ground control - caspianmedia.caspianmedia.com/document/aa930409c62985e3b... · bhbi’s triple...

TRANSCRIPT

T h e m a g a z i n e o f t h e C h a r t e r e d I n s t i t u t e o f I n t e r n a l A u d i t o r s

I s s u e 1 2 J u l y / A u g u s t 2 0 1 3

Fair dues: why it’s important to keep up to date on discrimination Too close for comfort: how to manage potential conflicts of interestAin’t misbehavin’: do hotlines for whistleblowers really work?

Kevin Goulding, group head of internal audit at Dublin Airport Authority, on flights, finance, security and duty-free shopping

Ground control

If you hold the CMIIA Award or the PIIA Award already, take the fast track route to enhanced CPD and further qualifications and achieve:

• TheCMIDiplomainStrategicManagement&Leadership

• CharteredManagerstatus

If you’re just starting out in your career in auditing you can study for your professional qualifications with BHBi and have the Triple Qualification built into your training!

Thiswillhelpyoubecomemoremarketable,enhanceyourcareerprospectsandgainaccesstoprofessionalnetworkswhilstalsodemonstratingahighlevelofstrategiccompetenceandauditandmanagerialprofessionalism.

For a confidential discussion on how BHBi can help you achieve more from your professional auditing qualification contact:

Mark [email protected]

Paul [email protected]

Are you a professional internal auditor holding either the IIA Diploma (PIIA) or IIA Advanced Diploma (CMIIA)?

Are you just starting out in your career in audit?

PREMIER PRACTICE

Ifso,contactBHBitofindouthowtheBHBi Triple Qualificationcouldhelpyouincreaseyourprofessionalstandingandbecomemoremarketable.

BHBi’s Triple Qualification comprises of:

• CMIIA/PIIAAward

• CharteredManagementInstitute(CMI)Level7DiplomainStrategicManagement&Leadership

• CharteredManager(CMgr)status

BHBi has been quality assured and assessed by the CMI to offer the fast track route to enhanced, continued professional development. Offering a wide range of practical professional resources, CMI membership will not only enhance your employability, but help take your professional practice to the next level and beyond.

www.bhbi.co.uk/triple-qualificationCharteredManageristhehigheststatusthatcanbeachievedinthemanagerialprofession.AwardedonlybyCMI,itisrecognisedthroughoutthepublicandprivatesectors,acrossallmanagementdisciplines.

4761 CMI Ad Audit Risk AW.indd 1 17/04/2013 12:52

Contents

Front3 the IIA view From the chief executive, Ian Peters.

5 World view From Richard Chambers, IIA Global president and CEO.

7 View from the top From Malcolm Zack, head of internal audit at Post Office Limited.

8 Update The latest news affecting the profession.

10 Conference preview What to look forward to at the IIA’s annual conference.

12 reportage The findings of the 2013 Eversheds Board Report.

FeAtUres14 Holiday maker Kevin Goulding, group head of IA at Dublin Airport Authority, on local traffic and global duty free.

18 on the level Why organisations must keep up with shifting views of discrimination.

22 What planet are you on? What the audit universe means for you.

24 Conflict resolution Conflicts of interest are hard to spot and can prove expensive to resolve.

28 Good call? Whistleblowing hotlines are cheap and popular. But do they work?

reGULArs32 tools for the job How to improve the way you communicate the value of internal audit.

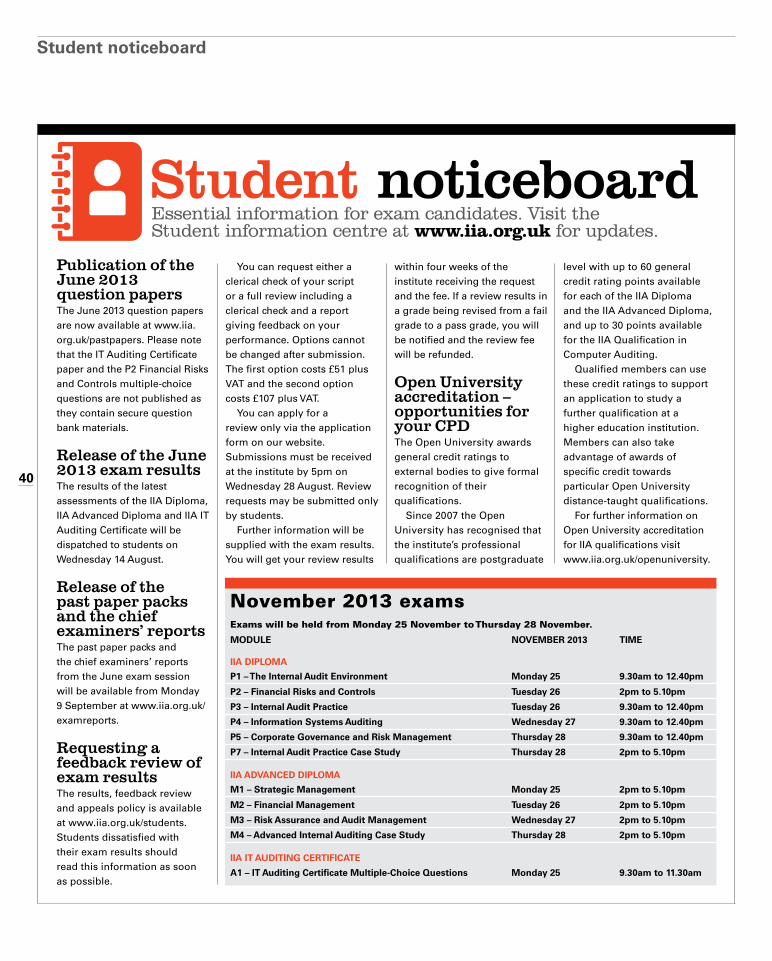

33 Career development Top tips for creating a new IA function from scratch.

34 You asked us Experts answer readers’ technical questions.

36 IIA update Institute news and membership matters.

38 Courses and events Key training dates.

40 student noticeboard Essential information for exam candidates.

18

22

28

We post more news and articles online every week. To access these, visit www.auditandrisk.org.uk

Published for the Chartered Institute of Internal Auditors

by Caspian Media Ltd, Unit G4, Harbour Yard, Chelsea

Harbour, London SW10 0XD020 7045 7500

Editors Keith Ryan

[email protected] 020 7045 7543

Ruth Prickett [email protected]

020 7045 7572

Chartered Institute of Internal Auditors

[email protected] 020 7498 0101

Subscriptions

[email protected] 020 7498 0101

AdvertisingIan Mehrer

[email protected] 020 7045 7596

Creative directorNick Dixon

Opinions expressed by contributors are their own.

Reproduction in whole or in part without written permission

is strictly prohibited.

ISSN 2048-8408.

T h e m a g a z i n e o f t h e C h a r t e r e d I n s t i t u t e o f I n t e r n a l A u d i t o r s

I s s u e 1 2 J u l y / A u g u s t 2 0 1 3

Fair dues: why it’s important to keep up to date on discrimination Too close for comfort: how to manage potential conflicts of interestAin’t misbehavin’: do hotlines for whistleblowers really work?

Kevin Goulding, group head of internal audit at Dublin Airport Authority, on flights, finance, security and duty-free shopping

Ground control

14

TeamMate AM is the solution of choice for 90,000 auditors in more than 2,200 organisations world-wide. AM addresses key audit management functions such as risk assessment, scheduling, documentation, issue tracking and time reporting, enablingyou to standardise and streamlineyour entire audit process.

Increase Efficiency & Boost Productivity of your Audit Process

A Breakthrough inCompliance Management

TeamMate CM is focused on themanagement and testing of SOX,Basel III, Solvency II, IT Governance or any other set of internal controls. CM allows you to view and interact with controls through an innovative user-defined structure based on multiple Dimensions and Perspectives of data that leads to greater efficiencyand deeper insight.

