globefish highlights - issue 4/2013 - fao

TRANSCRIPT

HIGHLIGHTSA quarterly update on world seafood markets

31/10/2013 Issue 4/2013

Tel.: (+39) 06 57054163 - Fax: (+39) 06 57053020 - Email: [email protected] - Website: www.globefish.org

Bibliographic reference:GLOBEFISH Highlights2013FAO/GLOBEFISH Highlights (4/2013): p. 56

A quarterly updatebased onthe GLOBEFISH databank

About GLOBEFISHGLOBEFISH forms part of the Products, Trade and Marketing Branch of the FAO Fisheries and Aquaculture Department and is part of the FISH INFOnetwork (see below). It collects information from the main market areas in developed countries. for the benefit of the world’s producers and exporters. Part of its services is an electronic databank and the distribution of information through the GLOBEFISH European Fish Price Report, the GLOBEFISH Highlights, the GLOBEFISH Research Programme and the GLOBEFISH Commodity Updates.

The GLOBEFISH Highlights are based on information available in the databank, supplemented by market information from industry correspondents and from six regional services which form the FISH INFOnetwork: INFOFISH (Asia and the Pacific), INFOPESCA (Latin America and the Caribbean), INFOPECHE (Africa), INFOSAMAK (Arab countries), EUROFISH (Central and Eastern Europe) and INFOYU (China).

This issue of GLOBEFISH Highlights has been prepared by Audun Lem, Paola Sabatini and Karine Boisset with contributions from Shirlene M. Anthonysamy, Nada Bougouss, Victoria Chomo, Felix Dent, Fatima Ferdouse, Erik Hempel, Jianwei Lei, Rodrigo Misa, Sudari Pawiro, Ferit Rad, Meyling Tang, Stefania Vannuccini and Xiaowei Zhou. Hilary Cochrane provided editing services and Turan Rahimzadeh was responsible for the layout. The Norwegian Seafood Council provided data support for the FAO Fish Price Index.

GLOBEFISH Highlights are distributed to the subscribers of: INFOFISH Trade News, INFOPESCA Noticias Comerciales, INFOPECHE Nouvelles Commerciales, through EUROFISH and INFOYU. GLOBEFISH Highlights are also available in electronic form.

For subscription details please contact:

GLOBEFISH, FIPM/FAO Tel: (39-06) 5705 4163Viale delle Terme di Caracalla Fax: (39-06) 5705 302000153 Rome, ItalyEmail: [email protected]: www.globefish.org

All rights reserved. Reproduction and dissemination of material in this information product for educational or other non-commercial purposes are authorized without any prior written permission from the copyright holders provided the source is fully acknowledged. Reproduction of material in this information product for resale or other commercial purposes is prohibited without written permission of the copyright holders. Applications for such permission should be addressed to the Chief, Electronic Publishing Policy and Support Branch, Communication Division, FAO, Viale delle Terme di Caracalla, 00153 Rome, Italy or by e-mail to copyright@ fao. org

© FAO GLOBEFISH 2013

Global fish economy Aquaculture continues to boost overall supply but mar-kets are hesitant to pay current prices pushing quota-tions down from earlier levels. Fish consumption per capita continues to grow with aquaculture in the process of overtaking capture fisheries as a source of fish supply for direct human consumption p. 2

Lower supply and high prices are the characteristics of international shrimp trade at present

Lower production of farmed shrimp associated with the disease problems in Asia and Latin America during the first half of the year and poor supply forecast for the rest of the year have

pushed shrimp prices higher worldwide. p. 4

Overall 2013 tuna landings lower than last year Japan, the largest sashimi tuna mar-ket, has become less active with lower imports during the first half of the year. The canned tuna market fared better with improved imports by the

European Union and the USA. Canned tuna demand has also increased in many non-conventional markets. p. 11

In spite of good supply cod prices have not dropped globally

Overall the supply situation for the main species of groundfish is mixed. Taking all sources of supply into con-sideration, there is probably an over-

supply of cod; however, cod prices in Europe and Asia have in-creased over the summer months. p. 17

Octopus supplies increasing in main markets Octopus supplies are more abundant, particularly from Morocco, and this is reflected in busier trading in the main markets, such as Japan, Spain and Italy, which have all increased

imports substantially during the first half of the year. Squid supplies are also up slightly but supplies of cuttlefish remain tight. p. 21

Demand remains firm keeping prices steady and strong Production in China is currently reported to be down by 30% while other producers in Asia, Africa and Latin America continue to intensify

tilapia farming. Demand remains firm, which will help keep prices steady and strong. p. 25

Steady global demand but major markets slow down VASEP has forecast lower pro-duction in 2013, which together with other measures should help stabilize pangasius prices. Im-

ports into the EU took a step back while US imports grew marginally. Elsewhere, demand remains strong for pan-gasius fillet and is being met by both imported and local sources. p. 27

Turkey becomes largest producer but prices weaken and costs continue to rise

The increasing volumes of seabass and seabream that are coming to market have led to weaker prices. Although consumers have reason to be happy,

producers are in a different position as margins have taken a serious hit. p. 29

Booming market finally begins to cool as growing con-sumer resistance to mark-ups reverses upward trend

Since the recovery that began in late 2012, the salmon market has witnessed continued driving growth and a positive price trajectory lifting export revenues

to record levels, particularly for Norwegian producers supplying EU markets. This price trend has recently been reversed, how-ever, and there is evidence of weakening demand as high raw material costs filter down the value chain. p. 35

EU ban on mackerel and herring from the Faroe Islands brings Iceland to the negotiation table

The EU has followed through with its threat to impose trade restrictions on the Faroe Islands in August, and Nor-way has followed suit. This means that

mackerel and herring from the Faroes are banned in the EU and Norway, and the impact on the industry may soon be felt. There will be shifts in trade flows, and there may also be some price consequences as a result of this. p. 41

Rising price trend continues as a result of strong de-mand for fishmeal

The rising price trend for fishmeal con-tinued through the second quarter of 2013. With this latest increase, prices have risen approximately 43% between mid-2008 and mid-2013. Soymeal prices remained relatively flat over the same

period, thus this growing price differential may provide incen-tives for terrestrial farmers to substitute fishmeal with less ex-pensive feed alternatives. p. 46

Fish oil prices reach record highs The fish oil price continued its steady rise, reaching new highs in mid-2013. Growing demand for aquaculture prod-ucts will continue to put upward pres-sure on fish oil prices as a primary ingre-dient in fish feeds for carnivorous fish

species. p. 48

Decline in European Imports of Bivalve Molluscs Slows but Asian Demand Growing

Mussel trade within the European Union during the first six months of 2013 was dominated by intra-EU trade, with 72%, or 67 300 tonnes, of imports coming from countries within the European communi-

ty, in particular from Spain, Netherlands, Denmark, Italy and UK. p. 49

Fish and fishery products statistics p. 56

INSIDE THIS ISSUE...

2 Globefish Highlights October 2013

GLOBAL FISH ECONOMYaccess in the fisheries sector therefore has become more a question of the exporter’s ability to adhere to regulatory requirements in the importing country rather than an issue of tariffs. In addition, however, the proliferation of new voluntary market-based standards linked to sustainable production, traceability and certification are adding costs to the product with little immediate benefit to producers.

The outlook for the rest of the year is one of firming demand and somewhat higher prices in the run-up to the end-of-year festivities. A number of species continue to be in short supply and prices will remain at a sustained high level. In early 2014 a somewhat weaker market is likely to be seen again.

Whitefish revitalized

During the last month, whitefish, one of the most important commodities in global production

Aquaculture continues to boost overall sup-ply but markets are hesitant to pay current prices pushing quotations down from earlier levels. Fish consumption per capita continues to grow with aq-uaculture in the process of overtaking capture fish-eries as a source of fish supply for direct human con-sumption.

Production and markets

Overall production is boosted by a buoyant aquaculture sector guiding total supply for the year to a new record of 160 million tonnes. Fish consumption is also up, reaching almost 20 kg per capita. This reflects the increased availability of farmed products, but also that increasing volumes of wild species are now going to direct human consumption and less towards fishmeal production.

World trade is also up with both values and volumes entering international markets showing moderate growth. The market situation overall continues to be difficult, in particular in traditional developed country markets. The slightly higher prices of some farmed species therefore are more a symptom of supply shortages rather than strong demand.

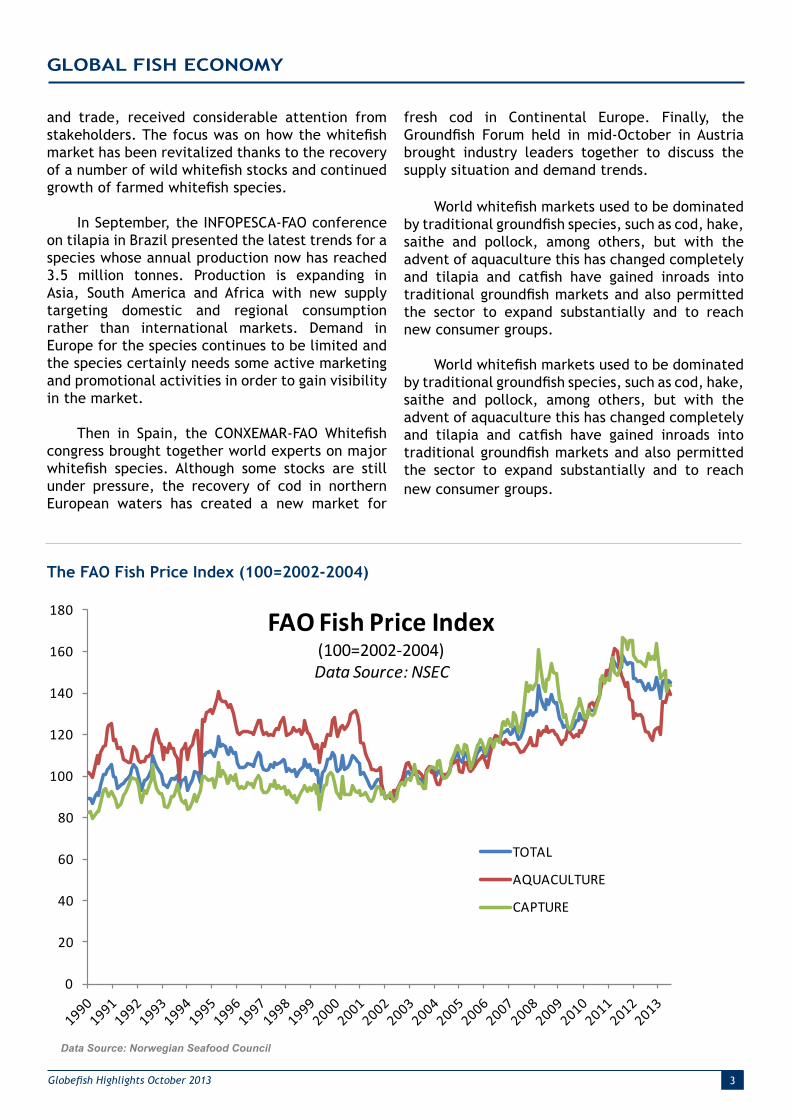

The FAO Fish Price Index shows that overall price levels remain high although they have receded from the top levels of late 2012. Supply problems for farmed salmon and shrimp have boosted aquaculture quotations whereas wild-caught whitefish species, tuna and pelagic species have been weaker. Other farmed species, such as seabass and seabream, were down as supply increases far exceed immediate market requirements.

