growth and opportunities in the international commercial ... and opportunities in... · growth and...

TRANSCRIPT

Growth and opportunities in the international commercial vehicle industry

Matthias WissmannPresidentGerman Association of the Automotive Industry (VDA)

International Press Workshop“Commercial Vehicles: On the Move for Everyone”18 July 2008, Frankfurt/Main

Commercial Vehicle Markets

I. Global

II. Germany

page 4

page 35

I. Global Commercial Vehicle Markets- Overview- by Region

- USA- Asia- Eastern Europe- Western Europe

page 4

page 9page 13page 24 page 30

4

Navistar JV

Toyota

Hino50.1%

Daihatsu51.1%

HyundaiMotor Company

Kia38.6% Asia Motors

PACCAR

DAFTrucks

LeylandTrucks

KenworthTruck

Ford

Otoyol JV

Nissan Motors44.6%

15%

Cooperation

Naveco(China)

Uralaz(Russia)

GM-Daewoo50.9%

Daimler HyundaiTruck Corp.

Source: Company data, Global Insight, VDA statistics

Volkswagen AG

ScaniaVWN100%

VW Trucksdo Brazil

General MotorsFuji HeavyInd. 8.7%

Isuzu

Opel/ Vauxhall

RenaultTrucks

MackTrucks Volvo BusVolvo Trucks

Renault

Nissan Diesel

Dacia

33.3%

PSA

Peugeot CitroënIveco

50%

Haveco(China)

50%

Otosan(Turkey)

DongfengYueda

Participation

FPT

Fiat

Volvo AB

5%

10%

MAN / ForceJV

MAN

Daimler Truck Group

Freightliner Truck Cooperation

Mercedes-Benz Trucks

Western StarSterling

Hero (India) JVMitsubishi FusoTruck and Bus

85%

Astra(Italy)

22%

34% 13.0%

PeterbiltMotors

30%

30%

Ford Trucks Brazil

100%

Thomas BuildBusses

Volvo Global Trucks

Eichler (India)

5.7%

27%

Fiat Professional

Caterpillar JV with Navistar

‚Blue Diamond‘ 50%

Mahindra & Mahindra JV

50%

50%

Freightliner

Increasing cooperation amongst the most importantcommercial vehicle manufacturers

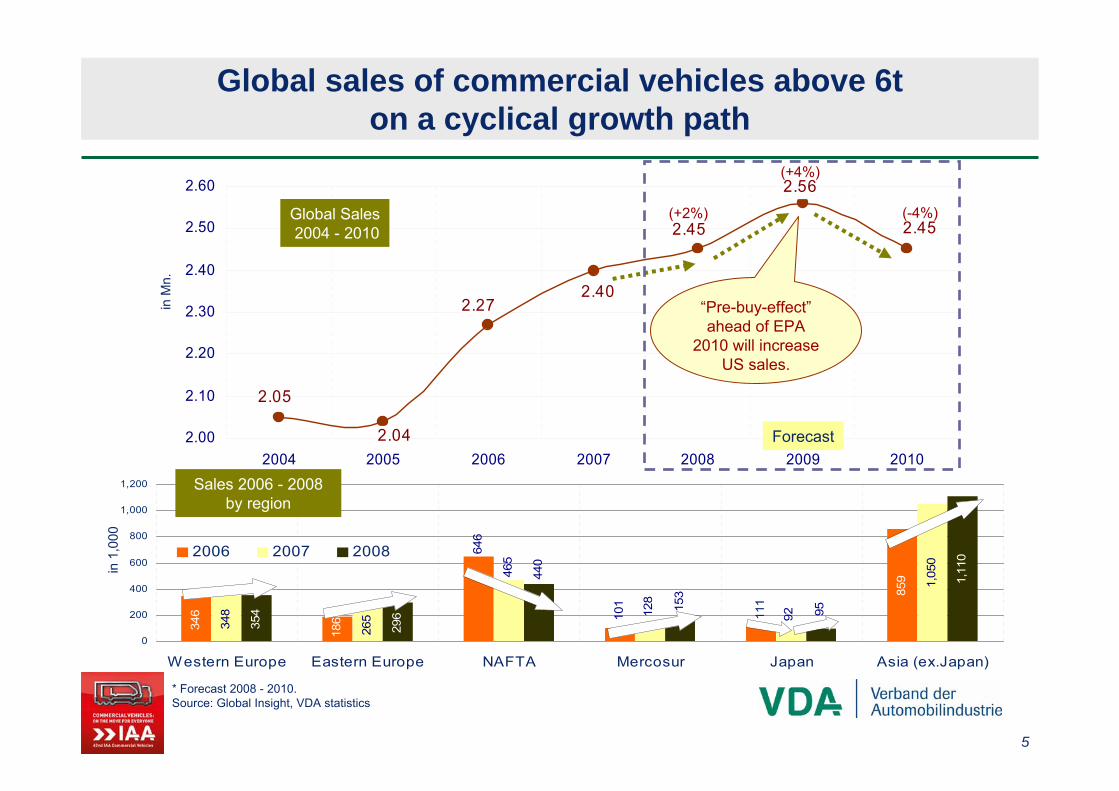

859

348

1,05

0

354

1,11

0

111

18634

6

646

101

128

92

265

465

95

296

440

153

0

200

400

600

800

1,000

1,200

Western Europe Eastern Europe NAFTA Mercosur Japan Asia (ex.Japan)

2006 2007 2008

2.452.45

2.402.27

2.04

2.05

2.56

2.00

2.10

2.20

2.30

2.40

2.50

2.60

2004 2005 2006 2007 2008 2009 2010

Global sales of commercial vehicles above 6t on a cyclical growth path

* Forecast 2008 - 2010.Source: Global Insight, VDA statistics

Sales 2006 - 2008 by region

Global Sales2004 - 2010

(+2%)

(+4%)

(-4%)

“Pre-buy-effect”ahead of EPA

2010 will increase US sales.

in M

n.

in 1

,000

Forecast

5

6

63687075

93101105

155162164166

224350

62

0 100 200 300 400

HinoIsuzu

ScaniaIveco

Ashok Ley.MAN

CNHTCNavistar

FAWDongfeng

TataPaccar

Volvo/RVIDaimler

Major Manufacturers of Medium and Heavy Trucks 2007

Daimler incl. Freightliner, Western Star, Sterling, Mitsubishi Fuso. Volvo incl. Renault/Nissan Diesel and Mack.Source: Company data, VDA statistics

Turnover(in Bn. Euro)

2007 2006Daimler 45.4 40.6Volvo/RVI 21.9 20.3Paccar 11.1 12.3MAN 10.4 8.7Scania 9.1 7.6

Sales in 1,000 unitsDaimler confirms its

position as the worldwide leading

manufacturer of medium and heavy trucks.

7

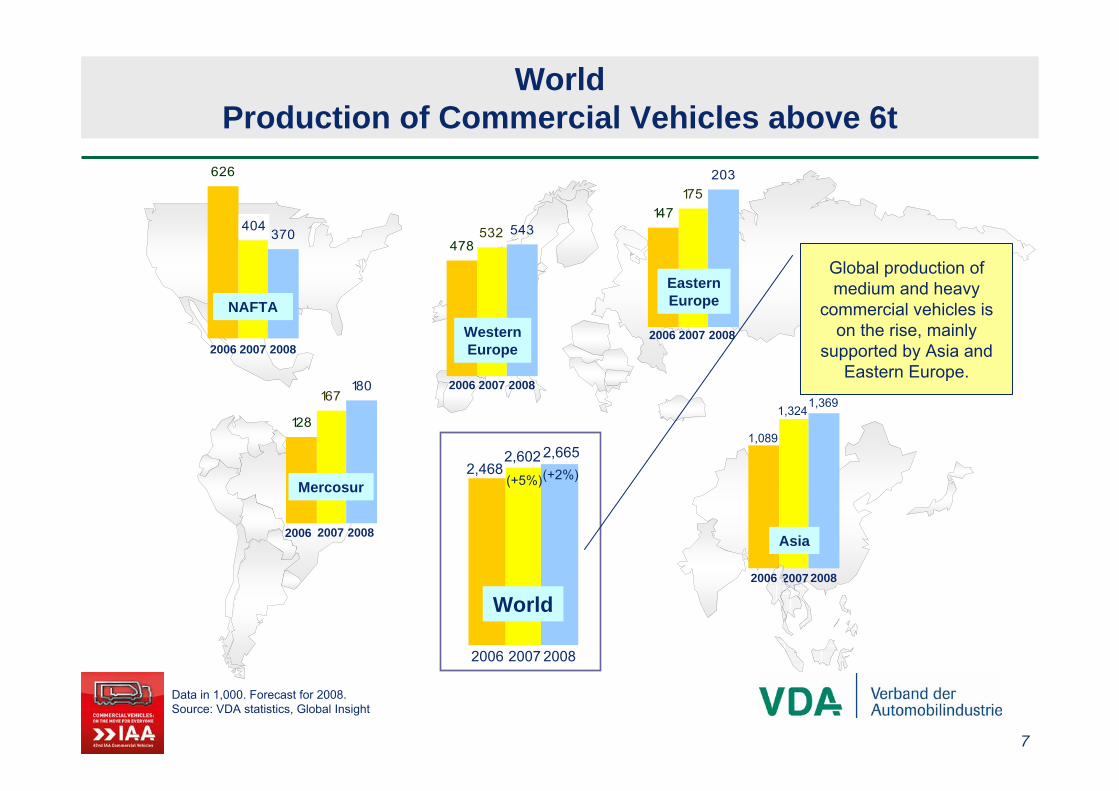

Data in 1,000. Forecast for 2008.Source: VDA statistics, Global Insight

WorldProduction of Commercial Vehicles above 6t

626

370404

NAFTA

2006 2007 2008

128

180167

Mercosur

2006 2007 2008

World

2006 2007 2008

147

203175

EasternEurope

2006 2007 2008

478543532

WesternEurope

2006 2007 2008

Asia

2007

1,089

1,3241,369

2,4682,602 2,665

Global production of medium and heavy

commercial vehicles ison the rise, mainly

supported by Asia and Eastern Europe.

2006 2008

(+5%)(+2%)

8

- Forthcoming increasing freighttransport also in industrial countries.

- Commercial vehicle will keepits No 1 goods carrier position.

- Emerging manufacturers like FAW, Dongfeng (China) or Ashok Leyland and Tata Motors (India) are looking for new

markets beyond their home regions.

- Increasing international cooperationhelps to realize synergy effects and to

challenge emerging markets.

- In many Asian and Eastern European countries growing economy means

growing transport acticity.- Former used vehicle markets like Russia

turn to new vehicle markets.

- Legal pressure for lower emissionsand higher safety will increase.

- Development of new drivetrains and reduction of weight by light construction.

- Improvement of cost structuresand profitability in face of different

international vehicle standards.- Coping with cyclicity of

commercial vehicle business.

Source: Euroforum, KPMG, VDA statistics

Emerging Markets

Transport Needs

International Cooperation

Environment

Costs

Emerging Manufacturers

Opportunities and Challenges for the international Commercial Vehicle Industry

Opp

ortu

nitie

s Challenges

Commercial VehicleIndustry

9

294291311

333346348

354

251279284

299287

258

226

194210

255252249

294

329339

251

213190199 202210

329

235

184

277284264

288312

277249

303

353353

393409

462

322

432

497

545

345

521

221

334

225

328350

424

189

371

150

200

250

300

350

400

450

500

550

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08*

Western Europe USA

* Forecast.Source: Ward‘s, VDA statistics

Rebound of US sales takes longer than expected, slight increase in sales in Western Europe

Trend USA

Trend Western Europe

in 1

,000

Western Europe passesUSA!

Sales of Commercial Vehicles above 6t

Rather flat salescycle in Western

Europe

EPA-Effect

amplifiesUS sales

cycle

8,000

13,000

18,000

23,000

2005 2006 2007 2008

146 142

203

253

284

151 145

0

50

100

150

200

250

300

'02 '03 '04 '05 '06 '07 '08

176 186

228243

261

220200

0

40

80

120

160

200

240

280

'02 '03 '04 '05 '06 '07 '08

Sales of Medium Trucksclasses 4 - 7

Source: Ward‘s, VDA statistics

-47%

in 1,000 in 1,000 Daimler 31.5

Paccar 25.1

Mack 8.8

Volvo 11.1

others 0.1

International 23.4

-4%

Daimler 19.4

International 21.1

Paccar 4.1

Ford 29.0

GM 14.5

others 11.9

Sales of Medium und Heavy Trucks

Medium Trucks

Heavy Trucks

Sales of Medium and Heavy Trucksby manufacturer (Jan. - May 2008)

-10%

Sales of Heavy Trucksclass 8

US truck sales improved recently, but no rebound in 2008

Sales of Medium TrucksJanuary - May 2008:

79,621 (-18%)

Sales of Heavy TrucksJanuary - May 2008:

53,631 (-30%)

US Forecast2008:

345,000 (-7%)

Trend and saisonal adjusted data

10

11

VW29.4

Ford16.3

Iveco7.4

Scania6.0

Volvo7.9

Mercedes31.4

others1.6

VW8.9

Ford17.3

Iveco19.1

Scania5.3

others17.5

Mercedes31.9

13.8

6.1

-5.2-7.0

-9.2 -9.3

14.4

33.531.8

29.1

2.8

9.2

28.2

-15

-10

-5

0

5

10

15

20

25

30

35

40

1.Q.05

1.Q.06

1.Q.07

-05/08

Mercosur: Brazil delivers strong impetusfor increasing sales of medium and heavy trucks

Cha

nge

in %

to p

revi

ous

year

Source: ADEFA, ANFAVEA, VDA statistics

Sales of Medium/Heavy Trucks (January - May 2008 )

Argentina: 12,084 (+21%)Brazil: 50,045 (+35%)

Mercosur: 62,129 (+32%)

Forecast 2008Argentina: 28,000 (+5%)Brazil: 125,000 (+24%)

Mercosur: 153,000 (+20%)

Brazil

Argentina

∑ Germanmanufacturers

60.8%

∑ Germanmanufacturers

40.8%

in %

in %

12

Nissan Diesel12.8

Hino10.9

Isuzu7.8

Tata8.0

Volvo4.8

Mercedes29.3

others26.4

• Sales of medium and heavycommercial vehicles have more

than tripled since 2000.

• Especially mining and construction with high transport

need; further impetus due to FIFA WM 2010.

