green watch

TRANSCRIPT

Green watch (Let’s think green!)

Volume 1; October 2015 ISSN:XXXXXXXX

Editor’sdesk

Green Watch is a youth initiative of few of the researchers, marketers in environmentindustry.Importanceofenvironmentalprotection,afforestation,biodiversity,conservationofnaturalresourceshasbecomecrucialthesedays.Environmentaldegradation,depletionofnaturalresources,carbonfootprint,GHGemissions,naturaldisastersetc.havebecomecauseof immense concern in frontofworld community. It is the responsibilityof all thestakeholders to save mother earth against all the evil business practices happeningworldwide.There is a lackof knowledge and awareness about various ill effects, humanandotherspeciescanfaceduetoenvironmentaldegradation.Complianceofgreenpoliciesandcarefulconsiderationofallthefactorsrelatingtosustainabilityistheneedofthehour.Graduallytheenvironmentalpolicies,regulationandenvironmentalpolicycompliancearegetting stringent. Various initiatives, policies and programmes are undertaken in theprocess of disseminating the information about environmental impacts and make thestakeholdersawareaboutit.Considerationofpeople,planetandprofit(3Ps)providesthebasis of sustainable development. Satisfaction of all the stakeholders and care forenvironmentisthestrategyforanybusinesstosustaininalongrun.Policyofreduce,reuseandrecycleshouldalwaysbeinfocusinthebusinessprocessing.Foraprosperousgreenworld, governments, businesses and civil society organizations with other stakeholdersmustcomeforwardtotacklethischallengeofclimatechange.

The initiative thus taken by Green Watch in order to disseminate information andknowledge,enhanceawarenessaboutsustainabilitymanagementpracticesalloveramongall the stakeholders. This global monthly update would try to report various activities,initiatives,greeninnovationandtechnology,casestudies,promotionofgreenenterprises,policy analysis, address the roles regarding natural resources management, renewableenergy,sustainabledevelopment,greenmarketing,responsiblebusinessmanagementetc.

Vision

Tobecomeaninternationalenvironmentalknowledgedisseminationplatformforvariousstakeholdersintheprocessofmakingagreenandprosperousplanet

Mission:

Tomakethecommunityawareaboutenvironmentalissues To motivate green enterprises and provide a platform to share, network and

broadenthescopeofgreenbusinessoperations Tocontributeintheprocessofmeetingmillenniumdevelopmentgoals(MDGs)

Editor

Contents

1. Sustainability:GoingBacktotheNature!

‐Dr.P.Koshy………………………………………………………………………………………………..

2. ElectronicWasteGenerationinIndia

‐BhaveshJha……………………………………………………………………………………………….

3. CarbonTradingInIndia–IssuesAndProspects

‐Mr.SumanRoyBarman,AmlanbrataChakraborty................................................

4.GreenMarketing:Strategicsteptowardsbusinessexcellence

‐Mr.BhaveshJha...............................................................................................................

5.WorldSustainabilityReview

1.Sustainability:goingbacktothenature!

‐Dr.P.Koshy1

Going out and travelling in public transport, in order to make arrangements for Green

EnterpriseSummit,thatweplannedtoorganiseonJune23inNewDelhi,facedasetback

owing to extremeheat, someof us gettingdehydrated and if not a sun stroke!Thus,we

postponed the Summit to August 4. We were unable to move in the sun to make the

arrangements.ManysuggestedorganisingitinJunewouldbedisastrousastherewouldbe

very low turnout.MycolleaguesatSamadhanFoundationwerealso finding itdifficult to

facethesun.

Climate change, depletion of ozone layer, green house gases etc are not few keywords

relatedtoenvironmentalsciencesbutareality.

Summerwas too harsh for the people across India this year, especially in theNorthern

region. Togetherwith power cuts and power shortage, lifewas reallymiserable. People

oftenrefusetocomeoutduringthedaytime,exceptthosewhohavenootheroption,who

arepoor,rickshawpullers,informalsectorworkers,manuallabourers,marketingandsales

peopleandseveralotherswhohavenootheroptionotherthanthat.Climatehaschanged

somuch.WinterinDelhiwasreallysoharshlasttime.Anita,mywife,whoisajournalistin

Muscat,cametoDelhitoenjoythewinterseasonkeptontellingmethat ‘sheisfindingit

difficult’andwasillthroughouthervacation.

Climatechangeisareality!What ishappeningnowseemstobea testdose!Theclimate

andtemperaturewouldbeatextremepolesintheyearsahead.

Therefore, livinganenvironment friendly life is something that isbeingadvocated.What

canwedoatindividuallevelstoaddresstheissue?Itcouldbefromusingpublictransport,

whenever it ispossible toavoidingprintingofunnecessarypapers thatwecansurelybe

avoidedarejusttwoexamples.Adoptionofgreenpracticescancomeintoallaspectsofour

life.Itisnotaquestionofadoptionforafewpollutingindustriesalone.

1Dr.P.KoshyisdirectorofInstituteofenterprisedevelopment&research.Hehasgreatinterestandhasbeenworkingforsustainabledevelopmentandgreenpracticesformanyyears.Hecanbecontactedatcaushie@gmail.com

Whenwebuyfoodinthestreet,manyofficegoersdothatinthecitiesthesedays,eatour

lunchonaplasticplatter.Aftereating, it isbeing thrown intosomewastewater flowing

riverorsomestreetcorner.Weareallcontributorstothisclutter.Afteramarriageparty,

theremainingwaste,thatinclude,chicken–muttonandotherfoodwastesareoftenbeing

dumpedintoasmallwaterflow,whichissemidryorinariverwhichhaslittlewater.Sois

thecasewithseveraloftourismbusinessfocusedfivestaror3starandotherhotels.We

canimaginewhatwouldbetheendproduct,whenwaste isbeingpumpedintonnestoa

staticwaterbody.Chickengunia,Dungyandviralinfectionsofseveralothernamesarevery

commoninoursociety.Managingorganicwasteproperlyisoneofthechallengesfacedby

Municipaladministrationsacrossthecountry.

Weneedtolookatthequestionofsustainabilityofoursociety.Howlongwecanhavean

economywhere wewill have to keep on pumpingmoney heavily during a recession in

infrastructure development projects, inmost caseswhich do notmake any sense?More

investmentforsmoothpassageoffastmovingvehicles,and8lanehighwayshavebecome

apriority rather than strengthening thepublic transport system. It is something like the

lopsidedpriorityofourplanningcommissionapparatusheadedbyMontekAlhuwalia,who

spent 3.5 million for toilet renovation at his office, when, crores of Indians defecate in

publicandusestreetcornersandopenspaceas their toilet.Anefficientpublic transport

system would drastically bring down CO2 emissions. When people opt for local trains,

metro trains, trams and buses etc, cars and two wheelers plying on the road would be

reducedsignificantly.Nostudyisrequiredtoprovethis.DelhiMetroisthebestcaseinthis

regard.

However,throughouttheworldtrendistoexpandtheeconomicactivitiesandcreatejobs

somehowthoroughallpossibleinvestmentsandexpansionofphysicalinfrastructure.But

creatinggreenjobsisthechallengeoffutureinnovatorsandentrepreneurialclass.

Buildingthebiggeststructureiswherethecompetitionforandhiddencorporateagenda

andnationalagendasofgovernmentslies.Plannershavetofocusonplanningforbuildinga

greeneconomyratherthandoingthingswhicharenotreallytheirjobs,likeMontekSingh

AhluwaliaworkingforthecauseofFDIinretailcausingthedestructionofmillionsofstreet

vendors,smallretailsectorwhichuseveryminimalpowerandstillhelpmovethiscountry

unlike the large retail chains who would contribute more harm to the environment. In

Germanyandinseveralpartsof theworld,evenintheUS,peopleareagainstWALMART

notjustfortheircontributiontojoblessgrowthbutalsoforenvironmentalrelatedreasons.