Economic outlook Markets continue to be influenced by uncertain

economic sentiments in traditional markets. In Japan, a weaker currency has made imports more expensive. In the USA, imports for the first half of the year were flat in both values and volumes. Developing country demand has been more positive with domestic demand boosting both local production, in particular of farmed products, and imports.

It is well-known that import duties on fish and fishery products for exports to developed country markets are generally low or inexistent. Market

World fish markets at a glance 2011 2012 2013 Change:

2013 over 2012 estim. f’cast

million tonnes %

WORLD BALANCE Production 156.2 156.9 160.0 2.0

Capture fisheries 93.5 90.6 90.1 -0.6

Aquaculture 62.7 66.3 69.9 5.4

Trade value (exports USD billion) 128.2 129.3 132.2 2.2

Trade volume (live weight) 57.4 57.6 57.8 0.3

Total utilization 156.2 156.9 160.0 2.0

Food 131.8 135.1 140.4 4.0

Feed 18.3 16.1 15.6 -3.1

Other uses 6.0 5.8 4.0 -30.8

SUPPLY AND DEMAND INDICATORS

Per caput food consumption:

Food fish (kg/year) 18.9 19.2 19.7 2.8

From capture fisheries (kg/year) 9.9 9.8 9.9 1.5

From aquaculture (kg/year) 9.0 9.4 9.8 4.3

Totals may not match due to rounding.

3Globefish Highlights October 2013

GLOBAL FISH ECONOMY

The FAO Fish Price Index (100=2002-2004)

Data Source: Norwegian Seafood Council

and trade, received considerable attention from stakeholders. The focus was on how the whitefish market has been revitalized thanks to the recovery of a number of wild whitefish stocks and continued growth of farmed whitefish species.

In September, the INFOPESCA-FAO conference on tilapia in Brazil presented the latest trends for a species whose annual production now has reached 3.5 million tonnes. Production is expanding in Asia, South America and Africa with new supply targeting domestic and regional consumption rather than international markets. Demand in Europe for the species continues to be limited and the species certainly needs some active marketing and promotional activities in order to gain visibility in the market.

Then in Spain, the CONXEMAR-FAO Whitefish congress brought together world experts on major whitefish species. Although some stocks are still under pressure, the recovery of cod in northern European waters has created a new market for

fresh cod in Continental Europe. Finally, the Groundfish Forum held in mid-October in Austria brought industry leaders together to discuss the supply situation and demand trends.

World whitefish markets used to be dominated by traditional groundfish species, such as cod, hake, saithe and pollock, among others, but with the advent of aquaculture this has changed completely and tilapia and catfish have gained inroads into traditional groundfish markets and also permitted the sector to expand substantially and to reach new consumer groups.

World whitefish markets used to be dominated by traditional groundfish species, such as cod, hake, saithe and pollock, among others, but with the advent of aquaculture this has changed completely and tilapia and catfish have gained inroads into traditional groundfish markets and also permitted the sector to expand substantially and to reach new consumer groups.

0

20

40

60

80

100

120

140

160

180 FAO Fish Price Index(100=2002-2004)Data Source: NSEC

TOTAL

AQUACULTURE

CAPTURE

4 Globefish Highlights October 2013

Lower supply and high prices are the characteristics of international shrimp trade at present

Lower production of farmed shrimp associated with the disease problems in Asia and Latin America during the first half of the year and poor supply forecast for the rest of the year have pushed shrimp prices higher worldwide. US buyers are influencing market prices with strong demand, while Japanese imports are lower because of the weak yen. High shrimp prices have also made import demands lower on European markets.

SHRIMP

Supply

Farmed shrimp supply did not increase much in Asia or in Latin America during the peak production season of May-September. The early mortality syndrome (EMS) problems in Thailand are being addressed but this year’s harvest production almost certainly will be half of last year’s volume. In Viet Nam overall supply during the first half of the year declined because of persistent disease problems in the central provinces and also in the Mekong Delta area. However, vannamei production increased as a result of a shift back to vannamei from black tiger. Production in Indonesia has been relatively stable, but raw material prices have almost doubled compared with last year, as a result of the supply shortage in Southeast Asia and the depreciation of the rupiah against the US dollar. Although good production has been obtained in India, the unrest in Andhra Pradesh state has resulted in serious disruptions in harvesting, transportation and the movements of the labour force, making the supply of raw materials for export processing quite difficult in this, the main shrimp producing state.

In the USA the accumulated domestic landings

up to June totaled 18 366 tonnes, a decrease of 2% in comparison with the same period in 2012.

For the wild caught Argentinean ‘seabob’ shrimp

Shrimp production by main species (2011) (in tonnes)

(Penaeus muelleri), another good year is predicted for 2013. Landings during the January to July 2013 period were above 31 000 tonnes, indicating stable supply this year.

Market trends during the first half of the year

Raw material shortage worldwide kept shrimp prices firm with a temporary weakening during May and June. During the first half of the year, import growth was stagnant in the two large western markets of the EU and USA. In Japan, there was no real recovery in consumer demand as import costs increased, associated with the weak yen. Supply shortage at origins and strong demand from US buyers pushed shrimp prices to record high levels.

Japan

Demand for raw shrimp tempered in Japanese market

The Japanese market is totally dependent on imported supplies of shrimp and the weaker yen, increased landing costs and rising international prices all contribute to a tough situation. Demand for raw shrimp is suffering and preference for processed shrimp imports has increased. Japanese importers must compete with

White Shrimp in Japanese market,origin Indonesia

Source: Infofish ITN

Penaeus vannamei

40%

Giant tiger prawn 12%

Akiami paste shrimp 8%

Northern prawn, 5%

Others, 36%

Source: FAO

5

10

15

20

25

30

Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13

USD/kg

31/40

16/20

5Globefish Highlights October 2013

frozen shrimp were also at a record low from Thailand (-33%) from January to July 2013 compared with the same period last year.

Domestic sales prices have increased. By the end of August, wholesale prices of vannamei shrimp were 6% higher than those of July, even though the peak holiday demand was over by mid-August.

In late August, contract prices for Indian headless vannamei increased by nearly 20% to USD 15.70/kg compared with USD 13.10/kg in June. Export prices of black tiger shrimp from India also increased almost at the same rate, reaching USD 15.50/kg, CFR Japan. Competition is also strong from US buyers, while shrimp demand from Europe is improving as well.

No countervailing duties for countries involved

The US International Trade Commission (USITC) ruled four to two in favour of abandoning the imposition of countervailing duties on imported warmwater shrimp from the seven countries that had been accused of subsidizing their shrimp industries. The countries involved were Ecuador, China, India, Viet Nam, Thailand, Indonesia and Malaysia. The USITC did not find that there was a real damage for the US domestic shrimp industry.

The Gulf of Mexico shrimp producers supply only one-tenth of the shrimp consumed in the US. They are yet to decide whether to appeal the case. The producers had argued that fuel costs have hampered competition with shrimp farms in Asia as they “receive government support” and that government subsidies abroad threaten

US buyers but the weak yen makes this difficult. Hence imports slowed down, particularly for raw frozen shrimp. Poor supplies of shell-on shrimp from Thailand and high prices also affected shrimp demand in the supermarket trade. Imports of processed shrimp are a better option in the current situation.

Consumer demand slowed down after the summer holiday but prices increased further in Japanese wholesale trade, as a result of falling domestic inventories and poor supply forecast in producing countries. Export prices have also increased in south and Southeast Asian producing countries as many of these currencies have weakened against the US dollar and raw material prices continue to rise.

Imports

Imports during the period January to June 2013 fell below last year’s as result of lower supplies of raw frozen products. However, processed shrimp imports increased, which is a reflection of the market as domestic reprocessing costs escalate in Japan.

Imports of raw frozen shrimp in the January-June period were 1.38% lower, although supplies increased from Indonesia, Viet Nam and India. Processed shrimp imports went up by 2.18% compared with the same period last year. Supplies of cooked frozen shrimp and sushi shrimp were 6.13% and 32% higher respectively.

Global market trends

According to a recent survey, the import price of vannamei shrimp from Thailand increased by almost 50% (in yen terms) in July compared with the same month last year, which was a result of the weakening yen and rising export prices from the origin. Cumulative imports of raw

SHRIMP

ImportsShrimp (by product): Japan

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)

Live 0.0 0.1 0.1 0.0 0.3 0.5

Fresh/chilled 0.0 0.0 0.0 1.0 - -

Frozen, raw 84.1 85.2 86.4 83.6 85.7 84.5

Dried/salted/in brine 1.1 1.8 1.5 1.6 1.4 1.0

Cooked, frozen 9.1 8.7 9.7 9.8 11.3 11.9

Cooked & smoked 0.1 0.1 0.1 0.2 0.2 0.1

Frozen ebi ** ** ** ** ** 0.2

Prepared/preserved* 20.6 20.9 21.3 23.6 23.2 23.1

Sushi (with rice) 0.0 0.1 0.7 1.5 1.0 1.2

Total 115.0 116.9 119.8 120.4 123.1 122.2*(incl. tempura shrimp ) Source: Japan Customs

ImportsShrimp (frozen): Japan

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Indonesia 17.9 17.3 15.7 15.1 15.1 16.6

Viet Nam 15.6 14.0 16.3 13.0 14.1 14.8

Thailand 10.4 14.1 17.6 15.8 16.2 12.0

India 9.3 9.2 9.1 8.1 10.1 11.9

China 7.4 5.4 5.5 7.1 6.5 5.3

Argentina 0.4 0.7 0.9 2.3 3.7 4.8

Russia 5.2 4.5 4.4 4.4 3.8 3.7

Malaysia 2.0 2.4 3.1 4.5 3.5 2.5

Myanmar 2.7 3.1 2.1 2.6 2.4 2.2

Greenland 2.6 3.9 2.2 1.9 1.5 2.0

Canada 3.8 3.9 3.4 2.9 2.9 2.0

Bangladesh 1.5 1.5 1.4 1.2 1.2 1.9

Others 5.0 5.3 4.7 4.9 4.9 4.8

Total 84.1 85.2 86.4 83.7 85.7 84.6Source: Japan Customs

6 Globefish Highlights October 2013

to destroy the domestic shrimp business.

