of employee statutory profit sharing incurred and deferred from 2006 of $382,597 to other (income) expenses.

2. NIF B-13, Events subsequent to the date of the financial statements – This resulted in a change by establishing that events occurring after the date of the financial statements and their issuance date should not be included in the reported figures and should only be disclosed in the notes and recognized in the period in which they occurred. Figures should only be adjusted when subsequent events show that certain conditions already existed at yearend. The adoption of this new treatment did not result in any changes to the financial statements.

3. NIF C-13, Related parties – Broadens the concept of “related parties” to include, a) the overall business in which the reporting entity par-ticipates; b) close family members of key management or prominent executives; and c) any fund created in connection with a labor-related compensation plan. It also requires the following disclosures: 1) that the terms and conditions of payments made or received in transactions carried out between related parties reflect those of similar transactions performed between independent parties and the reporting entity, only if sufficient evidence exists; 2) benefits granted to the entity’s key management or prominent executives. Notes to the 2006 consolidated financial statements were amended to comply with these new provisions.

4. NIF D-6, Capitalization of comprehensive financing result – Requires capitalization of the comprehensive financing result attributable to qualify-ing assets, provided the investment in those assets is fully identifiable with the financing that gives rise to the financial burden. This was previ-ously an optional practice; its implementation therefore results in a change to the previous policy. The adoption of this new treatment did not lead to significant changes to 2007 financial information.

b. Recognition of the effects of inflation - The Company restates its consolidated financial statements in currency of constant purchasing power by applying inflation factors of the country of origin and the exchange rate in effect at the date of the most recent consolidated balance sheet presented. Accordingly, the consolidated financial statements of the prior year, which are presented have also been restated to Mexican pesos

Grupo Carso, S.A.B. de C.V. and Subsidiaries

31

of the same purchasing power and, therefore, differ from those originally reported in the prior year. Recognition of the effects of inflation results mainly in inflationary gains or losses on nonmonetary and monetary items that are presented in the financial statements under the following two line items:

• Insufficiencyinrestatedstockholders’equity- Primarily consists of the monetary position result accumulated through the initial first restatement, the variations derived from restating the value of inventories, property, machinery and equipment, and investments in shares of associated companies and others, less the respective deferred income tax effect.

• Monetarypositionresult- Monetary position result, which represents the erosion of purchasing power of monetary items caused by infla-tion, is calculated by applying NCPI factors to monthly net monetary position. (Gains) losses result from maintaining a net monetary (liability) asset position.

c. Cash and cash equivalents - This line item consists mainly of bank deposits in checking accounts and readily available daily investments of cash surpluses. This line item is stated at nominal value plus accrued yields, which are recognized in results as they accrue.

d. Financial instruments - According to its intent, from the date of acquisition, the Company classifies investments in financial instruments in one of the following categories: (1) trading, when the Company intends to trade debt and equity instruments in the short-term, before their maturity, if any. These investments are stated at fair value; any fluctuations in the value of these investments recognized within current earnings; (2) held-to-maturity, when the Company intends to and is financially capable of holding financial instruments until their maturity. These investments are recognized and maintained at amortized cost; and (3) available-for-sale investments, which include those that are classified neither as trading nor held-to-maturity. These investments are stated at fair value; any unrealized gains and losses resulting from valuation, net of income tax, are recorded as a component of other comprehensive income within stockholders’ equity and reclassified to current earnings upon their sale or maturity, if any. Fair value is determined using recognized market prices, and when the instruments are not listed on a recognized market, it is determined using technical valuation models recognized in the financial community.

Financial investments classified as held-to-maturity and available-for-sale are subject to impairment tests. If there is evidence that the reduction in fair value is other than temporary, the impairment is recognized in current earnings.

Financial liabilities derived from the issuance of debt instruments are recorded at the value of the obligations they represent. Any expenses, premi-ums and discounts related to the issuance of debt financial instruments are amortized over the life of the instruments.

e. Derivative financial instruments - Derivative financial instruments are acquired for trading or hedging purposes involving: a) interest rates, b) exchange rates applicable to long-term debt, c) metal prices, and d) natural gas prices, and are recognized as assets and liabilities at their fair value.

