globaleconomic outlook synchinglower - calpers › docs › board-agendas › 201901 › full ›...

TRANSCRIPT

Global conomic Outlook

Synchin Lower

CalPER Offsite, January 22, 2019

Joachim Fels

For in titutional inve tor u e only

PIMCO_Phil_05

PIMCO’s investment process Forums: Themes that anchor portfolio construction

Annual secular forum

(3–5 year outlook)

Assess long-term trends demographics, political factors, globalisation of trade and capital, productivity / technology

OUTLOOK

ecular Trend

Quarterly cyclical forum

Cyclical

Trend

(6–12 month outlook)

Major economy / emerging market inflation and GDP forecasts and fine tune the secular outlook

SOURCE PIMCO Refer to Appendix for additional investment strategy, outlook and risk information.

1

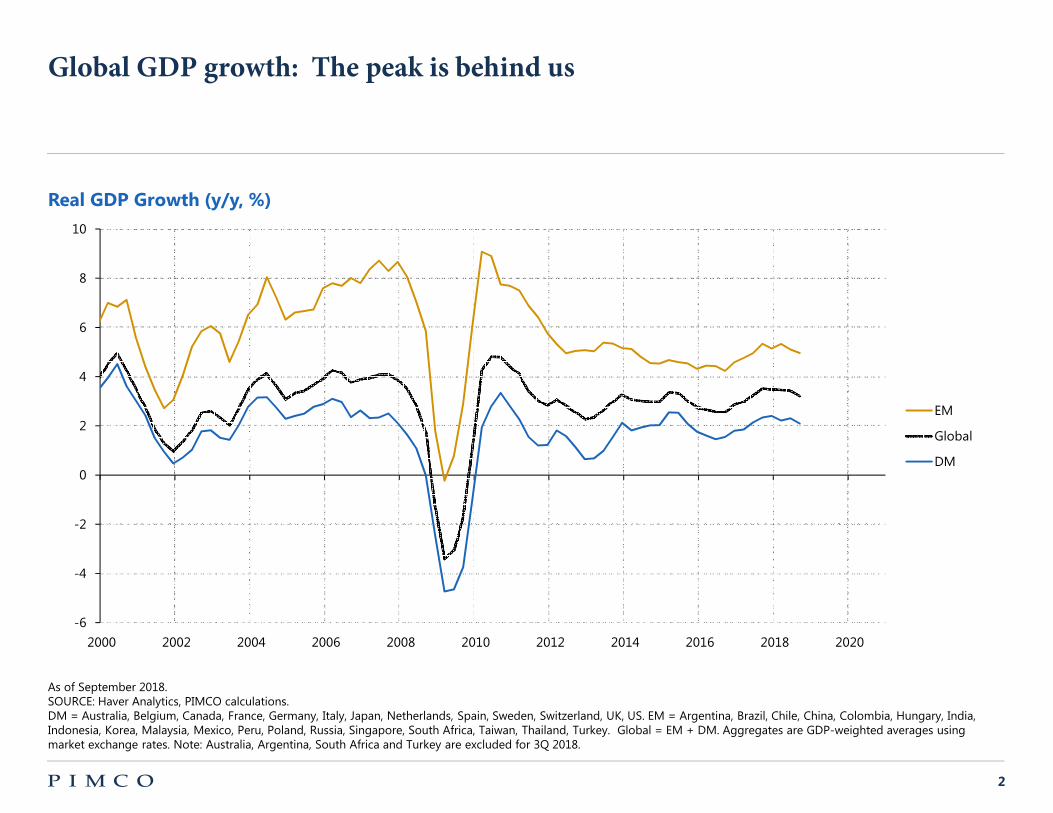

Global GDP growth: The peak is behind us

Real GDP Growth (y/y, %)

10

8

6

4

EM 2

Global

DM 0

-2

-4

-6

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

As of September 2018. SOURCE Haver Analytics, PIMCO calculations. DM = Australia, Belgium, Canada, France, Germany, Italy, Japan, Netherlands, Spain, Sweden, Switzerland, UK, US. EM = Argentina, Brazil, Chile, China, Colombia, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Poland, Russia, Singapore, South Africa, Taiwan, Thailand, Turkey. Global = EM + DM. Aggregates are GDP-weighted averages using market exchange rates. Note Australia, Argentina, South Africa and Turkey are excluded for 3Q 2018.

2

Headline inflation has peaked, core inflation flat like a pancake

Headline CPI Inflation (%y/y) Major Economy Core CPI Inflation (%y/y)

10 4

8 3

26

EM 1 Euro (HICP)

4 Global US

DM China

2 0 Japan

UK

-1

0

-2

-2

2007 2009 2011 2013 2015 2017 2019 -3

07 08 09 10 11 12 13 14 15 16 17 18 19

As of November 2018. SOURCE Haver Analytics, PIMCO calculations. DM = Australia, Belgium, Canada, France, Germany, Italy, Japan, Netherlands, Spain, Sweden, Switzerland, UK, US. EM = Argentina, Brazil, Chile, China, Colombia, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Poland, Russia, Singapore, South Africa, Taiwan, Thailand, Turkey. Global = EM + DM. Aggregates are GDP-weighted averages using market exchange rates.

