global sourcing annual report 2005 –preview

TRANSCRIPT

Global Sourcing

Annual Report 2005 – Preview

Proprietary & Confidential. © 2005 Everest Partners, L.P.2

Section I: Executive summary and implications for stakeholders

Section II: Offshore Market overview� Executive summary� Value proposition� Market state

� Maturity� Size

� Future prospects� Evolution of drivers/external forces� Evolution of demand structures� Market growth� Supply considerations

Section III: Buyer adoption� Executive summary� Adoption and penetration

� Geography� Size� Industry� Function/process

� Operating models

Section IV: Supplier developments� Executive summary � Impact of offshoring� Supplier segmentation� Future evolution and challenges

Topic

Table of contents (page 1 of 2)

4

1515182224283233363840

4242444648515354

5858606575

Proprietary & Confidential. © 2005 Everest Partners, L.P.3

Table of contents (page 2 of 2)

Section V: Savings� Executive summary � Estimating savings

� Discrepancies in savings� Savings analysis and estimates

� Controlling savings� Implications and case studies

Section VI: Billing rates and supplier margins� Executive summary � Background� Historical trends� Future outlook� Implications

Section VII: Location optimization� Executive summary � Analysis framework

Section VIII: Risks and case studies� Executive summary � Risk impact� Understanding offshoring risks

� Dimensions/types� Case studies

� A perspective on offshoring risks

Appendix: Glossary of terms

78788080849094

9898101104108117

120120122

131131133136137139144

148

Topic

Proprietary & Confidential. © 2005 Everest Partners, L.P.4

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

22.00%

24.00%

26.00%

28.00%

30.00%

Dec Mar Jun Sep Dec Mar Jun Sep Dec

10

12

14

16

18

26

20

22

24

Dec-02

Mar-03

Jun -03

Sep-03

Dec-03

Mar-04

Jun -04

Sep-04

Dec-04

28

30

IT - Package implementation

The Global Sourcing report will have over 100 pages of

insightful information

Pioneers Emerging rapid growth Reaching maturity

Market value creation

MaturityOffshore IT market

Offshore BPO market

“Pure” offshore revenues

Onsite revenues

23-24

12-13

17.5-18

5.5-6

11-11.5

1-1.5

Market sizeMarket maturity

Industry adoption Supplier performance

Business models

Rates, costs and margins

23%

60%15%

9%62%

31%

Indian third-party model

US$ 9.2 billion US$ 3.6 billion

MNC captive model

BPOIT services

MNC1 third-party model

100% =

BPO – Core processes

BPO - Call centers

IT - ADM

BPO - OthersIT -Others

IT – R&D

BPO - HRO

BPO - FAO

BPO -Procurement IT - Infrastructure

Offshore process maturity Offshore market2004, US$ billion

Offshore model share in Indian market2004, US$ billion

Offshore process maturity2004, Percentage (100% = US$35 billion)

Net margin for new global players

Net margin for select Tier 2 Indian players

Net margins across new global and select Tier II Indian SuppliersDec 2002-2004, Percentage (%)

0.4%

0.4%

4%

4%

12%

16%

19%

45%

Pharmaceuticals

Healthcare

Transportation

Retail

Manufacturing

Others

Telecom and hi-tech

Financial services

0

10

20

30

2001 2002 2003 2004

Supplier operating margins2000-2004, Percentage

Average annual decrease3: -1.5%

CAGR 1%

Billing rates2000-2004, US$/hr

On-siteOffshore

CAGR -6%

0

20

40

60

80

2001 2002 2003 2004

Operating costs/employeesUS$ (‘000)

CAGR 5.8%

0

10

20

30

40

2001 2002 2003 2004

Proprietary & Confidential. © 2005 Everest Partners, L.P.5

The overall offshore market has evolved from its early

stages and offers larger value creation opportunities

today

1 Estimated growthSource: Everest Research Institute

Key characteristics� Emergence of locations outside of India as strong, feasible offshore alternatives

� Rapid growth in offshoring of BPO services

� Offshoring of IT services other than ADM services

� Increase in size of offshore deals� Entry of US IT suppliers into offshore locations to meet cost pressures

� Rapid maturity of pure-play offshore suppliers

� Substantial M&A activity� Establishment of select operating models and standards