Valuation of financial instruments acquired for trading purposes is recognized in the statement of income under the comprehensive financing cost of the respective period, while financial instruments acquired for hedging purposes are immediately recognized at their fair value in earnings, net of costs, expenses or revenues resulting from the hedged assets or liabilities. For cash flow hedges, changes in fair value are immediately recognized in stockholder’s equity as a component of comprehensive income and then reclassified to current earnings during the period in which the asset, liability or forecast transaction (primary hedged position) affects the results of the period.

While certain derivative financial instruments are contracted for hedging from an economic point of view, they are not designated as a hedge for accounting purposes. Changes in fair value are recognized in current earnings as a component of comprehensive financing cost.

The Company has executed certain contracts whose effects have not yet been recognized and which given their nature, include an embedded derivative. Embedded derivatives are valued at fair value, and the effect is recorded in the statement of income.

f. Inventories and cost of sales - Inventories are stated at the lower of replacement cost or net realizable value. Cost of sales is restated using replacement cost at the time of sale.

g. Property,machineryandequipment- Are initially recorded at acquisition cost and restated using the NCPI. For fixed assets of foreign origin, restated acquisition cost expressed in the currency of the country of origin is converted into Mexican pesos at the market exchange rate in effect at the balance sheet date. Depreciation is calculated by the straight-line method based on the remaining useful lives of the related assets, considering a percentage of the estimated salvage value.

As of 2007, comprehensive financing result related to financial liabilities during the construction or installation of fixed assets, when an extended period is required for such purpose, is capitalized as part of the asset value when the amount is significant and provided the investment in these assets can be fully identified with the liabilities giving rise to the financial burden.

h. Impairment of long-lived assets in use - The Company reviews the carrying amounts of long-lived assets in use when an impairment indicator suggests that such amounts might not be recoverable, considering the greater of the present value of future net cash flows or the net selling price upon disposal. Impairment is recorded when the carrying amounts exceed the greater of the amounts mentioned above. The impairment indicators considered for these purposes are, among others, the operating losses or negative cash flows in the period if they are combined with a history or projection of losses, depreciation and amortization charged to results, which in percentage terms in relation to revenues are substantially higher than that of previous years, obsolescence, reduction in the demand for the products manufactured, competition and other legal and economic fac-tors. At December 31, 2007 and 2006, the impairment effect was $28,532 and $260,206 ($40,240 related to investment in shares and $219,966 to property, plant and equipment) respectively, and is presented under other (income) expenses, net in the statement of income.

i. Investment in shares of associated companies and others - This line item includes the investment in shares of associated companies and others. These investments are valued using the equity method.

j. Other assets - Intangible assets are recognized in the balance sheet provided that they can be identified, provide future economic benefits and control exists over such assets. Intangible assets with an indefinite useful life are not amortized, and intangible assets with a defined useful life are amortized systematically based on the best estimate of their useful life, determined in accordance with the expected future economic benefits. The carrying value of these assets is subject to annual impairment testing.

Grupo Carso, S.A.B. de C.V. and Subsidiaries

32

The intangible assets recognized by the Company are as follows:

1. Costs of development (or in the development phase of a project) are recognized as an intangible asset when they fulfill the characteristics established to be considered as such. As of December 31, 2007 and 2006, there are no material assets derived from this item.

2. Patents and brand names represent payments made for the respective use rights. As of December 31, 2007 and 2006, there are no material assets derived from this item.

3. The development expenses incurred in mining lots for exploitation, whose amortization is included in cost of sales.

Environmental control plans and projects are presented under the heading of other assets. The expenses incurred for this item are applied to the provision for remediation, and the subsequent increase in such provision is charged to results if it refers to present obligations, or to other assets if it refers to future obligations, in the year in which determined.

k. Provisions- Provisions are recognized for current obligations that result from a past event, that are probable to result in the future use of economic resources, and that can be reasonably estimated.

l. Provision for environmental remediation - The Company has adopted environmental protection policies within the framework of applicable laws and regulations. However, due to their activities, the Group’s industrial subsidiaries, and more specifically its mining subsidiaries, sometimes perform activities that adversely affect the environment. Consequently, the Company implements remediation plans (which are generally approved by the competent authorities) that involve estimating the expenses incurred for this purpose.

Based on accounting standards, a provision is created for this item, which consists of applying a charge to results when environmental impairment has already occurred, and recording a deferred asset subject to amortization (site restoration) when future impairment is foreseen (see note 9).

