global oil gas - wolfe research · global oil & gas collapse of the ... source: bloomberg...

TRANSCRIPT

Paul SankeyManaging Director, Global Oil & Gas646‐582‐[email protected]

David T. Clark, CFA646‐582‐[email protected]

Silvio Micheloto, CFA646‐582‐[email protected]

Vin Lovaglio646‐582‐[email protected]

Bob Parija, CFA646‐582‐[email protected]

Global Oil & GasCollapse of the Saudi Put, Rise of the

Eagle Ford CallJanuary 12, 2015

This report is limited solely for the use of clients of Wolfe Research. Please refer to the DISCLOSURE SECTION located at the end of this report for Analyst Certifications and Other Disclosures. For Important Disclosures, please go to www.WolfeResrearch.com/Disclosures or write to us at Wolfe Research LLC, 420 Lexington Avenue, Suite 648, New York, NY 10170. 1

2

New Forecasts and How The Market Has Changed

Note: “Big Four” basins included in this chart are Bakken, Eagle Ford, Permian and Niobrara/DJ BasinSource: EIA, IEA, Company reports, Wolfe Research estimates

40

50

60

70

80

90

100

110

3Q14

E

4Q14

E

Spot

1Q15

E

2Q15

E

3Q15

E

4Q15

E

1Q16

E

2Q16

E

3Q16

E

4Q16

E

1Q17

E

2Q17

E

3Q17

E

4Q17

E

Consensus WTI

WR WTI

Strip WTI

40

50

60

70

80

90

100

110

3Q14

E4Q

14E

Spot

1Q15

E2Q

15E

3Q15

E4Q

15E

1Q16

E2Q

16E

3Q16

E4Q

16E

1Q17

E2Q

17E

3Q17

E4Q

17E

Consensus Brent

WR Brent

Strip Brent

0

20

40

60

80

100

120

Feb‐08 Jul‐09 Nov‐10 Apr‐12 Aug‐13 Dec‐14 May‐16 Sep‐17 Feb‐19

2008 2009 2010 2011 2012 2013 2014

$74 for YE17delivery

$66 front month

Current futures strip

2008 futures strip

30

40

50

60

70

80

90

100

110

120

Feb‐08 Jul‐09 Nov‐10 Apr‐12 Aug‐13 Dec‐14 May‐16 Sep‐17 Feb‐19

$/bb

l

2009 2010 2011 2012 2013 2014 2015

$72/bbl for 2018 delivery

$22 contango overthree year curve ‐ and

first contango post 2010$50/bbl spot

Contango steeper in 2008/9

BRENT WTI

Get ready for really bad earningsThat get worse in 2015

3Source: Bloomberg Finance LP, Wolfe Research estimates

Technology change destroys cartelsAssuming market is now set not by call on OPEC by “Call on Big Four US” Marginal cost of US supply is long term price setter; economics not politics

Cut 2015 from $75 to $56/BrentCut long term oil price from $90 to $80/Brent

4

Energy capex in the S&P 500

Source: Wolfe Research Portfolio Strategy, Standard & Poor’s, Compustat, Factset

4%

4%

7%

7%

9%

10%

11%

12%

33%

0% 5% 10% 15% 20% 25% 30% 35%

Healthcare

Materials

Telecom

Staples

Tech

Industrials

Cons Disc

Utilities

Energy

Sector Contributions to Overall S&P 500 Capex

5

Demand growth & global oil pricesLong‐term OECD & Non‐OECD oil demand growth

Source: IEA, BP,. Wolfe Research

Oil broke $50/bbl (real 2013 US$ in 1986 and did not rise above that until 2005

But unlike 1986 larger total market today faces more rapid decline rates in marginal growth –market should adjust much faster

0

10

20

30

40

50

60

70

80

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000 55,000 60,000 65,000 70,000 75,000 80,000 85,000 90,000 95,000

Oil

pric

e $/

bbl

Global Liquids Production Kbd

SAUDI & OPEC NGLs IRAQ

KUWAITUAE

QATARProc Gains Biofuels VE

NEZUELA

LIBY

A/OMAN

/EGYP

T

IRAN

US DW GULF OF MEX

ICO

MAL

AYSIA

INDONESIA

ASIA

PAC

NIGER

IA

CASPIAN

NORT

HAM

ERICAN

CONVE

NTIONAL

MEX

ICO

RUSSIA

CHINA ONSH

ORE

/SHA

LLOW

CANAD

IAN OIL SAN

DS IN

SITU

COLO

MBIA/

ARGEN

TINA/

ECUAD

OR

NORT

HSEA

ANGOLA

OFFSH

ORE

OTH

ERAF

RICA

/MIDDL

E EA

ST

BRAZ

ILCA

NAD

IANOIL SAN

DS MINING

NORT

HAM

ERICAN

UNCO

NVE

NTIONAL

CORE

NORT

HAM

ERICAN

UNCO

NVE

NTIONAL

2nd

TIER PLAY

SNORT

HAM

ERICAN

UNCO

NVE

NTIONAL

MAR

GINAL

The sustainable level for global oil prices in the medium-term should be set by the short-cycle cash cost of supply of existing production. For long-cycle projects, that is cash opex and ongoing sustaining

capex per barrel. For short-cycle unconventional, it is the cost of drilling an incremental well (i.e., not the

full-cycle cost including allocation of infrastructure/SG&A, etc.). Given the time lag in

reducing production (several months or quarters), short -term support is inherently uncertain.

We calculate the WTI price breakeven for a zero percent return for the marginal producers/areas of the

key unconventional basins to be about $70/bbl.

In 2008 oil fell to the level of cash costs in the Canadian oil sands ($35-40/bbl).

The growth of US uonventional has moved the cost of the marginal barrel higher, but in the short term, given the amount of supply imbalance, oil sands

may still be the floor.

