grindrod de-risking retirement payers and growers may 2015

TRANSCRIPT

DE-RISKING RETIREMENT STRATEGIES

Paul Stewart Head: Fund Management

May 2015

AGENDA

Update on Grindrod Asset Management – Paul Stewart

Marc Thomas – Post Retirement thinking

Ian Anderson – Portfolio attributes

Marc Thomas – Pre Retirement thinking

“More dangerous yet is the shift in focus away

from retirement income to return on investment

that has come with the introduction of saver-

managed DC plans: Investment decisions are now

focused on the value of the funds, the returns on

investment they deliver, and how volatile those

returns are. Yet the primary concern of the saver

remains what it always has been: Will I have

sufficient income in retirement to live comfortably?”

- Robert C. Merton, MIT Sloan School of Economics

Harvard Business Review, March 2014

We conceptualised the Grindrod Asset Management business offering

on 3 key ideas:

Differentiated products aimed at meeting particular investor needs

Delivering on our primary promise of income and income growth

Competitive long-term investment results against the benchmark

and peer group.

A REFLECTION ON WHERE WE CAME FROM

Most asset managers, globally and in South Africa, are peer group and capital

return focussed;

We saw the pre- and post-retirement markets as being poorly serviced by

asset managers

We decided on “outcomes-based investing” as a core principle addressing the

dual problems of income provision and inflation-hedged income growth

Yield and growth in yield is our major measureable and deliverable

We registered the trademark

We realigned our fund range along these principles in 2012.

1. DIFFERENTIATED PRODUCTS MEETING INVESTOR NEEDS

2. DELIVERING ON OUR PROMISE OF INCOME GROWTH

Source: Grindrod Asset Management

230,805

285,725

329,209

100,000

150,000

200,000

250,000

300,000

350,000

2012 2013 2014

ANNUAL INCOME PRODUCED FROM R5m INVESTMENT

164,000

219,000

290,500

100,000

150,000

200,000

250,000

300,000

350,000

2012 2013 2014

ANNUAL INCOME PRODUCED FROM R5m INVESTMENT

Grindrod Stable Growth Fund Grindrod Managed Growth Fund

3. P&G® ALSO DELIVER COMPETITIVE LONG-TERM RETURNS

3 years to 30 April 2015

Annualised

income

return

Annualised

capital

return

Annualised

total return

Annualised

benchmark

return

Peer

group

rank

Grindrod Stable

Growth A 5.31% 11.05% 16.36%

(TER 1.27%)

7.47% (CPI +2%)

1/80

Grindrod Managed

Growth A 4.64% 16.38% 21.02%

(TER 1.25%)

9.64% (CPI +4%)

1/90

Grindrod High

Income A 6.89% 1.24% 8.13%

(TER 1.17%)

6.67% (Stefi +1%)

8/50

Grindrod Equity

Income Growth A (*since inception – 2 Jul 2013)

3.72% 20.94%

24.66% (TER 1.23%)

*19.93% (SA Gen Eq. Ave.)

18/162

TER is measured over the last 12 months to 31 March 2015

Source: Grindrod Asset Management, Moneymate

Payers & Growers® brand has seen very pleasing growth:

AuM growth of 22.4% over 12 months to 30 April 2015

GCI Manco assets grow by 58.7% for the year to 30 April 2015

159 IFA‟s consistently supporting the business

- across the country in all provinces and markets

Both direct and LISP business channels growing

Institutional clients now number ten – up from five 12 months ago

Launched Grindrod Global Equity Income Growth Fund

and Grindrod Global Managed Growth Funds domiciled in Ireland

Launched our Tax-free Savings Plan on 1 April 2015.

BUSINESS MILESTONES ACHIEVED

Marc Thomas May 2015

DE-RISKING RETIREMENT STRATEGIES

Pre-retirement Post-retirement

Retirement

Retirement

BlackRock: America‟s Retirement Needs 2013

“the challenge of decumulation has yet to be effectively addressed”

William Sharpe: Nobel Laureate Economics,CFA Conference May 2014

“I am focussing my attention on this issue (retirement income). And it‟s a really hard problem-the hardest problem I‟ve ever considered- because its multidimensional…”

Thaler: Behavioural Finance Professor. Your Wealth and Life UBS 2015

“.. One issue that‟s on everyone‟s mind is that we don‟t have satisfactory solutions for dealing with the decumulation phase of life. This is a problem because figuring out the best way to draw down a pile of money is a much harder problem than accumulation.”