Pioneers Emerging rapid growth Reaching maturity

Market value creation

Key characteristics� Emergence of India as a feasible offshore destination for IT services

� Setup of captives by select large global players

� Development of a handful of offshore suppliers

1998-991993-94 2000-01

Key characteristics� Increased adoption by a large number of companies

� Increased focus on processes and quality among suppliers

� Emergence of some operating models and standards

2005

Proprietary & Confidential. © 2005 Everest Partners, L.P.6

Mega companies - heavy adopters

Other users2

100% = ~5001

companies100% = US$ 7.7billion

Large companies – heavy adopters

Share of IT services imports from India

US-based companies

Mega companies - steady users

Large companies3 – steady users

IT services imports (from India) by US-based companies2004 Percentage (%)

1 Companies with revenues greater than US$10 billion2 Excludes companies with very small offshore deals2 Companies with revenues between US$1 billion and US$10 billion

Source: Everest Research Institute analysis

Offshore adoption is being driven by only a handful of the

Mega1 companies, with most of the other companies

being steady but small users

3%

25%13%

40%

6%

6%

26%

9%

20%

52%

Proprietary & Confidential. © 2005 Everest Partners, L.P.7

Companies offshoring are using multiple business

models

Typical offshore business models

Pure Captive Model• An internal cost center or a 100% subsidiary company to cater exclusively to the parent company

• Examples: Amex, Dell,

HSBC, Ford, Sun, etc.

Captive model

Build Operate Transfer (BOT)/ Joint Venture (JV)• Provider-owned/joint operations that are allowed to be transferred back to the customer

• Example: eServe-Citibank

Strategic alliance/Joint venture model

Inverted BOT• The offshore provider who provides only implementation support to start with and is allowed to buy in to the entity later

• Examples: AIG- Polaris, BA -

WNS

Pure third party offshoring• Use of a offshore provider to outsource business processes or IT services

• Examples: Lehman-Wipro,

NY Life-Infosys, Amazon-

Daksh

Third party offshoring model

Managed third party offsoring• Full/ part-time resources on the ground to facilitate transition, relationship mgmt and transfer of organization and domain knowledge to third party providers

• Example: Greenpoint-

Progeon

Offshore business models

Illustrative

Eventually, BOT model ends up as captive whereas inverted BOT ends up as third party

Proprietary & Confidential. © 2005 Everest Partners, L.P.8

13

41

29

13

4

Savings from offshore, while high, tend to be

inconsistent

20-29 30-39 40-49 50-59 60+

Buyers achieving select range of savingsPercentage

While 70 percent of buyers achieved savings between 30 and 50 percent, 30 percent of the buyers experienced savings that were outside this range, reinforcing the wide range of savings achieved in offshore contracts

While 70 percent of buyers achieved savings between 30 and 50 percent, 30 percent of the buyers experienced savings that were outside this range, reinforcing the wide range of savings achieved in offshore contracts

Range of savings (%)

Source: Everest 2004 Offshore Market Survey

Proprietary & Confidential. © 2005 Everest Partners, L.P.9

Recommended approach to defining and calculating savings

Gross savings = (percent of services offshored X labor arbitrage) + percent productivity improvement1

Net savings = Gross savings – (setup costs/contract term) – governance costs

Savings disparity occurs partially due to the variation in

definitions and complexity of calculations

Key notes

� The formulae above are for annualized savings over the term of a typical offshoring deal� Productivity improvements are assumed to include the entire process, and not only the offshored element (which might vary from one situation to another). Further, they refer to only cost savings and not quality improvements

� A portion of the savings might be reinvested into the business. These reinvestments are assumed to be actual savings, and accordingly, reinvestments are not deducted when calculating savings

� In addition to the above factors, macro-economic factors, such as inflation and exchange rate fluctuation, will affect savings over time

� Quality improvements in the offshored process can also increase savings

1 Effective savings on the original cost base, using appropriate formula for converting throughput increases to savingsSource: Everest Research Institute analysis

Proprietary & Confidential. © 2005 Everest Partners, L.P.10

However, a large part of the disparity arises due to

potential variations in the many factors which

impact savings, such as productivity

Annualized productivity improvement Percentage

No productivityImprovement

0-30% productivity improvement

30%+ productivityimprovement

27

38

35

Note:Productivity improvements were derived by measuring a wide range of relevant productivity measures such as average call handle time, number of invoices processed per FTE, claims per hour, agent utilization, reduction in development tine, etc.