3

10

2

0

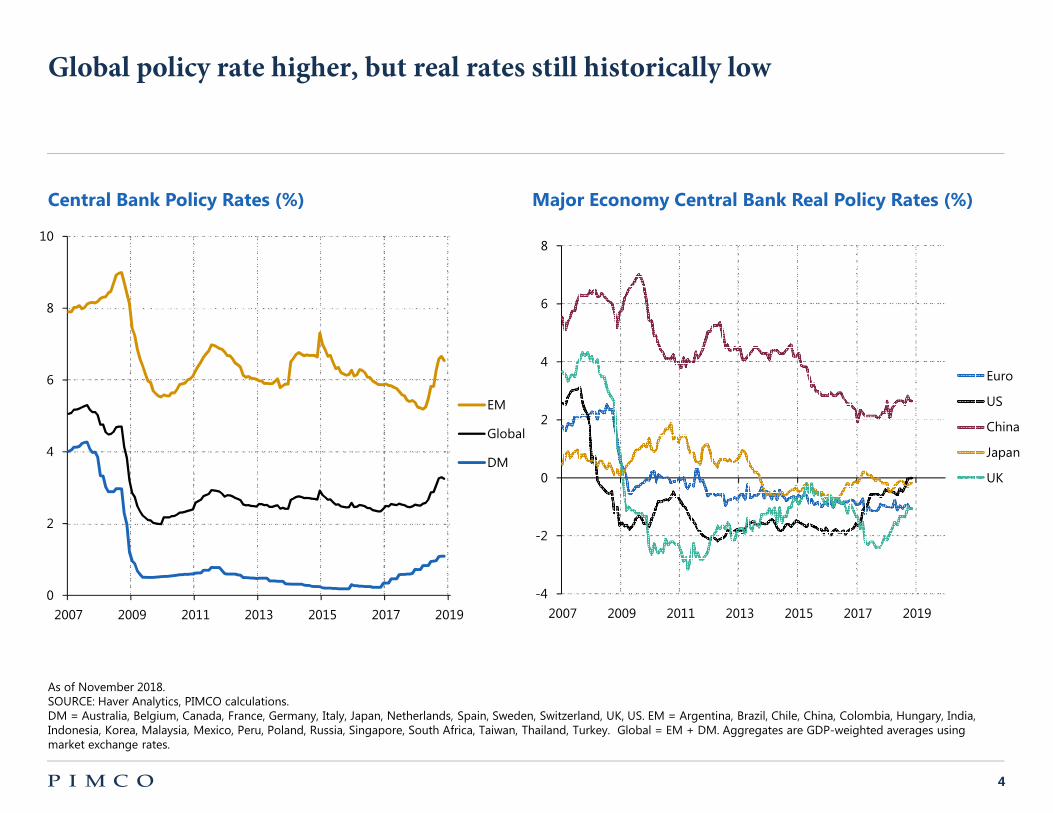

Global policy rate higher, but real rates still historically low

Central Bank Policy Rate (%) Major Economy Central Bank Real Policy Rate (%)

8

8 6

6

4

EM

Global

DM

4

2

0

Euro

US

China

Japan

UK

-2

-4

2007 2009 2011 2013 2015 2017 2019 2007 2009 2011 2013 2015 2017 2019

As of November 2018. SOURCE Haver Analytics, PIMCO calculations. DM = Australia, Belgium, Canada, France, Germany, Italy, Japan, Netherlands, Spain, Sweden, Switzerland, UK, US. EM = Argentina, Brazil, Chile, China, Colombia, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Poland, Russia, Singapore, South Africa, Taiwan, Thailand, Turkey. Global = EM + DM. Aggregates are GDP-weighted averages using market exchange rates.

4

95

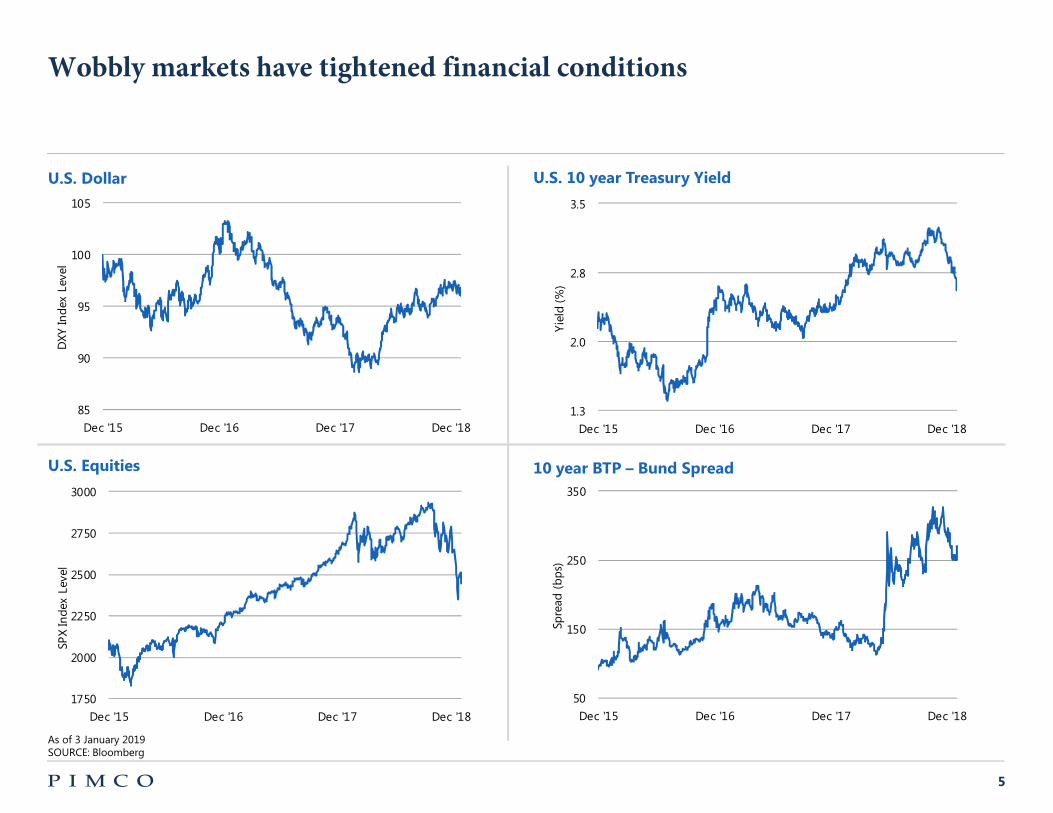

Wobbly markets have tightened financial conditions

U.S. 10 year Trea ury Yield U.S. Dollar

105 3.5

100

2.0 90

85 1.3 Dec '15 Dec '16 Dec '17 Dec '18 Dec '15 Dec '16 Dec '17 Dec '18

Yie

ld(%

)

DXY

Ind

ex L

evel

2.8

U.S. Equitie 10 year BTP – Bund Spread

350 3000

2750

2000

1750 50

Dec '15 Dec '16 Dec '17 Dec '18 Dec '15 Dec '16 Dec '17 Dec '18

As of 3 January 2019 SOURCE Bloomberg

250

SPX

Inde

x Le

vel

Spre

ad (

bp

s)