USA - Imports

In general, shrimp supplies to the US market are lower both because of EMS in Asia and the high occurrence of white spot disease in Latin American countries, mainly Mexico.

The supply shortfall from Thailand was 32% in the January to June period against the same period last year. Ecuador is still in second place but the difference has narrowed considerably this year. Indian supplies during this period increased by 82%, moving from 9th place in 2009 to 3rd this year in half-yearly imports. Despite the import surge from India, overall import during the first half of the year was nearly 16 000 tonnes or 7% down on last year. However, in terms of price and volume of imports, the US continues to dominate international shrimp trade.

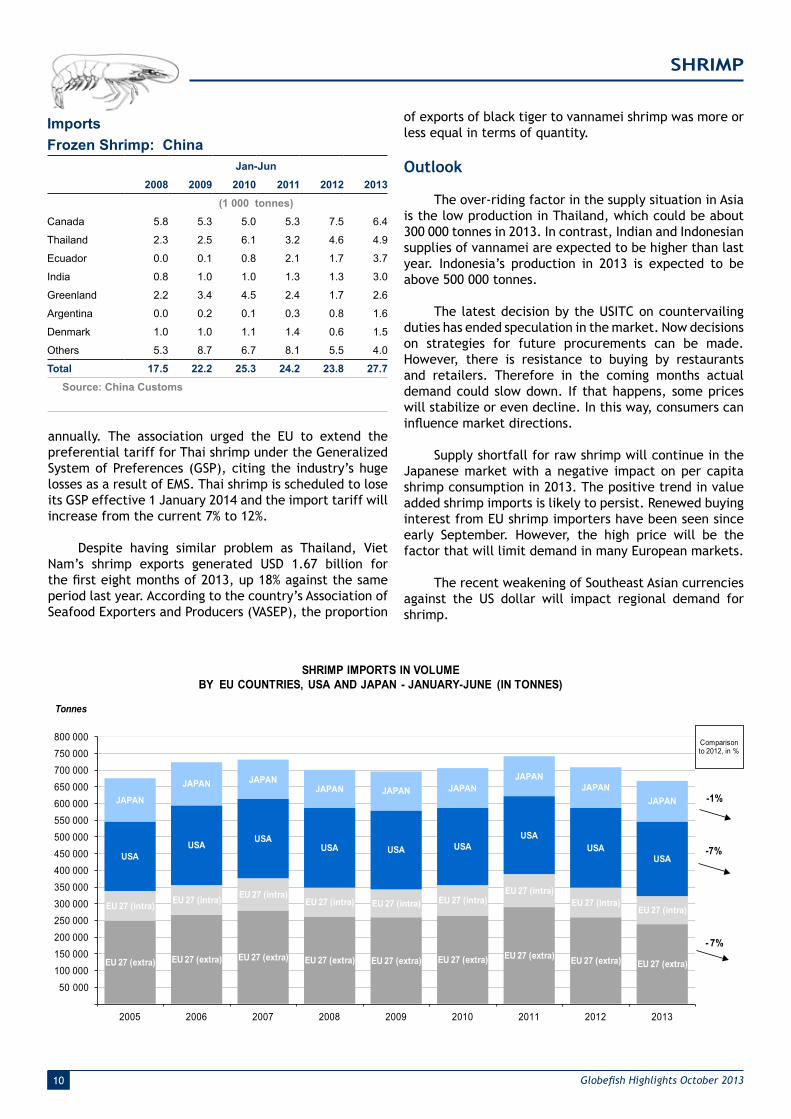

Europe - Quiet market for the first half of the year

European shrimp markets were quiet during the first six months of the year. Sluggish domestic demand and high shrimp prices because of short supplies prompted many European buyers to withdraw from the international market as they were unable to compete with buyers from other countries. Buying activities were mainly focused

SHRIMP

on immediate needs. Only in the last two months have concerted efforts been made to buy consistently and pay competitive prices to refill depleted inventories.

The slow demand is reflected in lower shrimp imports into the EU. For the first six months of the year total shrimp imports into the EU-27 declined by 7% while shipments from the third countries (extra-trade) declined by 7.7% on a year on year basis. There were sharp drops in supplies from Thailand (-33.3%), China (-12.4%), Ecuador (-5.7%) and also Viet Nam (-4.5%). Increased supplies from India (+12.5%), Greenland (+7.4%) and Denmark (+11.2%) were unable to offset the declines.

Shrimp imports into major European markets also posted negative growths except to Italy, which grew marginally by almost 4% as more shipments were recorded from Spain (+13.9%) and Argentina (+36.8%). Imports from

Shrimp prices (16-20 count) in main wholesale markets, USA and Japan

Source: Infofish ITN

3

4

5

6

7

8

Aug-03 Aug-04 Aug-05 Aug-06 Aug-07 Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13

USD/lbGulf brown, New York

Indian white, Tokyo

ImportsShrimp: USA

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Thailand 71.1 73.4 81.4 77.0 60.1 41.0

Ecuador 31.8 33.3 35.8 35.0 44.1 39.1

India 5.5 8.6 7.3 14.9 20.4 37.1

Indonesia 43.2 40.1 29.4 35.3 37.4 35.8

Viet Nam 15.1 14.6 14.1 16.9 16.8 18.9

China 23.7 17.5 18.8 16.2 16.2 16.1

Malaysia 10.4 7.4 9.1 9.2 10.9 8.4

Mexico 7.8 12.4 10.5 6.7 10.8 7.3

Peru 4.1 5.2 4.2 4.9 4.6 5.5

Guyana 5.2 5.8 4.3 4.0 6.1 4.8

Others 19.4 18.1 14.1 12.3 12.5 9.8

Total 237.311 236.3 229.0 232.4 239.8 223.8Source: NMFS

ImportsShrimp: USA

Jan-Jun

Product

2011 2012 2013

1 000 tonnes

million USD

1 000 tonnes

million USD

1 000 tonnes

million USD

Peeled frozen 84.5 808.3 90.5 821.2 93.2 844.1

Other frozen 36.7 343.6 33.8 330.8 27.0 272.5

Breaded 20.5 134.1 18.4 125.1 16.4 109.2

Other preparations 2.0 11.2 1.3 7.3 1.1 6.4

Headless shell-on frozen

All sizes 86.9 754.6 94.7 777.1 84.6 773.4

< 15 6.4 98.8 8.4 123.1 7.3 112.2

15/20 6.6 79.6 8.7 87.3 6.5 69.7

21/25 12.4 127.5 11.9 104.2 12.8 129.7

26/30 12.9 112.5 14.8 123.6 14.5 134.8

31/40 17.4 133.2 17.7 128.8 16.4 136.6

41/50 10.8 73.3 11.8 79.7 11.7 89.4

51/60 11.0 74.1 10.2 65.0 8.1 56.2

61/70 5.4 33.3 6.3 39.0 4.1 26.7

> 70 3.9 22.3 4.7 26.6 3.1 18.3

Other products 1.8 17.6 1.2 7.8 1.5 19.1

Total 232.4 2 069.0 239.8 2 069.3 223.8 2 024.8Source: NMFS

7Globefish Highlights October 2013

SHRIMP

Ecuador, the largest supplier, went down slightly by 2.1%.

Germany is highly dependent on shrimp supplies from Asia and the most affected country as German imports dropped sharply by more than 16% with lower shipments from Thailand (-27.8%), Viet Nam (-23.4%) and Bangladesh (-21.6%). Only India shipped more to this market (+9%).

India and Bangladesh are two major Asian producing countries that have not been affected by the EMS problem and they generally did well in all major markets. Imports from India and Bangladesh to the UK market increased sharply by 13.5% and 27.6% respectively, but shipments from Thailand, the number one supplier, dropped by 24.5%. Shrimp imports into France also declined marginally by 1.6% this year largely as a result of lower supply from Thailand (-47.1%), which could not be compensated for by increased supplies from Ecuador (+21.9%), Bangladesh (+44.4%), India (+3.2%) and also Viet Nam (+4.8%).

The largest shrimp market in the EU, Spain, continued

Imports/ExportsShrimp: EU-27 (by country of origin)

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)IMPORTSEcuador 37.5 32.7 37.0 48.6 44.0 41.5

Greenland 33.9 32.9 31.8 34.7 28.4 30.5

India 26.1 29.7 27.1 28.9 26.4 29.7

Denmark 24.9 22.9 24.7 22.4 19.7 21.9

Thailand 13.7 18.9 28.7 28.6 24.9 16.6

Netherlands 17.3 16.9 18.0 22.1 19.9 16.1

Bangladesh 14.4 16.1 16.8 17.5 15.7 15.7

China 18.7 16.1 17.6 20.0 17.8 15.6

Argentina 8.5 13.9 11.5 17.9 13.8 14.9

Viet Nam 11.9 10.3 15.3 20.3 15.4 14.7

Canada 16.2 15.7 14.3 14.1 16.5 11.4

Spain 7.5 8.8 10.2 10.0 12.5 10.6

Belgium 11.1 10.4 10.9 13.8 11.1 10.5

Others 106.8 97.8 92.4 89.0 80.0 72.4

Grand Total 348.4 343.1 356.4 387.9 346.4 322.1Total Intra Imports 87.2 85.4 92.2 98.4 87.7 83.2Total Extra Imports 261.3 257.7 264.2 289.5 258.7 238.9EXPORTSGrand Total 171.3 167.9 168.2 180.6 156.9 147.9Total Intra Exports 119.2 119.7 121.9 136.8 120.3 114.1Total Extra Exports 52.1 48.2 46.3 43.9 36.6 33.9

Source: EUROSTAT

ImportsShrimp: Italy

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Ecuador 8.6 9.2 10.6 11.0 9.5 9.3