DECUMULATION/DRAWDOWN CHALLENGE

SEQUENCE OF RETURNS: INCOME DRAWDOWN

New thinking:

but in a different direction

“Substituting Top 100 Dividend Paying stocks for S&P 500 Index stocks

had very beneficial effects on the “SAFEMAX” for retirees during the period.

The SAFEMAX was increased by about 25 percent (i.e. from 4% to 5%)

during this period, which translates into a significant improvement of lifestyle

for those retirees… and they also saw very substantial increases

in their portfolio longevity” Bengen

“We found that this focus on dividends had a significantly positive impact

on both the portfolio‟s withdrawal rate and its sustainability…

we found that using a strategy focused on companies with high and growing

dividends alleviates the stress of regular withdrawals.”

Thornburg Investment Management

INCOME DRAWDOWN:PORTFOLIO SUSTAINABILITY Impact of including yield and income growth in drawdown portfolios

HYPOTHETICAL INCOME, BALANCE, AND RETURN SHEET

R3m invested on 06/07/2012

Initial drawdown rate of 6%

Escalating at 6% per annum

July is anniversary month

Unit balance is dropping moderately

Reinvestment of distributions lower than income drawdowns

Income growth will stabilise the decline and then increase the units

(2,000)

(1,000)

-

1,000

2,000

3,000

Drawdown Reinvestment

174,500

175,000

175,500

176,000

176,500

177,000

177,500

178,000

178,500

179,000

Unit balance

Only 1.6% decline

in units

GRINDROD STABLE GROWTH FUND (JAN 2014)

GRINDROD STABLE GROWTH FUND (JULY 2014)

(2,000)

(1,000)

-

1,000

2,000

3,000

07/1

2

08/1

2

09/1

2

10/1

2

11/1

2

12/1

2

01/1

3

02/1

3

03/1

3

04/1

3

05/1

3

06/1

3

07/1

3

08/1

3

09/1

3

10/1

3

11/1

3

12/1

3

01/1

4

02/1

4

03/1

4

04/1

4

05/1

4

06/1

4

Drawdown Reinvestment

172,000

173,000

174,000

175,000

176,000

177,000

178,000

179,000

180,000

Unit balance

Initial investment: R3,000,000.00

Initial drawdown rate: 6%

Income escalation: 6% per annum

Anniversary month: July

(2,000)

(1,000)

-

1,000

2,000

3,000

07

/12

08

/12

09

/12

10

/12

11

/12

12

/12

01

/13

02

/13

03

/13

04

/13

05

/13

06

/13

07

/13

08

/13

09

/13

10

/13

11

/13

12

/13

01

/14

02

/14

03

/14

04

/14

05

/14

06

/14

07

/14

08

/14

09

/14

10

/14

11

/14

12

/14

01

/15

02

/15

03

/15

04

/15

Drawdown Reinvestment

171,000

172,000

173,000

174,000

175,000

176,000

177,000

178,000

179,000

180,000

Unit balance

Initial investment: R3,000,000.00

Initial drawdown rate: 6%

Income escalation: 6% per annum

Anniversary month: July

GRINDROD STABLE GROWTH FUND – APRIL 2015

Year 1

July 2012 -

June 2013

Year 2

July 2013 -

June 2014

Year 31

July 2014 -

June 2015

Income drawdown requirement R180,000.00 R190,800.00 R202,248.00

Net income produced by fund R134,035.08 R172,555.19 R193,453.88

Income covered by portfolio 74.5% 90.4% 95.7%

Capital value at end of period R3,284,104.89 R3,528,361.24 n/a

GRINDROD STABLE GROWTH FUND – APRIL 2015 6% drawdown rate

1 Based on GrAM distributions forecasts and April 2015 ending unit balance

1. Client retirement becoming

MORE secure

2. Advisor AUM based fees

INCREASE

3. Capital and income LESS

vulnerable to volatility,

sequence, timing and top up

risk

Reliable income yield

Annual growth in income of close to CPI

Long term capital growth (Total Return) at/above CPI to sustain income for up

to 30 years

INCOME EFFICIENT PORTFOLIOS 3 important elements to provide for income dependent investors

Ian Anderson May 2015

DE-RISKING RETIREMENT STRATEGIES

IN JANUARY 2014, SA FUND MANAGERS...

forecast the 10-year bond yield to be 8.5 – 9.0% in 12 months

forecast the rand to be ZAR10.25/US$ in 12 months

thought that South African 10-year bonds were „overvalued‟

thought that resources would be the best performing equity sector in 2014

Source: Merrill Lynch Fund Manager Survey

HISTORIC PERFORMANCE – SA ASSET CLASSES

0

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ten year performance to 31/03/2015