WALMART is almost out fromGermany butMontekwants them in India.It has nothing

muchtodowithasustainabledevelopmentagendabutseemslikemoreofpersonalagenda

anddoingaconsultancyjob.

ButwhenmyfriendSudharshanGeorgewhoisresettlinginIndiaafterlivinginGermany

foroveraperiodof14yearsrefusetobuyaprivatevehicle.HeislivinginHyderabadand

usingpublictransport.Similarly,mycousinwhocamebacktoBangloreafteraperiod10

yearsofstayinUS,BinduandSanjay,insistontravellinginpublictransport.But,manyof

usarefindingitdifficultwithoutaprivatevehicle.

AirConditioners:aretheyreallyrequired?WillACsenhanceourefficiency?Iamnotsure.

ButAir‐Coolerswillgraduallydisappear,ifthetrendcontinues!

Greening the earth is a challenge. Going to offices using buses, metro rail/local train,

bicyclesandusingaircoolersratherthanACsarejustfewareasatpersonal levelwecan

contributeinprotectingtheenvironmentandasustainablegreenfuture!

2.ElectronicWasteGenerationinIndia

‐BhaveshJha2

Abstract

Increasinguseofinformationtechnologyanddaytodaynewinnovationsintechnological

sector has increased a hidden burden on the social and environmental front. Changing

lifestyles and increasing demand of white goods around the world have increased

technological obsoleteness every day.Managing outlivedwaste electrical and electronics

equipment have become a big challenge for the government and private sector entities.

With a boom in IT sector and rapid industrialisation, Indian electronic wastemarket is

increasingatarateof20%perannum.Differentstudiesshowaboutthisincreasingtrend

in the major cities. Electronic waste inventory management at the local level is a big

headacheforgovernments.Mostoftheelectronicwastescometoinformalsectorrecyclers.

Manyofthereasonsincludeabetterpriceforconsumer.Butthehandling,abstractionand

disposal systemof an informal recycler is very unhygienic for the environment. Strict

enforcement of different laws on producers’ responsibility and awareness generation

among the huge informal sectorworkforce about the hazardous impact of ewaste, safe

handling practices etc. are of immense importance. Governments and nongovernmental

organisationswillhavetoworkonastrategytomitigatethenegativeimpactsofelectronic

wasteinthesociety.

KeyWords: Consumerism,WEEE,TechnologicalObsoleteness, ElectronicWaste,Techno

Trash,WasteInventory,Environmentalhazards,WasteScenario,Management

ConsumerismandEwaste

The increasing economic growth and changing consumption trends worldwide have

resultedinasignificantriseinthedisposableincomesandconsumers’propensitytospend.

Theadvancementintechnologyandchanginglifestyle,statusorperceptionofconsumers

has driven this demand of electronic items. Consumers’ dependency on information and 2Mr.BhaveshJhaisanMBAinBusinessSustainabilityManagement(MBA)fromTERIUniversity,TheEnergy&ResourcesInstitute.Hehasakeeninterestinenvironmentandsustainabledevelopment,Environmentalandsocialimpactassessments,innovation,socialentrepreneurshipetc.Heisworkinginenvironmentalsector.Hecanbecontactedatbhaveshjha08@gmail.com

communication technology has been increasing very rapidly. The new innovations in

informationtechnologybecauseoftherisingdemandforhigherefficiencyandproductivity

in thebusinessesandworkhavebecomeamatterofday today life.Technologieswhich

werenewyesterdayhavebecomeobsolete for today.The increase indemand for “White

Goods segment” i.e. on consumer durables such as television sets, microwave ovens,

calculators,air‐conditioners,servers,printers,scanners,cellularphones,computersetc.is

forobvious.Thus, therecanbebroadrangeofwasteelectricandelectronicgoodswhich

have outlived their use, ready for disposal. These contain chemicalmaterials considered

hazardous forhumanwellbeingsandnatural environment.The increasing rateofwaste

electronic products and additionally the illegal import of junk electronics from abroad

createacomplexscenarioforsolidwastemanagementinIndia.

AccordingtoMinistryofenvironmentandforest(MoEF),E‐wasteissuchwastecomprises

ofwastesgeneratedfromusedelectronicdevicesandhouseholdapplianceswhicharenot

fitfortheiroriginalintendeduseandaredestinedforrecovery,recyclingordisposal.

Indianewastetrends&Scenario

TheIndianelectronicwasteindustryisboomingataveryrapidpace.It isexpectedtobe

increasingatarateof20%annually.Withincreasingpercapitaincome,changinglifestyles

andrevolutionsininformationandcommunicationtechnologies,Indiaisthesecondlargest

electronicwastegeneratorinAsia.Indiaisgeneratingaround4,00,000tonesofelectronic

wasteperyear according toMinistryofEnvironment andForestMoEF.Not only this, it

getsaround50,000tonesofewastethroughillegalmeansofimports.Accordingtoareport

on electronicsmarket, TATA StrategicManagementGroup says that India is expected to

have11%shareinglobalelectronicmarketby2020.

MoEF’2012reportsaysthatIndianelectronicwasteoutputhasjumped8timesinthelast

seven years i.e. 8, 00,000 tones now. India has majorly two types of electronic waste

marketcalledorganizedandunorganizedmarket.90%oftheelectronicwastegeneration

inthecountrylandsupintheunorganizedmarket.Andoutofthisonly5.7%ofewasteis

recycled.Electronicwasteaccountsfor70%oftheoveralltoxicwasteswhicharecurrently

found in landfillswhich is posing toxic chemical contamination in soil and other natural

resources. Another report from Central Pollution Control Board CPCB says that around

36,165 hazardouswaste generating industries in India accounts for 6.2million tones of

toxicwastes every year. Indian PC industry is growing at a rate of 25%annually as per

MAITstudy.

OutofthetotalelectronicwastegenerationinIndia,only40%ofthesearetakenintothe

recycling processes and rest 60% remains in warehouses due to inefficient and poor

collectionsystems.Generally,peoplehandoverelectronicwastetounauthorizedrecycling

centres/scrapdealersetc.forquickmoney.Thee‐wastescrapismanagedthroughvarious

managementalternativessuchasreuseofequipmentfromsecondhanddealers,backyard

recycling(manualdismantlingandsegregationintoplastic,glassandmetal)andfinallyinto

the municipal dumping yard. MAIT (Manufacturers Association for Information

Technology)studysaysthatwastefromdiscardedelectronicswillrisedramaticallyinthe

developingworldwithinadecade,withcomputerwasteinIndiaalonetogrowby500per

cent from2007 levels by 2020.Over100,000 tonnes from refrigerators, 275,000 tonnes

fromTVs,56,300tonnesfrompersonalcomputers,4,700tonnesfromprintersand1,700

tonnesfrommobilephone.

Techno‐Trash

The electronic waste due to Computerwaste also called techno trash is becomingmost

significant of all e‐waste due to the quantity as well as the fast generation rate. The

computer hardware sector has displayed an unusual growth in the past few years

maintainingpacewiththerapidgrowthinthesoftwaresector.Thecontinuousinnovations

andtechnologicalupgradationsinthehardwaresegment,obsolescenceriskremainsakey

areaofconcernforcompaniesthathavemadehugeinvestmentsintheirITsystems.

Management

ManagingElectronicwastehasbecomeaverybigchallenge.Theincreasingenvironmental

concernsand illeffectsofelectronicwasteonnaturalresources(soil,air,wateretc.)and

community at large has become an important issue to deal with. The governments and

private sector organisationswill have to play a crucial and responsible role in order to

properlymanageelectronicwaste.Properinventorisationandmanagementatlocallevels

has been very necessary in order to reduce the negative impacts of e waste in human

livelihood.GovernmentandprivateplayerscantieupwithdifferentNGOsworkinginthis

sectorandgetconsultationwithdifferentE‐wasteexperts.Throughaproperassessmentof

unorganisedsmallscaleindustrialhouses,theymaygettheactualloopholesinthesystem.