• Introduction Euro IV in 2010.Source: NAAMSA, VDA statistics

38,500

13,70512,693

11,725

16,327

20,814

27,406

33,080

37,069

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

'00 '01 '02 '03 '04 '05 '06 '07 '08

abo ve 8.5 t3.5 to 8.5 t

To tal

For.

in 1

,000

South AfricaSales of Medium and Heavy Commercial Vehicles

Market Share Heavy CVs(Jan. - May 2008, above 8.5 t)

in %

13

2005 20062007 2008*

R3

R4

R5

0

200

400

600

800

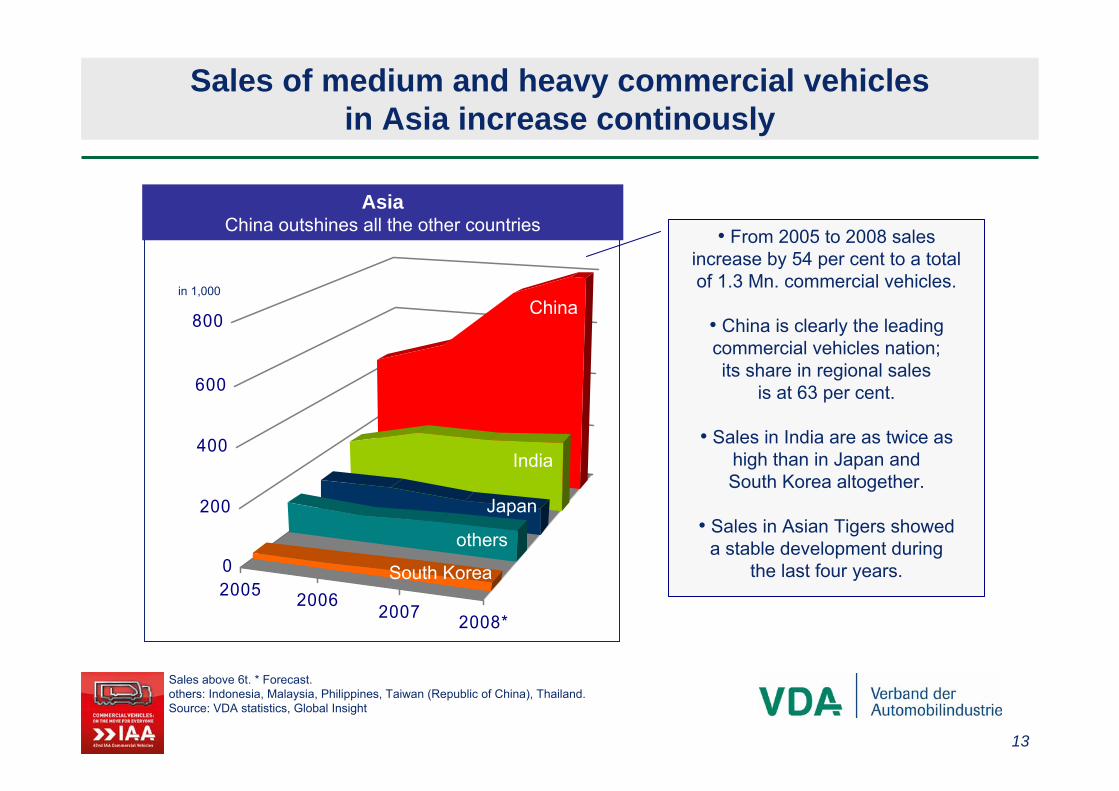

Sales of medium and heavy commercial vehiclesin Asia increase continously

Sales above 6t. * Forecast.others: Indonesia, Malaysia, Philippines, Taiwan (Republic of China), Thailand.Source: VDA statistics, Global Insight

Japan

South Korea

India

Chinain 1,000

others

AsiaChina outshines all the other countries • From 2005 to 2008 sales

increase by 54 per cent to a total of 1.3 Mn. commercial vehicles.

• China is clearly the leadingcommercial vehicles nation; its share in regional sales

is at 63 per cent.

• Sales in India are as twice as high than in Japan and South Korea altogether.

• Sales in Asian Tigers showeda stable development during

the last four years.

14

Source: Global Insight, VDA statistics

85 8377

112106 109 111

9592

0

20

40

60

80

100

120

'00 '01 '02 '03 '04 '05 '06 '07 '08For.

in 1

,000

Sales of Commercial

Vehiclesabove 6t

Japan: Sales of commercial vehiclesabove 6t with slight rebound

Ø 97k

Sales decrease in 2007 after pre-buy due to

new emission standard; in 2008 sales will increase slightly.

-17% +3%

Hino30.9%

Isuzu28.7%

others1.8%Nissan

Diesel15.4%

Mitsubishi Fuso

23.2%

Market share CV sales above 6t

15

Truck sales above 6 t.Source: VDA statistics, J.D. Power

BRICs: Commercial vehicle marketswith strong potential

ChinaSales 2008: 820k (+13%)

- 67% heavy trucks- Local production

meets demand- Population: 1.3 Mn.

IndiaSales 2008: 250k (+6%)

- 50% heavy trucks- Local production

meets demand- Population: 1.2 Mn.

BrazilSales 2008: 125k (+24%)

- 62% heavy trucks- net exporter

- Population: 192 Mn.

152174

236250 724

820

101

125

2007 2008

2007 2008

2007 20082007 2008

+24%

+14%

+6%+13%

RussiaSales 2008: 174k (+14%)

- 70% heavy trucks- net importer

- Population: 141 Mn.

16

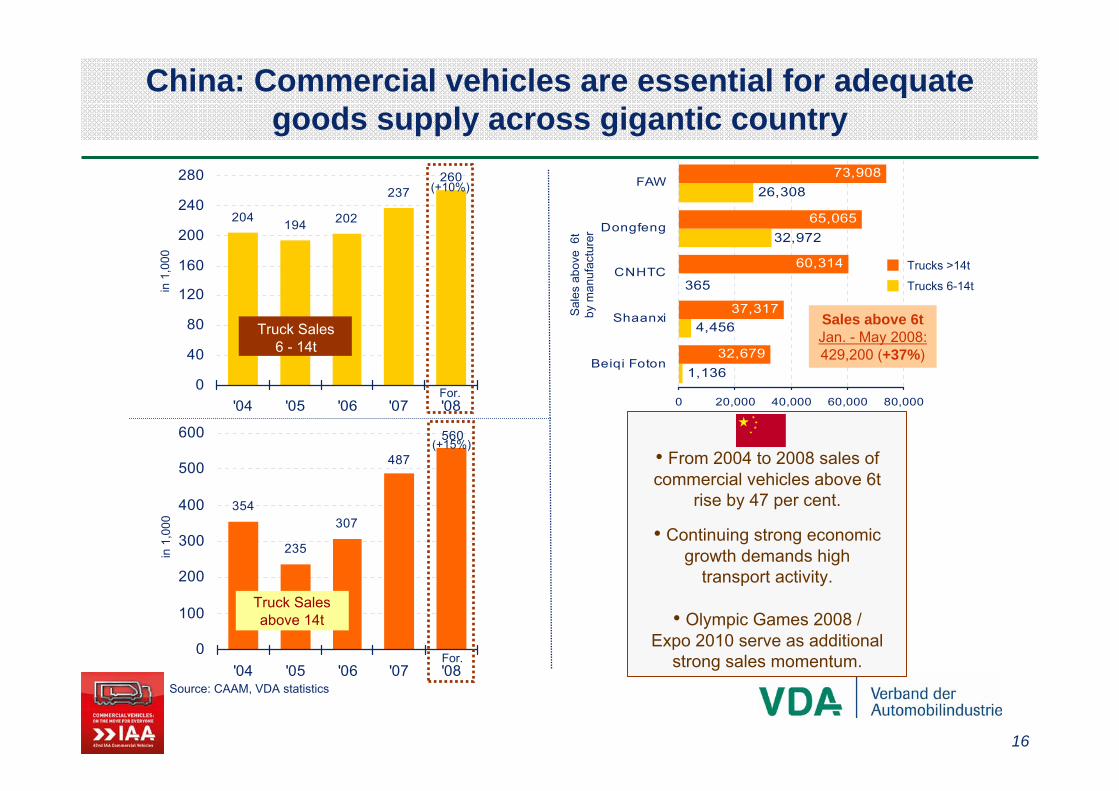

4,456

26,308

37,317

60,314

65,065

73,908

32,972

365

1,13632,679

0 20,000 40,000 60,000 80,000

Beiqi Foton

Shaanxi

CNHTC

Dongfeng

FAW

204 194 202

237260

0

40

80

120

160

200

240

280

'04 '05 '06 '07 '08

Truck Sales6 - 14t

354

235

307

487

560

0

100

200

300

400

500

600

'04 '05 '06 '07 '08

China: Commercial vehicles are essential for adequategoods supply across gigantic country

Truck Sales above 14t

Source: CAAM, VDA statistics

in 1

,000

in 1

,000

For.

For.

Trucks >14t

Trucks 6-14t

Sale

s ab

ove

6tby

man

ufac

ture

r

(+10%)

(+15%)

Sales above 6tJan. - May 2008:429,200 (+37%)

• From 2004 to 2008 sales of commercial vehicles above 6t

rise by 47 per cent.

• Continuing strong economicgrowth demands high

transport activity.

• Olympic Games 2008 / Expo 2010 serve as additional

strong sales momentum.

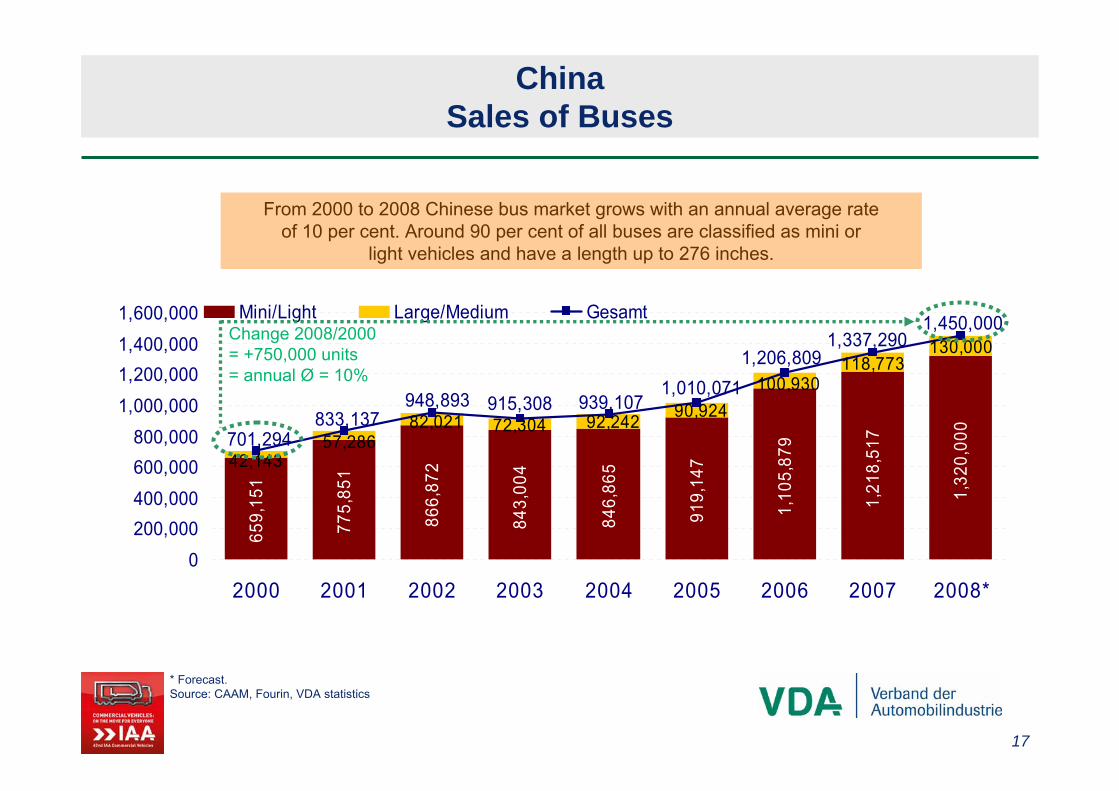

17

659,

151

775,

851

866,

872

843,

004

846,

865

919,

147

1,10

5,87

9

1,21

8,51

7

1,32

0,00

0

130,000118,773

100,93090,924

42,14357,286

82,021 72,304 92,242

1,010,071939,107915,308948,893

833,137701,294

1,206,8091,337,290

1,450,000

0200,000400,000600,000800,000

1,000,0001,200,0001,400,0001,600,000

2000 2001 2002 2003 2004 2005 2006 2007 2008*

Mini/Light Large/Medium GesamtChange 2008/2000 = +750,000 units= annual Ø = 10%

From 2000 to 2008 Chinese bus market grows with an annual average rate of 10 per cent. Around 90 per cent of all buses are classified as mini or

light vehicles and have a length up to 276 inches.

* Forecast.Source: CAAM, Fourin, VDA statistics

ChinaSales of Buses

18

Production of heavy commercial vehiclesin China is skyrocketing

Trucks above 14t, Buses above 394 ins. length.Source: Fourin, CAAM, VDA statistics

41 5590

169

270 281

379

254

335

531

700

0

100

200

300

400

500

600

700

800

'98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08For.

in 1

,000

(+59%)

Production of Heavy Commercial Vehicles

1998 - 2008

(+32%)

(+32%) • Production of heavycommercial vehicles in

China recently moves withan average annual growth

rate of 40 per cent.

• In 2007 Euro III was introduced. Euro IV will be established in 2010 and should accelerate

demand and productionof new and more efficient

commercials.

Change 2008/2005

= annual Ø 40%

19

* Forecast.Source: CAAM, SIAM, VDA statistics

29,636

78,313

148,591

500,000

221,022

361,624

64,00055,27748,20638,34725,977

16,8810

60,000

120,000

180,000

240,000

300,000

360,000

420,000

480,000

540,000

'03 '04 '05 '06 '07 '08*

China India

AsiaExport of Commercial Vehicles

Export of Commercial Vehicles

2003 - 2008

Export quota: 13%

Export quota: 11%

China‘s exports areeight times high as

India‘s exports, whereas exportquota is nearly

equal.

20

Exports:46,000Share:

15%

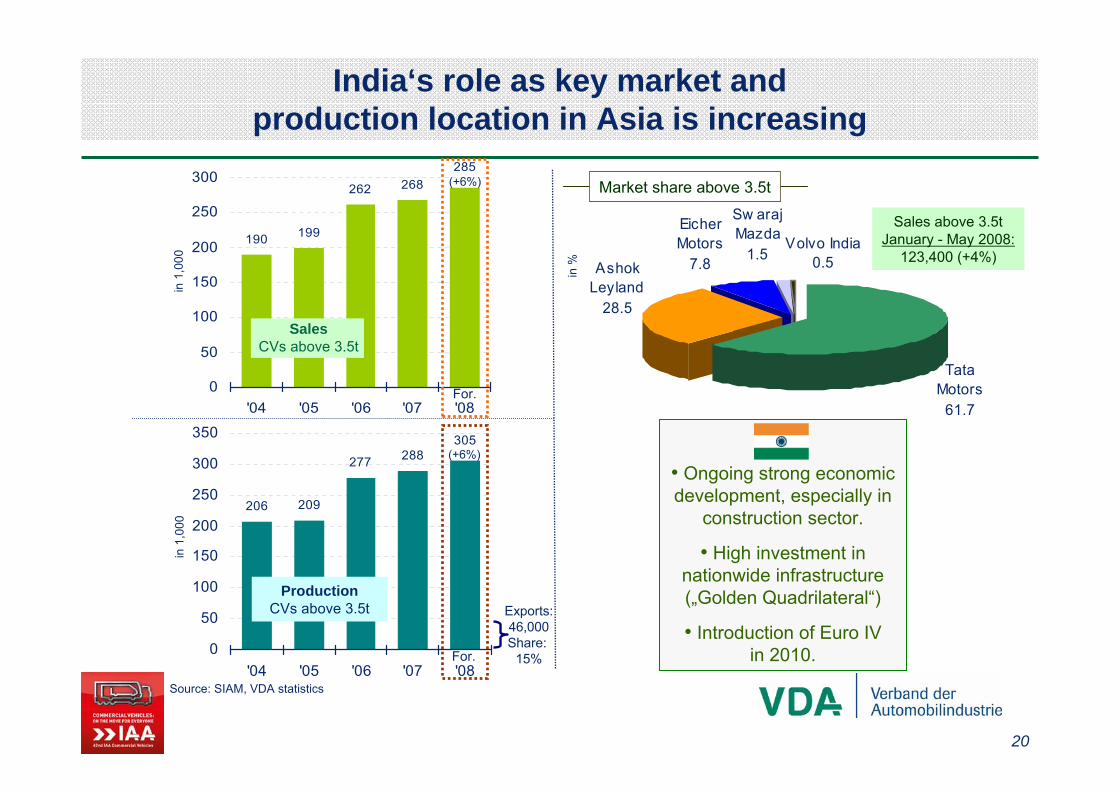

Tata Motors

61.7

Ashok Leyland

28.5

Sw araj Mazda

1.5Volvo India

0.5

Eicher Motors

7.8

190 199

262 268285

0

50

100

150

200

250

300

'04 '05 '06 '07 '08

SalesCVs above 3.5t

206 209

277 288305

0

50

100

150

200

250

300

350

'04 '05 '06 '07 '08

India‘s role as key market and production location in Asia is increasing

ProductionCVs above 3.5t

Source: SIAM, VDA statistics

in 1

,000

in 1

,000

Sales above 3.5tJanuary - May 2008:

123,400 (+4%)

in %

For.