6

Medium‐term global oil cost curveButterfly market, next psychological anchor is probably Oil Sands

mining/upgrading at $35‐40/bbl

Source: IEA, EIA, Wood Mackenzie, Company reports, Bloomberg Finance LP, Wolfe Research

7

Long term global oil cost curveDebatable where Saudi/OPEC fit, need around 100Mbd of development

Source: IEA, EIA, Wood Mackenzie, Company reports, Bloomberg Finance LP, Wolfe Research

0

20

40

60

80

100

120

140

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160 170 180 190 200 210 220 230 240 250 260 270 280 290 300 310 320

Oil

pric

e $/

bbl

Potential Oil Reserves Development

SAUDI

IRAQ

KUWAITUAE

QATAR

Proc Gains Biofuels

VENEZUELA

IRAN

US DW GULF OF MEX

ICO

Liby

a

MEX

ICO

RUSSIA

CHINA ONSH

ORE

/SHAL

LOW

CANAD

IAN OIL SAN

DS IN

SITU

Latin

American

Non

Ven

ezue

la

NORT

HSEA

ANGOLA

OFFSH

ORE

North American

Conven

tiona

l/EO

R

North

American

Uncon

v 2n

d Tier

CANAD

IANOIL SAN

DS MINING

US core unconventional sits very low in the long term development cost curve

Whereas OPEC is increasingly uninvestable at almost any price

NIGER

IA

US Big 4Unconven.

Afric

a conven

tiona

l

Asia BR

AZIL

US margina

l Uncon

ventioan

l

Nigeria

CASPIAN

0

20

40

60

80

100

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

New Development Barrels Base

100 bn barrels of required development for next decade

8

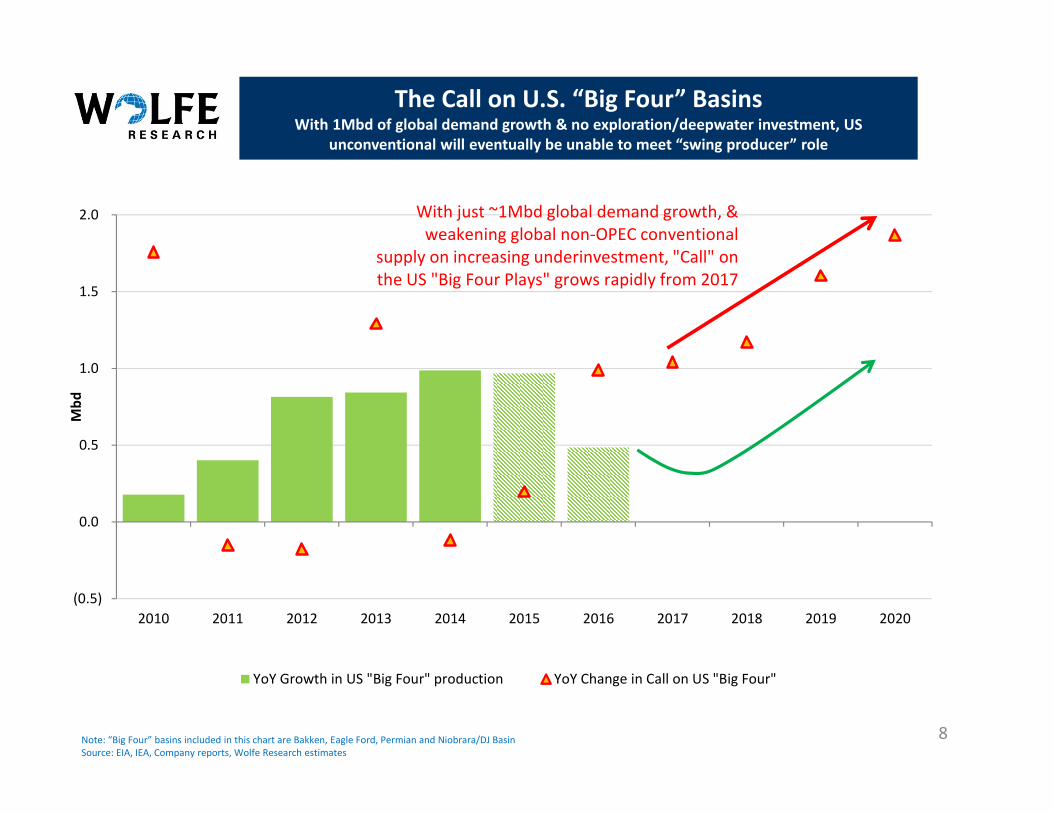

The Call on U.S. “Big Four” BasinsWith 1Mbd of global demand growth & no exploration/deepwater investment, US

unconventional will eventually be unable to meet “swing producer” role

Note: “Big Four” basins included in this chart are Bakken, Eagle Ford, Permian and Niobrara/DJ BasinSource: EIA, IEA, Company reports, Wolfe Research estimates

(0.5)

0.0

0.5

1.0

1.5

2.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Mbd

YoY Growth in US "Big Four" production YoY Change in Call on US "Big Four"

With just ~1Mbd global demand growth, & weakening global non‐OPEC conventional

supply on increasing underinvestment, "Call" on the US "Big Four Plays" grows rapidly from 2017

9

2015 CapexTotal Oil‐focused E&P budgets likely down 25‐30%

Source: Company reports, Bloomberg Finance LP, News reports, Wolfe Research

2015 capex YoY% change 2015 capex YoY $M change

PRODUCER CAPEX PLANSSummary DataCompanies that have announced 2015 plan 52Total companies we are tracking 902014 Capex of announced plans 195,5952014 Capex of remaining unannounced 240,277