SA Listed Property SA Equities SA Bonds SA Cash

SA Listed Property

SA Equities SA Bonds SA Cash

10 Years 22.4% 18.0% 8.9% 7.4%

5 Years 22.2% 16.1% 9.7% 5.8%

3 Years 25.2% 19.4% 9.0% 5.6%

1 Year 41.4% 12.5% 12.4% 6.1%

Source: I-Net Bridge

HISTORIC PERFORMANCE – SA FUND MANAGERS

SA Listed

Property SA Equities SA Bonds SA Cash

10 Years 22.4% 18.0% 8.9% 7.4%

5 Years 22.2% 16.1% 9.7% 5.8%

3 Years 25.2% 19.4% 9.0% 5.6%

1 Year 41.4% 12.5% 12.4% 6.1%

Multi-Asset Low Equity

Multi-Asset High Equity

10.1% 13.4%

10.3% 12.8%

11.5% 15.0%

10.3% 11.9%

16.0% 20.5% P&G portfolios – 3 years

20.0% 25.1% P&G portfolios – 1 year

Source: I-Net Bridge & Morningstar

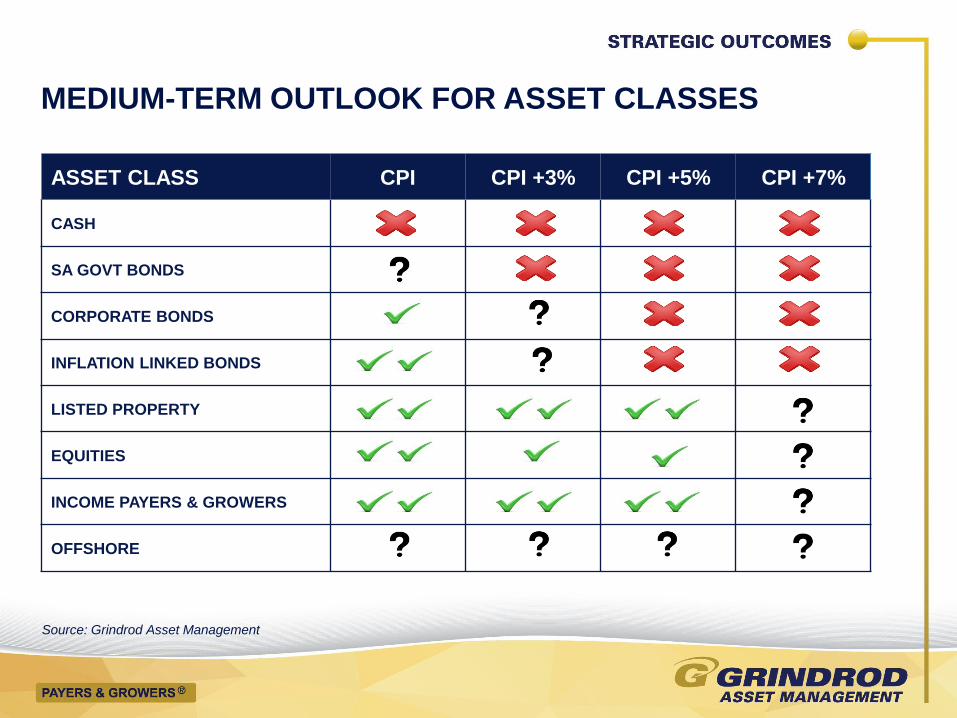

MEDIUM-TERM OUTLOOK FOR ASSET CLASSES

ASSET CLASS CPI CPI +3% CPI +5% CPI +7%

CASH

SA GOVT BONDS

CORPORATE BONDS

INFLATION LINKED BONDS

LISTED PROPERTY

EQUITIES

INCOME PAYERS & GROWERS

OFFSHORE

CPI

CPI

CPI

CPI

CPI

CPI

CPI

CPI CPI CPI CPI

CPI

CPI

CPI

CPI

CPI

CPI

CPI

CPI

CPI

CPI

CPI

CPI

CPI CPI CPI

CPI CPI

CPI CPI

CPI CPI

Source: Grindrod Asset Management

MEDIUM-TERM OUTLOOK FOR ASSET CLASSES Simple expected real returns

Source: Research Affiliates based on data from Robert Shiller, FactSet & Bloomberg

INCOME

ASSETS

Lis

ted

pro

pert

y

GROWTH

ASSETS

INCOME EFFICIENT PORTFOLIOS

INCOME EFFICIENT PORTFOLIOS

Listed property

Cash & Bonds

Equities

Listed property

Cash & Bonds

Equities

Listed property

Cash & Bonds

Equities

Listed property

GRINDROD STABLE GROWTH FUND

GRINDROD MANAGED GROWTH FUND

GRINDROD HIGH INCOME FUND

GRINDROD EQUITY INCOME GROWTH FUND

Source: Grindrod Asset Management

► SOUTH AFRICA - MULTI-ASSET - LOW EQUITY

► FORWARD INCOME YIELD 6.5%

► INCOME GROWTH (3 YEARS) 6.8% p.a.