2500

2250 150

5

62

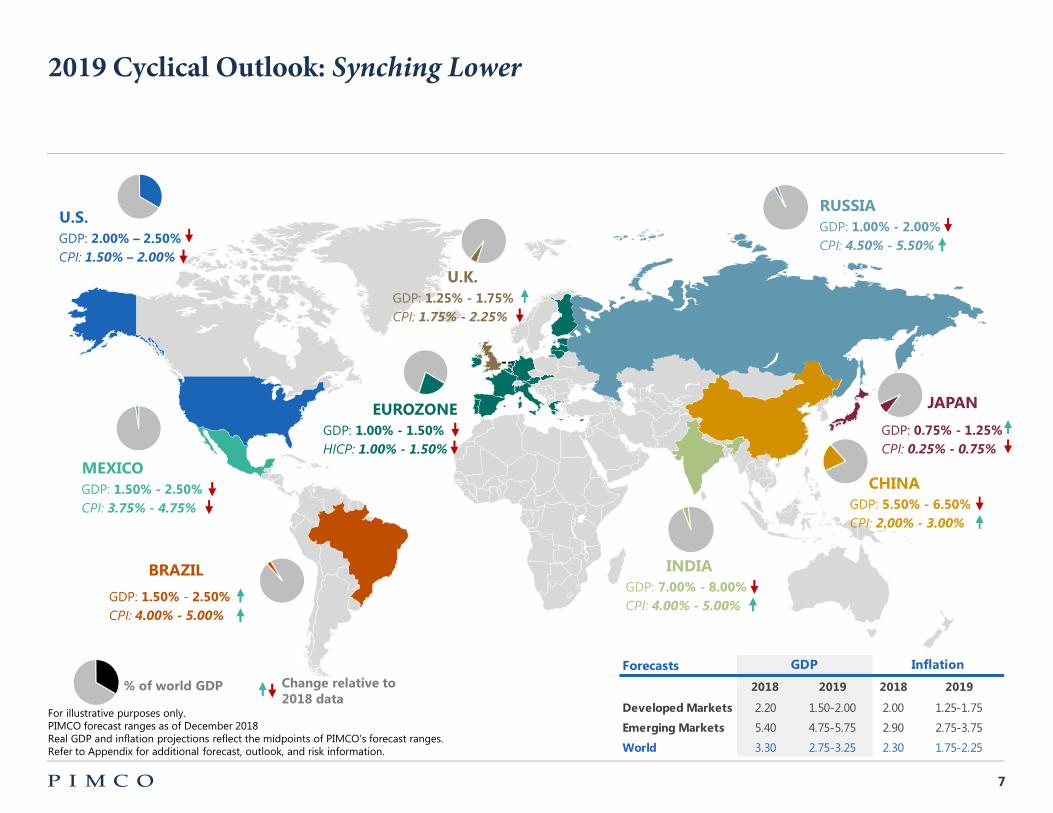

2019 Cyclical Outlook: ynching Lower

Composite PMIs U.S. Eurozone EM

Debates shaping the outlook for 2019:

exp

ansi

ona

ry

PMI

60

1. How ate is it in the cyc e? 58

56 2. The end of U.S. economic exceptiona ism?

54

3. Wi inf ation ever return? 52

4. The Fed pauses, then what? 50

48 5. U.S. versus China: truce or peace?

46

2012 2013 2014 2015 2016 2017 2018

As of December 2018 SOURCE Haver Analytics

44

6

--

2019 Cyclical Outlook: ynching Lower

U.S.

GDP 2.00% – 2.50%

CPI: 1.50% – 2.00%

U.K.

GDP 1.25% - 1.75%

CPI: 1.75% - 2.25%

EUROZONE

GDP 1.00% - 1.50%

HICP: 1.00% - 1.50%

MEXICO

GDP 1.50% - 2.50%

CPI: 3.75% - 4.75%

BRAZIL

GDP 1.50% - 2.50%

CPI: 4.00% - 5.00%

% of world GDP Change relative to 2018 data

For illustrative purposes only. PIMCO forecast ranges as of December 2018 Real GDP and inflation projections reflect the midpoints of PIMCO’s forecast ranges. Refer to Appendix for additional forecast, outlook, and risk information.

RUSSIA

GDP 1.00% - 2.00%

CPI: 4.50% - 5.50%

JAPAN

GDP 0.75% - 1.25%

CPI: 0.25% - 0.75%

CHINA

GDP 5.50% - 6.50%

CPI: 2.00% - 3.00%

INDIA

GDP 7.00% - 8.00%

CPI: 4.00% - 5.00%

Foreca t GDP Inflation

Developed Market

Emerging Market

World

2018

2.20

5.40

3.30

2019

1.50-2.00

4.75-5.75

2.75-3.25

2018

2.00

2.90

2.30

2019

1.25-1.75

2.75-3.75

1.75-2.25

Mk_3cs_intl_outlook_01 7

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

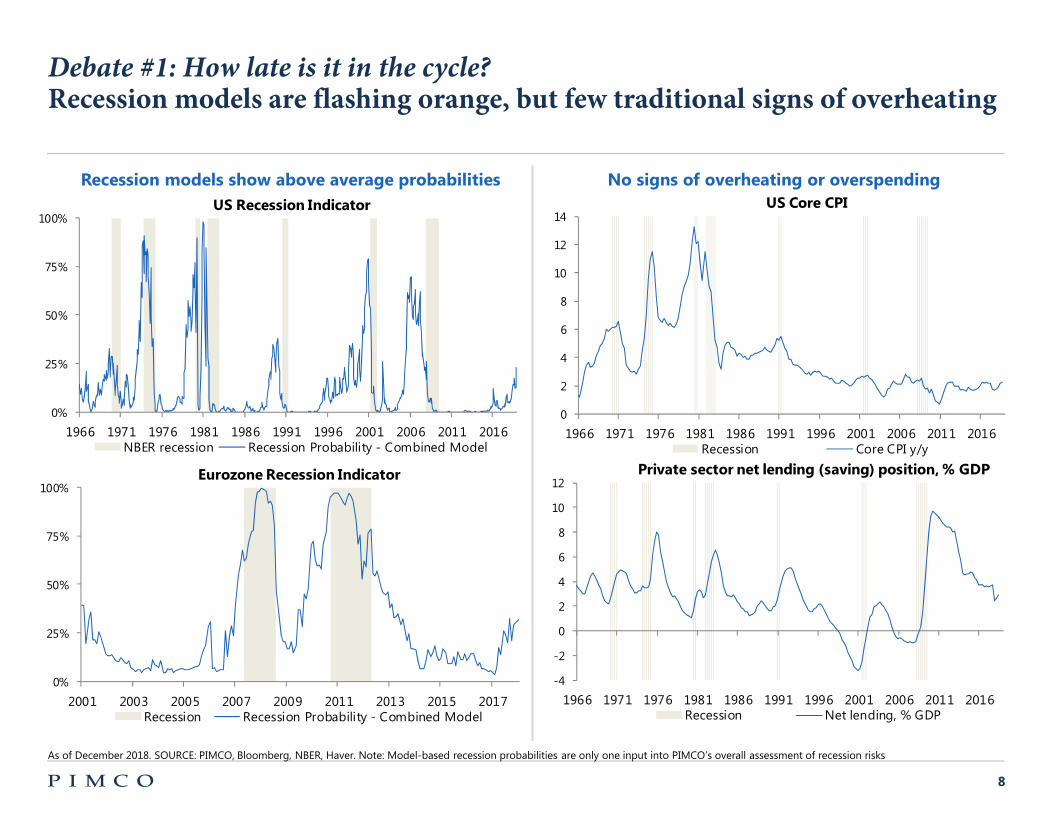

Debate #1: How late is it in the cycle? Recession models are flashing orange, but few traditional signs of overheating