Spain 1.9 2.7 2.4 3.0 3.6 4.1

Argentina 1.9 2.0 2.8 3.0 1.9 2.6

India 3.0 2.3 2.9 3.3 2.5 2.6

Denmark 3.1 2.1 2.3 2.1 1.3 1.7

Belgium 0.7 0.8 0.6 0.6 0.4 1.1

Netherlands 1.5 1.6 2.0 2.6 2.1 1.1

Viet Nam 0.9 0.6 1.0 1.2 0.5 0.9

Others 7.5 6.7 6.5 6.4 4.1 3.6

Total 28.9 28.1 31.0 33.3 25.9 26.9Source: ISTAT

ImportsShrimp: Germany

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Thailand 4.4 5.3 6.3 5.3 5.4 3.9

Viet Nam 3.8 3.3 3.8 6.7 4.7 3.6

Netherlands 3.0 2.9 3.1 3.7 3.2 3.0

Bangladesh 1.3 3.3 2.6 2.8 3.7 2.9

India 3.2 3.3 2.7 2.2 2.2 2.4

Belgium 2.7 1.8 2.5 2.2 1.8 1.8

UK 1.2 0.9 1.6 1.3 1.3 1.3

Others 6.7 6.7 6.3 6.8 6.5 5.1

Total 26.1 27.4 28.8 30.8 28.7 24.0Source: Germany Customs

ImportsShrimp: UK

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Thailand 3.3 4.7 6.5 8.1 9.4 7.1

India 3.9 3.5 3.4 3.5 3.7 4.2

Denmark 4.5 4.7 4.6 4.0 3.3 3.9

Bangladesh 2.2 2.8 2.8 3.0 2.9 3.7

Canada 1.6 2.3 3.1 3.4 3.8 2.8

Viet Nam 1.4 1.3 2.2 2.9 2.4 2.4

Indonesia 4.3 3.7 3.5 3.7 1.6 2.0

Iceland 4.4 3.7 3.5 2.7 2.7 1.9

China 0.6 0.4 1.2 1.5 1.9 1.7

Others 7.7 6.4 5.6 5.9 6.0 5.2

Total 33.9 33.5 36.3 38.7 37.8 34.9Source: Her Majesty’s Revenue & Customs

8 Globefish Highlights October 2013

SHRIMP

ImportsShrimp: France

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Ecuador 10.2 7.9 12.3 12.9 13.7 16.7

India 4.4 5.5 5.9 5.9 6.3 6.5

Netherlands 2.9 3.0 2.8 3.0 3.3 3.4

Venezuela 1.7 1.7 1.8 1.7 2.8 2.8

Madagascar 4.2 3.2 3.1 2.8 2.9 2.6

Bangladesh 1.7 1.5 2.3 2.5 1.8 2.6

Viet Nam 1.7 1.5 2.6 2.3 2.1 2.2

Spain 0.8 1.3 2.7 2.2 2.8 2.0

Thailand 1.5 2.6 4.4 4.6 3.4 1.8

Belgium 2.3 2.1 2.1 3.0 2.2 1.3

Others 15.2 14.2 12.8 8.1 9.0 7.4

Total 46.6 44.4 52.8 48.9 50.3 49.5Source: Direction Nationale des Statistiques du CommerceExtérieur – DNSCE

ImportsShrimp: Spain

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)IMPORTSArgentina 6.2 11.6 8.3 14.4 11.4 11.1

Ecuador 11.2 7.7 8.3 15.4 13.5 10.7

China 13.1 10.6 10.1 11.6 9.4 7.9

Senegal 1.4 0.8 0.7 1.7 2.4 2.4

Morocco 3.8 2.9 2.2 2.3 2.2 1.9

Belgium 1.8 1.8 1.7 2.0 1.3 1.6

Netherlands 1.6 1.7 1.4 1.8 1.4 1.4

Tunisia 0.6 0.5 1.0 1.2 1.2 1.4

Nicaragua 0.8 1.5 0.9 1.0 1.5 1.3

Peru 1.0 0.8 0.8 1.3 1.3 1.3

Others 17.8 17.2 19.3 20.3 12.3 10.3

Total 59.4 57.3 54.6 72.9 58.0 51.3EXPORTSItaly 3.7 4.9 4.9 8.9 6.7 7.5

France 1.9 3.9 3.2 3.0 4.5 3.3

Portugal 3.2 3.5 3.5 3.5 3.7 3.0

Greece 0.6 0.5 0.6 0.9 1.0 0.9

Others 1.4 1.6 0.9 1.7 1.9 1.7

Total 10.7 14.6 13.1 17.9 17.7 16.3Source: Agencia Tributaria

ImportsShrimp: Denmark

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)IMPORTSGreenland 32.4 31.6 30.8 33.8 27.5 29.7

Canada 11.5 10.2 7.0 6.3 9.7 7.1

USA 0.2 0.1 0.3 0.4 1.1 1.1

Iceland 2.2 0.6 0.9 1.0 0.7 0.9

Viet Nam 0.5 0.6 0.7 0.9 1.0 0.8

China 0.7 0.2 0.3 0.4 0.6 0.7

Others 7.0 7.0 5.8 4.2 4.0 4.7

Total 54.5 50.3 45.9 47.0 44.6 45.0EXPORTSSweden 9.4 9.8 9.2 10.8 10.6 11.2

Russia 17.3 10.6 7.3 4.6 3.7 2.9

UK 6.3 6.2 5.9 5.1 4.4 4.0

Norway 3.3 3.8 3.9 4.0 3.5 3.8

Germany 4.2 3.6 3.2 3.4 3.3 3.2

China 3.5 3.8 2.8 3.7 2.4 3.4

Italy 4.1 2.6 2.7 2.5 2.3 3.6

Netherlands 3.4 2.7 2.5 2.2 1.4 1.4

Morocco 0.6 2.1 2.4 1.8 1.1 2.7

France 1.8 1.6 1.5 1.3 0.9 1.0

Japan 1.9 1.5 1.4 1.4 0.9 0.8

Others 9.5 7.6 7.8 9.5 7.5 7.9

Total 65.4 56.0 50.6 50.3 42.1 45.9Source: EUROSTAT

on a downward trend. Imports declined by 11.6% while exports fell almost 8% in the January-June period this year. Supplies from all sources declined with shipments from Argentina, Ecuador and China, the three largest suppliers, falling by 2.6%, 20.7% and 16% respectively.

Supply shortages in Asia have benefited Denmark, the main shrimp producing/exporting country in the EU, to some extent. Exports from Denmark went up by 9.0% while imports, mainly of raw material for re-processing, were slightly up by 1% with more supplies coming from Greenland (+8%).

Imports by both the Netherlands and Belgium fell by 21.7% and 15.3% respectively. Re-export activities from these two countries were also affected. During the reporting period shrimp exports from the Netherlands declined by 15.5% while from Belgium the drop was 11.1%.

Asia - Demand from China continues to grow

Buyers from China have been actively buying shrimp from major producing countries in Asia, particularly from India. Purchases were made at competitive prices, matching those paid by US buyers. As a result, shrimp imports into China for January-June this year were

9Globefish Highlights October 2013

SHRIMP

Graphs source: European Price Report

Imports/ExportsShrimp: Netherlands

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)IMPORTSMorocco 2.6 3.5 4.0 4.1 4.5 3.1

Belgium 1.4 1.7 2.3 4.3 3.7 3.1

Germany 2.6 3.8 3.9 4.9 3.8 2.8

India 3.6 5.2 4.7 3.3 2.9 2.8

Bangladesh 1.1 2.6 2.9 2.5 2.5 1.9

Viet Nam 1.1 0.8 0.9 1.9 2.0 1.5

Indonesia 2.7 2.8 2.8 2.1 1.6 1.4

Denmark 2.3 1.8 2.2 1.8 1.3 1.0

China 0.9 1.6 1.0 0.8 0.9 1.0

Thailand 1.2 1.9 1.6 1.4 1.4 1.0

Others 4.9 6.1 4.5 6.8 6.4 4.7

Total 24.5 31.9 30.8 33.9 30.9 24.2EXPORTSMorocco 9.2 12.1 13.3 13.7 11.8 10.2

Germany 4.5 5.0 5.5 6.8 5.8 5.3

Belgium 6.0 6.4 6.9 7.5 6.0 5.1

France 4.6 6.8 7.6 6.8 5.9 4.5

Spain 1.3 2.4 1.0 0.8 1.2 1.0

Italy 1.1 0.9 1.4 1.8 1.4 0.8

Others 2.7 3.3 2.4 1.4 1.6 1.5

Total 29.3 36.8 38.0 39.0 33.6 28.4Source: EUROSTAT

Imports/ExportsShrimp: Belgium

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)IMPORTSIndia 5.2 6.0 4.1 7.4 5.8 8.0

Netherlands 5.8 5.6 6.1 9.0 8.4 5.4

Bangladesh 7.1 5.0 4.9 5.7 3.6 3.1

Viet Nam 1.4 1.3 2.2 2.0 1.3 1.9

Ecuador 4.4 4.1 2.5 5.6 3.7 1.3

Others 10.8 8.8 9.4 8.6 5.9 4.7

Total 34.7 30.7 29.2 38.2 28.7 24.3EXPORTSFrance 10.4 9.5 8.4 13.0 8.6 5.9

Netherlands 3.8 2.8 3.1 4.8 4.6 3.7

Spain 2.9 2.6 2.6 2.7 2.5 2.7

Germany 2.5 2.6 3.1 2.7 2.6 2.5

Italy 0.8 1.0 0.6 0.7 0.4 1.1

UK 4.1 2.3 1.7 1.1 0.5 1.1

Others 3.3 2.9 2.8 3.3 3.3 3.1

Total 27.8 23.7 22.3 28.3 22.6 20.1Source: EUROSTAT

10.10

3.505.006.508.009.50

11.00

Sep-

08

Jan -

09

May

-09

Sep-

09

Jan -

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

40-50 pc/kg

USD/kg

Whiteleg shrimp - Penaeus vannameiHead-on, shell-on, origin: Ecuador (fob)

11.40

7.20

5.20

3.05.07.09.0

11.013.0

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Black Tiger - In Europe, origin: Bangladesh8-12 16-2031-40USD/kg

significantly up by 16.4% with more supplies coming from both Asian and also Latin American sources. Supplies from Ecuador and India increased by 117.6% and 130.8% respectively, while from Greenland imports were up by around 53%. Canada remained the largest supplier to China but shipments dropped by 14.7% this year.