For.

(+6%)

(+6%)

• Ongoing strong economicdevelopment, especially in

construction sector.

• High investment in nationwide infrastructure(„Golden Quadrilateral“)

• Introduction of Euro IV in 2010.

Market share above 3.5t

21

19,7

80

24,7

13

25,8

25

27,8

13

28,9

26

37,3

37

46,0

00

26,1

65

25,6

73

23,0

87

20,9

88

21,2

43

27,0

59 28,0

00

41,02345,701 48,912

53,486 55,091

64,396

74,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2002 2003 2004 2005 2006 2007 2008*

bis 3,5 t ab 3,5 t GesamtChange 2008/2002= annual Ø = 10%

Sales of buses in India expanded quite well during the last years. Buses as an important means of transportation clearly benefit from the extension

and advancement of nationwide infrastructure.

* Forecast.Source: SIAM, VDA statistics

IndiaSales of Buses

22

IndiaProduction of Commercial Vehicles

Source: SIAM, VDA statistics

57 57 63 57 80 100 130169

208250

295

72111 92 92

117154

206209

277

288

305

0

100

200

300

400

500

600

'98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08

CVs above 3.5tCVs up to 3.5t

For.

in 1

,000

(+4%)

Production of Commercial Vehicles

1998 - 2008

(+33%)

(+6%)

• Since 2002 productionof light and heavy

commercial vehicles has increased steadily.

• In 2010 Euro IV will beintroduced and shouldprovide production with

further impetus.

• Investment of foreignmanufacturers like Volvo,

MAN or Daimler are a clear evidence for India‘srising attractiveness as

production location.

(+23%)(+20%)

(+18%)

23

Manufacturers strengthen their position in BRICs

MAN Force Trucks, a jointventure set up by MAN and

Force Motors, recently startedserial production of heavy

commercial vehicles in India.

Daimler and Hero Group start Indian joint venture Daimler Daimler Hero Commercial

Vehicles. First vehicles shall beassembled in 2010.

Volvo buys stake in Indian manufacturer Eicher Motors.

Both companies intend to set up a joint venture for

common commercialvehicles production.

Daimler is checkingpossibilities for an assembly plant in

Russia. Scania intendsto build up a plant withan annual capacity of

10,000 units.

MAN intends to enterBrazilian market in

cooperation with VW, which has considerablemarket share in Brazil.

MAN sees high potential in closer cooperation, especially regarding

components and engines.

Volvo is building up a plant in Russia with an annualcapacity of 15,000 trucks,

completion in 2009.

MAN produces trucksclose to Krakow (Poland) since 2007. This facilityalso delivers to Russia

and other CIS countries.

24

* Forecast.Source: VDA statistics, Global Insight

265

186

296

140146

117

100

125

150

175

200

225

250

275

300

'03 '04 '05 '06 '07 '08*

Eastern EuropeSales of Commercial Vehicles above 6t

Sales of Commercial Vehicles above 6t

2003 - 2008

Change 2008/2003 = +179,000 units

= annual Ø = 20%

in 1,000

10

152

73

24

8

11

24

77

174

8

0 50 100 150 200

Belarus

Ukraine

Turkey

New EU

Russ ia 20082007

Russia is heavyweightchampion in sales

of commercialvehicles above 6t in Eastern Europe.

in 1

,000

25

59 6371 71

86

111

125

0

20

40

60

80

100

120

'02 '03 '04 '05 '06 '07 '08

67 7082 83

103

152

174

0

30

60

90

120

150

180

'02 '03 '04 '05 '06 '07 '08 3.8%3.3%

3.3%3.2%

61.1%

1.6%5.9%

10.0%

17.4%

26.2%22.1%

3.2%

Source: VDA statistics, Global Insight

in 1

,000

in 1

,000

For.

Production CVs >6t

SalesCVs >6t

For.

• From 2002 to 2008 sales of commercial vehicles above 6t

rise by 160 per cent.

• Domestic manufacturers still play an important role in Russian

commercial vehicle business.

• Sales clearly exceedproduction.

KAMAZ

GAZ

MAZUralAz

ZIL

others

MANHyundai

CNHTC

ScaniaVolvo

Market share > 6 t(+14%)

(+12%)

RussiaProduction and Sales of Commercial Vehicles above 6t

26

7.2%

4.8%

4.5%

3.3%60.8%

3.1%10.5%

21.6%

25.6%16.1%

3.3%

1.4

0.8

2.0

3.43.7

4.64.8

0

1

2

3

4

5

'02 '03 '04 '05 '06 '07 '08

4.23.1

7.78.8

10.610.1

10.5

0

2

4

6

8

10

12

'02 '03 '04 '05 '06 '07 '08

in 1

,000

in 1

,000

Production CVs >6t

SalesCVs >6t

• Sales of commercial vehiclesabove 6t clearly benefit fromincreasing economic activity,

especially in industrial production.

• High transport activity in goodsexchange with most important

trade partner Russia.

• Local manufacturers gain a market share of 61 per cent.

UkraineProduction and Sales of Commercial Vehicles above 6t

Source: VDA statistics, Global Insight

MAZ

KAMAZ

KRAZ

ZIL

TATA

Dongfeng

Daimler

FAW

Volvo

others

(+4%)

(+4%)Market share > 6 t

For.

For.

27

* Forecast. Including pre-assembled vehicles.Source: ASM Holding, UkrAutoprom, VDA statistics

19,549

22,50824,267

28,000

24,389

26,760

6,2005,597

3,986

6,1235,536

2,484

0

5,000

10,000

15,000

20,000

25,000

30,000

'03 '04 '05 '06 '07 '08*

Russia

Ukraine

Russia and UkraineExport of Commercial Vehicles

Export of Commercial Vehicles

2003 - 2008• Russian exports aremore than four timeshigh than exports of

the Ukraine.

• Around 85 per centof all Russian exportsgoes to CIS countries.

• Russian export valuefor commercial

vehicles amounted to 560 Mn. Euro in 2007.

• The Ukraine deliversmainly to Russia

and Central Asiancountries.

28

2,210

3,306

6,935

142

240

379426 442

465 500

88134

203233

266

315

368

0

100

200

300

400

500

'02 '03 '04 '05 '06 '07 '08*

Source: OSD, VDA statistics

Production

Exports

TurkeyProduction, Sales and Exports of Commercial Vehicles

Productionand Exports

of CVs

Productionof Heavy Trucks

(January - May 2008)

in 1

,000

17

36

4853 52

47 47

0

10

20

30

40

50

60

'02 '03 '04 '05 '06 '07 '08*

Sales of CVs above

3.5t

in 1

,000

Ø 43k

For.

• In 2007 sales of commercial vehiclesslipped due to weaker economic

development and higher interest rates.

• For this year a stable developmentis expected.

• Turkish production and exports of commercial vehicles still rising.

Mercedes is leading manufacturerin heavy truck business.

Truc

ks a

bove

12t Mercedes

Ford

B.M.C.

(+1%)

For.

Export-quota:74%

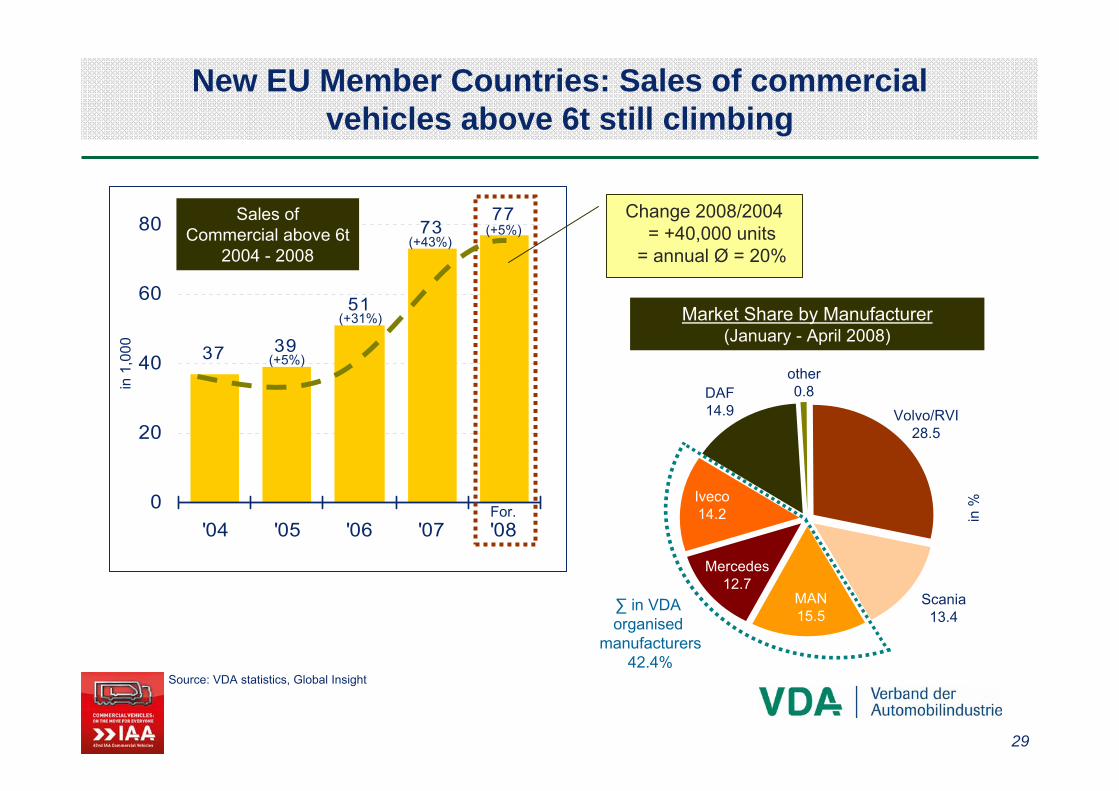

29

37 39

51

7377

0

20

40

60

80

'04 '05 '06 '07 '08

New EU Member Countries: Sales of commercialvehicles above 6t still climbing

For.

Source: VDA statistics, Global Insight

in 1

,000

Sales ofCommercial above 6t

2004 - 2008

Market Share by Manufacturer(January - April 2008)

∑ in VDA organised

manufacturers42.4%

(+5%)

(+31%)

(+43%)(+5%)

Change 2008/2004 = +40,000 units

= annual Ø = 20%

in %

Volvo/RVI28.5

Scania13.4

MAN15.5

Mercedes12.7

Iveco14.2

DAF14.9

other0.8

30

13.2%

28.2%

14.9% 1.0%

42.7%

8.2%

16.4%

18.1%

11.4%

26.0%

14.4%1.9%

46.3%

10.3%

16.9%

19.1%

294 291311

333 346 348 354

0

50

100

150

200

250

300

350

400

'02 '03 '04 '05 '06 '07 '08

Sales of CVs >6t

213 216233

252 263 270 277

0

50

100

150

200

250

300

'02 '03 '04 '05 '06 '07 '08

Western Europe: Slight increase in sales of commercial vehicles above 6t in 2008

Sales of CVs >16t

Source: VDA statistics

in 1

,000

in 1

,000

Market share above 6t(January - May 2008)

Mercedes

MAN

Iveco

DAFothers

Volvo/RVI

Scania

Mercedes

MAN

Iveco

DAF others

Volvo/RVI

Scania

For. For.

(+2%)(+3%)

Market share above 16t(January - May 2008)

31

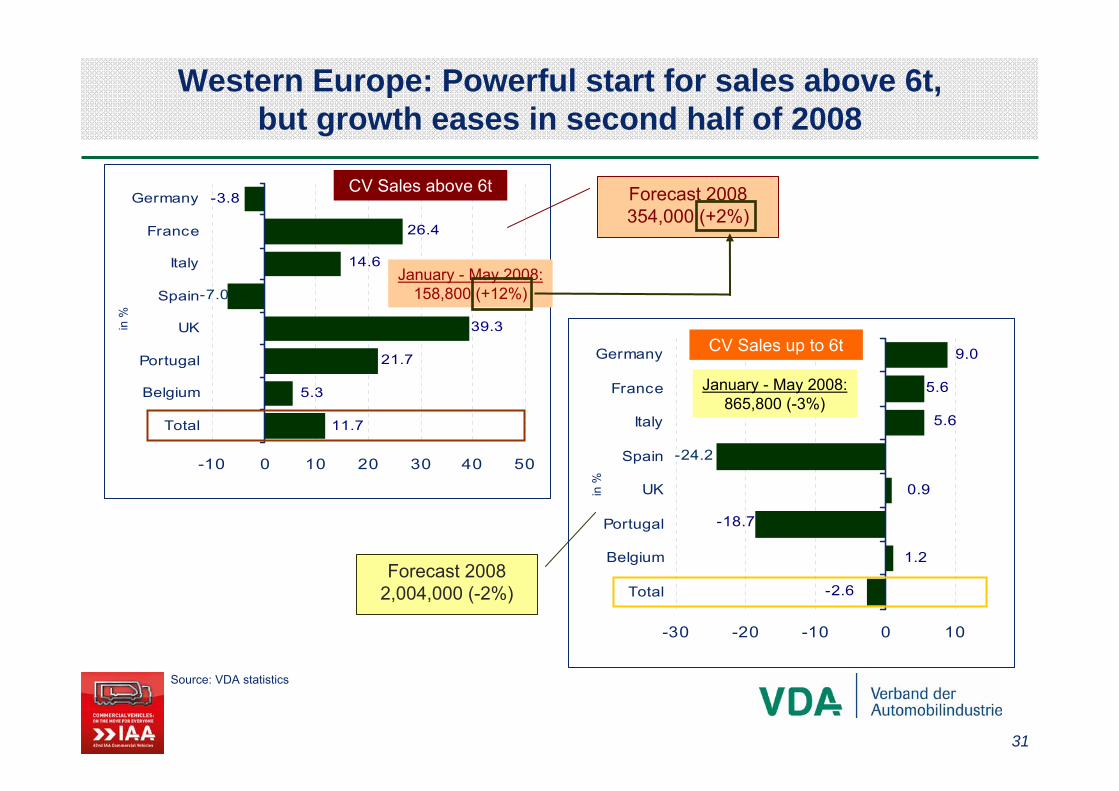

1.2

-18.7

-24.2

5.6

5.6

9.0

0.9

-2.6

-30 -20 -10 0 10

Total

Belgium

Portugal

UK

Spain

Italy

France

Germany

5.3

21.7

-7.0

14.6

26.4

-3.8

39.3

11.7

-10 0 10 20 30 40 50

Total

Belgium

Portugal

UK

Spain

Italy

France

Germany

Western Europe: Powerful start for sales above 6t, but growth eases in second half of 2008

January - May 2008:158,800 (+12%)

Source: VDA statistics

in %

CV Sales above 6t

in %

January - May 2008:865,800 (-3%)

CV Sales up to 6t

Forecast 2008 354,000 (+2%)

Forecast 2008 2,004,000 (-2%)

32

20.8 16.7 20.1 20.0

34.8 34.8 32.4 31.0

4.6 5.3 6.6 5.7

31.836.5 34.3 36.5

2.01.81.92.4

4.84.84.85.6

0

10

20

30

40

50

60

70

80

90

100

1997 2002 2007 -05/2008

Large PickupCompact VanFullsize VanHeavy VanMidsize VanSmall Van/ Micro Van/ Small Pickup

Western EuropeSales of Commercial Vehicles up to 6t by Segment

* Forecast.Source: VDA statistics

in %

• From 1997 to 2007 sales up to 6t increasedby 36 per cent to over

2 Mn. units. In 2008 there will

be a slight decreasein light commercial

vehicle sales.