Rece ion model how above average probabilitie

US Rece ion Indicator

No ign of overheating or over pending

US Core CPI

1971 1976 1981 1986 1991 1996 2001 2006 2011 2016 Recession Core CPI y/y

Private ector net lending ( aving) po ition,% GDP

100%

75%

50%

25%

0%

14

12

10

8

6

4

2

0

1966 1971 1976 1981 1986 1991 1996 2001 2006 2011 2016 1966 NBER recession Recession Probability - Combined Model

Eurozone Rece ion Indicator 12 100%

10

875%

6

450%

2

25% 0

-2

0% -4

1966 1971 1976 1981 1986 1991 1996 2001 2006 2011 2016 2001 2003 2005 2007 2009 2011 2013 2015 2017 Recession Net lending, % GDP Recession Recession Probability - Combined Model

As of December 2018. SOURCE PIMCO, Bloomberg, NBER, Haver. Note Model-based recession probabilities are only one input into PIMCO’s overall assessment of recession risks

8

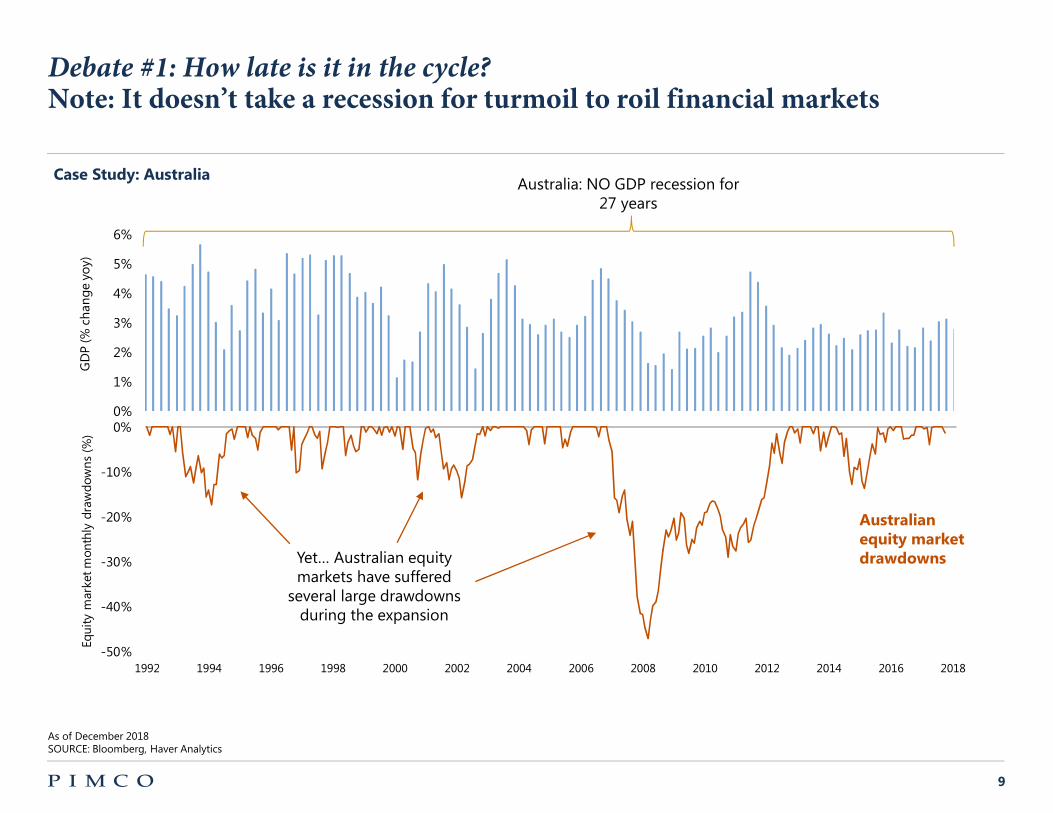

Debate #1: How late is it in the cycle? Note: It doesn’t take a recession for turmoil to roil financial markets

-40%

-30%

-20%

-10%

0%

Equi

ty m

arke

tmon

thly

dra

wdo

wns

(%)

0%

1%

2%

3%

4%

5%

6%

GD

P (%

cha

nge

yoy)