The estimated expenses to be incurred could be modified due to changes in the physical condition of the affected work zone, the activity performed, laws and regulations, variations affecting the prices of materials and services (especially for work to be performed in the near future), as well as the modification of criteria used to determine work to be performed in the affected area, etc.

m. Employeeretirementobligations-Liabilities from seniority premiums, pension plans for non-union employees and severance payments are recognized as costs over employee years of service and are calculated by independent actuaries using the projected unit credit method at net dis-count rates. Accordingly, the liability is being accrued which, at present value, will cover the benefit obligation projected to the estimated retirement date of the Company’s employees. As of December 31, 2007, certain subsidiary companies have created investment funds, but others have not; consequently, they are recorded through a reserve for labor obligations.

n. Statutoryemployeeprofitsharing(“PTU”)-Is recorded in the results of the year in which it is incurred and presented under other income and expenses in the accompanying consolidated statements of income. Deferred PTU is derived from temporary differences between the account-ing result and income for PTU purposes and is recognized only when it can be reasonably assumed that such difference will generate a liability or benefit, and there is no indication that circumstances will change in such a way that the liabilities will not be paid or benefits will not be realized.

o. Income taxes - Income taxes are recorded in results of the year in which they are incurred. Beginning October 2007, based on its financial projections, the Company must determine whether it will incur regular income tax (“ISR”) or the new Business Flat Tax (“IETU”) and, accordingly, recognize deferred taxes based on the tax it will pay. Deferred taxes are calculated by applying the corresponding tax rate to the applicable tempo-rary differences resulting from comparing the accounting and tax bases of assets and liabilities and including, if any, future benefits from tax loss carryforwards and certain tax credits. Deferred tax assets are recorded only when there is high probability of recovery.

Tax on assets (“IMPAC”) paid recognizes as a fiscal credit (and therefore as an account receivable) only in those cases in which the probability exists of recovering it against the tax to the utility of future periods.

p. Foreigncurrencybalancesandtransactions-Foreign currency transactions are recorded at the applicable exchange rate in effect at the transaction date. Monetary assets and liabilities denominated in foreign currency are translated into Mexican pesos at the applicable exchange rate in effect at the balance sheet date. Exchange fluctuations are recorded as a component of net comprehensive financing cost (income) in the consolidated statements of income.

q. Revenue recognition - Revenues are recognized in the period in which the risks and rewards of ownership of the inventories are transferred to customers, when the inventories are delivered or shipped to customers and the customer assumes responsibility for them. Services revenues are recognized in the period in which the services are rendered. Long-term construction contracts are accounted for using the percentage-of-completion method; therefore, revenues are recognized in proportion to the costs incurred. If total costs in the most recent cost estimate exceed total revenues according to the contract, the expected loss is recognized in current earnings.

Revenues related to construction over and above that specified in the original contract are recognized when they can be reliably quantified and there is reasonable evidence of their approval by the customer. Revenues related to claims for delays caused by bad weather are recognized when they can be reliably quantified and when, as a result of negotiations, there is reasonable evidence that the customer will accept the claim.

r. Earnings per share - Basic earnings per common share are calculated by dividing net income of majority stockholders by the weighted average number of shares outstanding during the year.

Grupo Carso, S.A.B. de C.V. and Subsidiaries

33

4. Financial instruments 2007 2006

Trading (1) $ 1,920,950 $ 1,907,126Held-to-maturity – 162,172Available-for-sale – 16,079 $ 1,920,950 $ 2,085,377

(1) The financial instruments held for trading purposes include principally the following:

Investment in guarantee for default on loan - In March 2004, the Company contracted a credit derivative financial instrument (“Credit Linked OTL Deposit Transaction” or “Credit Default Swap” or “CDS”) in which it invested US $50,000 thousand, which may be negotiated at any time with a maximum maturity of March 2009, at a fixed interest rate equal to 2.65% above the LIBOR rate. This derivative allows the counterparty of the CDS to transfer to the Company the risk of noncompliance on a specific loan portfolio issued by related parties. Consequently, on the maturity date of the CDS, the counterparty will pay the Company the initial amount of the investment, less any amount of the portfolio that was in default.

This instrument is not subject to valuation as a derivative financial instrument, because it constitutes a deposit with a credit guarantee. As of December 31, 2007, the Company believes that no adverse effect will be generated in the future.

5. Other accounts receivable 2007 2006