global research and consulting econometric advisors cbre econometric advisors client conference 2012...

TRANSCRIPT

Global Research and ConsultingEconometric Advisors

CBRE Econometric Advisors

Client Conference 2012 October 2, 2012

Global Research and ConsultingEconometric Advisors

CBRE Econometric Advisors Client Conference 2012

October 2, 2012 Seaport Hotel, Boston, MA

How Can The U.S. Grow?

Session 1 | U.S. Economic Outlook

Presented by:Jon Southard, Managing Director, Director of ForecastingWilliam Wheaton, Senior Consultant

CBRE | Page 2Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

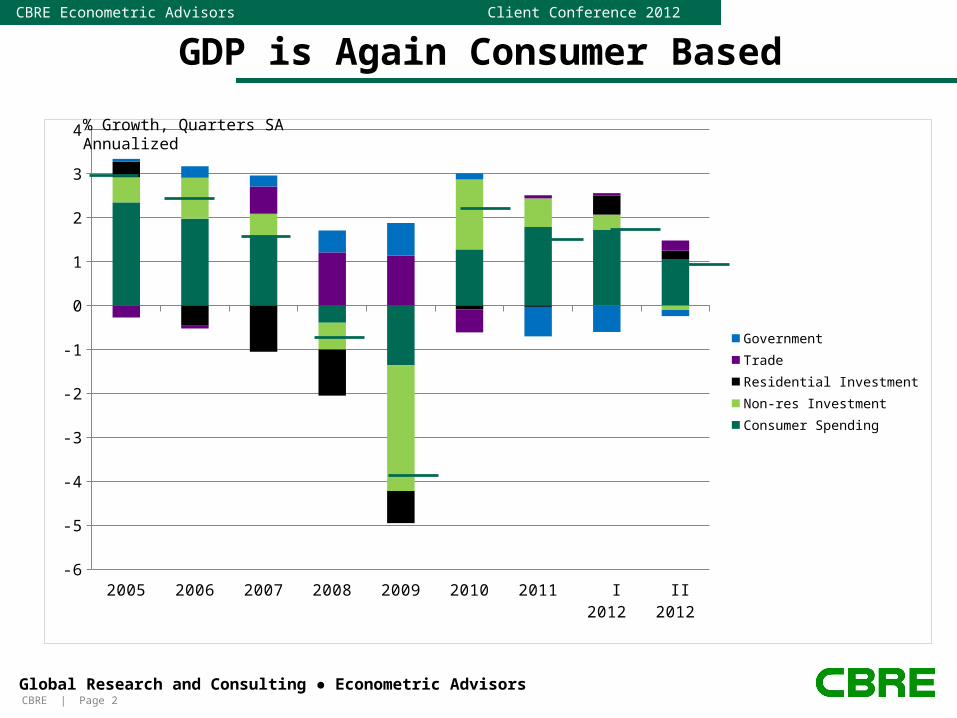

GDP is Again Consumer Based

2005 2006 2007 2008 2009 2010 2011 I 2012 II 2012-6

-5

-4

-3

-2

-1

0

1

2

3

4

Government

Trade

Residential Investment

Non-res Investment

Consumer Spending

% Growth, Quarters SA Annualized

CBRE | Page 3Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

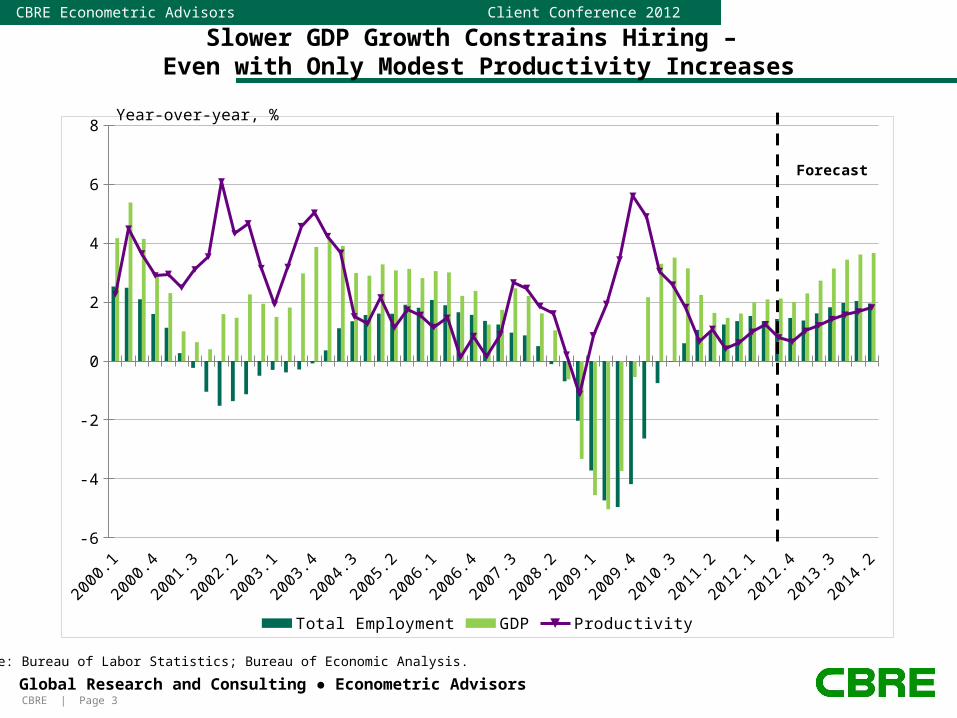

Slower GDP Growth Constrains Hiring – Even with Only Modest Productivity Increases

2000

.1

2000

.3

2001

.1

2001

.3

2002

.1

2002

.3

2003

.1

2003

.3

2004

.1

2004

.3

2005

.1

2005

.3

2006

.1

2006

.3

2007

.1

2007

.3

2008

.1

2008

.3

2009

.1

2009

.3

2010

.1

2010

.3

2011

.1

2011

.3

2012

.1

2012

.3

2013

.1

2013

.3

2014

.1-6

-4

-2

0

2

4

6

8

Total Employment GDP Productivity

Forecast

Source: Bureau of Labor Statistics; Bureau of Economic Analysis.