Though overseas demand has been very strong and prices have been rising rapidly, Indian shrimp packers have had to face environmental problems as well as political challenges. Raw materials shortage because of diminished crops, heavy rains, white spot disease and the on-going political problems in Andhra Pradesh have badly affected the delivery of shrimp from farms to processing plants, as the transportation systems were also paralyzed. As a result, ex-farm prices of vannamei shrimp in Andhra Pradesh reportedly jumped to INR 400-500/kg (USD 6.5-8.2) in August from INR 200-300/kg (USD 3.3-4.9/Kg) last year for the count 30/kg.

The Thai Shrimp Association said that there have been encouraging signs that EMS is abating and that shrimp supply in the second half of this year is expected to improve. Thai shrimp companies have been importing raw materials from other countries, such as Ecuador and India, to keep their processing plants running. The association predicted that shrimp exports from Thailand may drop by 50% this year because of the lower harvest. In the past Thailand shipped an average of 350 000 tonnes

10 Globefish Highlights October 2013

SHRIMP

annually. The association urged the EU to extend the preferential tariff for Thai shrimp under the Generalized System of Preferences (GSP), citing the industry’s huge losses as a result of EMS. Thai shrimp is scheduled to lose its GSP effective 1 January 2014 and the import tariff will increase from the current 7% to 12%.

Despite having similar problem as Thailand, Viet Nam’s shrimp exports generated USD 1.67 billion for the first eight months of 2013, up 18% against the same period last year. According to the country’s Association of Seafood Exporters and Producers (VASEP), the proportion

ImportsFrozen Shrimp: China

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Canada 5.8 5.3 5.0 5.3 7.5 6.4

Thailand 2.3 2.5 6.1 3.2 4.6 4.9

Ecuador 0.0 0.1 0.8 2.1 1.7 3.7

India 0.8 1.0 1.0 1.3 1.3 3.0

Greenland 2.2 3.4 4.5 2.4 1.7 2.6

Argentina 0.0 0.2 0.1 0.3 0.8 1.6

Denmark 1.0 1.0 1.1 1.4 0.6 1.5

Others 5.3 8.7 6.7 8.1 5.5 4.0

Total 17.5 22.2 25.3 24.2 23.8 27.7Source: China Customs

of exports of black tiger to vannamei shrimp was more or less equal in terms of quantity.

Outlook

The over-riding factor in the supply situation in Asia is the low production in Thailand, which could be about 300 000 tonnes in 2013. In contrast, Indian and Indonesian supplies of vannamei are expected to be higher than last year. Indonesia’s production in 2013 is expected to be above 500 000 tonnes.

The latest decision by the USITC on countervailing duties has ended speculation in the market. Now decisions on strategies for future procurements can be made. However, there is resistance to buying by restaurants and retailers. Therefore in the coming months actual demand could slow down. If that happens, some prices will stabilize or even decline. In this way, consumers can influence market directions.

Supply shortfall for raw shrimp will continue in the Japanese market with a negative impact on per capita shrimp consumption in 2013. The positive trend in value added shrimp imports is likely to persist. Renewed buying interest from EU shrimp importers have been seen since early September. However, the high price will be the factor that will limit demand in many European markets.

The recent weakening of Southeast Asian currencies against the US dollar will impact regional demand for shrimp.

EU 27 (extra) EU 27 (extra) EU 27 (extra) EU 27 (extra) EU 27 (extra) EU 27 (extra) EU 27 (extra) EU 27 (extra) EU 27 (extra)

EU 27 (intra) EU 27 (intra) EU 27 (intra)EU 27 (intra) EU 27 (intra) EU 27 (intra)

EU 27 (intra)EU 27 (intra)

EU 27 (intra)

USAUSA USA

USA USA USAUSA

USAUSA

JAPAN

JAPAN JAPANJAPAN JAPAN JAPAN

JAPANJAPAN

JAPAN

50 000100 000150 000200 000250 000300 000350 000400 000450 000500 000550 000600 000650 000700 000750 000800 000

2005 2006 2007 2008 2009 2010 2011 2012 2013

SHRIMP IMPORTS IN VOLUME BY EU COUNTRIES, USA AND JAPAN - JANUARY-JUNE (IN TONNES)

Tonnes

Comparison to 2012, in %

-7%

- 7%

-1%

11Globefish Highlights October 2013

TUNA

Overall 2013 tuna landings lower than last year

Japan, the largest sashimi tuna market, has become less active with lower imports during the first half of the year. The canned tuna market fared better with improved imports by the European Union and the USA. Canned tuna demand has also increased in many non-conventional markets.

In the Western Pacific, the 4-month FAD fishing ban remains in force until 31 October and since the start on 1 July catches have been reduced but the price of frozen skipjack for delivery to Thailand dropped to USD 1 900/tonne in July, which was the lowest since January 2012; it weakened further to USD 1 800/tonne in August and moved up to USD 1 920/tonne (CFR Bangkok) in mid-September.

In the Eastern Pacific tuna supplies to canners in Ecuador have dropped significantly from the coastal and deep-sea fisheries since late July because of adverse weather conditions, coupled with strong currents and colder ocean water temperatures. The IATTC fishing closed period was also in place from 29 July to 28 September and 35% of the fishing fleet was not fishing in that area. The remaining vessels will observe the second closure from 18 November 2013 to 18 January 2014. Skipjack stock volumes are good and Manta prices have levelled off at USD 2 050/tonne ex vessel.

In the Indian Ocean skipjack catches have improved and this has allowed the transhipment price from the Atlantic to drop to EUR 1 500/tonne FOB Seychelles compared with EUR 1 620/tonne recorded in August. Yellowfin volumes have not changed much, resulting in a slightly lower price of EUR 2 260/tonne, FOB Seychelles.

In the Atlantic Ocean, fishing off the African coast also remains favourable; the ex vessel price of skipjack in Abidjan dropped to EUR 1 490/tonne and to EUR 2 400/tonne for yellowfin.

Skipjack tuna 38%

Yellowfin tuna 18%Bigeye tuna

6%

Albacore 3%

Atlantic bluefin tuna 0.1%

Pacific bluefin tuna 0.1%

Others 33%

Tuna production by species (2011) (in tonnes)

Source: FAO

A similar price weakening was seen in Europe. In Spain, skipjack is being traded for EUR 1 630/tonne CFR, quite a substantial drop compared with EUR 1 700/tonne in August. As for yellowfin, prices in Italy are stable at EUR 2 600-2 650/tonne CFR, but Spanish prices have contracted sharply to EUR 2 450 CFR/tonne.

Japan

During the first half of the year, tuna landings in Japan posted a slight rise of 1.4% as a result of a significant increase in coastal landings of fresh bluefin and skipjack.

In August, there were unusually large landings of small sized bluefin (20-30 kg/per piece) on the Pacific Ocean side of Hokkaido, which were a result of an unexpected warmwater current in that region.

LandingsTuna: Japan

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Bluefin Fresh 1.9 0.6 0.6 1.1 0.6 1.0

Frozen 0.3 0.0 0.5 0.3 0.3 0.2

Albacore Fresh 23.9 26.6 20.8 23.4 30.3 28.0

Frozen 1.8 6.5 3.4 4.4 10.2 11.4

Bigeye Fresh 3.3 3.0 1.6 1.4 1.6 1.3

Frozen 11.0 9.1 8.1 8.7 10.9 12.3

Yellowfin Fresh 4.8 4.7 4.6 3.6 3.1 3.3

Frozen 4.7 3.2 2.5 3.2 17.3 8.5

Skipjack Fresh 20.4 20.7 19.6 20.8 16.3 28.6

Frozen 114.8 106.8 101.7 101.2 102.9 101.8

Total Fresh 64.4 58.6 47.3 50.3 51.9 62.3

Frozen 132.5 124.7 116.2 117.8 141.7 134.1

Grand Total 196.9 183.3 163.5 168.0 193.7 196.4Source: INFOFISH

12 Globefish Highlights October 2013

Demand for fresh chilled sashimi tuna has weakened on the Japanese market. Generally demand for sashimi tuna improves from beginning of autumn but this year sales were still down as a result of the warm weather, which is not favourable for raw fish consumption. Tuna prices, however, remain firm while supplies of air-flown tuna were low because of bad weather conditions in local and foreign fishing grounds during August and September. Recently one of the large department stores in Japan started to promote the sale of MEL Japan (Marine Eco-label Japan) certified local skipjack through its outlets.

In the second half of 2013, the seasonal catches for sanma or pike mackerel began to appear on the market; this is a competitor for fresh tuna in autumn.

In contrast to sashimi tuna, retail demand for red meat quality bigeye tuna remains high for Western Pacific origin fish because the quality is good. Lower quality tuna of Indian Ocean origin (caught off Somalia last year) is less popular in spite of lower prices and the market is showing a preference for better quality products. This year, supplies of frozen bigeye tuna are expected to be lower than last year and prices are already on the rise.

Kaiten sushi restaurant operators, however, remain loyal to Mexican and Australian bluefin tuna.

During the first half of the year, overall tuna imports (excluding canned tuna) remained below last year’s level in Japan. Imports of fresh and frozen tuna, including loins, totalled 113 162 tonnes compared with 129 410 tonnes imported in the same period in 2012.

Notably, imports of all types of frozen tuna, except albacore, remained below last year’s levels during the January to June period in 2013. Supply shortfall for frozen skipjack was particularly high at - 47%.

Despite the weakening yen, imports of red meat quality frozen tuna loins were stable during the first half of the year. Supplies during this period increased from the Republic of Korea and China but dropped significantly

Coldstorage holdingsTuna: Japan

Source: INFOFISH Trade News

TUNA

ImportsFresh/chilled tuna: Japan

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Yellowfin 8.0 8.3 7.9 7.6 6.5 5.1

Bigeye 7.5 7.8 5.8 5.6 6.6 5.6

Bluefin 1.9 2.8 2.2 1.2 1.6 2.3

S. bluefin 0.5 1.4 0.8 0.6 0.7 0.9

Albacore 0.1 0.1 0.0 0.0 0.0 0.0

Skipjack 0.0 0 0.0 0.0 0.0 0.0

Total 18.0 20.4 16.7 15.0 15.4 13.9Source: INFOFISH

Yellowfin

Bigeye

Albacore

Skipjack

Others

0

20

40

60

80

100

120

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

1000 tonnes

ImportsFrozen tuna: Japan

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Yellowfin 27.0 22.9 24.8 22.7 28.3 20.2

Bigeye 45.0 39.6 41.6 32.1 42.2 41.2

Skipjack 16.9 32 32.5 20.4 15.8 8.5

S. bluefin 0.0 1.0 1.2 0.5 0.6 0.7

Albacore 1.9 3.1 7.5 9.4 5.9 7.9

N. Bluefin 3.9 3.7 0.9 1.6 3.2 1.4

Total 94.7 102.3 108.5 86.7 96.2 79.9Source: INFOFISH

from Fiji and also from Indonesia. Viet Nam was the only source that increased supply from Southeast Asia. From south Asia, India appeared as a new source of supplies (although the quantity is still small), whereas frozen loin supply from Sri Lanka was down. Imports of frozen bluefin loins increased during the first half of the year, as more whole fish are being processed into frozen loin for longer shelf life.