2015 announced budgets vs. 2014 budgets 2014 So Far 2015 So Far YoY Change % ChangeTotal integrateds and E&Ps 195,595 172,082 (23,513) ‐12.0%Ex‐integrateds 109,595 86,582 (23,013) ‐21.0%Oil‐focused E&Ps only 97,013 74,509 (22,504) ‐23.2%US Oil‐focused (i.e., ex‐Canadians) 62,698 47,916 (14,782) ‐23.6%Canadians only 34,315 26,593 (7,722) ‐22.5%Integrateds only 86,000 85,500 (500) ‐0.6%Gas‐focused E&Ps only 12,582 12,073 (509) ‐4.0%

‐25,000

‐20,000

‐15,000

‐10,000

‐5,000

0

Totalintegratedsand E&Ps

Ex‐integrateds Oil‐focusedE&Ps only

US Oil‐focused(i.e., ex‐

Canadians)

Canadians only Gas‐focusedE&Ps only

Integratedsonly

US$

millions

‐25%

‐20%

‐15%

‐10%

‐5%

0%

US Oil‐focused(i.e., ex‐

Canadians)

Oil‐focusedE&Ps only

Canadians only Ex‐integrateds Totalintegratedsand E&Ps

Gas‐focusedE&Ps only

Integratedsonly

YoY % declin

e

10

The Call on U.S. “Big Four” BasinsUnderinvesting in “long‐cycle” production results in slower non‐OPEC/non‐Big Four growth on

a 1 year lag, but the sluggishness lasts for 2‐3 years

Note: “Big Four” basins included in this chart are Bakken, Eagle Ford, Permian and Niobrara/DJ BasinSource: EIA, IEA, Company reports, Wolfe Research estimates

‐0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Top 25 Oil Company Capex YoY Change % Non‐OPEC/Non‐Big Four Supply Growth YoY %

Major drop in investment in 2009 (Capex from top 25 companies down 17% YoY) led to 2‐3 years of sluggish growth for long cycle

non‐OPEC supply.

Underinvestment in 2015 will be just as substantial as 2009, expect long‐cycle supply to be increasingly weak from 2016 to 2018, leaving short‐cycle US unconventional to fill

rising demand

Capex likely down 20‐30%+ in

2015

0

100

200

300

400

500

600

1/9/2011 1/9/2012 1/9/2013 1/9/2014 1/9/2015Canadian Oil Rigs Canadian Gas Rigs Canadian Horizontal Rigs

$40

$50

$60

$70

$80

$90

$100

1,400

1,450

1,500

1,550

1,600

1,650

8/1/2014 9/1/2014 10/1/2014 11/1/2014 12/1/2014 1/1/2015

US Oil Rigs WTI Front Month (RHS)11

North American activityRig counts falling quickly now

Source: Bloomberg Finance LP, Baker Hughes, Wolfe Research

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1/9/2011 1/9/2012 1/9/2013 1/9/2014 1/9/201

US Oil Rigs US Gas Rigs US Horizontal Rigs

40

50

60

70

80

90

100

110

170

175

180

185

190

195

200

1/1/14

2/1/14

3/1/14

4/1/14

5/1/14

6/1/14

7/1/14

8/1/14

9/1/14

10/1/14

11/1/14

12/1/14

1/1/15

OIL RIGS WTI Front Month $/bbl (RHS)

US Active Rig Count Canadian Active Rig Count

Recent US Oil Rigs vs. WTI Bakken Oil Rigs vs. WTI

0

200

400

600

800

1,000

1,200

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

Jan‐07

Mar‐07

May‐07

Jul‐0

7Sep‐07

Nov‐07

Jan‐08

Mar‐08

May‐08

Jul‐0

8Sep‐08

Nov‐08

Jan‐09

Mar‐09

May‐09

Jul‐0

9Sep‐09

Nov‐09

Jan‐10

Mar‐10

May‐10

Jul‐1

0Sep‐10

Nov‐10

Jan‐11

Mar‐11

May‐11

Jul‐1

1Sep‐11

Nov‐11

Jan‐12

Mar‐12

May‐12

Jul‐1

2Sep‐12

Nov‐12

Jan‐13

Mar‐13

May‐13

Jul‐1

3Sep‐13

Nov‐13

Jan‐14

Mar‐14

May‐14

Jul‐1

4Sep‐14

Nov‐14

Jan‐15

Mar‐15

May‐15

Jul‐1

5Sep‐15

Nov‐15

Jan‐16

Mar‐16

May‐16

Jul‐1

6Sep‐16

Nov‐16

YoY Monthly Production Growth (LHS) Kbd Annual Growth Implied by Monthly Sequential (LHS) Kbd Major Basin Rig Count (RHS)

With a 15‐20% drop in rigs in "Big Four" basins (~200 rigs) over the course of the next year, we estimate a 500‐600kbd

deceleration in US oil production growth rate by YE15

US production growth , already 1Mbdin 2013, accelerated remarkably through 2014, which likely set off

alarm bells for Saudi in light of weak global demand growth

12

Capex cuts to rig count reductions to slower growth15‐20% drop in rigs in “Big Four” basins = ~500‐600kbd decline in growth rate by YE15

Note: “Big Four” basins included in this chart are Bakken, Eagle Ford, Permian and Niobrara/DJ BasinSource: EIA, Company reports, Wolfe Research estimates

150

160

170

180

190

200

210

220

J F M A M J J A S O N D

09‐'13 range 2012 2013 2014 2015

Starting 2015 ~20Mbd above

last year

10

15

20

25

30

35

40

45

50

55

J F M A M J J A S O N D

09‐'13 range 2013 2014 2015

With turnarounds, production growth & Saudi/Kuwait pushing for share, crude should back up from GC to