► SOUTH AFRICA - MULTI-ASSET - INCOME

► FORWARD INCOME YIELD 8.5%

► INCOME GROWTH (3 YEARS) 1.9% p.a.

INCOME EFFICIENT PORTFOLIOS

GRINDROD STABLE GROWTH FUND

GRINDROD MANAGED GROWTH FUND

GRINDROD HIGH INCOME FUND

GRINDROD EQUITY INCOME GROWTH FUND

► SOUTH AFRICA - MULTI-ASSET - HIGH EQUITY

► FORWARD INCOME YIELD 5.0%

► INCOME GROWTH (3 YEARS) 9.5% p.a.

► SOUTH AFRICA - EQUITY - GENERAL

► FORWARD INCOME YIELD 4.4%

► INCOME GROWTH (3 YEARS) 10.7% p.a.

Source: Grindrod Asset Management

INCOME EFFICIENT EQUITY PORTFOLIO

AVI

BAT

BIDVEST

CLICKS

FIRSTRAND

INVESTEC

LIBERTY

LIFE HEALTHCARE

MMI

MR PRICE MTN NAMPAK

OLD MUTUAL

REUNERT

SABMILLER

STANDARD BANK

SPAR

TIGER BRANDS

TRUWORTHS

VODACOM

WOOLWORTHS

DIVIDEND YIELD 4.0%

DIVIDEND GROWTH 10.9% p.a.

Source: Grindrod Asset Management

INCOME EFFICIENT EQUITY PORTFOLIO

Positions equally weighted

reduces risks to portfolio income stream (good businesses can cut dividends)

disciplined approach (regular rebalancing)

Emphasis on industries & products that matter

aging demographic – healthcare & financial services

communication – mobile telecomms

High quality businesses with relevant products and services;

high cash conversion ratios; clear dividend policies.

INCOME EFFICIENT LISTED PROPERTY PORTFOLIO

ACCELERATE

ARROWHEAD

DELTA

DIPULA

FAIRVEST

NEPI

SAFARI

TEXTON

TOWER

DIVIDEND YIELD

8.0%

DIVIDEND GROWTH

10.0% p.a.

Source: Grindrod Asset Management

INCOME EFFICIENT LISTED PROPERTY PORTFOLIO

Positions equally weighted

reduces risks to portfolio income stream (good businesses can cut dividends)

disciplined approach (regular rebalancing)

Yield and expected growth substantially above the market

current yield is more than 2% above market

expected distribution growth over next 3 years is more than 3% above market

Listed property is used to enhance the outcome

(high yield, high growth or combination of the two)

GRINDROD HIGH INCOME FUND

2.8%

2.1%

2.6%

1.9%

0.6%

1.4%

1.0% 1.2%

2.3% 2.1%

1.8%

4.5%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Jun '12 Sep '12 Dec '12 Mar '13 Jun '13 Sep '13 Dec '13 Mar '14 Jun '14 Sep '14 Dec '14 Mar '15

Pe

rce

nta

ge

Quarterly investment returns – A class

Capital Income Total Return

Source: Grindrod Asset Management

GRINDROD STABLE GROWTH FUND

2.2%

6.4%

7.1%

2.2%

1.2%

1.8%

3.7%

2.1%

4.5%

1.7%

5.4%

7.1%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Jun '12 Sep '12 Dec '12 Mar '13 Jun '13 Sep '13 Dec '13 Mar '14 Jun '14 Sep '14 Dec '14 Mar '15

Pe

rce

nta

ge

Quarterly investment returns – A class

Capital Income Total Return

Source: Grindrod Asset Management

GRINDROD MANAGED GROWTH FUND

2.3%

8.0%

9.0%

2.6%

1.5%

3.2%

5.1%

2.9%

5.1%

1.8%

7.6%

8.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Jun '12 Sep '12 Dec '12 Mar '13 Jun '13 Sep '13 Dec '13 Mar '14 Jun '14 Sep '14 Dec '14 Mar '15