Safe handling and disposal trainings should be provided to the unorganised recyclers.

Different awareness programmes and reach to the grass roots level unorganised sector

recyclerscanplayapivotalroleinefficientlymanagingewaste.

References

i. MAIT‐ GTZ E Waste Study Summary http://ewaste.mait.com/wp‐

content/uploads/2012/04/MAIT‐GTZ‐e‐Waste‐study‐summary.pdf,(Online)

ii. April4,2012,ThetimesofIndia(http://articles.timesofindia.indiatimes.com/2012‐

04‐04/pollution/31286986_1_total‐e‐waste‐automatic‐dispensers‐electronic‐tools),

(Online)

iii. E Waste Management Report, UNEP;

http://www.unep.or.jp/ietc/GPWM/data/T3/EW_1_2_WEEE_EwasteMngtRprt.pdf,

(Online)

iv. EWasteinIndia;Toxicslink;http://www.toxicslink.org/docs/06040_repsumry.pdf,

(Online)

v. Sustainable Development in India: MoEF, 2011,

http://www.uncsd2012.org/content/documents/Sust_Dev_Stocktaking.pdf,

(Online)

3.CarbonTradingInIndia–IssuesandProspects

‐Mr.SumanRoyBarman3

‐Mr.AmlanbrataChakraborty4

Abstract

Global warming is changing the global climate much faster, affecting living organisms.

Environmentalist, policymakers and general public are emphasizing on global policy for

protectingnaturalenvironment.Butdespitesuchemphasisauniformconsensus isyetto

bemade. EmissionofCarbondioxide toahugequantity ismainlyresponsible forGreen

HouseGas(GHG)productionaswellasglobalwarming.Carbontradingisthewaythrough

whichglobalwarmingcanbereducedtoalargeextent.Carbontradingisthoughttobean

alternativetolimittheemissionlevelofGHG,asresolvedintheKyotoprotocol.Themain

issueofKyotoprotocolhasbeen to control emissionsofGreenHouseGases (GHG) from

various industrial units throughout the world. The purpose of this paper is to analyze

prospectsofcarbontradinginIndiaaswellastherelatedissues.

KeyWords:Carbontrading,GHG,globalclimate,globalwarming,Kyotoprotocol

Introduction

Inrecentyearsglobalwarminghasbeenthemaincauseofglobalclimatechange.Theterm

globalwarmingisaprocess.Itisstatedthatthesun'sradiationcomesalongwithlightand

heatsupourplanet.Radiationthatiscomingisabsorbedanditwarmstheearthandgoes

backintospaceintheformofinfraredradiation.Someoftheoutgoinginfraredradiationis

actually trapped inside in our atmosphere. Due to this phenomenon, our environment

maintains certain temperature but problem occurs when the majority of the infrared

radiation is trapped insideatmosphereand it increasesthetemperatureandatmosphere

worldwide. This phenomenon causes climate change. Global warming is having serious

affectsandconsequencesandtheseareseawaterlevelrise,droughts,floods,storms,and

heat waves and tsunami. Developing countries are usually less prepared in facing

3Mr.SumanRoyBarmanisaresearchscholar,Dept.ofManagement,MonadUniversity,UttarPradesh.Hecanbecontactedatsrb_agt@rediffmail.com4Mr.AmlanbrataChakrabortyisaresearchscholar,Dept.OfCommerce,TripuraUniversity,[email protected]

environmental consequences. Developing countries are likely to be affected by volatile

cropproductionandecosystem.Thefactorscontributingtoglobalwarmingareexcessive

emissions of carbon dioxide and other GHGs such as methane, nitrous oxide, sulphur

hexafluoride,hydroflurocarbon.Tosavetheplanetfromtheimpactofclimatechange,itis

necessary to lessen the levels of emissions of GHG to a large extent. To accomplish the

objective the concept of CDM (Clean Development Mechanism) came into existence.

In1997, theKyotoprotocolorganizedby theUnitedNation'sFrameworkConventionon

ClimateChange inKyotowith anaim to reduceemissionsof greenhousegases and184

countries became committed to that protocol. The agreement came into force on 16th

February2005.Itwasdecidedthat,ifcommercialindustriesemitmorethanthepermitted

limit of carbon dioxide, should lower their emissions as per the prescribed limits,

otherwise they should buy carbon credits certificates. There is a provision that carbon

credits canbe sold or bought in themarket; if not then carbon taxwill be charged. It is

presumed that developed countries have beenmainly responsible for the high levels of

greenhousegasesemissions.Soonbasisofthatemissionlevelaccountabilityislikelytobe

assigned. The major resolution of Kyoto protocol is carbon trading, Clean Development

Mechanism(CDM)andJointImplementation(JI).

Objectives

Theobjectivesofthepresentpaperare:

1.TostudytheissuesandchallengesassociatedwithcarbontradinginIndia.

2.ToknowtheprospectsofcarbontradingofIndianIndustries.

ReviewofLiterature

S.PGonchaudhury,greenenvironmentalistofIndiaandalsotheManagingDirectorofWest

BengalGreenEnergyDevelopmentCropsaid,"Thesentimentswouldbebullishforcarbon

trading,BarakObama,theUSPresidentshowsabitofaggressivenessontheissues".

TimGroser,ClimateMinisterofNewZealandstated,"itistimeforgreengroupsaroundthe

worldtostarttoanalyzeclimatechangeproblemonthebasisofnotoftherhetoricofthe

90s,butsumnumericalanalysisofwheretheproblemliestoday".

Lord Nicholas Stern, former World Bank’s Chief Economist also opined that, "poorer

countriesalongwithChinaand Indiamust stepup to their responsibilities. It is abrutal

arithmetic – the changing structure of the world’s economy has been dramatic. That is

somethingdevelopingcountrieswillhavetofaceup".

ResearchMethodology

Secondary data has been used from various sources to analyze the current position of

carbontradinginIndia.Thedescriptivestudyhasbeenusedinthispaper.

CarbonTradingThroughouttheWorld

The United Nations Framework Convention on Climate Change (UNFCCC) has divided

countries/signatoriesoftheKyotoprotocolundertwomajorgroups.Annex–1Countries,

includingUnitedStatesofAmerica,UnitedKingdom,Japan,NewZealand,Canada,Australia,

Austria,Spain,FranceandGermanyetc.

Fourty‐onecountriesagreedtoreducegreenhousegasemissionsby5.2%belowtheir1990

emissions levels. Annex– 2 countries, which are in a sub group of Annex‐1 countries,

include24countriesbutexceptcountrieswith‘EconomiesInTransition’(EITs).Annex–2

countries are committed to buy emission credit fromdeveloping countries if they fail to

reduce predetermined emission levels. Developing countries fall under the category of

Non‐Annex‐1countries,includingIndia,SriLanka,Afghanistan,China,Brazil,Iran,Kenya,

Kuwait , Malaysia, Pakistan, Philippines, Saudi Arabia, Singapore, South Africa etc. A

number of 145 countries do not have any immediate restrictions under the UNFCCC.

Howeverthisclassificationisaimedtowardsanumberofcertainpurposes.

i. Toavoidrestrictionsongrowth,aspollutionisstronglylinkedtoindustrialgrowth,and

developingeconomiescouldpossiblygrowfast.

ii. To restrict above mentioned countries in selling emissions credits to industrialized

nationstopermitthosenationstoover‐pollute.

iii. iii. To avail of money and technologies from the developed countries as listed in

Annex–2.