Year-over-year, %

CBRE | Page 4Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

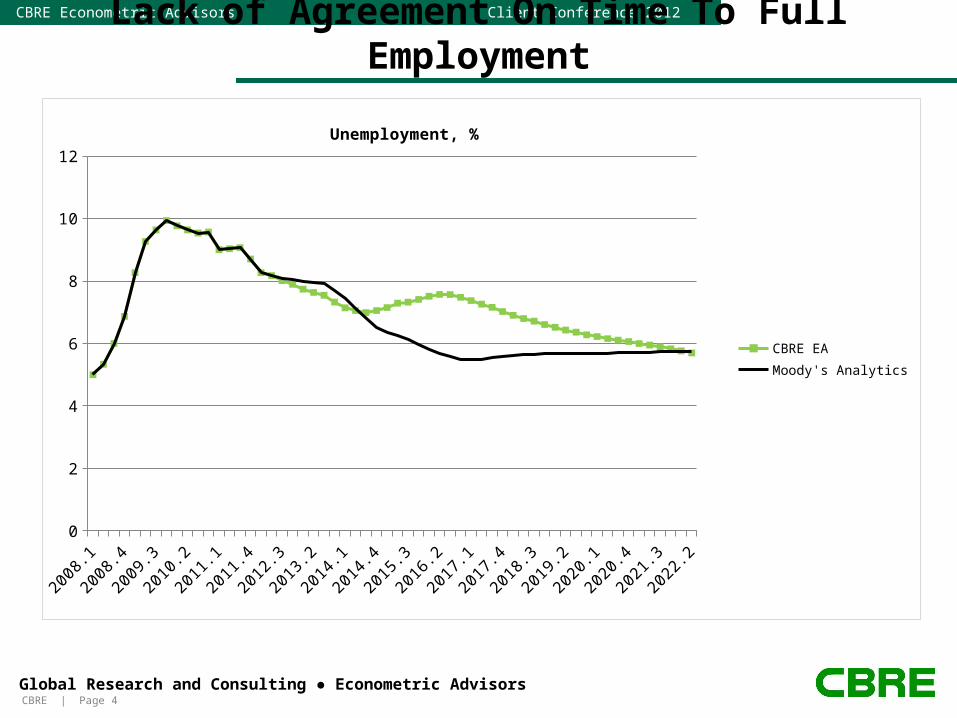

Lack of Agreement On Time To Full Employment

2008

.1

2008

.4

2009

.3

2010

.2

2011

.1

2011

.4

2012

.3

2013

.2

2014

.1

2014

.4

2015

.3

2016

.2

2017

.1

2017

.4

2018

.3

2019

.2

2020

.1

2020

.4

2021

.3

2022

.20

2

4

6

8

10

12

Unemployment, %

CBRE EA

Moody's Analytics

CBRE | Page 5Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

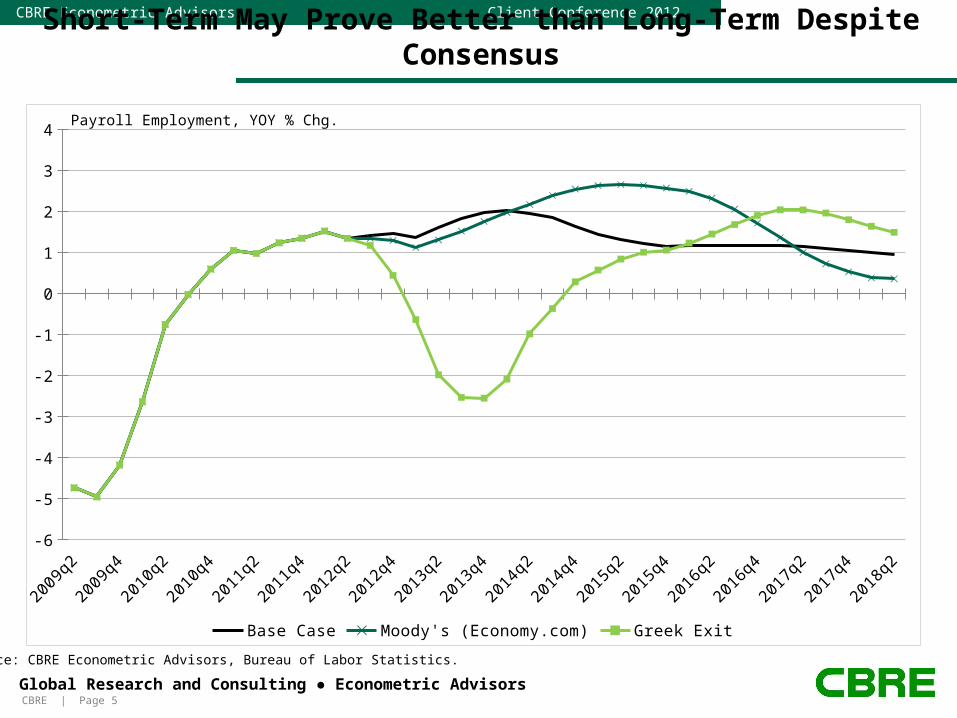

Short-Term May Prove Better than Long-Term Despite Consensus

2009

q2

2009

q4

2010

q2

2010

q4

2011

q2

2011

q4

2012

q2

2012

q4

2013

q2

2013

q4

2014

q2

2014

q4

2015

q2

2015

q4

2016

q2

2016

q4

2017

q2

2017

q4

2018

q2-6

-5

-4

-3

-2

-1

0

1

2

3

4

Base Case Moody's (Economy.com) Greek Exit

Payroll Employment, YOY % Chg.

Source: CBRE Econometric Advisors, Bureau of Labor Statistics.

CBRE | Page 6Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

Questions to be Answered:

Where will productivity go in the short term?

What are the mid-term term prospects for return to full employment?

What GDP sectors can contribute to future growth: consumption, housing, trade,..?

Are there different longer-term headwinds this cycle compared to the recent past? What are they and how strong?

CBRE | Page 7Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

Short Term (Keynesian) Sources of Growth

1). Consuming (rather than saving) gives a short run boost to economic growth. A housing recovery will provide another boost, but these can only go so far.

2). A trade surplus gives a boost to economic growth, but sustained surpluses invite exchange rate adjustments which bring trade back into balance.

3). Reductions in “structural unemployment” through better labor market operation. Is there “mismatch”?

4). Government deficits (borrowing from the future with the issuance of debt) will increase current consumption, but it is not sustainable. Deficit reductions induce temporary contractions.

LETS DEAL WITH KEYNESIAN ISSUES FIRST AND THEN TACKLE SOME LONGER-TERM QUESTIONS

CBRE | Page 8Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

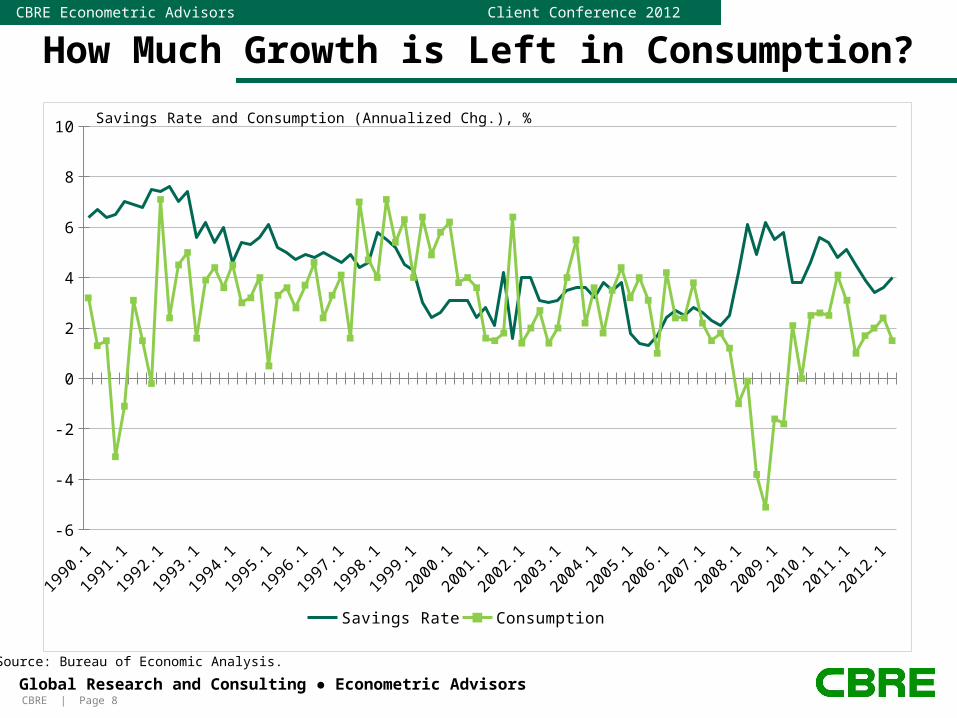

How Much Growth is Left in Consumption?

1990

.1

1990

.4

1991

.3

1992

.2

1993

.1

1993

.4

1994

.3

1995

.2

1996

.1

1996

.4

1997

.3

1998

.2

1999

.1

1999

.4

2000

.3

2001

.2

2002

.1

2002

.4

2003

.3

2004

.2

2005

.1

2005

.4

2006

.3

2007

.2

2008

.1

2008

.4

2009

.3

2010

.2

2011

.1

2011

.4-6

-4

-2

0

2

4

6

8

10

Savings Rate Consumption

Savings Rate and Consumption (Annualized Chg.), %

Source: Bureau of Economic Analysis.