Yet… Australian equity markets have suffered

several large drawdowns during the expansion

Australia NO GDP recession for 27 years

Au tralian equity market drawdown

Ca e Study: Au tralia

-50% 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

As of December 2018 SOURCE Bloomberg, Haver Analytics

9

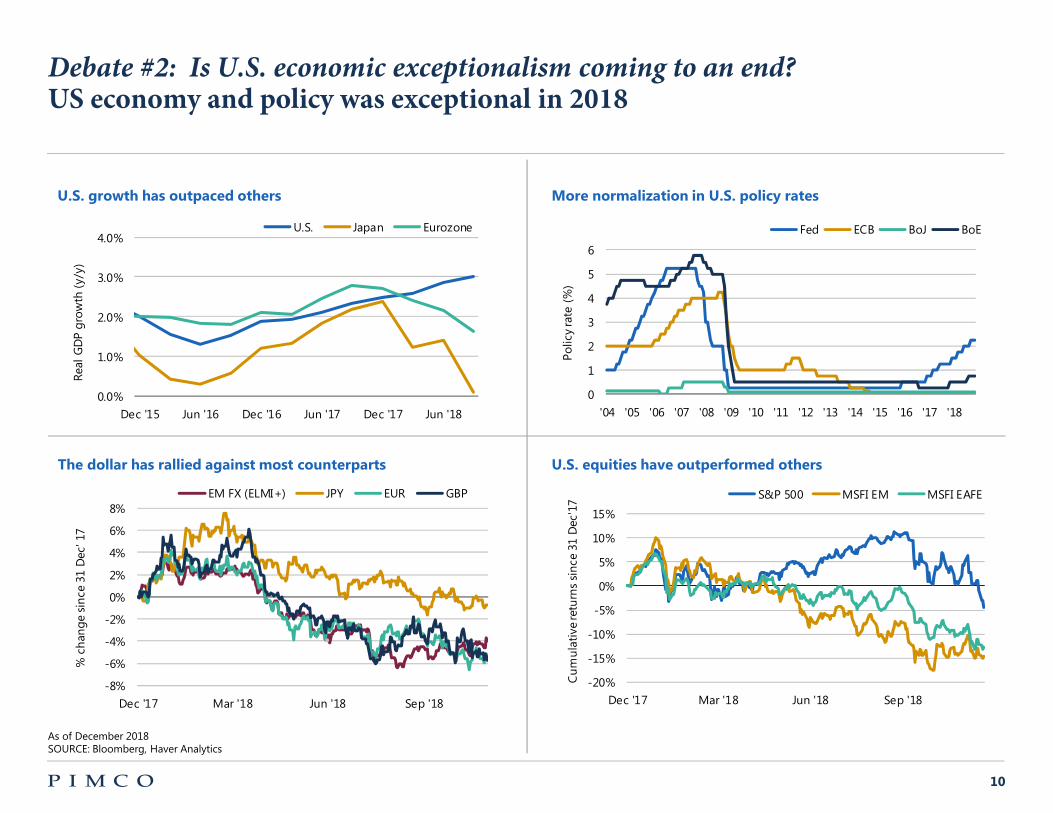

Debate #2: Is U. . economic exceptionalism coming to an end? US economy and policy was exceptional in 2018

U.S. growth ha outpaced other More normalization in U.S. policy rate

U.S. Japan Eurozone Fed ECB BoJ BoE

6

1.0%

2.0%

3.0%

4.0%

0.0% '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

Rea

l G

DP

gro

wth

(y/

y)

5

Polic

yra

te (

%)

4

3

2

1

0

Dec '15 Jun '16 Dec '16 Jun '17 Dec '17 Jun '18

The dollar ha rallied again t mo t counterpart U.S. equitie have outperformed other

EM FX (ELMI+) JPY EUR GBP S&P 500 MSFI EM MSFI EAFE

Cu

mu

lati

vere

turn

ssi

nce

31 D

ec'1

7 8% 15% 6%

4%

2%

0%

-2%

-4%

% c

han

ge

sin

ce31

Dec

' 17

10%

5%

0%

-5%

-10%

-15% -6%

-8% -20%

Dec '17 Mar '18 Jun '18 Sep '18 Dec '17 Mar '18 Jun '18 Sep '18

As of December 2018 SOURCE Bloomberg, Haver Analytics

10

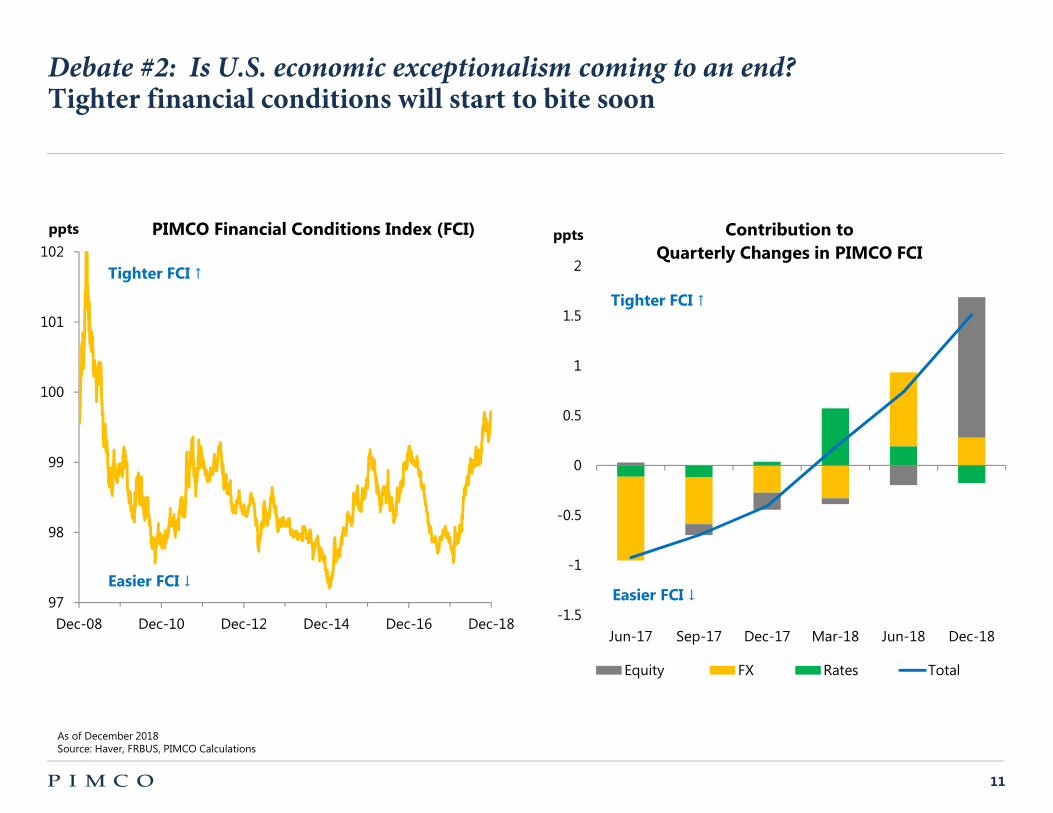

Debate #2: Is U. . economic exceptionalism coming to an end? Tighter financial conditions will start to bite soon