Sample size: 30 transactionsSource: Everest 2004 Offshore Market Survey

Proprietary & Confidential. © 2005 Everest Partners, L.P.11

While offshoring still has a small share of the overall IT

and BPO services business, supplier adoption of offshore

ranges from low to highCSC

Capgemini

EDS

Accenture

Perot

IBM GS

ACS

Sapient

Infosys

Wipro

TCS

Cognizant

Satyam

HCL

Mphasis

Offshore/onsite ratio of employees1

20052, 100% = Total ‘000s employees

79 119 59 123 18 191 52 2 40 49 42 20 21 24 8

Capegemini

CSC

IBM GS

EDS

Accenture

Perot

ACS

Sapient

Cognizant

Infosys

Satyam

Wipro

HCL

Mphasis

Onsite FTEs

Offshore FTEs

TCS

1 Includes the entire FTE’s of the organization – IT services and BPO2 As of June 30, 2005; estimated where data not available

Source: Everest Research Institute

Proprietary & Confidential. © 2005 Everest Partners, L.P.12

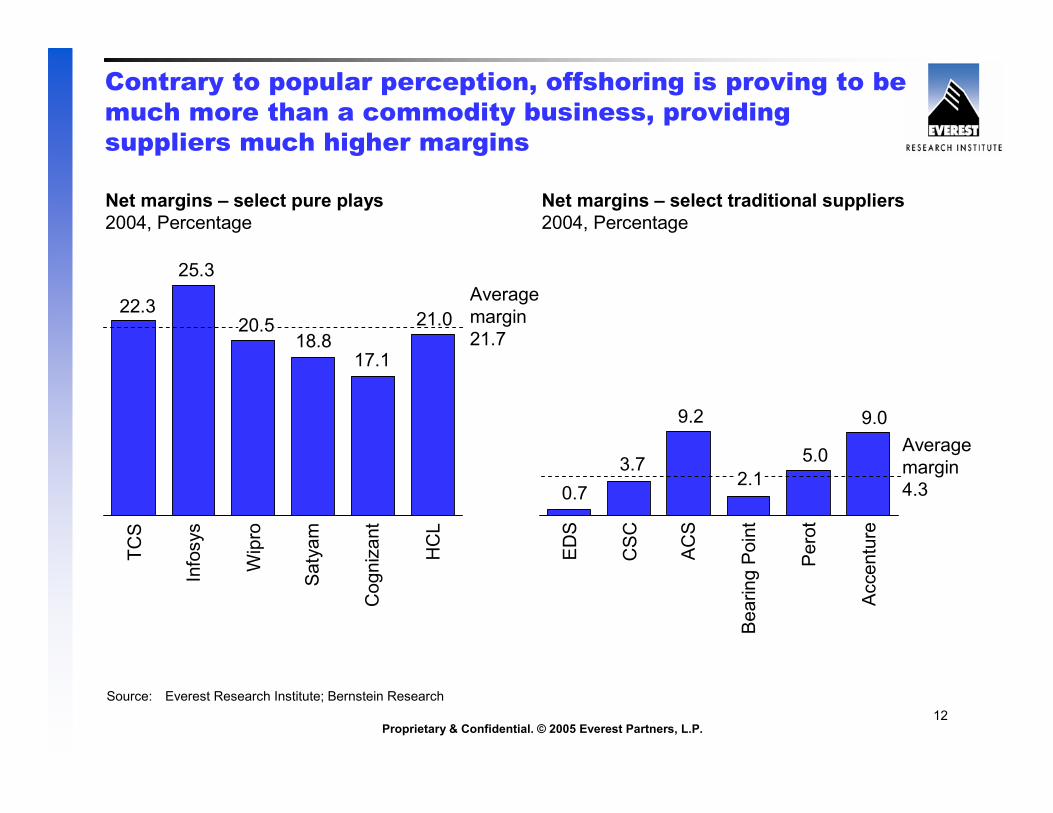

Contrary to popular perception, offshoring is proving to be

much more than a commodity business, providing

suppliers much higher margins

Net margins – select pure plays2004, Percentage

Net margins – select traditional suppliers2004, Percentage

Average margin 21.7

Average margin 4.3

22.3

0.7

9.2 9.0

18.817.1

21.0

25.3

TCS

Infosys

Wipro

Satyam

Cognizant

HCL

3.7 5.0

EDS

CSC

ACS

Bearing Point

Perot

Accenture

20.5

Source: Everest Research Institute; Bernstein Research

2.1

Proprietary & Confidential. © 2005 Everest Partners, L.P.13

In order to understand supplier segments in an offshoring

context, we view suppliers across two key dimensions

Rationale for “cutoffs”� Scale cutoff: 40,000 FTEs translates to roughly US$5 billion in revenues for IT services providers, an important size landmark in Everest’s opinion