The integration of TeamMate AM and TeamMate CM promotes leveraging and sharing of data and work�ows across the

Internal Audit and Compliance disciplines.

The Perfect Pairing

Learn more at TeamMateSolutions.com

View from the IIA

Bank vault a great leap for internal audit“The IIA is delighted to be able to announce the launch of the first code of guidance specifically aimed at enhancing the application of the institute’s international standards in the financial sector.”

Ian Peters, chief executive of the IIA.

Risk is an integral part of the financial services sector; it’s what makes money – and loses it. One common question during the financial crash of 2008 and the various problems that the sector has had with misselling, money-laundering and fraud has been “what were their internal auditors doing?”. Often, as Barclays’ head of internal audit Michael Roemer told us in the March/April issue of Audit &Risk, the answer to this is “quite a lot, actually”. However, internal audit is only as strong as the amount of credence it is given by the board. If you muzzle your guard dog then you can’t blame it for failing to bark at the burglars.

This is why the IIA is delighted to be able to announce the launch of the first code of guidance specifically aimed at enhancing the application of the institute’s international standards in the financial services sector. This is a milestone for the sector.

The guidance is based on the recommendations of an independent committee set up by the institute. The IIA has welcomed the recommendations and has published them in full, commending them to the sector.

It is being published at a crucial time in the history of financial services, as the sector is still working out the full implications of the report of the Parliamentary Commission on Banking Standards, which has suggested that senior bankers who are guilty of reckless misconduct should be sent to prison. The

Treasury welcomed this report and has promised to consider amendments to the banking bill to back it up with legislation.

Of course, the guidance alone, however helpful for internal auditors in the sector, cannot solve some of the key problems highlighted by the commission, namely that expectations of internal audit in the sector have been too low and that internal audit has not been able to play an influential enough role in supporting executives and non-executives in their responsibilities for managing risks and controlling the business.

This is why the real significance of the new guidance is that its primary target audience is not internal audit practitioners, but boards, audit committees and senior executives. Its recommendations should gain even greater force if senior executives realise that a strong internal audit function, with real access to core risk data and a voice that is heard loud and clear on the board, could help them to stay out of gaol if things go wrong.

The guidance should also help internal auditors to put their points across more consistently and forcefully. It is intended to give greater relevance to the IIAs international standards by ensuring that best practice internal audit is expected by boards

“The guidance should help internal auditors to put their points across more consistently and forcefully”

and audit committees and delivered by practitioners, consistently across the whole sector. The recommendations seek

to enhance internal audit’s role and influence by clarifying reporting

lines to the chair of the audit committee, demanding a broad scope and coverage for

internal audit so that the function decides for itself

what are the major areas of risk and establishing that no

area of risk is beyond its focus.Last, but by no means least, the

success of this groundbreaking new guidance could enable the institute to produce similar advice for other sectors in future. This is a new departure for us in an area that clearly needs improved support from our profession and touches all our lives, but tailored guidance to enhance understanding of the international standards could help internal auditors in a wide range of organisations.

If financial services institutions agree to set their guard dogs free, then the hounds can start to protect us all more effectively.

The full guidance can be found at www.iia.org.uk/policy/financial-services-initiative/

HAVE YOUR SAY Post your comments about this

article or any of the issues raised at www.auditandrisk.org.uk

3

Complete Audit Solution100 users

£500 per month

Prepare to be very, very impressedA 5 star product for a 1 star price

PlanPerform

AssignReport

Prepare the Audit, The Team, Location, Scope, Objectives, when , questions, notify users and add it to planners.

Assign questions to team members. Who can work offline to carry out the audit. Including attachment of supporting documents,scans or images.

Create remedial actions for issues that need to be resolved, give ownership and assign with an action by date and track to completion.

Produce an Audit report with the click of the mouse, including current state of actions, performance and statistics, everything for the audit committee

To find out more or to arrange a free trial visit:

www.symbiant.net/auditTrusted by names you know from charities to banks, government to PLC.

OF AWARD WINNING SOFTWARE

14Symbiant Management Suite - The total Audit solutionManagement Suite is a unique web based modular solution that allows the wholeworkforce to collaborate on Audit, Risk and Compliance issues.

IIA FP ad Template.indd 1 19/06/2013 10:40

View from IIA Global

Keep current guidance in a changing world“I’ve been reflecting on how the world has changed since the original COSO framework was published, how important that guidance became, and how resilient it has proven.”

Richard Chambers, president and CEO of IIA Global.

Responding to monumental changes in the way organisations conduct business, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) has updated its Internal Control – Integrated Framework for the first time in more than two decades.

As a member of the COSO board of directors, I’ve been reflecting on how much the world has changed since the original framework was published, how important that guidance became, and how resilient it has proven. The 1992 document remains the most widely used internal control framework in many countries. It is used throughout the world by leading international companies. It’s even referenced by the US Securities and Exchange Commission as a viable framework to evaluate and report on the design and effectiveness of internal controls over financial reporting.

When the original COSO framework was published, the internet was in its infancy. Facebook and Twitter were still a decade away – as well as a slew of corporate scandals that gave rise to the development of corporate governance legislation around the world. Internal auditing, outside the profession, was largely perceived as an accounting discipline.

Today, internal auditing cuts a much broader swath, drawing practitioners from a wider range of backgrounds, including engineering, communications and technology, to evaluate and improve the effectiveness of risk management, control and governance processes.

In the nearly 20 years since the inception of the original framework, business and operating environments have changed dramatically, becoming increasingly

complex, technologically driven and global in scope. At the same time, stakeholders are more engaged, seeking greater transparency and accountability for the integrity of the systems of internal control that support the business’s decisions and governance.

It is testament to the principle-based vision of the authors of the original framework that, despite these changes, the 2013 update, written by Pricewaterhouse-Coopers on behalf of the COSO board, does not refute the original framework. Instead it formalises the principles embedded in it and expands the discussion in the light of the different environment in which organisations are operating, taking into account issues such

as globalisation and increased expectations for governance oversight.

The 2013 framework addresses risks associated with technological advances, incorporates some of the lessons learned over the past decade about fraud, and emphasises that control is about more than just internal control over financial reporting.

COSO made a major step with this framework by expanding its applicability to operations and reporting objectives. This is especially important to internal auditors who are responsible for ensuring the effectiveness of governance and a variety of

internal controls in areas beyond finance. It

recognises that a system of internal control is all-encompassing.

One of the most noticeable differences is that

the 17 principles within the five components of internal control are

now spelled out. These principles clarify the requirements of effective internal control to facilitate designing and implementing a system of internal control and assessing its effectiveness. The framework also includes points of focus that highlight important characteristics relating to these principles.

COSO has also developed “Illustrative tools for assessing effectiveness of a system of internal control” offering templates and scenarios to help people apply the framework, and “Internal control over external financial reporting: a compendium of approaches and examples” offering practical approaches and examples to show how the framework’s components and principles can be applied when preparing external financial statements.

“When the original COSO framework was published, the internet was in its infancy.”

For Further inFormation richard Chambers writes a blog at

www.theiia.org/blogs/chambers and tweets at www.twitter.com/iiaCeo

5

Comprehensive Audit & Risk Management Software

• Modern screen design that operates globally over a range of network speeds without the restrictions of a browser interface• Flexible audit planning by entity structure & process• Home screen identification of items for your action and review• In-built audit methodology and audit report templates• Simple deployment and automatic software updates• Audit work can be focussed on risks identified from integrated risk registers

Pentana VisionGlobal audit management software

www.pentana.com/visionEnquiries: [email protected]

Call: +44 (0)1707 373335

IIA Audit & Risk Full Page July.indd 1 23/05/2013 16:56:35

View from the top

Diversity Strength in variety“Each person’s perspective is one window on a problem and having several perspectives means you can open those windows to produce effective solutions.”