ppt

102

101

100

99

98

97

PIMCO Financial Condition Index (FCI) ppt Contribution to

Quarterly Change in PIMCO FCI 2Tighter FCI ↑

1.5

1

0.5

0

-0.5

-1

Tighter FCI ↑

Ea ier FCI ↓ Ea ier FCI ↓

-1.5 Dec-08 Dec-10 Dec-12 Dec-14 Dec-16 Dec-18

Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Dec-18

Equity FX Rates Total

As of December 2018 Source Haver, FRBUS, PIMCO Calculations

11

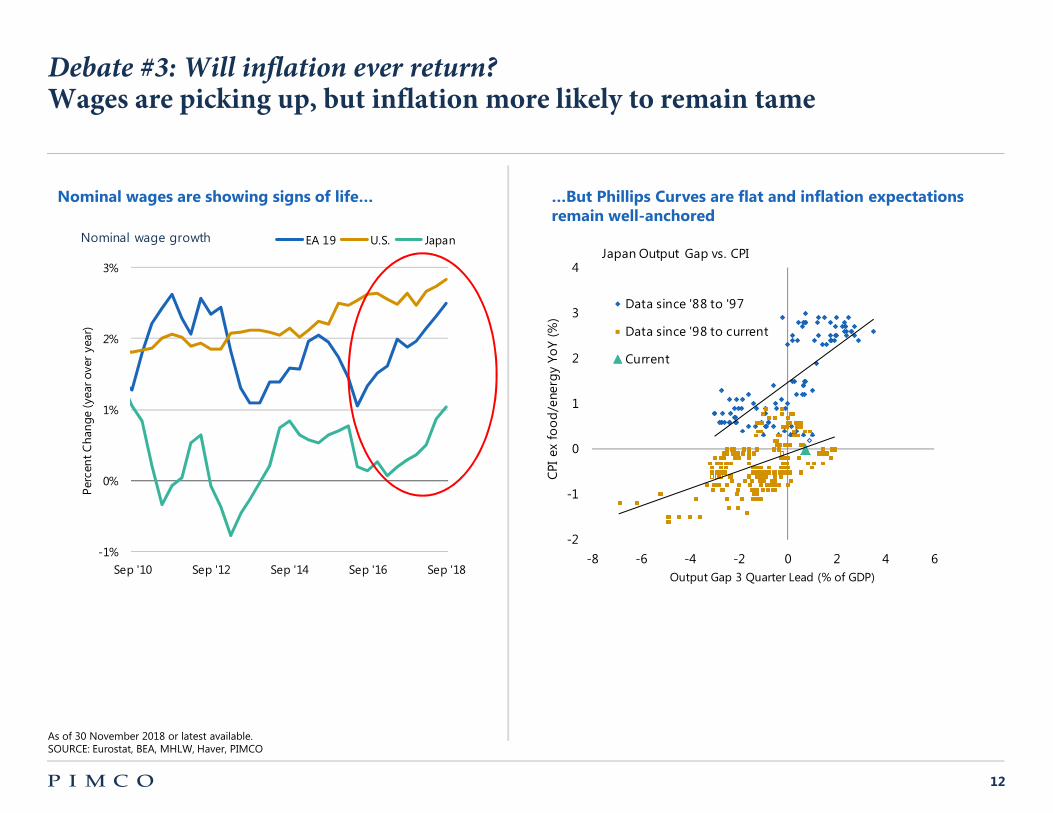

Debate #3: Will inflation ever return? Wages are picking up, but inflation more likely to remain tame

Nominal wage are howing ign of life… …But Phillip Curve are flat and inflation expectation remain well-anchored

Nominal wage growth EA 19 U.S. Japan Japan Output Gap vs. CPI

4

0%

1%

2%

3%

-1%

Data since '88 to '97

Data since '98 to current

Current

-8 -6 -4 -2 0 2 4 6

Per

cen

t C

han

ge(y

ear

over

yea

r)

CPI

ex

foo

d/e

nerg

y Yo

Y (%

) 3

2

1

0

-1

-2

Sep '10 Sep '12 Sep '14 Sep '16 Sep '18 Output Gap 3 Quarter Lead (% of GDP)

As of 30 November 2018 or latest available. SOURCE Eurostat, BEA, MHLW, Haver, PIMCO

12

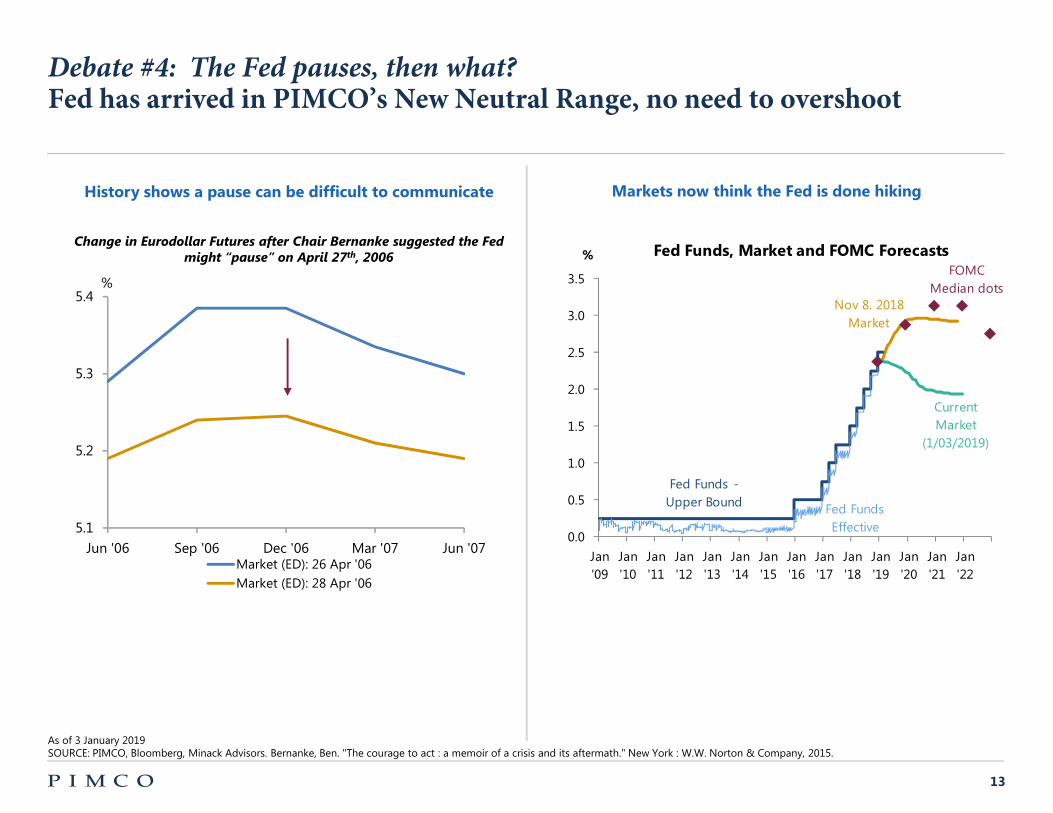

Debate #4: The Fed pauses, then what? Fed has arrived in PIMCO’s New Neutral Range, no need to overshoot

Market now think the Fed i done hiking Hi tory how a pau e can be difficult to communicate

Change in Eurodollar Futures after Chair Bernanke suggested the Fed Fed Fund , Market and FOMC Foreca t %might “pause” on April 27th, 2006

FOMC 3.5 % Median dots

Nov 8. 2018 3.0 Market

2.5

2.0 Current Market

(1/03/2019) 1.5

1.0

0.5

Effective 0.0

Fed Funds -Upper Bound Fed Funds

5.4

5.3

5.2

5.1

Jun '06 Sep '06 Dec '06 Mar '07 Jun '07 Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan

Market (ED) 26 Apr '06 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22

Market (ED) 28 Apr '06

As of 3 January 2019 SOURCE PIMCO, Bloomberg, Minack Advisors. Bernanke, Ben. "The courage to act a memoir of a crisis and its aftermath." New York W.W. Norton & Company, 2015.