• Compact/Fullsize and Heavy Vans compile

a market shareof 38 per cent.

• 37 per cent of all sold vehicles up to 6t

are small vehiclesup to 2t.

19971,507,000

20021,834,000

20072,048,000

2008*2,004,000 (-2%)

33

26.3

25.2

39.3

5.4

5.3

-25.9

23.8

-24.3

2.1

-35 -25 -15 -5 5 15 25 35 45

B elgium

Sweden

Danemark

A ustria

Netherlands

P o rtugal

Spain

Italy

UK

France

Germany

Loser Winner

+12.7%

Sales of buses above 8t in Western Europe 2008 with the highest increase in the last four years

Sales of Busesabove 8t

Jan. - May 2008: 12,700 (+13%) 5.5 5.3 4.9 4.8 4.5 4.6 4.9 4.94.8

26.7 26.724.7 24.8

25.9 26.3 26.5 26.6 27.5

0

4

8

12

16

20

24

28

'00 '01 '02 '03 '04 '05 '06 '07 '08For.

Source: VDA statistics, Analyse & Prognose GmbH

Western Europe

Germany

in 1,000

(+3%)

(+2%)

Sales of Buses above 8t 2000 - 2008

180.4

68.7

II. Germany- Domestic Market- Exports- Production- Trailerindustry- Key Figures- Freight Transport Market - Technics and emissionen

page 54 page 59page 65 page 70 page 78

page 35

page 85

35

GermanyProduction and Sales of Commercial Vehicles

units ±% units ± %

Commercial vehiclesNew registrations *) 30,325 6.6 170,000 5 CV up to 6 t GVW 21,349 8 117,500 9 CV up to 2 t GVW 2,477 20 13,000 28 CV over 2 up to 3,5 t GVW 18,210 6.5 101,000 7 CV over 3,5 up to 6 t GVW 662 3,500 5 CV over 6 t GVW 8,530 2 49,600 -3 CV over 6 up to 16 t GVW 2,755 -1 14,900 -4 CV over 16 t GVW 5,775 4 34,700 -2 Buses 446 52 2,900 13

Export 39,380 23 206,300 18 CV up to 6 t GVW 24,720 30 129,100 20 CV over 6 t GVW 13,950 14 73,700 15 Buses 710 -11.1 3,600 -3

Produktion 48,390 10 278,500 13 CV up to 6 t GVW 29,100 13 168,100 15 CV over 6 t GVW 18,500 6 106,000 9 Buses 790 3 4,500 7

June 2008 up to June 2008

Source: VDA statistics, Kraftfahrt-Bundesamt

36

GermanySales of Commercial Vehicles by Owner Class

33,792

26,099

20,276

16,550

9,682

10,044

9,803

10,962

34,228

22,957

20,113

15,285

9,298

8,451

8,195

12,403

0 7,000 14,000 21,000 28,000 35,000

other public and privateservices

trade, repair of motor vehiclesand consumer goods

employees and non-activepersons

traffic, telecommunication

renting

manufacturing industry

construction

others

1-6 2007

1-6 2008

units

-1%

+14%

+1%

+8%

+4%

-12%

+20%

+20%

Sales up to June 2008

Source: VDA statistics, Kraftfahrt-Bundesamt

renting7%

manufacturing industry7%

construction8%

others7%

traffic, telecommunication12%

trade, repair of motor vehicles and consumer

goods19%

other public and private services

25%

employees and non-active persons

15%

37

7.98.3

8.88.4

9.2

7.87.7

6.4

0.90.70.70.90.91.11.3

1.7

0.0

2.0

4.0

6.0

8.0

10.0

2002 2003 2004 2005 2006 2007 1-6 2007 1-6 2008

cv over 10 to 12 t cv over 12 to 14 t

GermanySales of Commercial Vehicles over 10 to 14 t

shar

eof

cv

over

10 to

14

t in

sale

sof

cv

over

6 t

Source: VDA statistics, Kraftfahrt-Bundesamt

38

20,4

86

20,5

71

39,7

82

35,6

89

32,4

60

30,6

82

25,6

30

23,7

51

23,3

43

21,1

33

41,2

69

34,2

58

26,6

32

25,3

69

19,6

33

18,4

58

0

7,000

14,000

21,000

28,000

35,000

42,000

2002 2003 2004 2005 2006 2007 Jan.-Jun.2007

Jan.-Jun.2008

semitrailer tractors

semitrailers

GermanySales of Semitrailer Tractors and Semitrailers

units

+124%+67%

Source: VDA statistics, Kraftfahrt-Bundesamt

-0.4%+10.5%

39

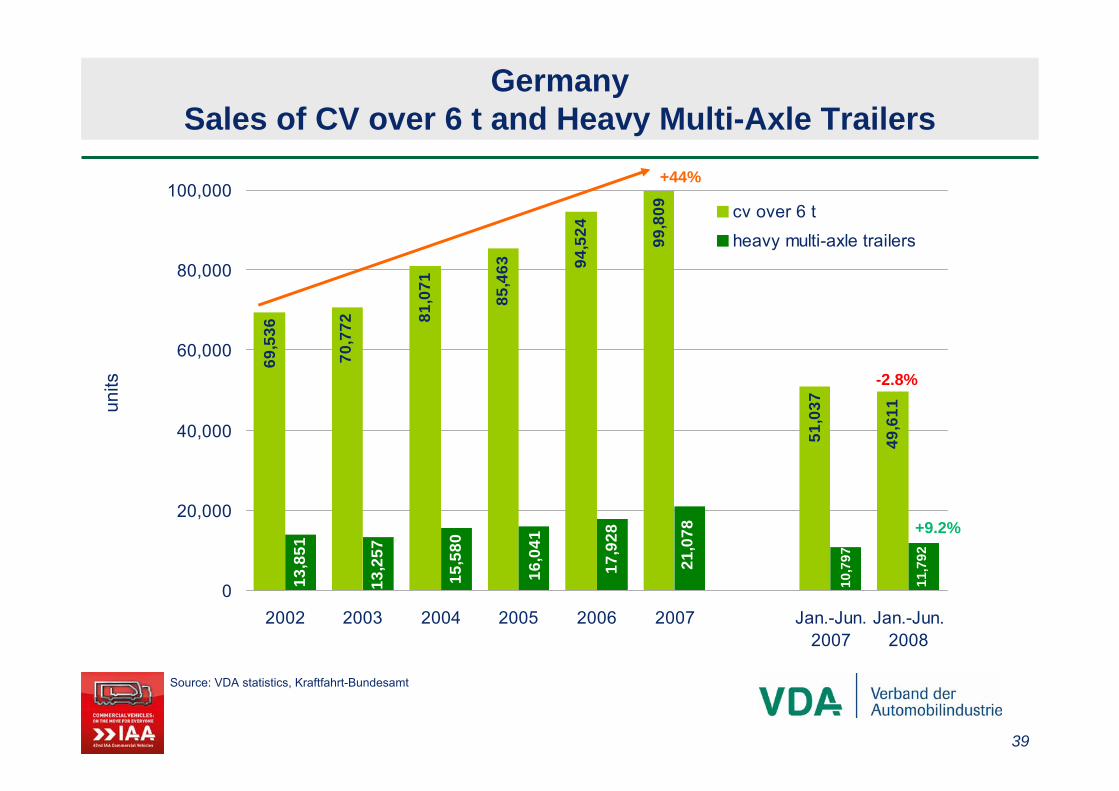

GermanySales of CV over 6 t and Heavy Multi-Axle Trailers

units

Source: VDA statistics, Kraftfahrt-Bundesamt

69,5

36

70,7

72 81,0

71

85,4

63 94,5

24 99,8

09

51,0

37

49,6

11

13,8

51

13,2

57

15,5

80

16,0

41

17,9

28

21,0

78

10,7

97

11,7

92

0

20,000

40,000

60,000

80,000

100,000

2002 2003 2004 2005 2006 2007 Jan.-Jun.2007

Jan.-Jun.2008

cv over 6 t

heavy multi-axle trailers

+44%

-2.8%

+9.2%

40

GermanyNew Registrations of Tippers

units

1,25

3

1,03

0

2,03

3

2,04

0

2,13

2

2,22

8

2,23

4

2,35

0

4,53

1

4,88

25,85

6

5,55

3

5,96

0 6,84

7

7,99

5

8,73

6

0

3,000

6,000

9,000

2002 2003 2004 2005 2006 2007 Jan.-Jun.07

Jan.-Jun.08

up to 6 t over 6 t

-7.2%

+21.7%

Source: VDA statistics, Kraftfahrt-Bundesamt

41

GermanySales of Heavy Trucks and Trailers with Tanker Body

units

Source: VDA statistics, Kraftfahrt-Bundesamt

307

162

54660

0

533

53357

0

577

545

553

551

720 740

752

856

856

1,17

1

1,13

1

0

200

400

600

800

1,000

1,200

2002 2003 2004 2005 2005 2006 2007 Jan.-Jun. 07

Jan.-Jun. 08

Trucks over 6 t with tanker body (haz. goods)

Trailers over 6 t with tanker body (haz. goods)

-0.4%

-47.2%

42

13,8

39 15,6

65

18,3

48

18,9

46

17,7

33

17,8

02 19,3

63 20,6

06

21,2

36

19,6

58

12,9

72 14,7

36

0

5,000

10,000

15,000

20,000

25,000

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

1-6

2007

1-6

2008

units

26.0

38

25.6

58

26.2

00

24.5

85

22.6

73

22.6

04

21.5

72

21.6

72

22.4

21

19.0

84

12.0

03

12.0

75

0

5.000

10.000

15.000

20.000

25.000

30.000

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

1-6

2007

1-6

2008

Motor Caravans Caravans

+0,6%

+13.6%

GermanyNew Registrations of Motor Caravans and Caravans

Source: VDA statistics, Kraftfahrt-Bundesamt

43

44.4

25.1

19.9

2.0 3.15.5

42.1

27.0

19.0

2.5 3.2

6.2

39.2

28.2

18.0

3.1 3.5

8.0

0

9

18

27

36

45

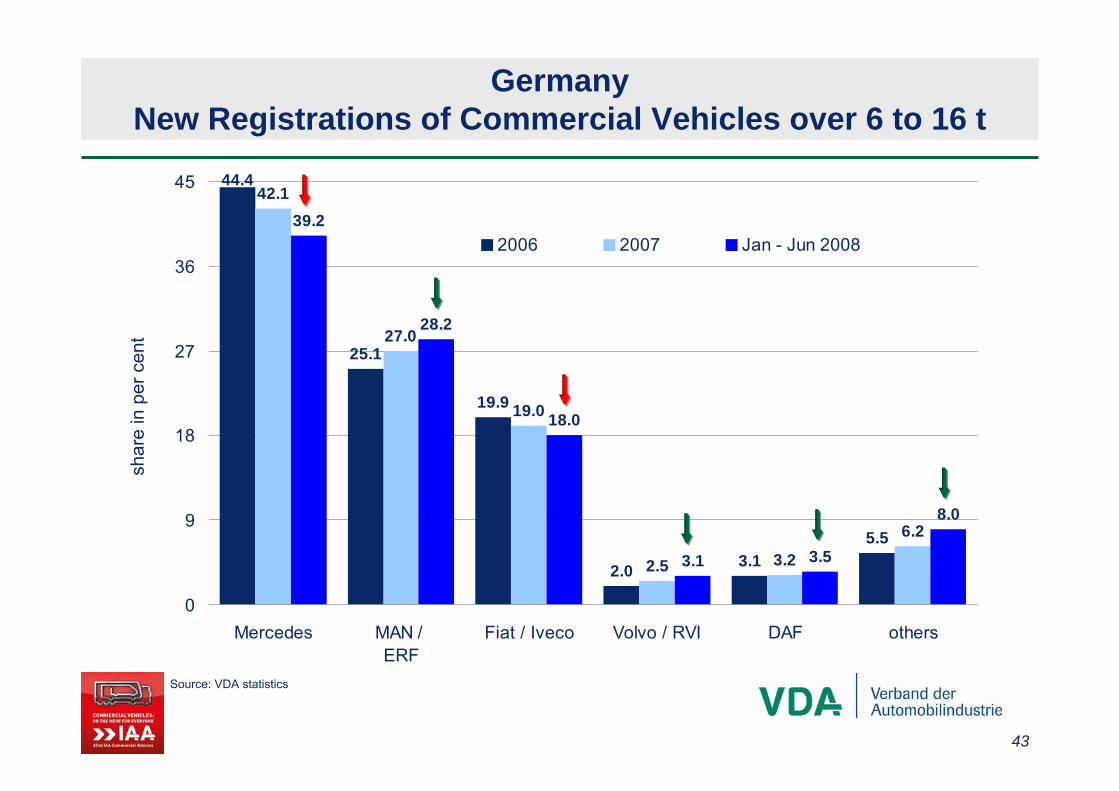

Mercedes MAN / ERF

Fiat / Iveco Volvo / RVI DAF others

2006 2007 Jan - Jun 2008

GermanyNew Registrations of Commercial Vehicles over 6 to 16 t

shar

ein

per

cen

t

Source: VDA statistics

44

GermanyNew Registrations of Commercial Vehicles over 16 t

shar

ein

per

cen

t

Source: VDA statistics

38.5

27.3

9.6 9.07.2 6.5

1.9

24.9

10.8 9.8

7.1 7.1

1.8

32.8

27.3

12.510.5

7.7 6.8

2.4

38.5

0

10

20

30

40

Mercedes MAN / ERF Volvo / RVI DAF Scania Fiat / Iveco others

2006 2007 Jan - Jun 2008

45

21.5

8.27.3

8.5

6.4 6.1

25.4

8.6

6.17.6 8.3

5.7

24.0

5.9

7.99.2

3.02.7

11.8

27.5

22.0

2.8

13.5

21.0

12.8

5.5

10.7

0

5

10

15

20

25

30

VW-Group Mercedes Fiat / Iveco Ford Opel Renault PSA jap. brands others

2006 2007 Jan - Jun 2008

GermanyNew Registrations of Commercial Vehicles up to 6 t

shar

ein

per

cen

t

Source: VDA statistics

46

774,

000

888,

000

883,

000

965,

300

906,

600931,

900

926,

000

914,

900

905,

400

899,

500

906,

700

908,

400

896,

000

710,000

740,000

770,000

800,000

830,000

860,000

890,000

920,000

950,000

980,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

GermanyParc* of CV over 6 t (excl. buses)

*reference date: 1.1.; 2008 without temporary unregistered vehicles

units

Exports of used CV brings a low level of the parc of heavy trucks

Source: VDA statistics

47

6,4

7,9

8,5 8,4

6,7 6,9

7,6

8,8

9,7

8,3

7,1

7,9

4,0

5,0

6,0

7,0

8,0

9,0

10,0

11,0

bis 3,5t 3,5t-6t 6t-12t 12t-16 >16t total

01.07.1998 01.01.2003 01.01.2008 *)

GermanyAverage age of Commercial Vehicle Parc

In y

ears

In the last 10 years the average age of commercial vehicle parc is increased by one year

*) incl. teporary unregistered vehiclesSource: KBA, VDA statistics.