Malcolm Zack, head of internal audit at Post Office Limited.

Internal audit had its roots in accountancy and finance, so it’s not surprising that many people in the profession are financially qualified. But what has changed over the quarter century that I’ve been working in the risk, audit and governance arena is the ever broadening remit of internal audit. The IIA in the UK and globally has consistently built, developed and upgraded internal auditing as a profession and a brand to be proud of.

As a head of function I have to be able to provide a view of risk and control across the business, so I cannot rely purely on the traditional source of internal auditors. In the three major organisations where I have headed the audit function, I have sought people with more diverse backgrounds, experiences, organisations and qualifications. Yes, one does need financial expertise at the core, but I could not meet my remit to the board without bringing in staff from other disciplines as well. This includes encouraging internal transfers from the business and, significantly, seeking IIA or CIA qualified staff.

Combining these skills can build a more rounded service. One of the best project auditors I have had so far in my teams was previously an experienced project manager, not an auditor. Their management skills were highly advanced and their experience juggling many demands as a project manager was an excellent grounding for running several audit projects simultaneously. When I was establishing a new team to focus on distribution and operations, I hired an experienced qualified internal auditor from outside the organisation, but also brought in a member

of staff from the business who was steeped in operations. While they knew little of internal audit, their controls and process background dovetailed well with the external hire so we could map business knowledge with risk and control expertise. Adding others with different sector experiences enabled the team to help the business move its control dial significantly.

Most of the teams I have worked with have been relatively small, but I have

been privileged to work with people from other countries who can bring different perspectives to these teams. Each person’s perspective is one window on a problem and having several perspectives means you can open those windows to produce effective solutions. Having a French man help a Peruvian on an audit in Sweden, and doing it all in English, is a bit of an eye-opener.

I joined the Post Office in October 2012 to set up its internal audit department following

its demerger from Royal Mail in April 2012. Post Office is undergoing an exciting and challenging transformational change across more than 11,700 branches – the

largest retail network in the UK. It’s a diverse organisation covering financial services,

telephony, insurance, mails, foreign exchange, mail services and government services, so the

risks are diverse too. Post Office is also keen to support diversity with

the aim of bringing in a range of thoughts and encouraging people from a

wide variety of backgrounds with different experiences to build change.

As the Post Office internal audit team develops, it will reflect those values. To meet the increasing expectations of the board, the internal audit team needs to be diverse in its thinking and capability. I will always need financial expertise in my audit teams, but it is essential to seek complementary strengths from elsewhere. A team that plays to its strengths will achieve much.

About the AuthorMalcolm Zack FCA MBA BCom is head

of internal audit at Post Office Limited. He was previously group audit director at the Brakes Group, vice-president head of operational review at Visa Europe, and held audit, risk and consulting roles at Sainsbury’s Kingfisher and the Burton Group (now Arcadia). He is a chartered accountant and a member of the IIA’s Audit Committee. The views expressed here are his own.

Having a French man help a Peruvian on an audit in Sweden, and doing it all in English, is a bit of an eye-opener

7

8

The Financial Reporting Council (FRC) has made “significant” changes to the UK’s external auditing regime through a revised standard.

The corporate reporting watchdog has issued a revised auditing standard (ISA 700) to enhance transparency in the auditor’s report by increasing communication with investors. External auditors reporting on companies that apply the UK Corporate Governance Code will be required to explain more about their work.

The FRC is also requiring boards to describe the work of the audit committee in annual reports and for the auditor to report if the board’s disclosures do not address matters it has communicated to the audit committee. Auditors will also have to inform the committee about significant audit judgments. The changes will affect audits of financial statements for reporting periods on or after 1 October 2012. The full survey report can be downloaded at http://bit.ly/13CLVZJ

There are 89 major Whitehall projects facing significant obstacles to implementation, according to a Cabinet Office review. The Major Projects Authority’s (MPA) review of the government’s 170 largest projects – together worth more than £350bn – used a traffic-light warning system to rank the schemes. Fifty-eight were rated “amber”, meaning successful delivery is “feasible”, but “significant issues exist requiring management attention”. The abolition of the Audit Commission is in this group.

A further 23 projects, including the Universal Credit single-benefit programme and the Department for Transport’s High Speed 2 rail programme to build a new line linking London to Birmingham, Manchester and Leeds, were rated “amber-red”, meaning successful delivery is in doubt. Eight schemes were “red”, where successful delivery appears “unachievable”. These included the rail franchising programme for the West Coast mainline, and a planned upgrade to the online application system for passports.

Cabinet Office minister Francis Maude said that reviews of major projects had helped to save taxpayers more than £1.7bn since the MPA was formed in 2011.”The report can be found at: http://bit.ly/1b0l2Bj

ILO: Lack of jobs will cause “lost decade”Soaring stock markets and higher profits have pushed up executive pay and left companies with cash, but they have failed to create jobs, according to the International Labour Organisation (ILO).

The United Nations (UN) agency’s annual World of Work report warns that the world’s advanced economies will suffer a “lost decade” of jobs growth, and that the risk of social unrest is rising as inequality worsens. This will be “a major global challenge for the years to come”.

The report predicts that employment rates in advanced economies will

not reach pre-crisis levels until after 2017, more than ten years after the global financial crash began.

A separate report by Eurostat, the statistics office of the EU, has found that unemployment in the Eurozone rose to 12.2 per cent in April. At 24.4 per cent, youth unemployment was double the wider jobless rate and up from 24.3 per cent in March. In Greece almost two-thirds of those under 25 are unemployed. In the UK the figure is 20.2 per cent. Read the ILO’s World of Work report at http://bit.ly/LIMqYg. Eurostat’s figures are at http://bit.ly/10MAtIX

We round up the latest business and regulatory news to affect the internal audit profession.UPDATE

AddITIOnAL nEWs, fEATuREs And VIEWs are posted online all the time. Go to www.auditandrisk.org.uk to see what’s new.

8

c-suite executives shift views on Risk Regulatory changes have caused 70 per cent of c-suite executives to make “substantial” or “moderate” changes to risk management and reporting processes in the past two years, according to a report by KPMG.

To see the report, visit http://bit.ly/Wn4GG5

fRC revises standard on audit reports

Whitehall has 89 “problem projects”

99

un waRns companies to engage moRe with disasteR Risk

HsBC hires ex-MI5 bossHSBC has hired former MI5 chief Sir Jonathan Evans to help Britain’s biggest bank clean up its act after US authorities fined it nearly US$2bn for acting as a conduit for Mexican drug money and breaking sanctions.

Evans will join as a non-executive director and will sit on HSBC’s financial system vulnerabilities committee.

Other banks have made high-profile hires to improve their regulatory compliance records. Barclays made Hector Sants, former CEO of the Financial Services Authority, its head of compliance and government relations, while Royal Bank of Scotland made Jon Pain, another former FSA director, its compliance chief.

The United Nations has warned that economic losses from disasters have spun out of control. It is calling on the world’s business community to incorporate disaster risk management into their investment strategies to avoid further losses. To read the latest Global Assessment Report (GAR13) by the un Office for disaster Risk Reduction (unIsdR), go to http://bit.ly/13dxZ1A

natuRal catastRophe Risk RepoRtZurich Insurance Group’s “Natural catastrophes: business risks and preparedness” survey has found that companies recognise the potential risks posed by natural catastrophes, yet still have insufficient mitigation plans. for more information, go to http://bit.ly/11Eb7M8

IT security standards setter ISACA has issued new guidance outlining key questions for boards of directors to ask to ensure their enterprise’s cloud initiative is in line with business objectives and the organisation’s risk tolerance.