CBRE | Page 9Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

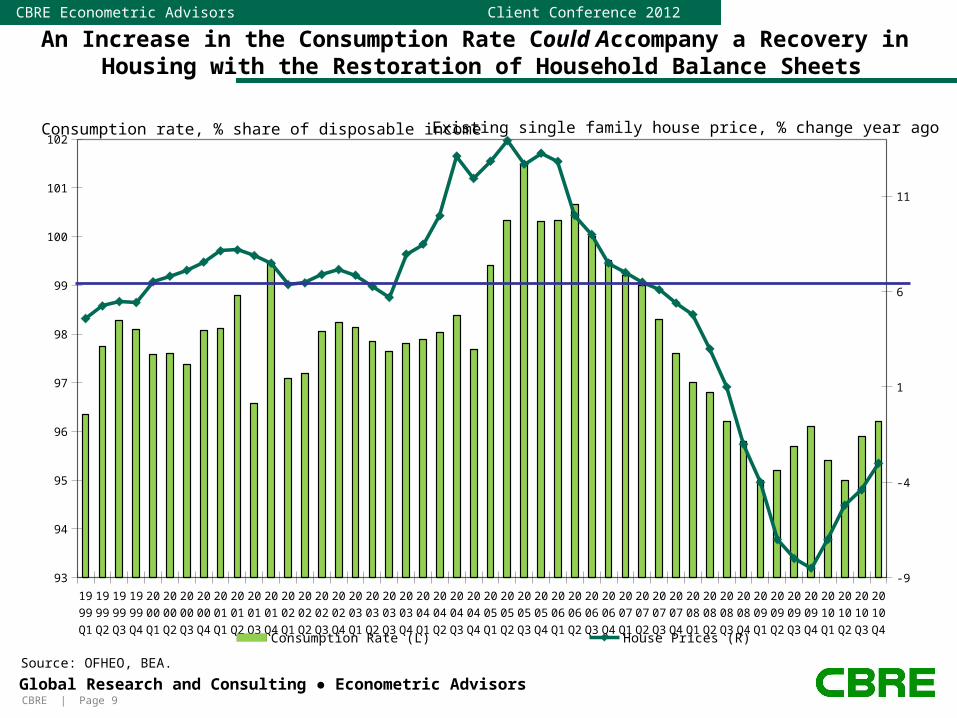

An Increase in the Consumption Rate Could Accompany a Recovery in Housing with the Restoration of Household Balance Sheets

1999Q1

1999Q2

1999Q3

1999Q4

2000Q1

2000Q2

2000Q3

2000Q4

2001Q1

2001Q2

2001Q3

2001Q4

2002Q1

2002Q2

2002Q3

2002Q4

2003Q1

2003Q2

2003Q3

2003Q4

2004Q1

2004Q2

2004Q3

2004Q4

2005Q1

2005Q2

2005Q3

2005Q4

2006Q1

2006Q2

2006Q3

2006Q4

2007Q1

2007Q2

2007Q3

2007Q4

2008Q1

2008Q2

2008Q3

2008Q4

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

93

94

95

96

97

98

99

100

101

102

-9

-4

1

6

11

Consumption Rate (L) House Prices (R)

Source: OFHEO, BEA.

Consumption rate, % share of disposable income Existing single family house price, % change year ago

CBRE | Page 10Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

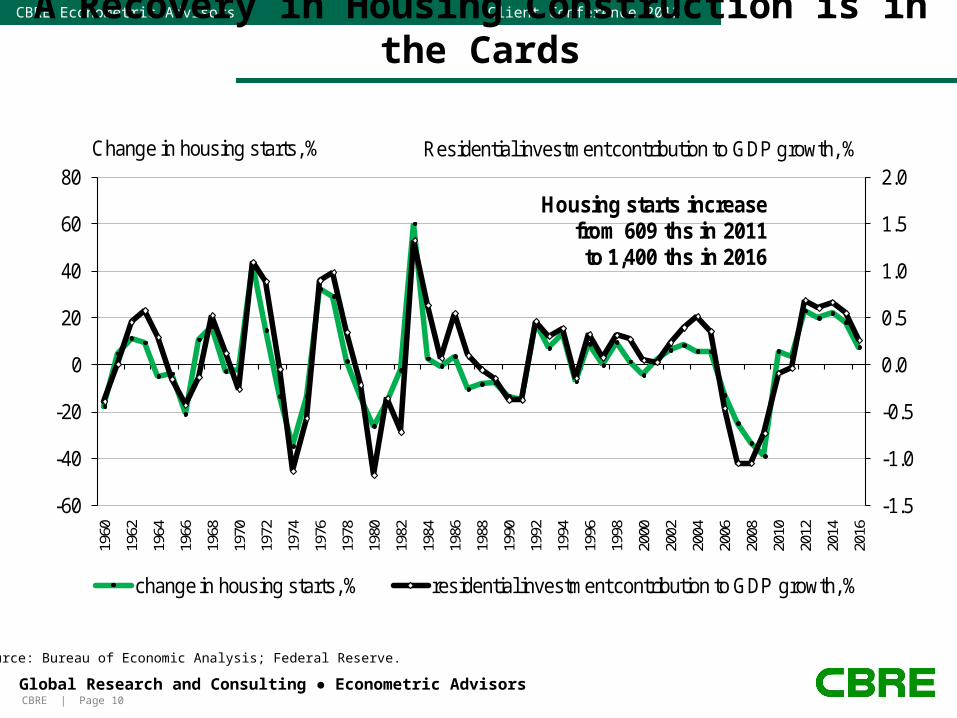

A Recovery in Housing Construction is in the Cards

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-60

-40

-20

0

20

40

60

80

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

change in housing starts, % residential investment contribution to GDP growth, %

Change in housing starts, % Residential investment contribution to GDP growth, %

Housing starts increasefrom 609 ths in 2011to 1,400 ths in 2016

Source: Bureau of Economic Analysis; Federal Reserve.

CBRE | Page 11Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

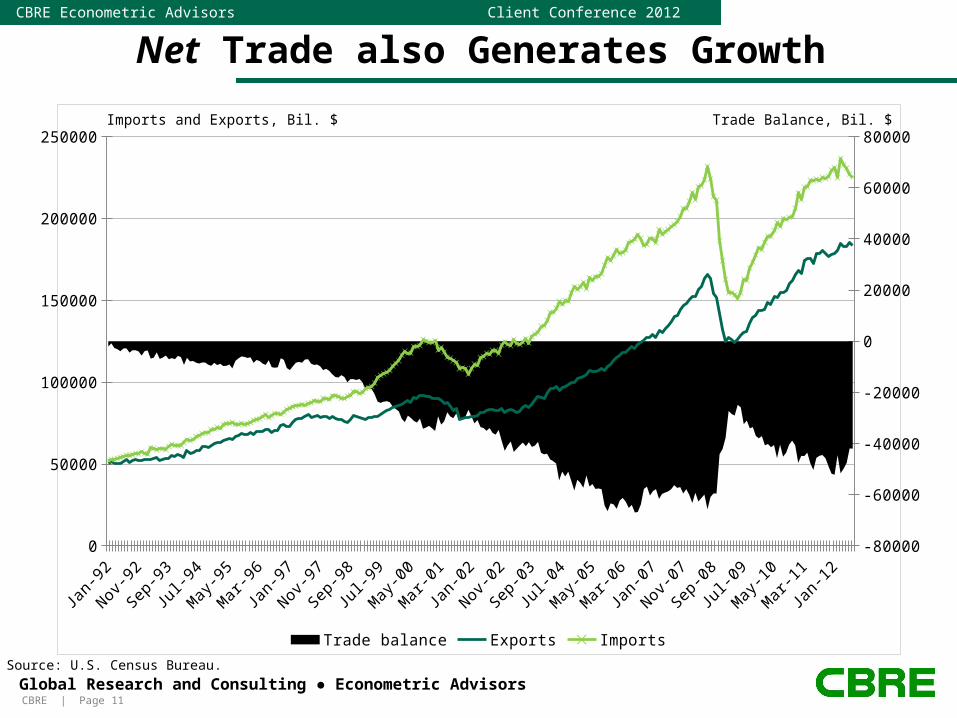

Net Trade also Generates Growth

0

50000

100000

150000

200000

250000

-80000

-60000

-40000

-20000

0

20000

40000

60000

80000

Trade balance Exports Imports

Imports and Exports, Bil. $ Trade Balance, Bil. $

Source: U.S. Census Bureau.