Cushing in 1H15

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Feb‐10

Mar‐10

Apr‐10

May‐10

Jun‐10

Jul‐1

0Au

g‐10

Sep‐10

Oct‐10

Nov‐10

Dec‐10

Jan‐11

Feb‐11

Mar‐11

Apr‐11

May‐11

Jun‐11

Jul‐1

1Au

g‐11

Sep‐11

Oct‐11

Nov‐11

Dec‐11

Jan‐12

Feb‐12

Mar‐12

Apr‐12

May‐12

Jun‐12

Jul‐1

2Au

g‐12

Sep‐12

Oct‐12

Nov‐12

Dec‐12

Jan‐13

Feb‐13

Mar‐13

Apr‐13

May‐13

Jun‐13

Jul‐1

3Au

g‐13

Sep‐13

Oct‐13

Nov‐13

Dec‐13

Jan‐14

Feb‐14

Mar‐14

Apr‐14

May‐14

Jun‐14

Jul‐1

4Au

g‐14

Sep‐14

Oct‐14

Nov‐14

Dec‐14

'000

bbls

Asia/Pacific

Middle East

AtlanticBasin/Med

Waterborne storage up

~30Mbd since beginning of November

13

“Too Much Oil” ‐ crude stocks risingFloating storage, Cushing, PADD 3 all rising quickly

Source: Bloomberg Finance LP, EIA, Wolfe Research

US Crude Inventory PADD 3 Crude Inventory

Cushing Crude Inventory

1,000

1,010

1,020

1,030

1,040

1,050

1,060

1,070

1,080

1,090

1,100

J F M A M J J A S O N D

Mbb

l

09‐'13 range 2013 2012 2014 2015

Counter‐seasonal increase at end of year, almost always falls in

December

Global Floating Storage

‐20

‐15

‐10

‐5

0

5

10

15

20

2520

40

60

80

100

120

140

160

J‐04 J‐05 J‐06 J‐07 J‐08 J‐09 J‐10 J‐11 J‐12 J‐13 J‐14 J‐15

($/bbl)

($/bbl)

WTI 1st Month WTI 12th Month 12m Contango (RHS)

12 month WTI contango hit $15 in late Dec 2008, and $23 mid‐Jan 2009

Current 12 month contango is widnening, but is still only ~$7.50

14

WTI contangoMay need to steepen towards $20 to reverse decline in WTI

Source: Bloomberg Finance LP, Wolfe Research

New recommendation deck Balanced recs for Market Weight Sector

15

OUTPERFORM – all plays on “Call on US unconventional” EOG RESOURCES (EOG, Reiterate OP, $105 PT) HESS CORP. (HES, Reiterate OP, $85 PT) – watch for very weak results CONOCOPHILLIPS (COP, Reiterate OP, $76 PT) – enforced capital discipline unlike CVX ANADARKO (APC, Reiterate OP, $96 PT) DEVON ENERGY (DVN, Reiterate OP, $73 PT)

UNDERPERFORM CHEVRON (CVX, Downgrade to UP, $100 PT) APACHE CORP. (APA, Downgrade to UP, $55 PT) MURPHY OIL (MUR, Downgrade to UP, $43 PT) CANADIAN NATURAL RESOURCES (CNQ, UP, C$28 PT) CALIFORNIA RESOURCES CORP. (CRC, $4 PT)

PEER PERFORM EXXONMOBIL (XOM, Reiterate PP) OCCIDENTAL (OXY, Reiterate PP) NOBLE ENERGY (NBL, Reiterate PP) SUNCOR ENERGY (SU, Downgrade to PP) MARATHON OIL (MRO, Downgrade to PP)

“It is not the strongest or the most intelligent who will survive but those who can best manage change” ‐ Darwin

16

Refining Downgrade Sector relative valuations

Source: FactSet, Wolfe Research

Refiners 2015 EV/EBITDA and P/E

Refiners share of SP500 EPS vs. share of mkt cap Refiners P/E relative to market

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

Dec-98

Dec-99

Dec-00

Dec-01

Dec-02

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Forecast Refiners Attributable Income as % of S&P500

Current Refiners Sector Weight % of S&P500

PSX

VLO

MPC

HFCTSO

WNR

PBF

DK

3.5x

4.0x

4.5x

5.0x

5.5x

6.0x

6.5x

7.0x

7.0x 8.0x 9.0x 10.0x 11.0x 12.0x 13.0x

2015

EV/

EBITDA

2015 P/E

0%

20%

40%

60%

80%

100%

120%

140%

0%

20%

40%

60%

80%

100%

120%

140%

Dec-98

Dec-99

Dec-00

Dec-01

Dec-02

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Refiners P/E vs Market P/E

Refiners % of Market - Historical Average

17

Wolfe Research Commodity Price Deck

Source: Bloomberg Finance LP, Wolfe Research

$/bbl 2012 2013 1Q14 2Q14 3Q14 4Q14 2014E 1Q15E 2Q15E 3Q15E 4Q15E 2015E 1Q16E 2Q16E 3Q16E 4Q16E 2016E

COMMODITY PRICES

Brent 112.17 108.19 107.86 109.76 102.16 75.84 98.91 48.00 54.00 59.00 65.00 56.50 70.00 75.00 75.00 80.00 75.00WTI 94.37 97.98 98.61 103.11 97.67 72.94 93.00 45.00 50.00 55.00 61.00 52.75 65.00 70.00 70.00 75.00 70.00Midland 90.07 96.22 92.72 95.47 87.07 69.65 86.23 43.00 48.00 53.50 59.50 51.00 64.00 69.00 69.00 74.00 69.00LLS 111.69 107.45 104.37 105.59 101.09 75.83 96.72 47.00 53.00 57.50 63.50 55.25 68.00 73.00 73.00 78.00 73.00Clearbrook 88.39 92.87 94.82 98.42 91.23 67.10 87.89 39.00 44.00 48.00 53.00 46.00 58.00 63.00 63.00 68.00 63.00Syncrude 92.60 97.31 98.29 103.70 94.99 70.23 91.80 42.00 47.00 52.00 58.00 49.75 62.00 67.00 67.00 72.00 67.00ANS 110.70 107.79 105.96 109.52 102.30 75.12 98.23 47.00 52.00 57.00 63.00 54.75 67.00 72.00 72.00 77.00 72.00WTS 88.67 95.27 93.18 95.87 88.98 70.74 87.00 43.00 48.00 53.00 59.00 51.00 63.00 68.00 68.00 73.00 68.00Mars 106.88 102.35 100.86 100.81 97.45 72.02 93.00 43.00 49.00 53.50 59.50 51.00 64.00 69.00 69.00 74.00 69.00Maya 99.62 97.40 89.24 95.74 91.03 66.73 85.69 37.00 43.00 47.50 53.50 45.25 58.00 63.00 63.00 68.00 63.00WCS 71.82 73.49 77.67 83.84 78.77 57.44 74.43 29.00 34.00 39.00 45.00 36.75 49.00 54.00 54.00 59.00 54.00Henry Hub ($/mmBtu) 2.76 3.73 5.18 4.53 3.94 3.74 4.35 3.75 3.65 4.00 4.40 3.95 4.25 4.25 4.25 4.25 4.25UK NBP ($/mmBtu) 9.47 10.55 10.02 7.61 7.08 8.39 8.28 7.50 8.00 8.00 8.00 7.88 9.00 9.00 9.00 9.00 9.00