USA

There was a marginal decline in air-flown fresh tuna imports during the first half of the year although the import value increased from USD 107 million to USD 110 million, which could be linked with increased imports of high value Pacific bluefin tuna. Total imports of non-canned tuna during this time were 122 810 tonnes valued at USD 250 million compared with 143 075 tonnes and USD 232 million during the same period last year. Nearly 80% of these were frozen loins and steaks.

13Globefish Highlights October 2013

TUNA

are engaging in promoting canned tuna products as well as introducing new premium and convenience products.

As an indication of recovering domestic demand, canned tuna imports into the USA continued to show strong growth this year. During the first six months of 2013 imports of canned (and pouch) tuna grew by 12.2% in volume and 17.8% in value against the same period of last year. Significant growth was recorded for imports of popular light meat tuna in brine (+21.1%) and also more expensive pouched tuna (+7.8%). Thailand remained the largest supplier and has shipped almost 54 000 tonnes so far this year, up 26.7%. Almost 83% of the total canned tuna imported into the USA came from ASEAN countries and shipments from this group increased by around 12% this year.

Suppliers are also generally more optimistic about the USA market this year. Chicken of the Sea International (COS), expects revenue growth of 8% and volume growth of 2% this year. Its competitor, StarKist recently launched a newly branded “Made in America” canned Chunk Light Tuna in Water, and Chunk Light Tuna in Oil, prepared and packaged in American Samoa. Bumble Bee has released the autumn edition of its BeeWell for Life ebook – these are aimed at providing seasonally appropriate fitness tips and encouraging healthy living, as well as containing

ImportsTuna pouches: USA

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Thailand 10.8 11.5 11.7 9.6 9.6 10.3

Ecuador 6.6 5.2 6.5 5.8 5.5 7.0

Others 2.6 2.8 4.0 3.3 2.4 1.7

Total 20.0 19.5 22.2 18.7 17.5 19.0Source: NFMS

ImportsCanned tuna (excl. pouches): USA

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Thailand 32.8 36.7 56.0 51.5 32.9 43.7

Viet Nam 8.5 7.1 11.5 12.0 10.5 10.4

Philippines 16.2 14.8 11.1 14.1 11.8 9.1

China 2.1 3.4 2.8 4.1 4.3 5.6

Indonesia 9.0 7.7 8.3 6.3 4.9 5.0

Others 6.0 3.4 3.5 5.7 4.4 3.8

Total 74.6 73.1 93.2 93.6 68.8 77.6Source: NFMS

Demand for fresh chilled sashimi tuna remained stable in the USA, which is now the second largest market for non-canned tuna products.

Canned tuna: positive trends continue in major markets

The lower price of USD 2 000/tonne CFR Bangkok, at which skipjack has been traded since early July, has softened canned tuna prices by 2-5% in recent weeks. Demand for canned tuna in European and USA markets continues to improve. Packers in Asia reported better sales in the second quarter of 2013 as customers used up low-priced inventories.

USA

The confidence of US consumers has improved slightly as a result of positive economic indications and there are signs of willingness to spend more on products that meet changing tastes and provide value for money. To revive demand for canned tuna major tuna packers

ImportsFresh Tuna: USA

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Yellowfin 8.7 7.6 8.1 8.3 8.3 8.0

Bigeye 3.0 2.7 2.5 1.5 2.0 2.0

Albacore 0.3 0.4 0.2 0.3 0.4 0.4

Bluefin 0.2 0.2 0.3 0.2 0.2 0.3

Skipjack 0.0 0.0 0.0 0.0 0.0 0.0

Others 0.2 0.1 0.2 0.2 0.2 0.3

Total 12.4 11.0 11.3 10.5 11.1 11.0Source: NMFS

ImportsTuna loins: USA

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Thailand 8.0 4.7 13.2 14.2 8.6 13.3

Fiji 5.2 5.8 6.3 4.2 4.0 5.7

China 0.2 0.0 0.0 2.0 5.8 5.2

Mauritius 3.5 3.4 2.3 3.4 2.9 4.7

Ecuador 0.3 0.0 0.1 0.0 1.3 0.7

Trin & Tob 5.1 5.1 4.2 3.2 0.0 0.0

Others 1.1 2.3 7.3 4.9 8.2 6.0

Total 23.4 21.3 33.5 31.9 30.8 35.6Source: NFMS

14 Globefish Highlights October 2013

recipes using Bumble Bee’s canned products, including tuna.

Meanwhile the National Oceanic and Atmospheric Administration (NOAA) approved the new Dolphin Protection Consumer Act that came into effect on 13 July this year. The ruling includes a period of education and outreach to provide the fishing industry with additional guidance on enforcement up to 1 January 2014. NOAA said the new act is compliant with a WTO ruling and it requires that any canned tuna sold in the US with a Dolphin-Safe label must have a certification that no dolphins were killed or seriously injured in the process, no matter what gear type was used or where the tuna was caught.

Europe

On the whole consumer sentiment has improved and retailers have reported better sales of canned tuna in recent months. Innovative products and promotions were undertaken by major packers, and these, coupled with the growing popularity of private (supermarket) brands, have contributed to increasing imports. For the first 6 months of the year, canned tuna imports into the EU-27 (external) posted positive growth of 13.6% in volume and 31.8% in value on a year on year basis, amounting to 197 162 tonnes worth USD 1.14 billion.

Canned tuna shipments to selected European major markets also increased significantly except to Italy, which posted negative growth of almost 8% for the January to June 2013 period compared with the same period last year. Italy imported less from Spain (-19.1%), its largest supplier, but shipments from Seychelles increased sharply (+48.4%) indicating that buyers opted for cheaper alternatives.

Germany imported more canned tuna this year (+14.6%) with more supplies reported from Ecuador (+82%) and Thailand (+73.3%). Ecuador overtook the Philippines as the number one supplier as supplies from

TUNA

CFR PricesCanned tuna*: USA, EUROPE

* 48x6.5 oz Europe, 48x6 oz USA, chunk, origin Thailand Source: GLOBEFISH

the latter dropped by 15.6% during the reporting period.

Thailand and Ecuador also did well in the French market supplying 31% and 51.7% more respectively in 2013, while Cote d’Ivoire managed to increase its shipments by 19.4% overtaking Seychelles as the largest supplier.

British consumers bought 8.4% less canned fish in the last 12 months up to June this year, according to Nielsen’s report. The canned tuna market, however, seemed to be better this year as reflected in higher imports. Up to June 2013 imports increased by 7.3% with more supplies coming from Asian countries such as Thailand (+59.3%) and Indonesia (+50%). Shipments from Mauritius, the largest supplier to UK, dropped by more than 19%.

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep-

09

Nov-

09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov-

10

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep-

11

Nov-

11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov-

12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

USD/carton

USA

Europe

ImportsCanned tuna: France

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Côte d’Ivoire 16.0 11.7 10.0 6.1 10.8 12.9

Seychelles 7.9 6.6 6.5 9.5 12.0 12.5

Spain 10.6 10.0 11.1 16.7 8.9 10.5

Ecuador 4.3 7.2 6.6 7.4 5.8 7.6

Thailand 3.0 4.8 4.6 5.2 2.9 4.4

Madagascar 4.4 5.1 1.7 5.0 3.7 3.3

Mauritius 0.6 0.4 0.8 1.1 2.2 2.7

Ghana 2.2 3.2 3.8 4.3 3.0 2.2

Others 6.6 7.5 4.7 3.6 2.5 3.2

Total 55.5 56.5 49.8 58.9 51.9 59.3Source: Direction Nationale des Statistiques du CommerceExtérieur – DNSCE

ImportsCanned tuna: Germany

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Ecuador 15.2 8.2 5.0 5.1 3.9 7.1

Philippines 7.4 10.1 7.7 8.6 7.7 6.5

Papua NG 0.7 2.0 5.6 4.7 5.9 4.7

Netherlands 0.2 1.9 2.4 3.6 2.9 2.7

Thailand 3.6 2.1 2.4 1.9 1.5 2.6

Indonesia 3.1 3.6 3.1 4.2 3.1 2.0

Seychelles 3.9 0.6 1.9 1.0 0.1 0.3

Others 4.2 4.7 3.7 7.0 7.3 11.1

Total 38.3 33.1 31.8 36.1 32.3 37.0Source: Germany Customs

15Globefish Highlights October 2013

TUNA

Graphs Source: GLOBEFISH European Price Report

ImportsCanned tuna: Italy

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Spain 22.6 21.0 21.6 25.1 23.2 18.8

Seychelles 2.6 3.0 3.1 2.7 3.1 4.6

Côte d’Ivoire 4.0 5.4 2.9 2.2 4.6 3.7

Colombia 5.1 4.2 5.3 5.6 4.7 3.5

Ecuador 1.0 1.6 3.0 2.3 1.8 3.1

Portugal 1.0 0.8 0.5 0.8 1.0 1.1

Mauritius 1.5 1.2 1.6 1.5 1.2 1.0

Thailand 1.5 1.2 1.6 1.5 1.2 1.0

France 3.4 3.6 0.3 1.0 0.5 0.1

Others 2.1 2.3 1.6 2.1 3.1 4.0

Total 44.8 44.3 41.4 44.8 44.4 40.9Source: ISTAT

ImportsTuna loins: Italy

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Ecuador 5.0 7.3 5.1 5.5 5.0 6.0

Thailand 2.2 8.4 4.4 3.2 4.8 2.7

China 0.4 2.2 2.2 2.3 1.5 1.6

Kenya 3.4 0.7 1.0 1.9 1.3 1.6

Mauritius 3.4 1.5 2.2 0.7 1.5 1.0

Others 5.2 2.0 4.7 5.3 4.1 6.2

Total 19.6 22.1 19.6 18.9 18.1 19.1Source: ISTAT

ImportsTuna loins: Spain

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Ecuador 12.2 16.6 15.0 12.9 11.1 10.9