SignatoriesoftheKyotoprotocol(Annex–2countries)committedtolimitemissionsand

emissionreductiontargets.ThesepredeterminedtargetsaretermedasAssignedAmount

Units (AAUs), intended tomeet stated objectives during 2008 – 2012. Emission trading

allowscountries;thosehaveemissionunitsinexcess,toselltheseexcessunitstocountries

thoseareovertheirtargets.ARemovableUnit(RMU)meansanemissionallowanceswhich

areproducedinadditiontoAssignedAmountUnits(AAUs),asaresultofanincreaseinthe

National SinkPerformance5 Aforestation and Reforestation are the parameters based on

which ‘ARemovableUnit’ (RMU) is calculated. After completion of Joint Implementation

(JI) projects between two industrialized countries, Emission Reduction Units (ERU)

certificates are issued. A Certified Emission Reduction (CER) certificates derive after

successful completion of CDM projects. Every signatories under the Kyoto protocol are

neededtomaintainreservesalongwithERUsandCERs.

Carbondioxide (CO2),methane (CH4),nitrousoxide (N2O),hydro fluorocarbons (HFCs),

perflurocarbons (PFCs) and sulphur hexafluoride (SF6) are main six greenhouse gases

,thoseare required tobe reducedby thecountriesaswasagreed in Kyoto.Quotashave

beenfixedforallcountries(exceptNon‐Annex1countries)toemittheGHGsintheair.To

encouragegreenenvironmentfriendlybusinessactivities,carboncreditsandcarbonoffset

wereintroduced.Theconceptofcarboncreditorcarbonemissionallowancedevelopedin

implementationofCleanDevelopmentMechanism(CDM).Onecarboncreditpermitsone

tone of carbondioxide (CO2) or otherGHGs to be emitted in the air. Let us consider an

example,a coal‐based companywhich is generatingpower, is in fact generatingone tone

carbondioxideforeachonekilowattpower.Thesamecompanymayproduceonekilowatt

power through windmill then it reduces one tone CO2. For one tone reduction in

generationofcarbon‐‐dioxideonecarboncreditorcarbonemissionallowancetobegiven

to the country which reduced carbon dioxide emission, in way of certificates, who less

pollutestheenvironmentbyonetonecarbondioxide.Industriesthoseexceedorcrossthe

limits of prescribed quotas must buy carbon credit for excess discharge of GHGs, while

5A carbon sink is a natural or artificial reservoir that accumulates and stores some carbon‐containingchemicalcompoundforanindefiniteperiod.Theprocessbywhichcarbonsinksremovecarbondioxide(CO2)from the atmosphere is known as carbon sequestration. available inhttp://en.wikipedia.org/wiki/Carbon_sink

thosebelowprescribed limits can sell their carbon credits.Under international emission

trading mechanism countries have been enabled to trade in the international carbon

trading or carbon emission allowance market. For this purpose exchanges (like stock

exchange)havebeenestablished.

AccordingtoTable1TotalnumberofprojectsregisteredwithUNFCCCis7128uptoJuly

2013.Total Number of registered projects in India is 1342 and total number of CER s

issued to Indian Projects is 182.55Mn.China covers 51.64% of total number of projects

registeredwithUNFCCC,Indiaaccountedfor18.83%andBrazilcovers4.21%ofthetotal

registered projects during 31st July, 2013. Carbon trading encouraging worldwide

industriestoreduceharmfulemissionsofgreenhousegasestomaketheplanetmoreeco‐

friendlyandthusindustriesarebecomingmorefinanciallysoundbysellingcarboncredits.

FromtheFigure1, it isevident thatUnitedKingdom(31.07%) is themajor investor in

CDMfollowedbySwitzerland(20.78%)andJapan(9.47%)respectively.Manyindustries

showing their interest to adopt carbon trading toll and governments are also taking

initiativestoreducegreenhousegasemissions.Carbontradingisacollectiveglobaleffort

toconductgreenbusinesswithaminimumadverseeffectonourenvironment.According

totheBloombergNewEnergyFinance(BNEF)report,globalcarbonmarketfellby36%in

2012to61billioneuro.TheTable1alsoindicatesthepositionofCDMprojects.Chinaleads

with 3681 registered projects followed by India 1342 projects and Brazil 300 projects

respectively.

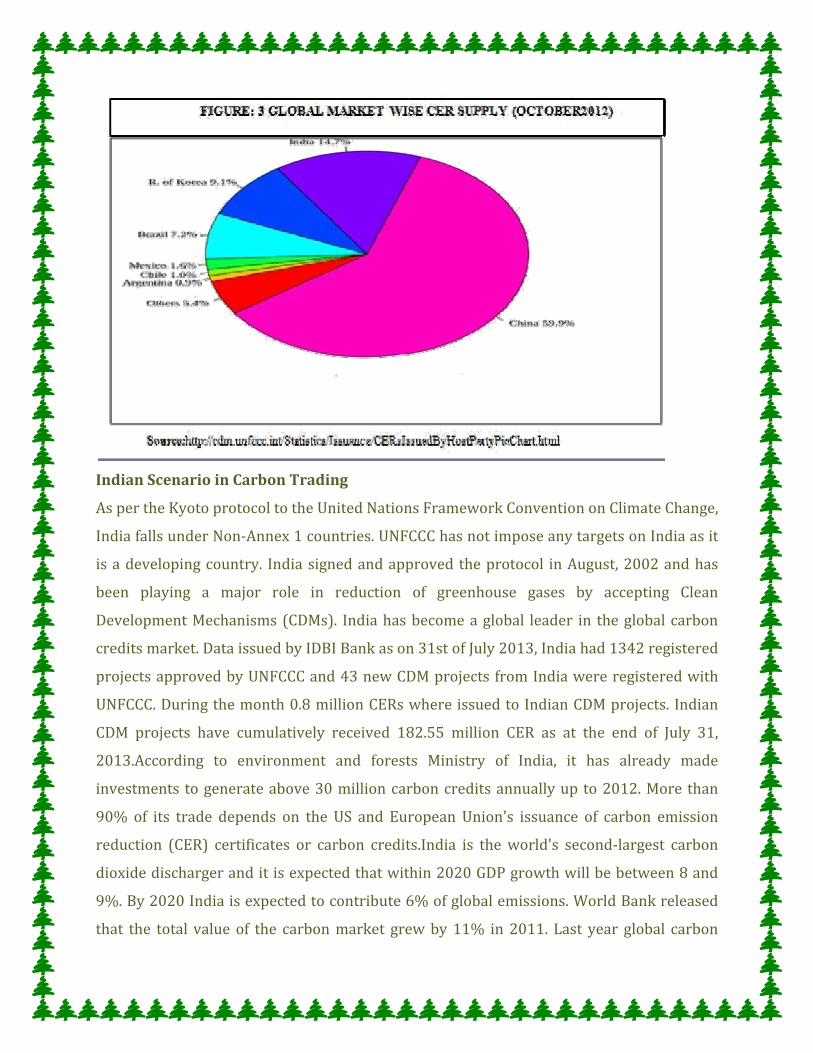

Figure 2 shows China is the biggest CER supplier in Asia. India and South Korea hold

secondandthirdpositionsrespectively.AccordingtoFIGURE3,Chinaholdsno.1position

with 59.9% of CER supply followed by India 14.7% and Republic of Korea with 9.1%

respectively.Ason31stofJuly2013,datareleasedbyUNFCCC‐‐1,365,586,552CERs

were issued. Out of 7590 CDM project 7128 projects are registered, 89 projects are

requestedforregistration,343projectsarependingforpublicationsand28projectsare

requestedforreviewwhereas2arerequestedforcorrections.