48

11,344

1,462

6,555

2,852

3,798

848

850

0

5,000

10,000

15,000

20,000

25,000

Western Europe Eastern Europe

buses

semitrailertractors

cv over 5 t

cv up to 5 t

5,471 (-1%)

22,547 (+1%)

(+6%)

(+2%)

(-7%)

(-13%)

(-

(+31%)(-19%)

(+7%) 91.4

23.0

196.2

90.4

128.6

34.6

46.6

25.4

0

100

200

300

400

500

Western Europe Eastern Europe

173.5 (+8%)

462.9 (+10%)

(+19%)

(+16%)

(+5%)

(-11%)

(-5%)

(+17%)

(-9%)(+14%)

GermanyExports of Used Commercial Vehicles up to April 2008

units

Total Exports:up to 5 t: 14,800 (+6%)over 5 t: 14,800 (+4%)Semitrailer tractors: 8,100 (+3%)Buses: 1,540 (-26%)Total: 39,200 (+3%)

Exports units

in million

euro

Export value

Export value per unit:W. Europe: 31,700 € (+9%)E. Europe: 20,500 € (+9%)Asia: 12,100 € (+26%)Africa: 8,600 € (+18%)

Source: VDA statistics

49

0

14,600

29,200

43,800

58,400

73,000

Jan Feb Mrch Apr May Jun Jul Aug Sep Oct Nov Dec

2006 2007 2008

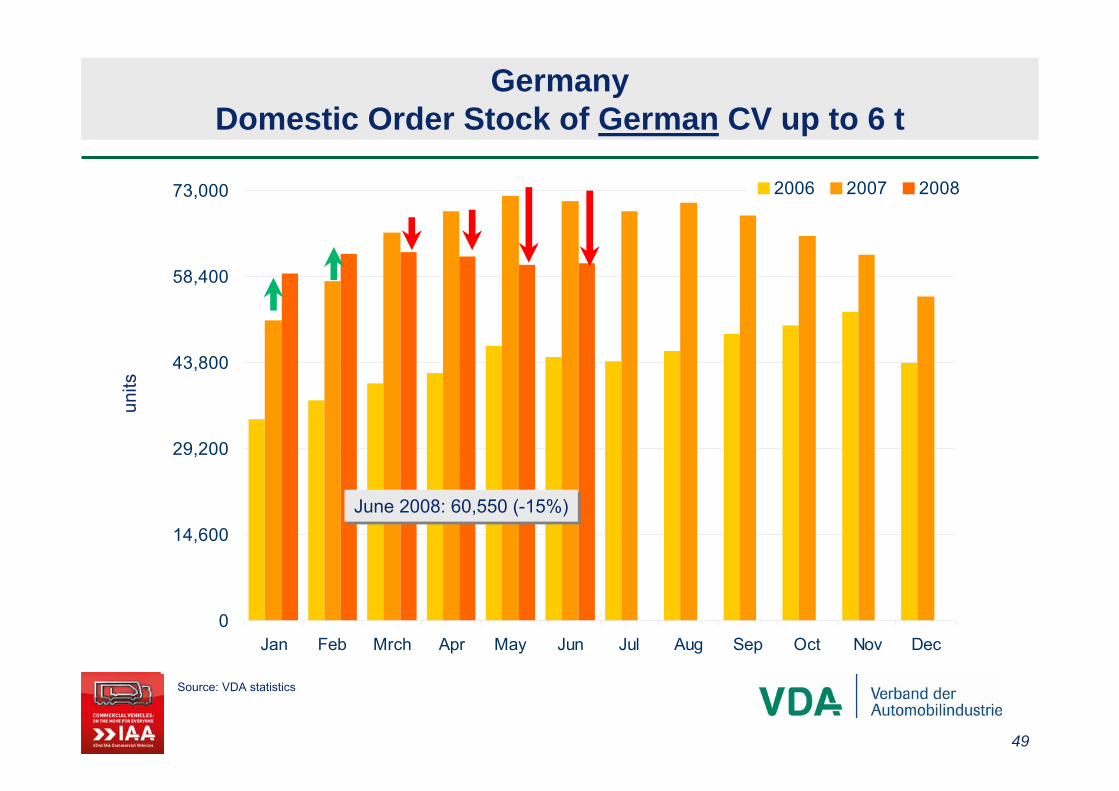

GermanyDomestic Order Stock of German CV up to 6 t

units

June 2008: 60,550 (-15%)June 2008: 60,550 (-15%)

Source: VDA statistics

50

0

10,800

21,600

32,400

43,200

54,000

Jan Feb Mrch Apr May Jun Jul Aug Sep Oct Nov Dec

2006 2007 2008

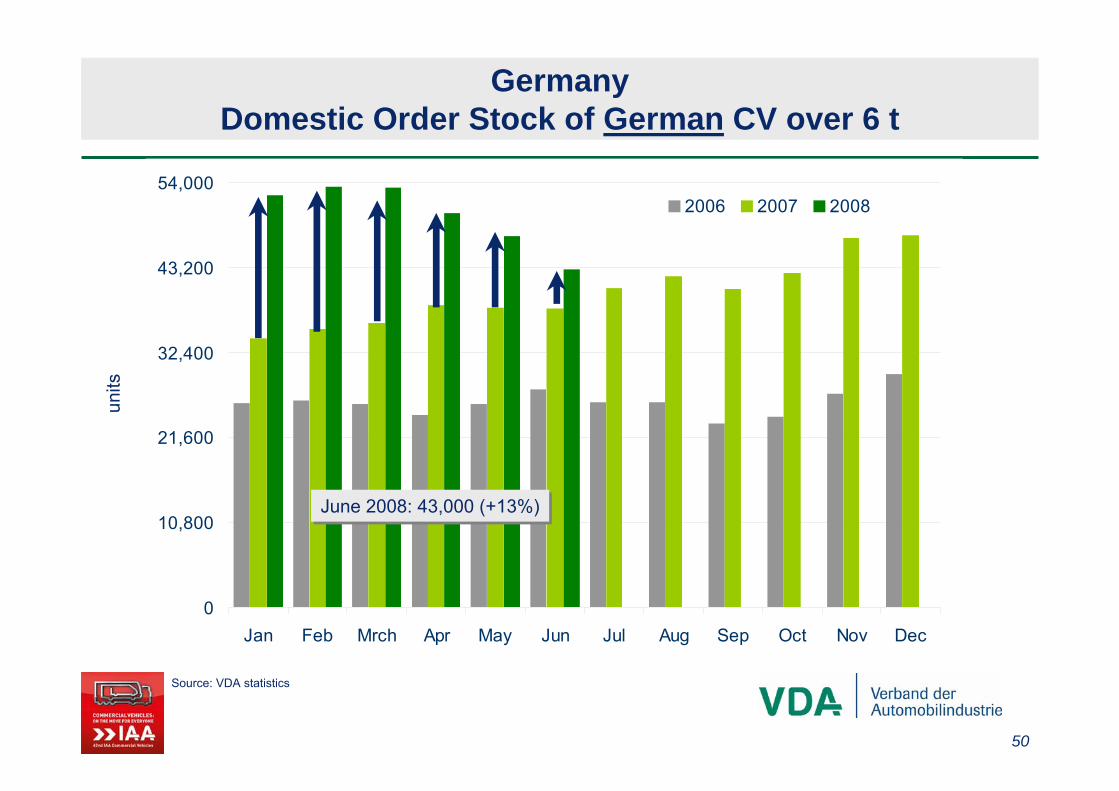

GermanyDomestic Order Stock of German CV over 6 t

units

June 2008: 43,000 (+13%)June 2008: 43,000 (+13%)

Source: VDA statistics

51

4,000

7,000

10,000

13,000

16,000

19,000

22,000

2006 2007 2008

units

Nfz bis 6 t

Nfz über 6 t

2008: 235 Tsd. (+3%)

2008: 95-98 Tsd. (-5% /-2%)

Jan.-Jun. 2008: +9%

2007: +12%

Jan.-Jun. 2008: -3%2007: +6%

Prognoses

Trends and seasonally-adjusted monthly figures

Source: VDA statistics

The elevated stock of orders of commercial vehiclessuggests a high new registration level for 2008

52

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2004 2005 2006 2007 2008

Trendkomponente und saisonbereinigte Monatszahlen

Jan.-Jun. 2008: -2%

Jan.-Jun. 2008: -4%

units

2007: 68 Tsd. (+9%)

2007: 31 Tsd. (-1%)

2008: 65-68 Tsd. (-5% / -1%)

2008: 30 Tsd. (-4%)

Quelle: VDA Statistik, Kraftfahrt-Bundesamt

Prognoses

GermanySales of Commercial Vehicles over 6 t

cv over 16 t

cv over 6 to 16 t

53

GermanySales of Commercial Vehicles

in E

inhe

iten

Quelle: VDA-Statistiken, Kraftfahrt-Bundesamt

0

50.000

100.000

150.000

200.000

250.000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Nfz bis 6 t Nfz über 6 t

In the last 15 years sales of lightcommercial vehicle increased by 31%

In the last 15 years sales of lightcommercial vehicle increased by 31%

In the last 15 years sales of heavy commercial vehicles increased by38% (34%)In the last 15 years sales of heavy commercial vehicles increased by38% (34%)

182,500

95,000bis

98,00070,800

235,000

54

15.676

10.821

10.640

10.168

9.101

6.600

5.635

5.320

3.655

3.640

1.896

1.192

0 2.000 4.000 6.000 8.000 10.000 12.000 14.000 16.000 18.000

Frankreich

OPEC

Spanien

Großbritannien

Italien

Polen

Russland

Südafrika

Tschechien

Rumänien

China

Südkorea

German Exports of CV > 6 t into selected countries, 2007 and Jan.-May 2008

Exp

orts

uni

ts(C

hang

e ag

ains

tpre

viou

sye

arin

bra

cket

s)

Jan.-June 08: 73.700 (+15%)

Jan.-May 08 vs. previous year

(-5%)

(+31%)

(+3%)

(-12%)

(-22%)

(+52%)

(+121%)

(+33%)

(+29%)

(+116%)

(+39%)

(+139%) -2%

-5%

+19%

-1%

+6%

+76%

±0%

+29%

+23%

+22%

-2%

+6%

Russia

Romania

Source: VDA statistics

South Korea

Czech Rep.

South Africa

Poland

Italy

UK

Spain

France

55

71

86 87

98 99 9688

105

116 118

132136

64

74

61%

78%

68%

66%

70%

67%67%

69%

61%61%

69%

65%

75%

0

20

40

60

80

100

120

140

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008* Jan .- Jun.2007

Jan .- Jun.2008

60%

65%

70%

75%

80%Export Exportquote

Commercial Vehicles over 6t:Exports rising continually

*) ForecastSource: VDA statistics

thou

sand

s

shareof exports

in production

+15%

The German exports of CV over 6 t haveincreased by 85% in the last ten years..

exports export ratio

56

38.234

23.532

18.998

15.564

13.750

11.921

7.833

6.741

6.237

4.135

3.364

3.094

1.731

1.680

0 5.000 10.000 15.000 20.000 25.000 30.000 35.000 40.000

GroßbritannienFrankreich

SkandinavienNiederlande

SpanienItalienTürkei

USAPolen

MexikoRumänienRusslandSüdafrika

Israel

German Exports of CV up to 6 t into selected regions, 2007 und Jan.-May 2008

Jan.-June 08: 129.100 (+20%)

Jan.-May 08 vsprevious year

(+187%)

(+15%)

(+110%)

(+36%)

(+33% )

(+38%)

(+44%)

(+216%)(+23%)

(+26%)

(+43%)

(+27%)

(+19%)

(+18%)

Exp

orts

uni

ts(C

hang

e ag

ains

tpre

viou

sye

arin

bra

cket

s)

+54%

+21% +53%

+178% +3%

+55%

+20%

+1%

+23%

-1%

-5%

+3%

+13%

+21%

Source: VDA statistics

South Africa

Russia

RomaniaMexico

Poland

Turkey

Italy

Spain

Netherlands

Scandinavia

France

UK

57

141 147 143

160170

145152

145

163 164

222233

107

129

64%

68%

74% 74%

77%

69%

70% 71%

65% 66%

67%

70%69%

0

40

80

120

160

200

240

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Jan .- Jun.2007

Jan .- Jun.2008

60%

65%

70%

75%

80%Export Exportquote

Commercial vehicles up to 6t: Dynamic export growth

thou

sand

s

shareof exports

in production

+20%

In the first six months of 2008 the export ratioattained a 77% peak.

*) ForecastSource: VDA statistics

exports export ratio

58

64,286

11,534 10,657

1,779

12,902

1,402

31,059

9,760 7,449

6,230

513

3,823

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

EU-15 EU-12 Rest ofEurope

Asia America

trucks > 6 t:59,700 (+16%)

trucks < 6 t:104,300 (+18%)

(+18%)

(+5%) (+51%)

(+5%)

(+45%)

(+2%)

(+11%)(+61%) (+25%)

(+101%)

(+16%)

(+96%)

Exports of German Commercial Vehicles by Region,up to May 2008

shar

ein

per

cen

tex

ports

units

(cha

nge

in p

er c

ent)

Source: VDA statistics

59

GermanyDomestic Production of Commercial Vehicles by GWR

25,204

22,948 22,94622,334 9,037

5,051

6,106 6,6736,265 2,738

101,877139,719 146,814 165,711 75,688

138,969300,926235,383229,960

246,416

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%2001 2005 2006 2007 up to May 2008

cv up to 6 t cv over 6 up to 12 t cv over 12 up to 16 t cv over 16 t

shar

ein

per

cen

tun

its

(+13%)

(-18%)

(-5%)

cv up to 6 t138,969

62%

cv over 6 up to 12 t9,037

4%

cv over 12 up to 16 t2,738

1%

cv over 16 t75,688

33%

up to May 2008

+

-

cv up to 6 t246,416

65%

cv over 6 up to 12 t25,204

7%

cv over 12 up to 16 t5,051

1%

cv over 16 t101,877

27%

2001

60

Domestic Production close to capacity limit –Foreign Production booming

2629

0

5

10

15

20

25

30

Ausland: Mai Inland: Jun.

2007 2008

+13%+12%

30

19

05

101520253035

Ausland: Mai Inland: Jun.

2007 2008

+12%

+6%106

153

0

40

80

120

160

Ausland: Jan-Mai Inland: Jan-Jun.

2007 2008

+3%

+9%

Source: VDA statistics

130

168

0

30

60

90

120

150

180

Ausland: Jan-Mai Inland: Jan-Jun.