13

-

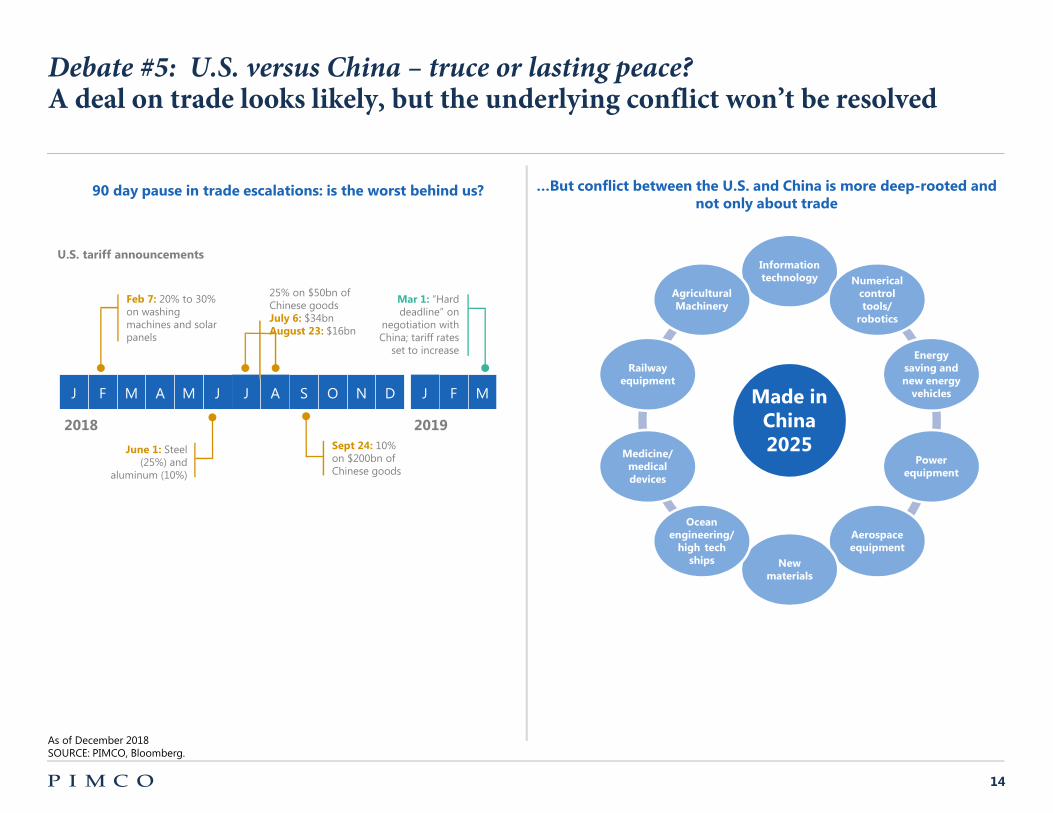

Debate #5: U. . versus China – truce or lasting peace? A deal on trade looks likely, but the underlying conflict won’t be resolved

…But conflict between the U.S. and China i more deep-rooted and 90 day pau e in trade e calation : i the wor t behind u ? not only about trade

Made in China 2025

Information technology Numerical

control tool /

robotic

Energy aving and new energy

vehicle

Power equipment

Aero pace equipment

New material

Ocean engineering/ high tech

hip

Medicine/ medical device

Railway equipment

Agricultural Machinery

U.S. tariff announcement

Feb 7: 20% to 30% on washing machines and solar panels

J F M A M J J A S O N D J F M

2018

June 1: Steel (25%) and

aluminum (10%)

25% on $50bn of Mar 1: “Hard

Chinese goods deadline” on

July 6: $34bn negotiation with

Augu t 23: $16bn China; tariff rates

set to increase

2019

Sept 24: 10% on $200bn of Chinese goods

As of December 2018 SOURCE PIMCO, Bloomberg.

14

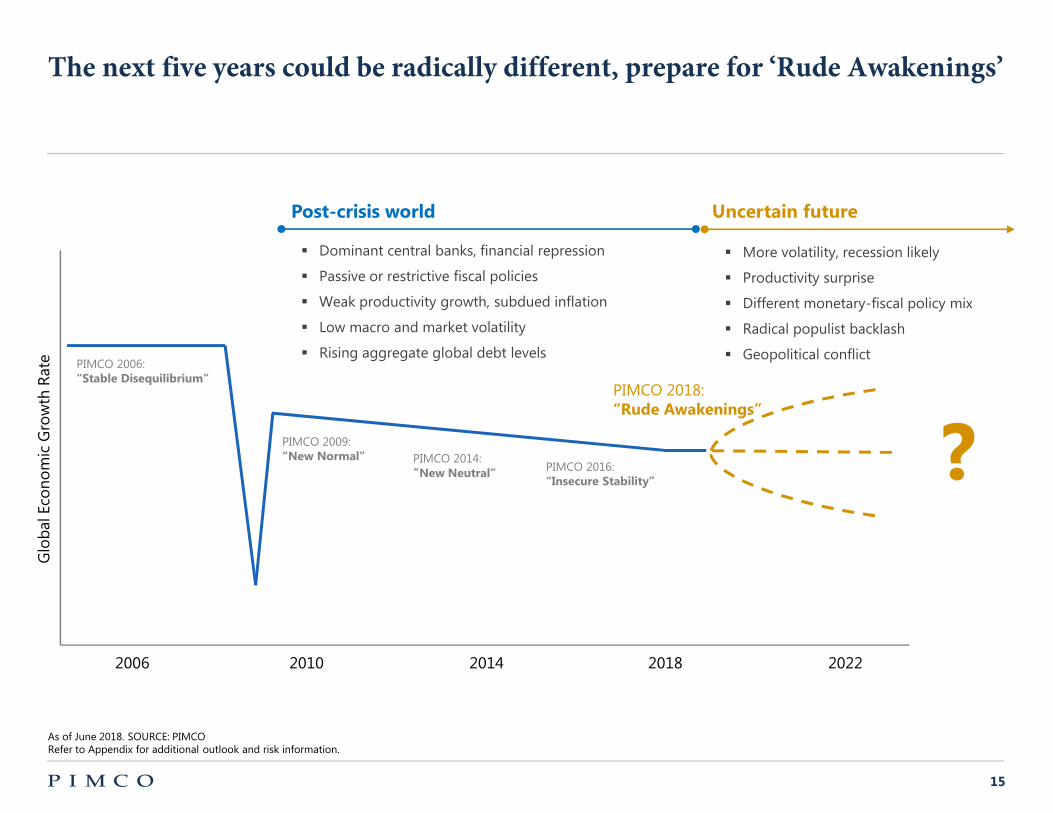

The next five years could be radically different, prepare for ‘Rude Awakenings’

Uncertain future

• More volatility, recession likely

• Productivity surprise

• Different monetary-fiscal policy mix

• Radical populist backlash

• Geopolitical conflict

PIMCO 2018 “Rude Awakening ”

?