CBRE | Page 12Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

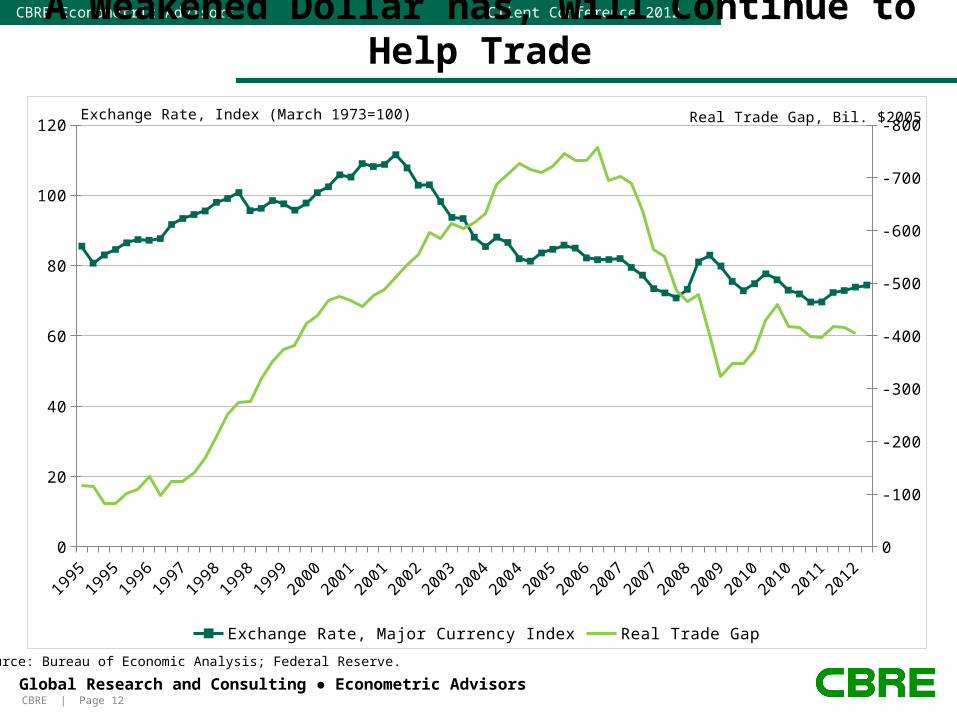

A Weakened Dollar has, will Continue to Help Trade

1995

1995

1996

1996

1997

1997

1998

1999

1999

2000

2000

2001

2002

2002

2003

2003

2004

2004

2005

2006

2006

2007

2007

2008

2009

2009

2010

2010

2011

2011

2012

0

20

40

60

80

100

120 -800

-700

-600

-500

-400

-300

-200

-100

0

Exchange Rate, Major Currency Index Real Trade Gap

Exchange Rate, Index (March 1973=100) Real Trade Gap, Bil. $2005

Source: Bureau of Economic Analysis; Federal Reserve.

CBRE | Page 13Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

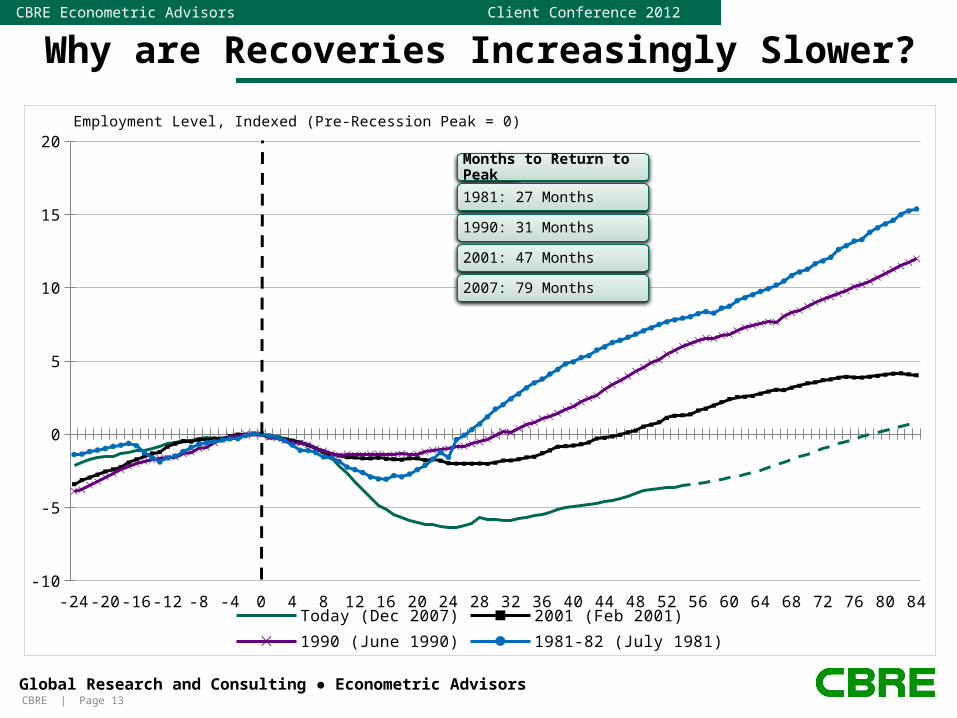

Why are Recoveries Increasingly Slower?

-24-21-18-15-12 -9 -6 -3 0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84-10

-5

0

5

10

15

20

Today (Dec 2007) 2001 (Feb 2001) 1990 (June 1990) 1981-82 (July 1981)

Employment Level, Indexed (Pre-Recession Peak = 0)

Months to Return to Peak

1981: 27 Months

1990: 31 Months

2001: 47 Months

2007: 79 Months

CBRE | Page 14Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

Is this also Caused by a Skill Mismatch, and also a Geographic Mismatch?

Perhaps firms cannot find candidates with suitable skills and unemployed workers have old skills that employers are not interested in. • If true, could explain persistent unemployment despite higher job

vacancy rate• Economies always have some degree of mismatch, but some believe

the extent of this mismatch has grown considerably• Housing market hold back workers from moving

Why we care. Re-training, selective immigration, fixing underwater houses, better labor market IT platforms could all help.

CBRE | Page 15Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

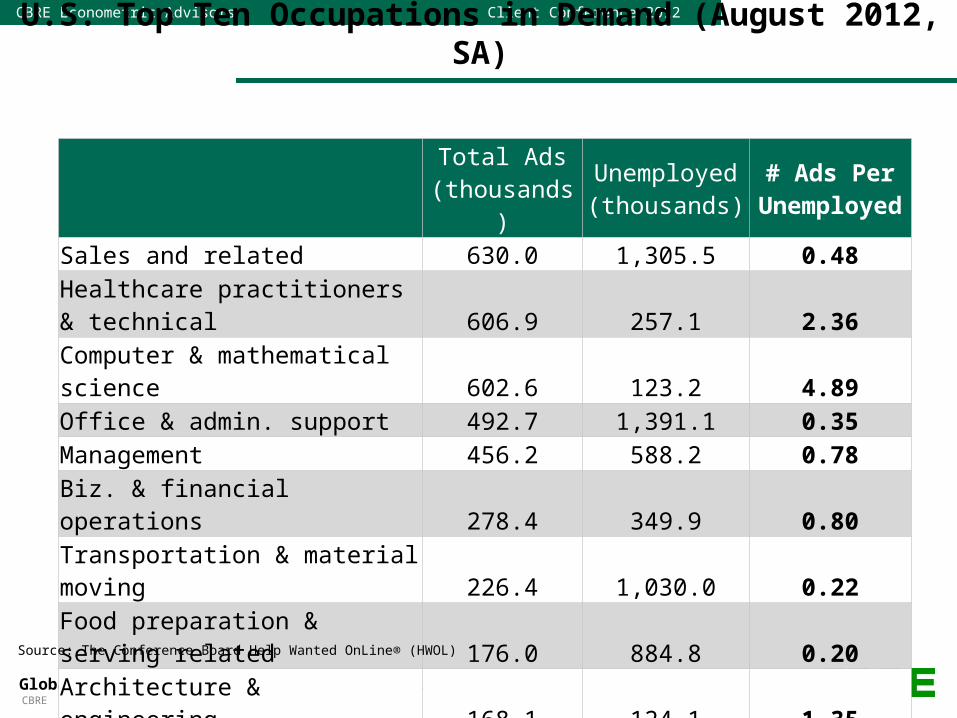

U.S. Top Ten Occupations in Demand (August 2012, SA)