CRUDE DIFFERENTIALS

Brent-WTI 17.80 10.21 9.25 6.65 4.49 2.90 5.80 3.00 4.00 4.00 4.00 3.80 5.00 5.00 5.00 5.00 5.00Brent-LLS 0.48 0.74 3.49 4.17 1.07 0.01 2.19 1.00 1.00 1.50 1.50 1.25 2.00 2.00 2.00 2.00 2.00Brent-Clearbrook 23.78 15.31 13.04 11.34 10.93 8.74 11.01 9.00 10.00 11.00 12.00 10.50 12.00 12.00 12.00 12.00 12.00Brent-Midland 22.10 11.97 15.14 14.29 15.09 6.19 12.68 5.00 6.00 5.50 5.50 5.50 6.00 6.00 6.00 6.00 6.00LLS-WTI 17.32 9.47 5.76 2.48 3.42 2.89 3.64 2.00 3.00 2.50 2.50 2.50 3.00 3.00 3.00 3.00 3.00WTI-Midland 4.30 1.76 5.89 7.64 10.60 3.29 6.86 2.00 2.00 1.50 1.50 1.75 1.00 1.00 1.00 1.00 1.00WTI-Clearbrook 5.98 5.10 3.79 4.69 6.44 5.84 5.19 6.00 6.00 7.00 8.00 6.75 7.00 7.00 7.00 7.00 7.00WTI-Syncrude 1.77 0.67 0.32 (0.59) 2.68 2.71 1.28 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00WTI-ANS (16.33) (9.81) (7.35) (6.41) (4.63) (2.18) (5.14) (2.00) (2.00) (2.00) (2.00) (2.00) (2.00) (2.00) (2.00) (2.00) (2.00)LLS-Mars 4.81 5.10 3.51 4.78 3.64 3.81 3.94 4.00 4.00 4.00 4.00 4.00 4.00 4.00 4.00 4.00 4.00WTI-WTS 5.69 2.71 5.43 7.24 8.69 2.20 5.89 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00Brent-Maya 12.55 10.79 18.62 14.02 11.13 9.11 13.22 11.00 11.00 11.50 11.50 11.25 12.00 12.00 12.00 12.00 12.00LLS-Maya 12.06 10.05 15.13 9.85 10.06 9.10 11.04 10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00WTI-Maya (5.25) 0.58 9.37 7.37 6.64 6.21 7.40 8.00 7.00 7.50 7.50 7.50 7.00 7.00 7.00 7.00 7.00WTI-WCS 22.55 24.49 20.94 19.27 18.90 15.50 18.65 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00Brent-WCS 40.35 34.69 30.19 25.92 23.39 18.40 24.48 19.00 20.00 20.00 20.00 19.75 21.00 21.00 21.00 21.00 21.00