� Offshore centricity cutoff: While this varies with suppliers’ business models, in general, Everest believes that having 20% of workforce offshore is indicative of a reasonable commitment to offshoring

100%

Scale (Total FTEs)

100,000

1. Are there suppliers who have achieved both scale and strong offshore presence?

2. How many large suppliers exist

who have the scale but have not

yet fully leveraged offshore?

3. How are the smaller suppliers doing in terms of leveraging offshore?

200,000

0

0%

Cutoff=40,000

Offshore centricity (Offshore FTEs as % of Total FTEs)

Cutoff=20%

50%

Supplier information collated from an Everest global survey on offshore capabilities –approximately 50 suppliers surveyed

Supplier information collated from an Everest global survey on offshore capabilities –approximately 50 suppliers surveyed

Supplier segmentation from an offshoring perspective2005

Source: Everest Research Institute

Proprietary & Confidential. © 2005 Everest Partners, L.P.14

Offshore billing rates and supplier margins have seen

significant variations over the last 7-8 years due to

changes in the market and competitive forces

Forces1 1998-2001 2001-2004

Offshore billing rates decreased by 6.0% p.a.; margins decreased by 1.5% p.a.

Demand for offshore services

Competitive intensity

Supplier cost structures

� Limited number of mature offshore suppliers

� Low cost structures� Low wages and wage increases� Favorable onsite-offshore mix

� Overall recession and an IT industry depression

� Increased supplier pressure due to � Increasing maturity of pure plays� Overcapacity built during 1998-2001

� Increase in cost structures� High wage growth

� Strong growth in overall IT spend� Surge of Y2K-related work� Dot-com boom leading to heavy investments in e-business

1 For the purpose of our analysis

Offshore billing rates increased by 12.0% p.a.; margins increased by 5.0% p.a.