Pe

rce

nta

ge

Quarterly investment returns – A class

Capital Income Total Return

Source: Grindrod Asset Management

GRINDROD EQUITY INCOME GROWTH FUND

4.4%

5.7%

3.8%

5.5%

2.6%

7.4%

8.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

Sep '13 Dec '13 Mar '14 Jun '14 Sep '14 Dec '14 Mar '15

Pe

rce

nta

ge

Quarterly investment returns – A class

Capital Income Total Return

Source: Grindrod Asset Management

INCOME FROM GROWTH ASSETS GRINDROD STABLE GROWTH FUND

230,805

285,725

329,209

360,848

384,507

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2012 2013 2014 2015f 2016f

Annual income produced from R5m investment – A class

Source: Grindrod Asset Management

TOTAL INCOME = R1,591,093

31.8% OF ORIGINAL INVESTMENT

INCOME FROM GROWTH ASSETS GRINDROD MANAGED GROWTH FUND

164,000

219,000

290,500

330,000

356,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2012 2013 2014 2015f 2016f

Annual income produced from R5m investment – A class

Source: Grindrod Asset Management

TOTAL INCOME = R1,359,500

27.2% OF ORIGINAL INVESTMENT

INCOME FROM GROWTH ASSETS GROWTH TRUMPS YIELD

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

2013 2014 2015f 2016f 2020f

Annual income produced from R5m investment – A class

High Income Fund Stable Growth Fund Managed Growth Fund

Source: Grindrod Asset Management

GRINDROD MANAGED GROWTH FUND ANOTHER PERSPECTIVE

Current NAV = R437.9m (as at 07/05/2015)

Income - 2015 Income - 2016 % change

Banking business R1,574,539 R1,773,445 12.6%

Mobile communications business R1,498,490 R1,605,587 7.1%

Fashion retailing business R1,454,230 R1,693,488 16.5%

Insurance business R1,424,029 R1,918,744 34.7%

Food production business R1,065,217 R1,162,895 9.2%

Electronics business R781,070 R781,070 0%

Tobacco business R526,133 R575,214 9.3%

Packaging business R513,764 R622,784 21.2%

Healthcare business R506,629 R570,336 12.6%

Food retailing business R471,374 R510,975 8.4%

Food service & logistics business R376,350 R425,005 12.9%

Brewing business R274,086 R299,584 9.3%

Health & beauty retailing business R352,634 R397,586 12.7%

Property portfolio R8,542,272 R9,317,050 9.1%

Cash & bonds R3,810,696 R3,810,696 0%

TOTAL R23,171,513 R25,464,468 9.9%

Source: Grindrod Asset Management

PORTFOLIO HEALTH MONITOR

GRINDROD MANAGED GROWTH FUND A CASE STUDY

Source: Grindrod Asset Management

45 YEARS OLD

CURRENT ANNUAL SALARY OF R490,769.23

COMPULSORY SAVINGS OF R878,370.85

CONTRIBUTIONS OF 8.25% OF ANNUAL SALARY

SALARY ESCALATES AT 6% PER ANNUM

COMPULSORY SAVINGS INVESTED

IN THE GRINDROD MANAGED GROWTH FUND

GRINDROD MANAGED GROWTH FUND SCENARIO PLANNING TOOL

Source: Grindrod Asset Management

0

100

200

300

400

500

600

700

800

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Simulated price performance

GRINDROD MANAGED GROWTH FUND SCENARIO PLANNING TOOL

Source: Grindrod Asset Management

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Simulated quarterly distributions

GRINDROD MANAGED GROWTH FUND INCOME COVERAGE RATIO

Source: Grindrod Asset Management

0%

50%

100%

150%

200%

250%

300%

350%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033

% Of annual salary covered by income from GMGF

Income coverage ratio (rhs) Annual salary (lhs) Retirement income (lhs)