China 1.2 1.6 2.2 3.1 1.6 5.0

Thailand 3.5 6.6 4.9 10.6 2.1 4.5

Guatemala 0.0 2.7 4.5 4.0 4.2 3.7

El Salvador 6.9 9.1 4.5 2.9 2.7 3.2

Mauritius 0.9 2.2 2.4 6.6 4.1 2.1

Indonesia 0.0 0.0 0.0 0.8 2.0 1.6

Others 1.9 4.6 2.9 3.8 4.7 5.1

Total 26.6 43.4 36.3 44.6 32.6 35.9Source: Agencia Tributaria

2.051.90

0.501.001.502.002.503.00

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep-

10N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-1

1Se

p-11

Nov

-11

Jan-

12M

ar-1

2M

ay-1

2Ju

l-12

Sep-

12N

ov-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3Se

p-13

Skipjack Bangkok CFR

Skipjack Ecuador, ex-vessel

USD/kg

Tuna - Pacific Ocean

2.45

1.63

0.501.001.502.002.503.00

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep-

10N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-1

1Se

p-11

Nov

-11

Jan-

12M

ar-1

2M

ay-1

2Ju

l-12

Sep-

12N

ov-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3Se

p-13

Yellowfin > 10 kg, Spain CFR

Skipjack main sizes, Spain CFREUR/kg

Tuna - Spanish canneries

1.49

2.26

1.63

2.40

0.501.001.502.002.503.00

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep-

10N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-1

1Se

p-11

Nov

-11

Jan-

12M

ar-1

2M

ay-1

2Ju

l-12

Sep-

12N

ov-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3Se

p-13

Skipjack, Seychelles, FOB

Yellowfin, Seychelles, FOB

Skipjack, Abidjan ex-vessel

Yellowfin, Abidjan, > 10 kg, ex-vessel

EUR/kg

Tuna - Indian/Atlantic Oceans

7.308.65

2.003.004.005.006.007.008.009.00

10.00

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep-

10N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-1

1Se

p-11

Nov

-11

Jan-

12M

ar-1

2M

ay-1

2Ju

l-12

Sep-

12N

ov-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3Se

p-13

Skipjack - frozen cooked loins, single cleaned, Spain/Italy DDP

Yellowfin - frozen cooked loins, double cleaned, Italy DDPUSD/kg

Tuna - Loins

16 Globefish Highlights October 2013

the UK (+159.4%), Germany (+83.9%), France (+62.3%), Argentina (+19.5%) and Chile (+68.5%). Surprisingly exports to Syria were also significantly up by 193.4%.

In the domestic market TUF reported that canned fish demand in Thailand was flat in the second half of last year compared with an average annual growth of 3-5% in recent years. In 2012, the overall market value of Thai canned fish was THB 6.2 billion (USD 207 million).

In China, the tuna canning industry is growing, particularly in Zhoushan and Ningbo cities. In Zhousan there are 15 companies processing tuna with an installed capacity of around 25 000 tonnes raw material a year, Atuna.com reports.

Canned tuna prices in Japan for locally produced products increased by 9.3% as a result of increased production costs and the weaker yen. The value of imported products also increased (+18%) on a year on year basis in the January to June period, despite a 1.7% shortfall in the imported volume. Thailand had a 70% share in this supply.

Outlook

This year supplies of sashimi quality frozen bigeye tuna are expected to be lower than last year’s and firmer price levels are forecast.

Canned tuna sales in Europe and the USA are expected to continue on a positive trend in the third quarter because of improved consumer’s confidence and better sales during summer. Canned tuna prices, however, will remain high as the skipjack price is predicted to rebound to above USD 2 000 towards the end of the year.

Source: ITN

CFR PricesFrozen Skipjack: Thailand and Africa

Taking advantage of the EU duty free import quota for pre-cooked tuna loins, Spain imported more from Asia this year, particularly from China (+212.5%) and Thailand (+114.3%). Nevertheless Ecuador remained the largest supplier of pre-cooked tuna loins to Spain, though shipment from this source dropped slightly (-1.8%) this year. Ecuador, however, managed to supply more (+20%) pre-cooked tuna loins to Italy.

Asia

Asian canned tuna producing countries are hopeful that they will get better market access to the EU markets next year. The Philippines is expecting to receive preferential treatment for its canned tuna exports to the EU under the enhanced Generalized Scheme of Preferences or GSP Plus program to be implemented from 1 January 2014 while Thailand has resumed its free trade agreement negotiation with the EU. To support the negotiation, 130 Thai companies including Thai Union Frozen Products (TUF) recently signed a memorandum of understanding to adopt the International Labour Organization’s Good Labour Practices (GLP) program. Many accusations have been targeted at the Thai tuna industry, especially from Spain, which has continually accused Thailand of labour violations and poor working conditions.

With better demand from some major markets Thai canned tuna exports maintained a positive trend and grew marginally by 1.4% in quantity during the first semester of this year against the same period of 2012. In value terms, however, the exports were more or less stagnant. Shipments to Egypt, the number one destination in the Middle East, dropped by almost half. Similar trends were recorded in exports to Libya (-12.9%), Papua New Guinea (-27.3%), Italy (-83.9%), South Africa (-15.5%), UAE (-27.3%) and to the largest market USA (-3.4%). Higher shipments to other markets, however, managed to offset the declines as exports to some European and Latin American markets increased significantly, for example to

TUNA

0

500

1000

1500

2000

2500

Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13

USD/tonne

Thailand

Africa

ExportsCanned tuna: Thailand

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)USA 43.7 48.1 59.8 53.3 37.2 36.0

Australia 18.7 15.3 20.6 23.6 16.0 15.9

Japan 12.8 12.9 11.6 14.8 13.5 14.5

Libya 18.1 15.5 11.1 4.2 15.8 13.8

Canada 14.8 16.3 14.4 16.9 12.8 13.2

Egypt 21.7 14.1 25.2 21.9 20.1 10.3

Saudi Arabia 10.5 7.1 12.0 10.2 10.9 9.1

UK 8.2 9.7 6.2 16.0 2.3 6.1

Tunisia * * * * 5.8 5.4

South Africa 5.0 5.6 4.9 4.6 5.4 4.6

Others 95.4 87.5 108.9 104.6 63.4 77.1

Total 248.9 232.1 274.7 270.1 203.2 206.0

* inlcuded under “others” Source: Thai Customs

17Globefish Highlights October 2013

GROUNDFISH

In spite of good supply cod prices have not dropped globally

Overall the supply situation for the main species of groundfish is mixed. Taking all sources of supply into consideration, there is probably an over-supply of cod; however, cod prices in Europe and Asia have increased over the summer months. China, in particular, is facing a serious shortage of supplies both for its fillet and surimi production, and this may have opened the Chinese market for exports of both raw material and surimi. For saithe and haddock, there is also a shortage of supplies and prices have pushed upward.

Supplies

The much publicized cod quota for the Barents Sea for this season (2013 – 2014) is very high at almost one million tonnes. This is shared mainly by Norway, Russia, and the EU. However Iceland has also increased its quotas for cod and haddock. The total allowable catch (TAC) of cod in Iceland was set at 214 000 tonnes, up from 195 400 tonnes last year (+9.5%). The Icelandic haddock quota was increased from 36 000 tonnes last year to 38 000 tonnes this year.

Cod

There has been much media speculation about low cod prices, but in fact this is not necessarily true in all cases. To some extent it depends of the product type and also on the geographic position of market. During the late spring and summer, a general increase in cod prices has actually been registered.

Fresh cod prices have increased in 2013 because of a growing demand for fresh fish. From Iceland it is reported that prices of fresh whitefish such as cod, haddock, saithe and redfish are up. It seems that there is a widely diversified market for whitefish products that is behaving quite differently these days from the norms of the past.

Norwegian average export prices for fresh, round

cod increased from NOK 15.30 per kg in April to NOK 22.23 per kg in August (+45.3%), while average export prices for round frozen cod increased from NOK 14.91 per kg in April to NOK 15.40 in August (+3.3%). For both of these products, prices peaked in July, at NOK 23.14 per kg for fresh cod and NOK 15.57 for frozen cod.

In September, Norway raised the minimum first-

Alaska43%

Hake15%Haddock

6%

Saithe5%

Cod18%

Whiting 3%

Others6%

Groundfish production by species (2011)

Source: FAO

ImportsFrozen cod: UK

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)China 11.2 6.7 6.3 7.7 8.4 10.0

Iceland 6.7 7.7 7.8 8.3 8.4 9.3

Russian Fed. 4.0 4.6 5.0 4.1 6.4 7.6

Norway 3.2 4.4 4.7 5.6 4.3 5.1

Denmark 4.6 3.6 3.5 3.7 3.8 4.7

Faroe Is. 3.2 3.1 3.0 3.5 3.6 4.4

Germany 1.5 0.9 3.3 4.3 4.1 4.0

Greenland 0.5 0.8 1.9 1.8 2.4 2.2

Poland 2.0 2.2 1.3 1.1 1.4 1.4

Others 3.0 1.7 1.9 2.0 1.1 1.5

Total 39.9 35.7 38.7 42.1 43.9 50.2Source: Her Majesty’s Revenue & Customs

ImportsFrozen cod fillets: Germany

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)China 6.7 4.4 4.0 7.4 5.5 5.7

Poland 1.5 0.9 4.1 2.1 2.6 3.6

Viet Nam 0.0 0.0 0.7 0.7 0.7 1.1

Denmark 1.1 0.8 1.1 1.3 0.8 0.5

Russian Fed 0.7 0.4 0.3 0.3 0.3 0.4

Norway 0.1 0.1 0.2 0.2 0.2 0.3

Iceland 0.2 0.5 0.4 0.3 0.0 0.1

Others 1.0 1.0 0.6 0.2 1.1 1.7

Total 11.3 8.1 11.4 12.5 11.2 13.4Source: Germany Customs

18 Globefish Highlights October 2013

hand cod price by between NOK 0.25 and 0.50 per kg. For the larger sizes, prices were increased by NOK 0.25, while for the smallest size (under 1 kg) prices were raised by NOK 0.50. Last year, Norwegian minimum cod prices were reduced in anticipation of the 33% increase in the cod quota for the Barents Sea.

Demand in China is also high because of shortage of domestic supplies for the processing industry. This has helped to drive up the price of cod in recent months.