IndianScenarioinCarbonTrading

AspertheKyotoprotocoltotheUnitedNationsFrameworkConventiononClimateChange,

IndiafallsunderNon‐Annex1countries.UNFCCChasnotimposeanytargetsonIndiaasit

isadevelopingcountry. Indiasignedandapprovedtheprotocol inAugust,2002andhas

been playing a major role in reduction of greenhouse gases by accepting Clean

DevelopmentMechanisms(CDMs). Indiahasbecomeaglobal leader in theglobalcarbon

creditsmarket.DataissuedbyIDBIBankason31stofJuly2013,Indiahad1342registered

projectsapprovedbyUNFCCCand43newCDMprojectsfromIndiawereregisteredwith

UNFCCC.Duringthemonth0.8millionCERswhereissuedtoIndianCDMprojects. Indian

CDM projects have cumulatively received 182.55 million CER as at the end of July 31,

2013.According to environment and forests Ministry of India, it has already made

investments togenerateabove30millioncarboncreditsannuallyup to2012.More than

90% of its trade depends on the US and European Union's issuance of carbon emission

reduction (CER) certificates or carbon credits.India is theworld's second‐largest carbon

dioxidedischargeranditisexpectedthatwithin2020GDPgrowthwillbebetween8and

9%.By2020Indiaisexpectedtocontribute6%ofglobalemissions.WorldBankreleased

that the total valueof the carbonmarket grewby11% in2011. Last year global carbon

credit trading was estimated at $ 5 billion. India has surplus carbon credits to sell to

developed countries. Industrial harmful products aremainly responsible for increase in

greenhouse gases by 60 to 70%, which adversely affect the ozone layer. Steel, cement,

power,textile,fertilizeretc.Industriesemitgreenhousegasesintheair.Chemicalplants,

windmill, biodiesel, bio gas, waste disposal units, plantation companies can generate

carboncreditsandearnmoney.ManyIndiancompaniesareshowingtheirinterestinCDM

toenjoythebenefitsofcarbontrading.Fewofthemareasfollows:

1. Jindal Vijay Nagar Steel: It has announced by the plant that with the next 10

years itwill be able to sell $ 225millionworth saved carbon. Thiswasmade

possible as their plant uses the corexfurance technology which restricts 15

milliontoneofcarbonemitsintotheatmosphere.

2. Powerguda in Andhra Pradesh: The village in Andhra Pradesh sold 147 MT

equivalent CO2 credits. This was possible by extracting biodiesel from 4500

pongamiatreesinrespectivevillage.

3. Handia Forest in Madhya Pradesh: In Madhya Pradesh it is estimated that a

numberof95verypoorruralvillageswouldjointlycontributeUS$300,000

every year from carbon emissions by restoring 10,000 hectares of degraded

communityforests.

RecentlytheUNFCCChasapprovedworld’slargestConcentratedSolarPower(CSP)project

ofReliancePowerasapartofemissionsoftradingscheme.ReliancePowerhasalreadygot

CDMregistration.ThiswillallowtheprojecttogenerateandsellCERsandinturnReliance

Power will earn revenues. Its power production capacity is expected to be more than

12,000MWwithapotential ability to generate60million carbon credits.TheReliance’s

CSPprojectinRajasthanisthelargestinvestmentofthiskindhaseverbeenmadebyany

privateentity.

TheMultiCommodityExchange(MCX),largestcommodityexchangeofIndiahasinitiated

futures trading in carbon credits on January 2000. From 11 April 2008, National

CommodityandDerivativesExchange(NCDEX)alsohasbeeninitiatedcarbontrading.Itis

expected that the National Commodity and Derivatives Exchange will help Indian

companies to earn more CERs from the rest of the world. According to IDBI, Carbon

DevelopmentNewsletterofAugust2013,Indiahasregistered1342projectswithUNFCCC

and182.505millionCERsalreadyhavebeenissuedtothoseregisteredprojects.

FutureImpactonCarbonTrading

First phase of Commitment made by the countries of Kyoto protocol ended on 31

December 2012. Many questions have been raised about the future of the Clean

Development Mechanism (CDM). This doubt was made clear in Durban where it was

decided that Kyoto protocol will be continued to the end of 2015 and thereafter new

instrumentwillbeadoptedforcarbontrading.SincetheCancunclimateconference,which

was held on Mexico from 29th November to 10th December 2010, CDM has been

witnessingseveralreformswhichwouldchangethismechanismovertime.Thesechanges

werefurtherstrengthenedinconferenceoftheparties‘COP17’inDurbanand‘COP18’in

Doha.Thesechangeswillenhancefutureofcarbontradingininternationalscenario.

TheEuropean Unionwas committed to reduce20%greenhouse gas emissionsby2020

from the 1990 level as against target of 5.2% set by Kyoto protocol by 2012. But few

membercountriesEuropeanUnionhavegoneagainstthecommitmentandhaveaskedto

set a lower target. If it is considered to reduce the emission level then it will affect

worldwide carbon trading. The report released byWorld Bank and the carbon expo at

Cologne, Germany describes how even worldwide economic turbulence, global carbon

market increased in 2011. The largest segment of the carbon market was that of EU

Allowances (EUAs) valued at $ 148 billion. Therewas also a substantial increase in the

volumeofsecondaryKyoto‐‐offsets(whichgrewby43%,to1.8billiontonesofCO2valued

atUS$23billion) fueledby increased in theCertifiedEmissionReduction (CER)market

andinthenascentsecondaryEmissionReductionUnit(ERU)market.Withtheendofthe

past commitment period of the Kyoto protocol in 2012, the post – 2012 primary CDM

marketincreasedbyarobust63%,toUS$2billiondespitedepressedpricesandlimited

long‐termvisibility.

The major carbon credit trading agency Lehman Brothers, USA immediately after filing

bankruptcy protection in September, closedown its carbon trading activities and many

othersfolloweditgivingaknockoutblowtothecarboncreditmarket.Figure4shows33%

respondents expect that India’s CDMmarket will grow where as 27% thinks that CDM

marketwillfall.37%respondentsopinedthattherewillbenoconsiderablechangeand5

% respondents were unsure about change in rate of Indian projects registered with

UNFCCCafterSecondcommitmentperiodofKyotoprotocol.

AccordingtoenvironmentministryofficialofIndia,initiativesaretakentoearn450million

carboncreditsby2020.Thetotalvalueofthecarbonmarketgrewby11%in2011,toUS$

176billionandtransactionvolumesreachedanewhighof$10.3billionofcarbondioxide

equivalent (CO2e) according to World Bank releases State and Trends carbon market

report2012.

MeanwhilethereareallegationsaboutmalpracticesinCarbonTradinginIndia.According

toAyesheaPerera,"MillionsofcarboncreditstradedbyIndiaandusedtooffsetemissions

inthedevelopedworldmaynotactuallyexist."ShealsoaddedthatAWikileakscablefrom

2008hasrevealedthatanumberofprojectsthattradeincarboncreditswereineligibleto

dosoandarenotthereforetradingin‘real’credits.Thecablesaysmostofthecarbon‐offset

projectsinIndiafailtomeettheCDMrequirementssetbytheUNFrameworkConvention

on Climate Change. It also describes the UN’s validation and registration process as

“arbitrary”.

Conclusion

CarbonTradingmustnot be seen as a compensatorymeasureof developed countries to

developingcountries.The largestpollutantof environment is industrial sectoraswell as

transport and communication .If it is thought that developed countries will continue to

increase industrialization in different states and developing as well as underdeveloped

countrieswillcompensateontheirbehalf,couldnotbeapropheticthought.Environmental

pollutionisnotaregionalissue,itisaglobalissue.Sotheprocessofindustrializationand

system of manufacturing should develop in an environment friendly way so that

environment pollution could be controlled. If nature moves out of control as has been

witnessed in various parts of theworld, then carbon trading will be useless andwhole

affect will be upon agricultural and allied commercial activity. In case of India a

comprehensiveCarbon tradingpolicy isyet tobe framed. It ismost important, that such

policyframeworkshouldimmediatelymake.

Reference

1."IndiaawaitsObama’sstandongreenenergyforcarbontradingprospects"byIndronil

Roychowdhury:Kolkata,Dec252008

availableinhttp://www.financialexpress.com/news/india‐awaits‐obamas‐stand‐on‐

green‐energy‐for‐carbon‐trading‐prospects/402646accessedon4.Sptember2013.