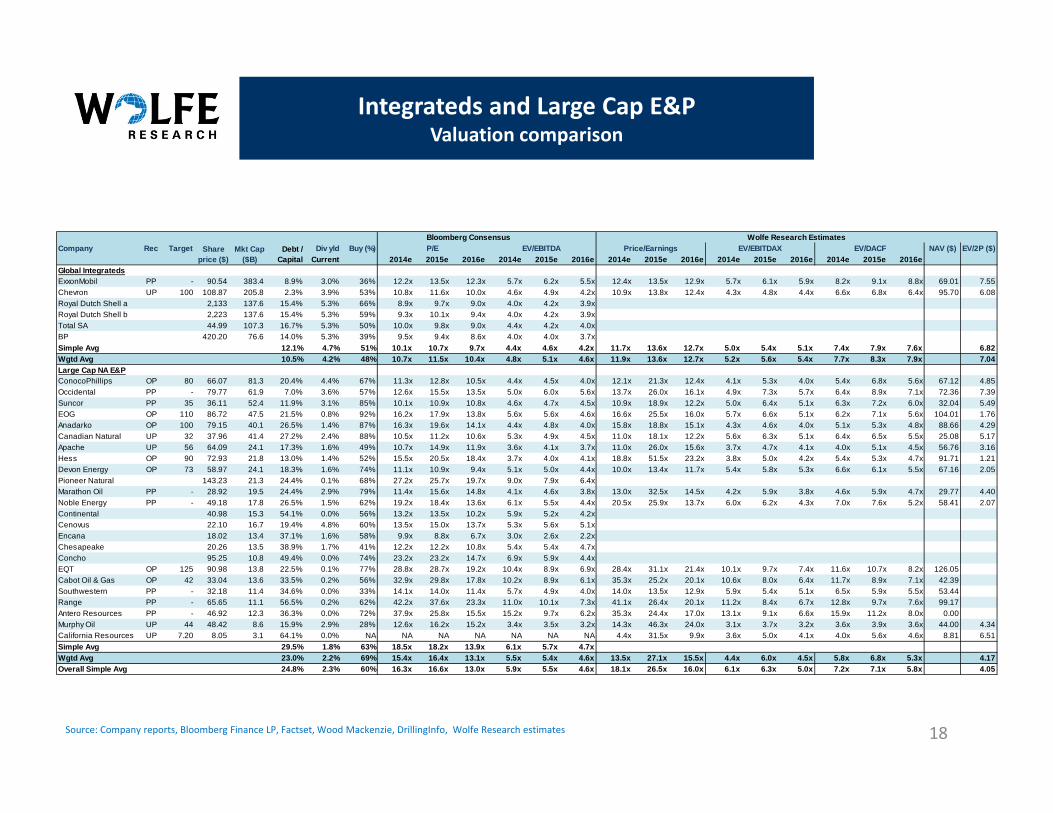

Integrateds and Large Cap E&PValuation comparison

18Source: Company reports, Bloomberg Finance LP, Factset, Wood Mackenzie, DrillingInfo, Wolfe Research estimates

Company Rec Target Div yld Buy (%) NAV ($) EV/2P ($)Current 2014e 2015e 2016e 2014e 2015e 2016e 2014e 2015e 2016e 2014e 2015e 2016e 2014e 2015e 2016e

Global IntegratedsExxonMobil PP - 90.54 383.4 8.9% 3.0% 36% 12.2x 13.5x 12.3x 5.7x 6.2x 5.5x 12.4x 13.5x 12.9x 5.7x 6.1x 5.9x 8.2x 9.1x 8.8x 69.01 7.55Chevron UP 100 108.87 205.8 2.3% 3.9% 53% 10.8x 11.6x 10.0x 4.6x 4.9x 4.2x 10.9x 13.8x 12.4x 4.3x 4.8x 4.4x 6.6x 6.8x 6.4x 95.70 6.08Royal Dutch Shell a 2,133 137.6 15.4% 5.3% 66% 8.9x 9.7x 9.0x 4.0x 4.2x 3.9xRoyal Dutch Shell b 2,223 137.6 15.4% 5.3% 59% 9.3x 10.1x 9.4x 4.0x 4.2x 3.9xTotal SA 44.99 107.3 16.7% 5.3% 50% 10.0x 9.8x 9.0x 4.4x 4.2x 4.0xBP 420.20 76.6 14.0% 5.3% 39% 9.5x 9.4x 8.6x 4.0x 4.0x 3.7xSimple Avg 12.1% 4.7% 51% 10.1x 10.7x 9.7x 4.4x 4.6x 4.2x 11.7x 13.6x 12.7x 5.0x 5.4x 5.1x 7.4x 7.9x 7.6x 6.82Wgtd Avg 10.5% 4.2% 48% 10.7x 11.5x 10.4x 4.8x 5.1x 4.6x 11.9x 13.6x 12.7x 5.2x 5.6x 5.4x 7.7x 8.3x 7.9x 7.04Large Cap NA E&PConocoPhillips OP 80 66.07 81.3 20.4% 4.4% 67% 11.3x 12.8x 10.5x 4.4x 4.5x 4.0x 12.1x 21.3x 12.4x 4.1x 5.3x 4.0x 5.4x 6.8x 5.6x 67.12 4.85Occidental PP - 79.77 61.9 7.0% 3.6% 57% 12.6x 15.5x 13.5x 5.0x 6.0x 5.6x 13.7x 26.0x 16.1x 4.9x 7.3x 5.7x 6.4x 8.9x 7.1x 72.36 7.39Suncor PP 35 36.11 52.4 11.9% 3.1% 85% 10.1x 10.9x 10.8x 4.6x 4.7x 4.5x 10.9x 18.9x 12.2x 5.0x 6.4x 5.1x 6.3x 7.2x 6.0x 32.04 5.49EOG OP 110 86.72 47.5 21.5% 0.8% 92% 16.2x 17.9x 13.8x 5.6x 5.6x 4.6x 16.6x 25.5x 16.0x 5.7x 6.6x 5.1x 6.2x 7.1x 5.6x 104.01 1.76Anadarko OP 100 79.15 40.1 26.5% 1.4% 87% 16.3x 19.6x 14.1x 4.4x 4.8x 4.0x 15.8x 18.8x 15.1x 4.3x 4.6x 4.0x 5.1x 5.3x 4.8x 88.66 4.29Canadian Natural UP 32 37.96 41.4 27.2% 2.4% 88% 10.5x 11.2x 10.6x 5.3x 4.9x 4.5x 11.0x 18.1x 12.2x 5.6x 6.3x 5.1x 6.4x 6.5x 5.5x 25.08 5.17Apache UP 56 64.09 24.1 17.3% 1.6% 49% 10.7x 14.9x 11.9x 3.6x 4.1x 3.7x 11.0x 26.0x 15.6x 3.7x 4.7x 4.1x 4.0x 5.1x 4.5x 56.76 3.16Hess OP 90 72.93 21.8 13.0% 1.4% 52% 15.5x 20.5x 18.4x 3.7x 4.0x 4.1x 18.8x 51.5x 23.2x 3.8x 5.0x 4.2x 5.4x 5.3x 4.7x 91.71 1.21Devon Energy OP 73 58.97 24.1 18.3% 1.6% 74% 11.1x 10.9x 9.4x 5.1x 5.0x 4.4x 10.0x 13.4x 11.7x 5.4x 5.8x 5.3x 6.6x 6.1x 5.5x 67.16 2.05Pioneer Natural 143.23 21.3 24.4% 0.1% 68% 27.2x 25.7x 19.7x 9.0x 7.9x 6.4xMarathon Oil PP - 28.92 19.5 24.4% 2.9% 79% 11.4x 15.6x 14.8x 4.1x 4.6x 3.8x 13.0x 32.5x 14.5x 4.2x 5.9x 3.8x 4.6x 5.9x 4.7x 29.77 4.40Noble Energy PP - 49.18 17.8 26.5% 1.5% 62% 19.2x 18.4x 13.6x 6.1x 5.5x 4.4x 20.5x 25.9x 13.7x 6.0x 6.2x 4.3x 7.0x 7.6x 5.2x 58.41 2.07Continental 40.98 15.3 54.1% 0.0% 56% 13.2x 13.5x 10.2x 5.9x 5.2x 4.2xCenovus 22.10 16.7 19.4% 4.8% 60% 13.5x 15.0x 13.7x 5.3x 5.6x 5.1xEncana 18.02 13.4 37.1% 1.6% 58% 9.9x 8.8x 6.7x 3.0x 2.6x 2.2xChesapeake 20.26 13.5 38.9% 1.7% 41% 12.2x 12.2x 10.8x 5.4x 5.4x 4.7xConcho 95.25 10.8 49.4% 0.0% 74% 23.2x 23.2x 14.7x 6.9x 5.9x 4.4xEQT OP 125 90.98 13.8 22.5% 0.1% 77% 28.8x 28.7x 19.2x 10.4x 8.9x 6.9x 28.4x 31.1x 21.4x 10.1x 9.7x 7.4x 11.6x 10.7x 8.2x 126.05Cabot Oil & Gas OP 42 33.04 13.6 33.5% 0.2% 56% 32.9x 29.8x 17.8x 10.2x 8.9x 6.1x 35.3x 25.2x 20.1x 10.6x 8.0x 6.4x 11.7x 8.9x 7.1x 42.39Southwestern PP - 32.18 11.4 34.6% 0.0% 33% 14.1x 14.0x 11.4x 5.7x 4.9x 4.0x 14.0x 13.5x 12.9x 5.9x 5.4x 5.1x 6.5x 5.9x 5.5x 53.44Range PP - 65.65 11.1 56.5% 0.2% 62% 42.2x 37.6x 23.3x 11.0x 10.1x 7.3x 41.1x 26.4x 20.1x 11.2x 8.4x 6.7x 12.8x 9.7x 7.6x 99.17Antero Resources PP - 46.92 12.3 36.3% 0.0% 72% 37.9x 25.8x 15.5x 15.2x 9.7x 6.2x 35.3x 24.4x 17.0x 13.1x 9.1x 6.6x 15.9x 11.2x 8.0x 0.00Murphy Oil UP 44 48.42 8.6 15.9% 2.9% 28% 12.6x 16.2x 15.2x 3.4x 3.5x 3.2x 14.3x 46.3x 24.0x 3.1x 3.7x 3.2x 3.6x 3.9x 3.6x 44.00 4.34California Resources UP 7.20 8.05 3.1 64.1% 0.0% NA NA NA NA NA NA NA 4.4x 31.5x 9.9x 3.6x 5.0x 4.1x 4.0x 5.6x 4.6x 8.81 6.51Simple Avg 29.5% 1.8% 63% 18.5x 18.2x 13.9x 6.1x 5.7x 4.7xWgtd Avg 23.0% 2.2% 69% 15.4x 16.4x 13.1x 5.5x 5.4x 4.6x 13.5x 27.1x 15.5x 4.4x 6.0x 4.5x 5.8x 6.8x 5.3x 4.17Overall Simple Avg 24.8% 2.3% 60% 16.3x 16.6x 13.0x 5.9x 5.5x 4.6x 18.1x 26.5x 16.0x 6.1x 6.3x 5.0x 7.2x 7.1x 5.8x 4.05