Proprietary & Confidential. © 2005 Everest Partners, L.P.15

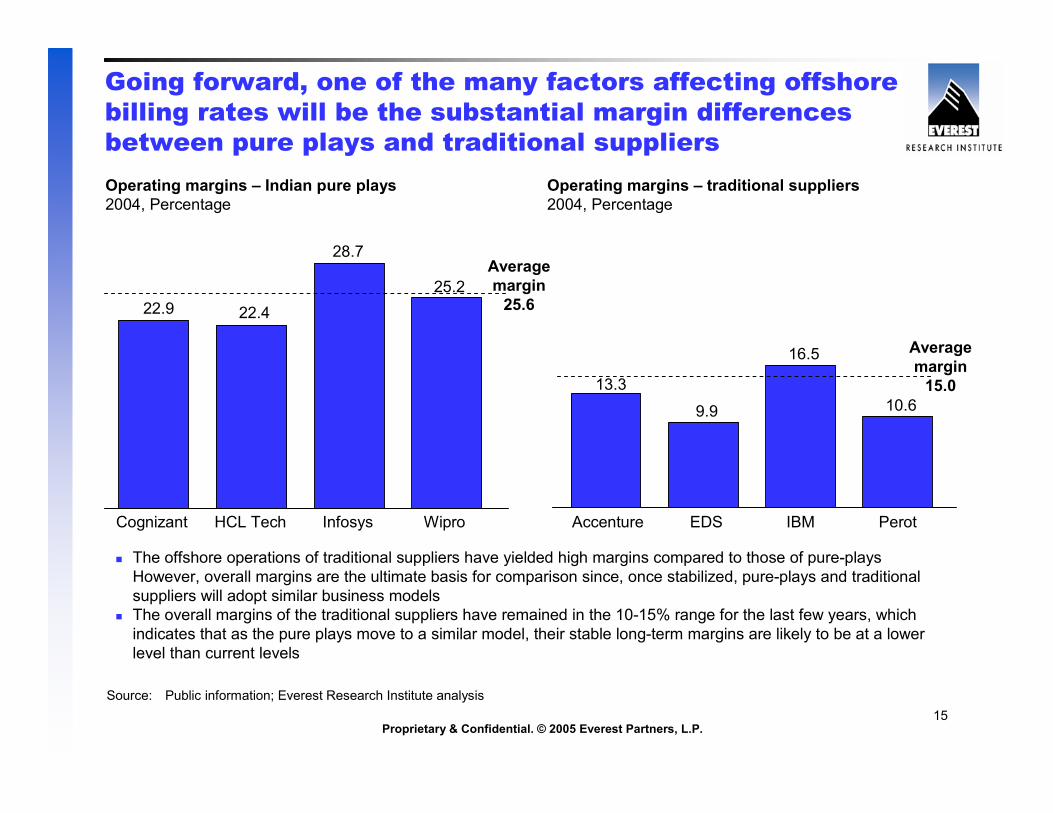

Going forward, one of the many factors affecting offshore

billing rates will be the substantial margin differences

between pure plays and traditional suppliers

Operating margins – Indian pure plays2004, Percentage

Operating margins – traditional suppliers2004, Percentage

Average margin 25.6

Average margin 15.0

� The offshore operations of traditional suppliers have yielded high margins compared to those of pure-plays However, overall margins are the ultimate basis for comparison since, once stabilized, pure-plays and traditional suppliers will adopt similar business models

� The overall margins of the traditional suppliers have remained in the 10-15% range for the last few years, which indicates that as the pure plays move to a similar model, their stable long-term margins are likely to be at a lower level than current levels

22.9 22.4

28.7

25.2

13.3

9.9

16.5

10.6

Cognizant HCL Tech Infosys Wipro Accenture EDS IBM Perot

Source: Public information; Everest Research Institute analysis

Proprietary & Confidential. © 2005 Everest Partners, L.P.16

Margin pressures will be strong too, but suppliers can

leverage measures such as improved utilization levels

and offshore-onsite revenue mix to combat rising costsEmployee utilization Sep-01 to Dec-04, Percentage

Sep-01

Dec-01

Mar-02

Jun-02

Sep-02

Dec-02

Mar-03

Jun-03

Sep-03

Dec-03

Mar-04

Jun-04

Sep-04

Dec-04

57% 56%45% 43% 36%

43% 44%55% 57% 64%

Offshore-onsite revenues mix FY 2000-2005E Offshore

Onsite

� The mix seems to be changing in favor of offshore due to the substantial increase of BPO services, which are predominantly delivered offshore

� Excluding offshore BPO revenues, the offshore proportion stands at about 50% for FY04

99-00 00-01 01-02 02-03 03-04

1 Infosys, Wipro, SatyamSource: Smith Barney, NASSCOM

7071

73

7778

7677

7877 76

7476

73 72

Proprietary & Confidential. © 2005 Everest Partners, L.P.17

Offshore location optimization is determined by two key

factors: the savings potential offered by the location, and

the maturity of the location for the given process

Framework for analysis of location optimization

Savings potential determined by comparing fully-loaded direct cost of destination with that of the source location� Direct salary cost� Management and administration costs

� Real estate cost� Telecom cost� Equipment cost� Cost impact of attrition

Savings potential

Location maturity

� Cultural compatibility� Government support� Infrastructure quality and availability

� Labor availability� Risks� Market activity

Limited savings opportunity –may be near-shore options

Optimal destinations

Not ready for offshoring

Could evolve as attractive locations

ILLUSTRATIVE

Source: Everest Research Institute

Relative importance of each dimension can be subjective. Further, overall scores can vary with buyer’s risk profiles

Excludes supplier margins, sales and marketing expenses, and centralized corporate overhead