2."LordStern:developingcountriesmustmakedeeperemissionscuts"byFionaHarvey,

TheGuardian,Tuesday4December2012availablein

url:http://www.theguardian.com/environment/2012/dec/04/lord‐stern‐developing‐

countries‐deeper‐emissions‐cuts

4.ibid.

5."KyotoProtocol"RetrievedSptember4,2013from

http://en.wikipedia.org/wiki/Kyoto_Protocol

6."Wikileaks:HowIndiaismanipulating

carboncredits"byAyesheaPerera

RetrievedSptember4,2013fromhttp://www.firstpost.com/politics/wikileaks‐how‐

india‐is‐manipulating‐carbon‐credits‐94984.html

7."Carbonsink"RetrievedSptember4,2013fromhttp://en.wikipedia.org/wiki/Carbon_sink

4.GreenMarketing:Strategicsteptowardsbusinessexcellence

‐BhaveshJha6

Abstract

Greenoreco‐friendlyproductsareproducts friendlytotheenvironmentandhaveaverylittle or nil impact on the environment. In the last few decades, the stricter rules andregulationandglobalpressuretomitigateanddecreasethecarbonemissionsalloverhasencouraged the corporate to look into the issue of depleting natural resources andenvironmental diversity. These days, Green has become a password for companies topromote their products and services in the market. The study shows the consumers'perception about green or eco labelled products and their buying behaviour trendsaccordingtotheavailabilityorcapabilityoftheconsumers.Obviously,anethicalbusinessoperation,production,andmarketingofgreenproductspursueaconsumertochangehis/herbuyingdecisionandtheirperceptionabouttheproducts.Corporatemayseethisasanopportunity to enhance their brand value and make a competitive edge over theircompetitors.Therespondentssayaboutthegapsininnovation,researchanddevelopmentpracticesofgovernmentandcorporateandhowtheyeyewashconsumersbythenameofgreenandsustainableproducts/services,especiallyinthedevelopingandunderdevelopedeconomies.Throughaproperinvestmentinresearchanddevelopmentonly,corporateandgovernments would be able to enhance their environmental efficiency and costeffectivenessinthemarket.Awarenessandavailabilityofgreenproductsandservicesanditspositivebearingontheecologicaldiversityofeconomycanplayasignificantrole.Thereis a need of stricter policymeasures and regulations, third party affect assessment andenvironmental auditing on the produced products. An interactive platform with theconsumersinthisregardtocommunicateanderadicatethenegativityfromtheirmindscanplayabigroleinintroducingasustainablelivelihoodinthesocietyatamicrolevel.

JELClassification:D11,E21,K32,L1,M31

KeyWords:Sustainableconsumption,EcofriendlyProducts/Services,PerceptionBuilding

6 Mr.BhaveshJhaisanMBAinBusinessSustainabilityManagement(MBA)fromTERIUniversity,TheEnergy&ResourcesInstitute.Hehasakeeninterestinenvironmentandsustainabledevelopment,Environmentalandsocialimpactassessments,innovation,socialentrepreneurshipetc.Heisworkinginenvironmentalsector.Hecanbecontactedatbhaveshjha08@gmail.com

1. IntroductionMarketalwayslooksforanopportunityandcomesupwithnewproductsorserviceswithnewpackage tomeet theneeds andwants of consumers.Greenhasbecomeapasswordthesedaysforalmosteachproductorservicestoplayupon.Nodoubtgreeningproducts/process/serviceshasbecomeverysignificantdue to the increasingcarbonemissionandglobal warming's negative affect on the society and environment. Gradually the greenorientedawarenessamongthepeopleandtheirconsciousnessabouttheenvironmentalilleffectwouldplay a crucial role in forming a perception about green and an eco‐friendlyproduct.Theperceptionwouldleadtoaresponsiblepurchasingpatternandthusthegreenwould become a hot cake in the market. Products with less carbon emission in theirformationhavebeenindemand.Greenproductsandservicesobviouslyprovideavaluetoa customer. In addition, it puts an extraburdenon thepockets of consumers.The studyshows the impacts of green products or services and different marketing variables likeproduct, packaging, distribution, promotion etc., in the consumption trends and buyingbehaviour. This would also deal with other factors associated with the buying decisionprocessforaconsumertoconsumeagreenproductorservice.

2. LiteratureReview

American Marketing Association defines green marketing as marketing of products andservicessafetoenvironment.Thisconsistsofalargeno.ofactivitiesundermarketingmix.The elements like product, place, pricing, promotion and distribution are primarilyconsidered in theprocessofofferinggreenproductsand services forenvironmental andsocialbenefitsviz.toreducewaste,increaseenergyefficiency,decreasetoxicemissionsetc.Over the few decades, consumers’ environmental concerns have risen (Gerard andEdmund,1998).Thisconcernhaspushedcorporatetorespondwithenvironmentfriendlyproducts,processes,promotionanddistribution.Nowgreenmarketinghasbecomeapartandparceloftheoverallcorporatestrategy(MenonandMenon,1997).Hwang,McDonaldandOates(2008)foundattitude/behaviourgaporvalues/actiongap,wherearound30%of consumers reported to have concern for environmental issues. But still people arestruggling to translate this concern into their purchases due to various factors viz.

Consumers' demographics (Age, gender, Education etc.)

Green Marketing elements (Product, packaging, Distribution,

promotion etc.)

Influencing Purchase Decision

availability, options, value of money, unawareness about the benefits etc. Increasingenvironmental knowledge and information about the ill impacts of natural resourcesdegradationhasencouraged this consciousness in themarketplace.The increasinggreenmarketsegmentpushestheconfidenceofcorporatetoincreasetheirgreenactivitiesintheproducts’ offering process. JacquelynOttman in his book, ‘GreenMarketing:OpportunityforInnovation’saysthatenvironmentalconsiderationsmustbeintegratedintoallaspectsofmarketing from theproductdevelopmentprocess to the communicationchannelsandshould be inclusive towards all the stakeholders. Consumer satisfaction, product safety,social acceptance and sustainability of products are few benefits of green marketingstrategy (Peattie, 1995). Green marketing strategy provides differentiation in terms ofcompetitiveness, long term sustainable presence, synergy and brand visibility in themarket. The paper has been written to understand consumer buying behaviour for ecofriendlyproductsandaddresstheconcernsforenvironmentaldegradation.

3. GreenorResponsibleConsumption

Responsibleconsumptionisanethicalresponseofaconsumerforaparticularproductorservice. Responsible consumption covers a macro view related to different activities inboth productions and consumption patterns. Some of the processes include recycling ofmaterials, efficient use of energy, protection of environment and the preservation ofbiodiversity etc. Thus Green consumption startswith purchasing products essential andenvironmentfriendly.Theseproductsarenotharmfultohumanhealthand,savedifferentkindsofexpenseslikeexpensesonpower,fuelanddisposal.Astheawarenessaboutgreenproducts and services is increasing, the responses from the consumer have been veryfavourable. Promotions on greener lines have been capturing market rapidly. Theresponsible consumption could not only preserve our environment but also boost oureconomyinaninclusivemanner.In this regards, some of the responsible behaviour of consumers and guidelinesforaresponsibleconsumptioncanbeexhibitedas:

i. Do not purchase unnecessarily. Reconsider before you purchase aproduct: Sinceproduction, process needs a big quantity of resources orexpenses, which can be saved, and the wastages as left products can bereduced.

ii. Chooseaproductwhichismoreenvironmentsfriendly:Differentgreenlabels are available tomake you aware about the substances used in theproduction. Different substances like heavy metal, chlorinated organiccompoundsetc.areveryharmfultoenvironmentandsociety.

iii. Preferaproduct forwhichrawmaterialshavebeenobtainedwithaminimum environmentaldestruction: In the process of obtaining rawmaterials,theconductsofbusinesseshavebeenveryunethical.Companies

miss‐utilizethenaturalresourcesandtheyhavenosenseofresponsibilityattachedwiththeiroperations.

iv. Chooseaproductwhichismoreenergyefficient:Productsusingnaturalresources likeoil orelectricity (thermalpower) shouldalwaysbe chosenonthebasisoftheirenergyconsumption.DifferentenergyratingsbyBEE(BureauofEnergyEfficiency)inthisregardsshouldbealwaysconsidered.

v. Chooseaproductwhichiseasyrecyclable:Inordertoreducewasteandits implicationson theearthandnatural environment.We should alwaysconsider a product which can be easily recycled and does not have anegativeimpactondisposal.

vi. Always try tochoosearecycledproduct: Productionof anewproductwith recycled resourcesor scrapsorwastesare called recycledproducts.Graduallywith increasing awareness levels and responsible consumptiontrends in the market would broaden the market of producing recycledproducts.