According to the white paper, boards should ask whether management teams have a plan for cloud computing and if they have weighed the value and opportunity costs. They should ask how cloud plans support the enterprise’s mission; whether executive teams have properly evaluated “organisational readiness” so that cloud processes work alongside those already in place; and whether management teams have considered existing investments that might be lost in their cloud planning.

Lastly, boards need to ask whether the organisation has strategies for measuring and tracking the value of cloud return versus risk.full details: www.isaca.org/cloud-governance

Cloud governance: 5 questions for boards

nHs “will not achieve £20bn savings”, say fdsMost NHS finance directors think the health service will fail to meet its target of £20bn “efficiency savings” by 2015, according to a King’s Fund survey.

Of the 51 finance directors polled by the health think-tank, almost all (96 per cent) estimated that the risk of the NHS failing to meet its £20bn efficiency target was “50:50 or worse”.

In terms of patient care, 40 per cent of finance directors believe the quality in their area has deteriorated over the previous year, and more than two-thirds (69 per cent) said that the government’s reforms had had a negative impact on performance.

According to the King’s Fund, this pessimistic outlook reflects the degree of financial pressure the NHS is currently facing. Savings so far have come largely from staff pay freezes and cuts in management costs.

The survey was published alongside the King’s Fund’s latest quarterly monitoring report on the NHS. This showed that the number of people who have waited more than four hours in hospital accident and emergency departments has hit a nine-year high.Read the full report at http://bit.ly/15x8BeX

10

“Expect More – Harnessing The Power” is the theme of the 2013 IIA conference, which takes place on 11-12 September at One Wimpole Street in London. Internal audit is facing increasing demands as organisations struggle with economic challlenges, so speakers will focus on how it can make a real difference to business success.

This year’s conference features over 30 sessions led by experts from well-known organisations. In addition to the main talks, delegates can choose from a range of practical sessions, where they can get advice, find out about tried-and-tested approaches and make contacts. The free exhibition will also provide opportunities to find out more, while networking over tea and coffee.

Day oneThe first day focuses on risk management. Speakers will look at the ways in which internal audit departments need to transform themselves into key players by identifying problems before they happen and providing insights into the effective management of risk so they add value to the organisation as strategic advisers.

Roger Marshall, director of the Financial Reporting Council, will give the keynote session on expecting more from internal audit and how new guidance on IA in financial services can be harnessed in other sectors. He will be followed by David Law, group risk and compliance director at Tunstall

Healthcare Group, who will offer a strategic overview on the key risk-management challenges currently facing boards.

Armand Lumens, chief internal auditor at Royal Dutch Shell, will then take the stage to share tips for delivering the successes of internal audit to the executive board. He will examine how to ensure that decision-makers in your organisation focus on the right risks, how to engage effectively with management teams and ways to ensure that the decision-makers receive the information they need.

After lunch delegates will separate into a variety of practical sessions focusing on different aspects of how to scan the horizon to identify emerging risks for their business.

Day two Sessions on the second day will focus on broadening the role of internal audit to ensure it is relevant and seen to add value to the business. The morning sessions offer a strategic overview with leading HIAs giving their views on contributing to business strategy and business change.

Sally Clark, chief of administration in Barclays Internal Audit, will examine how to give expertise and business insight into strategic initiatives and the ways this enables internal audit to contribute to strategy.

Mark Fensome, director of group audit services at Tui Travel, will follow this with a session on how internal audit can deliver value during business change and suggest

ways to develop the internal audit strategy to look at change. The rest of the morning will be spent in practical sessions that allow participants to explore a variety of topics from the changing role of internal audit and effective interaction with other assurance providers to the internal audit skills that will be needed in the future.

The final afternoon will focus on the soft skills required by all internal auditors. One of the key issues is communication, essential both at strategic level and when dealing with management at operational levels. Session leaders will examine the role of internal audit as a key area for growing potential talent.

The conference will end on a positive note, emphasising the strength we gain from the unity of the internal audit profession. The final session will discuss how to work across cultures, how to work together as professionals and how internal auditors can come together for the 2014 International Conference in London.

For more inFormationVisit www.iia.org.uk/conference to

see the programme and book a place, or contact [email protected]. Book before 31 July for a discounted price of £635 plus Vat (members) or £835 plus Vat (non-members). if you would like to exhibit at, or sponsor, the conference, contact [email protected].

Conference preview

Businesses and stakeholders are demanding more of internal audit, so the IIA’s 2013 conference focuses on its power to make a difference in challenging times.

Harness the power

Expect more – harnessing the power

Internal audit has never been more challenging. Continuing economic uncertainty and emerging risks mean that internal auditors are working harder than ever.

By taking the initiative, internal auditors can enhance their role and become even more relevant to the business. Our conference will provide the strategic and practical sessions you need to broaden the role and success of internal audit.

Sessions for this year include:

s Expecting more from internal audit – new guidance for boards

s Risk management – the key challenges facing boards

s Delivering internal audit success to your executive

s Horizon scanning – how to anticipate and identify emerging risks

s Giving expertise and business insight into strategic initiatives

s Internal audit and business change – delivering value

IIA Annual Conference 201311-12 September 2013

Find out more at www.iia.org.uk/conference

BOOK BY 31 JULY

EARLY BIRDS SAVE!

12

REPORTAGERisk strategy is now higher on the board agenda and a board’s key challenge is how to balance growth and risk, according to the 2013 Eversheds Board Report. The report also highlighted that diversity has risen up the board agenda, 61% of directors saying that diversity on the board is key to good board performance.

There is more evidence of positive dialogue between shareholders and boards. The average AGM approval rating for executive remuneration packages was over 90%, except in the US where it was 80.5%.

Boards have got smaller

the average board size was

13.4 directors

In 2012 it was

12.3 directors.

8% decrease in the average number of

directors on the board over

the past five years.

In 2007

93% of board directors

believe that an effective board

should have fewer than

12 members.

Risk strategy

13

The research involved 542 of the world’s leading companies, including the top 100 companies in the UK, Europe and the US, over 120 Asia-Pacific companies, 50 Middle Eastern companies and 30 companies from Brazil. To request a copy of “Eversheds Board Report: The Effective Board” visit: http://bit.ly/YZtn6n.

60 is the average age of directors.58 is the average age of chairmen and CEOs of the top 50 companies.

Directors are staying in their roles for longer. The global average tenure of directors is 6.7years on the board – an increase of 13% in five years. There is a positive relationship between longer tenure and share price over three- and five-year periods.

Top challenges facing the board were:

of directors said that their board’s approach to risk had changed in the past two years and it is now higher on the board agenda.72%

Growth strategy

Economic climate Regulations

Directors’ views on the type of diversity that has the most effect on board performance:

49% cited experience and sector diversity

25% cited international experience and background

16% cited age and generation

10% cited gender

the overall average decrease. The largest decrease was in Europe (60%) and the smallest decrease was in Australia (8%).

The number of executives on boards decreased in all regions.

34%

The trend is to have fewer executive directors on the board. • In 2007 there were

3.2 executives to 10.2 NEDs.

• In 2012 there were 2.1 executives to 10.2 NEDs.

• The top 50 companies had 2.4 executives to 8.2 NEDs – 22.3%.

51%

thought that chairmen could enhance the way in which boards engage with different stakeholders.

50%

increase in the percentage of female directors on boards across all regions. However, this is from a low base. The largest increases were in Europe (156%) and in Hong Kong (133%).

14

The airline industry has been one of the hardest hit since the global economic crisis gained momentum. While passenger numbers are moving back up to pre-2008 levels globally, profit margins have narrowed for most, and the environment is set to remain challenging for some time, according to the International Air Transport Association, the major industry body.