Total Ads (thousands)

Unemployed (thousands)

# Ads Per Unemploye

dSales and related 630.0 1,305.5 0.48Healthcare practitioners & technical 606.9 257.1 2.36Computer & mathematical science 602.6 123.2 4.89Office & admin. support 492.7 1,391.1 0.35Management 456.2 588.2 0.78Biz. & financial operations 278.4 349.9 0.80Transportation & material moving 226.4 1,030.0 0.22Food preparation & serving related 176.0 884.8 0.20Architecture & engineering 168.1 124.1 1.35Installation, maintenance, & repair 162.2 325.4 0.50Source: The Conference Board Help Wanted OnLine® (HWOL)

CBRE | Page 16Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

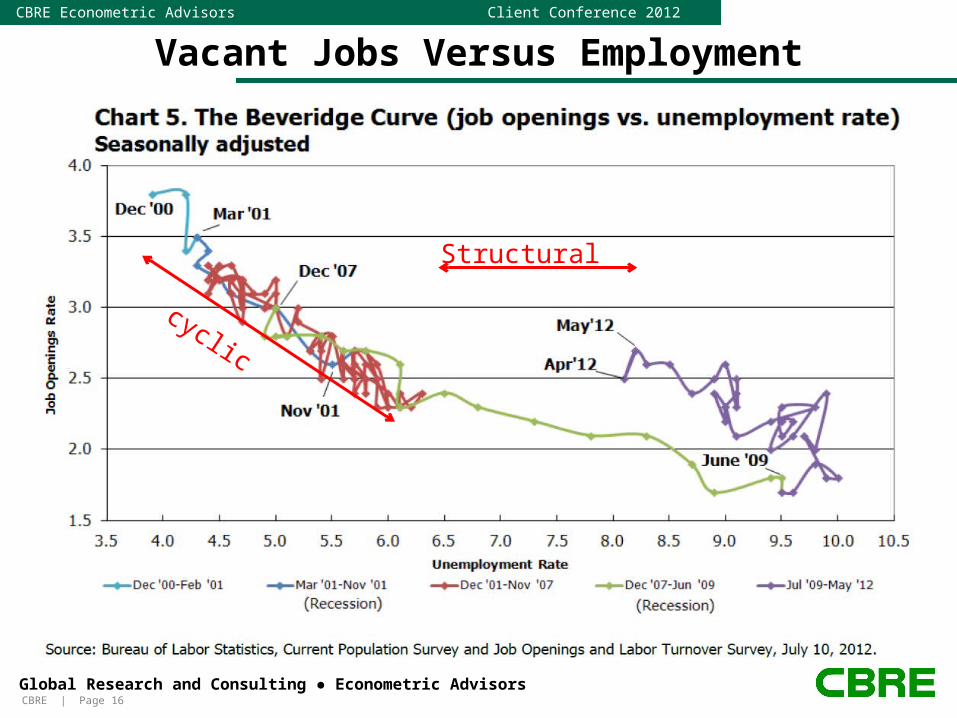

Vacant Jobs Versus Employment

Structural

cyclic

CBRE | Page 17Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

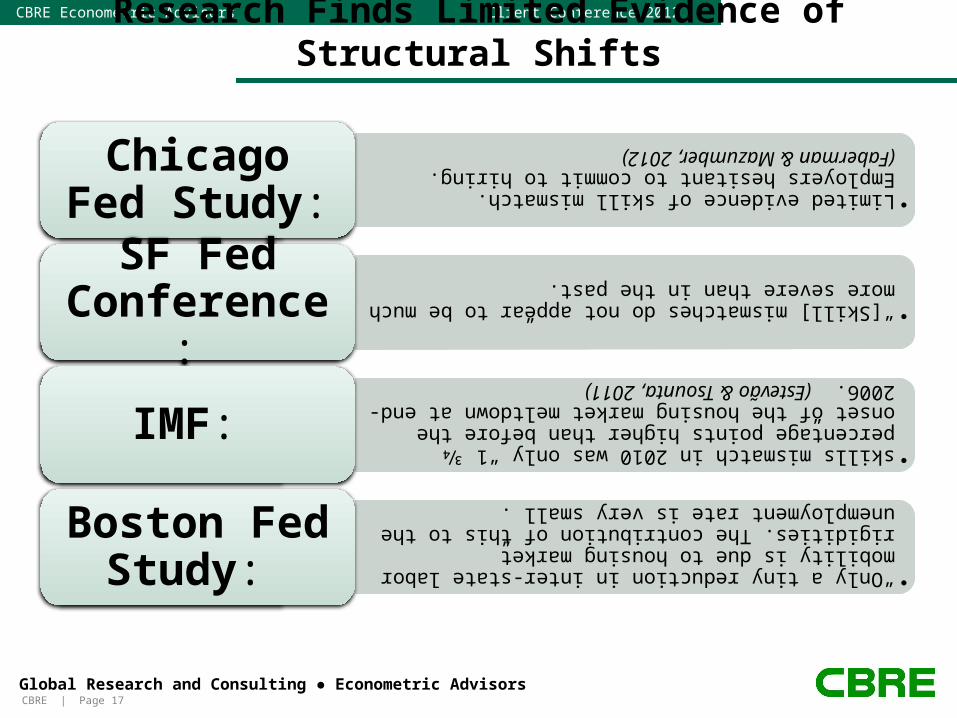

Research Finds Limited Evidence of Structural Shifts

•Limited evidence of skill mismatch. Employers hesitant to commit to hiring. (Faberman & Mazumber, 2012)

Chicago Fed Study:

•“[Skill] mismatches do not appear to be much more severe than in the past.”

SF Fed Conference:

•skills mismatch in 2010 was only “1 3⁄4 percentage points higher than before the onset of the housing market meltdown at end-2006.” (Estevão & Tsounta, 2011)

IMF:

•“Only a tiny reduction in inter-state labor mobility is due to housing market rigidities. The contribution of this to the unemployment rate is very small”.

Boston Fed Study:

CBRE | Page 18Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

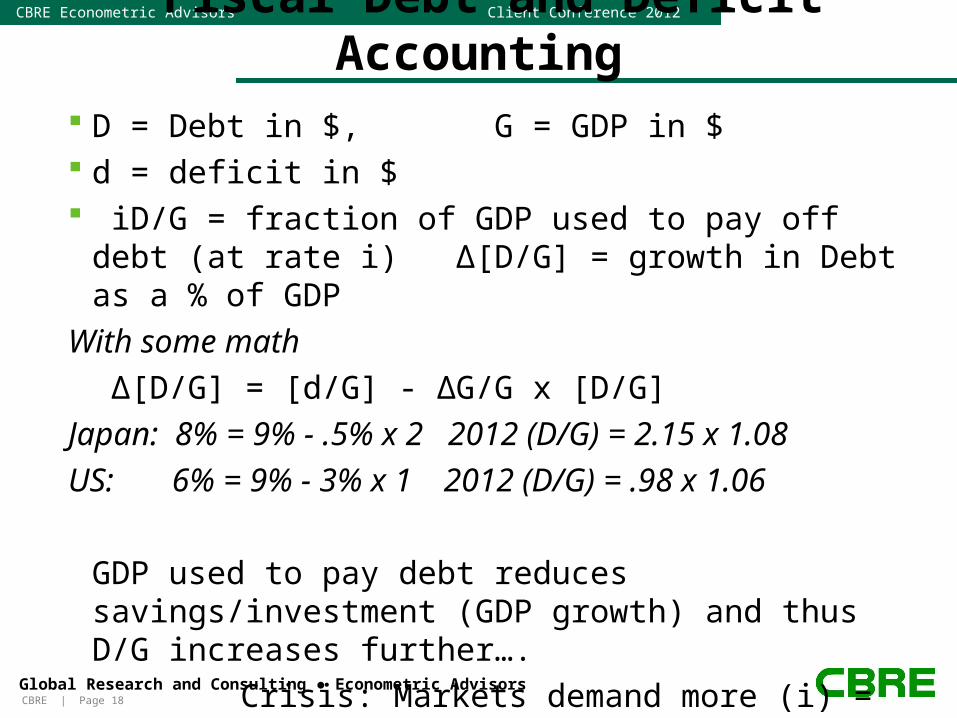

Fiscal Debt and Deficit Accounting D = Debt in $, G = GDP in $ d = deficit in $ iD/G = fraction of GDP used to pay off debt (at rate i)

∆[D/G] = growth in Debt as a % of GDP

With some math

∆[D/G] = [d/G] - ∆G/G x [D/G]

Japan: 8% = 9% - .5% x 2 2012 (D/G) = 2.15 x 1.08

US: 6% = 9% - 3% x 1 2012 (D/G) = .98 x 1.06

GDP used to pay debt reduces savings/investment (GDP growth) and thus D/G increases further….