4. ImportanceofGreenProducts/Services

Greenmarketingconsistsofdifferentactivitiestosatisfytheconsumers’needorwantsinthe market. Different elements are product itself, packaging, and distribution andpromotionactivities.Greenmarketingandgreenlabellinghasbecomeanimportantfactorforproductsorservicestosustaininthemarket.Greeningtheprocessinmakingaproductgivesanedgeoverthecompetitivenessnotonlyintheformofcosteffectivenessbutalsobetterbrandbuildingandvaluegenerationinthemarket.Greenpushforaproductgivesanewlifeandmoreorientationtoaproduct for itsconsumption.As increasingawareness,concerns and importance about eco friendly goodsamong the consumers increasing, theimportance of consuming product with green label has to increase at a rapid pace. Theresponsibilityofcorporateinprojectinggreenproductsanditsvaluehasbeenofimmenseimportance in this situation. Corporate have startedworking responsibly on sustainablesolutionswithlesscarbonemissionandlesserimpactontheenvironment.

5. CaseStudy:Responsibleconsumption

Perceptionofaconsumeralways likelytochangeforanavailablegreenproduct/servicewhich can be evaluated through their buying decisionsmaking. The questionnaire dealtwith different questions about their awareness on this issue, their motives behindconsumptionandmostimportantlythesuggestionsfordifferentgovernments/corporate.Theinferenceshavebeenclubbedtogetmoreinformativeanalysis.Anopenandtwowaydiscussionandinformationsharingbasedonquestionnairefacilitatedindrawingsomeoftheinferencesbecauseoftheirresponses.

a. Objective

Themainobjectiveofthestudyis“toassesstheimpactofgreenproductsorservicesonconsumptiontrends”and“toassessdifferentfactorsbehindthegreenbuyingpatternofaconsumer”

b. Methodologyi. Questionnaire:Aquestionnairecomprisedof15questionshasbeenusedtoassessthebuyingbehaviourandconsumptiontrendsforanyeconfriendlyproduct/servicesofaconsumer.

ii. FocussedGroupdiscussionsiii. SampleSize:40peoplehavebeenchosenforthisstudyfromvarious

socioeconomicprofilesindifferentpartsofDelhiiv. AgeGroup:Theagegroupoftherespondentsvariedfrom21to30

years.Therespondentsconsistofstudentsandprofessionals.c. ViewpointsofRespondents

Q’s:1. Doyouconcernforenvironmentalpollution?2. Doyouknowaboutglobalwarming?3. Doyouthinkthatthequalityofnaturalresourcesaroundyouhavebeenworse?

Almost all the respondents are aware about the depleting natural resources, they (80%respondents) have a concern for environmental pollution and 90% respondents knowaboutglobalwarmingand its ill effect.Around60%respondents says that thequalityofnaturalresourceshavegraduallydepleting.15%respondentshavenotgivenanswerssincetheyarenotinterestedinthissurveyandtheysimplysaysthattheyarestudentsandnotresponsibleforglobalwarmingandenvironmentaldegradations.

Q’s:4. Doyouthinkthatglobalwarminganditsimpactplaysanegativeroleonthe

societyandenvironment?5. Doyouknowaboutgreen/eco‐friendlyproducts?6. Doyouthinkthatawarenessamongthepeopleaboutgreenproductsand

90%

10% Know about Global Warming

Don't Know 60%

40%

Quality of Natural resources depleted in the last few years

Don't know

servicesisveryless?

Globalwarmingplays a very negative role in the social and environmental developmentprocess. The depletion of natural resources, increasing health hazards due toenvironmental pollution are known to all and almost all the respondents have favouredthisdirectrelationofenvironmentaldegradationandanegativeimpactonsociety.Almostall the respondents know about the green products but only throughword ofmouth ornews. Someof them say that it is only available for high end consumers and somehaveneverseenwhatexactlyagreenproductis.’Thereisalackofavailabilityinthemarketandifavailableitscostisextremelyhigh’;Onerespondentsays.Alltherespondentshavetalkedaboutawarenessabouttheseissueverylimited.Theawarenesscampaignsandknowledgeisnotavailableinopenpublicdomainandstillthereisahugelackofinformationamongtheactualconsumeraboutthisissue.

Q’s:7. Doyouthinkthatyourconsumptionpatterncanplayabigroleinorderto

mitigatetheadverseenvironmentalimpact?8. Areyouwillingtochangeyourlifestyletoreducethedamageonthe

environment?

Most of the respondents around 70% respondents don’t think that their step towards agreen consumption would play any role in mitigating the issue. Also they are notresponsibleforwhatishappening.Thegovernmentandcorporateareresponsibletotakedecisiononthis issueandtheyshouldtakestrictmeasuresandpolicy implementationtocut the carbon emission in the production process. Same no. of respondents (70%responses)saysthattheyarenotwillingtochangetheirlifestyle.Theyallaresurvivingatavery low lifestyle and they can’t change since most of them are students and earlyprofessionalswhoarenotinapositiontospendlavishlyonthesecostlyissues.

Q’s:9. Areyouwillingtobuyamoreenvironmentallyproductwithaneco‐labelonit?10. Haveyoueverpurchasedanyeco‐friendlyproduct?

30%

70%

Individual livelihood pattern would make any change in mitigating the issue

70%

30%

Not willing to chage lifestyle

Willing but how

11. Doesahigherpriceforagreenproductmakeachangeonyourdecisionmakingprocess?

All the respondents are willing to purchase an eco friendly product. But it should beavailableinthemarketatacompetitivecost.50%(20respondents)oftherespondentssaythat theyhavenotyetpurchaseanygreenproduct.This shows their lackof informationaboutdifferenteco labelling informationonproductsandknowledgegaponthis issue.Ahigher price for eco friendly product always plays a crucial role in forming the buyingdecisions. “The cost of a green product should be affordable also”; many respondentsquoted.

Q’s:12. Doyouthinkitisyourmoralresponsibilitytopurchaseagreenproduct?13. Doyouthinkthatgovernmentandcorporateshouldmoreinvestininnovationto

lowerdownthecostofproducingagreenproduct?

“Yes,itisourcollectiveandindividualresponsibilitytoconsumegreenproductsonly.”45% (19 respondents) of the respondents say. They also say that consumers are not at adecisionmakingpositionandcorporate/producershavetoplayapivotalroleinproducinggreen products at a reasonable cost. It is the responsibility of the governments andcorporateto invest inthe innovation,researchanddevelopgreensolutionsfortheneedsandwantsinthemarket.

50%50%

Not yet purchase any Green product

Yes, they have but don't know whether it is green or not

45%55%

Moral responsibility to consume green products

Don't know

Q’s:14. Whatisyourmotivebehindbuyinganenvironmentfriendlyproduct?(The

comparativelybetterenvironmentalperformance,lifestyle,Yourhealth,Agoodassociationwithquality,Consuminggreenproductsmakeyoufeelabetterqualityoflife)

15. Whatdoyouthinkisthebiggestchallengeinpurchasingagreenproduct?(Expensive,Limitedavailability,greenlabellingareconfusing/Nottrustworthy)

Themotivebehindbuyinganenvironmentfriendlyproduct(iftheypurchase)isprimarilyagoodhealthandabetterenvironmentalperformance.Mostoftherespondentssay(65%of respondents around25) if theyare tobuygreenproductsmainmotivewouldbeof agood health. The biggest challenges in purchasing these products are expensiveness andconfusionoverthecompanies’promisesfortheirproducts.“Mostofthecompaniesexceptafewhavebeensellingtheirwasteinthenameofgreenthatalsoathighercosts”;Saysfewoftherespondents.Alsothelevelofcorruption,misguidance,unethicalbusinessconductshavemadethiskindofdecisionverychallenging.