2007 2008

+17%

+15%

Production CV up to 6t

Production CV over 6t* **

*) without NAFTA: +25% **) without NAFTA: +5%

Foreign: Jan-May Domestic: Jan-Jun Foreign: May Domestic: Jun

Foreign: Jan-May Domestic: Jan-Jun Foreign: May Domestic: Jun

61

GermanyProduction of Buses

units

Source: VDA statistics

3,44

2

2,45

2

2,42

7

3,09

0

1,38

9

1,32

4

939

941

1,94

6

2,07

62,39

9

2,11

7

991

638

2,41

6

3,01

4

2,36

3

2,45

5

424

426

1,63

3

1,77

3

1,57

61,73

1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2002 2005 2006 2007 Jan.-Mai 2007 Jan.-Mai 2008

coachesurban public-transit busesoverland buseschassis

0%

+8%

+6%

0%

-5%

+55%

62

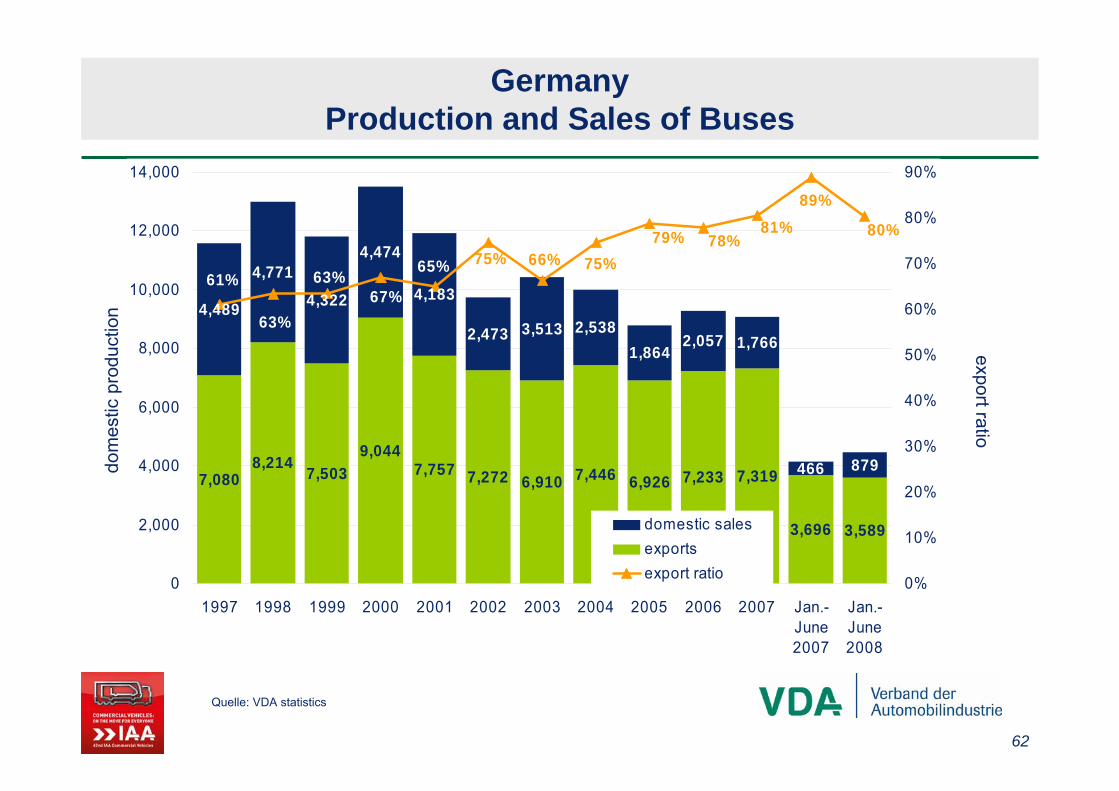

7,0808,214 7,503

9,0447,757 7,272 6,910 7,446 6,926 7,233 7,319

3,696 3,589

4,489

4,771

4,322

4,474

4,183

2,473 3,513 2,5381,864

2,057 1,766

466 879

80%

89%81%

78%79%75%66%75%65%

67%63%

63%

61%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Jan.-June2007

Jan.-June2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

domestic salesexportsexport ratio

GermanyProduction and Sales of Buses

dom

estic

prod

uctio

nexportratio

Quelle: VDA statistics

63

29.2

0.6

46.3

0.0

21.7

16.4

10.6

25.36.9

12.5

10.6

5.0

47.1

34.2

6.1

14.1

3.5

5.4

5.7

0.7

2.2

0

2.2

0.4

0.6

0.1

5.6

0 10 20 30 40 50 60 70 80

USA

Turkey

Czech Rep.

Spain

Portugal

Poland

Austria

Mexico

Canada

Japan

Brazil

Argentina

Jan.-May 2008: 129,600 CV up to 6t (+17%)

Jan.-May 2008: 153,000 CV over 6t (+3%)

Jan.-May 2008 32,100 buses (+13%)

Production Abroad: 314,700 (+9%)

German CV Production abroad Jan.-May 08booming except in NAFTAin 1,000

Source: VDA statistics

Share in world-wide production of German groups:CV up to 6 t: 50%CV over 6 t: 63%Buses: 90%CV tot.: 58%

11,000 (+23%)

64,700 (+26%)

74,900 (+11%)

5,000 (-50%)

12,800 (-14%)

12,600 (+1%)

52,500 (+36%)

29,800 (+3%)

9,100 (+8%)

30,900 (-26%)

6,100 (+8523%)

3,500 (+158%)

Forecast CV 2008: 732,000 (+5%)

64

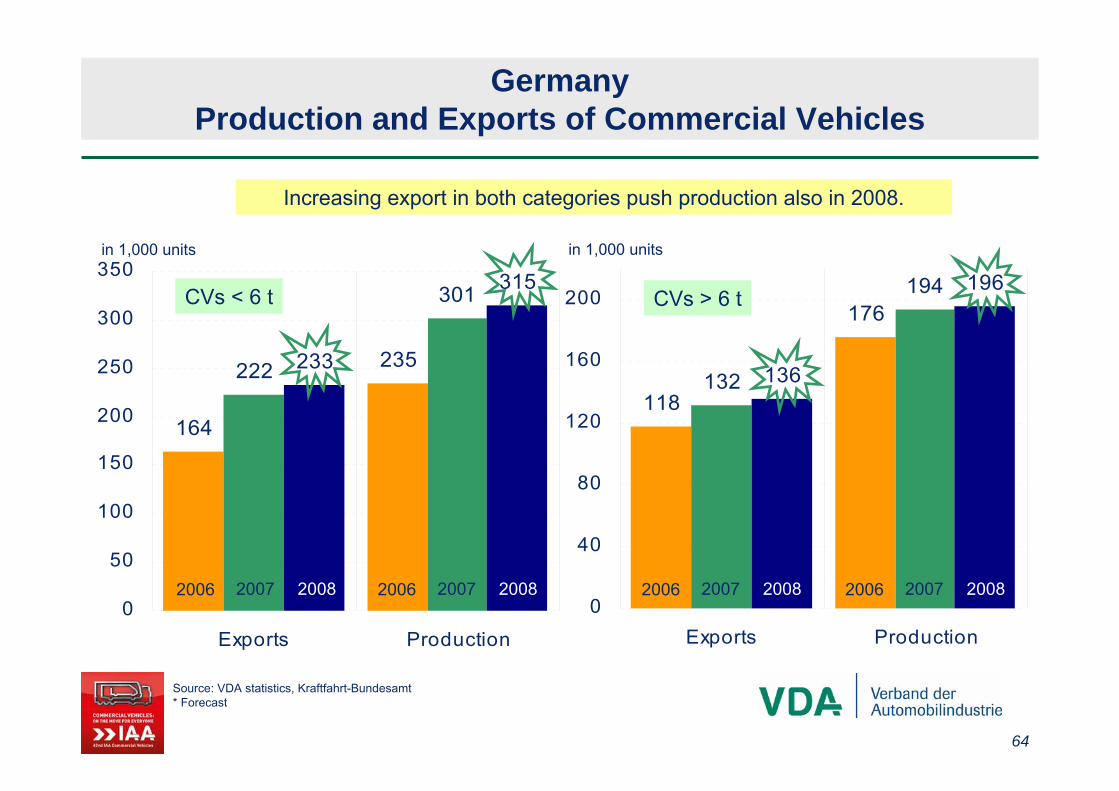

118

176

132

194

136

196

0

40

80

120

160

200

Exports Production

164

235222

301

233

315

0

50

100

150

200

250

300

350

Exports Production

GermanyProduction and Exports of Commercial Vehicles

Source: VDA statistics, Kraftfahrt-Bundesamt* Forecast

in 1,000 units

CVs < 6 t

Increasing export in both categories push production also in 2008.

CVs > 6 t

in 1,000 units

2006 2007 2008 2006 2007 2008 2006 2007 2008 2006 2007 2008

65

300

380

460

540

620

700

2005 2006 2007 2008

trend cycle and seasonally adjusted monthly figures *) change of statistical coverage from 2006 on

in M

io. E

uro

Turnover (domestic and abroad) in the trailer and body building industry*)

The trade surplus= balance of exports and importsincreased by 39% to 1.2 bn. €in the first four months of 2008.

domestic turnoverturnover abroad

Almost 60% of the turnover are export-

generated.

Almost 60% of the turnover are export-

generated.

1-4 2008:2,7 Bn. (+21%)

1-4 2008: 1,8 Bn. (+18%)

1-4 2008:Total: 4,5 Bn. (+19%)

Source: Statistisches Bundesamt

66

35,000

37,000

39,000

41,000

43,000

2005 2006 2007 2008

pers

ons

empl

oyed

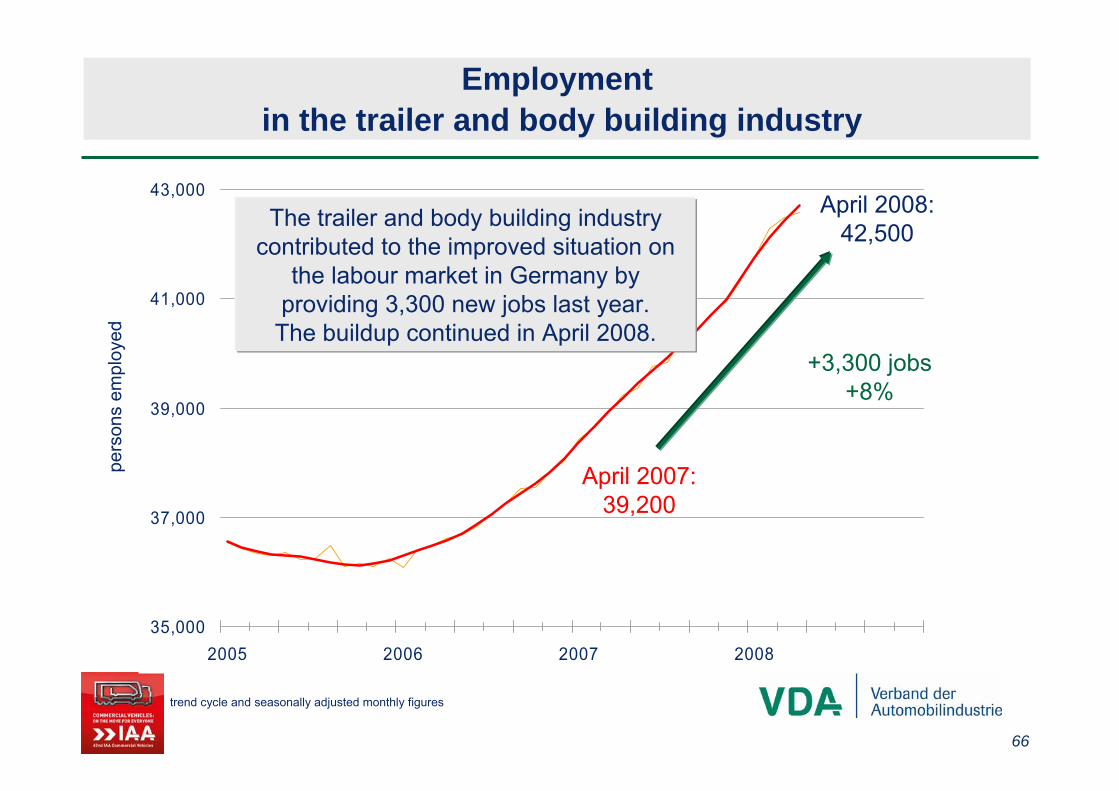

Employmentin the trailer and body building industry

trend cycle and seasonally adjusted monthly figures

April 2008:42,500The trailer and body building industry

contributed to the improved situation on the labour market in Germany by

providing 3,300 new jobs last year.The buildup continued in April 2008.

April 2007: 39,200

+3,300 jobs+8%

67

New Registrations of heavy Trailers >6 t vs. Ifo-Sentiment Indicator

1000

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

Jan98

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

80

85

90

95

100

105

110

115

Neuzulassungen Mehrachen-Anhänger >6t ifo Geschäftsklima

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

3200

3400

3600

Jan98

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

80

85

90

95

100

105

110

115

Neuzulassungen Sattelanhänger ifo GeschäftsklimaSemi-TrailerHeavy Multi Axle Trailer >6 t

The slowdown of the business sentiment since summer of 2007 is not reflected in the new registrations of heavy trailers.

Quelle: VDA-Statistiken

New RegistrationsNew Registrations

68

80

100

120

140

160

180

200

220

240

2000 2001 2002 2003 2004 2005 2006 2007 2008

Auftragseingang Produktion

Production and New Orders in the manufacturer group II: Normalisation trend is under way

Since 2006 orders havebeen increasingstrongly while

production has beenlagging behind

because of fully utilisedcapacities in the

manufacturer group II!

The arithmetical stock of ordersin the trailer, body & container

industry ensures a high production growth in 2008

Source: Statistisches Bundesamt.

69

170246

252252

273280281

302316

342346

353355

382398

403432

467491

507522

538

0

100

200

300

400

500

600

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Transportation in GermanyTransport Performance in Million Ton Kilometer

Significant enlivement of road transport

2005: +1.1 %2006: +7.3 %2007: +8.0 %2008: +5.3 %2009-2011*: +3.1

* Forecast.

Quelle: BVU/BMVBS

Until the year 2025 long distance roadtransport should increase by 84 per cent, short-haul road transport should grow by

11 per cent. (Transport Performance)

70

10,0 13,3 15,319,3

24,0 24,528,2

33,56,0

5,34,8

5,9

6,5 6,8

9,0

12,0

5,04,4

7,5

9,2

11,5 12,1

13,8

16,5

0

10

20

30

40

50

60

1993 1995 1997 1999 2001 2003 2005 2007

CV parts industry

Trailers and bodies

CV manufacturers

21,0 23,0

27,6

34,4

42,0 43,4

51,0

62,0

GermanyTurnover of the German Commercial Vehicle Industry

in b

illio

neu

ro 2007/1993: +195%

2007/1993: +195%

Source: VDA statistics

71

GermanyEmployment Situation in the German CV Industry April 2008 *

In Germany 2.5 million jobs depend on the production,sales and use of commercial vehicles.

Source: VDA statistics

car manufacturers 538,80071.3%

CV industry217,00028.7%

CV parts industry 91,100

Trailers and bodies42,500

CV manufacturers 84,400

* Data in brackets: april 2008

(532,800) 207,700)(39,200)

(87,100)

(81,600)

72

191.880

269.798

220.447

128.852

173.719

139.510

177.320

237.513

167.797

295.238

390.433

267.007

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

Manufacturing industry Automotive industry total Commercial vehicle industry

1995 19992003 2007

Productivity trend in the German industry– Turnover per employee –

Turn

over

in e

uro

per e

mpl

oyee

Source: VDA statistics

2007/1995: +91%

2007/1995: +91%

2007

/1995

: +12

5%

2007

/1995

: +12

5%

2007

/1995:

+129%

2007

/1995:

+129%

The productivity in the German commercial vehicle industry rose above-average.