Crisis: Markets demand more (i) = makes it worse

CBRE | Page 19Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

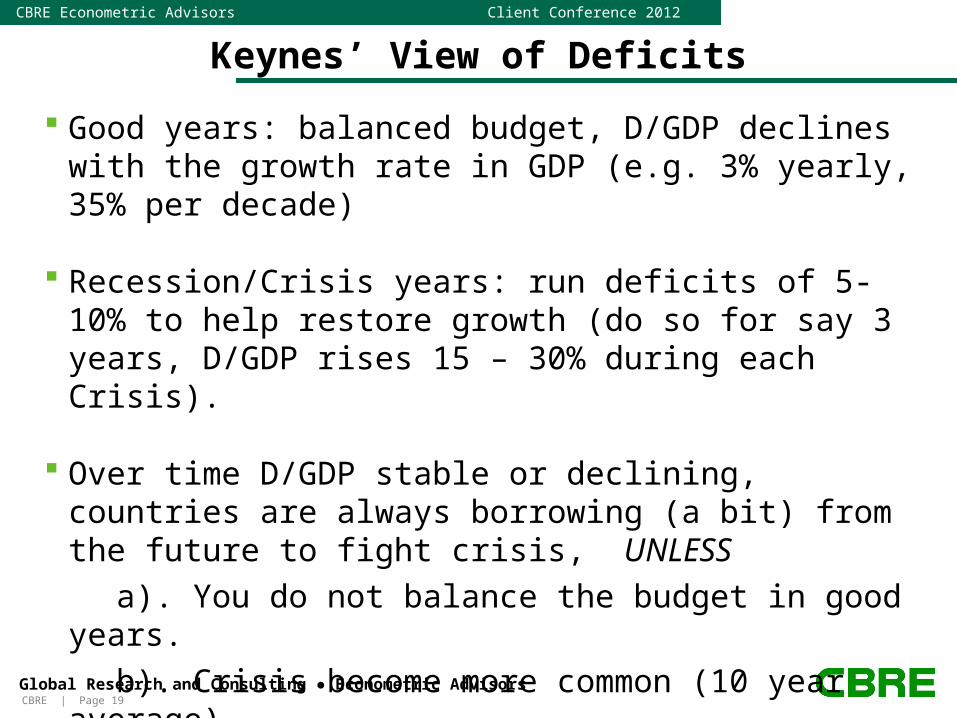

Keynes’ View of Deficits

Good years: balanced budget, D/GDP declines with the growth rate in GDP (e.g. 3% yearly, 35% per decade)

Recession/Crisis years: run deficits of 5-10% to help restore growth (do so for say 3 years, D/GDP rises 15 – 30% during each Crisis).

Over time D/GDP stable or declining, countries are always borrowing (a bit) from the future to fight crisis, UNLESS

a). You do not balance the budget in good years.

b). Crisis become more common (10 year average)

c). GDP grows more slowly.

d). Your initial D/GDP is (too) high (e.g. >1)

CBRE | Page 20Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

The Twin Impacts of Deficit Reductions

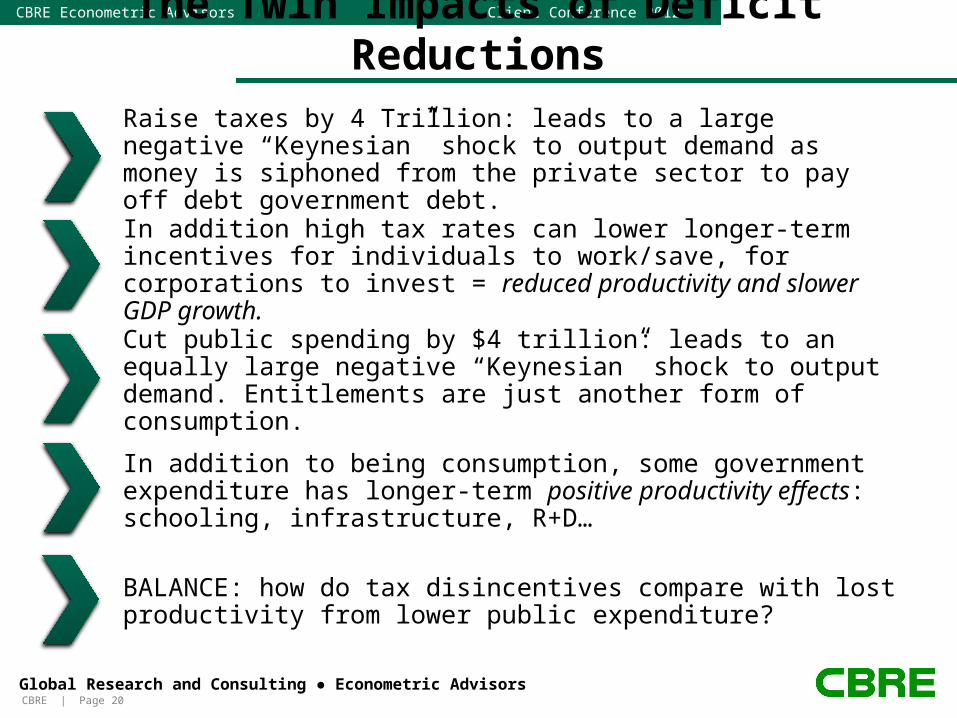

Raise taxes by 4 Trillion: leads to a large negative “Keynesian” shock to output demand as money is siphoned from the private sector to pay off debt government debt.

In addition high tax rates can lower longer-term incentives for individuals to work/save, for corporations to invest = reduced productivity and slower GDP growth.

Cut public spending by $4 trillion: leads to an equally large negative “Keynesian” shock to output demand. Entitlements are just another form of consumption.

In addition to being consumption, some government expenditure has longer-term positive productivity effects: schooling, infrastructure, R+D…

BALANCE: how do tax disincentives compare with lost productivity from lower public expenditure?

CBRE | Page 21Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

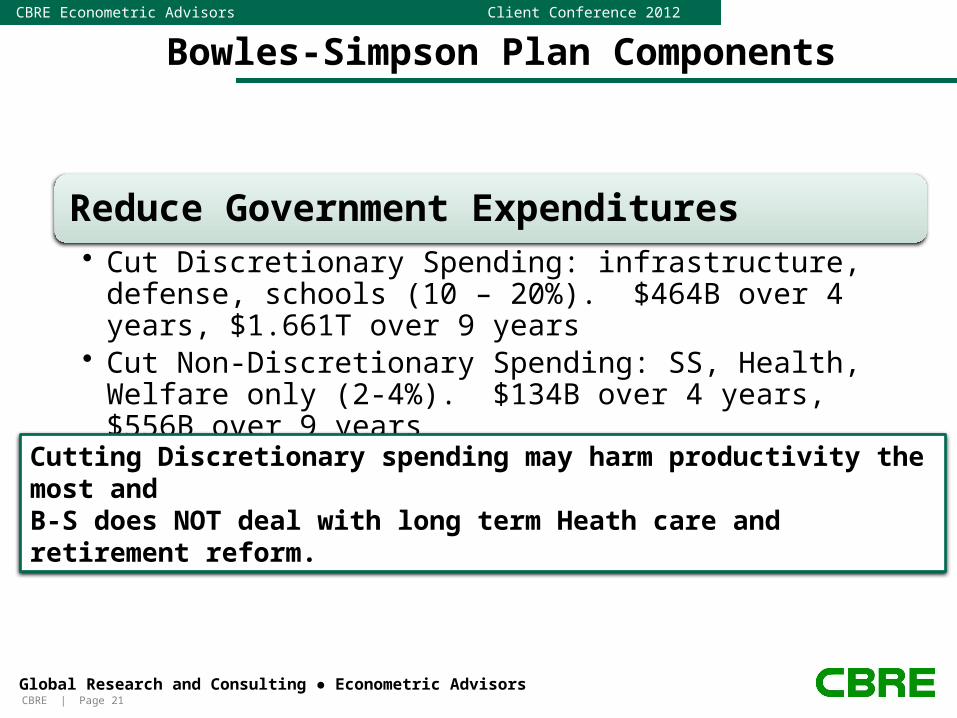

Bowles-Simpson Plan Components

Reduce Government Expenditures• Cut Discretionary Spending: infrastructure, defense, schools