Yet there are always some that buck the trend and succeed where others struggle. Dublin Airport Authority (DAA), which is state owned, but operates on a stand-alone commercial basis, runs Dublin and Cork airports and delivered a solid performance last year. Turnover increased by three per cent to €575m, while profits (excluding exceptional items) grew by 66 per cent to €43m. Group operating costs fell, while passenger numbers rose – 8.8 million passengers used the recently opened Terminal 2, which is driving the airport’s long-haul growth.

So far this year, the positive upturn looks set to continue and there are signs that even more people will be jetting to and from the Irish capital over the summer (see box on page 16).

Kevin Goulding, DAA’s group head of internal audit, is confident that the airports can cope with the projected surge in demand, and that the necessary controls

are in place to ensure that passengers have a smooth journey and that internal audit is

not run ragged. “Increased capacity and larger passenger numbers are always a risk issue, but the

opening of Terminal 2 a couple of years ago reduced those capacity risks,” he says.

Care of dutyBut Goulding’s internal audit team is working in a business that is far more complex than that of many airports. DAA has three strands to its operations. The most important and resource-intensive of these is running Dublin and Cork airports. In the past few years it has also developed a consulting arm that provides advice to airports that are, for example, planning to develop new terminals, facilities and business opportunities. Third, over the past 50 years, it has developed an enviable sideline in duty-free/duty-paid shopping with its retail business Aer Rianta International (ARI), one of the world’s largest airport

Holiday maker As the holiday season approaches, most people start thinking about a couple of weeks in the sun. But, as Kevin Goulding, group head of internal audit at Dublin Airport Authority, explains,the season brings more complicated challenges for those running airports.Words: Neil Hodge Photographs: Mark Nixon

Kevin Goulding: in numbers• 1998 to 2004 – senior internal auditor at Jefferson Smurfit Group plc (including secondments to the SAP implementation).• 2004 to 2011 – head of internal audit and risk management at Kingspan Group plc. • Jan 2012 to present – head of internal audit at DAA. • He is a qualified accountant with the Chartered Association of Certified Accountants and part of the IIA’s heads of internal audit service

15

“Increased capacity and larger passenger numbers are always a risk issue, but the opening of Terminal 2 reduced capacity risks.” { }

16

duty-free and duty-paid retailing companies with an interest in 24 airports in 14 countries.

During 2012 ARI generated profits of just over€€27m. It saw strong sales growth in the Middle East and in India, where annual sales at its Delhi Duty Free passed US$100m for the first time. ARI also opened its first Chinese stores in 2012 and has recently been selected as the preferred bidder for the duty- free business at Mumbai’s new Terminal 2, which means that ARI will be operating the key duty free outlets at India’s two main international gateways. This will give DAA a very strong position in one of the world’s most important growth markets.

As a result, Goulding says that internal audit’s work is increasingly involved with the way that the business is expanding internationally. “Bidding for duty-free contracts is big business for DAA and the organisation keeps an ear to the ground to find out when a new opportunity might become available. Our work involves providing assurance on financial statements. In order to win these contracts, the organisation has to give guarantees and provide sound financial forecasts on the amount of revenue and customers it can bring in. We need to check the information behind those figures,” he says.

His team will audit the activities of each ARI subsidiary every two to three years. “This process is complex for a number of reasons. First, it is a question of resources. We have a small team so we need to ensure that resources are deployed in the most effective way possible. The other issue is that many of the ARI operations are joint ventures, and we may need to agree a ‘right to audit’ with the other party. Added to that, joint venture partners may have their own internal audit teams and external auditors, so sometimes we can leverage off their work,” he explains.

Fully automaticAnother area of financial risk for internal audit relates to loss of revenue or “revenue leakage”. “The financial controls we have in place are robust and the business model we use has been established for a long time, so we are aware of the risk profile,” says Goulding. “However, some of our invoicing involves a degree of manual input and that is a concern. The business is trying to automate more of these processes, and internal audit is monitoring progress,” he says.

IT risk is already at the heart of his team’s work. “Our business is very IT-driven,” he says. “There are around 180 different types of IT system across the organisation; everything from the usual desktops to check-in terminals, CCTV, security scanners and arrival and departure monitors. We have identified about 25 of these as critical. We have to make sure that these systems will work and that there is a back-up process we can switch to very quickly if anything goes wrong. Business continuity is a major focus for us.”

To ensure that the risk of IT disruption remains low, internal audit has a policy of communicating the importance of “patch management” throughout the organisation.

“It is hugely important that everyone is using the latest – and safest – versions of software on their systems, so the IT department sends out communications notices to remind people to install the latest patches made available by software providers to get rid of any vulnerabilities,” he explains.

Developing high flyersGoulding believes that it is important for internal auditors to move into other departments in the organisation after two or three years. He also likes to “mix and match” his staff so that members of his team get to experience all aspects of internal audit work. “I don’t want people to be stuck looking at one area of work all the time, such as regulatory compliance. I want my team to be flexible and to experience the whole range of work that internal audit does so that they get variety, enhance their skills and can benefit the wider business if they move into another department in the organisation,” he says.

Goulding’s first dedicated internal audit role after qualifying was at paper and packaging company Jefferson Smurfit Group (now Smurfit Kappa), where he was mentored by a head of internal audit who constantly stove to make the function “best

Black box: the business figuresDublin Airport Authority (DAA) runs Dublin and Cork airports (Shannon Airport was ceded in December). In 2012 turnover increased by three per cent to €575m, while profits (excluding exceptional items) grew by 66 per cent to €43m. Group operating costs were slashed, running at eight per cent below 2008 levels when Dublin Airport was operating with only one terminal.Passenger numbers

at Dublin and Cork airports were up by 1.6 per cent – equating to 340,000 extra passengers – while the number of long-haul passengers travelling through Dublin Airport grew by 16 per cent, owing to new capacity on routes to the Middle East and to North America. About 10.3 million passengers used Terminal 1 at Dublin Airport in 2012, while 8.8 million passengers used the

recently opened Terminal 2, which is

driving the airport’s long-haul growth.

In the first three months of 2013 passenger numbers at Dublin were up four per cent and eight new services have started flying since the start of the year. The airport has secured new transatlantic capacity so that 224 flights a week will operate during the peak holiday season.

“Bidding for duty-free contracts is big business for DAA and the organisation keeps an ear to the ground for new opportunities”

17

in class”. “That experience shaped the way that I think about internal audit a lot. My then boss always looked at what value internal audit could add to the business and he put a strong emphasis on having different skill-sets, and I share exactly the same view,” he says.

He took up the role of group head of internal audit at Dublin Airport Authority (DAA) in January 2012. Before this he spent over seven years at Kingspan Group, which provides environmental, construction and renewable energy products. He enjoyed this job, which included setting up the internal audit and risk-management functions, but a seven-week spell in hospital after a routine appendix operation went wrong and nearly killed him put the constant travelling into perspective.

“Around 96 per cent of Kingspan’s business was outside Ireland, so my work involved a lot of air travel. I felt like George Clooney’s character in the film Up in the Air – I always seemed to have a bag packed and I was constantly living out of a suitcase, collecting air miles and hotel booking points. My near-death experience put my lifestyle into perspective, and I thought I’d look for a new challenge that kept me close to home,” he says.

One of Goulding’s first tasks when he took charge of the internal audit function at DAA

was to make personnel changes within the existing staff. “Over the previous three to five years some of the more experienced internal auditors had left the organisation to take up opportunities outside DAA. They had been replaced by personnel from other parts of the business with less traditional auditing experience, but with a great knowledge of the operation,” he says.