Po t-cri i world

• Dominant central banks, financial repression

• Passive or restrictive fiscal policies

• Weak productivity growth, subdued inflation

• Low macro and market volatility

• Rising aggregate global debt levels

PIMCO 2009 “New Normal” PIMCO 2014

Glo

bal

Eco

nom

ic G

row

th R

ate PIMCO 2006

“Stable Di equilibrium”

PIMCO 2016 “New Neutral”

“In ecure Stability”

2006 2010 2014 2018 2022

As of June 2018. SOURCE PIMCO Refer to Appendix for additional outlook and risk information.

15

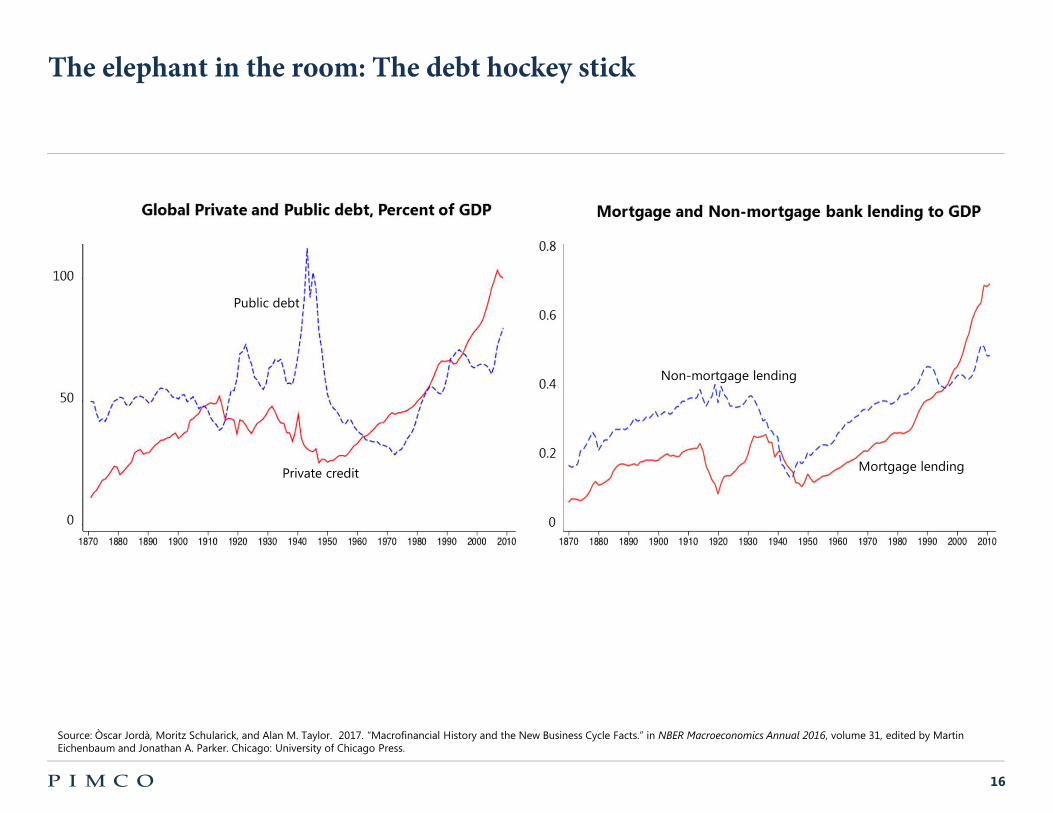

The elephant in the room: The debt hockey stick

Public debt

Private credit

Non-mortgage lending

Mortgage lending

Source Òscar Jordà, Moritz Schularick, and Alan M. Taylor. 2017. “Macrofinancial History and the New Business Cycle Facts.” in NBER Macroeconomics Annua 2016, volume 31, edited by Martin Eichenbaum and Jonathan A. Parker. Chicago University of Chicago Press.

16

Appendix

FORECAST Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve. INVESTMENT STRATEGY There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. OUTLOOK Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice. RISK Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or domiciled ecuritie may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Equitie may decline in value due to both real and perceived general market, economic, and industry conditions. This material contains the current opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO provides services only to qualified institutions and investors. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Inve tment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission.

These materials are being provided on the express basis that they and any related communications (whether written or oral) will not cause Pacific Investment Management Company LLC (or any affiliate) (collectively, “PIMCO”) to become an investment advice fiduciary under ERISA or the Internal Revenue Code, as the recipients are fully aware that PIMCO (i) is not undertaking to provide impartial investment advice, make a recommendation regarding the acquisition, holding or disposal of an investment, act as an impartial adviser, or give advice in a fiduciary capacity, and (ii) has a financial interest in the offering and sale of one or more products and services, which may depend on a number of factors relating to PIMCO (and its affiliates’) internal business objectives, and which has been disclosed to the recipient. These materials are also being provided on PIMCO’s understanding that the recipients they are directed to are all financially sophisticated, capable of evaluating investment risks independently, both in general and with regard to particular transactions and investment strategies. If this is not the case, we ask that you inform us immediately. You should consult your own separate advisors before making any investment decisions. These materials are also being provided on the express basis that they and any related communications will not cause PIMCO (or any affiliate) to become an investment advice fiduciary under ERISA or the Internal Revenue Code with respect to any recipient or any employee benefit plan or IRA because (i) the recipients are all independent of PIMCO and its affiliates, and (ii) upon review of all relevant facts and circumstances, the recipients have concluded that they have no financial interest, ownership interest, or other relationship, agreement or understanding with PIMCO or any affiliate that would limit any fiduciary responsibility that any recipient may have with respect to any Plan on behalf of which this information may be utilized. If this is not the case, or if there is any relationship with any recipient of which you are aware that would call into question the recipient’s ability to independently fulfill its responsibilities to any such Plan, we ask that you let us know immediately.

The information provided herein is intended to be used solely by the recipient in considering the products or services described herein and may not be used for any other reason, personal or otherwise.

CMR2019-0107-375046

17