(10 – 20%). $464B over 4 years, $1.661T over 9 years• Cut Non-Discretionary Spending: SS, Health, Welfare only (2-

4%). $134B over 4 years, $556B over 9 years

Cutting Discretionary spending may harm productivity the most and B-S does NOT deal with long term Heath care and retirement reform.

CBRE | Page 22Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

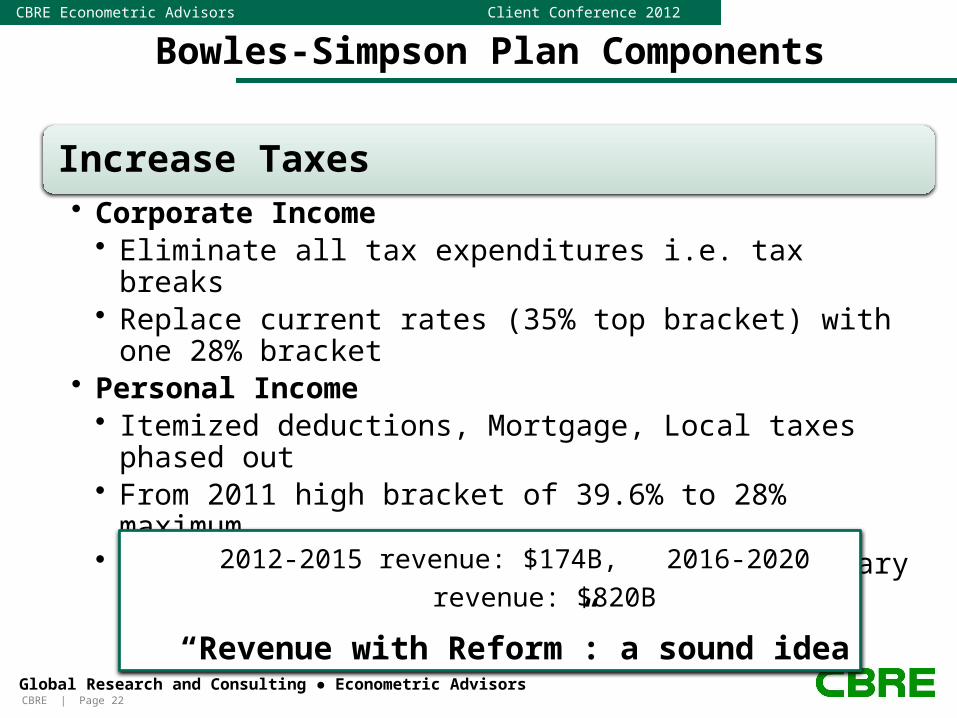

Bowles-Simpson Plan Components

Increase Taxes• Corporate Income

• Eliminate all tax expenditures i.e. tax breaks• Replace current rates (35% top bracket) with one 28%

bracket• Personal Income

• Itemized deductions, Mortgage, Local taxes phased out • From 2011 high bracket of 39.6% to 28% maximum• Capital gains and dividends taxed at ordinary income rates

2012-2015 revenue: $174B, 2016-2020 revenue:

$820B

“Revenue with Reform”: a sound idea

CBRE | Page 23Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

How Economies Grow in the Longer Term

Population growth increases GDP, but not GDP per capita which is real prosperity.

Workers generate GDP, retirees receive some form of transfer from them. • More workers less retirees = higher GDP per capita. • More retirees and less workers = lower GDP per capita. • Demographic dividend from a young population and Demographic

penalty from an older population eventually evens, but only in the long run.

• Hence Aging is a big drag and will reduce economic growth (next session)

CBRE | Page 24Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

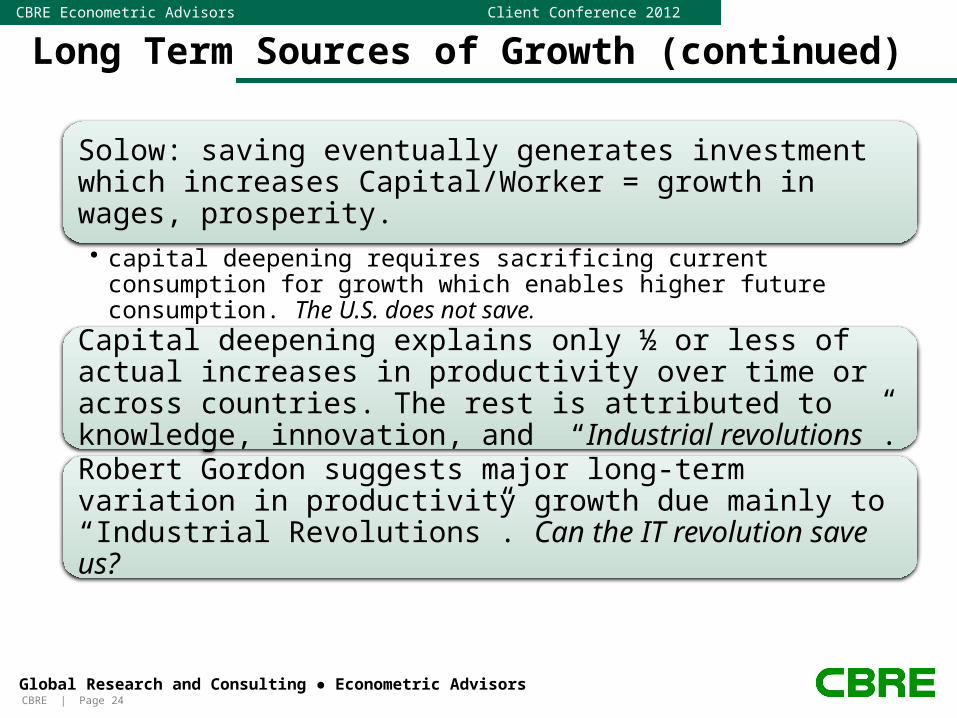

Long Term Sources of Growth (continued)

Solow: saving eventually generates investment which increases Capital/Worker = growth in wages, prosperity.

• capital deepening requires sacrificing current consumption for growth which enables higher future consumption. The U.S. does not save.

Capital deepening explains only ½ or less of actual increases in productivity over time or across countries. The rest is attributed to knowledge, innovation, and “Industrial revolutions”.

Robert Gordon suggests major long-term variation in productivity growth due mainly to “Industrial Revolutions”. Can the IT revolution save us?