“While their technical knowledge of the business was a huge asset, some of the team did not have all the requisite formal audit training and qualifications. Some of them had also been moved into the audit function temporarily and had stayed in the team longer than originally planned, so it was time to find new roles for them in the business. My approach is that the internal auditing department should be a springboard for new talent whereby recently trained and qualified auditors are brought into the organisation, and then move out into the business after about two years in audit,” he explains.

The redeployment took longer than expected, but Goulding says that he now has a team of five, including four qualified internal auditors. He is currently looking for an IT audit manager plus another internal auditor to focus on the international side of the business. This will make the team “about the right size for the organisation and quantity of work that we are doing”, he says.

His longer term plans could also involve internal audit working more closely with external teams. While he does not have a co-sourcing arrangement in place with any third-party provider at present, he concedes that he may look more closely at this option as the international side of the business grows. This could be particularly useful where the team needs local language skills, he points out. He also wants to build up the relationship internal audit has with external audit for “their shared mutual benefit”.

“In my last role at Kingspan we carried out a number of joint audit assignments across the US business with the external auditor so that skills and experience were pooled and costs were reduced. In effect, for certain locations I ensured that the requirements of the external audit programme were fully covered by the internal audit programme and that work papers were robust enough to be relied on by external audit,” he says.

“It is more difficult to create that relationship here because external audit is statutory, there are issues surrounding independence and safeguards would need to be established. However, there can be real benefits from sharing certain work to minimise duplication of effort and to ensure there is sufficient leverage off internal audit work,” he adds.

18

What is discrimination? It depends on what the law says – and on what your staff and customers think it is. New legislation can lead the way by prompting organisations to change the way they act and imposing penalties on those seen to be discriminatory, but it is not the whole story. Diversity and discrimination are two sides to the same coin and the opportunities as well as the risks continue to evolve.Words: Alice Hoey Illustration Paul Blow

“Despite the changes so far, UK laws may not yet have caught up with society’s desire for equal opportunities”

ON the level

The UK has had laws to protect individuals from discrimination on the basis of gender and race since the1970s

19

When the new Mental Health Discrimination Act came into force in April 2013, it changed relatively little – most significantly for businesses, it revoked a previous provision that prevented people from serving as company directors on account of their mental health problems – but it was symbolic. It addressed the last significant type of discrimination in our society today, mental health.

The UK has had laws to protect individuals from discrimination on the basis of gender and race since the 1970s, with protection expanded in the 1990s to include disability. Since the turn of the century, religion or belief, sexual orientation and age have also been added to the legislation.

The most significant legislative change, however, was the introduction of the Equality Act 2010, which brought all the discrimination laws under one statute and gave them equal weighting. It also expanded existing protection to include marriage and civil partnership, pregnancy and maternity, and gender reassignment.

Developing diversityDespite the changes so far, UK laws may not yet have caught up with society’s desire for equal opportunities. “There is, for example, some recognition by the public that discrimination based on factors such as social class exists,” says Dan Robertson, diversity and inclusion director at the Employers Network for Equality and Inclusion, “but the legislation on this issue is absent”.

The debates over diversity are far from over and can evolve

quickly. London’s prestigious Imperial College recently withdrew its offer of a short internship in its science labs from a fund-raising auction at Westminster School after there was an outcry on scientific blogs and among its own students, who protested that internships should be available only on merit, not for A-level students with the richest parents.

Similar concerns have been raised more broadly about unpaid work placements in large organisations, which are seen to give an advantage to people whose parents are willing and able to support them while they work.

Meanwhile politicians, church leaders and pressure groups across Europe have been hotly debating the issue of whether gay couples should be allowed to marry – the first French same-sex couple married in May, while the UK and German governments are struggling to find solutions that are acceptable to groups with strongly held opposing views.

Other nations also influence the development of UK legislation, says Karen Jackson, a partner at DID Law, which specialises in disability discrimination and workplace health issues.

“Some Scandinavian countries have taken the lead on the issue of gender equality in the boardroom. In Denmark, for example, they now have quotas as part of their effort to even out the gender balance at the top levels of large companies,” she says. The US tends to be at the extreme end of the curve. “For example, it has legislation protecting against genetic discrimination, where an

s

“Despite the changes so far, UK laws may not yet have caught up with society’s desire for equal opportunities”

employee is tested for a predisposition to genetic disease.” This issue may become more important in other countries if such tests become more widely available.

The ability of digital channels such as Facebook and Twitter to enable people to express discriminatory opinions – or tell ill-timed, insensitive jokes – is also affecting employers, who can be caught in the fall-out when staff hit the headlines. The recent appointment of Paris Brown, a 17-year-old hired as Kent’s first youth police and crime commissioner, fell apart when her silly, inflammatory tweets came to light. After several days of media attention and considerable embarrassment for the Kent police and crime commissioner who had hired her, Brown stepped down. The tweets were not seen as a criminal offence, but the authority was criticised for failing to check the candidate’s online media profile.

Emails can also provide evidence of discrimination. In the mid-1990s a woman who worked at a City bank brought a sex discrimination case against her employer and used personal email comments by colleagues and bosses as evidence. Few people were probably surprised at the time that some male bankers had sexist attitudes – but the case was notable for the way in

which it highlighted an emerging risk from internal emails.

But, according to Jackson, the UK government has little appetite to increase anti-discrimination protection at present.

She says that she has seen a fall in the number of claims relating to sex and race. “This is partly because the law around these has had longer to bite, but also because most employers are on side with these laws, understand them and provide diversity training around them,” she explains.

However, she is seeing more employment tribunals on the grounds of disability and age discrimination. This is unsurprising, she says, given the ageing population and the abolition of the default retirement age.

In future, she warns that organisations may need to pay more attention to other areas of discrimination that have had a lower profile in the past. “Religion and belief have had quite a high profile in the media, with cases such as Eweida v BA and the B&B owners who turned away a same sex couple hitting the headlines. Employers ought to be tuned into this,” she says.

Keeping step Internal audit plays an important role in ensuring organisations have the proper

procedures to assure against these risks. Most important, according to Alistair May, affiliate member of the IIA and head of internal audit at the Scottish Government, is assurance that the issues identified are being taken forward positively and that successful outcomes are achieved. “The key risk,” he says, “may be that the hoped for outcomes do not materialise, which would be particularly disappointing for both ministers and management.”

Discrimination has been a priority for the Scottish Government. “Most recently, following the Equality Act 2010, Scottish ministers made regulations placing specific duties on Scottish public authorities to enable the better performance of the public sector equality duty,” May says.

One legislative result of this focus was the offensive behaviour at football and threatening communications (Scotland) bill, which was passed in December 2011 and aims to tackle particular problems in Scottish football and society.

The Scottish Government is required to carry out an equality impact assessment when new policies are introduced. “As internal auditors, we are sometimes asked to provide advice on the development of new policies and this is one of the key areas

Court in the actWhat are the risks of failing to comply with equal opportunities and discrimination laws?

“One problem with anti-discrimination laws is that they can attract unscrupulous claims,” says discrimination lawyer Karen Jackson, who has defended many employers against employees who see a performance-linked dismissal as discrimination. “The best way for businesses to protect themselves is to ensure they have a thorough and well-documented policy but, more importantly, to police that in the workplace, crack down on unacceptable behaviours (especially among managers

who should be setting the tone) and provide regular training around the issues.” Training is essential, partly because people don’t always realise they are acting in a discriminatory way.

Businesses also need well-documented and fair HR procedures to back up their actions and decisions.

“It is alarming how often HR representatives make procedural errors that land their employers in hot water,” says Jackson. While this can be easily remedied with the right processes –

keeping a paper trail of documented meetings, phone calls and discussions – many organisations fail to

put these in place. “Employers often

can’t demonstrate that they considered a decision, because it happened during an informal chat between managers and HR and there is no record,” she says. While records such as file notes are useful, email should be limited because “it can leave a trail of incriminating evidence and employees can ask employers to provide data

about them under the Data Protection Act”.