Hake, haddock, pollock and hoki

There is a shortage of haddock supplies on the European market, and this has pushed prices up. Haddock prices in Norway went up by 27%, while cod and saithe prices dropped by 15% and 22%, respectively. Consequently, haddock prices are now on a par with cod prices, but then there is the danger that consumers will eventually protest against these high prices and move to other products.

It is expected that the haddock quotas for 2014, which will be set by the joint Russian-Norwegian fisheries commission in early October, will be lower than the 2013 quota. Thus, ICES has recommended that the quota be cut by 25% to just 150 000 tonnes, down from 200 000 tonnes in 2013 and 318 000 tonnes in 2012.

Russian catches of pollock increased slightly during

GROUNDFISH

the first half of 2013, to 1 045 610 tonnes, up by 0.4% from the same period last year. This year there has been a noticeable change in processing at sea. While production of H&G products during the first half of the year fell by 4.3% to 454 120 tonnes and frozen whole fish dropped by 6.6% to 67 120 tonnes, frozen-at-sea fillets went up by 59% to 28 690 tonnes.

New Zealand is expected to increase its hoki quota for the coming season. Hoki stocks have had a six-year growth period and last year 130 000 tonnes were landed. It is expected that the quota for the coming season will be raised to 150 000 tonnes. While this is considered a rather modest increase, it is welcomed as a responsible move that will continue to build up the stocks.

Demand for hoki is good locally, but also in European markets such as Poland, the Netherlands, Italy, France and the UK. There has also been an increasing demand for hoki blocks imported for further processing. Demand for hoki is expected to continue to grow and prices have also been increasing.

The Chinese processing industry is dependent on imports of raw material and when prices for Russian pollock increased recently Chinese processors were put under pressure, with falling profit margins. At the same time operating costs increased. Prices for double frozen

ImportsCod-like groundfish: USA

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)FilletsChina 35.1 38.2 34.4 42.2 41.0 40.0

Iceland 4.3 5.1 5.0 3.5 4.6 5.9

Russian Fed. NA 0.8 6.5 2.4 1.9 3.6

Canada 1.9 2.3 2.6 2.1 2.6 1.8

Norway 0.4 0.6 0.4 0.3 0.4 1.3

Others 3.4 2.4 1.3 1.6 4.1 6.5

Total 45.1 49.4 50.2 52.1 54.6 59.1Blocks/SlabsChina 17.8 21.4 18.1 17.3 17.1 15.4

Iceland 0.2 0.7 0.3 0.3 0.5 0.8

Argentina 1.5 0.5 0.3 0.2 0.5 0.6

Norway 0.0 0.1 0.4 0.5 0.2 0.4

Russian Fed. 0.3 1.8 0.8 0.6 0.3 0.2

Canada 0.3 0.3 0.1 0.1 0.2 0.1

Others 0.8 0.9 1.0 1.0 1.4 2.4

Total 20.9 25.7 21.0 20.0 20.2 19.9Gr. Total 66.0 75.1 71.2 72.1 74.8 79.0

Source: NMFS

ImportsFrozen hake fillets: Germany

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Namibia 1.1 0.9 1.1 1.4 1.7 1.6

Peru 2.2 1.6 2.3 2.1 0.5 1.4

Argentina 1.7 1.9 1.5 0.3 0.6 0.9

USA 2.5 2.4 2.8 2.4 2.6 0.4

Others 2.1 2.0 0.7 0.9 0.7 0.6

Total 9.6 8.8 8.4 7.1 6.1 4.9Source: Germany Customs

ImportsFrozen Alaska pollock fillets: Germany

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)China 43.9 46.0 44.1 45.7 38.1 46.0

USA 29.4 13.5 18.4 22.7 27.6 15.3

Russian Fed 16.7 13.2 9.1 8.5 4.5 6.3

Others 2.1 3.0 2.4 2.4 2.8 2.0

Total 92.1 75.8 74.0 79.3 73.0 69.6Source: Germany Customs

19Globefish Highlights October 2013

GROUNDFISH

Russian pollock increased from USD 1 300 to USD 1 400 – 1 500 per tonne. Chinese producers are now looking for an excuse to increase their own prices, so pollock products may be in line for a general price increase.

Surimi

The export value of surimi from the USA during the first half of the year declined by some 5% to USD 167.8 million. Export volume, on the contrary, increased by 4.9% to 73 486 tonnes. In other words, prices for US surimi fell during this period.

The largest decline was registered for exports to Japan, which fell by 18.5% by volume to 25 996 tonnes, and the value of US surimi exports to Japan fell by almost 25% to USD 52.4 million.

US exports to the Republic of Korea, in contrast, increased by almost 29% by volume to 19 248 tonnes. Export value to the Republic of Korea rose by 11.7% to USD 67 million.

The French surimi producer Fleury Michon reported a 15% drop in sales in France during the second quarter of 2013. The reasons given for this decline were bad weather, limited raw material supplies, a weak promotional effort, and the poor European economy.

In Japan, surimi production has been declining through the first half of the year. It is reported that the six onshore plants in Hokkaido saw a drop in production of as much as 18% during the first six months of the year. As a result, surimi inventory has been reduced by 19%.

Demand for surimi in China is growing, and at present, demand is outstripping supplies. Surimi products, such as fish balls, are very popular in China. Although China constructed several surimi plants in the first decade of

ImportsFrozen hake: Italy

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)Argentina 5.4 5.5 4.8 4.4 3.2 3.9

Namibia 1.2 1.8 2.1 2.1 2.3 3.1

S. Africa 2.7 2.8 2.6 2.6 2.9 3.0

Spain 2.3 2.3 3.6 3.3 2.6 2.4

Uruguay 1.3 1.6 3.4 3.5 1.2 1.9

Peru 0.1 0.0 0.0 0.1 0.3 0.8

Chile 0.1 0.5 0.8 0.4 0.3 0.3

Others 1.2 1.5 2.8 2.8 2.9 3.8

Total 14.3 16.0 20.1 19.2 15.7 19.2Source: ISTAT

ImportsFrozen Alaska pollock fillets: France

Jan-Jun2008 2009 2010 2011 2012 2013

(1 000 tonnes)China 11.5 12.9 9.8 14.7 12.5 11.2

Russian Fed. 4.2 3.4 2.4 2.9 2.5 5.8

USA 4.5 3.1 2.5 5.2 4.9 4.0

Germany 2.3 1.2 1.8 3.0 2.8 2.9

Others 0.2 0.6 0.8 0.2 0.3 0.3

Total 22.7 21.1 17.3 26.0 23.0 24.2Source: Direction Nationale des Statistiques du CommerceExtérieur – DNSCE

2.40

1.31.61.92.22.52.8

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Surimi - In France, origin: Spain

Stick 250 gr/pc

EUR/kg

Source: European Price Report

the century and has increased fishing efforts in the South China Sea, the plants have now been forced to turn to imported raw material to meet demand. It is estimated that Chinese surimi production in 2012 amounted to about 240 000 tonnes.

However, during the first months of 2013, surimi production fell by up to 30% as a result of the shortage of raw material. Surimi consumption is estimated to be growing rapidly, at over 10% per year. With the raw material shortage and with reduced production, China is now forced to import both fish for raw material and surimi products from other producing countries.

International trade

Norwegian exports of fresh cod grew dramatically during the first half of 2013. The volume in fact doubled compared with the same period in 2012. Shipments to all major markets were up.

Norwegian cod exports to the UK continued to grow during the second quarter of 2013. Norwegian cod exports were up by 89% to 4 613 tonnes during the second quarter, totalling 12 690 tonnes at an FOB value of NOK 291.8 million. That represents an increase in volume of 43.5%, but prices were much lower so the increase in

20 Globefish Highlights October 2013

value was just 0.2%.

In spite of this, cod lost market share on the UK market in 2012. According to data from market research company Nielsen, the volume of cod sold through supermarkets in the UK declined by 3.2%, to 39 485 tonnes in 2012 compared with 2011, with the value falling by 1.1% to GBP 317.7 million.

However there was considerable variation from product to product. Sales of fresh cod increased by as much as 8% to 11 607 tonnes, but prices fell so that the value of fresh cod sold declined by GBP 0.19 per kg. The volume of frozen cod sales fell by 7.2% to 27 878 tonnes, while prices for frozen cod held better and in fact registered a slight increase compared with 2011.

Imports of cod-like groundfish into the USA increased during the first six months of the year. Fillet imports increased by 8.2% to 59 100 tonnes, while imports of blocks and slabs declined slightly by 1.5% to 19 900 tonnes. At the same time major shifts between the relative positions of the main suppliers took place.

US imports of double frozen pollock blocks went down by as much as 28% during the first half of 2013. Imports fell from 70 000 tonnes to 50 000 tonnes. This is the lowest level for several years and well below peak years of 2005 (83 000 tonnes) and 2009 (77 000 tonnes). The main supplier as usual is China, which has had supply problems. These were reflected in the decline in shipments to the USA. Compensating for the lower imports from China, imports from Russia have increased four-fold, but from a very low base.

German imports of Alaska pollock fillets declined by 4.7% to 69 600 tonnes. China, as the main supplier, strengthened its position on this market and increased shipments by over 20%. The USA lost market share and experienced a 45% decline in shipments to Germany.

German imports of frozen cod fillets increased by almost 20% during the first half of the year. The main supplier, China, maintained its position, while Poland increased shipments by over 38%. German imports of frozen hake fillets declined, on the contrary, by almost 20%.

French imports of frozen Alaska pollock fillets were quite stable during the first half of the year at 24 200 tonnes. China shipped slightly less product to France, while Russia increased exports to France by 132% to 5 800 tonnes.

There was a 14% increase in UK imports of frozen cod in the first half of 2013. The main suppliers, China, Iceland and Russia, all supplied more, as did most other suppliers. Since 2009, the UK has had a steady increase in imports of frozen cod.

GROUNDFISH

CFR pricesGroundfish blocks: USA

Source: ITN

Frozen hake imports into Italy were also up during the first half of 2013. Total imports increased by 22% to 19 200 tonnes. Argentina, Namibia and South Africa are the main suppliers to this market.

Black cod

In the Pacific, black cod prices have remained stable in spite of the fact that fishermen are now targeting this species after the summer season. In general, prices for black cod are low compared with a year ago. There was good demand both in Europe and Asia (especially China) for this fish, but with the high price levels last year it took some time to bring down inventories.

At present supplies are improving, and therefore a certain downward price adjustment is expected. The changing market for luxury seafood in China is one of the driving factors.

Outlook