CBRE | Page 25Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

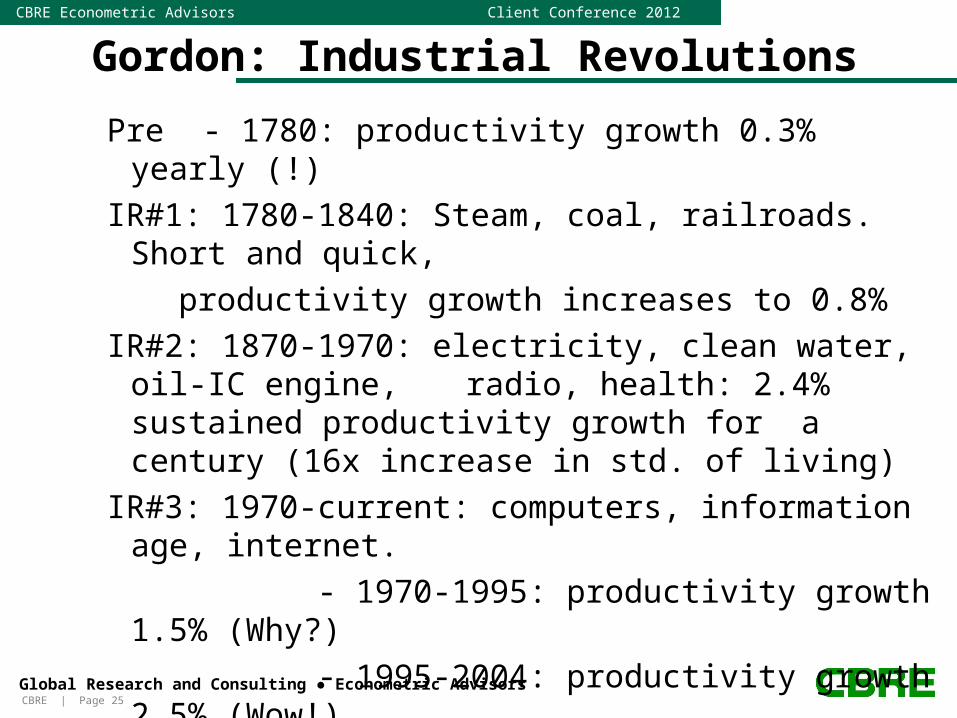

Gordon: Industrial Revolutions

Pre - 1780: productivity growth 0.3% yearly (!)

IR#1: 1780-1840: Steam, coal, railroads. Short and quick,

productivity growth increases to 0.8%

IR#2: 1870-1970: electricity, clean water, oil-IC engine, radio, health: 2.4% sustained productivity growth for a century (16x increase in std. of living)

IR#3: 1970-current: computers, information age, internet.

- 1970-1995: productivity growth 1.5% (Why?)

- 1995-2004: productivity growth 2.5% (Wow!)

- 2005-2012: productivity growth 1.3% (Ugh)

- 2013-2020: ?

CBRE | Page 26Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

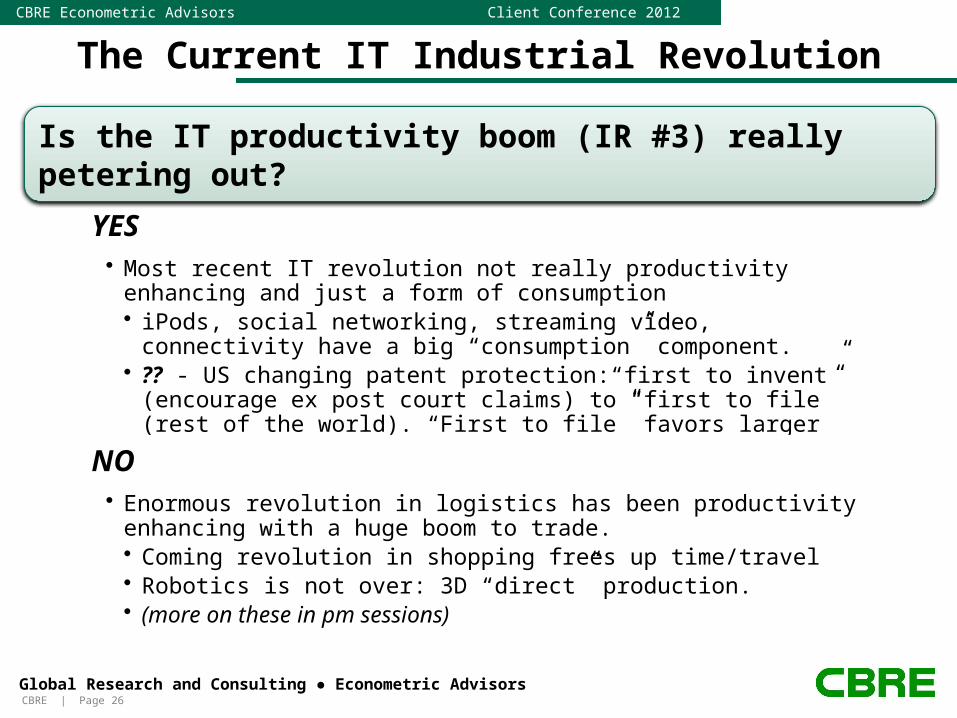

The Current IT Industrial Revolution

YES• Most recent IT revolution not really productivity enhancing and just a form

of consumption • iPods, social networking, streaming video, connectivity have a big

“consumption” component. • ?? - US changing patent protection:“first to invent” (encourage ex post

court claims) to “first to file” (rest of the world). “First to file” favors larger corporations, big patents

NO• Enormous revolution in logistics has been productivity enhancing with a

huge boom to trade.• Coming revolution in shopping frees up time/travel• Robotics is not over: 3D “direct” production.• (more on these in pm sessions)

Is the IT productivity boom (IR #3) really petering out?

CBRE | Page 27Global Research and Consulting ● Econometric Advisors

CBRE Econometric Advisors Client Conference 2012

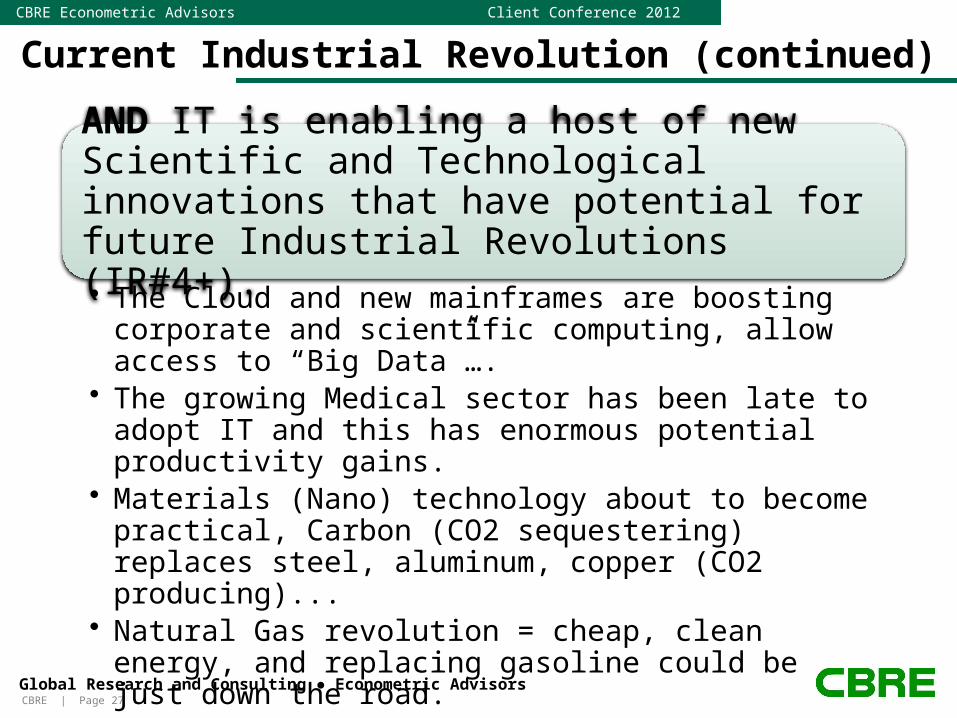

Current Industrial Revolution (continued)

AND IT is enabling a host of new Scientific and Technological innovations that have potential for future Industrial Revolutions (IR#4+). • The Cloud and new mainframes are boosting corporate

and scientific computing, allow access to “Big Data”…. • The growing Medical sector has been late to adopt IT and

this has enormous potential productivity gains. • Materials (Nano) technology about to become practical,

Carbon (CO2 sequestering) replaces steel, aluminum, copper (CO2 producing)...

• Natural Gas revolution = cheap, clean energy, and replacing gasoline could be just down the road.

• OUR BEST HOPE FOR GROWTH