Bloomberg Consensus Wolfe Research EstimatesShare

price ($)Mkt Cap

($B)Debt /

CapitalP/E EV/EBITDA Price/Earnings EV/EBITDAX EV/DACF

US RefinersValuation comparison

19Source: Company reports, FactSet, Wolfe Research estimates

Company Rec.2014e 2015e 2014e 2015e 2014e 2015e 2014e 2015e

US Large Cap RefinersPhillips 66 Peer Perform $67.31 38.0 79% -14% 10.6x 10.1x 6.1x 6.1x 10.5x 9.4x 5.5x 5.8xValero Outperform $63 $48.65 25.8 64% -8% 8.2x 8.9x 4.2x 4.5x 8.0x 8.6x 4.1x 4.4xMarathon Petroleum Outperform $103 $88.49 25.1 60% -3% 11.7x 10.9x 6.3x 5.7x 12.4x 10.4x 6.5x 5.7xHollyFrontier Peer Perform $35.71 7.1 8% -29% 11.5x 11.3x 5.2x 5.1x 11.5x 9.8x 5.4x 4.8xTesoro Peer Perform $72.86 9.4 60% 26% 10.9x 11.2x 5.5x 5.3x 10.4x 11.2x 5.3x 5.4xUS Small Cap RefinersWestern Refining Outperform $52 $37.21 3.8 20% -10% 8.3x 9.6x 5.5x 6.4x 8.9x 9.8x 5.6x 6.9xPBF Energy Peer Perform $25.22 2.5 29% -13% 6.4x 7.4x 3.8x 4.3x 6.7x 8.2x 3.8x 4.3xDelek US Outperform $38 $28.25 1.7 67% -17% 8.9x 11.9x 4.3x 4.8x 9.4x 8.3x 4.0x 4.0xAverage Peer Perform 14.2 48% -8% 9.6x 10.2x 5.1x 5.3x 9.7x 9.5x 5.0x 5.2x