Pre-retirement Post-retirement

Retirement

Retirement

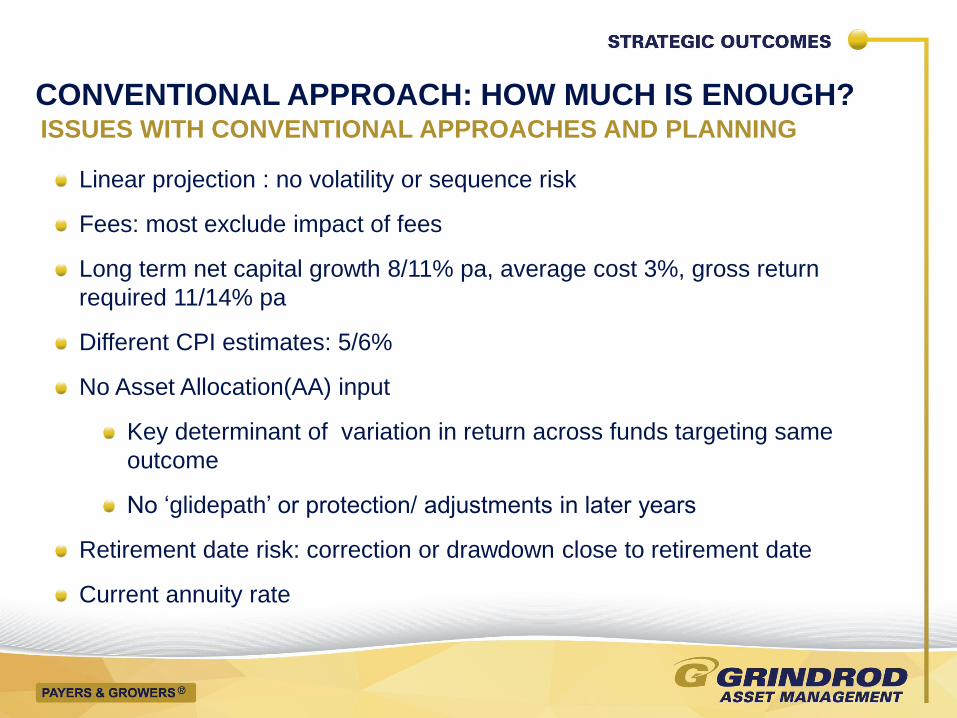

Linear projection : no volatility or sequence risk

Fees: most exclude impact of fees

Long term net capital growth 8/11% pa, average cost 3%, gross return

required 11/14% pa

Different CPI estimates: 5/6%

No Asset Allocation(AA) input

Key determinant of variation in return across funds targeting same

outcome

No „glidepath‟ or protection/ adjustments in later years

Retirement date risk: correction or drawdown close to retirement date

Current annuity rate

ISSUES WITH CONVENTIONAL APPROACHES AND PLANNING

CONVENTIONAL APPROACH: HOW MUCH IS ENOUGH?

HOW MUCH IS ENOUGH? ISSUES WITH CONVENTIONAL ASSUMPTIONS AND CALCULATORS

0

2

4

6

8

10

12

14

1 5 10 15 20 25

Mill

ion

s

Years

Linear projection : no volatility or sequence risk

A MORE REALISTIC LOOK MONTE CARLO: RANGE OF OUTCOMES FOR CPI+3

SEQUENCE RISK IN LATER YEARS HARDER TO RECOVER LOSSES ESPECIALLY IN LATTER YEARS

SEQUENCING RISK MAY LEAD TO PORTFOLIO RUIN

HOW MUCH IS ENOUGH?

Retirement date risk

Correction or drawdown close to retirement date.

-10% increases a 5% planned drawdown rate to 5,5%

Reduces real income growth period from 19 to 17 years and

success rate from 54% to 44%.

-15% increases a 5% planned drawdown rate to 5,8%

Reduces real income growth period from 19 to 14 years and

success rate from 54% to 40%

ISSUES WITH CONVENTIONAL ASSUMPTIONS AND CALCULATORS

ANNUITY RISK

Capital value

Annuity Rate

5% 4.5% 6%

NEED MORE

CAPITAL

NEED LESS

CAPITAL

UNKNOWABLE INTEREST/ANNUITY RATE CHANGES

ANNUITY RISK

Capital value

Annuity Rate

RSA 2000/ 14%

RSA 2006/ 8.6%

RSA 2015/ 7.2%, escalating@5%/ 4.2%

UNKNOWABLE INTEREST/ANNUITY RATE CHANGES

Shock after annuity

rates hit record low 29 April 2015

UK 1995/ 11.3%

UK 2008/ 7%

UK 2015/ 4.7%

UK 2015 escalating@CPI/ 2.7%

RETIREMENT RISK ZONE SEQUENCE RISK, ANNUITY RISK

High Annuity

Risk

GLIDEPATH OR TARGET DATE FUND MECHANICAL ASSET ALLOCATION ADJUSTMENTS

Almost certain to not achieve the projected capital value (not fully

invested)

Still have another 30 years to sustain income drawdown stress

25-50% less

income

or higher

drawdown rate

0

2

4

6

8

10

12

14

1 5 10 15 20 25

Mill

ion

s

Years

GLIDEPATH OR TARGET DATE FUND MECHANICAL ASSET ALLOCATION ADJUSTMENTS

Risk is better measured by the volatility in our prospective retirement

income than by the volatility in our portfolio value

A far better measure is the real sustainable spending a portfolio is likely to

deliver

Glidepath funds neither reflect current market conditions or yields, nor

adapt opportunistically to them

Projected Income

Morningstar: John Rekenthaler Vice President of Research for Morningstar 2014

“for investors approaching (or in) retirement, the better way to think about

progress is the growth (or shrinkage) of projected income.