73

194.161

124.706

65.185

187.075

302.513

408.049

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

450.000

CV manufacturers Trailers and bodies CV parts industry

1995 1999 2003 2007

Produktivity rise in the German commercial vehicle industry– Turnover per employee –

Turn

over

in E

uro

per E

mpl

oyee

Source: VDA statistics

High productivity by manufacturers and strong increase concerning parts.

2007

/1993

: +11

0%

2007

/1993

: +11

0%

2007

/1993

: +14

3%

2007

/1993

: +14

3%

2007/1993: +187%

2007/1993: +187%

74

28,611

30,968

35,044

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

36,000

1997 2002 2007

Production value trend oftrucks and semi-trailer trucks in Germany

aver

age

valu

epe

r sem

i-tra

ilert

ruck

in e

uro

Source: VDA statistics

Rising standards for environment and security lead to a pronounced qualitative growth (2007/1997: +32%),

but increasing share of vans beat down the average value

75

Trend of production value ofbuses in Germany

aver

age

valu

epe

r bus

in e

uro

Source: VDA statistics

179,530

206,497

251,140

0

50,000

100,000

150,000

200,000

250,000

300,000

1997 2002 2007

Rising standards for environment and security lead to a pronounced qualitative growth (2007/1997: +40%)

76

7,9

1,3

5,8

10,0

2,2

8,3

12,6

3,1

11,1

19,1

5,7

16,2

0,0

5,0

10,0

15,0

20,0

25,0

CV manufacturers Trailers and bodies CV parts industry

1995 1999 2003 2007

GermanyExports of the German Commercial Vehicle Industry

in b

illio

neu

ro

2007/1995: +338%

2007/1995: +338%

2007

/1995

: +14

2%

2007

/1995

: +14

2%

2007

/1995

: +17

5%

2007

/1995

: +17

5%

Source: VDA statistics

77

Germany: Foreign Trade Balance of the Commercial VehicleIndustry* in 2007: 11.1 billion € (+12%)

in b

illio

neu

ro

*Overall commercial vehicle exports - imports (excl. used vehicles)

1.120.873

1.097.123

794.636

581.851

366.476

280.733

243.798

657.330

769.188

541.377

118.729

183.742

0 200.000 400.000 600.000 800.000 1.000.000 1.200.000

France

United Kingdom

Spain

Italy

Poland

Czech Republic

Romania

Russia

Africa

NAFTA

Latin America

China

Source: Destatis, VDA statistics

78

Freight Transport in Germany until 2050

79

Freight Transport in the EU-27 until 2030

80

Germany – share of empty kilometers in all kilometersdriven of German lorries

source: Bundesamt für Güterverkehr

28.628.2

27.6

26.625.9

24.7

23.622.7

21.9

20.820.1

19.6 19.4

15

17

19

21

23

25

27

29

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

%

81

Germany tax burden of a 40-tons-truck-trailer-combination per year

source: BGL

(Euro II with air suspension, German inland transport) vehicle kilometers per year: 135.000 km; fuel consumption: 34 l/100 km

Source: EC-Commission, EC-Member States, BGL* date: august 2004** date: january 2006 (in B, L, PL on sulfur reduced diesel; in D, H, NL on sulfur free diesel; in DK including CO2-tax*** with consideration of petroleum tax reduction on commercially used diesel in B=3,64 cent/l, in F=2,5 cent/l

82

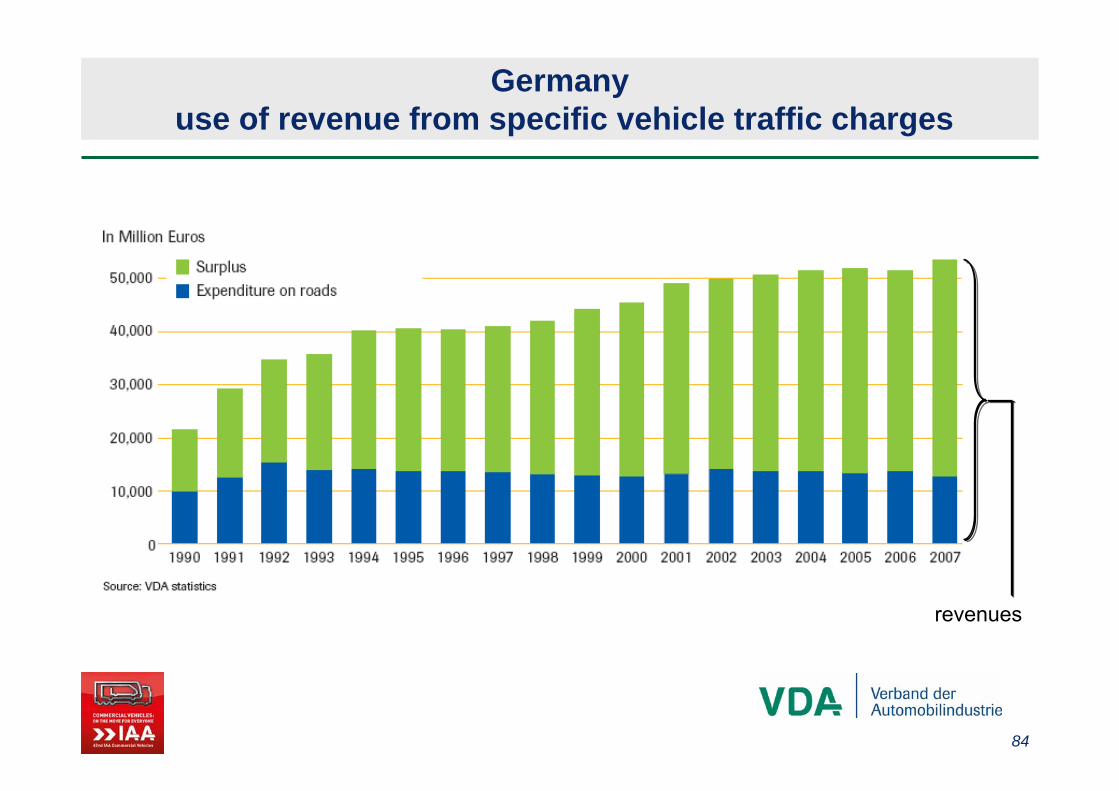

Germany – truck toll substitutes tax financing(origin of highway investment)

3,8 3,8 3,8 3,63,1

1,4 1,3 1,1 1,3 2,2

4,44,2

4,7 4,7 4,74,9

0

1

2

3

4

5

6

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Bill

ion

€

road chargetax

(liability) (plan)

5,2 5,14,9 4,9

5,3

§ 11 toll act

The... toll revenue is subjected in addition to the public budget for transport and iscompletely earmarked for improving transportinfrastructure, mainly for highways.

83

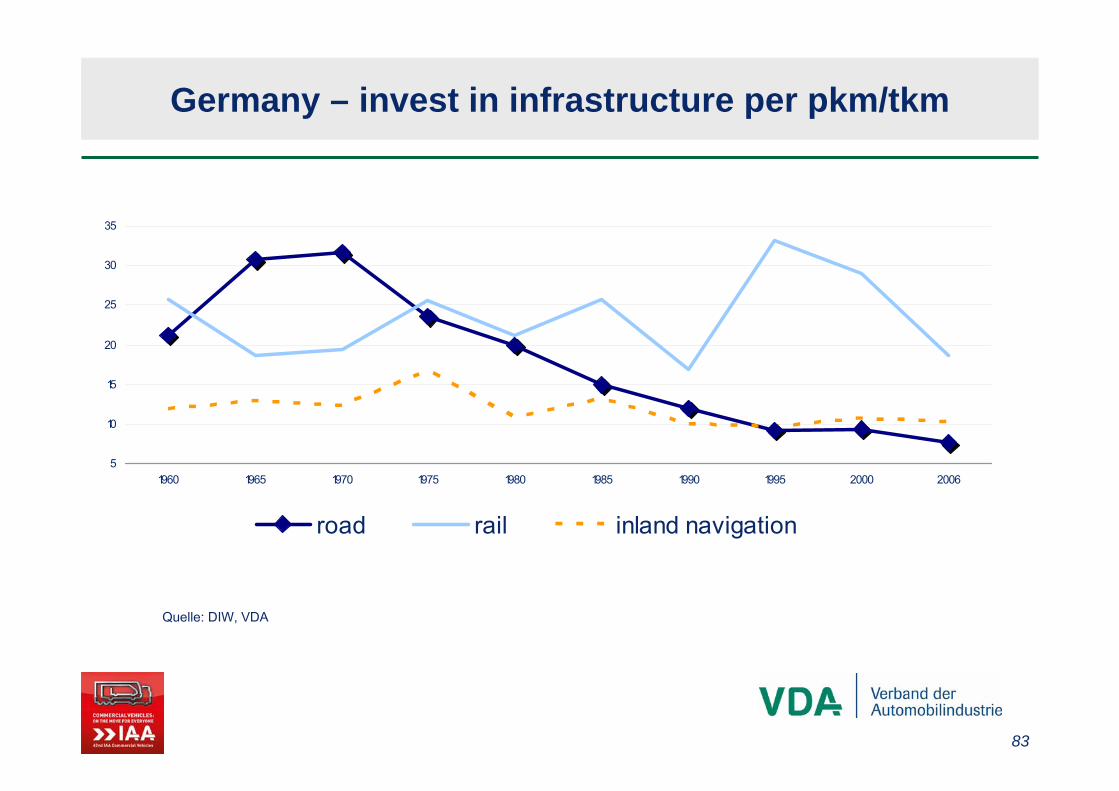

Germany – invest in infrastructure per pkm/tkm

5

10

15

20

25

30

35

1960 1965 1970 1975 1980 1985 1990 1995 2000 2006

road rail inland navigation

Quelle: DIW, VDA

84

Germany use of revenue from specific vehicle traffic charges

revenues

85

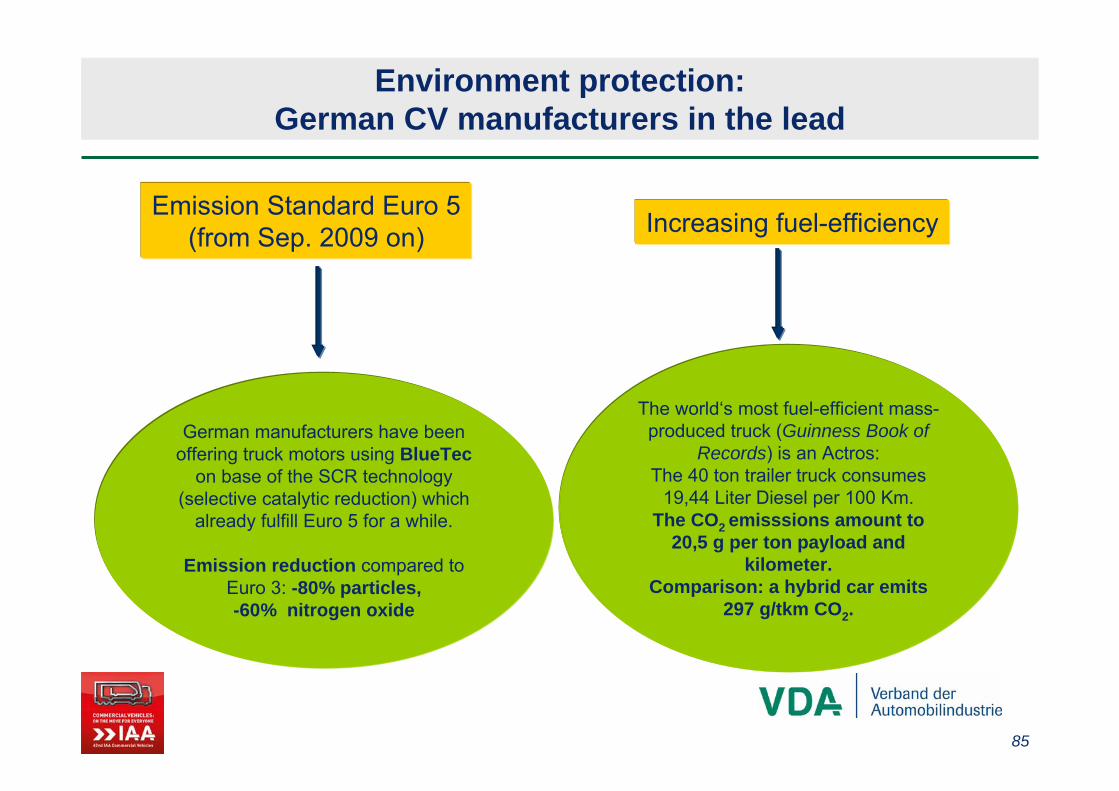

Environment protection: German CV manufacturers in the lead

German manufacturers have beenoffering truck motors using BlueTec

on base of the SCR technology (selective catalytic reduction) which

already fulfill Euro 5 for a while.

Emission reduction compared to Euro 3: -80% particles, -60% nitrogen oxide

Emission Standard Euro 5(from Sep. 2009 on) Increasing fuel-efficiency

The world‘s most fuel-efficient mass-produced truck (Guinness Book of

Records) is an Actros:The 40 ton trailer truck consumes

19,44 Liter Diesel per 100 Km. The CO2 emisssions amount to

20,5 g per ton payload and kilometer.

Comparison: a hybrid car emits297 g/tkm CO2.

86

Development of Exhaust Gas Emissions for Heavy Commercial Vehicles

With the upcomingEuro V emission

legislation since 1990 harmful emissions arereduced by 88 per cent

on the average.

87

Development of Exhaust Gas Emissionsof ligth commercial vehicles

With the upcoming Euro 5 emission legislation since 1990 harmful emissions are reduced by 97 per cent on the average.

Source: VDA

88

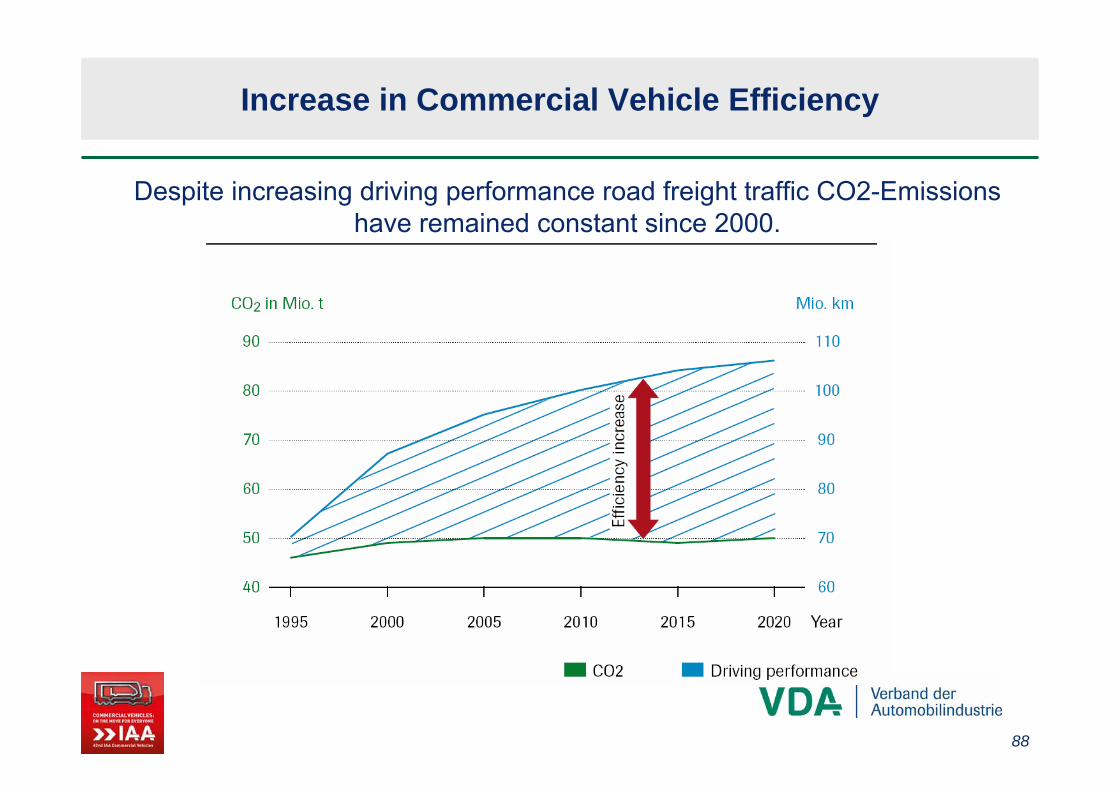

Increase in Commercial Vehicle Efficiency

Despite increasing driving performance road freight traffic CO2-Emissions have remained constant since 2000.