Crude Dist.Company Capacity NCI NAV

(000 b/d) 2014e 2015e 2014e 2015eUS Large Cap RefinersPhillips 66 2,156 18,596 1,675 11.1 $83 $3,105 7.5% 13.7% 14.4% 5.4% -1.8% 3.1% 4.4% 7.5%Valero 2,384 9,925 799 12.4 $67 $2,192 7.7% 13.0% 11.0% 7.7% 7.3% 2.7% 6.6% 9.2%Marathon Petroleum 1,714 17,489 1,592 11.0 $114 $4,410 14.7% 13.6% 13.8% -7.9% 6.5% 2.5% 3.7% 6.2%HollyFrontier 443 16,254 1,377 11.8 $46 ($440) -6.1% 8.5% 9.8% 13.2% 14.8% 9.2% 2.9% 12.1%Tesoro 850 14,298 1,765 8.1 $87 $1,414 11.6% 13.2% 10.5% 7.0% 6.1% 2.2% 5.6% 7.8%US Small Cap RefinersWestern Refining 250 24,244 2,886 8.4 $50 $603 13.8% 9.6% 8.1% 11.1% 15.0% 3.2% 8.2% 11.4%PBF Energy 540 6,326 688 9.2 $29 $427 14.8% 15.2% 11.3% -5.1% 7.9% 5.2% 5.3% 10.5%Delek US 140 14,037 1,523 9.2 $42 $97 5.4% 11.5% 11.6% 0.8% 7.8% 4.2% 5.0% 9.3%Average 15,146 1,538 11.0 8.7% 12.3% 11.3% 4.0% 8.0% 4.0% 5.2% 9.2%

1 Year % Chg

FactSet Consensus Wolfe ResearchP/E EV/EBITDA

ROCE

Share Price Buy (%)Target Price

Dividend Yield

Mkt Cap ($bn)

P/E EV/EBITDA

EV/CEDC ($)EV/bbl ($)

2015e Cash ReturnTotal Yield

Net Debt ($m)

Buyback Yield

FCF Yield Net Debt/ Capital

Disclosure Section

20

DISCLOSURE SECTION

Analyst Certification:

The analyst of Wolfe Research, LLC primarily responsible for this research report whose name appears first on the front page of this research report hereby certifies that (i) the recommendations and opinions expressed in this research report accurately reflect the research analysts’ personal views about the subject securities or issuers and (ii) no part of the research analysts’ compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this report.

Other Disclosures:

Wolfe Research, LLC Fundamental Stock Ratings Key:

Outperform (OP): The security is projected to outperform analyst's industry coverage universe over the next 12 months.

Peer Perform (PP): The security is projected to perform approximately in line with analyst's industry coverage universe over the next 12 months.

Underperform (UP): The security is projected to underperform analyst's industry coverage universe over the next 12 months.

Wolfe Research, LLC uses a relative rating system using terms such as Outperform, Peer Perform and Underperform (see definitions above). Please carefully read the definitions of all ratings used in Wolfe Research, LLC research. In addition, since Wolfe Research, LLC research contains more complete information concerning the analyst’s views, please carefully read Wolfe Research, LLC research in its entirety and not infer the contents from the ratings alone. In all cases, ratings (or research) should not be used or relied upon as investment advice and any investment decisions should be based upon individual circumstances and other considerations.

Wolfe Research, LLC Sector Weighting System:

Market Overweight (MO): Expect the industry to outperform the primary market index for the region (S&P 500 in the U.S.) by at least 10% over the next 12 months.

Market Weight (MW): Expect the industry to perform approximately in line with the primary market index for the region (S&P 500 in the U.S.) over the next 12 months.

Market Underweight (MU): Expect the industry to underperform the primary market index for the region (S&P 500 in the U.S.) by at least 10% over the next 12 months.

Wolfe Research, LLC Distribution of Fundamental Stock Ratings (As of December 31, 2014):

Outperform: 41% 2% Investment Banking Clients Peer Perform: 50% 1% Investment Banking Clients Underperform: 9% 0% Investment Banking Clients

Wolfe Research, LLC does not assign ratings of Buy, Hold or Sell to the stocks it covers. Outperform, Peer Perform and Underperform are not the respective equivalents of Buy, Hold and Sell but represent relative weightings as defined above. To satisfy regulatory requirements, Outperform has been designated to correspond with Buy, Peer Perform has been designated to correspond with Hold and Underperform has been designated to correspond with Sell.

Wolfe Research Securities and Wolfe Research, LLC have adopted the use of Wolfe Research as brand names. Wolfe Research Securities, a member of FINRA (www.finra.org) is the broker-dealer affiliate of Wolfe Research, LLC and is responsible for the contents of this material. Any analysts publishing these reports are dually employed by Wolfe Research, LLC and Wolfe Research Securities.

The content of this report is to be used solely for informational purposes and should not be regarded as an offer, or a solicitation of an offer, to buy or sell a security, financial instrument or service discussed herein. Opinions in this communication constitute the current judgment of the author as of the date and time of this report and are subject to change without notice. Information herein is believed to be reliable but Wolfe Research and its affiliates, including but not limited to Wolfe Research Securities, makes no representation that it is complete or accurate. The information provided in this communication is not designed to replace a recipient's own decision-making processes for assessing a proposed transaction or investment involving a financial instrument discussed herein. Recipients are encouraged to seek financial advice from their financial advisor regarding the appropriateness of investing in a security or financial instrument referred to in this report and should understand that statements regarding the future performance of the financial instruments or the securities referenced herein may not be realized. Past performance is not indicative of future results. This report is not intended for distribution to, or use by, any person or entity in any location where such distribution or use would be contrary to applicable law, or which would subject Wolfe Research, LLC or any affiliate to any registration requirement within such location. For additional important disclosures, please see www.WolfeResearch.com/Disclosures.

The views expressed in Wolfe Research, LLC research reports with regards to sectors and/or specific companies may from time to time be inconsistent with the views implied by inclusion of those sectors and companies in other Wolfe Research, LLC analysts’ research reports and modeling screens. Wolfe Research communicates with clients across a variety of mediums of the clients’ choosing including emails, voice blasts and electronic publication to our proprietary website.