Simple HR procedures, properly followed, can protect against claims of unfair dismissal on the basis of discrimination. For example, organisations must follow the right steps in the dismissal process – they shouldn’t go from a first informal chat to a dismissal without giving the employee warnings or help to improve. Witnesses at meetings are also a good idea, says Jackson. “In employment tribunal proceedings contemporaneous written evidence will almost always be preferred over an individual’s word.”

20

The ability of digital channels such as Facebook and twitter to enable people to express discriminatory opinions – or tell ill-timed, insensitive jokes – is also affecting employers, who can be caught in the fall-out when staff hit the headlines

we look at to ensure it is being addressed properly,” May says.

Legislative changes have not necessitated changes to internal audit procedures, because, May says, the government’s systems, processes and culture have evolved to reflect changes in attitudes and behaviours and new priorities. “For example, Scottish Government employees have a mandatory requirement to set a personal objective linked to diversity. This can be to do with working relations or conditions, developing processes or promoting policies. Some auditors can link their diversity objective to some of their audit assignment work where there is a natural alignment,” he explains.

Internal audit has had specific input in developing the Certificates of Assurance (CoA) process, he adds, which requires all deputy directors to complete a self-

assessment checklist. “The internal auditors were at the forefront in introducing the CoA process. This is now being reviewed and some of the diversity assurances it contains may need to be refreshed. We refer to these checklists in the course of related audit assurance work and look for evidence to support the self assessments declared.”

The up sideIt is easy to focus on avoiding the risk of discrimination and, ultimately, a legal battle. More positively, there are real benefits for organisations that embrace greater diversity.

“There are studies, specifically by McKinsey and Catalyst, that show a correlation between increased diversity and improved quality of decision-making, while a number of studies also link a higher representation of women on boards with

business performance,” says Robertson. “What’s more, treating people fairly has a positive impact on the ‘psychological contract’ and thus improves productivity and profitability. There are also benefits to being seen as an employer of choice,” he adds, pointing out that the post-baby-boom generations put a diverse workforce high on their wish-list for employers.

While most companies focus on discrimination as an employment issue, it’s worth remembering that in many cases a company’s staff are also its customers, local ambassadors and frontline communicators. One IT company in the US found that customers reacted better when they diversified their engineering teams by recruiting people from a wider range of backgrounds and training them internally. Sending people who reflected the range of people who worked in their customers’ offices, rather than a team entirely made up of white men who all had the same qualifications, meant that customers felt they could ask more questions and gained better service.

Supermarkets and DIY stores that have made an effort to recruit older staff have found that these employees are often better informed about products and more committed to their jobs than much younger staff, who see the job as a stepping stone to something else or a short-term option, although older workers may be less able to take on heavy physical work. Older customers often appreciate being able to talk to someone more like themselves who understands their needs.

You don’t need to spend much to ensure your company is an equal opportunities employer. The average cost of putting basic procedures in place is less than £1,000, according to the Employers Network for Equality and Inclusion.

As new issues come to the fore and attitudes in society shift, there is scope for further changes and emerging risks. Organisations and internal auditors need to stay on their toes.

21London’s prestigious Imperial College recently withdrew

its offer of a short internship in its science labs from a fund-raising auction at Westminster School after there was

an outcry on scientific blogs and among its own students who protested that internships should be available only

on merit, not for A-level students with the richest parents

One of the questions I am regularly asked in my professional and academic capacity is how I quantify my organisation’s internal

audit universe. To this my reply is usually: “Well it’s good to be an internal auditor rather than a scientist.”

Professor Brian Cox writing in the Wall Street Journal in April 2013 explained: “Quantum theory tells us that the universe we experience emerges from a bewildering, counterintuitive maelstrom of interactions between an infinity of recalcitrant sub-atomic particles.” Believe me, defining the internal audit universe is much simpler than that, although the principles may well be similar.

The definition of internal audit quoted in the International Professional Practices Framework (IPPF) gives us a clear steer that we should be concerned with an organisation’s operations; in other words, everything that our organisation encompasses and interacts with. In such terms, both the quantification of the scope of operations and their review clearly represents a massive task, but if we do not attempt to consider the entirety of the

whole, how can we decide where we should focus our attention?

So the issue becomes not “what is the size of the universe?”, as this is a simple if exhaustive exercise, but rather “what is the extent of the focus for our internal audit plan in strategic and operational terms?”. I therefore offer two views of how a head of internal audit might advise an audit committee over the components of the internal audit plans.

The increasing prominence of governance statements and the requirement for transparent reporting of significant risks provides guidance that what matters is the assurance needs of internal and external stakeholders. The aim of the board is to

deliver a clean opinion on the position of the organisation. It needs to

know whether internal audit is able through its periodic and annual reporting to deliver an assurance report that supports such a statement.

This should direct the focus of our internal audit

plan. Can we provide assurance opinions in relation to what the

board would not wish to report, presumably covering a triple bottom line of sustainability, corporate social responsibility and financial performance? We might consider this as the “corporate dashboard”.

22

If we do

not consider the whole, how can we decide where to focus

attention?

Professor Robin Pritchard explores the meaning of the universe in internal auditing terms.

What planet are you on?

A different way to approach this could be to look at where the board gets assurance from – this is a pre-requisite of governance codes and the IPPF (standard 2050). This requires analysis of the three lines of defence, in which inherent and residual risk are assessed, before management can provide assurance over the operation of procedures. At this stage we can assume that residual risk is likely to fall into one of three categories:

• Deep purple – an unacceptable level of risk remains, which is above the risk appetite of the board.• Purple – the level of risk exposure requires constant monitoring by executive management.• Violet – a level of risk that is unlikely to cause business disruption.

Such analysis of the risks can be transposed into three areas of internal audit activity. At the deep purple level management will implement solutions to bring risk exposure within the risk appetite of the board. Internal audit activity is likely to be of a consultancy or advisory nature.

In the purple area there is a control risk line where, if key controls failed, the organisation would be exposed to unacceptable or even catastrophic risk. This is where internal audit needs to provide assurance-based work as a third line of defence.

The violet area is likely to feature operational activity. Therefore some compliance audit may be appropriate to reassure the board about the continuity of control and to contribute to overarching opinions relating to control, governance and risk management.

The essential aspect of the internal audit plan is therefore risk-based, featuring not only the areas of perceived greatest risk, but also key controls within them. These will be the areas that the head of internal audit will recommend to the audit committee for attention, since this will directly support the governance statement. Areas where consultancy or compliance audit may be required are likely to be at the request of

executive or operational management. The significant question for heads of internal audit is, therefore, whether you are engaged with this level of strategic risk within your organisation. If so, do you have the appropriate level of resources and skills to deal with risk issues that will arise across the spectrum of activity that your organisation encounters? I believe that world-class internal audit teams are multidisciplinary and reflect the nature of the organisation, with audit staff also being appropriately trained in internal audit practice so that they can fully associate themselves with the fundamental responsibilities of the role.

We should therefore focus not on the whole universe, but on the most relevant aspects of it to help our organisations achieve objectives by delivering assurance that systems of control, governance and risk management are appropriate.

PROfessOR RObin PRitchaRd is head of the centre for internal

audit, Governance and Risk Management at birmingham city business school. he is chair of severnside housing and manages his own consultancy, Ra business services. for iia guidance on the audit universe visit www.iia.org.uk/audituniverse.