6. Hypotheses

Various hypotheses have been defined broadly on the basis of questionnaire and pointsfromfocussedgroupdiscussions.Theseare

i. HA1:Respondentshaveknowledgeaboutglobalwarming.H01:Respondentshavenoknowledgeaboutglobalwarming.

ii. HA2: Respondents consumption patterns could mitigate adverseenvironmentalimpact.H02: Respondents consumption patterns could not mitigate adverseenvironmentalimpact.

iii. HA3:RespondentsmoralresponsibilityistopurchasegreenproductsH03: Respondents moral responsibility is not to purchase greenproducts.

Table‐i:HypothesisTesting(Chi‐Squaretest)

Value df Asymp.Sig.

(2‐sided)ExactSig.(2‐sided)

ExactSig.(1‐sided)

PearsonChi‐Square

2.667a 1 .102

ContinuityCorrectionb

1.185 1 .276

LikelihoodRatio

2.597 1 .107

Fisher'sExactTest

.139 .139

Linear‐by‐Linear

Association2.600 1 .107

NofValidCases

40

Interpretation:

Table‐iprovidesrequiredinformationofChi‐squaretest.ThevalueofPearsonChi‐Square

is2.667andassociatedsignificancevalueis.102(whichislessthan0.05)with1degreeof

freedom.Therefore,nullhypothesis(H01)isrejectedandourhypothesis(HA1)isaccepted.

Table‐ii:HypothesisTesting(Chi‐Squaretest)

Value df Asymp.Sig.

(2‐sided)ExactSig.(2‐sided)

ExactSig.(1‐sided)

PearsonChi‐Square

.127a 1 .722

ContinuityCorrectionb

.000 1 1.000

LikelihoodRatio

.128 1 .720

Fisher'sExactTest

1.000 .505

Linear‐by‐LinearAssociation

.124 1 .725

NofValidCases

40

Interpretation:

Table‐iishowsthatthevalueofPearsonChi‐squaretestis.127andassociatedsignificancevalueis.722(whichislessthan0.05)with1degreeoffreedom.Thereforenullhypothesis(H02)isrejected.Ourhypothesis(HA2)isacceptedandstandspositive.

Table‐iii:HypothesisTesting(Chi‐Squaretest)

Value df Asymp.Sig. ExactSig. ExactSig.

(2‐sided) (2‐sided) (1‐sided)PearsonChi‐Square

4.177a 1 .041

ContinuityCorrectionb

2.947 1 .086

LikelihoodRatio

4.304 1 .038

Fisher'sExactTest

.055 .042

Linear‐by‐Linear

Association

4.073 1 .044

NofValidCases

40

Interpretation:

Table‐ iiidepicts thatthePearsonChi‐Squarevalue is4.177andassociatedvalue is .041,whichis lessthan0.05with1degreeoffreedom.Hence,nullhypothesis(H03) isrejectedandalternativehypothesis(HA3)isaccepted.

7. Limitations

Thestudyhassomelimitations.Thelimitationscanbeexhibitedas

i. Smallsizeofsampleii. Manyotherrelatedandimportantparametersaremissinglikefeaturesofmakinga

productgreen,theirassociatingfactors,energysavings,environmentalratingsetc.iii. Many times the respondents are not the decisionmaking persons, so itmay be a

hypotheticaldecisiontoconsiderhis/herresponses.

8. Conclusion

Increasing awareness about the environmental degradation and its ill effect, consumershave started consuming eco‐friendly products/ services. Themain constraint in buyingeco‐friendlyproductshasbeenthehighcost.Alsothecompaniesproducingproductsinthenameofenvironmentallyfriendlyhasbeeneyewashfortheconsumersandtheydon'trelyuponthefakepromotionalactivitiesinthenameofgreen.Consumerswanttheirfullvalueofmoneytobeutilisedwithperfectefficacy.Inthebuyingdecisionprocess,theywanttheirperceptiontobevalidabouttheproduct/organisation.Mostoftheconsumersifsatisfiedwith thebrandand theirethical codeof conduct then theirperceptionareunchangeableand they buy green labelled product. Green product and green marketing push theconsumerstoconsumesatisfactorily.Thereisstillahugecommunicationandinformation

gapaboutgreen/ecofriendlyproducts.Theresponsibleconsumptionandbuyingdecisionmaking process depends upon various factors such as cost proposition, perception andvalidityofproducts'promise,availabilityofproductsetc.Mostof thegreenproductsarenot available or if available are available for high end consumers. Government andcorporatehavetoplayacrucialroleandthroughresearch,innovationanddevelopmentofgreensolutionscanplayapivotalroleinpushingconsumerstofollowamoreresponsibleconsumption pattern. Through innovation and technologies, producers need to producegreen products at a competitive cost. The corporate should not involve in any kind ofnegativeeyewashing.Corporateneedstoenhancetheirethicalconductsofbusinessandatransparentmechanismtotackletheseissues.Governmentsandpolicymakersshouldalsotake stricter rules and regulations to promote green practices in business operations.Moreover spreading awareness about greens products is much more important as thisconcept is not known by the citizen and therefore there is dire need to spread theawarenessamongthesocietythroughregularseminars,printmedia,televisionmediaetc.This responsibility of making consumers aware about the green products is also oncompanies marketing these products. Though they have finest of product but withoutawareness,theirproductsarenotreachingtotheultimatecustomers.

9. References:i. Greendex2012:ConsumerChoiceandtheEnvironment–AWorldwideTracking

Survey.July2012(Online)ii. Chan,R.Y.K.(1999).EnvironmentalAttitudesandBehaviorofConsumersinChina.

JournalofInternationalConsumerMarketing,Vol.11,No.4iii. GreenBrands,IndiaInsights,2011

WorldSustainabilityReviewThereviewwoulddisseminateinformationonworldwidehappeningsintheworldasfarassustainablepracticesareconcerned.Bestofthenationalandinternationalpracticeswouldbe added in this section to provide a broader picture. The sectionwould also provide aplatform for various stakeholders to share the information and knowledge, suggest andenhancetheirunderstandingaboutthesame.

CallforPapersGreen Watch accepts submission on a rolling basis. You are requested to contributeresearch papers, case studies, articles, success stories etc. related to green policies,environmental law and regulations, activities and initiatives, sustainable development,greenmarketing,environmentmanagement,impactassessments,environmenthealthandsafety, green buildings, environment management plan, energy efficiency, renewableenergy, water conservation, rain water harvesting, climate change, clean developmentmechanism, environmental degradation, green marketing etc. Please send [email protected]

Writetous!

Green Watch is a monthly global not for profit update on policies, roles, activities andinitiativesrelatedtosustainabledevelopment.Weattempttokeepabreastitsreaderswithlatest information on various developments taking place in the area of sustainabledevelopment. If you have any news/ information related to green policies, programmes,initiatives, technology and innovation, success stories or any other relevant informationetc,youwouldliketosharewiththeworldwidegreencommunity.Pleasedosendthosetous:E‐mail:[email protected]

DisclaimerTheviewsoropinionsexpressedinvariousarticlesareofauthors.

ContactUsWewelcomeyourfeedback/comments,ideas/suggestionsorqueries.

Green watch (Let’s think green!)

B3,A80/81,Pandavnagar,NewDelhi110092,

IndiaEmail:[email protected]

TelephoneNo.01122482856For more information please visit https://www.facebook.com/editor.greenwatch