Projected income is a concept whose time has come…. Projected retirement

income is superior to total return for conveying to investors how they are

progressing toward their goals,

it‟s quite possible for a fund to succeed according to total return but fail as

measured by projected income,”

Blackrock: Chip Castille Managing Director,BlackRock US DC Group. May 2015

We need to shift our focus away from the total value of the nest egg, and

instead toward the annual income it could provide

NEW THINKING IN A DIFFERENT DIRECTION GLOBAL RESEARCH

UNDERSTANDING „REAL‟ RISK

Short-term risk (“shallow risk”)

- Price volatility

• Obvious

• Immediate

• Temporary

SOURCE: WILLIAM BERNSTEIN:

DEEP RISK

Long-term risk (“deep risk”)

- Devastation (war or anarchy – Egypt)

- Confiscation (taxes or seizure by government - Zimbabwe)

- Deflation (falling asset values - Japan)

- INFLATION

“Std Dev measures only shallow risk”

“You should actively seek shallow risk,

since it will enable you to buy at lower

prices”

COMPONENTS OF RETURN AND STANDARD DEVIATIONS 2000 – 2013 ANNUALISED

GRINDROD MANAGED GROWTH FUND

2.3%

8.0%

9.0%

2.6%

1.5%

3.2%

5.1%

2.9%

5.1%

1.8%

7.6%

8.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Jun '12 Sep '12 Dec '12 Mar '13 Jun '13 Sep '13 Dec '13 Mar '14 Jun '14 Sep '14 Dec '14 Mar '15

Pe

rce

nta

ge

Quarterly investment returns – A class

Capital Income Total Return

Source: Grindrod Asset Management

INCOME FROM GROWTH ASSETS GRINDROD MANAGED GROWTH FUND

164,000

219,000

290,500

330,000

356,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2012 2013 2014 2015f 2016f

Annual income produced from R5m investment

Source: Grindrod Asset Management

FOCUS ON TOTAL RETURN THE BENEFITS OF COMPOUNDING INCOME

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

2010 2011 2012 2013 2014

Cumulative return split on R5m initial investment Nedgroup Investments Property Fund

Income paid Capital appreciation Income reinvested (compounding)

Source: Grindrod Asset Management

R933k produces R74k pa= 14% more income

GRINDROD MANAGED GROWTH FUND RETIREMENT PLANNING:INCOME COVERAGE RATIO

Source: Grindrod Asset Management

0%

50%

100%

150%

200%

250%

300%

350%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

% OF ANNUAL SALARY COVERED BY INCOME FROM GMGF

Income coverage ratio (rhs) Annual salary (lhs) Retirement income (lhs)

“Incremental liabilities are not met by the cash

matching of bonds,….They are best matched

through productivity and inflation-related

investments – equity and real estate.”

PRE-RETIREMENT POST-RETIREMENT

DERISKING RETIREMENT STRATEGIES CHANGING THE APPROACH

Move away from an approach that is mostly based on unknowns and

therefore hope. This approach focuses on:

A short term only risk measure, volatility, measured by Std Deviation

Short term tactical or market timing techniques, which are high risk for

the client, especially in the retirement risk zone I.e., value strategy out of

favour

Creating portfolios that look efficient and optimised based on complex

mathematical models which are price centric and short term volatility

based, focus mostly on short term market conditions and bear no

relationship to client outcomes

-10% increases a 5% planned drawdown rate to 5,5%

Reduces real income growth period from 19 to 17 years and success rate from 54%

to 44%.

-15% increases a 5% planned drawdown rate to 5,8%

Reduces real income growth period from 19 to 14 years and success rate from

54% to 40%

PRE-RETIREMENT POST-RETIREMENT

DERISKING RETIREMENT STRATEGIES CHANGING THE APPROACH

To an approach that is based on tangible, predictable metrics, thereby

facilitating solid planning. This approach focuses on :

The only relevant retirement risk, predictable income and income growth

A metric that gives you a better indication of income position and risk

than portfolio values, the Income Coverage Ratio (ICR)

The ICR that facilitates a plan management process that matches the

clients income liability with their asset through time

-10% increases a 5% planned drawdown rate to 5,5%

Reduces real income growth period from 19 to 17 years and success rate from 54%

to 44%.