23

“World-class internal audit teams are multidisciplinary and reflect the nature of the organisation”{ }

categories of residual risk

Critical4

Major3

Moderate2

Minor1

AlmostNever

1

Unlikely

2

Likely

2

AlmostCertain

4

1 2 3 4

2 4 6 8

3 6 9 12

4 8 12 16

IMP

AC

t o

N b

Us

INe

ss

L IkeLIhooD of oCCUrrINg

Acceptable level of risk subject to regular monitoring

Risk management measures need to be put in place and monitored

Unacceptable level of risk exposure, which requires extensive management

24

Words: Peter Curtis

When the Financial Services Authority (FSA) fined fund manager Martin Currie £3.5m in 2012 for failing to manage a conflict of interest between clients, it was a sign of heightened regulatory scrutiny of asset managers’ approach to managing such issues.

In November last year, the FSA sent the chief executives of every UK asset manager a letter asking them to confirm that their firms had adequate conflict procedures in place. And, under the guise of the new Financial Conduct Authority (FCA), it is now said to be considering multi-million-pound fines for fund managers that use investors’ money to pay investment banks for access to the CEOs of their corporate clients (reportedly up to $20,000 an hour).

But conflicts of interest can occur in all types of organisation. For example, the Financial Reporting Council (FRC) recently announced two investigations into the audit arm of KPMG over possible conflicts. And last October the European Court of Auditors found that a number of EU agencies, including the European Food Safety Agency and

the European Medicines Agency, had failed to manage conflict of interest situations adequately.

Sources of conflictConflicts of interest can occur in a wide range of situations. They might involve a clash between an employee’s personal interests and those of their employer’s customer or stakeholder. Gifts and entertainment are obvious examples, whether it is a case of a head of procurement being paid to fly around the world to attend a prestigious sporting event by a supplier trying to sell them services, or a local councillor accepting a bottle of champagne from a company and subsequently sitting on a panel deciding whether to award them work. Or it could be an individual holding shares or having another financial interest in a client, supplier or competitor.

Other types of conflict occur between the interests of different clients. This is a particular problem for law firms, which are prohibited by the Solicitors Regulation Authority from acting for a client whose interests

Conflict resolution?While it might seem obvious that an MP should not accept cash from lobbyists to ask questions in Parliament, some conflicts of interest can be hard to spot and depend on an individual’s role as well as the sector they work in. So how can internal audit help firms to be on guard?

25

Conflicts of interest might involve a clash between an employee’s personal interests and those of their employer’s customer or stakeholder.{ }

Conflict resolution?

26

{ }An end to direct assistanceIAs need to be aware of a recent change to Financial Reporting Council standards for external auditors that will affect how the two sets of auditors can work together. “Direct assistance” – where external auditors take IAs into their audit team for a period of time – will now be prohibited.

It’s a move that has been taken precisely to avoid “conflicts of interest and a lack of independence”, explains Melanie McLaren, executive director of codes and standards at the FRC. “Clearly an internal auditor who is

employed by a company has a financial interest in it.”

External auditors will still be able to rely on the work of IAs provided that it has been scoped and managed by the internal audit function and that the external auditor is satisfied that it has been approached objectively and appropriately reviewed.

There is, of course, an ongoing debate at European level over the possible compulsory rotation of external auditors and restrictions on the consultancy services that they can provide. In the UK, the

FRC doesn’t support mandatory rotation, but changed the corporate governance code last autumn to stipulate (on a “comply-or-explain” basis) mandatory retendering of external audit contracts every ten years by FTSE 350 companies. “Our view is that investors deserve the best quality audit,” says McLaren. “In some parts of the market there isn’t a large number of firms capable of carrying out a sufficiently high-quality external audit,

largely because of the global reach or sectoral expertise needed.”

In terms of firms’ consultancy work, McLaren says the FRC isn’t

in favour of a cap on so-called audit-related services. “We think it would be better to say that there are certain services that can’t be provided (such as advocacy) and then place a requirement on audit committees to satisfy themselves in terms of independence, objectivity threats and safeguards on the other work.”

their own ethical codes and systems of regulatory oversight.

But legal problems are not the only danger from conflicts of interest – there’s also the risk of reputational damage. Angela Robertson, general counsel at Eversheds, notes: “If a law firm takes on a piece of work for a client and a conflict of interest is subsequently identified, it could severely damage or even kill that client relationship.

In some sectors – particularly those where clients are sensitive around conflict issues – it could have repercussions across the industry, because word would get out to others. Obviously there’s a risk of adverse publicity, particularly in the legal press.”

Reducing the risksHow can organisations reduce the risk of conflicts of interest occurring? The starting point is for all conflicts or potential conflicts to be declared or identified so they can be managed appropriately. At Wokingham Borough Council all councillors and senior managers are asked to complete a declaration of any known conflicts of interest annually.

“But this is only as effective as the training and understanding that goes with it,” explains Muir Laurie CMIIA, director of business assurance and democratic services and head of internal audit at the council.

“Issues for councils are typically around property and procurement for officers and planning for council members”

clash with those of another client or of the firm itself. As a result, many now have teams dedicated to detecting potential issues.

Concerns over a lack of independence can also be a problem for external auditors. In May, the FRC – which sets ethical standards to ensure their objectivity and impartiality – published its annual report into audit quality inspections. While it highlighted an improvement in the overall quality of external audit work, it also found that firms should reassess the adequacy of their independence and ethics procedures and the training they provide to staff at all levels. In one case, a former executive of an audited organisation rejoined its audit firm as a partner, but failed to dispose of a shareholding in the organisation for several months, in breach of ethical standards.

Whatever the nature of conflicts, there can be regulatory consequences for failing to manage them appropriately. Company boards have a statutory duty under the Companies Act 2006 to avoid conflicts of interest, while the UK corporate governance and stewardship codes (overseen by the FRC) place a range of requirements on boards and investors for handling independence and potential conflicts on a “comply-or-explain basis”. The Bribery Act 2010 has increased scrutiny over employees accepting gifts and entertainment. The professions also have

“I think some internal audit teams think that getting 100 per cent completion of those forms is all you need to do. But that doesn’t mean there aren’t conflicts of interest – managers may be unaware of them or knowingly leave them off forms because it might ruin relationships they have with contractors.”

Issues for councils in general are typically around property and procurement for officers and planning for council members. Laurie says that Wokingham runs governance training sessions for newly elected councillors. “If a council member is sitting on the planning committee hearing a planning application from one of their neighbours wanting to build a conservatory in their back garden, should they declare it? They should – and that’s the kind of practical example we try to give.”

In the legal sector, a lot of conflict management relies on processes and technology, explains Robertson. As well as being responsible for conflict management at Eversheds, she previously set up the global conflicts team at Clifford Chance after it had undergone two mergers. “Every single piece of new work for a client, whether new or existing, had to go through the central conflicts team to identify whether there were any legal or commercial conflicts of interest,” she explains.

27

}

USEFUL rESoUrcES• oEcD guidelines for managing

conflicts of interest in the public sector: http://bit.ly/15B4Yot• FSA paper on conflicts of interest between asset managers and their customers: http://bit.ly/13lfboW• Hargreaves Lansdown conflicts of interest policy: www.hl.co.uk/conflicts• 3M conflicts of interest policy (US): http://bit.ly/11YFsLy• companies Act 2006 – a director’s duty to avoid conflicts of interest (Pinsent Masons): http://bit.ly/18ojTxw

A law firm needs a good conflicts database containing details of all its current and historic clients and cases, she adds. “You need to be able to identify what work you’ve done for which client over a period of time. You’ve also got to have a good, clear process that everybody is aware of, so that you don’t start acting on a piece of work for a client until you’ve checked with the conflicts team, assuming you have one.” But lawyers must also be trained to understand the importance of giving the correct information to the conflicts team, she adds. “A conflicts system relies on people using it properly and inputting the right information.”

Getting the right culture and governance framework is also an important issue for asset managers – and reflects the FCA’s focus on consumer protection, believes Amanda Rowland, the partner who heads up PwC’s asset management regulation team.