Proprietary & Confidential. © 2005 Everest Partners, L.P.18

Toronto

Shanghai

Mumbai

Prague

PuneManila

Dalian

Budapest

Bangalore

Country/region comparisons offer some high-level

perspective, but within a region, savings potential and

maturity can vary significantly by city

ILLUSTRATIVE

KL

Potential savings per FTE p.a. (%)

Location maturityLow

Low

High

High

Location optimization for transactional F&A workIndian cities

Chinese cities

East European cities

Other cities

1 Excluding Manila and ShanghaiSource: Everest Research Institute

Proprietary & Confidential. © 2005 Everest Partners, L.P.19

Of the various offshore risk dimensions, operational

risks are the most frequent cause of offshore problems

1 Based on a sample of 28 deals, identified through secondary sources, in which the buyer had problems with offshoring2 The above categories do not add up to 100% since multiple sources of risk may have caused a problem/failure

Source: Everest Analysis, June 2005

Quality

Process control

Buyer adaptability

to offshoring

Transition and

knowledge transfer

Infrastructure

Source of operational risk1

Percentage (%)

50

36

21

21

14

Operational risk

Organizational risk

Legal risk

Financial risk

Strategic risk

Dimension of risk causing problem/failure1

Percentage (%)

61

50

25

21

14

Proprietary & Confidential. © 2005 Everest Partners, L.P.20

Examining various offshoring cases illustrates the kind

of operational problems encountered

Initial Q&A bottleneck due to limited US-based resources available to audit offshore work

Limited face time at the beginning of the process resulted in avoidable mistakes

Supplier’s internal audit detected employee misconduct while making outbound sales calls

Corporate clients’ call center in India discontinued due to customer complaints about quality of problem resolution and “thick accent”

Transition and knowledge transfer

Barry Wehmiller

Quality Dell

Buyer adaptability to offshoring

Radio Shack

Process control Capital One

Long lead times for acquiring the hardware in offshore location delayed development work for several months, leading to higher costs

Transition and knowledge transfer

DHL

Source: Everest Research Institute

Risk Buyer Problem(s) encountered

Proprietary & Confidential. © 2005 Everest Partners, L.P.21

Robust risk mitigation practices address and can

overcome offshoring risks

1 Based on a sample of 28 deals, identified through secondary sources, where the buyer had problems with offshoringSource: Everest Analysis, June 2005

Quality

Process control

Buyer adaptability

to offshoring

Transition and

knowledge transfer

Infrastructure

� Adequate training of offshore resources� Strong transition management, including knowledge transfer and documentation of processes

� Audit quality and security processes� Station some buyer resources offshore

� Employ job shadowing� Retain critical buyer resources through the transition period� Use pilots to identify bottlenecks in transitioning

� Upgrade maturity of buyer processes such as generation of specifications, etc.

� Clear communication with buyer’s employees

� Dedicated infrastructure� Redundant systems for critical infrastructure such as satellite links

ILLUSTRATIVEOperational Risk High-level mitigation mechanisms

Proprietary & Confidential. © 2005 Everest Partners, L.P.22

Get the answers today that lead to tomorrow’s

success

Everest Research Institute has the resources, experience, and capabilities to provide companies with the strategic intelligence, analysis, and insight that are crucial to making the right decisions in today’s outsourcing marketplace.

With the vision of our leadership team, the personal commitment, and indeed, the passion of our professionals to deliver real value to our clients, our organization is unsurpassed in its ability to guide your company’s future success.

Everest Research InstituteTwo Galleria Tower13455 Noel Road, Suite 2100Dallas, TX 75240+1-214-451-3000www.everestresearchinstitute.cominfo@everestresearchinstitute.com

Everest AustralasiaLevel 6, 90 Mount StreetNorth Sydney, NSW 2060Australia+61-3-9833-1018

Everest India Ground Floor, Tower AUnitech Business ParkSouth City - I, GurgaonNew Delhi National Capital Region India 122001+91-124-304-1000

Everest UKGainsborough House100 Pall MallSt. James's London, SW1Y 5HP+44-20-7664-8920

Everest Group150 E., 52nd Street, 16th FloorNew York, NY 10022+1-646-805-4000

Everest Canada5915 Airport Rd #400 Mississauga, ON L4V1T1Canada+1-905-405-5640