-15% increases a 5% planned drawdown rate to 5,8%

Reduces real income growth period from 19 to 14 years and success rate from

54% to 40%

PRE-RETIREMENT POST-RETIREMENT

DERISKING RETIREMENT STRATEGIES APPLYING ASSET LIABILITY MATCHING

This is achieved by:

Matching the clients current or future income liability ………….

through the Income Coverage Ratio ………

to a…..

-10% increases a 5% planned drawdown rate to 5,5%

Reduces real income growth period from 19 to 17 years and success rate from 54%

to 44%.

-15% increases a 5% planned drawdown rate to 5,8%

Reduces real income growth period from 19 to 14 years and success rate from

54% to 40%

Grindrod

Income Efficient Portfolio.

Grindrod Collective Investments RF) (Pty) Ltd (“the Manager”), Registration number 2008/022492/07, is a company incorporated in South Africa acting as a manager of collective investments schemes in securities in terms of Section 42 of the Collective Investments Schemes Control Act and is supervised by the Financial Services Board. The registered address of the Manager is 5 Arundel Close, Kingsmead Office Park, Durban, 4001. The Trustee and Custodian is Société Générale Johannesburg Branch. The Investment Management of the portfolios is outsourced to Grindrod Asset Management (Pty) Ltd, an authorised financial services provider, FSP 29834. Both the Manager and Grindrod Asset Management (Pty) Ltd are members of the Grindrod Financial Services Group. Client administration is outsourced to Maitland Group South Africa Limited, Tel: 021 681 8059; Address: Maitland House 1, River Park, Gloucester Road, Mowbray, 7700, Cape Town. Collective investment schemes are generally medium to long-term investments. The value of participatory interests or the investment may go down as well as up. Past performance is not necessarily a guide to future performance. Collective investment schemes are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available on request from the manager. There are no performance fees charged in the portfolio. The manager does not provide any guarantee either with respect to the capital or the return of a portfolio. A fund of funds is a portfolio that invests in portfolios of collective investment schemes that levy their own charges, which could result in a higher fee structure for the fund of funds. Participatory interests in the portfolios issued by the manager qualify as investment instruments for the purposes of Tax Free Savings and Investment account by virtue of Section 12T of the Income Tax Act. If you wish to invest in a Tax Free Savings and Investment Plan please ensure that you fill in the correct application form. Grindrod is required by law not to accept contributions in excess of the annual and lifetime limits. Grindrod does not monitor the contributions you may have with other service providers. Consequently, you undertake to advise Grindrod when your aggregate contribution across service providers has reached the annual limit and the lifetime limits. Grindrod is not responsible for the tax penalty which you may incur as a result of excess contributions made by you into the Investment Plan. A 40% penalty is payable on the contribution above limit. No transfers to another tax free investment service provider will be allowed before 1 March 2016. Grindrod does not charge any fees for withdrawal of the tax free investment. The General Investor Report is published on a quarterly basis and is available on request and on our website. The portfolio may borrow up to 10% of its net assets on a temporary basis. Such borrowings are permitted only to meet the portfolio’s obligations in relation to (i) the administration of the Fund relating to purchase or sale transactions; and/or (ii) the redemption or cancellation of participatory interests in the portfolio. Borrowings in relation to (i) above are only permitted for a period of up to 8 calendar days, and 61 calendar days in respect of (ii). Past portfolio performance is measured on a rolling monthly basis. The annual report, brochures, application form is available on our website. The portfolio may be closed to new investments at any time in order to be managed in accordance with its mandate. Forward pricing is used. Information on this document shall not be construed as financial advice as defined and/or contemplated in terms of the Financial Advisory and Intermediary Services Act, Act 37 of 2002 ("the FAIS Act"). Grindrod shall, wherever possible, avoid situations causing a conflict of interest. Where it is not possible to avoid such conflict, Grindrod shall advise you of such conflict in writing at the earliest reasonable opportunity and shall mitigate the conflict of interest in accordance with its conflict of interest Management Policy. You may send a blank email with a subject “conflict of interest” to the compliance officer, should you need a copy of this policy. Complaints should be directed to the Compliance Officer. The Complaints Resolution Policy is available on request. The Compliance Officer’s email address is [email protected]. Grindrod Collective Investments (RF) (Pty) Ltd and Grindrod Asset Management (Pty) Ltd (collectively referred to as “Grindrod”) are members of the Grindrod Financial Services Group and are supervised by the Financial Services Board

THANK YOU