89

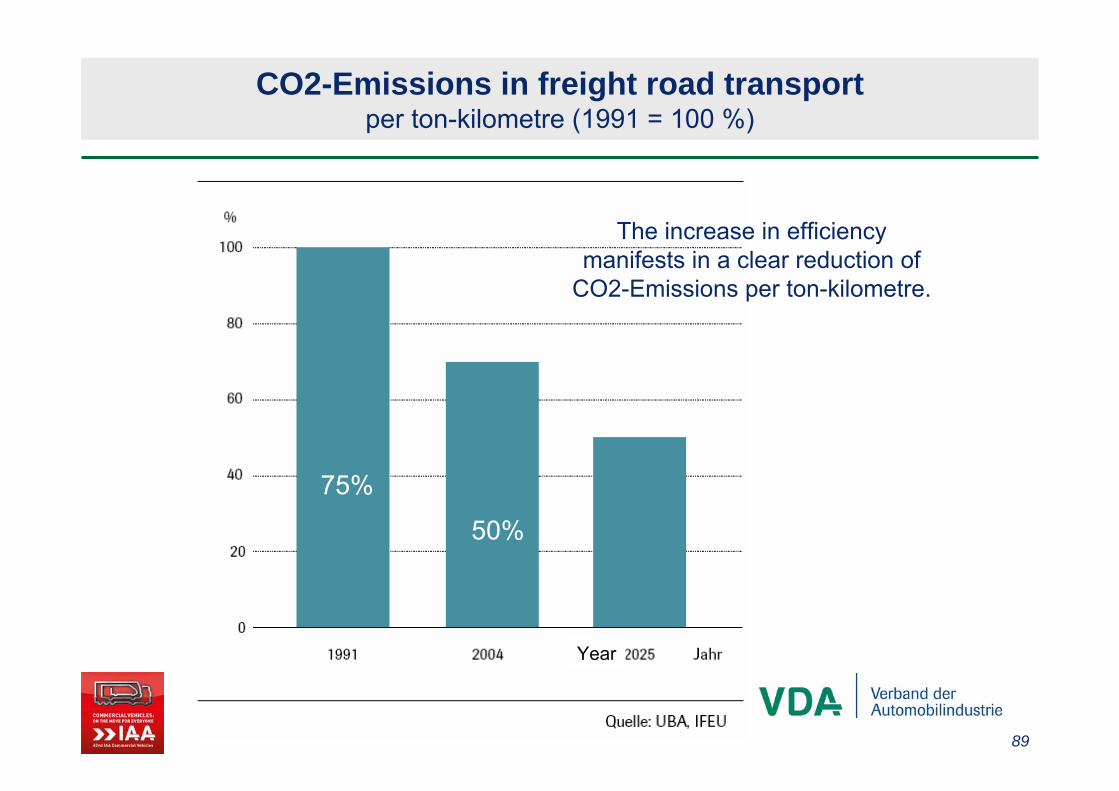

CO2-Emissions in freight road transportper ton-kilometre (1991 = 100 %)

The increase in efficiencymanifests in a clear reduction of

CO2-Emissions per ton-kilometre.

100%

75%

50%

Year

90

Development of CO2-Emissions of light commercial vehicles

Today a van consumes one thirdless than as recently as 1980

91

CO2-Emissions per ton-kilometre depending on average loadfaktor

Because of the fact that each carrier today isoptimally utilised in the market, big shifts fromroad transport to other carriers are not expected.

92

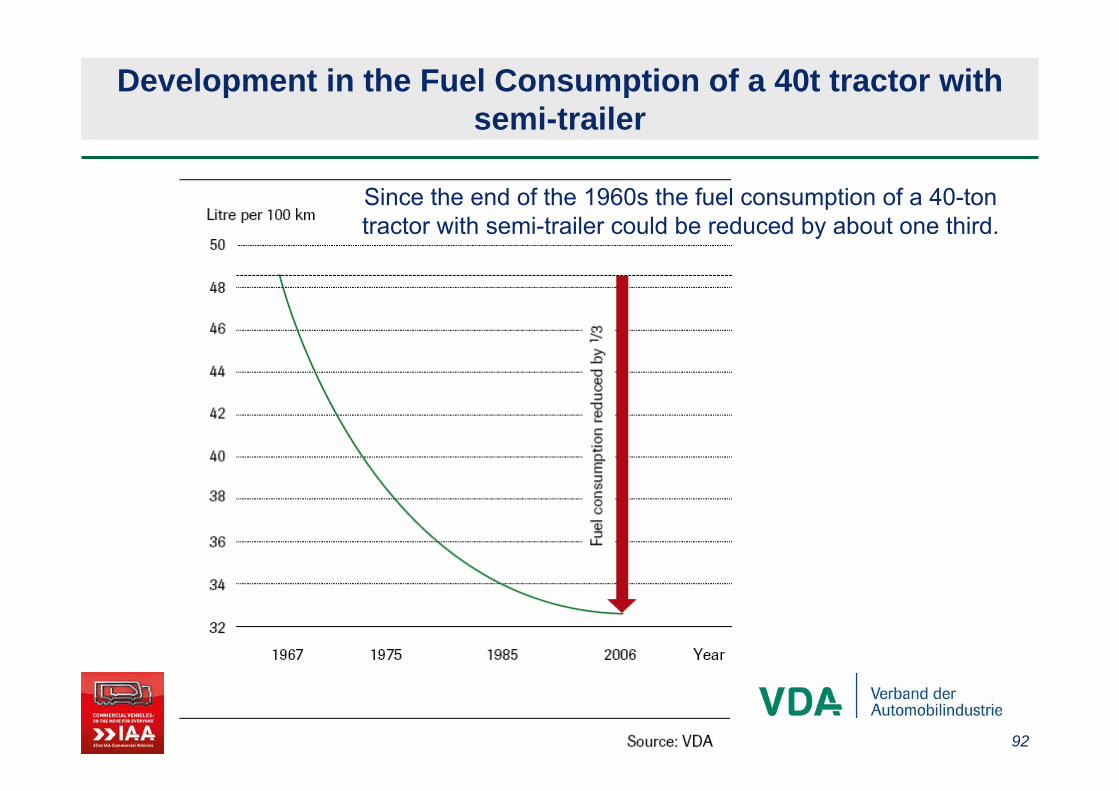

Development in the Fuel Consumption of a 40t tractor withsemi-trailer

Since the end of the 1960s the fuel consumption of a 40-ton tractor with semi-trailer could be reduced by about one third.

93

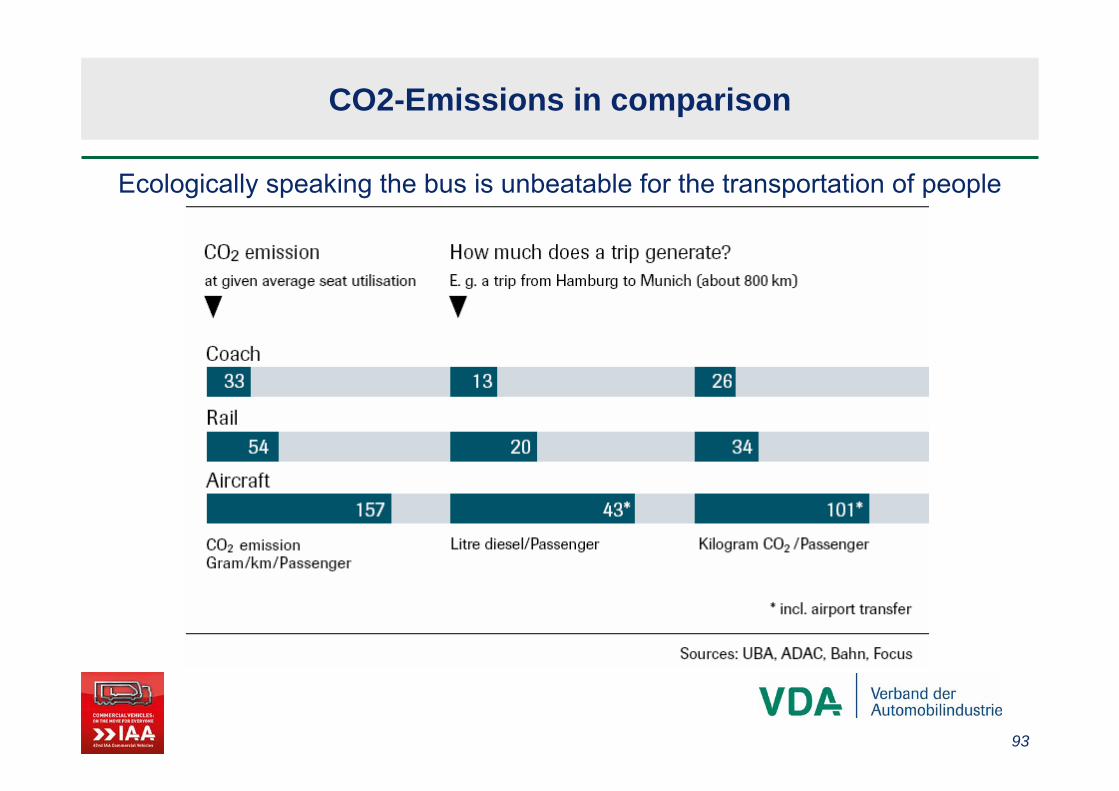

CO2-Emissions in comparison

Ecologically speaking the bus is unbeatable for the transportation of people

94

Buses by Euro Categories in Germanyparc new registrations

Source: VDA statistics, Kraftfahrt-Bundesamt

66%

49%

26%

32% 31%29%

2%

20%

31%

0% 0%

9%

0%

10%

20%

30%

40%

50%

60%

70%

1.1.2002 1.1.2005 1.1.2008

not reduced Euro I/II Euro III Euro IV/V

98%

5%2%

0% 0%1%

94%

60%

12%

5%

0% 1%

36%

87%

95%

0%

20%

40%

60%

80%

100%

2000 2003 2006 2007 1.H.2008

95

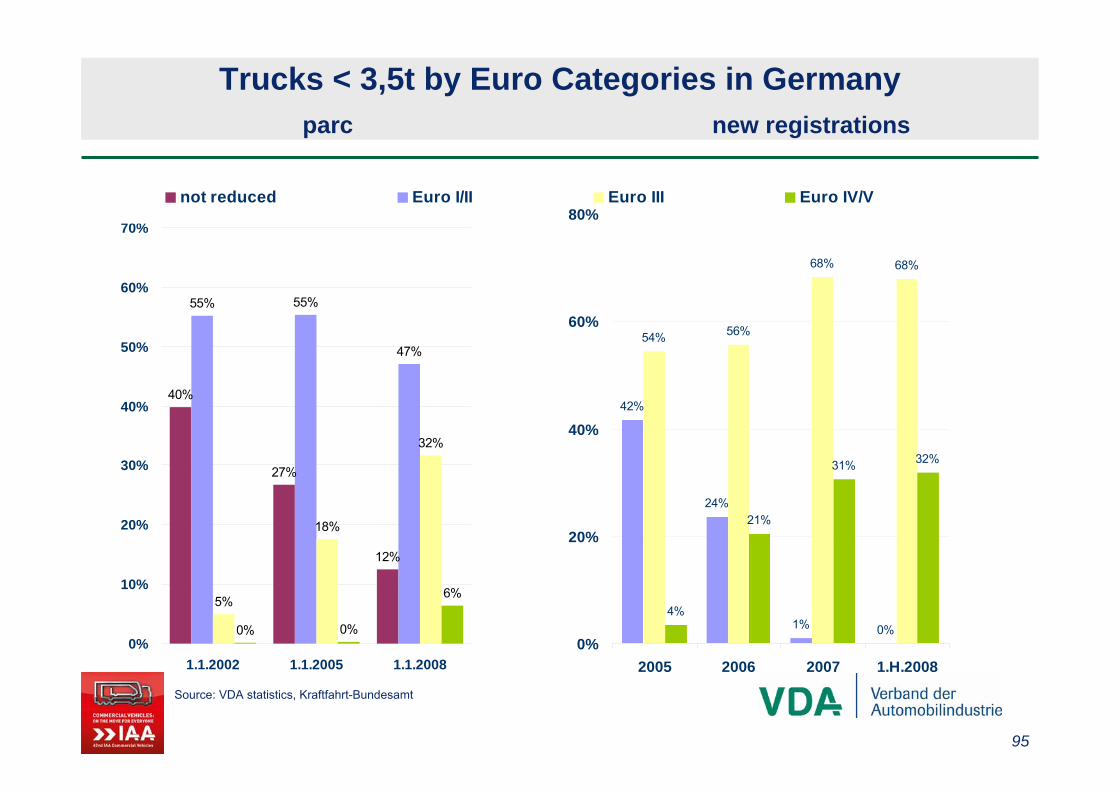

Trucks < 3,5t by Euro Categories in Germanyparc new registrations

Source: VDA statistics, Kraftfahrt-Bundesamt

40%

27%

12%

55% 55%

47%

5%

18%

32%

0% 0%

6%

0%

10%

20%

30%

40%

50%

60%

70%

1.1.2002 1.1.2005 1.1.2008

not reduced Euro I/II Euro III Euro IV/V

42%

24%

1% 0%

54% 56%

68% 68%

4%

21%

31% 32%

0%

20%

40%

60%

80%

2005 2006 2007 1.H.2008

96

Truck parc by Euro Categories in Germanytrucks 3,5 – 12t * trucks over 12 t *

38%

34%

28%

22%

40%37%

34%32%

22%

28%

33% 33%

0% 0%1%

9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1.1.2005 1.1.2006 1.1.2007 1.1.2008

not reduced Euro I/II

Source: VDA statistics, Kraftfahrt-Bundesamt* incl. truck tractors

16%13%

9%6%

38%

31%

22%

39%

0%2%

9%

45% 47% 47%50%

25%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

1.1.2005 1.1.2006 1.1.2007 1.1.2008

Euro III Euro IV/V

97

1% 0% 0% 0%

96%

7%4%3%

17%

84%

72%

0% 1%

9%

24%

81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 1.H.2008

Euro I/II Euro III Euro IV Euro V

Registrations by Euro Categories in Germanytrucks 3,5 – 12t * trucks over 12 t *

Source: VDA statistics, Kraftfahrt-Bundesamt* incl. truck tractors

82%

56%

2% 0%

5%9%

30%

24%

9%

33%

68%

75%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 1.H.2008